30.08.2010 weekly equity report

8

Weekly New 30/08/2010 wsletter-Equity Capitalhe eight.com

-

Upload

capital-height -

Category

Documents

-

view

254 -

download

4

Transcript of 30.08.2010 weekly equity report

Weekly Newsletter30/08/2010

Weekly Newsletter-Equity

Capitalheight.com

Capitalheight.com

www.capitalheight.com

Phone- (0731)4295950

Weekly Newsletter

Contents

Market Wrap

Market Performance

NSE Gainers

NSE Losers

NIFTY 5 Days Up

World Indices

Indian Equity Market

Technical Analysis

Nifty Spot

Bank Nifty Future

www.capitalheight.com

Phone- (0731)4295950

MARKET WRAP

Indian equity markets sliced 2.2% this week with Nifty at 5408 & Sensex at 17998.

Food price inflation eased by 0.3% at 10.05% & fuel price index same at 12.57%.

Global markets down on fear of economy slowdown despite better GDP data.

Indian equity markets sliced down last week gains as Nifty shredded 122 points settling

above 5400 at 5408 while Sensex cut 403 points below psychological level of 18k at

17998. Nifty was bearish throughout the week with marginal gains and is now in range

of 5350 – 5450. It touched weekly high of 5449 and low of 5392.

On the sectoral front, Bankex lost 2% or 278 points, down at 10741. HDFC, ICICI &

Kotak Bank lost 3%-4% while in metals, Hindalco, Sterlite & Sail lost 8%, 4.5% & 3%

respectively.

India’s food price index eased down 0.30% at 10.05% vs.10.35% while Fuel price index

remains unchanged at 12.57% for the year till mid August. With this, RBI sees headline

WPI inflation gauge easing down from 9.97% Govt. has announced stimulus for its

foreign trade policy 09-14, this stimulus will be worth Rs. 1050 Cr. & prospects to

achieve $ 200 billion export in FY11.

Dow Jones & S&P fell for third consecutive week. Dow Jones is down 0.60% still

above 10k at 10150 & S&P down 0.70% at 1064. NASDAQ too gave up 1.2%, down 26

pts at 2153. Dow Futures was sliced 90 points this week but in the end gained 170

points on better prelim GDP data at 1.6% vs. 1.5% & also lower job claims at 473k vs.

500k. European markets also ended positive with CAC at 3500 & DAX at 5950. FTSE

gained marginally up 0.12% or 6 pts at 5201 due to revised GDP q\q at 1.2% vs. 1.1%.

www.capitalheight.com

Phone- (0731)4295950

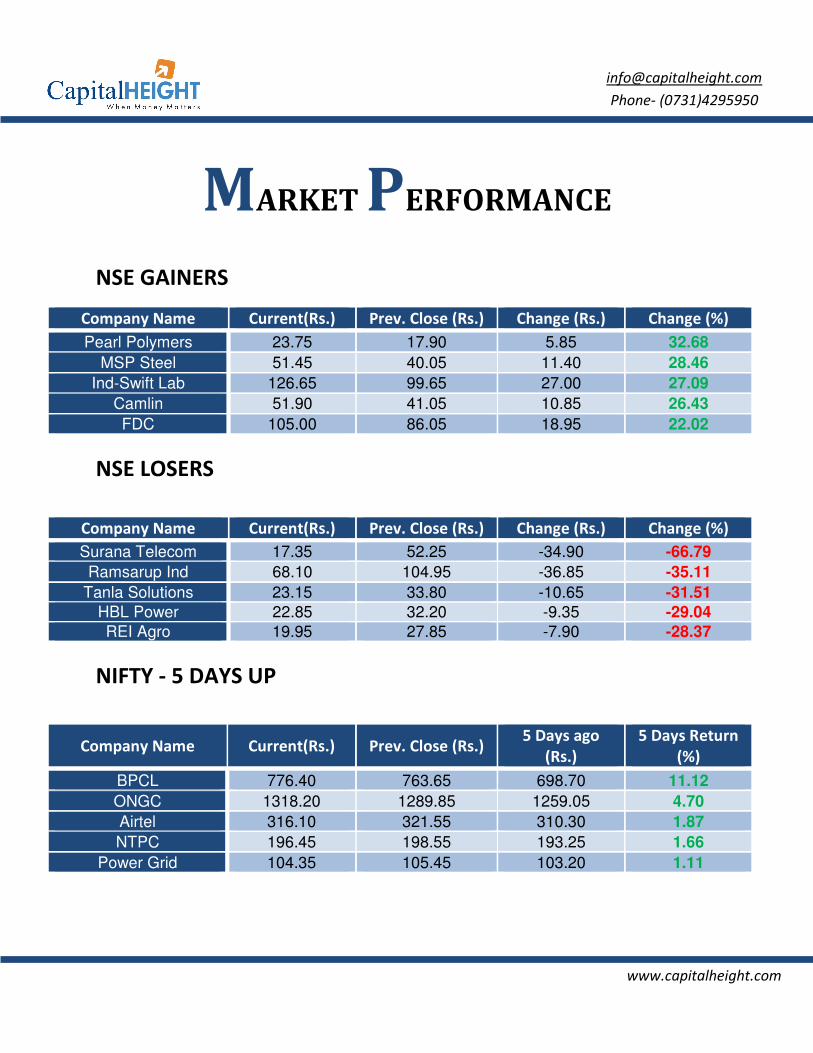

MARKET PERFORMANCE

NSE GAINERS

Company Name Current(Rs.) Prev. Close (Rs.) Change (Rs.) Change (%)

Pearl Polymers 23.75 17.90 5.85 32.68

MSP Steel 51.45 40.05 11.40 28.46

Ind-Swift Lab 126.65 99.65 27.00 27.09

Camlin 51.90 41.05 10.85 26.43

FDC 105.00 86.05 18.95 22.02

NSE LOSERS

Company Name Current(Rs.) Prev. Close (Rs.) Change (Rs.) Change (%)

Surana Telecom 17.35 52.25 -34.90 -66.79

Ramsarup Ind 68.10 104.95 -36.85 -35.11

Tanla Solutions 23.15 33.80 -10.65 -31.51

HBL Power 22.85 32.20 -9.35 -29.04

REI Agro 19.95 27.85 -7.90 -28.37

NIFTY - 5 DAYS UP

Company Name Current(Rs.) Prev. Close (Rs.) 5 Days ago

(Rs.)

5 Days Return

(%)

BPCL 776.40 763.65 698.70 11.12

ONGC 1318.20 1289.85 1259.05 4.70

Airtel 316.10 321.55 310.30 1.87

NTPC 196.45 198.55 193.25 1.66

Power Grid 104.35 105.45 103.20 1.11

www.capitalheight.com

Phone- (0731)4295950

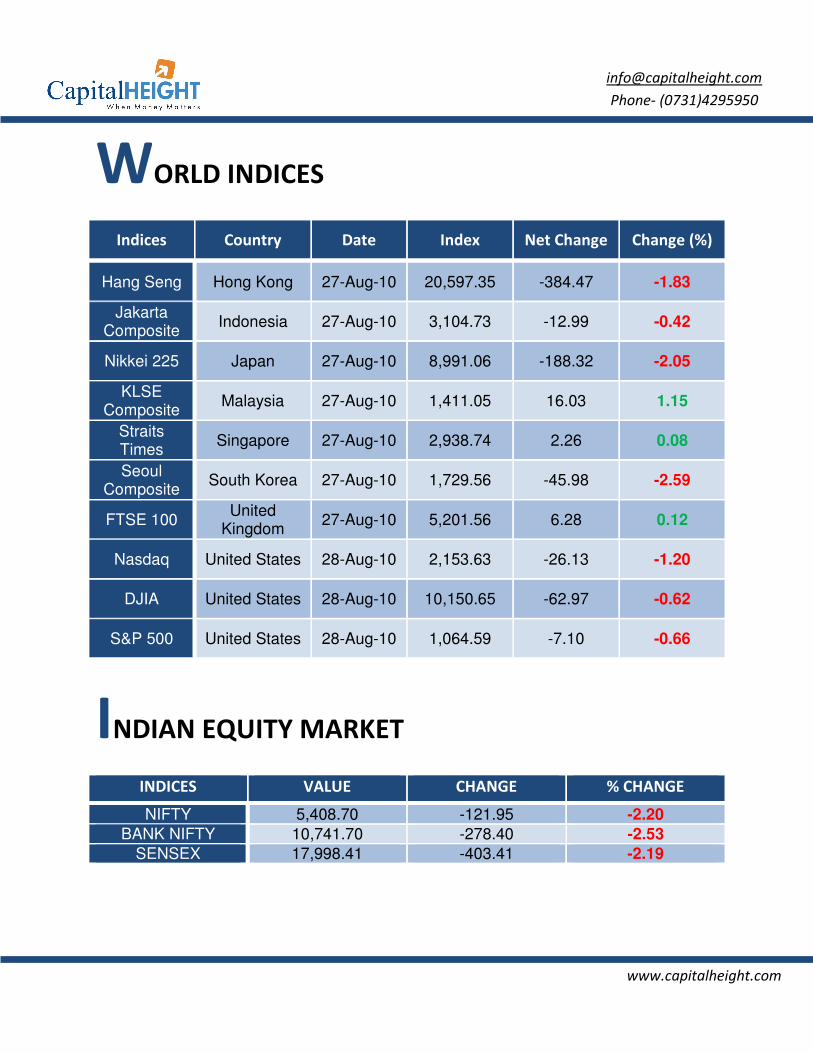

WORLD INDICES

Indices Country Date Index Net Change Change (%)

Hang Seng Hong Kong 27-Aug-10 20,597.35 -384.47 -1.83

Jakarta Composite

Indonesia 27-Aug-10 3,104.73 -12.99 -0.42

Nikkei 225 Japan 27-Aug-10 8,991.06 -188.32 -2.05

KLSE Composite

Malaysia 27-Aug-10 1,411.05 16.03 1.15

Straits Times

Singapore 27-Aug-10 2,938.74 2.26 0.08

Seoul Composite

South Korea 27-Aug-10 1,729.56 -45.98 -2.59

FTSE 100 United

Kingdom 27-Aug-10 5,201.56 6.28 0.12

Nasdaq United States 28-Aug-10 2,153.63 -26.13 -1.20

DJIA United States 28-Aug-10 10,150.65 -62.97 -0.62

S&P 500 United States 28-Aug-10 1,064.59 -7.10 -0.66

INDIAN EQUITY MARKET

INDICES VALUE CHANGE % CHANGE

NIFTY 5,408.70 -121.95 -2.20

BANK NIFTY 10,741.70 -278.40 -2.53

SENSEX 17,998.41 -403.41 -2.19

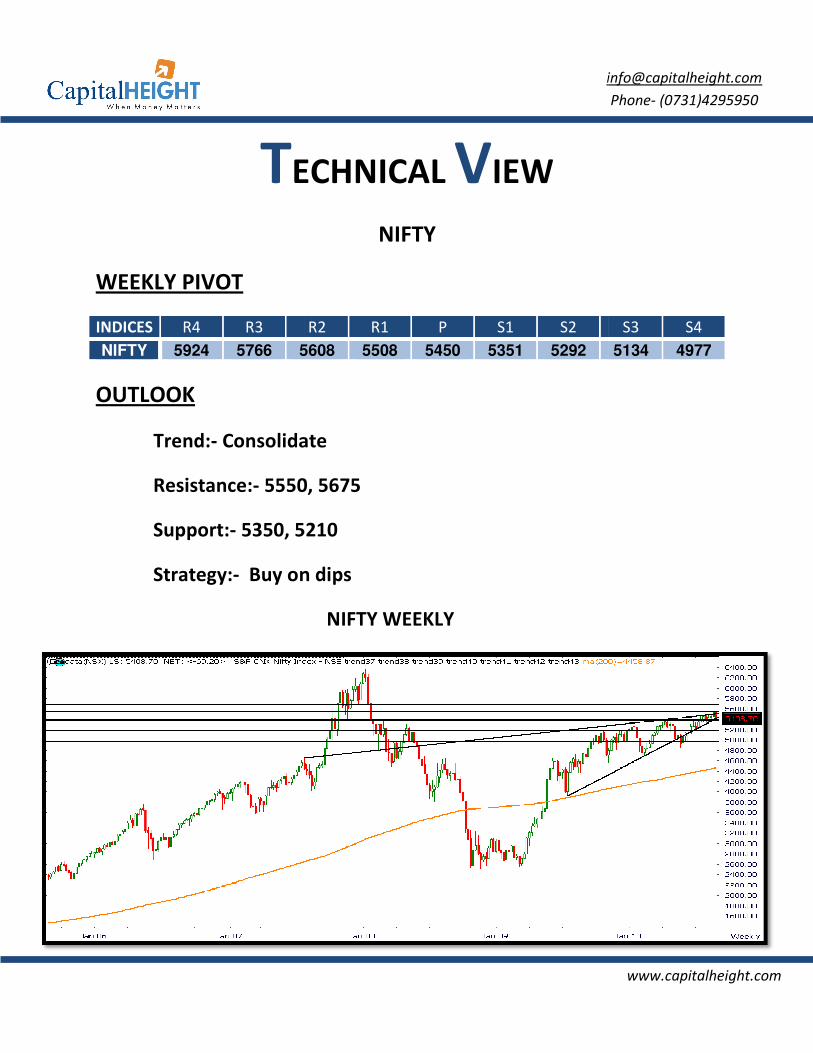

TECHNICAL

WEEKLY PIVOT

INDICES R4 R3

NIFTY 5924 5766 5608

OUTLOOK

Trend:- Consolidate

Resistance:- 5550

Support:- 5350, 5

Strategy:- Buy on dips

ECHNICAL VIEW

NIFTY

R2 R1 P S1 S2

5608 5508 5450 5351 5292

Consolidate

5550, 5675

, 5210

Buy on dips

NIFTY WEEKLY

www.capitalheight.com

Phone- (0731)4295950

S3 S4

5134 4977

WEEKLY PIVOT

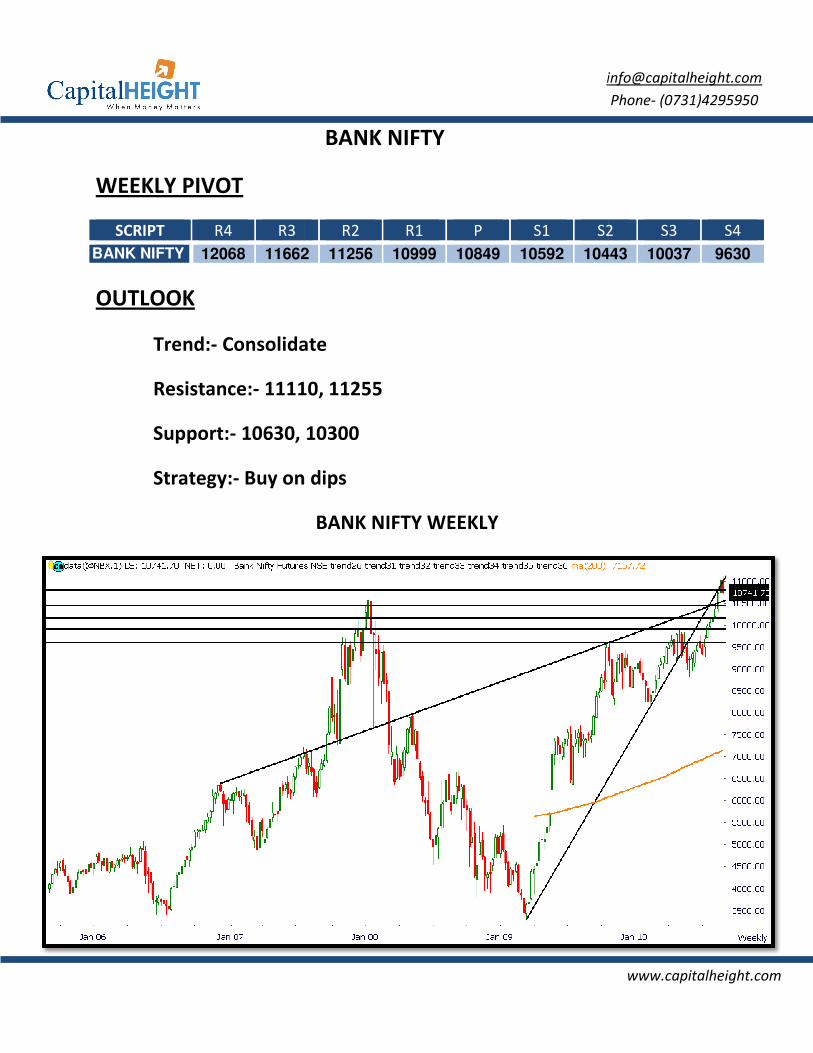

SCRIPT R4 R3

BANK NIFTY 12068 11662

OUTLOOK

Trend:- Consolidate

Resistance:- 11110

Support:- 10630,

Strategy:- Buy on dips

BANK NIFTY

R2 R1 P S1 S2

11662 11256 10999 10849 10592 10443

Consolidate

11110, 11255

, 10300

Buy on dips

BANK NIFTY WEEKLY

www.capitalheight.com

Phone- (0731)4295950

S2 S3 S4

10443 10037 9630

www.capitalheight.com

Phone- (0731)4295950

Disclaimer

The information and views in this report, our website & all the service we provide are believed to be reliable, but we do not

accept any responsibility (or liability) for errors of fact or opinion. Users have the right to choose the product/s that suits

them the most.

Sincere efforts have been made to present the right investment perspective. The information contained herein is based on

analysis and up on sources that we consider reliable.

This material is for personal information and based upon it & takes no responsibility

The information given herein should be treated as only factor, while making investment decision. The report does not

provide individually tailor-made investment advice. Capitalheight recommends that investors independently evaluate

particular investments and strategies, and encourages investors to seek the advice of a financial adviser. Capitalheight shall

not be responsible for any transaction conducted based on the information given in this report, which is in violation of rules

and regulations of NSE and BSE.

The share price projections shown are not necessarily indicative of future price performance. The information herein,

together with all estimates and forecasts, can change without notice. Analyst or any person related to Capitalheight might be

holding positions in the stocks recommended. It is understood that anyone who is browsing through the site has done so at

his free will and does not read any views expressed as a recommendation for which either the site or its owners or

anyone can be held responsible for . Any surfing and reading of the information is the acceptance of this disclaimer.

All Rights Reserved.

Investment in Commodity and equity market has its own risks.

We, however, do not vouch for the accuracy or the completeness thereof. we are not responsible for any loss incurred

whatsoever for any financial profits or loss which may arise from the recommendations above. Capitalheight does not

purport to be an invitation or an offer to buy or sell any financial instrument. Our Clients (Paid Or Unpaid), Any third party or

anyone else have no rights to forward or share our calls or SMS or Report or Any Information Provided by us to/with anyone

which is received directly or indirectly by them. If found so then Serious Legal Actions can be taken.