3Q 2016 Financial Results - listed...

28

19 October 2016 3Q 2016 Financial Results

Transcript of 3Q 2016 Financial Results - listed...

19 October 2016

3Q 2016 Financial Results

3Q16 Highlights

2

High demand for data and unmatched customer experience drive financial momentum

Network improvements

drives lower complaints

3Q15 4Q15 1Q16 2Q16 3Q16

60% customer interactions on

digital and self-care platforms

89% 89% 89% 87% 90%

3Q15 4Q15 1Q16 2Q16 3Q16

3Q15 4Q15 1Q16 2Q16 3Q16

2x traffic growth;

Hotspots under control

2x traffic

growth

>16%

reduction

Consistent 4G LTE data

download speed

Solid Q-o-Q momentum

• +2.8% service revenue

• +6.6% prepaid revenue

• +13.2% EBITDA

• +22.1% PAT

3

90% first contact resolutions across

all customer service touch points

Hotspots

YTD 2016

47% 50% 53% 59% 60%

3Q15 4Q15 1Q16 2Q16 3Q16

Financial review

4

11,956 11,579 11,164 11,015 10,903

3Q15 4Q15 1Q16 2Q16 3Q16

• Service revenue improvement from strong prepaid performance; postpaid stable

• New plans launched in previous quarters driving revenue traction; more to come

• More data propositions supporting ARPU; mitigating voice and SMS usage decline

Good revenue momentum

53 54 55 54 56

Blended ARPU (RM/mth)

Total RGS and Blended ARPU Service Revenue (RM mn)

5

Subscriptions (‘000)

2,154 2,055 2,113

6,365 6,290

3Q15 2Q16 3Q16 9M15 9M16

-1.2%

-1.9%

+2.8%

Surpassed one million Hotlink FAST users

Successful in acquiring higher value

prepaid internet users; MI ARPU 20%

higher

High MI penetration; 10% points higher

than legacy base

Continued to be the best plan for MI users;

also catalyst for migration of 3G users to

4G

6

8,850 8,520 8,196 8,108 8,007

3Q15 4Q15 1Q16 2Q16 3Q16

1,074 959 1,022

3,135 2,994

3Q15 2Q16 3Q16 9M15 9M16

Prepaid Revenue (RM mn)

Strong MI ARPU drives good revenue momentum

+6.6%

-4.8%

39 39 39 38 41

Prepaid RGS and ARPU

RGS30 Subscriptions (‘000) Prepaid ARPU (RM/mth)

• RGS traction improving towards end quarter

• Hotlink FAST attracting high MI ARPU users; MI penetration approaching 55%

• Stable contribution from foreign worker segment; focus on growing MI users for better wallet

share and profitability

7

-4.5%

MaxisONE Plan premium backed by market leading innovations and superior 4G user experience

Postpaid RGS growth driven by strong

MaxisONE Plan acquisition momentum

and lower churn

MaxisONE Share driving incremental port-ins

and pre-to-post migration; also generating

higher acquisition ARPA*

8

New MaxisONE Kid and 4G Pocket

WiFi to grow ARPA and MI usage

*ARPA – average revenue per account

Leading 4G LTE coverage and quality

support the momentum

2,784 2,765 2,696 2,660 2,678

3Q15 4Q15 1Q16 2Q16 3Q16

972 975 960

2,914 2,927

3Q15 2Q16 3Q16 9M15 9M16

Postpaid Revenue (RM mn)

MaxisONE Plan subscriptions approaching 1.5 million

-1.2%

-1.5%

98 102 102 102 100

Postpaid RGS and ARPU

• Added 18k new subscriptions this quarter; strong pick-up in subscribers with new device contracts

• MaxisONE Plan subscriptions approaching 1.5 million, ARPU at RM129/month

• Bundled revenue now at 67% of total postpaid revenue

9

+0.4%

RGS30 Subscriptions (‘000) Postpaid ARPU (RM/mth)

636 813 962 1,292 1,492

MaxisONE Plan Subscriptions (‘000)

316 333 249

669 741

3Q15 2Q16 3Q16 9M15 9M16

Capex (RM mn)

Differentiated LTE experience; leadership in network quality

• Leading 4G LTE pop coverage nationwide; at 88% on comparable peer basis

• 2x traffic growth; maintained consistent network quality

10

4G devices

4G average data usage

3Q15

2.4 million 4.2 million

2.3GB/mth 4.4GB/mth

* 4G population coverage based on stringent -98dBm quality criteria; comparable peer basis pop coverage at 88%

Network modernisation 83%

3Q16

93%

Pop coverage: 2G

3G

4G*

95%

91%

55%

96%

94%

81%

71% 72% 71% 70% 72%

3Q15 4Q15 1Q16 2Q16 3Q16

1.26 1.44 1.55

2.00

2.60

1.72 1.88 1.93

2.95

3.67

65% 67% 67% 68% 72%

75% 76% 77% 80% 81%

3Q15 4Q15 1Q16 2Q16 3Q16 3Q15 4Q15 1Q16 2Q16 3Q16

2G 3G 4G

>3x LTE traffic growth; average data usage at 4.4 GB/month

45 50 52 64 83

Growing data usage Higher smart-phone penetration Increasing 4G LTE traffic

Prepaid (GB/mth) Mobile Internet

Penetration

Postpaid (GB/mth) Postpaid Prepaid Data Traffic (‘000 TB)

11

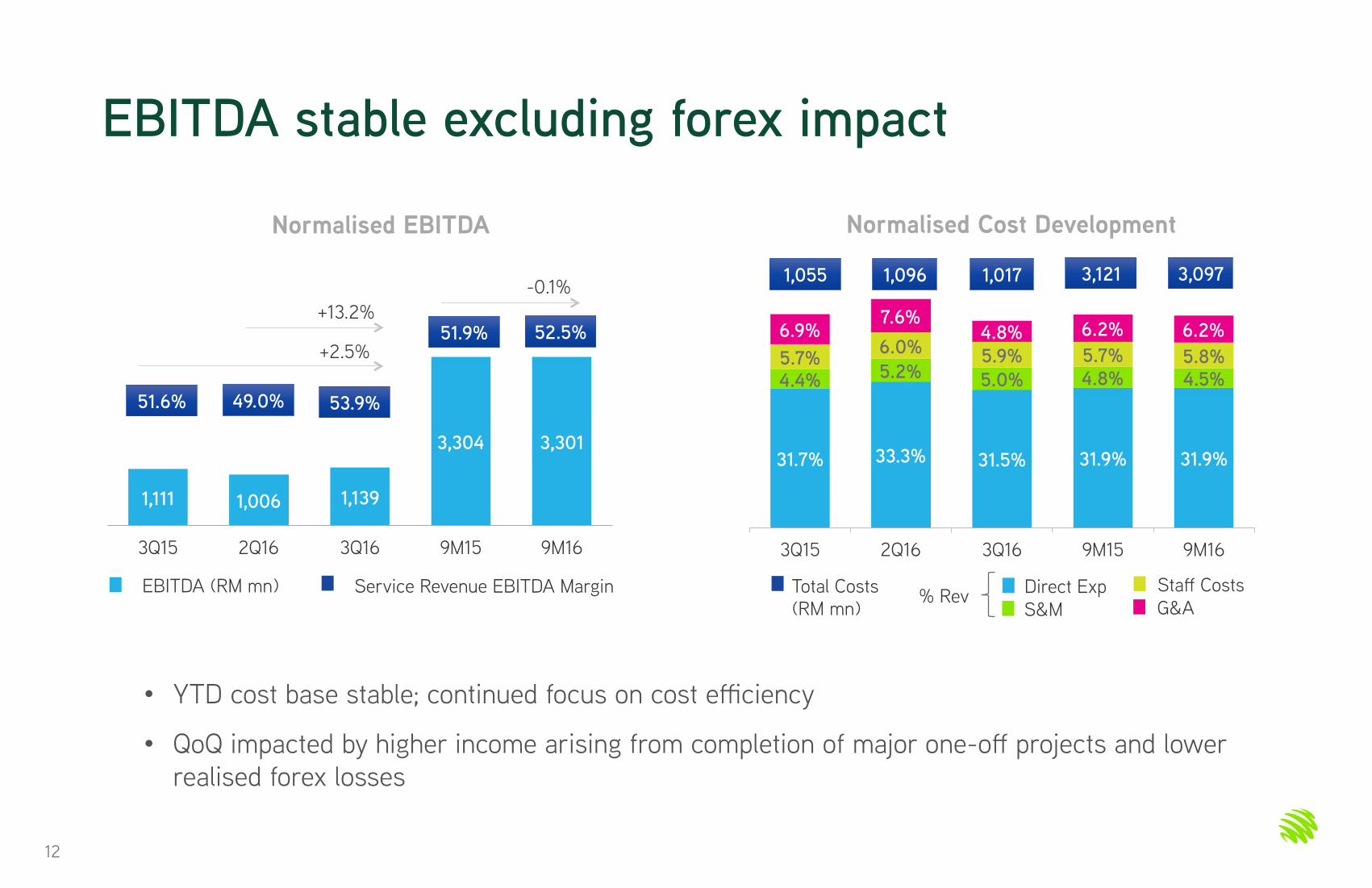

1,111 1,006 1,139

3,304 3,301

3Q15 2Q16 3Q16 9M15 9M16

EBITDA stable excluding forex impact

-0.1%

+2.5%

51.6% 49.0% 53.9%

EBITDA (RM mn) Service Revenue EBITDA Margin

Normalised Cost Development Normalised EBITDA

• YTD cost base stable; continued focus on cost efficiency

• QoQ impacted by higher income arising from completion of major one-off projects and lower

realised forex losses

31.7% 33.3% 31.5% 31.9% 31.9%

4.4% 5.2% 5.0% 4.8% 4.5% 5.7%

6.0% 5.9% 5.7% 5.8%

6.9% 7.6%

4.8% 6.2% 6.2%

3Q15 2Q16 3Q16 9M15 9M16

1,055 1,096 1,017

12

51.9% 52.5% +13.2%

3,121 3,097

Total Costs

(RM mn) S&M G&A Direct Exp Staff Costs

% Rev

27 8 4

140

21

3Q15 2Q16 3Q16 9M15 9M16

510 421 514

1,483 1,419

3Q15 2Q16 3Q16 9M15 9M16

Profit after Tax

-4.3%

+0.8%

Accelerated Depreciation (RM mn) Normalised Profit after Tax (RM mn)

• YTD PAT excludes RM71 million Home-related contract obligations reversal and asset impairment,

RM34 million unrealised forex gains (YTD15: RM101 million unrealised forex losses) and RM16

million accelerated depreciation net of tax (YTD15: RM105 million)

• YTD lower accelerated depreciation reflecting near completion of network modernisation

13

+22.1%

Summary: Positive trajectory; guidance reiterated

Service revenue, absolute EBITDA and

base capex at similar levels to FY2015

Business overview Guidance

14

Operational drivers stabilised; solid 3Q

Strengthen product innovation &

differentiation, more to come

Continuous investment in best 4G LTE

connectivity and digital experience

Key numbers

EBITDA, EBITDA margin and Profit After Tax on normalised basis

Effective 2Q16, network income has been re-classified as non-service revenue

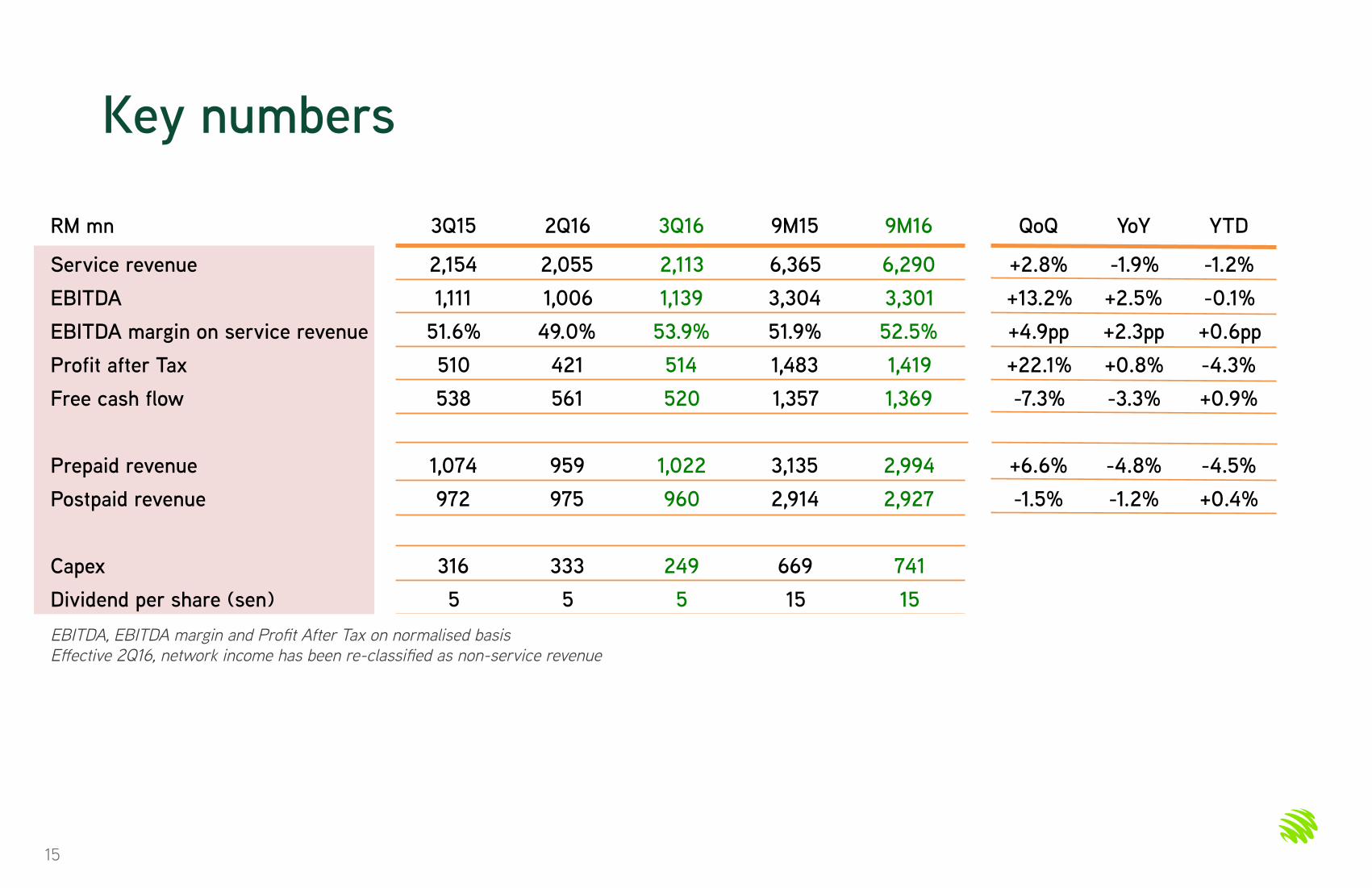

RM mn 3Q15 2Q16 3Q16 9M15 9M16 QoQ YoY YTD

Service revenue 2,154 2,055 2,113 6,365 6,290 +2.8% -1.9% -1.2% EBITDA 1,111 1,006 1,139 3,304 3,301 +13.2% +2.5% -0.1% EBITDA margin on service revenue 51.6% 49.0% 53.9% 51.9% 52.5% +4.9pp +2.3pp +0.6pp Profit after Tax 510 421 514 1,483 1,419 +22.1% +0.8% -4.3% Free cash flow 538 561 520 1,357 1,369 -7.3% -3.3% +0.9%

Prepaid revenue 1,074 959 1,022 3,135 2,994 +6.6% -4.8% -4.5% Postpaid revenue 972 975 960 2,914 2,927 -1.5% -1.2% +0.4%

Capex 316 333 249 669 741 Dividend per share (sen) 5 5 5 15 15

15

Q & A

16

Disclaimer This presentation by Maxis Berhad (“Maxis”) contains forward-looking statements. Forward-looking statements can be identified

by the use of forward-looking terminology such as the words “may”, “will”, “would”, “could”, “believe”, “expect”, “anticipate”,

“intend”, “estimate”, “aim”, “plan”, “forecast” or similar expressions and include all statements that are not historical facts.

Forward-looking statements made in this presentation involve known and unknown risks, uncertainties and other factors which

may cause actual future performance, outcomes and results to differ materially from those expressed or implied in such forward-

looking statements. Such forward-looking statements are based on numerous assumptions and reflect Maxis’ current views with

respect to future events and are not a guarantee of future performance. Maxis cannot give any assurance that such forward-

looking statements will be realized.

Factors which could affect actual future performance, outcomes and results include (without limitation) general industry and

economic conditions, interest rate trends, cost of capital and capital availability, availability of real estate properties, competition

from other companies and avenues for the sale/distribution of goods and services, shifts in customer demands, customers and

partners, changes in operating expenses, including employee wages, benefits and training, governmental and public policy

changes and the continued availability of financing in the amounts and the terms necessary to support future business.

Forward-looking statements made in this presentation are made only as at the date of this presentation and Maxis and its

subsidiaries, affiliates, representatives and advisers expressly disclaim any obligation or undertaking to release, publicly or

otherwise, any updates or revisions to any such forward-looking statements to reflect any change in Maxis’ expectations, new

information, future events, change in conditions or circumstances or otherwise.

This presentation has been prepared by Maxis. The information in this presentation, including forward-looking statements, has

not been independently verified. Without limiting any of the foregoing in this disclaimer, no representation or warranty, express

or implied, is made as to, and no reliance should be placed on, the fairness, accuracy or completeness of such information. Maxis

and its subsidiaries, affiliates, representatives and advisers shall have no liability whatsoever (whether in negligence or

otherwise) for any loss, damage, costs or expenses howsoever arising out of or in connection with this presentation.

17

Thank you

18

19

Appendices

Important definitions/notations (1)

• Service Revenue: Group revenue excluding device, hubbing revenues and network income

• EBITDA margin on Service Revenue: EBITDA as percentage of service revenue

• Normalised PAT: Adjusting for net of tax effects: (i) accelerated depreciation of RM20 million in 3Q15; RM6 million in 2Q16 and

RM3 million in 3Q16; (ii) reversal of asset impairment & contract obligation provision of RM71 million in 2Q16; (iii) unrealised forex

losses of RM68 million in 3Q15; RM3 million in 2Q16 and RM6 million in 3Q16

• Free Cash Flow: Cash Flow from Operations – Cash Flow from Investing Activities – Interest paid – Finance lease repayment

• Revenue generating subscriber/subscription (RGS30): Defined as active line subscriptions and exclude those that does not

have any revenue generating activities for more than 30 days

• WBB subscription: Subscriptions on data plans using USB modems and tablets

• FBI: Free basic Internet

• Smart-phone: Any devices with growing apps stores and active developers

20

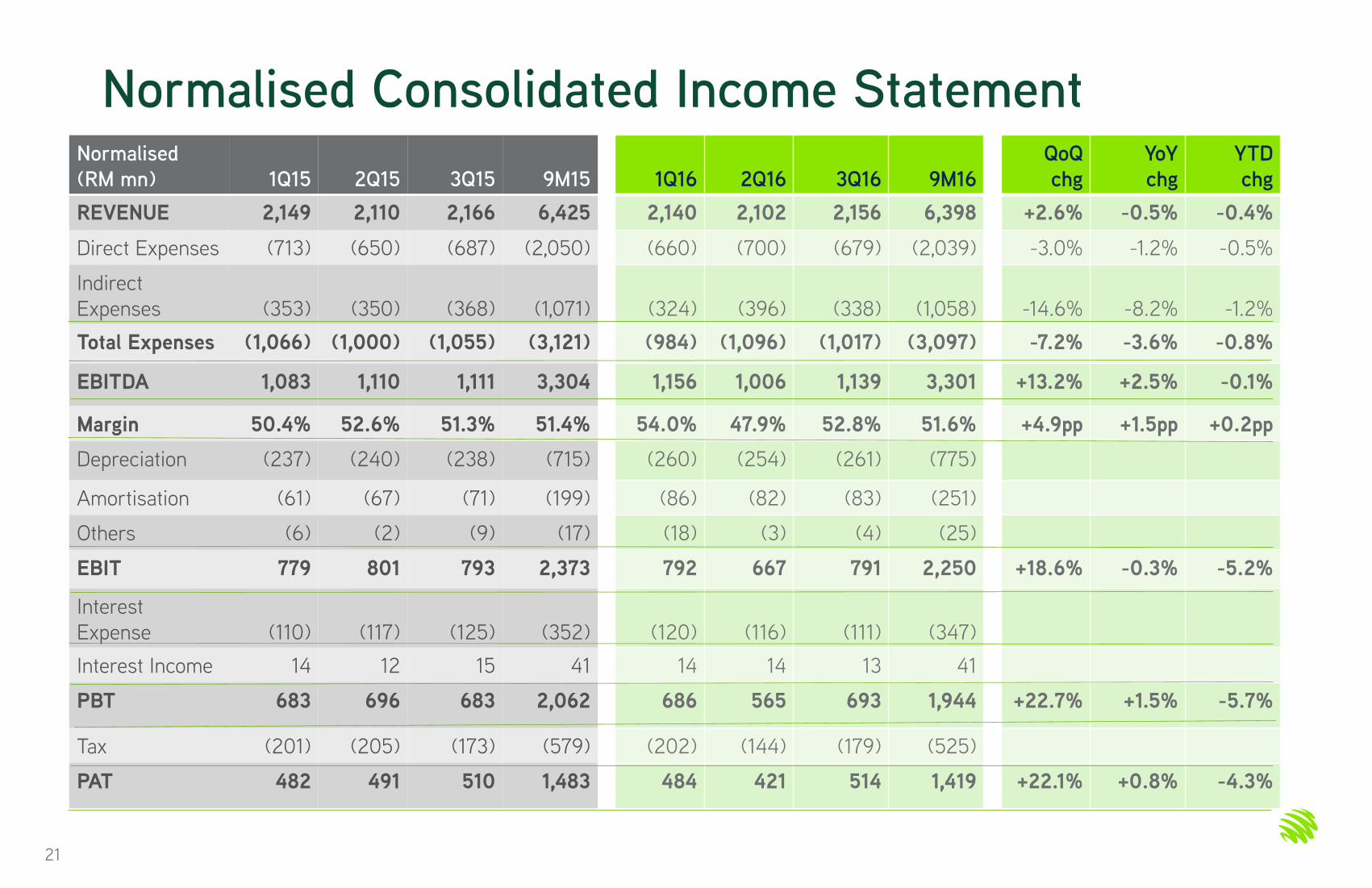

Normalised Consolidated Income Statement Normalised

(RM mn)

1Q15

2Q15

3Q15

9M15

REVENUE 2,149 2,110 2,166 6,425

Direct Expenses (713) (650) (687) (2,050)

Indirect

Expenses

(353)

(350)

(368)

(1,071)

Total Expenses (1,066) (1,000) (1,055) (3,121)

EBITDA 1,083 1,110 1,111 3,304

Margin 50.4% 52.6% 51.3% 51.4%

Depreciation (237) (240) (238) (715)

Amortisation (61) (67) (71) (199)

Others (6) (2) (9) (17)

EBIT 779 801 793 2,373

Interest

Expense

(110)

(117)

(125)

(352)

Interest Income 14 12 15 41

PBT 683 696 683 2,062

Tax (201) (205) (173) (579)

PAT 482 491 510 1,483

21

1Q16

2Q16

3Q16

9M16

2,140 2,102 2,156 6,398

(660) (700) (679) (2,039)

(324)

(396)

(338)

(1,058)

(984) (1,096) (1,017) (3,097)

1,156 1,006 1,139 3,301

54.0% 47.9% 52.8% 51.6%

(260) (254) (261) (775)

(86) (82) (83) (251)

(18) (3) (4) (25)

792 667 791 2,250

(120)

(116)

(111)

(347)

14 14 13 41

686 565 693 1,944

(202) (144) (179) (525)

484 421 514 1,419

QoQ

chg

YoY

chg

YTD

chg

+2.6% -0.5% -0.4%

-3.0% -1.2% -0.5%

-14.6%

-8.2%

-1.2%

-7.2% -3.6% -0.8%

+13.2% +2.5% -0.1%

+4.9pp +1.5pp +0.2pp

+18.6% -0.3% -5.2%

+22.7% +1.5% -5.7%

+22.1% +0.8% -4.3%

Reported Consolidated Income Statement Reported

(RM mn)

1Q15

2Q15

3Q15

9M15

REVENUE 2,149 2,110 2,166 6,425

Direct Expenses (713) (650) (689) (2,052)

Indirect

Expenses

(389)

(359)

(456)

(1,204)

Total Expenses (1,102) (1,009) (1,145) (3,256)

EBITDA 1,047 1,101 1,021 3,169

Margin 48.7% 52.2% 47.1% 49.3%

Depreciation (294) (296) (265) (855)

Amortisation (61) (67) (71) (199)

Others (6) (2) (9) (17)

EBIT 686 736 676 2,098

Interest Expense (110) (117) (125) (352)

Interest Income 14 12 15 41

PBT 590 631 566 1,787

Tax (178) (188) (144) (510)

PAT 412 443 422 1,277

22

1Q16

2Q16

3Q16

9M16

2,140 2,102 2,156 6,398

(656) (700) (682) (2,038)

(271)

(352)

(344)

(967)

(927) (1,052) (1,026) (3,005)

1,213 1,050 1,130 3,393

56.7% 50.0% 52.4% 53.0%

(269) (262) (265) (796)

(86) (82) (83) (251)

(18) 44 (4) 22

840 750 778 2,368

(120) (116) (111) (347)

14 14 13 41

734 648 680 2,062

(214) (165) (175) (554)

520 483 505 1,508

QoQ

chg

YoY

chg

YTD

chg

+2.6% -0.5% -0.4%

-2.6% -1.0% -0.7%

-2.3%

-24.6%

-19.7%

-2.5% -10.4% -7.7%

+7.6% +10.7% +7.1%

+2.4pp +5.3pp +3.7pp

+3.7% +15.1% +12.9%

+4.9% +20.1% +15.4%

+4.6% +19.7% +18.1%

Cash Flow Statement (RM mn) 3Q15 4Q15 1Q16 2Q16 3Q16

Cash flow from operating activities 1,109 1,267 705 1,129 994

Cash flow used in investing activities (429) (796) (259) (486) (345)

Purchase of property, plant &

equipment

(357)

(692)

(183)

(417)

(271)

Proceeds from disposal of PPE - 1 2 - 1

Purchase of intangible assets (72) (105) (78) (69) (75)

Cash flow before financing activities 680 471 446 643 649

Cash flow used in financing activities (934) (478) (956) (456) (926)

Dividends paid (375) (376) (376) (375) (376)

Debt drawdown - - - 3,500 840

Debt repayment (421) - (421) (3,500) (1,261)

Payment of finance costs (139) (101) (156) (80) (128)

Others 1 (1) (3) (1) (1)

Net change in cash (254) (7) (510) 187 (277)

Opening Cash Balance 1,557 1,303 1,296 786 973

Closing Cash Balance 1,303 1,296 786 973 696

RM mn 2Q16 3Q16

Debt# 8,751 8,300

Cash 973 696

Net Debt 7,778 7,604

Total Equity 4,438 4,584

Ratios 2Q16 3Q16

Net debt to

EBITDA*

1.72x 1.68x

Net debt to Equity 1.75x 1.66x

# Includes derivative financial instruments designated for hedging relationship on borrowings; excludes vendor financing

* EBITDA calculated as annualised YTD EBITDA

23

Revenue Composition (RM mn) 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16

Total Revenue

- Service

- Mobile

- EntFixed

- Int. Services

- Non-Service

- Device

- Hubbing

- Network income

2,065

2,041

1,946

64

31

24

2

14

8

2,123

2,090

1,988

68

34

33

7

22

4

2,149

2,122

2,019

65

38

27

9

13

5

2,110

2,089

1,984

64

41

21

6

10

5

2,166

2,154

2,046

63

45

12

4

4

4

2,176

2,155

2,047

61

47

21

12

4

5

2,140

2,122

2,005

67

50

18

12

2

4

2,102

2,055

1,934

67

54

47

12

-

35

2,156

2,113

1,982

74

57

43

23

-

20

Normalised EBITDA

Margin on Service

Revenue

52.9%

49.5%

51.0%

53.1%

51.6%

52.0%

54.5%

49.0%

53.9%

Note:

Commencing 1Q15, further breakdowns of mobile revenue are not disclosed as we are not applying fair value to new bundled plans including the MaxisONE Plan

Commencing 2Q16, retrospectively, network income has been re-classified as non-service revenue. Adjusted service, mobile, prepaid and postpaid revenues are tabled above

24

(‘000) 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16

Mobile Revenue

- Prepaid

- Postpaid

1,946

988

958

1,988

1,005

983

2,019

1,049

970

1,984

1,012

972

2,046

1,074

972

2,047

1,038

1,009

2,005

1,013

992

1,934

959

975

1,982

1,022

960

Normalised Financials and Costs (RM mn) 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16

Total Revenue 2,065 2,123 2,149 2,110 2,166 2,176 2,140 2,102 2,156

Total Expenses

- Direct

- Indirect

986

652

334

1,089

696

393

1,066

713

353

1,000

650

350

1,055

687

368

1,055

678

377

984

660

324

1,096

700

396

1,017

679

338

EBITDA 1,079 1,034 1,083 1,110 1,111 1,121 1,156 1,006 1,139

PBT 709 649 683 696 683 682 686 565 693

PAT 500 445 482 491 510 477 484 421 514

EBITDA Margin 52.3% 48.7% 50.4% 52.6% 51.3% 51.5% 54.0% 47.9% 52.8%

PAT Margin 24.2% 21.0% 22.4% 23.3% 23.5% 21.9% 22.6% 20.0% 23.8%

(RM mn) 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16

Total Expenses 986 1,089 1,066 1,000 1,055 1,055 984 1,096 1,017

Direct Expenses 652 696 713 650 687 678 660 700 679

Indirect Expenses

- S&M

- Staff Costs

- Bad Debts

- G&A

334

107

66

15

146

393

122

116

18

137

353

103

124

4

122

350

110

115

10

115

368

94

124

9

141

377

98

117

6

156

324

76

116

19

113

396

109

126

25

136

338

108

126

22

82

25

Reported Financials and Costs (RM mn) 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16

Total Revenue 2,065 2,123 2,149 2,110 2,166 2,176 2,140 2,102 2,156

Total Expenses

- Direct

- Indirect

995

652

343

1,123

696

427

1,102

713

389

1,009

650

359

1,145

689

456

1,014

676

338

927

656

271

1,052

700

352

1,026

682

344

EBITDA 1,070 1,000 1,047 1,101 1,021 1,162 1,213 1,050 1,130

PBT 643 502 590 631 566 673 734 648 680

PAT 451 335 412 443 422 470 520 483 505

EBITDA Margin 51.8% 47.1% 48.7% 52.2% 47.1% 53.4% 56.7% 50.0% 52.4%

PAT Margin 21.8% 15.8% 19.2% 21.0% 19.5% 21.6% 24.3% 23.0% 23.4%

26

(RM mn) 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16

Total Expenses 995 1,123 1,102 1,009 1,145 1,014 927 1,052 1,026

Direct Expenses 652 696 713 650 689 676 656 700 682

Indirect Expenses

- S&M

- Staff Costs

- Bad Debts

- G&A

343

107

66

15

155

427

122

116

18

171

389

103

124

4

158

359

110

115

10

124

456

94

124

9

229

338

98

117

6

117

271

76

116

19

60

352

109

126

25

92

344

108

126

22

88

RGS30, ARPU and Smart-phone penetration (‘000) 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16

Mobile Subs

- Prepaid

- Postpaid

- WBB

11,338

8,120

2,786

432

11,864

8,656

2,809

398

12,192

8,992

2,823

377

12,214

9,068

2,796

350

11,956

8,850

2,784

322

11,579

8,520

2,765

294

11,164

8,196

2,696

272

11,015

8,108

2,660

247

10,903

8,007

2,678

218

ARPU

(RM/mth)

3Q14

4Q14

1Q15

2Q15

3Q15

4Q15

1Q16

2Q16

3Q16

Blended

- Prepaid

- Postpaid

55

40

95

54

39

98

53

38

96

51

36

97

53

39

98

54

39

102

55

39

102

54

38

102

56

41

100

Notes:

WBB subscriptions defined as subscriptions on data plans using USB modems and tablets Commencing 1Q15, postpaid MOU is no longer disclosed as we are not applying fair value to new bundled plans including the MaxisONE Plan

Smart-phone defined as any devices with growing apps store and active developers

27

Smartphone

Penetration (%)

3Q14

4Q14

1Q15

2Q15

3Q15

4Q15

1Q16

2Q16

3Q16

Blended

- Prepaid

- Postpaid

54

50

67

57

54

67

62

60

72

65

63

73

67

65

75

69

67

76

70

67

77

70

68

80

74

72

81

Market Definition Subscriptions, ARPU and MOU (‘000) 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16

Mobile Subs

- Prepaid

- Postpaid

12,415

9,081

3,334

12,913

9,624

3,289

13,260

9,979

3,280

13,269

10,051

3,218

13,110

9,927

3,174

12,694

9,567

3,127

12,310

9,279

3,031

12,249

9,273

2,976

12,046

9,085

2,961

WBB 495 440 412 385 357 325 302 276 243

Mobile Internet

Users

7,600

8,800

9,000

9,100

9,000

8,800

8,500

8,400

8,500

Home

Connections

72

80

89

99

107

118

126

133

139

Notes

WBB subscriptions defined as subscriptions on data plans using USB modems and tablets – included in postpaid subscriptions Commencing 1Q15, postpaid MOU is no longer disclosed as we are not applying fair value to new bundled plans including the MaxisONE Plan

28

(‘000) 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16

Prepaid

- ARPU

- MOU (min/mth)

35

131

35

133

35

126

33

131

35

134

35

129

35

141

34

162

36

155

Postpaid 94 97 95 96 97 102 101 101 100

Blended 50 50 48 47 49 50 50 49 50