72372073-Chapter-03

72

© 2009 The McGraw-Hill Companies, Inc., All Rights Reserved ADJUSTING ACCOUNTS AND PREPARING FINANCIAL STATEMENTS Chapter 3

-

Upload

ragincajun -

Category

Documents

-

view

48 -

download

0

description

Chapter-03Accounting 1

Transcript of 72372073-Chapter-03

© 2009 The McGraw-Hill Companies, Inc.,

All Rights Reserved

ADJUSTING ACCOUNTS AND PREPARING FINANCIAL STATEMENTS

Chapter 3

McGraw-Hill/Irwin Slide 2McGraw-Hill/Irwin Slide 2

1 2 3 4 5 6 7 8 9 10 11 12

1 2 3 4

Annually

1 2

Monthly

Quarterly

Semiannually

THE ACCOUNTING PERIOD

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

C1

McGraw-Hill/Irwin Slide 3McGraw-Hill/Irwin Slide 3

Accounting

ACCRUAL BASIS VS CASH BASISAccrual Basis

Revenues are recognized when earned and expenses are recognized when incurred.

Cash Basis

Revenues are recognized when cash is received and expenses recorded when cash is paid.

Not GAAPNot GAAP

C2

權責發生基礎 現金基礎收入於賺得時認列 收入於取得現金時認列費用於發生時認列 費用於付出現金時認列一般公認會計原則 非一般公認會計原則

McGraw-Hill/Irwin Slide 4McGraw-Hill/Irwin Slide 4

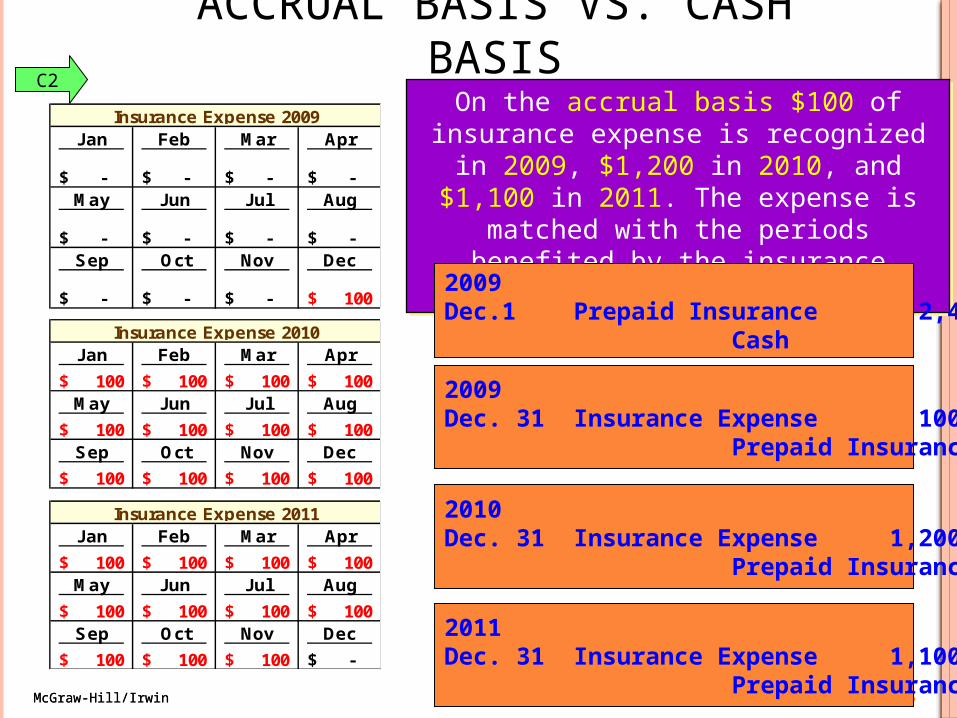

ACCRUAL BASIS VS. CASH BASIS

Example:FastForward paid $2,400 for a 24-month insurancepolicy beginning December 1, 2009.

On the cash basis the entire $2,400 would be recognized

as insurance expense in 2009. No insurance expense

from this policy would be recognized in 2010 or 2011,

periods covered by the policy.

On the cash basis the entire $2,400 would be recognized

as insurance expense in 2009. No insurance expense

from this policy would be recognized in 2010 or 2011,

periods covered by the policy.

Jan Feb Mar Apr

-$ -$ -$ -$ May Jun Jul Aug

-$ -$ -$ -$ Sep Oct Nov Dec

-$ -$ -$ 2,400$

Insurance Expense 2009

C2

Dec. 31 Insurance Expense 2,400 Cash 2,400

Paid a 24-month insurance policy.

McGraw-Hill/Irwin Slide 5McGraw-Hill/Irwin Slide 5

ACCRUAL BASIS VS. CASH BASIS

Jan Feb Mar Apr

-$ -$ -$ -$ May Jun Jul Aug

-$ -$ -$ -$ Sep Oct Nov Dec

-$ -$ -$ 100$

Jan Feb Mar Apr

100$ 100$ 100$ 100$ May Jun Jul Aug

100$ 100$ 100$ 100$ Sep Oct Nov Dec

100$ 100$ 100$ 100$

Jan Feb Mar Apr

100$ 100$ 100$ 100$ May Jun Jul Aug

100$ 100$ 100$ 100$ Sep Oct Nov Dec

100$ 100$ 100$ -$

Insurance Expense 2009

Insurance Expense 2010

Insurance Expense 2011

On the accrual basis $100 of insurance expense is recognized in 2009, $1,200 in 2010, and $1,100 in 2011. The expense is matched with the periods benefited by the

insurance coverage.

On the accrual basis $100 of insurance expense is recognized in 2009, $1,200 in 2010, and $1,100 in 2011. The expense is matched with the periods benefited by the

insurance coverage.

C2

2009Dec. 31 Insurance Expense 100 Prepaid Insurance 100

2009Dec.1 Prepaid Insurance 2,400 Cash 2,400

2010Dec. 31 Insurance Expense 1,200 Prepaid Insurance 1,200

2011Dec. 31 Insurance Expense 1,100 Prepaid Insurance 1,100

McGraw-Hill/Irwin Slide 6McGraw-Hill/Irwin Slide 6

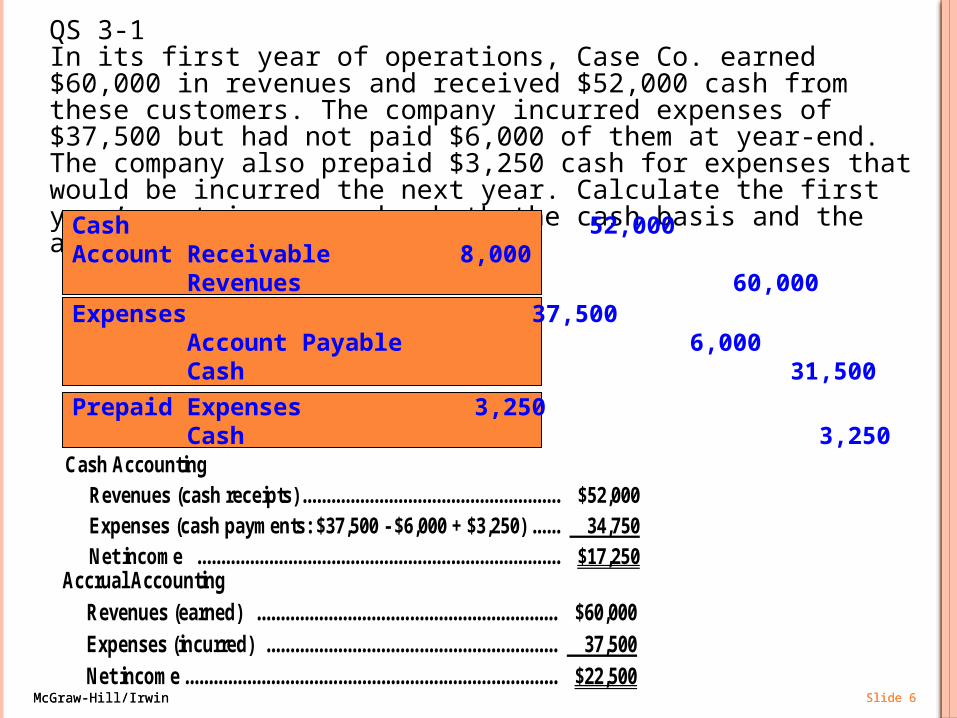

QS 3-1In its first year of operations, Case Co. earned $60,000 in revenues and received $52,000 cash from these customers. The company incurred expenses of $37,500 but had not paid $6,000 of them at year-end. The company also prepaid $3,250 cash for expenses that would be incurred the next year. Calculate the first year’s net income under both the cash basis and the accrual basis of accounting.

Cash 52,000Account Receivable 8,000 Revenues 60,000Expenses 37,500 Account Payable 6,000 Cash 31,500

Prepaid Expenses 3,250 Cash 3,250

Cash Accounting Revenues (cash receipts) ...................................................... $52,000 Expenses (cash payments: $37,500 - $6,000 + $3,250) ...... 34,750 Net income ............................................................................ $17,250 Accrual Accounting Revenues (earned) ............................................................... $60,000 Expenses (incurred) ............................................................. 37,500 Net income .............................................................................. $22,500

McGraw-Hill/Irwin Slide 7McGraw-Hill/Irwin Slide 7

We have delivered theproduct to our customer,

so I think we should recordthe revenue earned.

We have delivered theproduct to our customer,

so I think we should recordthe revenue earned.

RECOGNIZING REVENUES & EXPENSES

Revenue Recognition Principle

C2

McGraw-Hill/Irwin Slide 8McGraw-Hill/Irwin Slide 8

RECOGNIZING REVENUES & EXPENSES

Revenue Recognition PrincipleMatching Principle

Summaryof Expenses

Rent

Gasoline

Advertising

Salaries

Utilities

and . . . .

$1,000

500

2,000

3,000

450

. . . .

Now that we haverecognized the revenue,let’s see what expenses

we incurred togenerate that revenue.

C2

McGraw-Hill/Irwin Slide 9McGraw-Hill/Irwin Slide 9

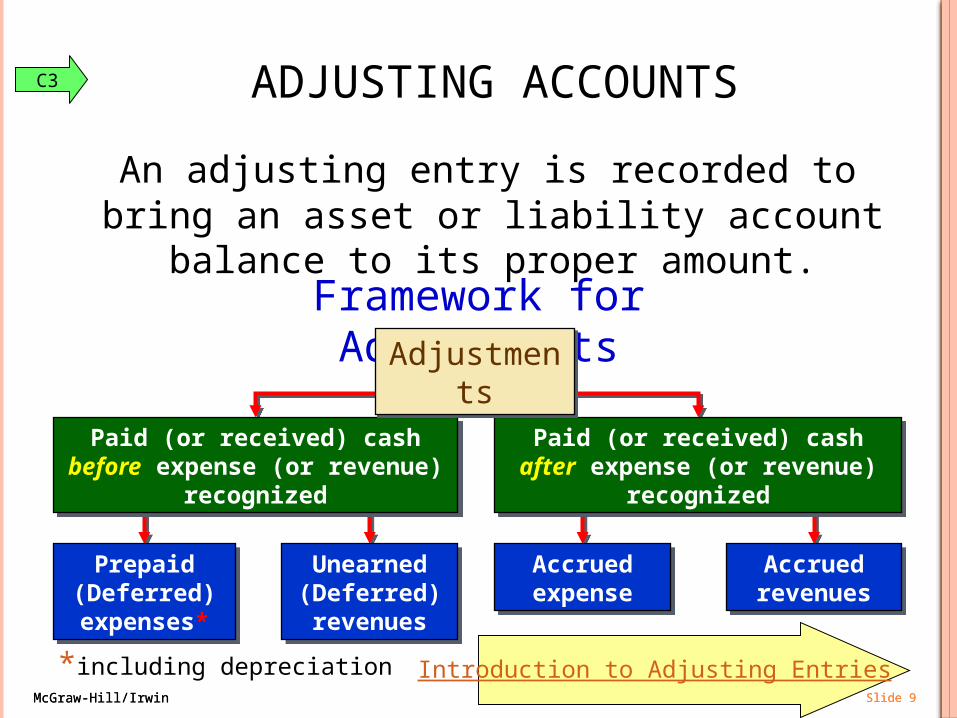

An adjusting entry is recorded to bring an asset or liability account balance to its proper amount.

ADJUSTING ACCOUNTS

Prepaid (Deferred) expenses*

Prepaid (Deferred) expenses*

Unearned (Deferred) revenues

Unearned (Deferred) revenues

AccruedexpenseAccruedexpense

AccruedrevenuesAccruedrevenues

Framework for Adjustments

*including depreciation

Paid (or received) cash before expense (or revenue) recognizedPaid (or received) cash before

expense (or revenue) recognizedPaid (or received) cash after

expense (or revenue) recognizedPaid (or received) cash after

expense (or revenue) recognized

AdjustmentsAdjustments

C3

Introduction to Adjusting Entries

McGraw-Hill/Irwin Slide 10McGraw-Hill/Irwin Slide 10

Here is the checkfor my 24-monthinsurance policy.

Here is the checkfor my 24-monthinsurance policy.

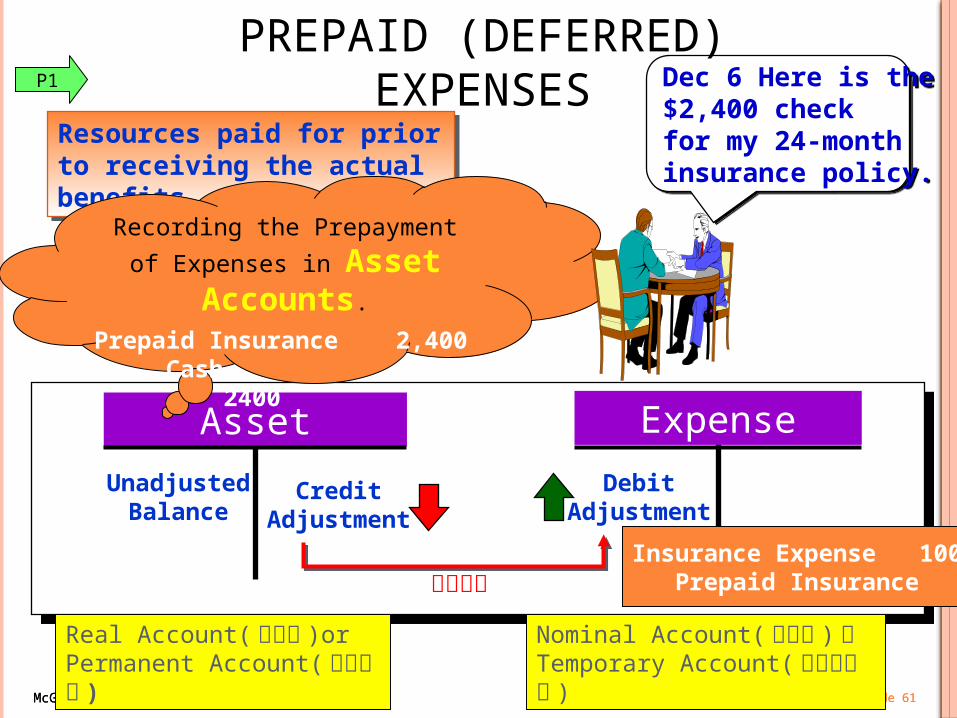

PREPAID (DEFERRED) EXPENSES

Resources paid for prior to receiving the actual benefits.Resources paid for prior to receiving the actual benefits.

CreditAdjustment

DebitAdjustment

P1

Expense

UnadjustedBalance

Asset

Real Account( 實帳戶 )or Permanent Account( 久性帳戶 )

Nominal Account( 虛帳戶 ) 或 Temporary Account( 暫時性帳戶 )

記實轉虛

Recording the Prepayment of

Expenses in Asset Accounts.

Prepaid Insurance XXX Cash XXX

Insurance Expense XXX Prepaid Insurance XXX

McGraw-Hill/Irwin Slide 11McGraw-Hill/Irwin Slide 11

PREPAID INSURANCE On 12/1/09, FastForward paid $2,400 for insurance for 2-

years (24-months, December 2009 through November 2011). FastForward recorded the expenditure as Prepaid

Insurance on 12/1/09. What adjustment is required?

On 12/1/09, FastForward paid $2,400 for insurance for 2-years (24-months, December 2009 through November

2011). FastForward recorded the expenditure as Prepaid Insurance on 12/1/09.

What adjustment is required?

Dec. 31 Insurance Expense 100 Prepaid Insurance 100

To record first month's expired insurance

Dec. 1 2,400 Dec. 31 100Bal. 2,300

Prepaid Insurance 637Dec. 31 100

Insurance Expense 128

P1

2009Dec.1 Prepaid Insurance 2,400 Cash 2,400

McGraw-Hill/Irwin Slide 12McGraw-Hill/Irwin Slide 12

On November 1, 2007, a company paid a $15,300 premium on a 36-month insurance policy for coverage beginning on that date. Refer to that policy and fill in the blanks in the following table.

EXERCISE 3-7(p.117)

15,300

0

0

0

15,300

15,300/36=425/per month

850

5,100

5,100

4,250

15,300

0

0

0

0

14,450

9,350

4,250

0

2007Nov.1 Prepaid Insurance 15,300 Cash 15,300

McGraw-Hill/Irwin Slide 13McGraw-Hill/Irwin Slide 13

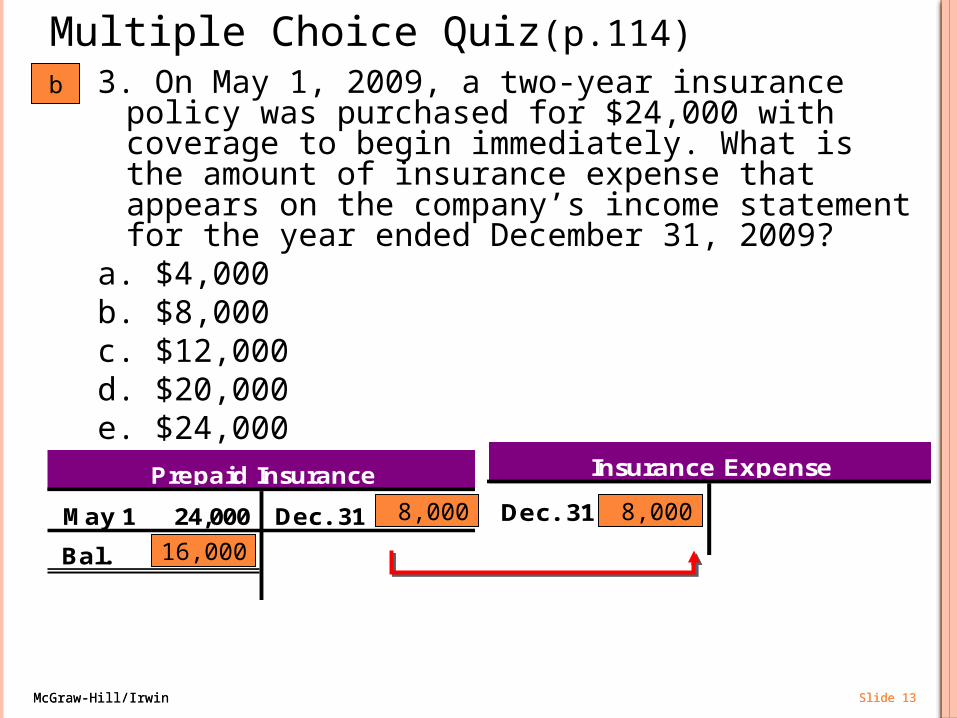

Multiple Choice Quiz(p.114)3. On May 1, 2009, a two-year insurance policy was

purchased for $24,000 with coverage to begin immediately. What is the amount of insurance expense that appears on the company’s income statement for the year ended December 31, 2009?

a. $4,000b. $8,000c. $12,000d. $20,000e. $24,000

b

May 1 24,000 Dec. 31

Bal.

Prepaid Insurance 637

Dec. 31

Insurance Expense 128

8,000 8,000

16,000

McGraw-Hill/Irwin Slide 14McGraw-Hill/Irwin Slide 14

SUPPLIES During 2009, FastForward purchased $9,720 of supplies. FastForward recorded the expenditures in the asset account,

“Supplies.” On December 31, 2009, a count of the supplies indicated $8,670 on hand, so $1,050 of supplies were used during December.

What adjustment is required?

During 2009, FastForward purchased $9,720 of supplies. FastForward recorded the expenditures in the asset account,

“Supplies.” On December 31, 2009, a count of the supplies indicated $8,670 on hand, so $1,050 of supplies were used during December.

What adjustment is required?

Dec. 31 Supplies Expense 1,050 Supplies 1,050

To record supplies used during 2009

Bought 9,720 Dec. 31 1,050Bal. 8,670

Supplies 126Dec. 31 1,050

Supplies Expense 652

P1

2009 Supplies 9,720 Cash 9,720

McGraw-Hill/Irwin Slide 15McGraw-Hill/Irwin Slide 15

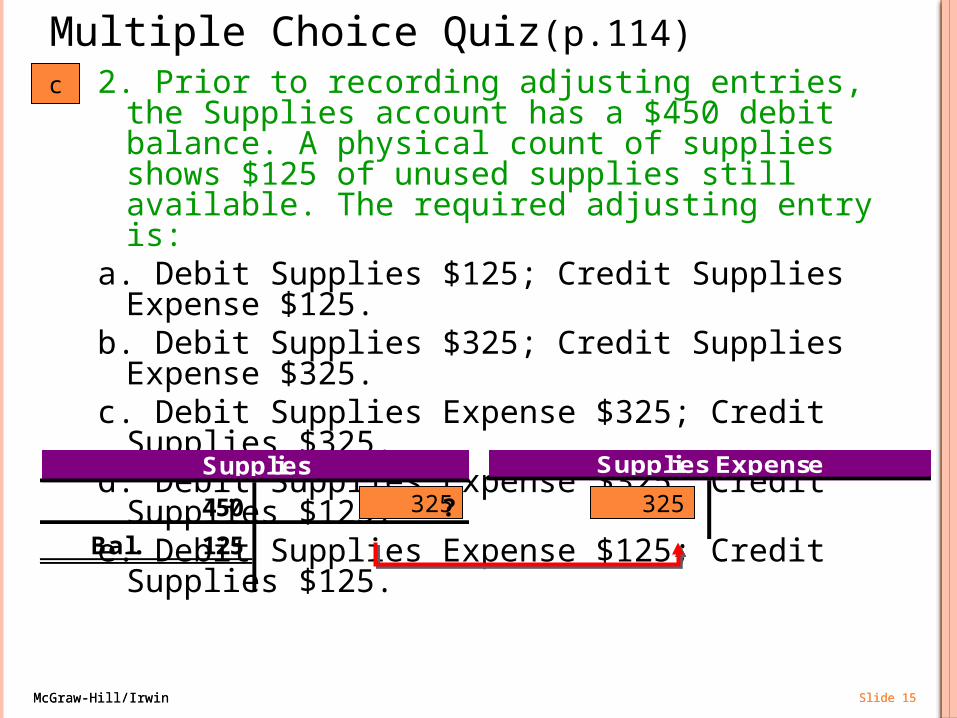

Multiple Choice Quiz(p.114)2. Prior to recording adjusting entries, the Supplies

account has a $450 debit balance. A physical count of supplies shows $125 of unused supplies still available. The required adjusting entry is:

a. Debit Supplies $125; Credit Supplies Expense $125.b. Debit Supplies $325; Credit Supplies Expense $325.c. Debit Supplies Expense $325; Credit Supplies $325.d. Debit Supplies Expense $325; Credit Supplies $125.e. Debit Supplies Expense $125; Credit Supplies $125.

c

450 ?

Bal. 125

Supplies 126 Supplies Expense 652

325 325

McGraw-Hill/Irwin Slide 16McGraw-Hill/Irwin Slide 16

OTHER PREPAID EXPENSES

1. Other prepaid expenses, such as Prepaid Rent, are accounted for exactly as Insurance and Supplies.

2. We should note that some prepaid expenses are both paid for and fully used up within a single period.

3. For example, a company may pay monthly rent on the first day of each month. This payment creates a prepaid expense on the first day of the month that fully expires by the end of the month.

4. In these special cases, we can record the cash paid with a debit to the expense account instead of an asset account.

1. Other prepaid expenses, such as Prepaid Rent, are accounted for exactly as Insurance and Supplies.

2. We should note that some prepaid expenses are both paid for and fully used up within a single period.

3. For example, a company may pay monthly rent on the first day of each month. This payment creates a prepaid expense on the first day of the month that fully expires by the end of the month.

4. In these special cases, we can record the cash paid with a debit to the expense account instead of an asset account.

P1

McGraw-Hill/Irwin Slide 17McGraw-Hill/Irwin Slide 17

Straight-LineDepreciationExpense

= Asset Cost - Salvage Value

Useful Life

DEPRECIATION

Depreciation is the process of allocating the cost of a plant asset over its useful life in a

systematic and rational manner.

P1

McGraw-Hill/Irwin Slide 18McGraw-Hill/Irwin Slide 18

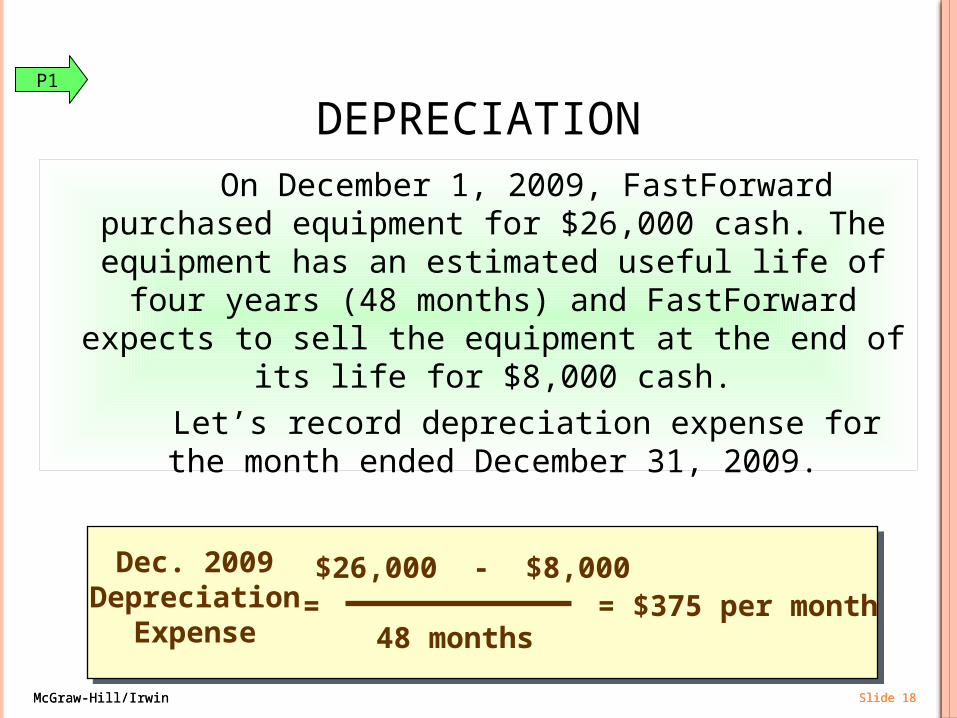

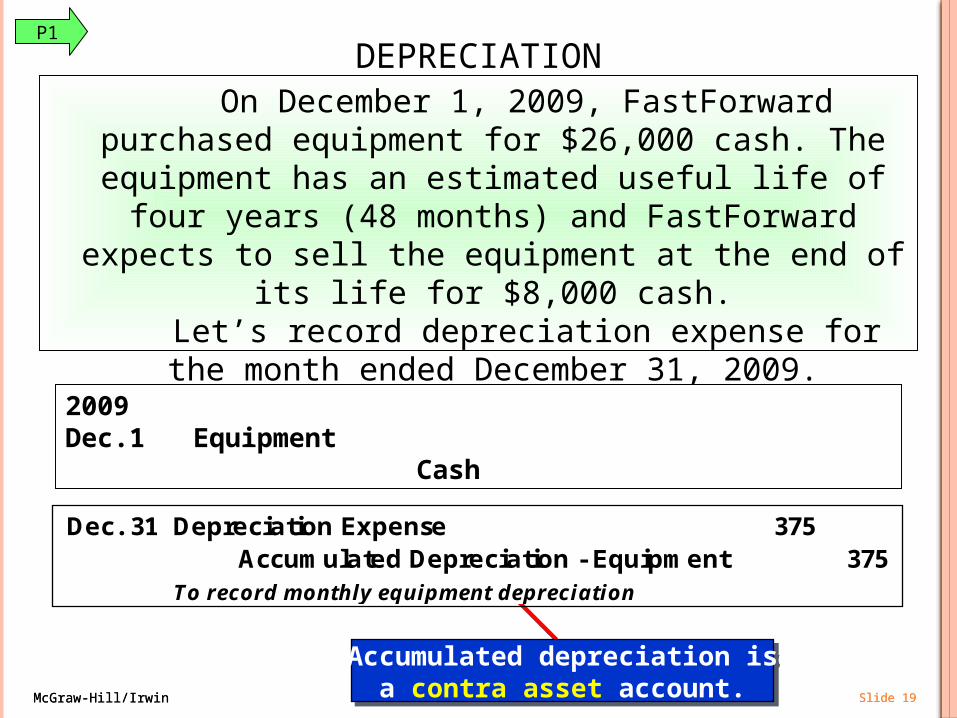

DEPRECIATION On December 1, 2009, FastForward purchased equipment for $26,000 cash. The equipment has an estimated useful life of four years (48 months) and

FastForward expects to sell the equipment at the end of its life for $8,000 cash.

Let’s record depreciation expense for the month ended December 31, 2009.

Dec. 2009Depreciation

Expense=

$26,000 - $8,000

48 months= $375 per month

P1

McGraw-Hill/Irwin Slide 19McGraw-Hill/Irwin Slide 19

Dec. 31 Depreciation Expense 375 Accumulated Depreciation - Equipment 375

To record monthly equipment depreciation

Accumulated depreciation isa contra asset account.

Accumulated depreciation isa contra asset account.

DEPRECIATION On December 1, 2009, FastForward purchased equipment for $26,000 cash. The equipment has an estimated useful life of four years (48 months) and

FastForward expects to sell the equipment at the end of its life for $8,000 cash.

Let’s record depreciation expense for the month ended December 31, 2009.

P1

2009Dec.1 Equipment 26,000 Cash 26,000

McGraw-Hill/Irwin Slide 20McGraw-Hill/Irwin Slide 20

1/1 26,000 12/31 375

12/31 375

Dr. Cr. Dec. 31 Depreciation Expense 375

Accumulated Depreciation - Equipment 375 To record monthly equipment depreciation

DEPRECIATIONP1

Equipment Depreciation Expense

Accumulated Depreciation

McGraw-Hill/Irwin Slide 21McGraw-Hill/Irwin Slide 21

FastForwardPartial Balance SheetAt December 31, 2009

Assets Cash .Equipment 26,000$ Less: accumulated depreciation (375) 25,625 . .Total Assets

$

DEPRECIATIONP1

Accumulated depreciation isa contra asset account.

Accumulated depreciation isa contra asset account.

Equipment is shown net of accumulated depreciation.

McGraw-Hill/Irwin Slide 22McGraw-Hill/Irwin Slide 22

QS 3-5(p.115)

a. Andrews Company purchases $45,000 of equipment on January 1, 2009. The equipment is expected to last five years and be worth $3,000 at the end of that time. Prepare the entry to record one year’s depreciation expense of $8,400 for the equipment as of December 31, 2009.

a. Depreciation Expense—Equipment 8,400 Accumulated Depreciation—Equipment 8,400

To record depreciation expense for the year.($45,000 - $3,000) / 5 years = $8,400

b. No depreciation adjustments are made for land as it is expected to last indefinitely

b. Fortel Company purchases $40,000 of land on January 1, 2009. The land is expected to last indefinitely. What depreciation adjustment, if any, should be made with respect to the Land account as of December 31, 2009?

Straight-LineDepreciationExpense

= Asset Cost - Salvage Value

Useful Life = 8,400=45,000-3,000

5 years

McGraw-Hill/Irwin Slide 23McGraw-Hill/Irwin Slide 23

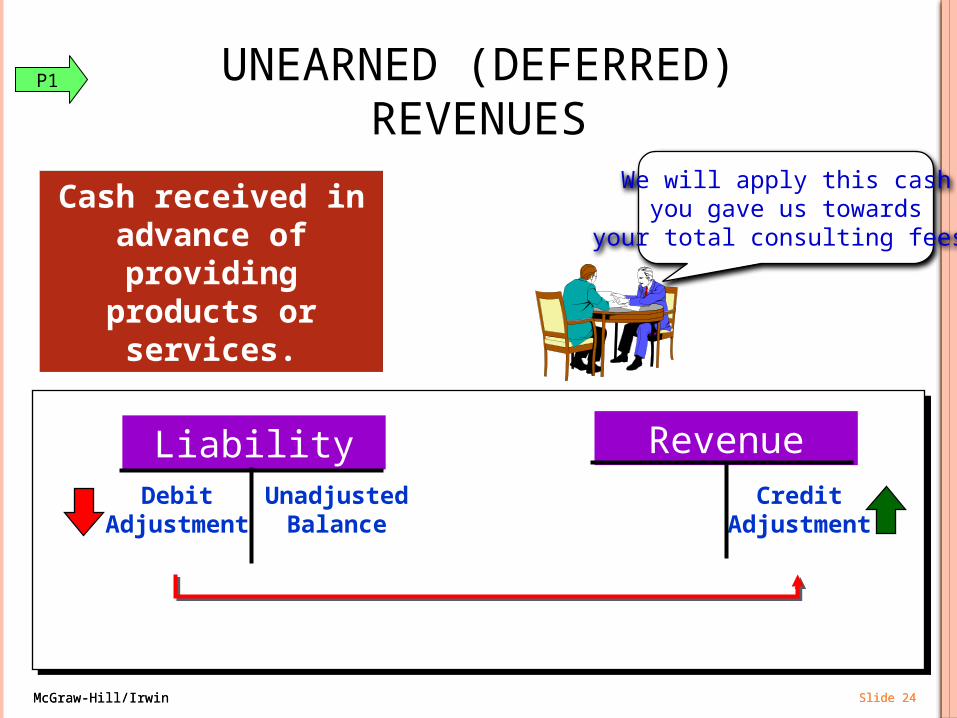

UNEARNED (DEFERRED)REVENUES

We will apply this cashyou gave us towards

your total consulting fees.

We will apply this cashyou gave us towards

your total consulting fees.Cash received in advance of

providing products or services.

P1

UnadjustedBalance

DebitAdjustment

CreditAdjustment

Liability Revenue

Real Account( 實帳戶 )or Permanent Account( 久性帳戶 )

Nominal Account( 虛帳戶 ) 或 Temporary Account( 暫時性帳戶 )

記實轉虛

Recording the Prepayment of Revenues in Liability Accounts.

Cash XXX Unearned Consulting Fee XXX

Unearned Consulting Fee XXX Consulting Revenue XXX

McGraw-Hill/Irwin Slide 24McGraw-Hill/Irwin Slide 24

UNEARNED (DEFERRED)REVENUES

We will apply this cashyou gave us towards

your total consulting fees.

Cash received in advance of providing products or services.

P1

Liability RevenueUnadjusted

BalanceDebit

AdjustmentCredit

Adjustment

McGraw-Hill/Irwin Slide 25McGraw-Hill/Irwin Slide 25

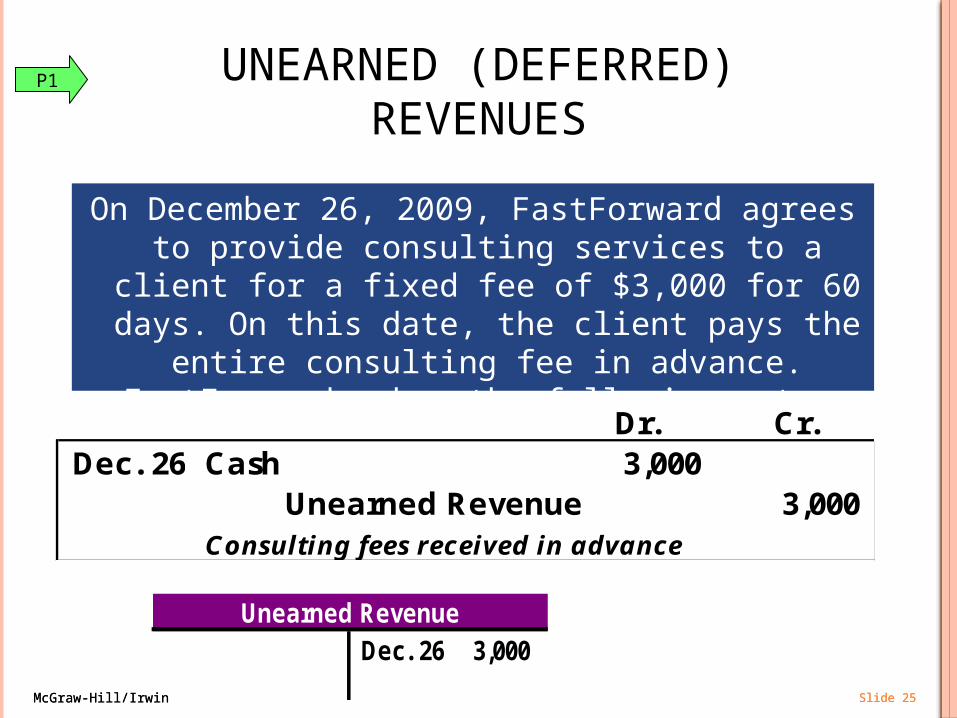

UNEARNED (DEFERRED)REVENUES

On December 26, 2009, FastForward agrees to provide consulting services to a client for a fixed fee of $3,000 for 60 days. On this date, the client pays the entire consulting fee in advance. FastForward

makes the following entry:

Dr. Cr. Dec. 26 Cash 3,000

Unearned Revenue 3,000 Consulting fees received in advance

Dec. 26 3,000Unearned Revenue

P1

McGraw-Hill/Irwin Slide 26McGraw-Hill/Irwin Slide 26

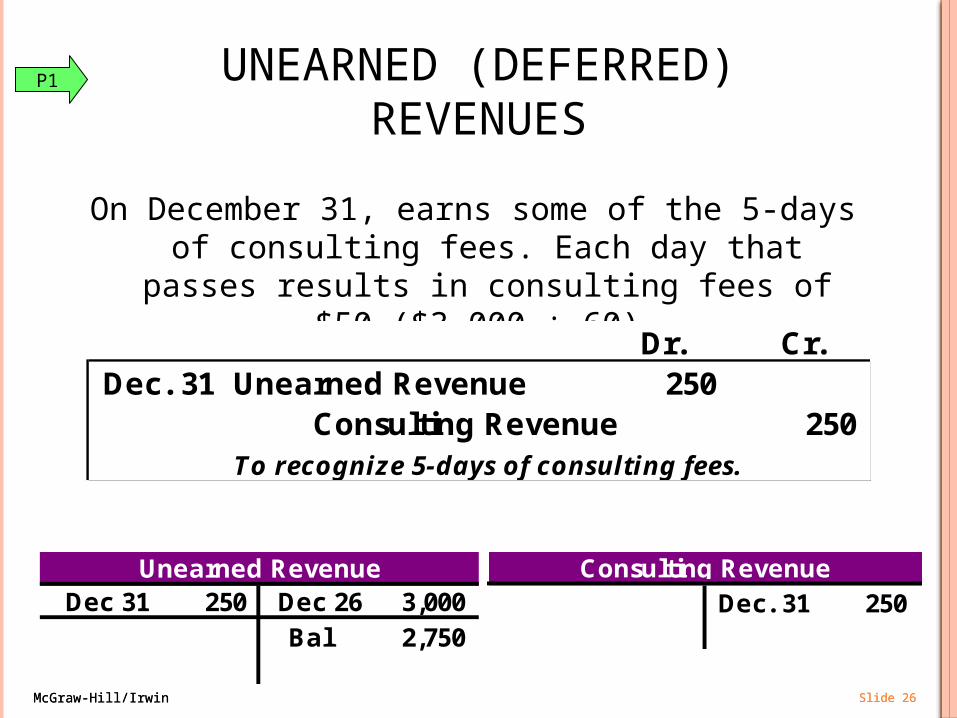

On December 31, earns some of the 5-days of consulting fees. Each day that passes results in

consulting fees of $50 ($3,000 ÷ 60).

Dr. Cr. Dec. 31 Unearned Revenue 250

Consulting Revenue 250 To recognize 5-days of consulting fees.

Dec 31 250 Dec 26 3,000Bal 2,750

Unearned RevenueDec. 31 250

Consulting Revenue

UNEARNED (DEFERRED)REVENUES

P1

McGraw-Hill/Irwin Slide 27McGraw-Hill/Irwin Slide 27

Multiple Choice Quiz(p.114)4. On November 1, 2009, Stockton Co. receives $3,600 cash from

Hans Co. for consulting services to be provided evenly over the period November 1, 2009, to April 30, 2010—at which time Stockton credited $3,600 to Unearned Consulting Fees. The adjusting entry on December 31, 2009 (Stockton’s yearend) would include a

a. Debit to Unearned Consulting Fees for $1,200.b. Debit to Unearned Consulting Fees for $2,400.c. Credit to Consulting Fees Earned for $2,400.d. Debit to Consulting Fees Earned for $1,200.e. Credit to Cash for $3,600.

a

Dec 31 ? Nov 1 3,600Bal

Unearned RevenueDec. 31 ?

Consulting Revenue1,200 1,200

2,400

McGraw-Hill/Irwin Slide 28McGraw-Hill/Irwin Slide 28

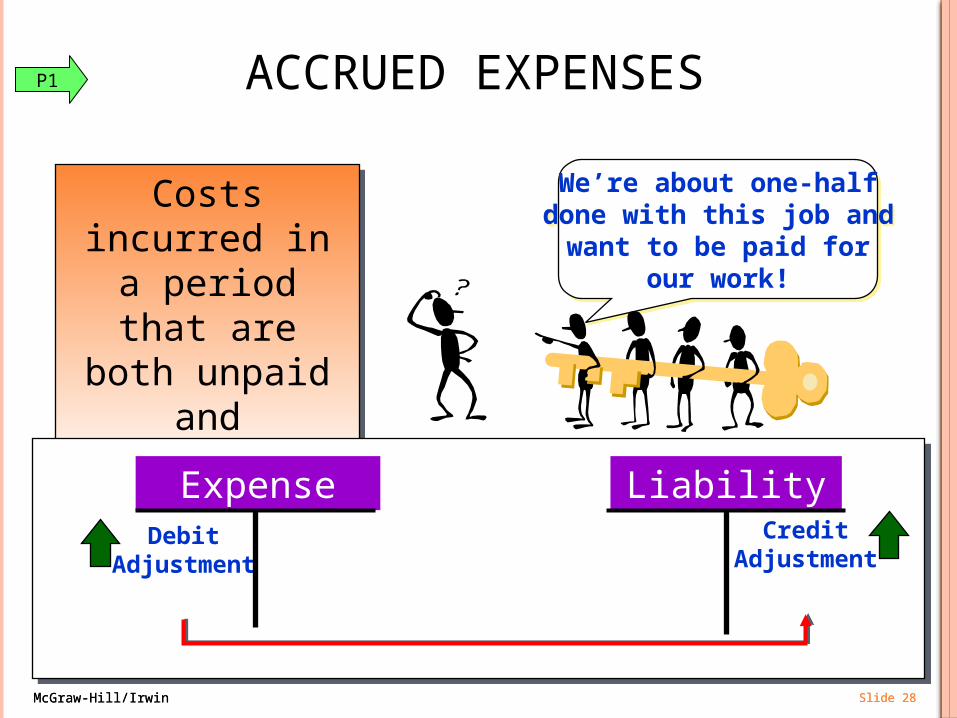

We’re about one-halfdone with this job and

want to be paid forour work!

We’re about one-halfdone with this job and

want to be paid forour work!

Costs incurred in a period that areboth unpaid and

unrecorded.

Costs incurred in a period that areboth unpaid and

unrecorded.

ACCRUED EXPENSES

CreditAdjustment

DebitAdjustment

P1

Expense Liability

McGraw-Hill/Irwin Slide 29McGraw-Hill/Irwin Slide 29

12/31/09Year end

Last paydate

12/26/09

Next paydate

1/9/10

Record adjustingjournal entry.

Record adjustingjournal entry.

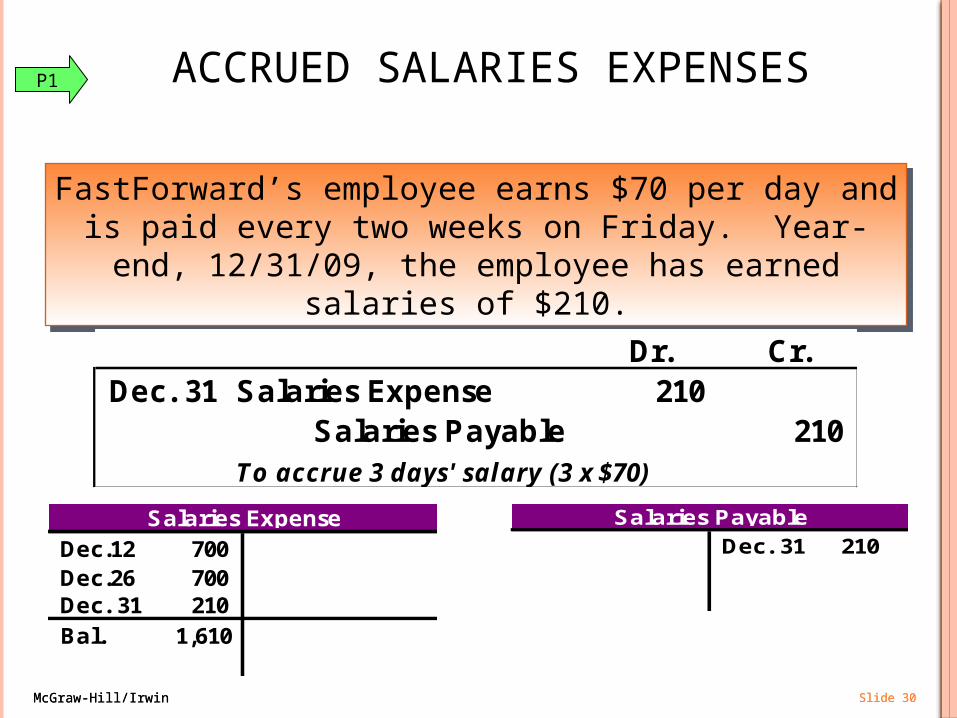

FastForward’s employee earns $70 per day and is paid every two weeks on Friday. Year-end, 12/31/09, falls on a Wednesday. The last payday of 2009, is Friday, 12/26/09.

From 12/26 until year-end is three working days. The employee has earned salaries of $210 for Monday through

Wednesday. They will not be paid until the next Friday.

FastForward’s employee earns $70 per day and is paid every two weeks on Friday. Year-end, 12/31/09, falls on a Wednesday. The last payday of 2009, is Friday, 12/26/09.

From 12/26 until year-end is three working days. The employee has earned salaries of $210 for Monday through

Wednesday. They will not be paid until the next Friday.

ACCRUED SALARIES EXPENSESP1

McGraw-Hill/Irwin Slide 30McGraw-Hill/Irwin Slide 30

Dr. Cr. Dec. 31 Salaries Expense 210

Salaries Payable 210 To accrue 3 days' salary (3 x $70)

Dec.12 700Dec.26 700Dec. 31 210Bal. 1,610

Salaries ExpenseDec. 31 210

Salaries Payable

ACCRUED SALARIES EXPENSES

FastForward’s employee earns $70 per day and is paid every two weeks on Friday. Year-end, 12/31/09, the

employee has earned salaries of $210.

FastForward’s employee earns $70 per day and is paid every two weeks on Friday. Year-end, 12/31/09, the

employee has earned salaries of $210.

P1

McGraw-Hill/Irwin Slide 31McGraw-Hill/Irwin Slide 31

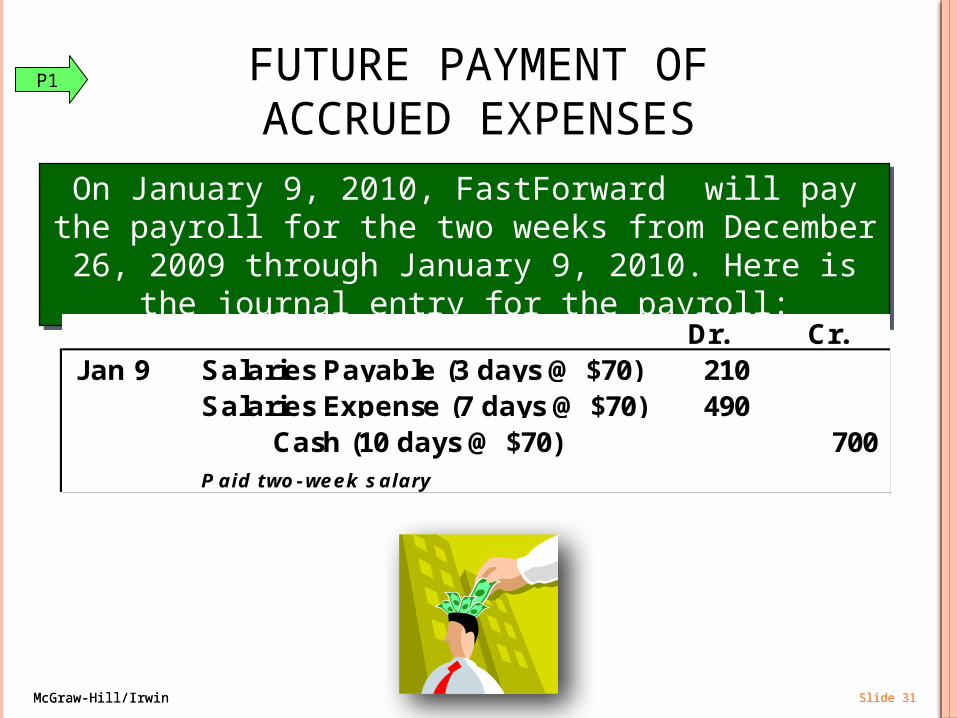

FUTURE PAYMENT OFACCRUED EXPENSES

On January 9, 2010, FastForward will pay the payroll for the two weeks from December 26, 2009 through January

9, 2010. Here is the journal entry for the payroll:

On January 9, 2010, FastForward will pay the payroll for the two weeks from December 26, 2009 through January

9, 2010. Here is the journal entry for the payroll:

Dr. Cr. Jan 9 Salaries Payable (3 days @ $70) 210

Salaries Expense (7 days @ $70) 490 Cash (10 days @ $70) 700

Paid two-week salary

P1

McGraw-Hill/Irwin Slide 32McGraw-Hill/Irwin Slide 32

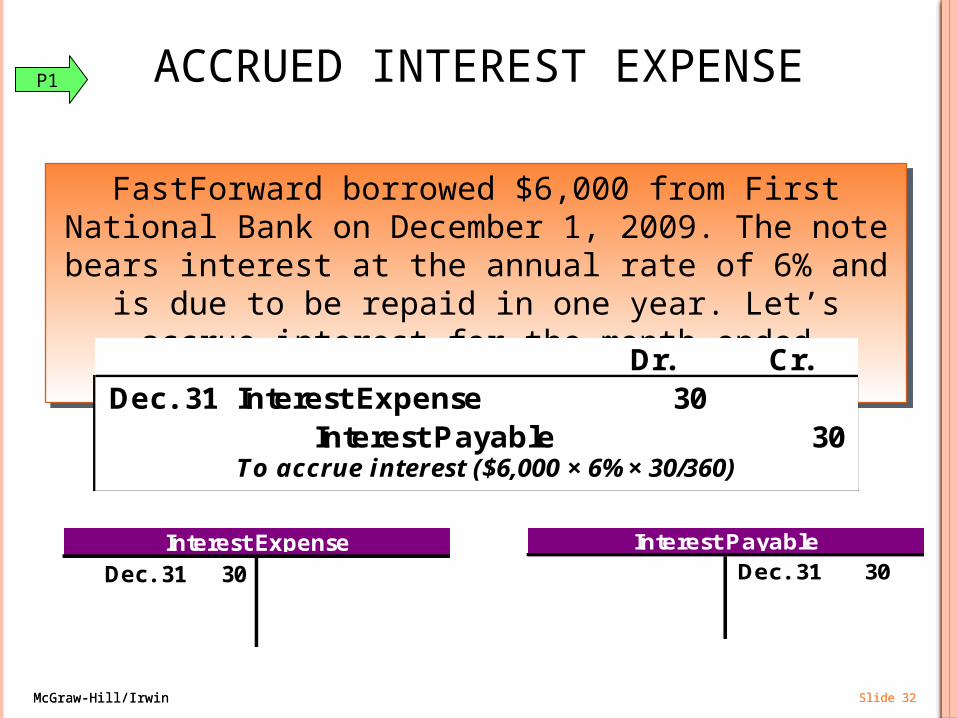

Dr. Cr. Dec. 31 Interest Expense 30

Interest Payable 30 To accrue interest ($6,000 × 6% × 30/360)

Dec. 31 30Interest Expense

Dec. 31 30Interest Payable

ACCRUED INTEREST EXPENSE

FastForward borrowed $6,000 from First National Bank on December 1, 2009. The note bears interest at the annual

rate of 6% and is due to be repaid in one year. Let’s accrue interest for the month ended 12/31/09.

FastForward borrowed $6,000 from First National Bank on December 1, 2009. The note bears interest at the annual

rate of 6% and is due to be repaid in one year. Let’s accrue interest for the month ended 12/31/09.

P1

McGraw-Hill/Irwin Slide 33McGraw-Hill/Irwin Slide 33

EXERCISE 3-6(p.118)

Apr. 30 Legal Fees Expense 4,500Legal Fees Payable 4,500

To record accrued legal fees.

May 12 Legal Fees Payable 4,500Cash 4,500

To pay accrued legal fees.

The following three separate situations require adjusting journal entries to prepare financial statements as of April 30. For each situation, present both the April 30 adjusting entry and the subsequent entry during May to record the payment of the accrued expenses.

a. On April 1, the company retained an attorney at a flat monthly fee of $4,500. This amount is payable on the 12th of the following month.

McGraw-Hill/Irwin Slide 34McGraw-Hill/Irwin Slide 34

EXERCISE 3-6(p.118)

Apr. 30 Interest Expense 1,900Interest Payable 1,900

To record accrued interest expense($5,700 x 10/30).

May 20 Interest Payable 1,900Interest Expense 3,800

Cash 5,700To record payment of accrued and

current interest expense ($5,700 x 20/30).

b. A $760,000 note payable requires $5,700 of interest to be paid at the 20th day of each month. The interest was last paid on April 20 and the next payment is due on May 20. As of April 30, $1,900 of interest expense has accrued.

McGraw-Hill/Irwin Slide 35McGraw-Hill/Irwin Slide 35

EXERCISE 3-6(p.118)

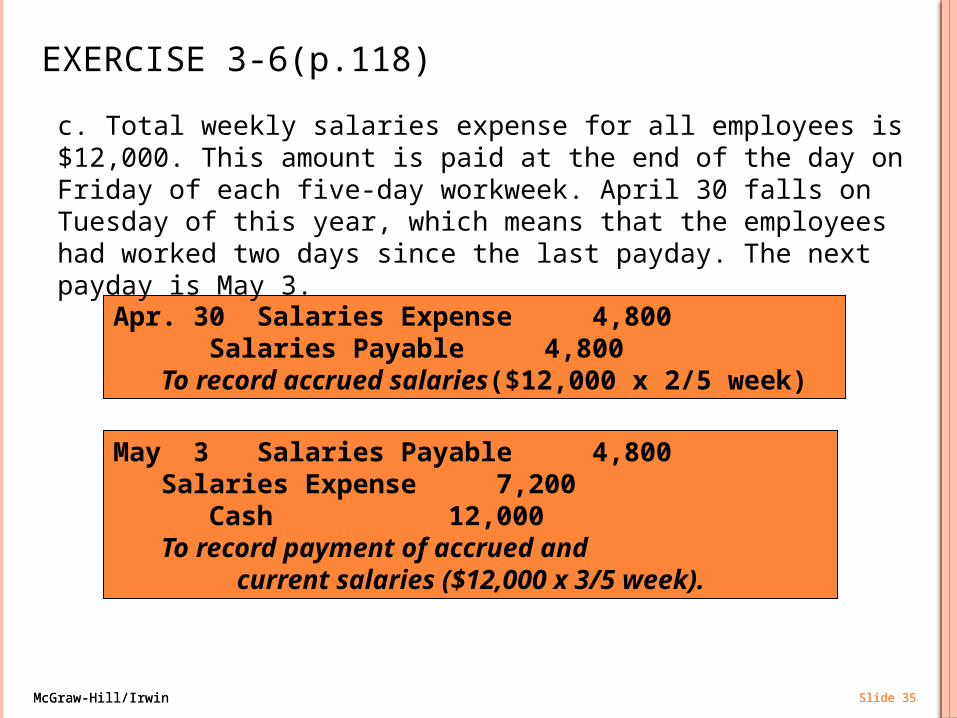

Apr. 30 Salaries Expense 4,800Salaries Payable 4,800

To record accrued salaries($12,000 x 2/5 week)

May 3 Salaries Payable 4,800Salaries Expense 7,200

Cash 12,000To record payment of accrued and

current salaries ($12,000 x 3/5 week).

c. Total weekly salaries expense for all employees is $12,000. This amount is paid at the end of the day on Friday of each five-day workweek. April 30 falls on Tuesday of this year, which means that the employees had worked two days since the last payday. The next payday is May 3.

McGraw-Hill/Irwin Slide 36McGraw-Hill/Irwin Slide 36

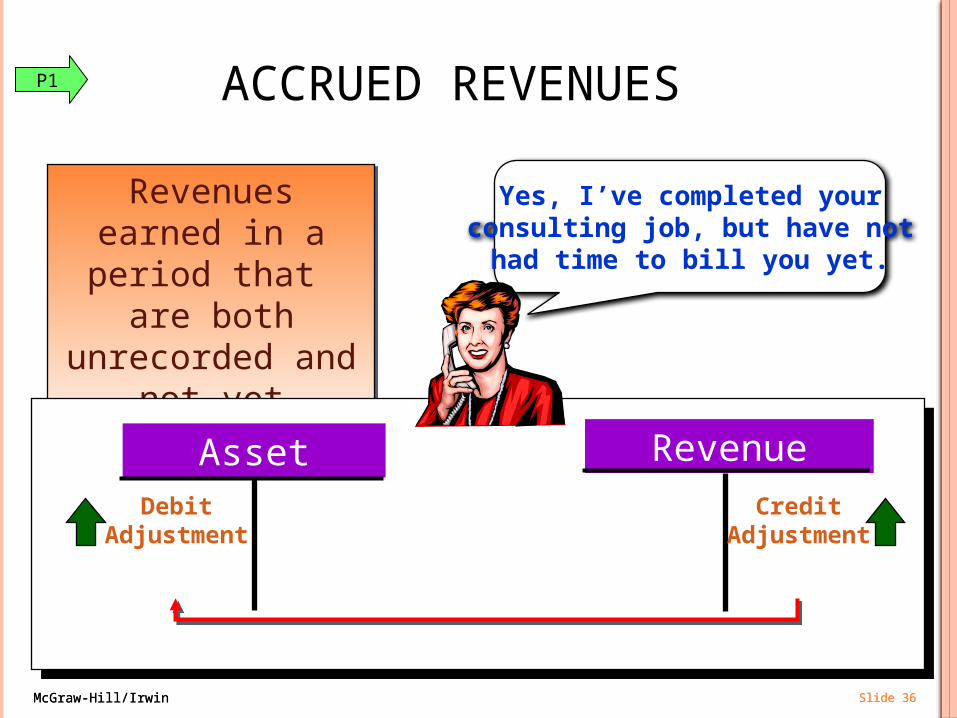

Yes, I’ve completed yourconsulting job, but have not

had time to bill you yet.

ACCRUED REVENUES

Revenues earned in a period that

are both unrecorded and not

yet received.

Revenues earned in a period that

are both unrecorded and not

yet received.

Asset Revenue

CreditAdjustment

DebitAdjustment

P1

McGraw-Hill/Irwin Slide 37McGraw-Hill/Irwin Slide 37

ACCRUED SERVICE REVENUES

On December 12, 2009, Fast Forward agrees to render consulting services under a 30-day fixed fee contract for $2,700 ($90 per day). All services are to be completed by

January 10, 2010, when the client will pay in full.

On December 12, 2009, Fast Forward agrees to render consulting services under a 30-day fixed fee contract for $2,700 ($90 per day). All services are to be completed by

January 10, 2010, when the client will pay in full.

Dr. Cr. Dec. 31 Accounts Receivable 1,800

Consulting Revenue 1,800 To accrue revenue (20-days @ $90 per day)

Other receivables1,900 Receipts 1,900

Dec. 31 1,800Bal. 1,800

Accounts ReceivableOther revenues

6,050 Dec. 31 1,800Bal . 7,850

Consulting Revenue

P1

McGraw-Hill/Irwin Slide 38McGraw-Hill/Irwin Slide 38

FUTURE RECEIPT OFSERVICE REVENUES

On January 10, 2010, FastForward completed its obligation under the consulting contract. The client was billed $2,700 and FastForward received $2,700 in cash

On January 10, 2010, FastForward completed its obligation under the consulting contract. The client was billed $2,700 and FastForward received $2,700 in cash

Dr. Cr. Jan 10 Cash 2,700

Accounts Receivable 1,800 Consulting Revenue 900

To record completion of contract and cash collection

Revenue in January10 days @ $90 = $900

P1

McGraw-Hill/Irwin Slide 39McGraw-Hill/Irwin Slide 39

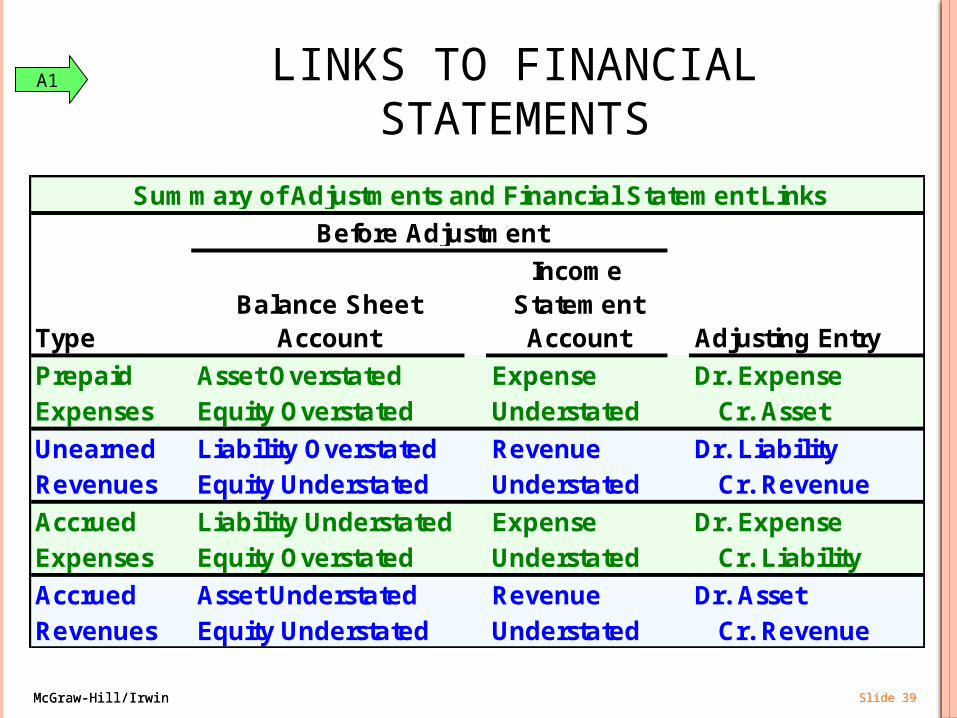

TypeBalance Sheet

Account

IncomeStatementAccount Adjusting Entry

Prepaid Asset Overstated Expense Dr. ExpenseExpenses Equity Overstated Understated Cr. Asset

Unearned Liability Overstated Revenue Dr. LiabilityRevenues Equity Understated Understated Cr. Revenue

Accrued Liability Understated Expense Dr. ExpenseExpenses Equity Overstated Understated Cr. Liability

Accrued Asset Understated Revenue Dr. AssetRevenues Equity Understated Understated Cr. Revenue

Before Adjustment

Summary of Adjustments and Financial Statement Links

LINKS TO FINANCIAL STATEMENTS

A1

McGraw-Hill/Irwin Slide 40McGraw-Hill/Irwin Slide 40

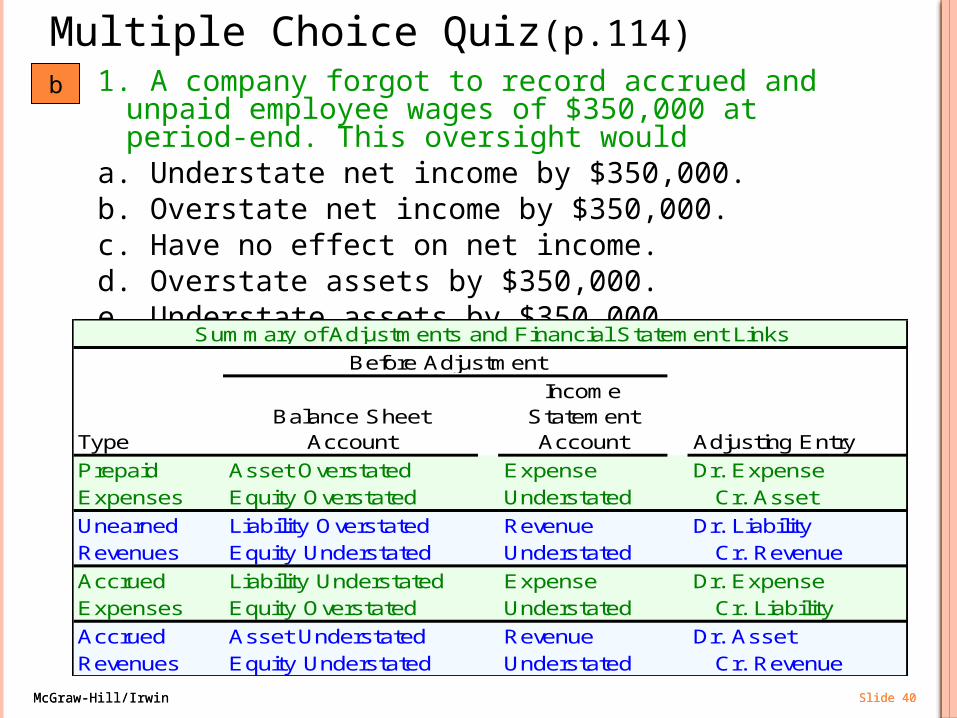

Multiple Choice Quiz(p.114)1. A company forgot to record accrued and unpaid employee

wages of $350,000 at period-end. This oversight woulda. Understate net income by $350,000.b. Overstate net income by $350,000.c. Have no effect on net income.d. Overstate assets by $350,000.e. Understate assets by $350,000.

b

TypeBalance Sheet

Account

IncomeStatementAccount Adjusting Entry

Prepaid Asset Overstated Expense Dr. ExpenseExpenses Equity Overstated Understated Cr. Asset

Unearned Liability Overstated Revenue Dr. LiabilityRevenues Equity Understated Understated Cr. Revenue

Accrued Liability Understated Expense Dr. ExpenseExpenses Equity Overstated Understated Cr. Liability

Accrued Asset Understated Revenue Dr. AssetRevenues Equity Understated Understated Cr. Revenue

Before Adjustment

Summary of Adjustments and Financial Statement Links

McGraw-Hill/Irwin Slide 41McGraw-Hill/Irwin Slide 41

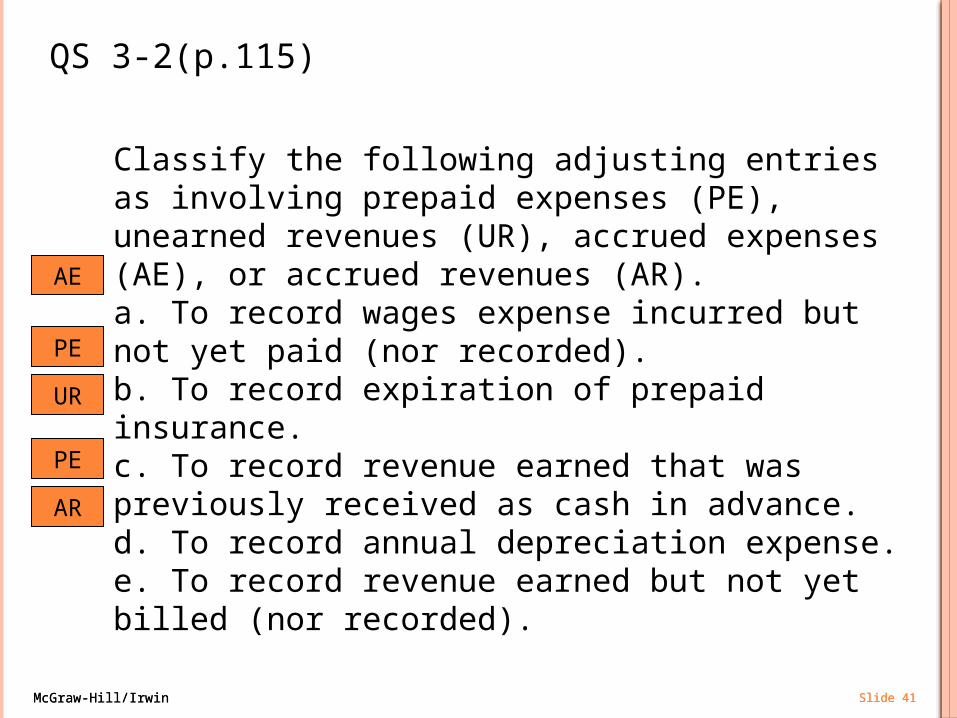

QS 3-2(p.115)

Classify the following adjusting entries as involving prepaid expenses (PE), unearned revenues (UR), accrued expenses (AE), or accrued revenues (AR).a. To record wages expense incurred but not yet paid (nor recorded).b. To record expiration of prepaid insurance.c. To record revenue earned that was previously received as cash in advance.d. To record annual depreciation expense.e. To record revenue earned but not yet billed (nor recorded).

AE

PE

UR

PE

AR

McGraw-Hill/Irwin Slide 42McGraw-Hill/Irwin Slide 42

______ 1. Interest Expense . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2,208 Interest Payable . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2,208______ 2. Insurance Expense . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3,180 Prepaid Insurance . . . . . . . . . . . . . . . . . . . . . . . . . . . 3,180______ 3. Unearned Professional Fees . . . . . . . . . . . . . . . . . . . . . 19,250 Professional Fees Earned . . . . . . .. . . . . . . . . . . . . . 19,250______ 4. Interest Receivable . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3,300 Interest Revenue . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3,300______ 5. Depreciation Expense . . . . . . . . . . . . . . . . . . . . . . . . . . 38,217 Accumulated Depreciation . . . . . . . . . . . . . . . . . . . . 38,217______ 6. Salaries Expense . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13,280 Salaries Payable . . . . . . . . . . . . . . . . . . . . . . . . . . . 13,280

EXERCISE 3-1(p.117)

B

F

C

A

D

E

In the blank space beside each adjusting entry, enter the letter of the explanation A through F that most closely describes the entry.A. To record accrued interest revenue. B. To record accrued interest expense. C. To record the earning of previously unearned income. D. To record this period’s depreciation expense. E. To record accrued salaries expense.F. To record this period’s use of a prepaid expense.

McGraw-Hill/Irwin Slide 43McGraw-Hill/Irwin Slide 43

EXERCISE 3-3(p.117)

Unearned Fee Revenue 5,000 Fee Revenue 5,000To record earned portion of fee received in advance ($15,000 x 1/3).

Wages Expense 7,500 Wages Payable 7,500To record wages accrued but not yet paid.

Depreciation Expense—Equipment 17,251 Accumulated Depreciation—Equipment 17,251To record depreciation expense for the year.

Office Supplies Expense 5,682 Office Supplies* 5,682To record office supplies used ($240 + $6,102 - $660).

a. One-third of the work related to $15,000 cash received in advance is performed this period.

b. Wages of $7,500 are earned by workers but not paid as of December 31, 2009.

c. Depreciation on the company’s equipment for 2009 is $17,251.

d. The Office Supplies account had a $240 debit balance on December 31, 2008. During 2009, $6,102 of office supplies are purchased. A physical count of supplies at December 31, 2009, shows $660 of supplies available.

For each of the following separate cases, prepare adjusting entries required of financial statements for the year ended (date of) December 31, 2009. (Assume that prepaid expenses are initially recorded in asset accounts and that fees collected in advance of work are initially recorded as liabilities.)

McGraw-Hill/Irwin Slide 44McGraw-Hill/Irwin Slide 44

EXERCISE 3-3(p.117)

Insurance Expense 2,700 Prepaid Insurance† 2,700To record insurance coverage expired ($4,000 - $1,300).

Interest Receivable 1,400 Interest Revenue 1,400To record interest earned but not yet received.

Interest Expense2,000 Interest Payable 2,000To record interest incurred but not yet paid.

e. The Prepaid Insurance account had a $4,000 balance on December 31, 2008. An analysis of insurance policies shows that $1,300 of unexpired insurance benefits remain at December 31, 2009.

f. The company has earned (but not recorded) $1,400 of interest from investments in CDs for the year ended December 31, 2009. The interest revenue will be received on January 10, 2010.

g. The company has a bank loan and has incurred (but not recorded) interest expense of $2,000 for the year ended December 31, 2009. The company must pay the interest on January 2, 2010.

McGraw-Hill/Irwin Slide 45McGraw-Hill/Irwin Slide 45

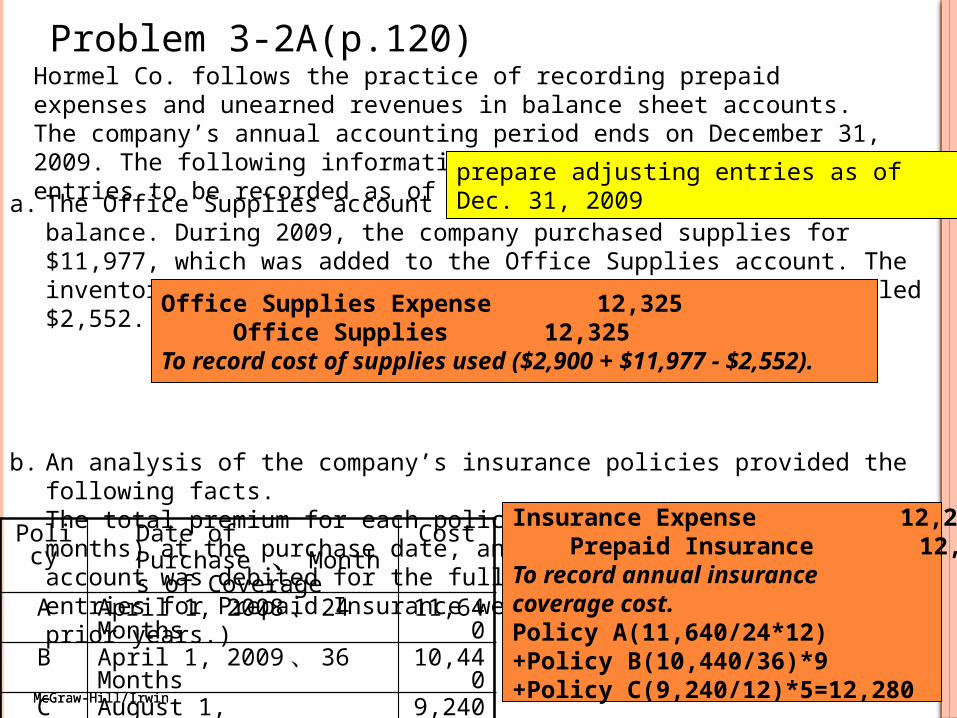

a. The Office Supplies account started the year with a $2,900 balance. During 2009, the company purchased supplies for $11,977, which was added to the Office Supplies account. The inventory of supplies available at December 31, 2009, totaled $2,552.

b. An analysis of the company’s insurance policies provided the following facts.The total premium for each policy was paid in full (for all months) at the purchase date, and the Prepaid Insurance account was debited for the full cost. (Year-end adjusting entries for Prepaid Insurance were properly recorded in all prior years.)

Problem 3-2A(p.120)

Office Supplies Expense 12,325 Office Supplies 12,325To record cost of supplies used ($2,900 + $11,977 - $2,552).

Insurance Expense 12,280 Prepaid Insurance 12,280To record annual insurance coverage cost.Policy A(11,640/24*12)+Policy B(10,440/36)*9+Policy C(9,240/12)*5=12,280

Hormel Co. follows the practice of recording prepaid expenses and unearned revenues in balance sheet accounts. The company’s annual accounting period ends on December 31, 2009. The following information concerns the adjusting entries to be recorded as of that date.

Policy Date of Purchase 、Months of Coverage

Cost

A April 1, 2008、 24 Months 11,640

B April 1, 2009 、 36 Months 10,440

C August 1, 2009 、 12Months

9,240

prepare adjusting entries as of Dec. 31, 2009

McGraw-Hill/Irwin Slide 46McGraw-Hill/Irwin Slide 46

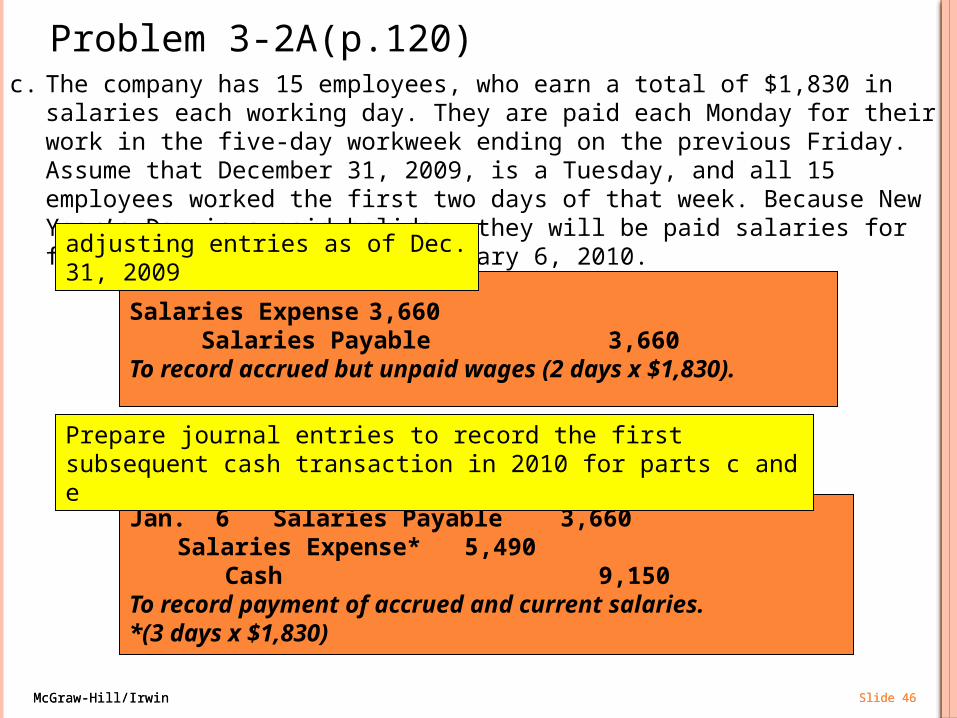

c. The company has 15 employees, who earn a total of $1,830 in salaries each working day. They are paid each Monday for their work in the five-day workweek ending on the previous Friday. Assume that December 31, 2009, is a Tuesday, and all 15 employees worked the first two days of that week. Because New Year’s Day is a paid holiday, they will be paid salaries for five full days on Monday, January 6, 2010.

Problem 3-2A(p.120)

Salaries Expense 3,660 Salaries Payable 3,660To record accrued but unpaid wages (2 days x $1,830).

Jan. 6 Salaries Payable 3,660Salaries Expense* 5,490

Cash 9,150To record payment of accrued and current salaries. *(3 days x $1,830)

Prepare journal entries to record the first subsequent cash transaction in 2010 for parts c and e

adjusting entries as of Dec. 31, 2009

McGraw-Hill/Irwin Slide 47McGraw-Hill/Irwin Slide 47

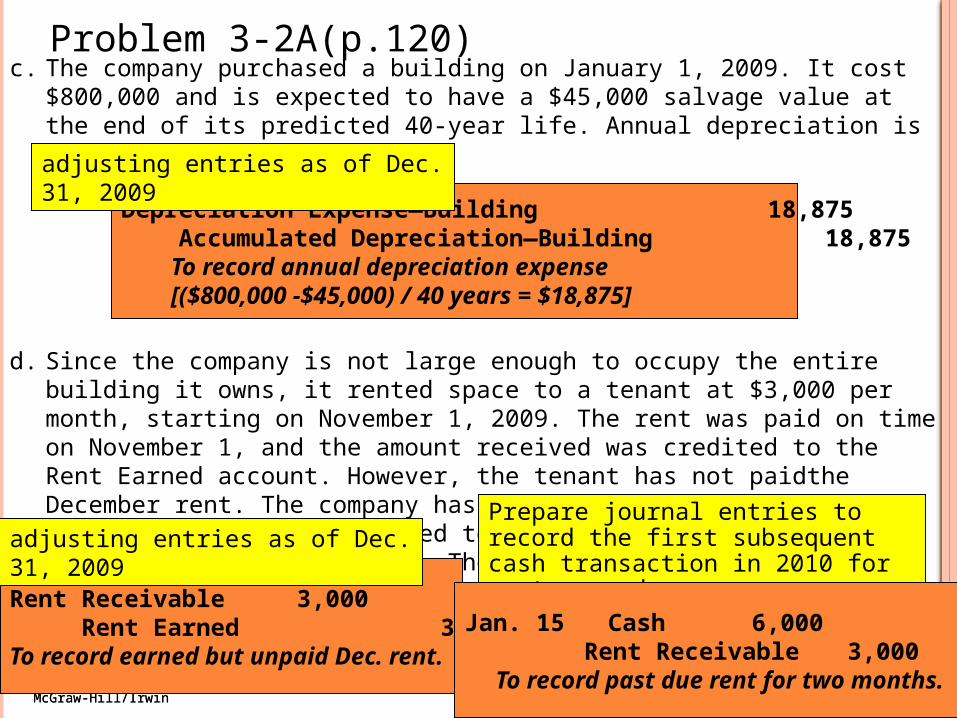

c. The company purchased a building on January 1, 2009. It cost $800,000 and is expected to have a $45,000 salvage value at the end of its predicted 40-year life. Annual depreciation is $18,875.

d. Since the company is not large enough to occupy the entire building it owns, it rented space to a tenant at $3,000 per month, starting on November 1, 2009. The rent was paid on time on November 1, and the amount received was credited to the Rent Earned account. However, the tenant has not paidthe December rent. The company has worked out an agreement with the tenant, who has promised to pay both December and January rent in full on January 15. The tenant has agreed not to fall behind again.

Problem 3-2A(p.120)

Rent Receivable 3,000 Rent Earned 3,000To record earned but unpaid Dec. rent.

Depreciation Expense—Building 18,875 Accumulated Depreciation—Building 18,875 To record annual depreciation expense [($800,000 -$45,000) / 40 years = $18,875]

adjusting entries as of Dec. 31, 2009

adjusting entries as of Dec. 31, 2009 Prepare journal entries to record the first subsequent cash transaction in 2010 for parts c and e

Jan. 15 Cash 6,000 Rent Receivable 3,000 Rent Earned 3,000

To record past due rent for two months.

McGraw-Hill/Irwin Slide 48McGraw-Hill/Irwin Slide 48

Problem 3-2A(p.120)

Unearned Rent 5,436Rent Earned 5,436

To record the amount of rent earned for November and December (2 x $2,718).

f. On November 1, the company rented space to another tenant for $2,718 per month. The tenant paid five months’ rent in advance on that date. The payment was recorded with a credit to the Unearned Rent account

adjusting entries as of Dec. 31, 2009

McGraw-Hill/Irwin Slide 49McGraw-Hill/Irwin Slide 49

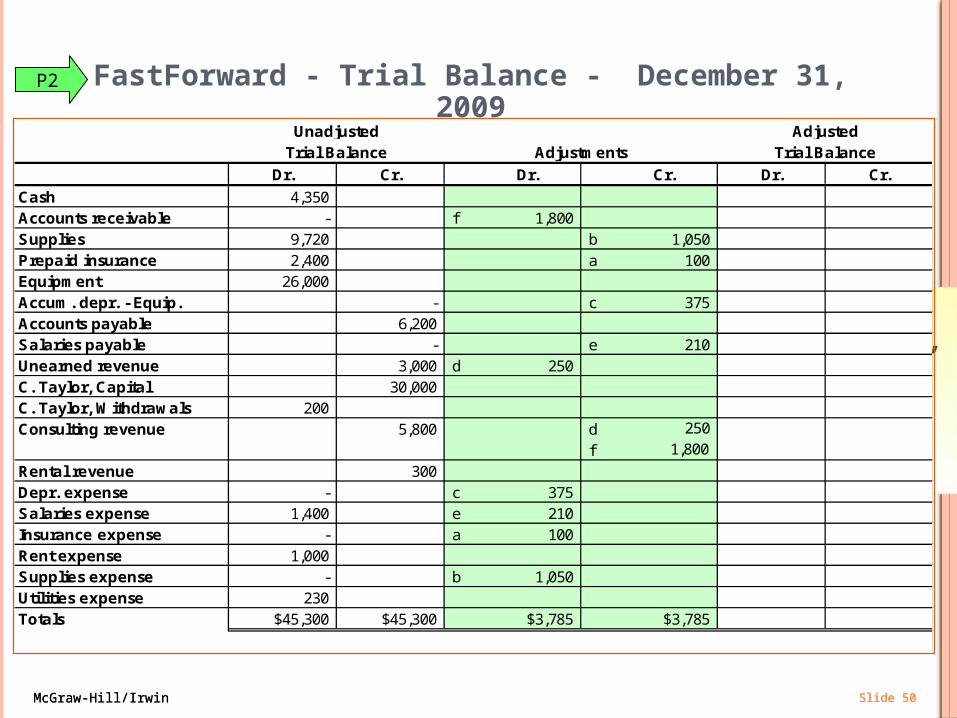

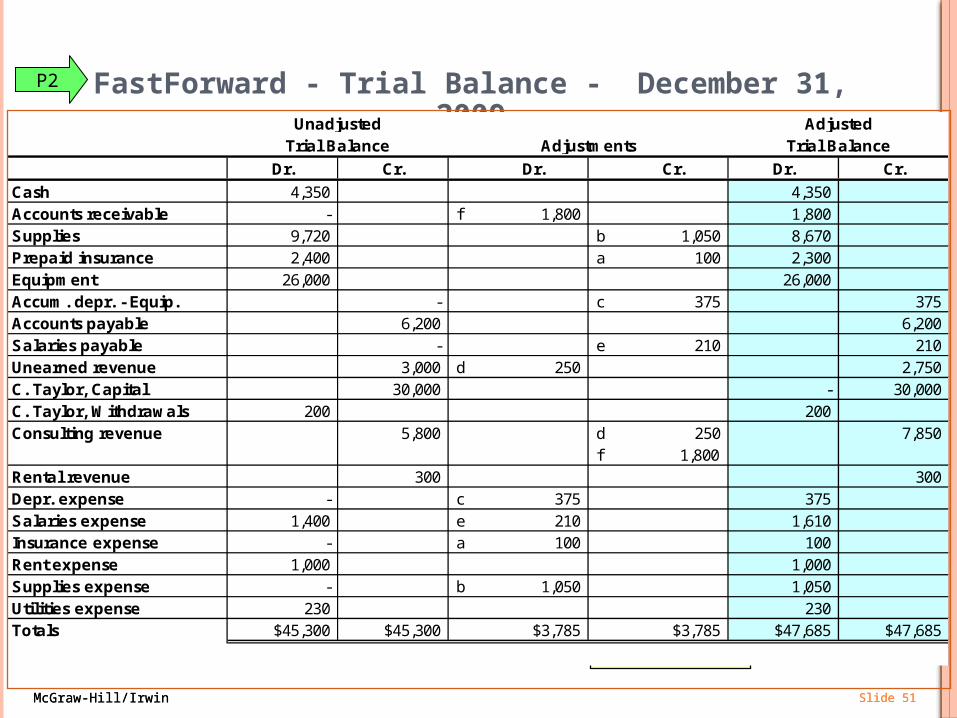

FastForward - Trial Balance - December 31, 2009

Dr. Cr. Dr. Cr. Dr. Cr.

Cash 4,350 Accounts receivable - Supplies 9,720 Prepaid insurance 2,400 Equipment 26,000 Accum. depr. - Equip. - Accounts payable 6,200 Salaries payable - Unearned revenue 3,000 C. Taylor, Capital 30,000 C. Taylor Withdrawals 200 Consulting revenue 5,800

Rental revenue 300 Depr. expense - Salaries expense 1,400 Insurance expense - Rent expense 1,000 Supplies expense - Utilities expense 230 Totals 45,300 45,300

AdjustedAdjusted Trial BalanceAdjustments

UnadjustedTrial Balance

First, the initial

unadjusted amounts are added to the worksheet.

P2

McGraw-Hill/Irwin Slide 50McGraw-Hill/Irwin Slide 50

Dr. Cr. Dr. Cr. Dr. Cr.

Cash 4,350 Accounts receivable - f 1,800 Supplies 9,720 b 1,050 Prepaid insurance 2,400 a 100 Equipment 26,000 Accum. depr. - Equip. - c 375 Accounts payable 6,200 Salaries payable - e 210 Unearned revenue 3,000 d 250 C. Taylor, Capital 30,000 C. Taylor, Withdrawals 200 Consulting revenue 5,800 d 250

f 1,800

Rental revenue 300 Depr. expense - c 375 Salaries expense 1,400 e 210 Insurance expense - a 100 Rent expense 1,000 Supplies expense - b 1,050 Utilities expense 230 Totals $45,300 $45,300 $3,785 $3,785

AdjustedTrial BalanceAdjustments

UnadjustedTrial Balance

Next, FastForward’s adjustments are added.

FastForward - Trial Balance - December 31, 2009P2

McGraw-Hill/Irwin Slide 51McGraw-Hill/Irwin Slide 51

Dr. Cr. Dr. Cr. Dr. Cr.

Cash 4,350 4,350 Accounts receivable - f 1,800 1,800 Supplies 9,720 b 1,050 8,670 Prepaid insurance 2,400 a 100 2,300 Equipment 26,000 26,000 Accum. depr. - Equip. - c 375 375 Accounts payable 6,200 6,200 Salaries payable - e 210 210 Unearned revenue 3,000 d 250 2,750 C. Taylor, Capital 30,000 - 30,000 C. Taylor, Withdrawals 200 200 Consulting revenue 5,800 d 250 7,850

f 1,800Rental revenue 300 300 Depr. expense - c 375 375 Salaries expense 1,400 e 210 1,610 Insurance expense - a 100 100 Rent expense 1,000 1,000 Supplies expense - b 1,050 1,050 Utilities expense 230 230 Totals $45,300 $45,300 $3,785 $3,785 $47,685 $47,685

AdjustedTrial BalanceAdjustments

UnadjustedTrial Balance

Finally, the totals are

determined.

FastForward - Trial Balance - December 31, 2009P2

McGraw-Hill/Irwin Slide 52McGraw-Hill/Irwin Slide 52

QS 3-9(p.116)

Dr. Cr. Dr. Cr. Dr. Cr.

Prepaid insurance 4,100 3,700

Interest Payable 0 800

Unadjusted AdjustedTrial Balance Adjustments Trial Balance

The following information is taken from Booker Company’s unadjusted and adjusted trial balances.

Given this information, which of the following is likely included among its adjusting entries?a. A $400 debit to Insurance Expense and an $800 debit to Interest Expense.b. A $400 debit to Insurance Expense and an $800 debit to Interest Payable.c. A $400 credit to Prepaid Insurance and an $800 debit to Interest Payable.

Insurance Expense

a 400

a 400 400

Interest Expense

b 800

b 800 800

McGraw-Hill/Irwin Slide 53McGraw-Hill/Irwin Slide 53

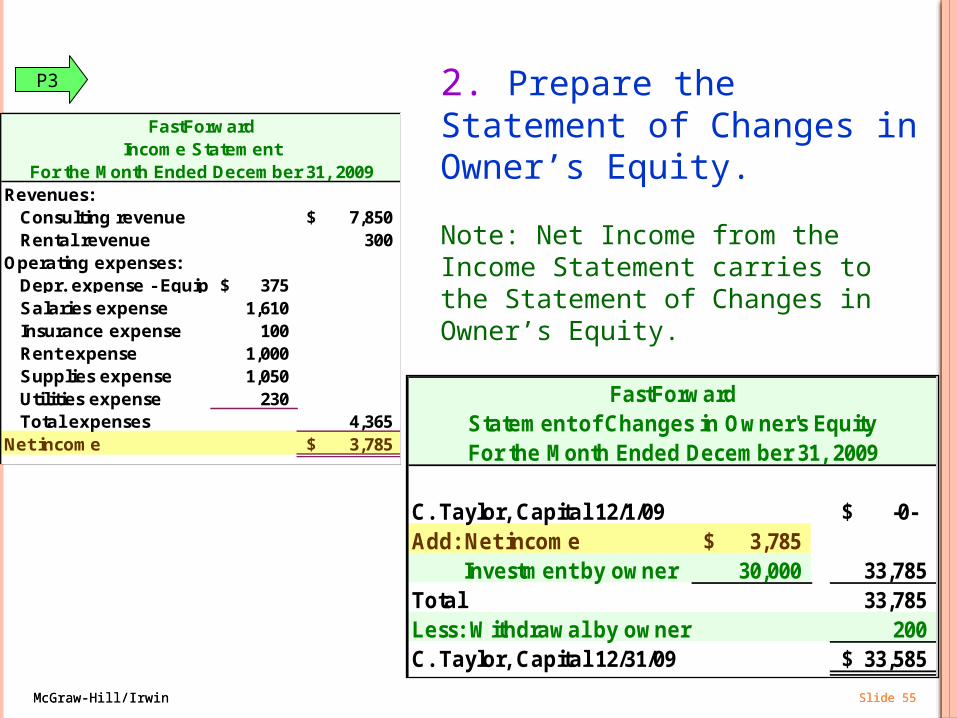

PREPARING FINANCIAL STATEMENTS

Let’s use Fast Forward’s adjusted trial balance to prepare the company’s financial statements.

P3

McGraw-Hill/Irwin Slide 54McGraw-Hill/Irwin Slide 54

FastForwardIncome Statement

For the Month Ended December 31, 2009Revenues: Consulting revenue 7,850$ Rental revenue 300 Operating expenses: Depr. expense - Equip. 375$ Salaries expense 1,610 Insurance expense 100 Rent expense 1,000 Supplies expense 1,050 Utilities expense 230 Total expenses 4,365 Net income 3,785$

1. Prepare the Income Statement

Dr. Cr.

Cash 4,350$

Accounts receivable 1,800

Supplies 8,670

Prepaid insurance 2,300

Equipment 26,000

Accum. depr. - Equip. 375$

Accounts payable 6,200

Salaries payable 210

Unearned revenue 2,750

C. Taylor, Capital 30,000

C. Taylor, Withdrawals 200

Consulting revenue 7,850

Rental revenue 300

Depr. expense 375

Salaries expense 1,610

Insurance expense 100

Rent expense 1,000

Supplies expense 1,050

Utilities expense 230

Totals 47,685$ 47,685$

Adjusted

December 31, 2009Trial Balance

P3

McGraw-Hill/Irwin Slide 55McGraw-Hill/Irwin Slide 55

2. Prepare the Statement of Changes in Owner’s Equity.

Note: Net Income from the Income Statement carries to the Statement of Changes in Owner’s Equity.

FastForwardIncome Statement

For the Month Ended December 31, 2009Revenues: Consulting revenue 7,850$ Rental revenue 300 Operating expenses: Depr. expense - Equip. 375$ Salaries expense 1,610 Insurance expense 100 Rent expense 1,000 Supplies expense 1,050 Utilities expense 230 Total expenses 4,365 Net income 3,785$

FastForwardStatement of Changes in Owner's EquityFor the Month Ended December 31, 2009

C. Taylor, Capital 12/1/09 $ -0-Add: Net income 3,785$ Investment by owner 30,000 33,785 Total 33,785 Less: Withdrawal by owner 200 C. Taylor, Capital 12/31/09 33,585$

P3

McGraw-Hill/Irwin Slide 56McGraw-Hill/Irwin Slide 56

Dr. Cr.

Cash 4,350$

Accounts receivable 1,800

Supplies 8,670

Prepaid insurance 2,300

Equipment 26,000

Accum. depr. - Equip. 375$

Accounts payable 6,200

Salaries payable 210

Unearned revenue 2,750

C. Taylor, Capital 30,000

C. Taylor, Withdrawals 200

Adjusted

December 31, 2009Trial Balance

FastForwardBalance Sheet

12/31/09Assets

Cash 4,350$

Accounts Receivable 1,800

Supplies 8,670

Prepaid Insurance 2,300

Equipment 26,000$

Accumulated Depreciation 375 25,625

Total assets 42,745$

Liabilities

Accounts Payable 6,200

Salaries Payable 210

Unearned Revenue 2,750

Total Liabilities 9,160

Equity

C Taylor, Capital 33,585

Total liabilities and Equity 42,745$

FastForwardStatement of Changes in Owner's EquityFor the Month Ended December 31, 2009

C. Taylor, Capital 12/1/07 $ -0-Add: Net income 3,785$ Investment by owner 30,000 33,785 Total 33,785 Less: Withdrawal by owner 200 C. Taylor, Capital 12/31/07 33,585$

3. Prepare the Balance Sheet

P3

McGraw-Hill/Irwin Slide 57McGraw-Hill/Irwin Slide 57

EXERCISE

Problem 3-3A (p.122)Problem 3-3B (Home Work)

McGraw-Hill/Irwin Slide 58McGraw-Hill/Irwin Slide 58

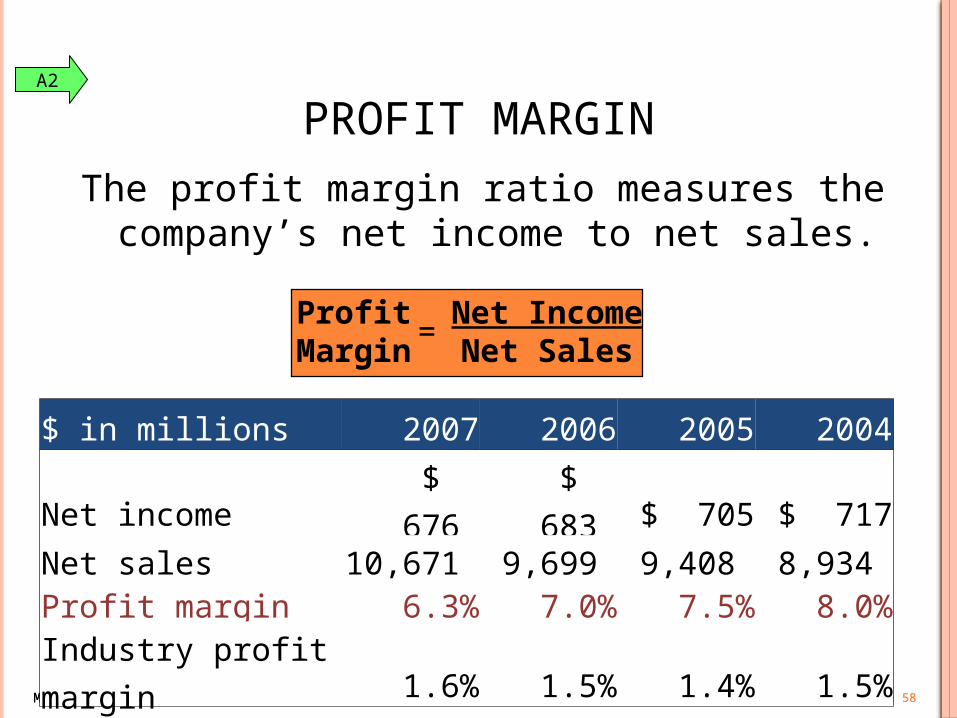

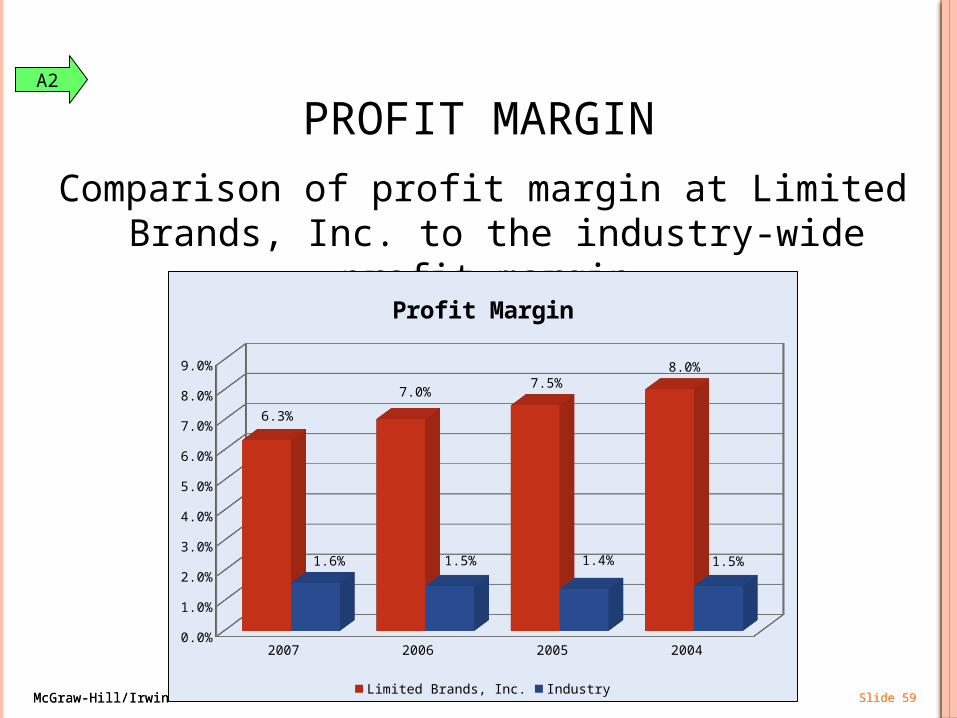

PROFIT MARGIN

The profit margin ratio measures the company’s net income to net sales.

ProfitMargin

Net Income Net Sales

=

$ in millions 2007 2006 2005 2004Net income $ 676 $ 683 $ 705 $ 717 Net sales 10,671 9,699 9,408 8,934 Profit margin 6.3% 7.0% 7.5% 8.0%Industry profit margin 1.6% 1.5% 1.4% 1.5%

A2

McGraw-Hill/Irwin Slide 59McGraw-Hill/Irwin Slide 59

PROFIT MARGIN

Comparison of profit margin at Limited Brands, Inc. to the industry-wide profit margin.

2007 2006 2005 20040.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

6.3%

7.0%7.5%

8.0%

1.6% 1.5% 1.4% 1.5%

Profit Margin

Limited Brands, Inc. Industry

A2

McGraw-Hill/Irwin Slide 60McGraw-Hill/Irwin Slide 60

Multiple Choice Quiz(p.114)5. If a company had $15,000 in net income for the year,

and its sales were $300,000 for the same year, what is its profit margin?

a. 20%b. 2,000%c. $285,000d. $315,000e. 5%

e

ProfitMargin

Net Income Net Sales

=

McGraw-Hill/Irwin Slide 61McGraw-Hill/Irwin Slide 61

Dec 6 Here is the $2,400 checkfor my 24-monthinsurance policy.

Dec 6 Here is the $2,400 checkfor my 24-monthinsurance policy.

PREPAID (DEFERRED) EXPENSES

Resources paid for prior to receiving the actual benefits.Resources paid for prior to receiving the actual benefits.

CreditAdjustment

DebitAdjustment

P1

Expense

UnadjustedBalance

Asset

Real Account( 實帳戶 )or Permanent Account( 久性帳戶 )

Nominal Account( 虛帳戶 ) 或 Temporary Account( 暫時性帳戶 )

記實轉虛

Recording the Prepayment of

Expenses in Asset Accounts.

Prepaid Insurance 2,400 Cash 2400

Insurance Expense 100 Prepaid Insurance 100

McGraw-Hill/Irwin Slide 62McGraw-Hill/Irwin Slide 62

Dec 6 Here is the $2,400 check

for my 24-monthinsurance policy.

Dec 6 Here is the $2,400 check

for my 24-monthinsurance policy.

PREPAID (DEFERRED) EXPENSES

Resources paid for prior to receiving the actual benefits.Resources paid for prior to

receiving the actual benefits.

UnadjustedBalance

CreditAdjustment

DebitAdjustment

3A

ExpenseAsset

Real Account( 實帳戶 )or Permanent Account( 久性帳戶 )

Nominal Account( 虛帳戶 ) 或 Temporary Account( 暫時性帳戶 )

記虛轉實

Recording the Prepayment of

Expenses in Expense Accounts.

Insurance Expense 2,400 Cash 2,400

Prepaid Insurance 2,300 Insurance Expense 2,300

McGraw-Hill/Irwin Slide 63McGraw-Hill/Irwin Slide 63

UNEARNED (DEFERRED)REVENUES

Dec 26, We will apply $3,000you gave us towards

your total consulting fees.

Dec 26, We will apply $3,000you gave us towards

your total consulting fees.Cash received in advance of

providing products or services.

P1

UnadjustedBalance

DebitAdjustment

CreditAdjustment

Liability Revenue

Real Account( 實帳戶 )or Permanent Account( 久性帳戶 )

Nominal Account( 虛帳戶 ) 或 Temporary Account( 暫時性帳戶 )

記實轉虛

Recording the Prepayment of Revenues in Liability Accounts.

Cash 3,000 Unearned Consulting Fee 3,000

Dec 31 Earned 250 Unearned Consulting Fee 250 Consulting Revenue 250

McGraw-Hill/Irwin Slide 64McGraw-Hill/Irwin Slide 64

UNEARNED (DEFERRED)REVENUES

Dec 26, We will apply $3,000you gave us towards

your total consulting fees.

Dec 26, We will apply $3,000you gave us towards

your total consulting fees.Cash received in advance of providing products or

services.

P1

UnadjustedBalance

DebitAdjustment

CreditAdjustment

Liability Revenue

Real Account( 實帳戶 )or Permanent Account( 久性帳戶 )

Nominal Account( 虛帳戶 ) 或 Temporary Account( 暫時性帳戶 )

Recording the Prepayment of Revenues in Revenue Accounts.

Cash 3,000 Consulting Revenue 3,000

Dec 31 Earned 250 Consulting Revenue 2,750 Unearned Consulting Fee 2,750

記虛轉實

McGraw-Hill/Irwin Slide 65McGraw-Hill/Irwin Slide 65

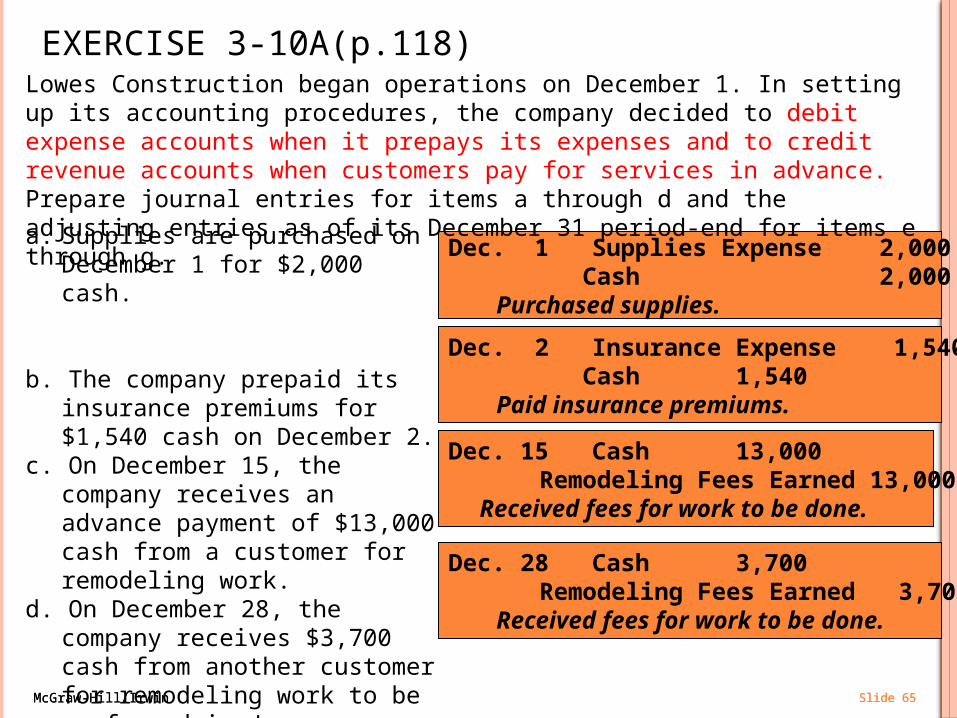

EXERCISE 3-10A(p.118)

Dec. 1 Supplies Expense 2,000 Cash 2,000Purchased supplies.

Dec. 2 Insurance Expense 1,540 Cash 1,540Paid insurance premiums.

a. Supplies are purchased on December 1 for $2,000 cash.

b. The company prepaid its insurance premiums for $1,540 cash on December 2.

c. On December 15, the company receives an advance payment of $13,000 cash from a customer for remodeling work.

d. On December 28, the company receives $3,700 cash from another customer for remodeling work to be performed in January.

Dec. 15 Cash 13,000 Remodeling Fees Earned 13,000

Received fees for work to be done.

Dec. 28 Cash 3,700 Remodeling Fees Earned 3,700Received fees for work to be done.

Lowes Construction began operations on December 1. In setting up its accounting procedures, the company decided to debit expense accounts when it prepays its expenses and to credit revenue accounts when customers pay for services in advance. Prepare journal entries for items a through d and the adjusting entries as of its December 31 period-end for items e through g.

McGraw-Hill/Irwin Slide 66McGraw-Hill/Irwin Slide 66

EXERCISE 3-10A(p.118)

Dec. 31 Supplies 1,840 Supplies Expense 1,840

Adjust expenses for unused supplies.

Dec. 31 Prepaid Insurance 1,200 Insurance Expense 1,200Adjust expenses for unexpired

coverage ($1,540 - $340).

e. A physical count on December 31 indicates that Lowes has $1,840 of supplies available.

f. An analysis of the insurance policies in effect on December 31 shows that $340 of insurance coverage had expired.

g. As of December 31, only one remodeling project has been worked on and completed. The $5,570 fee for this project had been received in advance.

Dec. 31 Remodeling Fees Earned 11,130 Unearned Remodeling Fees 11,130

Adjusted revenues for unfinished projects($13,000 + 3,700 - $5,570).

Lowes Construction began operations on December 1. In setting up its accounting procedures, the company decided to debit expense accounts when it prepays its expenses and to credit revenue accounts when customers pay for services in advance. Prepare journal entries for items a through d and the adjusting entries as of its December 31 period-end for items e through g.

McGraw-Hill/Irwin Slide 67McGraw-Hill/Irwin Slide 67

Problem 3-6AA(p.124)Riso Co. had the following transactions in the last two months of its year ended December 31.

Transactions Assume prepaid expenses are recorded as assets and unearned revenues as liabilities.

Assume prepaid expenses are recorded as expenses and unearned revenues as revenues.

Nov.1 Paid $2,000 cash for future newspaper advertising.

Nov.1 Paid $2,466 cash for 12 months of insurance through October 31 of the next year.

Nov.30 Received $4,200 cash for future services to be provided to a customer.

Nov.1Prepaid Advertising 2,000 Cash 2,000Paid for future advertising.

Nov.1Advertising Expense 2,000 Cash 2,000Paid for future advertising.

Nov.1Prepaid Insurance 2,466 Cash 2,466Paid insurance for one year.

Nov.1Insurance Expense 2,466 Cash 2,466Paid insurance for one year.

Nov.30Cash 4,200 Unearned Service Fees 4,200Received fees in advance.

Nov.30Cash 4,200 Service Fees Earned 4,200Received fees in advance.

McGraw-Hill/Irwin Slide 68McGraw-Hill/Irwin Slide 68

Problem 3-6AA(p.124)Transactions Assume prepaid expenses are recorded

as assets and unearned revenues as liabilities.

Assume prepaid expenses are recorded as expenses and unearned revenues as revenues.

Dec.1 Paid $2,400 cash for a consultant’s services to be received over the next three months.

Dec.15 Received $7,250 cash for future services to be provided to a customer.

Dec.31 Of the advertising paid for on November 1, $1,300 worth is not yet used.

Dec.1Prepaid Consulting Fees 2,400 Cash 2,400Paid for future consulting.

Dec.1Consulting Fees Expense 2,400 Cash 2,400Paid for future consulting.

Dec.15Cash 7,250 Unearned Service Fees 7,250Received fees in advance.

Dec.15Cash 7,250 Service Fees Earned 7,250Received fees in advance.

Dec.31Advertising Expense 700 Prepaid Advertising 700To adjust prepaid advertising. ($2,000 - $1,300).

Dec.31Prepaid Advertising 1,300 Advertising Expense 1,300To adjust for prepaid advertising.

McGraw-Hill/Irwin Slide 69McGraw-Hill/Irwin Slide 69

Problem 3-6AA(p.124)Transactions Assume prepaid expenses are recorded

as assets and unearned revenues as liabilities.

Assume prepaid expenses are recorded as expenses and unearned revenues as revenues.

Dec.31 A portion of the insurance paid for on November 1 has expired. No adjustment was made in November to Prepaid Insurance.

Dec.31 Services worth $1,600 are not yet provided to the customer who paid on November 30.

Dec.31Insurance Expense 411 Prepaid Insurance 411To adjust prepaid insurance ($2,466 x 2/12)

Dec.31Prepaid Insurance 2,055 Insurance Expense 2,055 To adjust for prepaid insurance ($2,466 x 10/12)

Dec.31Unearned Service Fees 2,600 Service Fees Earned 2,600 To adjust unearned service fees.($4,200-1,600)

Dec.31Service Fees Earned 1,600 Unearned Service Fees 1,600To adjust for unearned service fees.

McGraw-Hill/Irwin Slide 70McGraw-Hill/Irwin Slide 70

Problem 3-6AA(p.124)Transactions Assume prepaid expenses are recorded

as assets and unearned revenues as liabilities.

Assume prepaid expenses are recorded as expenses and unearned revenues as revenues.

Dec.31 One-third of the consulting services paid for on December 1 have been received.

Dec.31 The company has performed $4,350 of services that the customer paid for on December 15.

Dec.31Unearned Service Fees 4,350 Service Fees Earned 4,350To adjust unearned service fees.

Dec.31 Service Fees Earned 2,900 Unearned Service Fees 2,900To adjust for unearned servicefees.($7,250 - $4,350)

Dec.31Consulting Fees Expense 800 Prepaid Consulting Fees 800To adjust prepaid consulting fees ($2,400 x 1/3)

Dec.31Prepaid Consulting Fees 1,600 Consulting Fees Expense 1,600 To adjust prepaid consulting fees ($2,400 x 1/3)

McGraw-Hill/Irwin Slide 71McGraw-Hill/Irwin Slide 71

Problem 3-6AA(p.124)Required 3.Explain why the alternative sets of entries in requirements 1 and 2 do not result in different financial statement amounts.

There are no differences between the two methods in terms of the amounts that appear on the financial statements. In both cases, the financial statements reflect the following:

Advertising expense for two months $ 700Prepaid advertising as of December 31 1,300Insurance expense for two months 411Prepaid insurance as of December 31 2,055Consulting fees expense (1/3 of total paid) 800Prepaid consulting fees 1,600Service fees earned for two months ($2,600 + $4,350) 6,950Unearned service fees at 12/31 ($1,600 + $2,900) 4,500

When prepaid expenses and unearned revenues are recorded in balance sheet accounts, the related adjusting entries are designed to generate the correct asset, expense, liability, and revenue account balances. When prepaid expenses and unearned revenues are recorded in income statement accounts, the related adjusting entries are designed to accomplish exactly the same result.

McGraw-Hill/Irwin Slide 72McGraw-Hill/Irwin Slide 72

END OF CHAPTER 3