6895208 Public Pvt Sector Banks

22

Public Sector and Private Sector Banks in India: A Comparison SIES College of Management Studies Idea Research Paper Series A Research Initiative by Students Idea research is research essentially driven by students. The objective of this endeavour is to inculcate and develop research culture and rigour amongst our students right from the beginning through encouraging student- centric research. The research undertaken under this initiative would essentially be short-term, impact-based, yet simple. The objective is also to encourage a mutually symbiotic relationship between corporates and the student community at SIESCOMS through a targeted dissemination of the research outcomes. The papers carry the names of the authors and should be cited accordingly. The views, findings, and interpretations expressed in this paper are entirely those of the authors. They do not represent the views of SIESCOMS and its management. These working papers would be available online at www .si e s c oms. e du . No part of the paper can be reproduced

-

Upload

jerome-randolph -

Category

Documents

-

view

17 -

download

2

description

dfsfsatedwrt

Transcript of 6895208 Public Pvt Sector Banks

Public Sector and Private Sector Banks in India: A Comparison

SIES College of Management StudiesIdea Research Paper Series

A Research Initiative by Students

Idea research is research essentially driven by students. The objective of this endeavour is to inculcate and develop research culture and rigour amongst our students right from the beginning through encouraging student-centric research. The research undertaken under this initiative would essentially be short-term, impact-based, yet simple. The objective is also to encourage a mutually symbiotic relationship between corporates and the student community at SIESCOMS through a targeted dissemination of the research outcomes. The papers carry the names of the authors and should be cited accordingly. The views, findings, and interpretations expressed in this paper are entirely those of the authors. They do not represent the views of SIESCOMS and its management. These working papers would be available online at www .si e s c oms. e du . No part of the paper can be reproduced in any form without the prior permission of the authors. However, they can be quoted by citing the reference.

Idea Research Paper /06

Public Sector and Private Sector Banks in India: A Comparison

Abstract

What are the trends observed in the performance of Public Sector and Private Sector Banks? How do they perform when compared across the critical parameters of profitability, Non-performing Assets, deposits and lending, and cost of funds? This paper is a modest effort to compare public and private sector banks on the basis of eleven such crucial parameters. The various challenges and opportunities confronting the Public sector banks and Private sector banks have also been discussed.

Research Team

The research team consisted of the following PGDBF 1st year students:

Dishita Visaria

Komal Pahwa

Megha Gadge

Namita Pai

Nidhi Bhandari

Priya Girath

Faculty Guide: Dr. Vandita Dar, Associate Professor, Economics, SIES College of Management Studies, [email protected]

IntroductionThe Indian financial system comprises of four segments or components. These are financial institutions,

financial markets, financial instruments and financial services. Banks come under the financial institutions segment. Financial institutions are intermediaries that mobilize savings and facilitate allocation of funds in an efficient manner.The Indian financial system was quite well developed even prior to India’s political independence in August 1947. Both foreign and domestic banks were present and so was a well-developed stock market. Until the 1990s, the Indian financial system was tightly regulated. Following the balance of payments crisis in 1991-92, a stabilization program was initiated with the help of International Monetary Fund, which specifically included a reform of the financial system. The foundation for the financial sector reforms was laid by recommendations of the Committee on Financial System 1991 (Narasimham Committee). The Committee again reviewed the financial system in 1998 and made further recommendations. The objectives of the financial sector reforms were to bring about greater efficiency and competitiveness in all the spheres of the economic activity.

Banking in India has its origin in Vedic times, i.e. 2000 to 1400 BC. Indigenous bankers and moneylenders have played a vital role for centuries. Modern banking in India emerged between the 18 th and beginning of 19th centuries. In 1683, the officers of East India Company set up the first bank in Madras. Between 1770 and 1850 banks such as Bank of Hindustan, Commercial Bank, Calcutta Bank, Bank of Calcutta and Bank of Bombay. Later, Commercial Bank and Calcutta Bank merged to form Union Bank. Three Presidency Banks i.e. Bank of Bombay, Bank of Madras and Bank of Bengal which were set up between 1809 and 1843 were amalgamated to form the Imperial Bank of India in 1921.The Imperial Bank of India later became the State Bank of India.

The sudden boom of investment in the 1900’s led to the emergence of leading joint stock banks such as the Punjab National (1895), Bank of India (1906), Indian Bank (1907), Bank of Baroda (1909), Central bank of India (1911) and Union Bank of India (1919). The major functions of these banks were to finance foreign trade while domestic trade was largely handled by the Multani Shroffs and moneylenders. Between 1941 and 1945, the number of banks increased from 473 to 737 but these banks suffered from certain limitations such as inadequate capital structure and unsound methods of operations and management. Thus, the government in consultation with Reserve Bank of India enacted the Banking Companies Act in 1949. Between 1947 and 1969 banks were under private ownership of maharaja’s, or king s of the princely states of India and these banks served the rich families and industrial houses which narrowed the industrial growth of the banking system.

The Reserve Bank of India thus made it compulsory for reconstruction and / or merger of the weak units with the sound one’s as per the Banking Companies Act of 1960 and the number of banks declined from 548 in 1947 to 89 in 1969. Fourteen private banks were nationalized on July 19, 1969 and another six in 1980. One of the objectives of nationalization was to extend the reach of organized banking to rural areas and neglected sections of the society.

Between 1969 and 1992, there was rapid expansion of bank network. The number of bank branches increased from 8262 to 60570. The banking system spread to rural areas. Small Scale, tiny and cottage industries benefited from the spread of banking system. The share priority sector in total banking grew up from14 percentage in 1969 to 43% in 1990 and banking density improved from 64000 people per branch in 1969 to 14000 people per branch in 1991.

Public Sector BanksPublic sector banks are the ones in which the government has a major holding. They are divided into two

groups i.e. Nationalized Banks and State Bank of India and its associates. Among them, there are 19 nationalized banks and 8 State Bank of India associates. Public Sector Banks dominate 75% of deposits and 71% of advances in the banking industry (Indian financial system, by Bharti Pathak, 2003)

Private Sector BanksPrivate sector banks came into existence to supplement the performance of Public sector banks and serve

the needs of the economy better. As the public sector banks were merely in the hands of the government, banks had no incentive to make profits and improve the financial health. Nationalized killed competition and stifled competition in banking. Banks operated in regulatory environment with administered rate of interest structure, quantitative restrictions on credit flows, high reserve requirements and significant proportion of lend able resources going to the priority and government sectors. This resulted in low levels of investment and growth, decline in productivity and erosion of profitability of banking sector. Thus, Narasimham Committee I (1991) which recommended the free entry of new banks in the financial market provided they confirm the minimum start up capital and other requirements by the permission of Reserve Bank of India. Currently there are 31 Private Sector Banks, which includes 23 old, and 8 new banks. (Indian financial system, by Bharti Pathak, 2003)

Performance of Public and Private Sector Banks: A Comparison

The performance and the roles of private and public sector banks are undergoing changes. The banks, both private as well as public have to now operate in an increasingly competitive environment. The competition for public sector banks is coming from the private sector banks. Despite having the advantage of a substantial presence and penetration in the rural areas, the public sector banks are under tremendous pressure to maintain their margins and to survive the competition. The customer-centric approach of private sector banks have thrown open many more challenges for the public sector banks especially in retaining customers and expanding customer base.

We have compared Public and Private sector banks based on 11 parameters, which are critical while evaluating their performance. These criteria are as follows:1. Assets and Liabilities2. Share in Aggregate Deposits3. Priority Sector Lending4. Sensitive Sector Lending5. Credit Deposit Ratio6. Cost of Funds and Return on Funds7. Operating Profit and Net Profit8. Net Profitability of Banks9. Gross and Net NPAs10. Capital Adequacy Ratio11. ATM’s

The analysis and statistics for the above is depicted below-

1. Liabilities and Assets of Banks

As you can see below the percentage of total assets and liabilities of New Private sector banks is higher than the Public sector Banks

On the back of robust economic growth and industrial recovery, loans and advances witnessed strong growth, investments, in a rising interest rate scenario. Deposits showed a lackluster performance in the wake of increased competition from other saving instruments. Borrowings and net-owned funds (capital and reserves and surplus), however, increased sharply underscoring the growing importance of non-deposit resources of SCBs. Bank group-wise, assets of new private sector banks grew at the highest rate, followed by public sector banks and old private sector banks

Source: RBI NOTE: Scheduled commercial banks (SCBs) consist of 28 public sector banks (State Bank of India and its seven associates, nationalized banks and other public sector bank (one)), 9 new private sector banks, 20 old private sector banks and 31 foreign banks.

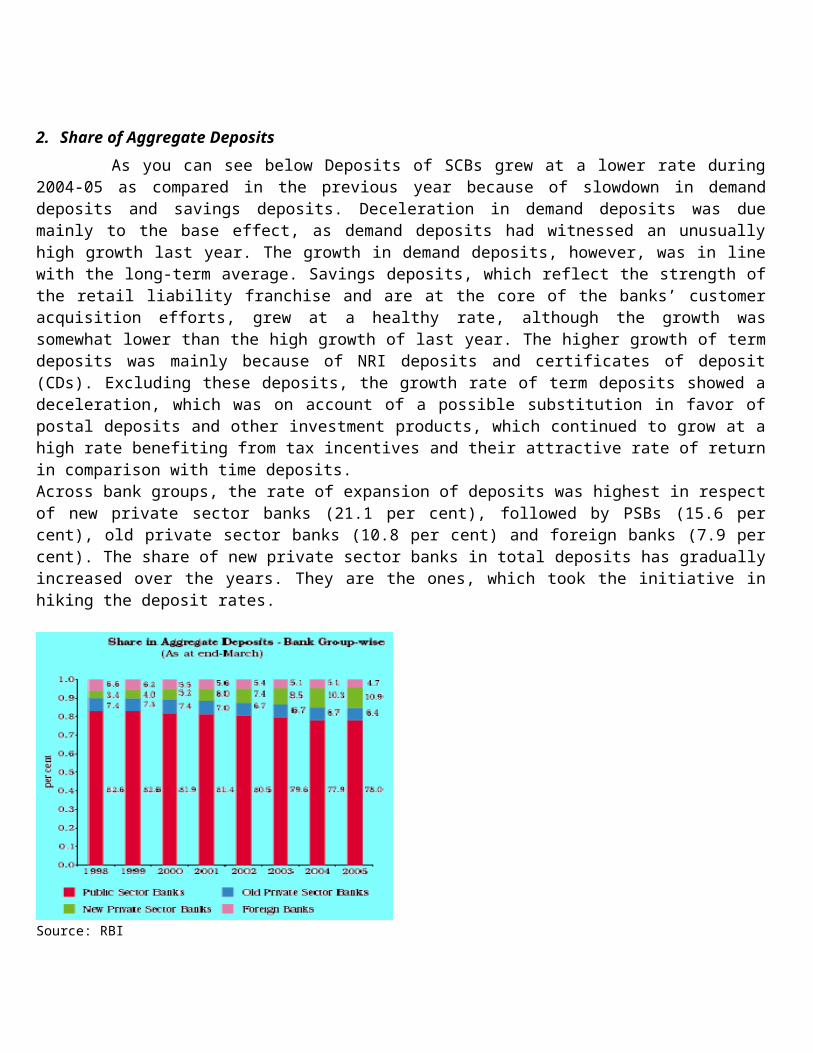

2. Share of Aggregate Deposits

As you can see below Deposits of SCBs grew at a lower rate during 2004-05 as compared in the previous year because of slowdown in demand deposits and savings deposits. Deceleration in demand deposits was due mainly to the base effect, as demand deposits had witnessed an unusually high growth last year. The growth in demand deposits, however, was in line with the long-term average. Savings deposits, which reflect the strength of the retail liability franchise and are at the core of the banks’ customer acquisition efforts, grew at a healthy rate, although the growth was somewhat lower than the high growth of last year. The higher growth of term deposits was mainly because of NRI deposits and certificates of deposit (CDs). Excluding these deposits, the growth rate of term deposits showed a deceleration, which was on account of a possible substitution in favor of postal deposits and other investment products, which continued to grow at a high rate benefiting from tax incentives and their attractive rate of return in comparison with time deposits.Across bank groups, the rate of expansion of deposits was highest in respect of new private sector banks (21.1 per cent), followed by PSBs (15.6 per cent), old private sector banks (10.8 per cent) and foreign banks (7.9 per cent). The share of new private sector banks in total deposits has gradually increased over the years. They are the ones, which took the initiative in hiking the deposit rates.

Source: RBI

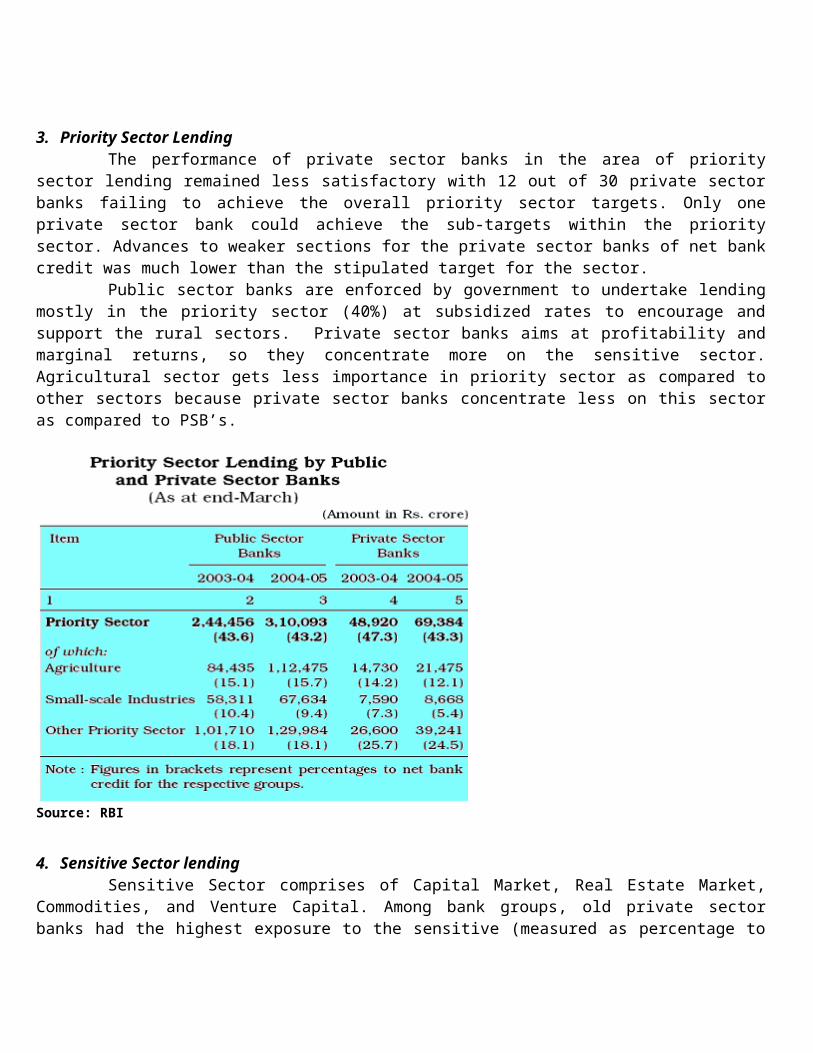

3. Priority Sector LendingThe performance of private sector banks in the area of priority sector lending remained less

satisfactory with 12 out of 30 private sector banks failing to achieve the overall priority sector targets. Only one private sector bank could achieve the sub-targets within the priority sector. Advances to weaker sections for the private sector banks of net bank credit was much lower than the stipulated target for the sector.

Public sector banks are enforced by government to undertake lending mostly in the priority sector (40%) at subsidized rates to encourage and support the rural sectors. Private sector banks aims at profitability and marginal returns, so they concentrate more on the sensitive sector. Agricultural sector gets less importance in priority sector as compared to other sectors because private sector banks concentrate less on this sector as compared to PSB’s.

Source: RBI

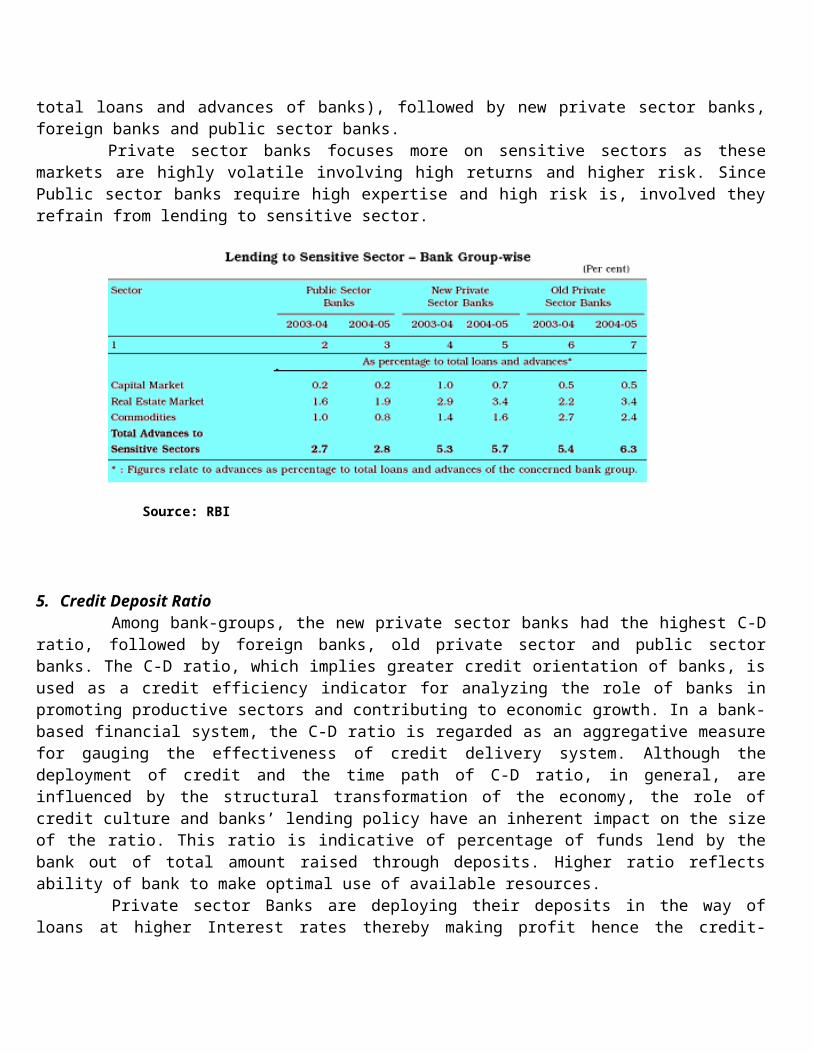

4. Sensitive Sector lendingSensitive Sector comprises of Capital Market, Real Estate Market, Commodities, and Venture Capital.

Among bank groups, old private sector banks had the highest exposure to the sensitive (measured as percentage to total loans and advances of banks), followed by new private sector banks, foreign banks and public sector banks.

Private sector banks focuses more on sensitive sectors as these markets are highly volatile involving high returns and higher risk. Since Public sector banks require high expertise and high risk is, involved they refrain from lending to sensitive sector.

Source: RBI

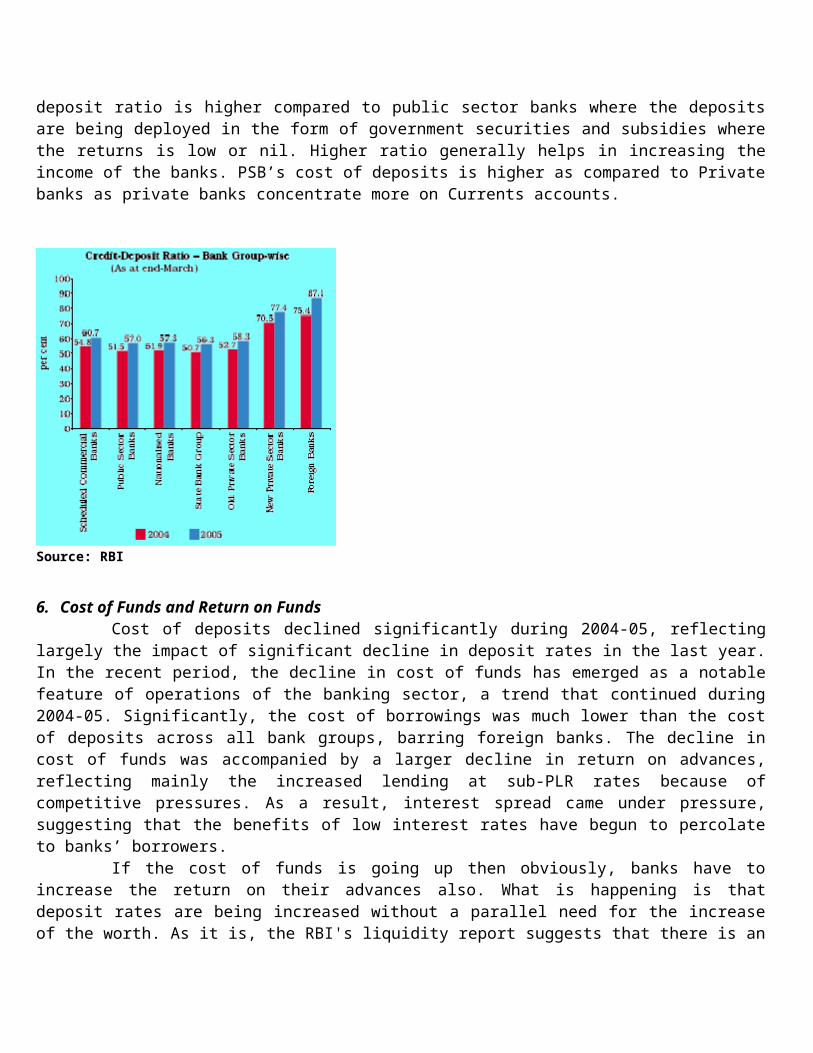

5. Credit Deposit RatioAmong bank-groups, the new private sector banks had the highest C-D ratio, followed by foreign

banks, old private sector and public sector banks. The C-D ratio, which implies greater credit orientation of banks, is used as a credit efficiency indicator for analyzing the role of banks in promoting productive sectors and contributing to economic growth. In a bank-based financial system, the C-D ratio is regarded as an aggregative measure for gauging the effectiveness of credit delivery system. Although the deployment of credit and the time path of C-D ratio, in general, are influenced by the structural transformation of the economy, the role of credit culture and banks’ lending policy have an inherent impact on the size of the ratio. This ratio is indicative of percentage of funds lend by the bank out of total amount raised through deposits. Higher ratio reflects ability of bank to make optimal use of available resources.

Private sector Banks are deploying their deposits in the way of loans at higher Interest rates thereby making profit hence the credit-deposit ratio is higher compared to public sector banks where the deposits are being deployed in the form of government securities and subsidies where the returns is low or nil. Higher ratio generally helps in increasing the income of the banks. PSB’s cost of deposits is higher as compared to Private banks as private banks concentrate more on Currents accounts.

Source: RBI

6. Cost of Funds and Return on FundsCost of deposits declined significantly during 2004-05, reflecting largely the impact of significant

decline in deposit rates in the last year. In the recent period, the decline in cost of funds has emerged as a notable feature of operations of the banking sector, a trend that continued during 2004-05. Significantly, the cost of borrowings was much lower than the cost of deposits across all bank groups, barring foreign banks. The decline in cost of funds was accompanied by a larger decline in return on advances, reflecting mainly the increased lending at sub-PLR rates because of competitive pressures. As a result, interest spread came under pressure, suggesting that the benefits of low interest rates have begun to percolate to banks’ borrowers.

If the cost of funds is going up then obviously, banks have to increase the return on their advances also. What is happening is that deposit rates are being increased without a parallel need for the increase of the

worth. As it is, the RBI's liquidity report suggests that there is an excess of liquidity. If it is so then why the banks are taking the deposits at much higher rate of interest. Since banks are taking the deposit at much higher rate of interest than the real rate at which they should take it, they feel that the interest on the advances should be increased.

Source: RBI

7. Operating and Net ProfitNet profits declined by 7.0 per cent (excluding the conversion impact i.e. conversion of non-banking

entity to banking entity) during 2004-05 as against an increase of 30.4 per cent in the last year. While net profits of nationalized banks, old private sector banks and foreign banks declined, those of SBI group and new private sector banks increased. Sharp increase in the net profits of new private sector banks was because of a sharp decline in provision and contingencies (loans).

Banks operating profit is calculated after deducting administrative expenses, which mainly includes salary cost and network expansion cost. Operating margins are profits earned by banks on its total interest income. Net Profit is calculated after deducting various cost of funds, since the cost of funds i.e. the borrowing costs are higher as compared to the lending rates offered, the PSB’s net profit is lesser compared to the private banks.

Source: RBI

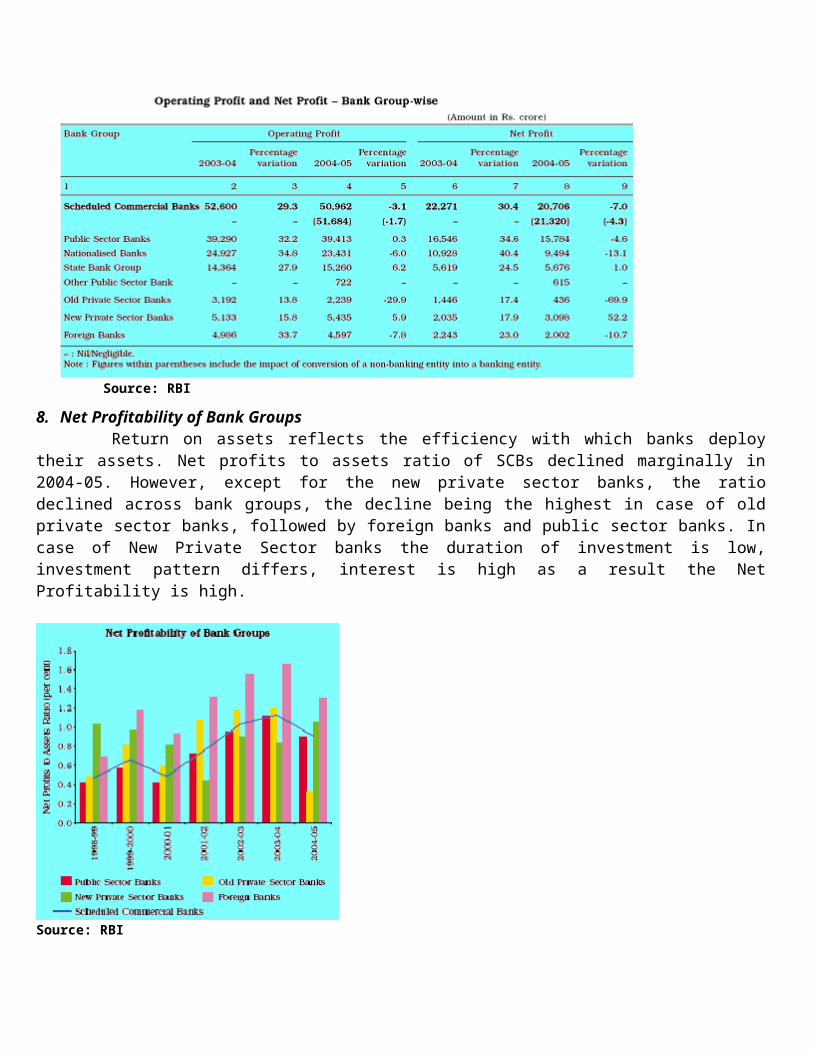

8. Net Profitability of Bank GroupsReturn on assets reflects the efficiency with which banks deploy their assets. Net profits to assets ratio

of SCBs declined marginally in 2004-05. However, except for the new private sector banks, the ratio declined across bank groups, the decline being the highest in case of old private sector banks, followed by foreign banks and public sector banks. In case of New Private Sector banks the duration of investment is low, investment pattern differs, interest is high as a result the Net Profitability is high.

Source: RBI

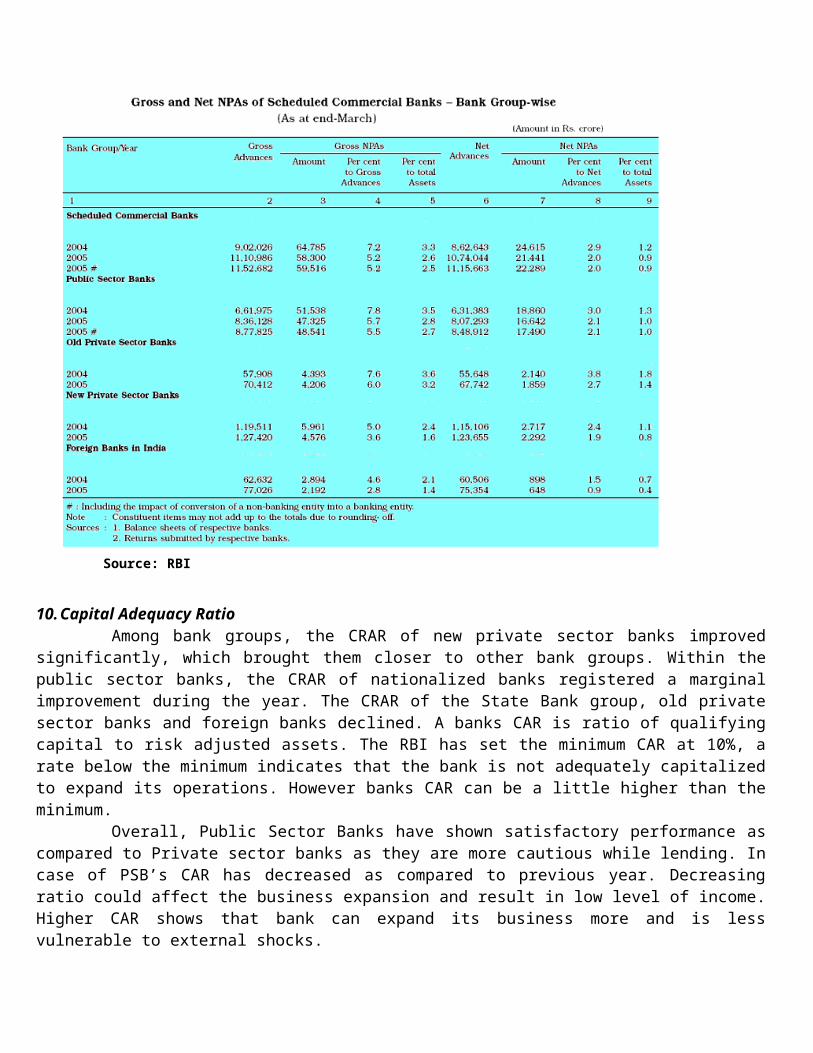

9. Gross and Net NPAs

With provisioning for NPAs being somewhat lower during 2004-05, the decline in the NPA ratio was attributable to both increased recovery of NPAs and overall reduction in asset slippages. In absolute terms, non-performing assets in ‘doubtful’ category increased, while those in sub-standard category declined sharply, reflecting the change in asset classification norm from the year ended March 2005, whereby an asset was treated as doubtful if it remained as NPA for 12 months as against the earlier norm of 18 months. However, NPAs in doubtful category as percentage of net advances declined significantly.

PSB's NPA ratio is satisfactory compared to private banks. Higher NPAs ratio shows that bank is unable to maintain the quality of its loans however; the ratio has been decreased compared to previous year. Private banks NPA ratio is higher as they are offering loans without having required deposits to lend them. PSB's have a better management and monitoring over their deposits and the defaulters, which may turn its lent amounts into a debt that could be returned by its defaulters comfortably as compared to the Private banks.

Source: RBI

10. Capital Adequacy RatioAmong bank groups, the CRAR of new private sector banks improved significantly, which brought

them closer to other bank groups. Within the public sector banks, the CRAR of nationalized banks registered a marginal improvement during the year. The CRAR of the State Bank group, old private sector banks and foreign banks declined. A banks CAR is ratio of qualifying capital to risk adjusted assets. The RBI has set the minimum

CAR at 10%, a rate below the minimum indicates that the bank is not adequately capitalized to expand its operations. However banks CAR can be a little higher than the minimum.

Overall, Public Sector Banks have shown satisfactory performance as compared to Private sector banks as they are more cautious while lending. In case of PSB’s CAR has decreased as compared to previous year. Decreasing ratio could affect the business expansion and result in low level of income. Higher CAR shows that bank can expand its business more and is less vulnerable to external shocks.

Source: RBI

11. ATMsTotal number of ATMs installed in the country was 17,642 at end-March 2005. New private sector

banks constituted the largest share of ATMs, followed by the SBI group, nationalized banks, old private sector banks and foreign banks. While nationalized banks and old private sector banks had more on-site ATMs than off-site ATMs, SBI group, new private sector banks and foreign banks had more off-site ATMs than on-site ATMs.

Source: RBI

Strategies and Challenges

Public Sector BanksThe public sector banks are turning the spotlight on the customer and offering quicker, better service. That

includes everything from ATM machines and computerized branches to never before seen marketing initiatives. Clearly, public sector banks have woken up to competition. Post-liberalization, several new generation private sector banks changed the face of the industry. Customers no longer had to stand in long queues or make 10 trips for loans to be sanctioned. These changes are taking place at a particularly fast pace in few of the banks including the State Bank of India, Corporation Bank, Indian Bank, Bank of Baroda and the Union Bank of India.

Private sector banks brought in concepts like customer relations officers focused marketing teams and single window banking. Moreover, with new technology, private sector banks like ICICI and HDFC Bank could offer customer services like ATMs, phone banking, internet banking, automatic money transfer, mobile banking, Core banking solutions and computerized monthly statements.Recently a new technology of cheque truncation is being introduced. As against physical travel of instruments, under cheque truncation only the image of the instrument would travel. This would totally alter the face of clearing systems facilitating faster realization of instruments. It is currently being implemented on a pilot basis in India.

Public sector banks’ focus had earlier remained on industrial credit, which was slowing down. Lending to corporates meant higher margins for banks. As interest rates came down corporates began to consider alternate sources of funds. Banks then began to explore possibilities like retail lending.

The two important challenges for public sector banks are: To maintain profitability inspite of government norms and regulations, as to maintain their PLR. Put in place appropriate technology of excellent standards that will make them be seen more as virtual

banks rather than brick and mortar. This will lead to consolidation of their respective network. They must be given autonomy -- operational

and administrative -- and be completely board driven, including in the selection of the chief executive officer. Finally, they must be taken out of the purview of the Central Vigilance Commission, even if it entails bringing them under the Companies Act. They need to improve in the services like ATMs, Credit and Debit cards. They lack behind in providing facilities like loans and other accounts. These branches are not interlinked with each other and customers visiting hours are less.

Private Sector Banks

There are two types of private sector banks, the old and the new. As far as the old (mostly regional banks) are concerned, inadequacy of capital will lead to their mergers sooner rather than later. Private sector banks have good technology for handling transactions and also offer attractive products, but it cannot be said that corporate governance and risk management are far superior to that of the Public Sector Banks. Some of the most important challenges for private sector banks are:

Priority sector credit: Generally, private sector banks lend money to individuals and corporate sector whereas sectors like agriculture, small-scale industries and retail trade small business is neglected.

Consolidation and Convergence: The recent merger that happened was of Lord Krishna Bank with Centurion Bank. RBI may be inclined to approve the merger. The regulator, which has been insisting on promoters of smaller banks to lower their holdings, would possibly prefer such mergers. Centurion Bank of Punjab needs the additional business to compensate for its relatively higher cost structures. It can cross-sell its banking products through the LKB network, including traditional banking products and fee-based services like wealth management products, to affluent NRI customers.

ConclusionIn any banking system, no bank -- public or private -- can survive unless it continuously strives to

transform its organization into a self-governing, self-correcting and self-adjusting entity.For banks to grapple with these problems and manage the future, structural and institutional rigidities need to be eased in two critical areas: comprehensive legal support for recovery of bad debts and a fundamental change in the pattern of governance for the PSBs.

While public sector banks are in the process of restructuring, private sector banks are busy consolidating through mergers and acquisitions (the sector has been recently opened up for foreign investments). PSB’s need to improve in the services like ATM’s, Credit and Debit cards. They lack behind in providing facilities like loans and other accounts. These branches are not interlinked with each other and working hours are less.

In case of Private sector banks customers are not aware of the facts and hidden costs in view, as there are various products and facilities provided by the banks. The charges that are been taken are also too high. Challenges and Opportunities exist for both the public sector as well as the private sector banks, their nature however differs.

From the 11 parameters, we have identified 3 areas of challenges separately for private and public sector banks. The Credit Deposit Ratio of Private sector banks is better compared to PSB’s The Capital Adequacy Ratio of PSB’s is satisfactory compared to that of Private Banks The Net Profit of PSB’s is better than Private Sector

References

1. Publications; Trends and Progress in India- Operations and Performance of Commercial Banks: www.rbi.org.in

2. RBI’s New Initiatives, the ICFAI University Press, May 20063. Bharati V. Pathak, Indian Financial System, Pearson Education Pvt. Ltd., 2003

Annexure

At present, there are 20 old private sector banks and 9 new private sector banks. The private sector banks, which have been formed after the banking sector reforms in 1991 are called as the new private sector banks. Below are the names of old and new private sector banks.

Old Private Sector Banks

1. Bank of Rajasthan Ltd. 2. Bharat Overseas Bank Ltd. 3. Catholic Syrian Bank Ltd.4. City Union Bank Ltd. 5. Dhanalakshmi Bank Ltd.6. Federal Bank Ltd.7. Ganesh Bank of Kurundwad Ltd8. ING Vysya Bank Ltd. 9. Jammu and Kashmir Bank Ltd. 10. Karnataka Bank Ltd. 11. Karur Vysya Bank Ltd. 12. Lakshmi Vilas Bank Ltd.13. Lord Krishna Bank Ltd. 14. Nainital Bank Ltd.15. Ratnakar Bank Ltd.16. Sangli Bank Ltd.17. SBI Commercial and International Bank Ltd18. South Indian Bank Ltd.19. Tamilnad Mercantile Bank Ltd. 20. United Western Bank Ltd.

New Private Sector Banks

1. Bank of Punjab Ltd. 2. Centurion Bank Ltd. 3. Development Credit Bank Ltd. 4. HDFC Bank Ltd.5. ICICI Bank Ltd. 6. IndusInd Bank Ltd.7. Kotak Mahindra Bank Ltd.8. UTI Bank Ltd. 9. Yes Bank Ltd.