A ccountingCentury 21 - ngl.cengage.comngl.cengage.com/assets/downloads/c21_PRO0000009057/... ·...

8

Century 21 A ccounting 11e Teaching Students Accounting since 1903 Get Your Students Certified Correlated to Accounting I, II, and Advanced Accounting Precision Exams!

Transcript of A ccountingCentury 21 - ngl.cengage.comngl.cengage.com/assets/downloads/c21_PRO0000009057/... ·...

Century 21Accounting 11e

Teaching Students Accounting since 1903

Get Your Students CertifiedCorrelated to Accounting I, II, and

Advanced Accounting Precision Exams!

2 Innovate with Century 21 Accounting 11e today! NGL.Cengage.com/Accounting

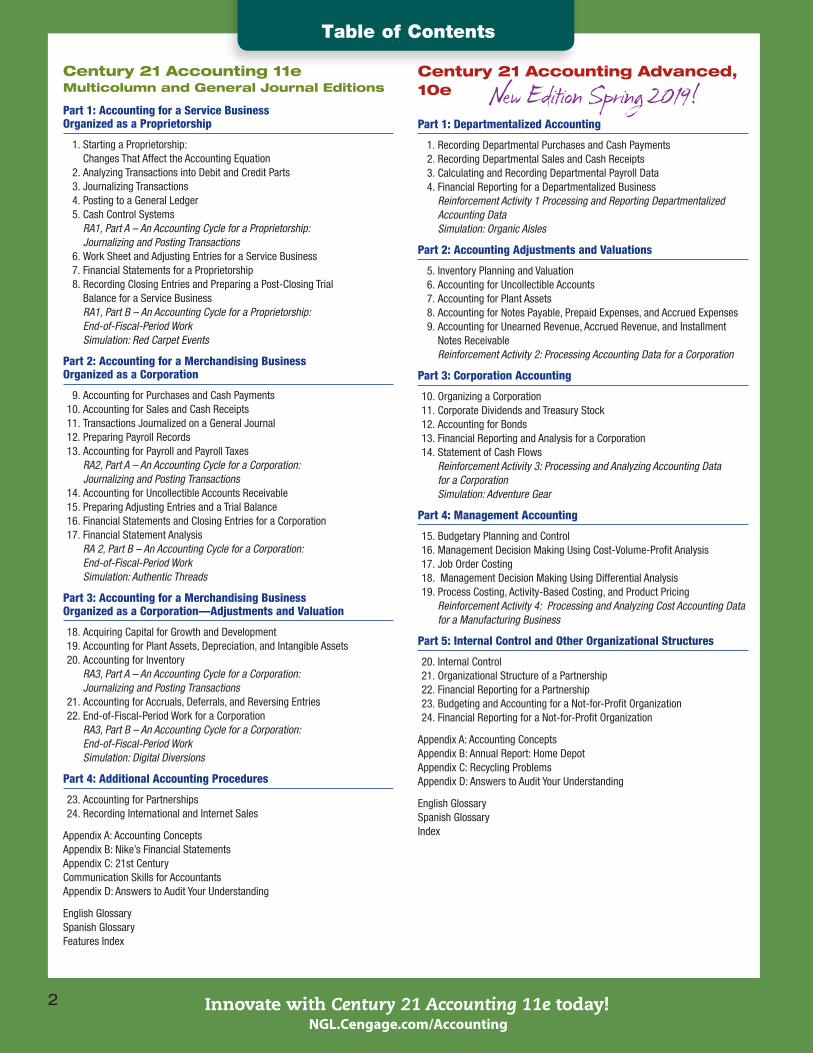

Century 21 Accounting 11eMulticolumn and General Journal Editions

Part 1: Accounting for a Service Business Organized as a Proprietorship

1. Starting a Proprietorship: Changes That Affect the Accounting Equation

2. Analyzing Transactions into Debit and Credit Parts 3. Journalizing Transactions 4. Posting to a General Ledger 5. Cash Control Systems

RA1, Part A – An Accounting Cycle for a Proprietorship: Journalizing and Posting Transactions

6. Work Sheet and Adjusting Entries for a Service Business 7. Financial Statements for a Proprietorship 8. Recording Closing Entries and Preparing a Post-Closing Trial

Balance for a Service BusinessRA1, Part B – An Accounting Cycle for a Proprietorship: End-of-Fiscal-Period WorkSimulation: Red Carpet Events

Part 2: Accounting for a Merchandising Business Organized as a Corporation

9. Accounting for Purchases and Cash Payments 10. Accounting for Sales and Cash Receipts 11. Transactions Journalized on a General Journal 12. Preparing Payroll Records 13. Accounting for Payroll and Payroll Taxes

RA2, Part A – An Accounting Cycle for a Corporation: Journalizing and Posting Transactions

14. Accounting for Uncollectible Accounts Receivable 15. Preparing Adjusting Entries and a Trial Balance 16. Financial Statements and Closing Entries for a Corporation 17. Financial Statement Analysis

RA 2, Part B – An Accounting Cycle for a Corporation: End-of-Fiscal-Period Work Simulation: Authentic Threads

Part 3: Accounting for a Merchandising Business Organized as a Corporation—Adjustments and Valuation

18. Acquiring Capital for Growth and Development 19. Accounting for Plant Assets, Depreciation, and Intangible Assets 20. Accounting for Inventory

RA3, Part A – An Accounting Cycle for a Corporation: Journalizing and Posting Transactions

21. Accounting for Accruals, Deferrals, and Reversing Entries 22. End-of-Fiscal-Period Work for a Corporation

RA3, Part B – An Accounting Cycle for a Corporation: End-of-Fiscal-Period Work Simulation: Digital Diversions

Part 4: Additional Accounting Procedures

23. Accounting for Partnerships 24. Recording International and Internet Sales

Appendix A: Accounting ConceptsAppendix B: Nike’s Financial StatementsAppendix C: 21st CenturyCommunication Skills for AccountantsAppendix D: Answers to Audit Your Understanding

English GlossarySpanish GlossaryFeatures Index

Century 21 Accounting Advanced, 10e

Part 1: Departmentalized Accounting

1. Recording Departmental Purchases and Cash Payments 2. Recording Departmental Sales and Cash Receipts 3. Calculating and Recording Departmental Payroll Data 4. Financial Reporting for a Departmentalized Business

Reinforcement Activity 1 Processing and Reporting Departmentalized Accounting DataSimulation: Organic Aisles

Part 2: Accounting Adjustments and Valuations

5. Inventory Planning and Valuation 6. Accounting for Uncollectible Accounts 7. Accounting for Plant Assets 8. Accounting for Notes Payable, Prepaid Expenses, and Accrued Expenses 9. Accounting for Unearned Revenue, Accrued Revenue, and Installment

Notes Receivable Reinforcement Activity 2: Processing Accounting Data for a Corporation

Part 3: Corporation Accounting

10. Organizing a Corporation 11. Corporate Dividends and Treasury Stock 12. Accounting for Bonds 13. Financial Reporting and Analysis for a Corporation 14. Statement of Cash Flows Reinforcement Activity 3: Processing and Analyzing Accounting Data

for a Corporation Simulation: Adventure Gear

Part 4: Management Accounting

15. Budgetary Planning and Control 16. Management Decision Making Using Cost-Volume-Profit Analysis 17. Job Order Costing 18. Management Decision Making Using Differential Analysis 19. Process Costing, Activity-Based Costing, and Product Pricing Reinforcement Activity 4: Processing and Analyzing Cost Accounting Data

for a Manufacturing Business

Part 5: Internal Control and Other Organizational Structures

20. Internal Control 21. Organizational Structure of a Partnership 22. Financial Reporting for a Partnership 23. Budgeting and Accounting for a Not-for-Profit Organization 24. Financial Reporting for a Not-for-Profit Organization

Appendix A: Accounting ConceptsAppendix B: Annual Report: Home DepotAppendix C: Recycling ProblemsAppendix D: Answers to Audit Your Understanding

English GlossarySpanish GlossaryIndex

Table of Contents

New Edition Spring 2019!

3Innovate with Century 21 Accounting 11e today! NGL.Cengage.com/Accounting

Transform Your High School Accounting Course with Century 21 Accounting, the leader in high school accounting education for more than 100 years.

Automated simulations give your students hands-on, real-world experience in accounting practice. Automated simulations have been updated (1) to be available inside C21 Accounting MindTap courses, (2) using HTML5 for better functionality, (3) with a modern interface that’s easy to use and simulates professional software, (4) and to allow you to pull a click stream report showing which steps students had trouble with in a simulation and allow you to watch a video of the student’s attempt for missed tasks.

z First Year

Simulation 1: Red Carpet EventsStudents encounter accounting principles and practical applications as they experience the challenges of operating an event-planning service business organized as a proprietorship. Students complete the simulation after Chapter 8. Estimated completion time: 4-8 hours

Simulation 2: Authentic ThreadsStudents bring fashion trends into the world of accounting while they practice accounting applications in this dynamic merchandising business organized as a corporation. Students complete the simulation after Chapter 17. Completion time 10-17 hours.

Simulation 3: Digital Diversions Students go digital in this engaging simulation with the latest retail software, cell phones, video cameras, music, and more in this merchandising business organized as a corporation. Students complete the simulation after Chapter 22. Estimated completion time: 10-17 hours

z Advanced

Simulation 1: Organic AislesStudents encounter accounting principles and practical applications as they experience the challenges of operating a departmentalized organic grocery store organized as a corporation. The company sells produce and grocery items. Students complete the simulation after Chapter 4. Estimated completion time: 10-20 hours

Simulation 2: Adventure GearStudents will sell extreme sports equipment while they practice accounting applications in this dynamic merchandising business organized as a corporation. Students complete the simulation after Chapter 14. Estimated completion time: 10-20 hours

Bring Accounting Practices to Life with Relevant Simulations

4 Innovate with Century 21 Accounting 11e today! NGL.Cengage.com/Accounting

Forensic Accounting presents criminal investigations involving fraud, providing students the opportunity to apply what they’re learning in class to a real-world scenario. Students will examine the fraud scenarios using

Excel® to analyze the data and continue the investigation.

Why Accounting? provides examples of how accounting skills are applicable in a variety of business situations. Tied to the National Career Clusters, this feature illustrates how accounting knowledge transfers into the workplace and validates accounting’s importance in the marketplace.

Careers in Accounting, designed to encourage students to think about their future in accounting, features a broad range of careers in the

accounting field and promotes accounting as a profession through one-on-one interviews with various accounting professionals.

48

FORENSIC ACCOUNTINGTheForensicAccountingactivitiesinthistextbookexposestudentstothetwopri-marycategoriesoffraud:fraudulentfinan-cialstatementsandoccupationalfraud.Ineachcase,studentsaregiventheopportu-nitytoplaytheroleofaforensicaccountant,usingExceltoolstoanalyzedata.Thisactivitysetsthetonefortheremaining11featuresinthetextbook.AlthoughtheIvarKreugerfraudoccurredearlylastcentury,itsinfluenceonrulesandlawsforfinancialreportingcontinuetothisday.Otherfeatureswillsummarizemorecurrentfrauds,includ-ingEnron,WorldCom,andHealthSouth,anddiscusshowthesefraudshavemotivatedchangesinrulesandregulations.ThePeter’sPoolsactivityattachedtothisfeaturerequiresstudentstousetheMONTHfunctionandtheSubtotaltooltoanalyzesales.Studentsdiscoverthattheowner,PeterWebb,appearstohaverecordedfalsesaleslateinDecembertoinflaterevenue.

Answer:Answerswillvary.

1.Saleshaveincreasedduringtheyear,increasingfrom$525.00inMayto$2,625.00inNovember.Duringthistime,thecompanyappearstohaveincreaseditspricefrom$100.00to$125.00pervisit.However,inDecember,salesspikedto$5,775.00asaresultofanotherapparentrateincrease,to$150.00pervisit,andasig-nificantincreaseinthenumberofclients.ThreefactssuggestthatDecembersaleshavebeenfalsified:(1)OverhalfofDecembersaleswererecordedafterDecember15.(2)AsaleoccurredonDecember25.(3)Asmanyassevensaleswererecordedonasingleday,December26.Furtherinvestigationshouldbeconductedtodeterminethevalidityofthesetransactionsbeforerelyingonthisinformationtosupportthepurchaseofthecompany.

2.Thetransactionscouldbesumma-rizedbytheDatecolumntoquan-tifythenumber(count)ofdailysales.Thisanalysiswouldidentifyotherdateswhereitwouldbediffi-cult,ifnotimpossible,forMr. Webbtocompletethatnumberofthree-hourcleaningprocedures.

Excelskillstaught:subtotals,MONTHfunction

FORMATIVE ASSESSMENT• Thisisanongoingprocess.Circulatethroughtheclassroomorlab,observingwhichstudentshaveproblemswiththeassignments.

• Troubleshooting:Makesurestudentscancorrectlyanalyzeeachtransactionstatementusingthefourquestionsintroducedinthislesson.Studentsmayhavetrouble(1)rememberingthatexpensesdecreaseowner’sequityor(2)rememberingthatexpenseaccountsshouldbedebited.• AssessstudentunderstandingbycheckingsolutionstoIndependentPracticeassignmentsandobservingtheiranswerstotheTermReviewandAuditYourUnderstandingquestions.

48 Chapter 2 Analyzing Transactions into Debit and Credit Parts

Pyramid Schemes

In 1912, Ivar Kreuger began his quest to take control of the European match

market. He borrowed money and sold stock in the company to buy out his competitors. After World War I, he loaned money to war-torn countries that dropped trade restrictions that had prevented his company from entering their markets. He also bribed government officials to become the sole provider of matches in that country. He later expanded his empire by purchasing a construction company in the United States.

The stock of the company was widely owned and provided investors with a high return on their investments. Everyone wanted to own a piece of his company. Kreuger’s fame and fortune landed him on the cover of Time magazine. He was welcome at the White House and enjoyed a lavish lifestyle including a Park Avenue penthouse in New York City furnished with paint-

ings by Rembrandt.

the pyramID COLLapsesUnknown to the public and undetected by accoun-tants, Kreuger was running a fraud known as a pyramid scheme. Investors being paid a return on their investment from the earnings of the business are, in fact, being paid with money contributed by new investors. The scheme is destined to collapse when the new investors are no longer willing to invest.

The stock market crash of 1929 and the Great Depression left few banks and individuals with any money to invest in Kreuger’s company. As rumors of his financial troubles grew, the value of the company’s stock tumbled. Unable to continue the pyramid scheme, Kreuger committed suicide in 1932.

In response to public outcry, Congress passed the Securities Act of 1933 that established the Securities and Exchange Commission and increased the amount and quality of information companies must provide to investors.

FOreNsIC aCCOUNtING aCtIvItIesPublic outcry over the financial disasters of the early twenty-first century—Enron and WorldCom in particular—led Congress to pass the Sarbanes-Oxley Act in the hope that these disasters would never be repeated.

The Forensic Accounting activities in this text-book highlight famous frauds and how Congress and the accounting profession have reacted by reforming laws governing financial reporting infor-mation. You will also learn about typical occupa-tional frauds involving employees stealing from their employers. An accountant who combines accounting and investigating skills to uncover fraud-ulent business activity, or to prevent such activity, is called a forensic accountant.

aCtIvIty

Peter Webb began his pool maintenance business in May. He visits each of his clients once a month for a three-hour cleaning procedure. Wanting to expand his business, he has provided Madilyn Lee, a potential investor, with financial informa-tion indicating that he is earning revenue of nearly $6,000 per month. Ms. Lee has asked you to analyze the information and provide her with a recommendation.

INstrUCtION

Open the spreadsheet FA_CH02. Follow the steps on the Instructions tab. After analyzing the data, answer the following questions:1. Should Ms. Lee invest in Mr. Webb’s business?

Write an e-mail to Ms. Lee that summarizes your findings and conclusion.2. What other analysis could be performed using

the Subtotal tool that would support your findings?

Source: Called to Account: Financial Frauds That Shaped the Accounting Profession, 2nd ed., Paul M Clikeman, Routledge (New York, New York), 2013.

FORENSIC ACCOUNTING

65424_ch02_hr_030-055.indd 48

10/6/17 3:21 PM

48

65431_ch02_hr_029a-055.indd 48

10/6/17 3:23 PM

Not For Sale

© C

enga

ge L

earn

ing,

Inc.

Thi

s con

tent

is n

ot fi

nal a

nd m

ay n

ot m

atch

the

publ

ishe

d pr

oduc

t.

24

Accounting is a language used to communicate finan-

cial information so that individuals can make informed

personal and business decisions. Financial information

is communicated by using a planned accounting system

to record, analyze, and interpret financial information.

In this chapter, you have learned that the accounting equ-

ation is stated as: Assets Liabilities Owner’s Equity5 1 .

This equation must remain in balance at all times. This

means that the left side of the equation (assets) must always

equal the right side of the equation (liabilities 1 owner’s

equity). As transactions occur, they are analyzed to demon-

strate their effect on the accounting equation while keeping

it balanced.

ChaPter SuMMary

ma

xx

IgO

/Sh

utt

er

StO

ck

.cO

m

What Is GAAP?

GAAP, or Generally Accepted

Accounting Principles, defines the

standards and rules that accountants

follow when reporting financial activities

in the United States. Important business

decisions are based on these financial

data. GAAP principles provide consistency

in reporting so companies can be com-

pared. For example, Brad is evaluating

whether to invest in Hewlett-Packard or

Dell Inc. He compares financial information

from both companies. Since both compa-

nies follow GAAP, Brad is assured that the

financial data being evaluated are generated

consistently. Therefore, he can make a better

business decision.Many different organizations have con-

tributed to the rules over the years; however, since

1973, the Financial Accounting Standards Board

(FASB) has been granted the authority by the Secu-

rities and Exchange Commission (SEC) to determine

GAAP. GAAP has been the uniformity standard for

U.S. companies. However, as many as 100 other

countries follow another set of accounting rules and

standards called International Financial Reporting

Standards (IFRS). IFRS are set by the International

Accounting Standards Board (IASB). The SEC has

recognized that global business opportunities and

international competition present the need for a

single set of accounting standards.

INstrUCtIONs

Describe other situations in which consistency in

standards helps to make informed comparisons and

decisions.

EXPLORE ACCOUNTINg

24 Chapter 1 Starting a Proprietorship: Changes That Affect the Accounting Equation

65424_ch01_hr_002-029.indd 24

9/30/17 8:35 PM

cLOsuRE

• Remind students that the accounting

equation will be used throughout the

study of accounting.

• Remind students that many transac-

tions affect the capital account.

• Remind students of the difference

between accounts payable (suppliers)

and accounts receivable (customers).

Have students draw a diagram

summarizing the types of

transactions that increase and

decrease owner’s equity.

Essential Questions

• As the owner of a service business, how

mightIincreasemyowner’sequity?

• Notallbusinessesextendthe“buynow,

paylater”option.HowwillIdetermine

when it would be best to allow my

customerstobuyonaccount?

• How will I determine when to buy on

account and the maximum liabilities I

shouldcarry?

EXtEndEd LEaRnIng

• Review A Look at Accounting Software

onpage23.

• AssignExploreAccountingonpage24.

ExpLoRE AccounTIng

Answers will vary but may include

ingredient listings and weights marked on

packages.

If desired, you could suggest current news

articles pertaining to business’s views of

the IFRS.

IndEPEndEnt PRactIcE

• Assign Mastery Problem 1-M for students

as a culminating problem that combines

all transactions from the chapter.

• Assign Challenge Problem 1-C to students

who work at an accelerated pace.

Students will learn to apply the concepts

Business Entity and Unit of Measurement

because the problem requires them

to identify which transactions should

be recorded by the business and what

amount to use for the transaction.

• Students can access Online Working

Papers to work end-of-chapter

problems on the computer.

• Students can access the website for the

Review and Quizzing activities.

• Assign Study Guide 1.

24

65431_ch01_hr_002a-029.indd 24

9/30/17 9:00 PM

Not For Sale

© C

enga

ge L

earn

ing,

Inc.

Thi

s con

tent

is n

ot fi

nal a

nd m

ay n

ot m

atch

the

publ

ishe

d pr

oduc

t.

12

12

Ste

Ph

en

cO

Bu

rn

/Sh

utt

er

StO

ck

.cO

m

Careers In AccountingSo You Want to Be an accountant

Many high school students consider a career in accounting. However, not many under-stand the variety of positions that are available in the field of accounting or the differences in the duties performed. The range of positions also comes with a range of educational and

experience requirements and a corresponding range of compensation.Many of the accounting-related job titles in a company can be arranged in a hierarchy based on educational requirements and average salary. A typical hierarchy is given below.The higher the position on the chart, the

higher the level of education and experience required for the position and the higher the level of compensation. For example, at the top of the chart, a CEO (Chief Executive Officer) and a CFO (Chief Financial Officer) would typically earn higher salaries than positions further down on the chart in the same company.

There are many accounting fields that are not related to any one company. These include auditor, forensic accountant, government accountant, and accountants in education. Each of these areas has its own education and experi-ence requirements.

Salary range: Salaries in the broad field of accounting range from $35,000 to over $200,000.

Qualifications: Educational requirements range from a high school accounting course to a four-year degree and higher. Special certifications can be acquired, which usually increase the sal-ary received.

Occupational Outlook: The projected growth in accounting positions varies, but many areas of accounting are expected to grow by up to 13% by 2024.Source: O*Net Online (http://www.onetonline.org).

©M

ILEN

NY,

ISTO

CK

Payroll ClerkAP/AR Clerk

Bookkeeper

GeneralLedger

AccountantTax

AccountantManagementAccountant

InternationalAccountant

InternalAuditor

Controller

CFO

CEO

65424_ch01_hr_002-029.indd 12

9/30/17 8:35 PM

careers In AccountingSuggest that students research one of the accounting positions on the flowchart to determine educational requirements and salary ranges. Answers will vary depending on the accounting position researched.

12

65431_ch01_hr_002a-029.indd 12

9/30/17 9:00 PM

Not For Sale

© C

enga

ge L

earn

ing,

Inc.

Thi

s con

tent

is n

ot fi

nal a

nd m

ay n

ot m

atch

the

publ

ishe

d pr

oduc

t.

• accounting• accounting system

• financial statements

• net worth statement

• asset• liability• personal net worth

• equity• ethics• business ethics

• service business

• proprietorship• business plan• GAAP

• equities• owner’s equity

• accounting equation

• transaction• account• account title• account balance

• capital account

• creditor• revenue• sale on account

• expense• withdrawals

terraCycle

millions of filters throughout the world. The tobacco

attached to the filters is recycled as compost, and the

filters are recycled into industrial products.

TerraCycle also has a program that allows individuals

or groups to recycle many products that are not nor-

mally recycled. Hundreds of types of objects can be col-

lected and recycled in these Zero Waste Boxes. Some of

the more unusual items include action figures, art sup-

plies, backpacks, plastic bottle caps, candy and snack

wrappers, and flip-flops.

TerraCycle works to create ways to recycle products

and packaging that would otherwise end up in landfills.

In 2016, TerraCycle estimated that it had recycled

3.5 billion items of waste.

CrItICaL thINKING

1. How is social entrepreneurship different from non-

profit organizations?

2. Identify a problem in your local community and

create a solution for it by identifying a social

entrepreneurship.

Have you ever thought about owning your own busi-

ness? Someone who owns, operates, and takes

the risk of a business venture is called an entrepreneur.

America was built on the hard work of entrepreneurs as

many men and women pursued their dream of business

ownership by developing new ideas and turning them

into business opportunities.

The goal of a business entrepreneur is to seek eco-

nomic benefit. In recent years, a new type of entrepre-

neur has emerged. These new entrepreneurs are driven

by the same innovation and productivity, yet they seek

social value in addition to profits. These entrepreneurs

are also agents of change. They direct their entrepre-

neurial energy toward seeking solutions for society’s

problems.Tom Szaky is one of today’s leading social entrepre-

neurs. Tom entered Princeton University in 2001. As a

student there, he identified a need for pre- and post-

consumer packaging recycling for major manufacturers.

This led him to found TerraCycle, which he ran out of his

dorm room. Although TerraCycle is a for-profit business,

its main goal is to encourage manufacturers to reduce

waste connected with their products. Early in the orga-

nization’s life, TerraCycle was offered a $1 million grand

prize from a nationwide business-plan competition.

Although TerraCycle was on the verge of bankruptcy,

Tom turned down the prize because the investors

required the company to reduce its focus on environ-

mental responsibility.

In 2012, TerraCycle introduced the concept of col-

lecting and recycling cigarette filters. It was the first

company to do so and has collected hundreds of

K e y t e r m s

Accounting In The Real World

Ima

ge

cO

ur

teSy

Of

ter

ra

cy

cle

, te

rr

ac

yc

le.c

Om

Source: www.terracycle.com

5

65424_ch01_hr_002-029.indd 5

9/30/17 8:34 PM

• Make sure students understand the

primary difference between an entre-

preneur and an employee.

• Explain that many business opportuni-

ties exist for entrepreneurs but that

many lack the knowledge to set up an

accounting system, resulting in serious

financial mistakes.

answers

1. A social entrepreneurship and a

not-for-profit organization both

seek to solve social problems. This

is the sole purpose of a not-for-

profit organization. However,

a social entrepreneurship also

intends to make a profit for the

entrepreneur.

2. Answers will vary but might

include a business that provides

shelter or food for the homeless,

daycare services for working par-

ents, or job-hunting education for

the unemployed.

dIffEREntIatEd InstRuctIOn

Limited English Proficiency (LEP) students: It is important that all students master the accounting terms. Create a bulle-

tin board or Word Wall displaying accounting terms in English and other languages represented in the classroom. This activity

will also bring awareness to the globalization of business.

Accounting In

The Real World

5

65431_ch01_hr_002a-029.indd 5

9/30/17 9:00 PM

Not For Sale

© C

enga

ge L

earn

ing,

Inc.

Thi

s con

tent

is n

ot fi

nal a

nd m

ay n

ot m

atch

the

publ

ishe

d pr

oduc

t.

Transform Your Course by Bringing Accounting Practices to Life

“Too many times, I believe that students don’t know how or where they will ever use the material they are learning in high school. These features help to bring the real world into the classroom and provide purpose.”

Kevin Willson, York Suburban School District, York, PA

The 11th Edition has incorporated exercises using Tableau. Tableau allows students to become familiar with analytics of big data. Tableau exercises can be found in Think Like an Accountant and Forensic Accounting features.

Commercial technology, integrated into the end of each chapter, equips students to work with Microsoft Excel®, Sage 50, and QuickBooks®, with step-by-step instructions and the flexibility to use multiple versions of software.

Accounting in the Real World fascinating chapter openers spotlight actual businesses that interest students, such as TerraCycle, Target, McDonald’s, and GoPro, with intriguing questions that connect chapter topics to what’s driving business decisions and today’s organizations.

5Innovate with Century 21 Accounting 11e today! NGL.Cengage.com/Accounting

Transform Your Course by Bringing Accounting Practices to Life

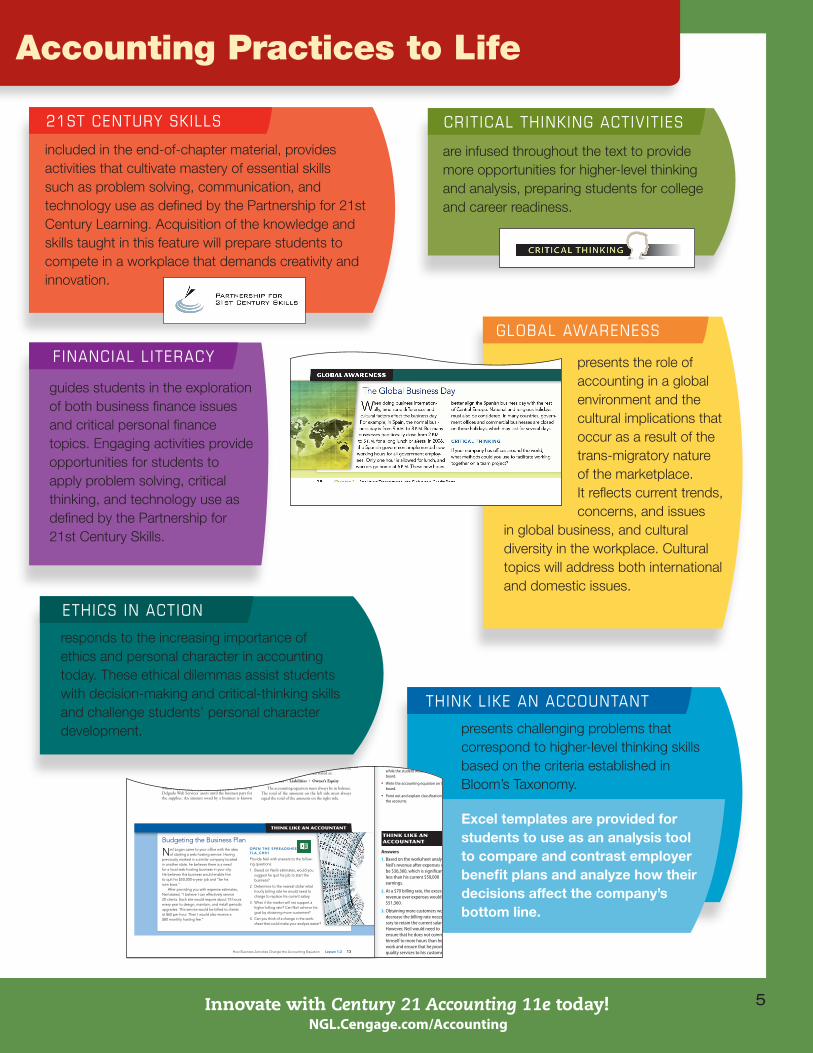

GLOBAL AWARENESS

presents the role of accounting in a global environment and the cultural implications that occur as a result of the trans-migratory nature of the marketplace. It reflects current trends, concerns, and issues

in global business, and cultural diversity in the workplace. Cultural topics will address both international and domestic issues.

CRITICAL THINKING ACTIVITIES

are infused throughout the text to provide more opportunities for higher-level thinking and analysis, preparing students for college and career readiness.

THINK LIKE AN ACCOUNTANT

presents challenging problems that correspond to higher-level thinking skills based on the criteria established in Bloom’s Taxonomy.

Excel templates are provided for students to use as an analysis tool to compare and contrast employer benefit plans and analyze how their decisions affect the company’s bottom line.

FINANCIAL LITERACY

guides students in the exploration of both business finance issues and critical personal finance topics. Engaging activities provide opportunities for students to apply problem solving, critical thinking, and technology use as defined by the Partnership for 21st Century Skills.

ETHICS IN ACTION

responds to the increasing importance of ethics and personal character in accounting today. These ethical dilemmas assist students with decision-making and critical-thinking skills and challenge students’ personal character development.

21ST CENTURY SKILLS

included in the end-of-chapter material, provides activities that cultivate mastery of essential skills such as problem solving, communication, and technology use as defined by the Partnership for 21st Century Learning. Acquisition of the knowledge and skills taught in this feature will prepare students to compete in a workplace that demands creativity and innovation.

How Business Activities Change the Accounting Equation Lesson 1-2 13

the accounting equation LO3

Delgado Web Services will own items such as cash and supplies that will be used to conduct daily operations. Anything of value that is owned is known as an asset. Assets have value because they can be used either to acquire other assets or to operate a business. For example, Delgado Web Services will use cash to buy supplies for the business. Delgado Web Services will then use the asset bought, supplies, to operate the web design service business.

Financial rights to the assets of a business are called equities. A business has two types of equities. (1) Equity of those to whom money is owed. For example, Delgado Web Services may buy some supplies and agree to pay for the supplies at a later date. The business from which supplies are bought will have a right to some of Delgado Web Services’ assets until the business pays for the supplies. An amount owed by a business is known

as a liability. (2) Equity of the owner. Michael Delgado owns Delgado Web Services and invests in the assets of the business. Therefore, he has the right to decide how the assets will be used. The amount remaining after the value of all liabilities is subtracted from the value of all assets is called owner’s equity.

The relationship among assets, liabilities, and own-er’s equity can be written as an equation. The equation showing the relationship among assets, liabilities, and owner’s equity is called the accounting equation. The accounting equation is most often stated as:

Assets = Liabilities + Owner’s Equity

The accounting equation must always be in balance. The total of the amounts on the left side must always equal the total of the amounts on the right side.

Assets

Left side amount$0

Liabilities Owner’s Equity

Right side amounts$0 $0

5

5

1

1

Budgeting the Business Plan

Neil Logan came to your office with the idea of starting a web hosting service. Having

previously worked in a similar company located in another state, he believes there is a need for a local web hosting business in your city. He believes this business would enable him to quit his $50,000-a-year job and “be his own boss.”

After providing you with expense estimates, Neil stated, “I believe I can effectively service 20 clients. Each site would require about 75 hours every year to design, maintain, and install periodic upgrades. This service would be billed to clients at $60 per hour. Then I would also receive a $80 monthly hosting fee.”

OPeN the sPreaDsheet tLa_Ch01

Provide Neil with answers to the follow-ing questions:

1. Based on Neil’s estimates, would you suggest he quit his job to start the business?

2. Determine to the nearest dollar what hourly billing rate he would need to charge to replace his current salary.

3. What if the market will not support a higher billing rate? Can Neil achieve his goal by obtaining more customers?

4. Can you think of a change in the work-sheet that could make your analysis easier?

THINK LIKE AN ACCOUNTANT

65424_ch01_hr_002-029.indd 13 9/30/17 8:35 PM

InPut• Explain that this lesson will present an

equation that shows the relationship among items of value a business has and the financial rights to the items.

• Remind students that an equation must have equal amounts on each side.

MOdEL• Invite a student to the board. Have

the class list assets they own while the student writes them on the board.

• Invite another student to the board. Have the class list liabilities they owe while the student writes them on the board.

• Write the accounting equation on the board.

• Point out and explain classifications of the accounts.

Think Like An Accountant

answers

1. Based on the worksheet analysis, Neil’srevenueafterexpenseswillbe$36,360,whichissignificantlyless than his current $50,000 earnings.

2. At a $70 billing rate, the excess of revenue over expenses would be $51,360.

3. Obtaining more customers would decrease the billing rate neces-sary to retain the current salary. However,Neilwouldneedtoensure that he does not commit himself to more hours than he can work and ensure that he provides quality services to his customers.

4. The excess of revenue over expenses could be changed to $50,000, and then the formula for the $60 billing rate could be changed to $50,000 plus the $72,840expenseslessthe$19,200hosting fees divided by the number of billable hours.

13

65431_ch01_hr_002a-029.indd 13 9/30/17 9:00 PM

Not For Sale

© C

enga

ge L

earn

ing,

Inc.

Thi

s con

tent

is n

ot fi

nal a

nd m

ay n

ot m

atch

the

publ

ishe

d pr

oduc

t.

6 Innovate with Century 21 Accounting 11e today! NGL.Cengage.com/Accounting

Transform Your Course with Century 21 Accounting MindTap

For Trial Access please visit NGL.Cengage.com/highschoolreview

MindTap helps you propel students from memorization to mastery. It’s the only online platform that gives you complete ownership of your course.

One Destination

MindTap offers an easy-to-use interface and serves as a single destination for teachers and students to access their eBook, Online Working Paper Assignments, study tools, and more. Organized by the structure of the Century 21 Accounting books, students navigate to each chapter to find content curated for your course.

MindTap is a personalized learning experience with relevant assignments that guide students to analyze, apply, and improve thinking. Teachers can measure and impact outcomes with ease.

with

Aplia-Powered Online Working Papers

Past users of Aplia Online Working Papers know how these assignments enhance the classroom experience by providing students with enhanced, immediate feedback that will provide students with additional instruction beyond right and wrong answers. They save teachers time with automatic grading and algorithmic problems, which offer students more practice. Online Working Papers mirror the C21 Accounting Print Working Papers, including:

▶ chapter tests

▶ online journals

▶ ledgers

▶ worksheets

▶ financial statements

▶ recycling papers

▶ and other forms

These Online Working Paper assignments are now INCLUDED within MindTap for Century 21 Accounting. This allows teachers to have all of their assessments in one location and make use of Aplia-powered performance reports as well as MindTap Analytics to truly gauge how their students are meeting course outcomes.

)))))))))))))))))))))

7Innovate with Century 21 Accounting 11e today! NGL.Cengage.com/Accounting

Take your Accounting Course to the Next Level!

View Student Performance and Engagement

MindTap for Century 21 Accounting with Aplia Online Working Papers provides a full view of your students.

Aplia-Powered Performance Reports in MindTap

▶ View Assignment Scores

• class average

• individual student

▶ View Question Scores within an Assignment

• class average

• individual student

▶ Performance Threshold Tool color codes scores and can be disabled or customized.

▶ Compare Students by the class average, time on task, and multiple attempts.

MindTap Progress App Analytics

▶ Track Student Scores for all Assignments

• class average

• individual student

▶ View Student Engagement

• time spent in course

• number of logins

• % of activities accessed including homework, tests, multimedia, and readings

MindTap for C21 Accounting Assignments beyond Online Working Papers:

▶ Animated Activities help students visualize accounting concepts

▶ Animated Activity Quizzes test students on those concepts

▶ End of Chapter Review are completed online for automatic feedback and grading

• Application Problems

• Mastery Problems

• Challenge Problems

)))5GL;5)GMNYEN85J,M)NMGEN!Q)%6"--$%1'0)

))))))))))))

)

“National Geographic”, “National Geographic Society” and the Yellow Border Design are registered trademarks of the National Geographic Society ® Marcas Registradas

Century 21 Accounting Multicolumn Journal 11e ©2019Item ISBNStudent Edition Complete Text, Chapters 1-24 9781337565424Student Edition + MindTap (1-year access) 9781337870603Teacher EditionsWraparound Teacher’s Edition 9781337565431Printed Working PapersChapters 1-17 9781337565530Chapters 18-24 9781337565547Chapters 1-24 bundle 9781337565554MindTap including SimulationsIncluding 1 simulation: Red Carpet Events 9780357032152Authentic Threads 9780357032183Digital Diversions 9780357032213Including 2 simulations: Red Carpet Events + Authentic Threads 9780357032244Red Carpet Events + Digital Diversions 9780357032275Authentic Threads + Digital Diversions 9780357032305Including all 3 simulations: Red Carpet Events, Authentic Threads, and Digital Diversions 9780357032336*For manual simulations and keys, please see Century 21 Accounting 10e update version

AssessmentCognero Test Bank Generator 9781337565523MindTapInstant Access MindTap Accounting for C21 Accounting MC 9781337565479

Century 21 Accounting General Journal 11e ©2019Item ISBNStudent Edition Complete Text, Chapters 1-24 9781337623124Student Edition + MindTap (1-year access) 9781337870641Teacher EditionsWraparound Teacher’s Edition 9781337623131Printed Working PapersChapters 1-17 9781337623230Chapters 18-24 9781337623247Chapters 1-24 bundle 9781337623254MindTap including SimulationsIncluding 1 simulation: Red Carpet Events 9780357027844Authentic Threads 9780357027882Digital Diversions 9780357027912Including 2 simulations: Red Carpet Events + Authentic Threads 9780357027943Red Carpet Events + Digital Diversions 9780357027974Authentic Threads + Digital Diversions 9780357028001Including all 3 simulations: Red Carpet Events, Authentic Threads, and Digital Diversions 9780357028032*For manual simulations and keys, please see Century 21 Accounting 10e update version

AssessmentCognero Test Bank Generator 9781337623223MindTapInstant Access MindTap Accounting for C21 Accounting GJ 9781337623179

Century 21 Accounting Advanced 10e ©2015Item ISBNStudent Edition Complete Text Chapters 1–24 9781111990640Teacher EditionsWraparound Teacher’s Edition 9781133103660 Instructor’s Resource CD 9781285073293 Instructor’s Resource Kit 9781133958512 Online Working PapersChapters 1–24 9781285847573Printed Working PapersChapters 1–14 9781133103684 Chapters 15–24 9781133103707 Chapters 1–24 bundle 9781285073286 Recycling Problems 9781111990930 Teacher Editions Working PapersTeacher’s Edition 1–14 9781133958536 Teacher’s Edition 15–24 9781133958529 Teacher’s Edition Recycling Problems 9781111990947 Automated Accounting OnlineAAO PAC for Textbook Problems 9781133944539Simulations Organic Aisles, Manual Simulation 9781133588276Organic Aisles, Automated Simulation w/ AAO 9781133588290 Adventure Gear, Manual Simulation 9781133588313 Adventure Gear, Automated Simulation w/ AAO 9781133588337 Simulation KeysTeacher’s Key, Organic Aisles, Manual Simulation 9781133588283 Teacher’s Key, Adventure Gear, Manual Simulation 9781133588320 AssessmentCengage Learning, powered by Cognero 9781285979663 Print Chapter and Part Tests 1-24 9781133103677 Teacher’s Edition Chapter Tests 1-24 9781111990923

Transform Your Course with Century 21 Accounting

For additional information, please contact your Sales Consultant at NGL.Cengage.com/RepFinder

Or visit us online at NGL.Cengage.com/Accounting for additional program information.