2989575

38

Retail Research 1 Monthly Report December 2012 Monthly Report December 2012

description

report

Transcript of 2989575

Retail Research

1

Monthly Report December 2012

Monthly Report

December 2012

Retail Research

2

Monthly Report December 2012

Table of ContentsTitle Slide No.Monthly Equity Commentary 03− Market Statistics 04− Bond yields, commodities and currencies 07− Comparison of Equity Returns in various emerging

markets 12 − Outlook Going Forward 17

Technical Commentary 26Learning Technical Analysis 29 Derivatives Commentary 31Learning Derivatives 33Extract of Calls during November 2012 35Gainers & Losers – November 2012 37Disclosure 38

Retail Research

3

Monthly Report December 2012

Monthly Equity Commentary

27 28 O 03 04 05 08 09 10 11 12 15 16 17 18 19 22 23 25 26 29 30 31 N 02

1914019120191001908019060190401902019 T18980189601894018920189001888018860188401882018800187801876018740187201870018680186601864018620186001858018560185401852018500184801846018440184201840018380

1-1.BSE SENSITIV.BSE - 02/11/12 Trend7

Daily

After correcting in the month of October the Indian markets bounced back smartly in November.The rally was led by global liquidity and hopes of reform implementation Though the start to the month was positive the second and third week were dull were in the market corrected.The positive momentum picked up again from the fourth week with the gains accelerating towards the end of the month on the back of positive cues from Europe.

Sensex Nifty

· Optimism over the reshuffle of Union Cabinet. · India's fiscal deficit during the Apr-Sept period rose to 65.6% of the full fiscal year 2012/13

target.

· India's manufacturing sector inched up in Oct, driven by new orders

(The HSBC India Manufacturing Purchasing Managers' Index (PMI) - a

measure of factory production - stood at 52.9 in Oct slightly up from

Sept, when it was 52.8).

· The RBI left interest rates on hold.

· The central bank raised the March-end inflation estimate to 7.5%, from 7%.

· Foreign direct investment (FDI) in India declined by about 20% in August compared to same

month in the previous year.

· Reserve Bank sharply lowered this fiscal's economic growth projection to 5.8%, from 6.5%

earlier.

· Indices edged lower as investors were worried about the US "fiscal cliff" & the euro-zone

economy.

· The HSBC PMI for the services sector fell to 53.8 in Oct from Sept seven-month high of 55.8.

· India’s foreign tourist arrivals for Oct 2012 saw a sluggish growth of 2.8%.

· Gross direct tax collection registered a growth at a mere 6.59% during the April-Oct period.

2 -0.4

Week No

% Chg

Key Positives Key Negatives

-0.2

· Car sales increased by 23.09% to 172,459 units in Oct.

1

· Cut in the cash reserve ratio for banks by RBI.

1.41.4

Retail Research

4

Monthly Report December 2012

Monthly Equity Commentary contd…

Given below is an overview of global markets’ performance during November 2012:Indices Oct-12 Nov-12 % Change

US - Dow Jones 13096.5 13025.6 -0.5

US - Nasdaq 2977.2 3010.2 1.1

UK - FTSE 5782.7 5866.8 1.5

Japan - Nikkei 8928.3 9446.0 5.8

Germany - DAX 7260.6 7405.5 2.0

Brazil - Bovespa 57068.0 57475.0 0.7

Singapore - Strait Times 3038.4 3070.0 1.0

Hong Kong – Hang Seng 21641.8 22030.4 1.8

India - Sensex 18505.4 19339.9 4.5

India - Nifty 5619.7 5879.9 4.6

Indonesia - Jakarta Composite 4350.3 4276.1 -1.7

Chinese - Shanghai composite 2068.9 1980.1 -4.3

The world markets ended the month of November 2012 on a mixed note Japan & India (Nifty and Sensex) were the top performers, which ended the month with decent gains of 5.8%, 4.6% & 4.5% respectively. Germany, Hong Kong, UK & US (Nasdaq) also managed to close in the green by 2.0%, 1.8%, 1.5% & 1.1% respectively. Among the losers, Chinese, Indonesia and US (Dow Jones) fell the most by 4.3%, 1.7% & 0.5% respectively.

HOME

Sensex Nifty

· Weakness in global stocks and weak economic data in the domestic market hit investor

sentiment adversely.

· Industrial production contracted by 0.4 % in September on account of dismal performance of

manufacturing and capital goods sectors.

· Strong buying by foreign institutional investors (FIIs) in November 2012.

· Finance Ministry permitted Life Insurance Corporation to invest up to

30% in a Company as against the earlier ceiling of 10%.

· Moody’s retains India’s stable outlook.

· Expectations that Greece will get bailout fund from the troika of

international lenders comprising the European Union, the European

Central Bank and the IMF.

· The Indian economy grew by 5.3% in the July-September period.

· Fiscal deficit in the first seven months of 2012-13 stood at 71.6 % of the

Budget Estimates (BE), slightly better than 74.4 per cent in the same

period a year ago,

0.9

· Indirect tax collection has shown only a moderate growth of 17% in April-October period as

against the annual growth target of 27%

5 4.5 4.5

· ICRA has cut the estimate for India’s economic growth for FY13 to 5.4% from 5.7%.

4 1.1

3 -2.0 -2.0

· India's headline inflation unexpectedly eased to its slowest pace in

eight months in October.

Key NegativesWeek No

% Chg

Key Positives

Retail Research

5

Monthly Report December 2012

Monthly Equity Commentary contd…

All sectoral indices ended on a positive note last month except Oil & Gas. Consumer Durable, Realty, Bankex, FMCG and Auto were the top five gainers, which rose by 15.8%, 12.8%, 7.8%, 6.2%, and 4.9% respectively. The loser was Oil & Gas, which fell by 1.2%.

BSE Indices 30-Nov-12 31-Oct-12 % Chg Remarks

Sensex 19339.9 18505.4 4.5

Smallcap 7275.7 6989.2 4.1

Midcap 6902.0 6566.0 5.1

BSE 500 7472.5 7118.8 5.0

BSE 200 2389.5 2276.2 5.0

BSE 100 5909.0 5621.0 5.1

· Index rose after reports stating Finance Minister P. Chidambaram has asked

banks to bail out builders, especially those involved in in the construction of

residential projects, to jump start growth.

· Unitech, DB Realty and Anant Raj Industries were the top performers, which

rose 37.2%, 34.9% and 21.4% respectively.

· Best sector performer of the month.

· Videocon industries, Gitanjali Gems, and Titan Industries, which contributes

74.4% to the overall weightage of the index, rose 25.3%, 22.3% & 20.2%

respectively.

· Domestic and foreign brokerages are very optimistic on Titan Inds’ (largest

weight in the index) performance in the medium term, which helped the index

to gain further.

Metal 10355.2 10149.1 2.0

· Index rose on hopes that banking laws (amendment) bill will be passed in the

winter session. HDFC Bank gained on build up of long positions ahead of the

event.

· Union Bank, IDBI Bank, Canara Bank, Indusind Bank, Axis Bank & HDFC Bank

were the top gainers which rose by 24.0%, 16.4%, 15.7%, 14.8%, 11.2% & 10.9%

respectively.

Power 1980.3 1952.1 1.4

Capital Goods 11080.2 10864.0 2.0

· Automakers rose on hopes of rising sales during the festival season.

· Top gainers were Ashok Lelyand, Tata Motors, M&M and Bajaj Auto gaining

20.9%, 7.7%, 6.9% and 6.4% respectively.

Auto 10814.5 10307.3 4.9

Bankex 13951.9 12947.3 7.8

Consumer Durables 8031.2 6937.7 15.8

Realty 1998.4 1771.6 12.8

Retail Research

6

Monthly Report December 2012

Monthly Equity Commentary contd…

Fund Activity: Net Buy /

Sell

Net Buy /

Sell

Open

Interest

Open

Interest

Nov-12 Oct-12 Nov-12 Oct-12

Equities (Cash) 9718 9578 · FIIs were reported as strong net buyers in Nov.

Index Futures 2228 406 10870 9348

· FIIs were net buyers along with an increase in

open interest over October, which indicates long

positions taken by them apart from the value

impact.

Index Options 5395 7340 37800 46103

· FIIs were net buyers, which was along with

decline in the open interest. This indicates

squaring up of earlier options.

Stock Futures 218 -3333 29938 27838

· FIIs were net buyers while the open interest

increased over October, which indicates building of

long positions in this segment apart from the value

effect.

Stock Options -455 -466 879 1516

· The Stock Options segment witnessed poor

participation.

Equities (Cash) -2397 -2520

· MF continued to be the net seller for the last 5

consecutive months.

Particulars Remarks

FII Activity (Rs. in Cr)

MF Activity

HOME

BSE Indices 30-Nov-12 31-Oct-12 % Chg Remarks

· Heavy selling pressure has dragged down the index.· Oil India, HPCL & Petronet LNG were the top losers followed by Gujarat State

Petronet, Cairn India, Reliance Industries and ONGC.

· A sharp surge in subsidy sharing burden adversely impacted ONGC's PSU 7177.7 7104.7 1.0

IT 5888.4 5718.7 3.0

· United Spirits (ahead of and post Diageo deal), Colgate Palmolive, Tata Global &

ITC were the top gainers, which rose by 69.4%, 12.2%, 10.3% and 5.5 respectively.

· Stocks gained after positive signs that the government might push through its

economic reforms to boost economic growth.

Healthcare 7946.5 7620.5 4.3

FMCG 6037.9 5687.3 6.2

Oil & Gas 8252.1 8355.0 -1.2

Retail Research

7

Monthly Report December 2012

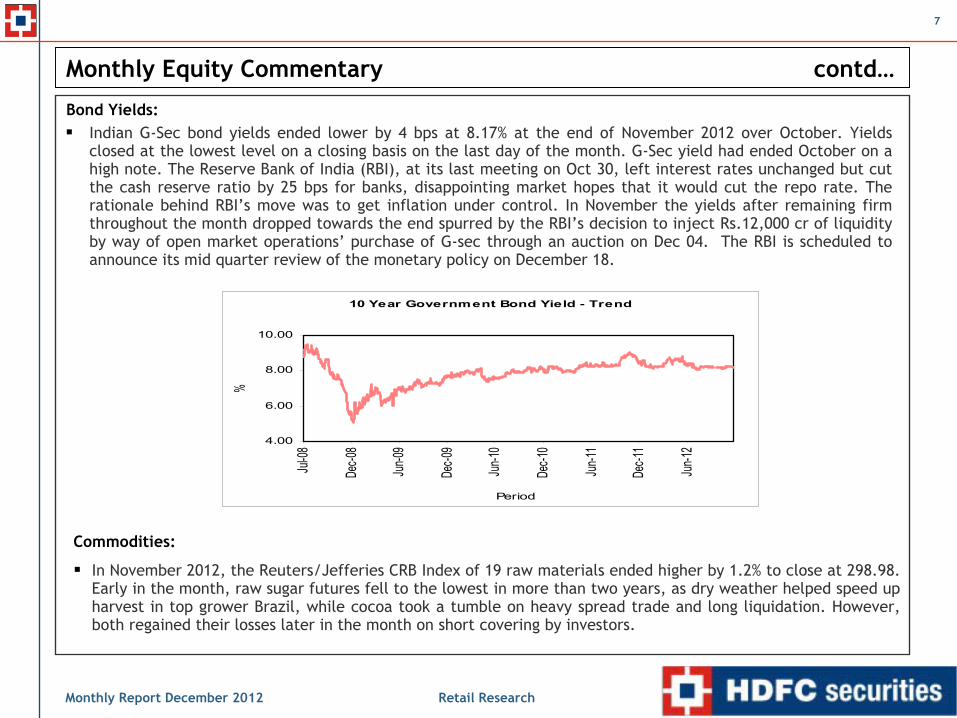

Bond Yields:

Monthly Equity Commentary contd…

Commodities:

In November 2012, the Reuters/Jefferies CRB Index of 19 raw materials ended higher by 1.2% to close at 298.98. Early in the month, raw sugar futures fell to the lowest in more than two years, as dry weather helped speed up harvest in top grower Brazil, while cocoa took a tumble on heavy spread trade and long liquidation. However, both regained their losses later in the month on short covering by investors.

Indian G-Sec bond yields ended lower by 4 bps at 8.17% at the end of November 2012 over October. Yields closed at the lowest level on a closing basis on the last day of the month. G-Sec yield had ended October on a high note. The Reserve Bank of India (RBI), at its last meeting on Oct 30, left interest rates unchanged but cut the cash reserve ratio by 25 bps for banks, disappointing market hopes that it would cut the repo rate. The rationale behind RBI’s move was to get inflation under control. In November the yields after remaining firm throughout the month dropped towards the end spurred by the RBI’s decision to inject Rs.12,000 cr of liquidity by way of open market operations’ purchase of G-sec through an auction on Dec 04. The RBI is scheduled to announce its mid quarter review of the monetary policy on December 18.

10 Year Government Bond Yield - Trend

4.00

6.00

8.00

10.00

Jul-0

8

Dec-0

8

Jun-0

9

Dec-0

9

Jun-1

0

Dec-1

0

Jun-1

1

Dec-1

1

Jun-1

2

Period

%

Retail Research

8

Monthly Report December 2012

Behaviour of commodity prices (including LME 3 month buyer prices for base metals) during the month ended November 2012 is given below. Analysts largely agreed that it was technical buying that was supporting the base metals rather than news of the release of the next tranche of aid to Greece. A revival in demand from Indian and American industries, along with stabilizing growth conditions in China, is expected to push up consumption of base metals in the coming months. However, analysts are cautious about the uncertainties on European economic conditions and the US fiscal cliff, which would influence trends.

Monthly Equity Commentary contd…

Commodity 30-Nov-12 31-Oct-12 % Chg Reasons

· Concern that U.S. lawmakers may fail to reach a

settlement in talks aimed at avoiding self-imposed tax

increases and budget cuts known as the fiscal cliff. If the

parties fail to reach an agreement, $600 billion in tax hikes

and spending cuts will auto

· Early in the month gold rallied on demand asr a safe haven

during a global economic meltdown

· First monthly increase since August on signals that

economic expansion in the U.S. is accelerating

· Optimism that U.S. lawmakers will reach a budget

agreement in time to avoid massive spending cuts and tax

hikes that could derail an economic recovery in the world's

largest oil consumer

· Supply from the Organization of Petroleum Exporting

Countries dropped by 0.2% to 30.95 million a day in October,

the lowest since last December, because of declines

in Nigeria, Iran and Saudi Arabia

· Concern that the clash between Israel and Hamas will

escalate into a wider conflict that would endanger Middle

East crude shipments

· China’s state stockpiler started stocking, giving the

impression prices could have hit a bottom

· Demand increasing with recovery in manufacturing.

Increase in auto sales (especially in China) led to higher

demand.

Gold 1712.7 1719.1 -0.37%

Crude Oil 88.9 86.2 3.10%

Aluminium 2079 1911 8.79%

Retail Research

9

Monthly Report December 2012

The Baltic Dry Index (BDI) gained 5.8% in the month to close at 1086. The index started the month on a poor note on poor global economic data and concerns from China. However, the BDI soon recovered as capesize rates increased and iron ore prices stabilized as China’s $158 bn stimulus plan kicks off. Improvement in China’s PMI led to anticipation of higher iron ore and coal demand, which led to a rise in rates and consequently the BDI.

Currencies

The USD was mixed vs other currencies in November 2012, however with a negative bias. The USD remained weak against most peers during the month as the fiscal cliff in the USA and possible developments in the Euro zone boosted other currencies while depreciating the USD. The Dollar Index (DXY), which Intercontinental Exchange Inc. uses to track the greenback against the currencies of six U.S. trade partners, rose by 0.4% in the month (mainly helped by yen depreciating vs the US$). The biggest gainers in the month were the Korean Won, Pakistan Rupee and Indonesia Rupiah while the biggest losers in the month were Japanese Yen, Brazilian Real and Indian Rupee.

Monthly Equity Commentary contd…

Commodity 30-Nov-12 31-Oct-12 % Chg Reasons

Copper 7954 7823 1.67%

· Signs that China’s economy is rebounding raised

expectations that consumption in the world’s largest user

will increase next year. China’s factory output expanded for

the first time in 13 months in November.

Zinc 2044 1875 9.01%· China’s state stockpiler started stocking, giving the

impression prices could have hit a bottom

Nickel 17225 16270 5.87%

Tin 21700 20050 8.23% · Heavy demand from alloy industries

· Speculators created positions amid a firm spot market

trend on pick up in demand from battery makers

· Analysts are predicting a shortfall next year with the

supply glut shrinking to 13,000 tons this year, from 156,000

tons in 2011, before flipping into a 154,000-ton shortfall in

2013.

Lead 2253 2080 8.32%

Retail Research

10

Monthly Report December 2012

Monthly Equity Commentary contd…

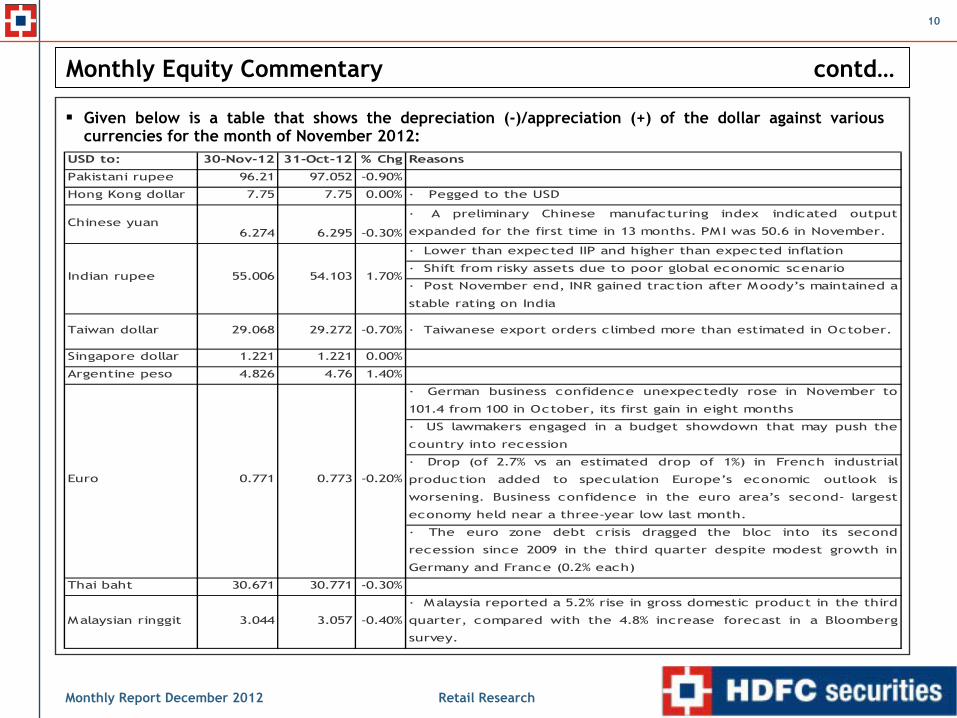

Given below is a table that shows the depreciation (-)/appreciation (+) of the dollar against various currencies for the month of November 2012:

USD to: 30-Nov-12 31-Oct-12 % Chg Reasons

Pakistani rupee 96.21 97.052 -0.90%

Hong Kong dollar 7.75 7.75 0.00% · Pegged to the USD

Chinese yuan6.274 6.295 -0.30%

· A preliminary Chinese manufacturing index indicated output

expanded for the first time in 13 months. PMI was 50.6 in November.

· Lower than expected IIP and higher than expected inflation

· Shift from risky assets due to poor global economic scenario

· Post November end, INR gained traction after Moody’s maintained a

stable rating on India

Taiwan dollar 29.068 29.272 -0.70% · Taiwanese export orders climbed more than estimated in October.

Singapore dollar 1.221 1.221 0.00%

Argentine peso 4.826 4.76 1.40%

· German business confidence unexpectedly rose in November to

101.4 from 100 in October, its first gain in eight months

· US lawmakers engaged in a budget showdown that may push the

country into recession

· Drop (of 2.7% vs an estimated drop of 1%) in French industrial

production added to speculation Europe’s economic outlook is

worsening. Business confidence in the euro area’s second- largest

economy held near a three-year low last month.

· The euro zone debt crisis dragged the bloc into its second

recession since 2009 in the third quarter despite modest growth in

Germany and France (0.2% each)

Thai baht 30.671 30.771 -0.30%

Malaysian ringgit 3.044 3.057 -0.40%

· Malaysia reported a 5.2% rise in gross domestic product in the third

quarter, compared with the 4.8% increase forecast in a Bloomberg

survey.

Euro 0.771 0.773 -0.20%

Indian rupee 55.006 54.103 1.70%

Retail Research

11

Monthly Report December 2012

Monthly Equity Commentary contd…

HOME

USD to: 30-Nov-12 31-Oct-12 % Chg Reasons

Indonesian rupiah 9578.54 9643.2 -0.70%

· Speculation that Japanese elections next month will hand power to

an opposition party that advocates more aggressive monetary

stimulus. Opposition leader, Shinzo Abe, increased pressure on

the Bank of Japan to add to stimulus measures that tend to weak

· Japan’s consumer prices (excluding fresh food) stagnated, adding

to political calls for the central bank to add to monetary easing at

the Dec. 20 meeting.

Brazilian real 2.094 2.034 2.90%

· Brazilian economy grew (0.9%) only half what economists expected

(2.3%) in the third quarter, suggesting the government may resort to

a weaker currency and low interest rates to prop up economic

activity

Korean won 1082.95 1094.21 -1.00%

Japanese yen 82.1 79.647 3.10%

Retail Research

12

Monthly Report December 2012

Comparison of Equity Returns in various markets - MSCI Indices in US$ terms

Monthly Equity Commentary contd…

MSCI Index Last

Monthly

Returns

3 Month

Returns

YTD

Returns

1 Year

Returns MSCI Index Last

Monthly

Returns

3 Month

Returns

YTD

Returns

1 Year

Returns

Emerging Markets Developed Markets

EM ASIA 432.5 2.8% 9.5% 14.2% 14.9% EUROPE 1,407.3 2.4% 6.7% 12.1% 10.3%

EM (EMERGING MARKETS) 1,007.0 1.2% 6.3% 9.9% 8.5% G7 INDEX 1,142.6 0.9% 2.0% 10.8% 10.7%

BRIC 283.5 0.5% 7.6% 5.9% 3.4% WORLD 1,315.5 1.1% 2.8% 11.2% 11.1%

EM EUROPE 444.9 0.2% 4.3% 12.6% 1.6%

EM EUROPE & MIDDLE EAST 378.2 0.2% 4.3% 12.6% 1.6% GREECE 79.0 7.0% 15.1% -3.3% -7.3%

EM LATIN AMERICA 3,580.3 -1.8% 1.1% -0.6% -2.5% AUSTRIA 1,088.4 5.5% 18.8% 15.9% 15.5%

FINLAND 341.4 5.4% 12.1% 5.3% -3.4%

CHINA 60.0 1.9% 14.2% 13.5% 16.3% BELGIUM 1,227.1 4.8% 7.3% 33.6% 32.8%

INDIA 430.2 4.4% 14.9% 24.0% 16.6% FRANCE 1,369.8 4.1% 7.9% 13.8% 9.9%

INDONESIA 873.1 -3.4% 4.4% 0.8% 4.1% SWITZERLAND 4,123.7 3.9% 10.0% 15.8% 17.8%

KOREA 408.2 2.7% 6.6% 14.3% 12.3% SWEDEN 6,449.6 3.2% 4.7% 13.9% 12.7%

MALAYSIA 469.0 -3.1% 0.2% 6.7% 10.7% NETHERLANDS 1,951.2 3.0% 7.6% 14.0% 14.1%

PHILIPPINES 475.0 5.4% 13.6% 40.0% 44.9% HONG KONG 8,784.6 2.9% 12.2% 23.4% 25.5%

TAIWAN 269.6 7.2% 7.9% 12.4% 15.8% CANADA 1,678.7 -0.6% 2.2% 5.4% 2.7%

THAILAND 396.7 1.5% 7.1% 23.4% 26.3% IRELAND 116.2 -2.1% 2.3% -1.9% 5.0%

BRAZIL 2,548.1 -3.1% -1.9% -9.9% -12.0% PORTUGAL 84.6 -2.5% 6.8% -9.1% -13.7%

CHILE 2,300.8 -3.3% -2.1% 1.5% 1.6%

COLOMBIA 1,263.8 -1.5% 7.3% 22.2% 26.1% Frontier Markets

MEXICO 6,839.1 1.6% 8.1% 22.1% 19.6% FM (FRONTIER MARKETS) 480.1 1.6% 4.9% 2.8% 1.6%

PERU 1,506.8 -0.8% 6.1% 8.9% 6.9%

CZECH REPUBLIC 414.0 -7.9% -11.0% -7.5% -7.8% SERBIA 220.5 9.4% 21.9% 1.5% -2.5%

HUNGARY 530.0 -3.8% 10.3% 22.4% 9.9% ESTONIA 658.6 8.5% 6.7% 27.3% 14.7%

POLAND 833.4 5.5% 11.8% 21.7% 11.5% BOTSWANA 752.7 7.6% 16.6% 12.6% 13.0%

RUSSIA 760.7 -0.5% 1.3% 3.3% -7.7% KUWAIT 586.3 6.6% 10.6% -0.3% -2.2%

TURKEY 593.2 0.3% 10.6% 50.1% 36.7% LITHUANIA 807.8 6.1% 1.9% 12.1% 8.7%

EGYPT 588.1 -14.7% -10.0% 33.5% 20.1% KAZAKHSTAN 568.6 6.0% 5.5% 28.8% 17.8%

MOROCCO 324.7 3.7% -1.3% -13.4% -18.3% BANGLADESH 636.8 -6.9% -8.6% -17.7% -24.1%

SOUTH AFRICA 528.5 -1.0% -0.5% 4.5% 2.2% UKRAINE 87.1 -9.4% -19.7% -50.9% -59.9%

Retail Research

13

Monthly Report December 2012

Comparison of Equity Returns in various markets - MSCI Indices in US$ terms

Most equity markets across the globe ended the month of November 2012 on a positive note. Europe was the best performer amongst the global equity markets with Greece, Austria and Finland being the top gainersduring the month, while Portugal, Ireland and Canada ended in the red. However, Latin America witnessed selling pressure and ended the month lower by 1.8%.

Among the Emerging Markets, Asia gained the most (2.8%) while BRIC rose by 0.5%. Europe and Europe & Middle East rose 0.2% each while Latin America ended in the negative (1.8%).

Among the developed markets, Greece gained the most (7%) during November 2012. Global lenders agreed last month to reduce Greek debt and release loans to keep the economy afloat. After 12 hours of talks, they decided steps to cut Greek debt to 124% of gross domestic product by 2020, and promised further measures to lower it below 110% in 2022. Following months of jockeying, the deal was broadly expected by markets and clears the way for Greece's euro zone neighbours and the International Monetary Fund (IMF) to disburse almost 35 billion euros of aid in December 2012. Overall, the latest Greek rescue deal will buy the country a bit more time. But unless the economy stages a miraculous recovery, the rest of the euro zone will soon be forced to make much more difficult decisions over just how far it is prepared to go to keep Greece inside the euro.

The Finland stock market ended in the green (up 5.4%) on some positive economic data and on hopes that Greece would get bailout soon. The Finnish economy is estimated to have expanded modestly in the third quarter, after shrinking in the previous quarter. Gross domestic product increased a seasonally adjusted 0.3 percent sequentially in the third quarter, recovering from second quarter's 1.1 percent decline. On an annual basis, the economy contracted a working-day adjusted 0.8 percent during the three-month period. Apart from Finland other European markets too rose in November on optimism that Greece revealed plans to spend up to (euro) 10 bn (US$13 bn) in a bond buyback program will help stabilize its mountainous debt.

Portuguese stock market witnessed fall of 2.5% in November 2012. In Lisbon, thousands of demonstrators marched to the parliament building, where deputies were debating the budget. Riot police charged in after at least five people were injured by stones and bottles thrown by protesters and several arrests were made. Portugal's Parliament on November 27, 2012 approved unprecedented tax increases despite a broad public outcry and concerns that the latest austerity package will prolong the bailed-out country's recession. The center-right coalition government used its parliamentary majority to pass its 2013 budget. Marches and protests were held in another 38 cities and towns across the country. Union leaders called for 10% surtax on share dividends, a 0.25% tax on stock market transactions and a crackdown on tax evasion as alternatives to what they described as the brutal income tax increases planned by the government.

Monthly Equity Commentary contd…

Retail Research

14

Monthly Report December 2012

Monthly Equity Commentary contd…

Frontier markets gained 1.6% during the month. Serbia and Estonia were the top gainers, rising 9.4% and 8.5% respectively while Botswana and Kuwait rose by 7.6% and 6.6% respectively. Lithuania and Kazhakstan ended higher by 6% each. However, Ukraine was the top underperformer losing 9.4% and Bangladesh fell by 6.9%.

Serbian stock exchange witnessed highest growth in November among all the Frontier markets. The Serbian government has provided regular state funding for the first half of 2013, by selling Eurobonds of USD 750mn at the international financial market. This is the second time in a month and a half that Serbia sold Eurobonds. On September 28, the country sold USD 1bn worth of the security, with the yield of 6.625 percent annually. Another successful issuance of Eurobonds belonging to the Republic of Serbia was carried out on November 14, when all USD 750mn of five-year Eurobonds with the yield of 5.45 percent and interest rate (coupon) were sold. This is a clear indication that the international market considers seriously the new government's program of fiscal consolidation and draft budget for 2013, which will halve the budget deficit. The Serbian government also adopted the fiscal strategy for 2013 with projections for 2014 and 2015, which defines the basic goals and guidelines in the implementation of economic and fiscal policy for the next three years. This strategy provides a moderate GDP growth of 2% in 2013, 3.5% in 2014 and 4% in 2015. Also, the goal of fiscal policy is to strongly reduce the fiscal deficit next year from 6.1% to 3.6% and to 1% in 2015. These goals can be met through tax policy measures (which was mostly implemented in the first three months of the new government), through the reduction of public expenditure and the implementation of structural reforms.

Ukraine was the top loser among the frontier markets (down 9.4%). Ukraine’s finance ministry revealed that the country’s state budget gap widened almost threefold in the first 10 months of the year, reaching US$4.1 bndue to falling revenues and a 16% pre-election spending spree by the government of President Viktor Yanukovich. Ukrainian citizens have rushed to trade soft hryvnias for hard dollars, bringing down the National Bank of Ukraine’s international reserves by US$2.4 bn in October alone. At the end of last month, these reserves stood at US$26.8 bn, the lowest level since December 2009. Ukraine, with its economy sliding into recession and budget deficit widening, has appealed to the IMF to initiate negotiations on a fresh, multibillion-dollar bailout loan program. A mission from the IMF headed by Christopher Jarvis is scheduled to arrive in Kiev on December 7 to initiate negotiations for a new “standby” agreement. Ukraine’s economic growth and hard currency earnings from exports are highly vulnerable to global shocks, particularly demand and prices for steel, the country’s top export.

The Emerging Markets ended the month of November on a positive note, up by 1.2%. EM-Asia index was the top gainer, up 2.8%. BRIC rose by 0.5% while EM-Europe & EM-Europe & Middle East rose by 0.2% each. However, EM-Latin America fell by 1.8%.

Retail Research

15

Monthly Report December 2012

Monthly Equity Commentary contd…

Rise in EM-Asia was led by Taiwan, which rose by 7.2%. Other countries like Philippines, India and Korea rose by 5.4%, 4.4% and 2.7% respectively. However, Indonesia and Malaysia ended the month in the red.

The IMF has predicted Taiwan's economic growth at 3.9 percent next year and this aided in boosting the stock exchange Taiex last month. That would be a big improvement on 2012. Taiwan's economy is weathering the economic storm, outperforming some of its regional counterparts on the back of reviving exports. The value of Taiwan's export orders in October increased by 3.2% compared with the same period last year due to launches of new technology products. Export orders amounted to $38.38 billion in October, a 1.9-percent increase month on month. The value of export orders in the first 10 months stood at $360.9 billion, showing a year-on-year decrease of 0.6 percent. Taiwan has made a massive leap to become the 16th-best country for business, according to the results of a survey conducted by U.S.-based Forbes Magazine. Taiwan, which ranked 26th in a similar poll last year, only trails third-ranking Hong Kong and fourth-ranking Singapore among the Asian economies on the Forbes' 2012 "Best Countries for Business" list.

The Jakarta stock exchange ended last month in the negative. Indonesia's economy grew at its slowest pace in more than two years in the third quarter as the global slowdown hurt demand for commodities, but strong investment and healthy domestic spending still kept it among the world's best performers. Gross domestic product grew 6.17% year-on-year in the quarter ending Sept. 30, slower than the previous quarter's 6.37% expansion. It was the slowest growth rate for Southeast Asia's largest economy since the first quarter of 2010, the Central Statistics Agency said. Crucially, exports were down 2.78% on-year. Businesses have warned that the government could opt for more populist policies ahead of 2014 presidential and parliamentarian elections, which also could deter investment. In addition, inflationary pressures are fueling labor protests for higher wages. Last month laborers from the greater Jakarta area demanded raises of nearly 70%, to 2.7 million rupiah ($280) per month.

EM-Europe and EM-Europe & Middle East rose by 0.2% each. The countries that rose the most include Poland and Morocco (up 5.5% and 3.7% respectively). The major losers were Egypt and Czech Republic, which fell by 14.7% and 7.9% respectively.

Retail Research

16

Monthly Report December 2012

Monthly Equity Commentary contd…

Morocco stock exchange ended the month in green following affirmation of investment grade accompanied by stable outlook by Fitch. Fitch has affirmed Morocco's Country Ceiling at 'BBB'. Morocco's 'BBB-' rating which is supported by a strong macroeconomic performance, as evidenced by low inflation, sustained GDP growth and general government debt (39% of GDP) in line with rating peers. Recent success in managing the political transition has underlined Morocco's political stability. Economic dependence on Europe (60% of current account receipts, 80% of foreign tourists and remittances and 50% of exports in 2011) and on oil imports contributed to higher fiscal and current account deficits in 2011 and represent significant downside risks. However, Fitch expects these 'twin deficits' to begin narrowing this year, supported by recent and prospective measures to reduce fuel subsidies, and supporting the Stable Outlook.

BRIC gained 0.5%. Amongst the BRIC countries, China rose by 1.9% while Brazil and Russia lost 3.1% and 0.5% respectively.

Chinese stocks rose in November led by some improving economic data. China’s factory output and retail sales exceeded forecasts and inflation unexpectedly cooled to the slowest pace in 33 months, signaling the government is boosting growth without driving a rebound in prices. Industrial production rose 9.6% in Oct from a year earlier. Retail sales growth of 14.5% picked up from Sept 14.2%. China’s exports rose more than estimated in October, adding to signs that the economy will rebound this quarter after industrial output climbed at the fastest pace in five months. Overseas shipments increased 11.6% from a year earlier. Imports increased 2.4%, the same pace as the previous month. The trade surplus was $32 bn. The HSBC China Manufacturing Purchasing Managers Index rose to 50.5 in November —a 13 month high.

EM-Latin America was the only emerging market to end in the negative. The top losers were Chile and Brazil, which fell by 3.3% and 3.1% respectively.

Brazilian stock exchange Bovespa ended in the negative as Brazil reported much slower economic growth in the third quarter than forecasters expected, piling pressure on President Dilma Rousseff to make deeper structural reforms and adding to fears that the global slowdown is hurting big emerging markets. HSBC's Purchasing Managers Index (PMI) for the Brazilian services sector fell to 50.4 in October from 52.8 in September on a seasonally adjusted basis, but remained above the 50 mark that divides expansion from contraction. The slowdown in economic activity at services companies during October was unexpected, as analysts were expecting the economy to gain further momentum in the fourth quarter. Analysts covering Brazil’s economy lowered their 2012 and 2013 growth forecasts for the second straight week, as a lack of investment and the weak global economy outweigh the effects of stimulus measures in the world’s second- biggest emerging market.

HOME

Retail Research

17

Monthly Report December 2012

Global Market Outlook

US fiscal cliff – if unresolved, could quickly reverse the sentiments

The recent sharp rally in most of the developed and emerging markets was largely on the optimism that the US leaders will reach deal to avoid "fiscal cliff". The fiscal cliff refers to the possibility of more than $600 bn of automatic tax hikes & spending cuts kicking in from Jan 2013, if the US Congress fails to act. However, it is to be noted that till now, there has been little progress in U.S. "fiscal cliff" talks. With barely a month left before the "fiscal cliff", Republicans and Democrats remained far apart in talks to avoid across-the-board tax hikes & spending cuts that threaten to throw the country back into recession.

In the U.S., the confidence level in the politicians (including the President) to solve the so-called fiscal cliff before the end of the year does not seem to be very high. Both sides (Republicans & Democrats) have sort of blinked indicating that they might compromise on a solution involving both tax increases and spending cuts. This uncertainty along with the uncertainty coming from social programs like the implementation of Obamacare are keeping many companies on the hiring sidelines and thus the lingering unemployment situation does not look like it will be solved anytime soon. Net result is that the US economy is also faltering as evidenced by the macroeconomic data.

We are still of the view that the fiscal cliff will be avoided and President Obama and the Congress will settle down to a deal over the next several weeks. President would definitely want to start his next and last term in office on a positive note. A solution to the fiscal cliff would definitely be positive for the equity markets in the US and likely have a positive impact on most global equity markets. It could also move the attention of market participants back to the many stimulus or quantitative easing programs around the world. However, the failure to reach a deal could result in massive uncertainties for the US economy and the consequent sharp sell off in the equity markets across the globe.

Latest economic data in China points towards an improvement; approaching low but sustainable GDP growth

The latest data out of the world's second-largest economy shows that China could be past the worst of the economic slowdown that's concerned policy makers. Given below are some of the economic data released in November, which gives evidence that the economy is improving gradually:

Monthly Equity Commentary contd…Outlook going forward

Retail Research

18

Monthly Report December 2012

China’s factory output and retail sales exceeded forecasts and inflation unexpectedly cooled to the slowest pace in 33 months, signaling the government is boosting growth without driving a rebound in prices. Industrial production rose 9.6% in Oct from a year earlier. That exceeded the 9.4% median estimate of analysts surveyed by Bloomberg News. Retail sales growth of 14.5% picked up from Sept 14.2%. The consumer- price index increased 1.7%.

The economy’s exports rose more than estimated in Oct. Overseas shipments rose 11.6% from a year earlier. Imports increased 2.4%, the same pace as the previous month. The trade surplus was $32 bn.

The pace of activity in China's vast manufacturing sector quickened for the first time in 13 months in Nov, a survey of private factory managers found, adding to evidence that the economy is reviving after seven quarters of slowing growth. The final reading for the HSBC Purchasing Managers' Survey (PMI) rose to 50.5 in November from 49.5 in October, in line with a preliminary survey. It was the first time since October 2011 that the survey crossed above 50 points, the line that demarcates accelerating from slowing growth. An official PMI survey of China's non-manufacturing sectors also ticked up, to 55.6 in November from 55.5 in October, led by expanded activity in construction services.

China's economic health has improved since September, with an array of indicators from factory output to retail sales and investment showing Beijing's pro-growth policies are starting to gain traction. Given the recent signs of recovery, many analysts expect the economy to snap out of its longest downward cycle since the global financial crisis, and start to trend upwards in the fourth quarter.

While the economic data points towards the improvement, the GDP data has been disappointing. China's annual economic growth has dipped to 7.4% in the third quarter, slowing for seven quarters in a row and leaving the economy on course for its weakest showing since 1999. We feel that the days of 10% growth are probably over and that China is transforming to slower growth. However, this in our view is likely to be more sustainable & quality growth. China is transforming its economic growth toward a more balanced direction, from export- and investment-driven growth toward a more domestically centered model based on internal consumption, rising incomes, and environmental sustainability. This transformation would not be easy. The Chinese need more confidence to raise consumption and a stronger support mechanism in terms of healthcare and pensions and less corruption. The policymakers will have to realize all of these and keep trying to improve things. The end of a de-stocking cycle and a greater pace of investment are expected to keep driving up domestic demand.

Monthly Equity Commentary contd…

Retail Research

19

Monthly Report December 2012

Near-term, we feel that China will avoid a "hard landing". Growth of 7% to 7.5% is more likely. That is good, though not great, by China's standards, but investors need to adjust to China expanding at a slower clip than over the past three decades. Even so, China will remain a global powerhouse, directly accounting for about a third of global growth in 2013-17. In 2013, investment spending in China will probably exceed investment in the US and euro area combined.

European debt issues unlikely to be resolved anytime soon Europe, China's number one export market, does not seem to be any closer to putting their four-year old sovereign debt issues into the background permanently. Spanish and Portuguese workers are holding their first joint general strike while unions in Greece, Italy, France and Belgium are also holding work stoppages as part of a "European Day of Action and Solidarity" (as reported by Reuters). It certainly does not look like stability between the populace and the governments in the EU is coming anytime soon. This has been festering for about four years with the governments trying to solve their debt issues with spending cuts in a region where government spending has hardly been challenged in the past. Austerity in Europe is helping the debt problems but it is not doing much for the faltering economy nor for the protesting populace who have been accustomed to a plethora of social programs in Europe.

The agreement between Eurozone finance ministers and the IMF to save Greece from defaulting and to help the nation to cut the debt to target levels of 124% of GDP by 2020 and lower than 110% in 2022 are some of the positive steps. However, plans to forgive Greek debt, a step negotiators think is necessary to restore fiscal balance in Greece, have been shelved. Whether Greece would be able to live upto its promises or would it ask for another round of bailout in future is a big question. That only time will tell. The country’s crisis has seen many false dawns, and there are several open questions even about the latest plan. But the hope is that it will help restore a degree of confidence in Greece's future and make the euro zone look less fragile. Besides Greece, there are many other nations like Spain, Portugal & Italy, who could need support like Greece to survive.

Eurozone debt issue is a major problem that does not look like it will go away anytime soon and thus there is a likelihood that the EU economy will continue to falter and have a negative impact on sentiments globally, though in spurts.

Monthly Equity Commentary contd…

Retail Research

20

Monthly Report December 2012

Monthly Equity Commentary contd…

Indian Market Outlook

Stronger INR improves corporate profitability in Sept 2012 quarter, however, slower sales growth is a concern

An ETIG analysis of 2,300 companies, excluding banks, financial firms and oil marketing companies, based on data for 13 quarters, shows a turnaround in corporate profitability and operating profit margins. India Inc'soperating profit margins improved to 14.5%, which was the highest in the past five quarters. Net profit for the quarter rose 25% year-on-year – the highest in the past two years and a welcome break after four consecutive quarters of a slide. The second-quarter earnings have beaten estimates marginally on tempered expectations. However, it may be too early to cheer considering that the earnings were boosted because of a strong rupee during the past quarter. The Indian rupee rallied strongly to 52 against the US dollar at the end of the September 2012 quarter - up from 56 at the start of the quarter, helping local companies to cut their forexlosses. This took a chunk off other expenditure, boosting operating profits. Since then the rupee has started sliding.

The latest earnings figures confirm a few worrying trends from the recent past. The growth in net sales, at 10.4%, was the slowest in the past three years, while other income - income from non-core business activities -still constitutes over one-fourth of pre-tax profits. And India Inc's leveraging has risen during this period. Adjusted for inflation, it indicates virtually no volume growth for mainline companies. The upside in profitability has come from lower input cost such as raw materials and power & fuel, lower interest rates and an absence offorex losses in this quarter. Sensex companies (excluding financials) reported their worst quarter in the last three years with operating margins coming in at a 10-quarter low of 16.9%, while net sales growth at 12.1% was the lowest in the last 12 quarters.

The quarter's revival in earning numbers was led by sectors such as tyres, steel, metals, mining and minerals, cement and cement products, FMCG, Infotech and power generation. Similarly, the aggregate numbers of smaller industries, such as hospitality, laminates and plywood, agrochemicals, petrochemicals and tyres were also better than the past few quarters. Sectors such as paper, sugar, solvent extraction and ferro-alloys reported a return to profitability, compared to a loss in the September 2011 quarter. However, the troubles for sectors such as capital goods, real estate and construction, automobiles and telecom continue, given their under-performance. Smaller sectors such as chemicals, auto ancillaries and plastic products also had their own set of problems, impacting profitability.

Retail Research

21

Monthly Report December 2012

Monthly Equity Commentary contd…

Sustaining growth shown in the July-Sept quarter appears difficult

The capex cycle in India continues to be dragged by several issues, such as high interest rates, coal linkages, land acquisition issues, environmental clearances, etc. Given the weak macro economic numbers, high inflation (though moderating, still above the RBI comfort zone) and the challenges in the form of a twin current account and trade deficit, sustaining growth shown in the July-Sept quarter appears difficult for Indian companies especially with the weakening of the rupee. The extent and nature of reforms is open to debate but we highlight that composition of India’s earnings precludes any meaningful increase in earnings of the broad market on domestic factors alone. This is because global-linked, government-controlled companies and regulated sectors account for 57% of fiscal 2013 net profits of the Sensex companies. The earnings of several sectors depend on (1) global factors (private sector energy, metals, IT) or (2) Government regulations (coal and public sector energy). Demand growth would become even more challenging in the forthcoming quarters once the government starts cutting back on expenditure in its bid to bring down fiscal deficit. At around 30% of India’s gross domestic product, the government is the biggest consumer and investor in the economy. Its effect is likely to felt the most in rural demand where government pumps in money through various schemes such as rural employment guarantee schemes, food & fertilizer subsidy and rural development schemes.

Analysts don’t expect any quick turnaround in the corporate investment cycle given the poor earning visibility in most capex heavy sectors such as metals, auto, oil & gas and capital goods. The much-sought-after earnings upgrade cycle is some time away. However the market performance may not be as bleak as the expected macro and corporate performance. Equity markets could still perform well based on technical factors (that include flows from foreign and local players, lack of alternative asset class with promising returns, falling interest rates that could divert fresh money into equities etc).

Fiscal Consolidation measures a key for sovereign rating

Fiscal deficit in the first seven months of 2012-13 stood at 71.6% per cent of the Budget Estimates (BE), slightly better than 74.4% per cent in the same period a year ago, according to Controller General of Accounts (CGA) data. The slight improvement in fiscal deficit position is mainly on account of some tightening on the expenditure front. Meanwhile, the government has raised the fiscal deficit target for the current fiscal to 5.3% from the Budget Estimates of 5.1% of the GDP.

Retail Research

22

Monthly Report December 2012

Monthly Equity Commentary contd…

Mr. Chidambaram has said that the government has imposed measures like rationalization of expenditure and optimization of available resources with a view to improve fiscal deficit condition in the current year. This includes 10% mandatory cut on non-plan expenditure in the current year, ban on holding of meetings and conferences at five star hotels, ban on creation of plan and non-plan posts and restrictions on foreign travel. The government also endeavours to restrict the expenditure on central subsidies. Despite all this, considering the GDP growth reported in H1FY13, we feel that the Government could find it difficult to achieve this revised target also.

Going forward, for FY14, the government has taken initiatives toward fiscal consolidation which include (1) Setting up a platform for cash transfers and (2) Focusing on implementing GST. If implemented, this could possibly offset market fears of "yet another easy budget" in FY14, ahead of the next general elections. This would be one of the key factors that could help India avert a sovereign rating downgrade and help the government peg a deficit of less than 5.5% in FY14.

Rupee likely to remain volatile – Reforms could aid the capital inflows, but high CAD poses a threat

Rupee depreciated 0.8% for the month to close at 54.53 vs USD on Nov 30. Global uncertainty and month-end dollar demand related to oil purchases led to the fall of Indian Rupee (INR) against the dollar. The INR could have depreciated more in the month, but it recovered sharply from the lows of 55.7 (closing basis) since Nov 27. The rupee’s slide was halted after Moody’s maintained its stable outlook on the nation’s Baa3 sovereign rating which is the lowest investment-grade rating, though fiscal deficit remains a hindrance for an upgrade. Finance Minister P. Chidambaram’s comment that the Government will be able to manage the fiscal deficit at 5.3% for the year through March compared to 5.8% last year also helped rupee to recover sharply towards the end of the month. INR rise was also supported by fiscal cliff concerns and agreement by European finance ministers to ease the terms on emergency aid for Greece, which weighed on the dollar.

Going forward, domestic political environment will determine the movement of INR. This month, the Government is going to consider and pass about 25 legislative Bills in Parliament including, key reforms such as approval of 51% FDI in multi-brand retail, fuel subsidy and liberalization of the insurance and pension sectors. 49% FDI in airlines is also one of the biggest and toughest reform initiatives like FDI in retail that the UPA Government has taken in its tenure of eight years. SEB debt restructuring also appears to aim at plugging the gaps.

Retail Research

23

Monthly Report December 2012

Monthly Equity Commentary contd…

Clearing FDI in multi-brand retail has been very difficult. The entire BJP-led NDA is united in opposing the FDI decision. The Left parties, AIADMK, BJD, AGP and some other parties are also against the decision. With voting on FDI in retail becoming a crucial issue in Parliament, BJP and Congress are leaving no stone unturned to muster their numbers and block the passage of the bill. If the Government is able to pass FDI in retail, it could be a major booster for the equity markets, which could further strengthen the rupee, as it would give a hint of some more reform implementation in the coming months.

While the reforms could aid the capital flows, the relatively high CAD is likely to limit any reserve build-up. India's inelastic oil demand and gold is likely to keep the current account deficit elevated at 3.7% of GDP in FY13 and 2.8% in FY14. This coupled with the declining forex import cover and rating agencies on the vigil, is likely to result in the INR remaining very volatile over the next few months. Standard and Poor’s has signaled a one in three likelihood of a rating downgrade and Fitch will also review India’s rating in December. A possible sovereign rating downgrade may result in further depreciation.

Limited scope of monetary easing

A combination of cyclical and structural factors has resulted in inflation remaining well above the RBI's comfort zone of 4%-5% over the last three years. The latest readings of the WPI and CPI stand at 7.5% and 9.7% respectively. While the commodity prices have softened, rupee is likely to stay volatile. Hence it is difficult to say whether the inflation would moderate significantly from hereon.

During 2012, the RBI has (1) cut the repo rate by 50bps from 8.5% to 8% (2) Lowered the SLR by 100bps from 24% to 23% and (3) Reduced the CRR by 175bps from 5.5% to 4.25%. Assuming that the inflation moderates to ~7% levels, it still would continue to remain above RBI’s comfort zone. Hence, despite growth coming off sharply from ~8% levels to 5.4% in FY13E, sticky inflation leaves little room for much monetary easing.

Retail Research

24

Monthly Report December 2012

Monthly Equity Commentary contd…

Market currently gaining on renewed confidence on positive global & domestic policy actions, however macro indicators still not encouraging

The market rally over the last few months has mainly been on renewed confidence on positive global and domestic policy actions. The optimism in the markets could be attributed to factors such as ample global liquidity, policy actions taken in developed economies, initiation of policy reform measures taken by Indian government and assumption that the growth would improve in FY14. FII’s confidence in the Indian Markets has once again increased. FIIs have been net buyers of Rs. 1000 bn since Jan 01, 2012. At the current levels, the Sensex trades at 14.5-15xFY14E EPS. The valuations are still not stretched and equities could continue attracting buoyant capital inflows. Reform implementation could help markets extend its gains.

While the valuations still look reasonable on a PE basis, the question is why market deserves to go up further especially when the macroeconomic indicators are still weak and awaiting improvements. GDP growth has fallen to 5.5% in Q1FY13 and to 5.3% in Q2FY13. In FY12, the GDP growth stood at 6.5% in FY12. There is a consensus that the growth has bottomed out and improvement is expected in H2FY13. Inflation and the twin deficits - current account deficit (CAD) and fiscal deficit are likely to remain an overhang in the near-term.

A sustainable improvement in growth would depend on positive catalysts like reversal in the investment cycle and capex activity, a pick-up in the weak global demand and corrective policy action by the government through fiscal consolidation measures, reforms in power, mining and land acquisition to stimulate economic growth.

M&A (is coming to life), capital raising (the government and some private sector) and rising corporate profitability (higher margins and lower sales) could lend vibrancy and volatility to the markets going forward.

Disinvestment a key to contain fiscal deficit

Disinvestment would be the key to contain the fiscal deficit. The government should kick-start its disinvestment program to generate capital receipts in view of the buoyancy in equity markets. The budgeted disinvestment target for FY13 stands at Rs. 30,000cr and the government has indicated that it intends to divest about Rs.12,000cr-Rs.13,000cr by December-end. Current positive sentiments in the markets, supportive global cues and permitting LIC to invest upto 30% equity in a company from 10% earlier have given some rays of hope. However, any change in the market sentiments could make this year’s disinvestments target impossible to achieve. Government could find it difficult to garner the budgeted level of tax receipts due to the general slowdown in the economy and it could even exceed its budgeted market borrowing programme.

Retail Research

25

Monthly Report December 2012

Monthly Equity Commentary contd…

Global Liquidity & Optimism of fast turnaround in fundamentals could help the markets extend gains in the month of December

The market participants seem to have digested the weak macro indicators. Now there is a consensus that the fundamentals of the Indian economy could start improving quickly from H2FY13, though there are no significant visible signs of improvement in fundamentals. We feel that this rally has more to do with the global liquidity & hopes of reform implementation in India rather than the being fundamentally driven. There is optimism that US would avoid fiscal cliff and Eurozone ministers would bailout other countries if necessary like Greece. These positive sentiments could continue to support the Indian markets, which could extent its gains in the month of December before the investors actually start focusing back on the fundamentals.

A decline in oil prices in real terms over the next few years, a more favorable external demand outlook and domestic structural reforms which can ease some supply-side constraints are some of the fundamental kickers that India needs at this point in time.

Going back 32 years to 1980, December has produced a 4.6% median return with an 80% probability– the best for any month in the calendar. Over the past 20 years, 1994, 2000, 2001 and 2011 are the only four occasions when December generated negative returns.

We expect the Sensex to trade in the range of 18500-20000 in the month of December. The ongoing optimism could even result in Sensex testing its all time highs of 21200 in the next one-two months. However, one needs to be cautious at higher levels and take some profits out of the table.

The key concerns include rise in geo political tensions, spike in Oil prices, rollback (or no implementation) of recently announced policy measures, pre mature elections in India, political gridlock in the US resulting in fiscal cliff, re-emergence of European risks – Greece exit, etc.

HOME

Retail Research

26

Monthly Report December 2012

Technical Commentary

We are assuming that from the level of 15,749, the Sensex is forming an impulse pattern as it is a wave ‘c’ of an a-b-c Flat pattern. And it has got structure label of 3-3-5. In this label 5 stands for an impulse pattern.

Whenever any impulse pattern is unfolding there are certain rules which must be followed and they are given below.

There are 3 waves in a sequence which are moving in the direction of the trend which in the present case is in upward direction. Out of this 3 waves one wave must be longer than the remaining two waves and it must be longer than 161.8% of any of these 2 waves. This rule is known as ‘Extension Rule’ in Neo Wave theory.

In the present case neither wave 1 nor wave 3 are 161.8% of each other. Hence the chances that wave 5 (which is currently going on) will become 161.8% of wave 1 or wave 3 are high. The 161.8% target for wave 5 is shown in the graph below.

Retail Research

27

Monthly Report December 2012

Technical Commentary contd…

There is another rule which is known rule of similarity and which states that the unextended waves will be similar in price. And in the present case wave 1 and wave 3 are almost exact in the price which is marked on the chart above.

Now there is a rule which states that the wave 3 cannot be the shortest when wave 1,3 and 5 are taken in consideration. In this case wave 3 is bigger than wave 1 (by just 3 points), and thus satisfies both the conditions of being larger than wave 1 and at the same time similar in the price.

Now as discussed above there are bright chances that wave 5 will be an extended wave whose future projections are given in the chart above.

Retail Research

28

Monthly Report December 2012

Technical Commentary - Month Gone By contd…

For the month of November the Sensex opened at 18,488, made an intraday low at 18,445 and finally closed at 18,562. On the next day it opened with a ‘Western Gap Up’ and continued its upward march for next 3 trading sessions. It formed an intermediate top at 18,973 and from there onwards the downward correction began.

There onwards the Sensex came down for 8 trading sessions and for 3 trading sessions the level of 18,256 was not breached which is marked on the chart above with red horizontal trend line.

After forming the intermediate bottom at 18,256 for next 4 trading sessions it is forming Up Day on the daily charts with one exception.

Finally the bulls took the charge of the situation and in next 3 trading sessions 2 ‘Western Gap Up’ patterns were formed and the Sensex breached the previous top which was the top formed by wave 3 at 19,137.

The new yearly high so far was made at 19,373 and finally the Sensex closed at 19,340.

The significant ‘Faster Retracement’ of the last move suggests that a new wave has begun and it will be labeled as wave 5.

HOME

Retail Research

29

Monthly Report December 2012

Learning Technical Analysis

The 3 most reliable technical indicators

There are thousands of indicators that are used to find opportunities in the market and profit from them. However, most of them do not give good signals and will get you in the market late. In this article we will present 3 indicators which can give you a trading edge.

Indicator #1: The Bollinger Bands

The Bollinger Bands were developed 20 years ago by John Bollinger, and were designed to show the volatility of the market on the screen in an easy-to-comprehend manner.

They give very good signals and can be used as support\resistance indicators, telling us - before the move occurs - that a reversal is prone to happen. When price touches the lower band it is oversold, and when price touches the upper band it is overbought.

The trading method for the Bollinger Bands is basically to look for price-action support and resistance levels, and confirm them with bounces on the Bollinger Bands themselves. This results in very high win rate and consistent profits.

Indicator #2: The Relative Strength Index (RSI)

The Relative Strength Index was developed 30 years ago by J. Welles Wilder, and is considered a powerful trading indicator that also has a predictive edge in the markets. It tells us when the price is overbought\oversold before the trends begin, so we can enter early and have great reward with little risk. The signals it gives are usually very accurate, and if confirmed using the Thomas DeMark mild bounce system it can even reach 70-80% win rate (depending on the timeframe). It is a very accurate indicator.

Indicator #3: Simple Moving Average

The Simple Moving Average, or the SMA, is an interesting indicator. Most traders use it as a trend-following indicator to enter trades after a trend has been established. However, it can be used in an entirely different way by using the bounce method.

Retail Research

30

Monthly Report December 2012

Learning Technical Analysis contd…

In this method, we wait for trend to establish, but instead of randomly entering, we wait for price to retrace to the moving average and bounce off it. Once a reversal signal is given we enter a trade in the direction of the trend with stop loss right below the moving average, thus entering at a tactical point with small stop loss and huge reward.

HOME

Retail Research

31

Monthly Report December 2012

The month of Nov 2012 saw the Nifty trading in a tight range between the 5548-5777 levels. The index broke out of this range towards the end of the month thereby confirming a continuation of the intermediate uptrend. M-o-M, the Nifty gained 4.63%.

In the cash market, FIIs were reported as net buyers of Rs. 9718 cr in Nov 2012 (In October, they were net buyers of Rs. 9578 cr). In the F&O space, the FIIs were net buyers in the Index Futures segment of Rs.2228 cr. The increase in the open interest in that segment reflects additional long positions taken and value effect. In the index Options segment, the FIIs were net buyers of Rs.5395 cr, which was accompanied with an increase in the open interest. In the Stock Futures segment, FIIs were small net buyers, while open interest rose mainly due to value effect.

The Nov series has started on a heavier note compared to the previous series. In terms of value, the Dec 2012 series has begun with market wide OI at Rs.1,03,801crs. Vs. Rs.96,625crs. at the beginning of the Nov 2012 series. It was Rs.1,04,572crs. at the beginning of the Oct 2012 series. The higher participation levels in the Dec series (compared to the previous series) indicates that traders are willing to take more risk.

Derivatives Commentary

Retail Research

32

Monthly Report December 2012

Rollovers to the Dec series were higher compared to the previous series. Nifty rollovers were at 72% Vs. 63% during the same time in the previous series. Market wide rollovers were at 84% Vs. 83% the same time in the previous series. The fact that the Dec Futures closed at a hefty premium of 46.4pts suggests rollover of long positions. The higher rollovers to the Dec series suggests that bull conviction levels have increased.

Coming to stock specific rollovers, highest rollovers were seen in Suzlon, Welcorp, Aditya Birla, Guj Flouro andTata Comm. The lowest rollovers were seen in Andhra Bank, Canara Bank, Wipro, Asian Paints and Exide Ind.

Reflecting the bullish trend in the markets, especially towards the end of the Nov series, the Nifty OI PCR climbed to 1.31 from 1.26 at the start of the previous series. Reflecting increasing volatility expectations, the Nifty IV climbed to 14.07% from 13.92% the same time in the previous series.

Technically, the Nifty is in a firm uptrend after finding support around the 5550 levels and convincingly crossing the previous intermediate highs of 5777. Nifty is likely to test the 6000 levels in the Dec series.

Index option activity suggests that traders are expecting the Nifty to trade within the 5800-6000 levels in the coming month. We say this because the maximum call writing and build up of OI is currently being seen in the 5900-6000 call strikes. Maximum put writing and build up is being seen in the 5800 put strikes.

So, it seems that market participants have a bullish bias with the 5800 level acting as a key support to watch.

HOME

Derivatives Commentary contd…

Retail Research

33

Monthly Report December 2012

Learning Derivatives Analysis

Bull Calendar Spread

Using calls, a bull calendar spread strategy can be setup by buying long term slightly out-of-the-money calls and simultaneously writing an equal number of near month calls of the same underlying security with the same strike price. The options trader applying this strategy is bullish for the long term and is selling the near month calls with the intention to ride the long term calls for free.

Bull Calendar Spread Construction

Sell 1 Near-Term OTM Call Buy 1 Long-Term OTM Call

Unlimited Upside Profit Potential

Once the near month options expire worthless, this strategy turns into a discounted long call strategy and so the upside profit potential for the bull calendar spread becomes unlimited.

Limited Downside Risk

The maximum possible loss for the bull calendar spread is limited to the initial debit taken to put on the spread. This happens when the stock price goes down and stays down until expiration of the longer term call.

This strategy is used when a trader wants to make profit from a steady increase in the stock price over a short period of time.

Example:

Suppose NIFTY is trading at 5300 levels, Mr. X is bullish on the market and expects it to rise in the near future say 2 months or so. He will sell one 5400 NIFTY April (near-month) OTM Call Option for a premium of Rs. 25 and buy one 5400 NIFTY May (next-month) OTM Call Option at a premium of Rs. 110. The lot size of NIFTY is 50. Hence, his net investment will be Rs. 4250. [(110-25)*50]

Retail Research

34

Monthly Report December 2012

Learning Derivatives Analysis contd…

Case 1: At Near-Month (April) expiry if NIFTY closes at 5000, then Mr. X will get to keep the premium amount i.e. Rs. 1250. (25*50)

At Mid-Month (May) expiry if NIFTY closes at 4800, then Mr. X will make a loss of premium amount i.e. Rs. 5500. (110*50).

His net payoff will result in a loss of Rs. 4250. (5500-1250)

Case 2: At Near-Month (April) expiry if NIFTY closes at 5100, then Mr. X will get to keep the premium amount i.e. Rs. 1250. (25*50)

At Mid-Month (May) expiry if NIFTY closes at 5300, then Mr. X will make a loss on premium amount i.e. Rs. 5500. (110*250).

His net payoff will result in a loss of Rs. 4250. (5500-1250)

Case 3: At Near-Month (April) expiry if NIFTY closes at 5500, then Mr. X will incur a loss of Rs. 3750. [(100-25)*50]

At Mid-Month (May) expiry if NIFTY closes at 5700, then Mr. X will make a profit of Rs. 9500. [(300-110)*250]

His net payoff will result in a profit of Rs. 5750. (9500-3750)

Reverse calendar spread:

If the trader, instead, buys a nearby month's options in some underlying market and sells that same underlying market's further-out options of the same strike price, this is known as a reverse calendar spread/bear calendar spread. This strategy will tend strongly to benefit from a decline in the overall implied volatility of that market's options over time.

Buy 1 Near-Term OTM Call

Sell 1 Long-Term OTM Call

HOME

Retail Research

35

Monthly Report December 2012

Index Futures Calls

Extract of Calls during November 2012 contd…

Stock and Nifty Options Calls

Trading/BTST/Futures Calls

Date B/S Trading Call Entry at Sloss Targets Exit Price / CMP Exit Date % G/L Comments Time Horizon Avg. Entry Abs. Gain/Loss

2-Nov-12 S Bank Nifty Nov Fut 1470-11520 11530.0 11360.0 11530.0 2-Nov-12 -0.3 Stop Loss Triggered 3-5 days 11495.0 -35.0

9-Nov-12 S Bank Nifty Fut 1705-11760 11765.0 11625.0 11656.0 9-Nov-12 0.5 Premature Profit Booked 2-3 days 11709.0 53.0

22-Nov-12 B Bank Nifty Future 490 - 11535 11480.0 11610.0 11589.0 22-Nov-12 0.6 Premature Profit Booked 2-3 days 11525.0 64.0

23-Nov-12 B Bank Nifty Future 1400-11455 11390.0 11550.0 11549.0 27-Nov-12 0.9 Premature Profit Booked 2-3 days 11447.0 102.0

Date B/S Trading Call Entry at Sloss Targets Exit Price / CMP Exit Date % G/L Comments Time Horizon Avg. Entry Abs. Gain/Loss

1-Nov-12 B M&M Nov 900 Call Option 22-24.5 17.1 40.0 31.0 2-Nov-12 32.9 Premature Profit Booked 1-3 days 23.3 7.7

2-Nov-12 B Adani Ent 230 Call Option 11-7 5.0 17.0 5.0 15-Nov-12 -50.0 Stop Loss Triggered 7 days 10.0 -5.0

5-Nov-12 B Reliance Cap 400 Call Option 17.6-13 11.0 25.0 21.8 7-Nov-12 36.3 Premature Profit Booked 3 days 16.0 5.8

8-Nov-12 B GAIL 360 Put Option 7-4 2.0 14.0 10.0 16-Nov-12 42.9 Premature Profit Booked 5 days 7.0 3.0

15-Nov-12 B M&M 880 Nov Put Option 7.7-6 5.0 15.0 5.0 19-Nov-12 -32.0 Stop Loss Triggered 3-5 days 7.4 -2.4

16-Nov-12 B ICICI Bank 1040 Put Option 16-13 10.0 25.0 24.9 16-Nov-12 55.6 Premature Profit Booked 3 days 16.0 8.9

16-Nov-12 B TCS 1300 Put Option 15.15-1 8.0 25.0 20.2 16-Nov-12 34.7 Premature Profit Booked 5 days 15.0 5.2

19-Nov-12 B Reliance 780 Call Option 6.5-4 2.0 12.0 11.9 29-Nov-12 95.1 Premature Profit Booked 3 days 6.1 5.8

20-Nov-12 B Bank Nifty 11300 Put Option 113-100 90.0 150.0 90.0 21-Nov-12 -15.5 Stop Loss Triggered 3 days 106.5 -16.5

27-Nov-12 B Bank Nifty 11700 Call Option 24-35 20.0 70.0 45.0 27-Nov-12 39.5 Premature Profit Booked 2-3 days 32.3 12.8

29-Nov-12 B SBI Dec 2150 Call Option 61-54 45.0 90.0 79.3 30-Nov-12 34.4 Premature Profit Booked 3 days 59.0 20.3

29-Nov-12 B Nifty 5800 Call Option 4-8.5 3.0 20.0 10.5 29-Nov-12 40.9 Premature Profit Booked 1 day 7.5 3.1

Date B/S Trading Call Entry at Sloss Targets Exit Price / CMP Exit Date % G/L Comments Time Horizon Avg. Entry Abs. Gain/Loss

1-Nov-12 B Aptech Training 67-67.8 66 72 66.0 12-Nov-12 -2.4 Stop Loss Triggered 1-3 days 67.6 -1.6

1-Nov-12 B Indo Rama 24.5-26 26.75 30.5 26.9 1-Nov-12 3.9 Premature Profit Booked 2-3 days 25.9 1

2-Nov-12 B Kwality 26-25.5 27 28.5 27.8 2-Nov-12 6.7 Premature Profit Booked 3-5 days 26 1.75

2-Nov-12 S Renuka Sugar Fut 31.5-32.5 32.7 29 32.5 7-Nov-12 -2.5 Premature Exit 1-3 days 31.65 -0.8

2-Nov-12 B Brigade 65-68 70.3 76 71.5 2-Nov-12 5.9 Premature Profit Booked 2-3 days 67.5 4

7-Nov-12 B Educomp 150-152.3 147 163 147.0 12-Nov-12 -3.4 Stop Loss Triggered 2-4 days 152.15 -5.15

8-Nov-12 B HT Media 98.3-97 95 108 100.8 8-Nov-12 2.5 Premature Profit Booked 3-5 days 98.3 2.5

8-Nov-12 B Hind Oil Exp 98-99.75 96 108 96.0 20-Nov-12 -3.6 Stop Loss Triggered 1-3 days 99.55 -3.55

8-Nov-12 B Saregama 86-89.5 91.3 97.5 92.8 8-Nov-12 4.0 Premature Profit Booked 2-3 days 89.25 3.55

12-Nov-12 B Madhucon Projects 34.5-36.5 34.25 40 34.3 15-Nov-12 -4.3 Stop Loss Triggered 2-3 days 35.8 -1.55

19-Nov-12 B VIP Industries 77.6-75 73 85 82.5 20-Nov-12 7.1 Premature Profit Booked 7 days 77 5.5

19-Nov-12 B 20 Microns 140-135 130 155 146.7 19-Nov-12 5.5 Premature Profit Booked 5 days 139 7.7

27-Nov-12 B Orbit Corp 55.1-53 52 61 57.7 29-Nov-12 4.8 Premature Profit Booked 5 days 55 2.65

27-Nov-12 B Liberty Shoe 99-104 112 117 113.6 27-Nov-12 10.1 Premature Profit Booked 2-3 days 103.15 10.45

29-Nov-12 B ICICI Bank 1045-1054.5 1025 1120 1097.9 30-Nov-12 4.3 Premature Profit Booked 2-4 days 1052.25 45.65

Retail Research

36

Monthly Report December 2012

Positional Calls

Extract of Calls during November 2012 contd…

HOME

Date B/S Trading Call Entry at Sloss Targets Exit Price / CMP Exit Date % G/L Comments Time Horizon Avg. Entry Abs. Gain/Loss

2-Nov-12 B Torrent Power 161.95-157 153.0 172.0 165.2 7-Nov-12 2.3 Premature Profit Booked 3 days 161.5 3.7

6-Nov-12 B Hexaware 113.8-112 110.0 124.0 110.0 15-Nov-12 -3.3 Stop Loss Triggered 1 week 113.8 -3.8

6-Nov-12 B DLF 198-205 197.0 225.0 213.5 8-Nov-12 4.5 Premature Profit Booked 2-3 days 204.4 9.1

7-Nov-12 B Praj Ind 46.25-45.25 44.3 50.5 48.5 15-Nov-12 4.8 Premature Profit Booked 5-7 days 46.3 2.2

20-Nov-12 B C Mahendra 85-89.5 83.0 114.0 83.0 26-Nov-12 -5.4 Stop Loss Triggered 2 weeks 87.7 -4.7

Retail Research

37

Monthly Report December 2012

Gainers & Losers – November 2012

Top Gainers From F&O Top Losers From F&O

Top Gainers From CNX 500 Top Losers From CNX 500

HOME

Price Price

31-Oct-12 30-Nov-12 % chg

MCDOWELL-N 1175.8 1996.2 69.8

UNITECH 23.1 31.7 37.2

RCOM 54.0 71.5 32.4

KTKBANK 135.6 175.3 29.3

BHARTIARTL 269.7 337.0 25.0

SUNTV 329.3 408.8 24.1

UNIONBANK 195.7 242.7 24.0

SUZLON 15.8 19.6 23.7

ASHOKLEY 23.5 28.4 21.1

TITAN 259.3 311.7 20.2

Price Price

31-Oct-12 30-Nov-12

INDIACEM 95.6 85.8 -10.3

OPTOCIRCUI 120.2 108.4 -9.8

CROMPGREAV 125.0 114.4 -8.5

NMDC 176.5 162.8 -7.8

GMRINFRA 20.1 18.6 -7.2

TECHM 948.5 880.1 -7.2

BHUSANSTL 492.6 461.8 -6.3

RANBAXY 526.1 504.2 -4.2

HINDPETRO 298.7 287.0 -3.9

PETRONET 168.2 162.5 -3.4

% chg

Price Price

31-Oct-12 30-Nov-12

MCDOWELL 1175.8 1996.2 69.8

JETAIRWAYS 335.6 527.1 57.0

SHREE ASHTA 2.2 3.3 53.5

SKS MICRO 112.8 165.4 46.6

FCH 153.5 220.8 43.9

SUJANATOW 5.4 7.7 42.6

L&TFH 54.2 75.0 38.5

UNITECH 23.1 31.7 37.2

DBREALTY 98.1 132.3 34.9

EROSMEDIA 162.6 215.3 32.4

% chg

Price Price

31-Oct-12 30-Nov-12

KEMROCK 74.4 56.5 -24.1

DCHL 7.5 6.2 -17.4

ORISSAMINE 4359.3 3744.2 -14.1

AIAENG 389.5 334.9 -14.0

ABAN 440.4 381.4 -13.4

INDSWFTLAB 56.3 48.8 -13.3

SIMPLEXINF 203.6 177.2 -12.9

INDIAGLYCO 213.9 186.8 -12.6

KGL 4.4 3.9 -12.5

SHANTIGEAR 66.6 58.3 -12.5

% chg

Retail Research

38

Monthly Report December 2012

HDFC Securities Limited, I Think Techno Campus, Bulding –B, ”Alpha”, Office Floor 8, Near Kanjurmarg Station,Opp. Crompton Greaves, Kanjurmarg (East), Mumbai 400 042 Phone (022) 30753400 Fax: (022) 30753435

Disclaimer: This document has been prepared by HDFC Securities Limited and is meant for sole use by the recipient and not for circulation. This document is not to be reported or copied or made available to others. It should not be considered to be taken as an

offer to sell or a solicitation to buy any security. The information contained herein is from sources believed reliable. We do not represent that it is accurate or complete and it should not be relied upon as such. We may have from time to time positions or options

on, and buy and sell securities referred to herein. We may from time to time solicit from, or perform investment banking, or other services for, any company mentioned in this document. This report is intended for non-Institutional Clients only.

Head of Research

Deepak Jasani

Technical/Derivatives Analyst

Adwait Sapre

Subash Gangadharan

Siddharth Deshpande

Nagaraj Shetti

Fundamental Analyst

Mehernosh Panthaki

Sneha Venkatraman

Tiju K Samuel

Kushal Sanghrajka

Siji Philip

RETAIL RESEARCH TEAM

Production

Sushma Chavan

Mutual Fund Analyst

Dhuraivel Gunasekaran