4 th International Congress on Kerala Studies 2015 Disruptive Technologies in Global Electricity...

14

4 th International Congress on Kerala Studies 2015 Disruptive Technologies in Global Electricity Industry: Implications for the Future 19 th July 2015, Kochi Dr Binu Parthan

-

Upload

philip-campbell -

Category

Documents

-

view

213 -

download

0

Transcript of 4 th International Congress on Kerala Studies 2015 Disruptive Technologies in Global Electricity...

4th International Congress on Kerala Studies 2015

Disruptive Technologies in Global Electricity Industry: Implications for the Future

19th July 2015, Kochi

Dr Binu Parthan

Global Change

Energy Utility Revenue/ Business Models remain static over 100 years!

Three disruptive technologies: Distributed Energy Storage; Electric Mobility; Distributed Photovoltaics.

Major changes in Europe and North America – Asia;

India and Kerala – prepare and evolve

2

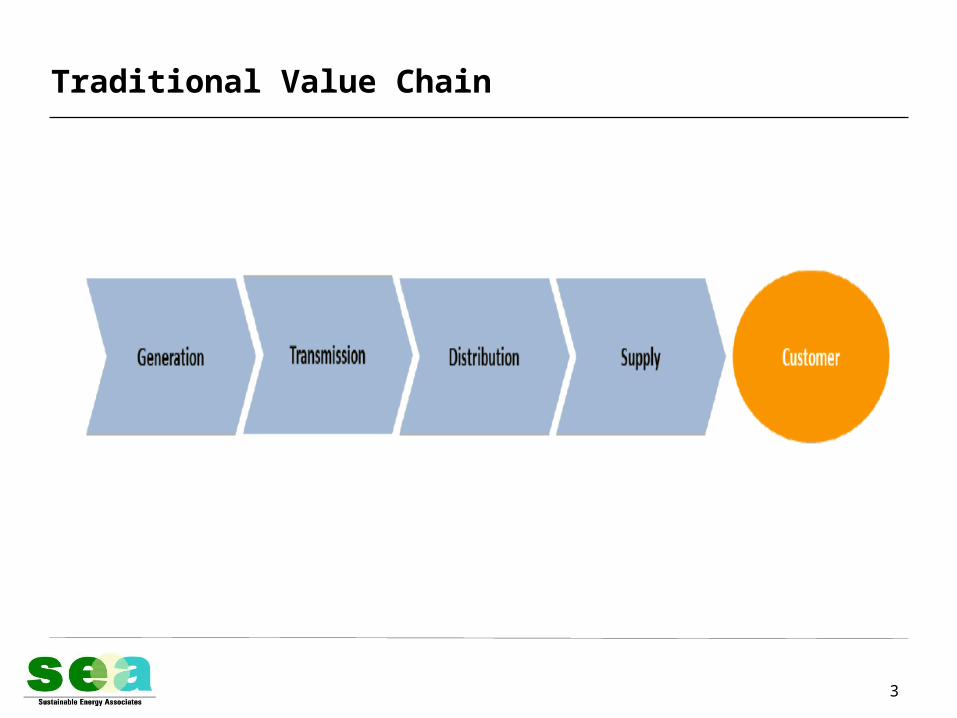

Traditional Value Chain

3

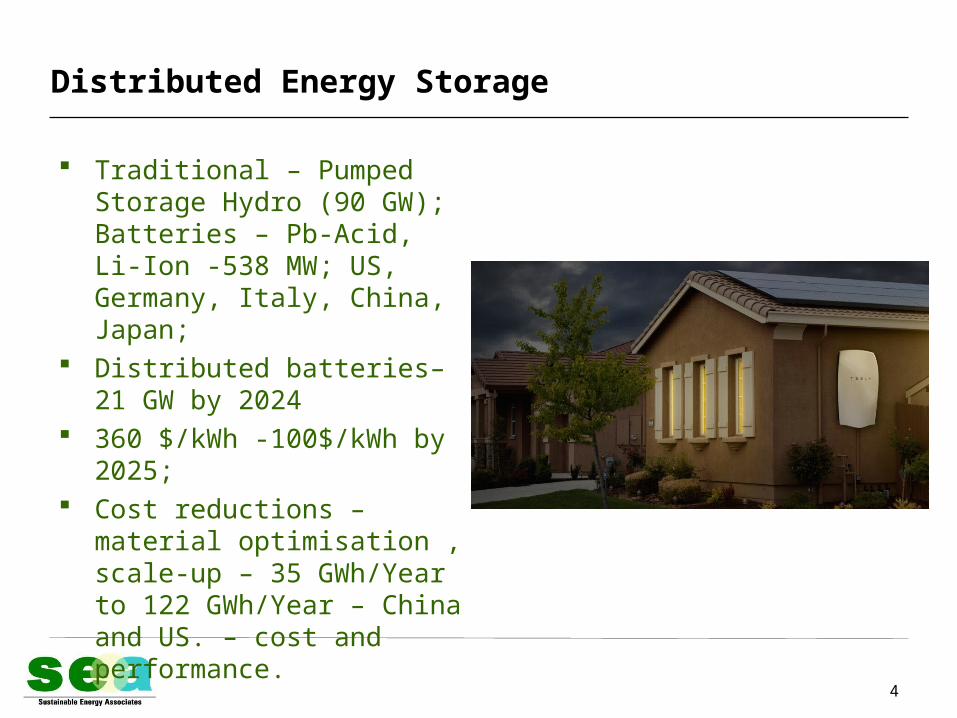

Distributed Energy Storage

Traditional – Pumped Storage Hydro (90 GW); Batteries – Pb-Acid, Li-Ion -538 MW; US, Germany, Italy, China, Japan;

Distributed batteries– 21 GW by 2024

360 $/kWh -100$/kWh by 2025; Cost reductions – material

optimisation , scale-up – 35 GWh/Year to 122 GWh/Year – China and US. – cost and performance.

4

Large-Scale Li-Ion Battery Plants

5

Electric Mobility

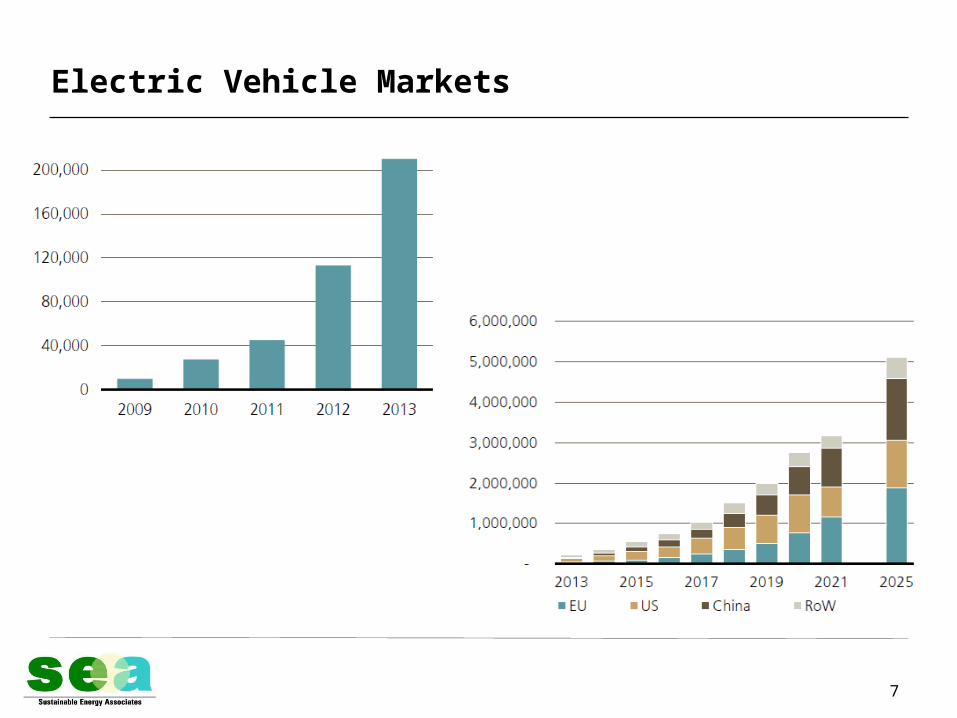

PEVs & PHEVs; High growth rates – 200,000 in

2013; Norway, Netherlands – 5% of

market; 200k – 5 million - 2025 Night-time, Off-peak electricity

demand; 20-50 kWh energy storage – 2-5

days of energy demand- V2G technology, sell electricity;

6

Electric Vehicle Markets

7

Distributed Photovoltaics

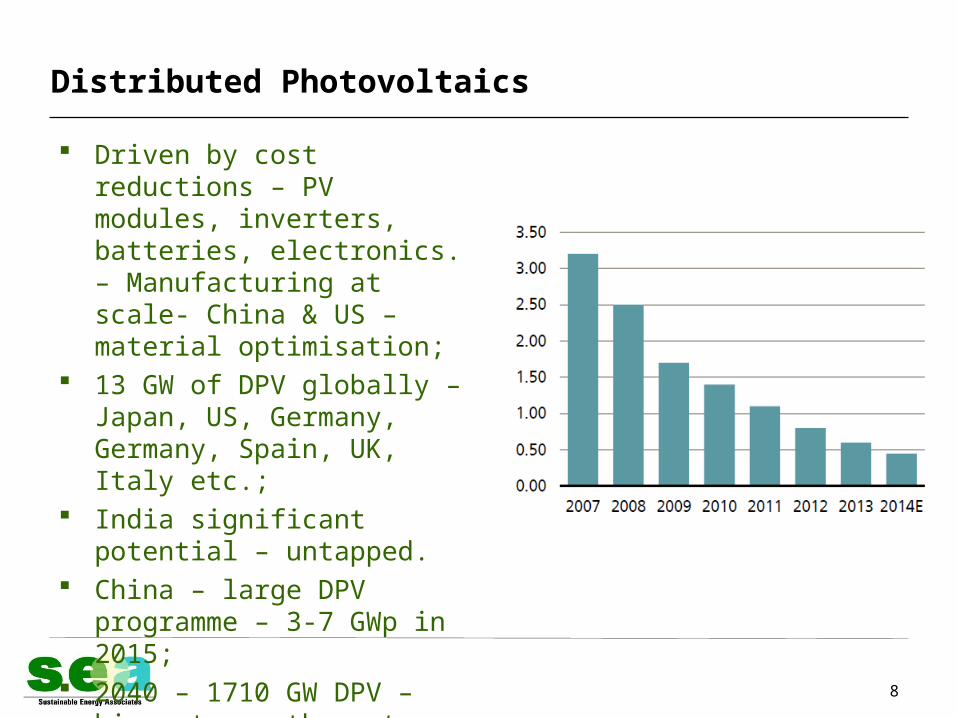

Driven by cost reductions – PV modules, inverters, batteries, electronics. – Manufacturing at scale- China & US – material optimisation;

13 GW of DPV globally – Japan, US, Germany, Germany, Spain, UK, Italy etc.;

India significant potential – untapped.

China – large DPV programme – 3-7 GWp in 2015;

2040 – 1710 GW DPV – biggest growth sector globally.

8

Innovations

EVs- charging infrastructure, superchargers, battery-swapping; self-driving cars;

PV – Inverters, BOS, Racking & mounting; Batteries material optimisation – anode

materials – energy density, lifetime, energy dissipation, charge-time reductions;

Financing – Zero upfront – leasing or PPAs ; Crowdfunding; SolarCoin – Crypto-currency;

Policy – Net-metering; wheeling and banking, battery storage policies. EVs – tax reductions, incentives, charging points, driving lanes and parking preferences etc.

9

Prosumer Evolution

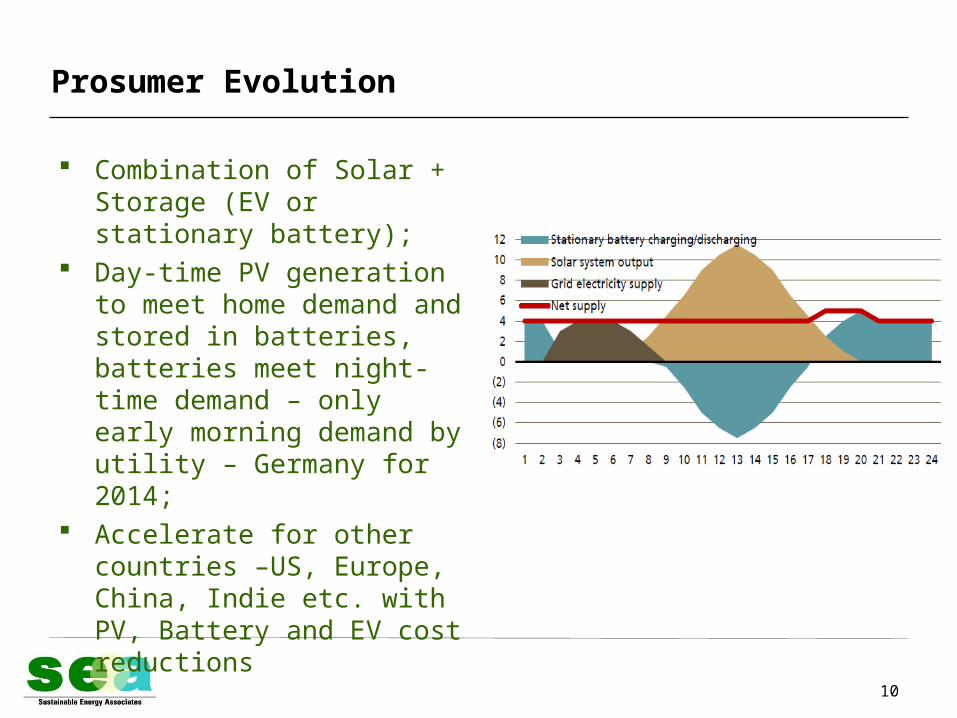

Combination of Solar + Storage (EV or stationary battery);

Day-time PV generation to meet home demand and stored in batteries, batteries meet night-time demand – only early morning demand by utility – Germany for 2014;

Accelerate for other countries –US, Europe, China, Indie etc. with PV, Battery and EV cost reductions

10

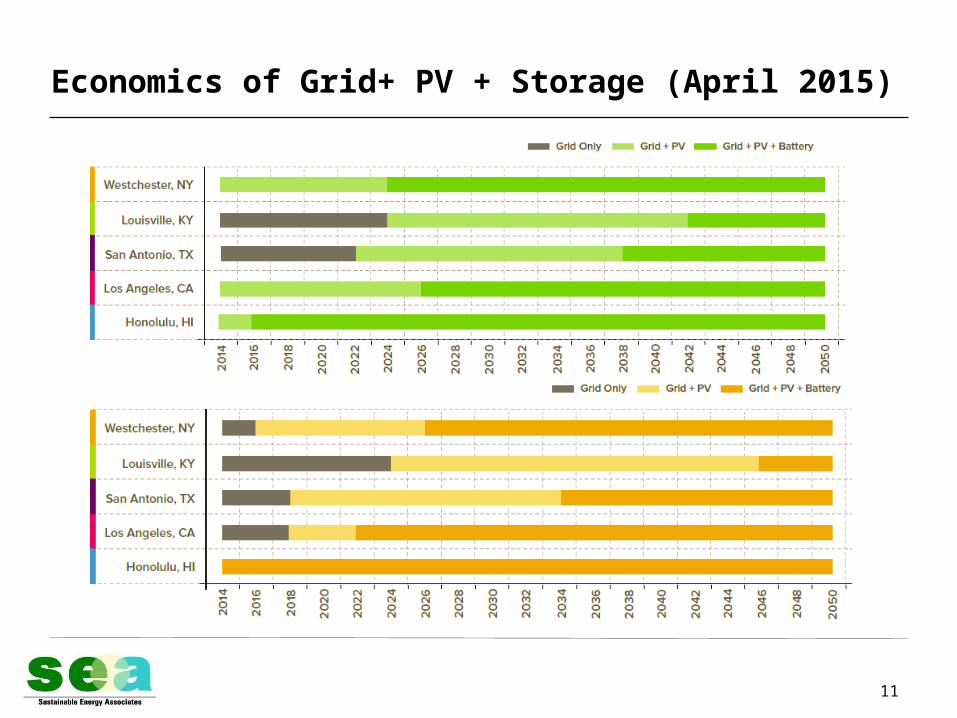

Economics of Grid+ PV + Storage (April 2015)

11

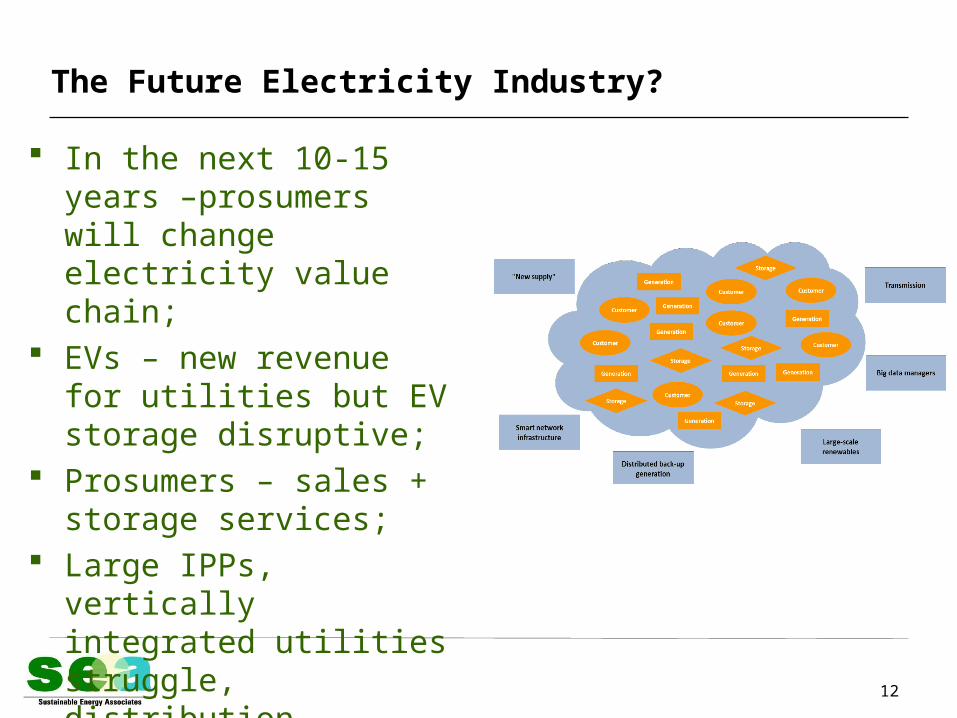

The Future Electricity Industry?

In the next 10-15 years –prosumers will change electricity value chain;

EVs – new revenue for utilities but EV storage disruptive;

Prosumers – sales + storage services;

Large IPPs, vertically integrated utilities struggle, distribution utilities benefit;

Some utilities, mange and own DPV + storage

12

Implications for India and Kerala

Existing ecosystem – back-up generators, battery, inverters – easier for prosumer uptake;

EV uptake – Govt. policies – shift to electrical demand – mixed due to storage;

Government & regulators play a role in the pace of diffusion;

Utility will continue to have a role in economically backward households.

The utility model will evolve. Lets prepare ourselves.

13