2021 Agricultural Outlook - USDA

36

Office of the Chief Economist Seth Meyer, Chief Economist, USDA 2021 Agricultural Outlook

Transcript of 2021 Agricultural Outlook - USDA

Office of the Chief EconomistOffice of the Chief Economist

Seth Meyer,Chief Economist, USDA

2021 Agricultural Outlook

Office of the Chief Economist

U.S. GDP and Disposable Incomemoved in opposite directions in 2020 and may unwind in 2021

23000

28000

33000

38000

43000

48000

53000

58000

10000

12000

14000

16000

18000

20000

22000

24000

Q1

2006

Q1

2007

Q1

2008

Q1

2009

Q1

2010

Q1

2011

Q1

2012

Q1

2013

Q1

2014

Q1

2015

Q1

2016

Q1

2017

Q1

2018

Q1

2019

Q1

2020

Q1

2021

Per-

capi

ta d

ispos

able

inco

me

GDP

(bill

ion

dolla

rs, a

nnua

lized

)

GDP Per capita disposable income

Great Recession

Source: Oxford Economics survey results

2

Office of the Chief Economist

Global trade quarterly growth ratesFluctuations in agricultural trade under global pandemic appear modest

3

Source: USDA-OCE/Virginia Tech-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

2005

Q1

2005

Q2

2005

Q3

2005

Q4

2006

Q1

2006

Q2

2006

Q3

2006

Q4

2007

Q1

2007

Q2

2007

Q3

2007

Q4

2008

Q1

2008

Q2

2008

Q3

2008

Q4

2009

Q1

2009

Q2

2009

Q3

2009

Q4

2010

Q1

2010

Q2

2010

Q3

2010

Q4

2011

Q1

2011

Q2

2011

Q3

2011

Q4

2012

Q1

2012

Q2

2012

Q3

2012

Q4

2013

Q1

2013

Q2

2013

Q3

2013

Q4

2014

Q1

2014

Q2

2014

Q3

2014

Q4

2015

Q1

2015

Q2

2015

Q3

2015

Q4

2016

Q1

2016

Q2

2016

Q3

2016

Q4

2017

Q1

2017

Q2

2017

Q3

2017

Q4

2018

Q1

2018

Q2

2018

Q3

2018

Q4

2019

Q1

2019

Q2

2019

Q3

2019

Q4

2020

Q1

2020

Q2

2020

Q3

2020

Q4

Quarterly growth in trade (Change from same quarter of previous year)

Agricultural Non-Agricultural

2008/9 Global Financial CrisisAg trade down 10-15%

Non-ag trade down 20-30%

2020 PandemicAg trade up 4%Non-ag trade down 6%

Office of the Chief Economist

COVID-19 drove wedge between farm & consumer pricespercent change from one year ago

-3%-2%-1%0%1%2%3%4%5%6%7%

-30%

-20%

-10%

0%

10%

20%

30%

40%

1/1/

2006

1/1/

2007

1/1/

2008

1/1/

2009

1/1/

2010

1/1/

2011

1/1/

2012

1/1/

2013

1/1/

2014

1/1/

2015

1/1/

2016

1/1/

2017

1/1/

2018

1/1/

2019

1/1/

2020

U.S. PPI Farm products U.S. CPI FoodSource: U.S. Bureau of Labor Statistics

right axis

left axis

4

Office of the Chief Economist

A drop in beef and pork plant capacity utilization was followed by a return to near normal

U.S. Beef and Pork Plant Capacity Utilization Daily Cattle and Hog Slaughter

Note: Excludes weekend operations. Adjusted to account for holiday operations.Sources: USDA, National Pork Board, and KC Fed Calculations

50556065707580859095100

50556065707580859095

100

Jan-

20

Feb-

20

Mar

-20

Apr-

20

May

-20

Jun-

20

Jul-2

0

Aug-

20

Sep-

20

Oct

-20

Nov

-20

Dec-

20

Jan-

21

Feb-

21

Beef

Pork

Percent of capacity, 5-day moving average

-50-40-30-20-10010203040

-50-40-30-20-10

010203040

Jan-

20

Feb-

20

Mar

-20

Apr-

20

May

-20

Jun-

20

Jul-2

0

Jul-2

0

Aug-

20

Sep-

20

Oct

-20

Nov

-20

Dec-

20

Jan-

21

Cattle Hogs

y/y percent change, 5-day moving average

5

Office of the Chief Economist

Temporary divergence in wholesale and retail beef and pork prices

Wholesale and Retail Beef Wholesale and Retail Pork

255075

100125150175200225

Jan-

20

Feb-

20M

ar-2

0

Apr-

20

May

-20

Jun-

20

Jul-2

0

Aug-

20

Sep-

20

Oct

-20

Nov

-20

Dec-

20

Jan-

21

Feb-

21

Boxed Beef Cutout Price (Choice/Select Avg.)*

Average Retail Price**

Index (Jan. 2020=100), 5-day moving average

255075

100125150175200225

Jan-

20

Feb-

20M

ar-2

0

Apr-

20

May

-20

Jun-

20

Jul-2

0

Aug-

20

Sep-

20

Oct

-20

Nov

-20

Dec-

20

Jan-

21

Feb-

21

Pork Carcass Cutout Price*

Average Retail Price**

Index (Jan. 2020=100), 5-day moving average

*Beef: negotiated prices and volume of boxed beef cuts delivered within 0-21 days and on average industry cutting yields. Pork: negotiated prices and volume of pork cuts delivered within 14 days and on average industry cutting yields. **Based on weekly national average of advertised prices, weighted based on carcass composition and interpolated to daily averageSource: USDA and KC Fed calculations.

6

Office of the Chief Economist

U.S. Motor Gasoline and Ethanol Domestic Usecorn marketing year

100

110

120

130

140

150

14/1

5

15/1

6

16/1

7

17/1

8

18/1

9

19/2

0

20/2

1

21/2

2

Billi

on G

allo

ns

Motor Gasoline

10

11

12

13

14

15

14/1

5

15/1

6

16/1

7

17/1

8

18/1

9

19/2

0

20/2

1

21/2

2

Billi

on G

allo

ns

Ethanol

Source: EIA, USDA

7

Office of the Chief Economist

Drought/dry conditions expandSept 1, 2020May 5, 2020

Source: U.S. Drought Monitor

8

Office of the Chief Economist

Derecho as seen by Synthetic Aperture Radar (SAR)NASAharvest.org Iowa derecho impact analysis

Before After

9

Office of the Chief Economist

U.S. corn & soybean prices have been surging

Source: CME 2-1-2022 @ 11:50am

10

Office of the Chief Economist

Soybean and corn export demand expands even as the crop size shrinks

(1,500) (1,300) (1,100)

(900) (700) (500) (300) (100) 100 300 500

Supply Feed &Residual

Ethanol Exports Carryout

Chan

ge (m

illio

n bu

shel

s)

Corn

(500)

(400)

(300)

(200)

(100)

-

100

200

300

400

Supply Crush Exports Carryout

Soybeans

Source: OCE-WAOB

11

Office of the Chief Economist

Global crop supplies have tightened

900

950

1,000

1,050

1,100

1,150

1,200

2015

/16

2016

/17

2017

/18

2018

/19

2019

/20

2020

/21

Corn

280

300

320

340

360

380

2015

/16

2016

/17

2017

/18

2018

/19

2019

/20

2020

/21

Soybeans

680

700

720

740

760

780

2015

/16

2016

/17

2017

/18

2018

/19

2019

/20

2020

/21

Wheat

mill

ion

met

ric to

ns

Source: OCE-WAOB

12

Office of the Chief Economist

Chinese soybean imports and crush suggest a strong turn around in their hog herd

mill

ion

met

ric to

ns

0102030405060708090

100

2000

/200

1

2001

/200

2

2002

/200

3

2003

/200

4

2004

/200

5

2005

/200

6

2006

/200

7

2007

/200

8

2008

/200

9

2009

/201

0

2010

/201

1

2011

/201

2

2012

/201

3

2013

/201

4

2014

/201

5

2015

/201

6

2016

/201

7

2017

/201

8

2018

/201

9

2019

/202

0

2020

/202

1

Imports CrushSource: OCE-WAOB

13

Office of the Chief Economist

China’s corn and soybean trade(and trade dependence)

14

-50

0

50

100

150

200

250

300

2000

/200

120

01/2

002

2002

/200

320

03/2

004

2004

/200

520

05/2

006

2006

/200

720

07/2

008

2008

/200

920

09/2

010

2010

/201

120

11/2

012

2012

/201

320

13/2

014

2014

/201

520

15/2

016

2016

/201

720

17/2

018

2018

/201

920

19/2

020

2020

/202

1

mill

ion

met

ric to

ns

Corn

Production Imports (net)

0

20

40

60

80

100

120

2000

/200

120

01/2

002

2002

/200

320

03/2

004

2004

/200

520

05/2

006

2006

/200

720

07/2

008

2008

/200

920

09/2

010

2010

/201

120

11/2

012

2012

/201

320

13/2

014

2014

/201

520

15/2

016

2016

/201

720

17/2

018

2018

/201

920

19/2

020

2020

/202

1

mill

ion

met

ric to

ns

Soybeans

Imports (net) CrushSource: OCE-WAOB

14

Office of the Chief Economist

China’s domestic corn prices surge boosting import margins

050

100150200250300350400450500

Jul-1

1

Oct

-11

Jan-

12

Apr-

12

Jul-1

2

Oct

-12

Jan-

13

Apr-

13

Jul-1

3

Oct

-13

Jan-

14

Apr-

14

Jul-1

4

Oct

-14

Jan-

15

Apr-

15

Jul-1

5

Oct

-15

Jan-

16

Apr-

16

Jul-1

6

Oct

-16

Jan-

17

Apr-

17

Jul-1

7

Oct

-17

Jan-

18

Apr-

18

Jul-1

8

Oct

-18

Jan-

19

Apr-

19

Jul-1

9

Oct

-19

Jan-

20

Apr-

20

Jul-2

0

Oct

-20

Jan-

21

$/m

etric

ton

South China Corn Price U.S. Corn FOB Gulf U.S. Corn LandedSource: CNGOIC and USDA *Landed does not include VAT or tariff.

15

Office of the Chief Economist

China Energy Feedstuff Imports Forecast Record High, Exceeding 2014/15

0.00.51.01.52.02.53.03.54.04.55.0

Mill

ion

met

ric to

ns

U.S. Corn Ukraine Corn Other CornAustralia Barley Canada Barley Other BarleySorghum DDGS Field PeasSource: TDM

16

Office of the Chief Economist

China’s Corn Imports Exceeded TRQ For First Time in 2020more on the books just from the US than total TRQ for 2021

0

2

4

6

8

10

12

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Mill

ion

Met

ric To

ns

Range 2014-2019 2020 Imports TRQ Outstanding Sales

TRQ = 7.2 mmt or 283 mbu

17

Data: TDM and USDA-FAS Export Sales

US to China Outstanding Sales for 2020/21 Marketing Year, through Aug 31

Office of the Chief Economist

U.S. corn and soybean planted acreage

• In both 2019 and 2020 area considered ‘prevent plant’ was above average

• Simply going back to normal planting weather would increase total planted acres by several million acres

• Forecast prices, would further incentivize expanded acreage. Corn and soybean area expected to be a combined record 182 million acres

60

65

70

75

80

85

90

95

100

2014 2015 2016 2017 2018 2019 2020 2021

Mill

ion

acre

s

Corn SoybeansSource: OCE-WAOB

18

Office of the Chief Economist

Corn exports• China strong corn import

demand expected to continue to support solid US exports

• Brazil’s safrina corn area is up, but late planting limits yield prospects.

• Current phytosanitary restrictions in place by China on Brazilian corn is expected to reduce U.S. market share in key traditional export markets during the summer/fall.

01020304050607080

Mill

ion

met

ric to

nsU.S. exports Brazil exportsChina imports

Source: OCE-WAOB

19

Office of the Chief Economist

Local price strength leading to record Brazil corn areaJuly corn futures in Reais

10

15

20

25

30

352-

Jan

16-Ja

n

30-Ja

n

13-F

eb

27-F

eb

12-M

ar

26-M

ar

9-Ap

r

23-A

pr

7-M

ay

21-M

ay

4-Ju

n

18-Ju

n

Reai

s/bu

shel

2016 2017 2018 2019 2020 2021Source: CME, St. Louis Federal Reserve Economic Database

Slow soybean harvest in Brazil means delayed planting of the safrina corn crop

20

Office of the Chief Economist

U.S. wheat planted acres continue to decline

30

35

40

45

50

55

60

65

70

00/0

101

/02

02/0

303

/04

04/0

505

/06

06/0

707

/08

08/0

909

/10

10/1

111

/12

12/1

313

/14

14/1

515

/16

16/1

717

/18

18/1

919

/20

20/2

121

/22

mill

ion

acre

s

Wheat area has declined as gains in corn and soybean productivity push into wheat area

Wheat area expected to rise slightly, off the lowest area on record last year.

Winter wheat harvested area remains a question given prolonged dryness and recent extreme cold temperatures.

Source: OCE-WAOB

21

Office of the Chief Economist

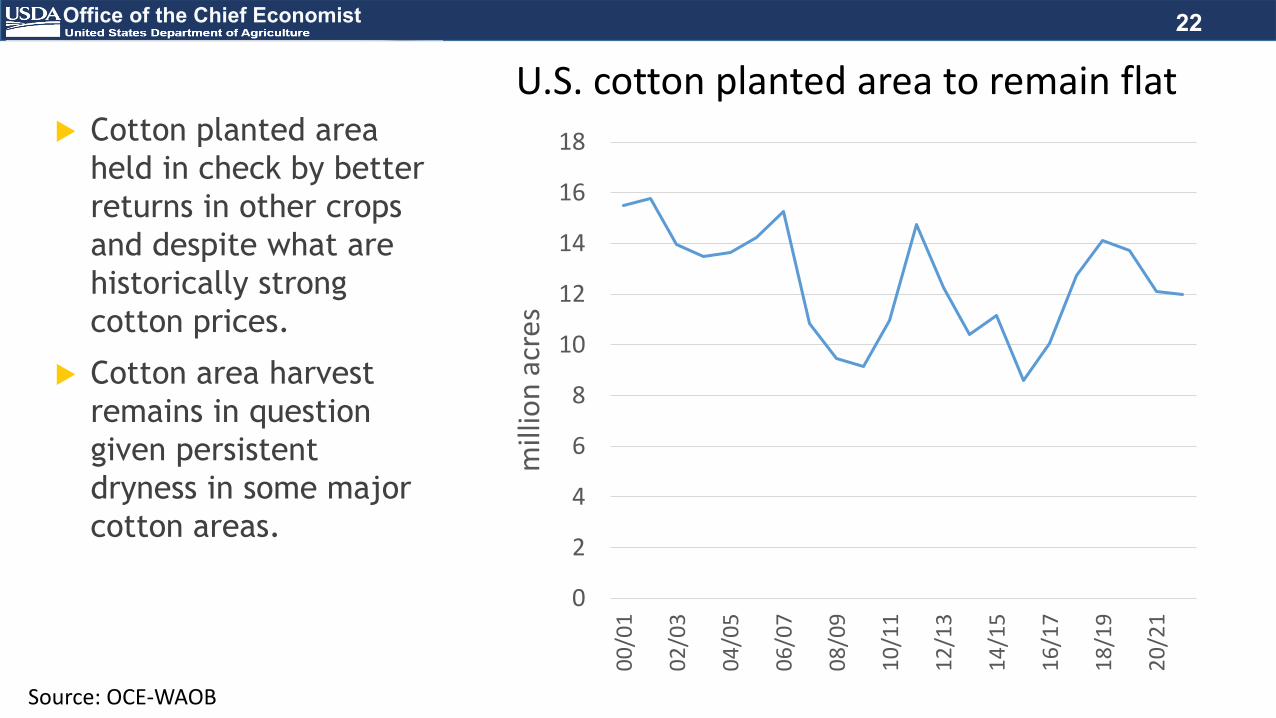

U.S. cotton planted area to remain flat

0

2

4

6

8

10

12

14

16

18

00/0

1

02/0

3

04/0

5

06/0

7

08/0

9

10/1

1

12/1

3

14/1

5

16/1

7

18/1

9

20/2

1

mill

ion

acre

s

Cotton planted area held in check by better returns in other cropsand despite what are historically strong cotton prices.

Cotton area harvest remains in question given persistent dryness in some major cotton areas.

Source: OCE-WAOB

22

Office of the Chief Economist

U.S. cotton exports Cotton stocks fell

last year on a smaller crop and solid exports

Cotton demand held up well in total and relative to other fibers in 2020

Despite the projected larger crop, carryout stocks are expected to tighten further

0

5

10

15

20

25

2000

/01

2001

/02

2002

/03

2003

/04

2004

/05

2005

/06

2006

/07

2007

/08

2008

/09

2009

/10

2010

/11

2011

/12

2012

/13

2013

/14

2014

/15

2015

/16

2016

/17

2017

/18

2018

/19

2019

/20

2020

/21

2021

/22

mill

ion

bale

s

Production ExportsSource: OCE-WAOB

23

Office of the Chief Economist

U.S. crop prices and area

2010/11 to 2014/15 avg

2015/16 to 2019/20 avg

2020/21 2021/22

Corn 5.29 3.50 4.30 4.20

Soybeans 12.26 8.96 11.15 11.25

Wheat 6.71 4.65 5.00 5.50

Rice 14.40 12.34 13.40 13.60Upland Cotton 76.3 65.5 68.0 75.0 0

50

100

150

200

250

300

2000

-01

2002

/03

2004

/05

2006

/07

2008

/09

2010

/11

2012

/13

2014

/15

2016

/17

2018

/19

2020

/21

Corn SoybeansWheat Other 8-crop

8-crop planted area

mill

ion

acre

s

Source: OCE-WAOB

Prices ($/unit)

24

Office of the Chief Economist

Supplies of forage may be an issue for cattle given prior dry conditions and current heavy feeding needs during cold

25

Office of the Chief Economist

Livestock prices2016 2017 2018 2019 2020 2021f

dollars per hundredweightCattle 120.86 121.52 117.12 116.78 108.51 115.00Hogs 46.16 50.48 45.93 47.95 43.18 50.50

cents per poundBroilers 84.3 93.5 97.8 88.6 73.2 84.5Turkeys 117.1 96.1 80.2 89.2 106.5 110.8

cents per dozenEggs 85.7 100.9 137.6 94.0 112.2 111.8

Source: OCE-WAOB

26

Office of the Chief Economist

China’s Live Hog and Sow Inventories

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

55,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

500,000

550,000Live Hog(thousand head)Sow(thousand head)

Live HogsThousand head

SowsThousand head

Source: MARA, USMEF

27

Office of the Chief Economist

Pork export strength continues to absorb production growth (growth since 2015)

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

2016 2017 2018 2019 2020 2021F

mill

ion

poun

ds

Production ExportsSource: OCE-WAOB

28

Office of the Chief Economist

U.S. Per-Capita Meat Disappearance

190

195

200

205

210

215

220

225

230

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

F

Poun

ds p

er c

apita

, Ret

ail B

asis

Source: OCE-WAOB

29

Office of the Chief Economist

Considerable Dairy Product Price Volatility

30

*Weighted Average Blocks and Barrels

2019 2020 2021F

Butter ($/lb) 2.2431 1.5808 1.455

Cheese ($/lb) 1.7586 1.9236 1.695

Nonfat Dry Milk ($/lb)

1.0419 1.0417 1.125

Whey ($/lb) 0.3799 0.3621 0.480

All Milk ($/lb) 18.63 18.30 17.15

0

0.5

1

1.5

2

2.5

3

Weekly National Dairy Product Sales Report

Butter Cheese* Nonfat Dry Milk Whey

Source: AMS-NDPSR Source: OCE-WAOB

30

Office of the Chief Economist

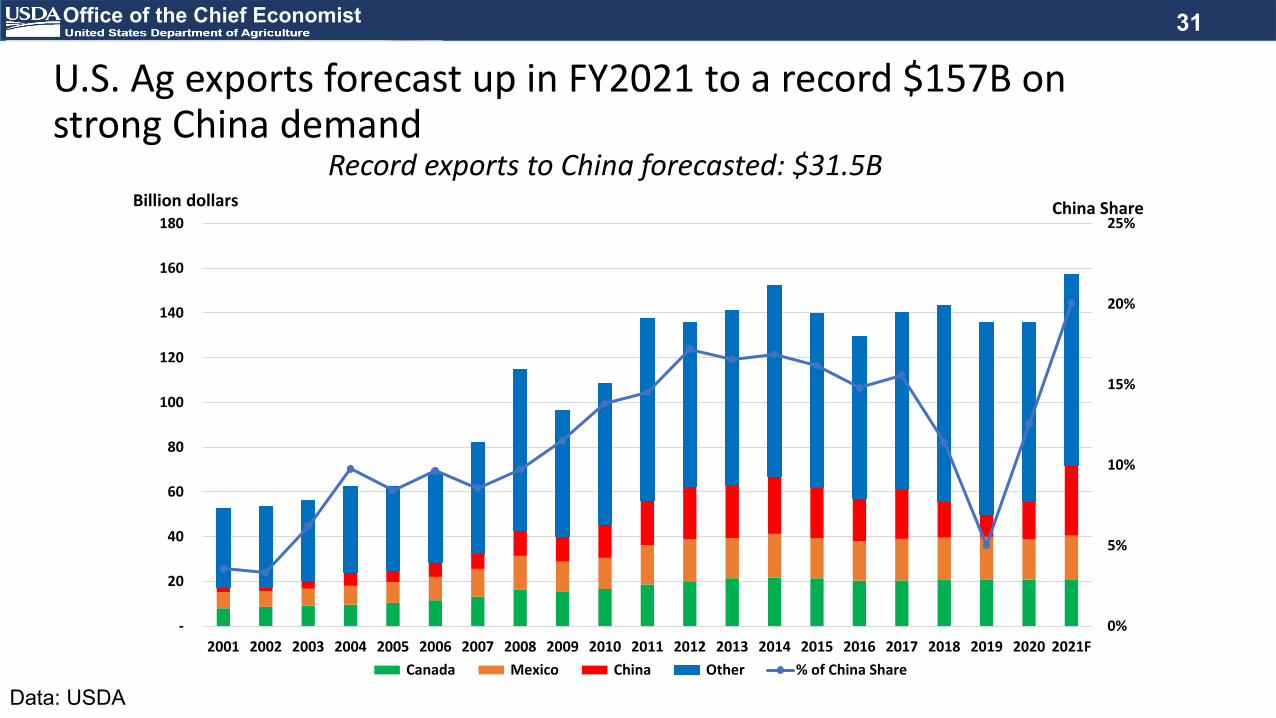

U.S. Ag exports forecast up in FY2021 to a record $157B on strong China demand

Data: USDA

31

Record exports to China forecasted: $31.5B

0%

5%

10%

15%

20%

25%

-

20

40

60

80

100

120

140

160

180

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021F Canada Mexico China Other % of China Share

Billion dollars China Share

Office of the Chief Economist

Total government payments increased as a result of adverse circumstances but are projected to fall in 2021

32

05

101520253035404550

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

Billions (2021$)

Other Government Payments MFP Covid-related (CFAP; Consolidated Appropriations Act, 2021; and PPP)

Source: Economic Research Service Farm Income

Office of the Chief Economist

Corn, soybeans, cattle and hogs push receipts higherand drive the $20.4 billion dollar increase in receipts

crop cash receipts livestock and dairy cash receipts

Source: Economic Research Service Farm Income

33

Office of the Chief Economist

Net cash farm income and net farm income are forecast to decrease in 2021

34

$111.4B

$128.3B

$0$20$40$60$80

$100$120$140$160$180

Billion dollars (2021$)

Net Farm Income (NFI) Net Cash Farm Income (NCFI)

2000-2020 Average NFI 2000-2020 Average NCFI

Data: USDA-ERS

Office of the Chief Economist

Outlook is positive - Uncertainties remain

• GDP expected to rebound, disposable income less certain.• Supply chain disruptions have moderated, at some cost.• Prospects for crops supported by solid domestic demand continued strong exports. • Livestock outlook supported by continued strong domestic demand and stable

exports.• Trade, particularly to China, a key element for 2021.• Good dairy demand but large product stocks.• Receipts from the market replacing ad-hoc assistance.• Weather will have the last say on supplies.

35

Office of the Chief Economist

Visit the OCE website for the latest USDA commodity reports and Agriculture Outlook Forum information @ www.usda.gov/oce

Questions? [email protected]

36

USDA’s 97th Annual Agricultural Outlook Forum: February 18-19, 2021