![Class 3 Ab + L AbL Review d/ dt [ AbL ] = k on [ Ab ][L] – k off [ AbL ]](https://static.fdocuments.in/doc/165x107/56815b21550346895dc8dddd/class-3-ab-l-abl-review-d-dt-abl-k-on-ab-l-k-off-abl-.jpg)

Class 3 Ab + L AbL Review d/ dt [ AbL ] = k on [ Ab ][L] – k off [ AbL ]

Upload

homeworkping3Category

view

189download

0

Branch OperationsCase Study

Document ID: ABL Branch Study

Proprietary and Confidential Information

Allied Bank LimitedLahore, Pakistan

By

Ibrahim Software

Document & Data Control

1. Project Information

Customer: Allied Bank Limited

Project: Typical Branch Operations Study

2. Document Information

Name: ABL Branch Study

Version: 1.0

Author(s): Sohail Aziz, Ijaz Ajmal, Nauman-ul-Haq

Approver(s): Mujahid Ali

Creation Date: 7th April 2006

3. Revision History

Author Date Version Description

ABL Typical Branch Operations Study

Table of Contents

Overview..............................................................................................................................5

Facilities visited..................................................................................................................5

Organization Structure.....................................................................................................6

1. General banking.....................................................................................................7

1.1 Account Opening Formalities...............................................................................7

1.2 Account Opening & Maintenance Process..........................................................71.2.1 Account Types...................................................................................................................................7

1.2.2 Initial Deposit Limit...........................................................................................................................7

1.2.3 Account Opening Forms (Package)...................................................................................................8

1.3 ATM Card Issuance............................................................................................20

1.4 Cash Deposit.........................................................................................................21

1.5 Cash Withdrawal.................................................................................................231.5.1 Cheque Dishonor..............................................................................................................................24

1.6 Physical Cash Management................................................................................251.6.1 Cash Management at Branch...........................................................................................................25

1.6.2 Cash Transfer...................................................................................................................................26

1.6.3 Cash Management at Main Branch..................................................................................................27

1.6.4 NIFT Operations..............................................................................................................................28

1.7 Bills........................................................................................................................291.7.1 Demand Draft...................................................................................................................................29

1.7.2 Pay Order.........................................................................................................................................33

1.7.3 DAC (Deposit at Call)......................................................................................................................34

1.7.4 Rupees Travelers Cheque (RTC).....................................................................................................35

1.7.5 Telegraphic Transfer (TT) / Mail Transfer (MT).............................................................................35

1.8 Clearing................................................................................................................361.8.1 Local Clearing..................................................................................................................................36

1.8.2 Inter City Clearing...........................................................................................................................39

1.9 Outward / Inward Bills for Collection (OBC/IBC)..........................................40

Ibrahim Fibres Limited 1 of 101

ABL Typical Branch Operations Study

1.9.1 OBC / IBC........................................................................................................................................40

1.10 Transfers...............................................................................................................42

1.11 Online Transactions.............................................................................................42

1.12 Term Deposit........................................................................................................451.12.1 SNDR..........................................................................................................................................45

1.12.2 PLS Based Term Deposit Receipt...............................................................................................46

1.12.3 Premium plus Account................................................................................................................46

1.12.4 Allied Profit Plus.........................................................................................................................48

1.12.5 Premium Term Deposit...............................................................................................................48

1.13 Inter Branch Transactions (Pak Account)........................................................48

1.14 ATM Operations..................................................................................................49

1.15 Locker Operations...............................................................................................51

1.16 Utility Bills............................................................................................................54

1.17 Prize Bonds...........................................................................................................55

1.18 General Accounts.................................................................................................561.18.1 Sundry Account...........................................................................................................................56

1.19 General Processes................................................................................................571.19.1 Daily Vouchers............................................................................................................................57

1.19.2 Advance Deposit and Advance Rent...........................................................................................57

1.19.3 Executive Visits...........................................................................................................................58

1.19.4 Peon Book...................................................................................................................................58

1.19.5 Stamps in Hand...........................................................................................................................58

1.19.6 Inward / Outward Dak.................................................................................................................58

1.19.7 Book of instructions....................................................................................................................59

1.19.8 Online List of Branches and Controlling Offices........................................................................59

1.19.9 Circular’s Index...........................................................................................................................59

1.19.10 Office Orders...............................................................................................................................60

1.19.11 Inter Branch Signature Book (IBS/AS).......................................................................................60

1.19.12 Keys Handling.............................................................................................................................60

1.19.13 Inventory Management...............................................................................................................61

1.19.14 Fixed Assets................................................................................................................................62

Ibrahim Fibres Limited 2 of 101

ABL Typical Branch Operations Study

1.19.15 Attendance Management.............................................................................................................62

1.19.16 Expenses......................................................................................................................................63

2 Finances................................................................................................................64

2.1 Advances...............................................................................................................65

2.2 Imports..................................................................................................................662.2.1 L.C Opening Process........................................................................................................................66

2.2.2 L.C Processing.................................................................................................................................66

2.3 Exports..................................................................................................................672.3.1 Export Process..................................................................................................................................67

2.4 Credit Application Package................................................................................682.4.1 Exposure Summary..........................................................................................................................69

2.4.2 Facility Summary.............................................................................................................................69

2.4.3 Sanction Advice...............................................................................................................................69

2.4.4 Basic Information Report (BIR)......................................................................................................69

2.5 Credit Approval...................................................................................................742.5.1 Security Type Descriptions..............................................................................................................76

2.6 Credit Administration Department (CAD).......................................................792.6.1 Disbursement Authorization Certificate (DAC) Issuance................................................................79

2.6.2 Security Document Management.....................................................................................................80

2.6.3 MIS Reporting..................................................................................................................................81

2.6.4 Vigilance Officer..............................................................................................................................82

3 Home Remittance Cell (HRC)............................................................................84

3.1 Remittances Processing.......................................................................................84

3.2 MIS Reporting.....................................................................................................85

4 Central Processing...............................................................................................87

4.1 Nostro Account Reconciliation...........................................................................87

4.2 Pak Account Reconciliation................................................................................89

4.3 Allied Bank Rupee Travelers Cheque................................................................89

Ibrahim Fibres Limited 3 of 101

ABL Typical Branch Operations Study

5 Alternate Delivery Channels...............................................................................90

5.1 ATM Card Generation........................................................................................90

5.2 Call Center...........................................................................................................91

5.3 SWIFT..................................................................................................................92

6 Special Asset Management (SAM).....................................................................94

7 Manual Registers.................................................................................................95

Ibrahim Fibres Limited 4 of 101

ABL Typical Branch Operations Study

OverviewThis document is based upon the study conducted to analyze the business processes and

practices being followed at a typical branch of Allied Bank. We have taken Allied Bank’s

Kashmir Road Branch as a “model branch” and have tried to cover maximum areas and

functions which exist within daily routine of Branch Operations.

Purpose of this study was to go through the existing business processes to identify the

room for improvements and Business Process re-engineering with the use of Information

Technology and specifically software systems e.g. introduction of workflows, integration

of information and centralization of database

Facilities visiteda. Kashmir Road Branch, Lahore

b. Nappier Road Branch, Lahore

c. CAD Office, Upper Mall, Lahore

d. FI, Cash Management, Trade Tower, Karachi

e. Central Processing (ABRTC, Reconciliation),Trade Tower, Karachi

f. ADC (SWIFT Center, ATM, Call Center),Central Office, Karachi

g. HRC, Saima Trade Tower, Karachi

Ibrahim Fibres Limited 5 of 101

ABL Typical Branch Operations Study

Organization Structure

Ibrahim Fibres Limited 6 of 101

ABL Typical Branch Operations Study

1. General banking

1.1 Account Opening Formalities

To open an account, different set of documents is required, depending upon type of

account. For example, individuals and joint accounts require a valid Computerized

National Identity Card (CNIC) or passport to open an account. An introducer is required,

preferably from the same branch / bank to get a new account opened.

1.2 Account Opening & Maintenance Process

1.2.1 Account Types

The main accounts types in ABL are

In Pak Rupee

i. PLS Saving

ii. Current

iii. Premium Plus

iv. Term Account

In Foreign Currency

i. Saving

ii. Current

iii. Term Account

Foreign currency accounts can only be opened in US$, JPY, GBP and Euro.

1.2.2 Initial Deposit Limit

a. Account opening is considered as non-financial information in system; this can be

opened without even a single rupee. There is no initial deposit limit for account

opening.

b. As a matter of general practice, an initial deposit of Rs.500 is required for opening a

new account. However special accounts of Zakat Mustahqeen, widows etc can be

opened with Rs.100.

Ibrahim Fibres Limited 7 of 101

ABL Typical Branch Operations Study

c. Initial deposit limit for foreign currency account is US $1,000. or equal amount in any

other currency.

Possible Improvements:

a. System should help in enforcement of initial deposit limit at the time of opening the

account, except for the accounts used by branch for its own certain requirements like

collection account etc.

b. Due to lower initial deposit limit, this is an observation of bank staff that those people

approach to get the account opened, who are not entertained by other banks due to

higher initial deposit limit. Mechanism needs to be defined to encourage the higher

initial deposit limit. As an example ABN AMRO does not provide cheque books to

the accounts holders having less then Rs.100,000 as an initial deposit at opening the

account. They encourage using ATM to small account holders.

1.2.3 Account Opening Forms (Package)

The account opening application package contains following forms in it:

a. Application Form (same for all types of accounts)

b. Signature Card(s)

c. ATM Form

d. KYC Form for Personal Accounts

e. KYC Form for Company Accounts

Account opening forms are physically placed in binder containing 50 to 70 forms and are

stored in strong room for the purpose of record, till undefined period. Proper inventory

management is not in place to handle this record.

Possible Improvements:

a. Lot of redundancy of information is there in different forms being used to collect

information. These forms should be made simple and more informative

b. There should be separate forms for Personal and Company Accounts

Ibrahim Fibres Limited 8 of 101

ABL Typical Branch Operations Study

c. Proper Inventory Management should be introduced for maintaining the record of

account opening forms at branches.

Information in the main application form is as follows:

1.2.3.1 Account Number

a. Account number is mandatory and comprises of following information:

CC-TTT-NNNN-X

Currency-Type-Number-Check Digit

Different currency codes and separate TT for each currency and type of accounts are

defined in UniBank

b. “Account Opening/Closing Register” is used to record all accounts opened and

closed in branch. This register is audited by the auditors to verify the account opening

formalities.

c. “FC Account Opening/Closing Register” is used to record all accounts opened and

closed in branch.

d. System doesn’t provide next available account number, user have to check it

manually so that no number is skipped in between. A list of next 100 account

numbers along with “check digit” is maintained manually to cover this shortcoming

of system. This is applicable to both local and foreign currency accounts.

Possible Improvements:

a. In account numbering it is possible to have same account number for different

branches. It is suggested that account number should be unique within the bank, so

that there should be no issue, even in case if certain branches are merged together.

b. Also needs to devise a mechanism to eliminate multiple accounts of a single customer

of same type in a branch(s).

1.2.3.2 Photograph

a. As per current practice, photograph is required for identification of customer who

can’t sign and use thumb impression or customers whose signatures are simple and

can easily be copied.

Ibrahim Fibres Limited 9 of 101

ABL Typical Branch Operations Study

b. Photograph is pasted on SS Card and account opening form. SS Card is scanned for

usage.

Possible Improvements:

a. System should have the provision to store photograph for customers / account

holder(s).

b. Biometrics scan of “thumb impression” should also be there so that identification of

client can be made within the centralized customer database. This technology is also

required as photographs of account holders become old dated, because no mechanism

is there to update photographs.

c. Customer should be encouraged to submit photographs. There should be some

mechanism to keep these photographs updated in the system.

1.2.3.3 Account Major Information (Account Title, NIC, Address)

a. Customer Name / Title information is mandatory in the system. There is fixed coding

scheme defined for Occupation or Business (Economic Sector, Line of Business).

Although this information is defined in the system but it is not being followed

properly by branches.

Possible Improvements:

a. Economic Sector, line of business usage should be properly conveyed to the branches.

Its usage can also be made mandatory.

b. Existing system does not have the provision to record more than one NIC number,

phone and address (either for business or home address).

c. System should provide a query to search account holder on the basis of CNIC and

Biometrics.

d. Multiple accounts of same type can be opened with the same CNIC. System should

prompt when same CNIC exists in database.

Ibrahim Fibres Limited 10 of 101

ABL Typical Branch Operations Study

1.2.3.4 Minor’s information

a. For minor’s information, date of birth is mandatory for account opening. This can be

verified from B-Form, Birth certificate, matriculation certificate, passport or any one

of these documents. Father’s or Mother’s NIC is required for account opening and

can also be fed in the system.

b. When the minor reaches the age of 18, the account is closed for minor and new

account is opened up. The general practice is that branch people mention the maturity

date on signature card. There is no information of minor account in the system.

Possible Improvements:

a. There should be some option in the system to prompt or restrict user from withdrawal

when the minor reaches the age of 18, so that he/she can be asked to operate the

account on his / her own authority and the status of account can be updated

accordingly.

b. System should provide information on the basis of account type.

1.2.3.5 Operating Instructions

a. This information is used to define the operational authority of the account, weather it

can be operated singly, jointly, either or survivor etc. System does not have the

provision to store this information.

b. In general practice, these instructions are written on SS Card (Specimen Signature

Card) so that these can be referred at the time of withdrawal transactions.

Possible Improvements:

a. Operating instructions should be properly parameterized in new system for an online

referral to account details at counters for proper their implementation.

1.2.3.6 Zakat Deductions

a. There are two options for the customer:

i. Allows bank to deduct Zakat

ii. Customer submits an affidavit that he/she will pay Zakat by himself / herself.

Ibrahim Fibres Limited 11 of 101

ABL Typical Branch Operations Study

b. Zakat deduction and computation feature is available in system for PLS saving

accounts and PPA operational account only. But the return submitted to SBP, routed

through COK is prepared manually.

Possible Improvements:

System should cater computation and deduction of Zakat from all applicable accounts.

Moreover the reporting requirements of SBP (product wise deduction of Zakat) should be

generated through system.

1.2.3.7 Address of Contact Person / Next of Kin Information

a. This information is gathered to ascertain the whereabouts of client. Incase of death of

account holder the claimer can claim up to Rs.30,000 by submitting an affidavit along

with other documents like death certificate. In case amount is above Rs.30,000,

succession certificate is also required along with other requirements.

Possible Improvement:

a. Next of kin information should be available in the system as currently manual form is

used for reference in case of any such requirement.

1.2.3.8 Special Instructions

a. There could be certain instructions from account holder that needs to be followed

while operating an account for example, if the Cheque amount is more then Rs.25,

000, then NIC should be taken from the drawer.

b. This information is hand written on SS Card and scanned for online referral, while

operating account.

Possible Improvements:

a. Special instructions should be properly parameterized in the new system for an online

referral to account details at counters for their proper implementation.

b. Special instructions and operating instructions should be placed in a sequence on

application form.

Ibrahim Fibres Limited 12 of 101

ABL Typical Branch Operations Study

1.2.3.9 Specimen Signature Card

a. For scanning of signature cards, scanners are available at all branches. Cards are

scanned and made available at the terminals for withdrawal so that teller can verify

the signatures. Multiple cards against one account can be stored.

b. Cash Deposit in-charge is responsible for scanning and record keeping.

c. In addition to the signature following additional information, if required, is written /

pasted on it.

i. Minor’s information

ii. Operating Instructions

iii. Special Instructions

iv. Photograph

e. System provides the facility to change the SS Card on request from client.

1.2.3.10 Introducer

a. Introducer should have minimum one year old active account with the bank.

b. Verification is normally done through the client as he/she is asked to get it verified

from the respective branch of that introducer.

c. Introducer is only responsible for the genuineness of the client identity and address

information. In special cases introducer can be from other bank as well and the person

has to get his signature verified from that branch.

Possible Improvements:

a. System should store information of introducer

b. Account opening date and other information of Introducer (if he/she is from other

branch) should be available from new system for verification on request.

c. Letter of thanks should be automatically printed or emailed from system. System

should keep track of the status of posting of letters.

1.2.3.11 Authorized Personnel Information

a. In case of personal account, this information is duplicated on the form where as for

other accounts directors or authorized personnel information is stored

Ibrahim Fibres Limited 13 of 101

ABL Typical Branch Operations Study

Possible Improvements:

a. The information regarding the authorized persons should be available in new system.

System should also cater partners, sole proprietor or director’s information.

1.2.3.12 Terms & Conditions

Possible Improvements:

a. System should help to identify / restrict the user to the clause 5 “mentioned on form”

that is “Only one account in a particular type can be opened in the same name within

same branch.

b. This is also important in ref to answer queries from different investigation agencies

e.g. NAB, which is interested to know the accounts opened against a given NIC.

1.2.3.13 Know Your Customer

a. There are two Performa’s available for KYC:

i. For Personal / Individuals Accounts (annexure A)

ii. For Company / Corporate Account (Annexure B)

b. Know Your Customer Form is an interview based Performa. It is mandatory and its

filling is audited by the audit department.

c. KYC form includes information of customer accounts with banks other than ABL.

d. System currently has one flag, which is to be enabled to indicate that all the KYC

information is captured manually

Possible Improvements:

a. This information can be made as part of main form, as most of the information is

already there, while missing fields can be incorporated within main form.

b. Signature should be made required for this, which can help in making information

authentic.

c. KYC information should be fed in the system.

d. KYC form should contain information of customer’s other accounts in other branches

of ABL.

Ibrahim Fibres Limited 14 of 101

ABL Typical Branch Operations Study

e. In general practice, the form is filled by the bank staff on their own rather than asking

the account holder.

1.2.3.14 Cheque Book Issuance

a. Separate cheque book is issued for each type of account (Pak Rupee/Foreign

currency)

b. In normal procedure, cheque book is not issued at the time of opening of account. It is

provided later and a separate request form is used for this purpose.

c. Entries are made into “Cheque Books Issuance” manual register with

acknowledgement from receiver.

d. There are two options to get the cheque book issued:

i. In manual procedure, a hand written request is launched to COK, mentioning the

account numbers and Title of Account against which cheque book is required.

NIFT send these cheque books directly to branches after completing the

procedure with stationary wing at COK.

ii. The second option introduced recently is to raise the requisition through UniBank.

This requisition is received by Inventory department at COK and the cheque

books are then forwarded to respective branch through NIFT.

e. System maintains the records of last three cheque book series. If a cheque is

presented from a cheque book which is closed, then one active cheque book is closed

and related cheque book is activated by consulting the “cheque book register” from

where start cheque number and number of leaf information are taken.

f. To cancel multiple cheques within one cheque book, there is no range option

available to select multiple cheques; user has to do it one by one leaf.

Possible Improvements:

a. System should provide the track of authorized person responsible for issuance of

cheque book.

b. System should keep track of all received and issued cheque books.

c. The instructions on the requisition slip should be compared with other banks and

should be standardized.

Ibrahim Fibres Limited 15 of 101

ABL Typical Branch Operations Study

d. All the cheques not presented should be available for withdrawal in new system

1.2.3.15 Profit Calculations

a. In PLS A/C, profit provisioning is done monthly on projected rates, decided at the

start of the periods (starting from Jan & July).

b. Profit is credited to the accounts periodically at the rate decided by the Bank. There

may be a difference between the projected and actual profit rates.

c. Withholding tax (i.e. 10%) is deducted from the profit after it is credited to accounts.

d. For PLS saving accounts profit calculation is made on the minimum balance available

from 7th to end of each month. In case Account is closed before six months then the

client can claim the profit but it is generally not been claimed.

Possible Improvements:

a. System should provide an inquiry on profit provisioned against accounts.

b. Pay order of deducted withholding tax amount should also be generated by system.

Tax chalan of withholding tax should also be auto generated.

1.2.3.16 Dormant and Inactive Accounts

a. If the account is not operative up till six months then it becomes Dormant. If the

account is not operative for 2 years its status is converted to “Inactive”.

b. Transactions in Dormant/Inactive accounts are accepted in system by use of certain

level (authority).

c. Both the statuses can be reverted back to “Active”. For this an application is required

from the account holder to complete the process.

Possible Improvements:

a. System should provide reporting on dormant and inactive accounts.

b. After certain period, Zero balance accounts are automatically closed by UniBank.

Staff at branches is not very much aware of the process followed by the software in

this regard.

Ibrahim Fibres Limited 16 of 101

ABL Typical Branch Operations Study

c. In general practice, if the account is dormant then the banker does not contact the

client. There should be a mechanism to inform customer in these cases.

1.2.3.17 Account Closing Process

a. To close an A/C, a written application is required along with the deduction / charges

of Rs.250.

b. Un-used leaves of cheque books need to be returned by the account holder. People

usually withdraw the entire amount and do not apply to close the account.

c. Account closing information is also updated in “Account Opening Register”

1.2.3.18 Deduction on Minimum Balance

A monthly deduction of Rs.50 is made from the accounts for maintaining average balance

less then Rs.10,000. This is done through the software and is not applicable on certain

accounts e.g. salaried, widows, pensioners and government employee’s accounts.

Following table shows picture of the data captured on account opening forms (package)

and incorporation of this information in existing system:

Account Opening Application Fields StatusBranch Code Date Account Number Term Deposit Number Type of Accounts Pak. Rupees Account Foreign Currency Account Currency Particulars of AccountsTitle of Account Initial Deposit N.I.C / Passport Number Occupation / Business Business Address Account Opening Application Fields Residence Address National Tax Number Tel (Off.) Fax

Ibrahim Fibres Limited 17 of 101

ABL Typical Branch Operations Study

Tel (Res.) Mobile E-mail Particulars of Term DepositAmount Tendered for Term Deposit of Period Days Months Years Roll over for same period With / Without Profit Instructions for disbursement of Profit (Monthly, Quarterly, Half Yearly, Yearly, On Maturity)Minor Info Date of Birth of Minor Date of Attaining Maturity Name of Guardian Operating Instructions The Account shall be Operated by Singly / Jointly Either or Survivor / any one singly Zakat Deduction Yes / No Address of Contact Person / Next of Kin Name Address Telephone No. Special Instructions Other Bank Services to be usedOn-line banking Facilities ATM / Debit Card Credit Card Safe Deposit Lockers Bank Account Statement (Monthly, Quarterly etc) IntroducerSignature Account No. Branch Banks Name Address NIC No. Tel (Off.) Tel (Res.)

Ibrahim Fibres Limited 18 of 101

ABL Typical Branch Operations Study

Mobile number E-mail Nature of Account (Individual, Partner Ship, etc.) Personal Info of Authorized Persons to operate account Name S/O, D/O, W/O NIC / Passport No. Date of Birth Nationality / Resident of Occupation / Business Name of Employer Signature / Thumb Impression Cheque book / Term Deposit Receipt Acknowledgement Received Cheque book Received Term Deposit Receipt No. Date Customer Signature Account Opening Authorized by Signature Name IBS No. Cheque Book Issued Cheque Book No. From Cheque Book No. To Authorized Officer’s Signature Term Deposit Receipt Issued Term Deposit Receipt No. Dated Authorized Officer’s Signature Acknowledgement Name Signature of Bank Official Customer’s Signature Right Thumb Impression Left Thumb Impression Allied Cash +First Name Sur Name Mother’s Maiden Name / Key Word Card #

Ibrahim Fibres Limited 19 of 101

ABL Typical Branch Operations Study

1.3 ATM Card Issuance

ATM issuance procedure contains following steps:

a. Customer fills in the additional Allied Cash + application Form. Except “mother

name” or “key word” all the information on this form is redundant to main account

opening form.(For ATM Card Generation Process, please refer to topic 4.4)

b. Once the card is received at branch, it is entered in the manual “ATM Issuance

Register”. The PIN information is received separately from card and usually with one

day’s delay

c. Customer approaches Manager Operation’s and acknowledges receipt by signing the

“ATM Issuance Register”.

d. In next step, customer approaches to Chief Manager for PIN Issuance and signs a

separate “ATM Pin Issuance Register”.

e. In last step the customer has to approach Manager Operation’s to get the ATM card

activated in system.

Possible Improvements:

a. System should hold complete ATM particulars of customer.

Ibrahim Fibres Limited 20 of 101

ABL Typical Branch Operations Study

b. Procedure of ATM issuance should be hassle free like credit card, where customer

does not need to collect ATM card from branch. Phone banking or Internet banking

can be a thought for card activation and PIN Code generation as many banks are

using it now days.

c. Information on ATM form is same like account opening form except sur name and

mother name/key word. Missing information can be part of account opening form to

avoid dual information.

1.4 Cash Deposit

a. Deposit slips for PLS and Current Accounts are different (in color as well). There are

two portions of deposit slip, one portion is given to the depositor with cash received

stamp and the other is kept for bank record. In case of shortage of deposit slips,

photocopies are used.

b. All the cash deposit transactions are first written in manual register “Long Book for

Cash Deposit” and are then entered in to the system. For foreign currency accounts

“FC Long Book” is maintained

c. At the time of posting, a super code for transactions above Rs.10,000 is randomly

generated by the system, which is written on the voucher. This number is required at

the time of supervision of transaction.

d. Posting details are available on instrument while passing it through MICR (Magnetic

Ink Character Recognition) machine.

e. In case of mistake in filling the deposit slip i.e. wrong account number or account

title, bank retains the amount in “Sundry Account”. After that either the customer is

contacted or just waited to claim the amount. Amount is credited to account after

getting an application and a photocopy of counter part of deposit slip.

Ibrahim Fibres Limited 21 of 101

ABL Typical Branch Operations Study

Possible Improvements:

a. Different deposit slips for Current and PLS Accounts can be made single (this

practice is being followed in other banks).

b. After introducing MICR, there should be no need to emboss stamps on instruments

like deposit slips and cheques.

c. Customer should leave counter when all system entry is done and a printing is made

by MICR, in this way long book can be discontinued.

d. Carbonized paper can be used for deposit slip to avoid double writing on counter

folio.

e. Due to absence of “Automated Token System”, usually a mess is created at teller

windows. Token system can help people to approach counter on their turn. Likewise,

utility bills counter can be different from general operations.

f. Limit of supervision entry can be enhanced.

g. By bringing the deposits related data feeding in real time mode, “Sundry Account

Register” can be discontinued.

Ibrahim Fibres Limited 22 of 101

ABL Typical Branch Operations Study

h. Seating arrangements at cash counters should be such that document movement can

be made easy till supervision step.

1.5 Cash Withdrawal

a. Cheque is presented at teller window. The instrument is first verified by teller and

then by MICR machine, which helps in identification of fake instruments.

b. Cheque is then verified from the system for “availability of balance”, “signatures”

and operating instructions if any. Instrument is then put in MICR to print posting

details.

c. Transaction is posted in the system. In case amount is equal to or higher than

Rs.10,000, transaction is supervised by another officer.

d. Withholding tax is deducted for amounts above than Rs.25,000, which is calculated

manually at the moment.

e. At the time of cash receipts and payments, denomination details are written on the

back of instrument which is used for the verification of the amount.

f. Transaction is written in the “Cashier Payment Long Book”. For foreign currency

accounts, a separate “FC Long Book” is maintained

Ibrahim Fibres Limited 23 of 101

ABL Typical Branch Operations Study

Possible Improvements:

a. System should calculate withholding tax charges of cheque amount more than

Rs.25,000 (or any other applicable tax). In case of unavailability of balance in

account, provision to record the transaction should be there in system, so that the

amount should be auto deducted on availability of the balance.

b. In principle cash payments to customer should be made after transaction is supervised

in system.

c. Seating arrangements at cash counters should be such that document movement can

be made easy till supervision step.

1.5.1 Cheque Dishonor

a. In case of cheque dishonor, there is a memorandum of reasons to attach with the

cheque while returning it back to the presenter.

b. To record the returned cheque transaction and to get its acknowledgement from

customer “Cheque Return Register” is maintained. This also helps to record details of

Ibrahim Fibres Limited 24 of 101

ABL Typical Branch Operations Study

deducted charges against dishonored cheques. Cheque return charges are Rs.200. per

instrument.

Possible Improvements:

System should maintain cheque return details like instrument number, date, amount,

return charges and reason.

1.6 Physical Cash Management

1.6.1 Cash Management at Branch

a. Every branch has certain limit approved for cash in hand which is insured as well.

Excess cash is transferred to main / controlling branch (Napier Road in this case). As

a practice minimum foreign currency is also maintained at branch. In case of any

inward clearing or withdrawals, foreign currency is arranged from main branch.

b. In case of excess cash retained at branch, a letter to regional office or directly to

insurance company for insurance coverage is written.

c. Within branch, both foreign currency and Pak rupee cash is placed in main safe,

located in strong room. Details of the amount taken In and Out are recorded each time

in a manual register “Cash In/Out register” with denomination details. Customer

Service Manager is responsible for cash in / out record and for reconciliation of

physical cash kept in main safe.

d. Daily cash reconciliation record is maintained in “Cashier Memo Book” with

denomination details. For reconciliation of foreign currency “FC Cashier Memo

Book” is maintained with currency and denomination details.

e. “Cashier Memo Book” contains information of cash closed on each day in following

details:

i. Unsorted Cash

ii. Sorted Cash (Issue able cash, Non - Issue able cash)

Ibrahim Fibres Limited 25 of 101

ABL Typical Branch Operations Study

1.6.2 Cash Transfer

a. Every branch has got a limit approved and insured for retention of cash. In case of

shortage or excess of cash, the main branch is informed on phone to arrange

transportation (send / receive) of cash. during transportation, cash in-transit is also

insured.

b. Cash sent to main branch is categorized in two heads i.e. Sorted and Un-sorted.

Different stamps are used to identify both categories of cash.

c. “Cash in-`Transit” is credited during transfer and debited same day on receiving

advice from controlling branch. Its details are recorded in manual register “Cash in

Transit Register”.

Possible Improvements:

a. System should treat physical cash available within main safe as “inventory”. All In

and out transactions should be recorded in system so that physical cash can be auto

reconciled in proper denominations at end of each day. In this case “Cashier memo

book” and “Cash In/Out Register” can be discontinued

Ibrahim Fibres Limited 26 of 101

ABL Typical Branch Operations Study

b. During cash transfer, cash in-transit transactions should be recorded and advices

should be generated through the system so that manual advices and “Cash in Transit

Register” can be discontinued.

c. Cash transfer should be made through system request rather to make a phone call or

fax to controlling branch. In this case proper documentation can also be maintained.

1.6.3 Cash Management at Main Branch

Main branch (Napier Road) is “Cash Chest” branch for Lahore and neighboring cities.

This branch is responsible to deliver cash, in case any branch request for cash shortage

and collects cash if any branch have excess cash than approved limit. This branch is also

responsible for transactions with SBP and other banks.

It covers 70 branches for its services. Cash transfer arrangements are made with Phoenix

security agencies. Currently branch has four vehicles, provided by Phoenix to serve all 70

branches.

1.6.3.1 Cash Transfer to Branches

a. Branches use fax or make a telephone call to main branch for cash requirement. If

amount is above than 0.5 million, then a counter signature of regional head is also

required.

b. Request details are maintained in “Intimation Register” with date and time.

c. “Cash Payment/Receipt Register” is maintained for cash transfers.

d. Due to shortage of vehicles Cash Chest Manager makes a route for cash delivery

(normally four routs to cover Lahore). Separate bags are maintained for each branch.

A seal is applied on each bag by Phoenix people and seal number is noted on

shipment document. Shipment document have three copies (one for main branch, one

for phoenix and one for receiving branch)

e. Van can carry maximum 200 million in a trip as per instruction of Phoenix. If more

than 200 million has to be transferred then main branch informs Phoenix and also to

insurance agency.

f. Private vehicle can not be used for cash transfers as per instructions

Ibrahim Fibres Limited 27 of 101

ABL Typical Branch Operations Study

1.6.3.2 Cash Collection from Branches

a. In case of excess cash, branches make a telephone call to main branch (and security

agency, in certain cases) to send vehicle for cash collection.

b. Shipment document along with cash is received at cash chest and respective branch is

informed telephonically on receiving of cash. Pak account advice is sent to branch

through courier next day.

c. For cash in wallet “Cash Chest Book” is maintained with denomination details.

d. Main branch sorts the cash before submitting it to SBP. 15 cash sorters are dedicated

to this exercise.

e. “Cash Sorters Signature Register” is maintained with denomination details for cash

given and taken from sorters.

1.6.3.3 Cash Transfer to SBP and Reconciliation

a. Transactions related to clearing accounts with other banks, SBP penalties and

government institutions are made through SBP account.

b. “Cash Chest” can have maximum 150 million cash in wallet. Excess cash has to be

transferred to SBP. In case excess cash could not be transferred to SBP, information

has to be passed on to COK and insurance company.

c. “Cash in Transit” account is used during cash transfer to SBP and is credited to SBP

account on receipt of advice from SBP. “State Bank Register” is maintained to record

transactions with SBP.

d. At day end or next day morning account statement is received from SBP and

transactions are reconciled with register.

1.6.4 NIFT Operations

a. Main branch is also responsible for inward and outward clearing operations with

NIFT. An office is maintained at NIFT premises to coordinate the operations.

b. Printed advices are provided by NIFT to coordinating office from where these are

mailed to respective branches.

c. Fund Transfer to other banks is done by main branch through SBP account.

Ibrahim Fibres Limited 28 of 101

ABL Typical Branch Operations Study

Possible Improvements:

a. Cash Request should be from system in form of email or workflow. In this way

“Intimation register” maintained at main branch can be discontinued.

b. System should handle all accounting entries and advices made during cash transfer. In

this way movement of manual advices can also be eliminated.

c. Seeing the sensitivity of Cash Chest, security can also be enhanced by introducing

CCTV and RFIDs so that movement of irrelevant personnel can be tracked.

d. If cash is sorted by SBP then 35 rupees per packet is charged by SBP. This cost is

higher than sorting it in house. To reduce this cost branches should be advised to sort

cash before sending it to main branch. Cash sorting machines can also be used at

main branch to facilitate this process.

e. ABL should devise a procedure to collect clearing data digitally and upload it into

system as NIFT is providing data electronically to some banks.

1.7 Bills

- Demand draft- Pay Order

- Deposit at Call (DAC)

- AB Rupee Travelers Cheques

- Telegraphic transfer / Mail transfer

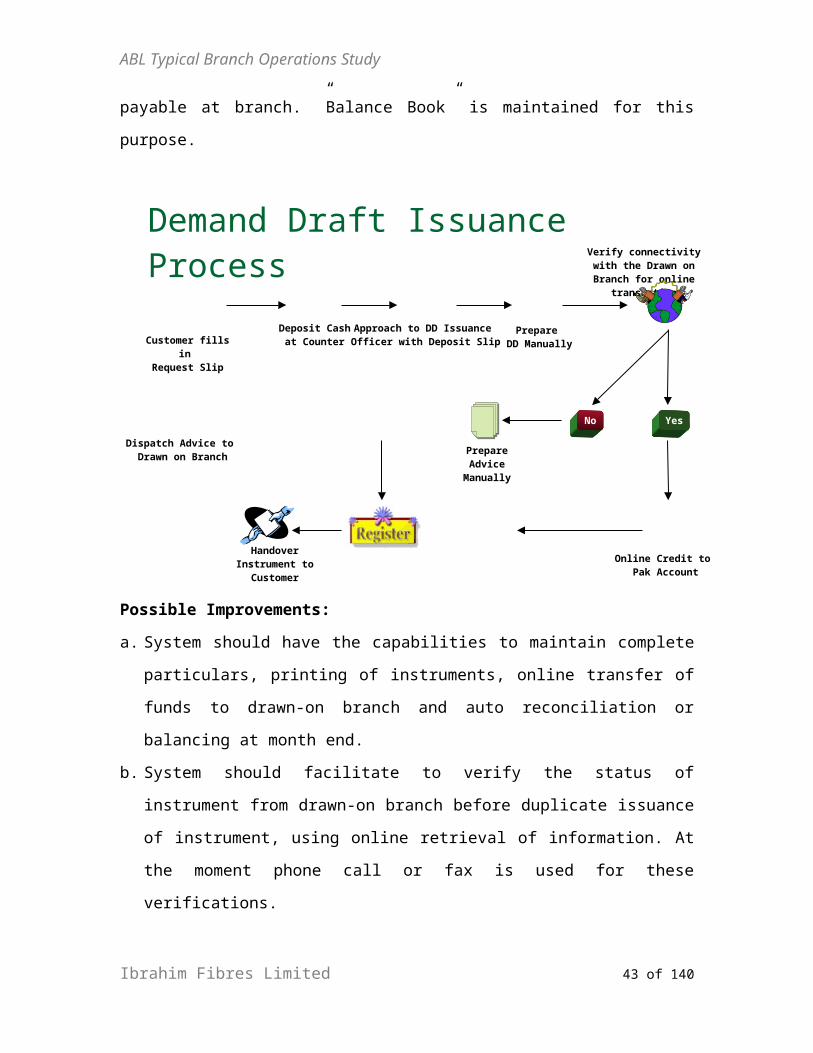

1.7.1 Demand Draft

Demand draft is an instrument which is normally used in intercity transfer of funds.

“Foreign Currency Demand Draft” can be issued in any applicable currency, which is

normally used for overseas transfer of funds. Any account holder or non-account holder

can request for DD. This instrument is valid for 6 months from the date of issuance. “DD

Issued Register” is used to record issued instruments. On expiry, instrument’s issue date

can be extended on client request by bank. DD can be cancelled or stopped for payment

(Detail in next section).

Ibrahim Fibres Limited 29 of 101

ABL Typical Branch Operations Study

1.7.1.1 DD Payable

a. Entry is made in “DD Payable Register” on the receipt of advice and payment date is

written on presentation/payment of Instrument. Pak account is used for transfer of

funds.

b. For account holder Rs.100 or 0.05% (whichever is higher) is charged. For non-

account holder Rs.150 or 0.1% (whichever is higher) is charged.

1.7.1.2 DD Issuance

a. DD request slip is filled by customer and cash is deposited at cash counter. This slip

is forwarded to concerned person to make instrument. In case of cheque, direct

approach is made to relevant person for DD issuance.

b. Three DD formats are used in ABL with different colors.

Demand Draft <= 1000

Demand Draft <= 5000 and >1000

Demand Draft > 5000

There are two methods for instrument issuance:

1.7.1.2.1 Online Advice

a. Online advice for DD is made in two steps,

i. “DD Issue Account” is credited and cash or customer account is debited in

UniBank.

ii. DD payable account of responding branch is credited and DD issuance account of

originating branch is debited.

b. The only deciding factor for the success of online transaction is the health of the link

with drawn-on branch. IBR DD is written on the instrument for the identification of

instrument for online transfer.

c. In case DD advice is not transferred through online, a manual advice is sent to the

branch and reversal entry is made in UniBank to reverse the effect of online

transaction. Instrument is made manually as printing facility is not available in

existing system.

Ibrahim Fibres Limited 30 of 101

ABL Typical Branch Operations Study

1.7.1.2.2 Manual Advice

a. After handing over the instrument to customer, manual advice is posted in system and

sent to the drawn-on branch.

b. Test Code is applied which is an authentication mechanism used by bank on every

kind of inter-branch advice (debit / credit), having amount equal to or greater than

Rs.100,000.

c. Test code is a sum of two numbers which are derived separately by manager and

accountant by adding up certain parameters. Test code is decoded by the receiving

branch to authenticate the validity of instrument. The detail of parameters/segments

used in test code generation is as follows:

For Accountant For Manager

Amount Amount

Date Fix Number

Variable Number Variable Number

1.7.1.3 Cancellation

For cancellation of instrument, customer submits an application along with original

instrument mentioning the reason of cancellation and release from payee. Postage charges

and Rs.100 are charged from customer as cancellation charges. Pak account of drawn-on

branch is debited.

1.7.1.4 Duplicate

In case of lost of instrument, customer can request the Bank for stop payment against that

DD. In this case bank verifies that the DD is not yet paid by drawn-on branch. Fax or

phone is used for getting confirmation of stop payment. Indemnity bond from the

customer is also required. Duplicate DD is issued with same number after receiving

charges Rs.200. “Duplicate DD” is also mentioned on instrument.

Ibrahim Fibres Limited 31 of 101

ABL Typical Branch Operations Study

1.7.1.5 Balancing

Purpose of balancing exercise is to identify outstanding instruments against which funds

are received but not paid by the branch. Balancing exercise is conducted monthly for DD

payable at branch. ”Balance Book” is maintained for this purpose.

Possible Improvements:

a. System should have the capabilities to maintain complete particulars, printing of

instruments, online transfer of funds to drawn-on branch and auto reconciliation or

balancing at month end.

b. System should facilitate to verify the status of instrument from drawn-on branch

before duplicate issuance of instrument, using online retrieval of information. At the

moment phone call or fax is used for these verifications.

c. Concept of e- Branch is under discussion among ADC, Cash Management and SBP.

Idea is to introduce DD or banker’s cheque, payable at any branch of bank. In this

case e-Branch has to be used as drawn-on branch and access to this virtual branch is

to be provided at every branch.

Ibrahim Fibres Limited 32 of 101

Demand Draft Issuance Process

Customer fills in Request Slip

Deposit Cashat Counter

Approach to DD Issuance Officer with Deposit Slip

Verify connectivity with the Drawn on Branch for

online transaction

Online Credit to Pak Account

Prepare AdviceManually

Prepare DD Manually

Dispatch Advice to Drawn on Branch

Handover Instrument to

Customer

YesNo

ABL Typical Branch Operations Study

1.7.2 Pay Order

Pay Order is an instrument which is usually used for same city (local) transfers. Credit

cash/transfer voucher is used as slip for pay order and at some places DD application

form is also used. P.O. validity time is six months, which is extendable by bank

1.7.2.1 PO Issuance

a. A separate program for issuance of pay order is used partially at some branches. In

case of manual issuance of P.O., information is maintained in “PO Register” and

accounting entries are posted in relevant GL accounts of UniBank.

b. In case of system generation, GL accounts are auto updated. Branches are using dot

matrix printers to print P.O. but in most of cases, instruments are made manually, due

to printing problems.

c. Charges of Rs.50 are charged from account holders and Rs.100 from non account

holders.

1.7.2.2 Cancellation

Customer submits an application along with original instrument mentioning the reason of

cancellation. Cancellation charges are Rs. 100.

1.7.2.3 Duplicate

In case of lost of instrument, customer can request the Bank for stop payment against

that P.O. In this case bank verifies that the P.O. is yet not paid by branch. Indemnity

bond from the customer is also requested, after that Duplicate P.O. with same instrument

number is issued by paying additional charges Duplicate issuance charges are Rs.150

Possible Improvements:

a. There should be a specific P.O. application form where details related to P.O.

particulars including name, address, phone # and NIC can be captured.

b. There should be a printer dedicated for P.O., DD and other instruments printing (due

to adjustment reasons).

Ibrahim Fibres Limited 33 of 101

ABL Typical Branch Operations Study

1.7.3 DAC (Deposit at Call)

a. DAC is a non transferable and non negotiable instrument valid for life time, which is

usually used for tenders or bids participation. Cash held against DAC is considered as

branch deposit.

b. An application form along with credit voucher is required to be filled by the customer

before issuing DAC. GL entry is made to get an update in branch affairs.

c. The terms and conditions for cancellation and stoppage are much strict as compared

to DD or PO.

d. Charges of Rs.50 are charged from account holders and Rs.100 from non account

holders.

1.7.3.1 Cancellation

An application along with original instrument and release or letter from concerned

department is required. There are no charges on cancellation of DAC.

1.7.3.2 Duplicate

a. For duplicate issuance of DAC, following documents required from customer:

i. Indemnity bond

ii. Copy of F.I.R.

iii. News paper Advertisement

iv. Authority letter from concern department (N.O.C)

v. Validation from legal advisor

b. Branch is not directly authorized for issuance of duplicate DAC and requires an

approval from controlling office.

c. There are no charges on issuance of duplicate DAC.

Possible Improvements:

a. System should have capability to capture detail of DAC product. Moreover, like all

other instruments, printing facility for DACs should also be there.

Ibrahim Fibres Limited 34 of 101

ABL Typical Branch Operations Study

1.7.4 Rupees Travelers Cheque (RTC)

a. RTC product is out dated and maximum worth of one RTC is reduced to Rs.10,000.

by SBP.

b. Additional information is required from customer on issuance of RTCs of amount

equal to or greater than Rs.100,000. SBP has imposed certain rules under which

information of the customer is captured and sent to SBP for purchases of RTCs worth

equal to or greater than Rs.500,000

c. This product is not supported by system and like all other instruments it is issued

manually.

d. Charges of Rs.10 per leaf or Rs.50 (which ever is higher) are charged.

e. Customer can get it en-cashed from any authorized branch of the bank. To reimburse

funds concerned branch has to lodge claim to COK (ABRTC wing).

1.7.4.1 Duplicate

Stop payment of RTC is a lengthy process; the information has to be conveyed to all

authorized branches through COK provided it is not already en-cashed. On confirmation

of stop payment, duplicate instrument can be issued. Duplicate issuance charges are

Rs.250 per leaf.

1.7.5 Telegraphic Transfer (TT) / Mail Transfer (MT)

This facility was used when online facility was not available. TT is used when a customer

desires to transfer funds from one branch to another on urgent basis. A manual advice is

sent through fax or courier service to responding branch.

1.8 Clearing

We can divide the clearing subject into two segments:

- Local Clearing

- Inter City

Ibrahim Fibres Limited 35 of 101

ABL Typical Branch Operations Study

1.8.1 Local Clearing

Clearing of instruments within the city is done through local clearing. There are three

types of local clearing:

- Routine Local Clearing

- Same Day Local Clearing

1.8.1.1 Routine Local Clearing

1.8.1.1.1 Inward

a. Instruments and summary (transfer scroll) are received in sealed bag from NIFT.

Acknowledgement is provided by the bank to the NIFT person who visits branch in

morning.

b. Transfer scroll consists of details of inward instruments and previous day outward

clearing instruments.

c. Detail of inward clearing instruments is recorded in a manual register “Inward

Clearing Register” and is matched with transfer scroll sent by NIFT. Each instrument

is then posted in the relevant account in the system in clearing mode, which decides

the fate of these instruments.

d. For realized instruments, branch credits PAK account of main branch (in this case,

Napier road) and debits concerned payee account accordingly

e. An advice is made mentioning the total amount of realized instruments and handed

over to the NIFT person along with unrealized instruments. Advice is sent to main

branch through NIFT.

f. Unrealized instrument are also recorded in “Cheque Return Register”

g. Main branch transfers funds to other banks through SBP accounts, while for ABL

branches, funds are transferred through PAK account.

h. In case of any mistake resulting in wrong realization of instruments, branch sends

debit note to for getting funds back from the collecting branch. If the payment has not

been made then the concerned branch returns the funds in form of pay order. If the

cash is with-drawn then it is very difficult for bank to get it back.

i. There are no charges on inward clearing but for unrealized instruments bank charge

Rs.200 per instrument.

Ibrahim Fibres Limited 36 of 101

ABL Typical Branch Operations Study

1.8.1.1.2 Outward

a. On receipt of instruments these are grouped into local, intercity and same day clearing

types.

b. Entry in “out ward clearing register” is made from the pay-in slip.

c. At receiving of instruments special crossing and clearing stamps are stamped on the

instrument and endorsement is done on the back of instrument to avoid its misuse, in

case of misplacement.

d. Entry is made in system in clearing mode to provide a float credit in respective

account. This float credit is not available for withdrawal till the instrument is realized

and finally credited to the account. System does maintain this information to keep

track of outward clearing transactions. This also helps in verification of account title

and status before sending instruments for outward clearing

e. Summary (transfer scroll) is made manually from instruments where as register entry

is made from pay-in slip. It is intentionally done to verify the difference in pay-in slip

and instruments, if any.

Ibrahim Fibres Limited 37 of 101

ABL Typical Branch Operations Study

f. Branch hands over the instruments and summary in a sealed bag to the NIFT person

who collects it in afternoon. In case of any delay, instruments can be delivered by

sending a person to NIFT office

g. After two days (in general practice), NIFT person delivers the fate of instruments

along with an advice and unrealized instruments in a sealed bag.

h. After getting fate of the instruments, credit is provided in UniBank through pay-in

slip. Bank deducts the charges against unrealized instruments.

1.8.1.2 Same Day Local Clearing

a. Same day clearing is opted on client’s requirement and is valid for instruments worth

Rs.500,000 and above. Only nominated branches are authorized for same day

clearing.

b. Incase of same day outward clearing, NIFT person collects instruments in morning. In

case of any delay, instruments can be delivered to NIFT office before 10:00 am. After

processing at NIFT, instruments are sent to destination branch till 12:00 pm.

c. On receipt of same day inward clearing, fate of instruments is decided at that very

moment. An advice is prepared and handed over to NIFT person along with

unrealized instruments

Ibrahim Fibres Limited 38 of 101

ABL Typical Branch Operations Study

d. Separate register is not maintained for same day inward clearing where as information

of same day outward clearing is maintained in “Outward Clearing Register” using a

separate portion.

e. To identify same day clearing transactions from routine clearing transactions, same

day clearing transactions are posted using “Transfer Mode”

f. Rest of the same day clearing process is same as of routine clearing process.

g. There are flat charges of Rs. 150 per instrument for same day out ward clearing.

1.8.2 Inter City Clearing

1.8.2.1 Inward (Intercity)

a. Inter city mode of clearing operates only in those cities where NIFT is available. At

the moment NIFT services are available in 10 major cities of Pakistan.

b. Instruments and summary (transfer scroll) from the local NIFT are received city wise

in separate packets at the branch by 11:30 am. Intercity clearing advice along with

unrealized instruments has to be returned at the same time

c. There is no separate register maintained for intercity inward clearing. This

information is directly entered in to the system in transfer mode.

d. The rest of the process is same as for same day inward clearing.

e. Charges for intercity outward clearing are 0.2 % and NIFT Charges areRs100 per

instrument. These are deducted by the sending branch (collecting bank). Intercity

register is maintained to record transactions of charges.

1.8.2.2 Outward (Intercity)

The process is same as of local outward clearing, except that the instruments are sent in

separate packet for each city. System does not maintain information for inter city outward

clearing.

Possible Improvements (over all clearing process):

a. After posting the inward and outward transactions in system, summary (transfer

scroll) / advice should be generated from the system.

Ibrahim Fibres Limited 39 of 101

ABL Typical Branch Operations Study

b. Bank and branch codes should be same as used in NIFT. At the moment system is not

maintaining bank/branch code information. Due to these limitations, clearing system

is being used in few branches whereas most of the branches are following manual

process.

c. In outward clearing, where data for instruments is already fed, interface should be

made user friendly to supervise realized instruments to credit funds in respective

accounts. System should help to mark unrealized instruments while others should be

auto credited to the respective accounts.

d. There should be separate sub modes available in system for different types of clearing

i.e. same day and inter city.

e. System should generate reports to facilitate clearing related inquiries so that manual

registers maintained for this purpose should be discontinued.

f. System should help in calculation and deduction of all applicable clearing charges.

g. In case of any urgent requirement system should facilitate exceptional outward

clearing of instruments which are entered as a batch against one date.

h. ABL should devise a procedure to collect clearing data digitally and upload it into

system as NIFT is providing data to some banks.

1.9 Outward / Inward Bills for Collection (OBC/IBC)

1.9.1 OBC / IBC

a. Instruments like PO, DD and cheque are operated through clean collection where the

facility of NIFT is not available and online transaction for that city is not possible.

b. In each city / region, one of the branches is nominated as main branch. Within the

bank instruments are sent directly to branch and in case of other bank these are sent to

main branch of ABL in that city / region.

c. Before sending these instruments for collection, special crossing and OBC stamps are

stamped on the instrument and endorsement is done on the back of instrument.

d. In case of within bank transactions, branch credits outward bill for collection and

debits outward bills for receiving. An entry is also recorded in “OBC Register”. On

receiving advice the collecting branch will reverse the contra liabilities and credit the

Ibrahim Fibres Limited 40 of 101

ABL Typical Branch Operations Study

customer account by responding IBCA. On receipt of OBC, the responding branch

provides the credit to originating branch through PAK account and debits the

customer account. An IBCA is also sent to originating branch through courier. On

amount equal to or greater than Rs.100,000, test code has also to be applied on IBCA.

e. For other banks, instruments are sent to the main branch in that region or city. Main

branch launches the instrument in local clearing or arrange collection of funds

through PO, DD or in person. On realization of instrument, main branch sends IBCA

to originating branch. Unrealized instruments are returned back to originating branch

along with “cheque return memorandum”. In case of unavailability of branch in that

region, OBCs can also be sent directly to the branch of other bank. In that case DD is

used to transfer the funds back to originating branch.

f. Minimum Rs.50 or 0.20% of the amount and maximum Rs.5,000 is charged on these

bills.

a. Balancing for OBCs is done on monthly basis.

Possible Improvements:

a. System should maintain complete information of IBC/OBC. In ideal case online

facility should be guaranteed in all branches, which is the best path for these inter-

branch transactions. Further, the proposed online inter-bank transactions can also

helps to facilitate customers and to avoid the lengthy process of transactions through

IBC / OBC.

b. Collection time for OBC is 72 hours. System should generate alerts to both branches

for the outstanding OBCs / IBCs

c. System should maintain floating credit in case of OBCs in a similar way it is

available in outward clearing.

d. System should provide online credit to concerned branch of realized clearing IBC.

Ibrahim Fibres Limited 41 of 101

ABL Typical Branch Operations Study

1.10 Transfers

Transfers are used where the branch needs to give credit to one or more account(s)

debiting other account against an instrument, advice or an instruction. For example salary

transfer of SUI Gas employees against an instruction System support is available

Possible Improvements:

a. While transferring funds, present limit of 8 entries in one batch should be improved.

Ideally there should be higher or no limits on the transactions in one batch.

b. Facility of e-banking should be introduced so that customers can directly upload the

request for transfer of funds. Further, facility for printing of instruments can also be

extended using standard BAI II format used by banks world wide

1.11 Online Transactions

Following types of transactions are handled through online facility:

i. Cash Deposit

ii. Cheque Encashment

iii. Funds Transfers

iv. Balance Inquiry

v. Account Statement

a. In online mode, account holder can withdraw up to Rs.500,000 per instrument by

him/her self and the limit is Rs.25,000 for person other then the account holder.

Where as in case of cash deposit it is Rs.5,000,000 per transaction.

b. Online slip is filled by the customer mentioning the transaction type listed above. Slip

is deposited along with the cash/instrument to the cashier for further processing.

c. In case of cheque, system usually takes a minute to load signature card to verify

signatures. After data entry each transaction needs to be supervised on the same

terminal where the transaction is posted.

d. Cash deposit transaction is done in three steps

i. System entry and supervision

ii. Generation of advice number of originating branch

Ibrahim Fibres Limited 42 of 101

ABL Typical Branch Operations Study

iii. Generation of document number of responding branch

e. In case of online cash deposit, supervision of transactions must be made by the

responding branch to make funds available for withdrawal through ATM or online.

f. In some cases entry is through from originating branch and the document numbers are

generated for both branches but the transaction is still not available at responding

branch. If the customer does not inquire (of the balance) in the above mentioned case

then branch comes to know of this problem during reconciliation (done twice during

the month), in this case manual advice is called from responding branch

g. Inquiry against advice number is available in system to confirm transactions, if link is

available.

h. Entry can be reversed in UniBank until system generates document number of

responding branch; otherwise system has to reverse entries through online.

i. Online register is maintained for online transactions, purpose of this register is to

keep track of charges against online transactions. That also helps in MIS reporting.

j. Online charges are waived-off for account holder maintaining average balance of

Rs.500,000. System provides the average balance of each account during online

transactions.

k. Bank has started accepting clearing instruments in the branches through online

processing facility. A procedure has been devised to credit collection account (non

checking current account specially opened for this purpose) on realization of

instrument. After that funds are transferred in to the customer’s account through

online by debiting the collection account.

l. In case of online banking state bank doesn’t permit to debit the limit account.

Ibrahim Fibres Limited 43 of 101

ABL Typical Branch Operations Study

Ibrahim Fibres Limited 44 of 101

ABL Typical Branch Operations Study

Possible Improvements:

a. Online slip requires improvements in its contents and layout, as it is quite

complicated due to its support of multiple transaction types. Carbonized slips can be

used to avoid duplicate writing on counter folio.

b. System should allow supervision of online transactions on a separate terminal.

Currently it can only be done from the terminal where the transaction is posted.

System should allow the user to supervise transactions in a batch format rather than

doing it one by one.

c. There should be a two way commit or roll back in case of link failure so that data

consistency and integrity can be ensured at both sending and receiving ends.

d. Backup links or multiple sites should be available so that if one site goes down, data

can be sent or received from other site. Perhaps in new core banking system we could

have multiple backup links

e. The responding branch should have notification or alert generated at their end to

know that there are transactions available for supervision.

f. In case of account statement through online it is only available for current half year.

Account statement should be available at least for current and previous half year.

1.12 Term Deposit

Term deposits are profit & loss sharing based fixed deposit accounts and these deposits

are accepted in multiple of Rs.1,000. There are two categories of term deposit:

- Short Notice Deposit Receipt (SNDR)

i. Seven Days (from 7 to 29 days)

ii. Thirty Days (from 30 days onwards)

- Term Deposit Receipt (TDR)

1.12.1 SNDR

a. It is a non transferable, non negotiable and non accumulative account. Account

opening form is same as for all other types of accounts.

Ibrahim Fibres Limited 45 of 101

ABL Typical Branch Operations Study

b. On opening of SNDR account, SNDR receipt is issued to the customer mentioning

the period (either 7 or 30 days).

c. The rate of SNDR is dependant upon the amount and days of deposit.

d. The profit is calculated according to the terms of SNDR which is usually paid on

projected rates at maturity.

e. For each SNDR instrument an account is opened in system. If customer needs

multiple instruments then he/she will have to open equal number of accounts

1.12.2 PLS Based Term Deposit Receipt

Period for this type of deposit is one month to 10 year. TDR has a separate register “TDR

Register”. There are total 10 terms and each term has a separate”TT” in UniBank. Profit

provisioning for these accounts is made on monthly basis and profit is paid on half yearly

basis or as per instruction of customer. The rate of TDR is dependant upon the amount

and period of deposit.

Possible Improvements:

a. System should handle SNDR profit provisioning and its payments.

b. System should maintain all particulars of SNDR.

c. System should have option to issue multiple instruments against single account.

1.12.3 Premium plus Account

Premium Plus Account (PPA) is further divided in to two types:

i. PPA Operational account

ii. PPA Term deposit account

1.12.3.1 PPA Operational Account