A Case Study Analysis on the Asian Financial Crisis of 1997 and Zapa Chemicals

44

12/27/2015 Case Study Analysis Case 1: Asian Crisis of 1997 Case 2: ZAPA Chemicals and BuBa Group Work United International University

-

Upload

sadman-ahmed -

Category

Economy & Finance

-

view

151 -

download

0

Transcript of A Case Study Analysis on the Asian Financial Crisis of 1997 and Zapa Chemicals

12/27/2015

Case Study Analysis Case 1: Asian Crisis of 1997

Case 2: ZAPA Chemicals and BuBa

Group Work United International University

Course Instructor: Muhammad Enamul Haque,

Assistant Professor,

School of Business & Economics,

UIU.

Prepared By:

Name University ID

Syed Mohammad Shoaib 111 122 188

Ferdous Ahmed 111 121 091

Sadman Shoumik Ahmed 111 121 187

Tariqul Hossain Tishad 111 121 502

Mahfuza Begum 111 121 385

Course Title: International Financial Management

Course Code: FIN – 4322

Type of course: Major

Credits: 3

Section: A

Class Room: 308

Trimester: Fall 2015

Submission Date: 27/12/2015

Contents

Letter of Transmittal ...................................................................................................................................... 3

Executive Summary ....................................................................................................................................... 4

Case 1: Government Intervention during the Asian Crisis ............................................................................. 5

Section 1 – Introduction ................................................................................................................................ 6

Problems ....................................................................................................................................................... 6

Section 2 – Background ............................................................................................................................... 10

Relevant Facts ............................................................................................................................................. 11

Section 3 – Solutions ................................................................................................................................... 15

Case 2: Zapa Chemical and BuBa ................................................................................................................. 35

Section 1 – Introduction .............................................................................................................................. 36

Problems ..................................................................................................................................................... 36

Section 2 – Background ............................................................................................................................... 37

Relevant Facts ............................................................................................................................................. 37

Section 3 – Solutions ................................................................................................................................... 39

Letter of Transmittal

25th December, 2015

Muhammad Enamul Haque,

Assistant Professor,

School of Business & Economics,

United International University.

Subject: Case Study Analysis.

Dear Sir,

This report is written in the academic context and is part of our course

requirement.

This report consists of the answers that explain what went wrong with the Asian

Crisis as well as Zapa Chemicals. We have given analysis from our own academic

knowledge as well as from outside sourced so as to make a complete answer.

We hope that this report was up with your expectations as we tried our best to

follow your guidelines.

We hope you will appreciate our effort. We also thank you wholeheartedly.

Yours sincerely,

Ferdous Ahmed. (On behalf of group)

Executive Summary

The first case is on a very broad context as it focuses on the economy as a

whole. The second case, however, is much narrower on the context as it looks

at the issues of a particular company in relation to the economy.

The Asian crisis was one of the worst financial disasters in the history of Thailand.

The investors moved away large sums money away, inflation spiraled out of

control, and it ultimately put pressure on the exchange rates of the Baht. Due to

Thailand’s problems alone, the effect of the crisis spread along different countries

in Asia. The impacts prove how integrated the economies of today are. Much of

the fault lies on the failed policies of the government and weak regulatory regime.

The exchange rate exposure and the legal hurdles can be quite a burden when

transferring funds across the borders. In the case of Zapa Chemicals, the tax

filing problem did not help them to transfer funds. They didn’t know when exactly

the funds would be available for receiving. The risk management of the firm is

quite a hefty task for foreign companies to successfully pursue.

Case 1: Government Intervention during the Asian Crisis

Section 1 – Introduction

The case is about the Asian crisis that occurred due to the financial crisis in

Thailand and the consequences that ensued in the other countries in Asia. The

crisis began in Thailand and spread in countries across East Asia. The investors

began investing in high volumes in the highly growing Thai economy and eventually

it led to a burst bubble. The government has a key role to play when an economy

is in turmoil. This case illustrates how the government’s intervention efforts failed

in the face of financial disaster that was real estate driven. The crisis is a proof

that government intervention isn’t necessarily successful, as the IMF bailed out

several countries that fell into the crisis.

Problems

1. Its high level of spending and low level of saving put upward pressure on

prices of real estate and products and on the local interest rate.

2. Normally, countries with high inflation tend to have weak currencies because

of forces from purchasing power parity. In Thailand’s case, however, the inflow

of funds provided Thai banks with more funds than the banks could use for

making loans. Consequently, in an attempt to use all the funds, the banks

made many very risky loans.

3. Commercial developers borrowed heavily without having to prove that the

expansion was feasible.

4. The large inflow of funds made Thailand more sensitive to a massive outflow

of funds if foreign investors ever lost confidence in the Thai economy.

5. Heavy borrowing by real estate companies and government occurred at

relatively high interest rates, making the debt expensive to the borrowers.

6. The loans may have seemed feasible based on the assumption that the

economy would continue its high growth, but such high growth could not be

sustainable.

7. As the supply of baht to be exchanged for dollars exceeded the U.S. demand

for baht in the foreign exchange market, the government eventually had to

surrender in its effort to defend the baht’s value.

8. This strategy backfired because the weakening of the baht forced these

corporations to exchange larger amounts of baht for the currencies needed

to pay off the loans. This led to higher cost of capital for the corporations.

9. The rescue package took time to finalize because Thailand’s government was

unwilling to shut down all the banks that were experiencing financial problems

as a result of their overly generous lending policies.

Spread of crisis throughout Southeast Asia

10. Like Thailand, the other Southeast Asian countries had very high growth in

recent years, which had led to overly optimistic assessments of future

economic conditions and thus to excessive loans being extended for projects

that had a high risk of default.

11. Thailand’s crisis made foreign investors realize that such a crisis could also

hit the other countries in Southeast Asia. Consequently, they began to withdraw

funds from these countries.

Impact of Asian Crisis in Hong Kong

12. The decline was primarily attributed to speculation that Hong Kong’s currency

might be devalued and that Hong Kong could experience financial problems

similar to the Southeast Asian countries.

Russia

13. As investors lost confidence in the Russian currency (the ruble), they began

to transfer funds out of Russia. In response to the downward pressure this

outflow of funds placed on the ruble

Korea

14. By November 1997, seven of South Korea’s conglomerates had collapsed. Due

to the collapse, the banks that financed the operations of the firms were stuck

with the equivalent of $52 billion in bad debt.

15. In November, South Korea’s currency (the won) declined substantially, and the

central bank attempted to use its reserves to prevent a free fall in the won

but with little success. It should have taken a lesson from the other countries

in Asia, instead of going for intervention.

16. This restriction (IMF conditions) resulted in some bankruptcies and

unemployment, as the banks could not automatically provide loans to all

conglomerates needing funds unless the funding was economically justified.

Latin America

17. Countries such as Chile, Mexico, and Venezuela were adversely affected

because they export products to Asia, and the weak Asian economies resulted

in a lower demand for the Latin American exports.

18. Latin American countries also got indirectly affected as some countries bought

from Asia due to cheap products which were cheaper than Latin American

products.

19. The adverse effects on Latin American countries put pressure on Latin

American currency.

20. The intervention was costly because it increased the cost of borrowing for

households, corporations, and government agencies in Brazil.

Europe

21. Europe experienced a reduced demand for their exports to Asia during the

crisis.

22. European banks were especially affected by the Asian crisis because they had

provided large loans to numerous Asian firms that defaulted.

United States

23. Stock prices of corporations fell. Many U.S. engineering and construction firms

were adversely affected as Asian countries reduced their plans to improve

infrastructure.

24. Some large U.S. commercial banks experienced significant stock price declines

because of their exposure (primarily loans and bond holdings) to Asian

countries.

Section 2 – Background

The causes of the debacle are many and disputed. Thailand's economy developed

into an economic bubble fueled by hot money. More and more was required as

the size of the bubble grew. The same type of situation happened in Malaysia,

and Indonesia, which had the added complication of what was called "crony

capitalism". The short-term capital flow was expensive and often highly conditioned

for quick profit. Development money went in a largely uncontrolled manner to

certain people only, not particularly the best suited or most efficient, but those

closest to the centers of power.

At the time of the mid-1990s, Thailand, Indonesia and South Korea had large

private current account deficits and the maintenance of fixed exchange rates

encouraged external borrowing and led to excessive exposure to foreign exchange

risk in both the financial and corporate sectors.

In the mid-1990s, a series of external shocks began to change the economic

environment – the devaluation of the China Yuan, and the Japanese yen due to

the Plaza Accord of 1985, raising of U.S. interest rates which led to a strong U.S.

dollar, the sharp decline in semiconductor prices; adversely affected their growth.

As the U.S. economy recovered from a recession in the early 1990s, the U.S.

Federal Reserve Bank under Alan Greenspan began to raise U.S. interest rates to

head off inflation.

This made the United States a more attractive investment destination relative to

Southeast Asia, which had been attracting hot money flows through high short-

term interest rates, and raised the value of the U.S. dollar. For the Southeast

Asian nations which had currencies pegged to the U.S. dollar, the higher U.S.

dollar caused their own exports to become more expensive and less competitive

in the global markets. At the same time, Southeast Asia's export growth slowed

dramatically in the spring of 1996, deteriorating their current account position.

Some economists have advanced the growing exports of China as a contributing

factor to ASEAN nations' export growth slowdown, though these economists

maintain the main cause of the crises was excessive real estate speculation.

China had begun to compete effectively with other Asian exporters particularly in

the 1990s after the implementation of a number of export-oriented reforms. Other

economists dispute China's impact, noting that both ASEAN and China experienced

simultaneous rapid export growth in the early 1990s.

Many economists believe that the Asian crisis was created not by market

psychology or technology, but by policies that distorted incentives within the

lender–borrower relationship. The resulting large quantities of credit that became

available generated a highly leveraged economic climate, and pushed up asset

prices to an unsustainable level. These asset prices eventually began to collapse,

causing individuals and companies to default on debt obligations.

Relevant Facts

Financial Crisis in Thailand

Prior to July 1997, however, Thailand’s currency was linked to the U.S. dollar,

which made Thailand an attractive site for foreign investors. This was the reason

for the large capital outflows.

On July 2, 1997, the baht was detached from the dollar.

As supply of the baht to be exchanged for dollars exceeded the US demand for

the baht in the foreign exchange market, the currency was overwhelmed by the

market forces. Therefore, the Thai government surrendered and let the currency

float in the market. In July 1997, the value of the baht plummeted. Over a 5-

week period, it declined by more than 20 percent against the dollar.

On July 2, 1997, the baht was detached from the dollar. Thailand’s central bank

then attempted to maintain the baht’s value by intervention.

Thailand’s central bank used more than $20 billion to purchase baht in the

foreign exchange market as part of its direct intervention efforts.

Thailand’s banks estimated the amount of their defaulted loans at over $30

billion.

On August 5, 1997, the IMF and several countries agreed to provide Thailand

with a $16 billion rescue package. Japan provided $4 billion, while the IMF

provided $4 billion.

Effect on Other Asian countries

In August 1997, Bank Indonesia (the central bank) used more than $500 million

in direct intervention to purchase rupiah in the foreign exchange market in an

attempt to boost the value of the rupiah.

On October 30, 1997, a rescue package for Indonesia was announced, but the

IMF and Indonesia’s government did not agree on the terms of the $43 billion

package until the spring of 1998.

Impact of the Asian Crisis on Hong Kong

On October 23, 1997, prices in the Hong Kong stock market declined by 10.2

percent on average; considering the 3 trading days before that, the cumulative

4-day effect was a decline of 23.3 percent.

Hong Kong used indirect intervention and it had to increase interest rates to

discourage investors from transferring their funds out of the country.

Impact of the Asian Crisis on Russia

IN July 1998, the IMF (with some help from Japan and the World Bank) organized

a loan package worth $22.6 billion for Russia.

In August 1998, Russia’s central bank intervened to prevent the ruble from

declining. But on August 26, however, it gave up its fight to defend the ruble’s

value, and market forces caused the ruble to decline by more than 50 percent

against most currencies on that day.

Impact of the Asian Crisis on South Korea

By November 1997, seven of South Korea’s conglomerates had collapsed. Due to

the collapse, the banks that financed the operations of the firms were stuck with

the equivalent of $52 billion in bad debt.

On December 3, 1997, the IMF agreed to enact a $55 billion rescue package for

South Korea.

Impact of the Asian Crisis on Japan

In April 1998, the Bank of Japan used more than $20 billion to purchase yen in

the foreign exchange market. Although, this effort to boost the yen’s value was

unsuccessful.

Impact of the Asian Crisis on China

Surprisingly, China did not experience the adverse economic effects of the Asian

crisis because it had grown less rapidly than the Southeast Asian countries in

the year prior to the crisis. This was also because lending wasn’t extravagant as

the Chinese government controlled most of the banks that provided credit to

support growth.

Impact on Latin American Countries

The central bank of Brazil used about $7 billion of reserves in a direct intervention

to buy the real in the foreign exchange market and protect the real from

depreciation.

Impact of the Asian Crisis on the United States

The effects of the Asian crisis were even felt in the United States. Stock values

of U.S. firms, such as 3M Co., Motorola, Hewlett-Packard, and Nike that conducted

much business in Asia declined.

Who was responsible?

The problems that occurred can’t be blamed upon a single party. They poured

their money into Thailand. Thai banks accepted the deposits and were sitting on

excess liquidity. Developers and corporations had a strong demand for loans. The

strong demand outweighed the supply of liquidity from banks. This led to high

interest rates and expensive loans. It was a ‘domino’ effect.

Investors – Investors were expecting the Thai economy to grow continually,

something which was not sustainable. The investors didn’t think rationally and

invested massive amounts of money, letting into their optimistic assumptions. The

investors were speculating and expected unprecedented levels of growth that

could not continue forever.

Banks – Banks had large deposits with them and they started to lend money

aggressively. In order to utilize the excess funds, banks make risky loans in a

very lax fashion. They didn’t properly assess the default risk of the borrowers.

Borrowers – The developers, corporations and even government agencies

capitalized on the opportunity and took loans while anticipating more growth.

They were caught in the momentum and expected the economy to grow for an

indefinite period of time. Even the government borrowed heavily to improve the

country’s infrastructure.

Section 3 – Solutions

Q1.1: Was the depreciation of the Asian currencies during the Asian crisis due

to trade flows or capital flows?

The baht depreciated as a result of the capital flows. The financial crisis started

with the capital flows. But various other countries faced a declining currency as

a result of the trade flows. But not all the Asian currencies depreciated due to

the capital flows. Different countries faced declining currencies due to different

types of flows.

Thailand – The baht experienced downward pressure in July 1997 as the foreign

investors recognized the weaknesses in the Thai economy. Due to the large sale

of Baht in the foreign exchange market, the value of baht went down. Hence, the

currency depreciated due to a large amount of capital outflow. The investors’

loss of confidence was the main reason behind the massive funds outflow.

Japan – Japan was particularly affected due to the dwindling exports to the Asian

countries. The depreciation in the currency value meant that the countries in

crisis had to pay more units per Japanese yen to import the products. The

demand for the Japanese products declined. Many Japanese corporations had

subsidiaries in these countries and the incomes had declined substantially when

it was converted back to the Japanese Yen. The depreciation of the Japanese

currency was due to the trade flow.

Southeast Asian Countries (Malaysia, Singapore, Philippines, Taiwan, Indonesia) –

These countries suffered because of a combination of capital as well as trade

flows. These countries were also similar to Thailand in that they had relatively

high interest rates, and their governments tended to stabilize their currencies.

Consequently, these countries had attracted a large amount of foreign investment

as well. Investors took lesson from the Thailand crisis and they moved their funds

out of their countries. Due to the crisis in Thailand, the demand for goods and

services from the neighboring countries tanked. The demand for their products

declined and hence their economies also faced economic crisis. The effects of

Thailand crisis were contagious to these Southeast Asian nations. Philippines

suffered severely as the demand for their products dropped and their economic

growth fell to virtually zero in 1998.

Hong Kong – The stock prices declined by 10.2 percent in 1997. The decline

occurred as speculators thought that the country’s currency could be devalued

and financial crisis could occur. The decline in Hong Kong occurred due to loss

of confidence.

Russia – The investors looked for other countries where the crisis could take

place. They speculated on Russia. As investors lost confidence in the Russian

currency (ruble), they began to transfer funds out of Russia. This downward

pressure on the currency caused the crisis and the Russian central bank engages

in direct intervention.

Q1.2: Why do you think the degree of movement over as short period may

depend on whether the reason is trade flows or capital flows?

The degree of movement within a short period of time, no doubt, depends on

whether it’s a capital flow or trade flow. Both these flows are different in nature

and as a result, they have different implications too. The capital flow can take

place instantly over a telecommunication network and the exchange rate

adjustments take place immediately. The trade flows do not change immediately

due to a crisis. The effects of the trade flows take time to capitalize and the

exchange rate changes slowly. The effects take place within a longer period.

Q2: Why do you think the Indonesian rupiah was more exposed to an abrupt

decline in value than the Japanese yen during the Asian crisis (even if their

economies experienced the same degree of weakness)?

Factors suggesting Indonesian Rupiah was more exposed to decline:-

1. There was severe political uncertainty and lack of determination on the part

of the government program for solving the crisis.

2. Investors didn’t trust the government and hence they had a lack of confidence.

This lack of confidence led to many problems and set off a chain reaction.

3. Sixteen financially distressed private banks closed down in November 1997 as

their loans weren’t repaid by the clients. This closure of banks led to deposit

runs by the customers and capital flights which was the ultimate cause of

external liquidity crunch.

4. Imports became restrained as there was an acute shortage of foreign reserves

to pay for it. Banks were in a turbulent situation as they accepted letters of

credits and later didn’t recover their money.

5. The fear of further currency depreciation put exchange rate and interest rates

under even more pressure.

6. The government made a decision to move the deposits from the commercial

banks to central bank and this worsened the liquidity crunch further.

7. The weather related problem from El Nino which caused the forest fires and

drought affected the agricultural sector. Rice production decreased by almost

10% leading to more problems like reduced exports and higher local prices.

8. Countries which imported products from Indonesia were also in recession. In

particular, Japan and South Korea were in financial crisis. This led to lower

exports, while deteriorating the economy even more. Indonesia was also

dependent on oil exports. At this particular time oil prices fell.

9. The economic problem was compounded by political uncertainty because of

the elections in 1997. President Suharto resigned amid rising prices and

unemployment in the country.

Factors suggesting that the Japanese economy was stronger

1. Japan didn’t have high level of investment from the foreign investors, and also

had a more export oriented economy.

2. There was less political uncertainty in the country.

3. Foreign investors didn’t bring in ‘hot money’, so the chances of capital flight

couldn’t hurt the economy. Japan was more susceptible to trade flows rather

than capital flows.

4. There was no severe weather problem affecting business.

5. There was no fear or lack of confidence.

6. Japan was more dependent on the local manufacturing industries and overseas

subsidiaries which made it stronger than Indonesia. Indonesia was more

dependent exports for its GDP.

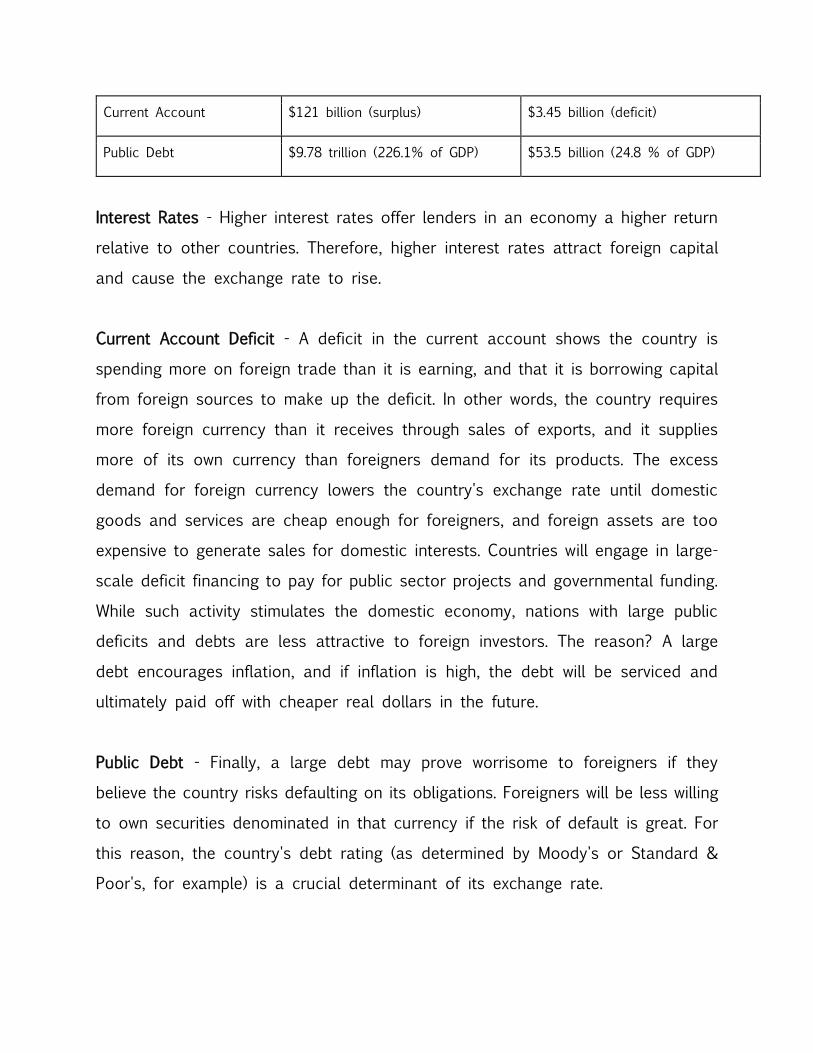

Exchange rate determinants table

Japan Indonesia

GDP $4.32 trillion $215.7 billion

Inflation 1.80% 10.31%

Real Interest Rates 1.8% 8.2%

Current Account $121 billion (surplus) $3.45 billion (deficit)

Public Debt $9.78 trillion (226.1% of GDP) $53.5 billion (24.8 % of GDP)

Interest Rates - Higher interest rates offer lenders in an economy a higher return

relative to other countries. Therefore, higher interest rates attract foreign capital

and cause the exchange rate to rise.

Current Account Deficit - A deficit in the current account shows the country is

spending more on foreign trade than it is earning, and that it is borrowing capital

from foreign sources to make up the deficit. In other words, the country requires

more foreign currency than it receives through sales of exports, and it supplies

more of its own currency than foreigners demand for its products. The excess

demand for foreign currency lowers the country's exchange rate until domestic

goods and services are cheap enough for foreigners, and foreign assets are too

expensive to generate sales for domestic interests. Countries will engage in large-

scale deficit financing to pay for public sector projects and governmental funding.

While such activity stimulates the domestic economy, nations with large public

deficits and debts are less attractive to foreign investors. The reason? A large

debt encourages inflation, and if inflation is high, the debt will be serviced and

ultimately paid off with cheaper real dollars in the future.

Public Debt - Finally, a large debt may prove worrisome to foreigners if they

believe the country risks defaulting on its obligations. Foreigners will be less willing

to own securities denominated in that currency if the risk of default is great. For

this reason, the country's debt rating (as determined by Moody's or Standard &

Poor's, for example) is a crucial determinant of its exchange rate.

Q3: During the Asian crisis, direct intervention did not prevent depreciation of

currencies. Offer your explanation for why the interventions did not work.

Reasons for failure of direct intervention

The countries didn’t have enough reserves to put an upward pressure on their

currencies.

The currencies were overwhelmed by the free market forces and the direct

intervention wasn’t enough to offset the effect of the downward pressure

placed on the currencies.

The supply and demand of the Thai currency was mismatched. The supply of

baht to be exchanged for dollars exceeded the U.S. demand for baht in the

foreign exchange market, the government eventually had to surrender in its

effort to defend the baht’s value

The direct intervention usually works well when the government tries to

maintain the currency relative to a few currencies. But since the financial crisis

had occurred in many countries around the world, it was difficult to intervene

and cushion the effect of the depreciation of the currencies.

Q4.1: During the Asian Crisis, some local firms in Asia borrowed U.S. dollars

rather than local currency to support local operations. Why would they borrow

dollars when they really needed their local currency to support operation?

Corporations borrowed in other currencies, but they primarily borrowed in U.S.

dollars. They borrowed from foreign countries as the interest rates were high in

their home countries. The local interest rates were high because it had to be

compensated for the rising inflation. Corporations took advantage of this

opportunity to decrease their cost of capital by borrowing overseas. Furthermore,

at the peak of the economic boom, the local currencies were quite strong relative

to the dollar. This currency stability led the corporations to borrow in U.S. dollars.

Q4.2: Why did this strategy backfire?

However, the strategy backfired because of the weakening of the baht forced

these corporations to exchange larger amounts of baht for the currencies needed

to pay off the loans. This increased the cost of capital for the firms. 30 billion…

Q5.1: The Asian crisis showed that a currency crisis could affect interest rates.

Why did the crisis put upward pressure on interest rates in Asian countries?

When the funds were flowing inward, it put a downward pressure on the interest

rates. The opposite happened during the financial crisis; as the capital quickly

flowed outward, the interest rates rose due to upward pressure. Massive capital

outflows occurred as investors detected the weakness in the economy and lost

their hopes of further gains.

The baht’s value relative to the dollar was pressured by the large sale of baht

in exchange for dollars.

As a result, the government raised interest rates to encourage investors to keep

their money in Thailand.

The Asian crisis also demonstrated how interest rates could be affected by flows

of funds out of countries. Exhibit 6A.2 illustrates how interest rates changed from

June 1997 (just before the crisis) to June 1998 for various Asian countries. The

increase in interest rates can be attributed to the indirect interventions intended

to prevent the local currencies from depreciating further, or to the massive

outflows of funds, or to both of these conditions. In particular, interest rates of

Indonesia, Malaysia, and Thailand increased substantially from their pre-crisis

levels. Those countries whose local currencies experienced more depreciation had

higher upward adjustments. Since the substantial increase in interest rates (which

tends to reduce economic growth) may have been caused by the outflow of

funds, it may have been indirectly due to the lack of confidence by investors and

firms in the ability of the Asian central banks to stabilize the local currencies.

Q5.2: Why did it put downward pressure on U.S. interest rates?

It put downward pressure on the rates, as there were more dollars in the market

and the US banks had more excess funds. The loans held by the American banks

were in chance of default, so the rates decreased providing less return for the

depositors. This would also have helped the issuers of loans as they had hurdles

to pay it back.

Q6.1: It is commonly argued that high interest rates reflect high expected inflation

and can signal future weakness in a currency. Based on this theory, how would

expectations of Asian exchange rates change after interest rates in Asia increased?

There is a positive correlation between interest rates and inflation in the economy.

If inflation goes up, interest rates have to be adjusted in an upward manner to

reflect the demand of the investors. The investors will definitely seek higher rates

to compensate for the high expected inflation. The peoples’ purchasing power will

be reduced due to high inflation. If purchasing power is reduced then the economy

will be hurt. Companies and other foreign investors won’t be interested to invest

in the country.

Expectations by investors would be dismal as they know the currency will fall

further. They wouldn’t be able to get the return that they had wanted to. For

example, if a foreign corporation wants to invest in project with a discount rate

of 15%, and if inflations soars; the actual return would not be same after

adjusting for incremental inflation. Shareholders would view the project as risky

and hence it wouldn’t add value to the firm. Therefore, investors would not invest

in the future.

Q6.2: Why? Is the underlying reason logical?

Shareholders would view the project as risky and hence it wouldn’t add value to

the firm. Therefore, investors would not invest in the future. Most of the

shareholders are risk averse and they look for safe haven securities when investing

in the stocks is too risky. This is the logical for the corporations as well. Why

would they invest in something that wouldn’t yield value?

Q7.1: During the Asian crisis, why did the discount of the forward rate of Asian

currencies change?

The discount on the forward rate became more pronounced as the Asian interest

rates increased. Due to interest rate parity, the larger interest rate gap causes a

larger forward discount of the currency with the higher interest rate.

Q7.2: Do you think it increased or decreased? Why?

The forward rate decreased compared to the spot rate. The discount increased

as a result.

Q8.1: During the Hong Kong crisis, the Hong Kong stock market declined

substantially over a 4-day period due to concerns in the foreign exchange market.

Why would stock prices decline due to concerns in the foreign exchange market?

Whenever the shareholders invest their hard earned money, they always look at

the fundamentals of the business. When they see certain problems that are

harmful to the business, most inevitably, their expectations will be pessimistic and

they will lose confidence.

On October 23, 1997, prices in the Hong Kong stock market declined by 10.2

percent on average; considering the 3 trading days before that, the cumulative

4-day effect was a decline of 23.3 percent. The decline was primarily attributed

to speculation that Hong Kong’s currency might be devalued and that Hong Kong

could experience financial problems similar to the Southeast Asian countries. The

fact that the market value of Hong Kong companies could decline by almost one-

fourth over a 4-day period demonstrated the perceived exposure of Hong Kong

to the crisis. During this period, Hong Kong maintained its pegged exchange rate

system with the Hong Kong dollar tied to the U.S. dollar.

Political problems

Hong Kong’s political issues and change of rule had affected it financially.

On 1 July 1997, the transfer of sovereignty of Hong Kong from the United

Kingdom to the People's Republic of China took place, officially marking the end

of Hong Kong's 156 years under British colonial governance.

The terms for the return of Hong Kong to Chinese rule in July 1997 carefully

protected the territory’s separate economic characteristics, which have been so

beneficial to the Chinese economy. Under the Basic Law, a “one country-two

systems” policy was formulated which left Hong Kong monetarily and economically

separate from the mainland with exchange and trade controls remaining in place

as well as restrictions on the movement of people. Hong Kong was hit hard by

the Asian Financial Crisis that struck the region in mid-1997, just at the time of

the handover of the colony back to Chinese administrative control. The crisis

prompted a collapse in share prices and the property market that affected the

ability of many borrowers to repay bank loans. Unlike most Asian countries, Hong

Kong Special Administrative Region and mainland China maintained their

currencies’ exchange rates with the U.S. dollar rather than devaluing.

Soon after Hong Kong's reversion to China, the city suffered an economic double-

blow from the Asian financial crisis and the pandemic ofH5N1 bird flu; in December

1997, officials had to destroy 1.4 million chickens and ducks to contain the virus

from spreading. Subsequently, mismanagement of Tung's housing policy disrupted

the market supply, sent properties prices in Hong Kong tumbling and caused

many homeowners to become bankrupt due to negative equity.

Stock prices would definitely decline due to devaluation or revaluation, as the

value of the currency relative to other currencies would change and that would

affect the bottom-line of the businesses. If the Hong Kong dollar is devalued,

then the subsidiaries located in the country would send back lower earnings to

their country of origin. The manufacturing sector could be hurt, especially if they

sourced raw materials from foreign countries as the prices would increase.

Ultimately, it would lead to lesser profits and that would be a disincentive for

the investors. The expectation for better business in the future could decline and

this is what led to the fall in the stock prices. This usually happens when there

are many multinational companies listed in on the stock exchange.

Q8.2: Why would some countries be more susceptible to this type of situation

than others?

Countries such as Hong Kong would be more susceptible to this situation as they

have foreign companies operating on their land. The countries which depend more

on their domestic economy and have more resources produced within their

boundaries would be less susceptible.

Q9.1: On August 26, 1998, the day that Russia decided to let the ruble float

freely, the ruble declined by about 50 percent. On the following day, called

“Bloody Thursday,” stock markets around the world (including the United States)

declined by more than 4 percent. Why do you think the decline in the ruble had

such a global impact on stock prices?

Global impact on stock prices

The stock prices declined as there were American companies operating within

Russia. Obviously, even though the sales remained constant, the money remitted

back to America would reduce. The crisis affected Russia and US could lose

contract orders from Russia and this would decrease the revenues of the

companies involved. Investors lost their confidence of better business prospects

for the future and this is what led to the fall by 4% in stock prices. It is this

integration of trade between the countries that leads to global impact upon stock

prices.

Q9.2: Was the markets’ reaction rational?

Based on this analysis, we can say that the markets’ reaction is rational. The

market seems to be semi-strong form efficient as investors have publicly available

information as well as past prices data. The investors have judged the business

prospects based on the fundamentals of the business based on earnings,

expenditure and profits. It is only natural to expect that the sales will go down

due to the ruble decline.

Q9.3: Would the effect have been different if the ruble’s plunge had occurred in

an earlier time period, such as 4 years earlier? Why?

4 years ago – The effect would most certainly be much more different.

First of all, the investors wouldn’t even comprehend that the crisis would affect

the Russian economy. There was no crisis 4 years ago. They wouldn’t have such

expectations as they wouldn’t anticipate problems in the absence of past

information. People usually anticipate or forecast such disasters after they have

occurred in other countries.

Secondly, investors wouldn’t move their money out of Russia due to fear of

financial crisis. Consequently, the government wouldn’t have to intervene directly

to offset the reaction from market forces.

Therefore, the ruble wouldn’t decline and the global impact on stock prices

wouldn’t materialize.

Q10: Normally, a weak local currency is expected to stimulate the local economy.

Yet, it appeared that the weak currencies of Asia adversely affected their

economies. Why do you think the weakening of the currencies did not initially

improve their economies during the Asian crisis?

Global economic growth and interest rates remain low, resulting in central banks

using unconventional means to try to boost growth. While most central banks are

not explicitly targeting weaker currencies, it has become an unspoken goal. For

example, the euro zone and Japan have loosened monetary policy and seen their

currencies fall against the U.S. dollar.

Potential implications of a lower currency include:-

Export growth: A country's exports can gain market share as its goods get cheaper

relative to goods priced in stronger currencies. The resulting increases in sales

can boost economic growth and jobs, as well as increase corporate profits for

companies that do business in foreign markets.

Rising inflation: Inflation can climb when economies import goods from countries

with stronger currencies, since it takes more of a weak currency to buy the same

amount of goods priced in a stronger currency. Currently, low economic growth

has resulted in deflation, or falling prices, becoming a bigger risk than inflation

in many countries. A deflationary mindset is undesirable because once consumers

begin to expect regular price declines, they may start to postpone spending and

businesses may begin to delay investment, resulting in a self-perpetuating cycle

of slowing economic activity.

Relief for debtors: A weak currency can boost inflation, and therefore incomes

and tax receipts, while the value of debt is unchanged, making it easier for local

currency borrowers to pay down debts. Alternatively, a weak currency makes

paying back debt issued to foreign investors and priced in foreign currency more

expensive. Much of the developed world still has high debt burdens, making

inflation somewhat desirable.

However, the price increase for imports can harm citizens' purchasing power. The

policy can also trigger retaliatory action by other countries which in turn can

lead to a general decline in international trade, harming all countries.

This is the reason why a weak currency can lead to harmful effects for the

economy in the long run.

Q11.1: During the Asian crisis, Hong Kong and China successfully intervened (by

raising their interest rates) to protect their local currencies from depreciating.

Nevertheless, these countries were also adversely affected by the Asian crisis.

Why do you think the actions to protect the values of their currencies affected

these countries’ economies?

Since the currencies of China and Hong Kong were tied to the dollar, they

appreciated against the other Asian currencies. Thus, their products became more

expensive to the other Asian countries, which adversely affected their international

trade balance with other Asian countries.

Q11.2: Why do you think the weakness of other Asian currencies against the

dollar and the stability of the Chinese and Hong Kong currencies against the

dollar adversely affected their economies?

Hong Kong got affected as its currency was pegged to the U.S. dollar. USA got

affected by the crisis in Asia, and this in turn affected Hong Kong as due to the

peg. The dollar depreciated and so did the Hong Kong dollar. However, I don’t

think it was adversely affected as it weathered the storm and by raising interest

rates and giving the investors an incentive.

China was affected only slightly. It did not have weakness in the economy. The

Chinese government had more control over economic conditions because it still

owned most real estate and still controlled most of the banks that provided

credit to support growth. There were much fewer bankruptcies. The government

was also able to maintain the value of the Yuan against the dollar.

Q12.1: Why do you think the values of bonds issued by Asian governments

declined during the Asian crisis?

The values decline as there was no chance of them paying it to the bank from

where the borrowed. The currency declines also played a significant part here as

they were borrowed from foreign banks and the values declined during the

repayment time. The default risk was looming and banks couldn’t get their money

unless the government had bailed them out.

Q12.2: Why do you think the values of Latin American bonds declined in response

to the Asian crisis?

Global investors within crisis countries also spread bear markets. In December

1997, as Republic of Korea distinguishing among the channels of contagion can

be hazardous. In an emerging market selloff many channels seem to be working

at once, particularly when new information hits the market. Nevertheless it is

useful to identify the different ways by which contagion can spread. It is also

worth recognizing that sometimes what appears to be contagion is just separate

markets reacting to a common external shock—for example, to the 1994 rise in

US interest rates, or to the oil price increases of the 1970s. Trade links provide

a natural channel for financial contagion. Consider the Thai devaluation. Last

year’s fall in the baht made Thai exports cheaper to foreign buyers. For countries

such as Indonesia that compete in export markets with Thailand, that means

foreign demand for exports falls as importers in the US and Japan switch to the

now-cheaper Thai goods. Korean investors liquidated holdings of Latin American

Eurobonds in order to cover their dollar obligations. As prices on Brazilian and

Argentine dollar-denominated bonds fell, Brazilian banks that had purchased the

bonds on borrowed funds were forced to sell Brazilian local currency denominated

assets for dollars, reducing the Brazilian Central Bank’s stock of foreign reserves

and making Brazil a target for attack. These episodes show how a sudden drop

in liquidity brought about by falling prices for one kind of asset may induce a

fire sale of other assets, even with no change in fundamentals.

Mexico’s proximity to the United States and the Clinton administration's

commitment to NAFTA made the United States effectively a lender of last resort

to Mexico. That reduced potential liquidity problems in the region. Creditors’

worries about the likelihood of repayment on Mexican debts were assuaged,

allowing spreads on Mexican and other Latin bonds to compress fairly rapidly.

Q13: Why do you think the depreciation of the Asian currencies adversely affected

U.S. firms? (There are at least three reasons, each related to a different type of

exposure of some U.S. firms to exchange rate risk.)

The depreciation is harmful for US companies, as the cash repatriated back from

the Asian countries would reduce due to the weaker value of in relation to dollar.

3 types of exposure

Transaction exposure: One obvious way in which most MNCs are exposed to

exchange rate risk is through contractual transactions that are invoiced in foreign

currencies. The sensitivity of the firm’s contractual transactions in foreign

currencies to exchange rate movements is referred to as transaction exposure.

Since many US companies had subsidiaries in the Asian countries, the dollar

inflows from these countries would be very low due to a corresponding fall in

their currencies. On the other hand the outflow would be higher as the dollar

has appreciated.

Translation exposure: A related method for assessing exposure is the value-at-

risk (VAR) method, which measures the potential maximum 1-day loss on the

value of positions of an MNC that is exposed to exchange rate

movements. Tomorrow or the day after that, a US firm could receive some

payments for services or goods provided. The firms could expect a reduction in

the payments due to a potential decline in the currencies.

Economic Exposure: The value of a firm’s cash flows can be affected by exchange

rate movements if it executes transactions in foreign currencies, receives revenue

from foreign customers, or is subject to foreign competition. The sensitivity of the

firm’s cash flows to exchange rate movements is referred to as economic exposure

(also sometimes referred to as operating exposure). An MNC’s cash flows are

affected by its transaction exposure (as illustrated earlier in this chapter. Thus,

an MNC’s transaction exposure is a subset of its economic exposure.

But economic exposure also includes other forms beyond transaction exposure

in which a firm’s cash flows can be affected by exchange rate movements.

Q14.1: During the Asian crisis, the currencies of many Asian countries declined

even though their governments attempted to intervene with direct intervention or

by raising interest rates. Given that the abrupt depreciation of the currencies was

attributed to an abrupt outflow of funds in the financial markets, what alternative

Asian government action might have been more successful in preventing a

substantial decline in the currencies’ values?

Alternative Actions

Sterilized intervention: If the central bank of the Asian country goes for the

intervention by adjusting for the change in money supply, then it can definitely

shelter itself from currency decline. The Asian governments went intervening in

the foreign market by spending billions of dollars. If they simultaneously engage

in government bond sale, then they can get back the dollars that they had spent

for the intervention. This way the foreign reserves of the central bank would be

replenished and the currency wouldn’t decline.

Currency Inflation: Governments are the only entities that can legally create their

respective currencies. When they can get away with it, governments always want

to inflate the currency. Why? Because it provides a short-term economic boost

as companies charge more for their products and it also reduces the value of

the government bonds issued in the inflated currency and owned by investors.

Inflated money feels good for a while, especially for investors who see corporate

profits and share prices shooting up, but the long-term impact is an erosion of

value across the board. Savings are worth less, punishing savers and bond buyers.

For debtors, this is good news because they now have to pay less value to retire

their debts - again, hurting the people who bought bank bonds based off those

debts. This makes borrowing more attractive, but interest rates soon shoot up to

take away that attraction.

Q14.2: Are there any possible adverse effects of your proposed solution?

Sterilized Intervention: There won’t be a severe impact on the central bank or the

economy of the currencies. But the problem is that this is a short term solution

and it is not sustainable. The government can only take loans for the limited

period of time. If the government keeps on borrowing, then the interest payments

will skyrocket.

Currency Inflation: The government can easily print money and spread it in the

market. This move may have adverse effects as peoples’ purchasing power will

reduce and investors may demand more in interest rates.

Case 2: Zapa Chemical and BuBa

Section 1 – Introduction

This case focuses on the hedging of a currency exposure, a long Deutschemark

position, by a U.S.-based multinational chemical company. The case takes place

during the August - September period in 1992 when the European Monetary

System experienced a crisis as a result of a variety of world political and economic

events, including the monetary policies pursued by the Bundesbank of Germany.

Problems

1. Zapa Chemical was due to receive DM 7.6 million from Germany after the sale

of a chemical distributorship. Because of the special tax and sales document

filings in Germany, it could not yet be determined when exactly the funds

would be available for repatriation.

2. At that time Stephanie had debated whether the dollar was a low as it was

going to go, or just hesitating before sliding further. Stephanie felt there were

a number of forces which could drive the dollar still lower.

3. Economic growth in US was slowing. The high interest rates in Germany and

the low interest rates in the U.S., an unusual scenario by any account, was

resulting in a massive capital flow from dollar-denominated assets into

Deutschmarks.

4. The political situation was also hurting the dollar. The markets had historically

favored and rewarded Republican economic policies as opposed to the politics

of the Democrats.

5. Stephanie felt that there were too many unknowns, and it was difficult to

judge which way the dollar would move.

6. The huge interest differentials between U.S. dollar and Deutschmark assets

resulted in forward rates which were extremely unattractive.

7. The week of September 14th had been quite turbulent. The dollar had fallen,

risen, and fallen again.

Section 2 – Background

Stephanie Mayo had originally been given the exposure for management in mid-August.

Zapa Chemical had sold a specialty chemical distributorship in Stuttgart, Germany. The

proceeds of the sale, approximately DM7.6 million, would be brought back to the United

States sometime in November. Because of special tax and sales document filings in

Germany, it could not yet be determined when exactly the funds would be available for

repatriation.

The U.S. dollar had been falling like a rock since late March. The central bank of

Germany, the Bundesbank, had added momentum to the drop when it had increased the

German base lending rate by 75 basis points (3/4 of a percent) to 9.75% on July 16th.

Relevant Facts

Zapa Chemical’s Original Exposure

•Sale proceeds of approximately DM 7.6 million

•Effect of exchange rate movements

–if the DM depreciates, the equivalent dollar value decreases as well (and vice versa)

•Problem

–date for repatriation of funds is initially unclear

–only vague estimate: “sometime in November”

Hedging decision – To hedge or not to hedge, which hedging instrument to use.

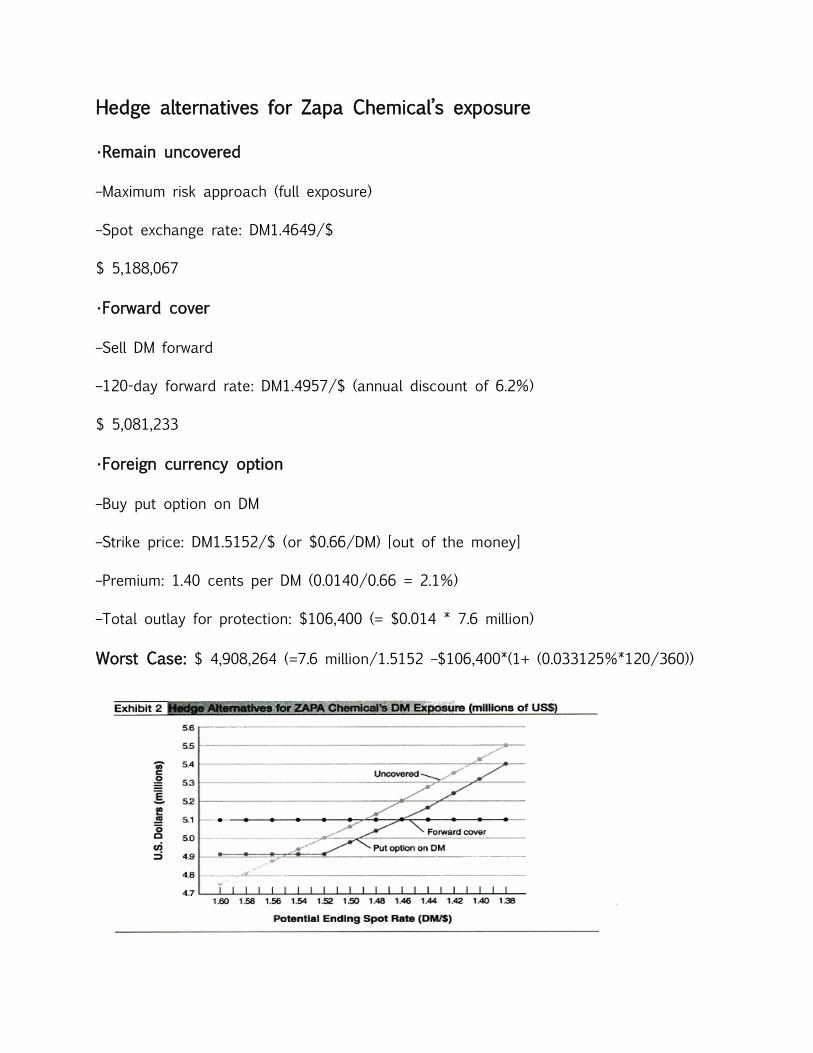

Hedge alternatives for Zapa Chemical’s exposure

•Remain uncovered

–Maximum risk approach (full exposure)

–Spot exchange rate: DM1.4649/$

$ 5,188,067

•Forward cover

–Sell DM forward

–120-day forward rate: DM1.4957/$ (annual discount of 6.2%)

$ 5,081,233

•Foreign currency option

–Buy put option on DM

–Strike price: DM1.5152/$ (or $0.66/DM) [out of the money]

–Premium: 1.40 cents per DM (0.0140/0.66 = 2.1%)

–Total outlay for protection: $106,400 (= $0.014 * 7.6 million)

Worst Case: $ 4,908,264 (=7.6 million/1.5152 –$106,400*(1+ (0.033125%*120/360))

Stephanie Mayo decides to buy the put-option in order to be able to participate

in exchange rate currency gains.

Section 3 – Solutions

Q1: Should Stephanie Mayo sell the put option protection already in place? Use

the current market rates and prices to defend your logic.

In August 1992, Stephanie Mayo hedged DM 7.6mil to be received in November

1992. In this case the worst scenario is US $ appreciation. So that is why she

hedged with covered put option.

Stephanie does not expect to exercise the put. The put is only for safety net,

just in case. If she expected the dollar to appreciate, a forward hedge would

have been more appropriate.

Here’s the background,

-First, US dollar declined rapidly (01.Sept.92: all-time low DM1.39/$). The U.S.

dollar falls DM1.39/$.

-Then, US dollar appreciated (16.Sept.92: DM1.51/$). The bank of England raises

its base lending rate to defend the falling British Pound. By afternoon the Bank

considers a further rate increase, but instead withdraws from the Exchange Rate

Mechanism (ERM) of the EMS. Sweden raises the base lending rate from 75% to

500% to stop speculators from shorting the krona. Currency volatilities and option

premiums skyrocket as crisis continues.

-Volatility still high. Currency volatilities and option premiums skyrocket as crisis

continues.

Sale of put option would expose ZAPA to adverse Exchange rate movements.

-3 months until repatriation in December.

-Increased option value reflects not only the favorable Exchange Rate movement,

but also the increased volatility (risk!).

-Possible solution to avoid exposure: sell put and enter into forward agreement.

Comparison of different hedging strategies:

Sale of put option & forward hedge (at DM 1.5255/$) lead to higher

outcome than option hedge in the worst case as well as at the current

spot rate. Eurocurrency interest rates had not changed since august.

Forward hedge does not allow to benefit from falling US dollar.

Q2: How have the events of September altered Stephanie’s view of the DM/$

exchange rate?

Initially, Stephanie expected the dollar to fall further:

-Buba was driving interest rates up to slow monetary growth, all in an effort to

stop the inflationary forces resulting from reunification.

–Interest rate differentials (US: 3.3125%; Germany: 9.750%). Three month

Eurodollar deposits were paying a 3.3125%, while similar Euro-Deutschemark were

paying 9.75%. And there were no signs of either rate moving toward the other.

•September turbulence:

–Uncertainty in Europe due to French vote on Maastricht Treaty. The Maastricht

Treaty had ben sign by the Council of Ministers in December 1991, but had to

ratify by each country.

–Stress in the EMS (devaluation pressure on Italian Lira and British Pound); Italian

Lira and British Pound withdrawn from ERM.

–Spanish peseta devalued 5% in the ERM. Other currencies had come under

speculative attacks on Friday. The high interest rates in Germany had continue

to bleed capital out of the other major European capital markets.

•After the dollar had fallen, risen, and fallen again, Stephanie wished to reevaluate

her put option position.

Q3: How has the volatility of the put option changed between August and

September?

Answer: The volatility of the put option increased in September. Dollar value

increased then decreased then again decreased. Other currency like British Pound

also devalued. August premium oscillated between $0.5 and $1.50 per DM and

September premium oscillated between $0.5 and $2.50 per DM.

Exhibit: Daily changes in the DM/$ spot rate and the DM put option premium

Q4: If you are the Vice President for Treasury at Zapa, what benchmarks would

you use to measure the hedging effectiveness? How would this alter Stephanie’s

hedging?

Answer: In ZAPA chemicals the management considers Treasury, a cost center

not a profit center. The management is responsible to follow conservative

management style for any exposure. So when the expenses of running the cost

center were lower the management was appreciative.

If I were the Vice President for Treasury at Zapa, I would use cost as a benchmark

to measure the hedging effectiveness. Standard portfolio theory can be used

where maximizing the expected value µ, and minimizing the variance σ^2 or risk

is focused.