2Q / 1H 2019 IFRS Results · 2 Disclaimer No representation or warranty (express or implied) is...

19

August 16, 2019 Financial Presentation 2Q / 1H 2019 IFRS Results

Transcript of 2Q / 1H 2019 IFRS Results · 2 Disclaimer No representation or warranty (express or implied) is...

August 16, 2019

Financial Presentation2Q / 1H 2019 IFRS Results

2

Disclaimer

No representation or warranty (express or implied) is made as to, and no reliance should be placed on, the

fairness, accuracy or completeness of the information contained herein and, accordingly, none of the

Company, or any of its shareholders or subsidiaries or any of such person's officers or employees accepts

any liability whatsoever arising directly or indirectly from the use of this presentation.

This presentation contains certain forward-looking statements that involve known and unknown risks,

uncertainties and other factors which may cause the Company's actual results, performance or

achievements to be materially different from any future results, performance or achievements expressed or

implied by such forward-looking statements. PAO TMK does not undertake any responsibility to update

these forward-looking statements, whether as a result of new information, future events or otherwise.

This presentation contains statistics and other data on PAO TMK’s industry, including market share

information, that have been derived from both third party sources and from internal sources. Market statistics

and industry data are subject to uncertainty and are not necessarily reflective of market conditions. Market

statistics and industry data that are derived from third party sources have not been independently verified by

PAO TMK. Market statistics and industry data that have been derived in whole or in part from internal

sources have not been verified by third party sources and PAO TMK cannot guarantee that a third party

would obtain or generate the same results.

2Q / 1H 2019 Summary Financial Results and Market Update

3

2Q 2019 vs. 1Q 2019 Summary Financial Highlights

4

Sales were up QoQ, mainly due to higher sales at the Russian

division

Revenue was higher QoQ, mainly due to a stronger

performance at the Russian division

+5% QoQ +4% QoQ

Adjusted EBITDA was up QoQ, mainly due to stronger EBITDA

at the Russian division Net profit was up QoQ

+11% QoQ

175195

14%15%

0%

3%

6%

9%

12%

15%

18%

0

50

100

150

200

1Q2019 2Q2019

EB

ITD

A m

arg

in,

%

US

$ m

ln

Source: TMK data

4759

0

20

40

60

80

1Q2019 2Q2019

US

$ m

ln

+26% QoQ

978 1,031

0

300

600

900

1,200

1Q2019 2Q2019

Thousand t

onnes

1,257 1,307

0

500

1,000

1,500

1Q2019 2Q2019

US

$ m

ln

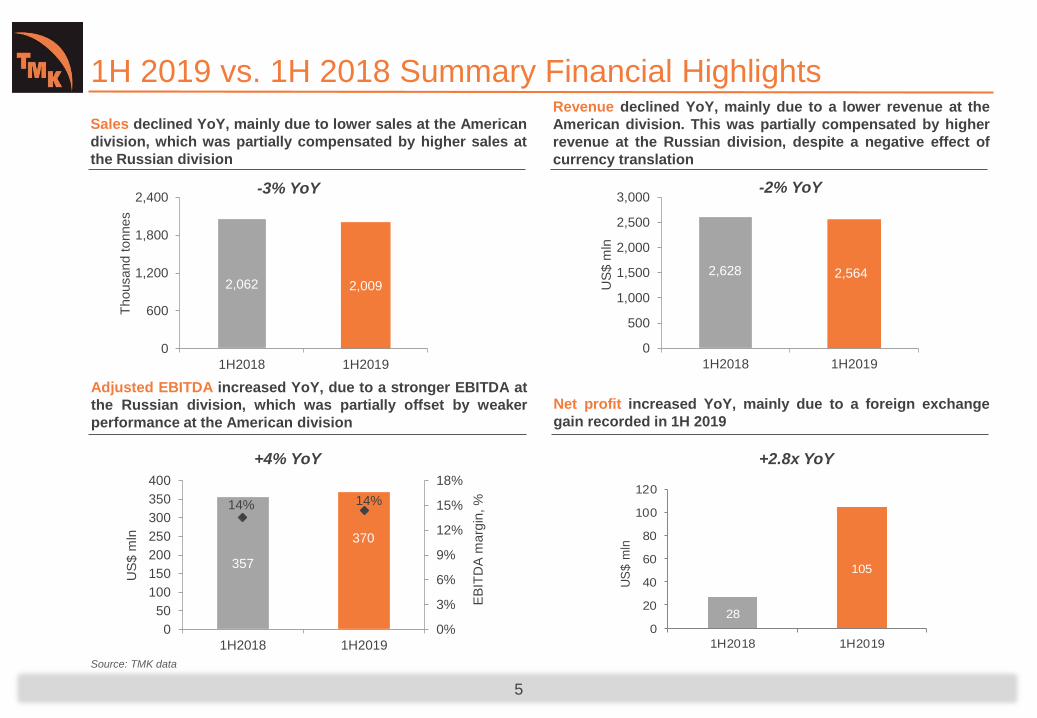

1H 2019 vs. 1H 2018 Summary Financial Highlights

5

Sales declined YoY, mainly due to lower sales at the American

division, which was partially compensated by higher sales at

the Russian division

Revenue declined YoY, mainly due to a lower revenue at the

American division. This was partially compensated by higher

revenue at the Russian division, despite a negative effect of

currency translation

-3% YoY -2% YoY

Adjusted EBITDA increased YoY, due to a stronger EBITDA at

the Russian division, which was partially offset by weaker

performance at the American division

Net profit increased YoY, mainly due to a foreign exchange

gain recorded in 1H 2019

+4% YoY +2.8x YoY

28

105

0

20

40

60

80

100

120

1H2018 1H2019

US

$ m

ln

Source: TMK data

357

370

14% 14%

0%

3%

6%

9%

12%

15%

18%

0

50

100

150

200

250

300

350

400

1H2018 1H2019

EB

ITD

A m

arg

in, %

US

$ m

ln

2,062 2,009

0

600

1,200

1,800

2,400

1H2018 1H2019

Thousand t

onnes

2,628 2,564

0

500

1,000

1,500

2,000

2,500

3,000

1H2018 1H2019

US

$ m

ln

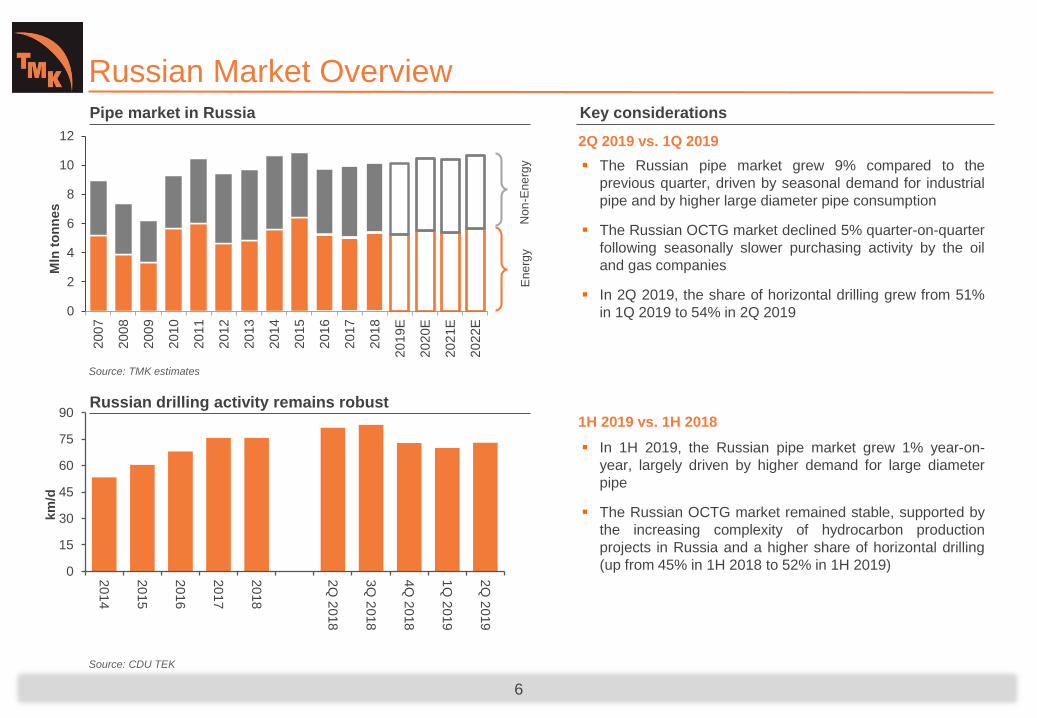

Russian Market Overview

6

Source: TMK estimates

Source: CDU TEK

Non

-En

erg

yE

ne

rgy

Key considerationsPipe market in Russia

Russian drilling activity remains robust

0

2

4

6

8

10

12

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19E

20

20E

20

21E

20

22E

Mln

to

nn

es

In 1H 2019, the Russian pipe market grew 1% year-on-

year, largely driven by higher demand for large diameter

pipe

The Russian OCTG market remained stable, supported by

the increasing complexity of hydrocarbon production

projects in Russia and a higher share of horizontal drilling

(up from 45% in 1H 2018 to 52% in 1H 2019)

The Russian pipe market grew 9% compared to the

previous quarter, driven by seasonal demand for industrial

pipe and by higher large diameter pipe consumption

The Russian OCTG market declined 5% quarter-on-quarter

following seasonally slower purchasing activity by the oil

and gas companies

In 2Q 2019, the share of horizontal drilling grew from 51%

in 1Q 2019 to 54% in 2Q 2019

2Q 2019 vs. 1Q 2019

1H 2019 vs. 1H 2018

0

15

30

45

60

75

90

20

14

20

15

20

16

20

17

20

18

2Q

2018

3Q

2018

4Q

2018

1Q

2019

2Q

2019

km

/d

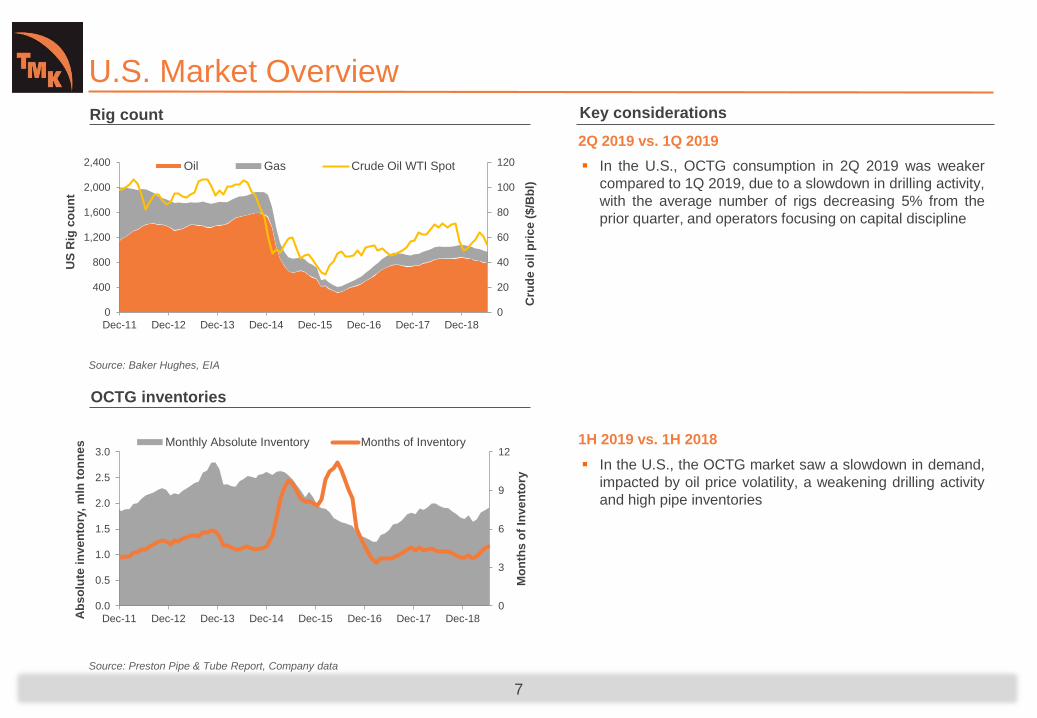

U.S. Market Overview

7

Source: Baker Hughes, EIA

Source: Preston Pipe & Tube Report, Company data

Rig count

OCTG inventories

In the U.S., the OCTG market saw a slowdown in demand,

impacted by oil price volatility, a weakening drilling activity

and high pipe inventories

In the U.S., OCTG consumption in 2Q 2019 was weaker

compared to 1Q 2019, due to a slowdown in drilling activity,

with the average number of rigs decreasing 5% from the

prior quarter, and operators focusing on capital discipline

2Q 2019 vs. 1Q 2019

1H 2019 vs. 1H 2018

Key considerations

0

20

40

60

80

100

120

0

400

800

1,200

1,600

2,000

2,400

Dec-11 Dec-12 Dec-13 Dec-14 Dec-15 Dec-16 Dec-17 Dec-18

Cru

de

oil

pri

ce

($

/Bb

l)

US

Rig

co

un

t

Oil Gas Crude Oil WTI Spot

0

3

6

9

12

0.0

0.5

1.0

1.5

2.0

2.5

3.0

Dec-11 Dec-12 Dec-13 Dec-14 Dec-15 Dec-16 Dec-17 Dec-18

Mo

nth

s o

f In

ve

nto

ry

Ab

so

lute

in

ve

nto

ry,

mln

to

nn

es Monthly Absolute Inventory Months of Inventory

2Q 2019 vs. 1Q 2019 Results

8

685

293

690

341

0

200

400

600

800

Seamless Welded

Thousand to

nnes

1Q2019 2Q2019

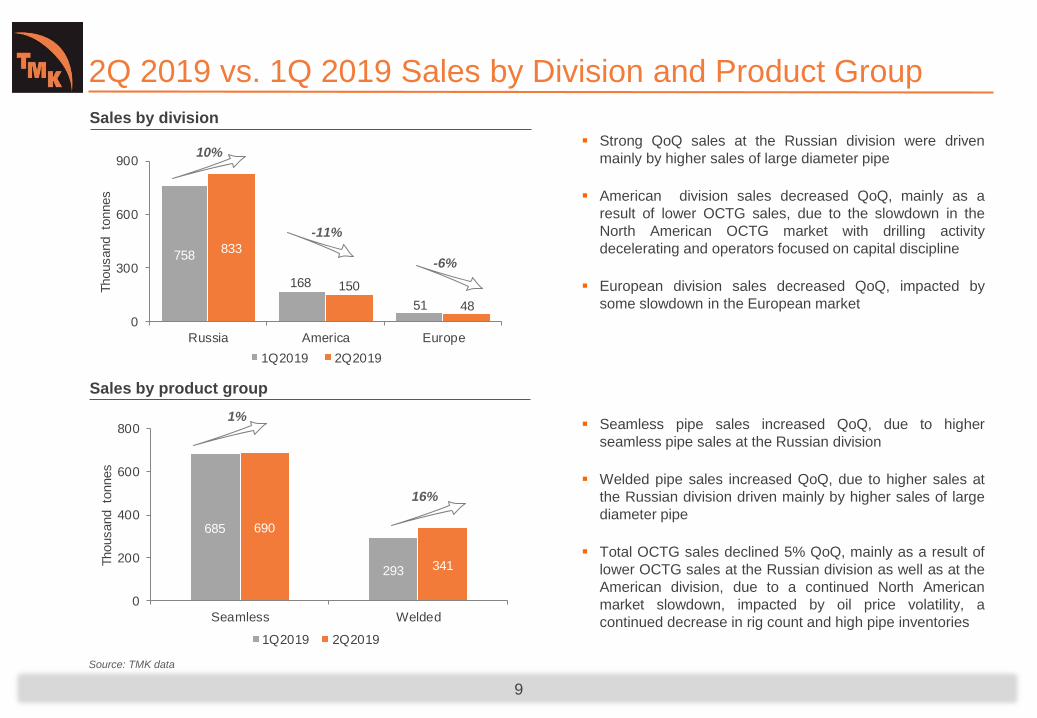

2Q 2019 vs. 1Q 2019 Sales by Division and Product Group

9

Seamless pipe sales increased QoQ, due to higher

seamless pipe sales at the Russian division

Welded pipe sales increased QoQ, due to higher sales at

the Russian division driven mainly by higher sales of large

diameter pipe

Total OCTG sales declined 5% QoQ, mainly as a result of

lower OCTG sales at the Russian division as well as at the

American division, due to a continued North American

market slowdown, impacted by oil price volatility, a

continued decrease in rig count and high pipe inventories

Strong QoQ sales at the Russian division were driven

mainly by higher sales of large diameter pipe

American division sales decreased QoQ, mainly as a

result of lower OCTG sales, due to the slowdown in the

North American OCTG market with drilling activity

decelerating and operators focused on capital discipline

European division sales decreased QoQ, impacted by

some slowdown in the European market

Source: TMK data

Sales by division

Sales by product group

758

168

51

833

150

48

0

300

600

900

Russia America Europe

Thousand to

nnes

1Q2019 2Q2019

1%

-11%

10%

-6%

16%

2Q 2019 vs. 1Q 2019 Revenue by Division

10

Revenue Revenue per tonne*

Source: Consolidated IFRS financial statements, TMK data

Revenue at the Russian division grew QoQ, driven by higher

welded pipe sales and a positive effect of currency translation

Revenue at the American division was affected by weaker

welded pipe sales, mainly due to OCTG pipe

Revenue at the European division decreased QoQ, mainly due

to lower sales and unfavorable pricing environment

Russian division revenue per tonne was flat QoQ

American division revenue per tonne was higher QoQ, due to a

change in the product mix with a higher share of seamless pipe

European division revenue per tonne decreased QoQ, due to

pricing pressure

Note: Certain monetary amounts, percentages and other figures included in this presentation are subject to rounding adjustments. Totals therefore do not always add up to exact arithmetic sums.

1,167

1,794

1,3611,165

1,830

1,265

0

500

1,000

1,500

2,000

Russia America Europe

US

$/t

onne

1Q2019 2Q2019

885

30270

970

27463

0

200

400

600

800

1,000

Russia America Europe

US

$ m

ln

1Q2019 2Q2019* Revenue /tonne for the Russian and American divisions is calculated as total revenue divided by pipe

sales. Revenue for the European division is calculated as total revenue divided by pipe+billets sales

0%

-9%

-11%

2%

-7%

10%

137

30

8

166

21

8

0

30

60

90

120

150

Russia America Europe

US

$ m

ln

1Q2019 2Q2019

2Q 2019 vs. 1Q 2019 Adjusted EBITDA by Division

11

Adjusted EBITDA Adjusted EBITDA margin

Source: Consolidated IFRS financial statements, TMK data

Russian division Adjusted EBITDA increased QoQ, supported

by a better sales mix, as well as lower scrap prices

American division Adjusted EBITDA decreased QoQ

European division Adjusted EBITDA was almost flat QoQ

Russian division Adjusted EBITDA margin increased by 1 p.p.

QoQ, reflecting a better product mix with a higher share of large

diameter pipe in the welded segments, as well as lower raw

material prices

American division Adjusted EBITDA margin declined QoQ

European division Adjusted EBITDA margin increased QoQ

Note: Certain monetary amounts, percentages and other figures included in this presentation are subject to rounding adjustments. Totals therefore do not always add up to exact arithmetic sums.

16%

10%

12%

17%

8%

13%

0%

5%

10%

15%

20%

Russia America Europe

%

1Q2019 2Q2019

21%

-31%

-1%

1H 2019 vs. 1H 2018 Results

12

1,399

662

1,375

634

0

400

800

1,200

1,600

Seamless Welded

Thousand to

nnes

1H2018 1H2019

1H 2019 vs. 1H 2018 Sales by Division and Product Group

13

Seamless pipe volumes declined YoY, as higher sales at

the Russian division were offset by weaker sales at the

American division

Welded pipe sales decreased YoY, as higher sales at the

Russian division were offset by weaker sales at the

American division

Total OCTG sales increased 2% YoY, driven by stronger

seamless OCTG sales at the Russian division

Russian division sales increased YoY, driven mainly by

higher sales of large diameter pipe and seamless OCTG

pipe

Sales volumes at the American division decreased YoY

due to the lower OCTG sales, impacted by slowdown in the

North American OCTG market with drilling activity

decelerating and operators focused on capital discipline

European division sales was almost flat YoY

Source: TMK data

Sales by division

Sales by product group

1,553

409

100

1,591

318

99

0

400

800

1,200

1,600

2,000

Russia America Europe

Thousand to

nnes

1H2018 1H2019

2%

-4%

-22%

-1%

-2%

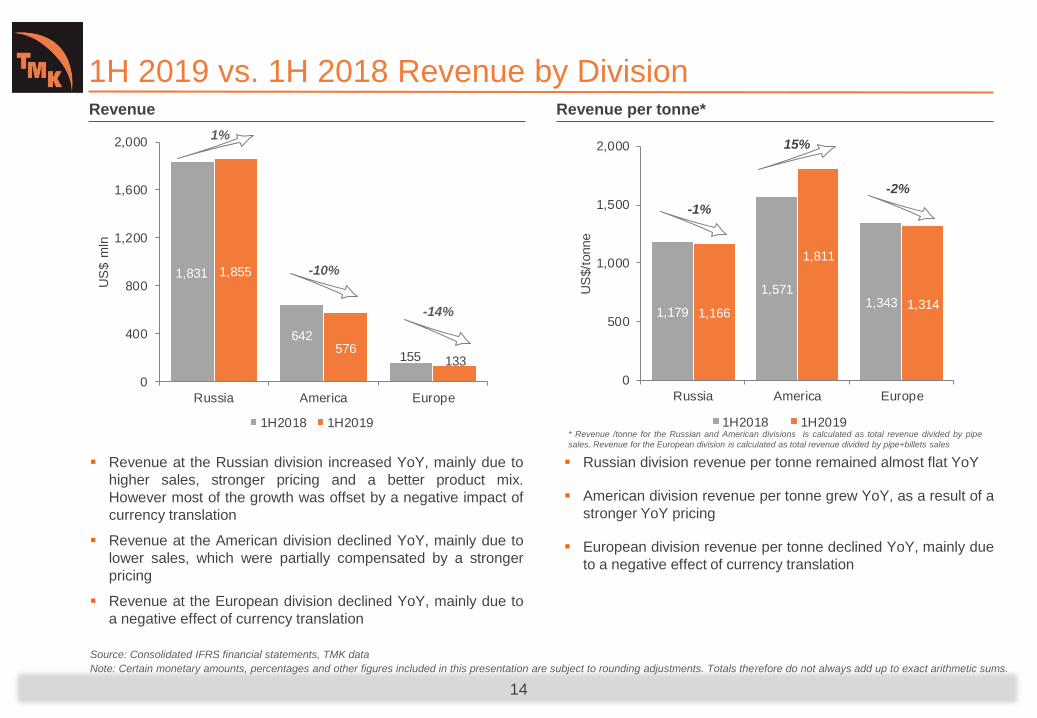

1H 2019 vs. 1H 2018 Revenue by Division

14

Revenue Revenue per tonne*

Source: Consolidated IFRS financial statements, TMK data

Revenue at the Russian division increased YoY, mainly due to

higher sales, stronger pricing and a better product mix.

However most of the growth was offset by a negative impact of

currency translation

Revenue at the American division declined YoY, mainly due to

lower sales, which were partially compensated by a stronger

pricing

Revenue at the European division declined YoY, mainly due to

a negative effect of currency translation

Russian division revenue per tonne remained almost flat YoY

American division revenue per tonne grew YoY, as a result of a

stronger YoY pricing

European division revenue per tonne declined YoY, mainly due

to a negative effect of currency translation

Note: Certain monetary amounts, percentages and other figures included in this presentation are subject to rounding adjustments. Totals therefore do not always add up to exact arithmetic sums.

* Revenue /tonne for the Russian and American divisions is calculated as total revenue divided by pipe

sales. Revenue for the European division is calculated as total revenue divided by pipe+billets sales

1,179

1,5711,343

1,166

1,811

1,314

0

500

1,000

1,500

2,000

Russia America Europe

US

$/t

onne

1H2018 1H2019

1,831

642

155

1,855

576133

0

400

800

1,200

1,600

2,000

Russia America Europe

US

$ m

ln

1H2018 1H2019

-2%

1%

-10%

-14%

-1%

15%

1H 2019 vs. 1H 2018 Adjusted EBITDA by Division

15

Adjusted EBITDA Adjusted EBITDA margin

Source: Consolidated IFRS financial statements, TMK data

Adjusted EBITDA in the Russian division increased YoY, driven

by an improved sales mix towards a higher share of OCTG and

large diameter pipe

American division Adjusted EBITDA declined YoY, due to lower

sales in both seamless and welded segments

European division Adjusted EBITDA declined YoY, impacted by

higher selling and administrative expenses and by a negative

effect of currency translation

Russian division Adjusted EBITDA margin increased YoY, as a

result of an improved sales mix towards a higher share of

OCTG and large diameter pipe

American division Adjusted EBITDA margin was down YoY,

due to weaker product mix

European division Adjusted EBITDA margin declined YoY,

impacted by higher selling and administrative expenses

Note: Certain monetary amounts, percentages and other figures included in this presentation are subject to rounding adjustments. Totals therefore do not always add up to exact arithmetic sums.

14%

12%

17%16%

9%

12%

0%

5%

10%

15%

20%

Russia America Europe

%

1H2018 1H2019

256

75

26

303

50

16

0

50

100

150

200

250

300

350

Russia America Europe

US

$ m

ln

1H2018 1H2019

18%

-36%

-33%

Seamless – Core to Profitability

16

1H 2019 gross profit breakdown

Source: Consolidated IFRS financial statements, TMK data

Note: Certain monetary amounts, percentages and other figures included in this presentation are subject to rounding adjustments. Totals therefore do not always add up to exact arithmetic sums.

US$ mln(unless stated otherwise)

2Q2019QoQ,

%1H2019

YoY,

%

Sales - Pipes, kt 690 1% 1,375 -2%

Revenue 906 1% 1,804 0%

Gross profit 217 2% 429 5%

Margin, % 24% 24%

Avg revenue/tonne (US$) 1,314 0% 1,313 2%

Avg gross profit/tonne (US$) 314 1% 312 6%

Sales - Pipes, kt 341 16% 634 -4%

Revenue 350 14% 657 -5%

Gross profit 31 36% 54 24%

Margin, % 9% 8%

Avg revenue/tonne (US$) 1,026 -2% 1,036 0%

Avg gross profit/tonne (US$) 92 17% 86 30%

SE

AM

LE

SS

WE

LD

ED

Sales of seamless pipe generated 70% of total

revenues in 1H 2019

Gross profit from seamless pipe sales represented

89% of 1H 2019 total gross profit

Gross profit margin from seamless pipe sales

amounted to 24% in 1H 2019

Seamless89%

Welded11%

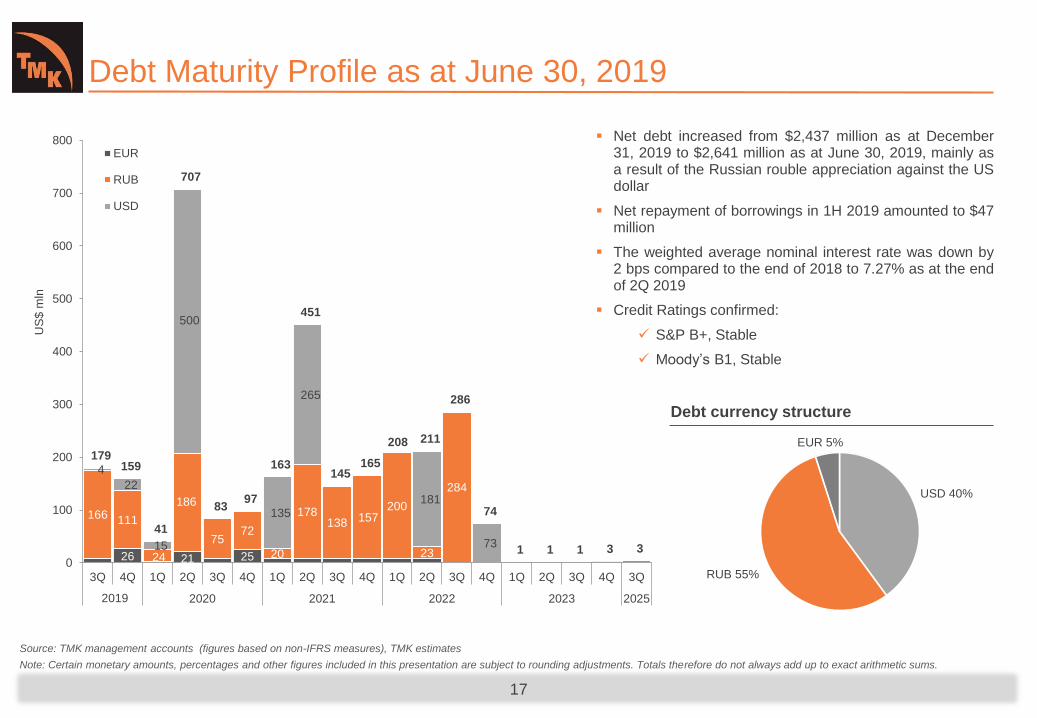

Debt Maturity Profile as at June 30, 2019

17

Debt currency structure

Source: TMK management accounts (figures based on non-IFRS measures), TMK estimates

Note: Certain monetary amounts, percentages and other figures included in this presentation are subject to rounding adjustments. Totals therefore do not always add up to exact arithmetic sums.

Net debt increased from $2,437 million as at December31, 2019 to $2,641 million as at June 30, 2019, mainly asa result of the Russian rouble appreciation against the USdollar

Net repayment of borrowings in 1H 2019 amounted to $47million

The weighted average nominal interest rate was down by2 bps compared to the end of 2018 to 7.27% as at the endof 2Q 2019

Credit Ratings confirmed:

S&P B+, Stable

Moody’s B1, Stable

26 21 25

166 111

24

186

7572

20

178138 157

200

23

284

4

22

15

500

135

265

181

73

179 159

41

707

83 97

163

451

145 165

208 211

286

74

1 1 1 3 3

0

100

200

300

400

500

600

700

800

3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 3Q

2020 2021 2022 2023 2025

US

$ m

ln

EUR

RUB

USD

USD 40%

RUB 55%

EUR 5%

2019

18

Outlook and Trends

In Russia, TMK expects pipe consumption by domestic oil and gas companies to remainstable in 2019. The increased complexity of hydrocarbon production projects in Russia isexpected to result in higher demand for high tech products. TMK anticipates EBITDA at theRussian division to increase for the full-year 2019, supported by an increase in pipeshipments, with the EBITDA margin to be slightly above the level of full-year 2018.

In North America, the market situation is most likely to remain challenging with oil and steelprice volatility, a slowdown in drilling activity and operators focusing on capital discipline, allresulting in lower pipe demand and pressure on prices.

In Europe, a challenging market environment and pricing pressure, coupled with a seasonalslowdown in activities in the European market in the third quarter might impact theEuropean division’s financial performance for the full-year 2019. However, overall TMKexpects to see sustained demand for seamless industrial pipe in full-year 2019 with thesales mix for the European division comprising a higher share of high value-addedproducts.

TMK Investor Relations

40/2a, Pokrovka Street, Moscow, 105062, Russia

+7 (495) 775-7600