9 Insights Into Potential RDC Litigation Carrubba...

18

Insights into Potential RDC Litigation Legal Issues and Reasonable Commercial Standards October 27, 2015 Paul Carrubba, Adams and Reese Mary Hockridge, Mobile Strategy Partners

Transcript of 9 Insights Into Potential RDC Litigation Carrubba...

Insights into Potential RDC Litigation Legal Issues and Reasonable Commercial Standards

October 27, 2015

Paul Carrubba, Adams and Reese

Mary Hockridge, Mobile Strategy Partners

Presentation Content

THIS PRESENTATION IS DESIGNED TO PROVIDE

ACCURATE AND AUTHORITATIVE INFORMATION

REGARDING ITS SUBJECT MATTER. IT IS PRESENTED

WITH THE UNDERSTANDING THAT THE PRESENTER IS

NOT RENDERING LEGAL, ACCOUNTING, OR OTHER

PROFESSIONAL SERVICES. IF LEGAL ADVICE OR OTHER

EXPERT ASSISTANCE IS REQUIRED, THE SERVICES OF A

COMPETENT PROFESSIONAL PERSON SHOULD BE

SOUGHT.

Agenda

• Understanding, Identifying and Resolving Duplicates

• The Impact and Consequences of Duplicates

• Ordinary Care and Reasonable Commercial Standards

• Duplicates and Holder in Due Course Claims

• Proposed Amendment to Reg CC

• Summary & Questions

3

Understanding Duplicates Customer initiated duplicate transactions happen when an RDC

depositor accidentally or fraudulently negotiates an RDC

deposited check more than once.

Depositor

Bank - RDC Deposit

Payor Bank

ICL

Bank - ATM Deposit

ICL

4

1st Presentment

Duplicate Presentment

Return or Adjustment

Drawer

Impact to Banks:

• New technology and processes to

identify and prevent checks from

paying against their customers’

account more than once

• A growing number of operational

resources are required to research

and adjust duplicates

• Cost of fraud losses and write offs

resulting from duplicates

Where are Duplicates Identified

5

Depositary Bank

In-Channel & Cross Channel Duplicate

Detection

Incoming Returns and Adjustments

Payor Bank

Posting System Duplicate Detection

Customer Reported

Duplicates

Proactive - Identify and Prevent the

Duplicate

Reactive - Externally identified

Statistics for Duplicates

• Based on several large financial institutions, rate of duplicates identified in item

processing and day two operations is as follows:

• 2,250 duplicates per 1,000,000 - mobile deposits

• 100 duplicates per 1,000,000 - all debits processed (deposits and

inclearings)

0%

20%

40%

60%

80%

100%

120%

Time Lapse Between Duplicates

% of items

Cumulative %

Payor Bank - Dealing with Duplicates

Using Returns Using Adjustments

• Only an option if returned before the Midnight deadline

• Pros & Cons of Returns vs. Adjustments • Faster settlement and you do not lose

right of return if item is a counterfeit • Adjustment reversal • Potential for negative impact to the

depositor if the duplicate was due to a bank processing error

• Adjustment Options • Paid item (PAID) type (1)

• Within 6 months the adjustment is made with entry

• 6 months to a year - without entry and Fed has 20 days to respond

• Warranty Claim (WIC) type (2) • Must be with one year and it is without

entry and the Fed has up to 80 days to respond

http://www.frbservices.org/operations/checkadjustments/paid.html

http://www.frbservices.org/operations/checkadjustments/wic.html

(1)

(2)

7

Operational Best Practices

Establish, document, and follow procedures that meet

reasonable commercial standards

• Consistent with general industry practices

• Can be validated by expert opinions and/or testimony

• Are followed consistently

– Maintain an adequate number of trained resources to perform

procedures

– Utilize and stay current on technology that automates transaction

monitoring

8

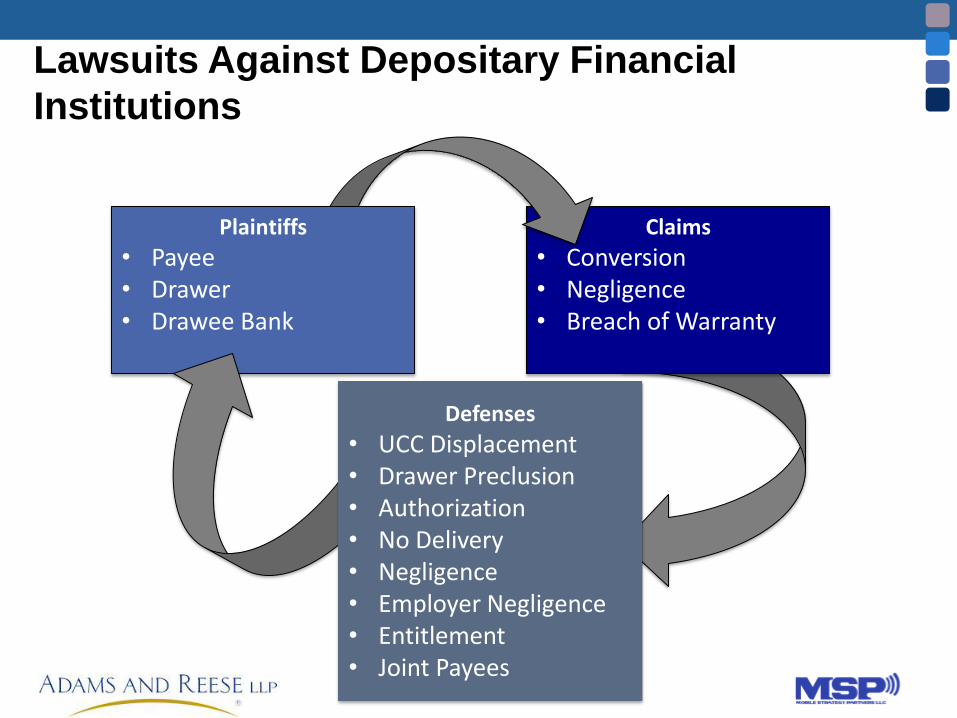

Lawsuits Against Depositary Financial

Institutions

9

Claims

• Conversion • Negligence • Breach of Warranty

Plaintiffs

• Payee • Drawer • Drawee Bank

Defenses

• UCC Displacement • Drawer Preclusion • Authorization • No Delivery • Negligence • Employer Negligence • Entitlement • Joint Payees

Ordinary Care and Reasonable Commercial

Standards

• UCC provides guidelines for what “Ordinary Care” and

“Reasonable Commercial Standards” mean in practice,

but does not specifically define what actions are

required

• In lawsuits, the judge or jury must determine whether a

party’s actions met reasonable commercial standards

• If a party’s action do not meet reasonable commercial

standards, they may be required to bear responsibility

for some or all of the loss

10

Case Law Example #1

Continental Casualty Company Inc. v. American National Bank & Trust

• Facts: • Comptroller of Company had Company issue 9 checks payable to ANB

• Comptroller deposited the 9 checks to his personal account via an ATM

• Company sued bank claiming negligence

• Defense: • Bank defended claiming that the checks were deposited by an automated means. It was not

required (UCC 3-103) to examine the checks

• Court Decision: • Court held for Company claiming 3-103 was not applicable to depository Bank applicable only

to Payor Bank

• ANB was negligent for accepting the checks payable to ANB without making an inquiry of the

Company

11

Case Law Example #2

Lower Court Case – Plaintiff/Defendant Names not cited*

• Facts: • Secretary of Company deposited checks payable to Company into her personal account

via an ATM over a two year period

• Company sued depository Bank for conversion and negligence

• Defense: • Company was negligent in not supervising employee

• Bank did not fail to exercise ordinary care by not examining the checks (3-103)

• Court Decision: • Court held for bank that 3-103 defense is applicable to a depository bank and deposits to

an ATM is an automated process

• *Source: The Law of Bank Deposits, Collections and Credit Cards, author Barclay Clark

12

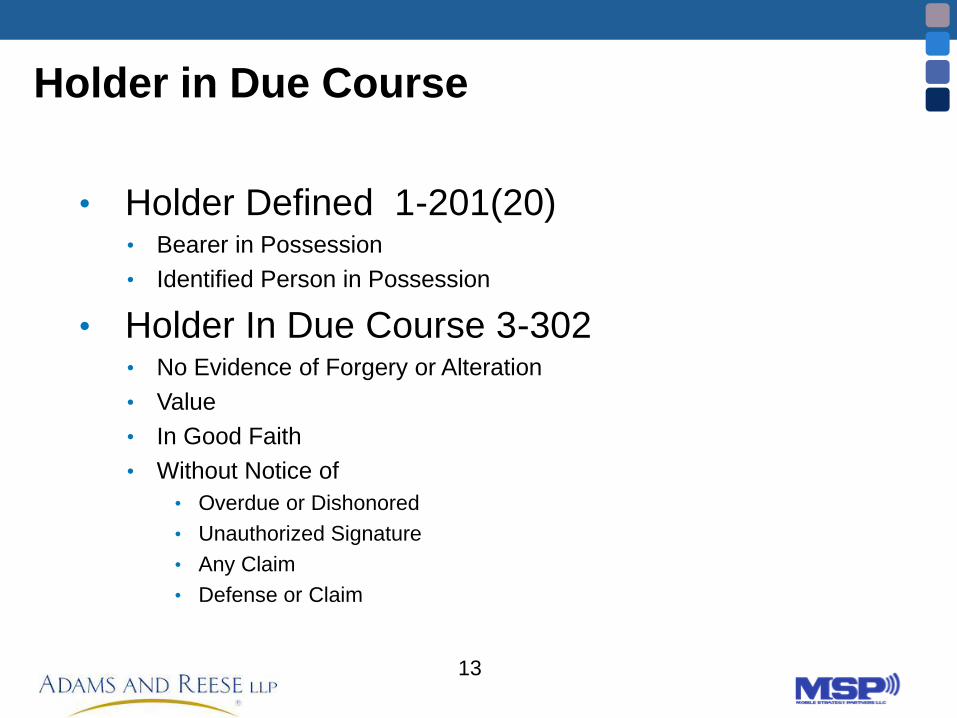

Holder in Due Course

• Holder Defined 1-201(20) • Bearer in Possession

• Identified Person in Possession

• Holder In Due Course 3-302 • No Evidence of Forgery or Alteration

• Value

• In Good Faith

• Without Notice of

• Overdue or Dishonored

• Unauthorized Signature

• Any Claim

• Defense or Claim

13

Holder in Due Course

• Holder In Due Course Takes Free of: • All Claims to the Instrument

• All Defenses

• Holder Not In Due Course Takes Subject to: • Claims to the Instrument

• Defenses

14

Regulation CC Amendment

• 229.34 (g) Depositary Bank Indemnification

• Accepts Remote Deposit Capture Image

• Receives Settlement

• Item not Charged Back

• Indemnifies Other Depositary Bank That

Sustains Loss by Taking Original Check for

Deposit

15

Summary

• RDC duplicates have a growing impact on financial institutions

• Preventing duplicate on-us items from posting

• Reversing duplicates reported by customers

• Identifying duplicates across deposit channels

• Handling incoming adjustments and returns caused by duplicates

• Banks should consider reasonable commercial standards as they

establish their policies and procedures for RDC

• To strengthen their defense in a lawsuit, an RDC bank should:

• Follow their own procedures

• Be in compliance with applicable regulations and guidance

16

About The Presenters

• Paul Carrubba

• Adams and Reese, LLC

• 601-292-0788

• www.arlaw.com

• Mary Hockridge

• Mobile Strategy Partners

• 650-219-4864

• www.mobilestrategypartners.com

18