3. IPCC Cost Accounting and Financial Management · PDF filePadhuka’s Cost Accounting...

20

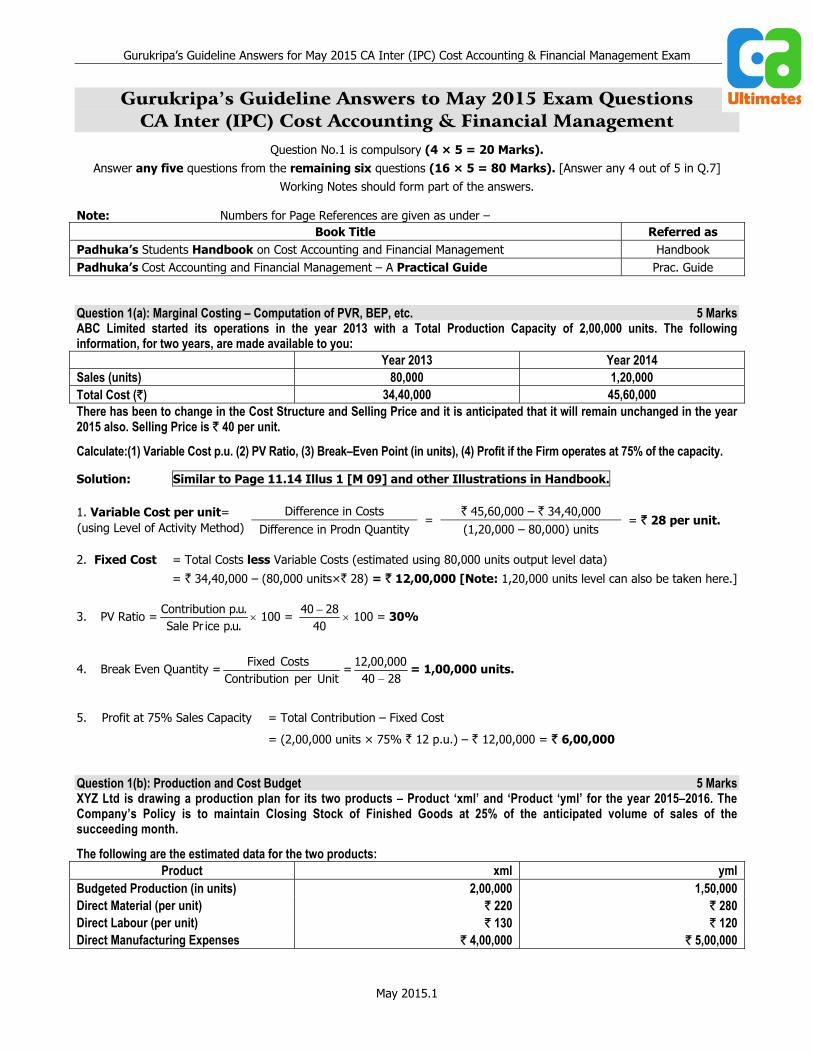

Gurukripa’s Guideline Answers for May 2015 CA Inter (IPC) Cost Accounting & Financial Management Exam May 2015.1 Gurukripa’s Guideline Answers to May 2015 Exam Questions CA Inter (IPC) Cost Accounting & Financial Management Question No.1 is compulsory (4 × 5 = 20 Marks). Answer any five questions from the remaining six questions (16 × 5 = 80 Marks). [Answer any 4 out of 5 in Q.7] Working Notes should form part of the answers. Note: Numbers for Page References are given as under – Book Title Referred as Padhuka’s Students Handbook on Cost Accounting and Financial Management Handbook Padhuka’s Cost Accounting and Financial Management – A Practical Guide Prac. Guide Question 1(a): Marginal Costing – Computation of PVR, BEP, etc. 5 Marks ABC Limited started its operations in the year 2013 with a Total Production Capacity of 2,00,000 units. The following information, for two years, are made available to you: Year 2013 Year 2014 Sales (units) 80,000 1,20,000 Total Cost (`) 34,40,000 45,60,000 There has been to change in the Cost Structure and Selling Price and it is anticipated that it will remain unchanged in the year 2015 also. Selling Price is ` 40 per unit. Calculate:(1) Variable Cost p.u. (2) PV Ratio, (3) Break–Even Point (in units), (4) Profit if the Firm operates at 75% of the capacity. Solution: Similar to Page 11.14 Illus 1 [M 09] and other Illustrations in Handbook. 1. Variable Cost per unit= (using Level of Activity Method) Difference in Costs = ` 45,60,000 – ` 34,40,000 = ` 28 per unit. Difference in Prodn Quantity (1,20,000 – 80,000) units 2. Fixed Cost = Total Costs less Variable Costs (estimated using 80,000 units output level data) = ` 34,40,000 – (80,000 units×` 28) = ` 12,00,000 [Note: 1,20,000 units level can also be taken here.] 3. PV Ratio = . u . p ice Pr Sale . u . p on Contributi × 100 = 40 28 40 − × 100 = 30% 4. Break Even Quantity = Unit per on Contributi Costs Fixed = 28 40 000 , 00 , 12 − = 1,00,000 units. 5. Profit at 75% Sales Capacity = Total Contribution – Fixed Cost = (2,00,000 units × 75% ` 12 p.u.) – ` 12,00,000 = ` 6,00,000 Question 1(b): Production and Cost Budget 5 Marks XYZ Ltd is drawing a production plan for its two products – Product ‘xml’ and ‘Product ‘yml’ for the year 2015–2016. The Company’s Policy is to maintain Closing Stock of Finished Goods at 25% of the anticipated volume of sales of the succeeding month. The following are the estimated data for the two products: Product xml yml Budgeted Production (in units) 2,00,000 1,50,000 Direct Material (per unit) ` 220 ` 280 Direct Labour (per unit) ` 130 ` 120 Direct Manufacturing Expenses ` 4,00,000 ` 5,00,000

Transcript of 3. IPCC Cost Accounting and Financial Management · PDF filePadhuka’s Cost Accounting...

Gurukripa’s Guideline Answers for May 2015 CA Inter (IPC) Cost Accounting & Financial Management Exam

May 2015.1

Gurukripa’s Guideline Answers to May 2015 Exam Questions CA Inter (IPC) Cost Accounting & Financial Management

Question No.1 is compulsory (4 × 5 = 20 Marks). Answer any five questions from the remaining six questions (16 × 5 = 80 Marks). [Answer any 4 out of 5 in Q.7]

Working Notes should form part of the answers. Note: Numbers for Page References are given as under –

Book Title Referred as Padhuka’s Students Handbook on Cost Accounting and Financial Management Handbook Padhuka’s Cost Accounting and Financial Management – A Practical Guide Prac. Guide Question 1(a): Marginal Costing – Computation of PVR, BEP, etc. 5 Marks ABC Limited started its operations in the year 2013 with a Total Production Capacity of 2,00,000 units. The following information, for two years, are made available to you:

Year 2013 Year 2014 Sales (units) 80,000 1,20,000 Total Cost (`) 34,40,000 45,60,000 There has been to change in the Cost Structure and Selling Price and it is anticipated that it will remain unchanged in the year 2015 also. Selling Price is ` 40 per unit.

Calculate:(1) Variable Cost p.u. (2) PV Ratio, (3) Break–Even Point (in units), (4) Profit if the Firm operates at 75% of the capacity. Solution: Similar to Page 11.14 Illus 1 [M 09] and other Illustrations in Handbook. 1. Variable Cost per unit= (using Level of Activity Method)

Difference in Costs =

` 45,60,000 – ` 34,40,000 = ` 28 per unit.

Difference in Prodn Quantity (1,20,000 – 80,000) units 2. Fixed Cost = Total Costs less Variable Costs (estimated using 80,000 units output level data)

= ` 34,40,000 – (80,000 units×` 28) = ` 12,00,000 [Note: 1,20,000 units level can also be taken here.] 3. PV Ratio =

.u.picePrSale.u.ponContributi× 100 =

402840 −

× 100 = 30%

4. Break Even Quantity =UnitperonContributi

CostsFixed=

2840000,00,12

−= 1,00,000 units.

5. Profit at 75% Sales Capacity = Total Contribution – Fixed Cost

= (2,00,000 units × 75% ` 12 p.u.) – ` 12,00,000 = ` 6,00,000 Question 1(b): Production and Cost Budget 5 Marks XYZ Ltd is drawing a production plan for its two products – Product ‘xml’ and ‘Product ‘yml’ for the year 2015–2016. The Company’s Policy is to maintain Closing Stock of Finished Goods at 25% of the anticipated volume of sales of the succeeding month.

The following are the estimated data for the two products: Product xml yml

Budgeted Production (in units) 2,00,000 1,50,000 Direct Material (per unit) ` 220 ` 280 Direct Labour (per unit) ` 130 ` 120 Direct Manufacturing Expenses ` 4,00,000 ` 5,00,000

sandy

Typewriter

Get CA CMA CS Updates and More From Caultimates.com

sandy

Typewriter

sandy

Typewriter

Gurukripa’s Guideline Answers for May 2015 CA Inter (IPC) Cost Accounting & Financial Management Exam

May 2015.2

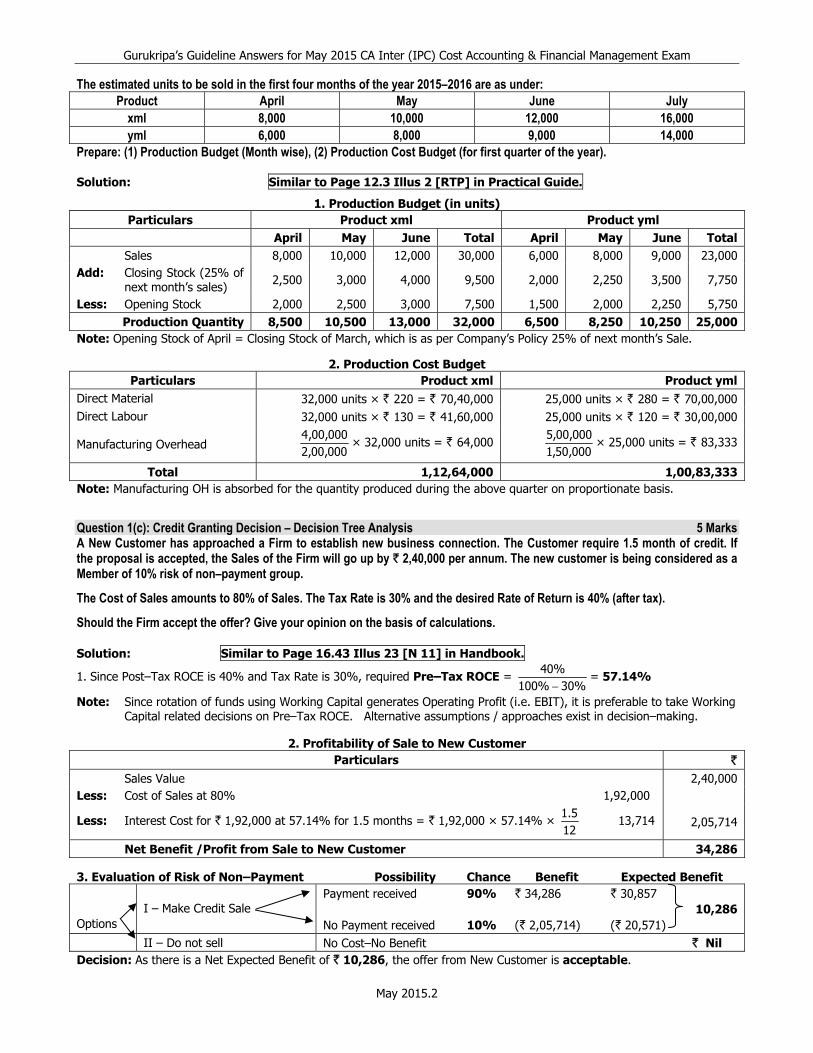

The estimated units to be sold in the first four months of the year 2015–2016 are as under: Product April May June July

xml 8,000 10,000 12,000 16,000 yml 6,000 8,000 9,000 14,000

Prepare: (1) Production Budget (Month wise), (2) Production Cost Budget (for first quarter of the year). Solution: Similar to Page 12.3 Illus 2 [RTP] in Practical Guide.

1. Production Budget (in units) Particulars Product xml Product yml

April May June Total April May June TotalSales 8,000 10,000 12,000 30,000 6,000 8,000 9,000 23,000

Add: Closing Stock (25% of next month’s sales) 2,500 3,000 4,000 9,500 2,000 2,250 3,500 7,750

Less: Opening Stock 2,000 2,500 3,000 7,500 1,500 2,000 2,250 5,750 Production Quantity 8,500 10,500 13,000 32,000 6,500 8,250 10,250 25,000

Note: Opening Stock of April = Closing Stock of March, which is as per Company’s Policy 25% of next month’s Sale.

2. Production Cost Budget Particulars Product xml Product yml

Direct Material 32,000 units × ` 220 = ` 70,40,000 25,000 units × ` 280 = ` 70,00,000 Direct Labour 32,000 units × ` 130 = ` 41,60,000 25,000 units × ` 120 = ` 30,00,000

Manufacturing Overhead 000,00,2000,00,4

× 32,000 units = ` 64,000 000,50,1000,00,5

× 25,000 units = ` 83,333

Total 1,12,64,000 1,00,83,333Note: Manufacturing OH is absorbed for the quantity produced during the above quarter on proportionate basis. Question 1(c): Credit Granting Decision – Decision Tree Analysis 5 Marks A New Customer has approached a Firm to establish new business connection. The Customer require 1.5 month of credit. If the proposal is accepted, the Sales of the Firm will go up by ` 2,40,000 per annum. The new customer is being considered as a Member of 10% risk of non–payment group.

The Cost of Sales amounts to 80% of Sales. The Tax Rate is 30% and the desired Rate of Return is 40% (after tax).

Should the Firm accept the offer? Give your opinion on the basis of calculations. Solution: Similar to Page 16.43 Illus 23 [N 11] in Handbook.

1. Since Post–Tax ROCE is 40% and Tax Rate is 30%, required Pre–Tax ROCE = %30%100

%40−

= 57.14%

Note: Since rotation of funds using Working Capital generates Operating Profit (i.e. EBIT), it is preferable to take Working Capital related decisions on Pre–Tax ROCE. Alternative assumptions / approaches exist in decision–making.

2. Profitability of Sale to New Customer

Particulars `

Sales Value 2,40,000 Less: Cost of Sales at 80% 1,92,000

Less: Interest Cost for ` 1,92,000 at 57.14% for 1.5 months = ` 1,92,000 × 57.14% × 12

5.1 13,714 2,05,714

Net Benefit /Profit from Sale to New Customer 34,286 3. Evaluation of Risk of Non–Payment Possibility Chance Benefit Expected Benefit Options

I – Make Credit Sale

Payment received 90% ` 34,286 ` 30,857 10,286

No Payment received 10% (` 2,05,714) (` 20,571) II – Do not sell No Cost–No Benefit ` Nil Decision: As there is a Net Expected Benefit of ` 10,286, the offer from New Customer is acceptable.

sandy

Typewriter

Get CA CMA CS Updates and More From Caultimates.com

sandy

Typewriter

sandy

Typewriter

Gurukripa’s Guideline Answers for May 2015 CA Inter (IPC) Cost Accounting & Financial Management Exam

May 2015.3

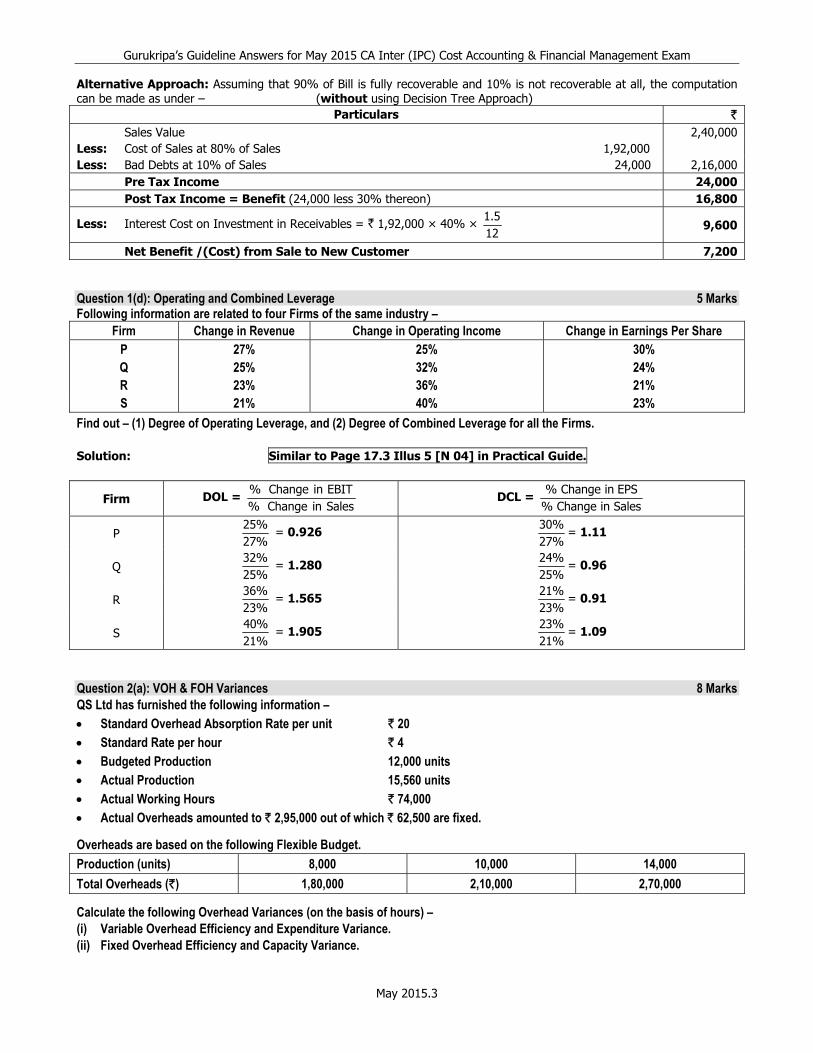

Alternative Approach: Assuming that 90% of Bill is fully recoverable and 10% is not recoverable at all, the computation can be made as under – (without using Decision Tree Approach)

Particulars ` Sales Value 2,40,000 Less: Cost of Sales at 80% of Sales 1,92,000 Less: Bad Debts at 10% of Sales 24,000 2,16,000 Pre Tax Income 24,000 Post Tax Income = Benefit (24,000 less 30% thereon) 16,800

Less: Interest Cost on Investment in Receivables = ` 1,92,000 × 40% × 12

5.1 9,600

Net Benefit /(Cost) from Sale to New Customer 7,200 Question 1(d): Operating and Combined Leverage 5 Marks Following information are related to four Firms of the same industry –

Firm Change in Revenue Change in Operating Income Change in Earnings Per Share P 27% 25% 30% Q 25% 32% 24% R 23% 36% 21% S 21% 40% 23%

Find out – (1) Degree of Operating Leverage, and (2) Degree of Combined Leverage for all the Firms. Solution: Similar to Page 17.3 Illus 5 [N 04] in Practical Guide.

Firm DOL = SalesinChange%EBITinChange% DCL =

SalesinChange%EPSinChange%

P %27%25

= 0.926 %27%30

= 1.11

Q %25%32

= 1.280 %25%24

= 0.96

R %23%36

= 1.565 %23%21

= 0.91

S %21%40

= 1.905 %21%23

= 1.09

Question 2(a): VOH & FOH Variances 8 Marks QS Ltd has furnished the following information – • Standard Overhead Absorption Rate per unit ` 20 • Standard Rate per hour ` 4 • Budgeted Production 12,000 units • Actual Production 15,560 units • Actual Working Hours ` 74,000 • Actual Overheads amounted to ` 2,95,000 out of which ` 62,500 are fixed.

Overheads are based on the following Flexible Budget. Production (units) 8,000 10,000 14,000 Total Overheads (`) 1,80,000 2,10,000 2,70,000

Calculate the following Overhead Variances (on the basis of hours) – (i) Variable Overhead Efficiency and Expenditure Variance. (ii) Fixed Overhead Efficiency and Capacity Variance.

sandy

Typewriter

Get CA CMA CS Updates and More From Caultimates.com

sandy

Typewriter

sandy

Typewriter

Gurukripa’s Guideline Answers for May 2015 CA Inter (IPC) Cost Accounting & Financial Management Exam

May 2015.4

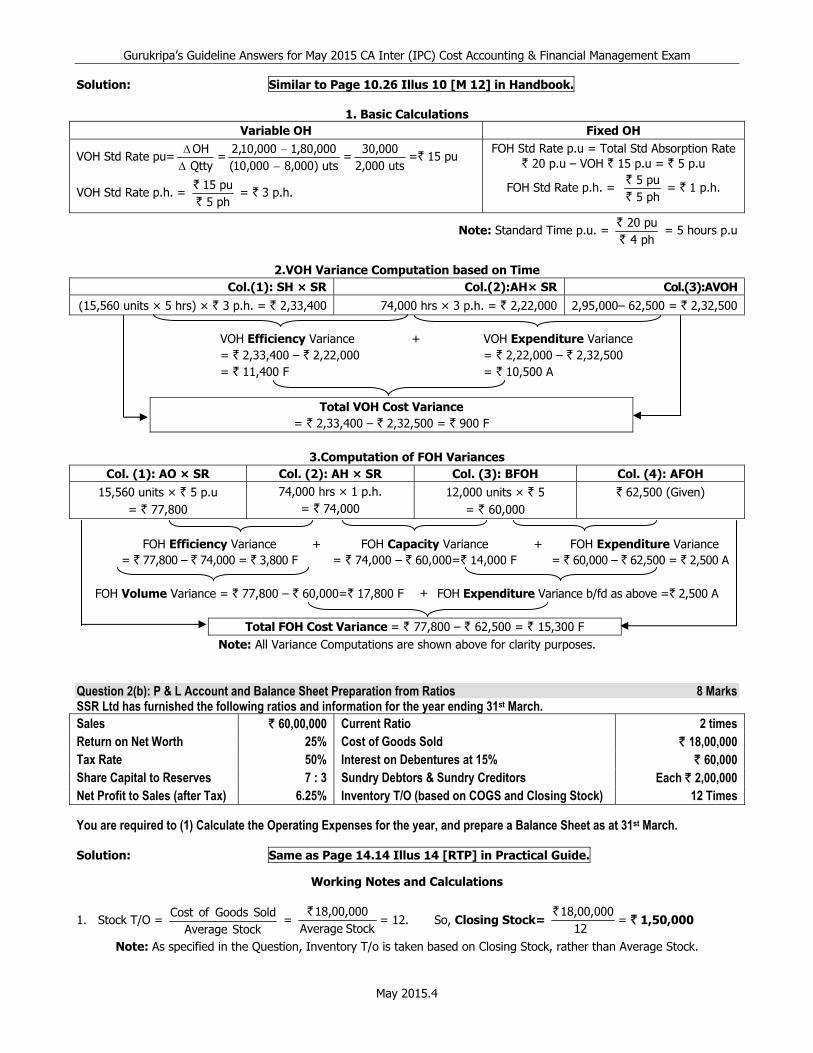

Solution: Similar to Page 10.26 Illus 10 [M 12] in Handbook.

1. Basic Calculations Variable OH Fixed OH

VOH Std Rate pu=QttyOH

ΔΔ

=uts)000,8000,10(

000,80,1000,10,2−−

=uts000,2

000,30=` 15 pu

VOH Std Rate p.h. = ph5pu15

``

= ` 3 p.h.

FOH Std Rate p.u = Total Std Absorption Rate ` 20 p.u – VOH ` 15 p.u = ` 5 p.u

FOH Std Rate p.h. = ph5pu5

``

= ` 1 p.h.

Note: Standard Time p.u. = ph4pu20

``

= 5 hours p.u

2.VOH Variance Computation based on Time Col.(1): SH × SR Col.(2):AH× SR Col.(3):AVOH

(15,560 units × 5 hrs) × ` 3 p.h. = ` 2,33,400 74,000 hrs × 3 p.h. = ` 2,22,000 2,95,000– 62,500 = ` 2,32,500

VOH Efficiency Variance = ` 2,33,400 – ` 2,22,000 = ` 11,400 F

+ VOH Expenditure Variance = ` 2,22,000 – ` 2,32,500 = ` 10,500 A

Total VOH Cost Variance

= ` 2,33,400 – ` 2,32,500 = ` 900 F

3.Computation of FOH Variances

Col. (1): AO × SR Col. (2): AH × SR Col. (3): BFOH Col. (4): AFOH 15,560 units × ` 5 p.u

= ` 77,800 74,000 hrs × 1 p.h.

= ` 74,000 12,000 units × ` 5

= ` 60,000 ` 62,500 (Given)

FOH Efficiency Variance

= ` 77,800 – ` 74,000 = ` 3,800 F + FOH Capacity Variance

= ` 74,000 – ` 60,000=` 14,000 F + FOH Expenditure Variance

= ` 60,000 – ` 62,500 = ` 2,500 A FOH Volume Variance = ` 77,800 – ` 60,000=` 17,800 F + FOH Expenditure Variance b/fd as above =` 2,500 A

Total FOH Cost Variance = ` 77,800 – ` 62,500 = ` 15,300 F

Note: All Variance Computations are shown above for clarity purposes. Question 2(b): P & L Account and Balance Sheet Preparation from Ratios 8 Marks SSR Ltd has furnished the following ratios and information for the year ending 31st March. Sales ` 60,00,000 Current Ratio 2 times Return on Net Worth 25% Cost of Goods Sold ` 18,00,000 Tax Rate 50% Interest on Debentures at 15% ` 60,000 Share Capital to Reserves 7 : 3 Sundry Debtors & Sundry Creditors Each ` 2,00,000 Net Profit to Sales (after Tax) 6.25% Inventory T/O (based on COGS and Closing Stock) 12 Times You are required to (1) Calculate the Operating Expenses for the year, and prepare a Balance Sheet as at 31st March. Solution: Same as Page 14.14 Illus 14 [RTP] in Practical Guide.

Working Notes and Calculations

1. Stock T/O = StockAverage

SoldGoodsofCost =

StockAverage18,00,000 `

= 12. So, Closing Stock= 12

18,00,000 `= ` 1,50,000

Note: As specified in the Question, Inventory T/o is taken based on Closing Stock, rather than Average Stock.

sandy

Typewriter

Get CA CMA CS Updates and More From Caultimates.com

sandy

Typewriter

sandy

Typewriter

Gurukripa’s Guideline Answers for May 2015 CA Inter (IPC) Cost Accounting & Financial Management Exam

May 2015.5

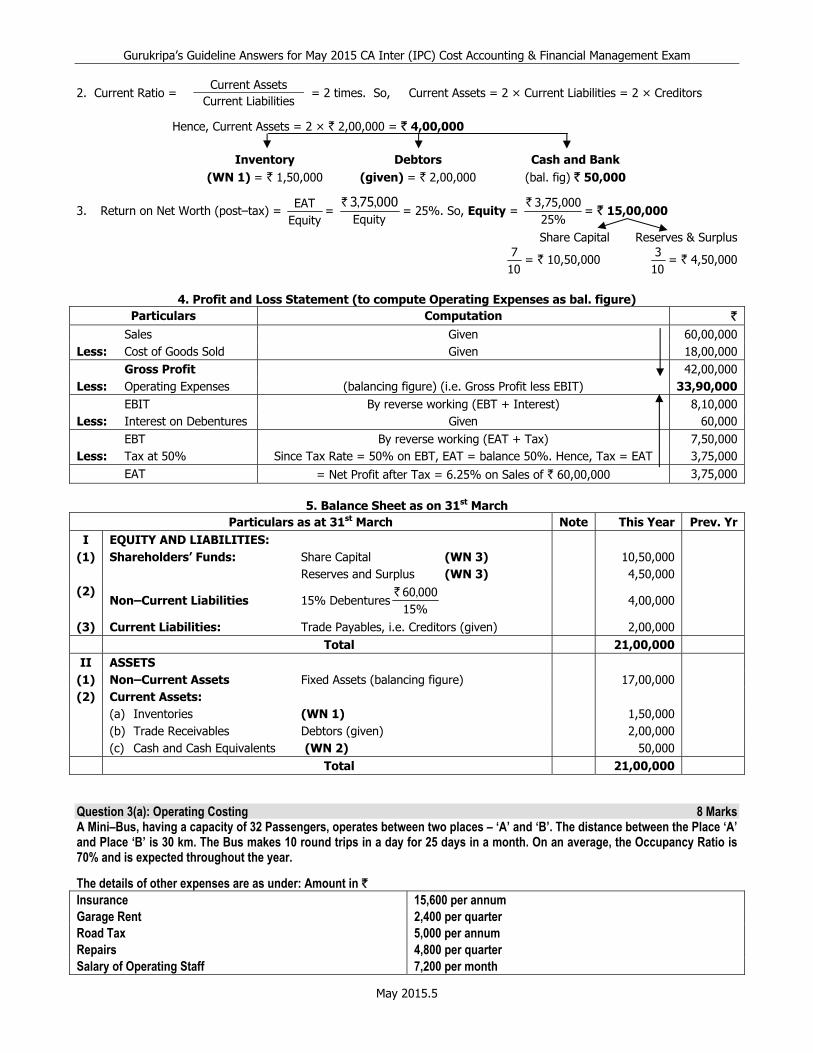

2. Current Ratio = Current Assets

= 2 times. So, Current Assets = 2 × Current Liabilities = 2 × Creditors Current Liabilities

Hence, Current Assets = 2 × ` 2,00,000 = ` 4,00,000 Inventory Debtors Cash and Bank (WN 1) = ` 1,50,000 (given) = ` 2,00,000 (bal. fig) ` 50,000

3. Return on Net Worth (post–tax) = EquityEAT

= Equity

000753 ,, `= 25%. So, Equity =

%253,75,000 `

= ` 15,00,000

Share Capital Reserves & Surplus

107

= ` 10,50,000 103

= ` 4,50,000

4. Profit and Loss Statement (to compute Operating Expenses as bal. figure)

Particulars Computation `

Sales Given 60,00,000 Less: Cost of Goods Sold Given 18,00,000 Gross Profit 42,00,000 Less: Operating Expenses (balancing figure) (i.e. Gross Profit less EBIT) 33,90,000 EBIT By reverse working (EBT + Interest) 8,10,000 Less: Interest on Debentures Given 60,000 EBT By reverse working (EAT + Tax) 7,50,000 Less: Tax at 50% Since Tax Rate = 50% on EBT, EAT = balance 50%. Hence, Tax = EAT 3,75,000 EAT = Net Profit after Tax = 6.25% on Sales of ` 60,00,000 3,75,000

5. Balance Sheet as on 31st March Particulars as at 31st March Note This Year Prev. Yr

I EQUITY AND LIABILITIES: (1) Shareholders’ Funds: Share Capital (WN 3) 10,50,000 Reserves and Surplus (WN 3) 4,50,000 (2)

Non–Current Liabilities 15% Debentures%1500060, `

4,00,000

(3) Current Liabilities: Trade Payables, i.e. Creditors (given) 2,00,000 Total 21,00,000 II ASSETS (1) Non–Current Assets Fixed Assets (balancing figure) 17,00,000 (2) Current Assets: (a) Inventories (WN 1) 1,50,000 (b) Trade Receivables Debtors (given) 2,00,000 (c) Cash and Cash Equivalents (WN 2) 50,000 Total 21,00,000 Question 3(a): Operating Costing 8 Marks A Mini–Bus, having a capacity of 32 Passengers, operates between two places – ‘A’ and ‘B’. The distance between the Place ‘A’ and Place ‘B’ is 30 km. The Bus makes 10 round trips in a day for 25 days in a month. On an average, the Occupancy Ratio is 70% and is expected throughout the year. The details of other expenses are as under: Amount in ` Insurance 15,600 per annum Garage Rent 2,400 per quarter Road Tax 5,000 per annum Repairs 4,800 per quarter Salary of Operating Staff 7,200 per month

sandy

Typewriter

Get CA CMA CS Updates and More From Caultimates.com

sandy

Typewriter

sandy

Typewriter

Gurukripa’s Guideline Answers for May 2015 CA Inter (IPC) Cost Accounting & Financial Management Exam

May 2015.6

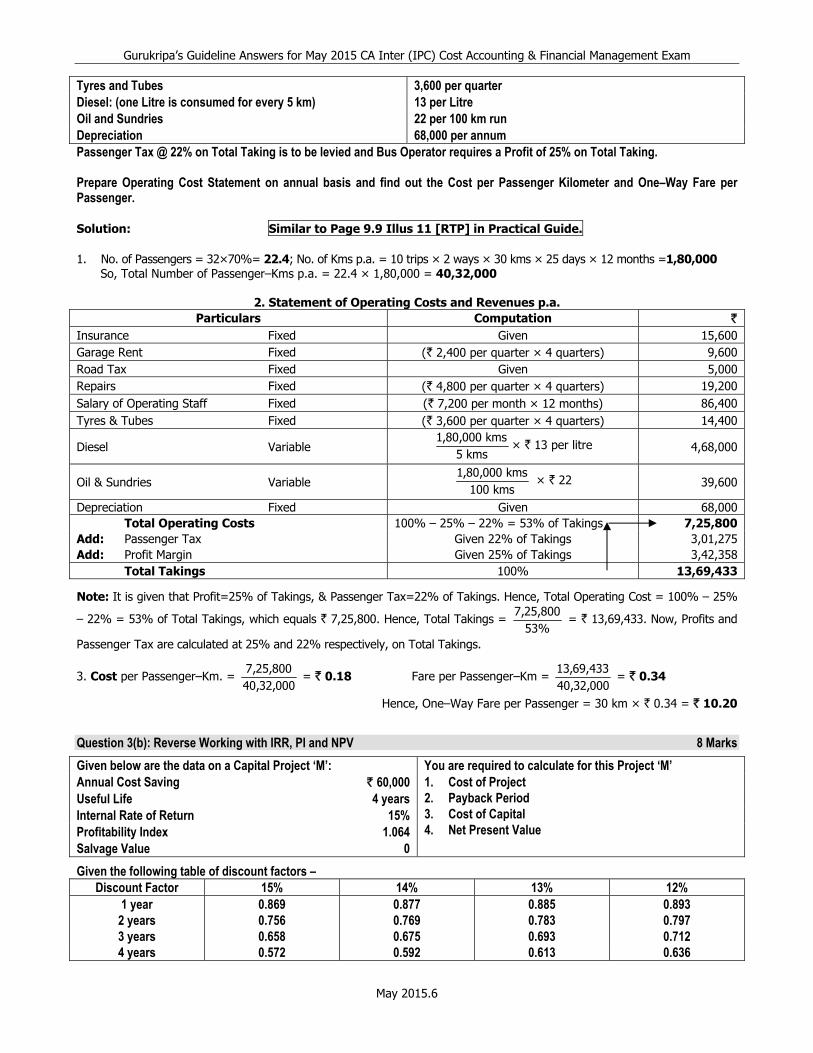

Tyres and Tubes 3,600 per quarter Diesel: (one Litre is consumed for every 5 km) 13 per Litre Oil and Sundries 22 per 100 km run Depreciation 68,000 per annum Passenger Tax @ 22% on Total Taking is to be levied and Bus Operator requires a Profit of 25% on Total Taking. Prepare Operating Cost Statement on annual basis and find out the Cost per Passenger Kilometer and One–Way Fare per Passenger. Solution: Similar to Page 9.9 Illus 11 [RTP] in Practical Guide. 1. No. of Passengers = 32×70%= 22.4; No. of Kms p.a. = 10 trips × 2 ways × 30 kms × 25 days × 12 months =1,80,000

So, Total Number of Passenger–Kms p.a. = 22.4 × 1,80,000 = 40,32,000

2. Statement of Operating Costs and Revenues p.a. Particulars Computation `

Insurance Fixed Given 15,600 Garage Rent Fixed (` 2,400 per quarter × 4 quarters) 9,600 Road Tax Fixed Given 5,000 Repairs Fixed (` 4,800 per quarter × 4 quarters) 19,200 Salary of Operating Staff Fixed (` 7,200 per month × 12 months) 86,400 Tyres & Tubes Fixed (` 3,600 per quarter × 4 quarters) 14,400

Diesel Variable kms5kms000,80,1

× ` 13 per litre 4,68,000

Oil & Sundries Variable kms100kms000,80,1

× ` 22 39,600

Depreciation Fixed Given 68,000 Total Operating Costs 100% – 25% – 22% = 53% of Takings 7,25,800Add: Passenger Tax Given 22% of Takings 3,01,275 Add: Profit Margin Given 25% of Takings 3,42,358 Total Takings 100% 13,69,433

Note: It is given that Profit=25% of Takings, & Passenger Tax=22% of Takings. Hence, Total Operating Cost = 100% – 25%

– 22% = 53% of Total Takings, which equals ` 7,25,800. Hence, Total Takings = %53800,25,7

= ` 13,69,433. Now, Profits and

Passenger Tax are calculated at 25% and 22% respectively, on Total Takings.

3. Cost per Passenger–Km. = 000,32,40800,25,7

= ` 0.18 Fare per Passenger–Km = 000,32,40433,69,13

= ` 0.34

Hence, One–Way Fare per Passenger = 30 km × ` 0.34 = ` 10.20 Question 3(b): Reverse Working with IRR, PI and NPV 8 Marks

Given below are the data on a Capital Project ‘M’: You are required to calculate for this Project ‘M’ Annual Cost Saving ` 60,000 1. Cost of Project

2. Payback Period 3. Cost of Capital 4. Net Present Value

Useful Life 4 years Internal Rate of Return 15% Profitability Index 1.064 Salvage Value 0

Given the following table of discount factors – Discount Factor 15% 14% 13% 12%

1 year 0.869 0.877 0.885 0.893 2 years 0.756 0.769 0.783 0.797 3 years 0.658 0.675 0.693 0.712 4 years 0.572 0.592 0.613 0.636

sandy

Typewriter

Get CA CMA CS Updates and More From Caultimates.com

sandy

Typewriter

sandy

Typewriter

Gurukripa’s Guideline Answers for May 2015 CA Inter (IPC) Cost Accounting & Financial Management Exam

May 2015.7

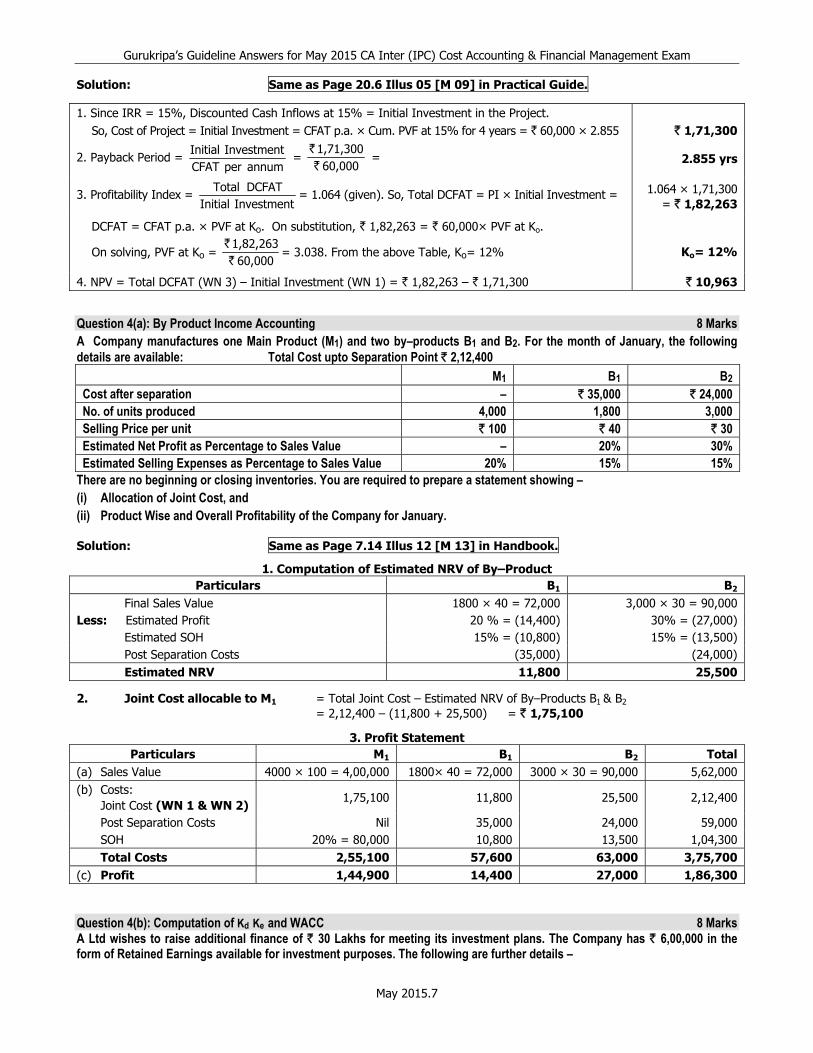

Solution: Same as Page 20.6 Illus 05 [M 09] in Practical Guide.

1. Since IRR = 15%, Discounted Cash Inflows at 15% = Initial Investment in the Project. So, Cost of Project = Initial Investment = CFAT p.a. × Cum. PVF at 15% for 4 years = ` 60,000 × 2.855 ` 1,71,300

2. Payback Period = annumperCFAT

InvestmentInitial =

60,0001,71,300 `

` = 2.855 yrs

3. Profitability Index = InvestmentInitial

DCFATTotal= 1.064 (given). So, Total DCFAT = PI × Initial Investment = 1.064 × 1,71,300

= ` 1,82,263

DCFAT = CFAT p.a. × PVF at Ko. On substitution, ` 1,82,263 = ` 60,000× PVF at Ko.

On solving, PVF at Ko = 60,000

1,82,263 `

`= 3.038. From the above Table, Ko= 12%

Ko= 12%

4. NPV = Total DCFAT (WN 3) – Initial Investment (WN 1) = ` 1,82,263 – ` 1,71,300 ` 10,963 Question 4(a): By Product Income Accounting 8 Marks A Company manufactures one Main Product (M1) and two by–products B1 and B2. For the month of January, the following details are available: Total Cost upto Separation Point ` 2,12,400 M1 B1 B2 Cost after separation – ` 35,000 ` 24,000 No. of units produced 4,000 1,800 3,000 Selling Price per unit ` 100 ` 40 ` 30 Estimated Net Profit as Percentage to Sales Value – 20% 30% Estimated Selling Expenses as Percentage to Sales Value 20% 15% 15%

There are no beginning or closing inventories. You are required to prepare a statement showing – (i) Allocation of Joint Cost, and (ii) Product Wise and Overall Profitability of the Company for January. Solution: Same as Page 7.14 Illus 12 [M 13] in Handbook.

1. Computation of Estimated NRV of By–Product Particulars B1 B2

Final Sales Value 1800 × 40 = 72,000 3,000 × 30 = 90,000Less: Estimated Profit 20 % = (14,400) 30% = (27,000)

Estimated SOH 15% = (10,800) 15% = (13,500)Post Separation Costs (35,000) (24,000)Estimated NRV 11,800 25,500

2. Joint Cost allocable to M1 = Total Joint Cost – Estimated NRV of By–Products B1 & B2 = 2,12,400 – (11,800 + 25,500) = ` 1,75,100

3. Profit Statement Particulars M1 B1 B2 Total

(a) Sales Value 4000 × 100 = 4,00,000 1800× 40 = 72,000 3000 × 30 = 90,000 5,62,000(b) Costs:

Joint Cost (WN 1 & WN 2) 1,75,100 11,800 25,500 2,12,400

Post Separation Costs Nil 35,000 24,000 59,000SOH 20% = 80,000 10,800 13,500 1,04,300Total Costs 2,55,100 57,600 63,000 3,75,700

(c) Profit 1,44,900 14,400 27,000 1,86,300 Question 4(b): Computation of Kd Ke and WACC 8 Marks A Ltd wishes to raise additional finance of ` 30 Lakhs for meeting its investment plans. The Company has ` 6,00,000 in the form of Retained Earnings available for investment purposes. The following are further details –

sandy

Typewriter

Get CA CMA CS Updates and More From Caultimates.com

sandy

Typewriter

sandy

Typewriter

sandy

Typewriter

Gurukripa’s Guideline Answers for May 2015 CA Inter (IPC) Cost Accounting & Financial Management Exam

May 2015.8

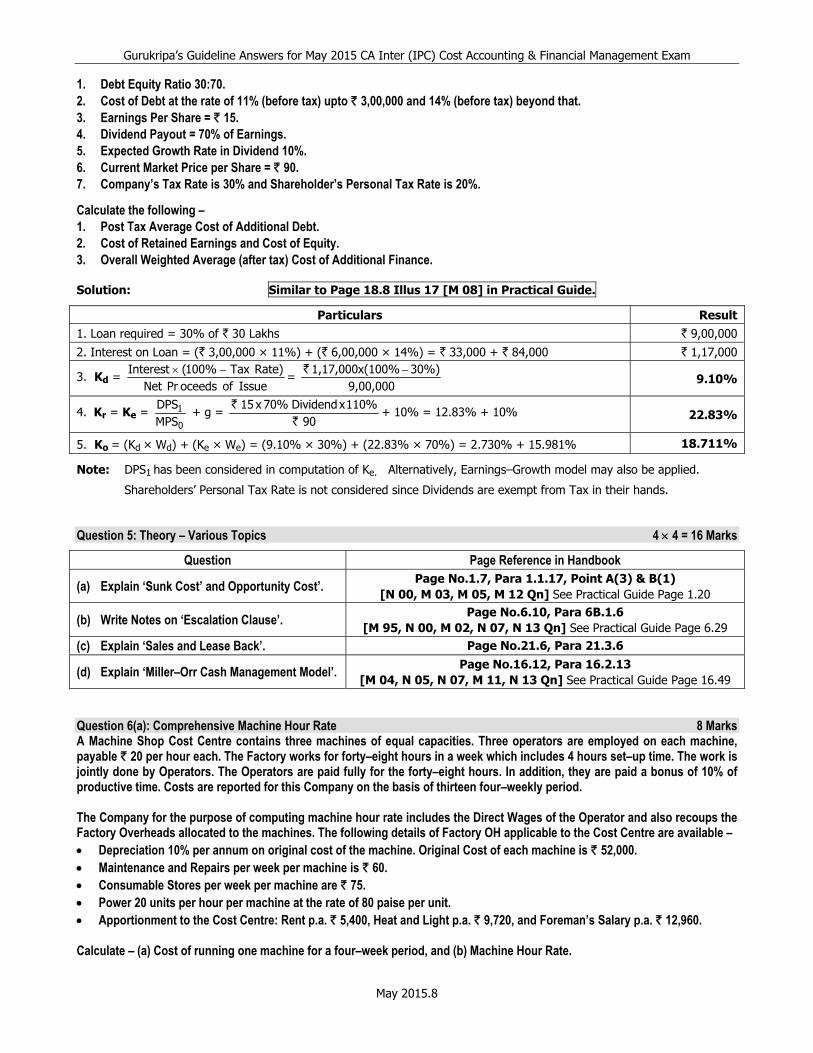

1. Debt Equity Ratio 30:70. 2. Cost of Debt at the rate of 11% (before tax) upto ` 3,00,000 and 14% (before tax) beyond that. 3. Earnings Per Share = ` 15. 4. Dividend Payout = 70% of Earnings. 5. Expected Growth Rate in Dividend 10%. 6. Current Market Price per Share = ` 90. 7. Company’s Tax Rate is 30% and Shareholder’s Personal Tax Rate is 20%. Calculate the following – 1. Post Tax Average Cost of Additional Debt. 2. Cost of Retained Earnings and Cost of Equity. 3. Overall Weighted Average (after tax) Cost of Additional Finance. Solution: Similar to Page 18.8 Illus 17 [M 08] in Practical Guide.

Particulars Result1. Loan required = 30% of ` 30 Lakhs ` 9,00,000

2. Interest on Loan = (` 3,00,000 × 11%) + (` 6,00,000 × 14%) = ` 33,000 + ` 84,000 ` 1,17,000

3. Kd = IssueofoceedsPrNet

)RateTax%100(Interest −×=

9,00,00030%)100%1,17,000x( −`

9.10%

4. Kr = Ke = 0

1MPSDPS

+ g = 90

%110xDividend%70x15`

`+ 10% = 12.83% + 10% 22.83%

5. Ko = (Kd × Wd) + (Ke × We) = (9.10% × 30%) + (22.83% × 70%) = 2.730% + 15.981% 18.711%

Note: DPS1 has been considered in computation of Ke. Alternatively, Earnings–Growth model may also be applied.

Shareholders’ Personal Tax Rate is not considered since Dividends are exempt from Tax in their hands. Question 5: Theory – Various Topics 4 × 4 = 16 Marks

Question Page Reference in Handbook

(a) Explain ‘Sunk Cost’ and Opportunity Cost’. Page No.1.7, Para 1.1.17, Point A(3) & B(1) [N 00, M 03, M 05, M 12 Qn] See Practical Guide Page 1.20

(b) Write Notes on ‘Escalation Clause’. Page No.6.10, Para 6B.1.6 [M 95, N 00, M 02, N 07, N 13 Qn] See Practical Guide Page 6.29

(c) Explain ‘Sales and Lease Back’. Page No.21.6, Para 21.3.6

(d) Explain ‘Miller–Orr Cash Management Model’. Page No.16.12, Para 16.2.13 [M 04, N 05, N 07, M 11, N 13 Qn] See Practical Guide Page 16.49

Question 6(a): Comprehensive Machine Hour Rate 8 Marks A Machine Shop Cost Centre contains three machines of equal capacities. Three operators are employed on each machine, payable ` 20 per hour each. The Factory works for forty–eight hours in a week which includes 4 hours set–up time. The work is jointly done by Operators. The Operators are paid fully for the forty–eight hours. In addition, they are paid a bonus of 10% of productive time. Costs are reported for this Company on the basis of thirteen four–weekly period. The Company for the purpose of computing machine hour rate includes the Direct Wages of the Operator and also recoups the Factory Overheads allocated to the machines. The following details of Factory OH applicable to the Cost Centre are available – • Depreciation 10% per annum on original cost of the machine. Original Cost of each machine is ` 52,000. • Maintenance and Repairs per week per machine is ` 60. • Consumable Stores per week per machine are ` 75. • Power 20 units per hour per machine at the rate of 80 paise per unit. • Apportionment to the Cost Centre: Rent p.a. ` 5,400, Heat and Light p.a. ` 9,720, and Foreman’s Salary p.a. ` 12,960. Calculate – (a) Cost of running one machine for a four–week period, and (b) Machine Hour Rate.

sandy

Typewriter

Get CA CMA CS Updates and More From Caultimates.com

sandy

Typewriter

sandy

Typewriter

Gurukripa’s Guideline Answers for May 2015 CA Inter (IPC) Cost Accounting & Financial Management Exam

May 2015.9

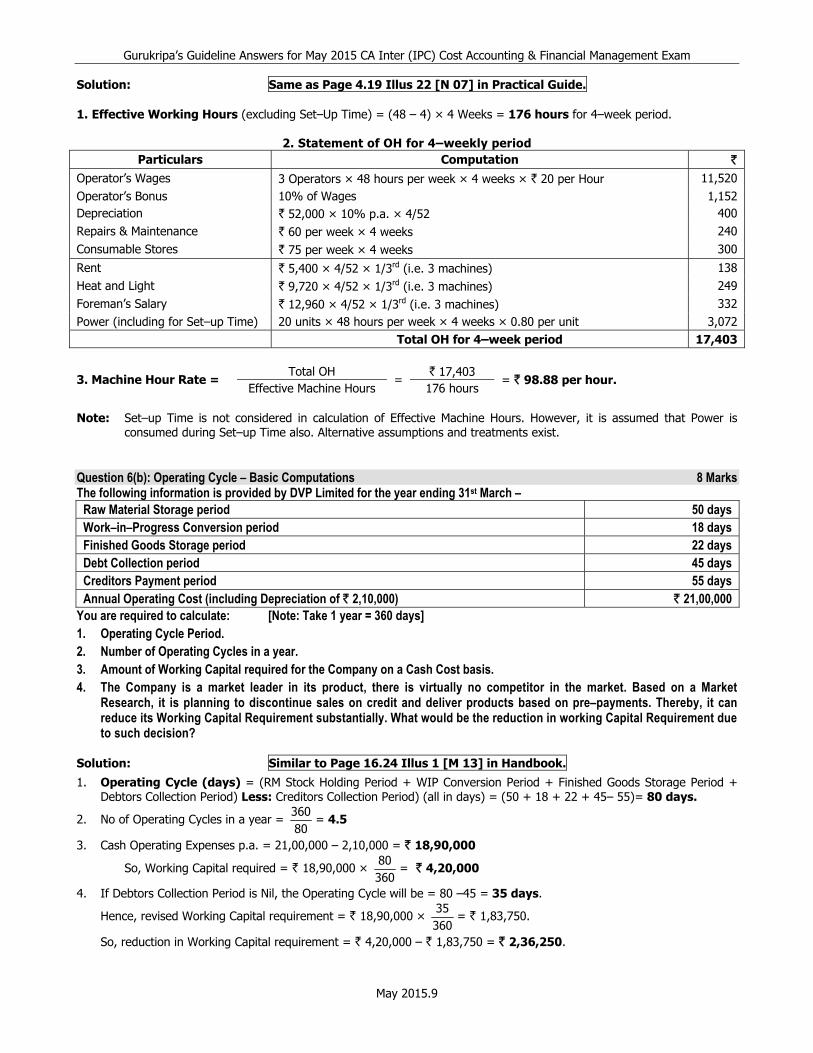

Solution: Same as Page 4.19 Illus 22 [N 07] in Practical Guide. 1. Effective Working Hours (excluding Set–Up Time) = (48 – 4) × 4 Weeks = 176 hours for 4–week period.

2. Statement of OH for 4–weekly period Particulars Computation `

Operator’s Wages 3 Operators × 48 hours per week × 4 weeks × ` 20 per Hour 11,520 Operator’s Bonus 10% of Wages 1,152 Depreciation ` 52,000 × 10% p.a. × 4/52 400 Repairs & Maintenance ` 60 per week × 4 weeks 240 Consumable Stores ` 75 per week × 4 weeks 300

Rent ` 5,400 × 4/52 × 1/3rd (i.e. 3 machines) 138 Heat and Light ` 9,720 × 4/52 × 1/3rd (i.e. 3 machines) 249 Foreman’s Salary ` 12,960 × 4/52 × 1/3rd (i.e. 3 machines) 332 Power (including for Set–up Time) 20 units × 48 hours per week × 4 weeks × 0.80 per unit 3,072 Total OH for 4–week period 17,403

3. Machine Hour Rate = Total OH

= ` 17,403

= ` 98.88 per hour. Effective Machine Hours 176 hours

Note: Set–up Time is not considered in calculation of Effective Machine Hours. However, it is assumed that Power is

consumed during Set–up Time also. Alternative assumptions and treatments exist. Question 6(b): Operating Cycle – Basic Computations 8 Marks The following information is provided by DVP Limited for the year ending 31st March –

Raw Material Storage period 50 days Work–in–Progress Conversion period 18 days Finished Goods Storage period 22 days Debt Collection period 45 days Creditors Payment period 55 days Annual Operating Cost (including Depreciation of ` 2,10,000) ` 21,00,000

You are required to calculate: [Note: Take 1 year = 360 days] 1. Operating Cycle Period. 2. Number of Operating Cycles in a year. 3. Amount of Working Capital required for the Company on a Cash Cost basis. 4. The Company is a market leader in its product, there is virtually no competitor in the market. Based on a Market

Research, it is planning to discontinue sales on credit and deliver products based on pre–payments. Thereby, it can reduce its Working Capital Requirement substantially. What would be the reduction in working Capital Requirement due to such decision?

Solution: Similar to Page 16.24 Illus 1 [M 13] in Handbook.

1. Operating Cycle (days) = (RM Stock Holding Period + WIP Conversion Period + Finished Goods Storage Period + Debtors Collection Period) Less: Creditors Collection Period) (all in days) = (50 + 18 + 22 + 45– 55)= 80 days.

2. No of Operating Cycles in a year = 80360

= 4.5

3. Cash Operating Expenses p.a. = 21,00,000 – 2,10,000 = ` 18,90,000

So, Working Capital required = ` 18,90,000 × 36080

= ` 4,20,000

4. If Debtors Collection Period is Nil, the Operating Cycle will be = 80 –45 = 35 days.

Hence, revised Working Capital requirement = ` 18,90,000 × 36035

= ` 1,83,750.

So, reduction in Working Capital requirement = ` 4,20,000 – ` 1,83,750 = ` 2,36,250.

sandy

Typewriter

Get CA CMA CS Updates and More From Caultimates.com

sandy

Typewriter

sandy

Typewriter

Gurukripa’s Guideline Answers for May 2015 CA Inter (IPC) Cost Accounting & Financial Management Exam

May 2015.10

Question 7: Theory – Various Topics – Answer any four of the following 4 × 4 = 16 Marks

Question Page Reference in Handbook

(a) Define ‘Cost Centre’ and state its types. Page No.1.12, Para 1.3.3

[RTP, N 91, N 92, M 95, M 97, N 02, M 08, M 11 Qn] See Practical Guide Page 1.20

(b) State benefits of Integrated Accounting. Page No.5.3, Para 5.2.2

[N 91, N 97, M 02, M 07, M 10, M 12 Qn] See Practical Guide Page 5.30

(c) Differentiate between ‘Factoring and ‘Bill Discounting’. Page No.16.23, Para 16.4.7 [N 09, M 13 Qn] See Practical Guide Page 16.49

(d) Discuss the Conflicts in Profit versus Wealth Maximization Principle of the Firm.

Page No.13.5, Para 13.2.4 [N 06, N 07, M 09, N 10, N 12 Qn]

See Practical Guide Page 13.20

(e) Define ‘Present Value’ and ‘Perpetuity’. Page No.19.7, Para 19.3.1 and

Page No.19.10, Para 19.3.3 [RTP Qn] See Practical Guide Page 19.6

Gurukripa’s Guideline Answers for May 2015 CA Inter (IPC) Cost Accounting & Financial Management Exam

May 2015.11

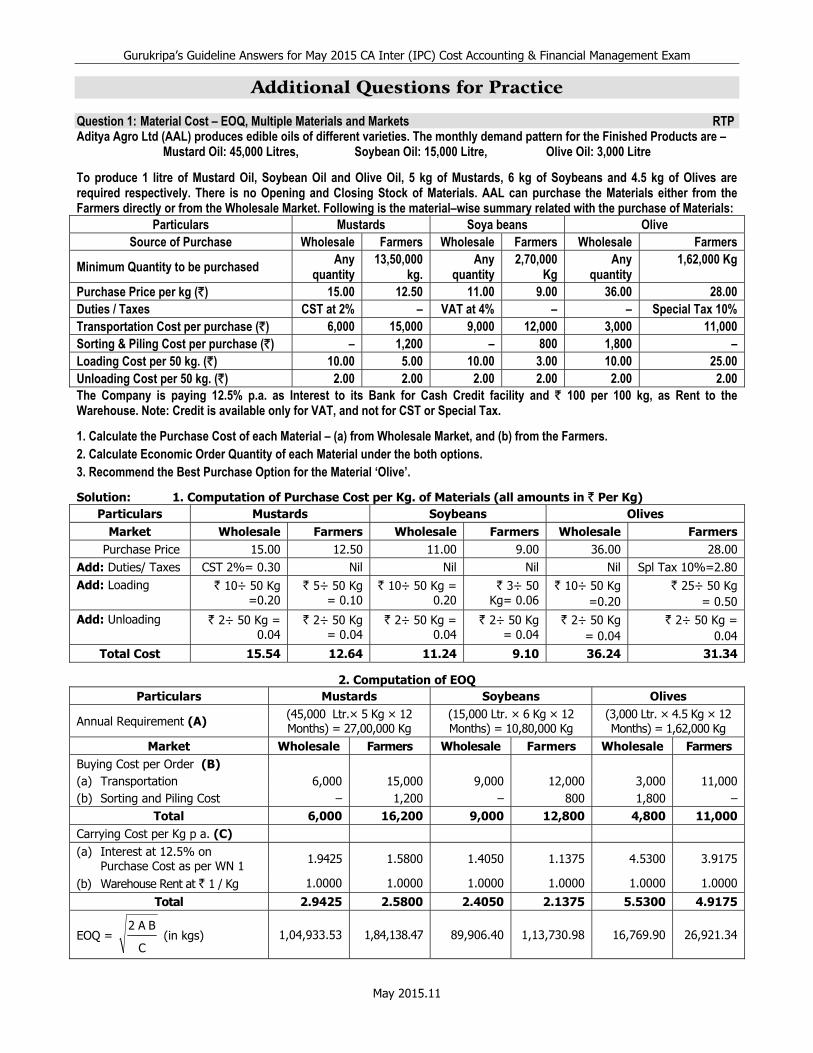

Additional Questions for Practice Question 1: Material Cost – EOQ, Multiple Materials and Markets RTP Aditya Agro Ltd (AAL) produces edible oils of different varieties. The monthly demand pattern for the Finished Products are –

Mustard Oil: 45,000 Litres, Soybean Oil: 15,000 Litre, Olive Oil: 3,000 Litre To produce 1 litre of Mustard Oil, Soybean Oil and Olive Oil, 5 kg of Mustards, 6 kg of Soybeans and 4.5 kg of Olives are required respectively. There is no Opening and Closing Stock of Materials. AAL can purchase the Materials either from the Farmers directly or from the Wholesale Market. Following is the material–wise summary related with the purchase of Materials:

Particulars Mustards Soya beans Olive Source of Purchase Wholesale Farmers Wholesale Farmers Wholesale Farmers

Minimum Quantity to be purchased Any quantity

13,50,000 kg.

Any quantity

2,70,000 Kg

Any quantity

1,62,000 Kg

Purchase Price per kg (`) 15.00 12.50 11.00 9.00 36.00 28.00 Duties / Taxes CST at 2% – VAT at 4% – – Special Tax 10% Transportation Cost per purchase (`) 6,000 15,000 9,000 12,000 3,000 11,000 Sorting & Piling Cost per purchase (`) – 1,200 – 800 1,800 – Loading Cost per 50 kg. (`) 10.00 5.00 10.00 3.00 10.00 25.00 Unloading Cost per 50 kg. (`) 2.00 2.00 2.00 2.00 2.00 2.00 The Company is paying 12.5% p.a. as Interest to its Bank for Cash Credit facility and ` 100 per 100 kg, as Rent to the Warehouse. Note: Credit is available only for VAT, and not for CST or Special Tax.

1. Calculate the Purchase Cost of each Material – (a) from Wholesale Market, and (b) from the Farmers. 2. Calculate Economic Order Quantity of each Material under the both options. 3. Recommend the Best Purchase Option for the Material ‘Olive’.

Solution: 1. Computation of Purchase Cost per Kg. of Materials (all amounts in ` Per Kg) Particulars Mustards Soybeans Olives

Market Wholesale Farmers Wholesale Farmers Wholesale Farmers Purchase Price 15.00 12.50 11.00 9.00 36.00 28.00 Add: Duties/ Taxes CST 2%= 0.30 Nil Nil Nil Nil Spl Tax 10%=2.80 Add: Loading ` 10÷ 50 Kg

=0.20 ` 5÷ 50 Kg

= 0.10 ` 10÷ 50 Kg =

0.20 ` 3÷ 50

Kg= 0.06 ` 10÷ 50 Kg

=0.20 ` 25÷ 50 Kg

= 0.50 Add: Unloading ` 2÷ 50 Kg =

0.04 ` 2÷ 50 Kg

= 0.04 ` 2÷ 50 Kg =

0.04 ` 2÷ 50 Kg

= 0.04 ` 2÷ 50 Kg

= 0.04 ` 2÷ 50 Kg =

0.04 Total Cost 15.54 12.64 11.24 9.10 36.24 31.34

2. Computation of EOQ Particulars Mustards Soybeans Olives

Annual Requirement (A) (45,000 Ltr.× 5 Kg × 12 Months) = 27,00,000 Kg

(15,000 Ltr. × 6 Kg × 12 Months) = 10,80,000 Kg

(3,000 Ltr. × 4.5 Kg × 12 Months) = 1,62,000 Kg

Market Wholesale Farmers Wholesale Farmers Wholesale Farmers Buying Cost per Order (B) (a) Transportation 6,000 15,000 9,000 12,000 3,000 11,000 (b) Sorting and Piling Cost – 1,200 – 800 1,800 –

Total 6,000 16,200 9,000 12,800 4,800 11,000Carrying Cost per Kg p a. (C) (a) Interest at 12.5% on

Purchase Cost as per WN 1 1.9425 1.5800 1.4050 1.1375 4.5300 3.9175

(b) Warehouse Rent at ` 1 / Kg 1.0000 1.0000 1.0000 1.0000 1.0000 1.0000

Total 2.9425 2.5800 2.4050 2.1375 5.5300 4.9175

EOQ = C

BA2 (in kgs) 1,04,933.53 1,84,138.47 89,906.40 1,13,730.98 16,769.90 26,921.34

sandy

Typewriter

Get CA CMA CS Updates and More From Caultimates.com

sandy

Typewriter

sandy

Typewriter

Gurukripa’s Guideline Answers for May 2015 CA Inter (IPC) Cost Accounting & Financial Management Exam

May 2015.12

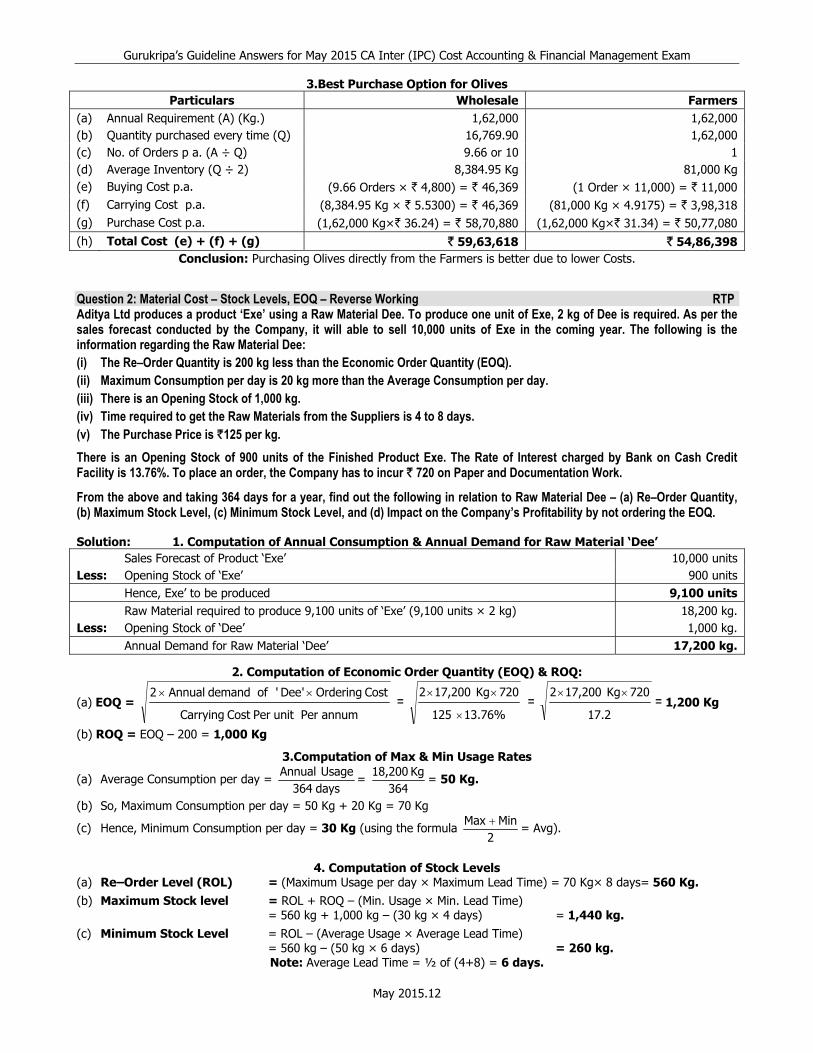

3.Best Purchase Option for Olives Particulars Wholesale Farmers

(a) Annual Requirement (A) (Kg.) 1,62,000 1,62,000 (b) Quantity purchased every time (Q) 16,769.90 1,62,000 (c) No. of Orders p a. (A ÷ Q) 9.66 or 10 1 (d) Average Inventory (Q ÷ 2) 8,384.95 Kg 81,000 Kg (e) Buying Cost p.a. (9.66 Orders × ` 4,800) = ` 46,369 (1 Order × 11,000) = ` 11,000 (f) Carrying Cost p.a. (8,384.95 Kg × ` 5.5300) = ` 46,369 (81,000 Kg × 4.9175) = ` 3,98,318 (g) Purchase Cost p.a. (1,62,000 Kg×` 36.24) = ` 58,70,880 (1,62,000 Kg×` 31.34) = ` 50,77,080 (h) Total Cost (e) + (f) + (g) ` 59,63,618 ` 54,86,398

Conclusion: Purchasing Olives directly from the Farmers is better due to lower Costs. Question 2: Material Cost – Stock Levels, EOQ – Reverse Working RTP Aditya Ltd produces a product ‘Exe’ using a Raw Material Dee. To produce one unit of Exe, 2 kg of Dee is required. As per the sales forecast conducted by the Company, it will able to sell 10,000 units of Exe in the coming year. The following is the information regarding the Raw Material Dee: (i) The Re–Order Quantity is 200 kg less than the Economic Order Quantity (EOQ). (ii) Maximum Consumption per day is 20 kg more than the Average Consumption per day. (iii) There is an Opening Stock of 1,000 kg. (iv) Time required to get the Raw Materials from the Suppliers is 4 to 8 days. (v) The Purchase Price is `125 per kg.

There is an Opening Stock of 900 units of the Finished Product Exe. The Rate of Interest charged by Bank on Cash Credit Facility is 13.76%. To place an order, the Company has to incur ` 720 on Paper and Documentation Work.

From the above and taking 364 days for a year, find out the following in relation to Raw Material Dee – (a) Re–Order Quantity, (b) Maximum Stock Level, (c) Minimum Stock Level, and (d) Impact on the Company’s Profitability by not ordering the EOQ. Solution: 1. Computation of Annual Consumption & Annual Demand for Raw Material ‘Dee’ Sales Forecast of Product ‘Exe’ 10,000 units Less: Opening Stock of ‘Exe’ 900 units Hence, Exe’ to be produced 9,100 units Raw Material required to produce 9,100 units of ‘Exe’ (9,100 units × 2 kg) 18,200 kg. Less: Opening Stock of ‘Dee’ 1,000 kg. Annual Demand for Raw Material ‘Dee’ 17,200 kg.

2. Computation of Economic Order Quantity (EOQ) & ROQ:

(a) EOQ = annumPernituPerCostCarrying

CostOrdering'Dee'ofemanddAnnual2 ×× = 13.76% 125

720Kg 17,2002

×

×× =

17.2

720Kg 17,2002 ××= 1,200 Kg

(b) ROQ = EOQ – 200 = 1,000 Kg

3.Computation of Max & Min Usage Rates

(a) Average Consumption per day = days 364Usage Annual

= 364

Kg 18,200= 50 Kg.

(b) So, Maximum Consumption per day = 50 Kg + 20 Kg = 70 Kg

(c) Hence, Minimum Consumption per day = 30 Kg (using the formula 2

Min Max += Avg).

4. Computation of Stock Levels

(a) Re–Order Level (ROL) = (Maximum Usage per day × Maximum Lead Time) = 70 Kg× 8 days= 560 Kg. (b) Maximum Stock level = ROL + ROQ – (Min. Usage × Min. Lead Time)

= 560 kg + 1,000 kg – (30 kg × 4 days) = 1,440 kg. (c) Minimum Stock Level = ROL – (Average Usage × Average Lead Time)

= 560 kg – (50 kg × 6 days) = 260 kg. Note: Average Lead Time = ½ of (4+8) = 6 days.

sandy

Typewriter

Get CA CMA CS Updates and More From Caultimates.com

sandy

Typewriter

sandy

Typewriter

Gurukripa’s Guideline Answers for May 2015 CA Inter (IPC) Cost Accounting & Financial Management Exam

May 2015.13

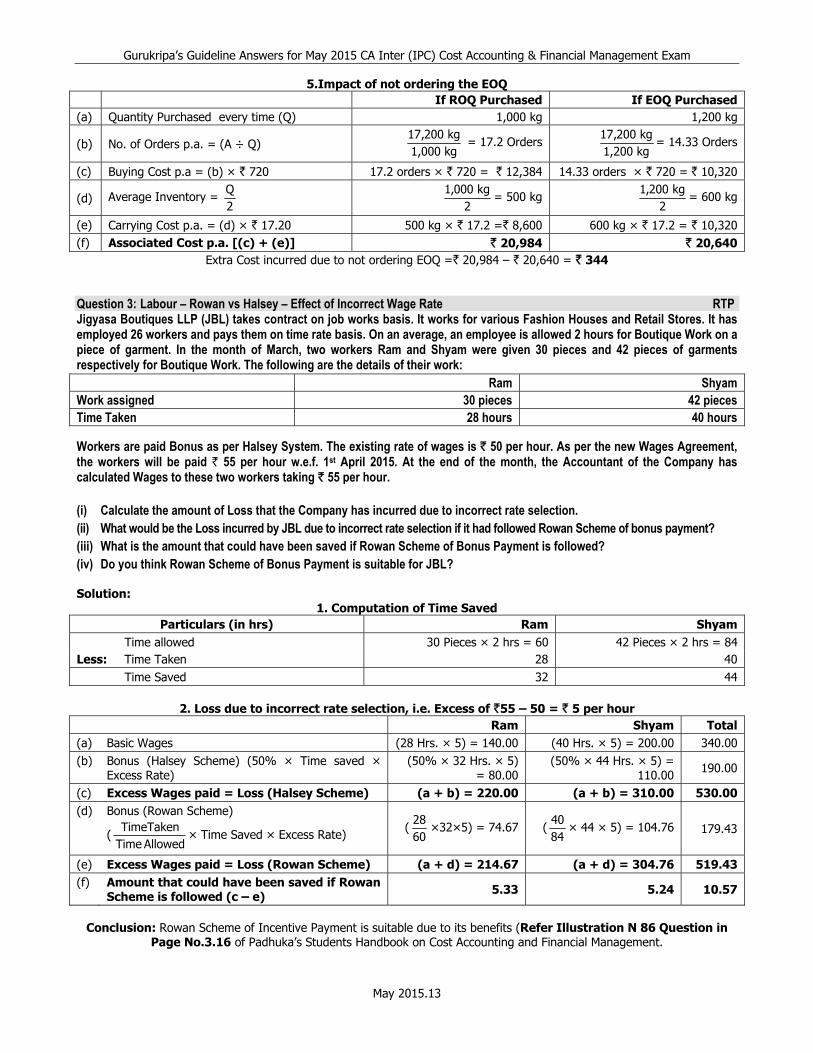

5.Impact of not ordering the EOQ If ROQ Purchased If EOQ Purchased

(a) Quantity Purchased every time (Q) 1,000 kg 1,200 kg

(b) No. of Orders p.a. = (A ÷ Q) kg1,000kg200,17

= 17.2 Orders kg1,200kg200,17

= 14.33 Orders

(c) Buying Cost p.a = (b) × ` 720 17.2 orders × ` 720 = ` 12,384 14.33 orders × ` 720 = ` 10,320

(d) Average Inventory = 2Q

2

kg000,1= 500 kg

2kg200,1

= 600 kg

(e) Carrying Cost p.a. = (d) × ` 17.20 500 kg × ` 17.2 =` 8,600 600 kg × ` 17.2 = ` 10,320 (f) Associated Cost p.a. [(c) + (e)] ` 20,984 ` 20,640

Extra Cost incurred due to not ordering EOQ =` 20,984 – ` 20,640 = ` 344 Question 3: Labour – Rowan vs Halsey – Effect of Incorrect Wage Rate RTP Jigyasa Boutiques LLP (JBL) takes contract on job works basis. It works for various Fashion Houses and Retail Stores. It has employed 26 workers and pays them on time rate basis. On an average, an employee is allowed 2 hours for Boutique Work on a piece of garment. In the month of March, two workers Ram and Shyam were given 30 pieces and 42 pieces of garments respectively for Boutique Work. The following are the details of their work:

Ram Shyam Work assigned 30 pieces 42 pieces Time Taken 28 hours 40 hours Workers are paid Bonus as per Halsey System. The existing rate of wages is ` 50 per hour. As per the new Wages Agreement, the workers will be paid ` 55 per hour w.e.f. 1st April 2015. At the end of the month, the Accountant of the Company has calculated Wages to these two workers taking ` 55 per hour. (i) Calculate the amount of Loss that the Company has incurred due to incorrect rate selection. (ii) What would be the Loss incurred by JBL due to incorrect rate selection if it had followed Rowan Scheme of bonus payment? (iii) What is the amount that could have been saved if Rowan Scheme of Bonus Payment is followed? (iv) Do you think Rowan Scheme of Bonus Payment is suitable for JBL? Solution:

1. Computation of Time Saved Particulars (in hrs) Ram Shyam

Time allowed 30 Pieces × 2 hrs = 60 42 Pieces × 2 hrs = 84 Less: Time Taken 28 40 Time Saved 32 44

2. Loss due to incorrect rate selection, i.e. Excess of `55 – 50 = ` 5 per hour

Ram Shyam Total(a) Basic Wages (28 Hrs. × 5) = 140.00 (40 Hrs. × 5) = 200.00 340.00 (b) Bonus (Halsey Scheme) (50% × Time saved ×

Excess Rate) (50% × 32 Hrs. × 5)

= 80.00 (50% × 44 Hrs. × 5) =

110.00 190.00

(c) Excess Wages paid = Loss (Halsey Scheme) (a + b) = 220.00 (a + b) = 310.00 530.00(d) Bonus (Rowan Scheme)

(AllowedTime

TimeTaken× Time Saved × Excess Rate) (

6028

×32×5) = 74.67 (8440

× 44 × 5) = 104.76 179.43

(e) Excess Wages paid = Loss (Rowan Scheme) (a + d) = 214.67 (a + d) = 304.76 519.43(f) Amount that could have been saved if Rowan

Scheme is followed (c – e) 5.33 5.24 10.57

Conclusion: Rowan Scheme of Incentive Payment is suitable due to its benefits (Refer Illustration N 86 Question in

Page No.3.16 of Padhuka’s Students Handbook on Cost Accounting and Financial Management.

sandy

Typewriter

Get CA CMA CS Updates and More From Caultimates.com

sandy

Typewriter

sandy

Typewriter

Gurukripa’s Guideline Answers for May 2015 CA Inter (IPC) Cost Accounting & Financial Management Exam

May 2015.14

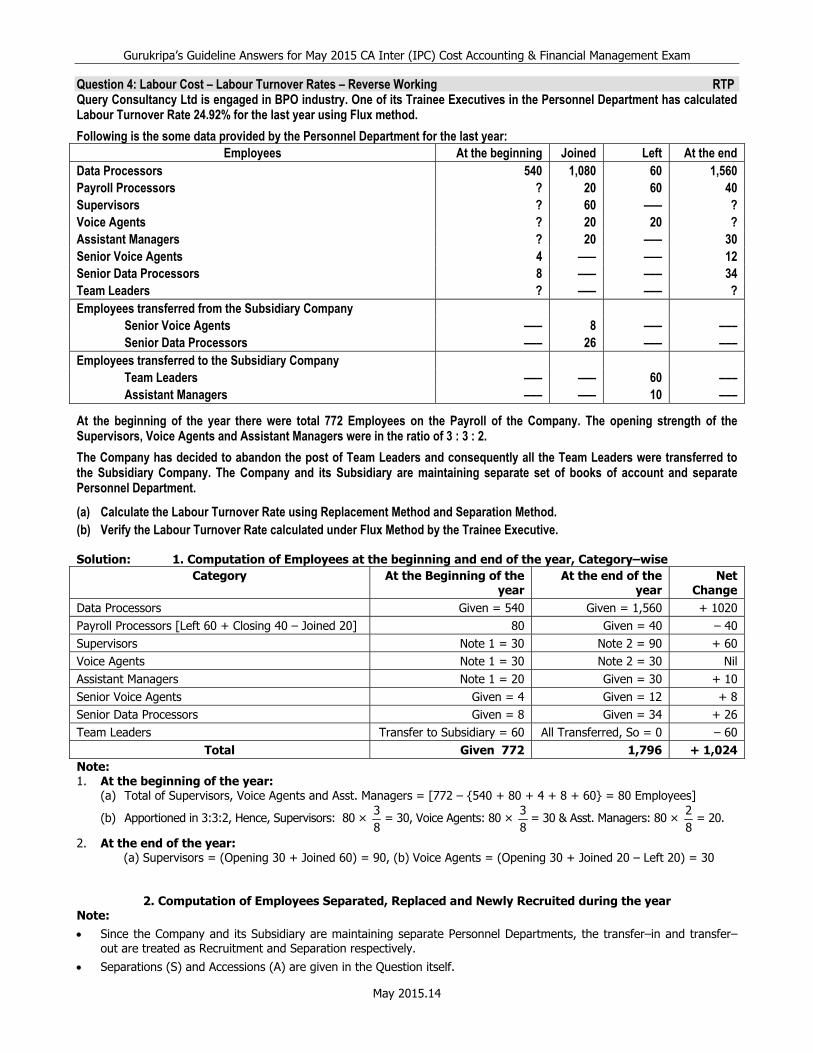

Question 4: Labour Cost – Labour Turnover Rates – Reverse Working RTP Query Consultancy Ltd is engaged in BPO industry. One of its Trainee Executives in the Personnel Department has calculated Labour Turnover Rate 24.92% for the last year using Flux method.

Following is the some data provided by the Personnel Department for the last year: Employees At the beginning Joined Left At the end

Data Processors 540 1,080 60 1,560 Payroll Processors ? 20 60 40 Supervisors ? 60 ––– ? Voice Agents ? 20 20 ? Assistant Managers ? 20 ––– 30 Senior Voice Agents 4 ––– ––– 12 Senior Data Processors 8 ––– ––– 34 Team Leaders ? ––– ––– ? Employees transferred from the Subsidiary Company Senior Voice Agents ––– 8 ––– ––– Senior Data Processors ––– 26 ––– ––– Employees transferred to the Subsidiary Company Team Leaders ––– ––– 60 ––– Assistant Managers ––– ––– 10 –––

At the beginning of the year there were total 772 Employees on the Payroll of the Company. The opening strength of the Supervisors, Voice Agents and Assistant Managers were in the ratio of 3 : 3 : 2.

The Company has decided to abandon the post of Team Leaders and consequently all the Team Leaders were transferred to the Subsidiary Company. The Company and its Subsidiary are maintaining separate set of books of account and separate Personnel Department.

(a) Calculate the Labour Turnover Rate using Replacement Method and Separation Method. (b) Verify the Labour Turnover Rate calculated under Flux Method by the Trainee Executive. Solution: 1. Computation of Employees at the beginning and end of the year, Category–wise

Category At the Beginning of the year

At the end of the year

Net Change

Data Processors Given = 540 Given = 1,560 + 1020 Payroll Processors [Left 60 + Closing 40 – Joined 20] 80 Given = 40 – 40 Supervisors Note 1 = 30 Note 2 = 90 + 60 Voice Agents Note 1 = 30 Note 2 = 30 Nil Assistant Managers Note 1 = 20 Given = 30 + 10 Senior Voice Agents Given = 4 Given = 12 + 8 Senior Data Processors Given = 8 Given = 34 + 26 Team Leaders Transfer to Subsidiary = 60 All Transferred, So = 0 – 60

Total Given 772 1,796 + 1,024Note: 1. At the beginning of the year:

(a) Total of Supervisors, Voice Agents and Asst. Managers = [772 – {540 + 80 + 4 + 8 + 60} = 80 Employees]

(b) Apportioned in 3:3:2, Hence, Supervisors: 80 × 83

= 30, Voice Agents: 80 × 83

= 30 & Asst. Managers: 80 × 82

= 20.

2. At the end of the year: (a) Supervisors = (Opening 30 + Joined 60) = 90, (b) Voice Agents = (Opening 30 + Joined 20 – Left 20) = 30

2. Computation of Employees Separated, Replaced and Newly Recruited during the year Note: • Since the Company and its Subsidiary are maintaining separate Personnel Departments, the transfer–in and transfer–

out are treated as Recruitment and Separation respectively. • Separations (S) and Accessions (A) are given in the Question itself.

sandy

Typewriter

Get CA CMA CS Updates and More From Caultimates.com

sandy

Typewriter

sandy

Typewriter

Gurukripa’s Guideline Answers for May 2015 CA Inter (IPC) Cost Accounting & Financial Management Exam

May 2015.15

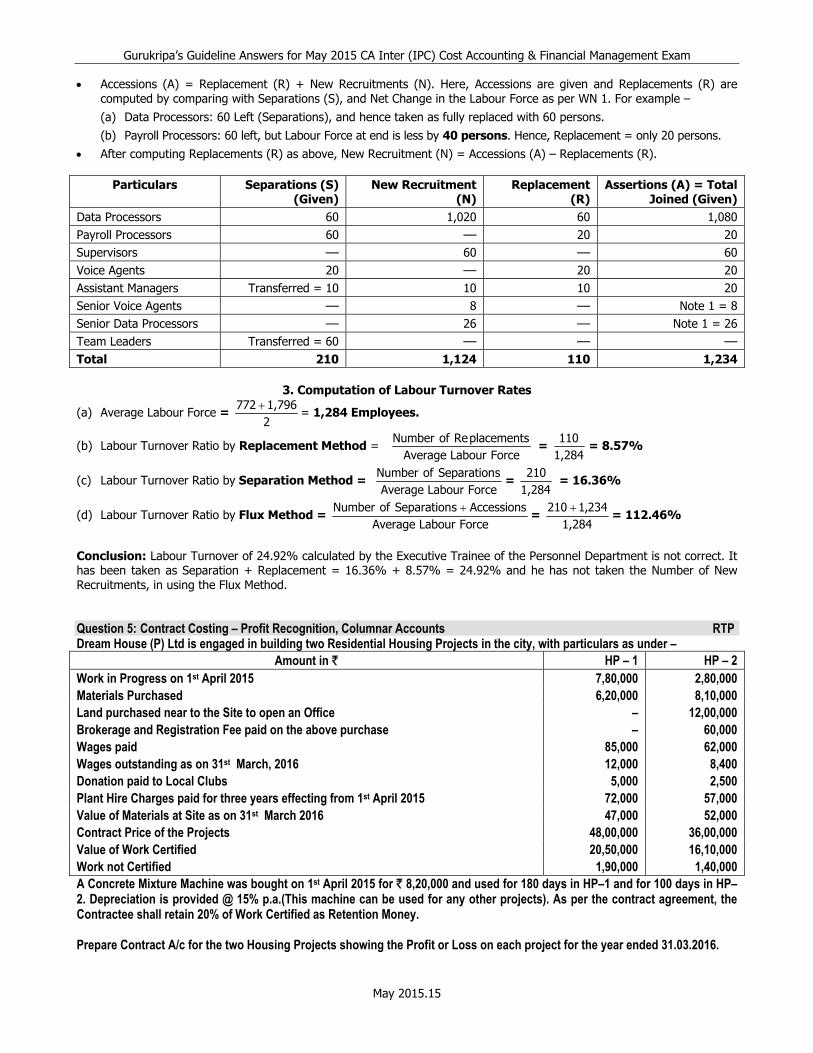

• Accessions (A) = Replacement (R) + New Recruitments (N). Here, Accessions are given and Replacements (R) are computed by comparing with Separations (S), and Net Change in the Labour Force as per WN 1. For example – (a) Data Processors: 60 Left (Separations), and hence taken as fully replaced with 60 persons. (b) Payroll Processors: 60 left, but Labour Force at end is less by 40 persons. Hence, Replacement = only 20 persons.

• After computing Replacements (R) as above, New Recruitment (N) = Accessions (A) – Replacements (R).

Particulars Separations (S) (Given)

New Recruitment (N)

Replacement (R)

Assertions (A) = Total Joined (Given)

Data Processors 60 1,020 60 1,080 Payroll Processors 60 –– 20 20Supervisors –– 60 –– 60 Voice Agents 20 –– 20 20 Assistant Managers Transferred = 10 10 10 20 Senior Voice Agents –– 8 –– Note 1 = 8 Senior Data Processors –– 26 –– Note 1 = 26 Team Leaders Transferred = 60 –– –– –– Total 210 1,124 110 1,234

3. Computation of Labour Turnover Rates

(a) Average Labour Force = 21,796772 +

= 1,284 Employees.

(b) Labour Turnover Ratio by Replacement Method = ForceLabourAverage

placementsReofNumber =

1,284110

= 8.57%

(c) Labour Turnover Ratio by Separation Method = ForceLabourAverage

sSeparationofNumber=

1,284210

= 16.36%

(d) Labour Turnover Ratio by Flux Method = ForceLabourAverage

AccessionssSeparationofNumber +=

1,284234,1210 +

= 112.46%

Conclusion: Labour Turnover of 24.92% calculated by the Executive Trainee of the Personnel Department is not correct. It has been taken as Separation + Replacement = 16.36% + 8.57% = 24.92% and he has not taken the Number of New Recruitments, in using the Flux Method. Question 5: Contract Costing – Profit Recognition, Columnar Accounts RTP Dream House (P) Ltd is engaged in building two Residential Housing Projects in the city, with particulars as under –

Amount in ` HP – 1 HP – 2 Work in Progress on 1st April 2015 7,80,000 2,80,000 Materials Purchased 6,20,000 8,10,000 Land purchased near to the Site to open an Office – 12,00,000 Brokerage and Registration Fee paid on the above purchase – 60,000 Wages paid 85,000 62,000 Wages outstanding as on 31st March, 2016 12,000 8,400 Donation paid to Local Clubs 5,000 2,500 Plant Hire Charges paid for three years effecting from 1st April 2015 72,000 57,000 Value of Materials at Site as on 31st March 2016 47,000 52,000 Contract Price of the Projects 48,00,000 36,00,000 Value of Work Certified 20,50,000 16,10,000 Work not Certified 1,90,000 1,40,000 A Concrete Mixture Machine was bought on 1st April 2015 for ` 8,20,000 and used for 180 days in HP–1 and for 100 days in HP–2. Depreciation is provided @ 15% p.a.(This machine can be used for any other projects). As per the contract agreement, the Contractee shall retain 20% of Work Certified as Retention Money. Prepare Contract A/c for the two Housing Projects showing the Profit or Loss on each project for the year ended 31.03.2016.

sandy

Typewriter

Get CA CMA CS Updates and More From Caultimates.com

sandy

Typewriter

sandy

Typewriter

Gurukripa’s Guideline Answers for May 2015 CA Inter (IPC) Cost Accounting & Financial Management Exam

May 2015.16

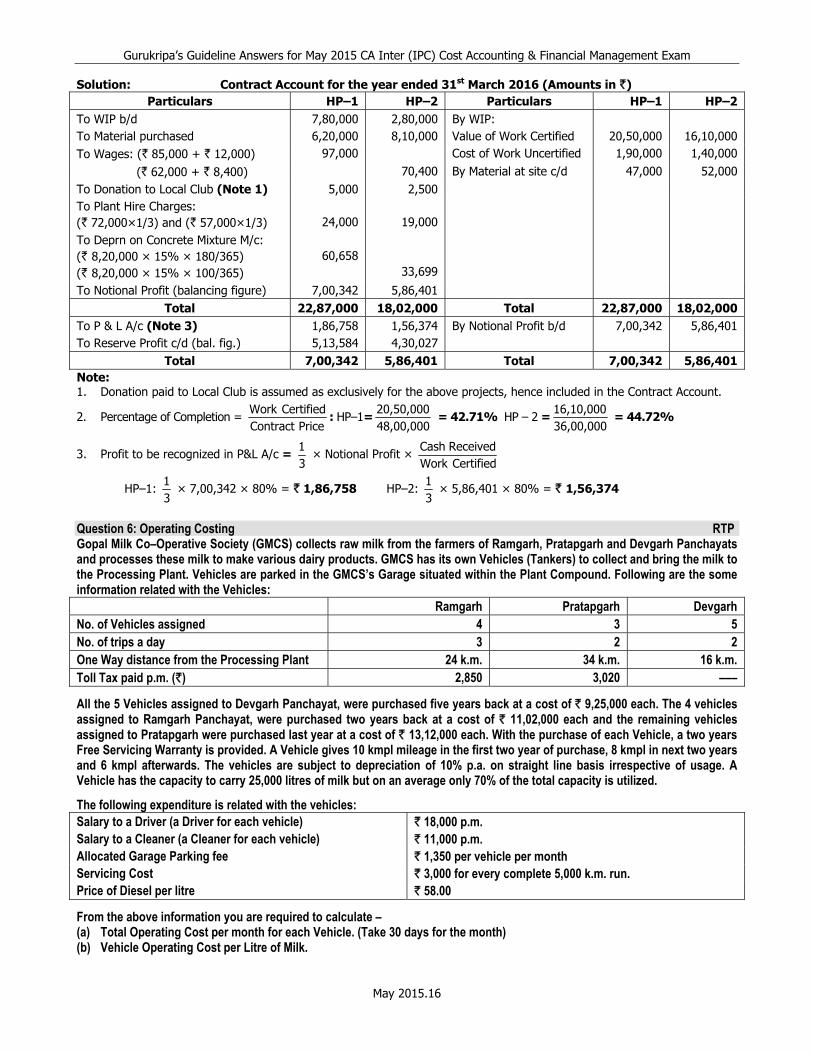

Solution: Contract Account for the year ended 31st March 2016 (Amounts in `) Particulars HP–1 HP–2 Particulars HP–1 HP–2

To WIP b/d 7,80,000 2,80,000 By WIP: To Material purchased 6,20,000 8,10,000 Value of Work Certified 20,50,000 16,10,000 To Wages: (` 85,000 + ` 12,000) 97,000 Cost of Work Uncertified 1,90,000 1,40,000

(` 62,000 + ` 8,400) 70,400 By Material at site c/d 47,000 52,000 To Donation to Local Club (Note 1) 5,000 2,500 To Plant Hire Charges: (` 72,000×1/3) and (` 57,000×1/3)

24,000

19,000

To Deprn on Concrete Mixture M/c: (` 8,20,000 × 15% × 180/365) (` 8,20,000 × 15% × 100/365)

60,658

33,699

To Notional Profit (balancing figure) 7,00,342 5,86,401 Total 22,87,000 18,02,000 Total 22,87,000 18,02,000

To P & L A/c (Note 3) 1,86,758 1,56,374 By Notional Profit b/d 7,00,342 5,86,401 To Reserve Profit c/d (bal. fig.) 5,13,584 4,30,027

Total 7,00,342 5,86,401 Total 7,00,342 5,86,401Note: 1. Donation paid to Local Club is assumed as exclusively for the above projects, hence included in the Contract Account.

2. Percentage of Completion = PriceContract

CertifiedWork: HP–1=

48,00,00020,50,000

= 42.71% HP – 2 =36,00,00016,10,000

= 44.72%

3. Profit to be recognized in P&L A/c = 31

× Notional Profit × CertifiedWorkReceivedCash

HP–1: 31

× 7,00,342 × 80% = ` 1,86,758 HP–2: 31

× 5,86,401 × 80% = ` 1,56,374

Question 6: Operating Costing RTP Gopal Milk Co–Operative Society (GMCS) collects raw milk from the farmers of Ramgarh, Pratapgarh and Devgarh Panchayats and processes these milk to make various dairy products. GMCS has its own Vehicles (Tankers) to collect and bring the milk to the Processing Plant. Vehicles are parked in the GMCS’s Garage situated within the Plant Compound. Following are the some information related with the Vehicles:

Ramgarh Pratapgarh Devgarh No. of Vehicles assigned 4 3 5 No. of trips a day 3 2 2 One Way distance from the Processing Plant 24 k.m. 34 k.m. 16 k.m. Toll Tax paid p.m. (`) 2,850 3,020 –––

All the 5 Vehicles assigned to Devgarh Panchayat, were purchased five years back at a cost of ` 9,25,000 each. The 4 vehicles assigned to Ramgarh Panchayat, were purchased two years back at a cost of ` 11,02,000 each and the remaining vehicles assigned to Pratapgarh were purchased last year at a cost of ` 13,12,000 each. With the purchase of each Vehicle, a two years Free Servicing Warranty is provided. A Vehicle gives 10 kmpl mileage in the first two year of purchase, 8 kmpl in next two years and 6 kmpl afterwards. The vehicles are subject to depreciation of 10% p.a. on straight line basis irrespective of usage. A Vehicle has the capacity to carry 25,000 litres of milk but on an average only 70% of the total capacity is utilized.

The following expenditure is related with the vehicles: Salary to a Driver (a Driver for each vehicle) ` 18,000 p.m. Salary to a Cleaner (a Cleaner for each vehicle) ` 11,000 p.m. Allocated Garage Parking fee ` 1,350 per vehicle per month Servicing Cost ` 3,000 for every complete 5,000 k.m. run. Price of Diesel per litre ` 58.00

From the above information you are required to calculate – (a) Total Operating Cost per month for each Vehicle. (Take 30 days for the month) (b) Vehicle Operating Cost per Litre of Milk.

sandy

Typewriter

Get CA CMA CS Updates and More From Caultimates.com

sandy

Typewriter

sandy

Typewriter

Gurukripa’s Guideline Answers for May 2015 CA Inter (IPC) Cost Accounting & Financial Management Exam

May 2015.17

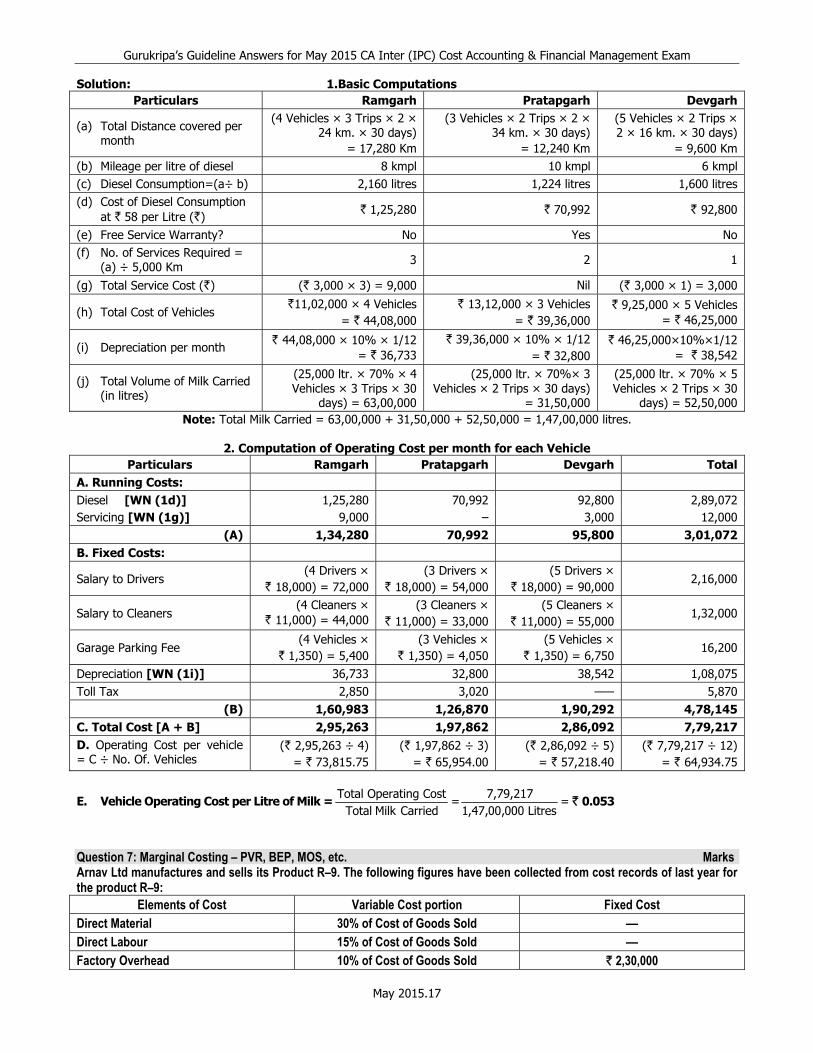

Solution: 1.Basic Computations Particulars Ramgarh Pratapgarh Devgarh

(a) Total Distance covered per month

(4 Vehicles × 3 Trips × 2 × 24 km. × 30 days)

= 17,280 Km

(3 Vehicles × 2 Trips × 2 × 34 km. × 30 days)

= 12,240 Km

(5 Vehicles × 2 Trips × 2 × 16 km. × 30 days)

= 9,600 Km (b) Mileage per litre of diesel 8 kmpl 10 kmpl 6 kmpl (c) Diesel Consumption=(a÷ b) 2,160 litres 1,224 litres 1,600 litres (d) Cost of Diesel Consumption

at ` 58 per Litre (`) ` 1,25,280 ` 70,992 ` 92,800

(e) Free Service Warranty? No Yes No (f) No. of Services Required =

(a) ÷ 5,000 Km 3 2 1

(g) Total Service Cost (`) (` 3,000 × 3) = 9,000 Nil (` 3,000 × 1) = 3,000

(h) Total Cost of Vehicles `11,02,000 × 4 Vehicles

= ` 44,08,000 ` 13,12,000 × 3 Vehicles

= ` 39,36,000 ` 9,25,000 × 5 Vehicles

= ` 46,25,000

(i) Depreciation per month ` 44,08,000 × 10% × 1/12 = ` 36,733

` 39,36,000 × 10% × 1/12 = ` 32,800

` 46,25,000×10%×1/12 = ` 38,542

(j) Total Volume of Milk Carried (in litres)

(25,000 ltr. × 70% × 4 Vehicles × 3 Trips × 30

days) = 63,00,000

(25,000 ltr. × 70%× 3 Vehicles × 2 Trips × 30 days)

= 31,50,000

(25,000 ltr. × 70% × 5 Vehicles × 2 Trips × 30

days) = 52,50,000 Note: Total Milk Carried = 63,00,000 + 31,50,000 + 52,50,000 = 1,47,00,000 litres.

2. Computation of Operating Cost per month for each Vehicle

Particulars Ramgarh Pratapgarh Devgarh TotalA. Running Costs: Diesel [WN (1d)] 1,25,280 70,992 92,800 2,89,072 Servicing [WN (1g)] 9,000 – 3,000 12,000

(A) 1,34,280 70,992 95,800 3,01,072B. Fixed Costs:

Salary to Drivers (4 Drivers ×

` 18,000) = 72,000 (3 Drivers ×

` 18,000) = 54,000 (5 Drivers ×

` 18,000) = 90,000 2,16,000

Salary to Cleaners (4 Cleaners ×

` 11,000) = 44,000 (3 Cleaners ×

` 11,000) = 33,000 (5 Cleaners ×

` 11,000) = 55,000 1,32,000

Garage Parking Fee (4 Vehicles ×

` 1,350) = 5,400 (3 Vehicles ×

` 1,350) = 4,050 (5 Vehicles ×

` 1,350) = 6,750 16,200

Depreciation [WN (1i)] 36,733 32,800 38,542 1,08,075 Toll Tax 2,850 3,020 ––– 5,870

(B) 1,60,983 1,26,870 1,90,292 4,78,145C. Total Cost [A + B] 2,95,263 1,97,862 2,86,092 7,79,217D. Operating Cost per vehicle = C ÷ No. Of. Vehicles

(` 2,95,263 ÷ 4) = ` 73,815.75

(` 1,97,862 ÷ 3) = ` 65,954.00

(` 2,86,092 ÷ 5) = ` 57,218.40

(` 7,79,217 ÷ 12) = ` 64,934.75

E. Vehicle Operating Cost per Litre of Milk =CarriedMilkTotal

CostperatingOotalT=

Litres000,00,47,17,79,217

= ` 0.053

Question 7: Marginal Costing – PVR, BEP, MOS, etc. Marks Arnav Ltd manufactures and sells its Product R–9. The following figures have been collected from cost records of last year for the product R–9:

Elements of Cost Variable Cost portion Fixed Cost Direct Material 30% of Cost of Goods Sold –– Direct Labour 15% of Cost of Goods Sold –– Factory Overhead 10% of Cost of Goods Sold ` 2,30,000

sandy

Typewriter

sandy

Typewriter

Get CA CMA CS Updates and More From Caultimates.com

sandy

Typewriter

sandy

Typewriter

Gurukripa’s Guideline Answers for May 2015 CA Inter (IPC) Cost Accounting & Financial Management Exam

May 2015.18

Elements of Cost Variable Cost portion Fixed Cost General & Administration Overhead 2% of Cost of Goods Sold ` 71,000 Selling & Distribution Overhead 4% of Cost of Sales ` 68,000 Last Year, 5,000 units were sold at `185 per unit. From the given data find the following: (a) Break–Even Sales (in Rupees) (b) Profit earned during last year (c) Margin of Safety (in %) (d) Profit if the Sales were 10% less than the Actual Sales. Solution:

1. Cost of Goods Sold (COGS) = Material + Labour + FOH + General & AOH So, COGS = (30% + 15%+ 10% + 2%) = 57% of COGS + 2,30,000 +71,000

So, 0.43 COGS = 3,01,000. Hence, COGS = 0.43

3,01,000 = 7,00,000

2. Cost of Sales (COS) = COGS + S&D OH So, COS = 7,00,000 + 4% of COS + 68,000

So, 96% COS = 7,68,000. So, COS = 96%

7,68,000= 8,00,000

3. Variable and Fixed Costs: Particulars Variable Cost (`) Fixed Cost (`)

Direct Material 7,00,000 × 30% = 2,10,000 – Direct Labour 7,00,000 × 15% = 1,05,000 – Factory Overhead 7,00,000 × 10% = 70,000 2,30,000 General & Administration OH 7,00,000 × 2% = 14,000 71,000 Selling & Distribution OH 8,00,000 × 4% = 32,000 68,000

Total 4,31,000 3,69,000

4. PV Ratio =Sales

onContributi × 100 =

SalesCosts Variable(-) Sales

× 100 = units)000,5x(185

4,31,000 (-) units)000,5x(185× 100 = 53.41%

5. Computations:

(a) Break–Even Sales = PVR

CostsFixed=

53.41%3,69,000

= ` 6,90,882.

(b) Profit earned during the last year = (Sales – Total Variable Costs) – Total Fixed Costs = (` 9,25,000 – ` 4,31,000) – ` 3,69,000 = ` 1,25,000

(c) Margin of Safety (%) = Sales Total

BES (-) Sales Total=

9,25,0006,90,882 (-) 9,25,000

= 25.31%

(d) Profit if the Sales were 10% less than the Actual Sales: (Assumed 10% reduction in Sale Qtty).

Profit = 90% of (` 9,25,000 – ` 4,31,000) – ` 3,69,000 = ` 4,44,600 – ` 3,69,000 = ` 75,600 Question 8: If a Company finds that its Cost of Capital has changed, does this affect the profitability of the Company? RTP 1. If the Company is financed mainly from short–term sources, an increase in interest rates will reduce its Profits. Hence, it

may choose to switch to long–term financing. This will be at a higher rate and profitability will be diminished. 2. If the Company is financed mainly from long–term sources, an increase in interest rates will not affect its profits

directly. However, higher interest rates may depress economic activity and its profits may fall accordingly. 3. If the Company is financed mainly from Retained Earnings or Equity, an increase in the required return of Shareholders

will lead to pressure for higher dividends. The Company may have insufficient funds to meet such demands.

sandy

Typewriter

Get CA CMA CS Updates and More From Caultimates.com

sandy

Typewriter

sandy

Typewriter

Gurukripa’s Guideline Answers for May 2015 CA Inter (IPC) Cost Accounting & Financial Management Exam

May 2015.19

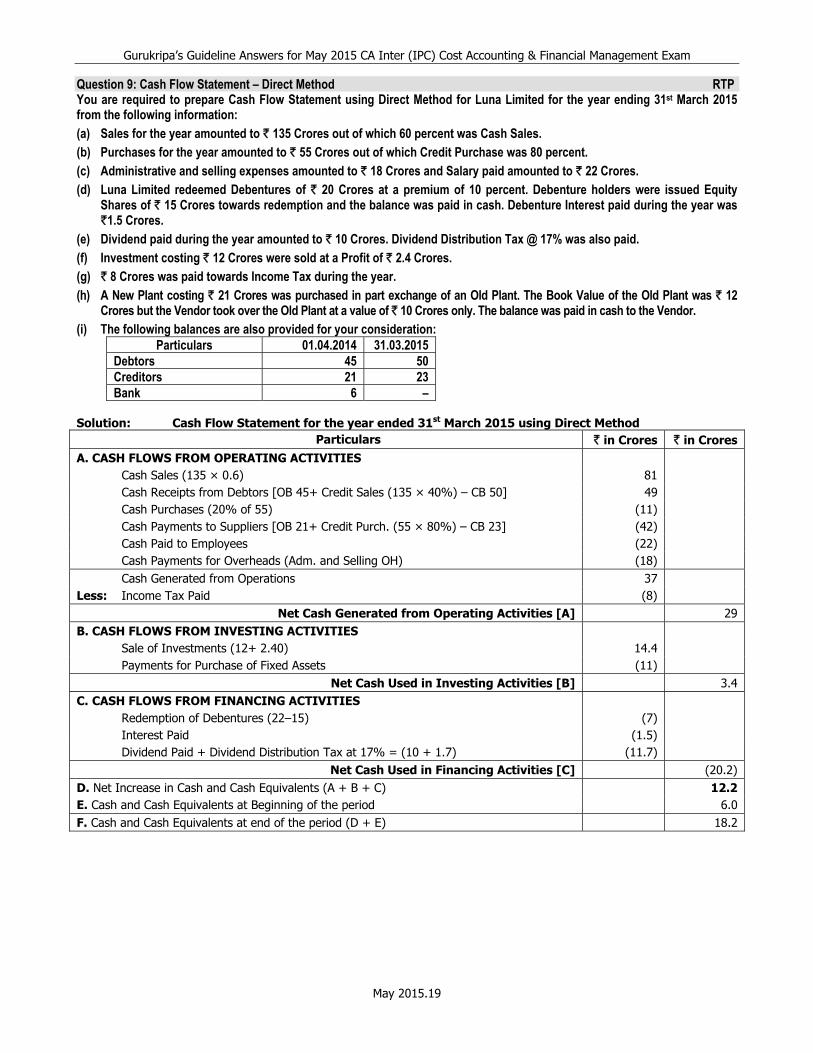

Question 9: Cash Flow Statement – Direct Method RTP You are required to prepare Cash Flow Statement using Direct Method for Luna Limited for the year ending 31st March 2015 from the following information: (a) Sales for the year amounted to ` 135 Crores out of which 60 percent was Cash Sales. (b) Purchases for the year amounted to ` 55 Crores out of which Credit Purchase was 80 percent. (c) Administrative and selling expenses amounted to ` 18 Crores and Salary paid amounted to ` 22 Crores. (d) Luna Limited redeemed Debentures of ` 20 Crores at a premium of 10 percent. Debenture holders were issued Equity

Shares of ` 15 Crores towards redemption and the balance was paid in cash. Debenture Interest paid during the year was `1.5 Crores.

(e) Dividend paid during the year amounted to ` 10 Crores. Dividend Distribution Tax @ 17% was also paid. (f) Investment costing ` 12 Crores were sold at a Profit of ` 2.4 Crores. (g) ` 8 Crores was paid towards Income Tax during the year. (h) A New Plant costing ` 21 Crores was purchased in part exchange of an Old Plant. The Book Value of the Old Plant was ` 12

Crores but the Vendor took over the Old Plant at a value of ` 10 Crores only. The balance was paid in cash to the Vendor. (i) The following balances are also provided for your consideration:

Particulars 01.04.2014 31.03.2015 Debtors 45 50 Creditors 21 23 Bank 6 –

Solution: Cash Flow Statement for the year ended 31st March 2015 using Direct Method

Particulars ` in Crores ` in CroresA. CASH FLOWS FROM OPERATING ACTIVITIES Cash Sales (135 × 0.6) 81 Cash Receipts from Debtors [OB 45+ Credit Sales (135 × 40%) – CB 50] 49 Cash Purchases (20% of 55) (11) Cash Payments to Suppliers [OB 21+ Credit Purch. (55 × 80%) – CB 23] (42) Cash Paid to Employees (22) Cash Payments for Overheads (Adm. and Selling OH) (18) Cash Generated from Operations 37 Less: Income Tax Paid (8) Net Cash Generated from Operating Activities [A] 29 B. CASH FLOWS FROM INVESTING ACTIVITIES Sale of Investments (12+ 2.40) 14.4 Payments for Purchase of Fixed Assets (11) Net Cash Used in Investing Activities [B] 3.4 C. CASH FLOWS FROM FINANCING ACTIVITIES Redemption of Debentures (22–15) (7) Interest Paid (1.5) Dividend Paid + Dividend Distribution Tax at 17% = (10 + 1.7) (11.7) Net Cash Used in Financing Activities [C] (20.2) D. Net Increase in Cash and Cash Equivalents (A + B + C) 12.2E. Cash and Cash Equivalents at Beginning of the period 6.0 F. Cash and Cash Equivalents at end of the period (D + E) 18.2

sandy

Typewriter

Get CA CMA CS Updates and More From Caultimates.com

sandy

Typewriter

sandy

Typewriter

Gurukripa’s Guideline Answers for May 2015 CA Inter (IPC) Cost Accounting & Financial Management Exam

May 2015.20

STUDENTS’ NOTES

sandy

Typewriter

Get CA CMA CS Updates and More From Caultimates.com

sandy

Typewriter

![19107552 13823737 Cost Accounting and Financial Management[1]](https://static.fdocuments.in/doc/165x107/552657f2550346ad6e8b4c7a/19107552-13823737-cost-accounting-and-financial-management1.jpg)