97-93-Banking Sector in India

82

UNIVERSITY OF MUMBAI PROJECT ON BANKING SECTOR IN INDIA SUBMITTED BY GURURAJ DEVADIGA PROJECT GUIDE PROF. LAILA DIAS SEMESTER V BACHELOR OF COMMERCE (BANKING AND INSURANCE) KHAR EDUCATION SOCIETY’S COLLEGE OFCOMMERCE & ECONOMICS KHAR (W), 2010-2011 1

-

Upload

gururaj-devadiga -

Category

Documents

-

view

223 -

download

0

Transcript of 97-93-Banking Sector in India

8/8/2019 97-93-Banking Sector in India

http://slidepdf.com/reader/full/97-93-banking-sector-in-india 1/82

UNIVERSITY OF MUMBAI

PROJECT ON

BANKING SECTOR IN INDIA

SUBMITTED BY

GURURAJ DEVADIGA

PROJECT GUIDE

PROF. LAILA DIAS

SEMESTER V

BACHELOR OF COMMERCE (BANKING AND INSURANCE)

KHAR EDUCATION SOCIETY’S

COLLEGE OFCOMMERCE & ECONOMICS

KHAR (W),

2010-2011

1

8/8/2019 97-93-Banking Sector in India

http://slidepdf.com/reader/full/97-93-banking-sector-in-india 2/82

DECLARATION

I, Mr. GURURAJ .R. DEVADIGA, student of TYBBI at

KHAR EDUCATION SOCIETY’S COLLEGE OF COMMERCE AND

ECONOMICS hereby declare that I have completed this

project on BANKING SECTOR IN INDIA in the academic year

2010-2011, in partial fulfillment of the degree for

SEMESTER V. The information submitted in this project is

true and original to the best of my knowledge.

____________________

Gururaj R .Devadiga

2

8/8/2019 97-93-Banking Sector in India

http://slidepdf.com/reader/full/97-93-banking-sector-in-india 3/82

CERTIFICATE

I, Prof. LAILA DIAS hereby certify that this project on

‘BANKING SECTOR IN INDIA’ has been completed by Mr.

GURURAJ .R. DEVADIGA, T.Y.B.B.I student of Khar

Education Society’s College of Commerce and Economics in

the academic year 2010-2011. The information submitted

in this project is true and original to the best of my

knowledge.

________________ ___________________

__________

Signature of Project Guide Signature of Co-ordinator

Signature of Principal

3

8/8/2019 97-93-Banking Sector in India

http://slidepdf.com/reader/full/97-93-banking-sector-in-india 4/82

ACKNOWLEDGEMENT

It gives me great pleasure while submitting this project on the topic ‘Banking

Sector in India’. This project provides an overview of the banking sector which is

the backbone of India’s growing economy.

I would like to begin by thanking my Project Guide, PROF. Laila Dias for helping

me throughout the project and for motivating me to give my best effort. It was a

pleasure working with such knowledgeable and helpful guide.

I would also express my gratitude to our principal Dr. Nandini Deshmukh who has

always kindled the quest for knowledge and created an atmosphere of excellence in

all round development.

Last but not the least I thank the Almighty, my family and friends for their support

and guidance in all my Endeavour’s.

4

8/8/2019 97-93-Banking Sector in India

http://slidepdf.com/reader/full/97-93-banking-sector-in-india 5/82

EXECUTIVE SUMMARY

Usually all persons want money for personal and commercial purposes. Banks are

the oldest lending institutions in Indian scenario. They are providing all facilities to

all citizens for their own purposes by their terms. To survive in this modern market

every bank implements so many new innovative ideas, strategies, and advanced

technologies. For that they give each and every minute detail about their institution

and projects to Public.

They are providing ample facilities to satisfy their customers i.e. Net Banking,

Mobile Banking, Door to Door facility, Instant facility, Investment facility, Demat

facility, Credit Card facility, Loans and Advances, Account facility etc. And such

banks get success to create their own image in public and corporate world. These

banks always accept innovative notions in Indian banking scenario like Credit

Cards, ATM machines, Risk Management etc.

The last decade has seen many positive developments in the Indian banking

sector. The policy makers, which comprise the Reserve Bank of India (RBI),

Ministry of Finance and related government and financial sector regulatory

entities, have made several notable efforts to improve regulation in the sector. The

sector now compares favorably with banking sectors in the region on metrics like

growth, profitability and non-performing assets (NPAs). A few banks have

established an outstanding track record of innovation, growth and value creation.

This is reflected in their market valuation. However, improved regulations,

5

8/8/2019 97-93-Banking Sector in India

http://slidepdf.com/reader/full/97-93-banking-sector-in-india 6/82

innovation, growth and value creation in the sector remain limited to a small part

of it.

The cost of banking intermediation in India is higher and bank penetration is far

lower than in other markets. India’s banking industry must strengthen itself

significantly if it has to support the modern and vibrant economy which India

aspires to be. While the responsibility for this change lies mainly with bank

managements, an enabling policy and regulatory framework will also be critical to

their success.

INDEX

SR NO. TOPIC PG NO.

1. AN INTRODUCTION TO BANKING SECTOR IN

INDIA

8

2. MEANING OF BANKS 12

6

8/8/2019 97-93-Banking Sector in India

http://slidepdf.com/reader/full/97-93-banking-sector-in-india 7/82

3. HISTORY OF BANKS 16

4. NATIONALIZATION OF BANKS 23

5. DISTINCTION BETWEEN BANK AND

MONEYLENDERS

25

6. CURRENT SCNEARIO 27

7. TYPES OF BANK 32

8. SWOT ANALYSIS 46

9. PEST ANALYSIS 51

10. RECENT BANKING DEVELOPMENT IN INDIA 55

11. 7 P’S OF BANKING 64

12. CONCLUSION 79

13. BIBLOGRAPHY 81

7

8/8/2019 97-93-Banking Sector in India

http://slidepdf.com/reader/full/97-93-banking-sector-in-india 8/82

AN INTRODUCTION TO THE BANKING SECTOR IN INDIA

Banks are the most significant players in the Indian financial market. They

are the biggest purveyors of credit, and they also attract most of the savings from

the population. Dominated by public sector, the banking industry has so far acted

as an efficient partner in the growth and the development of the country. Driven by

the socialist ideologies and the welfare state concept, public sector banks have long

been the supporters of agriculture and other priority sectors. They act as crucial

channels of the government in its efforts to ensure equitable economic

development.

The Indian banking can be broadly categorized into nationalized

(government owned), private banks and specialized banking institutions. The

Reserve Bank of India acts a centralized body monitoring any discrepancies and

shortcoming in the system. Since the nationalization of banks in 1969, the public

sector banks or the nationalized banks have acquired a place of prominence and

has since then seen tremendous progress. The need to become highly customer

focused has forced the slow-moving public sector banks to adopt a fast track

approach. The unleashing of products and services through the net has galvanized

players at all levels of the banking and financial institutions market grid to look

anew at their existing portfolio offering. Conservative banking practices allowed

8

8/8/2019 97-93-Banking Sector in India

http://slidepdf.com/reader/full/97-93-banking-sector-in-india 9/82

Indian banks to be insulated partially from the Asian currency crisis. Indian banks

are now quoting al higher valuation when compared to banks in other Asian

countries (viz. Hong Kong, Singapore, Philippines etc.) that have major problems

linked to huge Non Performing Assets (NPAs) and payment defaults. Co-

operative banks are nimble footed in approach and armed with efficient branch

networks focus primarily on the ‘high revenue’ niche retail segments.

The Indian banking has finally worked up to the competitive dynamics of

the ‘new’ Indian market and is addressing the relevant issues to take on the

multifarious challenges of globalization. Banks that employ IT solutions are

perceived to be ‘futuristic’ and proactive players capable of meeting the

multifarious requirements of the large customer’s base. Private Banks have been

fast on the uptake and are reorienting their strategies using the internet as a

medium The Internet has emerged as the new and challenging frontier of

marketing with the conventional physical world tenets being just as applicable

like in any other marketing medium.

The Indian banking has come from a long way from being a sleepy business

institution to a highly proactive and dynamic entity. This transformation has been

largely brought about by the large dose of liberalization and economic reforms

that allowed banks to explore new business opportunities rather than generating

revenues from conventional streams (i.e. borrowing and lending). The banking in

India is highly fragmented with 30 banking units contributing to almost 50% of

deposits and 60% of advances. Indian nationalized banks (banks owned by the

government) continue to be the major lenders in the economy due to their sheer

size and penetrative networks which assures them high deposit mobilization. The

9

8/8/2019 97-93-Banking Sector in India

http://slidepdf.com/reader/full/97-93-banking-sector-in-india 10/82

Indian banking can be broadly categorized into nationalized, private banks and

specialized banking institutions.

The Reserve Bank of India acts as a centralized body monitoring any

discrepancies and shortcoming in the system. It is the foremost monitoring body

in the Indian financial sector. The nationalized banks (i.e. government-owned

banks) continue to dominate the Indian banking arena. Industry estimates

indicate that out of 274 commercial banks operating in India, 223 banks are in the

public sector and 51 are in the private sector. The private sector bank grid also

includes 24 foreign banks that have started their operations here.

The liberalize policy of Government of India permitted entry to private

sector in the banking, the industry has witnessed the entry of nine new generation

private banks. The major differentiating parameter that distinguishes these banks

from all the other banks in the Indian banking is the level of service that is offered

to the customer. Their focus has always centered around the customer –

understanding his needs, preempting him and consequently delighting him with

various configurations of benefits and a wide portfolio of products and services.

These banks have generally been established by promoters of repute or by ‘high

value’ domestic financial institutions.

The popularity of these banks can be gauged by the fact that in a short span

of time, these banks have gained considerable customer confidence and

consequently have shown impressive growth rates. Today, the private banks

corner almost four per cent share of the total share of deposits. Most of the banks

in this category are concentrated in the high-growth urban areas in metros (that

10

8/8/2019 97-93-Banking Sector in India

http://slidepdf.com/reader/full/97-93-banking-sector-in-india 11/82

account for approximately 70% of the total banking business). With efficiency

being the major focus, these banks have leveraged on their strengths and

competencies viz. Management, operational efficiency and flexibility, superior

product positioning and higher employee productivity skills.

The private banks with their focused business and service portfolio have a

reputation of being niche players in the industry. A strategy that has allowed

these banks to concentrate on few reliable high net worth companies and

individuals rather than cater to the mass market. These well-chalked out

integrates strategy plans have allowed most of these banks to deliver superlative

levels of personalized services. With the Reserve Bank of India allowing these

banks to operate 70% of their businesses in urban areas, this statutory

requirement has translated into lower deposit mobilization costs and higher

margins relative to public sector banks.

11

8/8/2019 97-93-Banking Sector in India

http://slidepdf.com/reader/full/97-93-banking-sector-in-india 12/82

Meaning of Bank

People earn money to meet their day-to-day expenses on food, clothing, education

of children, housing, etc. They also need money to meet future expenses on

marriage, higher education of children, house building and other social functions.

These are heavy expenses, which can be met if some money is saved out of the

present income. Saving of money is also necessary for old age and ill health when

it may not be possible for people to work and earn their living.

The necessity of saving money was felt by people even in olden days. They used to

keep money in their homes. With this practice, savings were available for use

whenever needed, but it also involved the risk of loss by theft, robbery and other

accidents. Thus, people were in need of a place where money could be saved safely

and would be available when required. Banks are such places where people can

deposit their savings with the assurance that they will be able to withdraw money

from the deposits whenever required. People who wish to borrow money for

business and other purposes can also get loans from the banks at reasonable rate of

interest.

Banks also render many other useful services – like collection of bills, payment of

foreign bills, Safe-keeping of jewellery and other valuable items, certifying the

credit-worthiness of business, and so on. Banks accept deposits from the general

public as well as from the business community. Anyone who saves money for

future can deposit his savings in a bank. Businessmen have income from sales out

of which they have to make payment for expenses. They can keep their earnings

12

8/8/2019 97-93-Banking Sector in India

http://slidepdf.com/reader/full/97-93-banking-sector-in-india 13/82

from sales safely deposited in banks to meet their expenses from time to time.

Banks give two assurances to the depositors –

a. Safety of deposit, and

b. Withdrawal of deposit, whenever needed

On deposits, banks give interest, which adds to the original amount of deposit. It is

a great incentive to the depositor. It promotes saving habits among the public. On

the basis of deposits banks also grant loans and advances to farmers, traders and

businessmen for productive purposes.

Thereby banks contribute to the economic development of the country and well

being of the people in general. Banks also charge interest on loans. The rate of

interest is generally higher than the rate of interest allowed on deposits. Banks also

charge fees for the various other services, which they render to the business

community and public in general. Interest received on loans and fees charged for

services which exceed the interest allowed on deposits are the main sources of

income for banks from which they meet their administrative expenses.

The activities carried on by banks are called banking activity. ‘Banking’ as an

activity involves acceptance of deposits and lending or investment of money. It

facilitates business activities by providing money and certain services that help in

exchange of goods and services. Therefore, banking is an important auxiliary to

trade. It not only provides money for the production of goods and services but also

facilitates their exchange between the buyer and seller.

We may be aware that there are laws which regulate the banking activities in our

country.

Depositing money in banks and borrowing from banks are legal transactions.

Banks are also under the control of government. Hence they enjoy the trust and

13

8/8/2019 97-93-Banking Sector in India

http://slidepdf.com/reader/full/97-93-banking-sector-in-india 14/82

confidence of people. Also banks depend a great deal on public confidence.

Without public confidence banks cannot survive.

Bank definition:

A financial institution that is licensed to deal with money and its substitutes by

accepting time and demand deposits, making

loans, and investing in securities. The bank

generates profits from the difference in the

interest rates charged and paid.

Bank is a lawful organization, which accepts

deposits that can be withdrawn on demand. It

also lends money to individuals and business

houses that need it.

A bank is a financial intermediary that accepts deposits and channels those

deposits into lending activities, either directly or through capital markets. A bank

connects customers with capital deficits to customers with capital surpluses.

Role of Banking

Banks provide funds for business as well as personal needs of individuals. They

play a significant role in the economy of a nation. Let us know about the role of

banking.

• It encourages savings habit amongst people and thereby makes funds available

for productive use.

14

8/8/2019 97-93-Banking Sector in India

http://slidepdf.com/reader/full/97-93-banking-sector-in-india 15/82

• It acts as an intermediary between people having surplus money and those

requiring money for various business activities.

• It facilitates business transactions through receipts and payments by cheques

instead of currency.

• It provides loans and advances to businessmen for short term and long-term

purposes.

• It also facilitates import export transactions.

• It helps in national development by providing credit to farmers, small-scale

industries and self-employed people as well as to large business houses which lead

to balanced economic development in the country.

• It helps in raising the standard of living of people in general by providing loans

for purchase of consumer durable goods, houses, automobiles, etc.

15

8/8/2019 97-93-Banking Sector in India

http://slidepdf.com/reader/full/97-93-banking-sector-in-india 16/82

History

Banking in India originated in the last decades of the 18th century. The first banks

were The General Bank of India which started in 1786, and the Bank of Hindustan,

both of which are now defunct. The oldest bank in existence in India is the State

Bank of India, which originated in the Bank of Calcutta in June 1806, which

almost immediately became the Bank of Bengal. This was one of the three

presidency banks, the other two being the Bank of Bombay and the Bank of

Madras, all three of which were established under charters from the British East

India Company. For many years the Presidency banks acted as quasi-central banks,as did their successors. The three banks merged in 1921 to form the Imperial Bank

of India, which, upon India's independence, became the State Bank of India.

Indian merchants in Calcutta established the Union Bank in 1839, but it failed in

1848 as a consequence of the economic crisis of 1848-49. The Allahabad Bank ,

established in 1865 and still functioning today, is the oldest Joint Stock bank in

India.(Joint Stock Bank: A company that issues stock and requires shareholders to

be held liable for the company's debt) It was not the first though. That honor

belongs to the Bank of Upper India, which was established in 1863, and which

survived until 1913, when it failed, with some of its assets and liabilities being

transferred to the Alliance Bank of Simla.

When the American Civil War stopped the supply of cotton to Lancashire from the

Confederate States, promoters opened banks to finance trading in Indian cotton.

With large exposure to speculative ventures, most of the banks opened in India

during that period failed. The depositors lost money and lost interest in keeping

deposits with banks. Subsequently, banking in India remained the exclusive

16

8/8/2019 97-93-Banking Sector in India

http://slidepdf.com/reader/full/97-93-banking-sector-in-india 17/82

8/8/2019 97-93-Banking Sector in India

http://slidepdf.com/reader/full/97-93-banking-sector-in-india 18/82

Europeans, concentrated on financing foreign trade. Indian joint stock banks were

generally undercapitalized and lacked the experience and maturity to compete with

the presidency and exchange banks. This segmentation let Lord Curzon to observe,

"In respect of banking it seems we are behind the times. We are like some old

fashioned sailing ship, divided by solid wooden bulkheads into separate and

cumbersome compartments."

The period between 1906 and 1911, saw the establishment of banks inspired by the

Swadeshi movement. The Swadeshi movement inspired local businessmen and

political figures to found banks of and for the Indian community. A number of

banks established then have survived to the present such as Bank of India,

Corporation Bank , Indian Bank , Bank of Baroda, Canara Bank and Central Bank

of India.

The favor of Swadeshi movement lead to establishing of many private banks in

Dakshina Kannada and Udupi district which were unified earlier and known by the

name South Canara ( South Kanara ) district. Four nationalised banks started in

this district and also a leading private sector bank. Hence undivided Dakshina

Kannada district is known as "Cradle of Indian Banking".

During the First World War (1914-1918) through the end of the Second World

War (1939-1945), and two years thereafter until the independence of India were

challenging for Indian banking. The years of the First World War were turbulent,

and it took its toll with banks simply collapsing despite the Indian economy gaining indirect boost due to war-related economic activities. At least 94 banks in

India failed between 1913 and 1918.

Post-independence

18

8/8/2019 97-93-Banking Sector in India

http://slidepdf.com/reader/full/97-93-banking-sector-in-india 19/82

The partition of India in 1947 adversely impacted the economies of Punjab and

West Bengal, paralyzing banking activities for months. India's independence

marked the end of a regime of the Laissez-faire for the Indian banking. The

Government of India initiated measures to play an active role in the economic life

of the nation, and the Industrial Policy Resolution adopted by the government in

1948 envisaged a mixed economy. This resulted into greater involvement of the

state in different segments of the economy including banking and finance. The

major steps to regulate banking included:

• In 1948, the Reserve Bank of India, India's central banking authority, was

nationalized, and it became an institution owned by the Government of

India.

• In 1949, the Banking Regulation Act was enacted which empowered the

Reserve Bank of India (RBI) "to regulate, control, and inspect the banks in

India."

• The Banking Regulation Act also provided that no new bank or branch of an

existing bank could be opened without a license from the RBI, and no two

banks could have common directors.

However, despite these provisions, control and regulations, banks in India except

the State Bank of India, continued to be owned and operated by private persons.

This changed with the nationalization of major banks in India on 19 July 1969.

19

8/8/2019 97-93-Banking Sector in India

http://slidepdf.com/reader/full/97-93-banking-sector-in-india 20/82

Liberalization

In the early 1990s, the then Narsimha Rao government embarked on a policy of

liberalization, licensing a small number of private banks. These came to be knownas New Generation tech-savvy banks, and included Global Trust Bank (the first of

such new generation banks to be set up), which later amalgamated with Oriental

Bank of Commerce, Axis Bank (earlier as UTI Bank ), ICICI Bank and HDFC

Bank . This move, along with the rapid growth in the economy of India, revitalized

the banking sector in India, which has seen rapid growth with strong contribution

from all the three sectors of banks, namely, government banks, private banks and

foreign banks.

The next stage for the Indian banking has been set up with the proposed relaxation

in the norms for Foreign Direct Investment, where all Foreign Investors in banks

may be given voting rights which could exceed the present cap of 10%,at present it

has gone up to 74% with some restrictions.

The new policy shook the Banking sector in India completely. Bankers, till this

time, were used to the 4-6-4 method (Borrow at 4%; Lend at 6%; Go home at 4) of

functioning. The new wave ushered in a modern outlook and tech-savvy methods

of working for traditional banks. All this led to the retail boom in India. People not

just demanded more from their banks but also received more.

Currently (2007), banking in India is generally fairly mature in terms of supply,

product range and reach-even though reach in rural India still remains a challenge

for the private sector and foreign banks. In terms of quality of assets and capital

adequacy, Indian banks are considered to have clean, strong and transparent

balance sheets relative to other banks in comparable economies in its region. The

20

8/8/2019 97-93-Banking Sector in India

http://slidepdf.com/reader/full/97-93-banking-sector-in-india 21/82

Reserve Bank of India is an autonomous body, with minimal pressure from the

government. The stated policy of the Bank on the Indian Rupee is to manage

volatility but without any fixed exchange rate-and this has mostly been true.

With the growth in the Indian economy expected to be strong for quite some time-

especially in its services sector-the demand for banking services, especially retail

banking, mortgages and investment services are expected to be strong. One may

also expect M&As, takeovers, and asset sales.

In March 2006, the Reserve Bank of India allowed Warburg Pincus to increase its

stake in Kotak Mahindra Bank (a private sector bank) to 10%. This is the first timean investor has been allowed to hold more than 5% in a private sector bank since

the RBI announced norms in 2005 that any stake exceeding 5% in the private

sector banks would need to be vetted by them.

In recent years critics have charged that the non-government owned banks are too

aggressive in their loan recovery efforts in connection with housing, vehicle and

personal loans. There are press reports that the banks' loan recovery efforts have

driven defaulting borrowers to suicide

Nationalization

The RBI was nationalized on January 1, 1949 in terms of the Reserve Bank of

India (Transfer to Public Ownership) Act, 1948 (RBI, 2005b).

By the 1960s, the Indian banking industry had become an important tool to

facilitate the development of the Indian economy. At the same time, it had emerged

21

8/8/2019 97-93-Banking Sector in India

http://slidepdf.com/reader/full/97-93-banking-sector-in-india 22/82

as a large employer, and a debate had ensued about the possibility to nationalise

the banking industry. Indira Gandhi, the-then Prime Minister of India expressed the

intention of the GOI in the annual conference of the All India Congress Meeting in

a paper entitled "Stray thoughts on Bank Nationalisation." The paper was received

with positive enthusiasm. Thereafter, her move was swift and sudden, and the GOI

issued an ordinance and nationalised the 14 largest commercial banks with effect

from the midnight of July 19, 1969. Jayaprakash Narayan, a national leader of

India, described the step as a "masterstroke of political sagacity." Within two

weeks of the issue of the ordinance, the Parliament passed the Banking Companies

(Acquisition and Transfer of Undertaking) Bill, and it received the presidential

approval on 9 August 1969.

A second dose of nationalization of 6 more commercial banks followed in 1980.

The stated reason for the nationalization was to give the government more

control of credit delivery. With the second dose of nationalization, the GOI

controlled around 91% of the banking business of India. Later on, in the year

1993, the government merged New Bank of India with Punjab National Bank .

It was the only merger between nationalized banks and resulted in the

reduction of the number of nationalised banks from 20 to 19. After this, until

the 1990s, the nationalised banks grew at a pace of around 4%, closer to the

average growth rate of the Indian economy.

22

8/8/2019 97-93-Banking Sector in India

http://slidepdf.com/reader/full/97-93-banking-sector-in-india 23/82

Nationalization of Banks in India

The nationalization of banks in India took place in 1969 by Mrs. Indira Gandhi the

then prime minister. It nationalised 14 banks then. These banks were mostly owned

by businessmen and even managed by them.

• Central Bank of India

• Bank of Maharashtra

• Dena Bank

• Punjab National Bank

• Syndicate Bank

• Canara Bank

• Indian Bank

• United Bank of India

• UCO Bank

• Bank of India

Before the steps of nationalization of Indian banks, only State Bank of India (SBI)

was nationalised. It took place in July 1955 under the SBI Act of 1955.

Nationalization of Seven State Banks of India (formed subsidiary) took place on

23

8/8/2019 97-93-Banking Sector in India

http://slidepdf.com/reader/full/97-93-banking-sector-in-india 24/82

19th July, 1960.

The State Bank of India is India's largest commercial bank and is ranked one of the

top five banks worldwide. It serves 90 million customers through a network of

9,000 branches and it offers -- either directly or through subsidiaries -- a wide

range of banking services.

The second phase of nationalization of Indian banks took place in the year 1980.

Seven more banks were nationalised with deposits over 200 crores. Till this year,

approximately 80% of the banking segment in India was under Government

ownership.

After the nationalization of banks in India, the branches of the public sector banks

rose to approximately 800% in deposits and advances took a huge jump by

11,000%.

• 1955: Nationalization of State Bank of India.

• 1959: Nationalization of SBI subsidiaries.

• 1969: Nationalization of 14 major banks.

• 1980: Nationalization of seven banks with deposits over 200 corers.

• Indian Overseas Bank

• Bank of Baroda

• Union Bank

• Allahabad Bank

24

8/8/2019 97-93-Banking Sector in India

http://slidepdf.com/reader/full/97-93-banking-sector-in-india 25/82

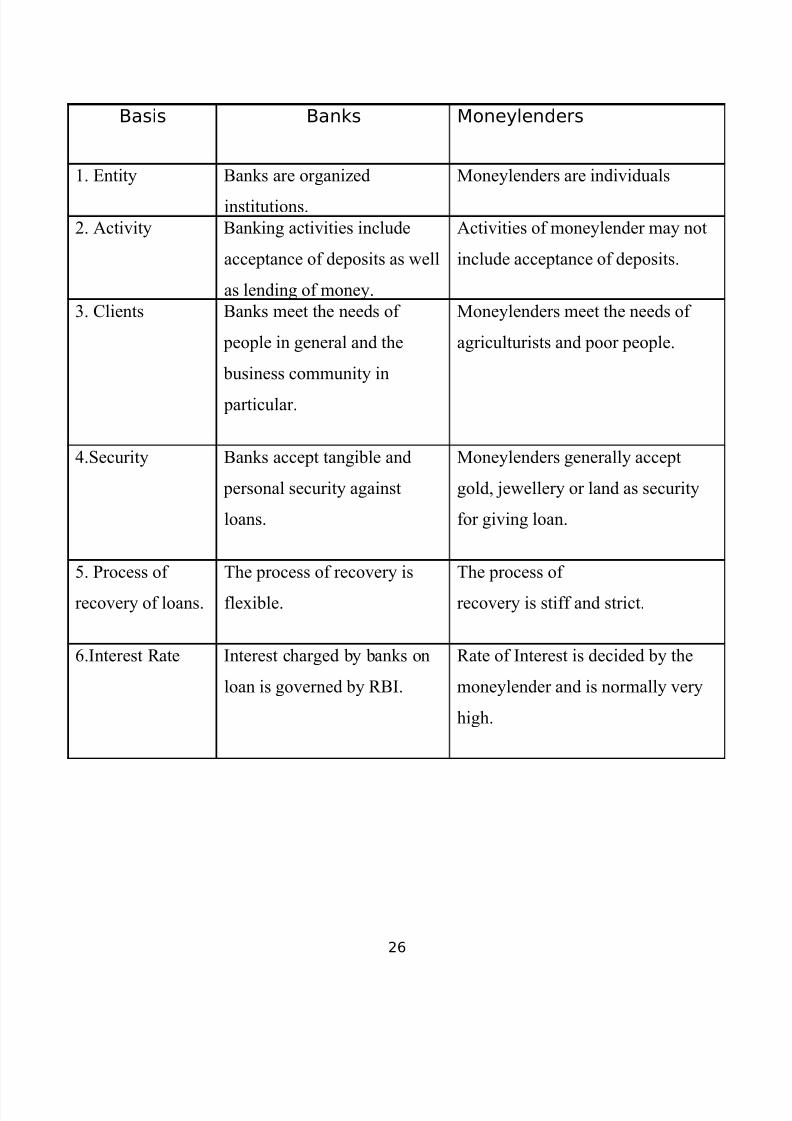

Distinction between banks and moneylenders

You may be thinking that a bank is like a moneylender who provides funds to

borrowers and charges interest on the loan. But it is not so. A bank is quite

different from a moneylender. A bank performs two main functions. Firstly, it

accepts deposits, and on that basis it lends money. The moneylenders, on the other

hand, advance money out of their own private wealth and usually do not accept

deposits from others. The following table shows the distinction between a bank and

moneylender

25

8/8/2019 97-93-Banking Sector in India

http://slidepdf.com/reader/full/97-93-banking-sector-in-india 26/82

26

Basis Banks Moneylenders

1. Entity Banks are organized

institutions.

Moneylenders are individuals

2. Activity Banking activities include

acceptance of deposits as well

as lending of money.

Activities of moneylender may not

include acceptance of deposits.

3. Clients Banks meet the needs of

people in general and the

business community in

particular.

Moneylenders meet the needs of

agriculturists and poor people.

4.Security Banks accept tangible and

personal security against

loans.

Moneylenders generally accept

gold, jewellery or land as security

for giving loan.

5. Process of

recovery of loans.

The process of recovery is

flexible.

The process of

recovery is stiff and strict.

6.Interest Rate Interest charged by banks on

loan is governed by RBI.

Rate of Interest is decided by the

moneylender and is normally very

high.

8/8/2019 97-93-Banking Sector in India

http://slidepdf.com/reader/full/97-93-banking-sector-in-india 27/82

Current scenario

Banks have come a long way since their origin of having started out with the basic

act of lending and borrowing money. The word Bank was derived from the Italian

word “banco”, which means “bench” over which transactions happened during the

earliest days when banking as a concept came into existence. A bank needs an

approval from the government to set up its

business. This approval or license is

applied differently in different countries.

The set of regulations vary according to the

government policies and other norms

established by the government of that

country.

Towards the last few decades of the 18th

century the concept of banking was

introduced in India. The oldest bank in India is the State Bank of India, a PSU that

was initially set up in June 1806 and is currently the largest commercial bank.

Central banking for which the Reserve Bank of India (RBI) is responsible took

over these duties from the then Imperial Bank of India. After India’s independence

in 1947, RBI was nationalized and given a wider scope to exercise its powers and

judgment. A nationalization spree occurred in 1969, when 14 of the largest

commercial banks was provided this status following another nationalization

process of the next six largest banks in 1980.

27

8/8/2019 97-93-Banking Sector in India

http://slidepdf.com/reader/full/97-93-banking-sector-in-india 28/82

According to a recent count, India has 88 scheduled commercial banks (SCBs). Of

this there are 27 public sector banks (with the Government of India holding a

stake), 31 private banks (these do not have government stake; they may be publicly

listed and traded on stock exchanges) and 38 foreign banks. They have a combined

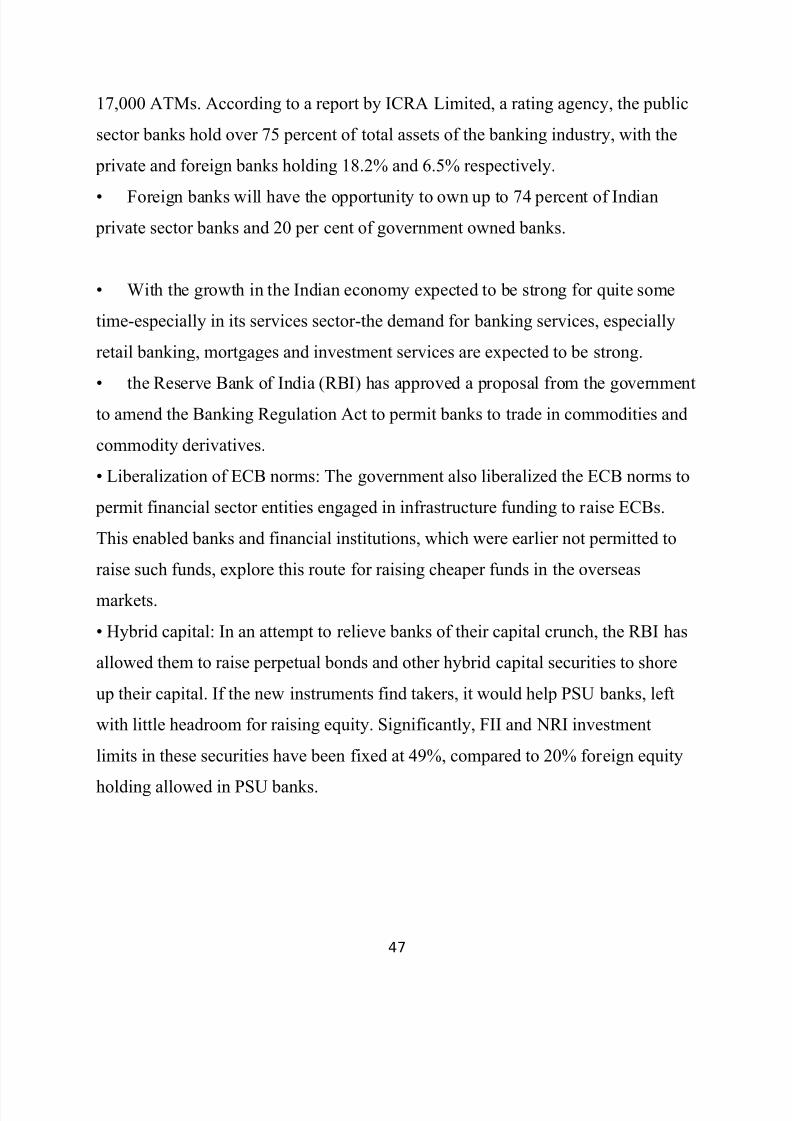

network of over 53,000 branches and 17,000 ATMs.

According to a report by ICRA Limited, a rating agency, the public sector banks

hold over 75 percent of total assets of the banking industry, with the private and

foreign banks holding 18.2% and 6.5% respectively.

Here is a partial list of the most popular banks in the country.

HDFC bank

HDFC - Housing

Development Finance

Corporation

ICICI bank

SBI

Axis bank

Allahabad bank

Bank of Rajasthan

City Union bank

Indusl and bank

Catholic Syrian bank Karnataka bank Limited

Karur Vysya bank

Limited

Kotak Mahindra bank

28

8/8/2019 97-93-Banking Sector in India

http://slidepdf.com/reader/full/97-93-banking-sector-in-india 29/82

8/8/2019 97-93-Banking Sector in India

http://slidepdf.com/reader/full/97-93-banking-sector-in-india 30/82

Bank of Maharashtra

Central Bank of India

Corporation bank

Dena bank

UCO bank

Vijaya bank

Indian overseas bank till here

NATURE OF BANKING IN INDIA

A banking company in India has been defined in the banking companies

act,1949.as one “which transacts the business of banking which means the

accepting, for the purpose of lending or investment of deposits of money from

the public, repayable on demand or otherwise and withdraw able by cheque,

draft, order or otherwise.”

Most of the activities a Bank performs are derived from the above definition. In

addition, Banks are allowed to perform certain activities which are ancillary to this

business of accepting deposits and lending. A bank's relationship with the public,

therefore, revolves around accepting deposits and lending money. Another activity

which is assuming increasing importance is transfer of money - both domestic and

foreign - from one place to another. This activity is generally known as "remittance

business" in banking parlance. The so called forex (foreign exchange) business is

largely a part of remittance albeit it involves buying and selling of foreign

currencies.

30

8/8/2019 97-93-Banking Sector in India

http://slidepdf.com/reader/full/97-93-banking-sector-in-india 31/82

FUNCTIONING OF A BANK

Functioning of a Bank is among the more complicated of corporate operations.

Since Banking involves dealing directly with money, governments in most

countries regulate this sector rather stringently. In India, the regulation traditionally

has been very strict and in the opinion of certain quarters, responsible for the

present condition of banks, where NPAs are of a very high order. The process of

financial reforms, which started in 1991, has cleared the cobwebs somewhat but a

lot remains to be done. The multiplicity of policy and regulations that a Bank has

to work with makes its operations even more complicated, sometimes bordering on

illogical. This section, which is also intended for banking professional, attempts to

give an overview of the functions in as simple manner as possible. Banking

Regulation Act of India, 1949 defines Banking as "accepting, for the purpose of

lending or investment of deposits of money from the public, repayable on demand

or otherwise and withdraw able by cheques, draft, and order or otherwise."

31

8/8/2019 97-93-Banking Sector in India

http://slidepdf.com/reader/full/97-93-banking-sector-in-india 32/82

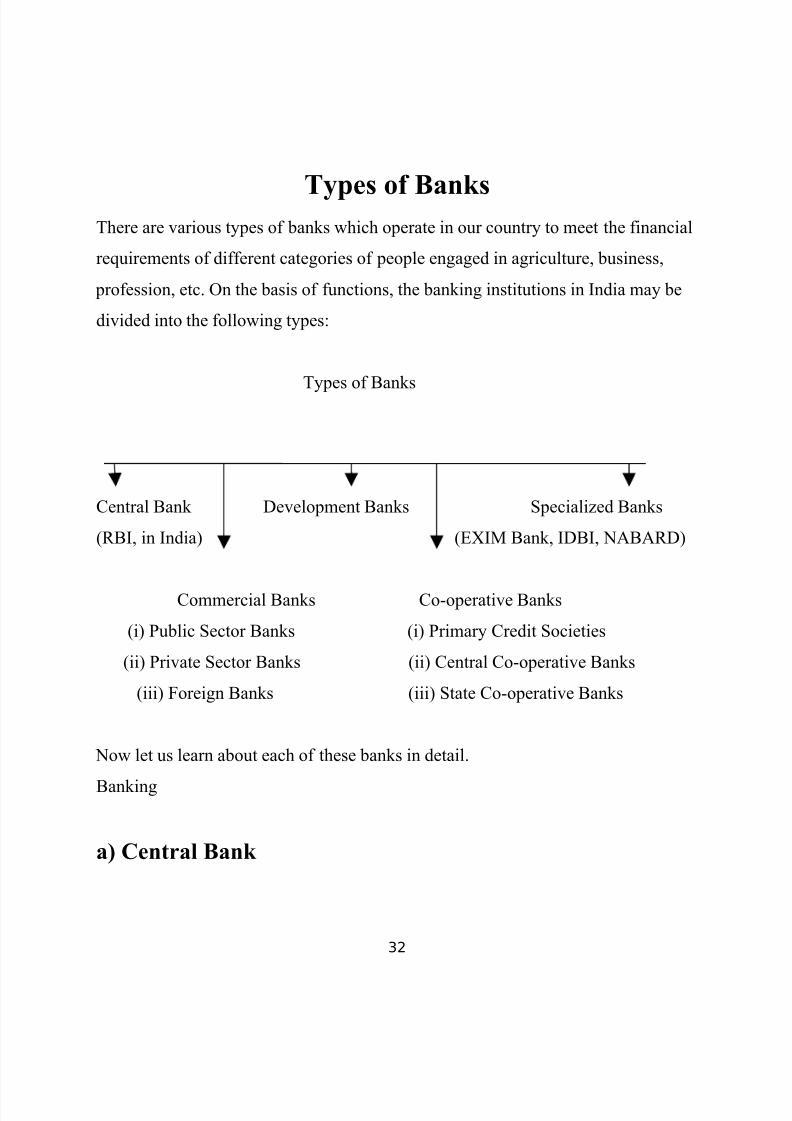

Types of BanksThere are various types of banks which operate in our country to meet the financial

requirements of different categories of people engaged in agriculture, business,

profession, etc. On the basis of functions, the banking institutions in India may be

divided into the following types:

Types of Banks

Central Bank Development Banks Specialized Banks

(RBI, in India) (EXIM Bank, IDBI, NABARD)

Commercial Banks Co-operative Banks

(i) Public Sector Banks (i) Primary Credit Societies

(ii) Private Sector Banks (ii) Central Co-operative Banks

(iii) Foreign Banks (iii) State Co-operative Banks

Now let us learn about each of these banks in detail.

Banking

a) Central Bank

32

8/8/2019 97-93-Banking Sector in India

http://slidepdf.com/reader/full/97-93-banking-sector-in-india 33/82

8/8/2019 97-93-Banking Sector in India

http://slidepdf.com/reader/full/97-93-banking-sector-in-india 34/82

Types of Commercial banks: Commercial banks are of three types i.e.,

Public sector banks, Private sector banks and foreign banks.

(i) Public Sector Banks: These are banks where majority stake is held by the

Government of India or Reserve Bank of India. Examples of public sector banks

are: State Bank of India, Corporation Bank, Bank of Boroda and Dena Bank, etc.

(ii) Private Sectors Banks: In case of private sector banks majority of share

capital of the bank is held by private individuals. These banks are registered as

companies with limited liability. For example: The Jammu and Kashmir Bank Ltd.,

Bank of Rajasthan Ltd.,Development Credit Bank Ltd, Lord Krishna Bank Ltd., Bharat Overseas Bank

Ltd., Global Trust Bank, Vysya Bank, etc.

(iii) Foreign Banks: These banks are registered and have their headquarters in a

foreign country but operate their branches in our country. Some of the foreign

banks operating in our country are Hong Kong and Shanghai Banking Corporation

(HSBC), Citibank, American

Express Bank, Standard & Chartered Bank, Grindlay’s Bank, etc. The number of

foreign banks operating in our country has increased since the financial sector

reforms of 1991.

c) Development Banks

Business often requires medium and long-term capital for purchase of machinery

and equipment, for using latest technology, or for expansion and modernization.

Such financial assistance is provided by Development Banks. They also undertake

other development measures like

Public Sector Banks comprise 19 nationalised banks and State Bank of India and

its 7 associate banks. Business Studies subscribing to the shares and debentures

34

8/8/2019 97-93-Banking Sector in India

http://slidepdf.com/reader/full/97-93-banking-sector-in-india 35/82

issued by companies, in case of under subscription of the issue by the public.

Industrial Finance Corporation of India (IFCI) and State Financial

Corporations (SFCs) are examples of development banks in India.

d) Co-operative Banks

People who come together to jointly serve their common interest often form a co-

operative society under the Co-operative Societies Act. When a co-operative

society engages itself in banking business it is called a Co-operative Bank. The

society has to obtain a license from the Reserve Bank of India before starting

banking business. Any co-operative bank as a society is to function under the

overall supervision of the Registrar, Co-operative Societies of the State. As regards

banking business, the society must follow the guidelines set and issued by the

Reserve Bank of India.

Types of Co-operative Banks

There are three types of co-operative banks operating in our country. They are

primary credit societies, central co-operative banks and state co-operative banks.

These banks are organized at three levels, village or town level, district level and

state level.

(i) Primary Credit Societies: These are formed at the village or town level with

borrower and non-borrower members residing in one locality. The operations of

each society are restricted to a small area so that the members know each other and

are able to watch over the activities of all members to prevent frauds.

(ii) Central Co-operative Banks: These banks operate at the district level having

some of the primary credit societies belonging to the same district as their

members. These banks provide loans to their members (i.e., primary credit

35

8/8/2019 97-93-Banking Sector in India

http://slidepdf.com/reader/full/97-93-banking-sector-in-india 36/82

societies) and function as a link between the primary credit societies and state co-

operative banks.

(iii) State Co-operative Banks: These are the apex (highest level) co-operative

banks in all the states of the country. They mobilize funds and help in its proper

channelization among various sectors. The money reaches the individual borrowers

from the state co-operative banks through the central co-operative banks and the

primary credit societies.

e) Specialized Banks

There are some banks, which cater to the requirements and provide overall support

for setting up business in specific areas of activity. EXIM Bank, SIDBI and

NABARD are examples of such banks. They engage themselves in some specific

area or activity and thus, are called specialized banks. Let us know about them.

i. Export Import Bank of India (EXIM Bank): If you want to set up a business

for exporting products abroad or importing products from foreign countries for sale

in our country, EXIM bank can provide you the required support and assistance.

The bank grants loans to exporters and importers and also provides information

about the international market. It gives guidance about the opportunities for export

or import, the risks involved in it and the competition to be faced, etc.

ii. Small Industries Development Bank of India (SIDBI): If you want to

establish a small-scale business unit or industry, loan on easy terms can be

available through SIDBI. It also finances modernization of small-scale industrial

units, use of new technology and market activities. The aim and focus of SIDBI is

to promote, finance and develop small-scale industries.

iii. National Bank for Agricultural and Rural Development (NABARD): It is a

central or apex institution for financing agricultural and rural sectors. If a person is

36

8/8/2019 97-93-Banking Sector in India

http://slidepdf.com/reader/full/97-93-banking-sector-in-india 37/82

engaged in agriculture or other activities like handloom weaving, fishing, etc.

NABARD can provide credit, both short-term and long-term, through regional

rural banks. It provides financial assistance, especially, to co-operative credit, in

the field of agriculture, small-scale industries, cottage and village industries

handicrafts and allied economic activities in rural areas.

Functions of Commercial Banks

The functions of commercial banks are of

two types.

(A) Primary functions; and

(B) Secondary functions.

Let us discuss details about these

functions.

(i) Primary functions

The primary functions of a commercial

bank include:

a) Accepting deposits; and

b) Granting loans and advances.

a) Accepting deposits

The most important activity of a commercial bank is to mobilise deposits from the

public. People who have surplus income and savings find it convenient to deposit

the amounts with banks.

Depending upon the nature of deposits, funds deposited with bank also earn

interest. Thus,

37

8/8/2019 97-93-Banking Sector in India

http://slidepdf.com/reader/full/97-93-banking-sector-in-india 38/82

Business Studies deposits with the bank grow along with the interest earned. If the

rate of interest is higher, public are motivated to deposit more funds with the bank.

There is also safety of funds deposited with the bank.

b) Grant of loans and advances

The second important function of a commercial bank is to grant loans and

advances. Such loans and advances are given to members of the public and to the

business community at a higher rate of interest than allowed by banks on various

deposit accounts. The rate of interest charged on loans and advances varies

according to the purpose and period of loan and also the mode of repayment.

i) Loans

A loan is granted for a specific time period. Generally commercial banks provide

short-term loans. But term loans, i.e., loans for more than a year may also be

granted. The borrower may be given the entire amount in lump sum or in

installments. Loans are generally granted against the security of certain assets. A

loan is normally repaid in installments. However, it may also be repaid in lump

sum.

ii) Advances

An advance is a credit facility provided by the bank to its customers. It differs from

loan in the sense that loans may be granted for longer period, but advances are

normally granted for a short period of time. Further the purpose of granting

advances is to meet the day-to-day requirements of business. The rate of interest

charged on advances varies from bank to bank.

Interest is charged only on the amount withdrawn and not on the sanctioned

amount.

38

8/8/2019 97-93-Banking Sector in India

http://slidepdf.com/reader/full/97-93-banking-sector-in-india 39/82

Types of Advances

Banks grant short-term financial assistance by way of cash credit, overdraft and

bill discounting.

Let us learn about these.

a) Cash Credit

Cash credit is an arrangement whereby the bank allows the borrower to draw

amount up to a specified limit. The amount is credited to the account of the

customer. The customer can withdraw this amount as and when he requires.

Interest is charged on the amount actually withdrawn. Cash Credit is granted as per

terms and conditions agreed with the customers.b) Overdraft

Overdraft is also a credit facility granted by bank. A customer who has a current

account with the bank is allowed to withdraw more than the amount of credit

balance in his account.

It is a temporary arrangement. Overdraft facility with a specified limit may be

allowed either on the security of assets, or on personal security, or both.

c) Discounting of Bills

Banks provide short-term finance by discounting bills that is, making payment of

the amount before the due date of the bills after deducting a certain rate of

discount. The party gets the funds without waiting for the date of maturity of the

bills. In case any bill is dishonoured on the due date, the bank can recover the

amount from the customer.

Banking

ii) Secondary functions

39

8/8/2019 97-93-Banking Sector in India

http://slidepdf.com/reader/full/97-93-banking-sector-in-india 40/82

In addition to the primary functions of accepting deposits and lending money,

banks perform a number of other functions, which are called secondary functions.

These are as follows.

Issuing letters of credit, traveler’s cheque, etc.

b. Undertaking safe custody of valuables, important document and securities by

providing safe deposit vaults or lockers.

c. Providing customers with facilities of foreign exchange dealings.

d. Transferring money from one account to another; and from one branch to

another branch of the bank through cheque, pay order, demand draft.

e. Standing guarantee on behalf of its customers, for making payment for purchase

of goods, machinery, vehicles etc.

f. Collecting and supplying business information.

g. Providing reports on the credit worthiness of customers.

i. Providing consumer finance for individuals by way of loans on easy terms for

purchase of consumer durables like televisions, refrigerators, etc.

j. Educational loans to students at reasonable rate of interest for higher studies,

especially for professional courses.

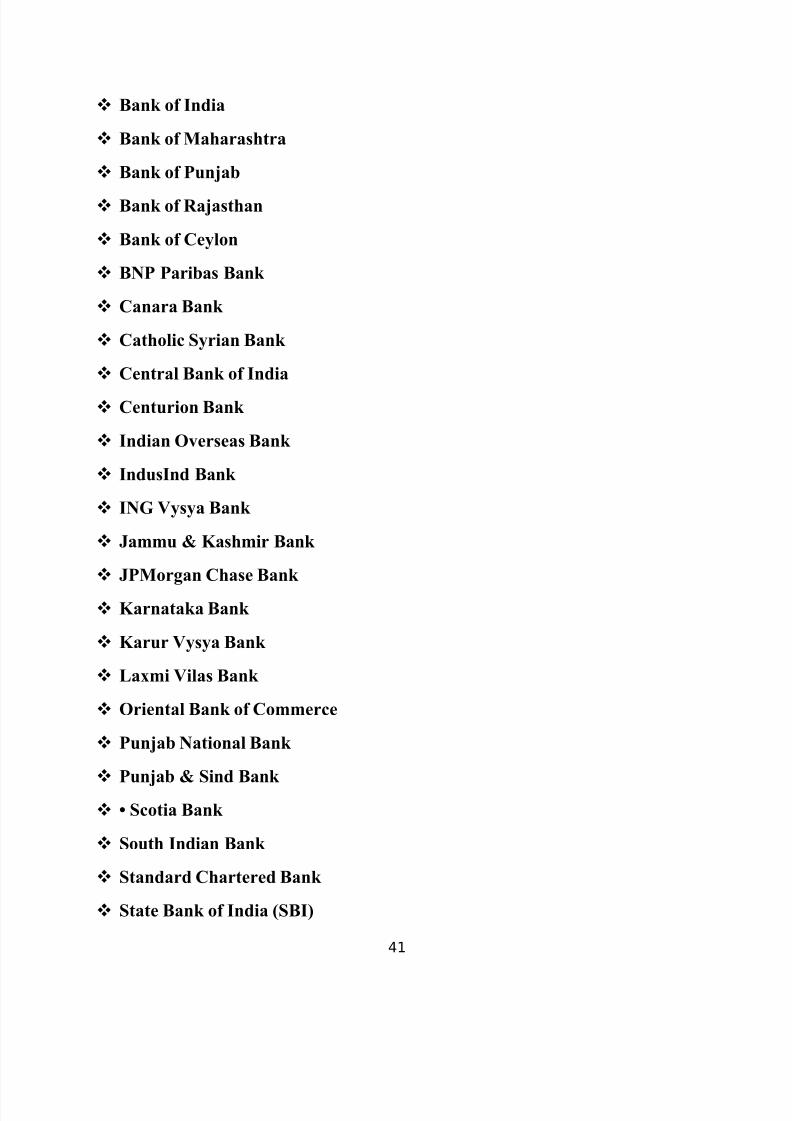

Major Banks in India

ABN-AMRO Bank

Abu Dhabi Commercial Bank

American Express Bank

Andhra Bank

Allahabad Bank

Bank of Baroda

40

8/8/2019 97-93-Banking Sector in India

http://slidepdf.com/reader/full/97-93-banking-sector-in-india 41/82

Bank of India

Bank of Maharashtra

Bank of Punjab

Bank of Rajasthan

Bank of Ceylon

BNP Paribas Bank

Canara Bank

Catholic Syrian Bank

Central Bank of India

Centurion Bank

Indian Overseas Bank

IndusInd Bank

ING Vysya Bank

Jammu & Kashmir Bank

JPMorgan Chase Bank

Karnataka Bank

Karur Vysya Bank

Laxmi Vilas Bank

Oriental Bank of Commerce

Punjab National Bank

Punjab & Sind Bank

• Scotia Bank

South Indian Bank

Standard Chartered Bank

State Bank of India (SBI)

41

8/8/2019 97-93-Banking Sector in India

http://slidepdf.com/reader/full/97-93-banking-sector-in-india 42/82

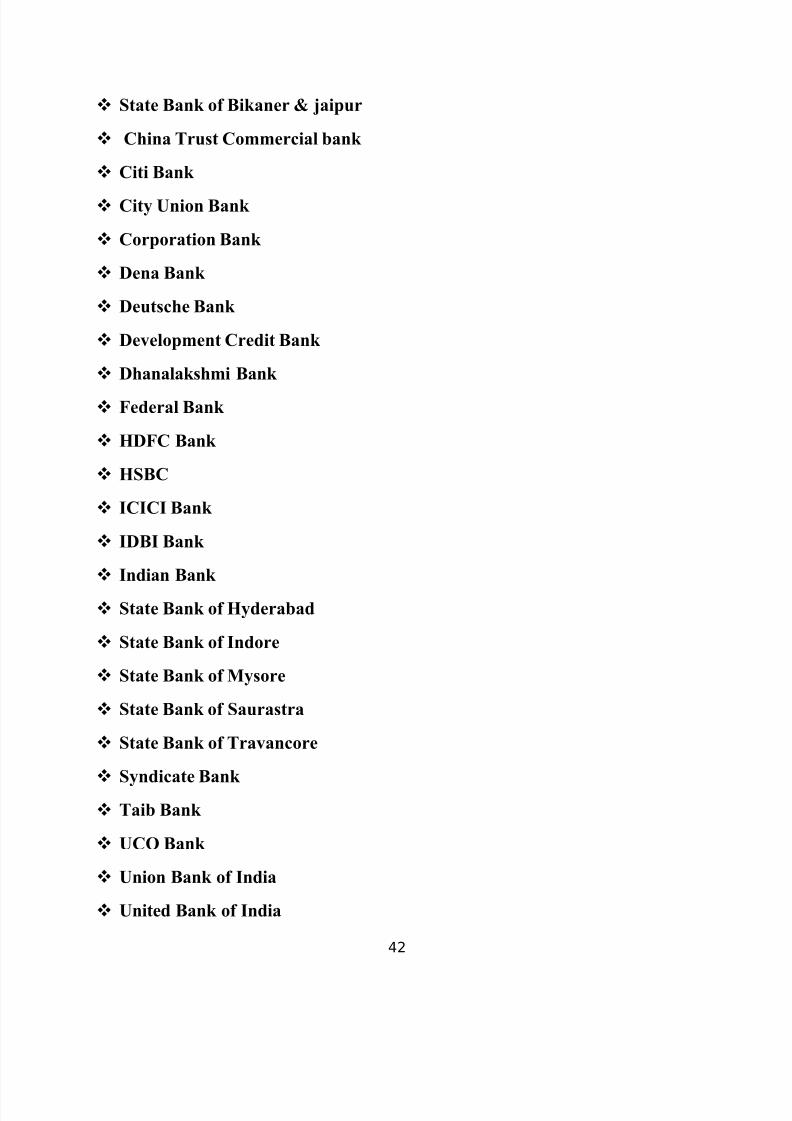

State Bank of Bikaner & jaipur

China Trust Commercial bank

Citi Bank

City Union Bank

Corporation Bank

Dena Bank

Deutsche Bank

Development Credit Bank

Dhanalakshmi Bank

Federal Bank

HDFC Bank

HSBC

ICICI Bank

IDBI Bank

Indian Bank

State Bank of Hyderabad

State Bank of Indore

State Bank of Mysore

State Bank of Saurastra

State Bank of Travancore

Syndicate Bank

Taib Bank

UCO Bank

Union Bank of India

United Bank of India

42

8/8/2019 97-93-Banking Sector in India

http://slidepdf.com/reader/full/97-93-banking-sector-in-india 43/82

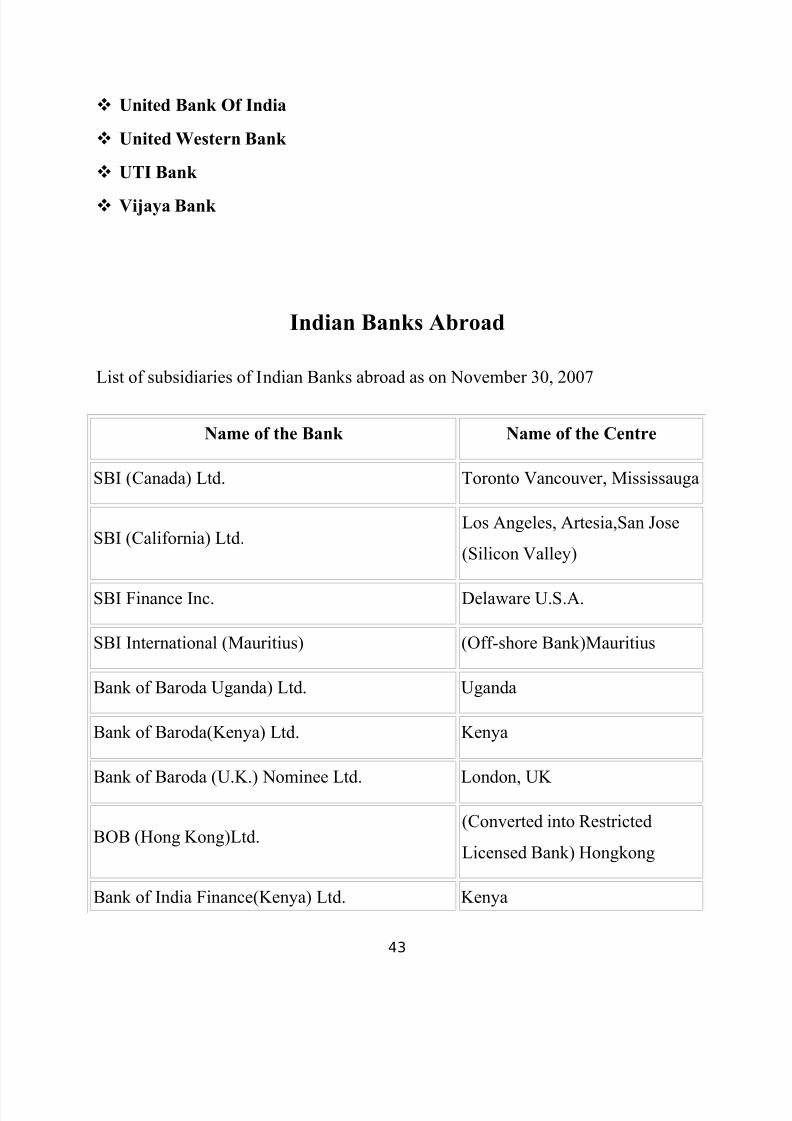

United Bank Of India

United Western Bank

UTI Bank

Vijaya Bank

Indian Banks Abroad

List of subsidiaries of Indian Banks abroad as on November 30, 2007

Name of the Bank Name of the Centre

SBI (Canada) Ltd. Toronto Vancouver, Mississauga

SBI (California) Ltd.Los Angeles, Artesia,San Jose

(Silicon Valley)

SBI Finance Inc. Delaware U.S.A.

SBI International (Mauritius) (Off-shore Bank)Mauritius

Bank of Baroda Uganda) Ltd. Uganda

Bank of Baroda(Kenya) Ltd. Kenya

Bank of Baroda (U.K.) Nominee Ltd. London, UK

BOB (Hong Kong)Ltd.(Converted into Restricted

Licensed Bank) Hongkong

Bank of India Finance(Kenya) Ltd. Kenya

43

8/8/2019 97-93-Banking Sector in India

http://slidepdf.com/reader/full/97-93-banking-sector-in-india 44/82

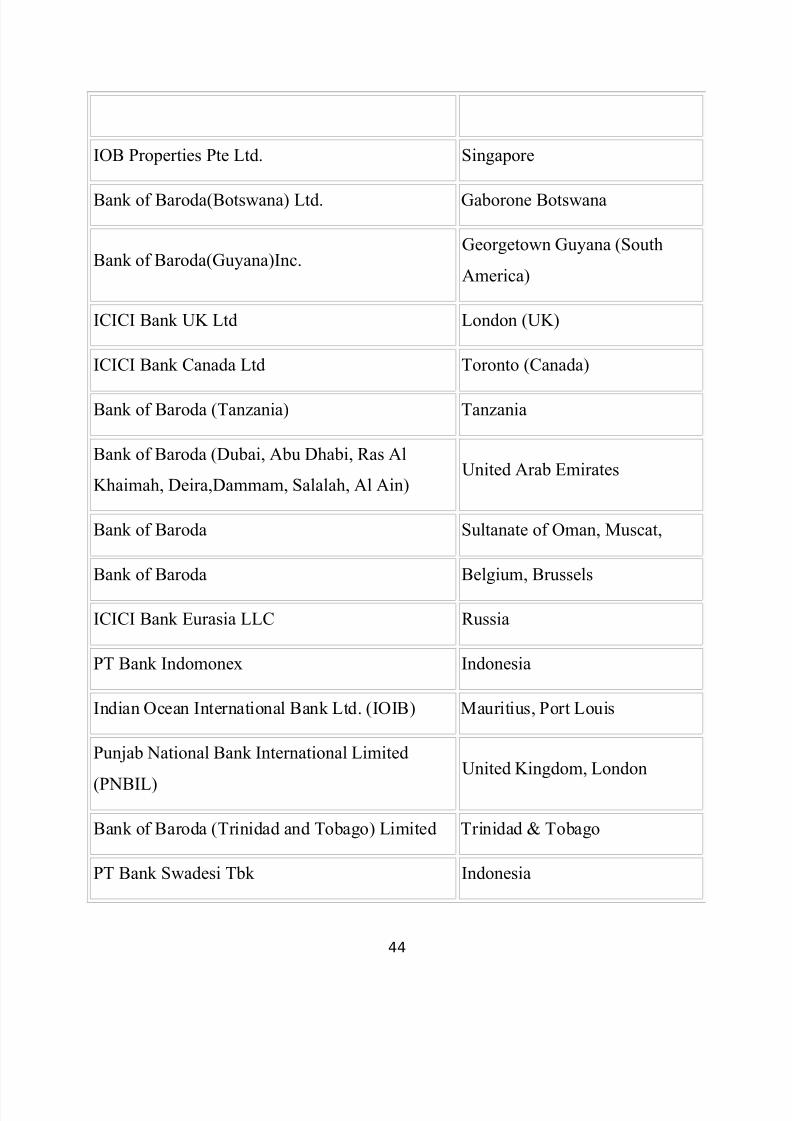

IOB Properties Pte Ltd. Singapore

Bank of Baroda(Botswana) Ltd. Gaborone Botswana

Bank of Baroda(Guyana)Inc.Georgetown Guyana (South

America)

ICICI Bank UK Ltd London (UK)

ICICI Bank Canada Ltd Toronto (Canada)

Bank of Baroda (Tanzania) Tanzania

Bank of Baroda (Dubai, Abu Dhabi, Ras Al

Khaimah, Deira,Dammam, Salalah, Al Ain)United Arab Emirates

Bank of Baroda Sultanate of Oman, Muscat,

Bank of Baroda Belgium, Brussels

ICICI Bank Eurasia LLC Russia

PT Bank Indomonex Indonesia

Indian Ocean International Bank Ltd. (IOIB) Mauritius, Port Louis

Punjab National Bank International Limited

(PNBIL)

United Kingdom, London

Bank of Baroda (Trinidad and Tobago) Limited Trinidad & Tobago

PT Bank Swadesi Tbk Indonesia

44

8/8/2019 97-93-Banking Sector in India

http://slidepdf.com/reader/full/97-93-banking-sector-in-india 45/82

Bank of Baroda (Trinidad and Tobago) Limited Trinidad & Tobago

45

8/8/2019 97-93-Banking Sector in India

http://slidepdf.com/reader/full/97-93-banking-sector-in-india 46/82

SWOT ANALYSIS OF BANKS

STRENGTH

Indian banks have compared favorably on growth, asset quality and profitability

with other regional banks over the last few years. The banking index has grown at

a compounded annual rate of over 51 per cent since April 2001 as compared to a

27 per cent growth in the market index for the same period.

• Policy makers have made some notable changes in policy and regulation to

help strengthen the sector. These changes include strengthening prudential norms,

enhancing the payments system and integrating regulations between commercial

and co-operative banks.

• Bank lending has been a significant driver of GDP growth and employment.

Extensive reach: the vast networking & growing number of

branches & ATMs. Indian banking system has reached even

to the remote corners of the country.• The government's regular policy for Indian bank since 1969has paid rich

dividends with the nationalization of 14 major private banks of India.

• In terms of quality of assets and capital adequacy, Indian banks are considered

to have clean, strong and transparent Balance sheets relative to other banks in

comparable economies in its region.

• India has 88 scheduled commercial banks (SCBs) - 27 public sector banks

(that is with the Government of India holding a stake)after merger of New Bank of

India in Punjab National Bank in 1993, 29 private banks (these do not have

government stake; they may be publicly listed and traded on stock exchanges) and

31 foreign banks. They have a combined network of over 53,000 branches and

46

8/8/2019 97-93-Banking Sector in India

http://slidepdf.com/reader/full/97-93-banking-sector-in-india 47/82

17,000 ATMs. According to a report by ICRA Limited, a rating agency, the public

sector banks hold over 75 percent of total assets of the banking industry, with the

private and foreign banks holding 18.2% and 6.5% respectively.

• Foreign banks will have the opportunity to own up to 74 percent of Indian

private sector banks and 20 per cent of government owned banks.

• With the growth in the Indian economy expected to be strong for quite some

time-especially in its services sector-the demand for banking services, especially

retail banking, mortgages and investment services are expected to be strong.

• the Reserve Bank of India (RBI) has approved a proposal from the government

to amend the Banking Regulation Act to permit banks to trade in commodities and

commodity derivatives.

• Liberalization of ECB norms: The government also liberalized the ECB norms to

permit financial sector entities engaged in infrastructure funding to raise ECBs.

This enabled banks and financial institutions, which were earlier not permitted to

raise such funds, explore this route for raising cheaper funds in the overseas

markets.

• Hybrid capital: In an attempt to relieve banks of their capital crunch, the RBI has

allowed them to raise perpetual bonds and other hybrid capital securities to shore

up their capital. If the new instruments find takers, it would help PSU banks, left

with little headroom for raising equity. Significantly, FII and NRI investment

limits in these securities have been fixed at 49%, compared to 20% foreign equity

holding allowed in PSU banks.

47

8/8/2019 97-93-Banking Sector in India

http://slidepdf.com/reader/full/97-93-banking-sector-in-india 48/82

WEAKNESS

• PSBs need to fundamentally strengthen institutional skill levels especially in

sales and marketing, service operations, risk management and the overall

organizational performance ethic & strengthen human capital.

• Old private sector banks also have the need to fundamentally strengthen skill

levels.

• The cost of intermediation remains high and bank penetration is limited to

only a few customer segments and geographies.• Structural weaknesses such as a fragmented industry structure, restrictions on

capital availability and deployment, lack of institutional support infrastructure,

restrictive labour laws, weak corporate governance and ineffective regulations

beyond Scheduled Commercial Banks (SCBs), unless industry utilities and service

bureaus.

Refusal to dilute stake in PSU banks: The government has refused to dilute its

stake in PSU banks below 51% thus choking the headroom available to these banks

for raining equity capital.

• Impediments in sectoral reforms: Opposition from Left and resultant cautious

approach from the North Block in terms of approving merger of PSU banks may

hamper their growth prospects in the medium term.

OPPORTUNITY

• The market is seeing discontinuous growth driven by new products and

services that include opportunities in credit cards, consumer finance and wealth

48

8/8/2019 97-93-Banking Sector in India

http://slidepdf.com/reader/full/97-93-banking-sector-in-india 49/82

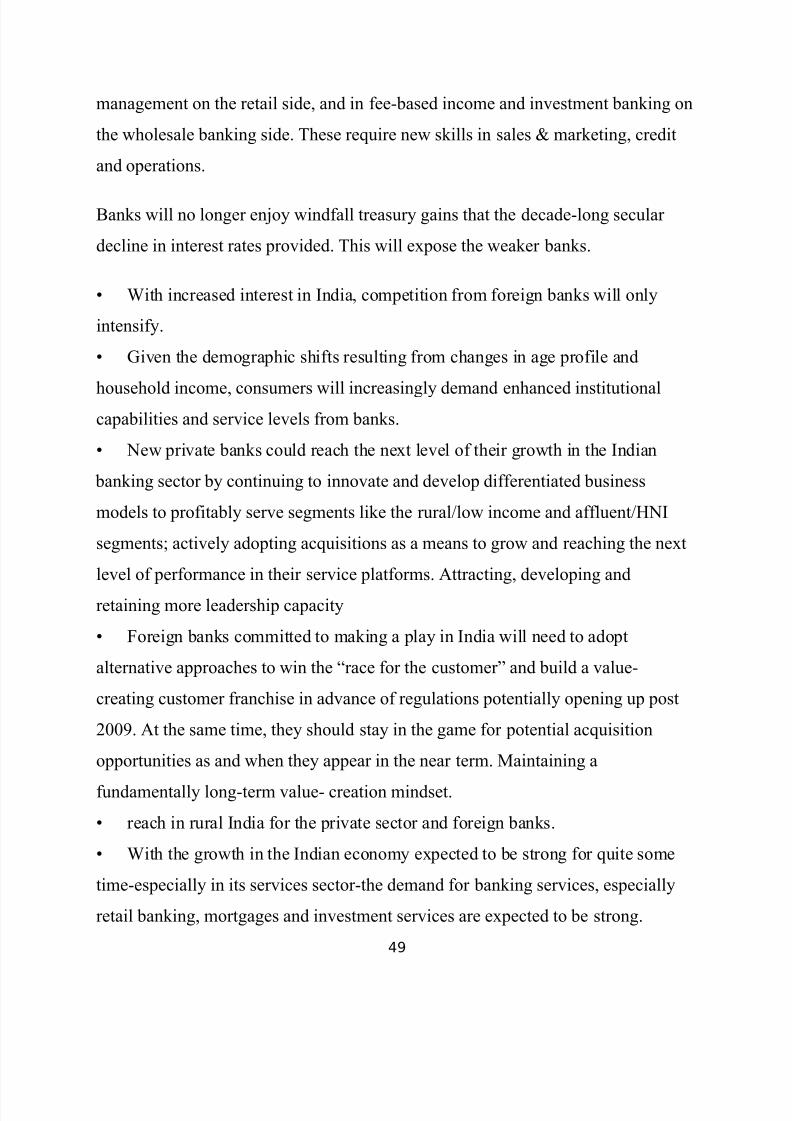

management on the retail side, and in fee-based income and investment banking on

the wholesale banking side. These require new skills in sales & marketing, credit

and operations.

Banks will no longer enjoy windfall treasury gains that the decade-long secular

decline in interest rates provided. This will expose the weaker banks.

• With increased interest in India, competition from foreign banks will only

intensify.

• Given the demographic shifts resulting from changes in age profile and

household income, consumers will increasingly demand enhanced institutionalcapabilities and service levels from banks.

• New private banks could reach the next level of their growth in the Indian

banking sector by continuing to innovate and develop differentiated business

models to profitably serve segments like the rural/low income and affluent/HNI

segments; actively adopting acquisitions as a means to grow and reaching the next

level of performance in their service platforms. Attracting, developing and

retaining more leadership capacity

• Foreign banks committed to making a play in India will need to adopt

alternative approaches to win the “race for the customer” and build a value-

creating customer franchise in advance of regulations potentially opening up post

2009. At the same time, they should stay in the game for potential acquisition

opportunities as and when they appear in the near term. Maintaining a

fundamentally long-term value- creation mindset.

• reach in rural India for the private sector and foreign banks.

• With the growth in the Indian economy expected to be strong for quite some

time-especially in its services sector-the demand for banking services, especially

retail banking, mortgages and investment services are expected to be strong.

49

8/8/2019 97-93-Banking Sector in India

http://slidepdf.com/reader/full/97-93-banking-sector-in-india 50/82

8/8/2019 97-93-Banking Sector in India

http://slidepdf.com/reader/full/97-93-banking-sector-in-india 51/82

8/8/2019 97-93-Banking Sector in India

http://slidepdf.com/reader/full/97-93-banking-sector-in-india 52/82

simple text messages sent from your mobile. The messages are then recognized by

the bank to provide you with the required information.

All these technological changes have forced the bankers to adopt customer-

based approach instead of product-based approach.

ECONOMICAL ENVIROMENT

Banking is as old as authentic history and the modern commercial banking

are traceable to ancient times. In India, banking has existed in one form or the

other from time to time. The present era in banking may be taken to have

commenced with establishment of bank of Bengal in 1809 under the government

charter and with government participation in share capital. Allahabad bank was

started in the year 1865 and Punjab national bank in 1895, and thus, others

followed

Every year RBI declares its 6 monthly policy and accordingly the various

measures and rates are implemented which has an impact on the banking sector.

Also the Union budget affects the banking sector to boost the economy by giving

certain concessions or facilities. If in the Budget savings are encouraged, then

more deposits will be attracted towards the banks and in turn they can lend more

money to the agricultural sector and industrial sector, therefore, booming the

economy. If the FDI limits are relaxed, then more FDI are brought in India through

banking channels.

52

8/8/2019 97-93-Banking Sector in India

http://slidepdf.com/reader/full/97-93-banking-sector-in-india 53/82

POLITICAL/ LEGAL ENVIROMENT

Government and RBI policies affect the banking sector. Sometimes looking

into the political advantage of a particular party, the Government declares some

measures to their benefits like waiver of short-term agricultural loans, to attract the

farmer’s votes. By doing so the profits of the bank get affected. Various banks in

the cooperative sector are open and run by the politicians. They exploit these banks

for their benefits. Sometimes the government appoints various chairmen of the

banks.

Various policies are framed by the RBI looking at the present situation of the country for better control over the banks.

SOCIAL ENVIROMENT

Before nationalization of the banks, their control was in the hands of the

private parties and only big business houses and the effluent sections of the society

were getting benefits of banking in India. In 1969 government nationalized 14

banks. To adopt the social development in the banking sector it was necessary for

speedy economic progress, consistent with social justice, in democratic political

system, which is free from domination of law, and in which opportunities are open

to all. Accordingly, keeping in mind both the national and social objectives,

bankers were given direction to help economically weaker section of the society

and also provide need-based finance to all the sectors of the economy with flexible

and liberal attitude. Now the banks provide various types of loans to farmers,

53

8/8/2019 97-93-Banking Sector in India

http://slidepdf.com/reader/full/97-93-banking-sector-in-india 54/82

working women, professionals, and traders. They also provide education loan to

the students and housing loans, consumer loans, etc.

Banks having big clients or big companies have to provide services like

personalized banking to their clients because these customers do not believe in

running about and waiting in queues for getting their work done. The bankers also

have to provide these customers with special provisions and at times with benefits

like food and parties. But the banks do not mind incurring these costs because of

the kind of business these clients bring for the bank.

Banks have changed the culture of human life in India and have made lifemuch easier for the people.

54

8/8/2019 97-93-Banking Sector in India

http://slidepdf.com/reader/full/97-93-banking-sector-in-india 55/82

Recent banking developments in India

The Indian banking sector has witnessed wide ranging changes under the influence

of the financial sector reforms initiated during the early 1990s. The approach to

such reforms in India has been one of gradual and non-disruptive progress through

a consultative process. The emphasis has been on deregulation and opening up the

banking sector to market forces. The Reserve Bank has been consistently working

towards the establishment of an enabling regulatory framework with prompt and

effective supervision as well as the development of technological and institutional

infrastructure.

Persistent efforts have been made towards adoption of international benchmarks as

appropriate to Indian conditions. While certain changes in the legal infrastructure

are yet to be effected, the developments so far have brought the Indian financial

system closer to global standards.

Statutory Pre-emptions

In the pre-reforms phase, the Indian banking system operated with a high level of

statutory preemptions, in the form of both the Cash Reserve Ratio (CRR) and the

Statutory Liquidity Ratio (SLR), reflecting the high level of the country’s fiscal

deficit and its high degree of monetization. Efforts in the recent period have been

focused on lowering both the CRR and SLR. The statutory minimum of

25 per cent for the SLR was reached as early as 1997, and while the Reserve Bank

continues to pursue its medium-term objective of reducing the CRR to the statutory

55

8/8/2019 97-93-Banking Sector in India

http://slidepdf.com/reader/full/97-93-banking-sector-in-india 56/82

minimum level of 3.0 per cent, the CRR of the Scheduled Commercial Banks

(SCBs) is currently placed at 5.0 per cent of NDTL (net demand and time

liabilities). The legislative changes proposed by the Government in the Union

Budget, 2005-06 to remove the limits on the SLR and CRR are expected to provide

freedom to the Reserve Bank in the conduct of monetary policy and also lend

further flexibility to the banking system in the deployment of resources.

Interest Rate Structure

Deregulation of interest rates has been one of the key features of financial sector

reforms. In recent years, it has improved the competitiveness of the financial

environment and strengthened the transmission mechanism of monetary policy.

Sequencing of interest rate deregulation has also enabled better price discovery and

imparted greater efficiency to the resource allocation process. The process has

been gradual and predicated upon the institution of prudential regulation of the

banking system, market behaviour, financial opening and, above all, the underlying

macroeconomic conditions.

Interest rates have now been largely deregulated except in the case of: (i) savings

deposit accounts; (ii) non-resident Indian (NRI) deposits; (iii) small loans up to

Rs.2 lakh; and (iv) export credit.

After the interest rate deregulation, banks became free to determine their own

lending interest rates.

56

8/8/2019 97-93-Banking Sector in India

http://slidepdf.com/reader/full/97-93-banking-sector-in-india 57/82

As advised by the Indian Banks’ Association (a self-regulatory organisation for

banks), commercial banks determine their respective BPLRs (benchmark prime

lending rates) taking into consideration:

(i) actual cost of funds; (ii) operating expenses; and (iii) a minimum margin to

cover regulatory requirements of provisioning and capital charge and profit

margin. These factors differ from bank to bank and feed into the determination of

BPLR and spreads of banks. The BPLRs of public sector banks declined to 10.25-

11.25 per cent in March 2005 from 10.25-11.50 per cent in March 2004.With a

view to granting operational autonomy to public sector banks, public ownership in

these banks was reduced by allowing them to raise capital from the equity market

of up to 49 per cent of paid-up capital. Competition is being fostered by permitting

new private sector banks, and more liberal entry of branches of foreign banks,

joint-venture banks and insurance companies.

Recently, a roadmap for the presence of foreign banks in India was released which

sets out the process of the gradual opening-up of the banking sector in a

transparent manner. Foreign investments in the financial sector in the form 238

BIS Papers No 28 of Foreign Direct Investment (FDI) as well as portfolio

investment have been permitted. Furthermore, banks have been allowed to

diversify product portfolio and business activities. The share of public sector banks

in the banking business is going down, particularly in metropolitan areas. Some

diversification of ownership in select public sector banks has helped further the

move towards autonomy and thus provided some response to competitive

pressures. Transparency and disclosure standards have been enhanced to meet

international standards in an ongoing manner.

57

8/8/2019 97-93-Banking Sector in India

http://slidepdf.com/reader/full/97-93-banking-sector-in-india 58/82

Exposure Norms

The Reserve Bank has prescribed regulatory limits on banks’ exposure to

individual and group borrowers to avoid concentration of credit, and has advised

banks to fix limits on their exposure to specific industries or sectors (real estate) to

ensure better risk management. In addition, banks are also required to observe

certain statutory and regulatory limits in respect of their exposures to capital

markets.

Asset-Liability Management

In view of the growing need for banks to be able to identify, measure, monitor and

control risks, appropriate risk management guidelines have been issued from time

to time by the Reserve Bank, including guidelines on Asset-Liability Management

(ALM). These guidelines are intended to serve as a benchmark for banks to

establish an integrated risk management system. However, banks can also develop

their own systems compatible with type and size of operations as well as risk

perception and put in place a proper system for covering the existing deficiencies

and the requisite upgrading. Detailed guidelines on the management of credit risk,

market risk, operational risk, etc. have also been issued to banks by the Reserve

Bank. The progress made by the banks is monitored on a quarterly basis. With

58

8/8/2019 97-93-Banking Sector in India

http://slidepdf.com/reader/full/97-93-banking-sector-in-india 59/82

regard to risk management techniques, banks are at different stages of drawing up

a comprehensive credit rating system, undertaking a credit risk assessment on a

half yearly basis, pricing loans on the basis of risk rating, adopting the Risk-

Adjusted Return on Capital (RAROC) framework of pricing, etc.

Some banks stipulate a quantitative ceiling on aggregate exposures in specified risk

categories; analyze rating-wise distribution of borrowers in various industries, etc.

In respect of market risk, almost all banks have an Asset-Liability Management

Committee. They have articulated market risk management policies and

procedures, and have undertaken studies of behavioural maturity patterns of

various components of on-/off-balance sheet items.

Board for Financial Supervision (BFS)

An independent Board for Financial Supervision (BFS) under the aegis of the

Reserve Bank has been established as the apex supervisory authority for

commercial banks, financial institutions, urban banks and NBFCs. Consistent with

international practice, the Board’s focus is on offsite and on-site inspections and on

banks’ internal control systems. Offsite surveillance has been strengthened through

control returns.

The role of statutory auditors has been emphasized with increased internal control

through strengthening of the internal audit function. Significant progress has been

made in implementation of the Core Principles for Effective Banking Supervision.

59

8/8/2019 97-93-Banking Sector in India

http://slidepdf.com/reader/full/97-93-banking-sector-in-india 60/82

The supervisory rating system under CAMELS has been established, coupled with

a move towards risk-based supervision.

Consolidated supervision of financial conglomerates has since been introduced

with bi-annual discussions with the financial conglomerates. There have also been

initiatives aimed at strengthening corporate governance through enhanced due

diligence on important shareholders, and fit and proper tests for directors.

A scheme of Prompt Corrective Action (PCA) is in place for attending to banks

showing steady deterioration in financial health. Three financial indicators, viz.

capital to risk-weighted assets ratio

(CRAR), net non-performing assets (net NPA) and Return on Assets (RoA) have

been identified with specific threshold limits. When the indicators fall below the

threshold level (CRAR, RoA) or go above it (net NPAs), the PCA scheme

envisages certain structured/discretionary actions to be taken by the regulator.

The structured actions in the case of CRAR falling below the trigger point may

include, among other things, submission and implementation of a capital

restoration plan, restriction on expansion of risk weighted assets, restriction on

entering into new lines of business, reducing/skipping dividend payments, and

requirement for recapitalization.

The structured actions in the case of RoA falling below the trigger level may

include, among other things, restriction on accessing/renewing costly deposits and

CDs, a requirement to take steps to increase fee-based income and to contain

administrative expenses, not to enter new lines of business, imposition of

restrictions on borrowings from the interbank market, etc.

In the case of increasing net NPAs, structured actions will include, among other

things, undertaking a special drive to reduce the stock of NPAs and containing the

generation of fresh NPAs, reviewing the loan policy of the bank, taking steps to

upgrade credit appraisal skills and systems and to strengthen follow-up of

60

8/8/2019 97-93-Banking Sector in India

http://slidepdf.com/reader/full/97-93-banking-sector-in-india 61/82

advances, including a loan review mechanism for large loans, following up suit

filed/ decreed debts effectively, putting in place proper credit risk management

policies/processes/procedures/prudential limits, reducing loan concentration, etc.

Discretionary action may include restrictions on capital expenditure, expansion in

staff, an increase of stake in subsidiaries. The Reserve Bank/Government may take

steps to change promoters/ ownership and may even take steps to

merge/amalgamate/liquidate the bank or impose a moratorium on it if its position

does not improve within an agreed period.

Technological Infrastructure

In recent years, the Reserve Bank has endeavored to improve the efficiency of the

financial system by ensuring the presence of a safe, secure and effective payment

and settlement system. In the process, apart from performing regulatory and