22-1 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by...

28

22-1 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig Deegan Slides prepared by Craig Deegan Chapter 22 Accounting for general insurance contracts

-

Upload

joel-stafford -

Category

Documents

-

view

230 -

download

5

Transcript of 22-1 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by...

22-1 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig DeeganSlides prepared by Craig Deegan

Chapter 22

Accounting for general insurance contracts

22-2 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig DeeganSlides prepared by Craig Deegan

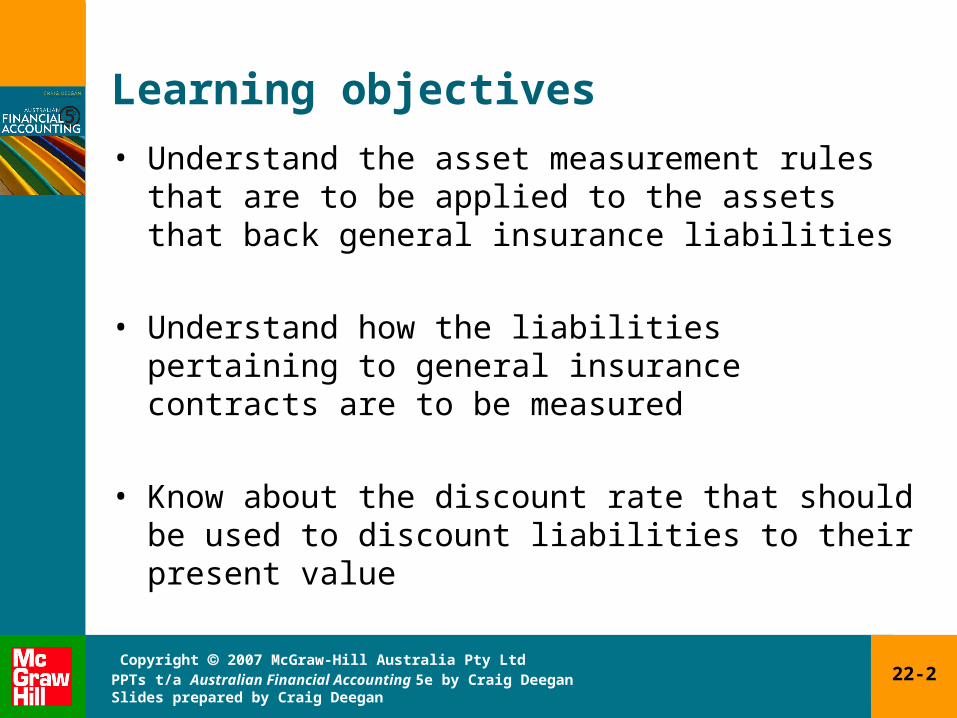

Learning objectives

• Understand the asset measurement rules that are to be applied to the assets that back general insurance liabilities

• Understand how the liabilities pertaining to general insurance contracts are to be measured

• Know about the discount rate that should be used to discount liabilities to their present value

22-3 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig DeeganSlides prepared by Craig Deegan

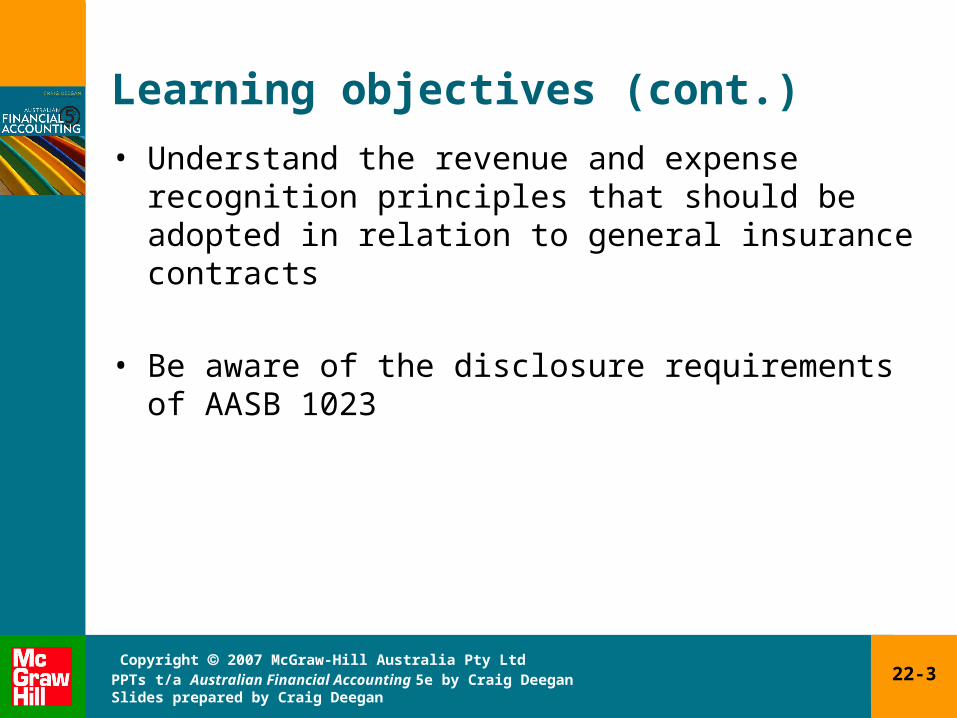

Learning objectives (cont.)

• Understand the revenue and expense recognition principles that should be adopted in relation to general insurance contracts

• Be aware of the disclosure requirements of AASB 1023

22-4 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig DeeganSlides prepared by Craig Deegan

Status of newly converged accounting standards

• For Phase I of the IASB’s ‘Insurance Project’, the AASB has significantly altered and reissued– AASB 1023 ‘General Insurance Contracts’– AASB 1038 ‘Life Insurance Contracts’

• The AASB also released– AASB 4 ‘Insurance Contracts’

22-5 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig DeeganSlides prepared by Craig Deegan

Introduction to general insurance contracts

• Currently we have three accounting standards dealing with insurance1. AASB 4

2. AASB 1023

3. AASB 1038

• The IASB is currently working on Phase II of the ‘Insurance Project’– it is expected that a revised standard will replace these three

standards

• This chapter focuses on AASB 1023

22-6 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig DeeganSlides prepared by Craig Deegan

The role of the HIH Royal Commission

• It appears that the re-release of AASB 1023 was affected by the Royal Commission

• Collapse of HIH Insurance Ltd in 2001 was one of the worst corporate collapses in Australia

• Justice Neville Owen commented that– the interpretation of certain key accounting standards was not

straightforward– wider participation in standard setting would be beneficial– the ‘true and fair’ concept is not given sufficient consideration

22-7 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig DeeganSlides prepared by Craig Deegan

The role of the HIH Royal Commission (cont.)

• Justice Neville Owen commented that (cont.)– an important factor contributing to HIH’s failure was

inaccurate reporting of financial information– inadequate reporting was caused partly by misinterpretation

of and deficiencies in standards

• Justice Owen’s recommendations for AASB 1023 were the following– the definition of insurance should include a requirement for

material transfer of insurance risk– insurance liabilities should be valued at level of sufficiency of

at least 75 per cent

22-8 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig DeeganSlides prepared by Craig Deegan

The role of the HIH Royal Commission (cont.)

• Justice Owen’s recommendations for AASB 1023 (cont.)– entities should disclose in their financial statements: valuation

of insurance liabilities, 75 per cent level of sufficiency and margin adopted

– premium revenue and insurance liabilities should be recognised on commencement of contract

– in estimating the present value of liabilities, a risk-free rate similar to that of prudential standards should be used

– companies should disclose a 10-year claims development table

22-9 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig DeeganSlides prepared by Craig Deegan

Introduction to the requirements of AASB 1023

• AASB 1023 applies to– general insurance contracts– certain assets backing general insurance liabilities– financial liabilities and financial assets under non-insurance

contracts– certain assets backing financial liabilities under non-insurance

contracts

• General insurance contract– insurance contract that is not a life insurance contract

22-10 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig DeeganSlides prepared by Craig Deegan

Introduction to the requirements of AASB 1023 (cont.)

• Life insurance contract– insurance contract or financial instrument with a discretionary

participation feature regulated under the Life Insurance Act 1995

• General insurance– typically for losses associated with theft, storms, vehicle

accidents, fire and flood– plays a valuable role in economic activity

22-11 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig DeeganSlides prepared by Craig Deegan

Recognition of insurance premium revenue

• Revenue to be brought to account from the ‘attachment date’ provided it can be measured reliably (AASB 1023)– attachment date is the date from which the insurer accepts

the risk

• Revenue recognised should be tied to the pattern of the incidence of risk

• Most insurers bring revenue to account on a time basis, with an equal amount being attributed to each period– considered appropriate if risks are uniform throughout the life

of the policy

22-12 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig DeeganSlides prepared by Craig Deegan

Recognition of insurance premium revenue (cont.)

• Steps in measuring premium revenue (AASB 1023)a) estimate total amount of expected premium revenue;

b) estimate total expected claims expense and timing of claims;

c) estimate pattern of incidence of risk from b); and

d) recognise premium revenue in a) when it will be earned

22-13 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig DeeganSlides prepared by Craig Deegan

Revenue associated with unclosed business

• Unclosed business– business written close to the balance date in respect of which

the date of attachment of risk precedes the balance date– insurer agrees to accept the risk before the customer has

completed policy contract (i.e. cover note)– estimate of earned portion of premium relating to unclosed

business is necessary for inclusion in premium revenue

22-14 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig DeeganSlides prepared by Craig Deegan

Reinsurance

• Common for insurers to reinsure some or all of their insurance portfolio with another insurer

• Direct insurer– the entity that originally wrote an insurance contract– must show all premiums received, including those redirected– premiums transferred to reinsurer are an expense of the

direct insurer

22-15 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig DeeganSlides prepared by Craig Deegan

Reinsurance (cont.)

• Reinsurer (AASB 1023)– party that has an obligation under a reinsurance contract to

compensate an insured party if an insured event occurs– reinsurance premiums received are treated in the same way

as premiums accepted by direct insurer, i.e. as revenue

22-16 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig DeeganSlides prepared by Craig Deegan

Reimbursement of government charges

• Part of premium relates to government charges (e.g. stamp duty) imposed on the insured party– not treated as revenue by insurer but as revenue held on

behalf of the government (i.e. a liability)

• Charges levied on insurer (e.g. licence fees and workers’ compensation insurance) incorporated in insurance premium– treated as part of premium revenue

22-17 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig DeeganSlides prepared by Craig Deegan

Insurance claims

• Claims settled and paid during the year are treated as expenses of the period

• Expenses and liabilities should include outstanding claims at period end

• Outstanding claims liability measured as (AASB 1023)– central estimate of present value of expected future payments

for claims and additional risk margin– central estimate is mean of distribution

22-18 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig DeeganSlides prepared by Craig Deegan

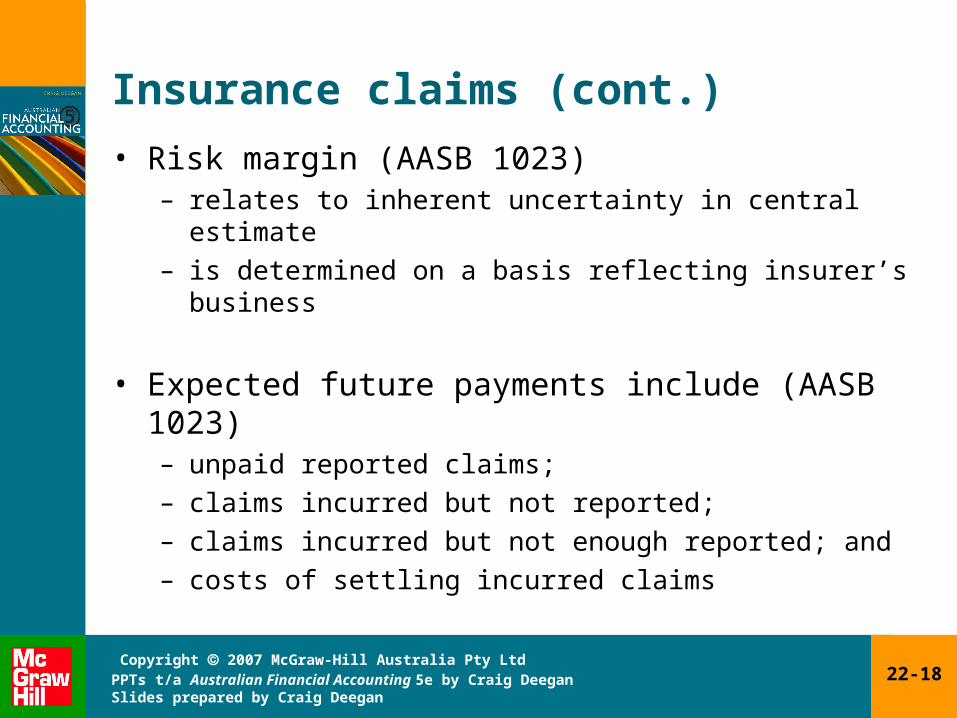

Insurance claims (cont.)

• Risk margin (AASB 1023)– relates to inherent uncertainty in central estimate– is determined on a basis reflecting insurer’s business

• Expected future payments include (AASB 1023)– unpaid reported claims;– claims incurred but not reported;– claims incurred but not enough reported; and– costs of settling incurred claims

22-19 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig DeeganSlides prepared by Craig Deegan

Requirement to discount obligations

• Outstanding claims liability are to be discounted to present value using (AASB 1023)– time value of money using risk-free discount rates based

on current observable, objective rates that relate to the nature, structure and term of future obligation

• Government bond rate might be appropriate

• Increase in present value of claim from one period to the next is included in claims expense (AASB 1023)

22-20 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig DeeganSlides prepared by Craig Deegan

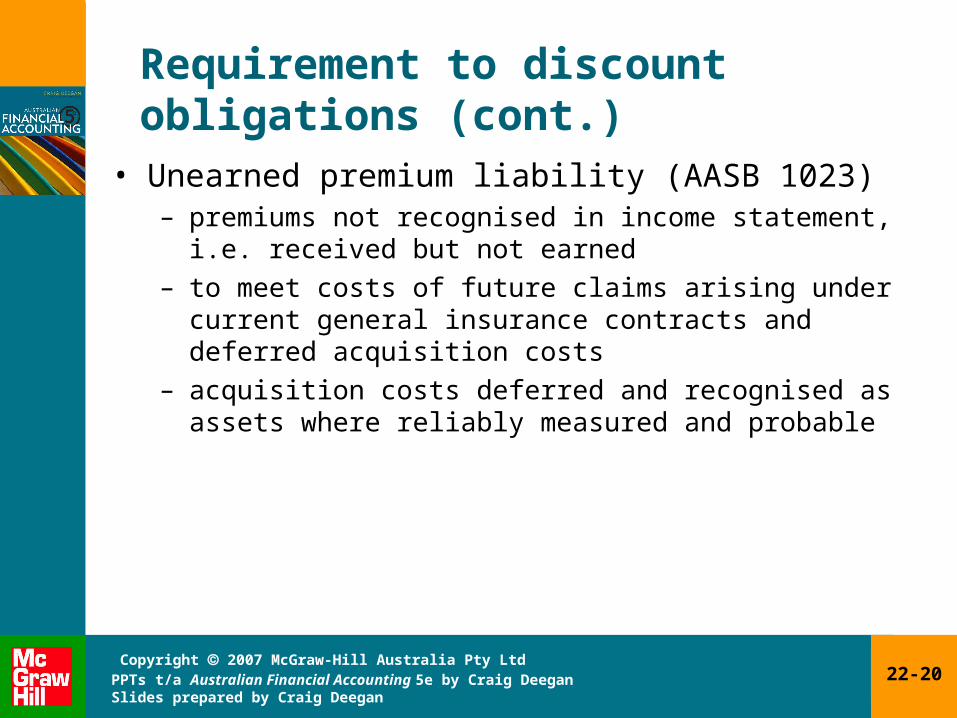

Requirement to discount obligations (cont.)

• Unearned premium liability (AASB 1023)– premiums not recognised in income statement, i.e. received

but not earned– to meet costs of future claims arising under current general

insurance contracts and deferred acquisition costs– acquisition costs deferred and recognised as assets where

reliably measured and probable

22-21 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig DeeganSlides prepared by Craig Deegan

Liability adequacy test

• Assessment of whether carrying amounts of insurance liabilities need to be increased based on a review of future cash flows (AASB 1023)

• Present value of future claims to be compared with unearned premiums

• If present value exceeds unearned premium liability (AASB 1023)– liability is deficient; and

– further liability and expense is to be recognised

22-22 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig DeeganSlides prepared by Craig Deegan

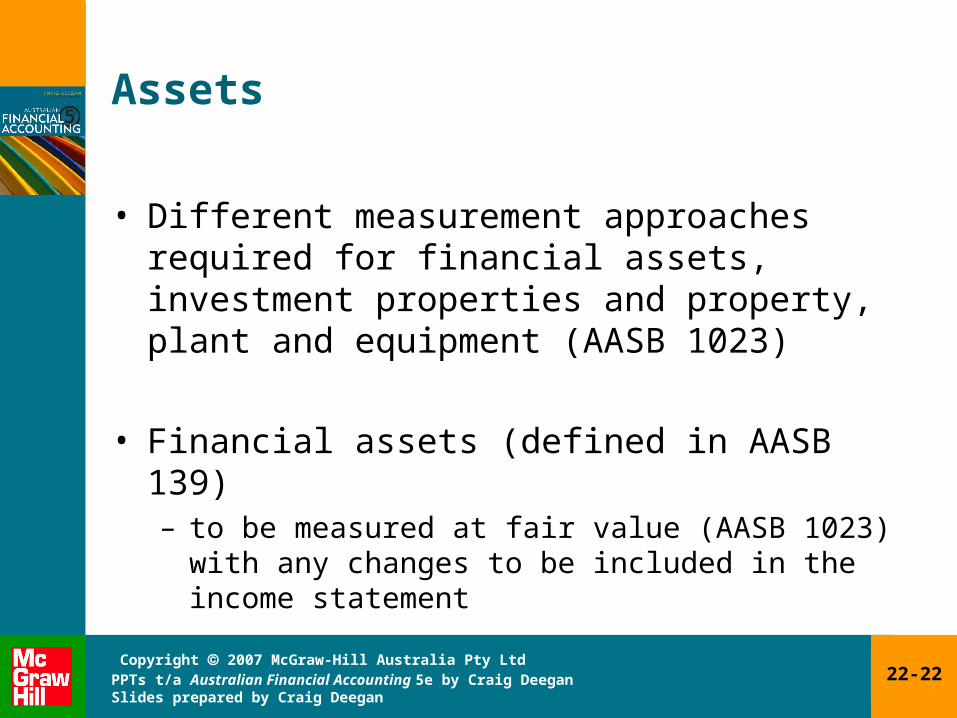

Assets

• Different measurement approaches required for financial assets, investment properties and property, plant and equipment (AASB 1023)

• Financial assets (defined in AASB 139)– to be measured at fair value (AASB 1023) with any

changes to be included in the income statement

22-23 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig DeeganSlides prepared by Craig Deegan

Assets (cont.)

• Investment properties (AASB 140 and AASB 1023)– property held to earn rentals or for capital appreciation

to be measured using fair value model under AASB 140

– any gain or loss recognised in profit or loss

• Property, plant and equipment (AASB 1023)– to be measured using revaluation model under AASB

116

– increases in value to a revaluation reserve unless a reversal

22-24 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig DeeganSlides prepared by Craig Deegan

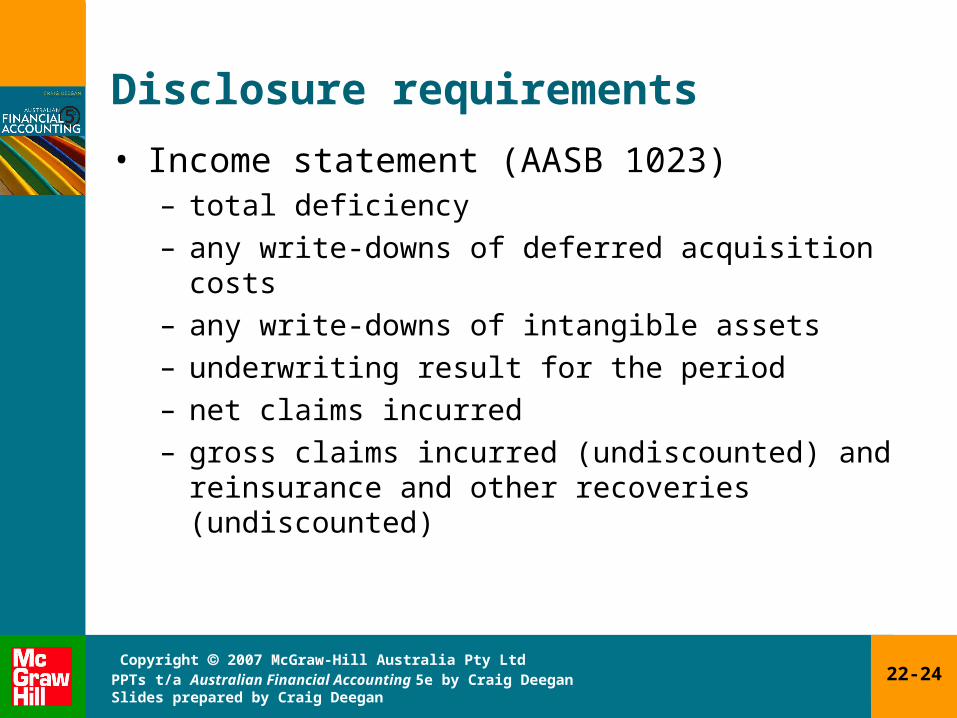

Disclosure requirements

• Income statement (AASB 1023)– total deficiency

– any write-downs of deferred acquisition costs

– any write-downs of intangible assets

– underwriting result for the period

– net claims incurred

– gross claims incurred (undiscounted) and reinsurance and other recoveries (undiscounted)

22-25 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig DeeganSlides prepared by Craig Deegan

Disclosure requirements (cont.)

• Balance sheet (AASB 1023)– for outstanding claims liability, central estimate and risk

margin

– percentage risk margin adopted

– probability of adequacy

– process used to determine risk margin

22-26 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig DeeganSlides prepared by Craig Deegan

Consistency with other standards

• AASB 1023 requires certain measurement approaches for ‘assets backing general insurance liabilities’

• For assets not ‘backing general insurance liabilities’, alternative approaches could be used

• Would different valuation bases confuse account users?

22-27 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig DeeganSlides prepared by Craig Deegan

Opposition to AASB 1023

• Major opposition to original AASB 1023– requirement to include unrecognised gains and losses

on investments in the profit and loss

– claimed to introduce a degree of volatility to the accounts

• Also argued that results driven by marked-to-market investments would distort general insurers’ performance

• Some volatility will remain under current version of AASB 1023

22-28 Copyright 2007 McGraw-Hill Australia Pty Ltd PPTs t/a Australian Financial Accounting 5e by Craig DeeganSlides prepared by Craig Deegan

Summary

• The chapter addresses accounting issues relating to general insurance contracts

• Main issues are– how and when revenue should be recognised– how and when insurance claims should be recognised– how assets should be valued

• Revenues to be recognised on the basis of pattern of incidence of risk

• Insurance claims settled and paid to be treated as expenses

• Unpaid insurance claims recognised as liabilities to be discounted to present values