3-665 Cover

37

RACE TO THE TOP: ATTRACTING AND ENABLING GLOBAL SUSTAINABLE BUSINESS Business Survey Report The World Bank Group • Corporate Social Responsibility Practice The CSR Practice advises developing country governments on public policy roles and instruments they can most usefully deploy to encourage corporate social responsibility. October 2003

Transcript of 3-665 Cover

RACE TO THE TOP:

ATTRACTING AND ENABLING

GLOBAL SUSTAINABLE BUSINESS

Business Survey Report

The World Bank Group • Corporate Social Responsibility PracticeThe CSR Practice advises developing country governments on public policy roles andinstruments they can most usefully deploy to encourage corporate social responsibility.

October 2003

2121 Pennsylvania Avenue, NWWashington, DC 20433 USA

The CSR Practice is part of the Private SectorDevelopment Vice Presidency, jointly operatedby the International Finance Corporation andthe World Bank.

Telephone: 202 473 7646Facsimile: 202 522 2138E-mail : [email protected] Internet: www.worldbank.org/privatesector/csr

RACE TO THE TOP:

ATTRACTING AND ENABLING

GLOBAL SUSTAINABLE BUSINESS

Business Survey Report

Jonathan E. Berman, Project Director,Political and Economic Link Consulting (PELC)

Tobias Webb, Project Coordinator,Ethical Corporation

Douglas J. Fraser, Senior Project Specialist

Pharis J. Harvey, Senior Project Specialist

Jennifer Barsky and Ayesha Haider, Senior Project Associates

Katie Dunn, Susan Forde, Aaron Graham, Hilton Mundy,Saad Tayara, and Ingrid Williams, Project Associates

October 2003

This report is a product of the staff of the World Bank. The findings, interpretations and conclusionsexpressed herein do not necessarily reflect the views of the Board of Executive Directors of the WorldBank or the governments they represent. The World Bank does not guarantee the accuracy of the dataincluded in this work.

Printed on Acid-Free Recycled Paper.

List of Figures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . v

Executive Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

1.0 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

1.1 Project Description . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

1.2 Project Commission . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

1.3 Project Methodology. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

1.3.1 Sample selection . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

1.3.2 Interview methodology . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

1.3.3 Data analysis methodology . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

2.0 Analysis of Survey Respondents . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

2.1 Size of Respondent Companies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

2.2 Sector of Respondent Companies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

2.3 Location of Respondent Companies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

2.4 Level of Respondent within the Company . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

3.0 Analysis of Survey Results . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

3.1 Importance of CSR to International Investors and Buyers . . . . . . . . . . . . . . . . 11

3.1.1 Policies on CSR issues . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

3.1.2 Change in CSR’s importance over time . . . . . . . . . . . . . . . . . . . . . . . . 12

3.1.3 Leading standards . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

3.2 Importance of CSR in Selecting New Partners and Locations . . . . . . . . . . . . . 14

3.2.1 Point at which CSR issues are considered . . . . . . . . . . . . . . . . . . . . . . 14

3.2.2 CSR as a factor in selecting partners and locations . . . . . . . . . . . . . . . 14

3.2.3 Importance of various CSR issues . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

3.2.4 Sources used to assess CSR issues in new ventures . . . . . . . . . . . . . . . 16

Table of Contents

iii

3.2.5 Role of CSR as compared to other factors

in new venture assessment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

3.3 CSR Challenges for International Firms. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

3.3.1 Local partner commitments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

3.3.2 Resources to help partners keep commitments. . . . . . . . . . . . . . . . . . . 18

3.3.3 Assessment of location as distinct from assessment of partner . . . . . . 19

3.3.4 Local regulation and enforcement . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19

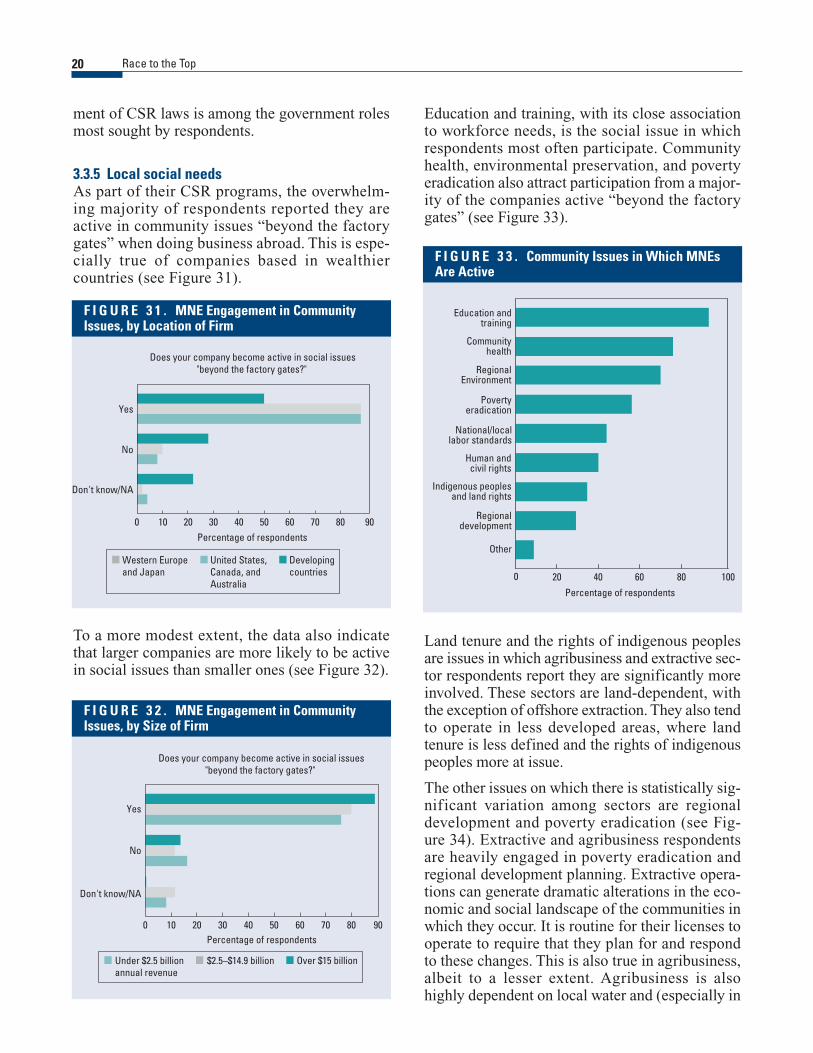

3.3.5 Local social needs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

3.3.6 Role of local organizations in meeting CSR challenges . . . . . . . . . . . . 21

3.3.7 Role of host governments in meeting CSR challenges . . . . . . . . . . . . . 21

3.3.8 Partnerships sought with governments . . . . . . . . . . . . . . . . . . . . . . . . . 23

3.3.9 Changes over the last five years . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23

4.0 Conclusions & Recommendations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25

4.1 Attracting Sustainable Trade and Investment . . . . . . . . . . . . . . . . . . . . . . . . . . 25

4.1.1 Strong laws, strongly enforced . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25

4.1.2 CSR codes, standards and forums. . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25

4.1.3 CSR and the new venture assessment cycle.. . . . . . . . . . . . . . . . . . . . . 26

4.1.4 Local partners as a country marketing tool. . . . . . . . . . . . . . . . . . . . . . 26

4.1.5 The sources that matter . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26

4.2 Enabling Sustainable Trade and Investment . . . . . . . . . . . . . . . . . . . . . . . . . . . 27

4.2.1 Large companies, likely partners . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27

4.2.2 Cultivating CSR relationships for developing-country MNEs . . . . . . . 27

4.2.3 Bringing religious institutions to the table . . . . . . . . . . . . . . . . . . . . . . 27

4.2.4 Multicorporation partnerships . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28

4.2.5 Building a local partner base . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28

Table of Contentsiv

Figure 1. Respondents’ Total Annual Revenue by Sector. . . . . . . . . . . . . . . . . . . . . . 9

Figure 2. Individual Respondents’Annual Revenues. . . . . . . . . . . . . . . . . . . . . . . . . 9

Figure 3. Percentage of Respondents in Each Sector . . . . . . . . . . . . . . . . . . . . . . . . 10

Figure 4. Percentage of Respondents by Location . . . . . . . . . . . . . . . . . . . . . . . . . . 10

Figure 5. Positions of Interviewees . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

Figure 6. Board-Approved Policies on CSR Issues: All Respondents . . . . . . . . . . . 11

Figure 7. Board-Approved Policies on CSR Issues: Distinctions by Sector . . . . . . 11

Figure 8. Board-Approved Policies on CSR Issues: Location Analysis. . . . . . . . . . 12

Figure 9. CSR Policy Implementation Mechanisms . . . . . . . . . . . . . . . . . . . . . . . . 12

Figure 10. Duration of CSR Policies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

Figure 11. CSR Standards & Forums: A Recent Influence . . . . . . . . . . . . . . . . . . . . 13

Figure 12. MNE Investment in CSR: Increases over Last Five Years . . . . . . . . . . . . 13

Figure 13. Impact of Multisector Standards & Forums on MNEs . . . . . . . . . . . . . . . 14

Figure 14. Influence of External Standards: Distinctions by Location . . . . . . . . . . . 14

Figure 15. Influence of External Standards: Distinctions by Sector . . . . . . . . . . . . . 14

Figure 16. When CSR Is Typically Reviewed in New Venture Assessment. . . . . . . . 15

Figure 17. CSR as a Factor in Partner & Location Selection . . . . . . . . . . . . . . . . . . . 15

Figure 18. CSR as Selection Factor: Distinctions by Location of MNE . . . . . . . . . . 15

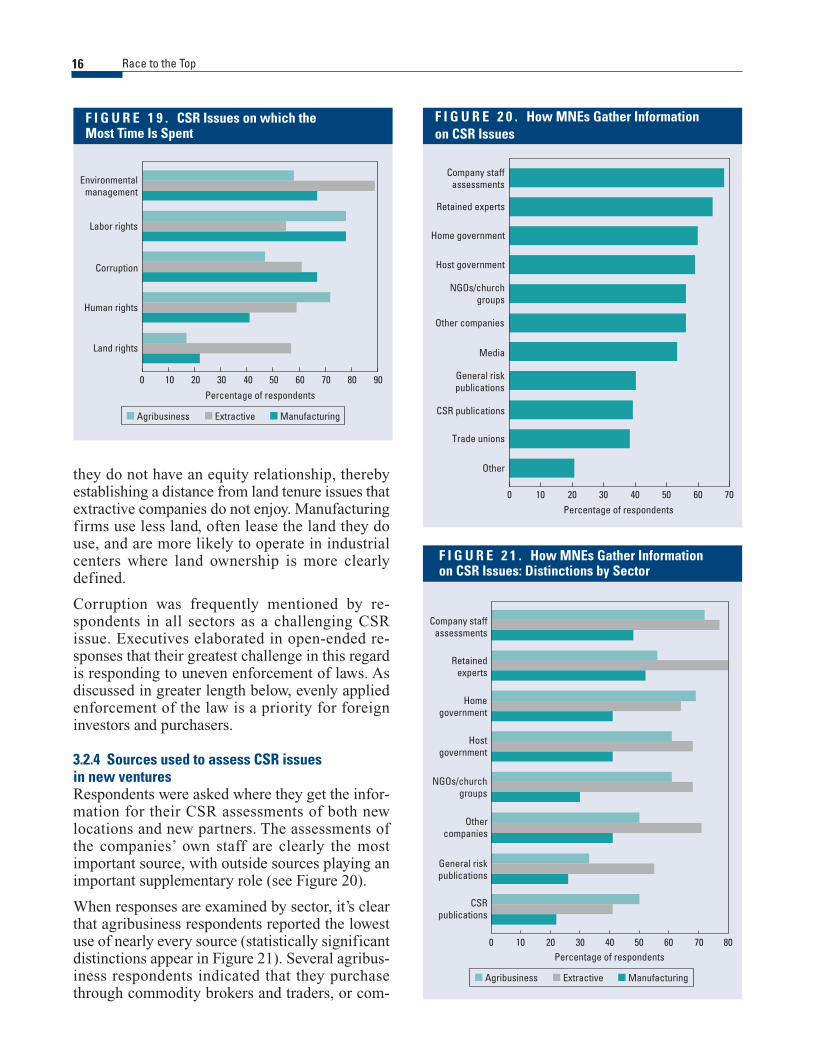

Figure 19. CSR Issues on which the Most Time Is Spent . . . . . . . . . . . . . . . . . . . . . 16

Figure 20. How MNEs Gather Information on CSR Issues . . . . . . . . . . . . . . . . . . . . 16

Figure 21. How MNEs Gather Information on CSR Issues: Distinctions by Sector . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

Figure 22. How MNEs Gather Information on CSR Issues: Low Cost Sources . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

List of Figures

v

Figure 23. Influence of CSR on New Venture Assessment Relative to More Traditional Criteria . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

Figure 24. Influence of CSR on New Venture Assessment Relative to Five Years Ago. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

Figure 25. Level of CSR Commitment Requested by MNEs of Local Partners . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

Figure 26. How MNEs Verify Partner CSR Commitments . . . . . . . . . . . . . . . . . . . . 18

Figure 27. CSR Assistance MNEs Offer Local Partners . . . . . . . . . . . . . . . . . . . . . . 19

Figure 28. Importance of Country Performance vs. Partner Performance. . . . . . . . . 19

Figure 29. CSR-Related Laws and Ease of Business Operations . . . . . . . . . . . . . . . 19

Figure 30. CSR-Related Enforcement and Ease of Business Operations . . . . . . . . . 19

Figure 31. MNE Engagement in Community Issues, by Location of Firm . . . . . . . . 20

Figure 32. MNE Engagement in Community Issues, by Size of Firm. . . . . . . . . . . . 20

Figure 33. Community Issues in Which MNEs Are Active . . . . . . . . . . . . . . . . . . . . 20

Figure 34. Community Issues in which MNEs Are Active: Distinctions by Sector. . 21

Figure 35. Most Important Civil Society Partners for MNEs . . . . . . . . . . . . . . . . . . 21

Figure 36. Perceived Importance of Trade Unions as CSR Partners . . . . . . . . . . . . . 21

Figure 37. Perceived Importance of Host Government as CSR Partners . . . . . . . . . . 22

Figure 38. CSR Issues on which MNEs Seek Partnership with Host CountryGovernments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

Figure 39. Social Issues on which MNEs Seek Government Partnership: Distinctions by Sector . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

Figure 40. Host Government Actions Sought by MNEs . . . . . . . . . . . . . . . . . . . . . . 22

Figure 41. How MNEs’Approach to CSR Has Changed over the Last Five Years . . 23

Figure 42. Mainstreaming CSR in the Last Five Years: Analysis by Size of Firm. . . 23

Table of Figuresvi

RACE TO THE TOP:

ATTRACTING AND ENABLING

GLOBAL SUSTAINABLE BUSINESS

The World Bank Group’s CSR Practice com-missioned PELC and Ethical Corporation

to conduct a study to explore two related issues:(a) how corporate social responsibility (CSR)issues influence the investment and purchasedecisions of multinational enterprises (MNEs)around the world and (b) how governments in the developing world can create environmentsthat companies will find attractive from a CSRperspective.

ANALYSIS OF SURVEY RESPONDENTSBetween December 2002 and March 2003, in-depth interviews were conducted with execu-tives of 107 multinational enterprises in theextractive, agribusiness, and manufacturing sec-tors. The study was designed to capture theviews of the largest purchasers and investors inthe target sectors, as well as CSR leaders in eachsector.

� Total revenues of companies participating inthe study: US$1.66 trillion.

� Average respondent’s annual revenues:US$15.5 billion.

� Over 85 percent of respondents are publiclyowned.

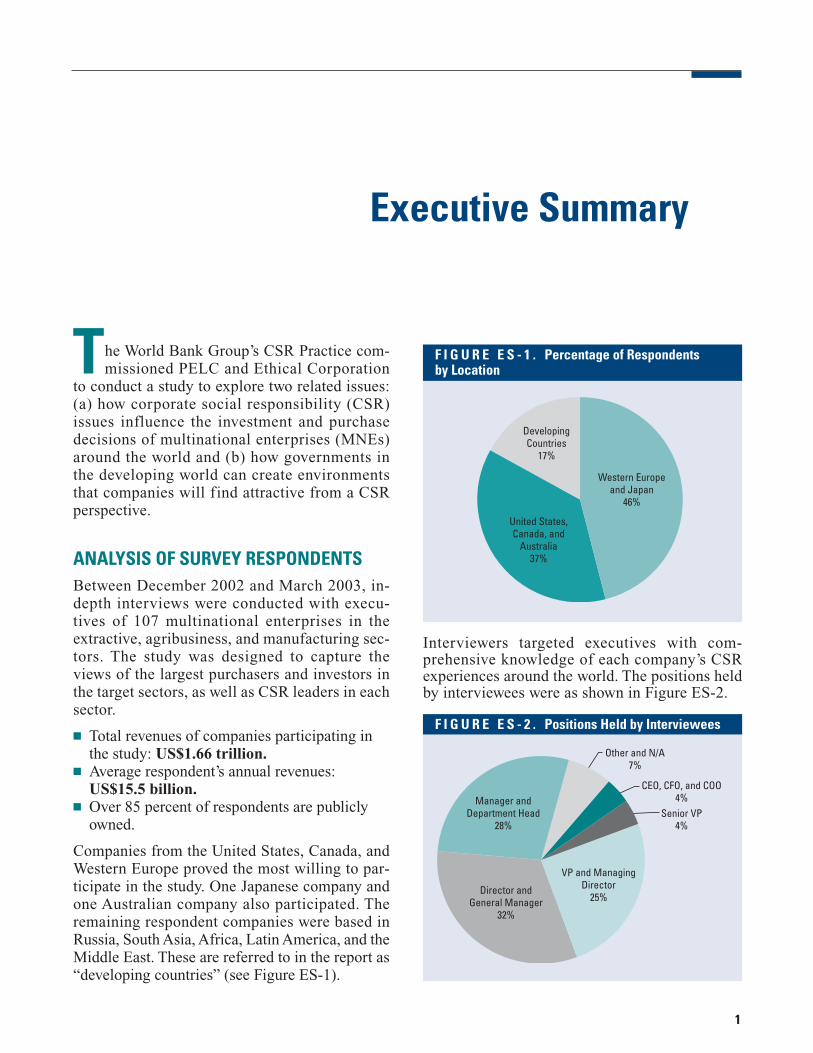

Companies from the United States, Canada, andWestern Europe proved the most willing to par-ticipate in the study. One Japanese company andone Australian company also participated. Theremaining respondent companies were based inRussia, South Asia, Africa, Latin America, and theMiddle East. These are referred to in the report as“developing countries” (see Figure ES-1).

Interviewers targeted executives with com-prehensive knowledge of each company’s CSRexperiences around the world. The positions heldby interviewees were as shown in Figure ES-2.

Executive Summary

1

Western Europeand Japan

46%

United States,Canada, and

Australia37%

DevelopingCountries

17%

F I G U R E E S - 1 . Percentage of Respondents by Location

CEO, CFO, and COO4%

Senior VP4%

VP and ManagingDirector

25%Director and

General Manager32%

Manager andDepartment Head

28%

Other and N/A7%

F I G U R E E S - 2 . Positions Held by Interviewees

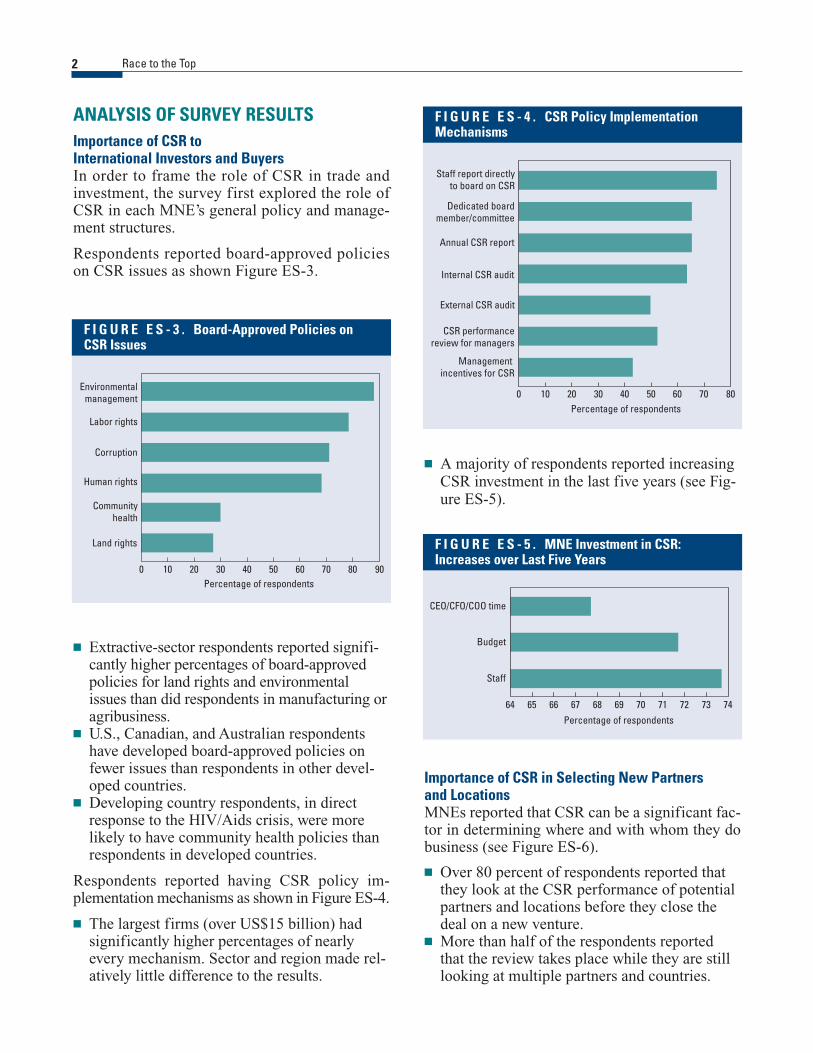

ANALYSIS OF SURVEY RESULTSImportance of CSR to International Investors and BuyersIn order to frame the role of CSR in trade andinvestment, the survey first explored the role ofCSR in each MNE’s general policy and manage-ment structures.

Respondents reported board-approved policieson CSR issues as shown Figure ES-3.

Race to the Top2

� Extractive-sector respondents reported signifi-cantly higher percentages of board-approvedpolicies for land rights and environmentalissues than did respondents in manufacturing oragribusiness.

� U.S., Canadian, and Australian respondentshave developed board-approved policies onfewer issues than respondents in other devel-oped countries.

� Developing country respondents, in directresponse to the HIV/Aids crisis, were morelikely to have community health policies thanrespondents in developed countries.

Respondents reported having CSR policy im-plementation mechanisms as shown in Figure ES-4.

� The largest firms (over US$15 billion) hadsignificantly higher percentages of nearlyevery mechanism. Sector and region made rel-atively little difference to the results.

� A majority of respondents reported increasingCSR investment in the last five years (see Fig-ure ES-5).

0 10 20 30 40 50 60 70 80 90Percentage of respondents

Land rights

Communityhealth

Human rights

Corruption

Labor rights

Environmentalmanagement

F I G U R E E S - 3 . Board-Approved Policies on CSR Issues

0 10 20 30 40 50 60 70 80Percentage of respondents

Staff report directlyto board on CSR

Dedicated boardmember/committee

Annual CSR report

Internal CSR audit

External CSR audit

CSR performancereview for managers

Management incentives for CSR

F I G U R E E S - 4 . CSR Policy ImplementationMechanisms

64 65 66 67 68 69 70 71 72 73 74Percentage of respondents

Staff

Budget

CEO/CFO/COO time

F I G U R E E S - 5 . MNE Investment in CSR:Increases over Last Five Years

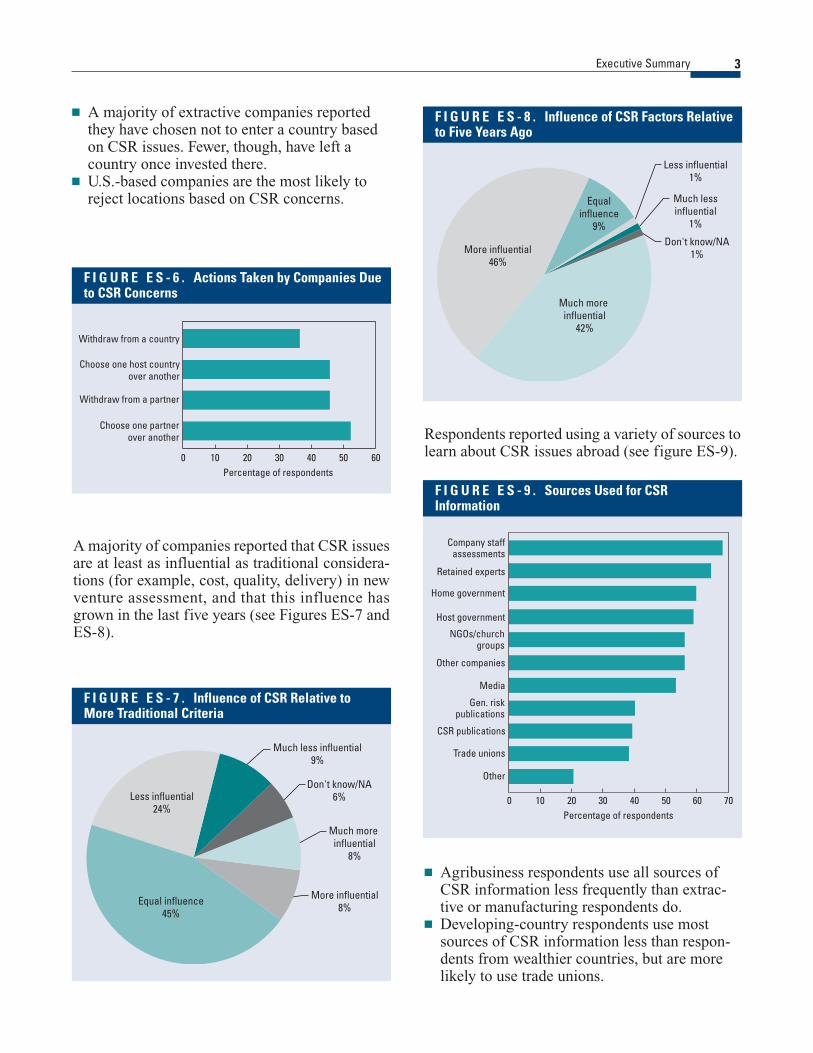

Importance of CSR in Selecting New Partners and LocationsMNEs reported that CSR can be a significant fac-tor in determining where and with whom they dobusiness (see Figure ES-6).

� Over 80 percent of respondents reported thatthey look at the CSR performance of potentialpartners and locations before they close thedeal on a new venture.

� More than half of the respondents reportedthat the review takes place while they are stilllooking at multiple partners and countries.

� A majority of extractive companies reportedthey have chosen not to enter a country basedon CSR issues. Fewer, though, have left acountry once invested there.

� U.S.-based companies are the most likely toreject locations based on CSR concerns.

Executive Summary 3

A majority of companies reported that CSR issuesare at least as influential as traditional considera-tions (for example, cost, quality, delivery) in newventure assessment, and that this influence hasgrown in the last five years (see Figures ES-7 andES-8).

Respondents reported using a variety of sources tolearn about CSR issues abroad (see figure ES-9).0 10 20 30 40 50 60

Percentage of respondents

Choose one partnerover another

Withdraw from a partner

Choose one host countryover another

Withdraw from a country

F I G U R E E S - 6 . Actions Taken by Companies Dueto CSR Concerns

Much more influential

8%

More influential8%

Equal influence45%

Less influential24%

Much less influential9%

Don't know/NA6%

F I G U R E E S - 7 . Influence of CSR Relative toMore Traditional Criteria

Much more influential

42%

More influential46%

Equalinfluence

9%

Less influential1%

Much lessinfluential

1%

Don't know/NA1%

F I G U R E E S - 8 . Influence of CSR Factors Relativeto Five Years Ago

0 10 20 30 40 50 60 70Percentage of respondents

Company staffassessments

Retained experts

Home government

Host government

NGOs/churchgroups

Other companies

Media

Gen. riskpublications

CSR publications

Trade unions

Other

F I G U R E E S - 9 . Sources Used for CSRInformation

� Agribusiness respondents use all sources ofCSR information less frequently than extrac-tive or manufacturing respondents do.

� Developing-country respondents use mostsources of CSR information less than respon-dents from wealthier countries, but are morelikely to use trade unions.

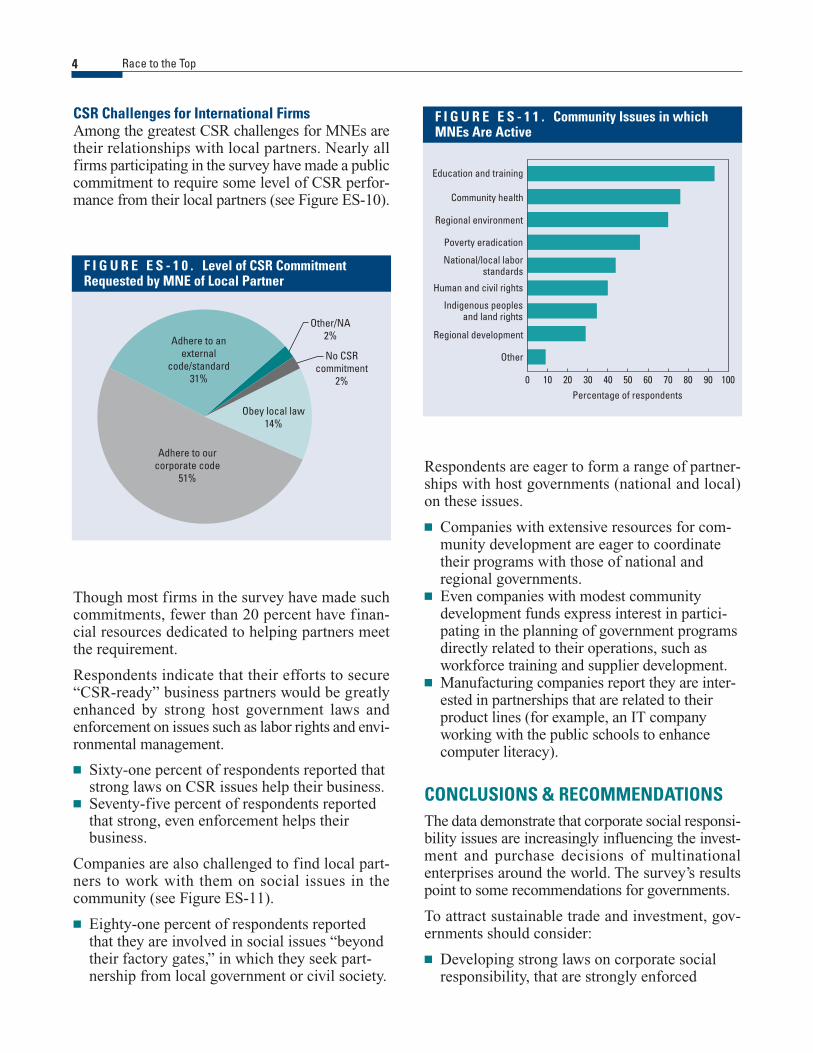

CSR Challenges for International FirmsAmong the greatest CSR challenges for MNEs aretheir relationships with local partners. Nearly allfirms participating in the survey have made a publiccommitment to require some level of CSR perfor-mance from their local partners (see Figure ES-10).

Respondents are eager to form a range of partner-ships with host governments (national and local)on these issues.

� Companies with extensive resources for com-munity development are eager to coordinatetheir programs with those of national andregional governments.

� Even companies with modest communitydevelopment funds express interest in partici-pating in the planning of government programsdirectly related to their operations, such asworkforce training and supplier development.

� Manufacturing companies report they are inter-ested in partnerships that are related to theirproduct lines (for example, an IT companyworking with the public schools to enhancecomputer literacy).

CONCLUSIONS & RECOMMENDATIONSThe data demonstrate that corporate social responsi-bility issues are increasingly influencing the invest-ment and purchase decisions of multinationalenterprises around the world. The survey’s resultspoint to some recommendations for governments.

To attract sustainable trade and investment, gov-ernments should consider:

� Developing strong laws on corporate socialresponsibility, that are strongly enforced

Race to the Top4

No CSRcommitment

2%

Other/NA2%

Obey local law14%

Adhere to ourcorporate code

51%

Adhere to anexternal

code/standard31%

F I G U R E E S - 1 0 . Level of CSR CommitmentRequested by MNE of Local Partner

0 10 20 30 40 50 60 70 80 90 100Percentage of respondents

Education and training

Community health

Regional environment

Poverty eradication

National/local laborstandards

Human and civil rights

Indigenous peoplesand land rights

Regional development

Other

F I G U R E E S - 1 1 . Community Issues in whichMNEs Are Active

Though most firms in the survey have made suchcommitments, fewer than 20 percent have finan-cial resources dedicated to helping partners meetthe requirement.

Respondents indicate that their efforts to secure“CSR-ready” business partners would be greatlyenhanced by strong host government laws andenforcement on issues such as labor rights and envi-ronmental management.

� Sixty-one percent of respondents reported thatstrong laws on CSR issues help their business.

� Seventy-five percent of respondents reportedthat strong, even enforcement helps theirbusiness.

Companies are also challenged to find local part-ners to work with them on social issues in thecommunity (see Figure ES-11).

� Eighty-one percent of respondents reportedthat they are involved in social issues “beyondtheir factory gates,” in which they seek part-nership from local government or civil society.

Executive Summary 5

� Addressing MNEs CSR concerns early in theMNEs’ new venture assessment cycle

� Using local “CSR-ready” companies to pro-mote the country as an investment location

� Channeling CSR information into media thatmatter to MNEs

� Improving their understanding of the corporateCSR codes of target MNEs, and engagingmore effectively in international CSR forums.

To enable sustainable trade and investment, gov-ernments should consider:

� Approaching large MNEs for partnerships,using their CSR systems to contribute to devel-opment objectives

� Cultivating local CSR resources for smallerand developing-country MNEs

� Engaging local religious institutions moreeffectively in contributing to the enabling CSR

� Brokering multicorporate partnerships where single-company action is difficult orinappropriate

� Building a base of “CSR-ready” localcompanies.

1.1 Project DescriptionThis study examines two related issues: (a) howcorporate social responsibility (CSR) issues influ-ence the investment and purchase decisions ofmultinational enterprises (MNEs) around the worldand (b) how governments in the developing worldcan create environments that companies will findattractive from a CSR perspective.1

The report is based on a survey of MNEs thataddressed:

� Formal corporate social policy� Implementation mechanisms for social policy� Corporate social policy and practice in regard

to new trade and investment ventures� Ongoing challenges confronting corporate

social policy in the developing world� The role of local partners, and especially host

governments, in meeting those challenges� How countries can attract trade and investment

by enabling CSR.

The survey is described in detail below; the surveyquestions are provided as an annex to this report.Responses were analyzed for statistical signifi-cance and interpreted by experts with 10–30 years of experience in trade and investmentattraction and corporate social policy.

1.2 Project CommissionThe World Bank Group’s Corporate SocialResponsibility (CSR) Practice commissioned the

study. The CSR Practice advises developing-country governments on public policy roles andinstruments they can most usefully deploy toencourage corporate social responsibility.2 Toconduct the study, the World Bank commissionedPolitical and Economic Link Consulting (PELC)and Ethical Corporation Magazine. PELC, a con-sultancy with practices in both foreign investmentattraction and corporate social policy, has con-ducted several engagements on the ties amongCSR, trade, and investment.3 Ethical CorporationMagazine is a leading source of information onglobal corporate social issues.4

1.3 Project MethodologyThe study is based on in-depth interviews withexecutives of more than 100 MNEs in the extrac-tive, agribusiness, and manufacturing sectors.5

While insufficient to represent all companies ineach of the target sectors, the responses are indica-tive of trends among:

� The largest companies in each sector� A community of mid-sized companies com-

mitted to CSR.

1.3.1 Sample selectionThe largest MNEs were targeted in each of thethree target sectors, with primary emphasis on tenindustries.

Introduction

1

7

1 There are many definitions of corporate social responsi-bility. The World Bank CSR Practice defines CSR as “thecommitment of business to contribute to sustainable eco-nomic development, working with employees, their fami-lies, the local community, and society at large to improve

their quality of life in ways that are both good for businessand good for development.”2 More information on the CSR Practice can be found athttp://www.worldbank.org/privatesector/csr/index.htm.3 www.pelc.net4 www.ethicalcorp.com5. A complete analysis of survey respondents appears in thesection following this one.

Extractive Agribusiness Manufacturing

Mining Bananas ApparelOil & Gas Coffee Electronics

Cocoa FootwearTea Toys

Once the primary industries were exhausted, com-panies were targeted in additional industrieswithin the three target sectors. Each sector wasevenly targeted.

Global leaders in each sector, as well as companiesthat have taken a high CSR public profile, were tar-geted for participation in the survey. The goal of thetargeting was to learn the current approach of thelargest companies in each sector, as well as to exam-ine trends among companies in the forefront of cor-porate social responsibility.

Finally, the targeting strove for global geographicdistribution, within the set of companies that buy orinvest internationally, and within each target sector.Within these parameters, more than 200 developing-country companies were contacted with the aim oftargeting both sector leaders in the developing worldas well as developing-country companies that hadexpressed an interest in CSR issues through EthicalCorporation’s various media.

In total, more than 600 companies were solicitedfor participation, and 107 were interviewed. Inaddition to the leading companies in each sector,efforts were made to obtain geographic breadth inthe sample. Targeting included companies in theUnited States, Canada, Western Europe, East Asia,and every region of the developing world. Inter-viewers fluent in Chinese (Mandarin), Dutch,English, French, German, Portuguese, and Spanishwere made available.

1.3.2 Interview methodologyAll companies received an initial telephone call, inwhich interviewers introduced the Bank GroupCSR Practice, its contractors, and the nature of the

project. The range of information sought for thestudy required that interviewees be executiveswith comprehensive knowledge of the company’sexperience in implementing its CSR policiesaround the world. Typically, interviewers wouldconsult with the staff of the company’s chief exec-utive or chief operating officer, who would assistin identifying the appropriate executive at eachcompany. An analysis of the positions intervie-wees held can be found in the following section:Analysis of Survey Respondents.

Executives who expressed a willingness to partici-pate scheduled an interview time. They then receiveda follow-up e-mail or fax with more detailed infor-mation about the project and the nature of the inter-view. Interviewers provided a list of questions tothose executives who requested it.

In most cases, the scheduled interview was con-ducted by phone. Interviews were based on a com-bination of open-end and closed-end questionsand were typically of 45–90 minutes in duration.The interview template can be found as an annexto this report.

1.3.3 Data analysis methodologyData from the interviews were recorded by theinterviewers during the interview or immediatelyfollowing. Where possible, responses to openquestions were precoded in the survey design. Fur-ther coding was conducted as open-end responseswere entered for tabulation at the conclusion ofthe survey period to refine and enhance the pre-coding. Open questions that did not yield a con-centration of responses were not coded, though theproject staff made use of them to illustrate pointsindicated elsewhere in the data.

Data were cross-tabulated using analysis variablesincluding company location, size, and sector. Qual-itative analysis was delivered by project senior staffbased on analysis of the data, review of open ques-tion responses, and follow-up consultations withinthe target sectors.

Race to the Top8

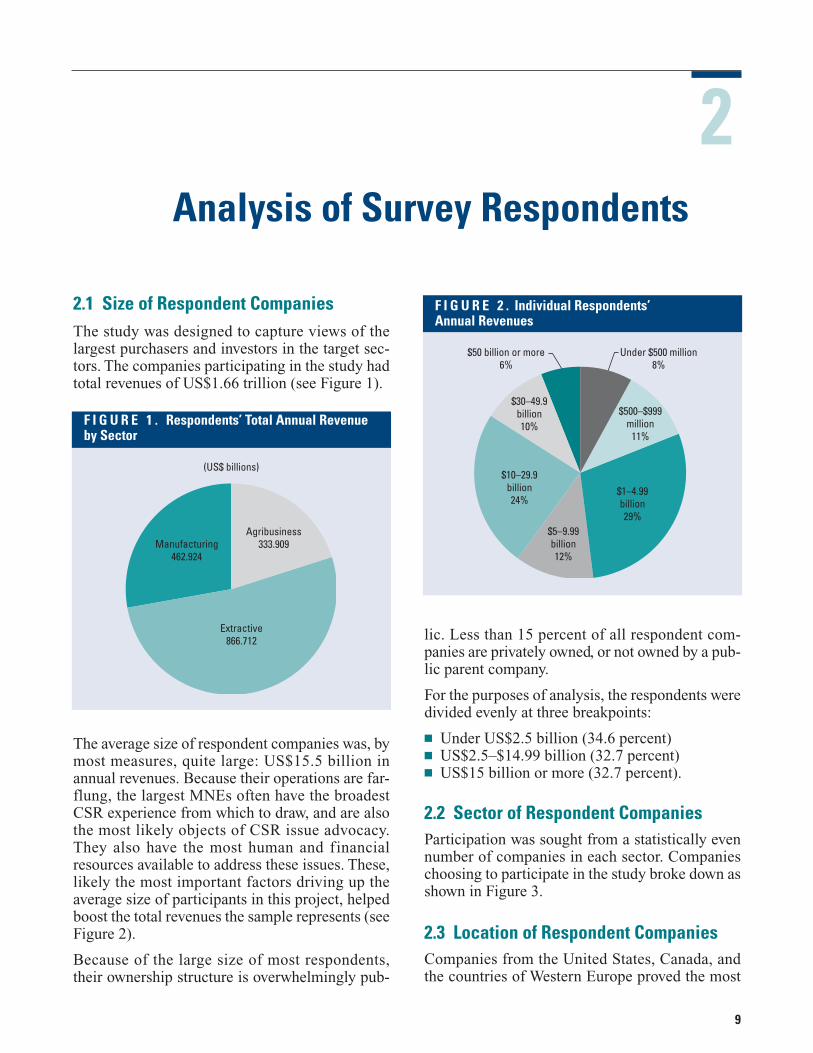

2.1 Size of Respondent CompaniesThe study was designed to capture views of thelargest purchasers and investors in the target sec-tors. The companies participating in the study hadtotal revenues of US$1.66 trillion (see Figure 1).

lic. Less than 15 percent of all respondent com-panies are privately owned, or not owned by a pub-lic parent company.

For the purposes of analysis, the respondents weredivided evenly at three breakpoints:

� Under US$2.5 billion (34.6 percent)� US$2.5–$14.99 billion (32.7 percent)� US$15 billion or more (32.7 percent).

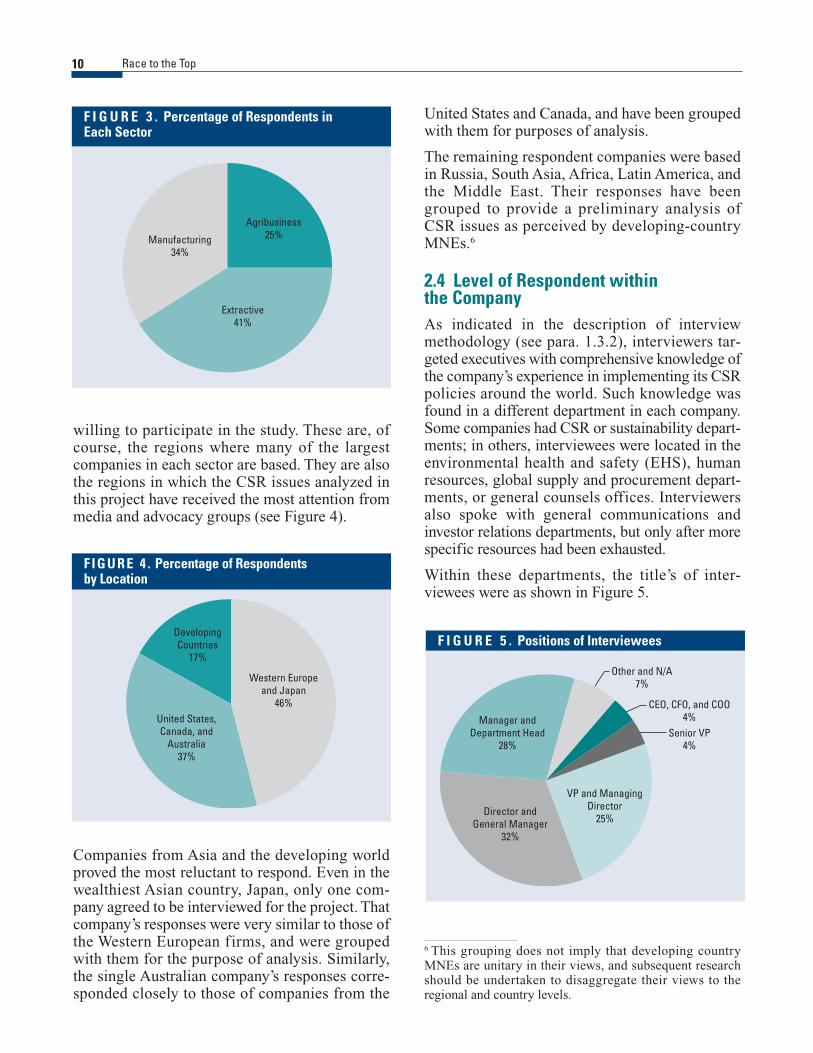

2.2 Sector of Respondent CompaniesParticipation was sought from a statistically evennumber of companies in each sector. Companieschoosing to participate in the study broke down asshown in Figure 3.

2.3 Location of Respondent CompaniesCompanies from the United States, Canada, andthe countries of Western Europe proved the most

Analysis of Survey Respondents

2

9

$50 billion or more6%

$30–49.9billion10%

$10–29.9billion24%

$5–9.99billion12%

$1–4.99billion29%

$500–$999million

11%

Under $500 million8%

F I G U R E 2 . Individual Respondents’ Annual Revenues

Agribusiness333.909

Extractive866.712

Manufacturing462.924

(US$ billions)

F I G U R E 1 . Respondents’ Total Annual Revenue by Sector

The average size of respondent companies was, bymost measures, quite large: US$15.5 billion inannual revenues. Because their operations are far-flung, the largest MNEs often have the broadestCSR experience from which to draw, and are alsothe most likely objects of CSR issue advocacy.They also have the most human and financialresources available to address these issues. These,likely the most important factors driving up theaverage size of participants in this project, helpedboost the total revenues the sample represents (seeFigure 2).

Because of the large size of most respondents,their ownership structure is overwhelmingly pub-

willing to participate in the study. These are, ofcourse, the regions where many of the largestcompanies in each sector are based. They are alsothe regions in which the CSR issues analyzed inthis project have received the most attention frommedia and advocacy groups (see Figure 4).

United States and Canada, and have been groupedwith them for purposes of analysis.

The remaining respondent companies were basedin Russia, South Asia, Africa, Latin America, andthe Middle East. Their responses have beengrouped to provide a preliminary analysis ofCSR issues as perceived by developing-countryMNEs.6

2.4 Level of Respondent within the CompanyAs indicated in the description of interviewmethodology (see para. 1.3.2), interviewers tar-geted executives with comprehensive knowledge ofthe company’s experience in implementing its CSRpolicies around the world. Such knowledge wasfound in a different department in each company.Some companies had CSR or sustainability depart-ments; in others, interviewees were located in theenvironmental health and safety (EHS), humanresources, global supply and procurement depart-ments, or general counsels offices. Interviewersalso spoke with general communications andinvestor relations departments, but only after morespecific resources had been exhausted.

Within these departments, the title’s of inter-viewees were as shown in Figure 5.

Race to the Top10

6 This grouping does not imply that developing countryMNEs are unitary in their views, and subsequent researchshould be undertaken to disaggregate their views to theregional and country levels.

Western Europeand Japan

46%United States,Canada, and

Australia37%

DevelopingCountries

17%

F IGURE 4 . Percentage of Respondents by Location

Agribusiness25%

Extractive41%

Manufacturing34%

F I G U R E 3 . Percentage of Respondents in Each Sector

CEO, CFO, and COO4%

Senior VP4%

VP and ManagingDirector

25%Director and

General Manager32%

Manager andDepartment Head

28%

Other and N/A7%

F I G U R E 5 . Positions of Interviewees

Companies from Asia and the developing worldproved the most reluctant to respond. Even in thewealthiest Asian country, Japan, only one com-pany agreed to be interviewed for the project. Thatcompany’s responses were very similar to those ofthe Western European firms, and were groupedwith them for the purpose of analysis. Similarly,the single Australian company’s responses corre-sponded closely to those of companies from the

3.1 Importance of CSR to InternationalInvestors and BuyersIn order to frame the study’s principal inquiry intoenabling CSR-driven trade and investment, the sur-vey first explored the role of CSR in MNEs generalpolicy and management structures. Respondentswere asked about:

� Company policy on CSR issues� Management mechanisms used to implement

CSR policy� Changes in CSR policy in recent years� Changes in resources dedicated to CSR in

recent years� Influence of external CSR standards on corpo-

rate CSR policy.

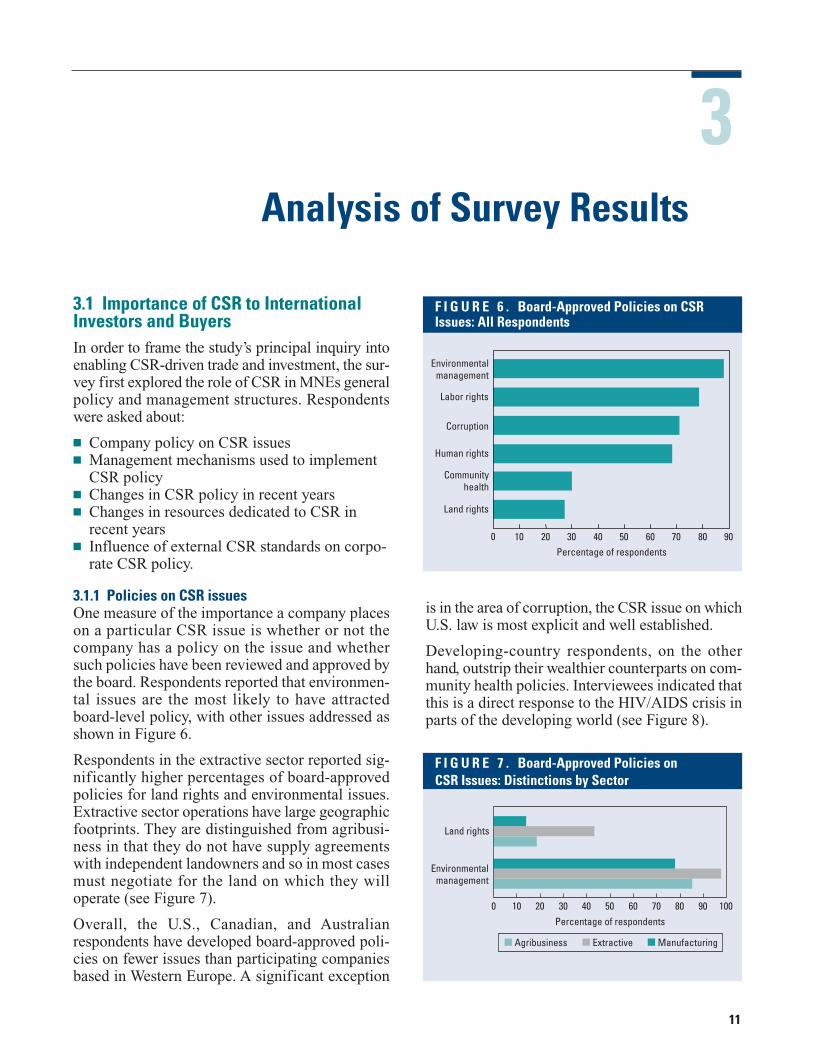

3.1.1 Policies on CSR issuesOne measure of the importance a company placeson a particular CSR issue is whether or not thecompany has a policy on the issue and whethersuch policies have been reviewed and approved bythe board. Respondents reported that environmen-tal issues are the most likely to have attractedboard-level policy, with other issues addressed asshown in Figure 6.

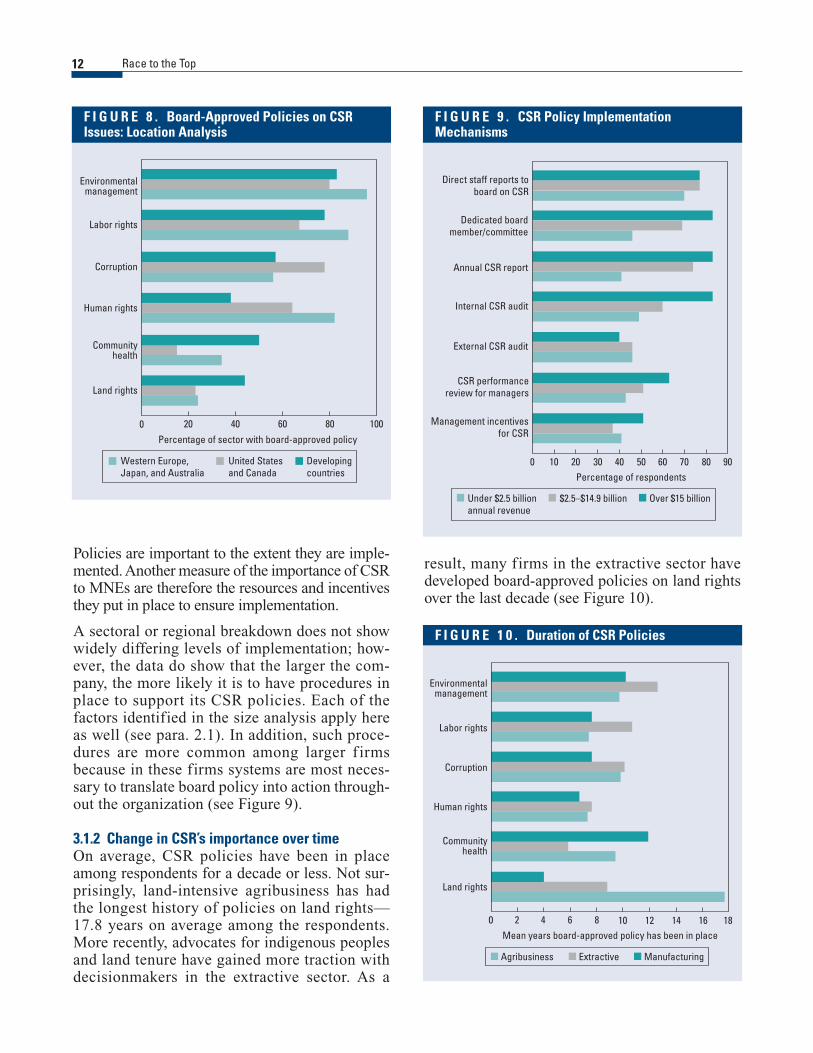

Respondents in the extractive sector reported sig-nificantly higher percentages of board-approvedpolicies for land rights and environmental issues.Extractive sector operations have large geographicfootprints. They are distinguished from agribusi-ness in that they do not have supply agreementswith independent landowners and so in most casesmust negotiate for the land on which they willoperate (see Figure 7).

Overall, the U.S., Canadian, and Australianrespondents have developed board-approved poli-cies on fewer issues than participating companiesbased in Western Europe. A significant exception

is in the area of corruption, the CSR issue on whichU.S. law is most explicit and well established.

Developing-country respondents, on the otherhand, outstrip their wealthier counterparts on com-munity health policies. Interviewees indicated thatthis is a direct response to the HIV/AIDS crisis inparts of the developing world (see Figure 8).

Analysis of Survey Results

3

11

0 10 20 30 40 50 60 70 80 90Percentage of respondents

Land rights

Communityhealth

Human rights

Corruption

Labor rights

Environmentalmanagement

F I G U R E 6 . Board-Approved Policies on CSRIssues: All Respondents

0 10 20 30 40 50 60 70 80 90 100Percentage of respondents

Land rights

Environmentalmanagement

Agribusiness Extractive Manufacturing

F I G U R E 7 . Board-Approved Policies on CSR Issues: Distinctions by Sector

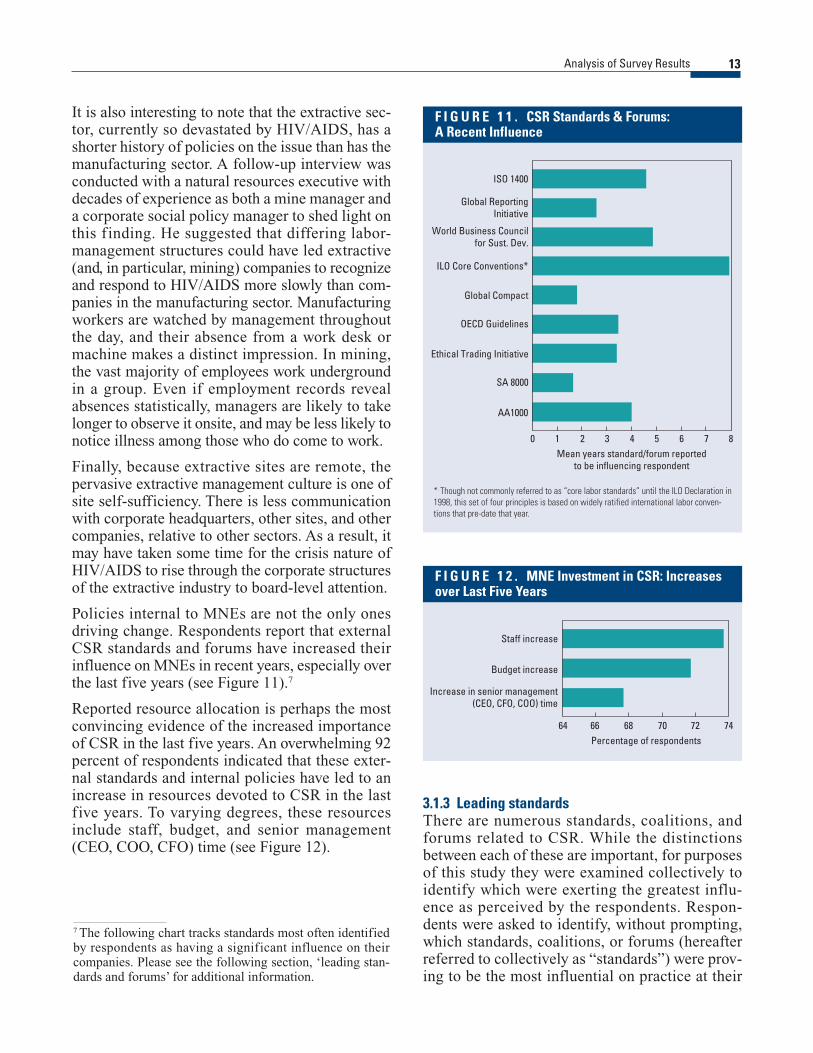

Policies are important to the extent they are imple-mented. Another measure of the importance of CSRto MNEs are therefore the resources and incentivesthey put in place to ensure implementation.

A sectoral or regional breakdown does not showwidely differing levels of implementation; how-ever, the data do show that the larger the com-pany, the more likely it is to have procedures inplace to support its CSR policies. Each of thefactors identified in the size analysis apply hereas well (see para. 2.1). In addition, such proce-dures are more common among larger f irmsbecause in these firms systems are most neces-sary to translate board policy into action through-out the organization (see Figure 9).

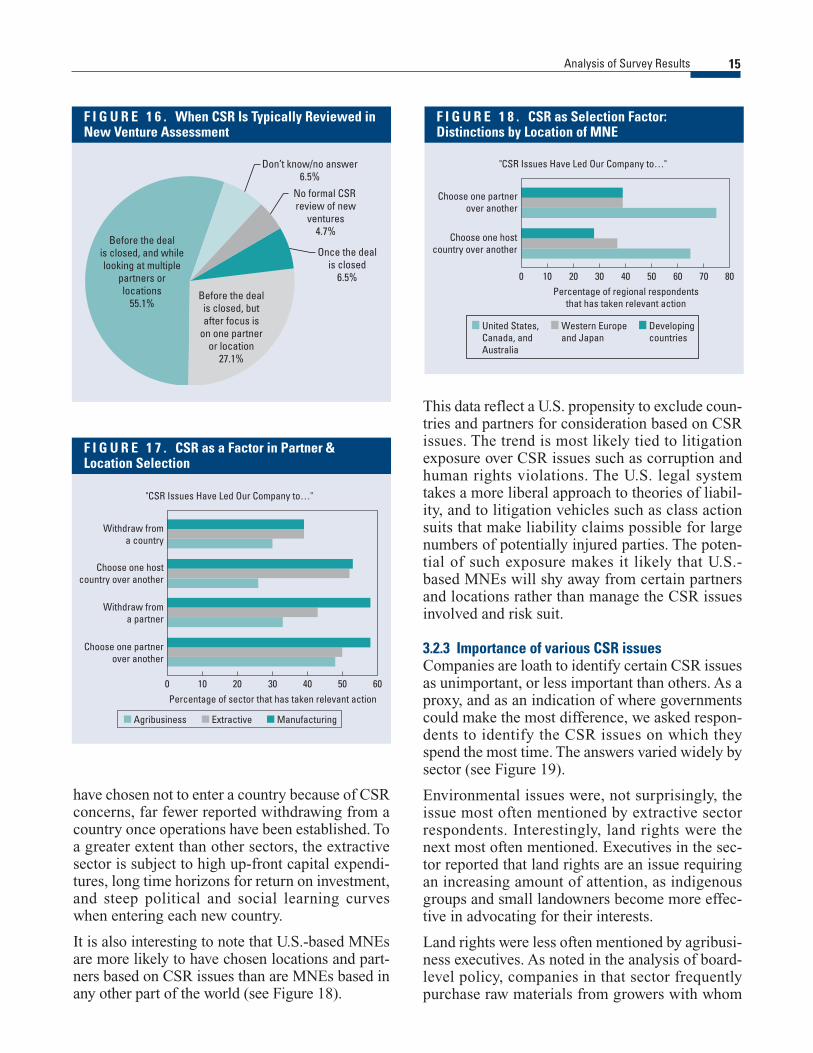

3.1.2 Change in CSR’s importance over timeOn average, CSR policies have been in placeamong respondents for a decade or less. Not sur-prisingly, land-intensive agribusiness has had the longest history of policies on land rights—17.8 years on average among the respondents.More recently, advocates for indigenous peoplesand land tenure have gained more traction withdecisionmakers in the extractive sector. As a

result, many firms in the extractive sector havedeveloped board-approved policies on land rightsover the last decade (see Figure 10).

Race to the Top12

Western Europe,Japan, and Australia

United Statesand Canada

Developingcountries

0 20 40 60 80 100Percentage of sector with board-approved policy

Land rights

Communityhealth

Human rights

Corruption

Labor rights

Environmentalmanagement

F I G U R E 8 . Board-Approved Policies on CSRIssues: Location Analysis

0 90807060302010 5040Percentage of respondents

Direct staff reports toboard on CSR

Dedicated boardmember/committee

Annual CSR report

Internal CSR audit

External CSR audit

CSR performancereview for managers

Management incentivesfor CSR

Under $2.5 billion annual revenue

$2.5–$14.9 billion Over $15 billion

F I G U R E 9 . CSR Policy ImplementationMechanisms

0 2 4 6 8 10 12 14 16 18Mean years board-approved policy has been in place

Land rights

Communityhealth

Human rights

Corruption

Labor rights

Environmentalmanagement

Agribusiness Extractive Manufacturing

F I G U R E 1 0 . Duration of CSR Policies

Analysis of Survey Results 13

It is also interesting to note that the extractive sec-tor, currently so devastated by HIV/AIDS, has ashorter history of policies on the issue than has themanufacturing sector. A follow-up interview wasconducted with a natural resources executive withdecades of experience as both a mine manager anda corporate social policy manager to shed light onthis finding. He suggested that differing labor-management structures could have led extractive(and, in particular, mining) companies to recognizeand respond to HIV/AIDS more slowly than com-panies in the manufacturing sector. Manufacturingworkers are watched by management throughoutthe day, and their absence from a work desk ormachine makes a distinct impression. In mining,the vast majority of employees work undergroundin a group. Even if employment records revealabsences statistically, managers are likely to takelonger to observe it onsite, and may be less likely tonotice illness among those who do come to work.

Finally, because extractive sites are remote, thepervasive extractive management culture is one ofsite self-sufficiency. There is less communicationwith corporate headquarters, other sites, and othercompanies, relative to other sectors. As a result, itmay have taken some time for the crisis nature ofHIV/AIDS to rise through the corporate structuresof the extractive industry to board-level attention.

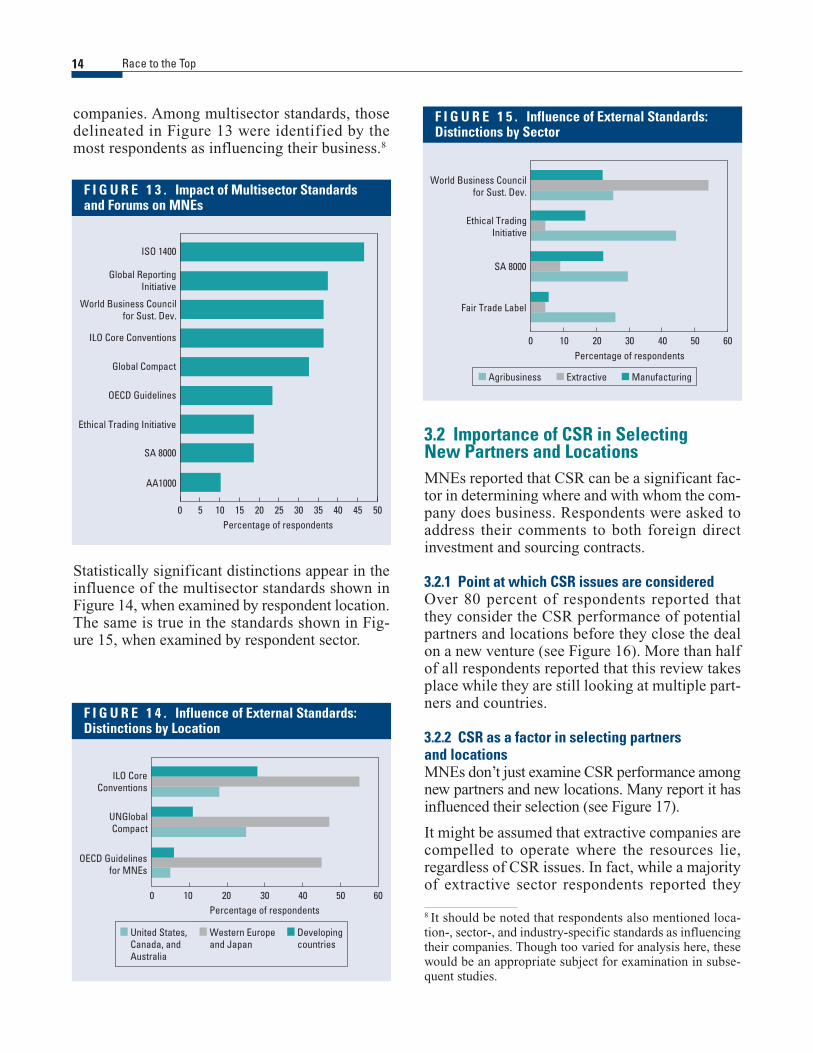

Policies internal to MNEs are not the only onesdriving change. Respondents report that externalCSR standards and forums have increased theirinfluence on MNEs in recent years, especially overthe last five years (see Figure 11).7

Reported resource allocation is perhaps the mostconvincing evidence of the increased importanceof CSR in the last five years. An overwhelming 92percent of respondents indicated that these exter-nal standards and internal policies have led to anincrease in resources devoted to CSR in the lastfive years. To varying degrees, these resourcesinclude staff, budget, and senior management(CEO, COO, CFO) time (see Figure 12).

3.1.3 Leading standardsThere are numerous standards, coalitions, andforums related to CSR. While the distinctionsbetween each of these are important, for purposesof this study they were examined collectively toidentify which were exerting the greatest influ-ence as perceived by the respondents. Respon-dents were asked to identify, without prompting,which standards, coalitions, or forums (hereafterreferred to collectively as “standards”) were prov-ing to be the most influential on practice at their

7 The following chart tracks standards most often identifiedby respondents as having a significant influence on theircompanies. Please see the following section, ‘leading stan-dards and forums’ for additional information.

0 1 87652 3 4Mean years standard/forum reported

to be influencing respondent

ISO 1400

Global ReportingInitiative

World Business Councilfor Sust. Dev.

ILO Core Conventions*

Global Compact

OECD Guidelines

Ethical Trading Initiative

SA 8000

AA1000

F I G U R E 1 1 . CSR Standards & Forums: A Recent Influence

*. Though not commonly referred to as “core labor standards” until the ILO Declaration in1998, this set of four principles is based on widely ratified international labor conven-tions that pre-date that year.

64 66 68 70 72 74Percentage of respondents

Staff increase

Budget increase

Increase in senior management(CEO, CFO, COO) time

F I G U R E 1 2 . MNE Investment in CSR: Increasesover Last Five Years

companies. Among multisector standards, thosedelineated in Figure 13 were identif ied by themost respondents as influencing their business.8

Race to the Top14

3.2 Importance of CSR in Selecting New Partners and LocationsMNEs reported that CSR can be a significant fac-tor in determining where and with whom the com-pany does business. Respondents were asked toaddress their comments to both foreign directinvestment and sourcing contracts.

3.2.1 Point at which CSR issues are consideredOver 80 percent of respondents reported thatthey consider the CSR performance of potentialpartners and locations before they close the dealon a new venture (see Figure 16). More than halfof all respondents reported that this review takesplace while they are still looking at multiple part-ners and countries.

3.2.2 CSR as a factor in selecting partners and locationsMNEs don’t just examine CSR performance amongnew partners and new locations. Many report it hasinfluenced their selection (see Figure 17).

It might be assumed that extractive companies arecompelled to operate where the resources lie,regardless of CSR issues. In fact, while a majorityof extractive sector respondents reported they

0 5 10 15 20 25 30 35 40 45 50Percentage of respondents

ISO 1400

Global ReportingInitiative

World Business Councilfor Sust. Dev.

Global Compact

ILO Core Conventions

OECD Guidelines

SA 8000

Ethical Trading Initiative

AA1000

F I G U R E 1 3 . Impact of Multisector Standards and Forums on MNEs

0 605040302010Percentage of respondents

ILO CoreConventions

UNGlobalCompact

OECD Guidelinesfor MNEs

United States,Canada, andAustralia

Western Europeand Japan

Developingcountries

F I G U R E 1 4 . Influence of External Standards:Distinctions by Location

0 605040302010Percentage of respondents

World Business Councilfor Sust. Dev.

Ethical TradingInitiative

SA 8000

Fair Trade Label

Agribusiness Extractive Manufacturing

F I G U R E 1 5 . Influence of External Standards:Distinctions by Sector

8 It should be noted that respondents also mentioned loca-tion-, sector-, and industry-specific standards as influencingtheir companies. Though too varied for analysis here, thesewould be an appropriate subject for examination in subse-quent studies.

Statistically significant distinctions appear in theinfluence of the multisector standards shown inFigure 14, when examined by respondent location.The same is true in the standards shown in Fig-ure 15, when examined by respondent sector.

Analysis of Survey Results 15

This data reflect a U.S. propensity to exclude coun-tries and partners for consideration based on CSRissues. The trend is most likely tied to litigationexposure over CSR issues such as corruption andhuman rights violations. The U.S. legal systemtakes a more liberal approach to theories of liabil-ity, and to litigation vehicles such as class actionsuits that make liability claims possible for largenumbers of potentially injured parties. The poten-tial of such exposure makes it likely that U.S.-based MNEs will shy away from certain partnersand locations rather than manage the CSR issuesinvolved and risk suit.

3.2.3 Importance of various CSR issuesCompanies are loath to identify certain CSR issuesas unimportant, or less important than others. As aproxy, and as an indication of where governmentscould make the most difference, we asked respon-dents to identify the CSR issues on which theyspend the most time. The answers varied widely bysector (see Figure 19).

Environmental issues were, not surprisingly, theissue most often mentioned by extractive sectorrespondents. Interestingly, land rights were thenext most often mentioned. Executives in the sec-tor reported that land rights are an issue requiringan increasing amount of attention, as indigenousgroups and small landowners become more effec-tive in advocating for their interests.

Land rights were less often mentioned by agribusi-ness executives. As noted in the analysis of board-level policy, companies in that sector frequentlypurchase raw materials from growers with whom

have chosen not to enter a country because of CSRconcerns, far fewer reported withdrawing from acountry once operations have been established. Toa greater extent than other sectors, the extractivesector is subject to high up-front capital expendi-tures, long time horizons for return on investment,and steep political and social learning curveswhen entering each new country.

It is also interesting to note that U.S.-based MNEsare more likely to have chosen locations and part-ners based on CSR issues than are MNEs based inany other part of the world (see Figure 18).

Don’t know/no answer6.5%

No formal CSR review of new

ventures4.7%

Once the dealis closed

6.5%

Before the dealis closed, butafter focus is

on one partneror location

27.1%

Before the dealis closed, and whilelooking at multiple

partners orlocations

55.1%

F I G U R E 1 6 . When CSR Is Typically Reviewed inNew Venture Assessment

Withdraw froma country

Choose one hostcountry over another

Withdraw froma partner

Choose one partnerover another

"CSR Issues Have Led Our Company to…"

0 10 20 30 40 50 60Percentage of sector that has taken relevant action

Agribusiness Extractive Manufacturing

F I G U R E 1 7 . CSR as a Factor in Partner &Location Selection

"CSR Issues Have Led Our Company to…"

0 8070605040302010Percentage of regional respondents

that has taken relevant action

Choose one hostcountry over another

Choose one partnerover another

United States,Canada, andAustralia

Western Europeand Japan

Developingcountries

F I G U R E 1 8 . CSR as Selection Factor:Distinctions by Location of MNE

they do not have an equity relationship, therebyestablishing a distance from land tenure issues thatextractive companies do not enjoy. Manufacturingfirms use less land, often lease the land they douse, and are more likely to operate in industrialcenters where land ownership is more clearlydefined.

Corruption was frequently mentioned by re-spondents in all sectors as a challenging CSRissue. Executives elaborated in open-ended re-sponses that their greatest challenge in this regardis responding to uneven enforcement of laws. Asdiscussed in greater length below, evenly appliedenforcement of the law is a priority for foreigninvestors and purchasers.

3.2.4 Sources used to assess CSR issues in new venturesRespondents were asked where they get the infor-mation for their CSR assessments of both newlocations and new partners. The assessments ofthe companies’ own staff are clearly the mostimportant source, with outside sources playing animportant supplementary role (see Figure 20).

When responses are examined by sector, it’s clearthat agribusiness respondents reported the lowestuse of nearly every source (statistically significantdistinctions appear in Figure 21). Several agribus-iness respondents indicated that they purchasethrough commodity brokers and traders, or com-

Race to the Top16

0 908070605040302010Percentage of respondents

Land rights

Human rights

Corruption

Labor rights

Environmentalmanagement

Agribusiness Extractive Manufacturing

F I G U R E 1 9 . CSR Issues on which the Most Time Is Spent

0 70605040302010Percentage of respondents

Company staffassessments

Retained experts

Home government

Host government

NGOs/churchgroups

Other companies

Media

General riskpublications

CSR publications

Trade unions

Other

F I G U R E 2 0 . How MNEs Gather Information on CSR Issues

0 10 20 30 40 50 60 70 80Percentage of respondents

Company staffassessments

Retainedexperts

Homegovernment

Hostgovernment

NGOs/churchgroups

Othercompanies

General riskpublications

CSRpublications

Agribusiness Extractive Manufacturing

F I G U R E 2 1 . How MNEs Gather Information on CSR Issues: Distinctions by Sector

modity marketing boards, thereby reducing theirrelationship to the location where the commodityis grown. As indicated in Figure 21, this dynamicseems to extend to verification of local partnercommitments as well. It should be noted that inWestern Europe, where projects such as the Ethi-cal Trading Initiative have sought to pierce thisanonymity in commodity foods, agribusinessrespondents reported greater attention to gatheringCSR information.

In addition to the findings shown above, whichreflect the sector analysis, the data also show thatcompanies from wealthier countries use all sourcesof CSR information more than companies from thedeveloping world. For resources such as special-ized publications and outside consultants, this maywell be a function of available financial resources.However, companies from wealthier countries arealso more likely to tap low-cost sources of infor-mation, such as nongovernmental organizations(NGOs), church groups, and other companies.

Interestingly, this gap disappears when it comes totalking with trade unions. Unions were morelikely to be consulted by developing-countryrespondents than by their counterparts based inthe United States, Canada, and Australia. In par-ticular, U.S.-based MNEs frequently indicated inopen responses that they did not perceive unionsas valuable sources of information, or indeed asvaluable interlocutors on CSR generally. On thewhole, participants based in Western Europe didnot share this view, as indicated in Figure 22.

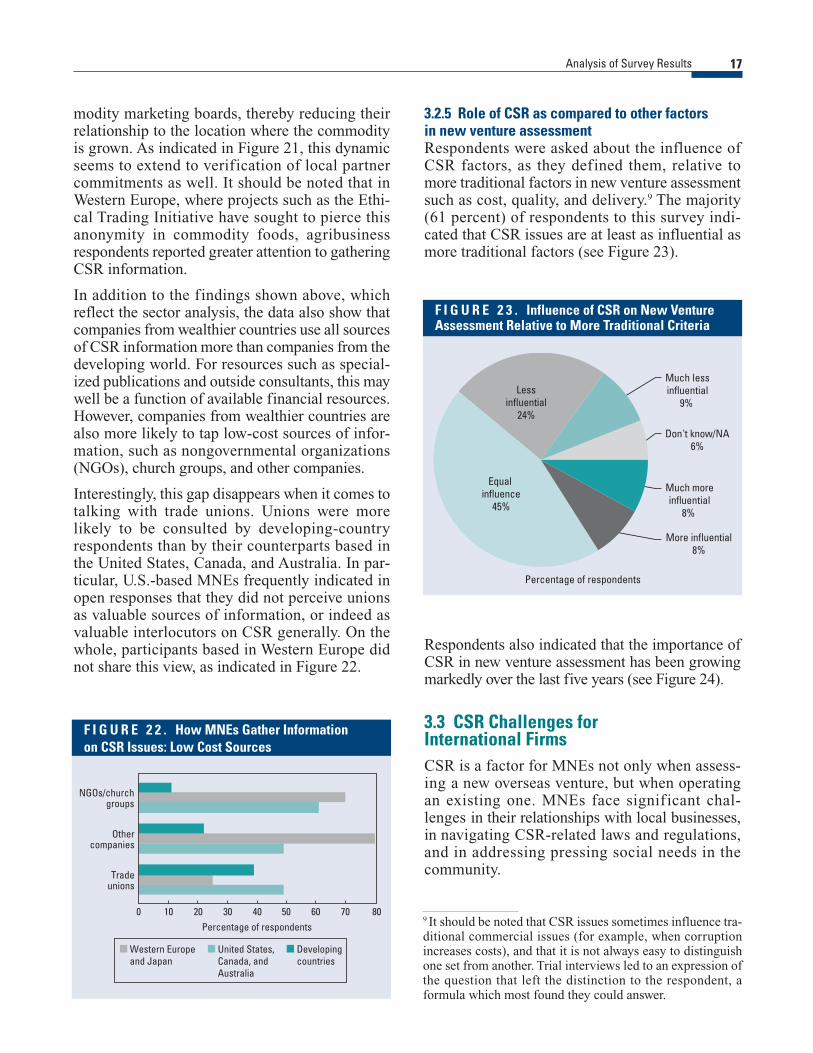

3.2.5 Role of CSR as compared to other factors in new venture assessmentRespondents were asked about the influence ofCSR factors, as they defined them, relative tomore traditional factors in new venture assessmentsuch as cost, quality, and delivery.9 The majority(61 percent) of respondents to this survey indi-cated that CSR issues are at least as influential asmore traditional factors (see Figure 23).

Analysis of Survey Results 17

0 10 20 30 40 50 60 70 80Percentage of respondents

NGOs/churchgroups

Othercompanies

Tradeunions

United States,Canada, andAustralia

Western Europeand Japan

Developingcountries

F I G U R E 2 2 . How MNEs Gather Information on CSR Issues: Low Cost Sources

9 It should be noted that CSR issues sometimes influence tra-ditional commercial issues (for example, when corruptionincreases costs), and that it is not always easy to distinguishone set from another. Trial interviews led to an expression ofthe question that left the distinction to the respondent, aformula which most found they could answer.

Percentage of respondents

Much moreinfluential

8%

More influential8%

Don't know/NA6%

Much lessinfluential

9% Less

influential24%

Equal influence

45%

F I G U R E 2 3 . Influence of CSR on New VentureAssessment Relative to More Traditional Criteria

Respondents also indicated that the importance ofCSR in new venture assessment has been growingmarkedly over the last five years (see Figure 24).

3.3 CSR Challenges for International FirmsCSR is a factor for MNEs not only when assess-ing a new overseas venture, but when operating an existing one. MNEs face signif icant chal-lenges in their relationships with local businesses,in navigating CSR-related laws and regulations,and in addressing pressing social needs in thecommunity.

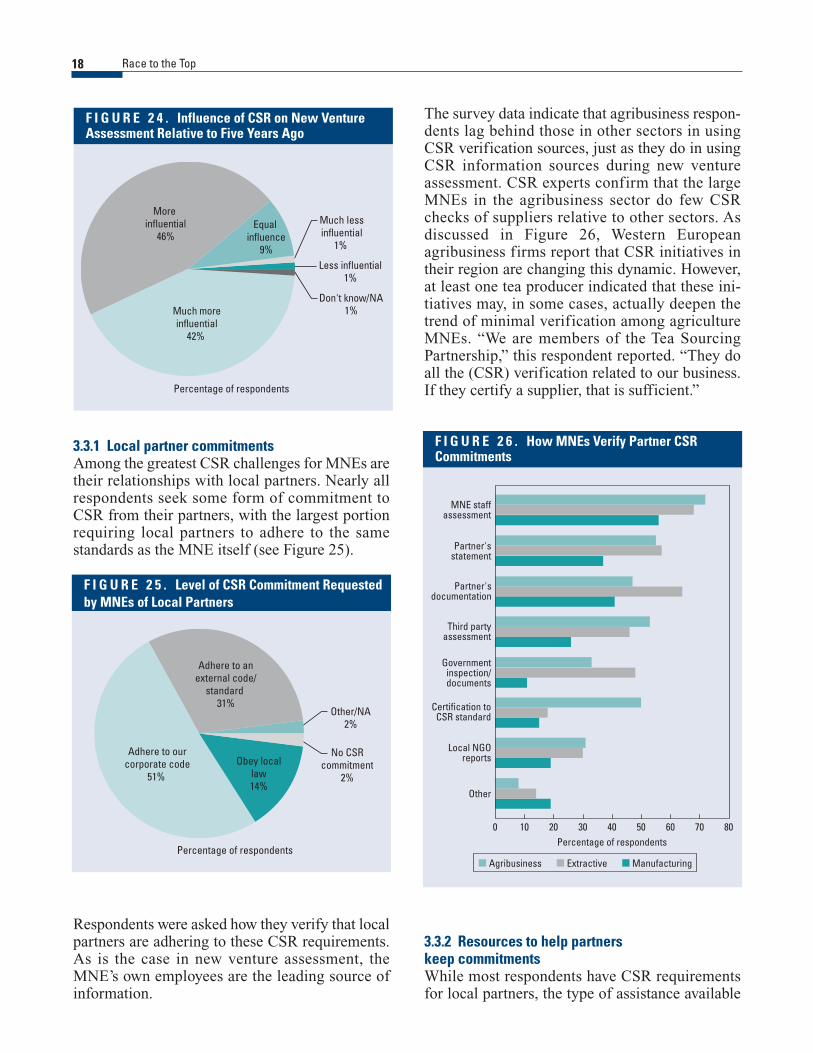

3.3.1 Local partner commitmentsAmong the greatest CSR challenges for MNEs aretheir relationships with local partners. Nearly allrespondents seek some form of commitment toCSR from their partners, with the largest portionrequiring local partners to adhere to the samestandards as the MNE itself (see Figure 25).

The survey data indicate that agribusiness respon-dents lag behind those in other sectors in usingCSR verification sources, just as they do in usingCSR information sources during new ventureassessment. CSR experts confirm that the largeMNEs in the agribusiness sector do few CSRchecks of suppliers relative to other sectors. Asdiscussed in Figure 26, Western Europeanagribusiness firms report that CSR initiatives intheir region are changing this dynamic. However,at least one tea producer indicated that these ini-tiatives may, in some cases, actually deepen thetrend of minimal verification among agricultureMNEs. “We are members of the Tea SourcingPartnership,” this respondent reported. “They doall the (CSR) verification related to our business.If they certify a supplier, that is sufficient.”

Race to the Top18

Percentage of respondents

Much moreinfluential

42%

Don't know/NA1%

Much lessinfluential

1%

Less influential1%

Equal influence

9%

More influential

46%

F I G U R E 2 4 . Influence of CSR on New VentureAssessment Relative to Five Years Ago

Obey locallaw14%

Adhere to anexternal code/

standard 31%

Adhere to ourcorporate code

51%

Other/NA2%

No CSRcommitment

2%

Percentage of respondents

F I G U R E 2 5 . Level of CSR Commitment Requestedby MNEs of Local Partners

0 10 20 30 40 50 60 70 80Percentage of respondents

MNE staffassessment

Partner'sstatement

Partner'sdocumentation

Third partyassessment

Governmentinspection/documents

Certification toCSR standard

Local NGOreports

Other

Agribusiness Extractive Manufacturing

F I G U R E 2 6 . How MNEs Verify Partner CSRCommitments

Respondents were asked how they verify that localpartners are adhering to these CSR requirements.As is the case in new venture assessment, theMNE’s own employees are the leading source ofinformation.

3.3.2 Resources to help partners keep commitmentsWhile most respondents have CSR requirementsfor local partners, the type of assistance available

Analysis of Survey Results 19

to help partners meet those commitments is quitelimited. Seventy-two percent of respondents doreport that they assist local partners in this regard.However, when asked to describe what kind ofassistance is available from the MNE, it appears tobe mostly in the form of instruction as to what isexpected (see Figure 27).

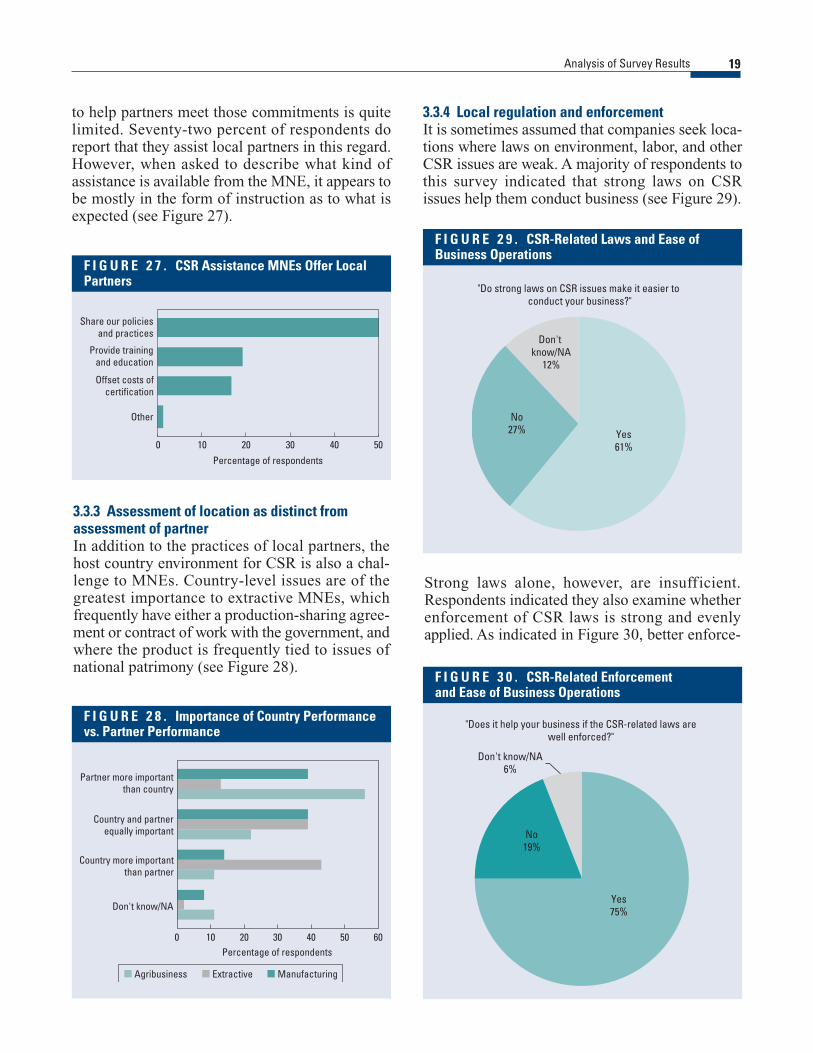

3.3.4 Local regulation and enforcementIt is sometimes assumed that companies seek loca-tions where laws on environment, labor, and otherCSR issues are weak. A majority of respondents tothis survey indicated that strong laws on CSRissues help them conduct business (see Figure 29).

50403020100

Percentage of respondents

Share our policiesand practices

Provide trainingand education

Offset costs ofcertification

Other

F I G U R E 2 7 . CSR Assistance MNEs Offer LocalPartners

0 10 20 30 40 50 60Percentage of respondents

Partner more importantthan country

Country and partnerequally important

Country more importantthan partner

Don't know/NA

Agribusiness Extractive Manufacturing

F I G U R E 2 8 . Importance of Country Performancevs. Partner Performance

Don't know/NA

12%

No27% Yes

61%

"Do strong laws on CSR issues make it easier to conduct your business?"

F I G U R E 2 9 . CSR-Related Laws and Ease ofBusiness Operations

3.3.3 Assessment of location as distinct fromassessment of partnerIn addition to the practices of local partners, thehost country environment for CSR is also a chal-lenge to MNEs. Country-level issues are of thegreatest importance to extractive MNEs, whichfrequently have either a production-sharing agree-ment or contract of work with the government, andwhere the product is frequently tied to issues ofnational patrimony (see Figure 28).

Strong laws alone, however, are insufficient.Respondents indicated they also examine whetherenforcement of CSR laws is strong and evenlyapplied. As indicated in Figure 30, better enforce-

No19%

Yes75%

Don't know/NA6%

"Does it help your business if the CSR-related laws arewell enforced?"

F I G U R E 3 0 . CSR-Related Enforcement and Ease of Business Operations

ment of CSR laws is among the government rolesmost sought by respondents.

3.3.5 Local social needsAs part of their CSR programs, the overwhelm-ing majority of respondents reported they areactive in community issues “beyond the factorygates” when doing business abroad. This is espe-cially true of companies based in wealthiercountries (see Figure 31).

Education and training, with its close associationto workforce needs, is the social issue in whichrespondents most often participate. Communityhealth, environmental preservation, and povertyeradication also attract participation from a major-ity of the companies active “beyond the factorygates” (see Figure 33).

Race to the Top20

0 10 20 30 40 50 60 70 80 90Percentage of respondents

Yes

No

Don't know/NA

Does your company become active in social issues"beyond the factory gates?"

United States,Canada, andAustralia

Western Europeand Japan

Developingcountries

F I G U R E 3 1 . MNE Engagement in CommunityIssues, by Location of Firm

0 10 20 30 40 50 60 70 80 90Percentage of respondents

Yes

No

Don't know/NA

Does your company become active in social issues"beyond the factory gates?"

Under $2.5 billion annual revenue

$2.5–$14.9 billion Over $15 billion

F I G U R E 3 2 . MNE Engagement in CommunityIssues, by Size of Firm

0 20 40 60 80 100

Percentage of respondents

Education andtraining

Communityhealth

RegionalEnvironment

Povertyeradication

National/locallabor standards

Human andcivil rights

Indigenous peoplesand land rights

Regionaldevelopment

Other

F I G U R E 3 3 . Community Issues in Which MNEsAre Active

To a more modest extent, the data also indicatethat larger companies are more likely to be activein social issues than smaller ones (see Figure 32).

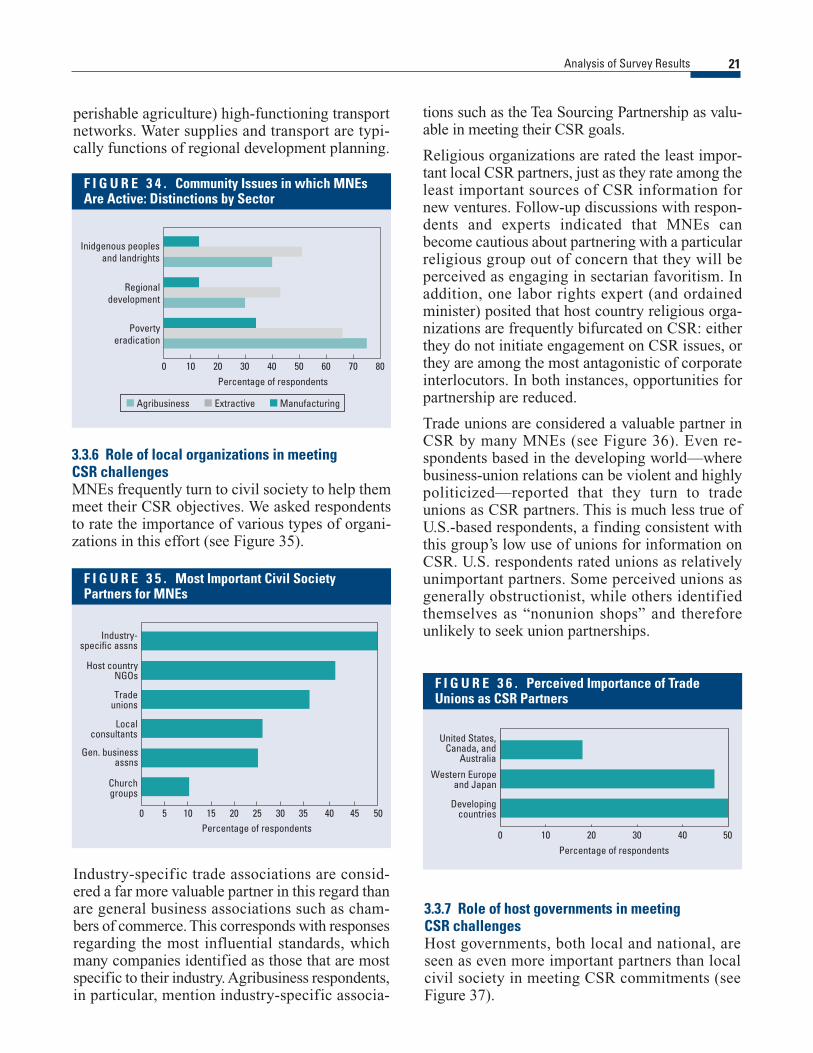

Land tenure and the rights of indigenous peoplesare issues in which agribusiness and extractive sec-tor respondents report they are significantly moreinvolved. These sectors are land-dependent, withthe exception of offshore extraction. They also tendto operate in less developed areas, where landtenure is less defined and the rights of indigenouspeoples more at issue.

The other issues on which there is statistically sig-nificant variation among sectors are regionaldevelopment and poverty eradication (see Fig-ure 34). Extractive and agribusiness respondentsare heavily engaged in poverty eradication andregional development planning. Extractive opera-tions can generate dramatic alterations in the eco-nomic and social landscape of the communities inwhich they occur. It is routine for their licenses tooperate to require that they plan for and respond to these changes. This is also true in agribusiness,albeit to a lesser extent. Agribusiness is alsohighly dependent on local water and (especially in

Analysis of Survey Results 21

3.3.6 Role of local organizations in meeting CSR challengesMNEs frequently turn to civil society to help themmeet their CSR objectives. We asked respondentsto rate the importance of various types of organi-zations in this effort (see Figure 35).

tions such as the Tea Sourcing Partnership as valu-able in meeting their CSR goals.

Religious organizations are rated the least impor-tant local CSR partners, just as they rate among theleast important sources of CSR information fornew ventures. Follow-up discussions with respon-dents and experts indicated that MNEs canbecome cautious about partnering with a particularreligious group out of concern that they will beperceived as engaging in sectarian favoritism. Inaddition, one labor rights expert (and ordainedminister) posited that host country religious orga-nizations are frequently bifurcated on CSR: eitherthey do not initiate engagement on CSR issues, orthey are among the most antagonistic of corporateinterlocutors. In both instances, opportunities forpartnership are reduced.

Trade unions are considered a valuable partner inCSR by many MNEs (see Figure 36). Even re-spondents based in the developing world—wherebusiness-union relations can be violent and highlypoliticized—reported that they turn to tradeunions as CSR partners. This is much less true ofU.S.-based respondents, a finding consistent withthis group’s low use of unions for information onCSR. U.S. respondents rated unions as relativelyunimportant partners. Some perceived unions asgenerally obstructionist, while others identifiedthemselves as “nonunion shops” and thereforeunlikely to seek union partnerships.

0 5 10 15 20 25 30 35 40 45 50Percentage of respondents

Industry-specific assns

Host countryNGOs

Tradeunions

Localconsultants

Gen. businessassns

Churchgroups

F I G U R E 3 5 . Most Important Civil SocietyPartners for MNEs

0 10 20 30 40 50 60 70 80Percentage of respondents

Inidgenous peoplesand landrights

Regional development

Povertyeradication

Agribusiness Extractive Manufacturing

F I G U R E 3 4 . Community Issues in which MNEsAre Active: Distinctions by Sector

0 10 20 30 40 50Percentage of respondents

United States,Canada, and

Australia

Western Europeand Japan

Developingcountries

F I G U R E 3 6 . Perceived Importance of TradeUnions as CSR Partners

Industry-specific trade associations are consid-ered a far more valuable partner in this regard thanare general business associations such as cham-bers of commerce. This corresponds with responsesregarding the most influential standards, whichmany companies identified as those that are mostspecific to their industry. Agribusiness respondents,in particular, mention industry-specific associa-

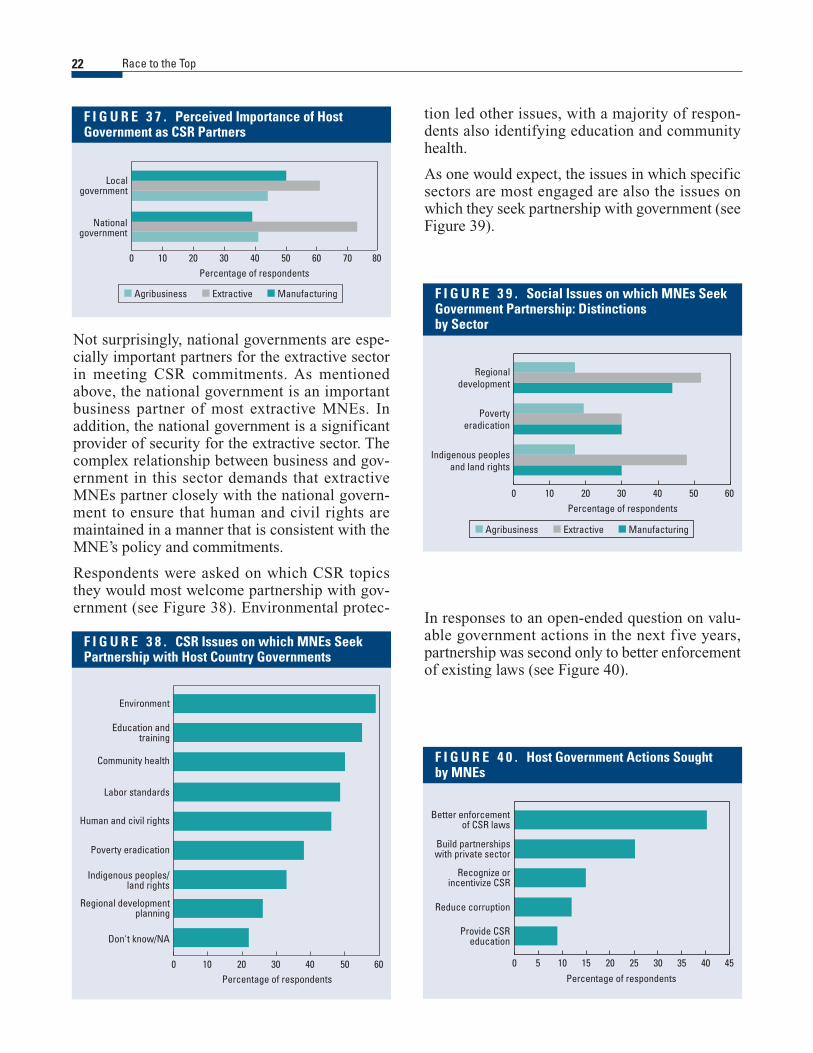

3.3.7 Role of host governments in meeting CSR challengesHost governments, both local and national, areseen as even more important partners than localcivil society in meeting CSR commitments (seeFigure 37).

perishable agriculture) high-functioning transportnetworks. Water supplies and transport are typi-cally functions of regional development planning.

Race to the Top22

0 10 20 30 40 50 60 70 80Percentage of respondents

Localgovernment

Nationalgovernment

Agribusiness Extractive Manufacturing

F I G U R E 3 7 . Perceived Importance of HostGovernment as CSR Partners

0 605040302010Percentage of respondents

Environment

Education andtraining

Community health

Labor standards

Human and civil rights

Poverty eradication

Indigenous peoples/land rights

Regional developmentplanning

Don't know/NA

F I G U R E 3 8 . CSR Issues on which MNEs SeekPartnership with Host Country Governments

0 605040302010Percentage of respondents

Regionaldevelopment

Povertyeradication

Indigenous peoplesand land rights

Agribusiness Extractive Manufacturing

F I G U R E 3 9 . Social Issues on which MNEs SeekGovernment Partnership: Distinctions by Sector

0 5 10 15 20 25 30 35 40 45Percentage of respondents

Better enforcementof CSR laws

Build partnershipswith private sector

Recognize orincentivize CSR

Reduce corruption

Provide CSReducation

F I G U R E 4 0 . Host Government Actions Sought by MNEs

Not surprisingly, national governments are espe-cially important partners for the extractive sectorin meeting CSR commitments. As mentionedabove, the national government is an importantbusiness partner of most extractive MNEs. Inaddition, the national government is a significantprovider of security for the extractive sector. Thecomplex relationship between business and gov-ernment in this sector demands that extractiveMNEs partner closely with the national govern-ment to ensure that human and civil rights aremaintained in a manner that is consistent with theMNE’s policy and commitments.

Respondents were asked on which CSR topicsthey would most welcome partnership with gov-ernment (see Figure 38). Environmental protec-

tion led other issues, with a majority of respon-dents also identifying education and communityhealth.

As one would expect, the issues in which specificsectors are most engaged are also the issues onwhich they seek partnership with government (seeFigure 39).

In responses to an open-ended question on valu-able government actions in the next five years,partnership was second only to better enforcementof existing laws (see Figure 40).

Analysis of Survey Results 23

3.3.8 Partnerships sought with governmentsThe kinds of public-private partnerships sought byrespondents vary widely.10 Respondents withextensive resources for community development(mostly in the extractive sector, but including afew agribusiness firms) are eager to coordinatetheir programs with those of national and regionalgovernments.

Even companies with limited community develop-ment funds expressed interest in participating in theplanning of government programs directly related totheir operations. Apparel companies in both Europeand the United States, for example, indicated theirinterest in working with trade ministries to help edu-cate local suppliers on CSR needs. Companies in allsectors indicated a desire to support education mea-sures that would lead to a more viable workforce.Many reported they are prepared to offer skills trans-fer to support such planning.

To a greater extent than other respondents, manu-facturing companies indicated they are interestedin partnerships that are related to their productlines. For example, one IT company is interested inworking with host country schools to enhancecomputer literacy and facility with the internet,while a large medical electronics company indi-cated it would welcome partnership with thenational health department to increase access to itstechnologies.

Not all manufacturing respondents limited theircomments on partnership to their product lines. Afew expressed interest in using their workplaces(and those of their suppliers) to facilitate socialprograms. One U.S. shoe manufacturer, for exam-ple, expressed interest in working with healthdepartments to promote preventive health carethrough factory visits.

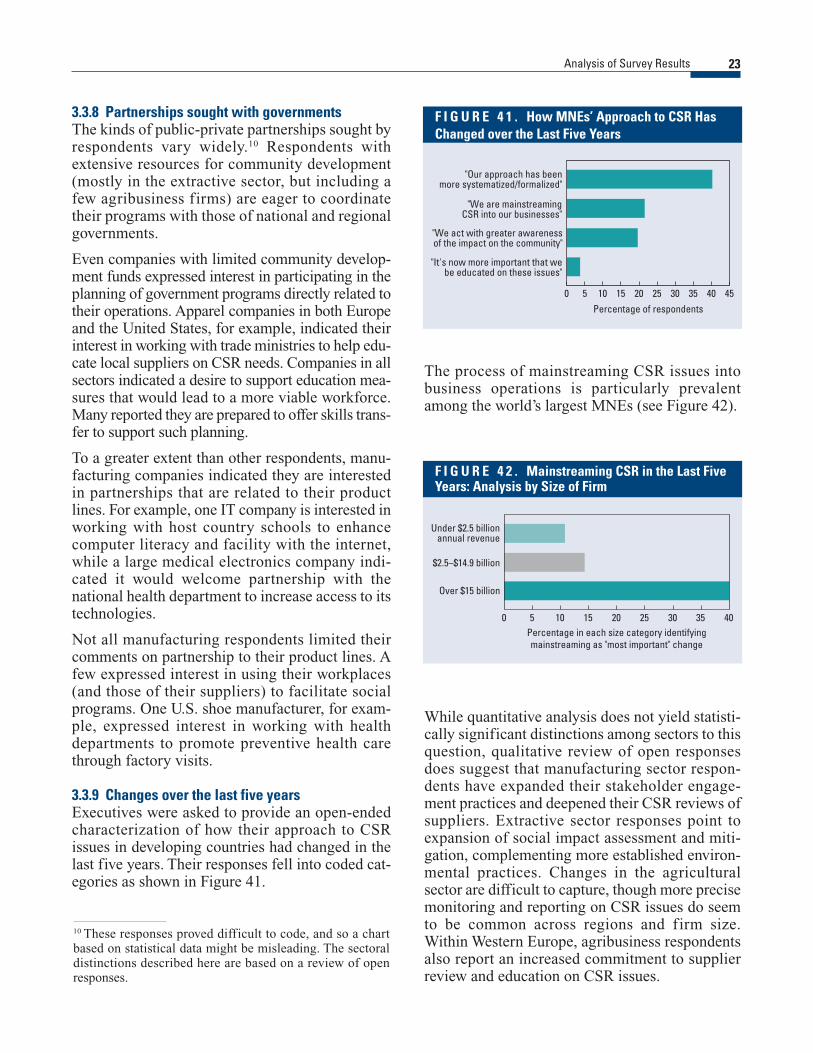

3.3.9 Changes over the last five yearsExecutives were asked to provide an open-endedcharacterization of how their approach to CSRissues in developing countries had changed in thelast five years. Their responses fell into coded cat-egories as shown in Figure 41.

10 These responses proved difficult to code, and so a chartbased on statistical data might be misleading. The sectoraldistinctions described here are based on a review of openresponses.

0 5 10 15 20 25 30 35 40 45Percentage of respondents

"Our approach has beenmore systematized/formalized"

"We are mainstreamingCSR into our businesses"

"We act with greater awarenessof the impact on the community"

"It's now more important that webe educated on these issues"

F I G U R E 4 1 . How MNEs’ Approach to CSR HasChanged over the Last Five Years

0 5 10 15 20 25 30 35 40Percentage in each size category identifyingmainstreaming as "most important" change

Under $2.5 billionannual revenue

$2.5–$14.9 billion

Over $15 billion

F I G U R E 4 2 . Mainstreaming CSR in the Last FiveYears: Analysis by Size of Firm

The process of mainstreaming CSR issues intobusiness operations is particularly prevalentamong the world’s largest MNEs (see Figure 42).

While quantitative analysis does not yield statisti-cally significant distinctions among sectors to thisquestion, qualitative review of open responsesdoes suggest that manufacturing sector respon-dents have expanded their stakeholder engage-ment practices and deepened their CSR reviews ofsuppliers. Extractive sector responses point toexpansion of social impact assessment and miti-gation, complementing more established environ-mental practices. Changes in the agriculturalsector are difficult to capture, though more precisemonitoring and reporting on CSR issues do seemto be common across regions and firm size.Within Western Europe, agribusiness respondentsalso report an increased commitment to supplierreview and education on CSR issues.

The study’s findings offer conclusions and rec-ommendations for a wide range of actors,

including development institutions, home govern-ments, and civil society. However, given the focusof the CSR Practice on the role of the public sec-tor in providing an enabling environment forcorporate social responsibility, conclusions andrecommendations focus on implications for hostcountries and, specifically, opportunities for hostgovernment action.

Conclusions and recommendations fall into twobroad categories:

� Attracting sustainable trade and investment� Enabling sustainable trade and investment.

4.1 Attracting Sustainable Trade and InvestmentThe results of the survey suggest that CSR issuesplay an important and growing role when MNEsconsider new trade and investment ventures. TheWorld Bank Group’s Investment Climate Depart-ment is identifying links between effective tradeand investment attraction and the CSR interests ofmultinational enterprises. Based on this study, thefollowing conclusions and resulting recommenda-tions are presented:

4.1.1 Strong laws, strongly enforcedAccording to the MNEs participating in this study,a “race to the bottom” of CSR laws and CSRenforcement is not a winning strategy for attract-ing trade investment from their companies. Sixty-one percent of respondents indicated that it isstrong laws on CSR issues that they seek. Manyhost countries (including many in the developingworld) already have strong national laws on therange of CSR issues discussed in this study.Respondents indicated that, far from being a hand-

icap to trade and investment attraction, such lawsare attractive.

Of course, laws are only relevant to the extent theyare enforced. Respondents indicated that the gov-ernment action they would most welcome is enforcement of laws related to CSR issues.Respondents indicated that unevenly applied lawsencourage corruption, which imposes both costsand risks on MNEs. Some respondents also com-mented that uneven enforcement leads to selectiveenforcement against MNEs as a soft form of pro-tectionism, or even as an expression of tensionbetween the home and host governments.

In open responses, respondents repeatedly indi-cated that a country where the law is stronglyenforced across the board is more attractive. To theextent that a potential host country can project astrong image with regard to enforcing the law, it islikely to prove attractive to potential investors andpurchasers.

4.1.2 CSR codes, standards and forumsWhen seeking to determine what guidelines willinfluence an MNE’s new venture assessment, gov-ernments and potential partners should look firstto the company’s own code of conduct. Fifty-onepercent of respondents pointed to their own com-pany’s code as guiding their requirements for localpartners.

While only 31 percent of respondents requireadherence to an external code or standard, theinfluence of these codes and related forums onrespondents has grown in recent years. Amongmultisector codes, host countries and partnersmight wish to pay most attention to ISO 1400 andthe ILO conventions, as more than half of respon-dents identified these as among the most influen-tial on their companies.

Conclusions & Recommendations

4

25

Respondents identified The World BusinessCouncil for Sustainable Development (WBCSD)and the Global Reporting Initiative (GRI) are themost influential forums. To date, these and otherCSR forums have been primarily the domain of large MNEs and their home governments—frequently to the consternation of their own mem-bers and secretariats. Potential host countries andlocal partners would serve their own interests bybecoming more active in the forums with the mostinfluence on respondent MNEs’ policy and prac-tice. Consultations with members and senior staffof these forums indicate such overtures, far from a“storming of the gates,” would be welcome.

4.1.3 CSR and the new venture assessment cycleIn seeking to attract trade and investment, it maybe a mistake to assume that CSR is considered byMNEs only after a partner or location is selected.Fifty-four percent of responding MNEs examineCSR issues while they are still looking at multiplelocations and partners. Fifty-three percent havechosen one host country over another because ofCSR issues. Fifty-seven percent have chosen onepartner over another.

These findings suggest that potential host govern-ments and partners with a strong CSR story to tellshould tell it early in the venture assessment. Sucha strategy has implications for many proactivemarketing and promotional efforts, including cor-porate literature, trade missions, trade fairs, andeven consular and diplomatic activities.

These findings are especially relevant to compa-nies and countries seeking trade and investmentfrom the United States. Seventy-four percent ofU.S., Canadian, and Australian respondents (and ahigher percentage of U.S. respondents alone) haverejected potential locations based on CSR issues,and 62 percent have done the same for potentialpartners. Some host countries and companies thathave been prominently mentioned in U.S. litiga-tion regarding CSR issues are already aware of theneed for speed in addressing the allegation and forsubsequent promotional efforts. These findingsreinforce the importance of such measures.

4.1.4 Local partners as a country marketing toolMost MNEs surveyed have made commitments totheir stakeholders regarding the CSR performance oftheir local partners. However, corporate resources

devoted to developing partners that can meet thoseobligations are scarce, with fewer than 20 percent ofrespondents offering financial assistance or eventraining. If they are to maintain their partner-relatedcommitments, MNEs are in need of host countriesthat can supply “CSR-ready” suppliers.

CSR-ready suppliers are likely to be a more valu-able country marketing tool in some sectors thanothers. Earlier work in this field indicated that themanufacturing sector is responsive to countrymarketing strategies based on competitive clustersof such suppliers.11

By contrast, several extractive sector respondentsindicated that their principal local partner choicesare frequently limited to the host nation’s state-owned or parastatal national firms, or other com-panies with a similarly significant politicalposition. This is consistent with extractive sectorrespondents’ emphasis on country-level CSR per-formance rather than partner performance. Whilethere are no doubt cases in which extractive com-panies have chosen local partners based on CSRissues, the results of this survey do not clearlyindicate that the extractive sector as a whole iseagerly seeking “CSR-ready” partners in hostcountries.

In agribusiness, there is a division by MNE loca-tion. Agribusiness respondents overall appear rel-atively disengaged from partner-level CSR issues.However, Western European agribusiness respon-dents report that CSR initiatives in their regionhave increased the visibility of practices amongoverseas food commodity suppliers. For this rea-son, host countries that seek to market a cluster ofCSR-ready partners in the agribusiness sectormight best be served focusing their efforts onWestern European MNEs.

4.1.5 The sources that matterMNEs looking for information on CSR perfor-mance (at the country and partner levels) expresseda preference for certain sources. In seeking toattract trade and investment based on CSR, hostcountries and partners should choose their media

Race to the Top26

11 PELC-Global Access Corp. project on national competi-tive advantage and CSR in the apparel, footwear, and toyindustries (2000). Also, the Worldwide Responsible ApparelProgram’s host country endorsement initiatives.

Conclusions and Recommendations 27

with the same care as other marketers. For infor-mation on CSR, no source is nearly as important torespondents as the assessments of their own staff.This is where the potential host country and partnershould focus resources.

Beyond internal staff, home governments wereidentified as a priority source. Potential host coun-tries and partners should bring their strong CSRperformance to the attention of target home coun-tries’ embassies, ministries of commerce, anddevelopment agencies.