7 - 1 ©2003 Prentice Hall Business Publishing, Cost Accounting 11/e, Horngren/Datar/Foster Flexible...

56

7 - 1 ©2003 Prentice Hall Business Publishing, Cost Accounting 11/e, Horngren/Datar/F Flexible Budgets, Variances, and Management Control: I Budgeti ng Lectur e

-

Upload

david-harvey -

Category

Documents

-

view

220 -

download

0

Transcript of 7 - 1 ©2003 Prentice Hall Business Publishing, Cost Accounting 11/e, Horngren/Datar/Foster Flexible...

7 - 1©2003 Prentice Hall Business Publishing, Cost Accounting 11/e, Horngren/Datar/Foster

Flexible Budgets, Variances,and Management Control: IFlexible Budgets, Variances,and Management Control: I

Budgeting Lecture

2

7 - 2

Distinguish

a static budget

from a flexible budget.

Learning Objective 1Learning Objective 1

7 - 3

Static and Flexible BudgetsStatic and Flexible Budgets

Static BudgetPlanned level ofoutput at start ofthe budget period

Based on

Flexible BudgetBudgeted revenuesand cost based on

actual level of output

Based on

7 - 4

Static Budget ExampleStatic Budget Example

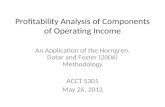

Assume that Pasadena Co. manufacturesand sells dress suits.

Budgeted variable costs per suit are as follows:Direct materials cost $ 65Direct manufacturing labor 26Variable manufacturing overhead 24Total variable costs $115

7 - 5

Static Budget ExampleStatic Budget Example

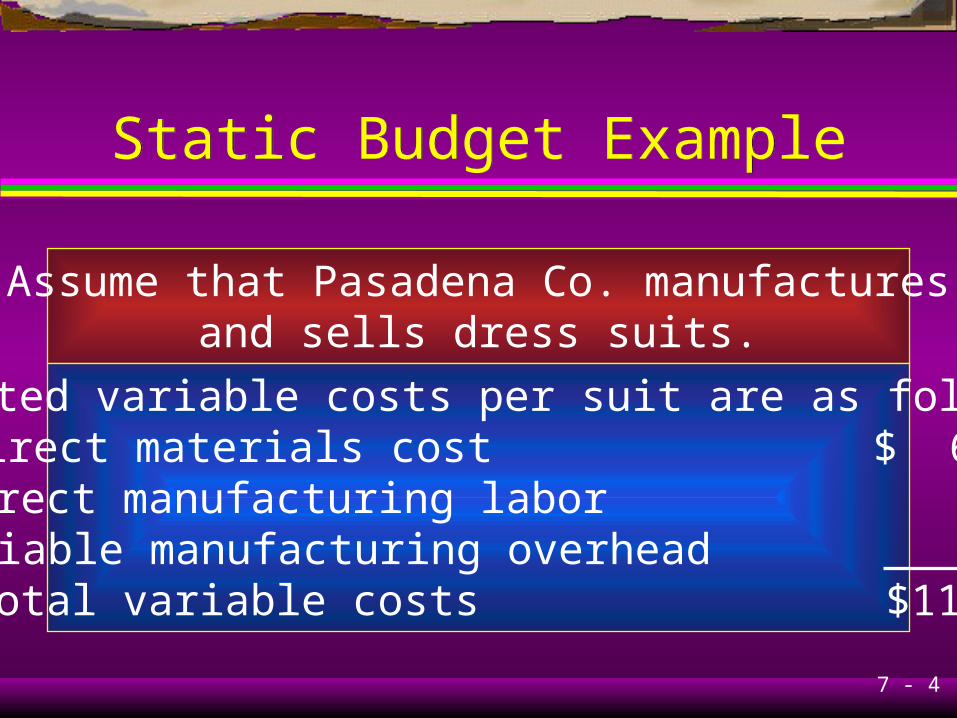

Budgeted selling price is $155 per suit.

Fixed manufacturing costs are expectedto be $286,000 within a relevant range

between 9,000 and 13,500 suits.

Variable and fixed period costs are ignored.

The static budget for year 2004 is basedon selling 13,000 suits.

What is the static-budget operating income?

7 - 6

Static Budget ExampleStatic Budget Example

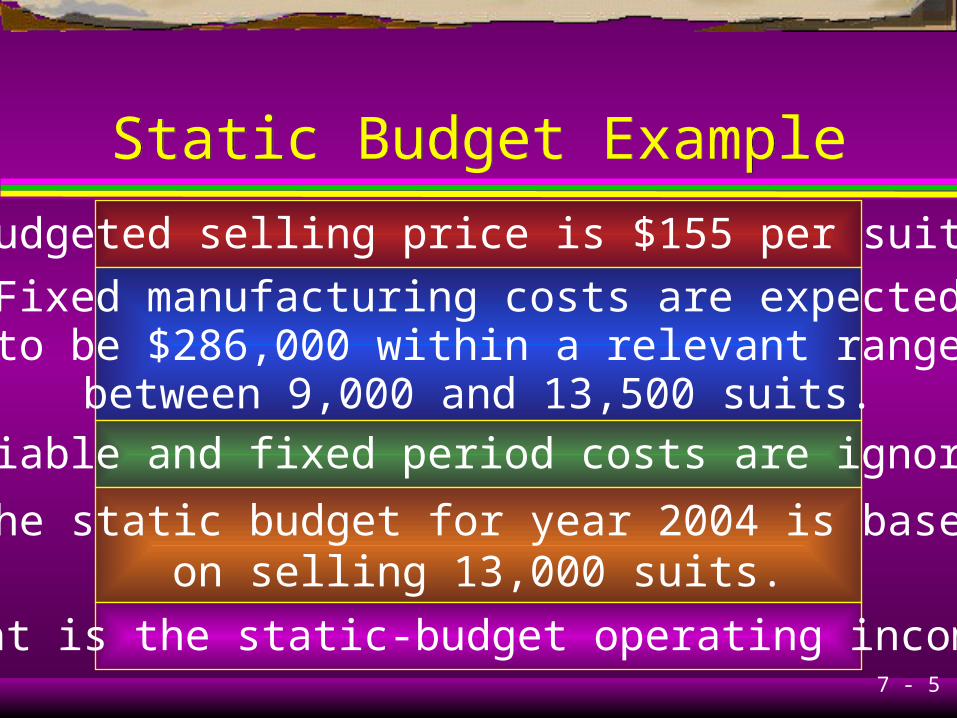

Revenues (13,000 × $155) $2,015,000Less Expenses:Variable (13,000 × $115) 1,495,000Fixed 286,000Budgeted operating income $ 234,000

Assume that Pasadena Co. produced and sold10,000 suits at $160 each with actual variablecosts of $120 per suit and fixed manufacturing

costs of $300,000.

7 - 7

Static Budget ExampleStatic Budget Example

Revenues (10,000 × $160) $1,600,000 Less Expenses: Variable (10,000 × $120) 1,200,000 Fixed 300,000 Actual operating income $ 100,000

What was the actual operating income?

7 - 8

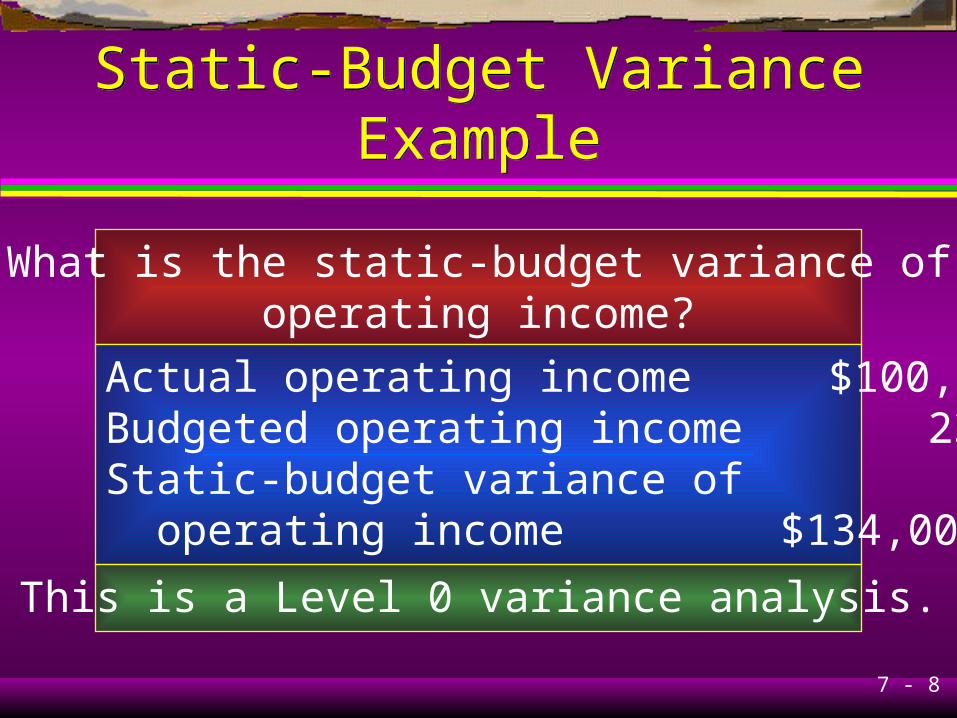

Static-Budget Variance ExampleStatic-Budget Variance Example

What is the static-budget variance ofoperating income?

Actual operating income $100,000Budgeted operating income 234,000Static-budget variance of operating income $134,000 U

This is a Level 0 variance analysis.

7 - 9

Static-Budget Variance ExampleStatic-Budget Variance Example

Static-Budget Based Variance Analysis(Level 1) in (000) Static Budget Actual Variance

Suits 13 10 3 URevenue $2,015 $1,600 $415 UVariable costs 1,495 1,200 296 FContribution margin $ 520 $ 400 $120 UFixed costs 286 300 14 UOperating income $ 234 $ 100 $134 U

7 - 10

Learning Objective 2Learning Objective 2

Develop a flexible budgetand compute flexible-budgetvariances and sales-volume

variances.

7 - 11

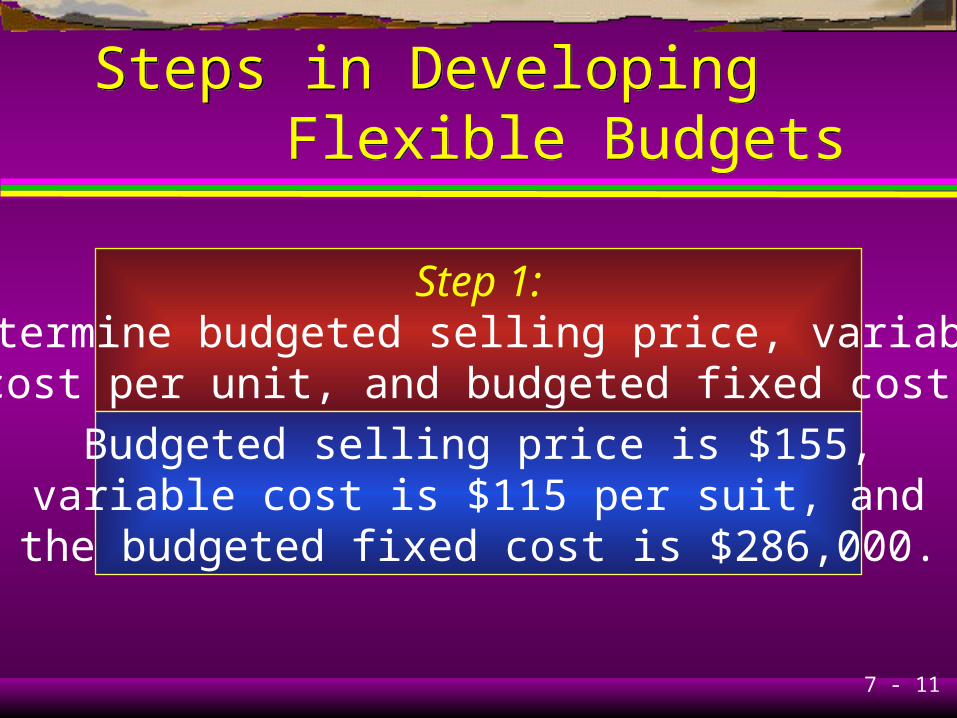

Steps in Developing Flexible Budgets

Steps in Developing Flexible Budgets

Step 1:Determine budgeted selling price, variable

cost per unit, and budgeted fixed cost.

Budgeted selling price is $155,variable cost is $115 per suit, and

the budgeted fixed cost is $286,000.

7 - 12

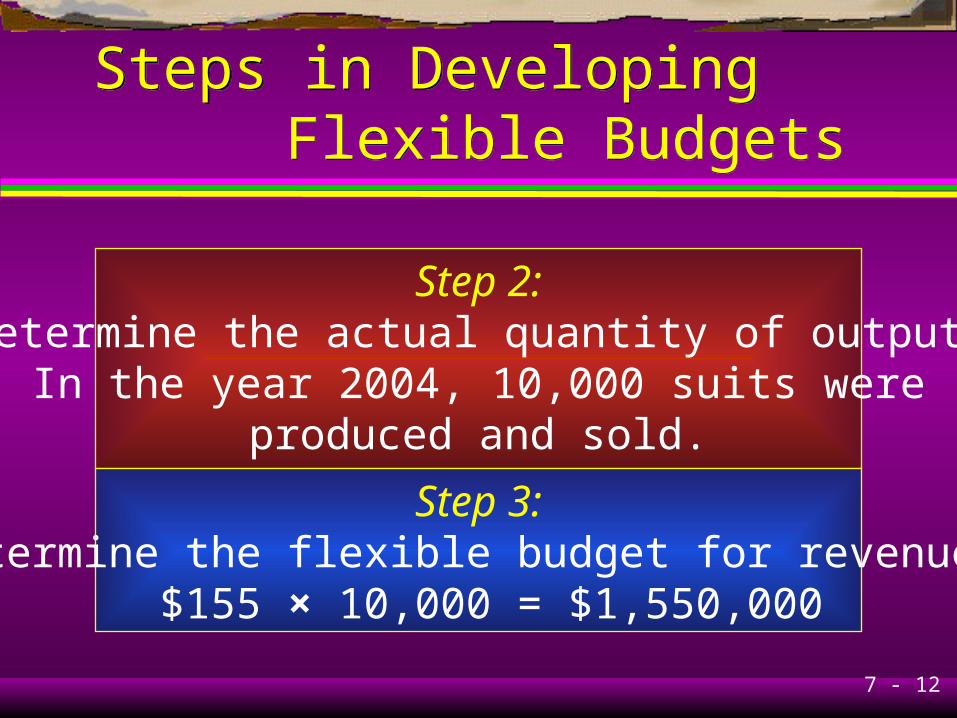

Steps in Developing Flexible Budgets

Steps in Developing Flexible Budgets

Step 2:Determine the actual quantity of output.

In the year 2004, 10,000 suits wereproduced and sold.

Step 3:Determine the flexible budget for revenues.

$155 × 10,000 = $1,550,000

7 - 13

Steps in Developing Flexible Budgets

Steps in Developing Flexible Budgets

Step 4:Determine the flexible budget for costs.

Variable costs: 10,000 × $115 = $1,150,000Fixed costs 286,000Total costs $1,436,000

7 - 14

VariancesVariances

Level 2 analysis provides informationon the two components of the

static-budget variance.

1. Flexible-budget variance

2. Sales-volume variance

7 - 15

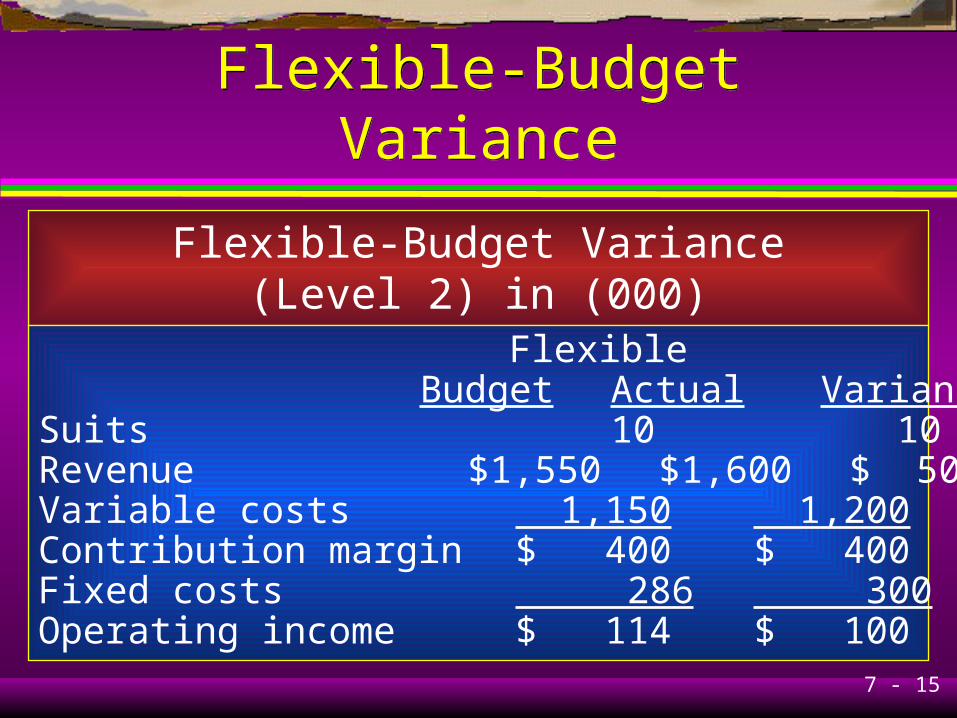

Flexible-Budget VarianceFlexible-Budget Variance

Flexible-Budget Variance(Level 2) in (000) Flexible

Budget Actual VarianceSuits 10 10 0Revenue $1,550 $1,600 $ 50 FVariable costs 1,150 1,200 50 UContribution margin $ 400 $ 400 $ 0Fixed costs 286 300 14 UOperating income $ 114 $ 100 $ 14 U

7 - 16

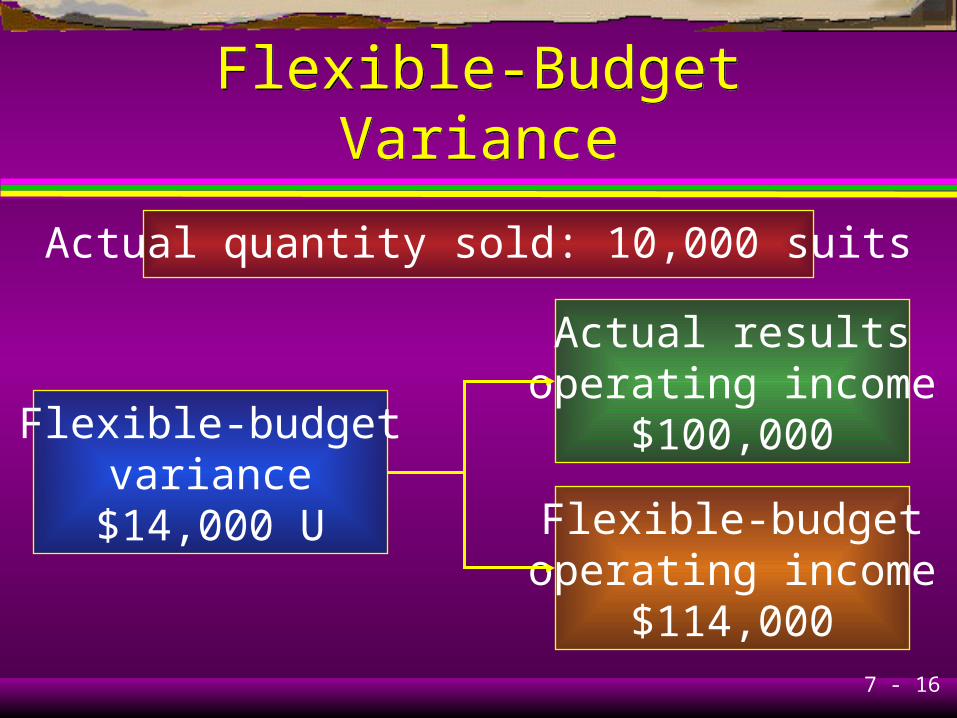

Flexible-Budget VarianceFlexible-Budget Variance

Actual quantity sold: 10,000 suits

Flexible-budgetvariance

$14,000 U

Actual resultsoperating income

$100,000

Flexible-budgetoperating income

$114,000

7 - 17

Flexible-Budget VarianceFlexible-Budget Variance

Total flexible-budget variance= Total actual results

– Total flexible budget for actual sales level

7 - 18

Flexible-Budget VarianceFlexible-Budget Variance

Actual Budgeted Amount Amount

Selling price $160 $155Variable cost 120 115Contribution margin $ 40 $ 40

7 - 19

Flexible-Budget VarianceFlexible-Budget Variance

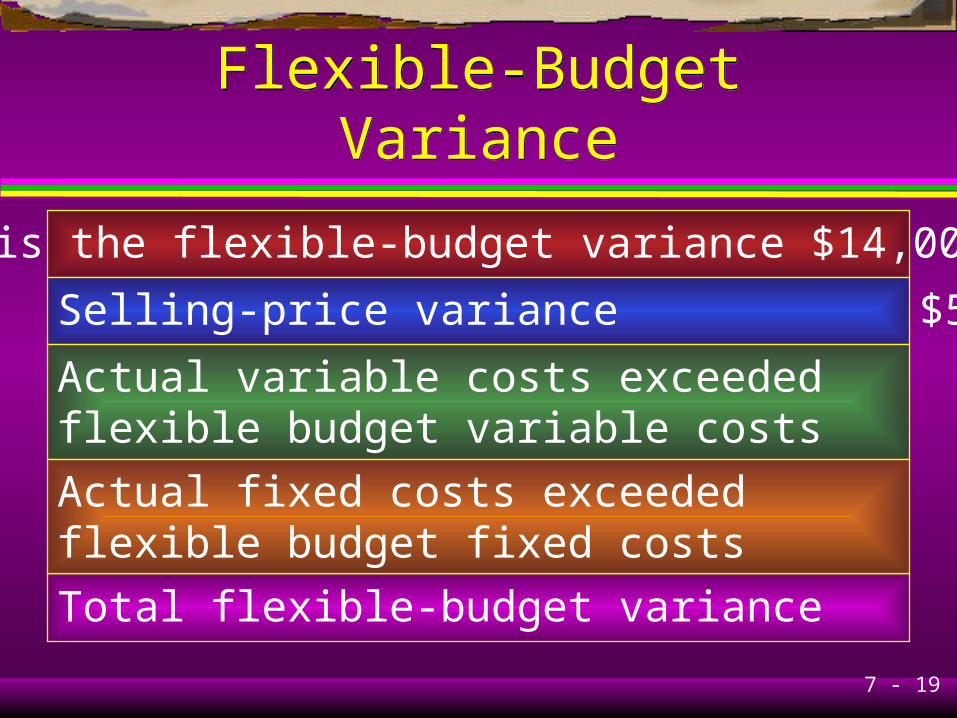

Why is the flexible-budget variance $14,000 U?

Selling-price variance $50,000 F

Actual variable costs exceededflexible budget variable costs 50,000 U

Actual fixed costs exceededflexible budget fixed costs 14,000 U

Total flexible-budget variance $14,000 U

7 - 20

Sales-Volume VarianceSales-Volume Variance

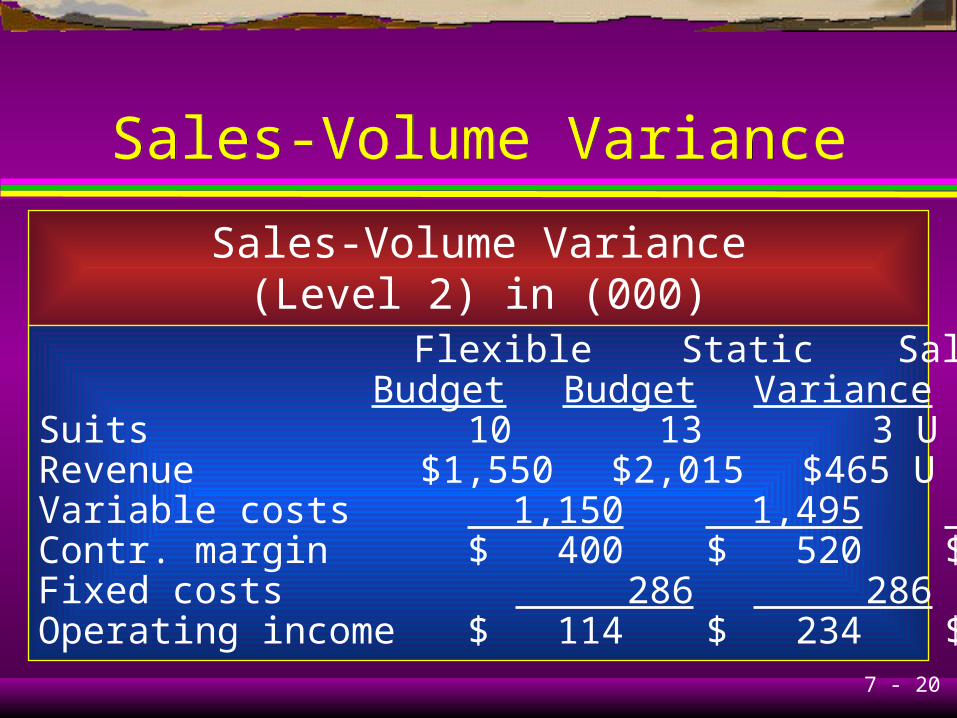

Sales-Volume Variance(Level 2) in (000) Flexible Static Sales-Volume

Budget Budget VarianceSuits 10 13 3 URevenue $1,550 $2,015 $465 UVariable costs 1,150 1,495 295 FContr. margin $ 400 $ 520 $120 UFixed costs 286 286 0Operating income $ 114 $ 234 $120 U

7 - 21

Sales-Volume VarianceSales-Volume Variance

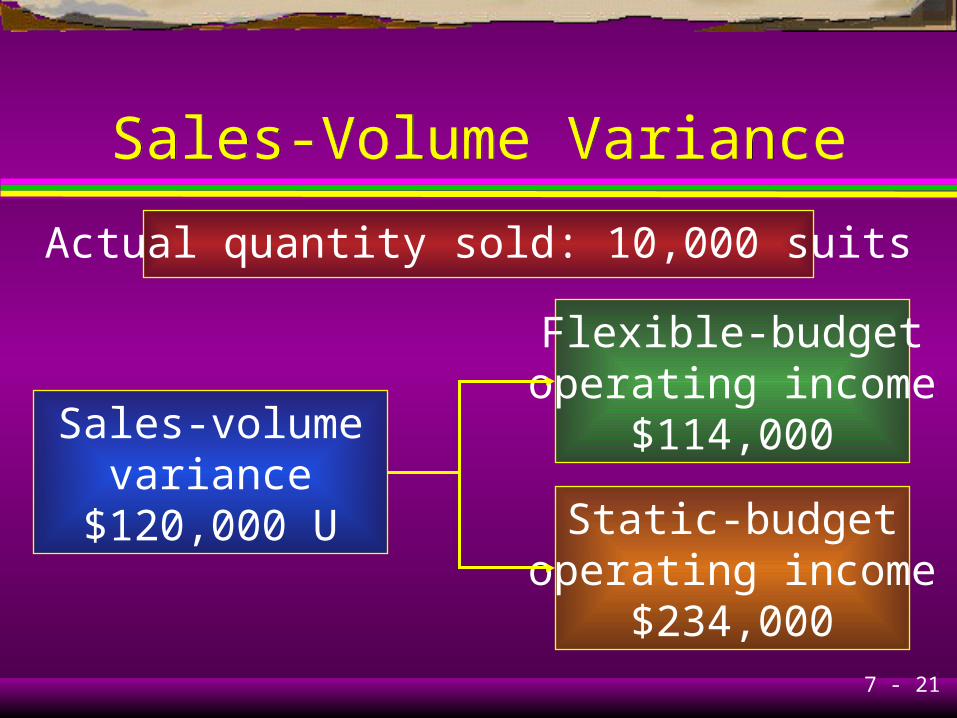

Actual quantity sold: 10,000 suits

Sales-volumevariance

$120,000 U

Flexible-budgetoperating income

$114,000

Static-budgetoperating income

$234,000

7 - 22

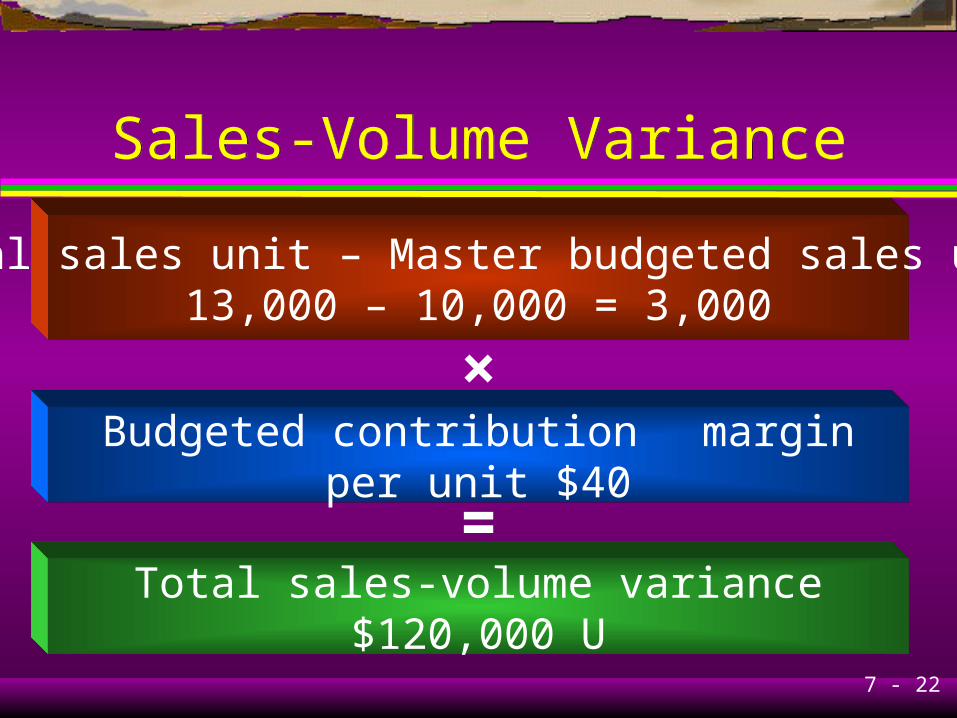

Sales-Volume VarianceSales-Volume Variance

Total sales-volume variance $120,000 U

=

Actual sales unit – Master budgeted sales units13,000 – 10,000 = 3,000×

Budgeted contribution margin per unit $40

7 - 23

Budget VariancesBudget Variances

Static-budgetvariance

$134,000 U

Flexible-budgetvariance

$14,000 U

Level 1

Sales-volumevariance

$120,000 ULevel 2

7 - 24

Learning Objective 3Learning Objective 3

Explain why standard costs areoften used in variance analysis.

7 - 25

StandardsStandards

Pasadena’s budgeted cost for each variabledirect cost item is computed as follows:

Standard inputallowed for

one output unit

Standard costper input unit

×

7 - 26

StandardsStandards

4.00 square yards allowed per output unit at $16.25 standard cost per square yard.

Standard cost per output unit 4.00 × $16.25 = $65.00

7 - 27

StandardsStandards

2.00 manufacturing labor-hours of inputallowed per output unit at $13.00 standard

cost per hour.

Standard cost per output unit2.00 × $13.00 = $26.00

7 - 28

Learning Objective 4Learning Objective 4

Compute price variancesand efficiency variances

for direct-cost categories.

7 - 29

Actual DataActual Data

Direct materials purchased and used:42,500 square yards at $15.95

Labor hours: 21,500 at $12.90

Cost of direct materials = $677,875

Cost of direct manufacturing labor = $277,350

7 - 30

Price Variance ExamplePrice Variance Example

Direct-material price variance

Actual price – Budgeted price

× Actualquantity

($15.95 – $16.25) × 42,500 = $12,750 F=

=

7 - 31

Price Variance ExamplePrice Variance Example

Direct-labor price variance

Actual price – Budgeted price

× Actualquantity

($12.90 – $13.00) × 21,500 = $2,150 F=

=

7 - 32

Price Variance ExamplePrice Variance Example

What is the journal entry when the materials pricevariance is isolated at the time of purchase?

Materials Control 690,625Direct-Materials Price Variance 12,750Accounts Payable Control 677,875To record direct materials purchased

7 - 33

Efficiency Variance ExampleEfficiency Variance Example

Direct-material efficiency variance

Actual quantity – Standard

quantity× Standard

price

(42,500 – 40,000) × $16.25 = $40,625 U=

=

7 - 34

Efficiency Variance ExampleEfficiency Variance Example

Direct-labor efficiency variance

Actual quantity – Standard

quantity× Standard

price

(21,500 – 20,000) × $13.00 = $19,500 U=

=

7 - 35

Efficiency VarianceEfficiency Variance

What is the journal entry to record materials used?

Work in Process Control 650,000Direct-Materials Efficiency Variance 40,625

Materials Control 690,625To record direct materials used

7 - 36

Price and Efficiency VariancePrice and Efficiency Variance

What is the journal entry for direct manufacturing labor?

Work in Process Control 260,000Direct ManufacturingLabor Efficiency Variance 19,500

Direct-ManufacturingLabor Price Variance 2,150Wages Payable 277,350

To record liability for direct manufacturing labor

7 - 37

Flexible Budget MaterialVariance Example

Flexible Budget MaterialVariance Example

ActualCost

$677,875

BQ × BP40,000 × $16.25

$650,000

AQ × BP42,500 × $16.25

$690,625

$12,750 F $40,625 U

$27,875 U

7 - 38

Flexible Budget LaborVariance Example

Flexible Budget LaborVariance Example

ActualCost

$277,350

BQ × BP20,000 × $13.00

$260,000

AQ × BP21,500 × $13.00

$279,500

$2,150 F $ 19,500 U

$17,350 U

7 - 39

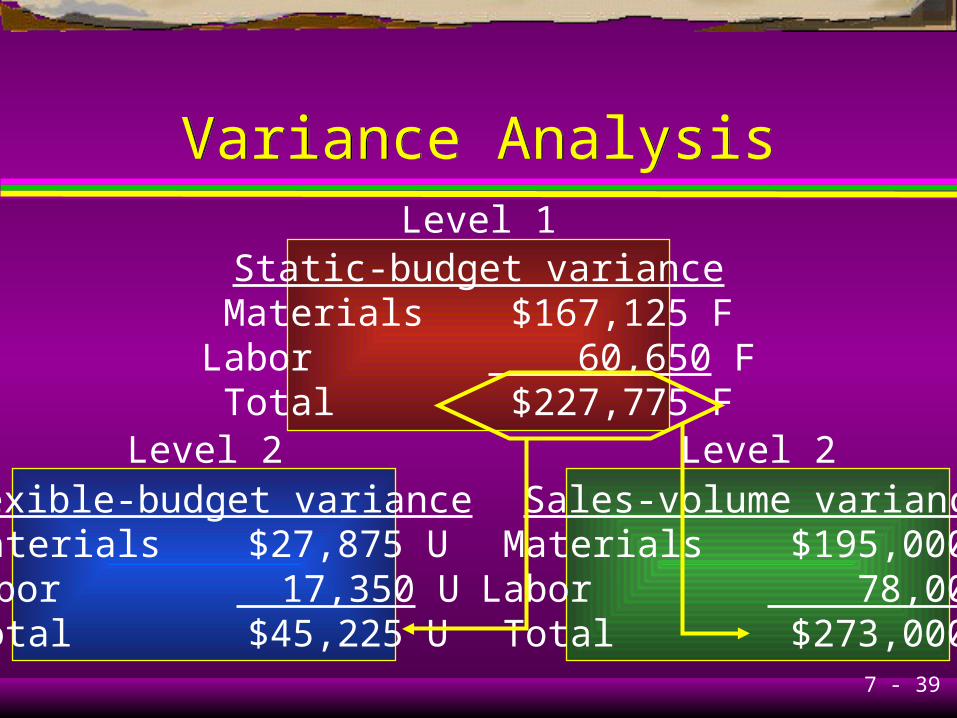

Static-budget varianceMaterials $167,125 FLabor 60,650 FTotal $227,775 F

Flexible-budget varianceMaterials $27,875 ULabor 17,350 UTotal $45,225 U

Sales-volume varianceMaterials $195,000 FLabor 78,000 FTotal $273,000 F

Level 1

Level 2

Variance AnalysisVariance Analysis

Level 2

7 - 40

Flexible-budget varianceMaterials $27,875 ULabor 17,350 UTotal $45,225 U

Price varianceMaterials $12,750 FLabor 2,150 FTotal $14,900 F

Efficiency varianceMaterials $40,625 ULabor 19,500 UTotal $60,125 U

Level 2

Level 3

Variance AnalysisVariance Analysis

Level 3

7 - 41

Learning Objective 5Learning Objective 5

Explain why purchasingperformance measures should

focus on more factors thanjust price variances.

7 - 42

Performance MeasurementUsing Variances

Performance MeasurementUsing Variances

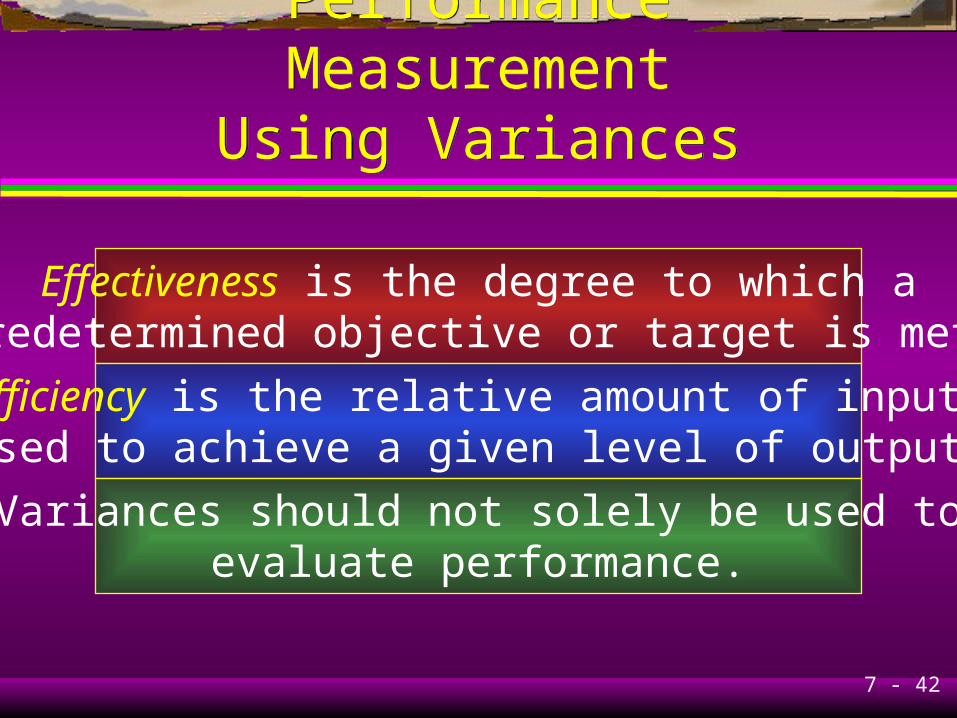

Effectiveness is the degree to which apredetermined objective or target is met.

Efficiency is the relative amount of inputsused to achieve a given level of output.

Variances should not solely be used toevaluate performance.

7 - 43

When to Investigate VariancesWhen to Investigate Variances

When should variances be investigated?

Subjective judgments

Rules of thumb as “investigate all variancesexceeding $10,000 or 25% of expected cost,

whichever is lower.”

7 - 44

Learning Objective 6

Integrate continuousimprovement

into variance analysis.

7 - 45

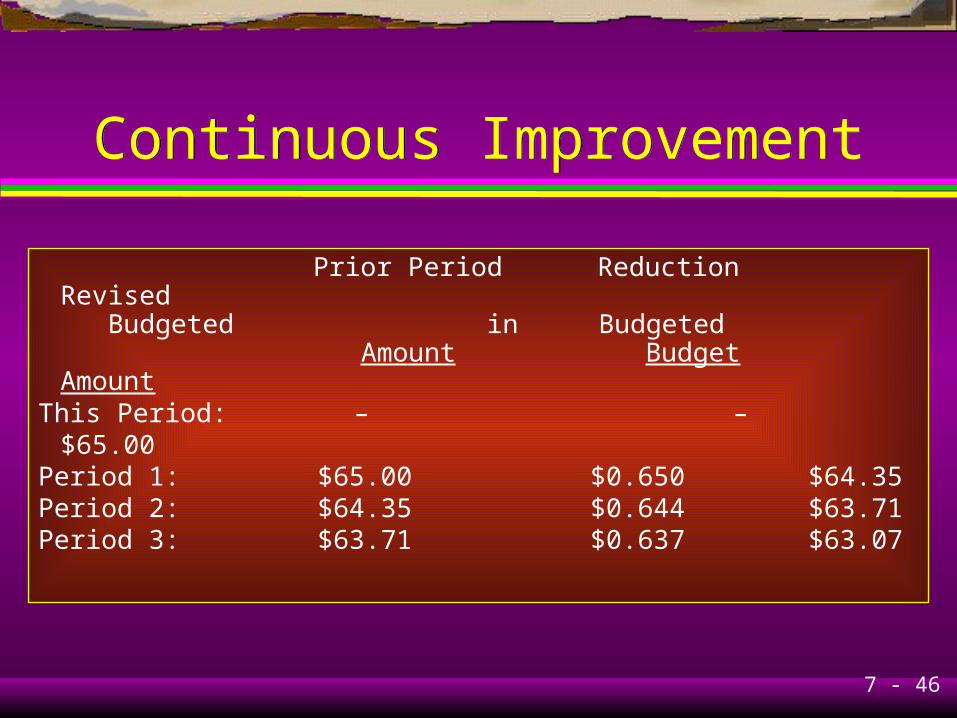

Continuous ImprovementContinuous Improvement

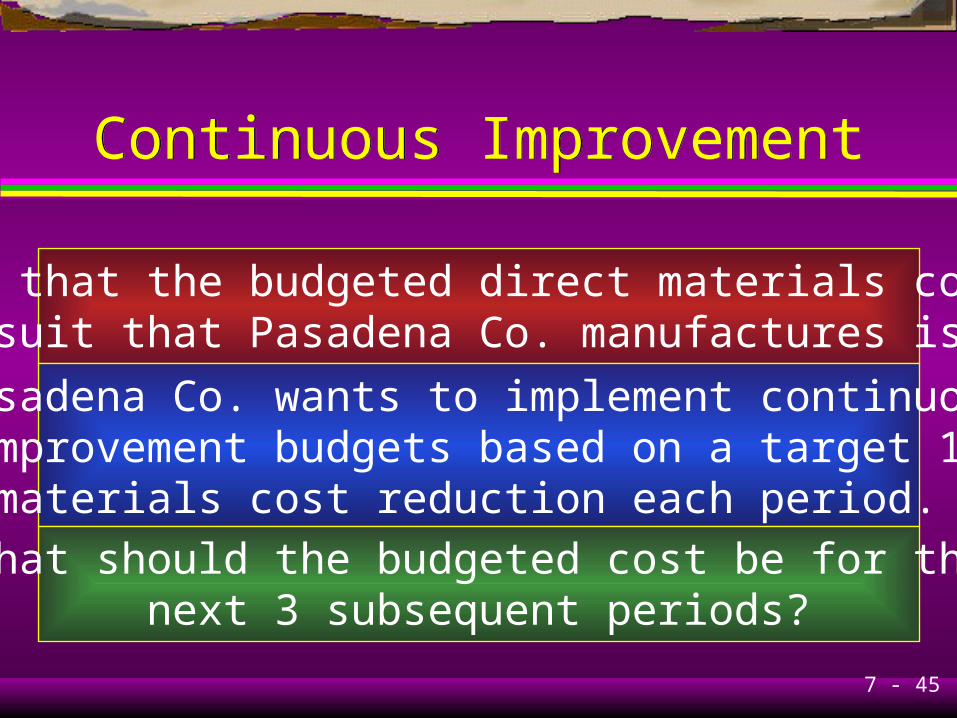

Assume that the budgeted direct materials cost foreach suit that Pasadena Co. manufactures is $65.

Pasadena Co. wants to implement continuousimprovement budgets based on a target 1%

materials cost reduction each period.

What should the budgeted cost be for thenext 3 subsequent periods?

7 - 46

Continuous ImprovementContinuous Improvement

Prior Period Reduction Revised Budgeted in Budgeted

Amount Budget AmountThis Period: – – $65.00Period 1: $65.00 $0.650 $64.35Period 2: $64.35 $0.644 $63.71Period 3: $63.71 $0.637 $63.07

7 - 47

Learning Objective 7

Perform variance analysis inactivity-based costing systems.

7 - 48

Flexible Budgeting andActivity-Based CostingFlexible Budgeting andActivity-Based Costing

Materials costs and direct manufacturing laborcosts are examples of output-unit level costs.

Batch-level costs are resources sacrificedon activities that are related to a group of

units of product(s) or service(s) rather thanto each individual unit of product or service.

7 - 49

Flexible Budgeting andActivity-Based CostingFlexible Budgeting andActivity-Based Costing

Denver Co. produces metal planters (MP).

Assume that material-handling labor costs varywith the number of batches produced rather

than the number of units in a batch.

Material-handling labor costs are direct batchlevel costs that vary with the number of batches.

7 - 50

Flexible Budgeting and Activity-Based Costing

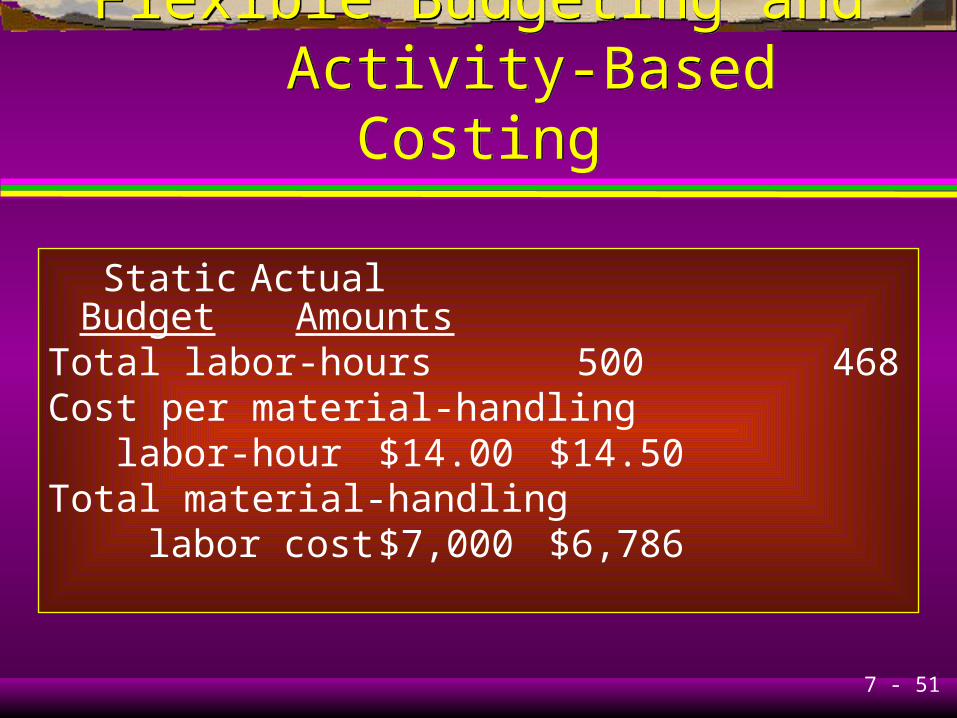

Flexible Budgeting and Activity-Based Costing

Static ActualBudget Amounts

Units produced and sold 18,000 15,660Batch size 180 174Number of batches 100 90Material-handling labor-hours per batch 5.00 5.20

7 - 51

Flexible Budgeting and Activity-Based Costing

Flexible Budgeting and Activity-Based Costing

Static ActualBudget Amounts

Total labor-hours 500 468Cost per material-handling labor-hour $14.00 $14.50Total material-handling

labor cost $7,000 $6,786

7 - 52

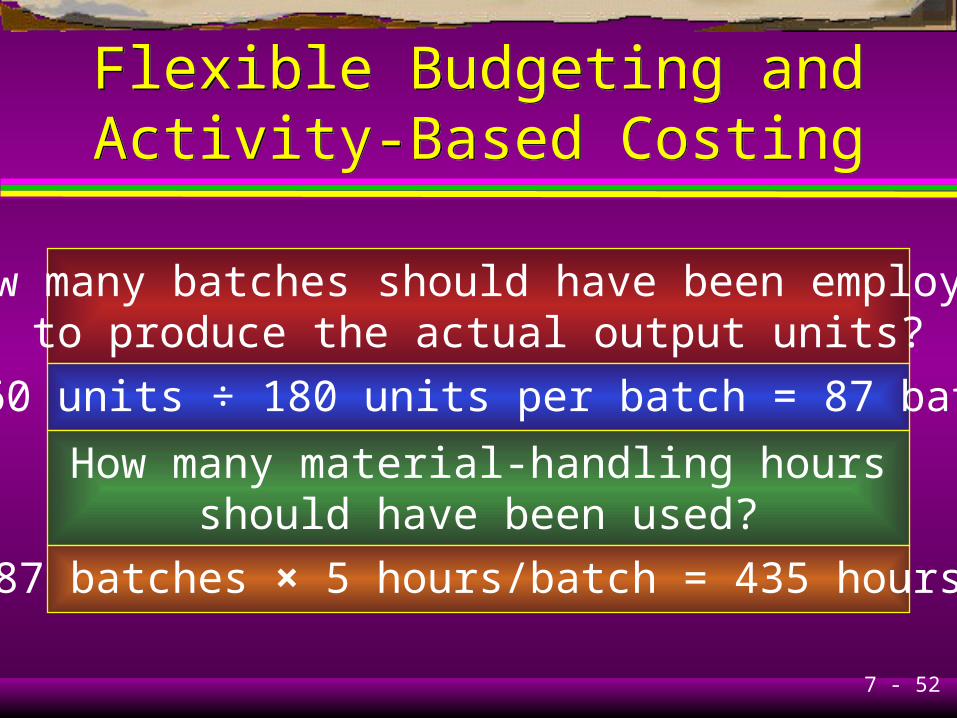

Flexible Budgeting andActivity-Based CostingFlexible Budgeting andActivity-Based Costing

How many batches should have been employedto produce the actual output units?

15,660 units ÷ 180 units per batch = 87 batches

How many material-handling hoursshould have been used?

87 batches × 5 hours/batch = 435 hours

7 - 53

Flexible Budgeting andActivity-Based CostingFlexible Budgeting andActivity-Based Costing

What is the flexible budget formaterial-handling labor-hours?

435 hours × $14.00/labor-hour = $6,090

Flexible-budget costs $6,090 Actual costs 6,786 Flexible-budget variance $ 696 U

7 - 54

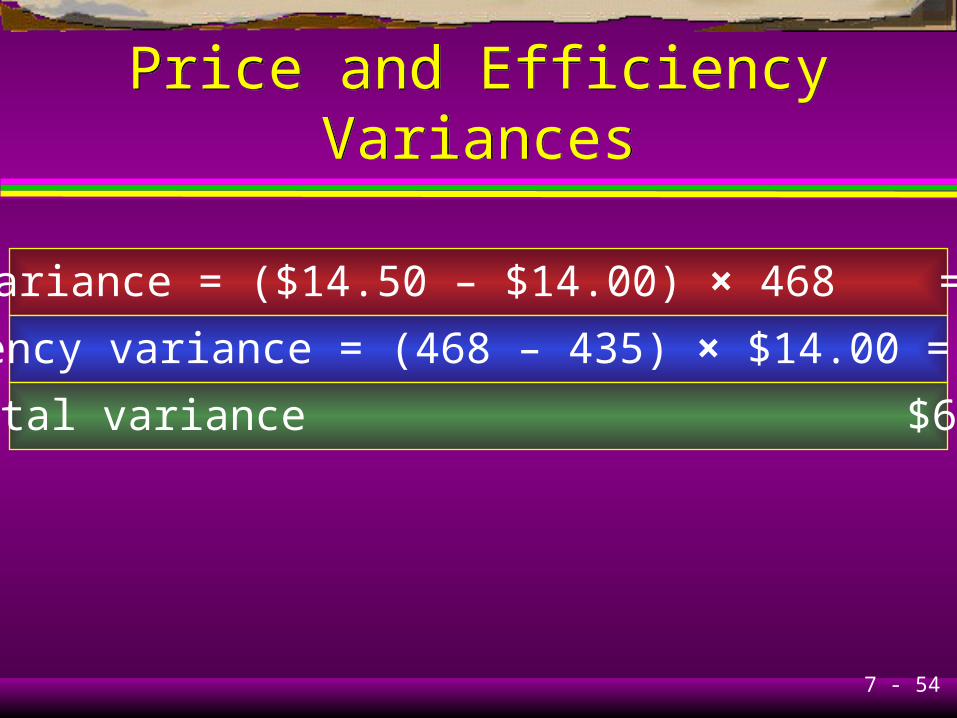

Price and Efficiency VariancesPrice and Efficiency Variances

Price variance = ($14.50 – $14.00) × 468 = $234 U

Efficiency variance = (468 – 435) × $14.00 = $462 U

Total variance $696 U

7 - 55

Learning Objective 8

Describe benchmarkingand how it is used

in cost management.

7 - 56

BenchmarkingBenchmarking

It refers to the continuous process ofmeasuring products, services, and activities

against the best levels of performance.