4 Audit Cycle

30

AUDIT CYCLE By Prof. Dr Safdar Ali Butt

-

Upload

zindgikikhatir -

Category

Documents

-

view

214 -

download

0

Transcript of 4 Audit Cycle

8/10/2019 4 Audit Cycle

http://slidepdf.com/reader/full/4-audit-cycle 1/30

AUDIT CYCLEBy

Prof. Dr Safdar Ali Butt

8/10/2019 4 Audit Cycle

http://slidepdf.com/reader/full/4-audit-cycle 2/30

2

Audit Cycle

Essentially an external audit takes thefollowing course:

Appointment of an external auditor

The Audit File

Assessment of Internal Controls

Audit Programs

Audit work and techniques

Audit Report

8/10/2019 4 Audit Cycle

http://slidepdf.com/reader/full/4-audit-cycle 3/30

3

Appointment

Mode of appointment

Eligibility for appointment

Initial inquiries Acceptance or Engagement Letter

8/10/2019 4 Audit Cycle

http://slidepdf.com/reader/full/4-audit-cycle 4/30

4

Mode of Appointment

Shareholders appoint the external auditorsat Annual General Meeting.

Auditor’s name is proposed and secondedby shareholders. If more than one name isproposed, an election takes place.

Before an audit firm’s name is proposed,their prior consent should be taken by theproposer.

8/10/2019 4 Audit Cycle

http://slidepdf.com/reader/full/4-audit-cycle 5/30

5

Who can be appointed

an external auditor?

Must have a practicing license. This meanshe should be a qualified charteredaccountant or equivalent.

In Pakistan, most external audits ofcompanies are performed by auditingfirms rather than individuals.

SBP and SECP have rated/classified auditfirms according to their strength andexperience, etc.

8/10/2019 4 Audit Cycle

http://slidepdf.com/reader/full/4-audit-cycle 6/30

6

Who cannot be appointed

an external auditor?

An employee or director of the company.

A person who is a spouse, partner or servant ofan employee of the company.

A debtor or a beneficiary of the company.

A company.

A person who has been for any legal reason

disqualified from being the auditor of thecompany, or any of its subsidiary or holdingcompany.

8/10/2019 4 Audit Cycle

http://slidepdf.com/reader/full/4-audit-cycle 7/307

Appointment by

Partners or sole traders

The sole trader can appoint the externalauditor himself.

In case of partnership, the majority ofpartners can appoint the external auditor.

8/10/2019 4 Audit Cycle

http://slidepdf.com/reader/full/4-audit-cycle 8/30

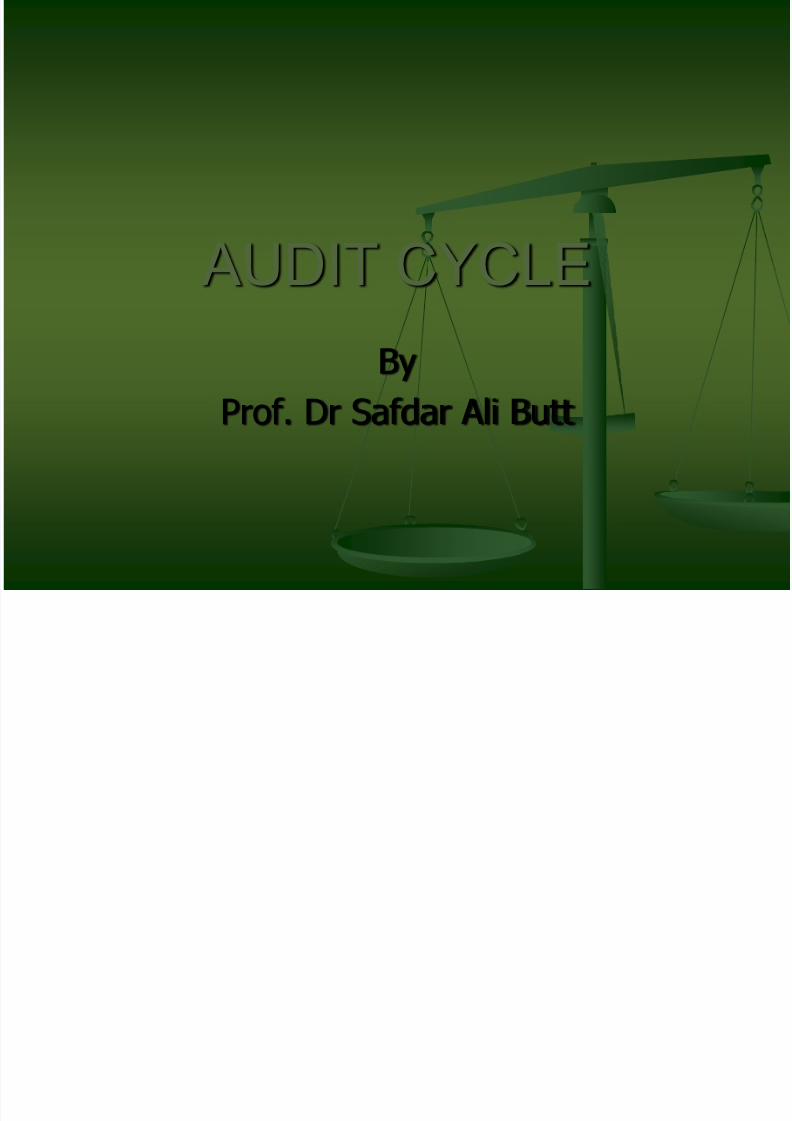

Rights of an auditor

Access to all books and records of thecompany, where ever they may be.

Raise queries or ask for any informationneeded by him and get it.

Attend and speak at AGMs.

8

8/10/2019 4 Audit Cycle

http://slidepdf.com/reader/full/4-audit-cycle 9/30

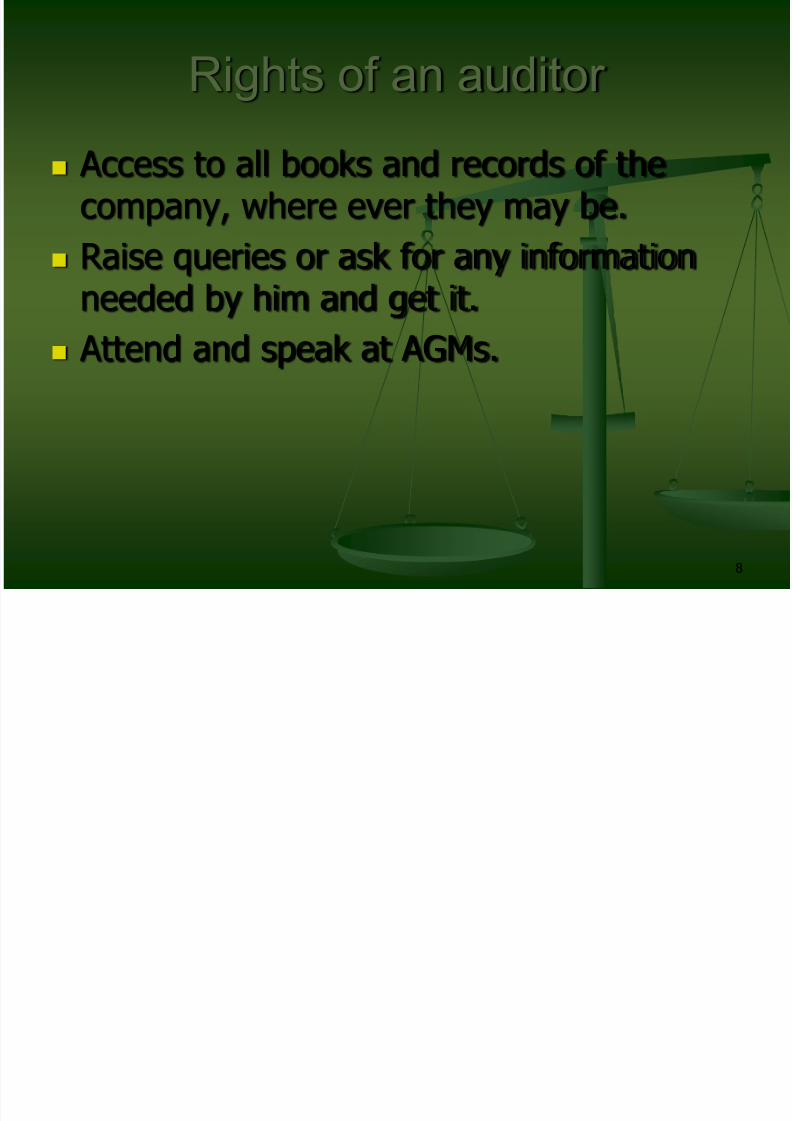

Removal of Auditor

Resignation or voluntary

Forced removal:

Only at General Meeting of shareholders. Permission of SECP

Auditor has a right to make a representationat shareholders meeting.

9

8/10/2019 4 Audit Cycle

http://slidepdf.com/reader/full/4-audit-cycle 10/30

10

Acceptance of Appointment

Upon passing of the resolution of hisappointment, the external auditor isnotified.

Some negotiation on terms and fees etcmust take place before the externalauditor gives his preliminary consent.

The external auditor takes certain stepsbefore he formally accepts theappointment.

8/10/2019 4 Audit Cycle

http://slidepdf.com/reader/full/4-audit-cycle 11/30

8/10/2019 4 Audit Cycle

http://slidepdf.com/reader/full/4-audit-cycle 12/30

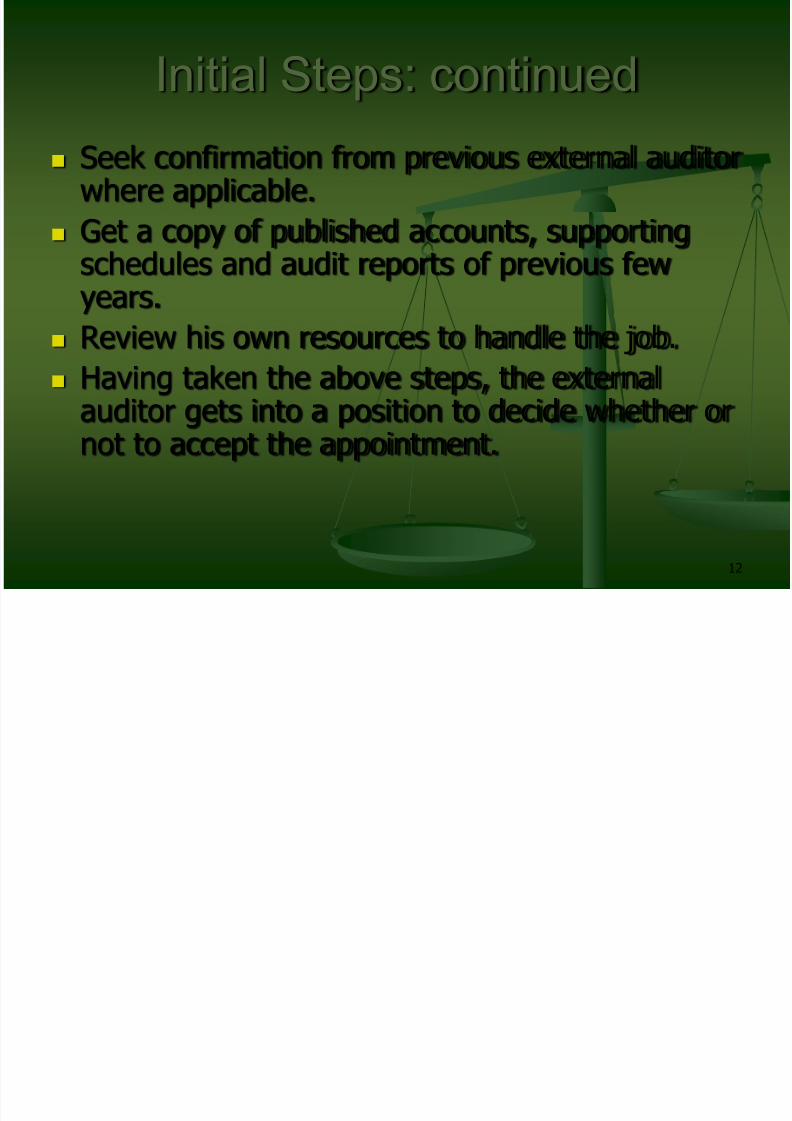

12

Initial Steps: continued

Seek confirmation from previous external auditorwhere applicable.

Get a copy of published accounts, supporting

schedules and audit reports of previous fewyears.

Review his own resources to handle the job.

Having taken the above steps, the external

auditor gets into a position to decide whether ornot to accept the appointment.

8/10/2019 4 Audit Cycle

http://slidepdf.com/reader/full/4-audit-cycle 13/30

13

Engagement Letter

No appointment letter is issued to anexternal auditor.

Instead, the external auditor issues anEngagement Letter outlining the scopeand terms of his assignment.

The company must accept theEngagement Letter and abide by itsprovisions.

8/10/2019 4 Audit Cycle

http://slidepdf.com/reader/full/4-audit-cycle 14/30

14

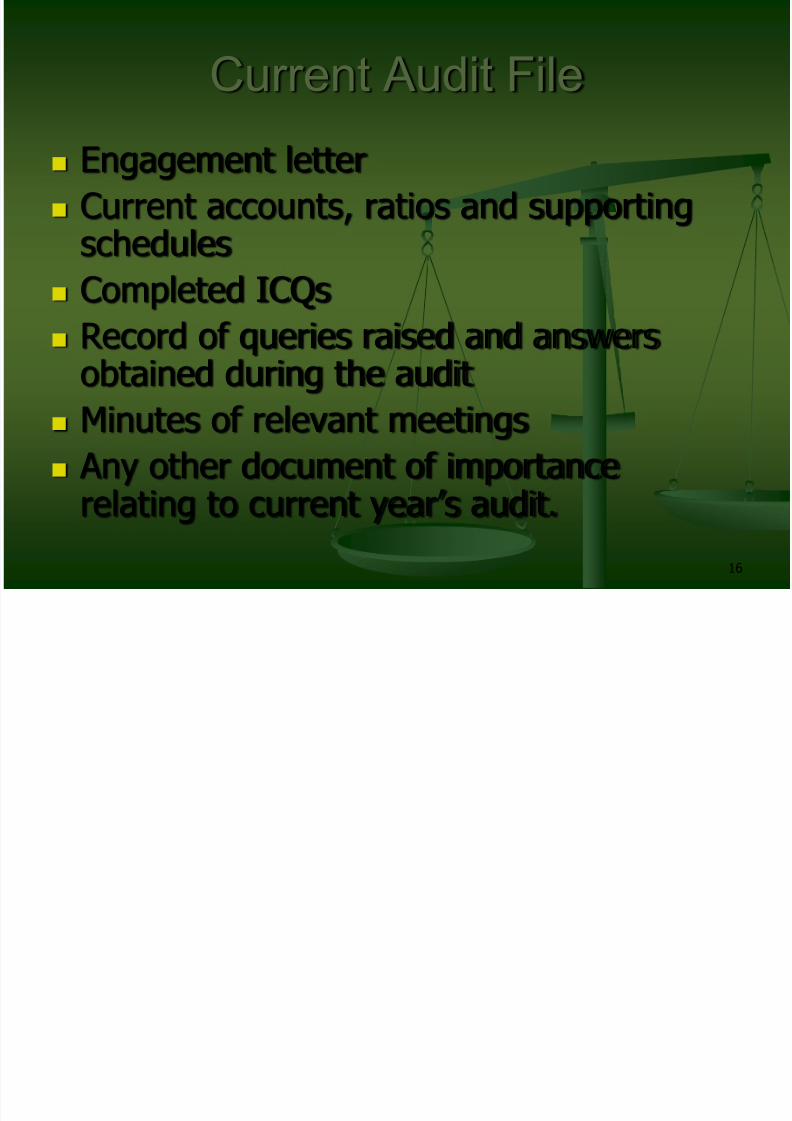

Audit Files

Permanent file

Current file

8/10/2019 4 Audit Cycle

http://slidepdf.com/reader/full/4-audit-cycle 15/30

8/10/2019 4 Audit Cycle

http://slidepdf.com/reader/full/4-audit-cycle 16/30

8/10/2019 4 Audit Cycle

http://slidepdf.com/reader/full/4-audit-cycle 17/30

8/10/2019 4 Audit Cycle

http://slidepdf.com/reader/full/4-audit-cycle 18/30

8/10/2019 4 Audit Cycle

http://slidepdf.com/reader/full/4-audit-cycle 19/30

19

Assessing Internal Control

Before the audit commences, the external auditorevaluates the internal control system of thecompany. In this regard:

The first step is to find out what internal controlsexist. This is done by preparing Internal ControlQuestionnaires.

The second step is to assess how effectively thesystem is actually enforced. This is done by testchecking the answers to ICQs.

8/10/2019 4 Audit Cycle

http://slidepdf.com/reader/full/4-audit-cycle 20/30

8/10/2019 4 Audit Cycle

http://slidepdf.com/reader/full/4-audit-cycle 21/30

21

Audit Program

An Audit Program is an actual plan of audit work. A large number of APs are prepared to cover thevarious activities of the company, as one APcovers only one aspect. It contains:

The list of tasks to be performed by auditworkers;

Instructions on how to perform them;

Depth and breadth to which audit work must bedone.

How to record the findings.

8/10/2019 4 Audit Cycle

http://slidepdf.com/reader/full/4-audit-cycle 22/30

22

Using Audit Programs

AP is prepared by senior audit managers afterreviewing the findings of ICQs.

The actual audit work is done by junior audit

staff. Completed APs are reviewed by audit seniors

and further test checks may be made by them toensure their validity.

Standard Audit Programs (SAPs) may be usedfor routine, common aspects of accountingrecords and tasks.

8/10/2019 4 Audit Cycle

http://slidepdf.com/reader/full/4-audit-cycle 23/30

23

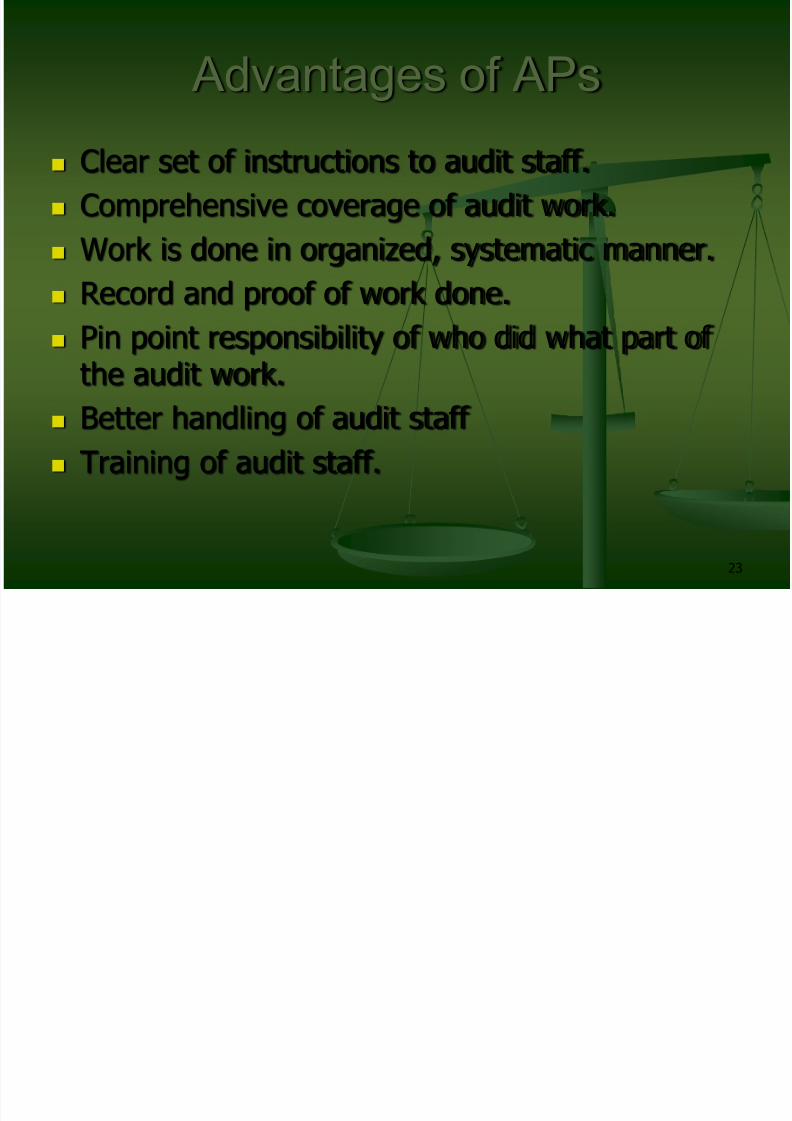

Advantages of APs

Clear set of instructions to audit staff.

Comprehensive coverage of audit work.

Work is done in organized, systematic manner.

Record and proof of work done.

Pin point responsibility of who did what part ofthe audit work.

Better handling of audit staff Training of audit staff.

8/10/2019 4 Audit Cycle

http://slidepdf.com/reader/full/4-audit-cycle 24/30

24

Disadvantages of APs

Make work mechanical.

Rigidity and inflexibility

May inhibit efficient audit staff. Inefficient staff simply aim at completing

the AP and hide behind it.

If clients’ staff gets to know aboutcontents of AP, they can rig records.

8/10/2019 4 Audit Cycle

http://slidepdf.com/reader/full/4-audit-cycle 25/30

25

Detailed Audit Work

Once APs have been prepared, actualchecking work commences. Audit staffstart doing work according to APs.

Audit senior keep reviewing the work of juniors through checks and notes books.

Completed APs are studied by seniors.

If deemed necessary further checks maybe carried out.

8/10/2019 4 Audit Cycle

http://slidepdf.com/reader/full/4-audit-cycle 26/30

26

Completion of Audit Work

Once detailed audit work has been done,the audit seniors form an opinion on thework done. This is communicated to the

client in two ways:

Audit Report

Management Letter

8/10/2019 4 Audit Cycle

http://slidepdf.com/reader/full/4-audit-cycle 27/30

8/10/2019 4 Audit Cycle

http://slidepdf.com/reader/full/4-audit-cycle 28/30

28

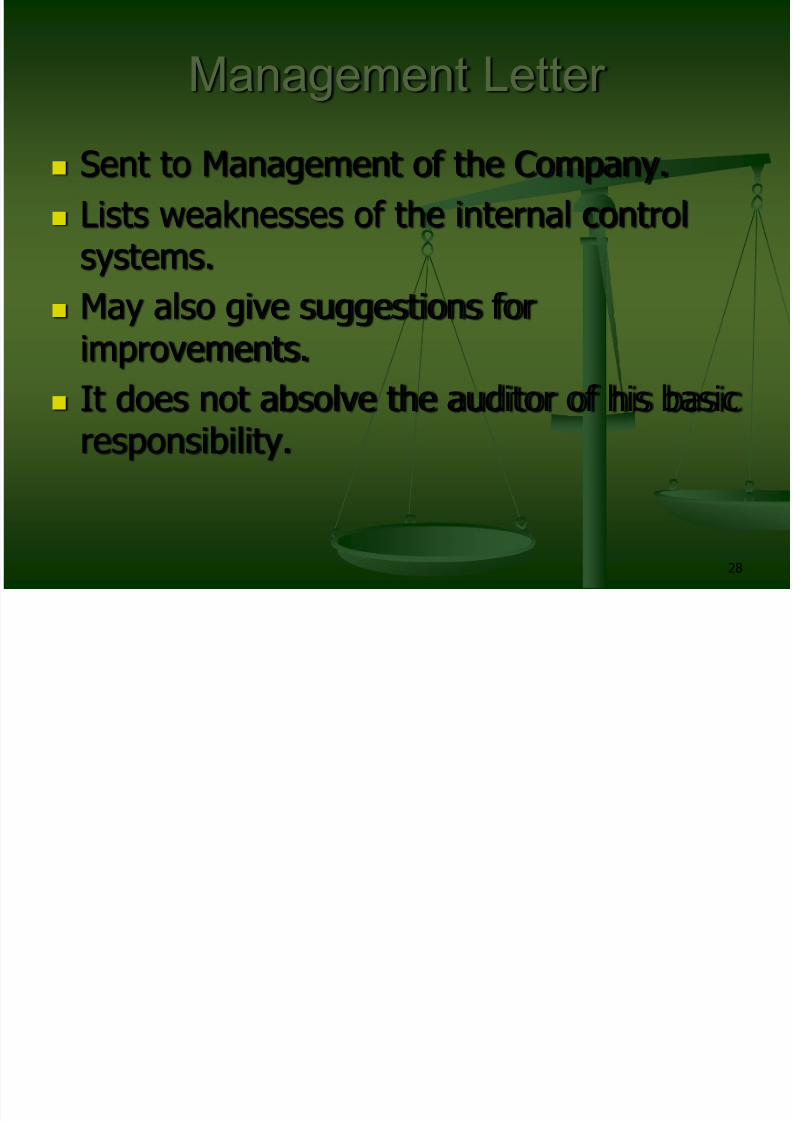

Management Letter

Sent to Management of the Company.

Lists weaknesses of the internal controlsystems.

May also give suggestions forimprovements.

It does not absolve the auditor of his basicresponsibility.

8/10/2019 4 Audit Cycle

http://slidepdf.com/reader/full/4-audit-cycle 29/30

8/10/2019 4 Audit Cycle

http://slidepdf.com/reader/full/4-audit-cycle 30/30

Thank you

30