4.2 BANKING IN KARNATAKA STATE -...

55

62 4.1 INTRODUCTION The previous chapter dealt with conceptual review and extensive literature survey covering human resource management in general and in banking industry. In this chapter a brief account of history of development of banking industry in Karnataka state since independence has been provided in the first part. Thereafter in the second part the detailed profile of selected private sector banks has been provided. In the last part of this section the detail profile of respondent has been provided. 4.2 BANKING IN KARNATAKA STATE Karnataka has a rich cultural heritage. Early epigraphs of ancient Karnataka do refer to goods and financial transactions. They speak about trade activities, rate of interest that prevailed and the community living that existed in those days. Temples acted as banks and the socio-economic activities of the society revolved around the temples. Karnataka has made a greater stride in modern banking in India during 20 th century. The functioning of organised banking sector was evidenced with the establishment of the branches of the then Presidency Banks. i.e. The Bank of Bombay (1840) and The Bank of Madras (1843) which opened their branch offices at Dharwad in 1863 and at Bangalore cantonment in 1864 respectively. In course of time, many more branches of the Presidency Banks were opened at Belgaum (1867), Hubli (1870) and Kumta (1872-73). Mangalore branch of the Madras Presidency Bank was started to meet the requirements of the port traders. Dharwad branch was opened mainly to facilitate the cotton traders of the Bombay-Karnataka area. The Un-organised banking sector was mainly dominated by the local money lenders viz. Sahukars, Zamindars and Traders. Money-lending was a profitable business. It was commonly practised by all communities. The Marwadis, Gujarathis, Jains, Mahajans, Chettiyars, and Multhani money lenders from the North India came and settled in important trading centres of Karnataka. They are engaged in money lending business even to-day. Bangalore cantonment area was dominated by the European money lenders (Including widows of army officers) together with the natives. During the British days even special civil courts were set up to settle such money lending disputes called as small causes courts, amounting to Rs. 500/-

Transcript of 4.2 BANKING IN KARNATAKA STATE -...

62

4.1 INTRODUCTION

The previous chapter dealt with conceptual review and extensive literature

survey covering human resource management in general and in banking industry. In

this chapter a brief account of history of development of banking industry in

Karnataka state since independence has been provided in the first part. Thereafter in

the second part the detailed profile of selected private sector banks has been provided.

In the last part of this section the detail profile of respondent has been provided.

4.2 BANKING IN KARNATAKA STATE

Karnataka has a rich cultural heritage. Early epigraphs of ancient Karnataka do

refer to goods and financial transactions. They speak about trade activities, rate of

interest that prevailed and the community living that existed in those days. Temples

acted as banks and the socio-economic activities of the society revolved around the

temples. Karnataka has made a greater stride in modern banking in India during 20th

century. The functioning of organised banking sector was evidenced with the

establishment of the branches of the then Presidency Banks. i.e. The Bank of Bombay

(1840) and The Bank of Madras (1843) which opened their branch offices at Dharwad

in 1863 and at Bangalore cantonment in 1864 respectively. In course of time, many

more branches of the Presidency Banks were opened at Belgaum (1867), Hubli (1870)

and Kumta (1872-73). Mangalore branch of the Madras Presidency Bank was started

to meet the requirements of the port traders. Dharwad branch was opened mainly to

facilitate the cotton traders of the Bombay-Karnataka area.

The Un-organised banking sector was mainly dominated by the local money

lenders viz. Sahukars, Zamindars and Traders. Money-lending was a profitable

business. It was commonly practised by all communities. The Marwadis, Gujarathis,

Jains, Mahajans, Chettiyars, and Multhani money lenders from the North India came

and settled in important trading centres of Karnataka. They are engaged in money

lending business even to-day. Bangalore cantonment area was dominated by the

European money lenders (Including widows of army officers) together with the

natives. During the British days even special civil courts were set up to settle such

money lending disputes called as small causes courts, amounting to Rs. 500/-

63

In the absence of strict regulatory measures which came much later, especially

after independence, the promoting of a banking company was much easier. Small

banking companies with limited capital base and inexperienced management were the

common features. There was mushroom growth of banking. Even in semi-urban and

rural areas banks were promoted. Nearly half the total number of banks born in the

state was registered during 1930-1940.

The swadeshi movement also contributed much for the growth of commercial

banking activities in the state, promoted specially by the local traders. Most of these

banks had a limited life span. In those days, the banks were started with impressive

names to attract to customers, especially on the basis of religion, caste and

community. Many a time, local community spirit reflecting itself in commercial spirit

contributed much for the faster growth of community banking. This tendency was

very much evident especially in Dakshina Kannada (South Kanara), which is said to

be the cradle of modern banking industry in Karnataka. The contribution of undivided

Dakshina Kannada district to the modern banking industry is unique. Branch banking

was started here as early as 1923. During the four decades (1906-1945), the district

became the cradle and crèche in nursing as many as 22 banks.

In different parts of the integrated areas of Karnataka, sporadic commercial

banking activities were ushered in at different times, based on local demand, expertise

and economic potentialities. In princely State of Mysore the period of

Commissioner’s rule (1831-1881) was of great significance. It ushered in an era of

modernisation by adopting the British system of administration in all spheres

including banking. The establishment of Bangalore cantonment in 1809 and shifting

of the state secretariat from Mysore to Bangalore in 1831 gave a fillip to commercial

and industrial activity in Bangalore which was partly supported by the banking

institutions.

The joint stock banks that were promoted in princely Mysore were Bangalore

based banks i.e Bangalore Bank Ltd and Mysore Bank Corporation Ltd., both

registered in 1868 with a share capital of Rs. 7 lakhs and Rs. 2 lakhs respectively. As

said earlier, Bangalore City including then Cantonment area had a rich potentiality

and infrastructure which boosted the growth of banking both in the organised and

unorganised sectors.

64

During 1868-1876, there were nearly 24 banking companies operating in

Bangalore city area. During the next few decades i.e. from 1890 to 1949 about 12

banking companies were found in Bangalore city, all did not survive. Among the

Bangalore based banks, the Bangalore Union Bank was founded in 1980 had the

longest service of fifty years before its liquidation in 1940. The Devanga Bank (1926)

was amalgamated with the Vijaya Bank in 1963. The Vysya Bank (1930) and the

Bank of Mysore (1913) survived and the latter becoming State Bank of Mysore at a

later stage.

The royal capital, Mysore, did not lag behind in promoting joint stock banks.

In 1874 ( six years later than Bangalore), two banking companies, viz., The Rajadhani

Bank and the Town Bank of Mysore were promoted here and continued to function

not beyond 1913. A decade thereafter, in 1885 Nanjanguda Srikanteshwara Swamy

Bank was promoted. This is the only bank which served for nearly 80 years till its

licence was refused in 1965. During the period of two-and a half decades ( 1884-

1908) as many as 17 joint stock companies were promoted here, combining banking

and trading. Among the oldest banks of the princely Mysore which are no more now,

a mention may be made of Chitradurga Savings Bank founded in 1870 at Chitradurga

which had a record service of nearly 96 years before its merger with KARNATAKA

Bank Ltd in 1966.

Agricultural Banks: In 1984, the Mysore Government had promoted a new

breed of banks styled as Agricultural Banks, by adopting the principles of limited

guarantee of joint-stock companies in their structure and co-operative principles in

their modus operandi. These banks were mainly meant for extending agricultural

credit to the poor farmers at a cheaper interest and to save the peasants from ruinous

interest rates and exploitation by the money lenders. By 1901, there were 64 such

banks in the princely state. The credit facilities extended by these institutions at

cheaper rates were misused by the big land holders. Many of these banks became

defunct and by 1917 all these banks were closed. Although, it was a unique

experiment, but failed due to lack of supervision and liberal financial assistance by the

Government to these institutions.

In the former Bombay-Karnataka area, where the urban co-operative

movement was strong enough, the ventures for promoting commercial banks by the

local merchants were very much limited. However, some of the earliest efforts to

65

promote local commercial banks in this region were: the Union Bank of Bijapur and

Sholapur (1908), Bagalkot Commercial Bank ( 1922), Sri Lakshmi Bank, Hangal

( 1929) of Dharwad District, Hubli City Bank (1930), Belgaum Bank, Belgaum

(1930) and the Bank of Citizens(1939) Belgaum. The earliest commercial bank in

Uttara Kannada district was Bank of Rural India founded at Karwar in 1940. By

1930-40, the Bombay and Mangalore based banks specially Canara, Syndicate,

Corporation Bank, Union Bank, S.B.I and Central Bank of India opened their

branches in the commercial towns of Bombay-Karnataka area. In the former

Hyderabad Bank in 1941, there were no conspicuous commercial banking ventures.

However, from Gulburga district, the Saraswati Bank (1922), Gulbarga

Banking Co. (1930) and Commercial Banking Company, Yadgiri (1938) were some

of the earlier banking enterprises. Raichur had two banks i.e Sri Sharada Banking Co.

(1937) and Osmania Aziz Bank (1933), Bidar had no commercial banks till 1946. In

the former Madras Presidency area which included the present South Canara, Uduapi,

Coorg, Bellary districts and Kollegal taluk of present Chamrajnagar district,

commercial banking was in full swing.

As of now 7 SBI and associate banks, 20 other nationalised banks 6 RRB’s ,20

private banks,12 foreign banks and 2 non-scheduled commercial banks are operating

with 5768 branches in Karnataka state as on 31st march 2009.

66

Table No. 4.1

THE FACT SHEET OF BANKING IN KARNATAKA STATE

NAME OF THE BANKS RURAL SEMI-

URBAN

URBAN METRO TOTAL

SBI & ASSOCIATES 284 302 247 266 1099

State Bank of Bikaner and

Jaipur

3 3

State Bank of Hyderabad 27 44 32 16 119

State Bank of India 52 136 101 129 418

State Bank of Indore 2 2

State Bank of Mysore 205 121 109 101 536

State Bank of Patiala 1 4 5

State Bank of Travancore 1 4 11 16

NATIONALISED

BANKS

855 512 646 633 2646

Allahabad Bank 2 - 12 9 23

Andhra Bank 3 15 27 45

Bank of Baroda 8 1 20 23 52

Bank of India 19 8 24 28 79

Bank of Maharashtra 6 6 22 14 48

Canara Bank 222 111 118 114 565

Central Bank of India 11 21 26 31 89

Corporation Bank 96 70 69 68 303

Dena Bank 5 9 12 26

IDBI BANK Ltd 3 9 4 16

Indian Bank 6 13 22 33 74

Indian overseas Bank 23 6 28 25 82

Oriental Bank of

Commerce

4 10 11 25

Punjab and Sind Bank 3 2 5

Punjab National Bank 7 1 17 24 49

Syndicate Bank 219 141 117 82 559

UCO Bank 1 5 9 21 36

Union Bank of India 16 31 33 33 113

United Bank of India 4 6 10

Vijaya Bank 214 88 79 66 447

67

Table No. 4.1 (continued)

NAME OF THE BANKS RURAL SEMI-

URBAN

URBAN Metro TOTAL

REGIONAL RURAL

BANKS

889 207 84 3 1183

Cauvery Kalpathru Grameena

Bank

161 34 14 3 212

Chickmangalur –Kodagu

Grameena Bank

44 6 2 52

Karnataka Vikas Grameen

Bank

280 101 34 415

Krishna Grameena Bank 99 7 9 115

Pragathi Gramin Bank 282 54 23 359

Visveshvaraya Grameena

Bank

23 5 2 30

OTHER SCHEDULED

COMMERCIAL BANKS

( Private Banks)

136 177 244 256 813

AXIS Bank Ltd 2 10 23 22 57

Bank of Rajasthan Ltd 1 2 3

Catholic Syrin Bank Ltd 1 4 5 5 15

City Union Bank Ltd 2 6 7 15

Development credit Bank Ltd 1 3 4

Federal Bank Ltd 1 9 16 13 39

HDFC Bank Ltd 6 7 20 40 73

ICICI Bank Ltd 1 34 27 34 96

Indusind Bank Ltd 2 4 3 9

ING Vysya Bank 27 20 29 29 105

Jammu and Kashmir Bank Ltd 2 3 5

KARNATAKA Bank Ltd 87 79 69 44 279

Karur Vysya Bank Ltd 3 11 9 23

KOTAK MAHINDRA Bank 3 1 9 13

Laxmi Vilas Bank Ltd 1 9 7 17

Ratnakar Bank Ltd 3 5 4 1 13

South Indian Bank Ltd 2 2 11 16 31

Tamilnad Mercantile Bank 3 2 5

The Dhanalakshmi Bank Ltd 2 6 8

YES Bank Ltd 1 1 1 3

68

Table No. 4.1 (continued)

NAME OF THE BANKS RURAL SEMI-

URBAN

URBAN Metro TOTAL

FOREIGN BANKS 1 2 15 18

ABN Amro Bank N V 1 1 2

Abu Dhabi Commercial

Bank Ltd

1 1

Bank of America N T and

S.A

1 1

Bank of Nova Scotia 1 1

Barclays Bank PLC 1 1

BNP Paribas 1 1

Calyon Bank 1 1

Citibank N.A 2 2

DBS Bank Ltd 1 1

Deutsche Bank Ltd 1 1

Hongkong and Shanghai

Banking Corportion Ltd.

1 2 3

Standard Chartered Bank 3 3

NON-SCHEDULED

COMMERCIAL BANKS

2 5 2 9

KRISHNA Bhima

Samruddhi Local Area

Bank Ltd.

2 5 1 8

Subhadra Local Area Bank

Ltd

1 1

(Sources: RBI Reports)

69

4.3 PROFILE OF SELECTED PRIVATE SECTOR BANKS

4.3.1 KARNATAKA BANK LTD:

(An Old Generation Private Sector Banks)

HISTORY OF THE BANK

KARNATAKA Bank Limited, a leading 'A' Class Scheduled Commercial

Bank in India, was incorporated on February 18th, 1924 at Mangalore, a coastal town

of Dakshina Kannada district in Karnataka State. The bank took shape in the

aftermath of patriotic zeal that engulfed the nation during the freedom movement of

20th Century India. Over the years the Bank grew with the merger of Sringeri Sharada

Bank Ltd., Chitradurga Bank Ltd. and Bank of Karnataka. With over 85 years of

experience at the forefront of providing professional banking services and quality

customer service, the bank has a national presence of the bank with a network of 464

branches 171 ATM outlets, 8 regional offices, one International Division, one Data

Centre, one customer care centre, 5 Service branches. 2 Currency chest, 6 Extension

counters and two Central processing canters spread across 20 states and 2 Union

Territories. Managed by a dedicated & professional management team,

KARNATAKA Bank has more than 5,256 employees, 71,822 shareholders and over

3.7 million customers. Today, KARNATAKA Bank has emerged as a leading

financial service institution in India.

MISSION STATEMENT

"Our mission is to be a technology savvy, customer centric progressive bank

with a national presence, driven by the highest standards of corporate governance and

guided by sound ethical values”.

70

Table No. 4.2

THE BOARD OF DIRECTORS OF KARNATAKA BANK LTD.

Name Designation

Ananthakrishna Chairman & CEO

S.R.Hedge Director

M.Sitarama Murty Director

D Harshendra Kumar Director

P Jayarama Bhat Managing Director

M Bheema Bhat Director

R.V Shastri Director

S.V.Manjunath Director

H Ramamohan Director

(Sources: KARNATAKA Bank Annual Reports)

TECHNOLOGY OF THE BANK

Over the years, KARNATAKA Bank has focused on one task, one mission -

To Give You the Best in Services and In Products. Among other Banks, it was

KARNATAKA Bank which first realized the importance of having a Centralized

Banking System and was among the first to deploy the Core Banking System in the

year 2000. This system enabled bank to store and processes all the customers'

accounts from one single place - the Data Center at Bangalore. To ensure that

customers have the best, bank has deployed the State-Of-Art technology from the best

players in the Industry like Infosys, Sun and Wipro. These systems provide the

highest reliability thus enabling the bank to offer to the customers Non-Stop services

of the highest order. Bank has taken a lead and implemented a Disaster Recovery

Center. This center will replicate the Banks Centralized Banking system and all its

data. This center will also be the backup for the ATM operations. In the event of a

natural disaster in Bangalore, this center will immediately come into force and

provide full continuous service.

71

AWARDS AND RECOGNITIONS

The Bank has won the prestigious Sun and NDTV Green IT award 2009

instituted by Sun Microsystems and NDTV, recognizing organizations which have

pledged their positive commitment to the planet and engage in eco- efficient green

technologies to run their business. Sun Microsystems and NDTV have recognized the

banks implementation of core banking in rural branches using thin clients, solar

power modules and VSAT connection thereby reducing the power and carbon

footprint accounting for global warming, a burning issue all over the world.

HUMAN RESOURCE DEVELOPMENT

Development of human resources is an important factor for the development

of any industry. Banking is not an exception to that. It involves various aspects like

continuous training, rewards by way of promotions, appreciations etc. During the year

2008-09, 1517 Officers, 814 clerks and 72 Sub-staff were given training under various

aspects to update / improve the knowledge. Staff Training College of the bank has got

state of the art infrastructure facilities and expert faculty members to impart training

to the staff members. The bank is also a member of Southern India Banks Training

College, Bangalore, which has expertise in imparting training. The officers are also

being deputed to various trainings like National Institute of Bank Management, Pune,

College of Agriculture Banking, Pune, and Institute for Development and Research in

Banking Technology, Hyderabad, State Bank Staff College, Hyderabad etc., wherever

specialized training is found necessary. In addition, executives / senior managers are

also deputed to premier institutions like Indian Institute of Management, Ahmedabad

for Leadership Development Programme.

72

Table No. 4.3

THE DISTRIBUTION OF TOTAL EMPLOYEES OF THE BANK ON THE

BASIS OF DESIGNATION AND SEX

Designation/sex Male Female TOTAL

Officer 1660 162 1832

Clerk 1421 1078 2499

Sub staff 818 107 925

Total 3899 1347 5256

(Sources: KARNATAKA Bank HR Department)

As in the past, the Bank has cordial and healthy industrial relations with the

employees. The number of employees in the bank stood at 5,256 as on 31st March

2010. The business per employee (excluding inter-bank deposits) has improved from

Rs.5.89 crore as on 31st March 2008 to Rs.6.49 crore as on 31st March 2009.

CORPORATE GOVERNANCE

Bank is committed to the best practices of corporate governance to protect the

interest of all the stakeholders of the bank, viz shareholders, depositors, customers

and employees and society at large and aims to maintain transparency at all levels.

SOCIAL INITIATIVES

As a responsible corporate citizen, it has been the vision of KARNATAKA

Bank to empower community through socio- economic development of the poorer

people in the society. As part of its Corporate Social Responsibility (CSR), initiatives,

the bank has been contributing its best for promotion of public interest by

encouraging community development by focusing on financial inclusion, rural

development, education, health care, housing, environment etc. The bank’s initiatives

in this area are channelled through institutions /organizations that specialize in these

activities.

73

In pursuit of rural orientation, the bank has adopted Amasebail village in

Udupi district where it is acting as a channelizing and monitoring agency for the

utilization of funds by the beneficiaries. In line with its corporate mission, the bank

attaches due importance to ethics in business and obligations to the society. The bank

has also sponsored social awareness programmes like de-addiction programme aiming

at social amelioration

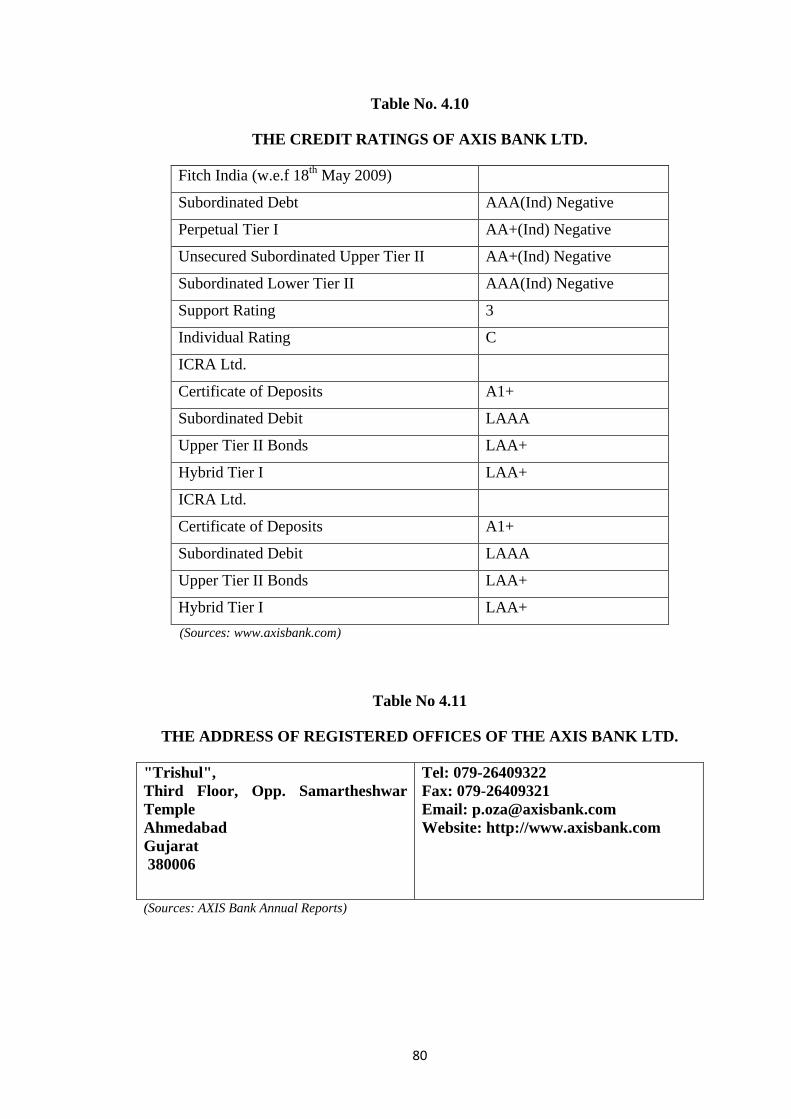

CREDIT RATING

The credit rating agency, ICRA Ltd. (ICRA), one of the leading credit rating

agencies of the country, has accorded A1+ rating to the Banks Certificate of Deposit

Programme. The rating symbol, A1 + indicates highest degree of safety for timely

payment of principal and interest.

Further, ICRA and Credit Analysis & Research Limited (CARE) have

assigned LA+ (pronounced L A plus) and CARE A + (Single A Plus) ratings

respectively indicating adequate credit quality to Rs 200 crore raised by the bank

during the year under report, by way of Unsecured Redeemable Non-Convertible

Subordinated (lower Tier-ll) debt instruments. Further, the rating agencies have also

retained the ratings for Rs 150 crore raised by the Bank by issue of similar instrument

during last financial year

Table No.4.4

THE ADDRESS OF THE REGISTERED OFFICE OF KARNATAKA BANK

LTD.

Address Mahaveera Circle,, Pumpwell - Kankanady,

District Mangalore

State Karnataka

Pin Code 575002

Tel. No. 0824-2228222

Fax No. 0824-2225588

Email : [email protected] Internet : http://www.karnatakabank.com

(Sources: KARNATAKA Bank Annual Reports)

74

Table No. 4.5

THE LISTING INFORMATION OF THE KARNATAKA BANK

Face value of Equity shares 10

Market Lot of Equity shares 1

BSE CODE 532652

NSE CODE KTKBANK

BSE GROUP B

(Sources: KARNATAKA Bank Annual Reports)

Table No. 4.6

THE FINANCIAL INFORMATION ABOUT THE KARNATAKA BANK

Items 2005-06 2006-07 2007-08 2008-09 2009-10

No. of offices 412 428 453 469 486

No. of employees 4346 4456 4677 4947 5244

Business per employee (in Rs.

lakh) 478.29 524.00 589.00 649.00 727.00

Profit per employee (in Rs. lakh) 4.05 4.00 5.00 5.00 3.00

Capital and Reserves & surplus 1111 1239 1380 1567 1833

Deposits 13243 14037 17016 20333 23731

Investments 5549 5048 6327 8961 9992

Advances 7792 9553 10842 11810 14436

Interest income 1018 1256 1560 1948 2043

Other income 167 174 237 321 311

Interest expended 652 836 1102 1444 1708

Operating expenses 204 238 306 347 386

Cost of Funds (CoF) 5.31 5.94 6.86 7.56 7.50

Return on advances adjusted to

CoF 3.42 3.45 4.15 4.72 3.08

Wages as % to total expenses 13.56 12.02 12.86 10.64 9.88

Return on Assets 1.28 1.15 1.37 1.25 0.67

CRAR 11.78 11.03 12.17 13.48 12.37

Net NPA ratio 1.18 1.22 0.98 0.98 1.31

(Sources: KARNATAKA Bank Annual Reports and Website of iba.org)

75

Table No. 4.7

THE SERVICES PROVIDED BY THE KARNATAKA BANK LTD.

(a) LOANS

1. KBLVIDYANIDHI (Education Loan Scheme)

2. KBL EASY RIDE (For Two Wheelers)

3. KBL CAR FINANCE (For New and Second Hand Cars)

4. VAHANA MITHRA (Finance for Commercial Vehicle)

5. KBL VARTHAK (Loan Scheme for Traders)

6. KBL UDYOG MITHRA (Loan Scheme for Professionals)

7. KBL Salaried Persons Loan (Scheme for Financing Salaried persons)

8. K-POWER (Personal Loans)

9. KBL INSTA CASH (For Consumption Purposes)

10. KBL APNA GHAR (Home Loan)

(B) DEPOSITS

1. Tax Planner: New tax saving deposit Schemes

2. Abhyudaya Cash Certificate: A growth oriented scheme with maximum

returns

3. Fixed Deposits: A high interest deposit scheme

4. Soulabhya Deposit: A flexible 'twin gain' Deposit Scheme

5. Cumulative Deposit: A monthly deposit scheme

6. Insurance linked Savings Bank Deposit: Free accident insurance coverage

7. Resident Foreign Currency (Domestic) Account

8. NRI Services: Wide range of Deposit schemes for Non-Resident Indians

9. Senior Citizens Deposit Scheme: Respecting our elders

76

(C) INSURANCE

1) Life insurance with MetLife India Insurance Co. Ltd., an affiliate of MetLife, the

140 year old, largest life insurance company in the USA.

2) General insurance with Universal Sompo General Insurance Co.

(D) MUTUAL FUNDS

M/s Franklin Templeton Asset Management India (P) ltd

M/s Tata Asset Management Ltd

M/s ICICI Prudential Asset Management Company Ltd.

(E) DEMAT SERVICES

(H) FUNDS TRANSFER SERVICES WITH WESTERN UNION MONEY

TRANSFER

ATM services (Visa classic Debit Card, Visa Gold Debit Card, and Student

prepaid card)

(I) MOBILE BANKING SERVICES

(Sources: KARNATAKA Bank Marketing Department)

77

4.3.2 AXIS BANK

(A New Generation Indian Bank: A Profile)

HISTORY OF THE BANK

AXIS Bank was the first of the new private banks to have begun operations in

1994, after the Government of India allowed new private banks to be established. The

Bank was promoted jointly by the administrator of the specified undertaking of the

Unit Trust of India (UTI - I), Life Insurance Corporation of India (LIC) and General

Insurance Corporation of India (GIC) and other four PSU insurance companies, i.e.

National Insurance Company Ltd., The New India Assurance Company Ltd., The

Oriental Insurance Company Ltd. and United India Insurance Company Ltd. The

Bank today is capitalized to the extent of Rs. 405.17 crores with the public holding

(other than promoters and GDRs) at 53.09%.

The Bank's Registered Office is at Ahmedabad and its Central Office is

located at Mumbai. The bank has a very wide network of more than 1000 branches

and Extension Counters (as on 31st March 2010). The Bank has a network of over

4055 ATMs (as on 31st March 2010) providing 24 hrs a day banking convenience to

its customers. This is one of the largest ATM networks in the country. The bank has

strength in both retail and corporate banking and is committed to adopting the best

industry practices internationally in order to achieve excellence.

VISION 2015

“To be the preferred financial solution provider excelling in customer delivery

through insight, empowered employees and smart use of technology”

CORE VALUES

Customer Centricity, Ethics, Teamwork, Ownership, and Transparency

TECHNOLOGY OF THE BANK

AXIS Bank uses a ‘finacle’ core banking software for its banking operations

which is developed by Infosys Ltd. India.

78

Table No. 4.8

LIST OF BOARD OF DIRECTORS OF AXIS BANK

Dr. Adarsh Kishore Non-Executive Chairman

Smt. Shikha Sharma Managing Director & CEO

Shri M. M. Agrawal Deputy Managing Director

Shri N.C. Singhal Director

Shri J.R. Varma Director

Dr. R.H. Patil Director

Smt.Rama Bijapurkar Director

Shri R.B.L. Vaish Director

Shri M.V. Subbiah Director

Shri K. N. Prithviraj Director

Shri V. R. Kaundinya Director

Shri S. B. Mathur Director

(Sources: AXIS Bank Annual Reports)

PROMOTERS

The largest and the best financial institution of the country, UTI, has promoted

AXIS Bank Ltd... The Bank was set up with a capital of Rs. 115 crore, with UTI

contributing Rs. 100 crore, LIC - Rs. 7.5 crore and GIC and its four subsidiaries

contributing Rs. 1.5 crore each.

AWARDS AND RECOGNITIONS

AXIS Bank won the Best Bank Award 2009 (In new sector Bank categories)

presented by The Financial Express newspaper. The bank is awarded for its

outstanding performance in growth, profitability, credit quality and strength over the

past fiscal year.

AXIS Bank won the runner-up award for the best use of information

technology in retail banking at the IBA& TFCI: Banking Technology Awards 2007.

In the year 2009.AXIS Bank awarded as Business world Best Bank award

(fastest growing bank in India), Former AXIS Bank Chairman and CEO P J Nayak

79

got the Banker of the Year award for steering Axis to become India’s third largest

private sector bank in the year 2008.

Dec 5th

. 2005 AXIS Bank won International Financing Review (IFR) Asia

'India Bond House' award for the year 2005 in its appreciation record

HUMAN RESOURCE

Table No. 4.9

THE DISTRIBUTION OF TOTAL EMPLOYEES OF THE BANK ON THE

BASIS OF DESIGNATION AND SEX

Designation/sex Male Female TOTAL

Officer 3507 3514 7021

Executives 9600 4000 13600

Sub staff 719 300 1019

Total 13826 7814 21640

(Sources: AXIS Bank HR Department)

CORPORATE GOVERNANCE

The bank is committed to achieve a high standard of corporate governance and

it aspires to benchmark it with international best practices.

CORPORATE SOCIAL INITIATIVES

Through the AXIS Bank Foundation, the bank seeks to define and effectively

fulfil its Corporate Social Responsibilities as a corporate citizen and has therefore

agreed to allocate up to one percent of its net profit every year to the foundation for its

activities. During the year, the foundation partnered with sixteen more NGOs, taking

the partnership to a total of 41 NGOs, for educating underprivileged children and

special children all over India. The foundation has committed grants for projects

running up to three years. 536 education centres, involving 12 states are covered by

the foundation programmes. 47,055 children are covered under the programmes that

include 24,313 girls and 22,742 boys. The projects supported by the foundation

include focusing on quality.

80

Table No. 4.10

THE CREDIT RATINGS OF AXIS BANK LTD.

Fitch India (w.e.f 18th

May 2009)

Subordinated Debt AAA(Ind) Negative

Perpetual Tier I AA+(Ind) Negative

Unsecured Subordinated Upper Tier II AA+(Ind) Negative

Subordinated Lower Tier II AAA(Ind) Negative

Support Rating 3

Individual Rating C

ICRA Ltd.

Certificate of Deposits A1+

Subordinated Debit LAAA

Upper Tier II Bonds LAA+

Hybrid Tier I LAA+

ICRA Ltd.

Certificate of Deposits A1+

Subordinated Debit LAAA

Upper Tier II Bonds LAA+

Hybrid Tier I LAA+

(Sources: www.axisbank.com)

Table No 4.11

THE ADDRESS OF REGISTERED OFFICES OF THE AXIS BANK LTD.

"Trishul",

Third Floor, Opp. Samartheshwar

Temple

Ahmedabad

Gujarat

380006

Tel: 079-26409322

Fax: 079-26409321

Email: [email protected]

Website: http://www.axisbank.com

(Sources: AXIS Bank Annual Reports)

81

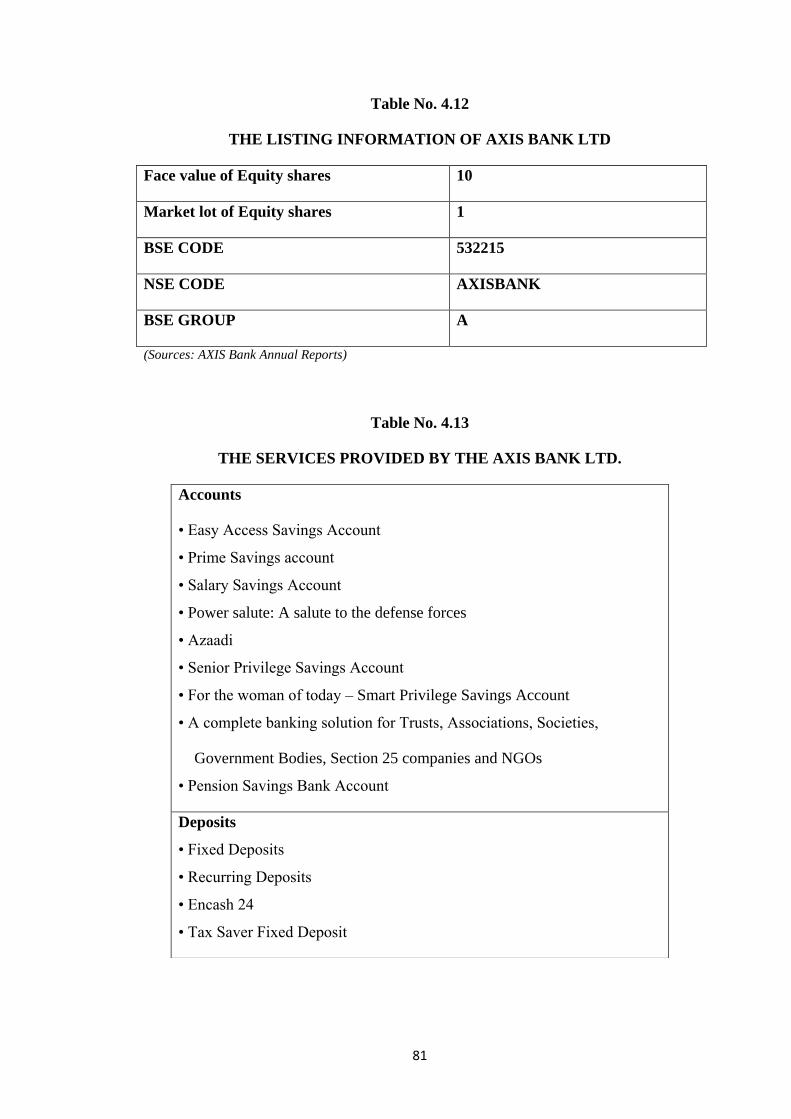

Table No. 4.12

THE LISTING INFORMATION OF AXIS BANK LTD

Face value of Equity shares 10

Market lot of Equity shares 1

BSE CODE 532215

NSE CODE AXISBANK

BSE GROUP A

(Sources: AXIS Bank Annual Reports)

Table No. 4.13

THE SERVICES PROVIDED BY THE AXIS BANK LTD.

Accounts

• Easy Access Savings Account

• Prime Savings account

• Salary Savings Account

• Power salute: A salute to the defense forces

• Azaadi

• Senior Privilege Savings Account

• For the woman of today – Smart Privilege Savings Account

• A complete banking solution for Trusts, Associations, Societies,

Government Bodies, Section 25 companies and NGOs

• Pension Savings Bank Account

Deposits

• Fixed Deposits

• Recurring Deposits

• Encash 24

• Tax Saver Fixed Deposit

82

(Sources: AXIS Bank Marketing Department)

Loans

• Power Homes

• Power Drive

• Personal Power

• Study Power

• Asset Power

• Two Wheeler Loan

• Loan against Security

• Consumer Power

Cards:

Apart from Gold & Silver credit cards, AXIS Bank provides

• AXIS Bank Meal Card

• AXIS Bank Gift Card

• LIC co-branded Annuity Card

Capital Markets

• Debt Solutions

• Equity Solutions

• Private Equity, Mergers & Acquisitions

• Advisory Services

• Trusteeship Services

• Depository Services

83

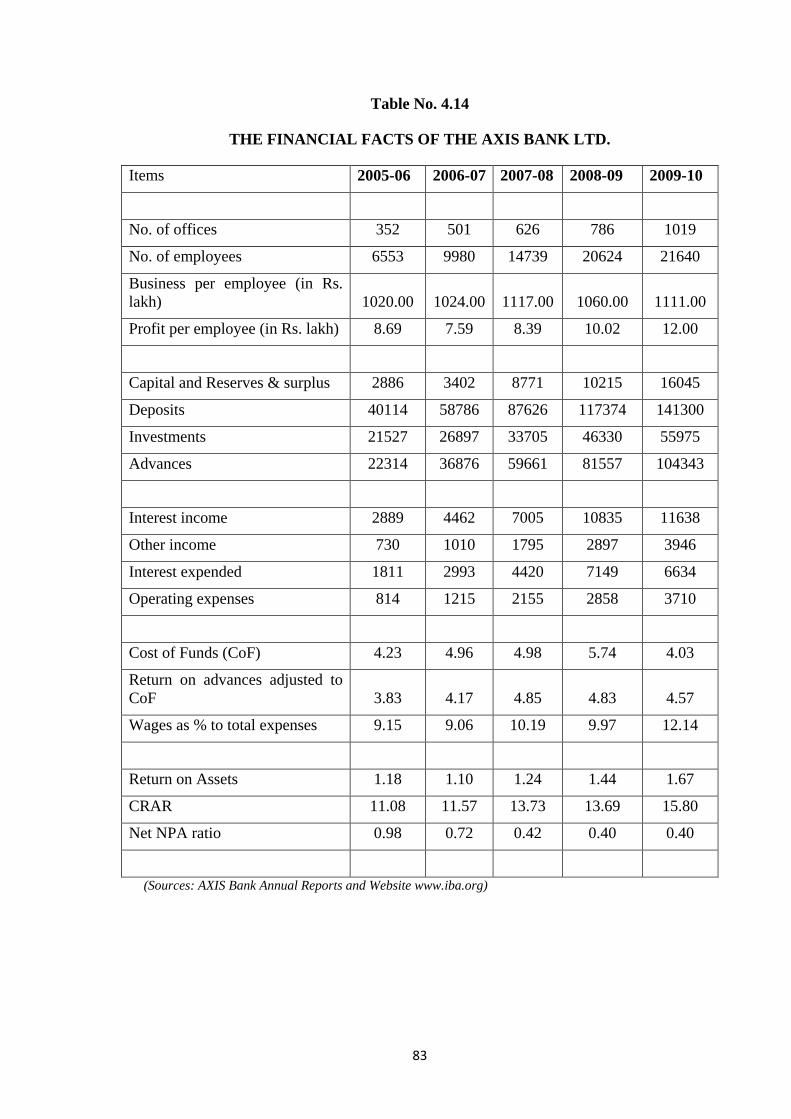

Table No. 4.14

THE FINANCIAL FACTS OF THE AXIS BANK LTD.

Items 2005-06 2006-07 2007-08 2008-09 2009-10

No. of offices 352 501 626 786 1019

No. of employees 6553 9980 14739 20624 21640

Business per employee (in Rs.

lakh) 1020.00 1024.00 1117.00 1060.00 1111.00

Profit per employee (in Rs. lakh) 8.69 7.59 8.39 10.02 12.00

Capital and Reserves & surplus 2886 3402 8771 10215 16045

Deposits 40114 58786 87626 117374 141300

Investments 21527 26897 33705 46330 55975

Advances 22314 36876 59661 81557 104343

Interest income 2889 4462 7005 10835 11638

Other income 730 1010 1795 2897 3946

Interest expended 1811 2993 4420 7149 6634

Operating expenses 814 1215 2155 2858 3710

Cost of Funds (CoF) 4.23 4.96 4.98 5.74 4.03

Return on advances adjusted to

CoF 3.83 4.17 4.85 4.83 4.57

Wages as % to total expenses 9.15 9.06 10.19 9.97 12.14

Return on Assets 1.18 1.10 1.24 1.44 1.67

CRAR 11.08 11.57 13.73 13.69 15.80

Net NPA ratio 0.98 0.72 0.42 0.40 0.40

(Sources: AXIS Bank Annual Reports and Website www.iba.org)

84

4.3.3 ICICI BANK LTD

(A New Generation Private Sector Banks)

HISTORY OF THE BANK

ICICI Bank was originally promoted in 1994 by ICICI Limited, an Indian

financial institution, and was its wholly-owned subsidiary. ICICI's shareholding in

ICICI Bank was reduced to 46% through a public offering of shares in India in fiscal

1998, an equity offering in the form of ADRs listed on the NYSE in fiscal 2000,

ICICI Bank's acquisition of Bank of Madura Limited in an all-stock amalgamation in

fiscal 2001, and secondary market sales by ICICI to institutional investors in fiscal

2001 and fiscal 2002. ICICI was formed in 1955 at the initiative of the World Bank,

the Government of India and representatives of Indian industry. The principle

objective was to create a development financial institution for providing medium-term

and long-term project financing to Indian businesses. In the 1990s, ICICI transformed

its business from a development financial institution offering only project finance to a

diversified financial services group offering a wide variety of products and services,

both directly and through a number of subsidiaries and affiliates like ICICI Bank. In

1999, ICICI become the first Indian company and the first bank or financial institution

from non-Japan Asia to be listed on the NYSE. After consideration of various

corporate structuring alternatives in the context of the emerging competitive scenario

in the Indian banking industry, and the move towards universal banking, the

managements of ICICI and ICICI Bank formed the view that the merger of ICICI with

ICICI Bank would be the optimal strategic alternative for both entities, and would

create the optimal legal structure for the ICICI group's universal banking strategy. The

merger would enhance value for ICICI shareholders through the merged entity's

access to low-cost deposits, greater opportunities for earning fee-based income and

the ability to participate in the payments system and provide transaction-banking

services.

The merger would enhance value for ICICI Bank shareholders through a large

capital base and scale of operations, seamless access to ICICI's strong corporate

relationships built up over five decades, entry into new business segments, higher

market share in various business segments, particularly fee-based services, and access

to the vast talent pool of ICICI and its subsidiaries. In October 2001, the Boards of

85

Directors of ICICI and ICICI Bank approved the merger of ICICI and two of its

wholly-owned retail finance subsidiaries, ICICI Personal Financial Services Limited

and ICICI Capital Services Limited, with ICICI Bank. The merger was approved by

shareholders of ICICI and ICICI Bank in January 2002, by the High Court of Gujarat

at Ahmedabad in March 2002, and by the High Court of Judicature at Mumbai and the

Reserve Bank of India in April 2002. Consequent to the merger, the ICICI group's

financing and banking operations, both wholesale and retail, have been integrated in a

single entity

Vision

“To be the leading provider of financial services in India and a major global bank”

Mission

The bank will leverage the people, technology, speed and financial capital to:

Be the banker of first choice for customers by delivering high quality, world-

class products and services.

Expand the frontiers of business globally.

Play a proactive role in the full realisation of India’s potential.

Maintain a healthy financial profile and diversify earnings across businesses

and geographies.

Maintain high standards of governance and ethics.

Contribute positively to the various countries and markets in which the bank

operates.

Create value for the stakeholders.

86

HUMAN RESOURCE

Table No. 4.15

THE DISTRIBUTION OF TOTAL EMPLOYEES OF THE BANK ON THE

BASIS OF DESIGNATION AND SEX

Designation/sex Male Female TOTAL

Officer 6319 3708 10027

Executives 15600 7900 23500

Sub staff 1529 200 1729

Total 23448 11808 35256

(Sources: ICICI Bank HR Department)

Table No. 4.16

THE BOARD OF DIRECTORS OF ICICI BANK LTD.

K V Kamath Chairman / Chair Person

N S Kannan Executive Director & CFO

Rajiv Sabharwal Executive Director

Sridar Iyengar Director

Anup K Pujari Director

M K Sharma Director

V Prem Watsa Director

Rajiv Sabharwal Executive Director

Chanda D Kochhar Managing Director & CEO

K Ramkumar Executive Director

Tushaar Shah Non Executive Director

Homi R Khusrokhan Director

M S Ramachandran Director

V Sridar Director

K Ramkumar Executive Director

(Sources: ICICI Bank Annual Reports)

87

TECHNOLOGY OF THE BANK

Over the years, the strategic partnership between ICICI Bank and Infosys that

started in 1994 has grown stronger and the close collaboration has resulted in many

innovations. For instance, in 1997, it was the first bank in India to offer Internet

banking with Finacle’s e-banking solution and established itself as a leader in the

Internet and e-commerce space. The bank followed it up with offering several

e-Commerce services like Bill Payments, Fund Transfers and Corporate Banking over

the net. The internet is a critical element of ICICI Bank’s award winning multi-

channel strategy that is one of the main engines of growth for the bank. Between 2000

and 2004, the bank has been able to successfully move over 70 percent of routine

banking transactions from the branch to the other delivery channels, thus increasing

overall efficiency.

Currently, only 25 percent of all transactions take place through branches and

75 percent through other delivery channels. This reduction in routine transactions

through the branch has enabled ICICI Bank to aggressively use its branch network as

customer acquisition units. On an average, ICICI Bank adds 300,000 customers a

month, which is among the highest in the world

AWARDS AND RECOGNITIONS

The ICICI BANK LTD won many awards for its committed and quality

services. Some of the awards details are as below

ICICI Bank was voted as the Most Trusted Brand among private sector banks

in the 2010 Economic Times - Brand Equity Most Trusted Brand Awards and ranked

7th in the list of Top 50 service brands

ICICI Bank received the 2010 World Finance UK award for: Excellence in

Remittance Business, Worldwide Excellence in NRI Services, Worldwide Excellence

in Private Banking Business, APAC Region.

ICICI Bank won the Best Trade Finance Bank and Best Foreign Exchange

Bank, India at the Finance Asia Country Awards for Achievement, Hong Kong.

ICICI Bank wins the Asian Banker Award for Best Banking Security System

88

ICICI Bank won the second prize in the Six Sigma Excellence Awards,

conducted by Indian Statistical institute, Bangalore for "Improving Sales for TV

Banking business" etc.

CORPORATE GOVERNANCE

The Bank is committed to follow the tenets of good corporate governance.

Right from its inception, the bank has assiduously practised good governance. It has

set up among other committees of the Board, a Compensation Committee which looks

into and recommends to the Board the amount of compensation payable to the

executive directors, the fees payable to other directors and framing the internal

guidelines for and management of the employee stock option scheme. The

Nomination Committee reviews the functioning of the members of the Board. The

Audit and Risk Committee reviews and monitors audit of branches and overall

systems and procedures. The Committee also monitors periodically risk management

measures to control risks like market risks, operational risks, liquidity risks, etc.

CREDIT RATING

We have obtained credit rating for an amount of Rs. 4,000 crore from the

following agencies: The Credit Analysis & Research Limited

(CARE) has assigned a rating of “CARE AAA” (Pronounced as “CARE triple A”) to

these Bonds. This is the highest rating for such instruments. Instruments carrying this

rating are considered to be of the best quality, carrying negligible investment risk.

Debt services payments are protected by stable cash flows with good margin.

While the underlying assumptions may change, such changes can be visualised are

most unlikely to impair the strong position of such instruments. ICRA Limited

(ICRA) has assigned a rating of “LAAA” (Pronounced L triple A) to these Bonds.

This is the highest rating for such instrument. This rating indicates highest safety and

a fundamentally strong position.

89

CORPORATE SOCIAL INITIATIVES

ICICI Bank’s Social Initiatives Group (SIG), a non-profit group set up within

ICICI Bank in 2000, pioneered work on health, education and access to finance. In

January 2008, ICICI Group established ICICI Foundation for Inclusive Growth,

which carries forward this legacy.

REGISTERED OFFICE:

“Landmark” Race Course Circle, Vadodra, and Gujarat-390007

Table No. 4.17

THE LISTING INFORMATION OF ICICI BANK LTD

Face Value Of Equity Shares 10

Market Lot Of Equity Shares 1

BSE Code 532174

NSE Code ICICIBANK

BSE Group A

(Sources: ICICI Bank Annual Reports)

90

Table No. 4.18

THE SERVICES PROVIDED BY THE ICICI BANK LTD.

Accounts and Deposits

Savings Account

Salary Account

Fixed Deposit

Recurring Deposit

Privilege Banking

Special Savings Account

Life Plus Senior Citizen Services

Security Deposits

Child Education Plan

Bank@Campus

EEFC Account

Resident Foreign Currency (Domestic)

Account

Advantage Woman Savings Account

No Frills Account

Rural Savings Account

Outward Remittance

Freedom Savings Account

Tax Saver FD

Young Star Account

Online Services

Bill Payment

Funds Transfer

Special Promotions & Offers

Ticket Booking

iMobile

Receive Funds

Shopping

Online Tax Calculation

Prepaid Mobile Recharge

Smart Money Order

Account-2-CardFT

Share Trading

Charity

Online Loans and Credit Cards

Loans

Home Loans

Personal Loans

Car Loans

Two wheeler Loans

Commercial Vehicle Loans

Loan Against Securities

Loan Against Gold Ornaments

Construction Equipment Loans

Pre-approved Loans

Retail Assets Branches

Loan@Click

Flexi Cash

Cards

Debit Card

Commercial cards

Investments

ICICI Bank Bonds

GOI Bonds

Mutual Funds

IPO

ICICI Bank Pure Gold

Forex Services

Senior Citizens Savings Scheme, 2004

Insurance

General Insurance

Demat

Wealth Management

(Sources: ICICI Bank Marketing Department)

http://www.icicibank.com/Personal-Banking/account-deposit/advantage-woman-savings-account/index.html

91

Table No 4.19

THE FINANCIAL FACTS OF THE ICICI BANK LTD.

Items 2005-06 2006-07 2007-08 2008-09 2009-10

No. of offices 569 716 1269 1430 1717

No. of employees 25384 33321 40686 34596 35256

Business per employee (in Rs.

lakh) 905.00 1027.00 1008.00 1154.00 1029.00

Profit per employee (in Rs.

lakh) 10.00 9.00 10.00 11.00 12.00

Capital and Reserves & surplus 22556 24663 46820 49533 51618

Deposits 165083 230510 244431 218348 202017

Investments 71547 91258 111454 103058 120893

Advances 146163 195866 225616 218311 181206

Interest income 14306 21996 30788 31093 25707

Other income 4181 6928 8811 7604 7478

Interest expended 9597 16358 23484 22726 17593

Operating expenses 5001 6691 8154 7045 5860

Cost of Funds (CoF) 4.01 5.34 6.40 5.72 4.18

Return on advances adjusted to

CoF 4.58 4.08 4.33 4.33 4.51

Wages as % to total expenses 7.41 7.01 6.57 6.62 8.21

Return on Assets 1.30 1.09 1.12 0.98 1.13

CRAR 13.35 11.69 13.97 15.53 19.41

Net NPA ratio 0.72 1.02 1.55 2.09 2.12

(Sources: ICICI Bank Annual Reports and Websites www.iba.org)

92

4.3.4 HDFC BANK LTD

(A New Generation Private Sector Bank)

HISTORY OF THE BANK

Housing Development Finance Corporation Limited, more popularly known

as HDFC Bank Ltd, was established in the year 1994, as a part of the liberalization of

the Indian Banking Industry by Reserve Bank of India (RBI). It was one of the first

banks to receive an 'in principle' approval from RBI, for setting up a bank in the

private sector. The bank was incorporated with the name 'HDFC Bank Limited', with

its registered office in Mumbai. The following year, it started its operations as a

Scheduled Commercial Bank. Today, the bank boasts of as many as 1412 branches

and over 3275 ATMs across India.

AMALGAMATIONS

In 2002, HDFC Bank witnessed its merger with Times Bank Limited (a

private sector bank promoted by Bennett, Coleman & Co. / Times Group). With this,

HDFC and Times became the first two private banks in the New Generation Private

Sector Banks to have gone through a merger. In 2008, RBI approved the

amalgamation of Centurion Bank of Punjab with HDFC Bank. With this, the Deposits

of the merged entity became Rs. 1,22,000 crore, while the Advances were Rs. 89,000

crore and Balance Sheet size was Rs. 1,63,000 crore.

MISSION & OBJECTIVES

Our mission is to be "a World Class Indian Bank", benchmarking ourselves

against international standards and the best practices in terms of product offerings,

technology, service levels, risk management and audit & compliance. The objective is

to build sound customer franchises across distinct businesses so as to be a preferred

provider of banking services to target retail and wholesale customer segments, and to

achieve a healthy growth in profitability, consistent with the Bank's risk appetite. The

bank is committed to do this while ensuring the highest levels of ethical standards,

professional integrity, corporate governance and regulatory compliance.

93

HUMAN RESOURCE

Table No. 4.20

THE DISTRIBUTION OF TOTAL EMPLOYEES OF THE BANK ON THE

BASIS OF DESIGNATION AND SEX

Designation/sex Male Female TOTAL

Officer 8647 6512 15159

Executives 25400 9600 35000

Sub staff 1600 129 1729

Total 35647 16241 51888

(Sources: HDFC Bank HR Department)

Table No. 4.21

THE LIST OF BOARD OF DIRECTORS OF HDFC BANK LTD.

Chander Mohan Vasudev Chairman / Chair Person

Harish Engineer Executive Director

Keki Mistry Director

Ashim Samanta Director

Aditya Puri Managing Director

Paresh Sukthankar Executive Director

Arvind Pande Director

Pandit Palande Director

Harish Engineer Executive Director

(Sources: HDFC Bank Annual Report)

TECHNOLOGY OF THE BANK

HDFC Bank has always prided itself on a highly automated environment, be it

in terms of information technology or communication systems. All the branches of the

bank boast of online connectivity with the other, ensuring speedy funds transfer for

the clients. At the same time, the bank's branch network and Automated Teller

Machines (ATMs) allow multi-branch access to retail clients. The bank makes use of

94

its up-to-date technology, along with market position and expertise, to create a

competitive advantage and build market share.

AWARDS AND RECOGNISATION

It is extremely gratifying that bank efforts towards providing customer

convenience have been appreciated both nationally and internationally.

Best Private Bank in India, awarded by The Banker and PWM 2010 Global Private

Banking Awards.

Business Leader of the Year - Mr. Aditya Puri, Economic Times Award for

Corporate Excellence 2010

Best Private Sector Bank , awarded by NDTV Business Leadership Awards 2010

Best Cash Management Bank in India, awarded by The Asset Triple A Awards.

Etc

CORPORATE GOVERNANCE

HDFC Bank recognizes the importance of good corporate governance,

which is generally accepted as a key factor in attaining fairness for all stakeholders

and achieving organizational efficiency. This Corporate Governance Policy, therefore,

is established to provide a direction and framework for managing and monitoring the

bank in accordance with the principles of good corporate governance.

CREDIT RATINGS

The bank was amongst the first four companies, which subjected itself to a

Corporate Governance and Value Creation (GVC) rating by the rating agency, The

Credit Rating Information Services of India Limited (CRISIL). The rating provides an

independent assessment of an entity's current performance and an expectation on its

"balanced value creation and corporate governance practices" in future.

95

The bank has been assigned a 'CRISIL GVC Level 1' rating for the second

consecutive year, which indicates that the bank's capability with respect to wealth

creation for all its stakeholders while adopting sound corporate governance practices

is the highest.

SOCIAL INITIATIVES

As its operations have grown, bank has retained its focus on various areas of

corporate sustainability that impact the socio economic ecosystem that we are part of.

HDFC Bank’s focus in the area of corporate sustainability includes social

sustainability& social welfare and financial inclusion. The bank has initiated a

number of programs to encourage economic, social and educational development

within the communities it operates while at the same time contributing to several

grass root level development programs across these geographies.

96

Table No. 4.22

THE PRODUCTS OF THE HDFC BANK LTD

Savings Accounts

Regular Savings Account

Savings Plus Account

Saving Max-Account

Senior Citizens Account

No-Frills Account

Institutional Savings Account

Salary Account

Payroll

Classic

Regular

Premium

Defence

No Frills Salary Account

Reimbursement Current Account

Kids Advantage Account

Pension Saving Bank Account

Family Saving Group

Kisan no frill Savings Account

Kisan club savings Account

Current Account

Plus current Account

Trade current Account

Premium current Account

Regular current Account

RFC-Domestic Account

Flexi-current Account

Apex current Account

Max current Account

Merchant advantage Account

Merchant advantage plus Account

Fixed Deposits

Regular Fixed Deposits

5 years tax savings FD A/C

Super saver facility

Sweep-in facility

Recurring Deposits

Demat Account

Safe Deposit Lockers

Loans

Smart Draft

Home loans

Two-wheeler loan

New car loans

Used car loans

Gold loan

Education loan

Loan against security

Loan against property

Loan against rental receivables

Health care finance

Retail Agri Loan

Tractor loans

Commercial Vehicle loan

Working Capital Finance

Construction equipment Finance

Warehouse receipt loans

Insurance

Mutual funds

ATM Banking

Net Banking

Mobile Banking

(Sources: HDFC Bank Marketing Department)

97

Table No. 4.23

THE FINANCIAL FACTS OF THE HDFC BANK

Items 2005-06 2006-07 2007-08 2008-09 2009-10

No. of offices 516 666 745 1422 1729

No. of employees 14878 21477 37386 52687 51888

Business per employee (in

Rs. lakh) 758.00 607.00 506.00 446.00 590.00

Profit per employee (in Rs.

lakh) 7.39 6.13 4.97 4.18 5.98

Capital and Reserves &

surplus 5300 6433 11497 14652 21522

Deposits 55797 68298 100769 142812 167404

Investments 28394 30565 49394 58818 58608

Advances 35061 46945 63427 98883 125831

Interest income 4475 6648 10115 16332 16173

Other income 1124 1516 2283 3291 3808

Interest expended 1930 3179 4887 8911 7786

Operating expenses 1691 2421 3746 5533 5764

Cost of Funds (CoF) 3.76 4.58 5.24 6.92 4.66

Return on advances adjusted

to CoF 5.15 5.99 7.38 8.04 6.11

Wages as % to total expenses 13.45 13.87 15.07 15.50 16.89

Return on Assets 1.38 1.33 1.32 1.28 1.53

CRAR 11.41 13.08 13.60 15.69 17.44

Net NPA ratio 0.44 0.43 0.47 0.63 0.31

(Sources: HDFC Bank Financial Reports and Web site www.iba.org)

98

4.3.5 KOTAK MAHINDRA BANK

(A New Generation Private Sector Bank)

HISTORY OF THE BANK

The Kotak Mahindra group is a financial organization established in 1985 in

India. It was previously known as the Kotak Mahindra Finance Limited, a non-

banking financial company. In February 2003, Kotak Mahindra Finance Ltd, the

group's flagship company was given the license to carry on banking business by the

Reserve Bank of India (RBI). Kotak Mahindra Finance Ltd. is the first company in the

Indian banking history to convert to a bank.

KOTAK MAHINDRA Bank Ltd is one of the fastest growing banks and

among the most admired financial institution in India. The Bank offers transaction

banking, operates lending verticals, manages IPOs and provides working capital

loans. They have one of the largest and most respected Wealth Management teams in

India, providing the widest range of solutions to high net worth individuals,

entrepreneurs, business families and employed professionals. The Bank has over 245

branches, a customer base of over 8 lakh and has spread all over India. The Bank

offers complete financial solutions for infinite needs of all individual & non-

individual customers depending on the customer's need - delivered through a state of

the art technology platform. During the year 2009-10, the Bank had 32 branches, 77

off site and 28 onsite ATMs taking the total number of branches to 249 numbers, 252

No off-site ATMs and 240 numbers on-site ATMs. They had a debit card base of

829,876. They opened a representative office in Dubai.

COMPANY SLOGAN

The path of prudence ‘Think investments’ ‘Think Kotak’. The bank of the

future will have 3 defining qualities: Simplicity, Humility and Prudence

COMPANY VISION

The global Indian financial services brand.

The most preferred employer in financial services.

The most trusted financial service company.

Value Creation

99

HUMAN RESOURCE

Table No. 4.24

THE DISTRIBUTION OF TOTAL EMPLOYEES OF THE BANK ON THE

BASIS OF DESIGNATION AND SEX

Designation/sex Male Female TOTAL

Officer 2011 1029 3040

Executives 3232 2100 5332

Sub staff 121 39 260

Total 5364 3168 8632

(Sources: KOTAK MAHINDRA Bank HR Department)

Table No. 4.25

THE BOARD OF DIRECTORS OF KOTAK MAHINDRA BANK LTD.

Shankar Acharya Chairman / Chair Person

C Jayaram Executive Director

Anand G Mahindra Director

Shivaji Dam Director

Sudipto Mundle Director

Uday Kotak Exec. Vice Chairman & Managing

Director

Dipak Gupta Executive Director

Cyril Shroff Director

Asim Ghosh Director

(Sources: KOTAK MAHINDRA Bank Financial Reports)

TECHNOLOGY OF THE BANK

KOTAK MAHINDRA Bank, a player in the area of wealth management, has

selected i-flex's holistic wealth management solution (created by : i-flex solutions,

a provider of technology solutions to the global financial services industry ) Flexcube

Private Banking, which will help KOTAK MAHINDRA Bank to manage

relationships with high net worth individuals. "Flexcube Private Banking gives us the

opportunity to address high net worth individuals comprehensively and provides us

with a competitive edge.

100

AWARDS AND RECOGNIZATION

At Kotak Mahindra Group takes a client-centric view and constantly innovate

to provide the customers with the best of services and infrastructure. Banks have

regularly received accolades that stand testimony to our success in this endeavour.

Some of the bank recent achievements are:

1) Banking Technology Excellence Awards Best Bank Award in IT Framework

and Governance among Other Banks' – 2009.

2) Best Corporate Governance Practices - Ranked among the top 5 companies in

Asia Pacific, 2009.

3) Best private Bank in India, for Wealth Management business, 2009.

4) Best Customer Relationship Achievement - Winner 2008 & 2009.etc

CORPORATE INITIATIVES

Community investment and development Kotak Mahindra views Corporate

Social Responsibility as an investment in society and in its own future. Kotak uses the

power of its human and financial capital to transform communities into vibrant,

desirable places for people to live. The group leverages its core competencies in three

areas:

1) Sustainability: An integral part of all Kotak Mahindra Group activities is to be

consistently responsible to shareholders, clients, employees, society and the

environment.

2) Economic Development: By helping people to achieve their financial goals,

Kotak strengthens the fabric of communities and helps them overcome

unemployment and poverty to help them shape their future.

3) Doing My Bit: A growing number of employees are committed to civic

leadership and responsibility with the support and encouragement of the Kotak

Group. A number of employees have been involved in strengthening

communities.

101

CREDIT RATINGS

1) Credit rating agency ICRA assigned the highest 'LAA' rating to the proposed

Rs 100 crore upper Tier II bonds programme of KOTAK MAHINDRA Bank.

The rating indicates high credit quality and low risk. The rating factors the

bank's strong position in commercial vehicle finance and improving franchise

in other retail asset segments such as personal loans and mortgage finance. It

also takes into account the bank's improving financial performance and ability

to maintain asset quality with negligible losses despite its greater focus on the

non- salaried individual segment.

2) ICRA also assigned 'A1+' rating to the Rs 500 crore short -term debt

programme of Investsmart Financial Services, which was increased from Rs

250 crore. The rating indicates highest quality and lowest credit risk in short

term.

Table No. 4.26

THE PRODUCTS AND SERVICES OF THE KOTAK MAHINDRA BANK

LTD.

BANKING AND SAVINGS

Banking Accounts

Credit Cards

Demat

Deposits

Convenience Banking

NRI Services

Privy League

Business

LOANS AND BORROWINGS

Personal Loans

Car Loans

Home Loans

Loans Against Property

Commercial Loans

Dealer Finance

INVESTMENT AND INSURANCE

Life Insurance

Mutual Funds

Share Trading

Structured Products

Gold

Estate Planning

Wealth Management

Consumer Research

Investing in IPOs

Portfolio Management

CORPORATE AND INSTITUTION

Corporate Finance

Custody Services

Investment Banking

Institutional Equities

Treasury

Private Equity

Institutional Equities

Realty Fund

(Sources: KOTAK MAHINDRA Bank Marketing Department)

102

REGISTERED OFFICE:

36-38A, Nariman Bhavan, 227, Nariman Point ,Mumbai ,Maharashtra ,400021

Table No. 4.27

THE LISTING INFORMATION OF THE KOTAK MAHINDRA BANK LTD.

Face Value Of Equity Shares 5

Market Lot Of Equity Shares 1

BSE Code 500247

NSE Code KOTAKBANK

BSE Group A

(Sources: KOTAK MAHINDRA Bank Financial Reports)

103

Table No. 4.28

THE FINANCIAL FACTS OF THE KOTAK MAHINDRA BANK LTD.

Items 2005-06 2006-07 2007-08 2008-09 2009-10

No. of offices 79 110 182 225 257

No. of employees 3597 5437 9058 8227 8632

Business per employee (in Rs.

lakh) 352.00 383.91 383.84 347.00 487.00

Profit per employee (in Rs.

lakh) 4.15 3.13 4.00 3.00 7.00

Capital and Reserves &

surplus 865 1662 3594 3906 4540

Deposits 6566 11000 16424 15645 23886

Investments 2856 6862 9142 9110 12513

Advances 6348 10924 15552 16625 20775

Interest income 719 1319 2535 3065 3256

Other income 218 319 463 274 628

Interest expended 339 699 1310 1547 1397

Operating expenses 387 613 1019 1196 1189

Cost of Funds (CoF) 4.82 5.11 6.14 6.00 4.50

Return on advances adjusted

to CoF 5.58 6.51 7.48 9.50 9.01

Wages as % to total expenses 23.59 22.33 22.29 21.28 22.56

Return on Assets 1.39 0.94 1.10 1.03 1.72

CRAR 11.27 13.46 18.65 20.01 18.35

Net NPA ratio 0.24 1.98 1.78 2.39 1.73

(Sources: KOTAK MAHINDRA Bank Financial Reports and Website www. iba.org)

104

4.3.6 YES BANK

(A New Generation Private Sector Bank)

HISTORY OF THE BANK

YES Bank was founded on 21st November, 2003 by a skilled industrialist Mr.

Rana Kapoor. He shaped a well educated apex organizing group to invent a qualified,

consumer centred and service provoked private Bank.

VISION AND COMMITMENT OF THE BANK

To be recognised as the WORLD’S BEST QUALITY BANK IN INDIA.

To provide a Delightful Banking Experience to all its customers.

To be a long term partner with all stakeholders particularly customers by

creating & sharing value.

YES BANK will continue to declare its promise through consistent communication

activities under the brand slogans "Experience our Expertise" and "YES for

YOU".

HUMAN RESOURCE

Table No. 4.29

THE DISTRIBUTION OF TOTAL EMPLOYEES OF THE BANK ON THE

BASIS OF DESIGNATION AND SEX

Designation/sex Male Female TOTAL

Officer 578 429 1007

Executives 1200 672 1872

Sub staff 116 39 155

Total 5364 3168 3034

(Sources: YES Bank HR Department)

105

Table No. 4.30

THE BOARD OF DIRECTORS OF YES BANK LTD.

Mr. Rana Kapoor Managing Director & CEO

Chairman, Nominations &

Governance Committee ,

Founding Promoter

Mr. Wouter Kolff Independent Director

Former Vice-Chairman, Managing

Board, Rabobank International,

Netherlands,

ABN Amro, Europe

Mr. Bharat Patel Independent Director

Chairman, Investor Relations

Committee

Mr. S.L Kapur Non - Executive Chairman

Former Secretary, Govt. of

India (Ministry of Food Processing

& SSI)

Mr. Arun K Mago Independent Director

Former Chief Secretary, Govt. of

Maharashtra

Chairman, Board Remuneration

Committee

Ms Radha Singh Independent Director

Former Union Agriculture

Secretary, Government of India

Mr Ajay Vohra Independent Director

Managing Partner of the Corporate,

Tax and Business Advisory Law

firm, Vaish Associates

Chairman, Audit & Compliance

Committee

(Sources: YES Bank Marketing Department)

106

TECHNOLOGY OF THE BANK

YES BANK firmly believes that Technology is one of its biggest differentiator

in the marketplace. Whilst the technologies that the bank we deploys are also

available to everybody else, the bank creates a difference by how we deploys them

and deliver superior value to our end customer.

YES BANK technology team is a truly strategic team that follows IS Lite

model of Gartner, wherein only Project Management, Architecture and Vendor

Management is done in-house, and rest everything (IT Operations, Infrastructure

Support etc) is outsourced. The bank thoroughly evaluated core & non core

technology strengths and consciously decided to outsource all non core activities to

organizations that can do it better than bank.

The YES BANK technology supports includes Wipro, Sanovi, Wincor

Nixdorf, VSNL, Reuters, Murex, Intel Corporation, i-Flex Solutions, De La Rue,

Cisco Systems, Cash Tech.

AWARDS AND RECOGNISATION

1. ‘Most Innovative Bank in India’ awarded by The New Economy First

Annual Banking and Finance Awards 2008 held in London and is the only

Indian Bank to bag this award till today.

2. NASSCOM Award ‘IT Innovations in Emerging India’ (April 2006).

3. YES BANK won the prestigious Emerging Markets Sustainable Bank of

the Year Award at the Financial Times/IFC, Washington Sustainable

Banking Awards held in London.

CORPORATE GOVERNANCE

As a new age private sector Bank, YES BANK is establishing the highest

standards of Corporate Governance right across the organisation. With an excellent

Board of Directors and the institution of all recommended sub committees, the bank is

already compliant with all statutory requirements.

107

CREDIT RATING

YES BANK has obtained a long-term credit rating of LAA- by ICRA and AA-

by CARE to raise an aggregate of INR 1.8 billion of subordinated Tier II debt.

ICRA (Moody's affiliate in India) has reaffirmed the Bank's,A1+ rating for its INR 15

billion Certificate of Deposit programme., A1+ rating indicates the highest level of

safety in the short-term.

SOCIAL INITIATES

'Responsible Banking' in India, where the concept of Corporate Social

Responsibility (CSR) and sustainability are integrated in its Business Focus. YES

BANK is committed to adding long term value to society, to differentiate itself in the

marketplace based on a strong 'sustainability mandate' and to build in flexibility and

openness as part of its core strategy. YES BANK received the Environment

Leadership award from USAID for contributions made through working in

partnerships to improve the environment /quality of life for the people of Asia

The team offers Responsible Corporate Citizenship Advisory Services to large

corporations, emerging institutions, NGOs and social businesses involved in the

environmental, education and health sectors, where social entrepreneurship is seen by

the Bank as a key driver to inclusive development in India. There is a strong focus on

identifying, developing and promoting scalable models of social entrepreneurship.

The advisory services are also extended to the Bank’s clients in Corporate Finance,

Business Banking, Agribusiness Rural & Social Banking and Retail Banking.

108

Table No. 4.31

THE PRODUCTS OFFERED BY THE YES BANK LTD.

1) Transaction Banking

2) Corporate Finance

3) Term loans

4) Account Services

5) Operating Accounts

6) EEFC Accounts

7) Working Capital

8) Overdraft

9) Order Invoice / Financing

10) Supply Chain Finance

(Sources: YES Bank Marketing Department)

REGISTERED OFFICE: Nehru Centre, 9th Floor, and Discovery of India, Dr. A B

Road Mumbai, and Maharashtra- 400018

Table No. 4.32

THE LISTING INFORMATION OF THE YES BANK LTD.

Face Value Of Equity Shares 10

Market Lot Of Equity Shares 1

BSE Code 532648

NSE Code YESBANK

BSE Group A

(Sources: YES Bank Financial Reports)

109

Table No. 4.33

THE FINANCIAL FACTS OF THE YES BANK LTD.

Items 2005-06 2006-07 2007-08 2008-09 2009-10

No. of offices 9 41 68 118 151

No. of employees 627 2443 3150 2671 3034

Business per employee (in Rs.

lakh) 848.08 530.50 683.12 988.36 1526.70

Profit per employee (in Rs.

lakh) 8.82 3.86 6.35 11.38 15.75

Capital and Reserves &

surplus 573 787 1319 1624 3090

Deposits 2910 8220 13273 16169 26799

Investments 1350 3073 5094 7117 10210

Advances 2407 6290 9430 12403 22193

Interest income 193 588 1305 2001 2370

Other income 97 195 361 435 576

Interest expended 105 416 974 1492 1582

Operating expenses 86 193 341 419 500

Cost of Funds (CoF) 4.72 6.36 7.83 8.67 6.05

Return on advances adjusted

to CoF 3.88 3.36 4.01 4.96 4.19

Wages as % to total expenses 26.27 19.26 15.39 11.41 12.34

Return on Assets 2.13 1.44 1.54 1.59 1.79

CRAR 16.40 13.60 13.60 16.60 20.60

Net NPA ratio 0.00 0.00 0.09 0.33 0.06

(Sources: YES Bank Financial Reports and Website www.iba.org)

110

4.4 PROFILE OF RESPONDENTS

Table No. 4.34

THE DISTRIBUTION OF RESPONDENT EMPLOYEES ON THE BASIS OF

‘DESIGNATION’

Name of the Bank/Grade Officers Clerk/Executives Total

KARNATAKA BANK 50 50 100

AXIS BANK 50 50 100

HDFC BANK 50 50 100

ICICI BANK 50 50 100

KOTAK MAHINDRA BANK 50 50 100

YES BANK 50 50 100

TOTAL 300 (50%) 300 (50%) 600

(Sources: Primary Data)

The above table reveals that, the proportion of officer grade employees and

clerk/executive grade employees are same in all the selected banks. The same detail is

shown in the chart below:

Chart No. 4.1

THE DISTRIBUTION OF EMPLOYEES ON THE BASIS OF ‘DESIGNATION

0

10

20

30

40

50

50 50 50 50 50 50 50 50 50 50 50 50

Officers

Clerk/Executives

111

Table No 4.35

THE DISTRIBUTION OF EMPLOYEES ON THE BASIS OF SEX

Name of the Bank/ SEX Male Female Total

KARNATAKA BANK 67 33 100

AXIS BANK 70 30 100

HDFC BANK 60 40 100

ICICI BANK 59 41 100

KOTAK MAHINDRA BANK 72 28 100

YES BANK 62 38 100

TOTAL 390(65%) 210(35%) 600

(Sources: Primary Data)

The above table reveals that the proportion of male is more (65%) than

proportion of female in every private sector bank.

Chart No. 4.2

THE DISTRIBUTION OF EMPLOYEES ON THE BASIS OF SEX

0%

20%

40%

60%

80%

100%

67 70 60 59 72 62

33 30 40 41 28 38

Female

Male

112

Table No. 4.36

THE DISTRIBUTION OF EMPLOYEES ON THE BASIS OF ‘EDUCATION

QUALIFICATION’

Name of the Bank/Qualification Graduate Post-graduate Total

KARNATAKA BANK 74 26 100

AXIS BANK 60 40 100

HDFC BANK 65 35 100

ICICI BANK 69 31 100

KOTAK MAHINDRA BANK 70 30 100

YES BANK 60 40 100

Total 398(66%) 202(33%) 600

(Sources: Primary Data)

The above table reveals that the proportion of Graduate and post-graduate are

more (66%) than under graduate in all new generation private sector banks.

Chart No. 4.3

THE DISTRIBUTION OF EMPLOYEES ON THE BASIS OF

‘EDUCATION QUALIFICATION’

The above chart shows that 34%of the respondent employees are post-

graduates and 66% are graduates

0

50

100 74 60 65 69 70

26 40 35 31 30

Graduate

Post-graduate

113

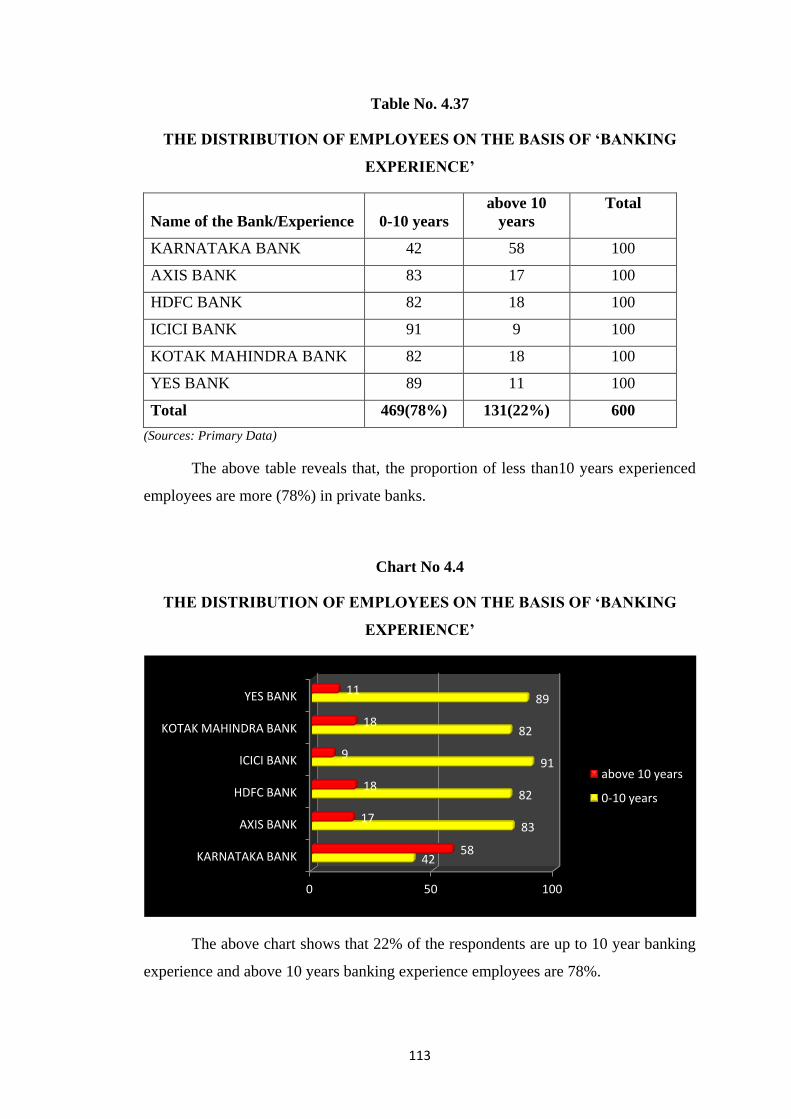

Table No. 4.37

THE DISTRIBUTION OF EMPLOYEES ON THE BASIS OF ‘BANKING

EXPERIENCE’

Name of the Bank/Experience 0-10 years

above 10

years

Total

KARNATAKA BANK 42 58 100

AXIS BANK 83 17 100

HDFC BANK 82 18 100

ICICI BANK 91 9 100

KOTAK MAHINDRA BANK 82 18 100

YES BANK 89 11 100

Total 469(78%) 131(22%) 600

(Sources: Primary Data)

The above table reveals that, the proportion of less than10 years experienced

employees are more (78%) in private banks.

Chart No 4.4

THE DISTRIBUTION OF EMPLOYEES ON THE BASIS OF ‘BANKING

EXPERIENCE’

The above chart shows that 22% of the respondents are up to 10 year banking

experience and above 10 years banking experience employees are 78%.

0 50 100

KARNATAKA BANK

AXIS BANK

HDFC BANK

ICICI BANK

KOTAK MAHINDRA BANK

YES BANK

42

83

82

91

82

89

58

17

18

9

18

11

above 10 years

0-10 years

114

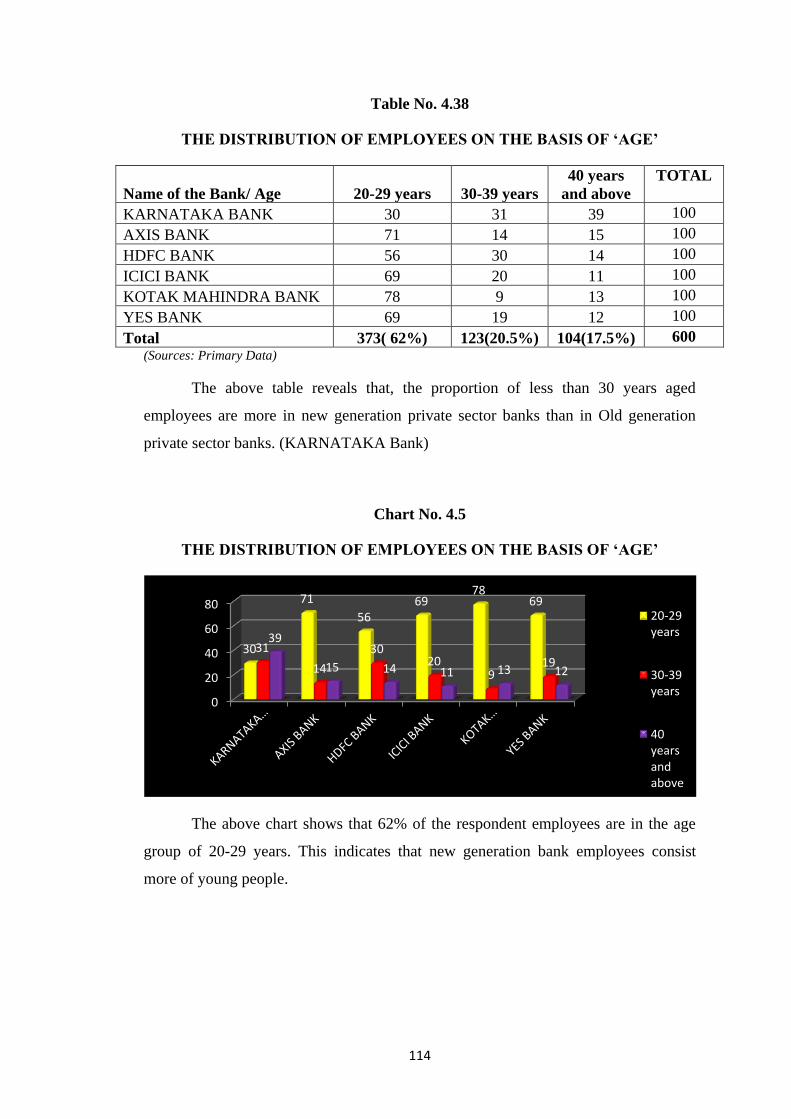

Table No. 4.38

THE DISTRIBUTION OF EMPLOYEES ON THE BASIS OF ‘AGE’

Name of the Bank/ Age 20-29 years 30-39 years

40 years

and above

TOTAL

KARNATAKA BANK 30 31 39 100

AXIS BANK 71 14 15 100

HDFC BANK 56 30 14 100

ICICI BANK 69 20 11 100

KOTAK MAHINDRA BANK 78 9 13 100

YES BANK 69 19 12 100

Total 373( 62%) 123(20.5%) 104(17.5%) 600

(Sources: Primary Data)

The above table reveals that, the proportion of less than 30 years aged

employees are more in new generation private sector banks than in Old generation

private sector banks. (KARNATAKA Bank)

Chart No. 4.5

THE DISTRIBUTION OF EMPLOYEES ON THE BASIS OF ‘AGE’

The above chart shows that 62% of the respondent employees are in the age

group of 20-29 years. This indicates that new generation bank employees consist

more of young people.

0

20

40

60

80

30

71

56 69

78 69

31

14

30 20

9 19

39

15 14 11 13 12

20-29 years

30-39 years

40 years and above

115

Table No. 4.39

THE DISTRIBUTION OF EMPLOYEES ON THE BASIS OF ‘MARITAL

STATUS’

(Sources: Primary Data)

The above table reveals that, the proportion of married employees is more

(59%) in all the Private Sector Banks as compared to proportion of unmarried

employees.

Chart No. 4.6

THE DISTRIBUTION OF EMPLOYEES ON THE BASIS OF ‘MARITAL

STATUS’

The chart shows that the total proportion of married respondent employees is

more than the proportion of unmarried employees.

0%

50%

100%

77

46 64

51 59 57

23

54 36

49 41 43

Unmarried

Married

Name of the Bank/Marital

status Married Unmarried

TOTAL

KARNATAKA BANK 77 23 100

AXIS BANK 46 54 100

HDFC BANK 64 36 100

ICICI BANK 51 49 100

KOTAK MAHINDRA BANK 59 41 100

YES BANK 57 43 100

Total 354(59%) 246(41%) 600

116

4.5 CONCLUSION

The Karnataka has a rich cultural heritage and also the cradle of many

commercial banks and as many as seven banks originated from the state. The

Karnataka state profile reveals that the number of commercial banks operating in the

state with number of branches and ATM network. The private bank profile reveals the

financial condition, profitability, man power, products and services. The profile of