A decision tree valuation of a pharmaceutical company with...

22

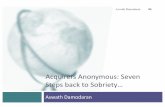

22 A decision tree valuation of a pharmaceutical company with one drug in the FDA pipeline… Aswath Damodaran 22 Test Abandon Succeed 70% Fail 30% -$50 -$140.91 Types 1 & 2 Type 2 Type 1 Fail 10% 10% 30% Develop Abandon Develop Abandon Develop Abandon Succeed Succeed Succeed Fail Fail Fail 75% 25% 80% 20% 80% 20% -$328.74 -$328.74 -$328.74 $585.62 -$328.74 -$97.43 -$366.30 -$366.30 $887.05 50% $50.36 $93.37 $573.71 -$143.69 $402.75

Transcript of A decision tree valuation of a pharmaceutical company with...

22

AdecisiontreevaluationofapharmaceuticalcompanywithonedrugintheFDApipeline…

Aswath Damodaran

22

Test

Abandon

Succeed

70%

Fail

30%-$50

-$140.91

Types 1 & 2

Type 2

Type 1

Fail

10%

10%

30%

Develop

Abandon

Develop

Abandon

Develop

Abandon

Succeed

Succeed

Succeed

Fail

Fail

Fail

75%

25%

80%

20%

80%

20%-$328.74

-$328.74

-$328.74

$585.62

-$328.74

-$97.43-$366.30

-$366.30

$887.05

50%

$50.36

$93.37

$573.71

-$143.69

$402.75

23

KeyTestsforRealOptions

Aswath Damodaran

23

¨ Isthereanoptionembeddedinthisasset/decision?¤ Canyouidentifytheunderlyingasset?¤ Canyouspecifythecontingencyunderwhichyouwillgetpayoff?

¨ Isthereexclusivity?¤ Ifyes,thereisoptionvalue.¤ Ifno,thereisnone.¤ Ifinbetween,youhavetoscalevalue.

¨ Canyouuseanoptionpricingmodeltovaluetherealoption?¤ Istheunderlyingassettraded?¤ Cantheoptionbeboughtandsold?¤ Isthecostofexercisingtheoptionknownandclear?

24

I.OptionsinProjects/Investments/Acquisitions

Aswath Damodaran

24

¨ Oneofthelimitationsoftraditionalinvestmentanalysisisthatitisstaticanddoesnotdoagoodjobofcapturingtheoptionsembeddedininvestment.¤ Thefirstoftheseoptionsistheoptiontodelaytakingainvestment,whenafirmhasexclusiverightstoit,untilalaterdate.

¤ Thesecondoftheseoptionsistakingoneinvestmentmayallowustotakeadvantageofotheropportunities(investments)inthefuture

¤ Thelastoptionthatisembeddedinprojectsistheoptiontoabandonainvestment,ifthecashflowsdonotmeasureup.

¨ Theseoptionsalladdvaluetoprojectsandmaymakea“bad” investment(fromtraditionalanalysis)intoagoodone.

25

A.TheOptiontoDelay

Aswath Damodaran

25

¨ Whenafirmhasexclusiverightstoaprojectorproductforaspecificperiod,itcandelaytakingthisprojectorproductuntilalaterdate.

¨ Atraditionalinvestmentanalysisjustanswersthequestionofwhethertheprojectisa“good” oneiftakentoday.

¨ Thus,thefactthataprojectdoesnotpassmustertoday(becauseitsNPVisnegative,oritsIRRislessthanitshurdlerate)doesnotmeanthattherightstothisprojectarenotvaluable.

26

ValuingtheOptiontoDelayaProject

Aswath Damodaran

26

Present Value of Expected Cash Flows on Product

PV of Cash Flows from Project

Initial Investment in Project

Project has negativeNPV in this section

Project's NPV turns positive in this section

27

Example1:Valuingproductpatentsasoptions

Aswath Damodaran

27

¨ Aproductpatentprovidesthefirmwiththerighttodeveloptheproductandmarketit.

¨ Itwilldosoonlyifthepresentvalueoftheexpectedcashflowsfromtheproductsalesexceedthecostofdevelopment.

¨ Ifthisdoesnotoccur,thefirmcanshelvethepatentandnotincuranyfurthercosts.

¨ IfIisthepresentvalueofthecostsofdevelopingtheproduct,andVisthepresentvalueoftheexpectedcashflowsfromdevelopment,thepayoffsfromowningaproductpatentcanbewrittenas:

Payofffromowningaproductpatent =V- I ifV>I=0 ifV≤I

28

PayoffonProductOption

Aswath Damodaran

28

Present Value ofcashflows on product

Net Payoff tointroduction

Cost of product introduction

ObtainingInputsforPatentValuation

Input Estimation Process

1. Value of the Underlying Asset • Present Value of Cash Inflows from taking projectnow

• This will be noisy, but that adds value.2. Variance in value of underlying asset • Variance in cash flows of similar assets or firms

• Variance in present value from capital budgetingsimulation.

3. Exercise Price on Option • Option is exercised when investment is made.• Cost of making investment on the project ; assumed

to be constant in present value dollars.4. Expiration of the Option • Life of the patent

5. Dividend Yield • Cost of delay• Each year of delay translates into one less year of

value-creating cashflowsAnnual cost of delay = 1

n

30

ValuingaProductPatent:Avonex

Aswath Damodaran

30

¨ Biogen,abio-technologyfirm,hasapatentonAvonex,adrugtotreatmultiplesclerosis,forthenext17years,anditplanstoproduceandsellthedrugbyitself.

¨ Thekeyinputsonthedrugareasfollows:¤ PVofCashFlowsfromIntroducingtheDrugNow=S=$3.422billion¤ PVofCostofDevelopingDrugforCommercialUse=K=$2.875billion¤ PatentLife=t=17yearsRisklessRate=r=6.7%(17-yearT.Bond rate)¤ VarianceinExpectedPresentValues=s2 =0.224(Industryaveragefirmvariancefor

bio-techfirms)¤ ExpectedCostofDelay=y=1/17=5.89%

¨ Theoutputfromtheoptionpricingmodel¤ d1=1.1362 N(d1)=0.8720¤ d2=-0.8512 N(d2)=0.2076CallValue=3,422exp(-0.0589)(17)(0.8720)- 2,875exp(-0.067)(17) (0.2076)=$907million

31

TheOptimalTimetoExercise

Aswath Damodaran

31 Patent value versus Net Present value

0

100

200

300

400

500

600

700

800

900

1000

17 16 15 14 13 12 11 10 9 8 7 6 5 4 3 2 1Number of years left on patent

Val

ue

Value of patent as option Net present value of patent

Exercise the option here: Convert patent to commercial product

32

Valuingafirmwithpatents

Aswath Damodaran

32

¨ Thevalueofafirmwithasubstantialnumberofpatentscanbederivedusingtheoptionpricingmodel.

ValueofFirm=Valueofcommercialproducts(usingDCFvalue+Valueofexistingpatents(usingoptionpricing)+(ValueofNewpatentsthatwillbeobtainedinthe

future– Costofobtainingthesepatents)¨ Thelastinputmeasurestheefficiencyofthefirmin

convertingitsR&Dintocommercialproducts.Ifweassumethatafirmearnsitscostofcapitalfromresearch,thistermwillbecomezero.

¨ Ifweusethisapproach,weshouldbecarefulnottodoublecountandallowforahighgrowthrateincashflows(intheDCFvaluation).

33

ValueofBiogen’sexistingproducts

Aswath Damodaran

33

¨ Biogenhadtwocommercialproducts(adrugtotreatHepatitisBandIntron)atthetimeofthisvaluationthatithadlicensedtootherpharmaceuticalfirms.

¨ Thelicensefeesontheseproductswereexpectedtogenerate$50millioninafter-taxcashflowseachyearforthenext12years.

¨ Tovaluethesecashflows,whichwereguaranteedcontractually,the pre-taxcostofdebtoftheguarantorswasused:PresentValueofLicenseFees=$50million(1– (1.07)-12)/.07

=$397.13million

34

ValueofBiogen’sFutureR&D

Aswath Damodaran

34

¨ Biogencontinuedtofundresearchintonewproducts,spendingabout$100milliononR&Dinthemostrecentyear.TheseR&Dexpenseswereexpectedtogrow20%ayearforthenext10years,and5%thereafter.

¨ Itwasassumedthateverydollarinvestedinresearchwouldcreate$1.25invalueinpatents(valuedusingtheoptionpricingmodeldescribedabove)forthenext10years,andbreakevenafterthat(i.e.,generate$1inpatentvalueforevery$1investedinR&D).

¨ Therewasasignificantamountofriskassociatedwiththiscomponentandthecostofcapitalwasestimatedtobe15%.

35

ValueofFutureR&D

Aswath Damodaran

35

Yr ValueofPatents R&DCost ExcessValue PV(at15%)

1 $150.00 $120.00 $30.00 $26.09

2 $180.00 $144.00 $36.00 $27.22

3 $216.00 $172.80 $43.20 $28.40

4 $259.20 $207.36 $51.84 $29.64

5 $311.04 $248.83 $62.21 $30.93

6 $373.25 $298.60 $74.65 $32.27

7 $447.90 $358.32 $89.58 $33.68

8 $537.48 $429.98 $107.50 $35.14

9 $644.97 $515.98 $128.99 $36.67

10 $773.97 $619.17 $154.79 $38.26

$318.30

36

ValueofBiogen

Aswath Damodaran

36

¨ ThevalueofBiogenasafirmisthesumofallthreecomponents– thepresentvalueofcashflowsfromexistingproducts,thevalueofAvonex(asanoption)andthevaluecreatedbynewresearch:Value=Existingproducts+ExistingPatents+Value:FutureR&D

=$397.13million+$907million+$318.30million=$1622.43million

¨ SinceBiogenhadnodebtoutstanding,thisvaluewasdividedbythenumberofsharesoutstanding(35.50million)toarriveatavaluepershare:¤Valuepershare=$1,622.43million/35.5=$45.70

37

TheRealOptionsTest:PatentsandTechnology

Aswath Damodaran

37

¨ TheOptionTest:¤ UnderlyingAsset:Productthatwouldbegeneratedbythepatent¤ Contingency:

n IfPVofCFsfromdevelopment>Costofdevelopment:PV- Costn IfPVofCFsfromdevelopment<Costofdevelopment:0

¨ TheExclusivityTest:¤ Patentsrestrictcompetitorsfromdevelopingsimilarproducts¤ Patentsdonotrestrictcompetitorsfromdevelopingotherproductstotreatthesamedisease.

¨ ThePricingTest¤ UnderlyingAsset:Patentsarenottraded.Notonlydoyouthereforehavetoestimatethepresentvaluesand

volatilitiesyourself,youcannotconstructreplicatingpositionsordoarbitrage.¤ Option:Patentsareboughtandsold,thoughnotasfrequentlyasoilreservesormines.¤ CostofExercisingtheOption:Thisisthecostofconvertingthepatentforcommercialproduction.Here,

experiencedoeshelpanddrugfirmscanmakefairlypreciseestimatesofthecost.

¨ Conclusion:Youcanestimatethevalueoftherealoptionbutthequalityofyourestimatewillbeadirectfunctionofthequalityofyourcapitalbudgeting.Itworksbestifyouarevaluingapubliclytradedfirmthatgeneratesmostofitsvaluefromoneorafewpatents- youcanusethemarketvalueofthefirmandthevarianceinthatvaluetheninyouroptionpricingmodel.

38

Example2:ValuingNaturalResourceOptions

Aswath Damodaran

38

¨ Inanaturalresourceinvestment,theunderlyingassetistheresourceandthevalueoftheassetisbasedupontwovariables- thequantityoftheresourcethatisavailableintheinvestmentandthepriceoftheresource.

¨ Inmostsuchinvestments,thereisacostassociatedwithdevelopingtheresource,andthedifferencebetweenthevalueoftheassetextractedandthecostofthedevelopmentistheprofittotheowneroftheresource.

¨ DefiningthecostofdevelopmentasX,andtheestimatedvalueoftheresourceasV,thepotentialpayoffsonanaturalresourceoptioncanbewrittenasfollows:

Payoffonnaturalresourceinvestment =V- X ifV>X=0 ifV≤X

39

PayoffDiagramonNaturalResourceFirms

Aswath Damodaran

39

Value of estimated reserve of natural resource

Net Payoff onExtraction

Cost of Developing Reserve

EstimatingInputsforNaturalResourceOptions

Input Estimation Process

1. Value of Available Reserves of the Resource • Expert estimates (Geologists for oil..); Thepresent value of the after-tax cash flows fromthe resource are then estimated.

2. Cost of Developing Reserve (Str ike Price) • Past costs and the specifics of the investment

3. Time to Expiration • Relinqushment Period: if asset has to berelinquished at a point in time.

• Time to exhaust inventory - based uponinventory and capacity output.

4. Variance in value of underlying asset • based upon variability of the price of theresources and variability of available reserves.

5. Net Production Revenue (Dividend Yield) • Net production revenue every year as percentof market value.

6. Development Lag • Calculate present value of reserve based uponthe lag.

41

ValuingGulfOil

Aswath Damodaran

41

¨ GulfOilwasthetargetofatakeoverinearly1984at$70pershare(Ithad165.30millionsharesoutstanding,andtotaldebtof$9.9billion).¤ Ithadestimatedreservesof3038millionbarrelsofoilandtheaveragecostofdevelopingthesereserveswasestimatedtobe$10abarrelinpresentvaluedollars(Thedevelopmentlagisapproximatelytwoyears).

¤ Theaveragerelinquishmentlifeofthereservesis12years.¤ Thepriceofoilwas$22.38perbarrel,andtheproductioncost,taxesandroyaltieswereestimatedat$7perbarrel.

¤ Thebondrateatthetimeoftheanalysiswas9.00%.¤ Gulfwasexpectedtohavenetproductionrevenueseachyearofapproximately5%ofthevalueofthedevelopedreserves.Thevarianceinoilpricesis0.03.

42

ValuingUndevelopedReserves

Aswath Damodaran

42

¨ Inputsforvaluingundevelopedreserves¤ Valueofunderlyingasset=Valueofestimatedreservesdiscountedbackforperiod

ofdevelopmentlag=3038*($22.38- $7)/1.052 =$42,380.44¤ Exerciseprice=Estimateddevelopmentcostofreserves=3038*$10=$30,380

million¤ Timetoexpiration=Averagelengthofrelinquishmentoption=12years¤ Varianceinvalueofasset=Varianceinoilprices=0.03¤ Risklessinterestrate=9%¤ Dividendyield=Netproductionrevenue/Valueofdevelopedreserves=5%

¨ Basedupontheseinputs,theBlack-Scholesmodelprovidesthefollowingvalueforthecall:d1=1.6548 N(d1)=0.9510d2=1.0548 N(d2)=0.8542CallValue=42,380.44exp(-0.05)(12)(0.9510)-30,380(exp(-0.09)(12) (0.8542)

=$13,306million

43

ValuingGulfOil

Aswath Damodaran

43

¨ Inaddition,GulfOilhadfreecashflows tothefirmfromitsoilandgasproductionof$915millionfromalreadydevelopedreservesandthesecashflows arelikelytocontinuefortenyears(theremaininglifetimeofdevelopedreserves).

¨ Thepresentvalueofthesedevelopedreserves,discountedattheweightedaveragecostofcapitalof12.5%,yields:¤ Valueofalreadydevelopedreserves=915(1- 1.125-10)/.125=$5065.83

¨ AddingthevalueofthedevelopedandundevelopedreservesValueofundevelopedreserves =$13,306millionValueofproductioninplace =$5,066millionTotalvalueoffirm =$18,372millionLessOutstandingDebt =$9,900millionValueofEquity =$8,472millionValuepershare =$8,472/165.3 =$51.25