361 Degree International Limited Annual Results Presentation 2011 March, 2012.

23

361 Degree International Limited Annual Results Presentation 2011 March, 2012

-

Upload

allen-copeland -

Category

Documents

-

view

222 -

download

3

Transcript of 361 Degree International Limited Annual Results Presentation 2011 March, 2012.

361 Degree International Limited

Annual Results Presentation 2011

March, 2012

The information contained in this presentation is intended solely for your personal reference. Such information is subject to change without notice, its accuracy is not guaranteed arid it may not contain all material information concerning 361 Degrees International Limited (the "Company"). The Company makes no representation regarding, and assumes no responsibility or liability for, the accuracy or completeness of, or any errors or omissions in, any information contained herein.

In addition, the information contains projections and forward-looking statements that reflect the Company's current views with respect to future events and financial performance. These views are based on current assumptions which are subject to various risks and which may change over time. No assurance can be given that future events will occur, that projections will be achieved, or that the Company's assumptions are correct. It is not the intention to provide, and you may not rely on this presentation as providing, a complete or comprehensive analysis of the Company's financial or trading position or prospects.

This presentation does not constitute an offer or invitation to purchase or subscribe for any securities or financial instruments or to provide any investment service or investment advice, and no part of it shall form the basis of or be relied upon in connection with any contract, commitment or investment decision in relation thereto.

Disclaimer

Table of Contents

361 Degrees International LimitedAnnual Results Presentation 2011

1. Operational Highlights 1

2. Financial Review 9

3. Outlook and Strategies 16

4. Q&A 17

1. Operational Highlights

1

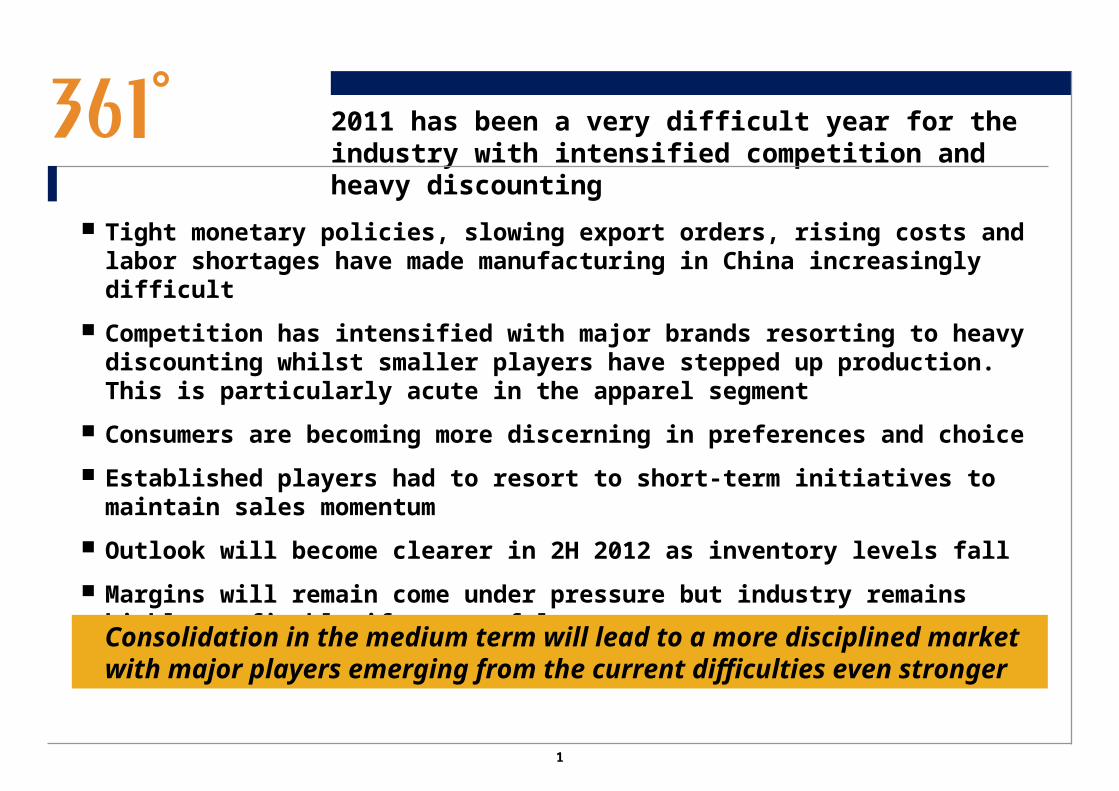

2011 has been a very difficult year for the industry with intensified competition and heavy discounting

Tight monetary policies, slowing export orders, rising costs and labor shortages have made manufacturing in China increasingly difficult

Competition has intensified with major brands resorting to heavy discounting whilst smaller players have stepped up production. This is particularly acute in the apparel segment

Consumers are becoming more discerning in preferences and choice

Established players had to resort to short-term initiatives to maintain sales momentum

Outlook will become clearer in 2H 2012 as inventory levels fall

Margins will remain come under pressure but industry remains highly profitable if successfulConsolidation in the medium term will lead to a more disciplined market with major players emerging from the current difficulties even stronger

2

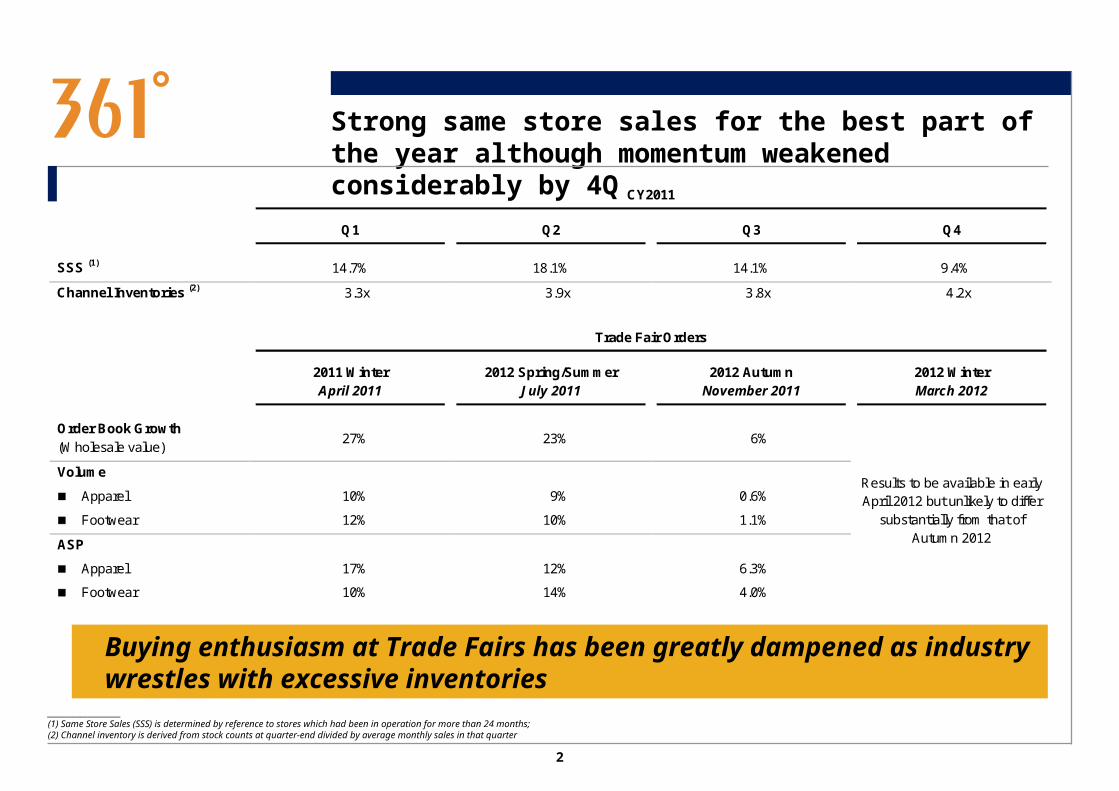

Strong same store sales for the best part of the year although momentum weakened considerably by 4Q

____________________(1) Same Store Sales (SSS) is determined by reference to stores which had been in operation for more than 24 months; (2) Channel inventory is derived from stock counts at quarter-end divided by average monthly sales in that quarter

CY2011

Q1 Q2 Q3 Q4

SSS (1) 14.7% 18.1% 14.1% 9.4%

Channel Inventories (2) 3.3x 3.9x 3.8x 4.2x

Trade Fair Orders

2011 Winter April 2011

2012 Spring/Summer July 2011

2012 Autumn November 2011

2012 Winter March 2012

Order Book Growth (Wholesale value)

27% 23% 6%

Volume

Apparel

Footwear

10%

12%

9%

10%

0.6%

1.1%

ASP

Apparel

Footwear

17%

10%

12%

14%

6.3%

4.0%

Results to be available in early April 2012 but unlikely to differ

substantially from that of Autumn 2012

Buying enthusiasm at Trade Fairs has been greatly dampened as industry wrestles with excessive inventories

3

Network has expanded modestly even as there are signs of saturation in certain provinces

____________________(1) Based on financial year to 30 June; FY2012 estimation (July to December 2011: 184)

Expansion will continue on an opportunistic and selective basis as good sites come into the market

Western Region1,505

Southern Region1,265

Eastern Region2,046

Northern Region3,049

2011 2010

No. of retail outlets 7,865 7,263

No. of retailers 3,410 3,459

Average No. of stores per retailer 2.3 2.1

Total retail space (sq.m.) 790,403 732,677

Net additions in the financial year (1)

1,735

1,506 1,423

872754

~600

0

500

1,000

1,500

2,000

FY2007 FY2008 FY2009 FY2010 FY2011 FY2012E

Tier 1 cities 8%

Tier 2 cities 20%

Tier 3 cities and smaller cities 72%

100%

No. of Stores (1)

4

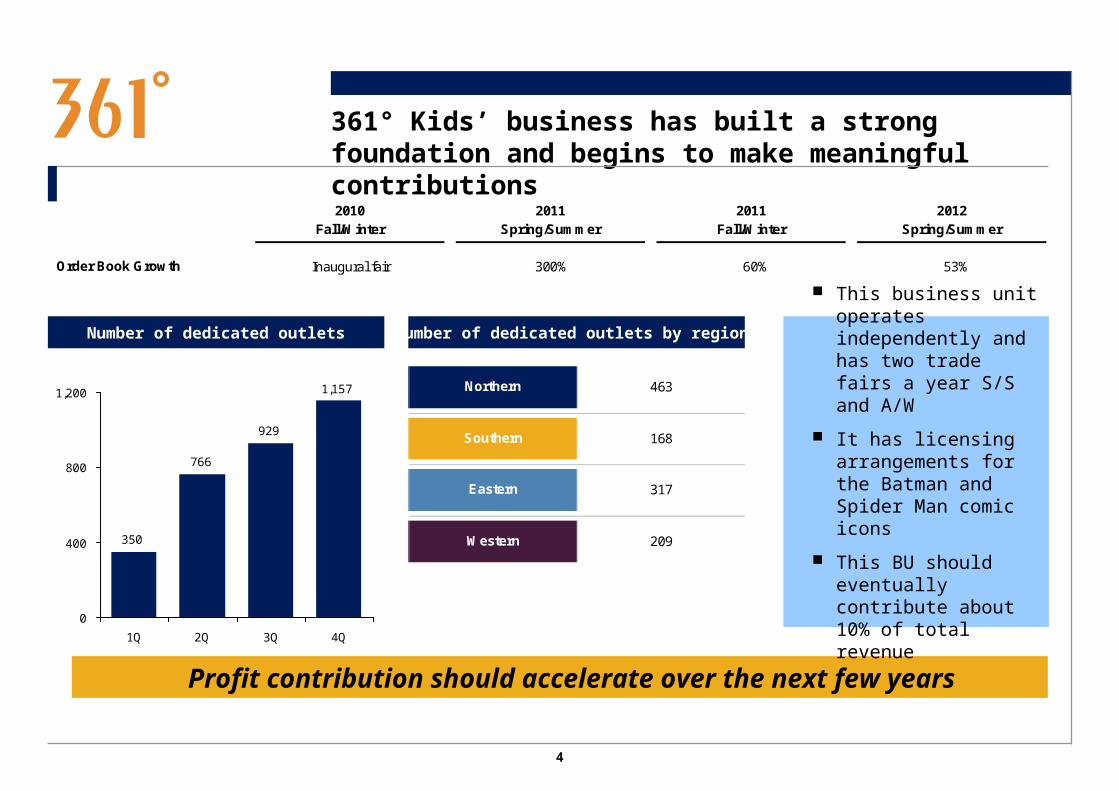

361° Kids’ business has built a strong foundation and begins to make meaningful contributions

Profit contribution should accelerate over the next few years

2010 Fall/Winter

2011 Spring/Summer

2011 Fall/Winter

2012 Spring/Summer

Order Book Growth Inaugural fair 300% 60% 53%

Number of dedicated outlets Number of dedicated outlets by region:

350

766

929

1,157

0

400

800

1,200

1Q 2Q 3Q 4Q

Northern 463

Southern 168

Eastern 317

Western 209

This business unit operates independently and has two trade fairs a year S/S and A/W

It has licensing arrangements for the Batman and Spider Man comic icons

This BU should eventually contribute about 10% of total revenue

5

ePOS now covers over 60% of the group’s outlets and has started to deliver good market intelligence

A full ERP Implementation will take time and further investment but remains a top priority

Coverage by stores: About 500 outlets are directly linked to the central servers in Xiamen, providing online and real-time data

ePOS data is now analyzed and fed into product cycle planning processes and retail store productivity and sales monitoring systems

Warehouse Management System (WMS) enables quicker delivery of finished goods through an elaborate scanning system

An I.T. Strategy Study has been conducted by IBM and its results are now studied for implementation

3,017

4,1464,529

4,95340.5%

54.0%58.0%

63.0%

1Q 2Q 3Q 4Q

ePOS connectivity % of total retail outlets

6

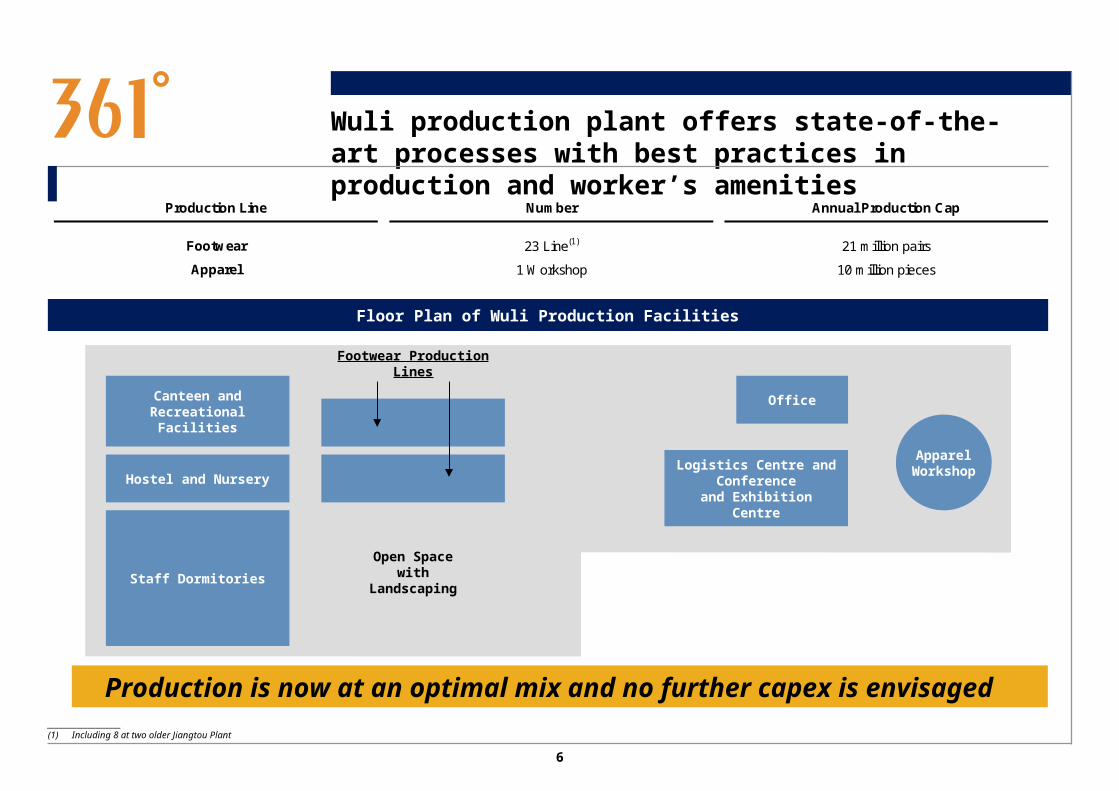

Wuli production plant offers state-of-the-art processes with best practices in production and worker’s amenities

Production is now at an optimal mix and no further capex is envisaged

Production Line Number Annual Production Cap

Footwear 23 Line(1) 21 million pairs

Apparel 1 Workshop 10 million pieces

Floor Plan of Wuli Production Facilities

Canteen and RecreationalFacilities

Hostel and Nursery

Staff Dormitories

Footwear Production Lines

Office

Logistics Centre and Conference

and Exhibition Centre

ApparelWorkshop

Open Spacewith

Landscaping

____________________(1) Including 8 at two older Jiangtou Plant

7

361° brand equity has strengthened significantly to command higher retail prices

Brand equity will become and increasingly important as the market becomesmore sophisticated although the value proposition remains core

Key Strategic Partners Major Event Sponsorships Celebrity Athlete Endorsements

361 is still focused on developing a multi-sport emphasis through key sponsorships of major international events organized in China

Celebrity sportsmen endorsements is part of a product marketing strategy with a more personal and emotive appeal

Steve Hooker

Kevin Love

Sun Yang

8

R&D spending, now at 1.5% of revenue, will continue to increase in the coming years

The Company has now established two key partnerships for research and development, in Beijing and Guangzhou, for apparel and footwear respectively. They employ over 300 staff who are engaged in identifying and testing new materials and fabrics, design and development work and tailor-made products for professional sportsmen who are sponsored by the Company

Company also collaborates with international design houses on a contract basis

There will be further product differentiation as the consumer market begins to be more demanding

2. Financial Review

9

2011 financial highlights

For the year ended 31 December

(RMB mil unless indicated otherwise)

2011 2010 Change (%)

Turnover 5,568.7 4,849.0 +14.8

Operating profit 1,385.0 1,146.8 +20.8

Net income 1,133.1 982.8 +15.3

Basic EPS (RMB cents) 54.8 47.6 +15.1

Dividend per share (HK cents)

Final 8.6 N/A N/A

Profitability ratios

Gross margin (%) 42.4 41.5 +0.9 p.p.

Operating margin (%) 24.9 23.7 +1.2 p.p.

Net margin (%) 20.4 20.1 +0.3 p.p.

Costs as a percentage of turnover

Staff costs (%) 7.4 5.4 +2.0 p.p.

Advertising and promotion (%) 10.9 10.3 +0.6 p.p.

R & D costs (%) 1.5 1.2 +0.3 p.p.

Balance Sheet Ratios

Average trade and bills receivables turnover cycle (days) 119 95 +24

Average trade and bills payables turnover cycle (days) 89 108 -19

Average inventory turnover cycle (days) Cash conversion cycle (days) 40 22 +18

Cash conversion cycle (days) 70 9 +61 2011 has been a difficult year for the industry but results are

satisfactory

10

Revenues improved by almost 15% because of a solidperformance by footwear

361 Kids3.4%

(3.3%)Accessories and others

2.1%(1.8%)

Apparel44.0%

(52.2%)

Footwear50.5%

(42.7%)

For the year ended 31 December 2011 (For the year ended 31 December 2010)

Footwear showed improvements in both volume and ASP as the expanded product range found appeal

Apparel suffered badly in an extremely competitive market with the entry of many local and international casual wear brands even as smaller sportswear brands expanded production

Kidswear continued to make solid progress as it gathers increasing appeal with national TV advertising on children's channels

For the year ended 31 December

(RMB ’000) 2011 2010 Change (%)

361° Products - Adults

Footwear 2,813,015 2,069,064 +36.0%

Apparel 2,452,216 2,532,034 -3.2%

Accessories and others 116,296 85,957 +35.3%

361° Products - Kids

187,151 161,955 +15.6%

Total 5,568,678 4,849,910 +14.8%

Higher wholesale prices will continue to be contributory but volumes areunder pressure as retail margins shrink

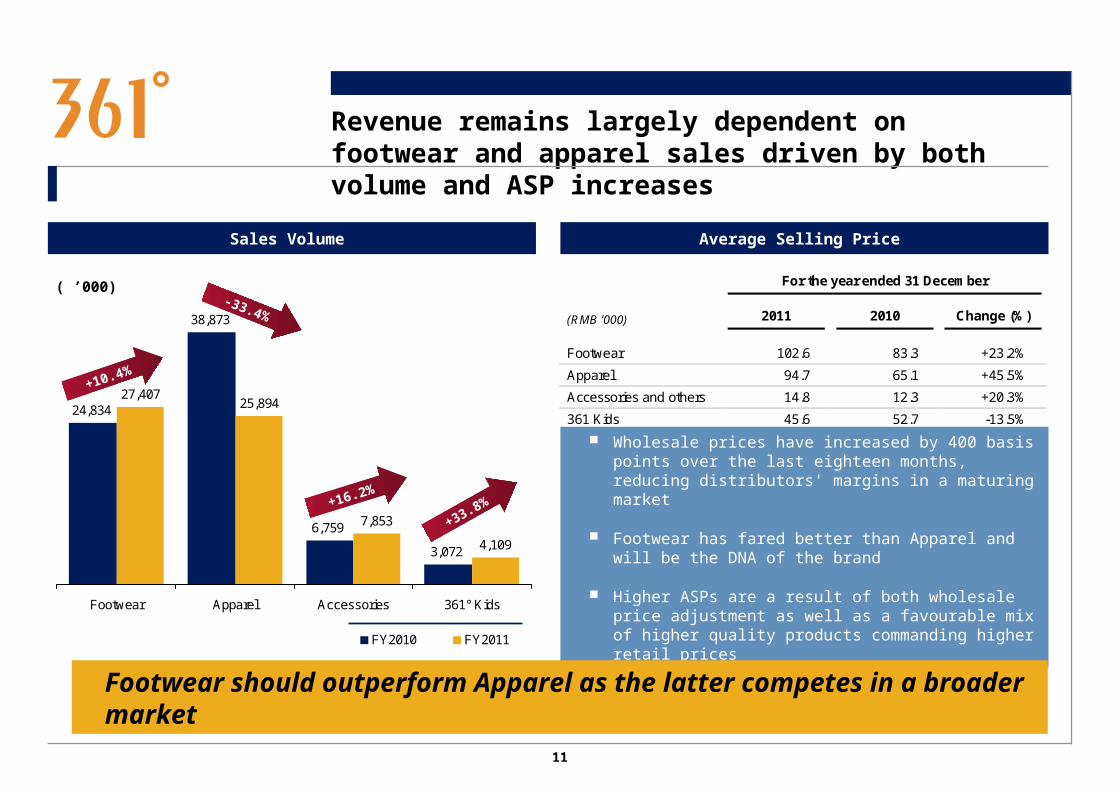

11

Revenue remains largely dependent on footwear and apparel sales driven by both volume and ASP increases

Sales Volume Average Selling Price

24,834

38,873

6,759

3,072

27,40725,894

7,853

4,109

Footwear Apparel Accessories 361° Kids

FY2010 FY2011

+10.4%

-33.4%

+16.2%

+33.8%

For the year ended 31 December

(RMB ’000) 2011 2010 Change (%)

Footwear 102.6 83.3 +23.2%

Apparel 94.7 65.1 +45.5%

Accessories and others 14.8 12.3 +20.3%

361 Kids 45.6 52.7 -13.5%

Wholesale prices have increased by 400 basis points over the last eighteen months, reducing distributors' margins in a maturing market

Footwear has fared better than Apparel and will be the DNA of the brand

Higher ASPs are a result of both wholesale price adjustment as well as a favourable mix of higher quality products commanding higher retail prices

Footwear should outperform Apparel as the latter competes in a broader market

( ’000)

12

Strong network presence in the western and northern regions will continue to provide solid support

For the year ended 31 December 2011 For the year ended 31 December 2010

Growth in likely to be uneven but the Group is well-positioned because of the geographical diversity of its net work

____________________(1) Eastern region includes Jiangsu, Zhejiang, Hubei, Anhui, Hunan, Shanghai and Jiangxi.(2) Southern region includes Guangdong, Fujian, Guangxi and Hainan.(3) Western region includes Sichuan, Yunnan, Guizhou, Shaanxi, Xinjiang, Gansu, Chongqing, Qinghai, Ningxia and Tibet.(4) Northern region includes Shandong, Beijing, Liaoning, Heilongjiang, Hebei, Henan, Shanxi, Jilin, Tianjin and Inner Mongolia.

For the year ended 31 Dec

(RMB ‘000) 2011 2010 Change (%)

Eastern(1) 1,284,743 1,152,477 +11.5%

Southern(2 1,253,969 1,177,693 +6.5%

Western(3) 1,007,115 810,740 +24.2%

Northern(4 2,022,851 1,708,100 +18.4%

23.1%

22.5%

18.1%

36.3% 35.2%

16.7%

24.3%

23.8%Eastern

Southern

Western

Northern

13

Margins showed slight improvement in 2011 and will probably remain relatively stable in 2012

Gross Profit and Gross Margin Operating Profit and Operating Margin

Over the medium term, gross margins will buckle under competition as consumers become more discerning and demanding

Net Profit and Net Margin ROA and ROE

2,010.52,362.8

41.5%42.4%

0

500

1,000

1,500

2,000

2,500

3,000

2010 2011

35%

40%

45%(RMB mn)

1,146.81,385.0

23.7%24.9%

0

500

1,000

1,500

2,000

2010 2011

20%

25%

30%(RMB mn)

982.81,133.1

20.1% 20.4%

0

300

600

900

1,200

1,500

1,800

2010 2011

0%

5%

10%

15%

20%

25%(RMB mn)

20.5% 20.4%

26.9% 26.3%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

2010 2011

ROE

ROA

14

Below the line costs have increased with the larger scale of operations

Total Expenses (% of turnover) Selling and distribution expenses increased by more than 12% primarily because of a larger spend in advertising and promotion expenses.. These have increased because of new contracts with celebrity sportsmen and additional assistance in the form of subsidies for display racking and shelves in the newly opened stores in the second half of 2011.

Administrative expenses increased by 30% due to heftier charges on depreciation arising from the completion of the Wuli Production Complex and higher R & D expenses.

13.8% 13.5%

4.7%5.4%

0%

3%

6%

9%

12%

15%

2010 2011

Selling and distribution expenses Adminstrative expenses

15

Because of a difficult 2011, the group has leveraged on itsfinancial strength to help distributors, retailers and suppliers

Average inventory turnover cycle Average trade and bills receivables turnover cycle

Accounts receivables have declined significantly in the 1Q of FY2012

Average trade and bills payables turnover cycle

22

40

0

10

20

30

40

50

2010 2011

95

119

0

30

60

90

120

150

2010 2011

108

89

0

40

80

120

2010 2011

Inventories have increased because of advanced deliveries of 2012 S/S products by some suppliers ahead of an early Chinese New Year

To help relieve cashflow pressures on the distributors and retailers, the Company has implemented various initiatives

Suppliers now prefer cash payments over bills because of liquidity problems

3. Outlook and Strategies

16

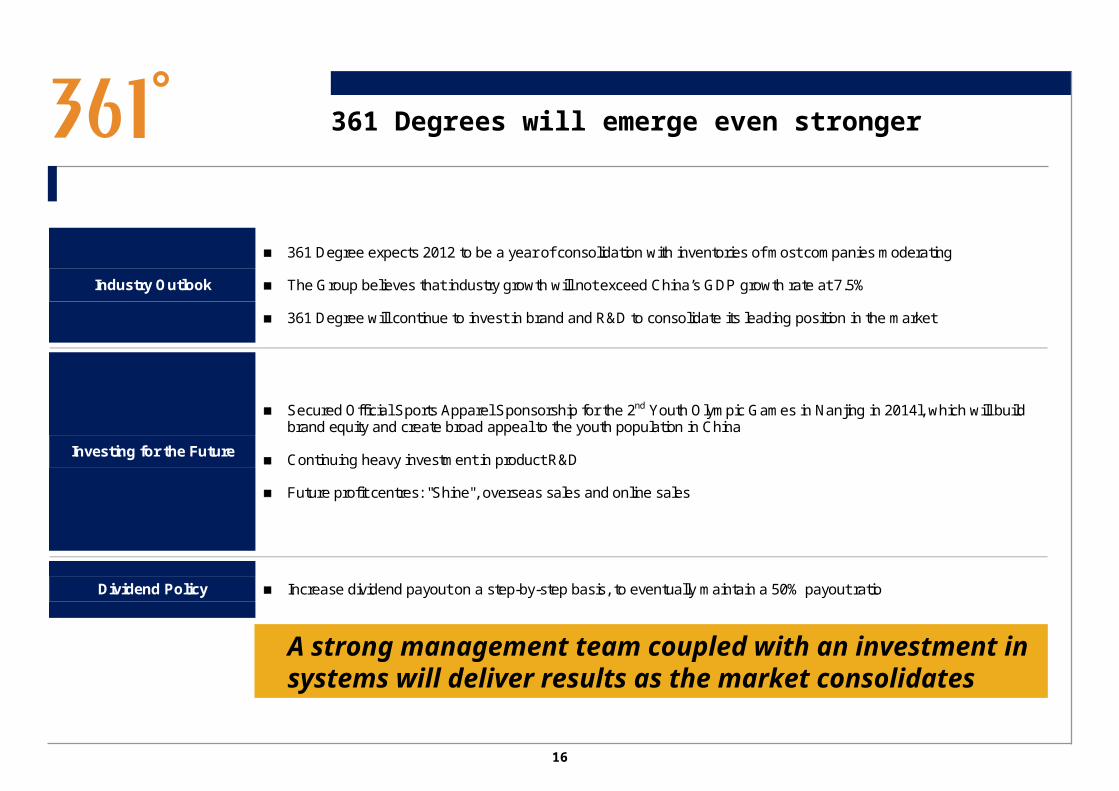

361 Degrees will emerge even stronger

A strong management team coupled with an investment insystems will deliver results as the market consolidates

Industry Outlook

361 Degree expects 2012 to be a year of consolidation with inventories of most companies moderating

The Group believes that industry growth will not exceed China’s GDP growth rate at 7.5%

361 Degree will continue to invest in brand and R&D to consolidate its leading position in the market

Investing for the Future

Secured Official Sports Apparel Sponsorship for the 2nd Youth Olympic Games in Nanjing in 2014l, which will build brand equity and create broad appeal to the youth population in China

Continuing heavy investment in product R&D

Future profit centres: "Shine", overseas sales and online sales

Dividend Policy Increase dividend payout on a step-by-step basis, to eventually maintain a 50% payout ratio

4. Q&A