![Old Wallgrove Road widening (Roberts Road to Wallgrove ... · Old Wallgrove Road [Roberts Road to M7 Interchanges] - Eastern Creek - Urban Design Report and Landscape Character &](https://static.fdocuments.in/doc/165x107/5f068d3b7e708231d4188d5b/old-wallgrove-road-widening-roberts-road-to-wallgrove-old-wallgrove-road-roberts.jpg)

738 - 780 Wallgrove Road Horsley Park NSW 2175 Wetherill ...Mar 21, 2013 · The preceding slides...

24

Brickworks Limited ABN. 17 000 028 526 738 - 780 Wallgrove Road Horsley Park NSW 2175 PO Box 6550 Wetherill Park NSW 1851 Tel +61 2 9830 7800 Fax +61 2 9620 1328 [email protected] www.brickworks.com.au 21 March 2013 Australian Securities Exchange Attention: Companies Department BY ELECTRONIC LODGEMENT Dear Sir/Madam, Please find attached a presentation and additional comments to be presented to analysts today regarding Brickworks’ investment in SOL, for immediate release to the market. Yours faithfully, BRICKWORKS LIMITED IAIN THOMPSON COMPANY SECRETARY For personal use only

Transcript of 738 - 780 Wallgrove Road Horsley Park NSW 2175 Wetherill ...Mar 21, 2013 · The preceding slides...

Brickworks Limited

ABN. 17 000 028 526

738 - 780 Wallgrove Road

Horsley Park NSW 2175

PO Box 6550

Wetherill Park NSW 1851

Tel +61 2 9830 7800

Fax +61 2 9620 1328

www.brickworks.com.au

21 March 2013

Australian Securities Exchange

Attention: Companies Department

BY ELECTRONIC LODGEMENT

Dear Sir/Madam,

Please find attached a presentation and additional comments to be presented

to analysts today regarding Brickworks’ investment in SOL, for immediate release

to the market.

Yours faithfully,

BRICKWORKS LIMITED

IAIN THOMPSON

COMPANY SECRETARY

For

per

sona

l use

onl

y

1

For

per

sona

l use

onl

y

Good Afternoon Ladies and Gentlemen, Following my presentation to Brickworks shareholders at our 2012 Annual General Meeting, the Board considered it appropriate for me to elaborate on Brickworks successful investment in Washington H Soul Pattinson (which I shall abbreviate to ‘SOL’ in this presentation). Today I will discuss what our investment in SOL is and the benefits it provides Brickworks. In light of recent media speculation, I will take you through the process that we conduct to review this investment as well as our current conclusions. I will then take any questions after that.

2

For

per

sona

l use

onl

y

Firstly – what is Brickworks investment in SOL?

3

For

per

sona

l use

onl

y

SOL is a company listed on the ASX, with a current equity capitalisation of approximately $3.3 billion. SOL is an investment conglomerate. By that I mean that its strategy is to invest in a range of listed and unlisted companies – to create a diversified portfolio yielding both capital growth and dividend income. SOL’s most significant current investment is 60% of New Hope Corporation, a top [100] ASX listed coal company – which has an equity market capitalisation of approximately $3.3 billion. SOL also has material investments in the $2 billion TPG Telecom as well as other listed companies like API, Ruralco and Clover. Also relevant to you as shareholders, SOL owns 45.5% of Brickworks. Brickworks first invested in SOL in 1969. Over time, Brickworks spent about $28 million to amass a 42.7% interest in SOL. This shareholding is now worth nearly $1.5 billion. This is more than 50-times our original investment. Additionally, over the 44 years of our investment, Brickworks has always received a dividend from SOL.

4

For

per

sona

l use

onl

y

Brickworks has a current equity market capitalisation of about $1.9 billion and approximately $300m of debt. Therefore, the total value of our enterprise is $2.2 billion. With our shareholding in SOL currently valued at $1.5 billion, this makes it worth about two-thirds of our total value. So, while the market generally categorises Brickworks as a “Building Products” company – that is not really correct. Like SOL, Brickworks is really an investment conglomerate – but with more direct investment in Building Products and Land.

5

For

per

sona

l use

onl

y

I have touched on the enormous capital growth we have received from our ownership in SOL. Now I want to explain some of the other benefits to you.

6

For

per

sona

l use

onl

y

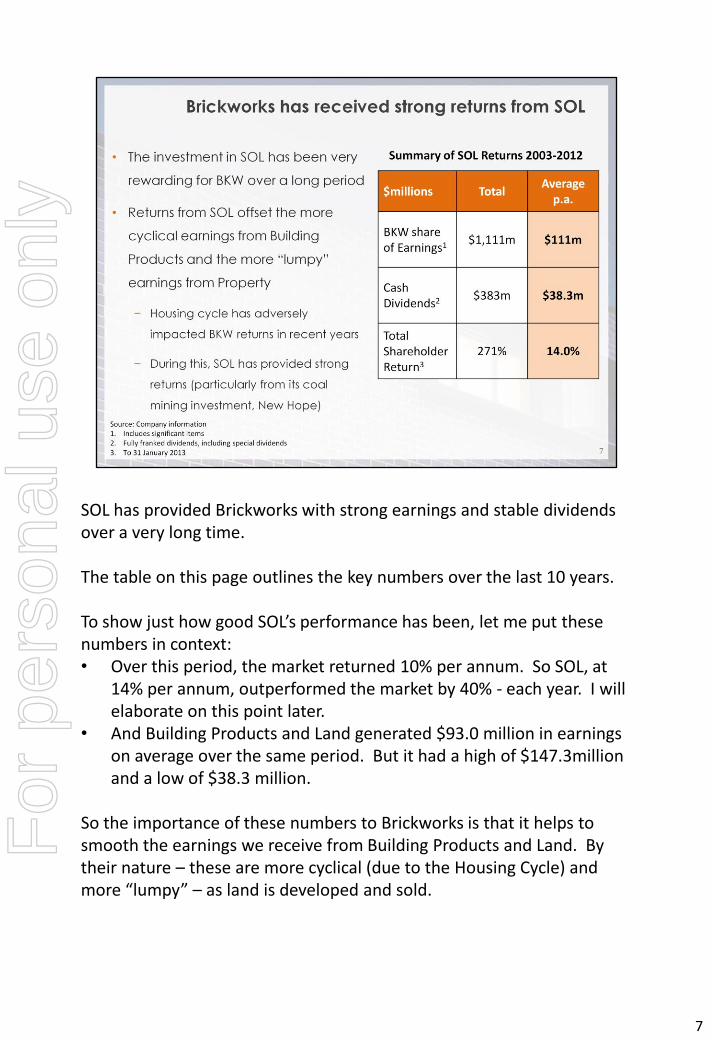

SOL has provided Brickworks with strong earnings and stable dividends over a very long time. The table on this page outlines the key numbers over the last 10 years. To show just how good SOL’s performance has been, let me put these numbers in context: • Over this period, the market returned 10% per annum. So SOL, at

14% per annum, outperformed the market by 40% - each year. I will elaborate on this point later.

• And Building Products and Land generated $93.0 million in earnings on average over the same period. But it had a high of $147.3million and a low of $38.3 million.

So the importance of these numbers to Brickworks is that it helps to smooth the earnings we receive from Building Products and Land. By their nature – these are more cyclical (due to the Housing Cycle) and more “lumpy” – as land is developed and sold.

7

For

per

sona

l use

onl

y

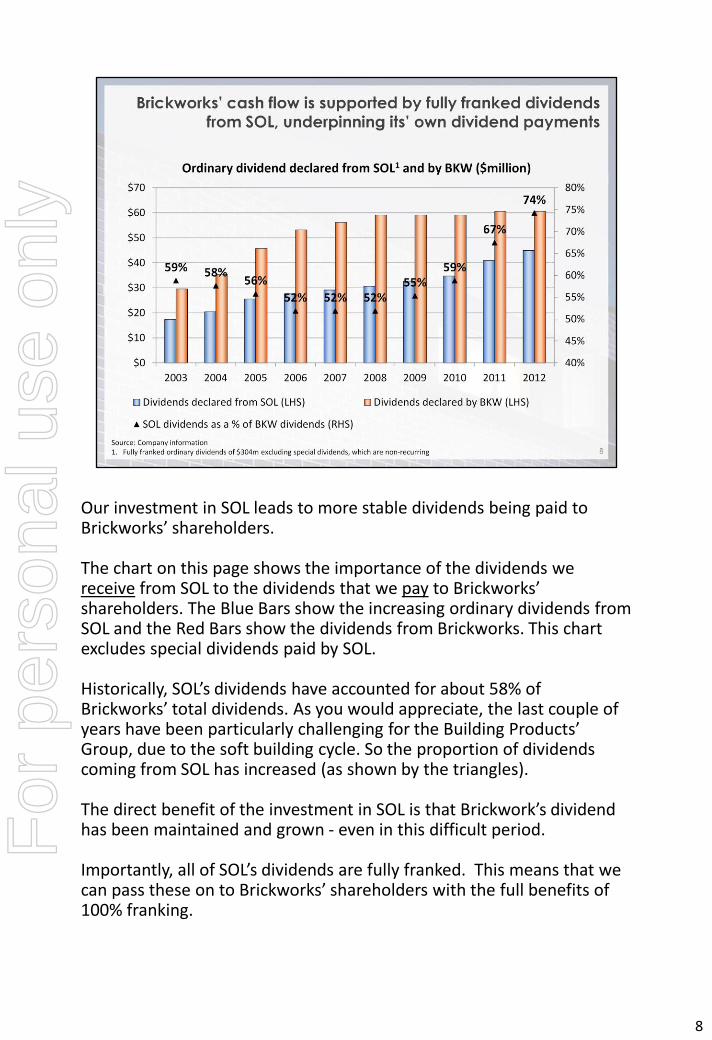

Our investment in SOL leads to more stable dividends being paid to Brickworks’ shareholders. The chart on this page shows the importance of the dividends we receive from SOL to the dividends that we pay to Brickworks’ shareholders. The Blue Bars show the increasing ordinary dividends from SOL and the Red Bars show the dividends from Brickworks. This chart excludes special dividends paid by SOL. Historically, SOL’s dividends have accounted for about 58% of Brickworks’ total dividends. As you would appreciate, the last couple of years have been particularly challenging for the Building Products’ Group, due to the soft building cycle. So the proportion of dividends coming from SOL has increased (as shown by the triangles). The direct benefit of the investment in SOL is that Brickwork’s dividend has been maintained and grown - even in this difficult period. Importantly, all of SOL’s dividends are fully franked. This means that we can pass these on to Brickworks’ shareholders with the full benefits of 100% franking.

8

For

per

sona

l use

onl

y

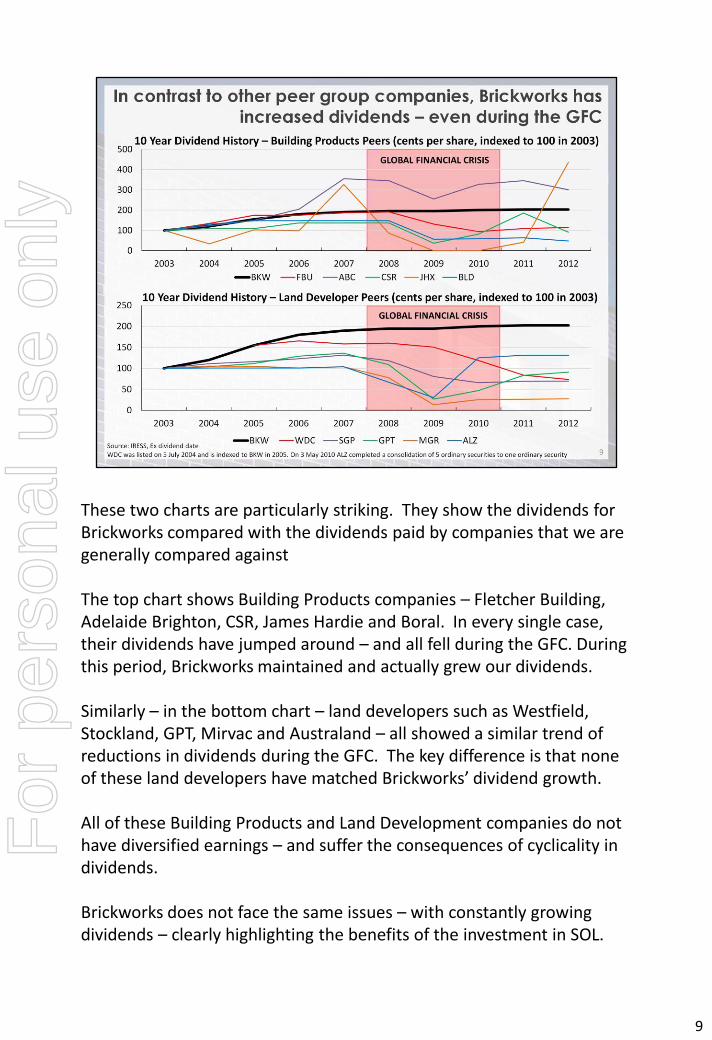

These two charts are particularly striking. They show the dividends for Brickworks compared with the dividends paid by companies that we are generally compared against The top chart shows Building Products companies – Fletcher Building, Adelaide Brighton, CSR, James Hardie and Boral. In every single case, their dividends have jumped around – and all fell during the GFC. During this period, Brickworks maintained and actually grew our dividends. Similarly – in the bottom chart – land developers such as Westfield, Stockland, GPT, Mirvac and Australand – all showed a similar trend of reductions in dividends during the GFC. The key difference is that none of these land developers have matched Brickworks’ dividend growth. All of these Building Products and Land Development companies do not have diversified earnings – and suffer the consequences of cyclicality in dividends. Brickworks does not face the same issues – with constantly growing dividends – clearly highlighting the benefits of the investment in SOL.

9

For

per

sona

l use

onl

y

Whilst dividends are important to shareholders, so is the share price. Long term investors generally want stability and growth – not to have extreme highs and lows – particularly in a short time period. This chart highlights the low volatility of Brickworks share price versus our key listed Building Product peer companies. In this, the broader ASX market performance is benchmarked to 1.0. As you can see, other Building Product companies react more than the market – as their volatility measure is greater than the Market. This means they go up more in good times and go down more in bad times. In contrast, Brickworks’ volatility is less than 1.0. This means that our share price does not get the same “peaks and troughs” as the market or other Building Products companies. Investors generally regard this kind of performance as “defensive” – meaning that they see it as having a lower risk of losing capital.

10

For

per

sona

l use

onl

y

The preceding slides outline why Brickworks is a much less risky investment proposition than the market – or our peer companies in Building Products and Land Development. The importance of this for you as shareholders is that it enables Brickworks to take a longer-term perspective than some other companies that are more at the whim of market fluctuations. This is very important in long-life businesses like brick manufacturing. To succeed in the longer term – as Brickworks has done since our formation in 1934 during the Great Depression – requires time to innovate. Value cannot be properly maximised if you are forced to make knee-jerk reaction to short term circumstances that will not persist longer term. Brickworks structure means that we are better placed to ride out the lows of the cycles – as we are facing in our Building Products business – so we can enjoy the highs – to the maximum. This long-term investment philosophy is fundamental to all we do at Brickworks.

11

For

per

sona

l use

onl

y

The outcomes of this long-term and low-risk philosophy is clearly demonstrated in these two graphs. Firstly – Brickworks (shown as the dark black line) is less volatile than our peers – with Building Products on the top chart and Land Developers on the bottom. Secondly – Brickworks performs well against all these peers. The ones doing better are Fletcher Building (which we have broadly tracked since the GFC) and Adelaide Brighton (which has a large construction materials arm that has benefited from the resources boom).

12

For

per

sona

l use

onl

y

The net result of Brickworks’ strategy, including our investment in SOL, is shown on this page. The results are very clear. Brickworks has outperformed the market in the short term, the medium term and the long term.

13

For

per

sona

l use

onl

y

14

For

per

sona

l use

onl

y

There has been a lot of press conjecture about Brickworks’ structure – including our investment in SOL. From the preceding pages – you will see that this has performed well – indeed we have outperformed on nearly every level. However, the Board and management will never rest on our laurels. We are continuously refining and reviewing our strategy. At a minimum, this is done annually – with a two day strategy review of each and every division. This happened again in February this year – with a substantial Strategy Review document – plus many of supporting management presentations. We have a great team of internal executives who prepare this work – supplemented by external experts as required. And this is not just a once a year exercise. At each and every board and committee meeting (of which there are 11 in total each year), our performance and strategy is scrutinised by your Directors.

15

For

per

sona

l use

onl

y

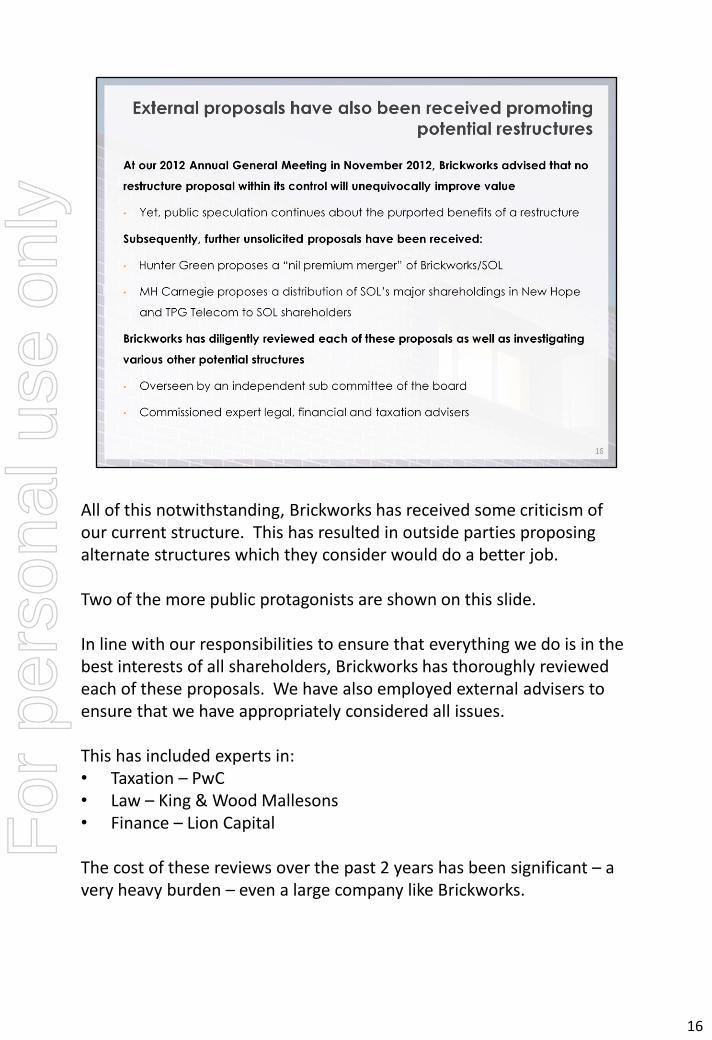

All of this notwithstanding, Brickworks has received some criticism of our current structure. This has resulted in outside parties proposing alternate structures which they consider would do a better job. Two of the more public protagonists are shown on this slide. In line with our responsibilities to ensure that everything we do is in the best interests of all shareholders, Brickworks has thoroughly reviewed each of these proposals. We have also employed external advisers to ensure that we have appropriately considered all issues. This has included experts in: • Taxation – PwC • Law – King & Wood Mallesons • Finance – Lion Capital The cost of these reviews over the past 2 years has been significant – a very heavy burden – even a large company like Brickworks.

16

For

per

sona

l use

onl

y

The independent review of each of the external proposals considered the “pros and cons” of each possible restructure – when compared with the existing structure. This slide outlines some of the key issues, which you can read through, relating to: • The general uncertainty of any uplift in value • Complex taxation issues • Significant cash costs and how they are funded • And the impact of certain shareholder actions We concluded that to date the external proposals simply did not stack up.

17

For

per

sona

l use

onl

y

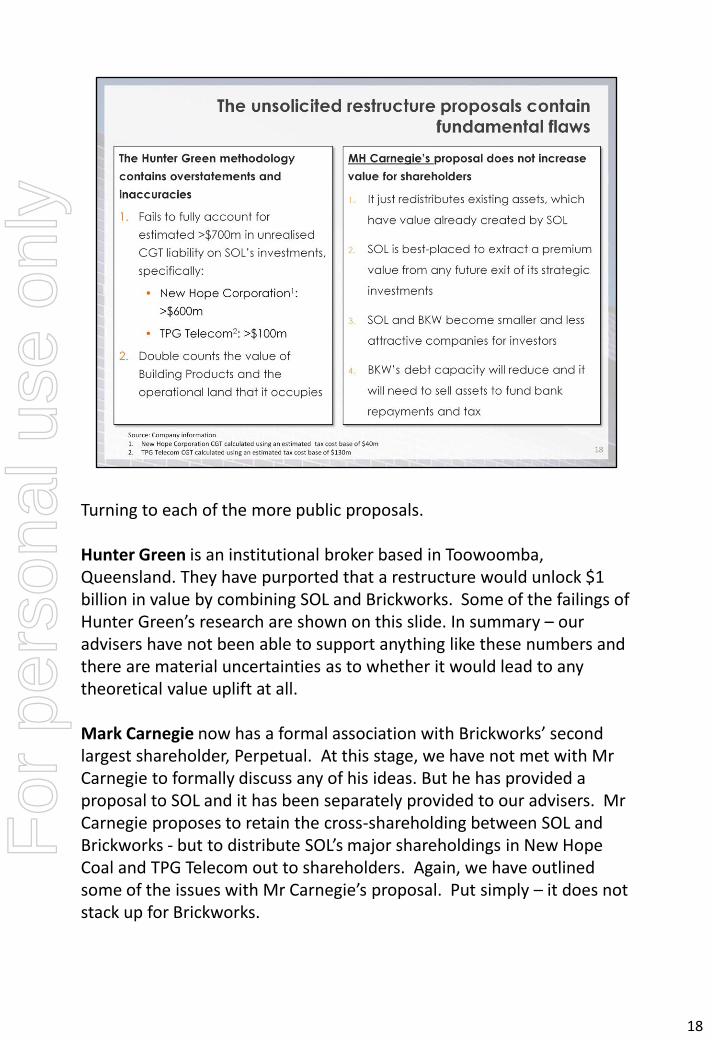

Turning to each of the more public proposals. Hunter Green is an institutional broker based in Toowoomba, Queensland. They have purported that a restructure would unlock $1 billion in value by combining SOL and Brickworks. Some of the failings of Hunter Green’s research are shown on this slide. In summary – our advisers have not been able to support anything like these numbers and there are material uncertainties as to whether it would lead to any theoretical value uplift at all. Mark Carnegie now has a formal association with Brickworks’ second largest shareholder, Perpetual. At this stage, we have not met with Mr Carnegie to formally discuss any of his ideas. But he has provided a proposal to SOL and it has been separately provided to our advisers. Mr Carnegie proposes to retain the cross-shareholding between SOL and Brickworks - but to distribute SOL’s major shareholdings in New Hope Coal and TPG Telecom out to shareholders. Again, we have outlined some of the issues with Mr Carnegie’s proposal. Put simply – it does not stack up for Brickworks.

18

For

per

sona

l use

onl

y

19

For

per

sona

l use

onl

y

Over the past 2 years, the independent directors of Brickworks have assessed numerous potential restructures. The clear and unanimous conclusion is that none of these proposals warrant any further work. I have outlined the key reasons on this slide. We do not see that there is any material value uplift – and that Brickworks is reasonably valued on the ASX when assessed against most broker valuations. Instead, we see a lot of risks and costs in changing the current structure. Indeed, we consider that any restructure will not be in the best interests all Brickworks’ shareholders. This may upset some shareholders, but their agendas and timeframes may not be consistent with the longer-term strategy of Brickworks.

20

For

per

sona

l use

onl

y

The purpose of this presentation is to provide all Brickworks shareholders with some transparency as to what has been happening behind the scenes as reported in numerous media articles. It will now be clear to you that the Board has been acting diligently to ensure that the interests of all shareholders are maximised. We have listened to everyone. We have sought expert independent advice. Nothing that we have seen adds more value in the long term than what we have in place at the moment. The investment in SOL has: • Increased in value by more than $1.4 billion • Provided nearly $400m in fully franked dividends in the last 10 years • Enabled Brickworks to outperform the market across all time periods Brickworks needs our investment in SOL to continue to creating lasting value for our shareholders. There is no better structure or investment that we have seen to date. So we will not be exploring any other restructure options – unless and until it can be clearly proven that they are better than what we currently have.

21

For

per

sona

l use

onl

y

22

I will now take any questions.

For

per

sona

l use

onl

y

23

For

per

sona

l use

onl

y

![Old Wallgrove Road widening (Roberts Road to Wallgrove ... · Old Wallgrove Road [Roberts Road to M7 Interchanges] - Eastern Creek| 3 TABLE OF CONTENTS 60213616 – Concept Design:](https://static.fdocuments.in/doc/165x107/5b2945cb7f8b9af9128b476b/old-wallgrove-road-widening-roberts-road-to-wallgrove-old-wallgrove-road.jpg)