Actuarial Study of Retiree Health Liabilities Under GASB 74/75

A Buck Consultants webinar

Gail Levenson and Rich Stover

April 11, 2013

Retiree prescription drug program: time to move to an Employer Group Waiver Plan (EGWP)?

April 11, 2013

A Buck Consultants webinar April 11, 2013

Today’s areas of focus

• Overview of Medicare Part D plan

• Impact of health care reform and Medicare changes on retiree prescription drug options

• Benefits of an EGWP

• Implementation considerations

Rich StoverPrincipal, H&P

Gail LevensonPrincipal, H&P

2

A Buck Consultants webinar

Employer retiree Rx options pre-health care reform

Retiree Drug Subsidy (RDS)

• Plan sponsor continues current prescription drug program

• Plan sponsor receives a subsidy for maintaining prescription drug benefits that is Actuarially Equivalent (AE) to standard Part D benefit

• RDS covers 20% to 25% of prescription drug cost

• “Double” tax benefit for corporate employers

Employer Group Waiver Plan (EGWP)

• Employer contracts with a vendor (usually a PBM) to provide benefits that can “match” the employer’s current plan design

• Eligible for “direct subsidy” instead of RDS

• Advantageous for plan that cannot satisfy AE requirements

• Governmentals can reflect under GASB

April 11, 2013

4

A Buck Consultants webinar

EGWP: how it works

Employer PBM CMS

• Employer contracts with PBM

• Contract can be either self-insured or fully-insured

• PBM implements employer’s plan design

• PBM receives financial subsidy from CMS

• PBM plan passes back all subsidies (in a self-insured plan) and charges administrative fee

• PBM assumes CMS compliance responsibilities

April 11, 2013

5

A Buck Consultants webinar

Value of RDS and EGWP pre-health care reform

$

Retiree

Drug Subsidy

EGWP Plan

April 11, 2013

6

A Buck Consultants webinar

Employer retiree Rx options post-health care reform

Retiree Drug Subsidy (RDS)

• RDS payments taxable starting in 2013

- Reduces real value of RDS to taxable groups

• Standard Part D benefit donut hole phased out by 2020

- No impact to actuarial equivalence testing

Employer Group Waiver Plan Plus Wrap (EGWP+Wrap)

• Standard Part D benefit donut hole phased out by 2020

- Additional federal funds available to EGWP

- Direct subsidy

- Catastrophic reinsurance

- 50% brand discount from drug manufacturers in coverage gap

April 11, 2013

7

A Buck Consultants webinar

Medicare Reinsurance 80%

Pla

n P

ays

15

%

5%

Co

ins

Plan Pays

21%79%

Coinsurance

50%

PharmaDiscount

Pla

n P

ays

2.5

%

47

.5%

Coin

sura

nce

Plan Pays 75%

25

%

Coin

sura

nce

$325 Deductible

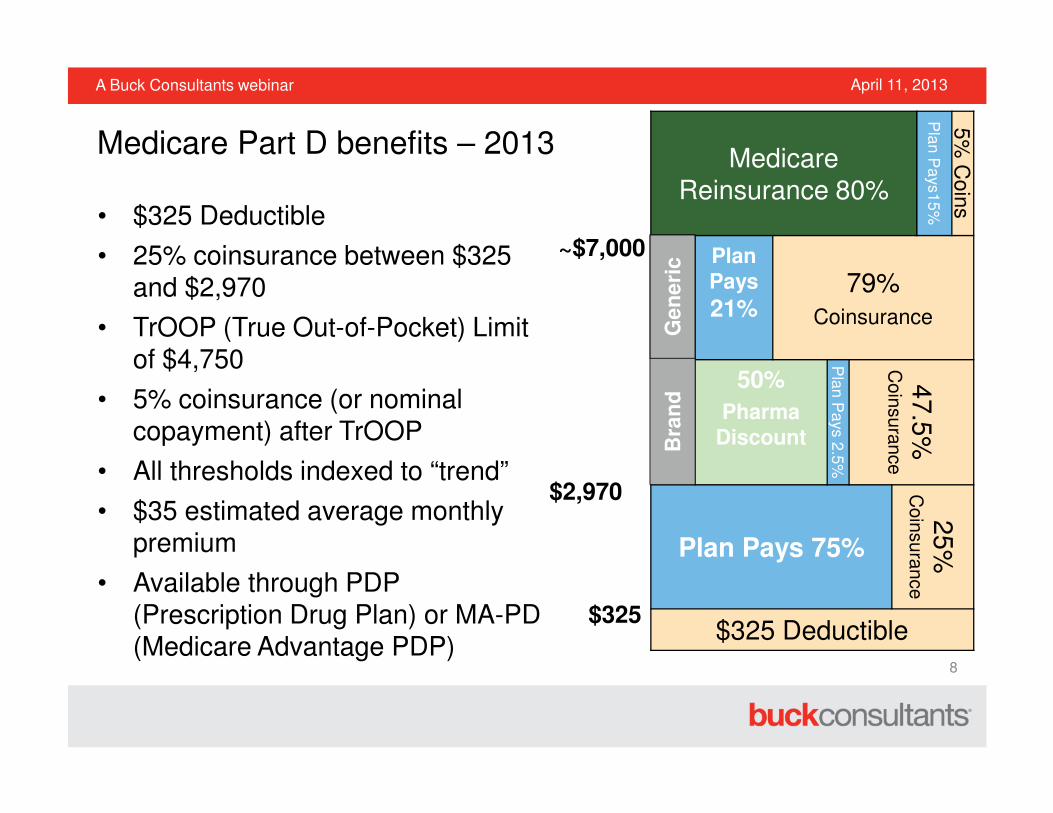

• $325 Deductible

• 25% coinsurance between $325 and $2,970

• TrOOP (True Out-of-Pocket) Limit of $4,750

• 5% coinsurance (or nominal copayment) after TrOOP

• All thresholds indexed to “trend”

• $35 estimated average monthly premium

• Available through PDP (Prescription Drug Plan) or MA-PD (Medicare Advantage PDP)

$325

$2,970

~$7,000

Ge

ne

ric

Bra

nd

Medicare Part D benefits – 2013

April 11, 2013

8

A Buck Consultants webinar

Medicare Part D benefit changes for 2014

2013 2014

Deductible $325 $310

Initial Coverage Limit $2,970 $2,850

True Out-of-Pocket (TrOOP) $4,750 $4,550

Catastrophic coverage copayment for generic drugs

$2.65 $2.55

Catastrophic coverage copayment for brand-name drugs

$6.60 $6.35

April 11, 2013

9

A Buck Consultants webinar

Donut Hole Coverage

• Expanded generic and brand coverage

- Donut hole filled in by 2020

• 50% discount on brand drugs

- Discount determined after any PDP provided gap coverage

- Pharmacy discounts and additional federal subsidies make EGWP more valuable relative to RDS

Year Generic Benefit Brand Benefit Brand Discount

2011 7% 0% 50%

2012 14% 0% 50%

2013 21% 2.5% 50%

2014 28% 2.5% 50%

2015 35% 5% 50%

2016 42% 5% 50%

2017 49% 10% 50%

2018 56% 15% 50%

2019 63% 20% 50%

2020 75% 25% 50%

Medicare Part D benefits – 2011 and beyond

April 11, 2013

10

A Buck Consultants webinar

Tax exclusion

eliminated in 2013

50% brand discount

Direct subsidy and catastrophicreinsurance

$

Retiree Drug Subsidy

EGWP+Wrap Plan

Health care reform changes value of RDS and EGWP

April 11, 2013

11

A Buck Consultants webinar

0

250

500

750

1000

1250

1500

1750

2000

DS, Catastrophic, Brand Discount

Direct Subsidy (DS)

RDS

• Average annual external financing amounts expected per enrollee

• EGWP+Wrap will enjoy federal direct subsidy, catastrophic reinsurance and manufacturer brand discounts

Source for RDS and Direct Subsidy:2010 Annual Report of the Board of Trustees ofthe Federal Hospital Insurance and FederalSupplemental Medical Insurance Trust Funds (8/5/2010)

Brand discount is estimated.

Projected Part D External Financing for EGWP+Wrap vs. RDS

April 11, 2013

12

A Buck Consultants webinar

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

PDP & MA-PD RDS

“About 20% of beneficiaries

participating in Part D were

covered by [the retiree drug]

subsidy in 2009…. As a result of

[healthcare reform] changes, RDS

program participation is assumed

to decline quickly to about 2% in

2016 and beyond.”

Source: 2010 Annual Report of the Board of Trustees ofthe Federal Hospital Insurance and Federal

Supplemental Medical Insurance Trust Funds (8/5/2010)

Medicare Trustees expect RDS participation to decline

April 11, 2013

13

A Buck Consultants webinar

• Employer contracts with a vendor (usually a PBM) to provide prescription drug benefits that can “match” the employer’s current plan design through two Rx plans:

- EGWP provides standard Part D benefits

- Wrap Plan fills in the gaps to keep retirees whole

• This approach leverages Pharma discounts and government subsidies

- Can take advantage of the closing of the Medicare Part D donut hole

• Member disruption is limited (but not zero as with RDS)

- One ID card for two Rx plans –single transaction coordination of benefits

Employer Group Waiver Plan Plus Wrap (EGWP+Wrap): alternative to RDS

April 11, 2013

14

A Buck Consultants webinar

• $200 cost for brand drug

• 20% coinsurance

Rx Payment Coverage

Current Plan

EGWPEGWP +

Wrap

Gross Cost $200 $200 $200

Base Plan Pays $160 $160 $5

Discount N/A $20 $100

Wrap Plan Pays N/A N/A $55

Retiree Pays $40 $20 $40

EGWP examples – Plan design (in donut hole)

April 11, 2013

15

A Buck Consultants webinar

Recent regulatory guidance

• CMS guidance on wrap

- Guidance issued in 2012 appeared to eliminate need for wrap

- Subsequent CMS guidance confirms wrap is still required

• ACA guidance has clarified the application of various ACA fees and taxes to EGWPs

- Transitional reinsurance fee

- Insurer fee

• Insured wrap programs may be subject to state regulations

April 11, 2013

16

A Buck Consultants webinar

Risk ScoreCMS provides greater reimbursement to EGWP plans covering sicker retirees

Size of LIS PopulationCMS provides greater reimbursement for low-income retirees. These funds passed to the retiree

Contribution StrategyWhat savings are shared with retirees through contributions. Particularly under a “capped” retiree medical plan

Generic UtilizationCMS reimbursement to EGWP is independent of changes in generic substitution rates

Cash FlowCMS reimbursement via EGWP is provided substantially sooner than RDS annual filers

Admin FeesEGWP fees may not be very competitive yet; consider RDS admin costs as an offset

Discounts and RebatesEGWP is a separate contract from your normal Rx benefit; watch for lost economies with the non-Medicare population.

FormularyAny difference in formulary restrictions between RDS plan and ‘replicated’ EGWP plan could impact savings

Volatility EGWP provides the ability to gain stability in yearly costs by insuring

Key variables in financial analysis

April 11, 2013

17

A Buck Consultants webinar

Are you a candidate for an EGWP?

• An employer participating in the RDS program

• A non-taxable entity

• A taxable entity with little or no tax liability

• An employer offering prescription drugs to Medicare-eligible retirees

• A plan sponsor with a drug plan that does not pass the actuarially equivalence test for RDS

• A government entity that wishes to reflect Medicare D impact in its GASB 43/45 accounting

• A post-65 retiree program with more than 100 eligible retirees and dependents

April 11, 2013

18

A Buck Consultants webinar

Implementation considerations

• Number of post-65 Medicare-eligible retirees and Medicare-eligible dependents

- Fully insured vs self insured

- Minimum number of lives vary by PBM

- There are several PBMs who will self insure a relatively small number of retirees (e.g., 250)

• Internal resources to support implementation

• Timing of implementation: preferably 6 months

April 11, 2013

19

A Buck Consultants webinar

Clinical

• Formulary

- CMS requires certain drugs to be covered and others to be excluded

- Brand drugs covered on the formulary are limited to eligible drugs by manufacturers who agreed to participate in the coverage gap discount program. This list is updated periodically by CMS.

- PBM can perform formulary disruption analysis

- Formal formulary exception process available to retirees for non-formulary drugs (can cover in wrap)

• Special programs (e.g., step therapy, prior authorization, dose optimization, etc.) may be impacted

- CMS has more stringent requirements on the management of medications for the Med D program

Implementation considerations

April 11, 2013

20

A Buck Consultants webinar

Plan design considerations

• No mandatory mail

- 90-day supply must be allowed at retail if a mail service benefit is offered

- May charge 3 copays for retail 90-day supply

• No mandatory generic

- No penalties allowed for dispensing brand when generic is available

• Catastrophic coverage

- Plan cannot exceed the CMS standard member cost-share limit of approximately 5%

- Benefit to both member and Plan as government reimburses 80% of the cost

April 11, 2013

21

A Buck Consultants webinar

How does the “Wrap” work?

• Covers drugs not included on the PBM’s Medicare Part D formulary

• Covers drugs excluded by Medicare, such as prescription drugs for cough and cold, erectile dysfunction , etc.

• Allows you to offer the same plan design available through your commercial plan, including copayments, coinsurance, and maximum out-of-pocket, if applicable

April 11, 2013

22

A Buck Consultants webinar

• Member Health Insurance Claim Number (HICN) required for eligibility

- Can be very difficult to gather HICNs

• Low income subsidies

- Provides premium and benefit assistance for low income participants

- Represents those up to 150% of the FPL

- Premium subsidies must be reimbursed directly to the individual within 45 days of receipt (on a monthly basis)

- Administrative challenge for most employers

• Benefit assistance happens at “point of service”

- Lower coinsurance/copays for low-income participants

- Plans reimbursed on an annual basis for the reduced costs to the participant

Employer administrative issues

April 11, 2013

23

A Buck Consultants webinar

Employer administrative issues (cont’d)

• High income penalties

- Individuals/couples making greater than $85,000/$170,000 pay higher premium for Medicare Part D coverage

- Determined by Social Security Administration (SSA) and happens directly through Social Security deductions

- Employer is not notified

- Employer can choose to reimburse retiree

• Late enrollment penalties

• Integrated deductibles/maximum out-of-pockets

- Will not work for EGWP plans

• Split Families

- EGWP and non-EGWP family members

- Each retiree must be provided separately

April 11, 2013

24

A Buck Consultants webinar

Member communications

• Integral part of a successful implementation

- Plethora of Medicare-required communication sent by PBM

- PBMs vary on what customization they will allow

- Customized employer communication recommended as other communication from government/PBM may be confusing and not applicable

- Recommend having comprehensive communication plan to coordinate between PBM-generated communication and employer-generated communication

April 11, 2013

25

A Buck Consultants webinar

• New Rx card/New “rules”

- Generally transparent and/or beneficial to retiree

• Late enrollment penalties and additional premium for high-income -disruptive

• Required communications to retirees

• Employer can not force retirees to enroll in EGWP– must allow them to opt out

• Medication Therapy Management Program (MTM)

- Auto-enroll required for those with certain conditions or drugs

- Participant can opt out

• Minor differences may exist in formulary, network, and therapeutic management

• Retiree confusion

Retiree issues

April 11, 2013

26

A Buck Consultants webinar

Case study

• Large self-funded employer

• Approximately 15,000 Medicare-eligible retirees

• Previously receiving RDS

• Implementation

- Implemented for 1/1/2013

- Started implementation in March 2012

• Savings

- Implemented Cash savings approximately $5 million over RDS

- The associated FAS Expense savings for 2012 were roughly $38 million

- Employer’s year-end 2011 APBO was reduced by $340 million due to the EGWP.

April 11, 2013

27

A Buck Consultants webinar

EGWP + Wrap Considerations

Pros:

• Economic savings expected with this approach

• Can account for now even if delay implementation to 2015

• Efficient approach to obtain federal Part D subsidies and the 50% brand discount

• Can replicate current level of Rx benefits

• No more RDS compliance

Cons:

• Can PBM administer almost seamlessly

• Communicating and implementing changes may be challenging

• Formulary control

• Restrictive generic not allowed

• Mandatory mail not allowed

• Caps on employer cost can limit employer savings

April 11, 2013

28

A Buck Consultants webinar

Next steps

• If you are considering moving to an EGWP

- Contact your Buck Account Executive to set up a call to discuss next steps

- Savings analysis

- EGWP 101 discussion

- Schedule a call with our EGWP experts

April 11, 2013

29

A Buck Consultants webinar

Join the conversation on Buck’s social media channelsblog.buckconsultants.com

linkedin.com/company/buck-consultants

twitter.com/buckconsultants

facebook.com/buckconsultants

www.buckconsultants.com