401(k) Boot Camp Part 2 - Verisight Transitional Home Page 401k Bootcamp... · 401(k) Boot Camp...

86

www.verisightgroup.com 401(k) Boot Camp – Part 2 Getting Money Into the Plan November 12, 2014 Presenter: Nancy J. Manary, Director Benefits Consulting Verisight, Inc.

-

Upload

vuonghuong -

Category

Documents

-

view

219 -

download

0

Transcript of 401(k) Boot Camp Part 2 - Verisight Transitional Home Page 401k Bootcamp... · 401(k) Boot Camp...

www.verisightgroup.com

401(k) Boot Camp – Part 2Getting Money Into the Plan

November 12, 2014

Presenter:

Nancy J. Manary, Director

Benefits Consulting

Verisight, Inc.

www.verisightgroup.com

401(k) Boot Camp – Part 2

• Part 1 – Getting People Into the Plan

– Eligibility rules and enrollment procedures

• Part 2 – Getting Money Into the Plan

– Contribution rules and ADP/ACP tests

2

www.verisightgroup.com

401(k) Boot Camp - Overview

Key Objectives for Attendees

• Understand your plan’s actual provisions

• Apply plan rules correctly to avoid common operational errors

• Increase your comfort level with respect to in-house plan responsibilities

• Improve the accuracy of your explanations of plan provisions to employees

• Make your plan run smoothly and effectively

3

www.verisightgroup.com

Reminder from Part 1

• Know the provisions of your plan

• Follow the provisions of your plan

• Treat all participants in a non-discriminatory manner

• Keep good records

• Call your TPA or plan consultant for assistance

4

www.verisightgroup.com

Definitions

• Plan Sponsor

– the employer in the case of an employee benefit plan established or maintained

by a single employer,

– the employee organization in the case of a plan established or maintained by an

employee organization, or

– in the case of a plan established or maintained by two or more employers or

jointly by one or more employers and one or more employee organizations, the

association, committee, joint board of trustees, or other similar group of

representatives of the parties who establish or maintain the plan.

• Plan Administrator

– person specifically so designated by the terms of the instrument under which the

plan is operated;

– in the absence of a designation in the case of a plan maintained by a single

employer, the employer.

5

www.verisightgroup.com

Definitions

• Third Party Administrator (TPA)

– Organization that is hired by the plan sponsor (typically the employer) to run

many day-to-day aspects of a retirement plan.

– Examples of responsibilities

• amending and restating plan documents;

• preparing employer and employee benefit statements;

• assisting in processing all types of distributions from the plan;

• preparing loan paperwork for plan participant;

• testing the plan each year to gauge its compliance with all IRS non-

discrimination requirements as well as plan and participant contribution

limits;

• allocation of employer contributions and forfeitures; calculating participant

vested percentages; and, preparing annual returns and reports required by

IRS, DOL or other government agencies.

6

www.verisightgroup.com

Definitions

• Recordkeeper

– Custodian of plan assets or the plan’s investment platform.

– Examples of responsibilities

• value investments;

• provide participants with statements on their accounts;

• process distribution checks

7

www.verisightgroup.com

CONTRIBUTION RULES -- OVERVIEW

8

www.verisightgroup.com

Contribution Rules - Overview

• Check the plan to determine which types of contributions are permitted

• Possible contribution types include

– Employee salary deferrals (Pre-tax and Roth)

– Employer matching (regular, safe harbor or both)

– Employer non-matching (regular, safe harbor or both)

• Plan may have different age & service requirements and/or entry dates for different

types of contributions.

9

www.verisightgroup.com

SALARY DEFERRAL CONTRIBUTION RULES

10

www.verisightgroup.com

Two types of deferrals – Traditional and Roth

• Traditional 401(k) salary deferrals

– Deferrals not subject to income tax at the time of deferral

– Deferrals taxed when distributed from the plan

– Investment income on traditional deferrals taxed when distributed from plan

• Roth 401(k) salary deferrals

– Deferrals subject to income tax at the time of deferral

– Deferrals not taxed when distributed from the plan

– Investment income on Roth deferrals can be completely income tax free if taken

as a “qualified distribution”

11

www.verisightgroup.com

Two types of deferrals – Traditional and Roth

• Roth deferrals do not increase the dollar limit on allowable salary deferral

– Dollar limit on deferrals applies to Roth deferrals, traditional deferrals, or a

combination of both

• Roth deferrals do not increase the limit on salary deferrals available to highly

compensated employees

– Non-discrimination testing applies to Roth deferrals as well as traditional

deferrals made by HCEs

12

www.verisightgroup.com

Roth conversions

• Small Business Jobs Act of 2010 adds a conversion option for 401(k) Plans

– The Plan must allow Roth Deferrals

– Only Participants eligible for an in-service distribution allowed by the Plan can

make a conversion

– Plan amendment is required to add this option

13

www.verisightgroup.com

SALARY DEFERRAL CONTRIBUTION LIMITS

14

www.verisightgroup.com

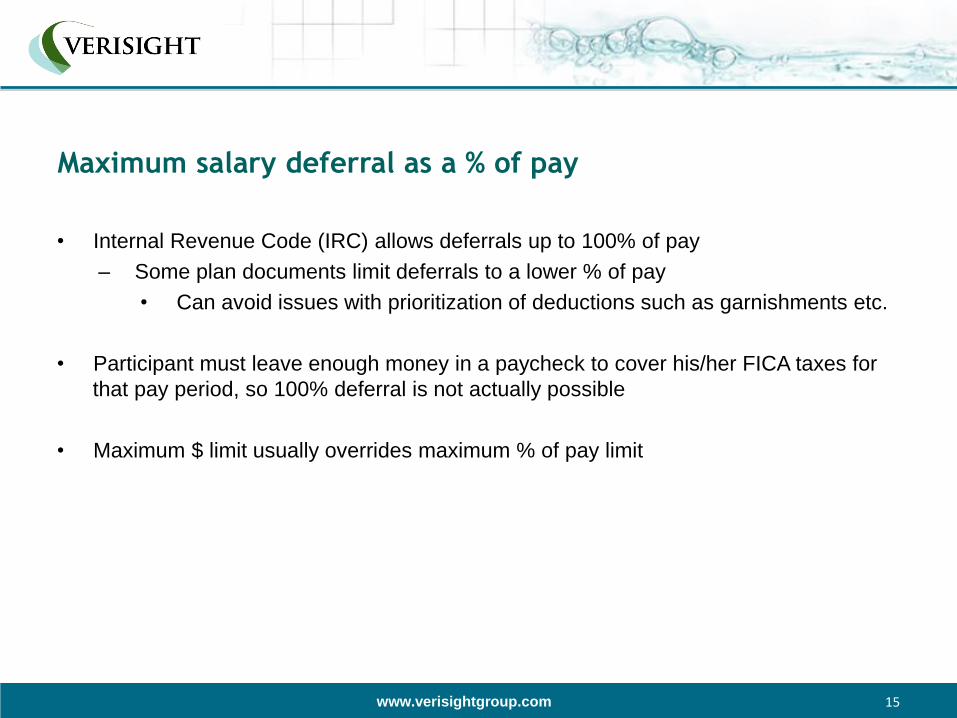

Maximum salary deferral as a % of pay

• Internal Revenue Code (IRC) allows deferrals up to 100% of pay

– Some plan documents limit deferrals to a lower % of pay

• Can avoid issues with prioritization of deductions such as garnishments etc.

• Participant must leave enough money in a paycheck to cover his/her FICA taxes for

that pay period, so 100% deferral is not actually possible

• Maximum $ limit usually overrides maximum % of pay limit

15

www.verisightgroup.com

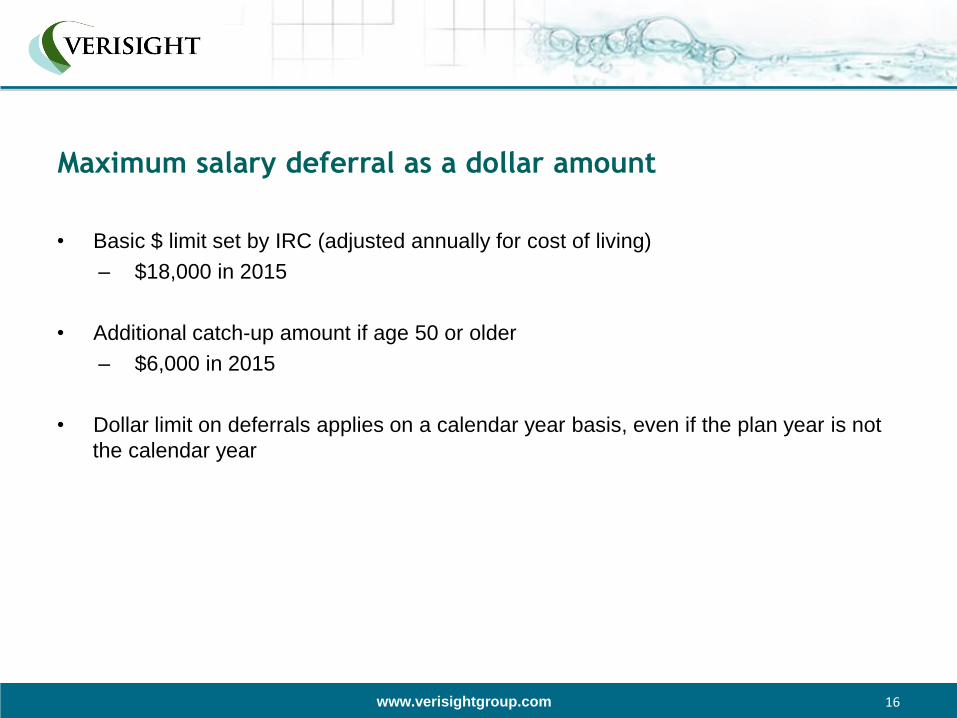

Maximum salary deferral as a dollar amount

• Basic $ limit set by IRC (adjusted annually for cost of living)

– $18,000 in 2015

• Additional catch-up amount if age 50 or older

– $6,000 in 2015

• Dollar limit on deferrals applies on a calendar year basis, even if the plan year is not

the calendar year

16

www.verisightgroup.com

Maximum salary deferral as a dollar amount

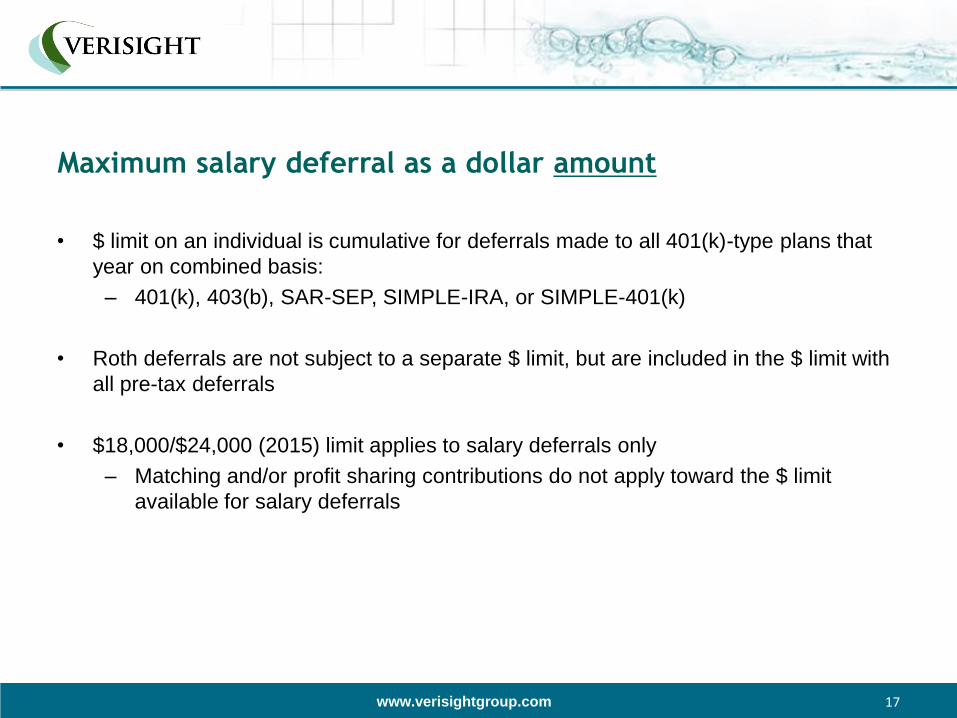

• $ limit on an individual is cumulative for deferrals made to all 401(k)-type plans that

year on combined basis:

– 401(k), 403(b), SAR-SEP, SIMPLE-IRA, or SIMPLE-401(k)

• Roth deferrals are not subject to a separate $ limit, but are included in the $ limit with

all pre-tax deferrals

• $18,000/$24,000 (2015) limit applies to salary deferrals only

– Matching and/or profit sharing contributions do not apply toward the $ limit

available for salary deferrals

17

www.verisightgroup.com

Salary deferral contribution limits

• Additional limits may apply to deferrals by highly compensated employees (HCEs)

due to non-discrimination testing (ADP test)

• HCEs may not be able to contribute maximum $ amount

18

www.verisightgroup.com

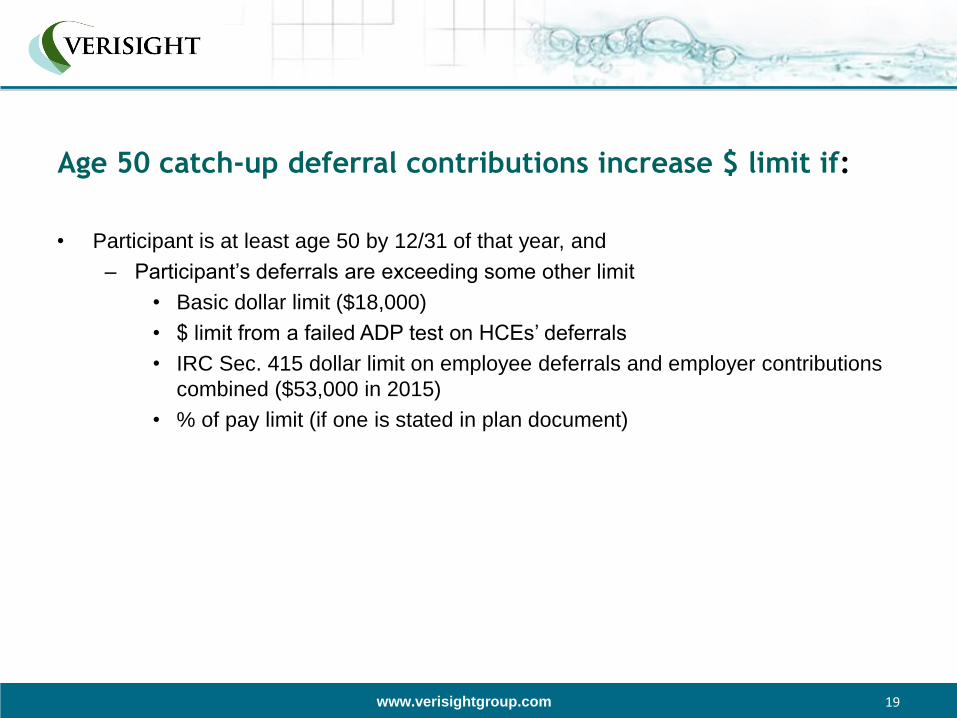

Age 50 catch-up deferral contributions increase $ limit if:

• Participant is at least age 50 by 12/31 of that year, and

– Participant’s deferrals are exceeding some other limit

• Basic dollar limit ($18,000)

• $ limit from a failed ADP test on HCEs’ deferrals

• IRC Sec. 415 dollar limit on employee deferrals and employer contributions

combined ($53,000 in 2015)

• % of pay limit (if one is stated in plan document)

19

www.verisightgroup.com

Audience Question

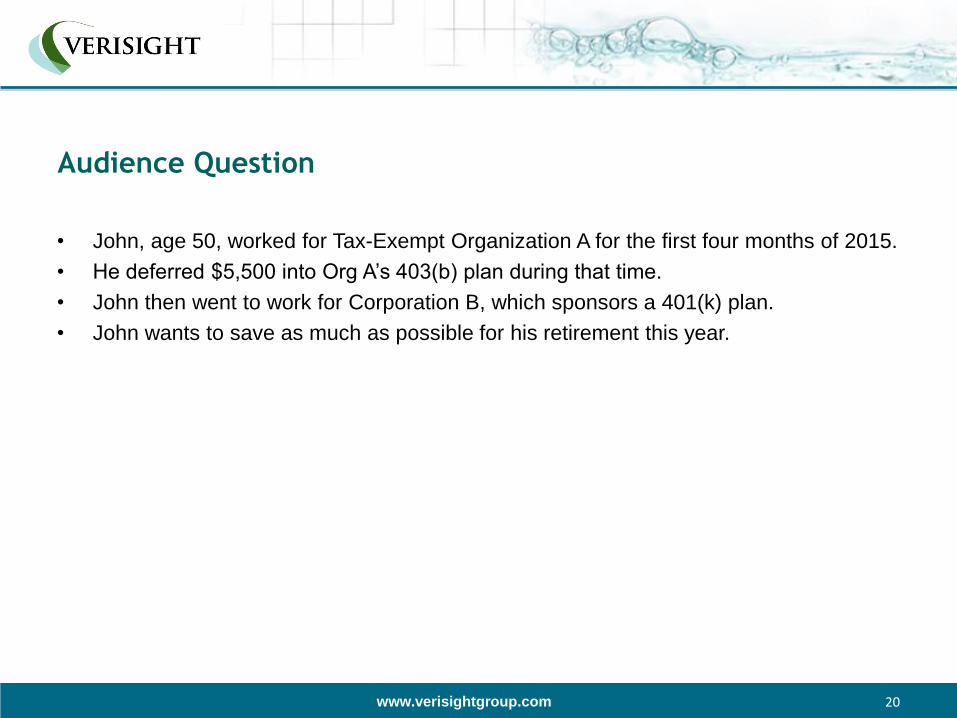

• John, age 50, worked for Tax-Exempt Organization A for the first four months of 2015.

• He deferred $5,500 into Org A’s 403(b) plan during that time.

• John then went to work for Corporation B, which sponsors a 401(k) plan.

• John wants to save as much as possible for his retirement this year.

20

www.verisightgroup.com

Audience Question

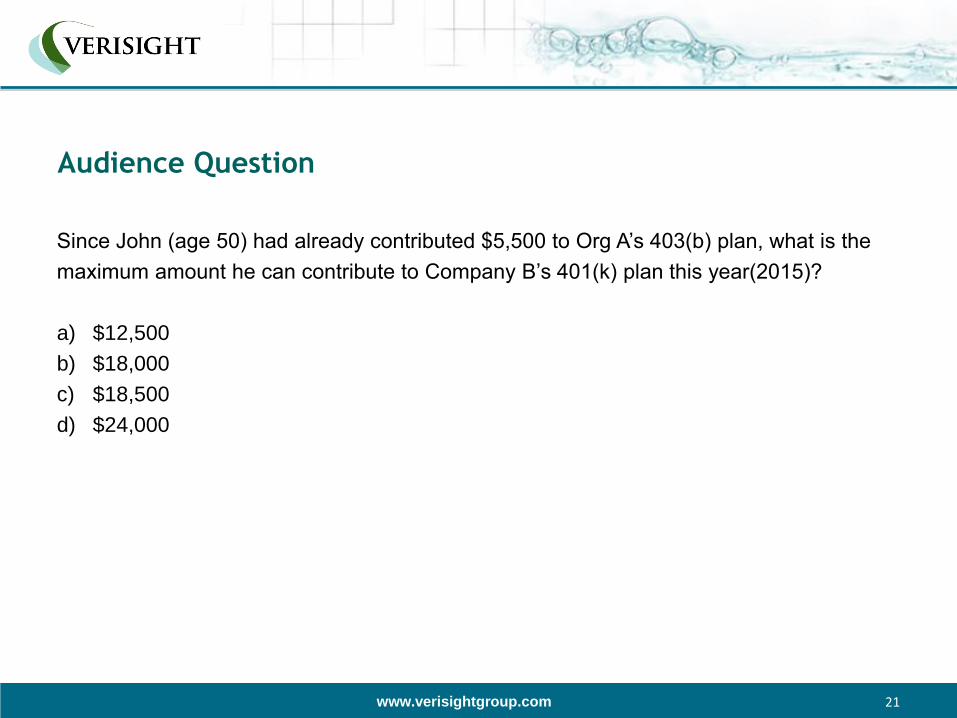

Since John (age 50) had already contributed $5,500 to Org A’s 403(b) plan, what is the

maximum amount he can contribute to Company B’s 401(k) plan this year(2015)?

a) $12,500

b) $18,000

c) $18,500

d) $24,000

21

www.verisightgroup.com

SALARY DEFERRAL OPERATIONAL ISSUES

22

www.verisightgroup.com

Employer’s responsibility for enforcing the $ limit

• Is the employer responsible for limiting an employee’s salary deferrals to the

maximum $ amount?

• Yes – but only for deferrals made from its own payroll

– Not expected to have knowledge of deferrals made by one of its employee to

another employer’s plan in the same calendar year

23

www.verisightgroup.com

Employer’s responsibility for enforcing the $ limit

• An employee is responsible for requesting a refund of excess deferrals if he/she

exceeds the maximum $ limit through multiple employers’ plans

– Deadline for request of refunds – March 1st following end of year in which

excess deferrals were made by the employee

– Deadline for employer to refund excess – April 15th following end of year in

which excess deferrals were made by employee

24

www.verisightgroup.com

Employer’s responsibility for enforcing the $ limit

• The employee can choose which plan to treat as holding the excess deferrals

– Last money in does not have to be the source of the refund

– Matching contributions attributable to refunded deferral amounts in excess of the

annual dollar limit are often forfeited to avoid discrimination issues.

• Check your plan document and discuss with your TPA

25

www.verisightgroup.com

Compensation from which deferrals are withheld

• Deferrals can only be made from “plan compensation”

• Some plans exclude certain types of compensation

– Bonuses

– Commissions

– Overtime

• Check your plan’s definition of “plan compensation”

• You cannot allow employees to make deferrals out of any compensation that is

excluded under the plan.

26

www.verisightgroup.com

Compensation from which deferrals are withheld

• Note: Most plans define “plan compensation” as the employee’s gross pay for the

year, without excluding any items such as bonuses, overtime, commissions, etc.

• Why? Excluding of any part of compensation may be discriminatory in practice, if the

exclusion affects non-highly compensated employees (NHCEs) more than it affects

highly compensated employees (HCEs).

27

www.verisightgroup.com

Compensation from which deferrals are withheld

Flip side of this issue:

• Employer cannot prevent an employee from making deferrals from any part of their

“plan compensation”

– If “plan compensation” includes overtime, you must withhold salary deferrals from

overtime pay

– If “plan compensation” includes commissions you must withhold salary deferrals

from commissions

• Even if commissions are paid in a separate check outside of the regular

payroll cycle

28

www.verisightgroup.com

Compensation from which deferrals are withheld

• If “plan compensation” includes bonuses, you must follow the employee’s salary

deferral instructions and withhold deferrals from bonuses

– Unless the employee gives separate deferral instructions for his/her bonus

– Separate deferral instructions allow employee to defer a different amount (or

nothing) out of a bonus than from regular pay

– Allowing separate deferral instructions from bonuses may be administratively

difficult for the payroll department

29

www.verisightgroup.com

Audience Question

Michelle, age 40, made a 10% of pay salary deferral election for 2015. Her base salary is

$160,000. She will be receiving a $50,000 bonus in a separate check on 12/31/2015.

The plan’s definition of compensation has no exclusions. How much, if anything, must be

withheld from Michelle’s bonus?

a) $2,000

b) $5,000

c) $8,000

d) $-0-, We do not withhold salary deferrals on bonuses.

30

www.verisightgroup.com

DEADLINE FOR DEPOSITING EMPLOYEE DEFERRALS

31

www.verisightgroup.com

Deadline for depositing employee withholdings

• As soon a salary deferrals (and/or loan payments) are withheld from an employee’s

paycheck, that money is classified by the DOL as a plan asset

• IRC and ERISA prohibit the employer from having use of plan assets

– Keeping deferrals in the employer’s checking account longer than necessary is

seen by DOL as borrowing money from the 401(k) plan.

• Use of plan assets by the employer is a prohibited transaction subject to penalty

taxes and other corrective measures

32

www.verisightgroup.com

Deadline for depositing employee withholdings

• DOL regulations require employers to deposit salary deferrals (and loan payments)

into a plan account as soon as administratively possible after the date the

amounts were withheld from pay.

• Failure to make the deposits as soon as administratively possible will subject the

employer to penalty taxes for late deposits and make-whole contributions to

participants for “lost earnings”.

33

www.verisightgroup.com

Deadline for depositing employee withholdings

• How soon is “as soon as administratively possible after the date the amounts were

withheld from pay”?

– It depends on each employer’s facts and circumstances.

– Since payroll taxes have to be deposited within a few days of payroll, DOL

assumes employers should be able to deposit 401(k) deferrals within a similarly

short time period

– Safe harbor period for small plans is 7 business days after it is withheld from

payroll

• DOL audits plans on this point and aggressively enforces the “as soon as

administratively possible” timing rule.

34

www.verisightgroup.com

Deadline for depositing employee withholdings

• Can you deposit deferrals up to 15 business days after the end of the month during

which deferrals were withheld?

• DOL regulations state that the latest date for depositing these contributions is 15

business days after the end of the month only if it was administratively impossible for

the employer to make the deposits sooner.

– There are very few reasons the DOL will accept to justify taking more than a

week--for small plans, possibly less for large plans--, to deposit deferrals into the

plan.

35

www.verisightgroup.com

Deadline for depositing employee withholdings

• Are there similar deadlines for depositing employer contributions?

• No – The deadline for depositing matching and/or profit sharing contributions into the

plan is the due date of the employer’s tax return for that year, including extensions

(as much as 8 ½ months after the end of the year).

– Exception: Safe harbor matching contributions that are calculated on a pay

period basis must be deposited at least quarterly.

36

www.verisightgroup.com

Deadline for depositing employee withholdings

• Timing of deposit of employer contributions must be non-discriminatory.

• Do not deposit employer contributions earlier for some participants than for others.

37

www.verisightgroup.com

MATCHING CONTRIBUTION BASIC RULES

38

www.verisightgroup.com

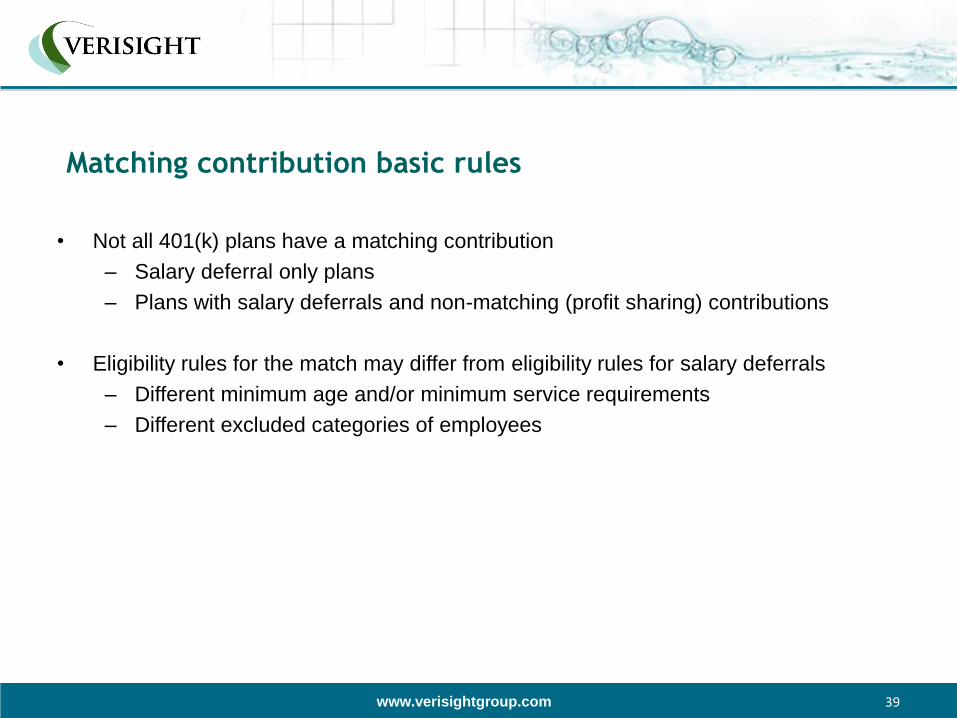

Matching contribution basic rules

• Not all 401(k) plans have a matching contribution

– Salary deferral only plans

– Plans with salary deferrals and non-matching (profit sharing) contributions

• Eligibility rules for the match may differ from eligibility rules for salary deferrals

– Different minimum age and/or minimum service requirements

– Different excluded categories of employees

39

www.verisightgroup.com

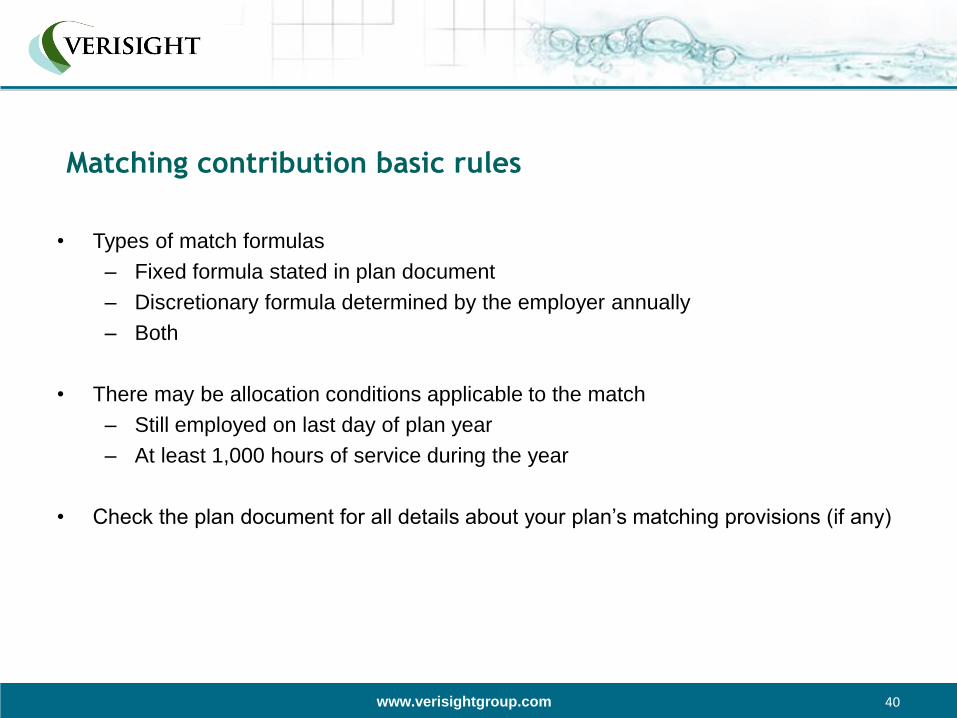

Matching contribution basic rules

• Types of match formulas

– Fixed formula stated in plan document

– Discretionary formula determined by the employer annually

– Both

• There may be allocation conditions applicable to the match

– Still employed on last day of plan year

– At least 1,000 hours of service during the year

• Check the plan document for all details about your plan’s matching provisions (if any)

40

www.verisightgroup.com

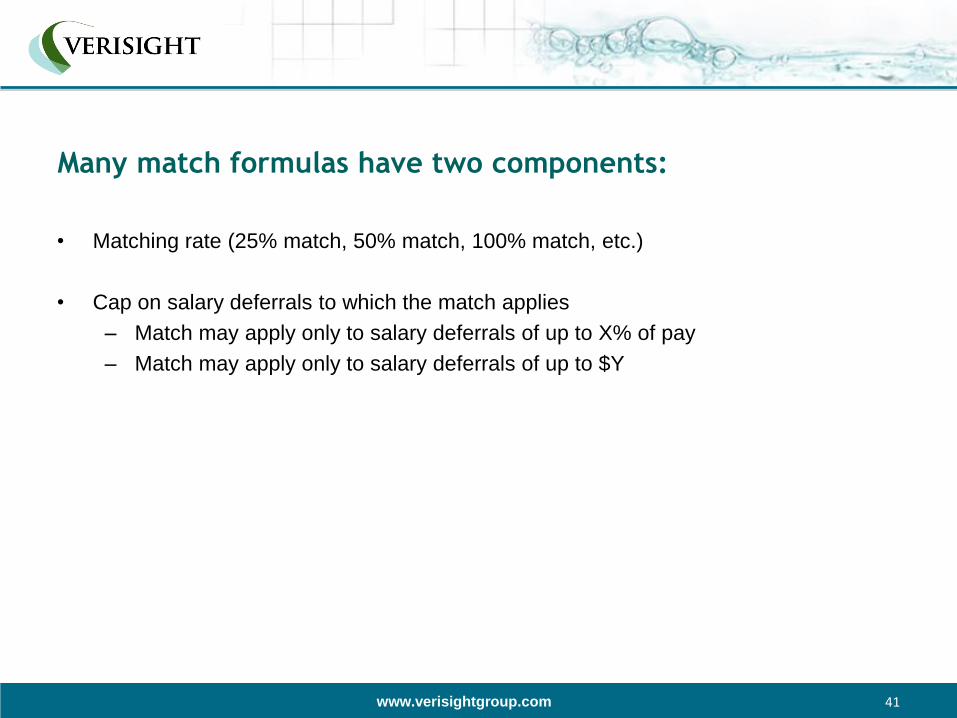

Many match formulas have two components:

• Matching rate (25% match, 50% match, 100% match, etc.)

• Cap on salary deferrals to which the match applies

– Match may apply only to salary deferrals of up to X% of pay

– Match may apply only to salary deferrals of up to $Y

41

www.verisightgroup.com

Matching contribution basic rules

• Examples of match formula with two components:

– 50% match, applicable to salary deferrals of up to 6% of pay

– 25% match, applicable to salary deferrals of up to $2,000

• Describe your match formula carefully when discussing it

– Avoid misleading employees about the match they can receive

– Avoid confusing the people who calculate the match

42

www.verisightgroup.com

Audience Question

HR rep tells employees “We match 50% up to 3% of pay”. What is the plan’s match

formula?

a) 50% match, applicable to salary deferrals of up to 3% of pay (maximum match

amount = 1.5% of pay)

b) 50% match, applicable to salary deferrals of up to 6% of pay (maximum match

amount = 3.0% of pay)

c) You cannot tell from this verbal description

43

www.verisightgroup.com

MATCHING CONTRIBUTION OPERATIONAL RULES

44

www.verisightgroup.com

Compensation used to calculate match

• Match amount must be calculated on “plan compensation”

• Cannot exclude certain types of pay [bonuses, commissions, overtime, etc.] when

calculating match amount

– Unless that type of pay is excluded from “plan compensation”

• Check your plan’s definition of “plan compensation”

– May be different for match purposes than for deferral purposes

– May exclude compensation earned prior to entry date in first year of eligibility

45

www.verisightgroup.com

Compensation used to calculate match

• Match formula applies only to compensation up to the maximum that can be taken

into consideration under a 401(k) plan

• Capped compensation = $265,000 in 2015

• Compensation in excess of the cap must be ignored when applying the match

formula

• Definition of Compensation for Safe Harbor Match must be safe harbor definition

46

www.verisightgroup.com

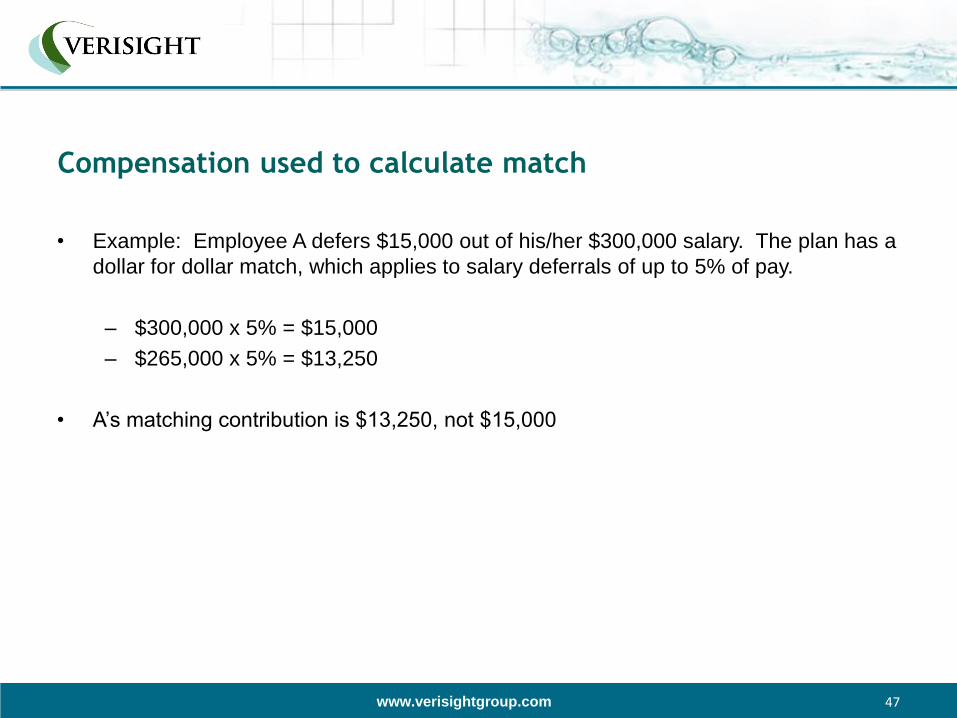

Compensation used to calculate match

• Example: Employee A defers $15,000 out of his/her $300,000 salary. The plan has a

dollar for dollar match, which applies to salary deferrals of up to 5% of pay.

– $300,000 x 5% = $15,000

– $265,000 x 5% = $13,250

• A’s matching contribution is $13,250, not $15,000

47

www.verisightgroup.com

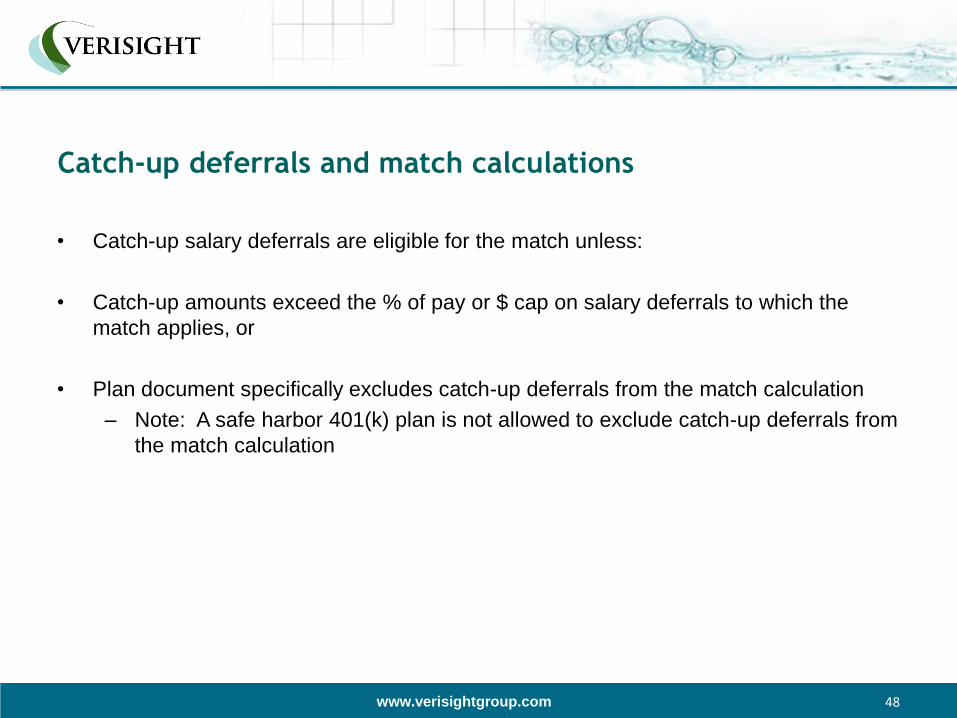

Catch-up deferrals and match calculations

• Catch-up salary deferrals are eligible for the match unless:

• Catch-up amounts exceed the % of pay or $ cap on salary deferrals to which the

match applies, or

• Plan document specifically excludes catch-up deferrals from the match calculation

– Note: A safe harbor 401(k) plan is not allowed to exclude catch-up deferrals from

the match calculation

48

www.verisightgroup.com

CALCULATING MATCHING CONTRIBUTIONS

49

www.verisightgroup.com

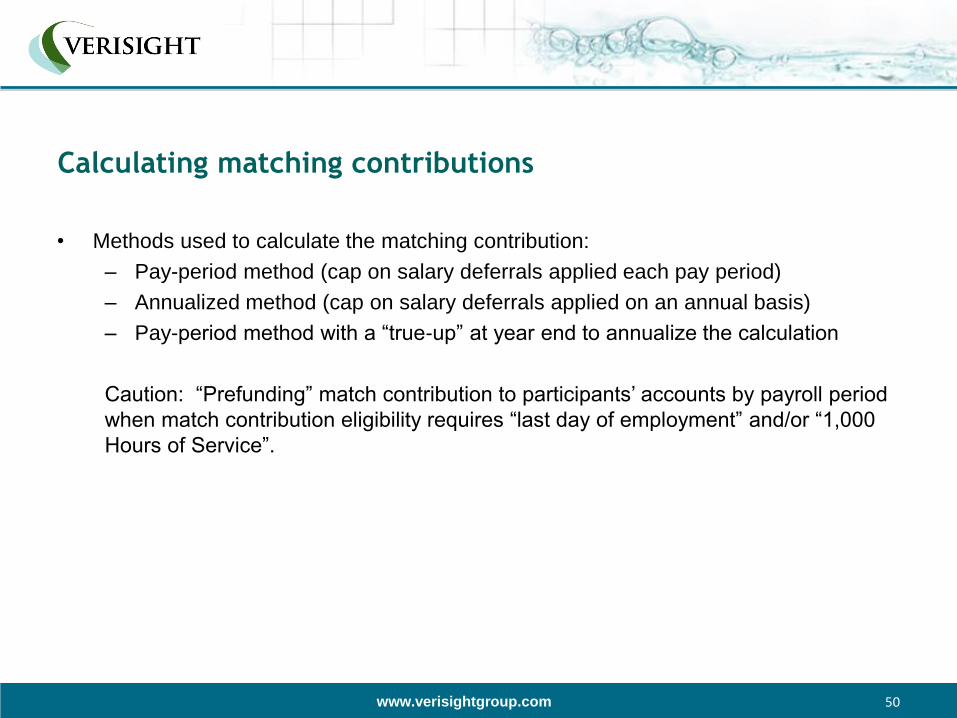

Calculating matching contributions

• Methods used to calculate the matching contribution:

– Pay-period method (cap on salary deferrals applied each pay period)

– Annualized method (cap on salary deferrals applied on an annual basis)

– Pay-period method with a “true-up” at year end to annualize the calculation

Caution: “Prefunding” match contribution to participants’ accounts by payroll period

when match contribution eligibility requires “last day of employment” and/or “1,000

Hours of Service”.

50

www.verisightgroup.com

Calculating matching contributions

• Check your plan document to see which match calculation method is specified

• If the plan has a discretionary match, the match calculation method may also be

discretionary and not stated in the plan document

– You must calculate the match using a consistent method for all participants.

51

www.verisightgroup.com

Summary

• Inform employees of the match calculation method

– Different match calculation methods can result in very different dollar amounts,

depending on how an employee’s deferrals are spread throughout the year

• Follow the match calculation method specified in the plan

– Or follow the method communicated to participants, if one is not stated in the

plan document

• Treat all participants the same when calculating the match

52

www.verisightgroup.com

Audience Question

Arnold prefers to defer out of his bonus instead of deferring by regular payroll deduction

all year. Arnold receives $90,000 in salary plus a $10,000 bonus in a separate check, for

a total of $100,000 in pay this year.

Arnold’s 401(k) plan has a 50% match, which applies to salary deferrals up to 4% of pay.

The match is calculated on a pay-period basis. Bonuses are included in the definition of

plan compensation.

53

www.verisightgroup.com

Audience Question

Arnold defers $4,000 out of his $10,000 bonus check. How much will Arnold receive as a match this year?

a) $2,000

b) $200

c) Cannot determine from the facts provided

54

www.verisightgroup.com

NON-DISCRIMINATION TESTING ON SALARY DEFERRALS

BY HIGHLY COMPENSATED EMPLOYEES

55

www.verisightgroup.com

Non-discrimination testing on HCEs

• Non-discrimination testing applies to salary deferrals made by highly compensated

employees (HCEs)

– The average % of pay deferred by HCEs is limited, based on the average % of

pay deferred by non-HCEs

• Similar non-discrimination testing applies to matching contributions made for HCEs

(not covered in this webcast due to time constraints)

– The average % of pay received as a match by HCEs is limited, based on the

average % of pay received as a match by non-HCEs

56

www.verisightgroup.com

Who is classified as an HCE?

• Any employee owning more than 5% of the business in the current year or prior year,

regardless of compensation

• Family members of > 5% owners, regardless of compensation [Family members =

owner-employee’s lineal ascendants, descendants, and spouse]

• Non-owner employees with compensation about a specified level in the prior year

[regardless of compensation in current year]

57

www.verisightgroup.com

Compensation threshold for determining non-owner HCEs

• Dollar threshold for 2015 HCEs:

– Earned more than $120,000 in 2015

• The non-owner HCE group can be limited to the top 20% of employees when ranked

by pay, using prior year data

58

www.verisightgroup.com

Non-discrimination testing on HCEs

• In-house staff handling the 401(k) plan can generally determine who is an HCE at the

beginning of a plan year

– HCE status is based on prior year’s compensation for non-owners

• HCE status is based on prior year or current year ownership status

– Therefore, newly hired owners or family members of owners are immediately

classified as HCEs in the year hired

– Current non-owner employee who becomes an owner during the year will

immediately become an HCE

59

www.verisightgroup.com

Why do you need to know who is an HCE for the current plan

year?

• So you can tell HCEs that their salary deferral contributions may be limited [based on

the average level of salary deferral participation by non-HCEs]

• So you can gather information about the amounts each HCE would like to defer this

year

– to see if their desired deferral levels are likely to pass or fail non-discrimination

testing

60

www.verisightgroup.com

NON-DISCRIMINATION TESTING - SALARY DEFERRALS

CONTRIBUTIONS

61

www.verisightgroup.com

Non-discrimination testing on salary deferrals

• Non-discrimination testing applies to salary deferral contributions made by HCEs

– Unless the plan is a Safe Harbor 401(k) plan

• The average % of pay that can be deferred by HCEs is determined by the average %

of pay deferred by non-HCEs

• Low levels of deferral participation by non-HCEs will result in low limits on the

amounts HCEs can defer

62

www.verisightgroup.com

Two testing methods available for limits on deferrals by HCEs

• Prior year testing

– Compare the average deferral % (ADP) of non-HCEs in the prior plan year to

the ADP of HCEs in the current plan year

• Current year testing

– Compare the average deferral % (ADP) of non-HCEs in the current plan year to

the ADP of HCEs in the current plan year

• HCE deferral percentages always based upon current year.

63

www.verisightgroup.com

Non-discrimination testing on salary deferrals

• Check the plan document so you know whether your plan uses prior year or current

year testing

• Prior year or current year ADP testing does not change which non-owners are

classified as HCEs in the current year.

– Determining which non-owners are HCEs is always based on employees’ prior

year compensation.

64

www.verisightgroup.com

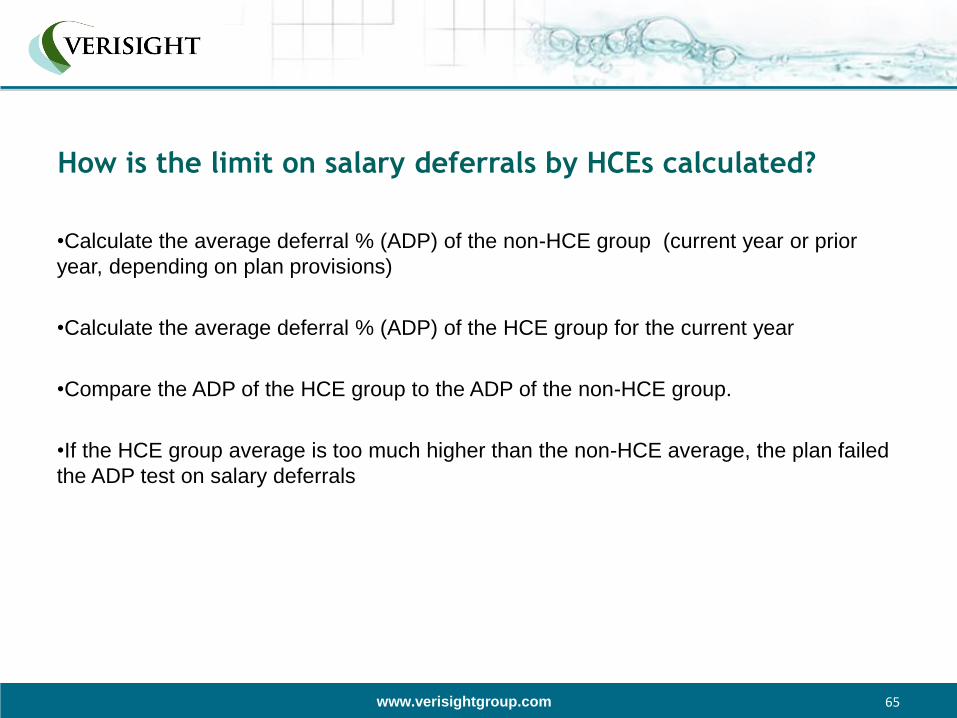

How is the limit on salary deferrals by HCEs calculated?

•Calculate the average deferral % (ADP) of the non-HCE group (current year or prior

year, depending on plan provisions)

•Calculate the average deferral % (ADP) of the HCE group for the current year

•Compare the ADP of the HCE group to the ADP of the non-HCE group.

•If the HCE group average is too much higher than the non-HCE average, the plan failed

the ADP test on salary deferrals

65

www.verisightgroup.com

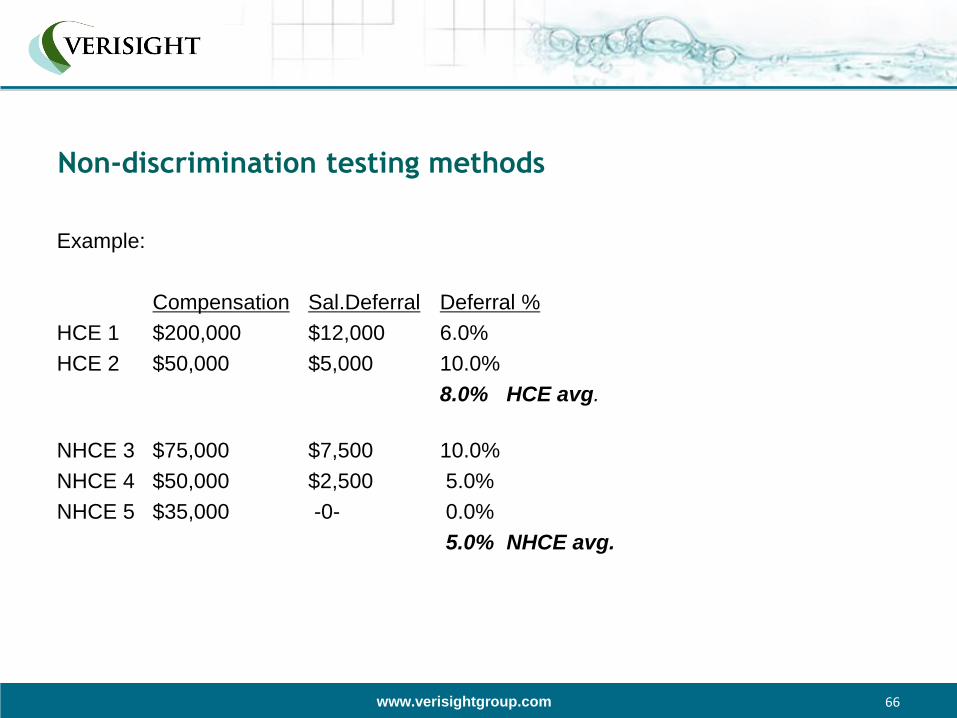

Non-discrimination testing methods

Example:

Compensation Sal.Deferral Deferral %

HCE 1 $200,000 $12,000 6.0%

HCE 2 $50,000 $5,000 10.0%

8.0% HCE avg.

NHCE 3 $75,000 $7,500 10.0%

NHCE 4 $50,000 $2,500 5.0%

NHCE 5 $35,000 -0- 0.0%

5.0% NHCE avg.

66

www.verisightgroup.com

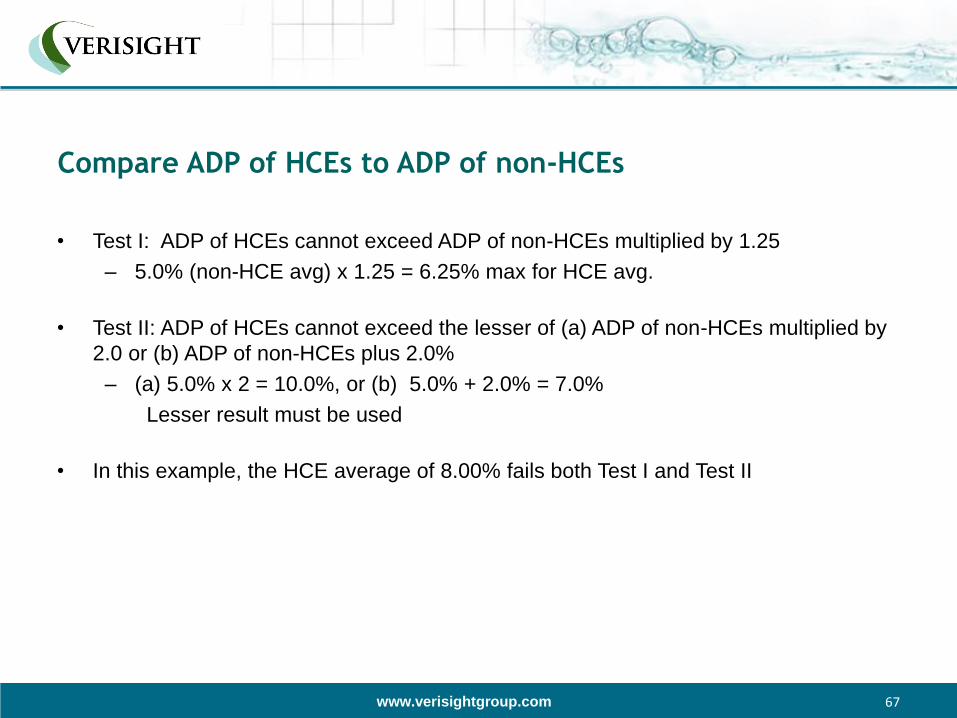

Compare ADP of HCEs to ADP of non-HCEs

• Test I: ADP of HCEs cannot exceed ADP of non-HCEs multiplied by 1.25

– 5.0% (non-HCE avg) x 1.25 = 6.25% max for HCE avg.

• Test II: ADP of HCEs cannot exceed the lesser of (a) ADP of non-HCEs multiplied by

2.0 or (b) ADP of non-HCEs plus 2.0%

– (a) 5.0% x 2 = 10.0%, or (b) 5.0% + 2.0% = 7.0%

Lesser result must be used

• In this example, the HCE average of 8.00% fails both Test I and Test II

67

www.verisightgroup.com

CORRECTING FAILED NON-DISCRIMINATION TESTS ON

SALARY DEFERRALS

68

www.verisightgroup.com

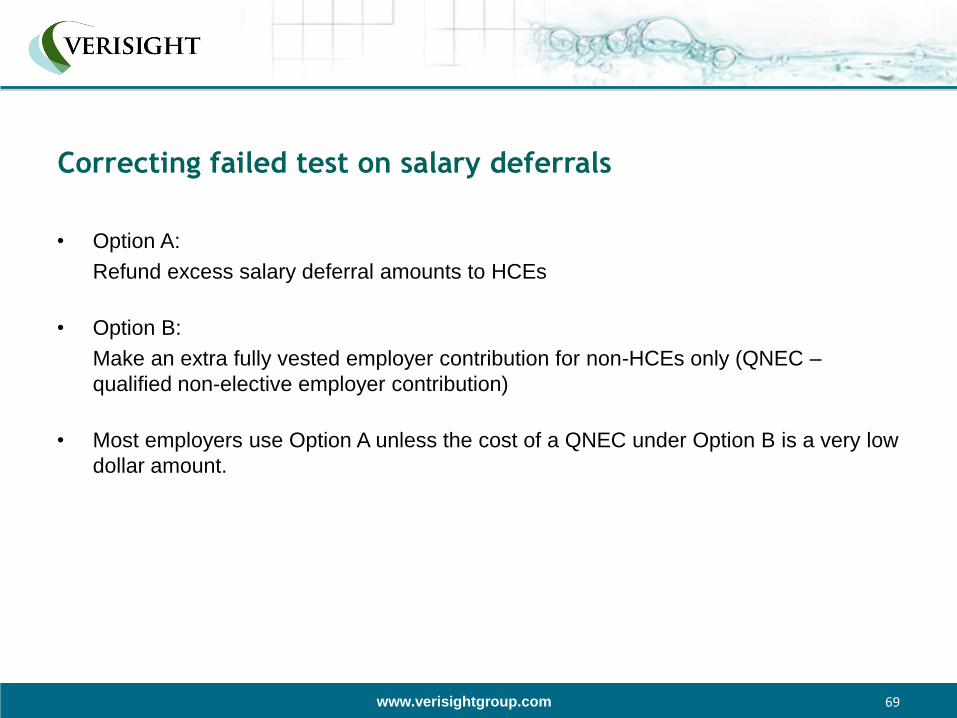

Correcting failed test on salary deferrals

• Option A:

Refund excess salary deferral amounts to HCEs

• Option B:

Make an extra fully vested employer contribution for non-HCEs only (QNEC –

qualified non-elective employer contribution)

• Most employers use Option A unless the cost of a QNEC under Option B is a very low

dollar amount.

69

www.verisightgroup.com

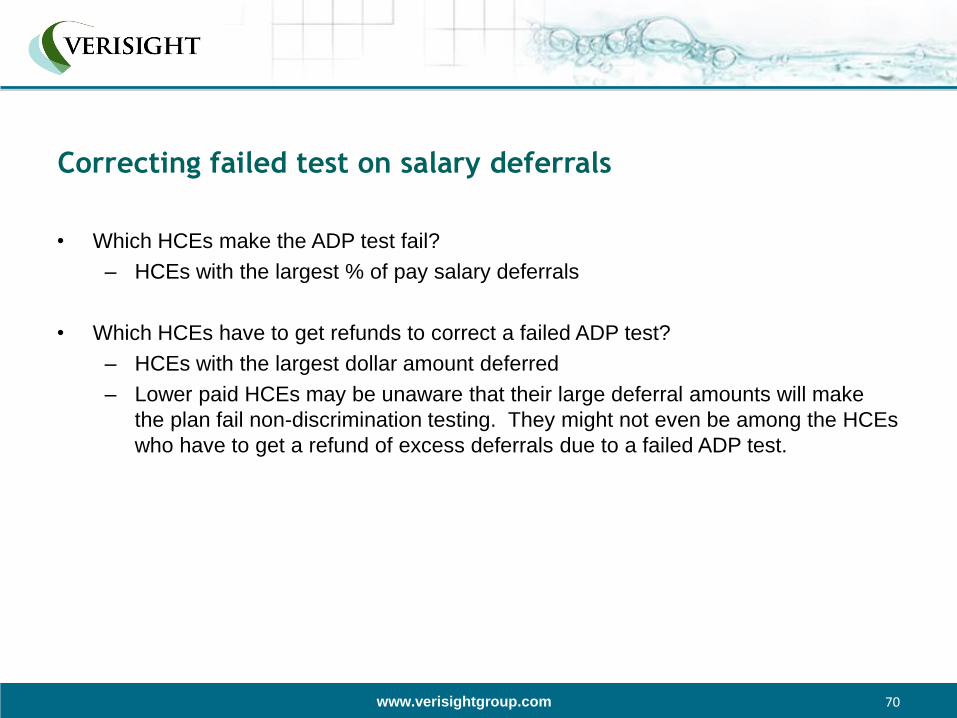

Correcting failed test on salary deferrals

• Which HCEs make the ADP test fail?

– HCEs with the largest % of pay salary deferrals

• Which HCEs have to get refunds to correct a failed ADP test?

– HCEs with the largest dollar amount deferred

– Lower paid HCEs may be unaware that their large deferral amounts will make

the plan fail non-discrimination testing. They might not even be among the HCEs

who have to get a refund of excess deferrals due to a failed ADP test.

70

www.verisightgroup.com

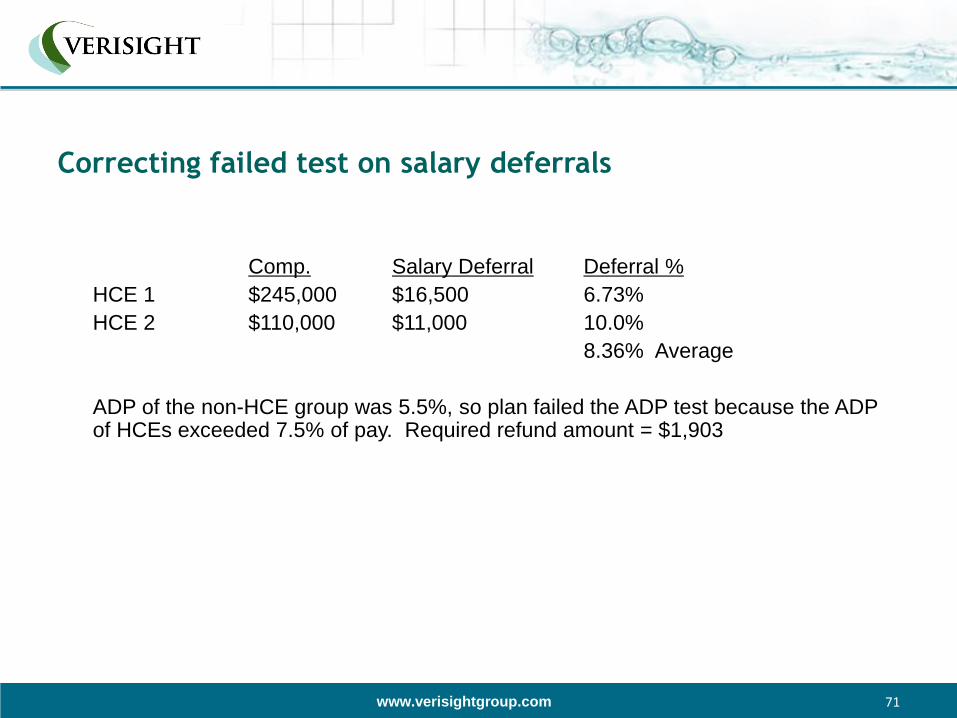

Correcting failed test on salary deferrals

Comp. Salary Deferral Deferral %

HCE 1 $245,000 $16,500 6.73%

HCE 2 $110,000 $11,000 10.0%

8.36% Average

ADP of the non-HCE group was 5.5%, so plan failed the ADP test because the ADP of HCEs exceeded 7.5% of pay. Required refund amount = $1,903

71

www.verisightgroup.com

Correcting failed test on salary deferrals

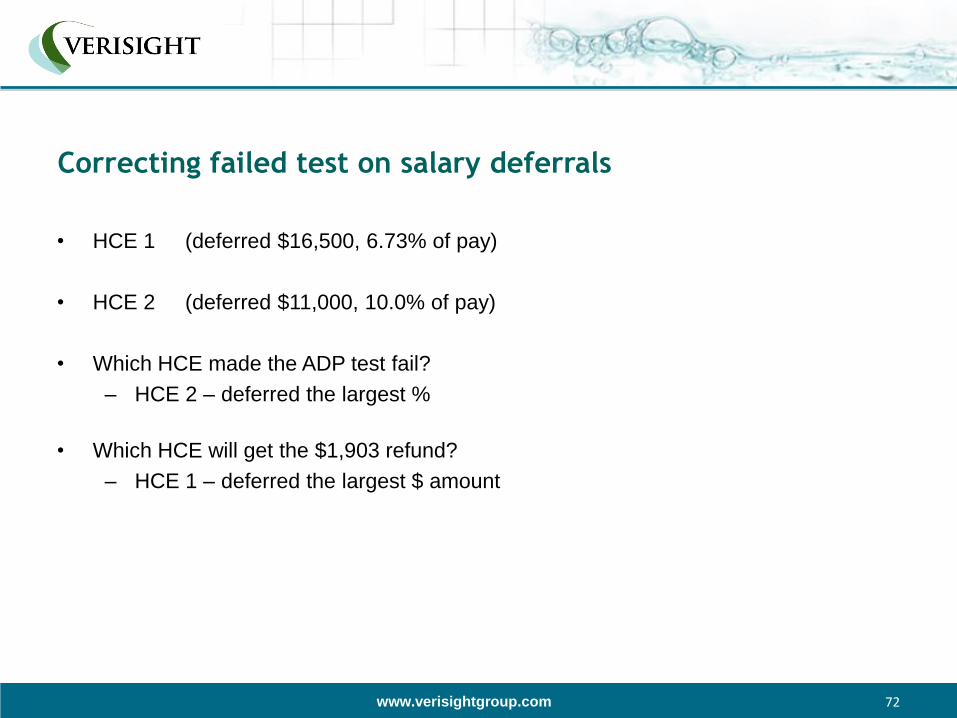

• HCE 1 (deferred $16,500, 6.73% of pay)

• HCE 2 (deferred $11,000, 10.0% of pay)

• Which HCE made the ADP test fail?

– HCE 2 – deferred the largest %

• Which HCE will get the $1,903 refund?

– HCE 1 – deferred the largest $ amount

72

www.verisightgroup.com

Deadline for refunding excess salary deferrals to correct a

failed ADP test

• 2 ½ months after end of plan year in which excess contributions occurred, to avoid a

10% penalty tax on employer for late refunds

• 3/15/2015 for plan year ending 12/31/2014

• By end of plan year following year in which excess contributions occurred, to avoid

plan disqualification

• 12/31/2015 for plan year ending 12/31/2014

73

www.verisightgroup.com

Tax treatment of refunded salary deferrals to HCEs

• Taxable to employee for the calendar year in which it is refunded

– If refunded to HCE within 2 ½ months following end of plan year (March 15 for

calendar year end plan).

• Refunded amount not subject to 10% penalty tax on distributions prior to 59 ½

• Refunded amount not eligible for rollover to an IRA

74

www.verisightgroup.com

COMMON IN-HOUSE OPERATIONAL ERRORS TO AVOID

75

www.verisightgroup.com

Common error #1

• Late deposit of salary deferral and/or loan payments into the plan.

76

www.verisightgroup.com

Required corrections for error #1:

• Make employees whole through employer contribution for lost earnings

– Lost earnings

• Calculator available on DOL website

(www.dol.gov/ebsa/calculator/main.html)

– Caution – use Calculator when submitting under the DOL’s Voluntary

Fiduciary Correction Program.

• Calculation based on the greater of: Plan’s investment rate of return, or the

IRS Underpayment Rate (currently at 3%)

– Employer pays excise tax for the prohibited transaction due to use of plan assets

(borrowing from the plan)

• Excise tax is 15% of amount employer would have paid in loan interest on

the amount “borrowed” from the plan

• Excise tax reported on IRS Form 5330

77

www.verisightgroup.com

Best practices to avoid error #1

• Make sure all in-house staff understand the financial consequences to the company if

deferrals are not deposited ASAP after every pay period.

• Give salary deferral deposits the same importance and timeliness as the deposit of

payroll tax withholdings.

• Have a back-up person available if the primary person who handles this task is on

vacation, out sick, or is being replaced due to a job change.

78

www.verisightgroup.com

Common error #2

• Not following the match calculation method specified in the plan document

• Typical errors of this type include:

– Calculating match on an annualized basis when plan document specifies pay-

period match calculation

– Calculating match on a pay-period basis without a year-end true-up when plan

document specifies an annualized calculation of the match

79

www.verisightgroup.com

Required corrections to error #2

• Recalculate the match using method specified in plan document

• Deposit additional match amounts for participants who did not receive the full amount

of match to which they were entitled

• Remove the excess match amounts from accounts of participants who received too

high a match, and transfer the excess to the forfeiture account.

80

www.verisightgroup.com

Best practices to avoid common error #2

• Train in-house staff to refer to plan document for exact specifications on the way the

match is to be calculated.

• Have the third party administrator check the in-house staff’s calculation of the match.

• Amend the plan document to change the match calculation to an alternate method, if

the alternate method is preferable to the company.

81

www.verisightgroup.com

Common error #3

• Not applying the same match calculation method to all participants.

• Typical error – Calculating the match on a pay-period basis (as specified in the plan)

for most participants, but doing an annualized match calculation for those who

capped at the $18,000 limit (2015)

82

www.verisightgroup.com

Required correction for error #3

• Recalculate the match for those participants capping at $18,000 (2015 limit) in

deferrals using the method specified in the plan and transfer the excess match

amount from their accounts to the forfeiture account.

83

www.verisightgroup.com

Best practices to prevent error #3

• Communicate clearly to all employees the method used to calculate the match, so

they can plan the timing of their salary deferrals accordingly.

• Train in-house staff to follow the plan’s provisions uniformly for all plan participants.

• Consider amending the plan document to use a different method of calculating the

match, if that would better fit the company’s objectives.

84

www.verisightgroup.com

Summary

• Understand your plan’s actual provisions for contributions: deferrals and match

– Type of contributions

– Limits on contributions

• Understand your plan’s operational issues for contributions

– Timing of deposits

– Nondiscrimination testing

• Understand common operational errors and how to avoid them

85

www.verisightgroup.com

Thank You!

401(k) Boot Camp Webinars:

• November 19, 2014 – Part 3 “Getting Money Out Of The Plan”

86