2021 - ascri.org

74

2 Private Equity and Venture Capital: Part of the solution SURVEY Venture Capital & Private Equity activity in Spain 2021

Transcript of 2021 - ascri.org

2

2021 SURVEYVenture Capital & Private Equity activity in Spain

Private Equityand Venture Capital:Part of the solution

Venture Capital & Private Equity activity in SpainVenture Capital & Private Equity activity in Spain

SURVEYVenture Capital & Private Equity activityin Spain

2021

WITHTHE SPONSORSHIPOF:

Príncipe de Vergara,55, 4º D • 28006 MadridTel. (34) 91 411 96 17 • www.ascri.org

twitter.com/ascri_infoyoutube.com/channel/UC9kShvR6TYH6IDcvZlqO_CA

linkedin.com/company/ascri

C

M

Y

CM

MY

CY

CMY

K

CUBIERTA-INFORME-2021.pdf 2 15/4/21 9:51

Sponsor by:

Venture Capital & Private Equity in Spain

Survey 2021

2

THIS REPORT HAS BEEN PREPARED BY Ángela Alférez (ASCRI Research Director).

Data obtained with collected in collaboration José Martí Pellón (Professor of Financial Economics at the Complutense University of Madrid) and Marcos Salas de la Hera (Partner of webcapitalriesgo).

All Rights Reserved ASCRI ® 2021The total or partial reproduction of the document, or its computer treatment, is not allowed transmission in any way or by any means, whether electronic, by photocopy, by registration or other methods, without prior and writ-ten permission of the copyright holder.

Methodological NoteASCRI has been preparing statistics on the Venture Capital & Private Equity sector in collaboration with webcapitalriesgo since 1987. The statistics published by the Association are intended to capture all of the activities of both domestic and international Venture Capital and Private Equity GPs (investment -through equity or quasi-equity-, fundraising and divestment) in Spanish companies with the aim of providing reliable data to the market, media, and government agencies and institutions. The information is collected on a confidential basis directly from the management companies themselves, whether ASCRI members or not. All information is collected through EDC (European Data Collective), the technological platform implemented by the main European Venture Capital and Private Equity Associations. This platform ensures a consistent methodology to guarantee the data on European Venture Capital and Private Equity is as complete and uniform as possible.Currently, ASCRI/webcapitalriesgo directly monitors more than 250 domestic and international management companies through the European EDC Platform.

3

ASCRI is the association that brings together Venture Capital

& Private Equity firms in Spain, as well as their investors,

including insurance companies and pension funds. The

members of ASCRI make mid- to long-term investments

in unlisted companies, from start ups to consolidated

companies, providing not only stable financing through

equity, but also innovation and management support.

The Association's mission is to connect the players in the

industry in Spain, representing their interests before the

Government, media and public opinion, both nationally

and internationally, through alliances and synergies

in Europe and Latin America. Its objectives include

establishing an appropriate regulatory framework for

the sector and communicating the positive impact of its

activities on the industrial fabric and job creation. As a

participant in the UN Global Compact, one of ASCRI's main

objectives is to promote the sustainability of its members

and their investee companies. ASCRI also aims to promote

professional development through training programs and

to actively raise awareness through the publication of

statistical reports and economic and social impact studies,

which show the added value contributed by this sector.

4

IndexSurvey 2021

5

Index

Introduction 7

Differencial values Private Equity & Venture Capital 8

Summary of 2020 11

Fundraising 16

Investment in Private Equity & Venture Capital 20

Middle Market Investments 25

Large Market. The International GP in Spain 28

Venture Capital 31

Divestment 36

Portfolio 38

2020 Main Transactions 40

Statistical appendix 46

The race for sustainability: Challenges and opportunities for the sector

62

General Partners included in this survery 66

6

7

"Spain remains an attractive market"

“W e are leaving behind 2020, a very complicated year that affected thousands of companies from a wide range of

sectors. The portfolio companies of our sector have been better able to weather the crisis and the Venture Capital & Private Equity industry has proven to be a source of resistance and competitiveness for their portfolios."

“2020 has been a difficult year, but we will not let it stop us from advocating for the key role that Venture Capital & Private Equity should play in the recovery of businesses. Venture Capital and Private Equity have tried to keep the workforces of their investee companies, offering them the liquidity and instruments needed to weather the recession.

The data published in this report supports the efforts made by GPs: in 2020, Venture Capital and Private Equity firms invested €6,275M, a significant figure considering the lack of megadeals and large transactions, in a record high number of transactions (838). Of these transactions, 672 were early stage investments by Venture Capital funds. This was one of the leading segments last year next to international investors, accounting for 80% of total volume invested. This weight represented by international investors shows the continued attractiveness of the Spanish market and trust in Spanish industry.”

“Private management companies raised €2,134.6M, in line with the 2018 record high, with the majority raised by domestic private management companies: Limited Partners (LPs) maintain their commitment and trust in the management of local firms. In this regard, ASCRI continues to promote the potential of Venture Capital and Private Equity for insurance companies and pension funds in Spain, one of the largest demands in the sector identified in the “Measures for Transformation of SMEs and Startups” report.”

“To date, the sector holds €38,000M under management, an amount that ensures operations will continue and that there is abundant capital available to continue carrying out transactions and strengthening our business fabric, both for startups and more mature SMEs.”

“ASCRI continues to support Spanish companies, responding to their financing needs, supporting them in their management and contributing to job creation. We are greatly appreciative for Diana Capital's continued support in preparing this report, which we hope will be of interest to you."

Aquilino PeñaChairman ASCRI /Founding Partner Kibo Ventures

José ZudaireASCRI Managing Director

8

Venture Capital & Private Equity Differentiating ValuesThrough its Venture Capital and Private Equity Economic and Social Impact study on Middle Market Investments in Spain, published in 2018, ASCRI studied the impact of

Venture Capital and Private Equity in 186 companies and confirmed the following conclusions:

Venture Capital and Private Equity is one of the basic pillars of financing for small and medium-sized companies, acting as an essential complement to bank financing.

Capital injections are complemented by strong business development support. Venture Capital and Private Equity firms are not limited merely to financing, but also offer the experience of their teams to: (1) offer strategic advising, (2) establish credibility with third parties, (3) help increase the professionalism of management teams, (4) provide an external business focus, and (5) convey best practices from other sectors.

Venture Capital & Private Equity has proven a key tool for driving the growth of companies and making companies more competitive. Venture Capital & Private Equity contributes to this growth in two ways: (1) driving growth in sales, turnover and EBITDA; and (2) in build-up transactions, ensuring continued growth in size through the acquisition of other companies, reducing sector fragmentation.

Companies backed by Venture Capital & Private Equity create more jobs, and this job creation persists over time. Looking at a broader time horizon, through 2015, the 186 companies that received Venture Capital & Private Equity investments increased their workforce by 27,485 workers, representing an aggregate increase of 30%, compared to the 2,000 jobs lost in the control group (-2.8% aggregate).

1. Alternate Financing

2. Added Value

3. Business Consolidation

4. Job Creation

9

Venture Capital & Private Equity Differentiating ValuesThe capital injection and business management support provided by the Venture Capital & Private Equity strengthened growth of the portfolio companies. In individual terms, each portfolio company increased sales by 17.1 million within three years from the investment, compared to 1.5 million for the control group companies. If the analysis is extended through 2015, this difference between investee and control group companies increases to 12.2 million euros per company.

Venture Capital & Private Equity funding of companies improves their ability to turn a profit. The 186 Venture Capital & Private Equity portfolio companies increase their EBITDA by the third year of the investment, by €294 million, at an average rate of 7% per annum. On the other hand, the control group experienced losses of €200 million (-6.4% YoY average).

Venture Capital & Private Equity funding multiplies the investment in its portfolio companies, driving production increases. In aggregate terms, total assets of companies receiving Venture Capital & Private Equity funding increased by €4,460 million in the third year after receiving the investment, representing annual growth of 7%, more than 4 percentage points above the control group (2.8% per annum).

Venture Capital & Private Equity supports management which contributes to increased value, mitigating the effects of recessions through the investment and searching for new markets in which to grow. A total 61 companies received Venture Capital & Private Equity funding in the middle market following the start of the crisis in 2009. Turnover of companies backed by Venture Capital & Private Equity grew by €23.7M at the end of three years, compared to €3.3M per control group company, representing 7 times more growth on average.

Venture Capital & Private Equity investment in the middle market is primarily centered on the other services sector (80 companies) and industry (53 companies). The remainder of the investments were distributed between the commerce (24 companies), commodities and supply (15 companies) and ICT (14 companies) sectors.

5. Acceleration of Business Growth

6. Improved Corporate Profits

7. Promoting Investment

8. Support for Distressed Companies

9. Impact in Various Sectors

10

ASCRI GlobalAt ASCRI we have a clear commitment to promote the inter-national area.

To do this, we continue to develop initiatives such as:

- The MoU or collaboration agreement with the counter-part associations of other countries, ABVCAP, ACVC, AIFI, Amexcap, APCRI, Arcap, ColCapital, France Invest, IATI, IDB / LAB, LAVCA, LPEA and PECAP with whom we are in continuous communication.

- LinkedIn site created specifically for the members of the MoU and that allows exchanging ideas, information, formu-lating queries and supporting business development bet-ween the member countries.

- Participation in international events, such as congresses or events, in which ASCRI has an active presence with the aim of developing the Spanish Venture Capital and Private Equi-ty sector, such as IPEM in Cannes, the Pacific Alliance, EVPA Annual Conference, Invest Europe Venture Capital Forum, Invest Europe investor's Forum or the annual congresses of the associations that are part of the MoU.

The MoU continues to expand its members: 2020 we've wel-comed Portugal (APCRI, Portuguese PRivate Equity Asocia-tion).

On 354 you will find expanded information on each of the MoU member Associations.

11

Summary of 2020

12

Summary of 2020

Second best figure on record for investment in Spain by Venture Capital & Private Equity GPs Despite the change in scenario caused by the global health crisis, a total of €6,257M was invested in Spanish companies.

Record high number of investments1 made in SpainWith 838 investments closed.

Spanish SMEs were the main recipient of Venture Capital and Private Equity investmentInvestments were made in 578 companies, 90% of which were SMEs.

International GPs continued their commitment to Spanish companiesInternational GPs contributed 75% of investment volume for the year. Record high number of investments in Spain (192).

Middle Market reached record highs in terms of volume and number of investmentsWith €2,581M across 92 investments. The role of international GPs stood out thanks to their intense activity in this segment and their role in driving this segment to record highs.

Venture Capital investment reached a record high for the second consecutive yearAll-time high in volume invested with a total investment of €833M in 433 Spanish start ups.

Domestic investors (LPs) were the main source of new capital for Spanish funds in both Venture Capital and Private EquitySpanish family offices stood out in their support of Venture Capital and Private Equity as an asset class.

Dry powder has maintained similar levels to those seen in recent yearsApproximately €4,081 million in equity available for investment, a long way from the 2008 record high (€6,000 million).

Record high in volume of funds managedA total of €38,053M, with international GPs representing 64%.

1 The number of investments as published in this report is calculated from the investor perspective, meaning that some investee companies may be double counted in the case of syndicated investments by Venture Capital and Private Equity firms. This explains why the number of investments does not match the number of investee companies.

13

Investment in 2020

Fundraising in 2020

-26.4% vs, 2019

+10.3%vs, 2019

-33%vs, 2019

€6,275.2M Equity investment

838 investmentsin 578 companies (90% SMEs)

€7.5MAverage investment round size

+ 11% vs, 2019

+ 18%vs, 2019

+1.5%vs, 2019

€2,134.6M Spanish Private Equity &

Venture Capital Funds

1,324.8Spanish Private Equity funds

€809.7MSpanish Venture Capital funds

Record high in fundraising of Venture Capital GPs for the second consecutive year

Investment and Fundraising vs. GDP

2018 2019 20202016 20172014 20150

3,000

1,000

2,000€2,135M€2,142M

Third best figure on record for investment Record high number of investments closed

Investment Number of investments

Investment in Spain / GDP (%) Domestic Funds Raised / GDP (%)Fundraising

2018 2019 20202016 20172014 20150

900

439

838

600

300

2019 20202017 201820152014 20160

8,000

6,000

10,000

€2.745M

€6.275M

4,000

2,000

2018 2019 20202017201620152014

0.21%0.18%0.20%0.17%0.21%

0.16%0.25%

0.26% 0.22%0.32%

0.43%0.50%

0.69%0.56%

14

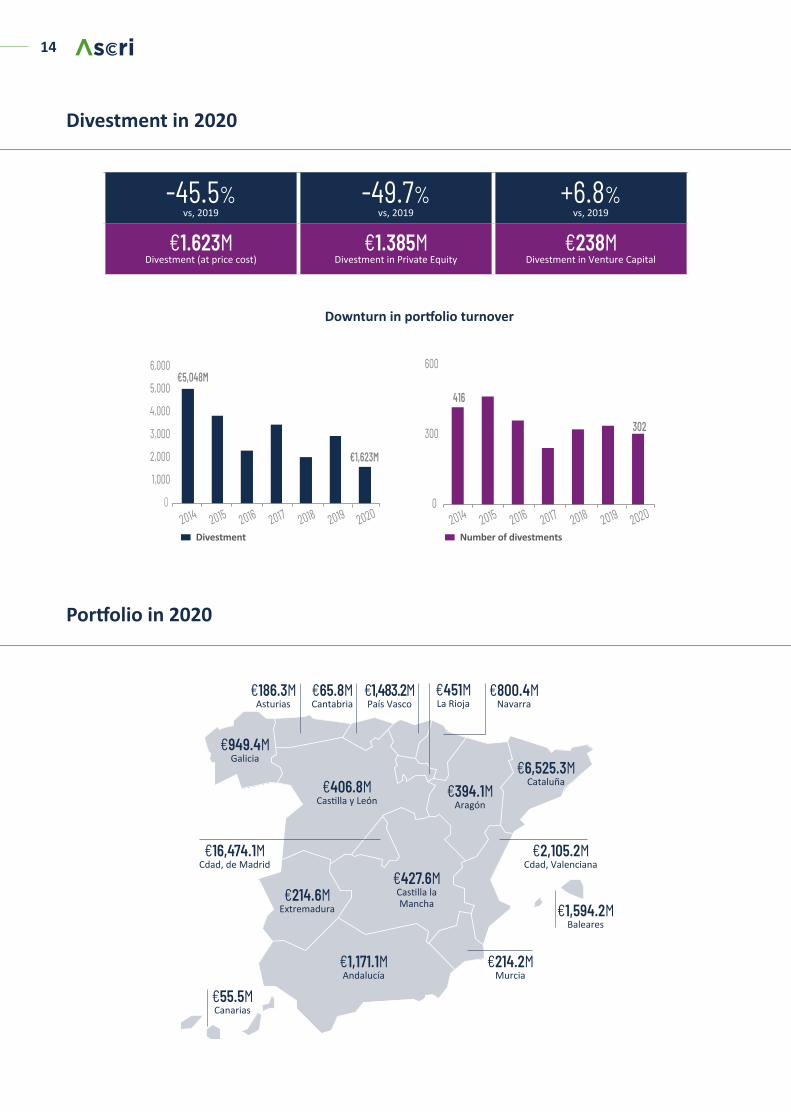

Divestment in 2020

Portfolio in 2020

-45.5% vs, 2019

-49.7%vs, 2019

+6.8%vs, 2019

€1.623M Divestment (at price cost)

€1.385MDivestment in Private Equity

€238MDivestment in Venture Capital

€1,171.1MAndalucía

€394.1MAragón

€6,525.3MCataluña

€16,474.1MCdad, de Madrid

€2,105.2MCdad, Valenciana

€214.6MExtremadura

€949.4MGalicia

€451MLa Rioja

€800.4MNavarra

€1,483.2MPaís Vasco

€214.2MMurcia

€65.8MCantabria

€427.6MCastilla la Mancha

€406.8MCastilla y León

€186.3MAsturias

€1,594.2MBaleares

€55.5MCanarias

Downturn in portfolio turnover

2018 2019 20202016 20172014 20150

600

300 302

416

2019 20202017 201820152014 20160

6,000

5,000

€1,623M

€5,048M

4,000

3,000

2,000

1,000

Divestment Number of divestments

15

Private Equity and Venture Capital industry in Spain

Employment

448,800 employees in the portfolio companies of Venture Capital and Private Equity GPs, all headquartered in Spain.

Footprint

2,796 investee companies of Venture Capital and Private Equity GPs, distributed across the various regions of Spain.

Momentum

90% of investee companies are small or medium-sized companies (SMEs).

TechnologyIT, Communications and Life Sciences led Venture Capital and Private Equity investments in 2020.

Scale

€29,583Min equity investments in 2,874 Spanish companies over the last five years.

Dimension

€38,053M funds under management (24,241 of international GPs).

Innovation

Barcelona and Madridtwo entrepreneurial and innovative hubs known worldwide.

Double-digit returns

18%average rate of return in Spanish funds divested by Venture Capital and Private Equity2.

Activity

464 Venture Capital and Private Equity GPs have a portfolio in Spain, 292 of which are international GPs.

2 This figure refers to the public fund of funds, Fond ICO Global, as obtained from the “Venture Capital and Private Equity's Potential for Insurers and Pension Funds in Spain” study. Published by ASCRI and BCG. January 2021.

16

Fundraising1 remained strong despite the new environment. With the outbreak of the health crisis in Europe during the second quarter of

the year and the subsequent closing of borders, there were several months of substantial uncertainty that affected many activities, including fundraising worldwide. However, the reopening and reactivation of certain economic sectors in the second half of the year, combined with the continued presence of those market conditions that have shaped this variable in recent years –as discussed in past reports, these conditions include abundant liquidity, attractiveness of Venture Capital and Private Equity as an asset for investors2 (LPs) and the support from the public sector through various programs, of which the FOND – ICO Global fund of funds, managed by Axis/ICO, and the European Investment Fund (EIF) stand out– drove growth in this variable in 2020.

New funds raised by private Private Equity and Venture Capital firms in Spain in 2020 exceeded €2,134.6M, rep-resenting an 11% increase from 2019 (€1,920M). Including new funds for public entities (€170.9M), new funds raised for the sector totaled €2,305.5.M (+5.2% from 2019).

Approximately 60 Venture Capital & Private Equity firms (“VC&PEs”) headed the raising or extension of funds by private domestic firms. A majority of new funds raised focused again on the middle market investment segment. In terms of the number of firms that increased funds, those aimed at funding start ups stood out (45 in total). As is the case globally, although at a different scale, a significant

part of funds raised are being concentrated in a small number of funds (approximately 56% of new funds raised were invested in seven funds, all of them above €80M). Fundraising by experienced market operators continues to lead. The following Private Equity vehicles, inter alia, stood out3: GPF Capital III (final closing of €300M) of GPF Capital, MCH Iberian Capital Fund V (first closing of €250M) of MCH Private Equity Investment, Oquendo IV (first closing) of Oquendo Capital, PHI Fund III (final closing of €80M) of PHI Industrial, Suma Capital Growth Fund II (final closing of €125M) of Suma Capital, as well as the first fund of Queka Real Partners, among others. Several funds were launched and closed to finance start ups, including, Nauta Tech Invest V (first closing) of Nauta, Seaya Ventures III (first closing of €84M) of Seaya Ventures, Samaipata II Capital (first closing, with a fund target of €100M) of Samaipata, JME Ventures III (final closing of €60M) of JME Ventures, K Fund II (first closing, with a fund target of €70M) of K Fund, Kibo Ventures Fund III (first closing, with a fund target of €100M) of Kibo Ventures, TBF I (€30M) of Think Bigger Capital, Ysios Biofund III (first closing of €155M, with a fund target of €200M) of Ysios Capital, 4Founders Capital II (first closing, with a fund target of €40M) of 4Founders Capital and Inveready Venture Finance (€50M) of Inveready, as well as numerous undisclosed capital extensions in Venture Capital & Private Equity vehicles. Regarding impact investing, several firms of this category have announced their first closings of investment vehicles: Q Impact, Bolsa Social Impacto, Global Social Impact and Ship2B (Ship2B

1 The fundraising variable analyzed in this chapter includes all new funds raised by Spanish Private Equity and Venture Capital firms during the fiscal year analyzed in the report (2019). The target of these funds raised is direct investment in unlisted companies. Infrastructure funds, real estate funds, funds of funds, secondary funds of funds, corporate bond funds and accelerator, incubator and business angel funds are not included in these statistics.

2 This chapter includes the following types of investors: Pension funds, financial institutions, family offices, public sector, funds of funds, insurers or corporate investors.3 Only those funds that have been disclosed are referred to herein..

New funds raised by type of entity (GP)

Source: ASCRI / webcapitalriesgo

Domestic private entity Domestic public entity

3,000

2,000

1,000

0

€ Mi

llion

s

2009 201220112010 201520142013 2018 2019 202020172016

Fundraising

17

Ventures), as well as an extension of the Creas fund, totaling an aggregate of funds for impact investment of €88M.

In 2020, funds raised by private domestic Private Equity GPs totaled €1,324.8M (€1,122.5M in 2019), whereas Venture Capital GPs totaled €809.7M (€797.7M in 2019), a record high for the second consecutive year for the GPs operating in this segment.

An estimated €4,080.8M in dry powder is currently available for investment by private domestic GPs (+4.6% from 2019), thanks to the intense fundraising activity in 2020, albeit still far from the record-high of 2008 (€6,000M). The capacity of the Spanish market to absorb available funds (the annual investment in recent years in Spanish companies has been between €6,000M and €8,000M), together with the need for channeling equity into SMEs during this new stage of the economic cycle, highlights the continued need for fundraising in the Spanish market.

At the global level,4 the recession caused by the health crisis did not have a particularly negative impact on fundraising. In 2020, this variable totaled €600,000M,5 representing a 14% decrease from 2019 (third best figure on record following 2017 and 2018). Investors (LPs) directed their interest in particular towards consolidated GPs with a focus on Europe, as is the case of CVC Capital Partners, who raised the largest fund for Europe (€21,300M) and the second largest in the industry (behind Blackstone, with €21,993M). Looking ahead to 2021, 89% of investors (LPs) planned to maintain or increase their allocations to Private Equity and Venture Capital, largely due to the strong returns they have received from this asset within a macro framework of expansionary policies with low interest rates, which penalizes fixed income assets, as well as high market volatility. Funds available for investment by Venture Capital & Private Equity GPs globally have been growing since 2012, reaching a record high of circa €2 trillion in 2020.

4 Data from “2021 Prequin Global Private Equity & Venture Capital Report”.5 The fundraising figure reported by Prequin includes other alternative investments as well as Private Equity and Venture Capital funds, unlike the methodology applied by ASCRI and other

European Associations, which solely follow the activity of Private Equity and Venture Capital funds.6 According to the National Institute of Statistics, Spain's gross domestic product in 2020 fell by 11% from 2019.

Investment decreased with respect to GDP. Given the decrease in investment in 2020, and despite the decline in Spanish GDP, funds invested as a percentage of GDP6 was 0.56%, a decrease of 12 p.p. compared to 2019, a record high year in terms of investment. Nevertheless, for the third consecutive year this indicator was above the European average (0.52%, according to Invest Europe), albeit still far from such countries as Norway (0.95% of investment as a percentage of GDP) and the United Kingdom (0.90%) who led the European ranking with respect to this variable in 2020. Venture Capital and Private Equity fundraising in relation to GDP grew 3 p.p., which placed this variable at 0.21% in 2020.

Fundraising and investments as a percentage of GDP

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

0.63%

0.84%

0.42%

0.21%

0.00%

Investment in Spain / GDP (%) National funds collected / GDP (%)Source: INE, ASCRI / webcapitalriesgo

18

Fundraising

For the second consecutive year, domestic investors (LPs) were the main source of new resources for the

Spanish Venture Capital & Private Equity sector. In terms of the contribution of new funds to

private domestic Venture Capital and Private Equity vehicles in 2020, by geographic origin Spanish investors stood out, contributing 70% of total funds raised (€2,134.6M). In absolute terms, the volume invested by domestic LPs grew by 24% compared to 2019, whereas international investors

Family of!ces become the primary investor (LP) in total funds raised by domestic private entities. As regards

capital raised by Spanish private VC&PEs, by type of investor (LP), family offices led new capital contributions, accounting for 43.2% of the €2,134.5M raised in 2020. Specifically, Spanish family offices committed €840.8M compared to €80.7M by international family offices, reflecting the renewed interest in this asset (in the last four years, Spanish family offices have contributed around 22% of new funds raised), making them the leading LP in funds raised by Spanish GPs. This is followed by the public sector,7 including FOND-ICO Global8 (investment vehicle for VC&PE funds managed by Axis Participaciones Empresariales/ICO) and the European Investment Fund (EIF),9 representing 17.8% (€380.4M) of funds contributed. Funds of Funds committed €214.9M. Corporations or non-financial companies were the fourth largest provider of funds, representing 7.4%. Domestic companies also stood out in this category, making a capital injection

of €135.2M to new funds raised, compared to €22.2M contributed by international corporations. Mimicking other asset managers (6.4% of total), pension funds were the sixth largest contributor, accounting for 4.5% of total new funds raised. For the first time, domestic pension funds recorded high participation rates in this asset class, contributing €75.5M10 of the €96.5M provided by this type of investor in 2020. Nonetheless, the contribution of domestic pension funds in Spanish VC&PE vehicles is still far from their international peers, with average annual contributions between 15% and 30%11 of total funds raised at the European level. Insurance companies committed just 2.5% of the total, with domestic insurance companies making the largest contribution totaling €52.8M of the total €53.4M contributed by this type of investor in 2020.

Government agencies were the main contributor (33.9%) of new funds raised for Venture Capital vehicles in 2020 (€809.7M), followed by family offices (31%).

60%

50%

30%

40%

20%

10%

0%

6%2%2% 4%6%6%

1.9% 0%6%

2%3%8%

34%

13%15%

1%

31%

2%

50%

Fami

ly offi

ce

Sove

reign

wea

lth fu

nds

Othe

r ass

etma

nage

rs

Gove

rnmen

tag

encie

s

Fund

of fu

nds

Corpo

rate

inves

tors

Insura

nce

Comp

anies

Pens

ion fu

nds

Finan

cial

Instit

ution

s

Source: ASCRI / webcapitalriesgo

Private Equity Funds Venture Capital Funds

New funds raised by Spanish private VC&PEs in 2020, by type of investor (LP)

7 This category includes public funding aimed at funds raised by domestic private entities.8 In 2020, Fond-ICO Global contributed €119M to VC&PE vehicles. Fond-ICO Global has approved commitments of €2,266M across 108 funds since its launch, through thirteen calls.9 Following the methodology of the other European Associations, the EIF contributions were included as public sector.10 This figure can be explained by the high contributions of two pension funds in two middle market vehicles.11 El peso de los fondos de pensiones en el total de recursos captados en 2019 por vehículos de Capital Privado europeos fue del 29%, posicionándose como el principal proveedor de

recursos. Fuente: "European Private Equity Activity 2019", publicado por Invest Europe en mayo 2020.

19

Spanish SMEs grew and consolidated its position as the main recipient of capital raised by Spanish private

entities.12 Specifically, in 2020, buyouts accounted for 42.3% of intended application of new funds raised, compared to 26.2% in 2019. Investments directed towards financing startups (seed, start up and late stage ventures) accounted for the second highest application of new funds (35.6%). This is due to the continued closings of domestic Venture Capital funds, nearly all of which are on their second and third generation. However, an ongoing challenge for the Spanish market is the fact that Spanish Venture Capital GPs are raising larger funds that provide them with the capacity to finance the last stages of Spanish start ups (late stage ventures), rounds that are currently

being led by international Venture Capital GPs, as their funds are generally much larger.

Source: ASCRI / webcapitalriesgo

2020 2019

Early Stages(Venture Capital)

Growth Capital

Leveraged Buyouts

Other

0% 20% 10% 30% 40% 50% 60%

73.32.0

75.521 52.8

0.7 17.8

197.1135.2

22.2

840.8

80.7

209.1 171.3

21.0- 35.899.9 70.7

7.7

400

600500

700800900

300200

0100

€ Mi

llion

s

Fami

ly offi

ceag

encie

s

Othe

r ass

et ma

nage

rs

Othe

r

Sove

reign

wealt

h fun

ds

Fami

ly offi

ce

Corpo

rate

inves

tors

Fund

of fu

nds

Insura

nce

comp

anies

Finan

cial

Instit

ution

s

Pens

ion fu

nds

Source: ASCRI / webcapitalriesgo

Domestic LPs International LPs

New funds raised by Spanish private VC&PEs entities according to geographic breakdown of investor (LP) in 2020

12 This data is developed based on the answers provided by respondent firms to the question “Intended application of new funds raised,” and some of said firms are managing broad market funds.

Intended application of new funds raised by Spanish private VC&PEs entities in 2020

provide €623.6M, a decrease of 27% from the prior year in terms of their commitments in domestic Venture Capital & Private Equity GPs. The mobility restrictions in place during the first months of 2020 largely explain this decrease in the participation of international investors. A majority of the funds from international investors came from Europe, totaling 23% (mainly from Luxembourg, France, Italy and

Germany), followed by the United States with 5%. Broken down by asset type, Spanish investors were the main source of new funds raised by Venture Capital vehicles, contributing €620M of the €809.7M recorded. In terms of Private Equity vehicles, domestic investors also stood out, providing 67% of total funds raised by these strategies (€1,324.8M).

20

Second best figure on record for Venture Capital and Private Equity investment in Spanish companies in 2020. Despite a difficult

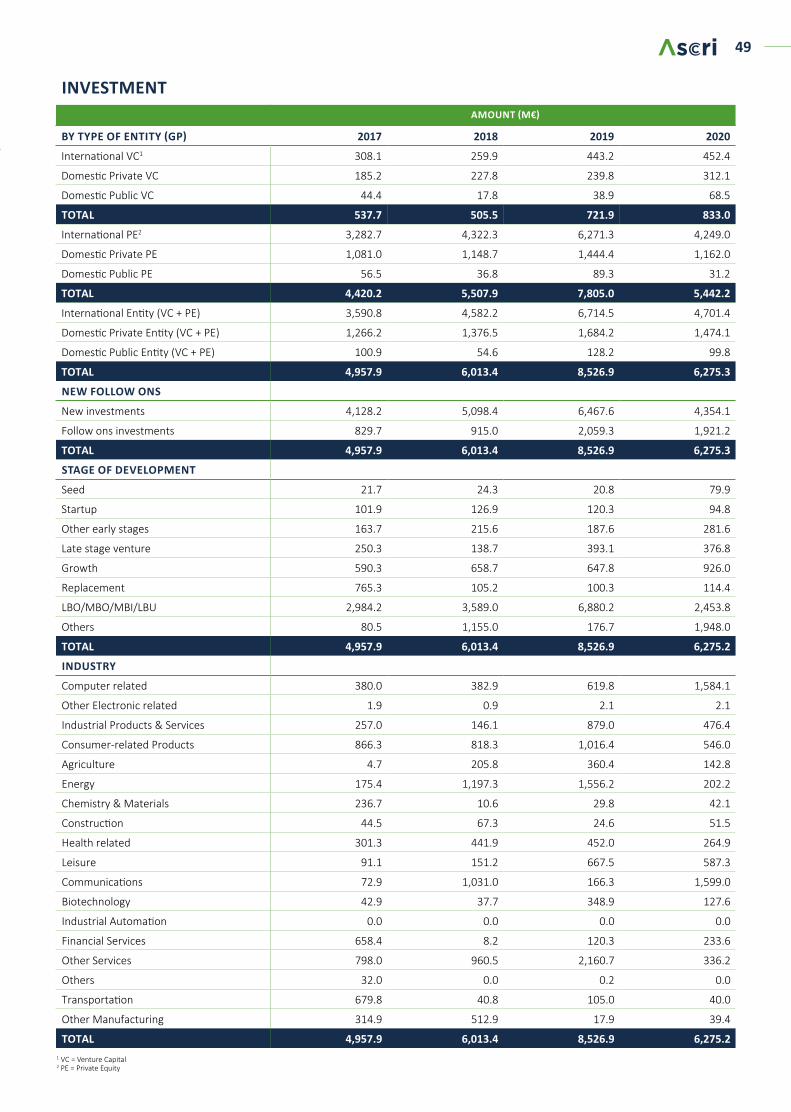

economic environment due to the outbreak of the health crisis, Venture Capital and Private Equity investments1 in Spain in 2020 totaled €6,275.2M,2 the third best figure on record. Nevertheless, this investment volume represents a 26.4% decrease from 2019 (€8,526.9M), a record year for Venture Capital and Private Equity investment in Spain. 69% of total volume was allocated to new investments, the same as in 2019. The remaining 31% (€1,921.2M) was allocated to follow ons.

A comparison between the two main segments of this sector shows that Private Equity investment totaled €5,442.2MM (-30.3% from 2019) across 166 investments. Venture Capital investment totaled €833M (+6.3% from 2019) across 672 investments.

The bunching effect of Venture Capital and Private Equity on many of its transactions, given that the equity provided by Venture Capital and Private Equity firms3 is accompanied by the financing of other investors, is referred to as the (total) transaction value.4 In 2020, this figure totaled €12,857.6M (-13.6% from 2019), of which €11,582.8M were Private Equity investments (€5,442.2M in equity + €6,140.6M co-investment and debt) and €1,274.9M were Venture Capital investments (€833M in equity + €441.9M co-investment).

The decreased investment volume in 2020 can be explained by the fewer number of transactions in the large market5 (equity investments over €100M per transaction), a segment headed by international funds. In contrast, the record highs recorded in the middle market6 (equity investments between €10M–€100M) and Venture Capital7 segments drove the good investment activity in 2020, with intense activity by international funds in both segments.

The cycle change caused by the global pandemic had a disparate impact on the Venture Capital and Private Equity sector throughout 2020. In the first half of the year investment volume totaled €1,561.5M (-64% from the first half of 2019), as the focus of activity at that time was specifically on managing portfolio companies with a view to mitigating the consequences of the global economic slowdown. In the second half of the year, in an environment with fewer mobility restrictions compared to the first half, a majority of the year’s investment activity took place, totaling €4,713.7M (+13.7% YoY), thanks in large part to the sustained prevalence in 2020 of certain market conditions, such as investor appetite (with significant available funds for investment), numerous investment opportunities in Spanish companies presenting an attractive offer and access to credit (particularly private), in addition to the decreased uncertainty and lack of visibility in terms of company valuation, which were defenitive factors in the first months of the year

Investment by type of entity (GP)

Investment

1 This chapter analyzes investment in terms of equity contributions by domestic (public and private) and international Venture Capital and Private Equity general (GPs) in Spanish companies. Therefore, investments made by Spanish firms outside of Spain, which totaled €266M across 128 investments in 2020, are not included. Likewise, investments made by infrastructure funds, real estate funds, funds of funds, corporate bond funds and accelerator, incubator and business angel funds are not included.

2 All figures in this report are provided in millions of euros (“€M”).3 The terms fund, manager (GP - General Partner) and Venture Capital and Private Equity Firm (VC&PE) are used indistinctly in this report to refer to Venture Capital and Private Equity

operators.4 Equity invested by Venture Capital and Private Equity GPs plus investments made by co-investors (institutional investors, Limited Partners (LPs), management teams, corporations,

shareholders, etc.) and, in the case of leveraged transactions, debt provided by the banks and/or alternative debt.5 For further information, please refer to the section: “Large Market. The International GP in Spain” of this report. 6 For further information, please refer to the section: “Middle Market” of this report.7 For further information, please refer to the section: “Venture Capital” of this report.

Source: ASCRI / webcapitalriesgo

International GP Domestic private GP Domestic public GP

Number of investments

€ M

illio

ns

2018 2019 2020201720162015201420132012201120102009

4,0005,0006,0007,0008,0009,000

3,0002,0001,000

0

21

Leveraged transactions9 represented 40% of total annual investment thanks to large and middle market activity. Venture Capital

reached a record high by investment volume, for the second consecutive year, and also reached a record high by number of investments. Investment by stage of the investee company, by volume, followed a similar pattern to that seen in recent years in which leveraged transactions stand out over other categories, totaling €2,453.8M in 2020, representing 39% of the total. Buyouts transactions fell significantly from 68 in 2019 to 49 in 2020. This decrease in buyouts can be explained in part by the lower banking activity directed at this type of corporate transactions, although there is a broad range of alternative

financing available through direct lending funds that are increasingly active in the Spanish market. International funds invested a total of €1,940.5M in buyouts, across 26 transactions (compared to €5,976.4M and 31 investments in 2019). This decrease in volume is primarily due to the lower number of large investments (>€100M in equity) closed by these funds, as only 3 of the 8 investments were buyouts, whereas 18 of the 19 large transactions closed in 2019 were buyouts. Domestic Private Equity GPs reduced their investment in buyouts to €513.3M across 23 investments (compared to €903.8M in 37 investments in 2019). The “other” category10 came in second thanks to several large equity investments over €100M relating to the purchase of listed shares (MásMóvil).

8 The number of investments as published in this report is calculated from the investor perspective, meaning that some investee companies may be double counted in the case of syndicated investments by Venture Capital and Private Equity firms.

9 Investments in mature companies using equity and external debt to acquire an interest in the company. Also referred to as LBO, MBO (buyouts) or MBI.10 The “other” category includes private investment in public equity (PIPE), restructuring, reorientation and refinancing transactions

A determining factor in the expansion of Venture Capital and Private Equity in recent years has been the activity of international funds, whose presence in Spain has continued to grow each year thanks to the attractiveness of the domestic market, the asset opportunities it offers in relevant sectors such as healthcare, education, technology, renewable energies and the food industry, and to excellent management teams with a corporate culture, all in a context of significant global investor appetite. The presence of these funds in the Spanish market started in the 90s with a clear investment focus on investing in consolidated companies. However, in recent years, not only has their activity increased in terms of volume, but also by types of transactions, including funding of companies from the initial to mature stages. Following the trend of previous years, the activity of international funds in the large market segment stands out, having invested €2,882M in 8 transactions. In 2020, international funds invested a total of €4,701.4M (second best figure on record following 2019), representing 75% of total annual investment, and closed a total of 192 investments, a record high for the eighth consecutive year. Yet again, the increased activity of international funds in the Venture Capital sector is also noteworthy, reaching a new record high in the number of investments made in Spanish start ups, with a total of 136, 20 of which were in seed capital, a stage that saw virtually no activity from international funds prior to 2020.

Furthermore, domestic private Venture Capital and Private Equity firms (hereinafter, “GPs”) invested a total of €1,474.1M (-30% from 2019) across 528 investments (+16 from 2019) a record high. As in recent years, investment contributions were supported by the momentum of the middle market. Meanwhile, private domestic Venture Capital funds stood out in terms of number of investments closed each year. Direct investment activity by domestic public GPs decreased to €99.8M (-22% YoY), allocated to 118 investments (-30.5% from 2019). Likewise, the public sector continued supporting Venture Capital and Private Equity through its investment activity (as Limited Partner or “LP”) both in Private Equity and Venture Capital vehicles, as further explained in the "Fundraising" section of this report.

A total of 578 Spanish companies (90% SMEs) received Venture Capital & Private Equity funding in 2020. Regarding the number

of investments in 2020, a record high of 838 investments8 in 578 companies was recorded as well. The proportion of new investments to expansions of previous investments has maintained basically the same ratio since 2014. Specifically, 59.9% of investments were directed towards companies that, until 2020, had never received Venture Capital or Private Equity investments. Between 2015 and 2020, the Venture Capital and Private Equity sector has funded approximately 3,293 companies, approximately 90% of which are SMEs.

22

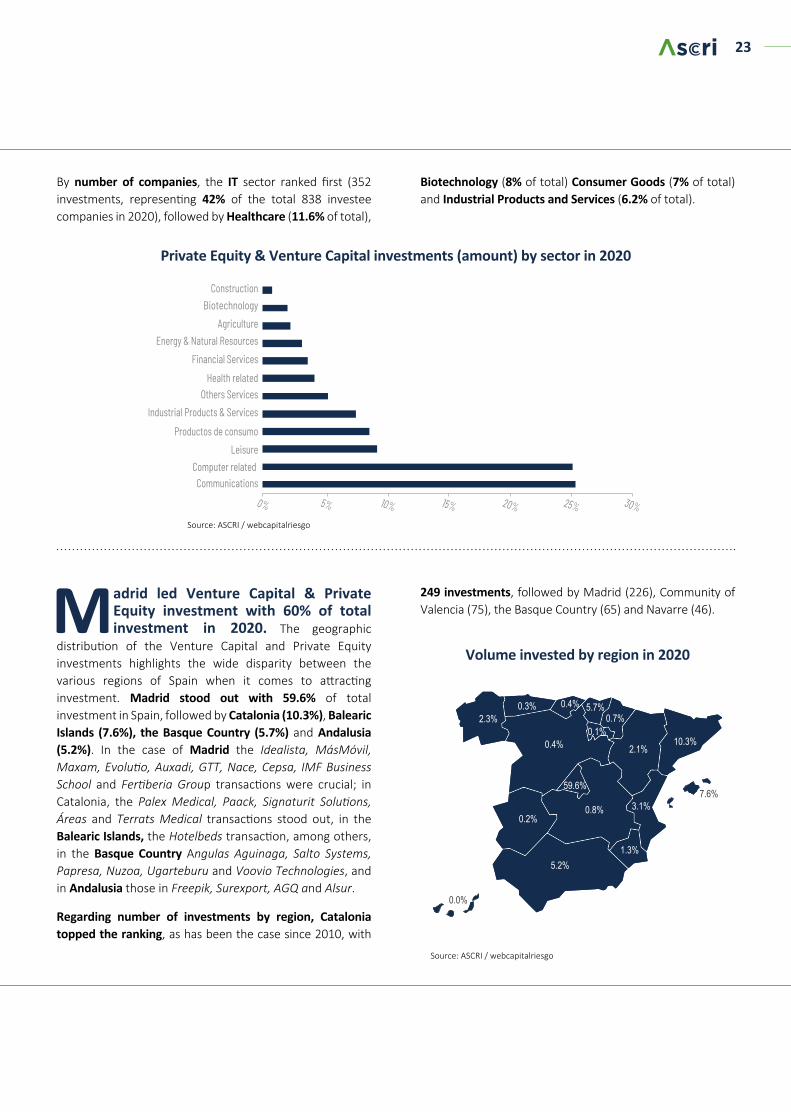

L ife Sciences17 reached a record high in number of investments, and the Communications and IT sectors were the

primary recipients of Venture Capital and Private Equity financing. Regarding sectors,18 Communications received 25.5% of funds invested, in transactions including MásMóvil (largest equity transaction in the history of the sector in Spain), Evolutio, Nice People at work and Excom Telecom Group, among others, followed

by IT (25.2%), in transactions including Idealista, Freepik, Paack, Jobandtalen and Signaturit Solutions, among others. These were followed in distant positions by: Leisure (9.4%), in transactions including Hotelbeds, Áreas and Goiko; Consumer Goods (8.7%), in transactions including Angulas Aguinaga, Salto Systems, Iberfrasa and Laboratorios Almond, among others; and Industrial Products and Services (7.6%), including companies such as Maxam Europe, GTT, Papresa and Imaweb.

The financing of growth in mature companies (growth capital11), with €926M invested, reached a record high since the beginning of the previous recession. International investors stood out for their recent increased presence in this category, with €373M invested in 22 investments, compared to €145.7M in 14 investments in 2019. In total, 94 growth capital investments were closed, far from levels seen between 2007-2008, years that saw around 160 investments p.a. A majority of these transactions were carried out by domestic entities (72 investments). [A list of the main growth capital and buyout investments is provided in pages 41, 42, 43].

Investment in startups through Venture Capital GPs reached a record high (€833M) for the second consecutive year (+6.3% from 2019).

By number of investments, companies in start up stages (Venture Capital) received the most investments with 672 closed (87% of total), setting a record high for the sixth consecutive year. A total of 203 investments were recorded in other early stage12, followed by 199 investments in start up13, late stage venture14 (151 investments) and seed15 (119) stages. For a detailed analysis of investments in the seed, start up, other early stage and late stage venture stages see Chapter 6, on Venture Capital. The remaining investee companies, by number, belong to the replacement16 (9 investments) and other (14 investments) categories.

Investment

11 Funding of growth in mature companies only through equity or capital.12 Other early stage: refers to follow-on rounds or Series B/C investments in startups.13 Investment in start ups: first round of investment in companies with early sales but negative EBITDA14 Late stage venture: Investment in growth companies with positive sales and EBITDA15 Seed: Investment in companies without sales16 Buying a minority stake from an existing shareholder of the investee company.17 Encompasses the Healthcare and Biotechnology sectors18 See page 60 of this report for a description of the activities included in each sector.

Stage distribution of Venture Capital & Private Equity investments

Source: ASCRI / webcapitalriesgo

Seed Start-up + other early

stages Late stage venture

Growth LBO/MBO/

MBI/LBU Other

1,000

3,000

5,000

7,000

9,000

0

€ Mi

llions

2014 2015 2016 2017 2019 20202018

23

Madrid led Venture Capital & Private Equity investment with 60% of total investment in 2020. The geographic

distribution of the Venture Capital and Private Equity investments highlights the wide disparity between the various regions of Spain when it comes to attracting investment. Madrid stood out with 59.6% of total investment in Spain, followed by Catalonia (10.3%), Balearic Islands (7.6%), the Basque Country (5.7%) and Andalusia (5.2%). In the case of Madrid the Idealista, MásMóvil, Maxam, Evolutio, Auxadi, GTT, Nace, Cepsa, IMF Business School and Fertiberia Group transactions were crucial; in Catalonia, the Palex Medical, Paack, Signaturit Solutions, Áreas and Terrats Medical transactions stood out, in the Balearic Islands, the Hotelbeds transaction, among others, in the Basque Country Angulas Aguinaga, Salto Systems, Papresa, Nuzoa, Ugarteburu and Voovio Technologies, and in Andalusia those in Freepik, Surexport, AGQ and Alsur.

Regarding number of investments by region, Catalonia topped the ranking, as has been the case since 2010, with

249 investments, followed by Madrid (226), Community of Valencia (75), the Basque Country (65) and Navarre (46).

Source: ASCRI / webcapitalriesgo

Volume invested by region in 2020

2.3%0.3% 5.7%

0.7%

2.1%10.3%0.4%

0.2%0.8%

59.6%

3.1%

1.3%5.2%

7.6%

0.0%

0.1%

0.4%

By number of companies, the IT sector ranked first (352 investments, representing 42% of the total 838 investee companies in 2020), followed by Healthcare (11.6% of total),

Biotechnology (8% of total) Consumer Goods (7% of total) and Industrial Products and Services (6.2% of total).

Source: ASCRI / webcapitalriesgo

Private Equity & Venture Capital investments (amount) by sector in 2020

5%0% 10% 15% 20%

Industrial Products & Services

Productos de consumoLeisure

Energy & Natural ResourcesFinancial Services

Communications

BiotechnologyConstruction

Agriculture

Health relatedOthers Services

Computer related

30%25%

24

Investment

Venture Capital and Private Equity activity in Spain primarily focused on financing SMEs. Investments in SMEs are dominating the

Spanish market. Of the 838 investments made in Spain by PE&VCs in 2020, 670 were made in SMEs with fewer than 100 employees.

According to transaction size, business finance below €1M ranked first (with 59.4% in 2020), while 24.2% of the companies received between €1 and 5 million, 4.4% between €5 and 10 million, 5.9% between €10 and 25 million and 5% between €25 and 100 million. The rest (1%) relates to transactions of more than 100 million.

Among these segments, the €1M–€2.5M segment (145 investments, record high) and the lower middle market segment (investments between €5 and €10M) stood out, continuing the intense activity of recent years with a total of 37 investments.

The decrease in large transactions resulted in a lower average amount per investment, which fell to €7.5M in 2020 (the average in 2019 was €11M). As regards companies, each of the 586 investee companies received an average of €10.8M in Venture Capital and Private Equity financing in 2020, compared to €14.5M in 2019.

Venture Capital & Private Equity investments (number) by company size in 2020

Source: ASCRI / webcapitalriesgo

Venture Capital Private Equity

0% 20% 40% 60% 80%

100%

0 to 99 employees

100 to 199 employees

200 to 499 employees

More than 500 employees

25

Middle market investments

Volumen Nº investments

2015 2017 2018 2019 20202016201420132012201120102009

€ Mi

llion

s

0

1,000

2,000

3,000

30 30 33 23 12 29 50 51 56 63 75 75 deals

Source: ASCRI / webcapitalriesgo

Middle Market

Record high in the Spanish middle market1

for the second consecutive year. The new scenario marked by the global pandemic did not

cause a slowdown in middle market activity, which reached a new record high in 2020, by both volume and number of investments. Driving factors in the gradual recovery of this investment segment in recent years include the availability of funds to several Spanish middle market GPs, thanks to intense fundraising for establishing new investment vehicles, coupled with the investor appetite of domestic and international funds. In 2020, the total amount invested in this market segment was €2,581M (compared to €2,069.8M in 2019), representing 41% of total investment in Venture Capital and Private Equity in Spain (€6,275.2M) compared to 26% in 2019. 92 investments were made in mid-sized companies, compared to 75 in 2019.

78.4% of invested capital was directed towards companies that had previously never received financing from any Venture Capital or Private Equity GPs (10 p.p. less than 2019). Regarding the number of investments, the proportion of new investments was somewhat lower than 2019: of the 92

investments closed, 70 were in new companies for Venture Capital and Private Equity GPs, compared to 75 investments closed in 2019, of which 65 were in new companies.

Intense activity of international firms in the middle market drove these investments to record levels. Domestic funds have traditionally led

the middle market segment in Spain. However, in 2020, international GPs increased their activity in this type of transaction to never-before-seen levels in Spain, thanks to their shifting investment focus from larger companies to mid-caps, which is a niche market in Spain that presents many opportunities within the current environment characterized by high competition for quality assets. In 2020, these funds invested €1,516.4M (+108% from 2019) in 47 investments (25 investments more than 2019). Of the 47 investments made in this segment in Spain, for the first time, their activity in financing late stage venture (9 investments) and growth capital (12 investments) stood out. Meanwhile, domestic funds invested a total of €1,064.8M (-20.6% from 2019) in middle market transactions across 45 investments (8 less than 2019).

1 Investments in mid-sized companies, with equity contributions between €10M and €100M.

26

Investment by transaction size followed a very similar pattern to that seen in recent years. The largest number of investments were made in the €25–50M equity investment range, accounting for 29 investments, 16 of which were made by international funds. This was followed by the €10–15M tranche, accounting for 24 investments this past year, 16 of which were led by domestic GPs.

The middle market has been one of the most active segments since 2015, when the economy began to recover from the previous crisis. Since then, successive annual record highs have been achieved both by volume and number of transactions, without the change in cycle caused by the current pandemic causing any slowdown in momentum. In fact, following the months of lockdown when Venture Capital and Private Equity firms were focused on preserving

the continuity of investee companies by providing liquidity, stability and management support, an intense reactivation has been seen thanks to the availability of funds by the majority of GPs, access to accompanying debt (in particular, credits) and investor appetite, especially by international funds. Likewise, from the supply side, the attractiveness of Spanish mid-caps (in particular those in counter-cyclical sectors), most of which have experience from previous crises and good management teams, has been decisive. In the new current scenario, in which funding (and equity in particular) will need to be mobilized towards companies to support them in the face of the crisis or to respond to their growth needs, Venture Capital and Private Equity, as an expert in long-term investment in the real economy, will be crucial.

Middle market investments by size of investment

2017 2018 2019 2020

600

400

200

0

€ Mi

llion

s

10 to 15 15 to 20 20 to 25 25 to 50 50 to 75 75 to 100

Source: ASCRI / webcapitalriesgo

27

Stage distribution of middle market investments

Leveraged transactions represented 53% of total middle market investments2. The availability of accompanying credit, including both

bank and alternative financing (such as corporate bond funds), has led to similar numbers in terms of LBOs in the middle market, from 40 in 2019 to 38 in 2020, totaling €1,359.7M in 2020 (€1,262.3M in 2019). As for Growth Capital, 33 investments were completed (10 more than 2019), recording a total volume of €776.9M. Venture Capital accounted for 14 investments (record high), totaling €242.8M (+12% from 2019). As regards GPs, international funds investing in the middle market focused primarily on buyouts (€875M across 21 transactions). Domestic funds distributed their investments between buyouts (€484.6M across 17 transactions) and growth capital (€428.3M across 21 transactions).

[A list of the main middle market transactions is provided in page 42 and 43.]

As regards sectors3, the middle market has historically focused on traditional industries. The Consumer Goods sector received the highest investment volume (€510.5M; 19.8% of total), followed by IT (€361.3M; 14% of total), thanks to the commitment of international funds to growing startups, Other Services (€283.7M; 11% of total), Industrial Products and Services (€257.8M; 10% of total) and Financial Services (€223.6M; 8.7%).

The following stand out in the sector distribution by number of investments: Consumer Goods (20 investments), IT (18), Industrial Products and Services (8), Financial Services (7), Healthcare (6) and Energy / Natural Resources (5).

2,000

3,000

1,000

0

€ Mi

llion

s

2016

2017

2018

2019

Seed Start-up + other early

stages Late stage venture

Growth LBO/MBO/MBI/LBU Others

2 Investments in mature companies using equity and external debt to acquire an interest in the company. Also referred to as leveraged transactions, MBO (buyouts) or MBI.3 See page 60 of this report for a description of the activities included in each sector.

28

Investments by international entities in Spain (by size of investment)

2014 2016 2017 2018 2019 20202015201320122011201020090

1,000 2,000 3,000 4,000 5,000 6,000 7,000 8,000

€ Mi

llion

s

Nº in

vest

men

ts

20181614121086420

2

54

67

9

4

9

139

19

8

Source: ASCRI / webcapitalriesgo

Investments > 100M€ Investments < 100M€ Nº inv. > 100M€

Large Market. The International GP in Spain

International funds led the large market in Spain. After three consecutive years of record highs, large transactions (>€100M in equity1, also known as

megadeals) in 2020 decreased from 2019, falling from an average of approximately 60% of total Venture Capital and Private Equity investments in Spanish companies in recent years to 46% (€2,882M). This decrease in large transactions can be explained in part by the operational difficulties faced as a result of the new scenario, lack of visibility and uncertainty in terms of assessing these types of targets. Following the trend of previous years, international firms led this type of investment thanks to their investment capacity, made possible by the size of the funds they manage, and which enables them to take on large investments.

In 2020 8 large transactions were closed in 5 companies: EQT (Idealista), Cinven, Providence Equity and KKR (MásMóvil)2, CPPIB, Cinven and EQT (Hotelbeds), Rhone Capital (Maxam) and EQT (Freepik). Of these eight transactions, three were public to private,3 following one

of the hallmark trends of 2019 at the global level. In 2020, average equity or capital invested per transaction in this segment totaled €748M compared to €448 in 2019.

L Investment of international Venture Capital and Private Equity GPs in Spain: second highest on record behind the all-time high

reached in 2019. The strength and recovery of the Spanish economy following the previous financial crisis has attracted Venture Capital and Private Equity investments by international firms, which are increasingly discovering Spain as an attractive market for investment opportunities and which, coupled with investor appetite, has resulted in four consecutive years of record high investments by international Venture Capital and Private Equity GPs in Spanish companies. In 2020, despite the new environment caused by the global health crisis and the entry into force of Royal Decree-Law 8/2020 and 11/2020, amending the regulations on foreign investments,4 international Venture Capital and Private Equity firms continued to focus on

1 All investment amounts published by ASCRI refer to the equity or capital invested.2 Largest equity transaction in the history of this sector in Spain.3 Market volatility combined with the abundant market liquidity has favored Public to Private transactions.4 From March 2020, when Royal Decree-Law 8/2020 and 11/2020, amending the foreign investment regime, entered into force, through March 2021, inquiries were received from

nearly 520 international investors regarding operations and requests for authorization by the Ministry of Industry. Of these, most requests were approved under the simplified procedure, only 26 required approval by the Council of Ministers and one investment had to meet certain conditions in order to receive final approval.

TRANSACTIONS CLOSED IN THE SPANISH LARGE MARKET

2017 2018 2019CVC Capital Partners (CLH), Hellman & Friedman (Allfunds Bank), Eurazeo (Iberchem), BC Partners (Pronovias), Providence (NACE), Lone Star (Esmalglass), Trilantic Partners (Grupo Pacha), CVC Capital Partners y PAI Management (Cortefiel), Rakuten (Cabify) CVC Capital Partners (Vitalia Home) y Warburg Pincus (Acceltya)

CVC Capital Partners (Gas Natural), Blackstone (Cirsa), Cinven (Ufinet Latam), Orient Hontai Capital (Imagina Media Audiovisual), Towerbrook Capital Partners, (Aernnova), Ardian, (Grupo Monbake), The Carlyle Group (Unideco (Codorniu Raventós), Cinven (Plantas de Navarra) e ICG (Suanfarma)

The Carlyle Group (Cepsa), CPPIB y Bridgepoint (Dorna Sports), Permira Asesores (Universidad Europea de Madrid), PAI Management (Areas), Rhone Capital, (Maxam), ICG, (Konecta), EQT Partners (Ingenomix), Advent International (Vitaldent), CVC (Alfonso X El Sabio), KKR (Telepizza), KKR (Grupo Alvic), Bridgepoint (Miya Water), Providence (Masmovil), Investindustrial (Neolith), The Carlyle Group (Jeanologia), Investindustrial (Natra), Platinum Equity (Iberconsa), Vista Equity (Accelya)

29

Spain, with investments reaching the second highest figure on record, investing a total of €4,701.3M in Spanish companies (compared to €6,714.5M in 2019), representing 74% of total Venture Capital and Private Equity investment in Spain. Of this amount, €2,882M were in megadeals, €1,516.4M were middle market transactions (equity investments between €10M and €100M) –a record high investment in middle market transactions by international managers–, and the rest (€303M) were transactions involving equity investments of less than €10M. As a sign of the confidence in the Spanish economy, the number of companies financed by international funds has increased steadily in recent years, setting annual highs each year since 2013. In 2020, these funds closed a total of 192 investments (55 above the record high of 2019), 118 of which were new investments (61.5%) and 74 extensions (38.5%), maintaining the percentages recorded in 2019.

In terms of volume, investments by international managers in Spain in 2020 were distributed across leveraged

transactions5 (€1,940.5M) and "other”6 (€1,935M) due to various equity investments over €100M relating to the purchase of listed shares (MásMóvil). By number of transactions, recent years have shown a growing interest of international venture capital funds in investing in Spanish start-ups, and in 2020, a new all time high was reached in number of transactions by this type of investor in this segment (136 investments), with the "late stage venture" category standing out as receiving the largest number of investments (53) compared to the other categories. Likewise, their investment in the seed stage stood out, totaling 20 investments compared to previous years in which no more than 3 seed stage investments were closed each year.

The number of international Venture Capital and Private Equity firms operating in Spain grew from 25 in 2006 to 2927 in 2020.

5 Investments in mature companies using equity and external debt to acquire an interest in the company. Also referred to as LBO, MBO (buyouts) or MBI.6 The “other” category includes private investment in public equity (PIPE), restructuring, reorientation and refinancing transactions.7 A list of the international VC&PEs with activity in Spain is provided at the end of this report.

Number of international entities investing in Spain (by size of funds managed)

Large GPs - manage or advise on more than €150M Medium GPs - manage or advise on between €50 - €150M Small GPs - manage or advise on less than €50M

2014 2016 2017 2018 2019 2020201520132012201120102009

Nº o

f ent

ities

105090130170210250

240 292

205182

157132

9884

61534641

!"#$%&'()*+ !"#$,*)-'('+ !"#$.*/0*1'+

30

Leveraged transactions led in international funds' portfolios. In 2020, the international funds companies portfolios[1] totaled €24,240.6M in 487

investments. Investment of international Venture Capital and Private Equity funds in Spain has been traditionally directed at consolidated companies, as evidenced by the composition of these funds' portfolios: 69.5% of volume is invested in consolidated companies through buyout transactions, 11.9% in other transactions,[2] 9.4% in startups and other early Venture Capital stages and 9.3% in companies in replacement and growth stages. However, more than 310 of the 487 portfolio investments were

made in Venture Capital, reflecting the interest in the Spanish entrepreneurial ecosystem.

Regarding sectors,[3] Other Services (21.1%), Energy / Natural Resources (12.8%), IT (12.4%), Consumer Goods (11.5%), Communications (9.7%), Financial Services (6.0%) and Industrial Products and Services (5.4%) were the sectors that accumulate the highest investment levels. By number, the 487 portfolio investments are primarily centered on IT (225 investments), followed by Healthcare (46), Consumer Goods (39), Other Services (36) and Biotechnology (28).

[1] Value (at price cost) of all investee companies managed.[2] The “other” category includes restructuring, reorientation and refinancing transactions.[3] See page 60 of this report for a description of the activities included in each sector.

Portfolio of international GPs in Spain by sectoral distribution (by volume) in 2020

Computer related 12.4%

Leisure 5.3%

Financial Services 6.0%

Other Services 21.1%

Energy/Natural Resources 12.8%

Transport 2.7%

Consumer related Products 11.5%

Health related 4,9%

Industrial Productos & Services 5.4%

Communications 9.7%

Number of investments by International GPs

Seed Start-up Other early stage Later stage venture Growth LBO Other Total

2018 3 16 43 22 9 22 2 117

2019 3 19 37 32 14 31 1 137

2020 20 14 49 53 22 26 8 192

31

Performance of Venture Capital Key Performance Indicators

• Record year for Venture Capital investment in Spanish start ups for the second consecutive year with a total investment of €833M.2 The numerous funding rounds for start ups in more advanced stages (Series B or “other early stage” and Series C or “late stage venture”) largely explain this year’s positive results.

• Momentum for the innovation ecosystem: 672 Venture Capital investments were made (record high) to fund 433 Spanish start ups, the third best figure on record following 2018 (459 start ups) and 2017 (449 start ups).

• A total of 18 start ups received investment rounds above €10M, the best figure on record, breaking the previous record from 2019 (12 start ups).

• Activity in the €1M - €5M investment range grew, contributing to the support of projects with scaling potential: in 2020, 168 investments3 were made totaling €333.8M, doubling the figures from five years ago (€161M in 81 investments in 2016).

• Record high investment by private domestic Venture Capital firms. New funds raised by these firms in recent years has enabled them to drive the funding of innovation in Spain. In 2020, €312M was invested

in 433 investments, a record high for both variables. Over 80% of investments were made to support companies in the earliest stages.

• Public Venture Capital firms continue to recover their direct investment activity in start ups, doubling the investment volume recorded in 2019. Their investment activity was particularly focused on the IT and life sciences sectors.

• Despite the new environment caused by the global pandemic, international Venture Capital funds have maintained their interest in the Spanish innovative ecosystem and, in fact, their investments in start ups reached a record high in investment volume (€452.4M), in number of investments (136 in 83 start ups) and in number of GPs who made at least one investment in a Spanish start up (98 compared to 68 in 2019), clearly reflecting the attractiveness of the Spanish market globally. In addition to the usual rounds for start ups in more advanced stages, international VC&PEs also invested in numerous early stage projects, a change from their previous investment trajectory in Spain.

• The maturity being reached by certain start ups headquartered in Madrid has led to over 60% of late stage investments in 2020 being made in this region.

MAIN CONCLUSIONS FOR 20201

1 All statistical data on the Venture Capital sector is available on pages 54 and 55. 2 METHODOLOGICAL NOTE: The statistical data provided by ASCRI/webcapitalriesgo on investment has been calculated on the basis of actual payments (equity and quasi-equity) made

by domestic and international Venture Capital and Corporate Venture firms to companies headquartered in Spain. This criterion differs from that used by other sources who account for investments in terms of future committed capital plus the equity received by the start up, regardless of the type of investor, a variable that we refer to as “transaction value.” All figures are provided in millions of euros.

3 The number of investments published in this report is calculated from the perspective of the funds, meaning that some investee companies may be double counted in the case of syndicated investments.

Venture Capital

Fundraising Investment Divestment

Fundraising DivestmentInvestment international VC Investment domestic private VC Investment domestic public VC

2018 2019 2020201620150

100200300400500600700

900800

0

100

200

300

400

500

2017 2018 2019 202020162015 2017 2018 2019 202020162015 20170

100200300400500600700800900

€ Mi

llions

€ Mi

llions

€ Mi

llions

32

Venture Capital

Summary of Venture Capital investment in Spanish start ups in 2020

4 A total of 433 companies received funding in 2020, 45 of which were co-invested by domestic and international funds.5 The number of investments accounts for each of the investment decisions made by the funds, such that a company may receive several investments at a time (funding round) if the

investment has been syndicated by several investors.

2020 DOMESTIC INTERNATIONAL

Corporate VC (Investment) €18.6M €34.3M

Private VC (Investment) €293.5M €418.1M

Public VC (Investment) €68.5M -

Active Investors (2020) 89 98

Total Investment €380.7M €452.4M

No. of Investments 536 136

Start Ups Invested 3954 83

Avg. Round (€M) €1M €5.5M

Avg. Ticket (€M) Investments €0.7M €3.3M

VENTURE CAPITAL ACTIVITY IN 2020

All-time high in volume invested by Venture Capital funds in Spanish start ups for the second consecutive year,

driving investments in more advanced stage projects. Venture Capital funds (89 domestic and 98 international entities) invested a total of €833M in Spanish companies in 2020, a 15.4% increase from 2019 (€721.9M), an all-time high. The scenario caused by the global pandemic raised concerns about the impact on investment across all types of companies, including start ups. However, although Venture Capital GPs placed a particular focus on guaranteeing the survival of their portfolio of investee companies during the first half of the year —in response to the need for acceleration of the digitalization processes of companies and support for health-related activities— support for technological

start ups grew, many of which are increasingly reaching a significant degree of consolidation that requires larger funding rounds. In 2020, a total of 18 start ups received funding in excess of €10M (6 more than in 2019), a record high. Most of these larger rounds were syndicated by international Venture Capital funds, as is becoming the norm in the Spanish market. By number of investments5, in 2020, there was again a shift towards higher tickets, in particular in the €1M–€2.5M (127 investments in 2020 compared to 91 in 2019) and €2.5M–€5M (41 investments in 2020, beating the 2019 record high) segments, resulting from the growing entrepreneurial ecosystem. International Venture Capital GPs continue to focus their investments on Spain, attracted by the ecosystem and its start ups, becoming a key player thanks to its participation in stages that require higher funding, although they are

• Venture Capital investment in terms of GDP grew, reaching 0.07% and surpassing the percentage recorded in 2019 (0.06%).

• Regarding the impact of Venture Capital investment in terms of its ability to drive funding from other co-investors towards start ups, i.e. transaction

value, defined as the sum of total equity invested by Venture Capital GPs (€833M) plus investments made by co-investors (such as LPs, management teams, corporations, etc., and which totaled €441.9M), in 2020, this variable broke €1,274.9M (+8.2% from 2019; €1,177.8M).

33

also increasingly active in the funding of Spanish start ups in earlier stages. As a sign of the attractiveness of the Spanish market, 98 international GPs made at least one Venture Capital investment in Spain, compared to 68 in 2019. In 2020, investment of these funds totaled €452.4M (+2% from 2019) (5 times the investment level of 10 years ago), the best figure on record, across 136 investments in 83 companies6 (30 more than in 2019, an all-time high).

As at the end of 2020, 198 of the approximately 292 international entities with Spanish portfolio companies were Venture Capital firms. At the national level, the sector had close to 113 firms investing in Venture Capital,7 75 of which were dedicated exclusively to Venture Capital and 6 of which were public.

Record high Venture Capital investment by domestic funds. Since 2016, new funds raised by private firms (many of which are already

on their third and fourth generation funds), together with increased leeway in the budgets of public institutions for direct investments, has driven the investment activity of domestic Venture Capital firms to new highs. In particular, domestic entities increased their investment in Spanish start ups to €380.7M (36.6% from the €278.7M invested in 2019). This volume was distributed across 536 investments, 80% for amounts below one million euros, which ensures support to the Spanish innovation ecosystem.

Venture Capital investments focused specifically on supporting the portfolio. In 2020, the funding and support of start ups was

particularly aimed at driving growth in portfolio companies, providing liquidity and ensuring their continuity, although several new projects were also promoted, which gave new life to the Spanish entrepreneurial ecosystem. In 2020, a total of 672 Venture Capital investments were made in 433 companies, of which 219 start ups received new Venture Capital funding (50 companies less than in 2019). Capital injections in 214 companies were used to support the portfolio (+32% vs. 2019, a 5-year high). As regards Venture Capital funds that channeled capital to new investments,

a total of €174.7M was invested, while €658.3M were directed at extensions and follow ons of portfolio companies.

The maturity of the ecosystem shifts investment towards larger rounds. In the last five years, start ups receiving larger investment

rounds have been gaining in prevalence over start ups receiving equity investments of less than €1M. Specifically, in 2020, 66% of start ups received investment rounds of less than €1M in equity, compared to 75% in 2019. This highlights the health of the innovation ecosystem in which new projects continue to receive funding for implementation, while the more mature start ups are also able to access funds to boost their growth.

Investments in more advanced stage projects increased, with record high investment in emerging projects. In 2020, the trend of recent

years was consolidated, in which the funding of start ups in more advanced stages with the potential to reach a global scale continues to receive the highest investment volume as a result of the growing need of start ups for equity. Specifically, late stage venture8 in 2020 received a total investment of €376.8M (second best figure on record behind 2019). This amount was distributed across 67 companies, 19 of which received Venture Capital funding for the first time (15 less than in 2019). Unlike previous years, by investment stage, investments in Series B or “other early stage9” reached a record-high with €281M in 119 start ups, strengthening Spanish start ups that are in the growth process but not yet turning a profit. In addition, for the first time, seed stage10 totaled €79.9M in investments (+284% from 2019), a record high, in 89 start ups, strengthening the selection of opportunities.

This distribution of investment, where all start ups regardless of stage obtain financing, strengthens the ecosystem. As is becoming the norm, international funds focused on financing start ups in their more mature stages, whereas private domestic funds focused on financing start ups in their earliest stages.

6 45 of these 83 start ups receiving investment were co-investments between domestic and international Venture Capital funds.7 Venture Capital and Private Equity firms with an investment focus on Venture Capital and that have portfolios in which seed, startup, other early stage and late stage venture account

for at least half of the portfolio.8 Late Stage Venture: Investment in growth companies with positive sales and EBITDA 9 Other Early Stage: refers to follow-on rounds or Series B/C investments in start ups10 Seed Stage: Investment in companies without sales

34

Venture Capital

Private Venture Capital GPs led investment. By type of entity, the significance of investment fell, primarily, in (domestic and international) private

entities as is becoming the norm, totaling €764.5M in investments in 2020 (91% of total volume invested), as compared to €68.5M in investments by public funds (best figure on record since the recovery from the last financial crisis started), across 103 investments (-20.8% from 2019). As mentioned in other reports, since the start of the 2008 financial crisis, public agencies, and in particular regional public agencies, have been reducing their direct investment activity, due in part to lower budget availability. However, in 2020, investment by public institutions recovered, particularly in the funding of new projects (€57M), and maintained its activity in sustaining projects in portfolio (€11.2M). At the same time, their role in funding SMEs and Spanish start ups has been carried out in recent years indirectly through the funds of funds programs launched by ICO (FOND-ICO Global, managed by Axis), the Catalonian Institute of Finance (Instituto Catalá de Finances - ICF) Cofides, and once again CDTI, having recently restored its fund of funds instrument, which channel funds to private domestic Venture Capital funds. In 2020, the public sector,

in its role as an investor (LP) in domestic Venture Capital funds,11 was again the main contributor with €274.8M,12 the best figure since statistics on this figure were first prepared. Undoubtedly, the new scenario caused by the pandemic will place the public sector as a main focus in the recovery of the industrial fabric, and its role will be crucial not only in direct investment but also as a catalyst of funding for the new Venture Capital funds, and therefore in the indirect funding of start ups, strengthening the public-private collaboration that this new situation demands.