A Better Investment Climate for Everyone - World...

288

2005 world development report A Better Investment Climate for Everyone

Transcript of A Better Investment Climate for Everyone - World...

2005world development report

A Better Investment Climatefor Everyone

01_WDR_FM.qxd 9/3/04 11:15 AM Page i

01_WDR_FM.qxd 9/3/04 11:15 AM Page ii

A Copublication of The World Bank

and Oxford University Press

2005world development report

A Better Investment Climatefor Everyone

01_WDR_FM.qxd 9/3/04 11:15 AM Page iii

© 2004 The International Bank for Reconstruction and Development / The World Bank1818 H Street, NWWashington, DC 20433Telephone: 202-473-1000Internet: www.worldbank.orgE-mail: [email protected]

All rights reserved.

1 2 3 4 07 06 05 04

A copublication of the World Bank and Oxford University Press.Oxford University Press198 Madison AvenueNew York, NY 10016

This volume is a product of the staff of the World Bank. The findings, interpretations, and con-clusions expressed herein do not necessarily reflect the views of the Board of Executive Direc-tors of the World Bank or the governments they represent.

The World Bank does not guarantee the accuracy of the data included in this work. Theboundaries, colors, denominations, and other information shown on any map in this work donot imply any judgment on the part of the World Bank concerning the legal status of any terri-tory or the endorsement or acceptance of such boundaries.

Rights and PermissionsThe material in this work is copyrighted. Copying and/or transmitting portions or all of thiswork without permission may be a violation of applicable law. The World Bank encourages dis-semination of its work and will normally grant permission promptly.

For permission to photocopy or reprint any part of this work, please send a request withcomplete information to the Copyright Clearance Center, Inc., 222 Rosewood Drive, Danvers,MA 01923, USA, telephone 978-750-8400, fax 978-750-4470, www.copyright.com.

All other queries on rights and licenses, including subsidiary rights, should be addressed tothe Office of the Publisher, World Bank, 1818 H Street, NW, Washington, DC 20433, fax 202-522-2422, e-mail [email protected].

Cover and interior design: Susan Brown SchmidlerCover illustration commissioned by the WDR 2005 team; © Linda Frichtel

ISBN 0-8213-5724-7 (clothbound)ISBN 0-8213-5682-8 (paperback)ISSN 0163-5085

Library of Congress Cataloging-in-Publication Data has been applied for.

01_WDR_FM.qxd 9/3/04 11:15 AM Page iv

Contents

v

Foreword xiiiAcknowledgments xvAbbreviations and Data Notes xvi

Overview 1The investment climate is central to growth and poverty reduction 1

Tackling costs, risks, and barriers to competition 4

Progress requires more than changes in formal policies 5

A process, not an event 7

Focus on delivering the basics 9

Going beyond the basics involves additional challenges 12

The international community can lend a hand 14

PA RT IImproving the Investment Climate 17

1 The investment climate, growth, and poverty 19Understanding the investment climate 20

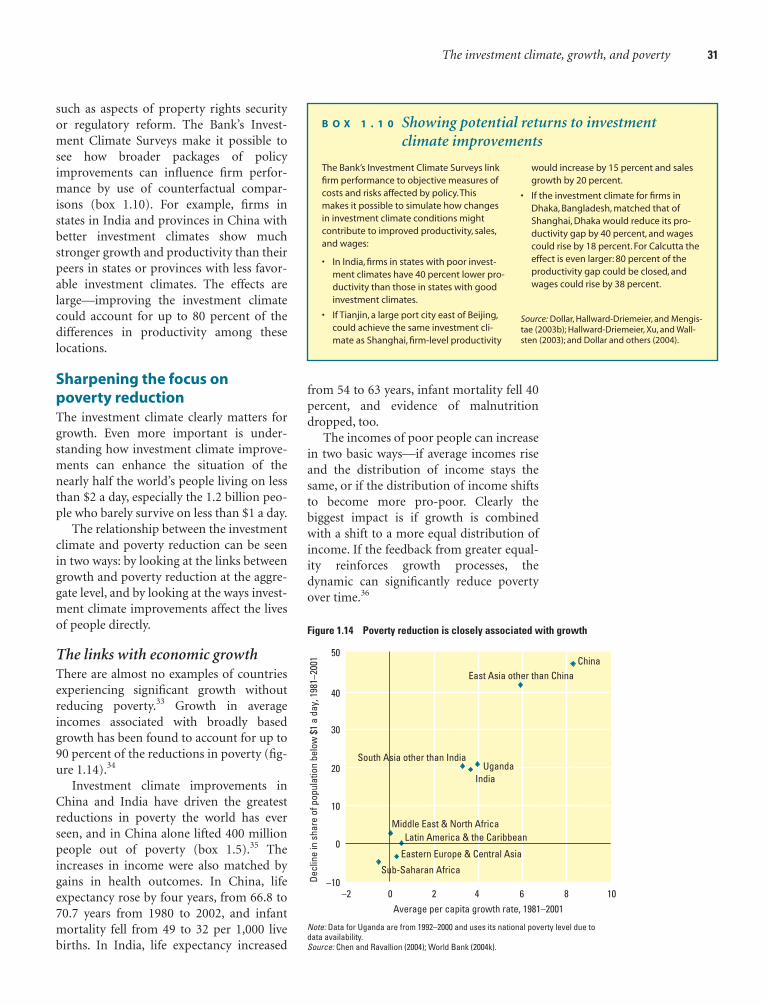

How investment climate improvements drive growth and reduce poverty 24

Sharpening the focus on poverty reduction 31

Creating a better investment climate for everyone 35

2 Confronting the underlying challenges 36The basic tension: Firm preferences or the public interest? 37

Restraining rent-seeking 40

Establishing credibility 45

Fostering public trust and legitimacy 50

Ensuring policy responses reflect a good institutional fit 53

Making progress 54

01_WDR_FM.qxd 9/3/04 11:15 AM Page v

vi CONTENTS

3 Tackling a broad agenda 56The investment climate as a package 56

Setting priorities 58

Managing individual reforms 68

Maintaining momentum 71

Strengthening capabilities 74

PA RT IIDelivering the Basics 77

4 Stability and security 79Verifying rights to land and other property 80

Facilitating contract enforcement 84

Reducing crime 89

Ending the uncompensated expropriation of property 92

5 Regulation and taxation 95Regulating firms 95

Taxing firms 106

Regulating and taxing at the border 111

6 Finance and infrastructure 115Financial markets 115

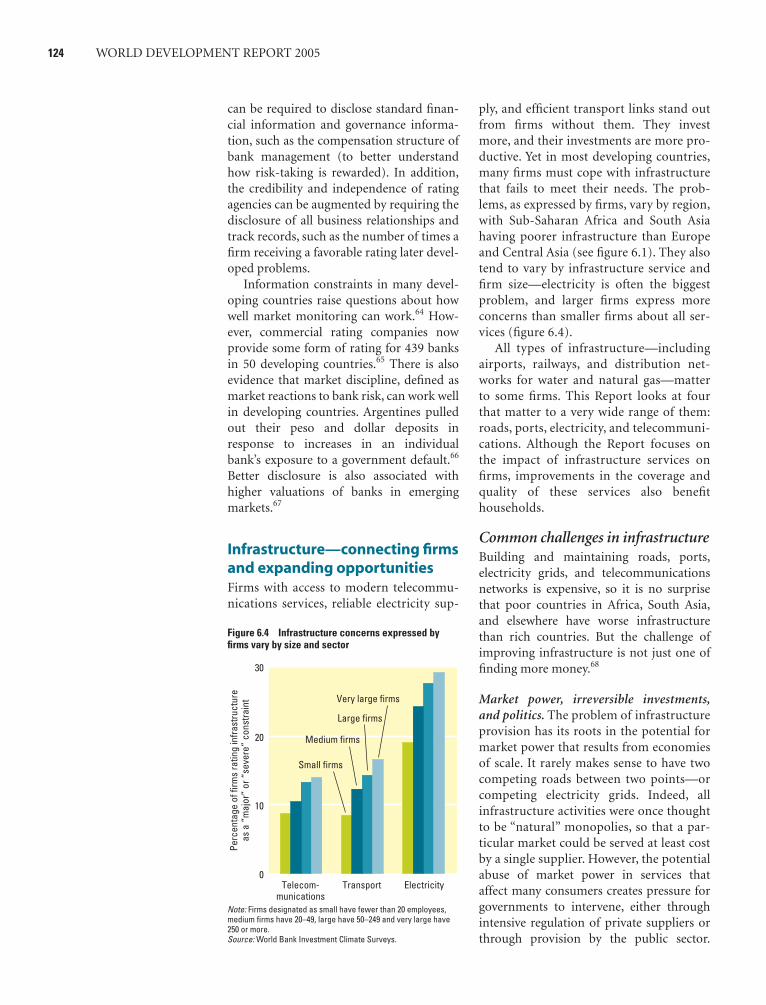

Infrastructure—connecting firms and expanding opportunities 124

7 Workers and labor markets 136Fostering a skilled and healthy workforce 137

Crafting interventions to benefit all workers 141

Helping workers cope with change 151

PA RT IIIGoing Beyond the Basics? 157

8 Selective interventions 159The allure—and traps—of selective interventions 159

Experience in specific areas 163

01_WDR_FM.qxd 9/3/04 11:15 AM Page vi

Contents vii

9 International rules and standards 175International arrangements and the investment climate 175

Enhancing credibility 176

Fostering harmonization 180

Addressing international spillovers 182

Future challenges 184

PA RT IVHow the International Community Can Help 187

10 How the international community can help 189Removing distortions in developed countries 189

Providing more, and more effective, assistance 190

Tackling the substantial knowledge agenda 195

Bibliographical note 198

Endnotes 199

References 210Background papers for the WDR 2005 241

Case studies commissioned by the U.K. Department for International Developmentfor the World Development Report 2005 242

Selected Indicators 243

Measuring the investment climate 244Challenges in measuring the investment climate 244

The World Bank’s new measures 245

Technical notes 250

Selected world development indicators 253Data sources and methodology 253

Changes in the System of National Accounts 253

Classification of economies and summary measures 254

Terminology and country coverage 254

Technical notes 265

01_WDR_FM.qxd 9/3/04 11:15 AM Page vii

viii CONTENTS

1 The investment climate perspective 2

2 How do firms in developing countries rate variousinvestment climate constraints? 5

3 Tackling a broad agenda—lessons from China, India,and Uganda 7

4 Main messages from World Development Report2005 15

1.1 What do we mean by the investment climate? 20

1.2 New sources of investment climate data from theWorld Bank 21

1.3 Geography matters, but it is not destiny 22

1.4 The environment matters for well-being andproductivity: Main messages from WDR 2003 25

1.5 Improving the investment climate and growth: thecases of China, India, and Uganda 27

1.6 Measuring productivity 28

1.7 Growth with a poor investment climate—possible,but unlikely to be sustained 29

1.8 Developing a product is a learning process—asHyundai shows 29

1.9 Firm dynamics 30

1.10 Showing potential returns to investment climateimprovements 31

1.11 How growth translates to rising incomes for poorpeople 32

1.12 Women and the investment climate 34

2.1 Governance and the investment climate 37

2.2 Firms in history 38

2.3 Firms and social responsibility 38

2.4 How do firm differences affect their policypreferences and priorities? 39

2.5 The predation of Gécamines in Mobutu’s Zaire 41

2.6 Natural resource endowments: Blessing or curse? 41

2.7 Combating corruption in Botswana and Lithuania 42

2.8 The form of intervention: How many cheers fortransparency? 44

2.9 Business associations and the investment climate 45

2.10 Reducing policy uncertainty to stimulate investment 46

2.11 Entrepreneurship and uncertainty 47

2.12 The power of credibility 49

2.13 Building credibility through persistence in Uganda 50

2.14 Shining the light on government–firm dealings innatural resources and infrastructure 52

2.15 Decentralization and the investment climate 53

2.16 E-government and the investment climate 54

3.1 Improving the investment climate, China’s way 57

3.2 India’s path 58

3.3 Do small firms play a special role in economicgrowth? 64

3.4 International integration is especially important forsmall states 65

3.5 Exporting and productivity—what is the link? 65

3.6 Trade liberalization in India—recent evidence 66

3.7 Foreign locals—the role of emigrants and diaspora 67

3.8 Expanding the zone of feasible and desirable policyimprovements 68

3.9 The Bulldozer initiative in Bosnia and Herzegovina 70

3.10 Consultative mechanisms in Latvia and Turkey 72

3.11 Shepherding investment climate improvements inVietnam 73

3.12 The evolution of a reform champion in Senegal 74

3.13 Networks of regulatory professionals in infrastructure 75

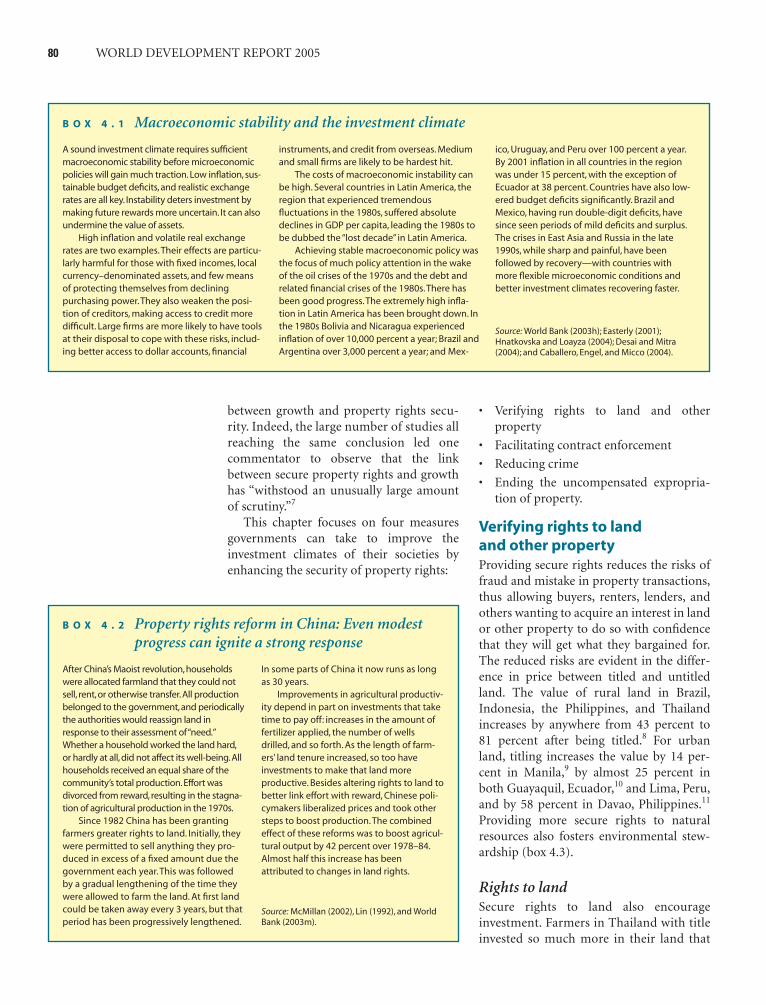

4.1 Macroeconomic stability and the investment climate 80

4.2 Property rights reform in China: Even modestprogress can ignite a strong response 80

4.3 Secure property rights and environmentalstewardship 81

4.4 The distribution of property rights 82

4.5 Thailand’s 20-year program to title rural land 83

4.6 De-monopolizing property transaction professionals 84

4.7 Intellectual property rights: The ongoing debate 85

4.8 Crime, poverty, and inequality 90

4.9 New York City’s police reforms—are they exportable? 91

4.10 Property wrongs: Is there ever a statute oflimitations? 93

5.1 Public ownership, regulation, and the investmentclimate 97

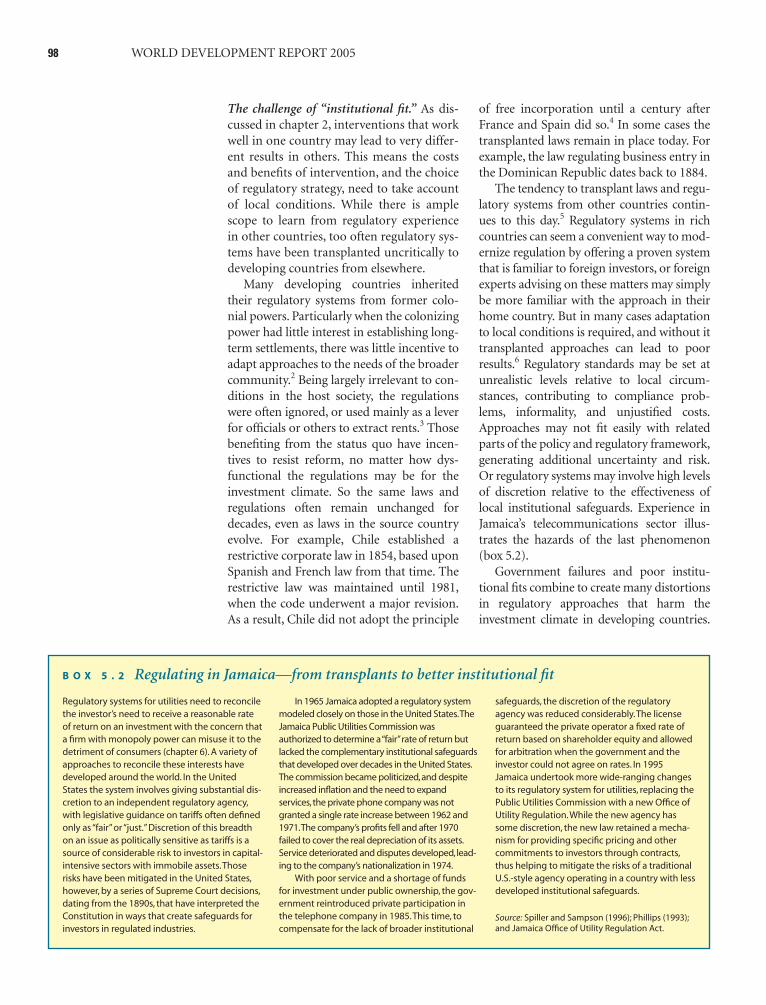

5.2 Regulating in Jamaica—from transplants to betterinstitutional fit 98

5.3 Environmental regulation and global integration 99

5.4 Easing business registration requirements in Vietnamand Uganda 101

5.5 One-stop shops—or one-more-stop shops? 101

Boxes

01_WDR_FM.qxd 9/3/04 11:15 AM Page viii

5.6 Balancing the tradeoffs between specificity anddiscretion in regulation 103

5.7 Contracting for certainty 103

5.8 Competition laws in developing countries 106

5.9 Taxation and global integration: A race to thebottom? 108

5.10 Who pays taxes levied on firms? 108

5.11 Tax receipts as lottery tickets? 110

5.12 Dealing with short-term international capital flows 113

5.13 Reducing customs delays in Singapore and Ghana 114

5.14 Contracting out customs in Mozambique 114

6.1 Governments and finance markets: A long anddifficult history 117

6.2 Expanding access to finance in rural areas—newapproaches in India 120

6.3 Commercial microfinanciers enter the market 120

6.4 Establishing a registry for movable collateral inRomania 121

6.5 Improving corporate governance in Brazil and SouthKorea 122

6.6 The political economy of electricity in India 125

6.7 Improving the investment climate for small privateproviders of infrastructure 127

6.8 Better government accounting, better governmentpolicy 128

6.9 Expanding rural access to electricity andtelecommunications 131

6.10 The power to improve productivity in Nigeria 132

6.11 Port reform in Colombia and India 134

6.12 The benefits of rural roads in Morocco and elsewhere 134

7.1 Malaria and HIV/AIDS cloud the investment climate 137

7.2 Why Intel chose Costa Rica as the site of amultimillion dollar plant 139

7.3 Tackling skill imbalances through public support fortraining and retraining programs 140

7.4 The core labor standards 141

7.5 The role and impact of unions 142

7.6 Labor regulation and global integration 146

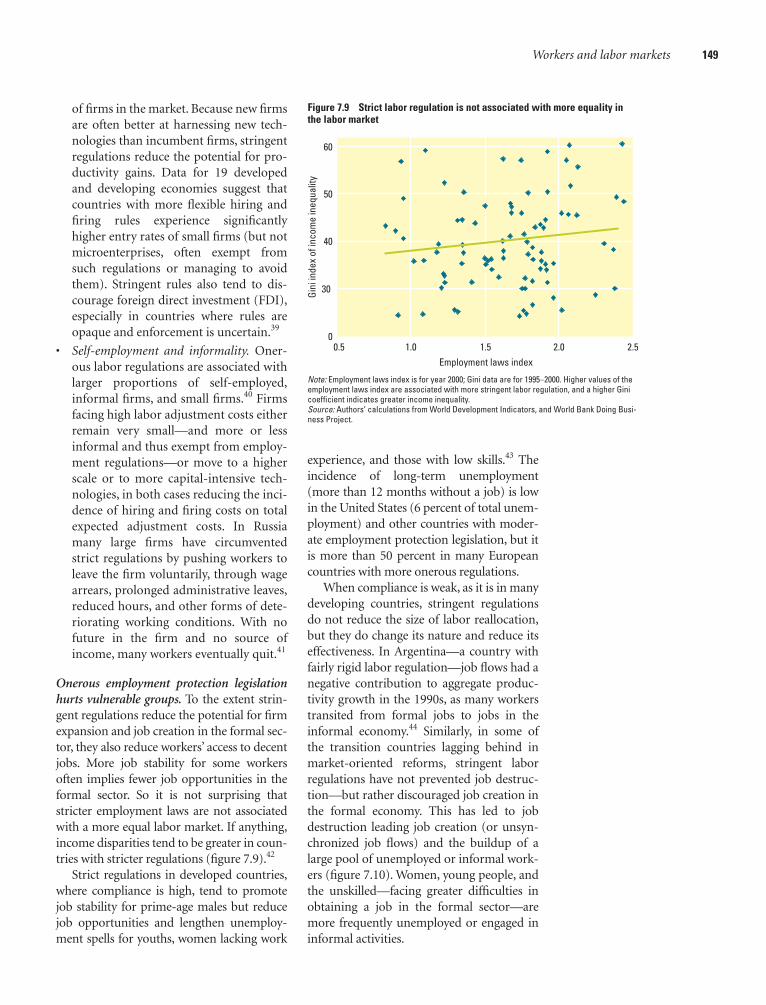

7.7 Do firms’ perceptions square with actual laborregulations? 148

7.8 Reforming severance pay in Colombia and Chile 154

8.1 Unforeseen successes in Bangladesh and Kenya 160

8.2 Picking “winners” can be an expensive gamble—SOTEXKA in Senegal 160

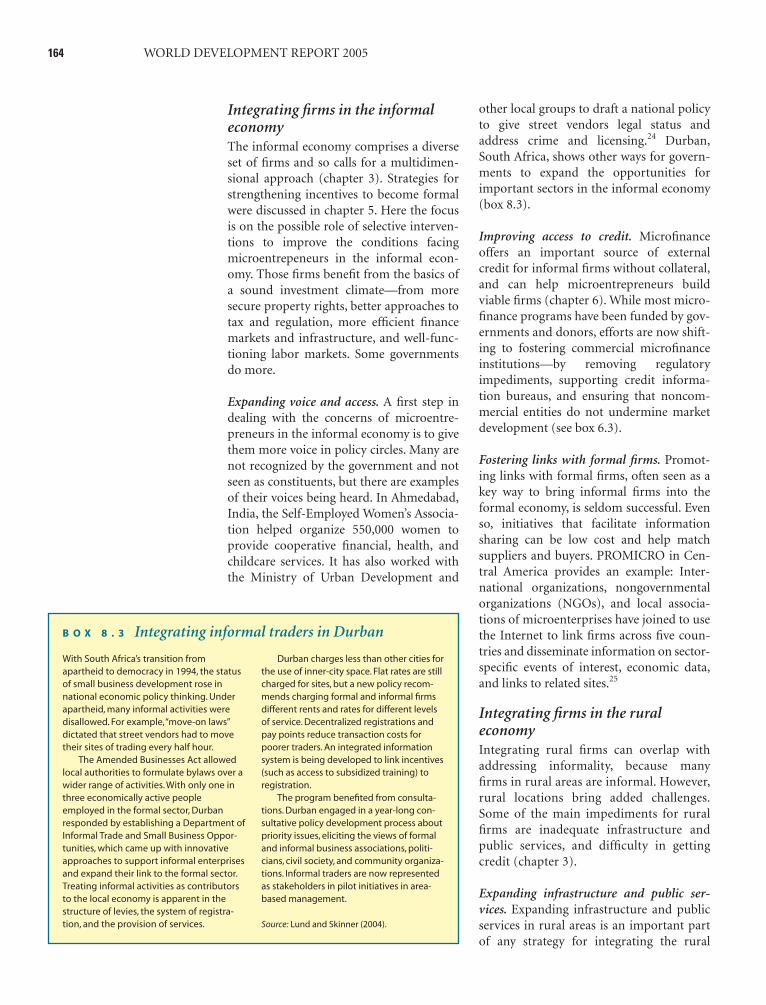

8.3 Integrating informal traders in Durban 164

8.4 Rural credit in Brazil 165

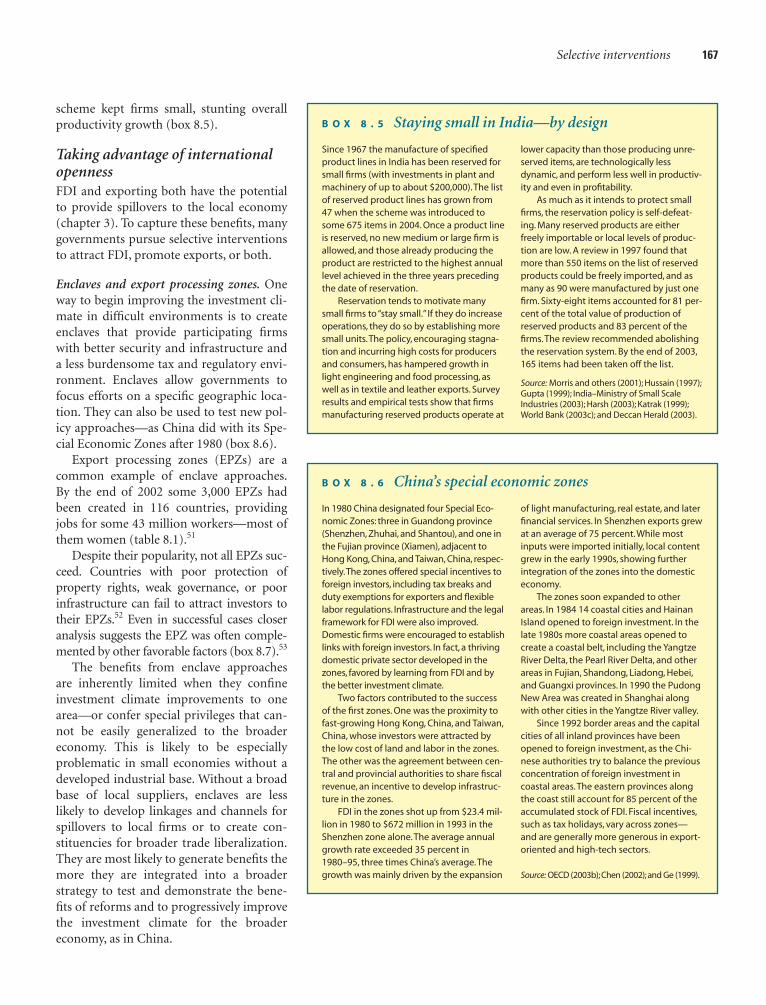

8.5 Staying small in India—by design 167

8.6 China’s special economic zones 167

8.7 Export processing zones in Mauritius and theDominican Republic 168

8.8 The WTO and selective intervention 169

8.9 Rolling the dice in Indianapolis 170

8.10 Competing to attract investment within countries 171

8.11 Fixing the FDI strategy for Mexico’s computerindustry 172

8.12 Successful “linkage programs” in Singapore andIreland 172

8.13 Public-private partnerships for R&D 174

9.1 Evaluating rules and standards—compliancemechanisms and participation 176

9.2 BITs—enhancing credibility one bit at a time? 177

9.3 NEPAD and its peer review mechanism 179

9.4 The evolving system of investor-state disputesettlement 181

9.5 Harmonizing business law in Africa—OHADA 181

9.6 International cooperation to combat corruption 183

9.7 Privatizing international cooperation on corporatesocial responsibility 184

9.8 A multilateral agreement on investment? 185

10.1 Multidonor technical assistance facilities and theinvestment climate 193

10.2 Knowing when to stop: UNDP’s microfinanceactivities in Bangladesh 194

Contents ix

Figures

1 Domestic private investment dominates foreign directinvestment 2

2 Productivity accounts for a significant share ofgrowth 3

3 More competitive pressure, more innovation 3

4 Growth is closely associated with poverty reduction 3

5 How 60,000 poor people rated jobs and self-employment as paths out of poverty 4

6 The informal economy is substantial in manydeveloping countries 4

01_WDR_FM.qxd 9/3/04 11:15 AM Page ix

x CONTENTS

7 Costs vary widely in level and composition 4

8 Small and informal firms are often hit hardest byinvestment climate constraints 5

9 Constraints reported by firms—comparing Bulgaria,Georgia, and Ukraine 8

10 Firms in many developing countries lack confidencein the courts to uphold their property rights 9

11 The inadequacies of finance and infrastructure aresevere for many developing countries 11

Firms rating finance and infrastructure as a “major”or “severe” constraint 11

12 Firms often rate skill shortage and labor regulationsas serious obstacles 11

13 Manufacturing value-added in a single country can far exceed net global official development finance 14

1.1 Institutions, broadly measured, clearly matter forgrowth 21

1.2 Costs vary widely in level and composition 23

1.3 Regulatory unpredictability is a big concern for firms 23

1.4 Competitive pressure can vary significantly betweencountries 23

1.5 Investment climate conditions vary within countries 24

1.6 Investment climate conditions can affect firmsdifferently 24

1.7 Significant economic growth is a modernphenomenon 25

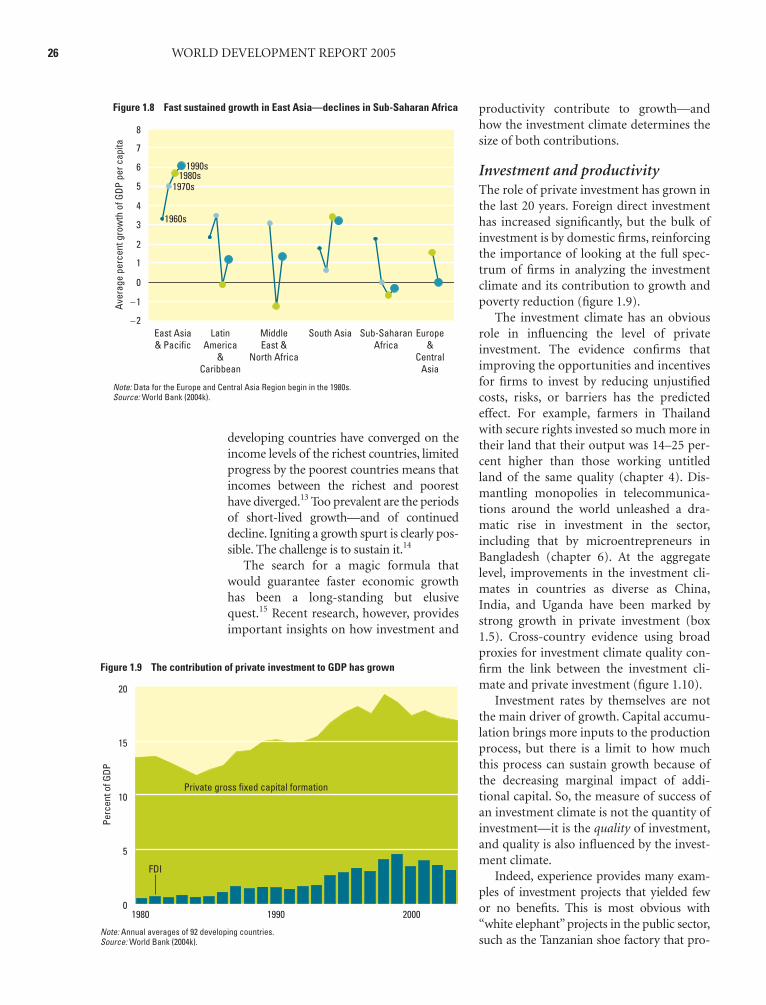

1.8 Fast sustained growth in East Asia—declines in Sub-Saharan Africa 26

1.9 The contribution of private investment to GDP hasgrown 26

1.10 Private investment has grown faster in countries withbetter investment climates 27

1.11 Differences in TFP account for the largest share ofdifferences in GDP growth per worker 28

1.12 More competitive pressure, more innovation 29

1.13 The contribution of net entry to productivity ishigher when barriers to entry are lower 30

1.14 Poverty reduction is closely associated with growth 31

1.15 Self-employment and wage income are the ways outof poverty 33

1.16 Growing economies generate more jobs—particularlyin developing countries 33

1.17 The informal economy is substantial in manydeveloping countries 34

1.18 Rising GDP is associated with rising tax revenues—expanding the opportunities to fund services for thepoor 35

Formal and informal firms have different perspectives 39

2.1 The main locus of bribe-taking can vary 41

2.2 More business start-up procedures increase bothdelays and corruption 42

2.3 More influential firms face fewer constraints 44

2.4 More influential firms innovate less 45

2.5 Cronyism is reduced by greater accountability—andlegislatures play an especially important role 46

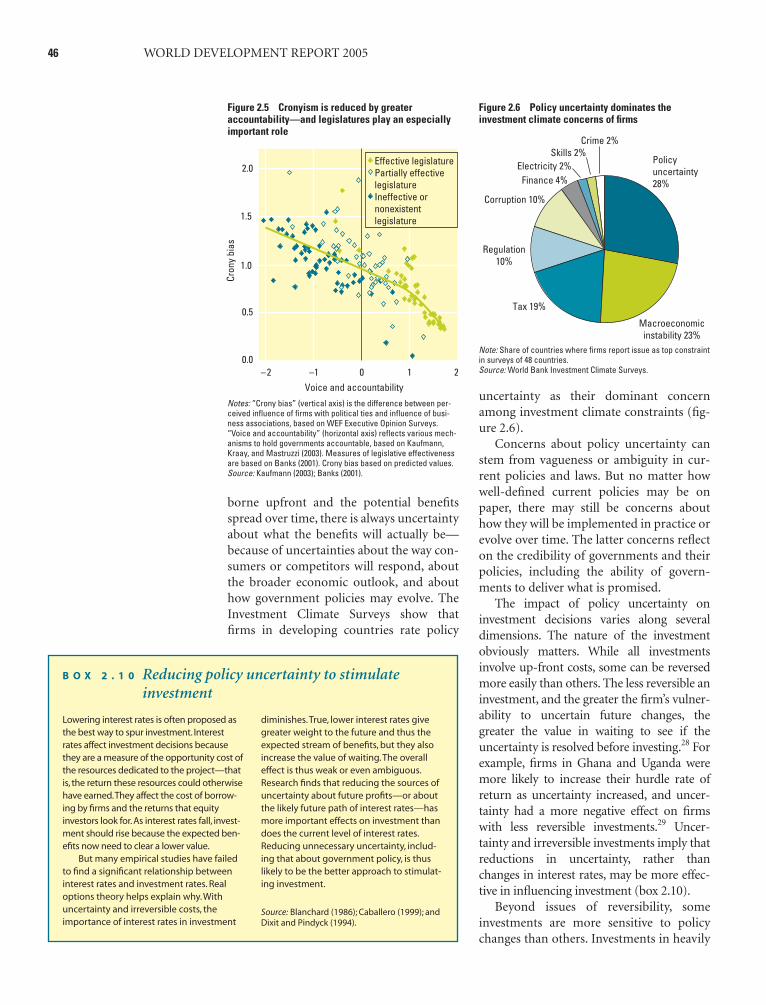

2.6 Policy uncertainty dominates the investment climateconcerns of firms 46

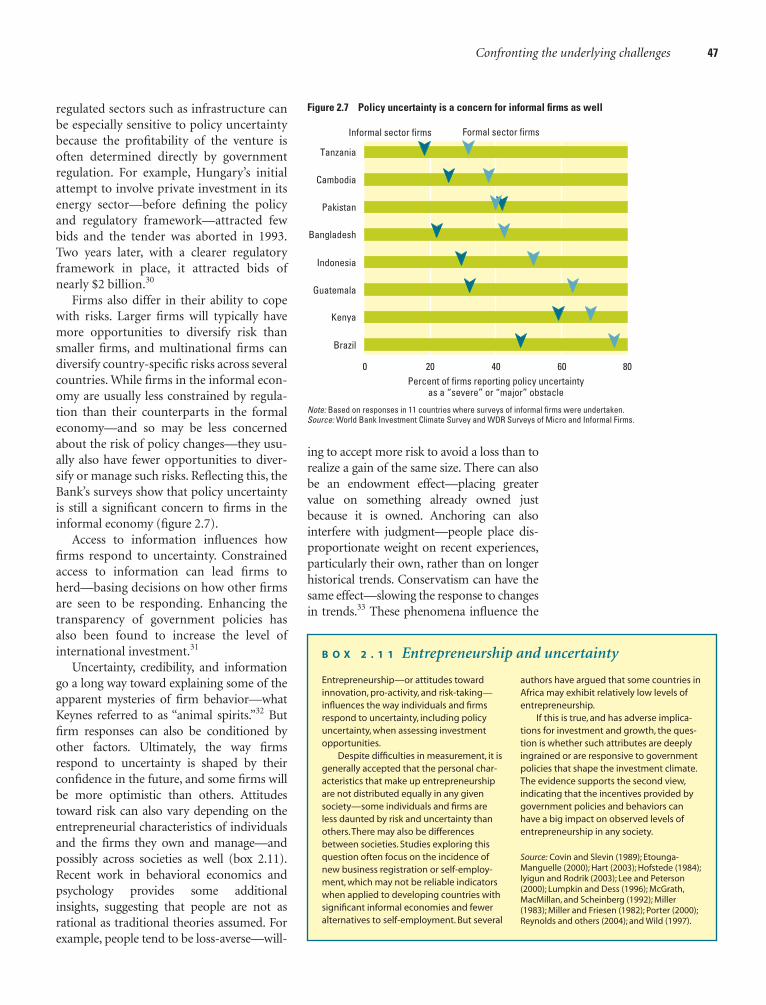

2.7 Policy uncertainty is a concern for informal firms aswell 47

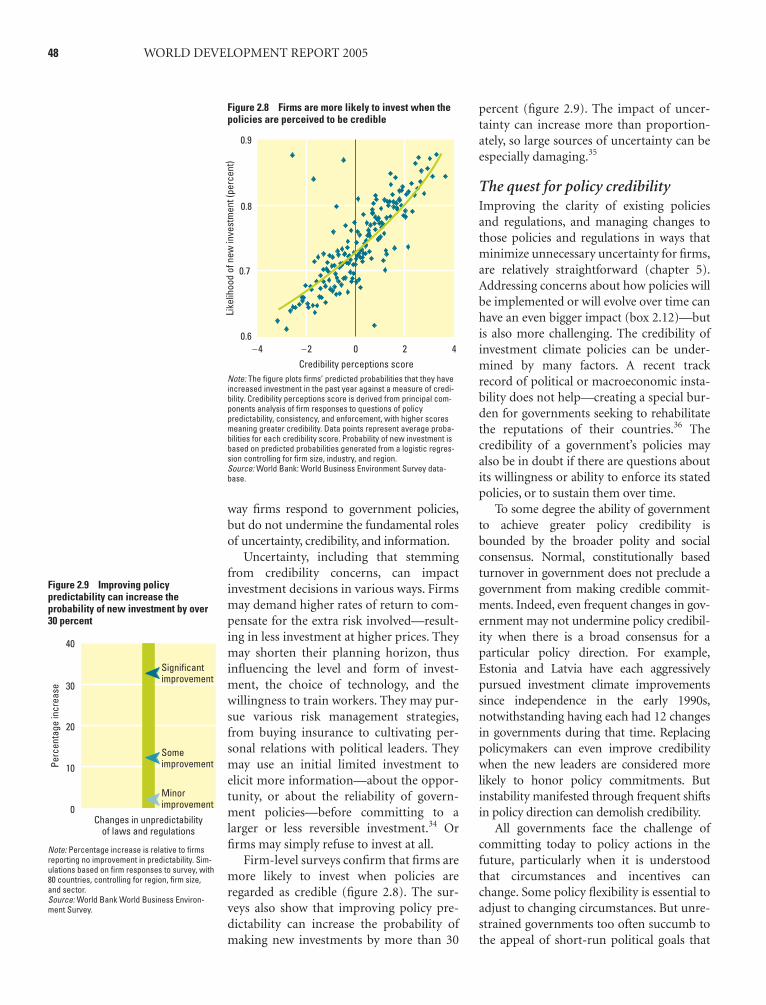

2.8 Firms are more likely to invest when the policies areperceived to be credible 48

2.9 Improving policy predictability can increase theprobability of new investment by over 30 percent 48

2.10 The power of restraint: governments with lessdiscretion present lower investment risk 49

2.11 Support for markets does not always track economicgrowth—as in Latin America 51

2.12 Strong support for international trade and business—but less confidence in corporations 52

3.1 Constraints reported by firms—comparing Bulgaria,Georgia, and Ukraine 59

3.2 Informality is a matter of degree 62

3.3 Women’s participation is concentrated in theinformal sector, among the smallest firms 62

3.4 The contribution of SMEs to GDP does not vary toomuch by income—but the relative importance ofinformal and formal firms shifts dramatically 63

3.5 Gross exports and FDI in developing economiesjumped in the 1990s 65

3.6 Gaining access to technological innovations—keysources 67

4.1 Not entitled? 81

4.2 Leasing activity is more prevalent in Tunisia than inEgypt or Lebanon, thanks to laws facilitatingrepossession 84

4.3 Many firms do not believe the courts will upholdtheir property rights 87

4.4 Reforms speed up court business in RepúblicaBolivariana de Venezuela 87

4.5 Crime takes a heavy toll on many Latin Americaneconomies 89

01_WDR_FM.qxd 9/3/04 11:15 AM Page x

4.6 Crime is a significant constraint on firms in allregions 89

4.7 Risky business 93

5.1 Low-income countries tend to regulate more 96

5.2 Starting a new business takes longer and is morecostly in developing countries 100

5.3 Larger firms spend more time dealing withregulations and are inspected more often 100

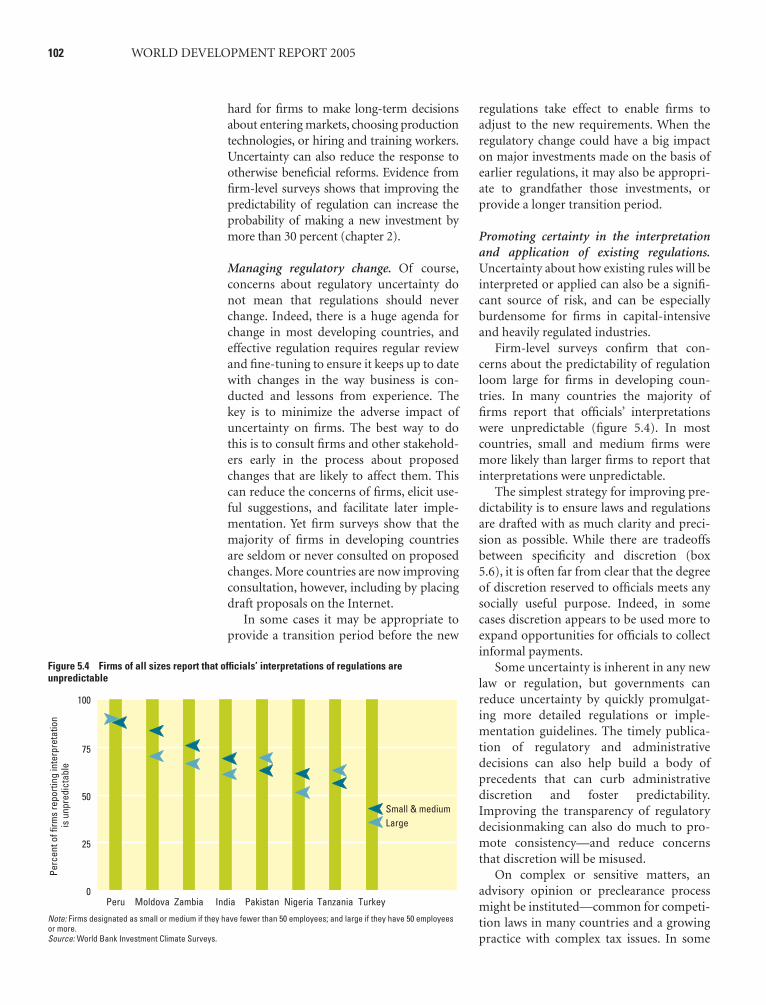

5.4 Firms of all sizes report that officials’ interpretationsof regulations are unpredictable 102

5.5 Despite strong laws, competition policy is seen to beless effective in low-income countries 105

5.6 Corporate tax and VAT rates are similar in high-income and developing countries 107

5.7 Corporate tax revenues remained stable or increasedduring the 1990s, except in ECA 107

5.8 Caught in the middle: Taxing firms in Uganda andCameroon 109

5.9 Many firms rate tax administration as a seriousobstacle 109

5.10 Most changes in national regulations governing FDIreduced restrictions 112

5.11 Restrictions on FDI have fallen in manufacturing, butpersist in other sectors 112

5.12 Clearing customs for imports—from under 2 days to 18 113

6.1 The inadequacies of finance and infrastructure aresevere for many developing countries 115

6.2 Sources of fixed investment financing differ for smalland large firms 116

6.3 State-owned banks are holding on, especially in Indiaand in the Middle East and North Africa 118

6.4 Infrastructure concerns expressed by firms vary bysize and sector 124

6.5 More developing countries are involving the privatesector in infrastructure provision 126

6.6 Investment in infrastructure projects with privateparticipation has recently fallen 126

6.7 Teledensity increases with the quality of the investmentclimate, even controlling for incomes 126

6.8 Perceived fairness allows lower rates of return to bepromised for a given legal protection 127

6.9 Long delays for phone connections are common,especially without competition 130

6.10 Liberalization and good regulation accelerate thegrowth of phone connections 130

6.11 Competition spurs the spread of mobile phones inSub-Saharan Africa 130

6.12 Competition in international calls is still limited orprohibited in much of the developing world 131

6.13 Many days of power outages a year, and a higher shareof firms having their own generators 132

6.14 The declining costs of transport andtelecommunications 133

7.1 Firms rate skill shortages and labor regulations asserious constraints in many countries 136

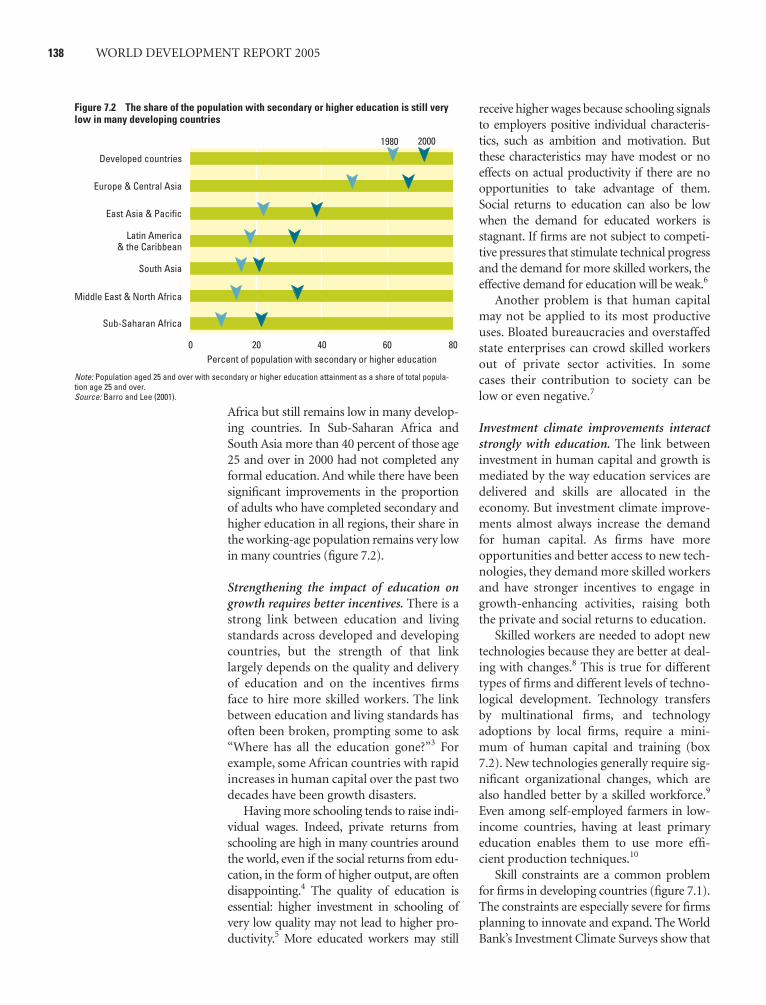

7.2 The share of the population with secondary or highereducation is still very low in many developingcountries 138

7.3 Skill constraints and innovative firms 139

7.4 The minimum wage is very high in many developingcountries and, at high levels, leads to weakcompliance 144

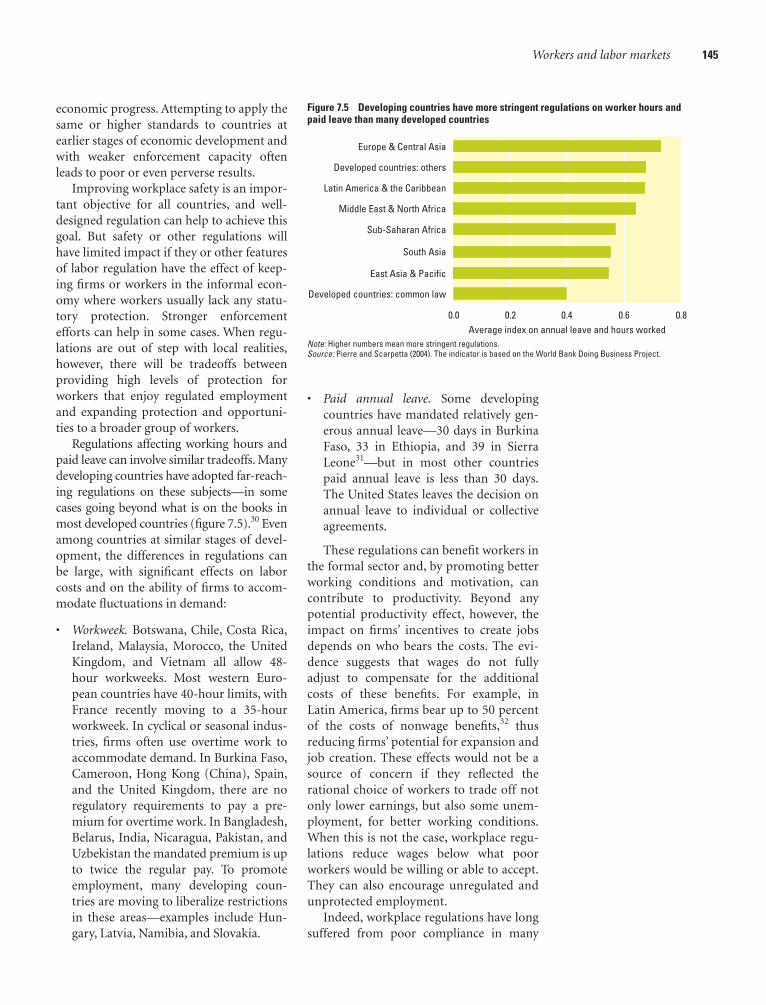

7.5 Developing countries have more stringent regulationson worker hours and paid leave than many developedcountries 145

7.6 High job turnover in developed and developingcountries in the 1990s 146

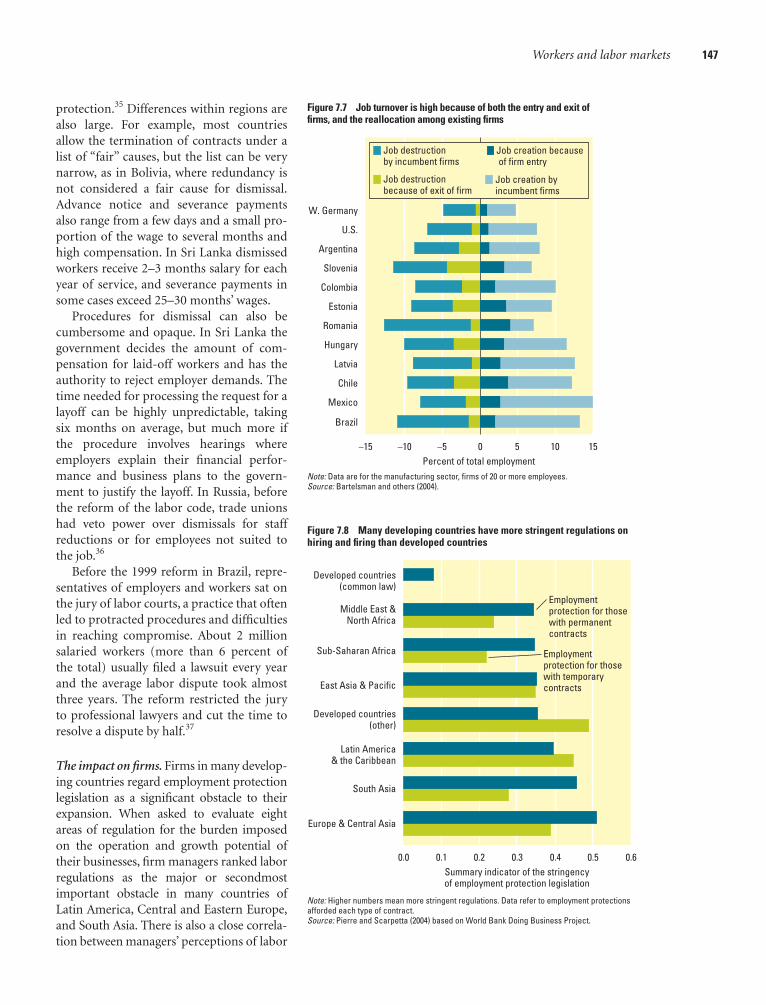

7.7 Job turnover is high because of both the entry and exitof firms, and the reallocation among existing firms 147

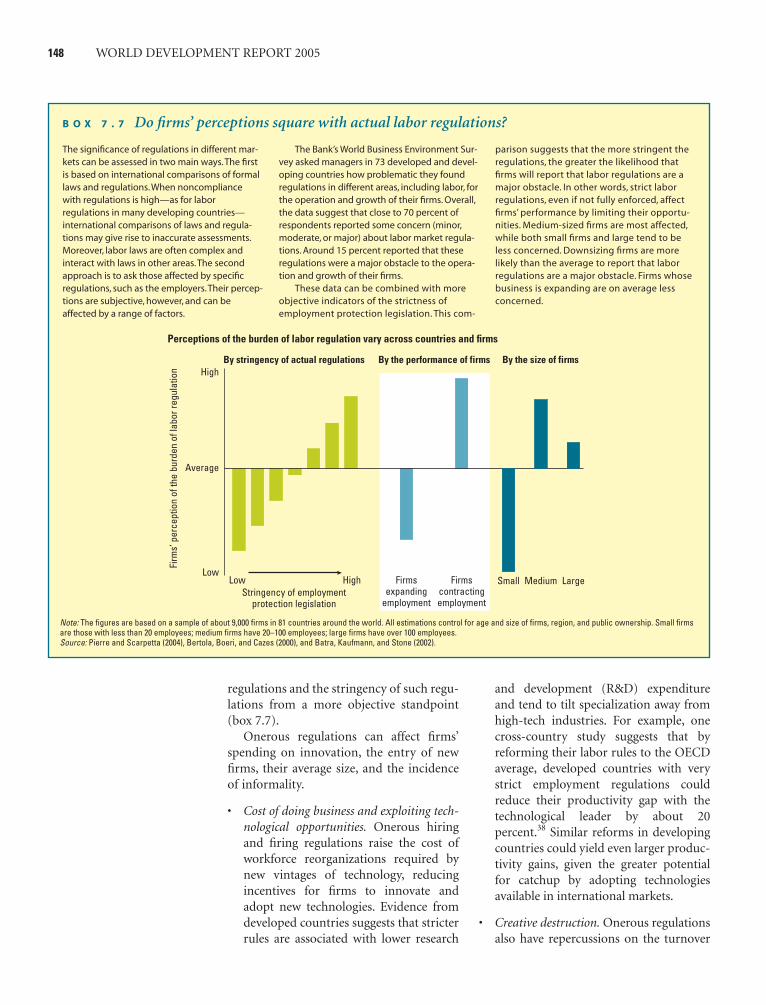

7.8 Many developing countries have more stringentregulations on hiring and firing than developedcountries 147

Perceptions of the burden of labor regulation varyacross countries and firms 148

7.9 Strict labor regulation is not associated with moreequality in the labor market 149

7.10 Unsynchronized job creation and destruction can giverise to unemployment or underemployment 150

7.11 Since the labor reform of 1990, there has been higherjob turnover in Colombia 150

7.12 Developing countries, particularly low-income ones,offer much weaker and less diverse protection againstunemployment risks than developed countries 151

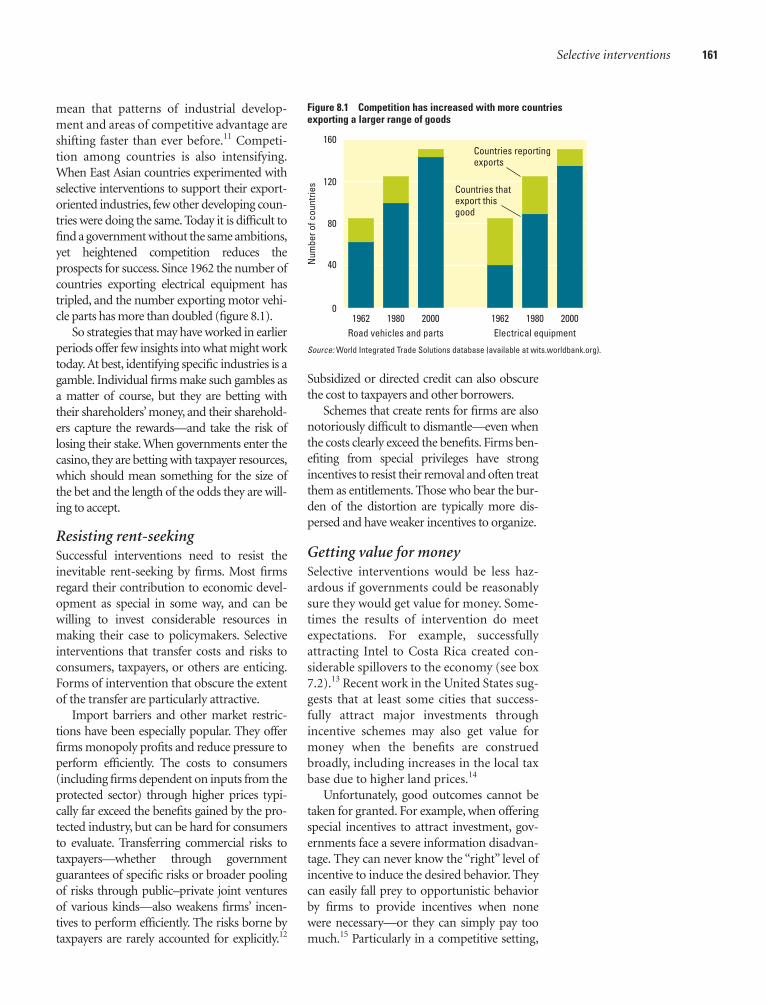

8.1 Competition has increased with more countriesexporting a larger range of goods 161

8.2 Incentives can be costly 170

8.3 Policy advocacy by investment promotion agenciesreceives a small share of budget 171

8.4 Grants make up the lion’s share of public funding forprivate R&D in many developed countries 173

9.1 Participation in bilateral investment treaties (BITs)has shot up in recent years 177

Contents xi

01_WDR_FM.qxd 9/3/04 11:15 AM Page xi

xii CONTENTS

9.2 NAFTA and Mexico’s investment profile 178

9.3 Regional economic cooperation agreementsproliferated in the 1990s 182

Standards are influencing business 184

10.1 Manufacturing value added in a single country can farexceed net global official development finance 189

Tables

1.1 Government policies and behaviors and investmentdecisions—some examples 22

2.1 Bribes vary by firm size, sector, and region 40

3.1 Who innovates? 67

3.2 Consultative forums dealing with investment climateissues—some illustrations 72

In some developing countries competition agenciesdeal with very few cases 106

5.1 Firms report that tax rates are one of their topconcerns 107

8.1 Export processing zones have proliferated into thethousands 168

8.2 Effective reductions in corporate tax rates due to fiscalincentives 169

8.3 IPAs are not cheap 171

8.4 Fiscal incentives for R&D in selected developingcountries 173

10.1 Support for investment climate reforms and to firmsand transactions 191

New investment climate measures from the WorldBank 245

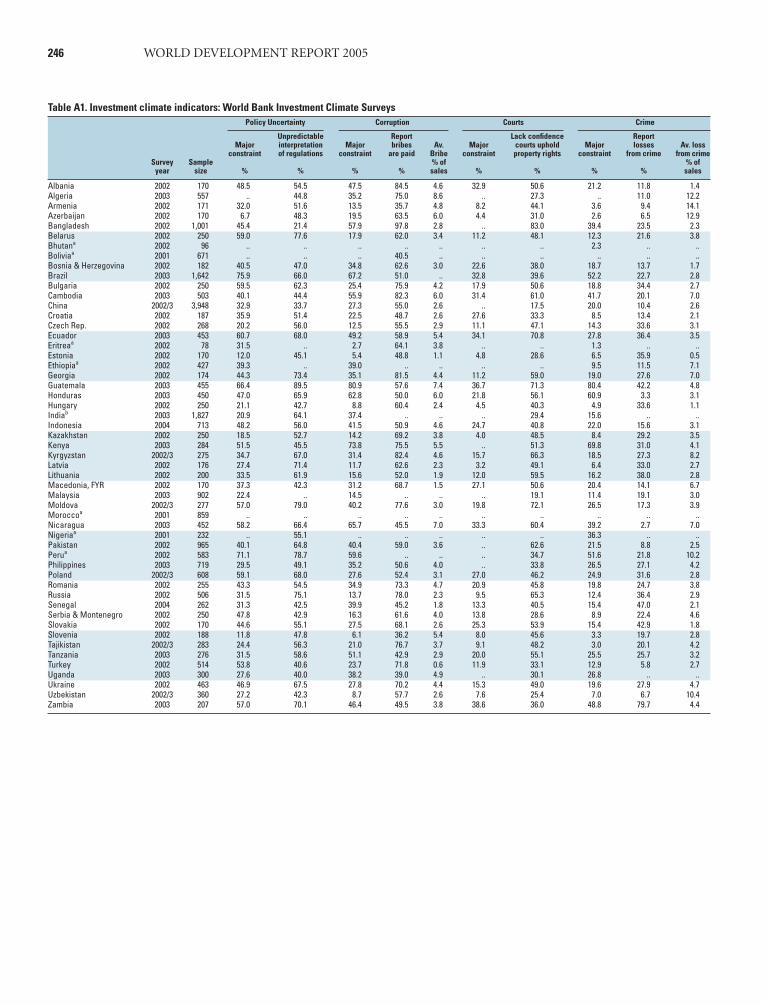

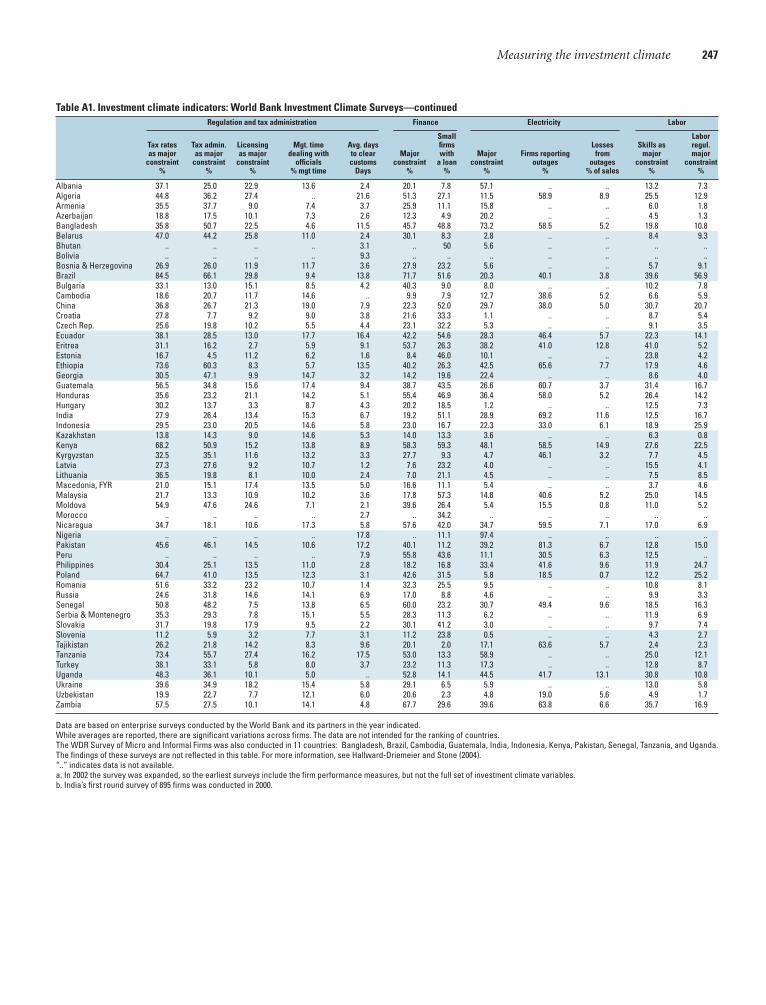

A1 Investment climate indicators: World BankInvestment Climate Surveys 246

A2 Investment climate indicators: expert polls and othersurveys 248

Other sources of investment climate–relatedindicators—selected examples 251

Classification of economies by region and income,FY2005 255

1 Key indicators of development 256

2 Poverty and income distribution 258

3 Economic activity 260

4 Trade, aid, and finance 262

5 Key indicators for other economies 264

01_WDR_FM.qxd 9/3/04 11:15 AM Page xii

This World Development Report is about creating opportunities for people to escape frompoverty and improve their living standards. It is about creating a climate in which firms andentrepreneurs of all types—from farmers and microenterprises to local manufacturing con-cerns and multinationals—have opportunities and incentives to invest productively, createjobs, and expand, and thereby contribute to growth and poverty reduction. The Report thusdeals with one of the central challenges of development.

Expanding opportunities for people in developing countries is a pressing concern for gov-ernments and for the global community. Nearly half the world’s population lives on less than $2a day, and 1.1 billion barely survive on less than $1 a day. Young people have more than doublethe average unemployment rate in all regions, and population growth will add nearly 2 billionmore people to developing countries over the next 30 years. Improving the climate for invest-ment in developing countries is essential to provide jobs and opportunities for young peopleand to build a more inclusive, balanced, and peaceful world.

There is good news. More governments are recognizing that their policies and behaviorsplay a critical role in shaping the investment climates of their societies, and they are makingchanges. China and India provide compelling examples: investment climate improvements inthese countries have driven growth and the most dramatic reductions in poverty in history.Many other governments are also taking on the agenda, but progress remains slow and uneven.Governments still saddle firms and entrepreneurs with unnecessary costs, create substantialuncertainty and risk, and erect unjustified barriers to competition.

This year’s World Development Report, the 27th in the World Bank’s flagship series, looks atwhat governments can do to create better investment climates for their societies. Drawing onnew research, including surveys of nearly 30,000 firms in 53 developing countries, other newdata, and country case studies, it makes four main points.

First, the Report emphasizes that the goal should be to create an investment climate that isbetter for everyone—in two dimensions. The investment climate should benefit society as awhole, not only firms. Well-designed regulation and taxation are thus an important part of agood investment climate. And the investment climate should embrace firms of all types, notjust large or influential firms. Small and large firms, local and foreign firms, and low-tech andhigh-tech firms each have important and complementary contributions to make to growth andpoverty reduction.

Second, the Report argues that efforts to improve the investment climate need to go beyondjust reducing business costs. Those costs can indeed be extraordinary in many countries,amounting to several times what firms pay in taxes. But policy-related risks dominate firms’concerns in developing countries and can cripple incentives to invest. And barriers to competi-tion remain pervasive, dulling incentives for firms to innovate and increase productivity. Gov-ernments need to address all three aspects of a good investment climate.

Third, the Report underscores that progress requires more than changes in formal policies.The gaps between policies and their implementation can be huge, with the vast informaleconomies in many developing countries providing the most palpable evidence. Governments

Foreword

xiii

01_WDR_FM.qxd 9/3/04 11:15 AM Page xiii

xiv WORLD DEVELOPMENT REPORT 2005

need to bridge these gaps and address deeper sources of policy failure that can undermine a soundinvestment climate. Governments need to tackle corruption and other forms of rent-seeking, tobuild credibility with firms, to foster public trust and legitimacy, and to ensure their policy interven-tions are crafted to fit local conditions.

Finally, the Report reviews strategies for tackling such a broad agenda. It emphasizes that perfec-tion is not required and that everything does not have to be done at once. But progress requires gov-ernments to address important constraints in ways that give firms the confidence to invest—and tosustain a process of ongoing improvements. Persistence pays off.

These findings are supported by detailed analysis and the many examples discussed throughoutthe Report, which should provide practical insights for policymakers and for others concerned withgrowth and poverty reduction in developing countries.

Improving the investment climate is the first pillar of the World Bank’s overall development strat-egy. The World Development Report 2005 complements last year’s WDR, which addressed key aspectsof the second pillar of that strategy: investing in and empowering people to take advantage of oppor-tunities. Together, these two Reports offer sound advice and research that will help the World Bankand our partners realize our common dream—a world free of poverty.

James D. WolfensohnPresidentThe World Bank

01_WDR_FM.qxd 9/3/04 11:15 AM Page xiv

xv

This Report has been prepared by a team led by Warrick Smith and comprising MaryHallward-Driemeier, Gaiv Tata, George Clarke, Raj Desai, Timothy Irwin, Richard Messick,Stefano Scarpetta, and Ekaterina Vostroknutova. Leora Klapper and Sunita Kikeri also con-tributed. The team was assisted by Yanni Chen, Alexandru Cojocaru, Zenaida Hernandez,Tewodaj Mengistu, Claudio E. Montenegro, and David Stewart. Bruce Ross-Larson was thedevelopmental editor. The work was initiated under the direction of Nicholas Stern and carriedout under the general direction of François Bourguignon.

Many others inside and outside the World Bank provided helpful comments, includingDaron Acemoglu, Erik Berglöf, Robin Burgess, Ha-Joon Chang, Shantayanan Devarajan, DavidDollar, John Haltiwanger, Michael Klein, Howard Pack, and Lant Pritchett. The DevelopmentData Group contributed to the data appendix and was responsible for the Selected WorldDevelopment Indicators. Much of the background research was supported by generous trustfund grants from the U.K. Department for International Development and from the Swedishand Swiss Governments.

The team undertook a wide range of consultations for this Report, which included work-shops in Berlin, Dar-es-Salaam, London, New Delhi, Shanghai, and Washington, D.C.; video-conferences with sites in Brazil, Egypt, Guatemala, Honduras, Japan, Lebanon, Nicaragua, Rus-sia, and Serbia and Montenegro; and an on-line discussion of the draft report. Participants inthese workshops, videoconferences, and discussions included researchers, government officials,and staff of nongovernmental and private-sector organizations.

Rebecca Sugui served as executive assistant to the team, Ofelia Valladolid as program assis-tant, and Madhur Arora and Jason Victor as team assistants. Evangeline Santo Domingo servedas resource management assistant.

Book design, editing, and production were coordinated by the World Bank’s Office of thePublisher under the supervision of Susan Graham, Denise Bergeron, and Janet Sasser.

Acknowledgments

01_WDR_FM.qxd 9/3/04 11:15 AM Page xv

APEC Asia-Pacific Economic CooperationBEEPS II Business Environment and Enterprise

Performance Survey II BITs Bilateral investment treatiesDFIs Development finance institutionsEPZs Export processing zonesEU European UnionFDI Foreign direct investmentGATT General Agreement on Tariffs and Trade GDP Gross domestic productGNI Gross national incomeHIV/AIDs Human immunodeficiency virus/

acquired immunodeficiency syndromeICRG International Country Risk GuideICS Investment Climate Surveys ICSID International Centre for Settlement of

Investment DisputesILO International Labour OrganisationIMF International Monetary FundMERCOSUR Common Market of the South

NAFTA North American Free Trade AgreementNEPAD New Partnership for Africa’s DevelopmentNGOs Nongovernmental organizationsOECD Organisation for Economic Co-operation and

DevelopmentPPP Purchasing power parity R&D Research and developmentSMEs Small and medium enterprisesTFP Total factor productivityU.N. United NationsUNCITRAL United Nations Commission on International

Trade LawUNCTAD United Nations Conference on Trade and

DevelopmentUNDP United Nations Development ProgrammeUSAID U.S. Agency for International DevelopmentVAT Value added taxWEF World Economic Forum WTO World Trade Organization

Abbreviations and Data Notes

Abbreviations

xvi

Data NotesThe countries included in regional and income groupings inthis Report are listed in the Classification of Economies tableat the beginning of the Selected World Development Indica-tors. Income classifications are based on GNP per capita;thresholds for income classifications in this edition may befound in the Introduction to Selected World DevelopmentIndicators. Group averages reported in the figures and tablesare unweighted averages of the countries in the group unlessnoted to the contrary.

The use of the word countries to refer to economiesimplies no judgment by the World Bank about the legal or

other status of a territory. The term developing countriesincludes low- and middle-income economies and thus mayinclude economies in transition from central planning, as amatter of convenience. The term developed countries is usedto denote the high-income economies.

Dollar figures are current U.S. dollars, unless otherwisespecified. Billion means 1,000 million; trillion means 1,000billion.

01_WDR_FM.qxd 9/3/04 11:15 AM Page xvi

1

Everyday, firms around the world face impor-tant decisions. A rural microentrepreneurconsiders whether to open a small business tocomplement her family's farm income. Alocal manufacturing company ponderswhether to expand its production line andhire more workers. A multinational enter-prise evaluates alternative locations for itsnext global production facility. Their deci-sions have important implications for growthand poverty in each location. And their deci-sions will depend largely on the way govern-ment policies and behaviors shape the invest-ment climate in those locations.

A good investment climate providesopportunities and incentives for firms—frommicroenterprises to multinationals—to investproductively, create jobs, and expand. It thusplays a central role in growth and povertyreduction. Improving the investment climatesof their societies is critical for governments inthe developing world, where 1.2 billion peoplesurvive on less than $1 a day, where youthshave more than double the average unem-ployment rate, and where populations aregrowing rapidly. Expanding jobs and otheropportunities for young people is essential tocreate a more inclusive, balanced, and peace-ful world.

New data from the World Bank providefresh insights into how investment climatesvary around the world and how they influ-ence growth and poverty. These includeInvestment Climate Surveys, which covermore than 26,000 firms in 53 developingcountries, and the Doing Business Project,which benchmarks regulatory regimes inmore than 130 countries.1 World Develop-ment Report 2005 draws on those data, othernew evidence, and emerging lessons of inter-national experience to look at what govern-ments at all levels can do to create a betterinvestment climate—an investment climate

that benefits society as a whole, not just firms,and one that embraces all firms, not just largeor politically connected firms. In short, a bet-ter investment climate for everyone.

The investment climate is centralto growth and poverty reductionPrivate firms—from farmers and microen-trepreneurs to local manufacturing compa-nies and multinational enterprises—are atthe heart of the development process. Drivenby the quest for profits, they invest in newideas and new facilities that strengthen thefoundation of economic growth and pros-perity. They provide more than 90 percent ofjobs, creating opportunities for people toapply their talents and improve their situa-tions. They provide the goods and servicesneeded to sustain life and improve livingstandards. They are also the main source oftax revenues, contributing to public fundingfor health, education, and other services.Firms are thus critical actors in the quest forgrowth and poverty reduction.

The contribution firms make to societyis mainly determined by the investment cli-mate—the location-specific factors thatshape the opportunities and incentives forfirms to invest productively, create jobs, andexpand (box 1). Government policies andbehaviors play a key role in shaping theinvestment climate. While governmentshave limited influence on factors such asgeography, they have more decisive influ-ence on the security of property rights,approaches to regulation and taxation(both at and within the border), the provi-sion of infrastructure, the functioning offinance and labor markets, and broadergovernance features such as corruption.Improving government policies and behav-iors that shape the investment climate dri-ves growth and reduces poverty.

Overview

02_WDR_Overview.qxd 8/24/04 11:42 AM Page 1

risks, and barriers to competition. As a resultof investment climate improvements in the1980s and 1990s, private investment as ashare of GDP nearly doubled in China andIndia; in Uganda it more than doubled.2 InPoland, Romania, Russia, Slovakia, andUkraine firms that believe their propertyrights are secure reinvest between 14 and 40percent more of their profits in their busi-nesses than those who don’t.3 Improvingpolicy predictability can increase the likeli-hood of new investment by more than 30percent. Reducing barriers to competition intelecommunications in the 1990s unleasheda surge of new investment worldwide—including investment by microentrepreneursin Bangladesh and Uganda.

But it is not just the volume of invest-ment that matters for growth—it is the pro-ductivity gains that result (figure 2).4 Agood investment climate encourages higherproductivity by providing opportunitiesand incentives for firms to develop, adapt,and adopt better ways of doing things—notjust innovations of the kind that mightmerit a patent but also better ways to orga-nize a production process, distribute goods,and respond to consumers.

What is required? Low barriers to the dif-fusion of new ideas, including barriers toimporting modern equipment and adjustingthe way work is organized. And an environ-ment that fosters the competitive processes

2 WORLD DEVELOPMENT REPORT 2005

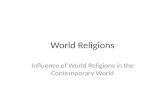

The investment climate reflects the many loca-tion-specific factors that shape the opportuni-ties and incentives for firms to investproductively, create jobs, and expand. A goodinvestment climate is not just about generatingprofits for firms—if that were the goal, the focuscould be limited to minimizing costs and risks. Agood investment climate improves outcomesfor society as a whole.That means that somecosts and risks are properly borne by firms. Andcompetition plays a key role in spurring innova-tion and productivity and ensuring that thebenefits of productivity improvements areshared with workers and consumers.

Looking at growth and poverty reductionthrough an investment climate lens offers sev-eral insights:

• It puts firms—the actors making investment andhiring decisions—at the center of the discussion.

• It recognizes that firms assess investmentopportunities and related government poli-cies and behaviors as part of a package.Thisreinforces the importance of looking at prop-erty rights, regulation, taxes, finance,infrastructure, corruption, and other areas ofgovernment policy and behavior as part of anintegrated whole, rather than in isolation.

• It highlights the forward-looking nature ofinvestment activity. Investment is based onexpectations about the future and not just oncurrent conditions.This underlines the impor-tance of governments fostering stability andcredibility, which are critical elements of asound investment climate.

• It treats as fundamental the need for policy-makers to balance the goal of encouragingproductive private investment with othersocial goals. Firms provide many benefits for

society, but the interests of firms and societyare not the same in all respects. Good publicpolicy is not about giving firms everythingthey might ask for, but rather about balancinga range of social interests.

A good investment climate provides oppor-tunities for people to better themselves, andimproving the investment climate is the first pil-lar of the World Bank’s overall developmentstrategy. A critical complementary agenda is toinvest in and empower people so they can takeadvantage of those opportunities; this is thesecond pillar of the Bank’s strategy. World Devel-opment Report 2004: Making Services Work forPoor People focused on key aspects of that sec-ond pillar.

Source: Authors and Stern (2002).

B O X 1 The investment climate perspective

Figure 1 Domestic private investment dominates foreign direct investment

Note: Annual averages of 92 developing countries.Source: World Bank (2004k).

0

5

10

15

Perc

ent o

f GDP

20

20001990

Private gross fixed capital formation

1980

FDI

Driving growthWith rising populations, economic growth isthe only sustainable mechanism for increas-ing a society's standard of living. A goodinvestment climate drives growth by encour-aging investment and higher productivity.

Investment underpins economic growthby bringing more inputs to the productionprocess. Foreign investment is becomingmore important in developing countries,but the bulk of private investment remainsdomestic (figure 1).

A good investment climate encouragesfirms to invest by removing unjustified costs,

02_WDR_Overview.qxd 8/24/04 11:42 AM Page 2

that Joseph Schumpeter called “creativedestruction”—an environment in whichfirms have opportunities and incentives totest their ideas, strive for success, and pros-per or fail.5 A good investment climatemakes it easier for firms to enter and exitmarkets in a process that contributes tohigher productivity and faster growth. Netmarket entry can account for more than 30percent of productivity growth.6 And firmsfacing strong competitive pressure are atleast 50 percent more likely to innovate thanthose reporting no such pressure (figure 3).

Reducing povertyThe critical role the investment climateplays in poverty reduction can be seen intwo ways. First, at the aggregate level, eco-nomic growth is closely associated withreductions in poverty (figure 4). Indeed,investment climate improvements in Chinadrove the most dramatic poverty reductionin history, lifting 400 million people out ofpoverty over 20 years. Second, the contribu-tion can be seen in the way a good invest-ment climate enhances the lives of peopledirectly, in their many capacities.

As employees. The World Bank’s “Voices ofthe Poor” study found that poor peopleidentified getting a job—whether throughself-employment or from wages—as theirmost promising path out of poverty (figure

5). The private sector accounts for morethan 90 percent of jobs in developing coun-tries.7 Better job opportunities also increaseincentives for people to invest in their edu-cation and skills, thus complementingefforts to improve human development.Firms that are more productive can also paybetter wages and invest more in training.8

As entrepreneurs. Hundreds of millions ofpoor people in developing countries maketheir living as microentrepreneurs—as farm-ers, as street vendors, as homeworkers, and ina range of other occupations. They oftenoperate in the informal economy, whichaccounts for more than half of economicactivity in many developing countries (figure6). Firms in the informal economy face manyof the same constraints as other firms,including insecure property rights, corrup-tion, policy unpredictability, and limitedaccess to finance and public services. Reliev-ing these constraints increases incomes forentrepreneurs and allows them to expandtheir activities. A good investment climatealso increases incentives to become part ofthe formal economy.

As consumers. A good investment climateexpands the variety and reduces the costs ofgoods and services, including those consumedby poor people. Investment climate improve-ments lowered food prices in countries

Overview: A better investment climate—for everyone 3

Figure 4 Growth is closely associated with poverty reduction

Note: All figures for 1992–98 except Bangladesh (1992–2000) and India (1993–99).Source: World Bank (2002d).

0

2

4

6

Aver

age

annu

al p

erce

nt c

hang

e 8

10

ChinaVietnamIndiaBangladeshPakistan

GDP per capita growth rate

Poverty reduction

Figure 3 More competitive pressure,more innovation

Note: Percentage increase is relative to firmsreporting no competitive pressure.Source: World Bank Investment ClimateSurveys/BEEPS II in 27 countries in EasternEurope and Central Asia.

50

25

Perc

enta

ge in

crea

se in

prob

abili

ty o

f und

erta

king

act

ivity

0

75

Introducenew product

Upgradeproduct

Somepressure

Moderatepressure

Majorpressure

Education 14%

Capital 45%

TFP 41%

Figure 2 Productivity accounts for asignificant share of growth

Note: Sources of growth for 84 countries from1960–2000. “TFP” is total factor productivity. Source: Bosworth and Collins (2003).

02_WDR_Overview.qxd 8/24/04 11:42 AM Page 3

4 WORLD DEVELOPMENT REPORT 2005

including Ethiopia, Ghana, Kenya, Vietnam,and Zambia.9 Lowering barriers to marketentry by 10 percent has been estimated toreduce the average price markup by nearly 6percent.10

As users of infrastructure, property, andfinance. Improving infrastructure, propertyrights, and finance can deliver broad bene-fits across the community. Building ruralroads helps firms get their goods to market,and in Morocco also increased primaryschool enrollment from 28 to 68 percent.11

Providing more secure rights to landencourages farmers and other firms toinvest and can ease their access to finance;in Peru more secure rights also allowedurban slum dwellers to increase theirincomes by working more hours outside thehome.12 Improving the functioning offinance markets helps firms take advantageof promising investment opportunities, andalso helps poor people weather familyemergencies, educate their children, andimprove their homes.

As recipients of tax-funded services or trans-fers. Firms and their activities are the prin-cipal sources of tax revenue for govern-ments, and growing economies generatemore taxes.13 A good investment climatecan thus expand the resources governmentshave available to fund public services(including health and education) and trans-fers to disadvantaged members of society.

Some investment climate improvementsdeliver broad benefits across society—suchas better macroeconomic stability and lesscorruption. Others have a more focusedimpact on particular locations or activities,creating opportunities for governments toinfluence the distribution of benefits. Gov-ernments can design those investment cli-mate improvements to be even more “pro-poor” by targeting constraints where poorpeople live and constraints to activitiespoor people benefit from, including in theircapacities as employees, entrepreneurs, andconsumers. This means that pro-poorapproaches are not limited to efforts thatfocus on constraints that face small firms.

Tackling costs, risks, and barriersto competitionGovernments influence the investment cli-mate through the impact of their policiesand behaviors on the costs, risks, and barri-ers to competition facing firms. Creating abetter investment climate requires govern-ments to tackle all three. Big variations ininvestment climates around the world high-light the potential for improvement.

CostsGovernment policies and behaviors influ-ence the costs of doing business and hencethe range of investment opportunities thatmight be profitable. Taxes are the mostobvious example. But governments alsohave important roles in providing publicgoods, supporting the provision of infra-structure, and addressing market failures.Weaknesses in government performance inthese roles can greatly increase the costs forfirms and make many potential opportuni-ties unprofitable. How greatly? The costs ofcontract enforcement difficulties, inade-quate infrastructure, crime, corruption, andregulation can amount to over 25 percent ofsales—or more than three times what firmstypically pay in taxes. Both the level and thecomposition of these costs vary widelyacross countries (figure 7).

Costs also have a time dimension. Thereare big variations in the time taken toobtain a telephone line and to clear goodsthrough customs, as well as in the time

Figure 6 The informal economy issubstantial in many developingcountries

Source: Schneider (2002).

0 25

Informal outputas percent of GDP

50 75

Thailand

Nigeria

Tanzania

Peru

Georgia

Russia

Sri Lanka

Morocco

Mexico

Figure 5 How 60,000 poor people rated jobs and self-employment as paths out of poverty

Source: Narayan and others (2000).

0 10 20 30 40 50 60 70

Other

Savings

Migration

Education

FemaleMale

Access to credit

Hard work, perseverance, or thrift

Skill acquisition

Access to agricultural land

Income from agriculture, livestock, or fishing

Benefit of family and kin

Income from wages or salaries

Self-employment or business

Percent

02_WDR_Overview.qxd 8/24/04 11:42 AM Page 4

Overview 5

managers need to spend dealing with offi-cials. The time it takes to register a newbusiness ranges from 2 days in Australia tomore than 200 days in Haiti.14

RisksBecause investment decisions are forwardlooking, firms’ judgments about the futureare critical. Many risks for firms, includinguncertain responses by customers and com-petitors, are a normal part of investment,and firms should bear them. But govern-ments have an important role to play inmaintaining a stable and secure environ-ment, including by protecting propertyrights. Policy uncertainty, macroeconomicinstability, and arbitrary regulation can alsocloud opportunities and chill incentives toinvest. Indeed, policy-related risks are themain concern of firms in developing coun-tries (box 2).

Barriers to competitionFirms prefer to face less competition, notmore. But barriers to competition that ben-efit some firms deny opportunities andraise costs for other firms and for con-sumers. They can also dull the incentives forprotected firms to innovate and increasetheir productivity. High costs and risks canact as barriers to entry. Governments alsoinfluence barriers more directly throughtheir regulation of market entry and exitand their response to anticompetitivebehavior by firms. Competitive pressure isreported to be significant by 90 percent offirms in Poland but only 40 percent of firmsin Georgia.15

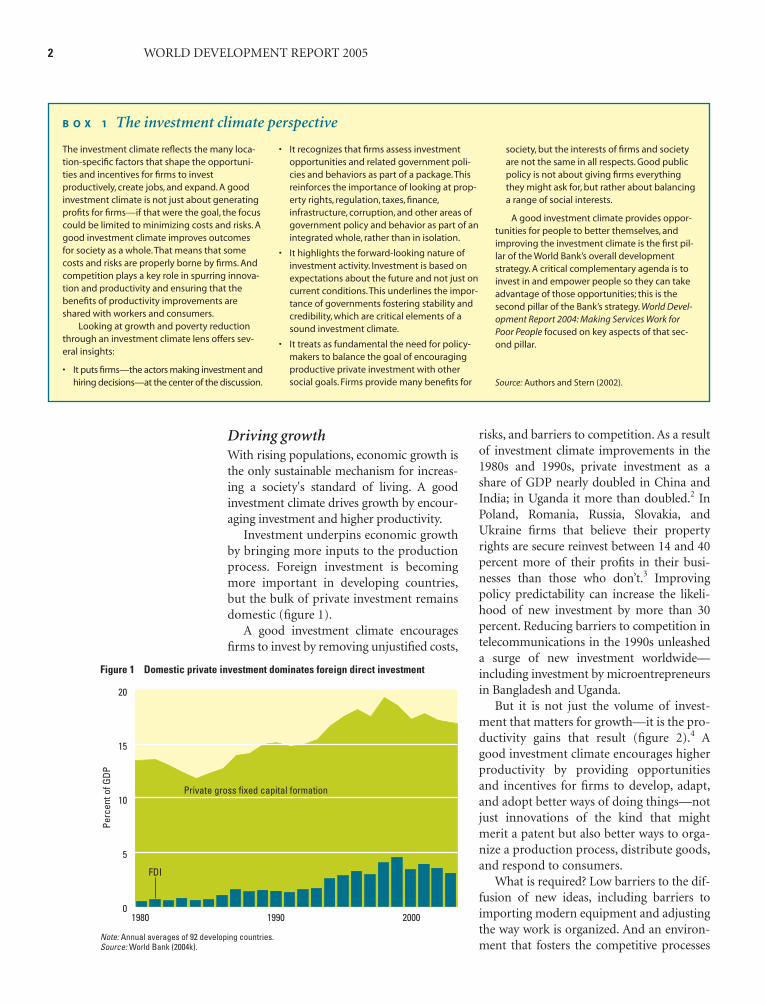

Variations within countries and across firmsEarly efforts to assess investment climatesfocused on developing a single indicator foreach country. But investment climates varynot only across countries but also withincountries because of differences in the waynational policies are administered and inthe policies and behaviors of subnationalgovernments. Even within a single location,the same conditions can affect firms differ-ently depending on the activity they areengaged in and their size, often hitting smalland informal firms the hardest (figure 8).

Figure 7 Costs vary widely in level and composition

Note: See figure 1.2 notes for methodology used.Source: World Bank Investment Climate Surveys. Countries chosen to illustrate range.

TanzaniaAlgeriaBrazilChinaPoland0

5

10

15

Cost

as

perc

ent o

f sal

es 20

25

30Contract enforcement difficultiesRegulationBribesCrimeUnreliable infrastructure

Early results of the World Bank’s program ofInvestment Climate Surveys cover morethan 26,000 firms in 53 countries.While pri-ority constraints can vary widely across and

even within countries, looking at the overallresults highlights the importance of policy-related risks, including policy uncertaintyand macroeconomic stability.

B O X 2 How do firms in developing countries rate variousinvestment climate constraints?

0 20 40 60Percent of firms reporting

80 100

TelecommunicationsAccess to landTransportation

Labor regulationsElectricity

Courts and legal systemSkills

Regulations & tax administrationCrime

Cost & access to financeCorruption

Tax rateMacro instability

Policy uncertainty

Severe obstacleMajor obstacleModerate obstacleMinor obstacle

Note: Firms were asked to rank the list of issues as to whether they were an obstacle to the growth and oper-ation of their business on a 5 point scale, from “no obstacle” to “severe obstacle.” Additional information onthe indicators is available at the back of the book, table A1.Source: World Bank Investment Climate Surveys.

02_WDR_Overview.qxd 8/24/04 11:42 AM Page 5

Progress requires more thanchanges in formal policiesMany investment climate improvementsrequire changes to laws and policies. Butmore is required. Over 90 percent of firms indeveloping countries report gaps betweenformal policies and what happens in prac-tice. And the content as well as the imple-mentation of policies are vulnerable to adeeper set of policy failures. At the heart ofthe problem lies a basic tension: Societiesbenefit greatly from the activities of firms,but the preferences of firms don’t fully matchthose of society. This tension is most evidentin taxation and regulation. Most firms com-plain about taxes, but taxes finance publicservices that benefit the investment climateand other social goals. Many firms wouldalso prefer to comply with fewer regulations,but sound regulation addresses market fail-ures and can therefore improve the invest-ment climate and protect other social inter-ests. Similar tensions can occur across mostareas of investment climate policymaking.

Creating a good investment climaterequires governments to balance these inter-ests. Complicating this task are the differ-ences in preferences and priorities betweenfirms. Firms have common perspectives onmany issues, but their views can diverge onothers—whether on market restrictions, the

structure of taxation, or the priority given toinfrastructure improvements in differentlocations. There can also be differences inpolicy preferences within firms, betweenowners and managers on matters of corpo-rate governance, or between owners andworkers on labor market policies. All gov-ernments must arbitrate those differences inan environment where firms, officials, andother stakeholders seek to tilt the outcometo their advantage.

Four resulting challengesResponding to this tension requires govern-ments to navigate four interrelated challengesthat cut across all areas of investment climatepolicy. The way governments respond tothose challenges has a big impact on invest-ment climates and thus on growth andpoverty. And each involves going beyondchanges in formal policies to confront deepersources of policy failure.

Restraining rent-seeking. Investment cli-mate policies are an enticing target for rent-seeking by firms, officials, and other groups.Corruption can increase the costs of doingbusiness—and when it extends to higherechelons of government, it can lead to deepdistortions in policies. Surveys show that themajority of firms in developing countriesexpect to pay bribes when dealing with offi-cials, but with big variations across coun-tries.16 Capture and patron-clientelism(reflecting unequal information and influ-ence in policymaking) can also create largedistortions, tilting policies in favor of somegroups at the expense of others. Eliminatingunjustified interventions in the economy,curbing discretion, and improving theaccountability of governments, particularlythrough greater transparency, help torestrain rent-seeking.

Establishing credibility. The confidence firmshave in the future—including the credibilityof government policies—determineswhether and how they invest. Policies thatlack credibility will fail to elicit the intendedinvestment response. Policy credibility canbe undermined by many things, includingthe temptations governments face to com-promise sound long-term policies to meetshorter-term or narrower goals (such as

6 WORLD DEVELOPMENT REPORT 2005

Figure 8 Small and informal firms are often hit hardestby investment climate constraints

Note: Based on 10 countries for which formal and informal surveyswere conducted, controlling for industry, country, ownership, andfirm age.Source: World Bank Investment Climate Surveys and WDR Surveysof Micro and Informal Firms.

50

25

Perc

enta

ge o

f firm

s

0

75

Have a loanfrom aformal

financialinstitution

Confidentthat courtswill uphold

propertyrights

Believeregulations

will beinterpretedconsistently

Large

MediumSmall

Informal

02_WDR_Overview.qxd 8/24/04 11:43 AM Page 6

extracting rents for policymakers or curryingfavor with some voters). Mechanisms thatallow governments to commit to sound poli-cies, discipline, and persistence all play a role.

Fostering public trust and legitimacy. Goodinvestment climates are nurtured by broadpublic support: a consensus in favor ofbuilding a more productive society can facil-itate policy improvements regardless of thepolitical party or group in office. Absence ofsuch support can make policy reform moredifficult and undermine the sustainability(and hence the credibility) of reforms. Openand participatory policymaking and effortsto ensure that the benefits of a better invest-ment climate extend widely in society canhelp to build that support.

Ensuring policy responses fit local condi-tions. To be effective, policy interventionsneed to take into account sources of poten-tial government failure and differences inlocal conditions. Failure to do so can lead topoor or even perverse results. Approachesthat demand enforcement capacity beyondthat available will not only fail to meet theirintended objective but also contribute toinformality and corruption and underminecredibility. Approaches that involve highlevels of discretion can expose firms to con-siderable uncertainty and risk when effec-tive safeguards against the misuse of thatdiscretion are not yet developed. Whileapproaches in today’s developed countriescan provide a valuable source of inspira-tion, care needs to be taken to adaptapproaches to local conditions. In somecases this may involve the choice of simplerrules with less discretion and additionalmeasures to restrain arbitrary behavior.

A process, not an eventGovernment policies and behaviors shapingthe investment climate cover a wide field,from contract enforcement and regulationto the provision of infrastructure and labormarket policy. Policies and behaviors in eacharea can influence the opportunities andincentives for firms. And the policy areasoften interact, with progress in one area pos-sibly influenced by progress in others. Thisimplies a broad agenda for government.

Overview 7

China, India, and Uganda illustrate somesimple lessons about strategies for makinginvestment climate improvements.

China and India have both grownimpressively in recent years, greatly reduc-ing poverty. China’s growth is officiallyreported at an average of 8 percent a yearfor the past 20 years, and the share of itspopulation living on less than $1 a day fellfrom 64 percent in 1981 to less than 17 per-cent in 2001. India’s growth has increasedfrom an average of 2.9 percent a year in the1970s to 6.7 percent by the mid-1990s, andthe share of its population living on lessthan $1 a day fell from 54 percent in 1980 to35 percent in 2000.

Yet neither country has an ideal invest-ment climate. China only recently gave con-stitutional recognition to private property,and its banking sector is dragged down bynonperforming loans. Problems in India’spower sector are legendary. Both countriesunleashed growth and reduced povertythrough what appeared to be fairly modestinitial reforms. China began with a rudimen-tary system of property rights that creatednew incentives for a substantial part of itseconomy. India began with early efforts toreduce trade barriers and other distortionsthat covered a significant part of its economy.

In both cases the reforms addressed impor-tant constraints, and were implemented inways that gave firms confidence to invest.And the initial reforms have been followed byongoing improvements that addressed con-straints that were less binding initially, andalso reinforced confidence in the future pathof government policy.

Such strategies are not limited to largecountries. Uganda launched its program ofinvestment climate improvements in theearly 1990s, after a period of civil conflict.Reforms covering many areas of the invest-ment climate provided the basis for grow-ing its economy by an average of more than4 percent per year during 1993—2002 (oreight times the average in Sub-SaharanAfrica) and reducing the share of its popula-tion living below the poverty line from 56percent in 1992 to 35 percent in 2000.Thepersistence of the government’s reformefforts enhanced its credibility, giving firmsthe confidence to invest.

Source: China: Chen and Wang (2001) Qian(2003), and Young (2000); India: Aghion andothers (2003), Ahluwalia (2002), De Long(2003), Rodrik and Subramanian (2004), Varsh-ney (1998), and Panagariya (2003); Uganda:Holmgren and others (2001) and World Bank(2001d).

B O X 3 Tackling a broad agenda—lessons from China,India, and Uganda

But no country has a perfect investmentclimate, and perfection on even one policydimension is not necessary for significantgrowth and poverty reduction. Experienceshows that progress can be made by address-ing important constraints in a way that givesfirms confidence to invest, and by sustaininga process of ongoing improvements (box 3).

Early rounds of economic reform weresometimes seen as one-off events. But invest-ment climate improvements involve an ongo-ing process of policy adjustment and finetuning across a wide domain. This is as truein today’s developed countries as it is indeveloping countries. Policies need regularreview to reflect changes in the conduct ofbusiness and lessons from ongoing experi-ence. Michael Porter has suggested thatreforms in this area are a marathon, not asprint,17 but even that assessment mayunderstate the task. International experienceprovides insights about the essential elementsof reform processes in this area: setting prior-

02_WDR_Overview.qxd 8/24/04 11:43 AM Page 7

ities, managing individual reforms, maintain-ing momentum, and strengthening govern-ment capabilities.

Setting prioritiesThe goal is to identify important con-straints that face firms. There are no stan-dard formulas. Instead, it requires an assess-ment in each case of current conditions, thepotential benefits from improvements, linkswith national or regional goals, and imple-mentation constraints.

Current conditions. The most important con-straints can differ widely across countries,even within a single region (figure 9). Gov-ernments can identify them by surveying andconsulting with firms, but recognizing thatexisting firms will not always reflect the per-spectives of future entrants. New sources ofdata also allow the benchmarking of currentpolicy performance against internationalcomparators in a growing number of areas—highlighting the scope for improvement.

Potential benefits. When the goal is to acceler-ate growth, an improvement that affects alarge part of the economy will usually have abigger impact than reforms that affect asmaller part. Progress in achieving a reason-able level of political and macroeconomic sta-bility is thus fundamental; without it reformsin other areas will gain little traction. Enhanc-ing policy credibility can also leverage the

investment response to reforms in any partic-ular policy area. A key consideration will bethe impact of improvements on opportunitiesfor poor people, including in their capacitiesas employees, entrepreneurs, and consumers.

Governments also need to consider ben-efits that may spill over beyond the firmsand activities affected most directly. Thesemay include spillovers to other firms (forexample, from foreign direct investment tolocal firms), to other policy areas (for exam-ple, from rights to land to access to finance),or to broader social goals (for example,infrastructure improvements benefiting thebroader community). There can also bespillovers to government capabilities, credi-bility, or constituency building.

Links with national or regional goals. Invest-ment climate improvements can affect firmsand activities differently. Because of this, pri-ority-setting will often be influenced by theweight governments place on a subset of thegoals a good investment climate can deliver.These often include integrating the informalor rural economies, unleashing the growthpotential of smaller firms, taking advantageof international openness, or enabling firmsto climb the technology ladder.

Implementation constraints. At any point therange of potential policy improvements willusually be constrained by administrative andpolitical feasibility. Well-designed strategiesaddress these constraints through effectivemanagement of reforms and ongoingstrengthening of government capabilities.

Managing individual reformsThere is often resistance to investment cli-mate reforms from those who benefit fromthe status quo. This resistance may comefrom firms or other interest groups benefit-ing from market distortions or other specialprivileges; officials benefiting from bribesor other perquisites of office; or even thewider community when the implications ofreform are not certain. Experience showsthat progress is possible when committedgovernments communicate to build publicsupport, engage stakeholders construc-tively, and (when appropriate) providesome form of compensation to those disad-

8 WORLD DEVELOPMENT REPORT 2005

Figure 9 Constraints reported by firms—comparingBulgaria, Georgia, and Ukraine

Note: Indices based on surveys of formal sector firms. Values arenormalized by regional maxima and minima for each indicator.Resulting indicators range from 0 (best) to 1 (worst). Countries cho-sen to highlight potential differences. See figure 3.1 notes for moredetails.Source: World Bank Investment Climate Surveys and BEEPS II.

Finance

1

0.5

Taxation

Regulation

Security & stability

Labor

Infrastructure

Ukraine

Georgia

Bulgaria

02_WDR_Overview.qxd 8/24/04 11:43 AM Page 8

Overview 9

vantaged by change. Special efforts to helpvulnerable groups cope with change are alsoimportant, particularly when economywidesafety nets are not yet in place.

Maintaining momentumMany countries are creating specialist insti-tutions to help with specific tasks and tosustain progress even through changes ingovernment. These institutions can per-form one or a combination of several roles:consultation with stakeholders, policy coor-dination, and the more systematic review ofexisting investment climate constraints.Latvia, Senegal, Turkey, and Vietnam illus-trate possible approaches. Governments arealso creating mechanisms to review newpolicy and regulatory proposals more sys-tematically so that they do not introduceunwarranted distortions.

Strengthening governmentcapabilitiesStrengthening capabilities in regulation isoften a high priority. Traditional models forbuilding capacity are being complementedby approaches that facilitate peer-to-peerlearning. Local capacity can also be aug-mented by contracting out some specialistfunctions—a common strategy even indeveloped countries. Governments need toimprove their ability to monitor the perfor-mance of their private sectors so that theycan identify trends and emerging issues andevaluate the impact of their policies.

Focus on delivering the basicsIndustrial development is usually a processof discovery, making it difficult to predictwhat a country or region will be good atproducing. This underscores the impor-tance of creating a good investment climatefor all firms in the economy and so focusingon improving the “basics.” Internationalexperience highlights promising approachesin each of the four core areas of a soundinvestment climate: stability and security,regulation and taxation, finance and infra-structure, and workers and labor markets.

Stability and securityThe outbreak of war or other widespreadviolence spells the end of almost all produc-tive investment, and a reasonable level of

political and macroeconomic stability is athreshold requirement for other policyimprovements to gain much traction. Unsta-ble or insecure environments have their mosttangible affect on investment through theirimpact on property rights, which link effortwith reward. The better protected theserights from government or third parties, thestronger the link between effort and reward,and thus the greater the incentives to opennew businesses, to invest more in existingones, and simply to work harder. Studies inmany countries show that the more securethe rights, the faster the growth. Improvingthe security of property rights requiresaction in four main areas: verifying rights toland and other property, facilitating contractenforcement, reducing crime, and ending theuncompensated expropriation of property.

Verifying rights to land and other property.Providing more secure rights to land andother property encourages investment andcan ease access to finance. Experience inPeru, Thailand, and many other countrieshighlights the benefits of clarifying owner-ship of land and maintaining an effectiveregistration system. Registries for equip-ment and other forms of moveable prop-erty also play an important role.

Facilitating contract enforcement. In manydeveloping countries, firms lack confidencein the courts to uphold their property rights(figure 10). Improving courts is thus a high

Figure 10 Firms in many developing countries lackconfidence in the courts to uphold their property rights

0 20 40 60 80 100

Malaysia

Algeria

Zambia

Brazil

Czech Rep.

Kenya

Kyrgyzstan

Guatemala

Moldova

Bangladesh

Percent

Source: Investment Climate Surveys. Countries chosen to illustrate range.

02_WDR_Overview.qxd 8/24/04 11:43 AM Page 9

priority. Facilitating the free flow of reputa-tion information and removing unnecessaryimpediments to the use of alternative dis-pute resolution mechanisms can also help.

Reducing crime. Crime imposes large costs onsocieties—around a quarter of GDP in somecountries in Latin America.18 Surveys showthat crime is also a serious constraint formany firms in all regions. Promising strategiesinvolve efforts to prevent and deter crime, aswell as to improve enforcement. Communitypolicing strategies along the lines of thoseapplied in New York City are being pursuedby more countries around the world.

Ending the uncompensated expropriation ofproperty. All governments reserve the right toexpropriate private property in some circum-stances. Reducing concerns about the arbi-trary exercise of this power requires crediblerestraints on expropriation without prompt,adequate, and effective compensation.

Regulation and taxationThe way governments regulate and tax firmsand transactions, domestically and at the bor-der, plays a big role in shaping the investmentclimate. Sound regulation addresses marketfailures that inhibit productive investmentand reconciles the interests of firms withwider social goals. Sound taxation generatesthe revenues to finance the delivery of publicservices that improve the investment climateand meet other social objectives. The chal-lenge all governments struggle with is how tomeet these objectives without underminingthe opportunities and incentives for firms toinvest productively, create jobs, and expand.While there can be tensions between firms’preferences and social goals in this area, thereis huge scope for improving approaches inmost developing countries without compro-mising broader social interests.

Improving domestic regulation. Too often,governments pursue regulatory approachesthat fail to achieve the intended social objec-tives because of widespread informality, yetharm the investment climate by imposingunnecessary costs and delays, inviting cor-ruption, increasing uncertainty and risk, andcreating unjustified barriers to competition.

The key is to strike a better balance betweenmarket failures and government failures,including by ensuring that approaches areadapted to local conditions and by enhanc-ing transparency. Successful reforms removeunjustified burdens and streamline proce-dures. They reduce regulatory uncertaintyand risk by curbing discretion and expand-ing consultation. And they remove unjusti-fied barriers to competition by reducing reg-ulatory barriers to entry and exit and bytackling anticompetitive behavior by firms.

Improving domestic taxation. Tax rates indeveloping countries are similar to those indeveloped countries. But a high level ofinformality, coupled with poor administra-tion and corruption, reduces revenue collec-tion, places a disproportionate burden onthose who do comply, and distorts competi-tion. Keeping the size of government incheck and spending public money efficientlyhelp ease the pressure on revenue collection.Beyond this, broadening the tax base andsimplifying tax structures can help. Increas-ing the autonomy of tax agencies has alsoimproved performance in Peru and manyother countries.

Improving regulation and taxation at theborder. Most countries have reduced barri-ers to international trade and investment inrecent years, but many barriers remain.Improving customs administrations canalso offer big benefits, with successfulapproaches exploiting information tech-nologies to reduce delays and corruption, asin Ghana, Morocco, and Singapore.19

Finance and infrastructureFinancial markets, when functioning well,connect firms to lenders and investors will-ing to fund their ventures and share some ofthe risks. Good infrastructure connectsfirms to their customers and suppliers andhelps them take advantage of modern pro-duction techniques. Conversely, inadequa-cies in finance and infrastructure create bar-riers to opportunities and increase costs andrisks for microenterprises as well as multi-nationals. By impeding new entry into mar-kets, inadequacies also limit the competitivediscipline facing incumbent firms, dulling

10 WORLD DEVELOPMENT REPORT 2005

02_WDR_Overview.qxd 8/24/04 11:43 AM Page 10

their incentives to innovate and improvetheir productivity. Such inadequacies arelarge in developing countries (figure 11).

Improving finance. The underlying chal-lenge with finance flows from informationproblems, which are often exacerbated byweak protection of property rights. Govern-ment intervention through state ownership,barriers to competition, directed or subsi-dized credit, and similar approaches cancreate deep distortions and retard financialmarket development. Better approachesrecognize that financial markets are notonly part of the investment climate forfirms, but are also profoundly shaped by theinvestment climate facing providers offinancial services. More governments arethus reducing barriers to competition(including paving the way for nonbankfinancial intermediaries and commercialmicrofinance), strengthening creditor andshareholder rights, supporting the estab-lishment of credit bureaus and other mech-anisms to address information problems,and improving bank regulation.

Improving infrastructure. The underlyingchallenge with infrastructure flows frommarket power associated with economies ofscale. But responses focusing on provisionby public sector monopolies have producedpoor results in many developing countries.Recognizing this, governments are nowfocusing on creating a better investment cli-mate for providers of infrastructure ser-vices. Competition, improved regulation,and private participation have transformedtelecommunications and are playing a big-ger role in electricity supply and ports. Forroads, promising strategies include con-tracting-out services and improving fund-ing mechanisms. Governments are alsoworking to improve management of publicresources—to get more for their moneywhen they finance or subsidize infrastruc-ture services.

Workers and labor marketsGovernment intervention in labor marketsshould help connect people to decent jobs.Improving policy performance requiresprogress on three fronts: fostering a skilled

workforce; crafting market interventions tobenefit all workers; and helping workerscope with change.

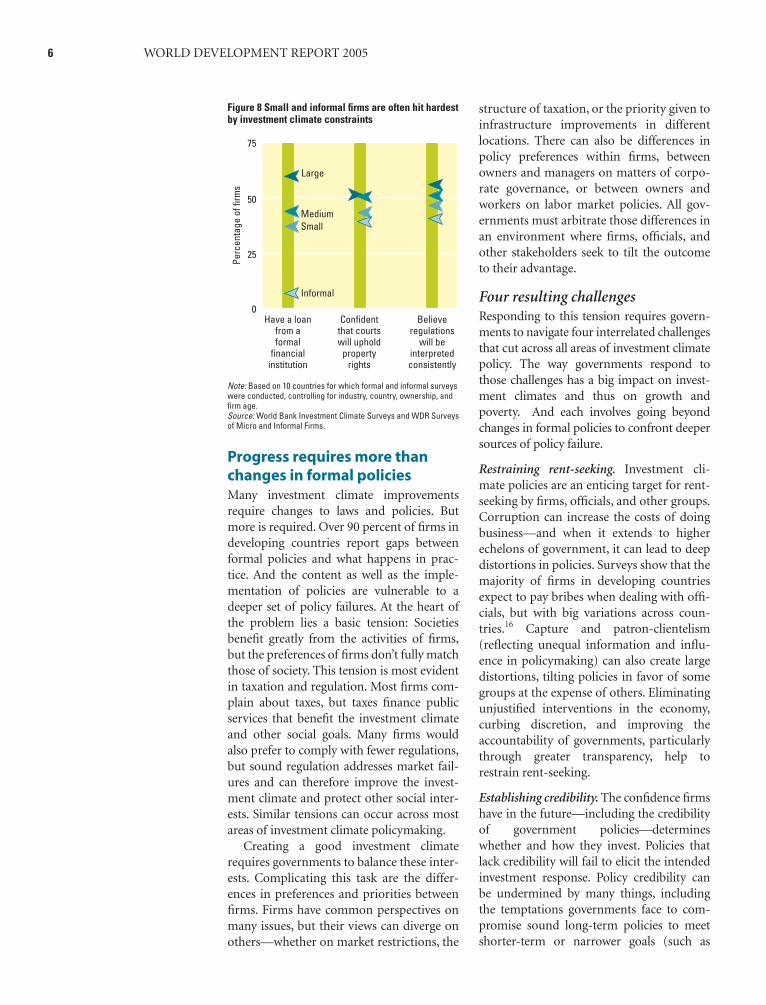

Fostering a skilled workforce. Improving theinvestment climate goes hand in hand withenhancing human capital. A skilled work-force is essential for firms to adopt new andmore productive technologies, and a betterinvestment climate raises the returns toinvesting in education. Government sup-port for education and training affects theprospects for individuals and the ability offirms to pursue new opportunities. Manyfirms in developing countries rate inade-quate skills of workers as a serious obstacleto their operations (figure 12). Govern-ments need to take the lead in making edu-cation more inclusive and relevant to theskill needs of firms, strengthening qualityassurance mechanisms, and creating a soundinvestment climate for providers of educa-tion and training services.

Crafting market interventions to benefit allworkers. Regulation of labor markets isusually intended to help workers. But ill-considered approaches discourage firmsfrom creating more jobs and contribute to aswelling of the informal workforce thatlacks statutory protection. When this is thecase, some workers may benefit, but the

Overview 11

Figure 11 The inadequacies of finance and infrastructure are severe for manydeveloping countries

0 10 20 30 40 50 60 70

FinanceInfrastructure

South Asia

Sub-Saharan Africa

Latin America & the Caribbean

Europe & Central Asia

East Asia & Pacific

Middle East & North Africa

Percent of firmsNote: Figure shows the share of firms that report access to finance, and any of electricity, telecommu-nications, or transportation, as “major” or “severe” obstacles to their business.Source: World Bank Investment Climate Surveys.

02_WDR_Overview.qxd 8/24/04 11:43 AM Page 11