27-28 February 2018 · PDF file9.00 CHAIR’S OPENING REMARKS ... National Sales Manager...

7

Sponsors MARKETING & PARTNERSHIPS: Lindsey Guest, [email protected] SPEAKING OPPORTUNITIES Corinna Algranti, [email protected] SPONSORSHIP OPPORTUNITIES: [email protected] Contact [email protected] for sponsorship opportunities storage.solarenergyevents.com 27-28 February 2018 LONDON, UK Would/would likely attend Energy Storage Summit again 100% In terms of face-time with company representatives on stands, as well as networking opportunities, this was the best storage related event that I have been to over the last year or so. Trevor Hunter, Coriolis Energy Already confirmed to attend in 2018:

Transcript of 27-28 February 2018 · PDF file9.00 CHAIR’S OPENING REMARKS ... National Sales Manager...

Sponsors

MARKETING & PARTNERSHIPS: Lindsey Guest, [email protected]

SPEAKING OPPORTUNITIESCorinna Algranti, [email protected]

SPONSORSHIP OPPORTUNITIES: [email protected]

Contact

for sponsorship opportunities

storage.solarenergyevents.com

27-28 February 2018 LONDON, UK

Would/would likely attend Energy StorageSummit again

100%In terms of face-time with company representatives on stands, as well as networking opportunities, this was the best storage related event that I have been to over the last year or so.Trevor Hunter, Coriolis Energy

Already confirmed to attend in 2018:

Sponsors

MARKETING & PARTNERSHIPS: Lindsey Guest, [email protected]

SPEAKING OPPORTUNITIESCorinna Algranti, [email protected]

SPONSORSHIP OPPORTUNITIES: [email protected]

FEATURED SPEAKERS

Contact

for sponsorship opportunities

MACQUARIE CAPITALUlrika WisingHead of Energy Storage and Energy Efficiency

WESTERN POWERRoger HeyFuture Network Manager

ANESCOSteve ShineChairman

WGLRichard WalshProgram Lead- Solar & Energy Storage (USA)

FERCNancy BowlerBranch Chief

Sponsors

MARKETING & PARTNERSHIPS: Lindsey Guest, [email protected]

SPEAKING OPPORTUNITIESCorinna Algranti, [email protected]

SPONSORSHIP OPPORTUNITIES: [email protected]

BOOK NOW! storage.solarenergyevents.com

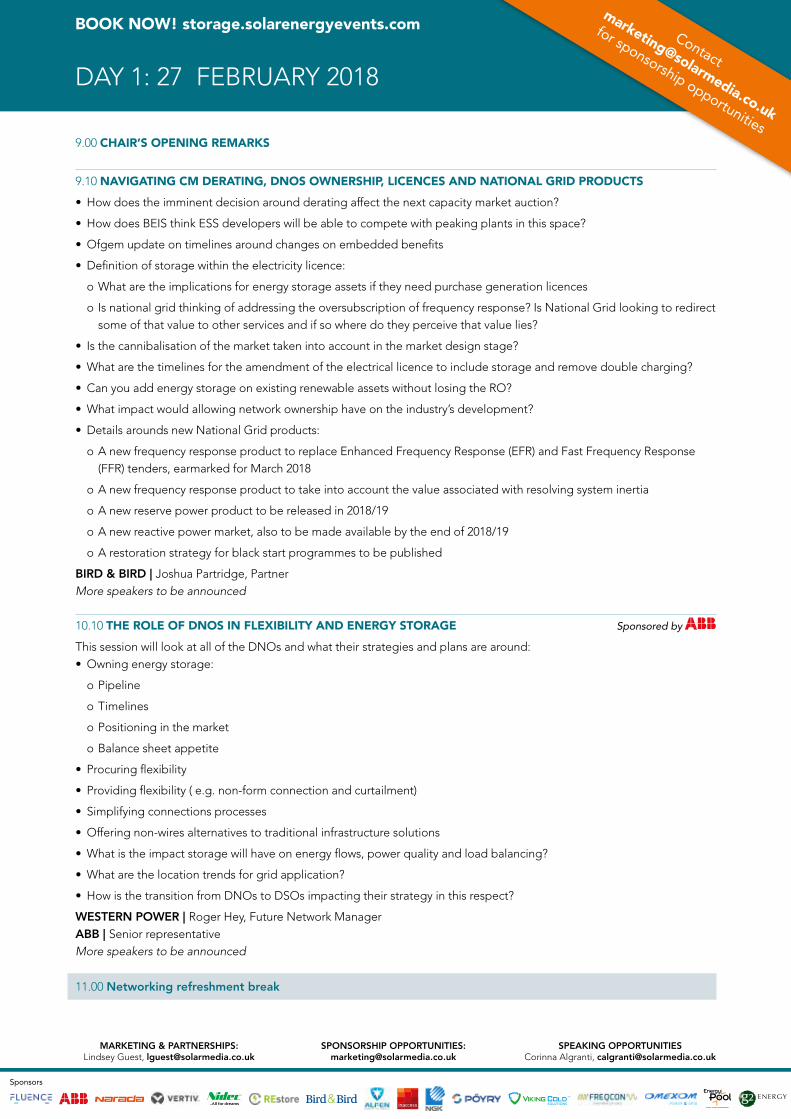

DAY 1: 27 FEBRUARY 2018

Contact

for sponsorship opportunities9.00 CHAIR’S OPENING REMARKS

9.10 NAVIGATING CM DERATING, DNOS OWNERSHIP, LICENCES AND NATIONAL GRID PRODUCTS

• How does the imminent decision around derating affect the next capacity market auction?

• How does BEIS think ESS developers will be able to compete with peaking plants in this space?

• Ofgem update on timelines around changes on embedded benefits

• Definition of storage within the electricity licence:

o What are the implications for energy storage assets if they need purchase generation licences

o Is national grid thinking of addressing the oversubscription of frequency response? Is National Grid looking to redirect some of that value to other services and if so where do they perceive that value lies?

• Is the cannibalisation of the market taken into account in the market design stage?

• What are the timelines for the amendment of the electrical licence to include storage and remove double charging?

• Can you add energy storage on existing renewable assets without losing the RO?

• What impact would allowing network ownership have on the industry’s development?

• Details arounds new National Grid products:

o A new frequency response product to replace Enhanced Frequency Response (EFR) and Fast Frequency Response (FFR) tenders, earmarked for March 2018

o A new frequency response product to take into account the value associated with resolving system inertia

o A new reserve power product to be released in 2018/19

o A new reactive power market, also to be made available by the end of 2018/19

o A restoration strategy for black start programmes to be published

BIRD & BIRD | Joshua Partridge, PartnerMore speakers to be announced

10.10 THE ROLE OF DNOS IN FLEXIBILITY AND ENERGY STORAGE Sponsored by

This session will look at all of the DNOs and what their strategies and plans are around:• Owning energy storage:

o Pipeline

o Timelines

o Positioning in the market

o Balance sheet appetite

• Procuring flexibility

• Providing flexibility ( e.g. non-form connection and curtailment)

• Simplifying connections processes

• Offering non-wires alternatives to traditional infrastructure solutions

• What is the impact storage will have on energy flows, power quality and load balancing?

• What are the location trends for grid application?

• How is the transition from DNOs to DSOs impacting their strategy in this respect?

WESTERN POWER | Roger Hey, Future Network ManagerABB | Senior representativeMore speakers to be announced

11.00 Networking refreshment break

Sponsors

MARKETING & PARTNERSHIPS: Lindsey Guest, [email protected]

SPEAKING OPPORTUNITIESCorinna Algranti, [email protected]

SPONSORSHIP OPPORTUNITIES: [email protected]

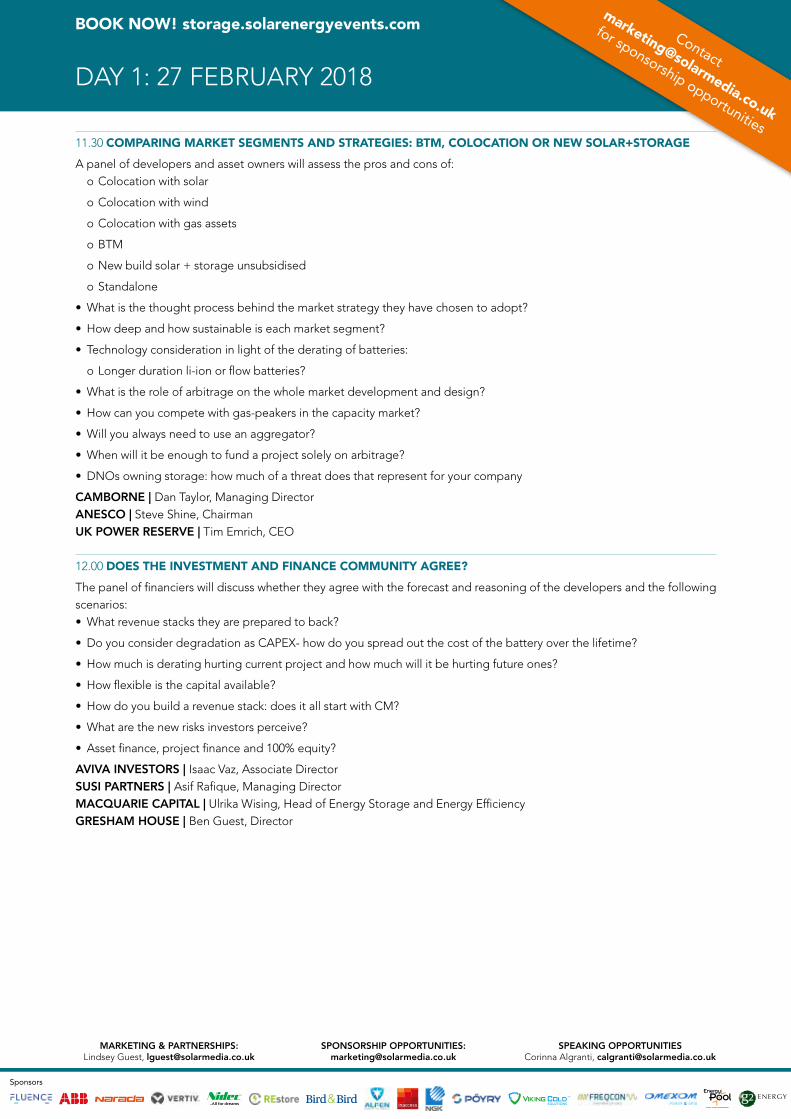

11.30 COMPARING MARKET SEGMENTS AND STRATEGIES: BTM, COLOCATION OR NEW SOLAR+STORAGE

A panel of developers and asset owners will assess the pros and cons of:o Colocation with solar

o Colocation with wind

o Colocation with gas assets

o BTM

o New build solar + storage unsubsidised

o Standalone

• What is the thought process behind the market strategy they have chosen to adopt?

• How deep and how sustainable is each market segment?

• Technology consideration in light of the derating of batteries:

o Longer duration li-ion or flow batteries?

• What is the role of arbitrage on the whole market development and design?

• How can you compete with gas-peakers in the capacity market?

• Will you always need to use an aggregator?

• When will it be enough to fund a project solely on arbitrage?

• DNOs owning storage: how much of a threat does that represent for your company

CAMBORNE | Dan Taylor, Managing DirectorANESCO | Steve Shine, ChairmanUK POWER RESERVE | Tim Emrich, CEO

12.00 DOES THE INVESTMENT AND FINANCE COMMUNITY AGREE?

The panel of financiers will discuss whether they agree with the forecast and reasoning of the developers and the following scenarios: • What revenue stacks they are prepared to back?

• Do you consider degradation as CAPEX- how do you spread out the cost of the battery over the lifetime?

• How much is derating hurting current project and how much will it be hurting future ones?

• How flexible is the capital available?

• How do you build a revenue stack: does it all start with CM?

• What are the new risks investors perceive?

• Asset finance, project finance and 100% equity?

AVIVA INVESTORS | Isaac Vaz, Associate DirectorSUSI PARTNERS | Asif Rafique, Managing DirectorMACQUARIE CAPITAL | Ulrika Wising, Head of Energy Storage and Energy EfficiencyGRESHAM HOUSE | Ben Guest, Director

BOOK NOW! storage.solarenergyevents.com

DAY 1: 27 FEBRUARY 2018

Contact

for sponsorship opportunities

Sponsors

MARKETING & PARTNERSHIPS: Lindsey Guest, [email protected]

SPEAKING OPPORTUNITIESCorinna Algranti, [email protected]

SPONSORSHIP OPPORTUNITIES: [email protected]

BOOK NOW! storage.solarenergyevents.com

DAY 1: 27 FEBRUARY 2018

Contact

for sponsorship opportunities

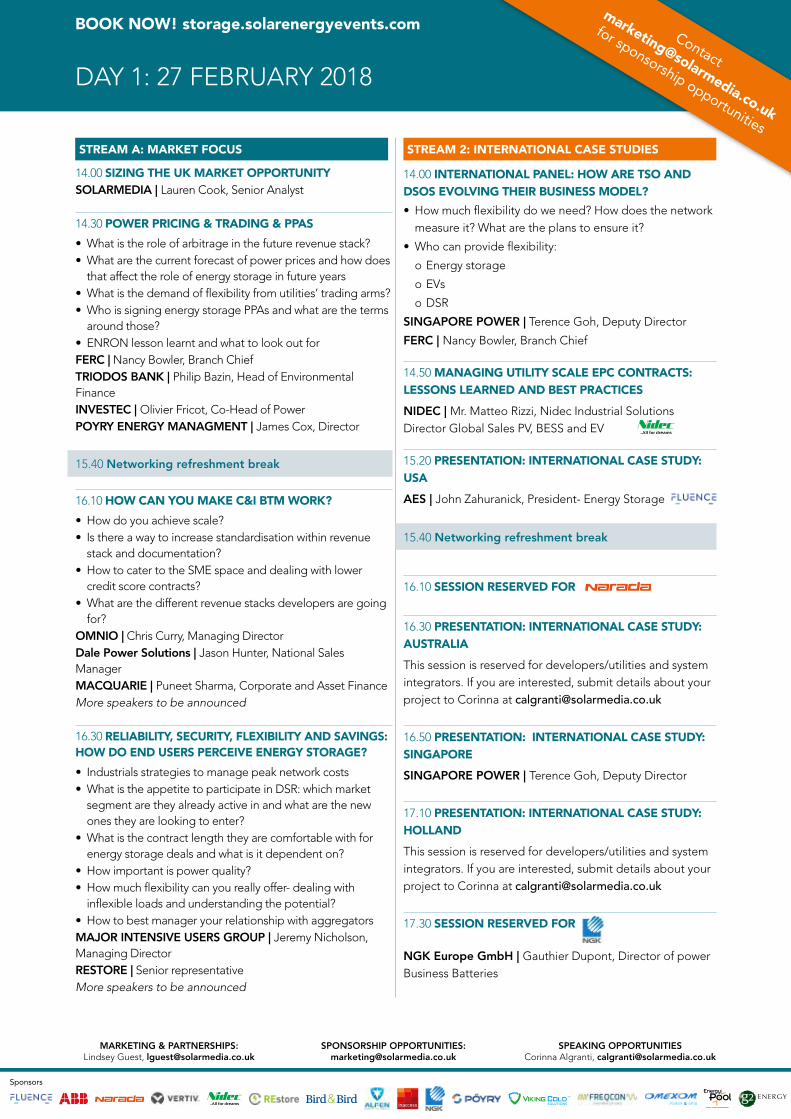

STREAM A: MARKET FOCUS

14.00 SIZING THE UK MARKET OPPORTUNITYSOLARMEDIA | Lauren Cook, Senior Analyst

14.30 POWER PRICING & TRADING & PPAS

• What is the role of arbitrage in the future revenue stack? • What are the current forecast of power prices and how does

that affect the role of energy storage in future years • What is the demand of flexibility from utilities’ trading arms?• Who is signing energy storage PPAs and what are the terms

around those?• ENRON lesson learnt and what to look out forFERC | Nancy Bowler, Branch ChiefTRIODOS BANK | Philip Bazin, Head of Environmental FinanceINVESTEC | Olivier Fricot, Co-Head of PowerPOYRY ENERGY MANAGMENT | James Cox, Director

15.40 Networking refreshment break

16.10 HOW CAN YOU MAKE C&I BTM WORK?

• How do you achieve scale?• Is there a way to increase standardisation within revenue

stack and documentation?• How to cater to the SME space and dealing with lower

credit score contracts?• What are the different revenue stacks developers are going

for?OMNIO | Chris Curry, Managing DirectorDale Power Solutions | Jason Hunter, National Sales ManagerMACQUARIE | Puneet Sharma, Corporate and Asset FinanceMore speakers to be announced

16.30 RELIABILITY, SECURITY, FLEXIBILITY AND SAVINGS: HOW DO END USERS PERCEIVE ENERGY STORAGE?

• Industrials strategies to manage peak network costs• What is the appetite to participate in DSR: which market

segment are they already active in and what are the new ones they are looking to enter?

• What is the contract length they are comfortable with for energy storage deals and what is it dependent on?

• How important is power quality?• How much flexibility can you really offer- dealing with

inflexible loads and understanding the potential?• How to best manager your relationship with aggregatorsMAJOR INTENSIVE USERS GROUP | Jeremy Nicholson, Managing DirectorRESTORE | Senior representativeMore speakers to be announced

STREAM 2: INTERNATIONAL CASE STUDIES

14.00 INTERNATIONAL PANEL: HOW ARE TSO AND DSOS EVOLVING THEIR BUSINESS MODEL?

• How much flexibility do we need? How does the network measure it? What are the plans to ensure it?

• Who can provide flexibility:

o Energy storage

o EVs

o DSR

SINGAPORE POWER | Terence Goh, Deputy Director

FERC | Nancy Bowler, Branch Chief

14.50 MANAGING UTILITY SCALE EPC CONTRACTS: LESSONS LEARNED AND BEST PRACTICES

NIDEC | Mr. Matteo Rizzi, Nidec Industrial Solutions Director Global Sales PV, BESS and EV

15.20 PRESENTATION: INTERNATIONAL CASE STUDY: USA

AES | John Zahuranick, President- Energy Storage

15.40 Networking refreshment break

16.10 SESSION RESERVED FOR

16.30 PRESENTATION: INTERNATIONAL CASE STUDY: AUSTRALIA

This session is reserved for developers/utilities and system integrators. If you are interested, submit details about your project to Corinna at [email protected]

16.50 PRESENTATION: INTERNATIONAL CASE STUDY: SINGAPORE

SINGAPORE POWER | Terence Goh, Deputy Director

17.10 PRESENTATION: INTERNATIONAL CASE STUDY: HOLLAND

This session is reserved for developers/utilities and system integrators. If you are interested, submit details about your project to Corinna at [email protected]

17.30 SESSION RESERVED FOR

NGK Europe GmbH | Gauthier Dupont, Director of power Business Batteries

Sponsors

MARKETING & PARTNERSHIPS: Lindsey Guest, [email protected]

SPEAKING OPPORTUNITIESCorinna Algranti, [email protected]

SPONSORSHIP OPPORTUNITIES: [email protected]

BOOK NOW! storage.solarenergyevents.com

DAY 2: 28 FEBRUARY 2018

Contact

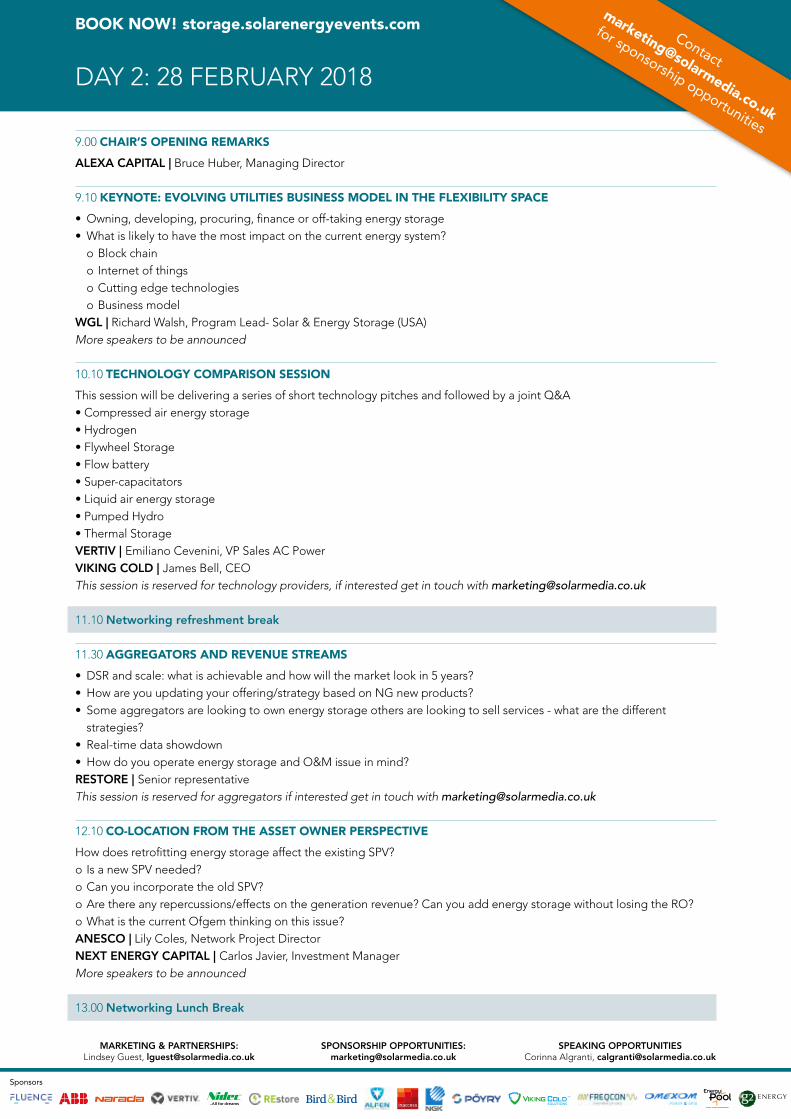

for sponsorship opportunities9.00 CHAIR’S OPENING REMARKS

ALEXA CAPITAL | Bruce Huber, Managing Director

9.10 KEYNOTE: EVOLVING UTILITIES BUSINESS MODEL IN THE FLEXIBILITY SPACE

• Owning, developing, procuring, finance or off-taking energy storage• What is likely to have the most impact on the current energy system?

o Block chaino Internet of thingso Cutting edge technologies o Business model

WGL | Richard Walsh, Program Lead- Solar & Energy Storage (USA)More speakers to be announced

10.10 TECHNOLOGY COMPARISON SESSION

This session will be delivering a series of short technology pitches and followed by a joint Q&A • Compressed air energy storage • Hydrogen • Flywheel Storage • Flow battery • Super-capacitators • Liquid air energy storage • Pumped Hydro • Thermal StorageVERTIV | Emiliano Cevenini, VP Sales AC PowerVIKING COLD | James Bell, CEOThis session is reserved for technology providers, if interested get in touch with [email protected]

11.10 Networking refreshment break

11.30 AGGREGATORS AND REVENUE STREAMS

• DSR and scale: what is achievable and how will the market look in 5 years?• How are you updating your offering/strategy based on NG new products?• Some aggregators are looking to own energy storage others are looking to sell services - what are the different

strategies?• Real-time data showdown• How do you operate energy storage and O&M issue in mind?RESTORE | Senior representative This session is reserved for aggregators if interested get in touch with [email protected]

12.10 CO-LOCATION FROM THE ASSET OWNER PERSPECTIVE

How does retrofitting energy storage affect the existing SPV?o Is a new SPV needed?o Can you incorporate the old SPV?o Are there any repercussions/effects on the generation revenue? Can you add energy storage without losing the RO?o What is the current Ofgem thinking on this issue?ANESCO | Lily Coles, Network Project DirectorNEXT ENERGY CAPITAL | Carlos Javier, Investment ManagerMore speakers to be announced

13.00 Networking Lunch Break

Sponsors

MARKETING & PARTNERSHIPS: Lindsey Guest, [email protected]

SPEAKING OPPORTUNITIESCorinna Algranti, [email protected]

SPONSORSHIP OPPORTUNITIES: [email protected]

BOOK NOW! storage.solarenergyevents.com

DAY 2: 28 FEBRUARY 2018

Contact

for sponsorship opportunities

15.40 Networking refreshment break

17.30 CONFERENCE ADJOURNS

STREAM 2: MARKET FOCUS

14.00 LOCAL AUTHORITIES PANEL

• London Storage tender to be awarded in December 2017

• Trent Basin project details

• Colocation with solar canopy and substations

NOTTINGHAM CITY COUNCIL | Wayne Bexton, Head of Energy

15.00 RESIDENTIAL AT SCALE: CASE STUDY

What are the different business models proposed to housing association and local authorities?

Where is the funding coming from?

M&G | David Kemp, Infrastructure Debt Fixed Income Director

16.10 O&M FOR ENERGY STORAGE

• How does and O&M contract looks like as opposed to other renewables ones?

• What are the key safety issues?

• Is there a lack of regulation around these issues?

This session is reserved for O&M providers. If you are interested get in touch with [email protected]

EV AND THE GRID

• How will the uptake of EVs will affect demand and flexibility needs?

STREAM 1: UK CASE STUDIES

14.00 COMPLETED EFR:

o Lesson learnt

o Timescales

o What needs to be changed for the next tender

GRIDSERVE | Mark Henderson, CIO

More speakers to be announced

15.00 UK CASE STUDY

VERTIV | Chris Campbell, VP Business Development

15.20 UK CASE STUDY

This session is reserved for developers/utilities and system integrators. If you are interested, submit details about your project to Corinna at [email protected]

16.10 UK CASE STUDY

ANESCO | Lily Coles, Network Project Director

16.30 UK CASE STUDY

This session is reserved for developers/utilities and system integrators. If you are interested, submit details about your project to Corinna at [email protected]

16.50 UK CASE STUDY

This session is reserved for developers/utilities and system integrators. If you are interested, submit details about your project to Corinna at [email protected]

17.10 UK CASE STUDY

This session is reserved for developers/utilities and system integrators. If you are interested, submit details about your project to Corinna at [email protected]