2020 Employee Benefits Webinar Series

36

Dawn Kramer, J.D. Compliance Center of Excellence October 15, 2020 2020 Employee Benefits Webinar Series Health Savings Accounts

Transcript of 2020 Employee Benefits Webinar Series

Dawn Kramer, J.D.

Compliance Center of Excellence

October 15, 2020

2020 Employee Benefits

Webinar SeriesHealth Savings Accounts

1. Basic Premise

2. What is a Qualified High Deductible Health Plan?

3. No Other Disqualifying Coverage

4. What is Health Savings Account?

5. Contributions and Distributions

6. Questions

2

Note: We will use a COVID-

19 Relief flag to reflect items

that are affected by

temporary COVID-19 relief.

COVID-19 Relief

Agenda

Marsh & McLennan Agency LLC

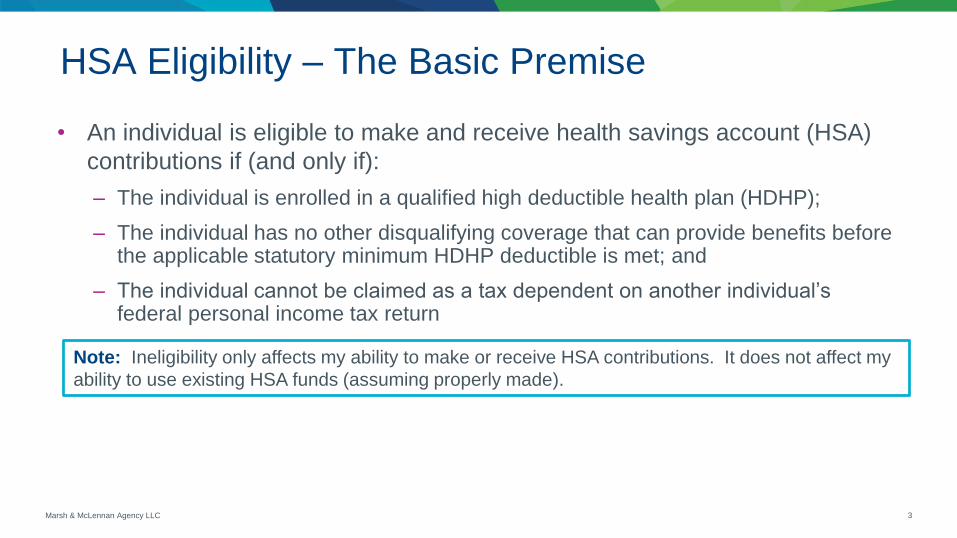

• An individual is eligible to make and receive health savings account (HSA)

contributions if (and only if):

– The individual is enrolled in a qualified high deductible health plan (HDHP);

– The individual has no other disqualifying coverage that can provide benefits before the applicable statutory minimum HDHP deductible is met; and

– The individual cannot be claimed as a tax dependent on another individual’s federal personal income tax return

3

Note: Ineligibility only affects my ability to make or receive HSA contributions. It does not affect my

ability to use existing HSA funds (assuming properly made).

HSA Eligibility – The Basic Premise

Marsh & McLennan Agency LLC 4

What is a Qualified

High Deductible Health Plan?

5

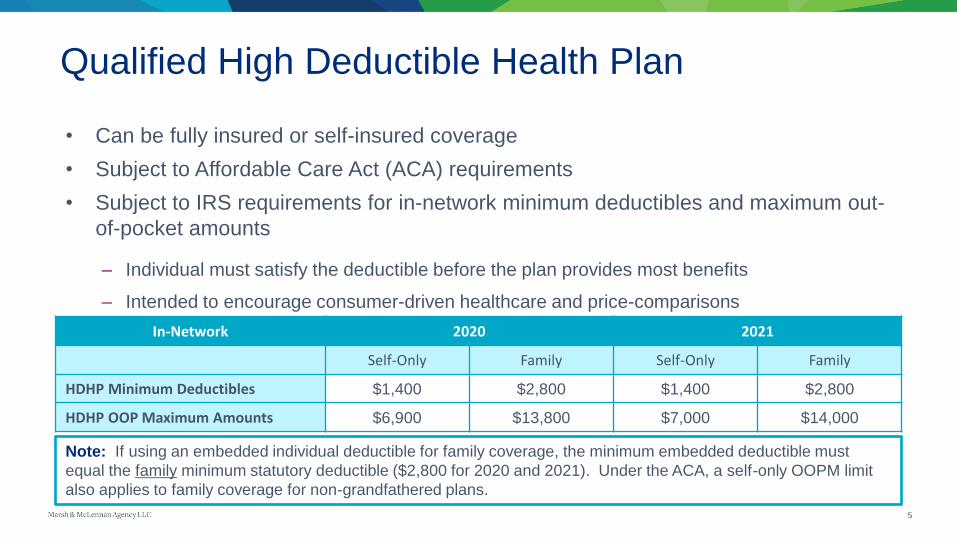

• Can be fully insured or self-insured coverage

• Subject to Affordable Care Act (ACA) requirements

• Subject to IRS requirements for in-network minimum deductibles and maximum out-

of-pocket amounts

– Individual must satisfy the deductible before the plan provides most benefits

– Intended to encourage consumer-driven healthcare and price-comparisons

In-Network 2020 2021

Self-Only Family Self-Only Family

HDHP Minimum Deductibles $1,400 $2,800 $1,400 $2,800

HDHP OOP Maximum Amounts $6,900 $13,800 $7,000 $14,000

Note: If using an embedded individual deductible for family coverage, the minimum embedded deductible must

equal the family minimum statutory deductible ($2,800 for 2020 and 2021). Under the ACA, a self-only OOPM limit

also applies to family coverage for non-grandfathered plans.

Qualified High Deductible Health Plan

Marsh & McLennan Agency LLC

• Preventive care (addressed in more detail on following slides)

• Disease management, EAP, and wellness if they do not provide significant

medical care

• Workers’ compensation or medical payments from property/casualty

coverage

• Specified disease or illness coverage

• Fixed indemnity coverage for hospitalization

• Accident, disability, dental, vision, or long-term care

6

Permitted Other Care/Coverage

7

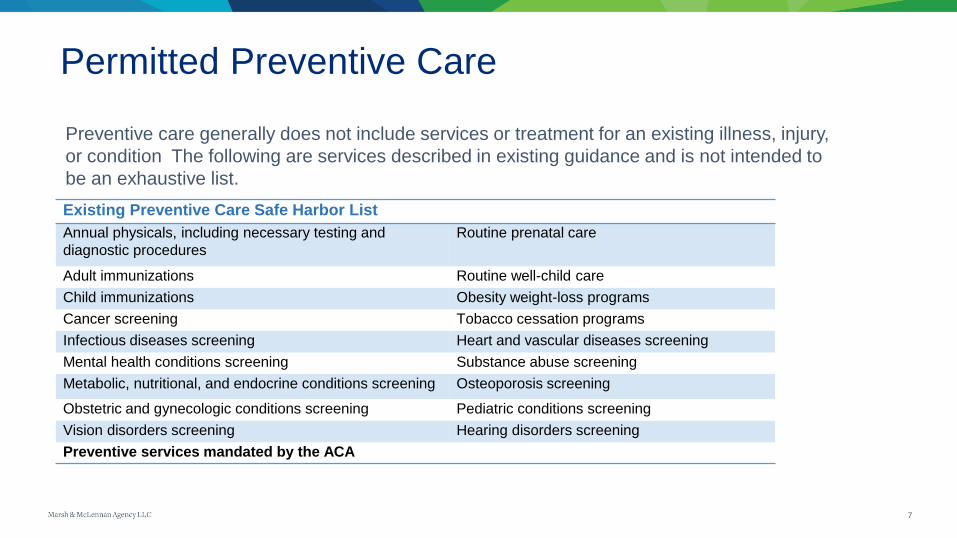

Preventive care generally does not include services or treatment for an existing illness, injury,

or condition The following are services described in existing guidance and is not intended to

be an exhaustive list.

Existing Preventive Care Safe Harbor List

Annual physicals, including necessary testing and

diagnostic procedures

Routine prenatal care

Adult immunizations Routine well-child care

Child immunizations Obesity weight-loss programs

Cancer screening Tobacco cessation programs

Infectious diseases screening Heart and vascular diseases screening

Mental health conditions screening Substance abuse screening

Metabolic, nutritional, and endocrine conditions screening Osteoporosis screening

Obstetric and gynecologic conditions screening Pediatric conditions screening

Vision disorders screening Hearing disorders screening

Preventive services mandated by the ACA

Permitted Preventive Care

8

IRS Notice 2019-45 permits – but does not require – HDHPs to cover the following additional

services as preventive on or after July 17, 2019. This list is exhaustive.

Services for Specified Conditions* For Individuals Diagnosed with

Angiotensin Converting Enzyme (ACE) inhibitors Congestive heart failure, diabetes, and/or coronary

artery disease

Anti-resorptive therapy Osteoporosis and/or osteopenia

Beta-blockers Congestive heart failure and/or coronary artery disease

Blood pressure monitor Hypertension

Inhaled corticosteroids Asthma

Insulin and other glucose lowering agents Diabetes

Retinopathy screening Diabetes

Peak flow meter Asthma

Glucometer Diabetes

Hemoglobin A1c testing Diabetes

International Normalized Ration (INR) testing Liver disease and/or bleeding disorders

Low-density Lipoprotein (LDL) testing Heart disease

Selective Serotonin Reuptake Inhibitors (SSRIs) Depression

Statins Heart disease and/or diabetes

Expansion of Permitted Preventive Care

9

IRS Notice 2020-15, 2020-29 (COVID-19 Testing and Treatment)

• HDHPs may provide coverage for COVID-19 testing, treatment, and items purchased related to

testing and treatment before an individual satisfies the minimum statutory deductible

– Testing and treatment includes diagnostic testing for influenza A & B, norovirus and other coronaviruses, and RSV

• Applies from January 1, 2020

IRS Notice 2020-29 (Telemedicine)

• HSA-eligibility is not affected by telemedicine (whether or not services are COVID-19 related or

otherwise excepted)

• Relief effective as of January 1, 2020 and continues through the end of plan years that begin

on or before December 31, 2021

– For example, this can last through June 30, 2022 for a plan year that began July 1, 2021

COVID-19 ReliefCOVID-19 Relief

Marsh & McLennan Agency LLC 10

No Other Disqualifying Coverage

Marsh & McLennan Agency LLC

• Health care flexible spending accounts (HCFSAs) and health reimbursement

arrangements (HRAs) that can reimburse for medical expenses are

generally disqualifying other coverage

– If employee’s spouse has general purpose HCFSA or HRA coverage, it disqualifies the employee

– It doesn’t matter if the employee submits any claims for reimbursement or not…it’s the ability to do so that matters

11

Spending Accounts

Marsh & McLennan Agency LLC

1. Offer a limited-purpose HCFSA or HRA that may only be used to

reimburse dental and vision expenses; or

2. Offer a post-deductible HCFSA or HRA that only reimburses general

medical expenses after the individual has met the minimum statutory

annual HDHP deductible; or

3. Combine the two

12

Note: The minimum statutory annual HDHP deductible might be less than the HDHP’s annual

deductible. For example, the 2020 minimum individual statutory deductible is $1,400, while an

HDHP’s 2020 individual deductible might be set at $1,800.

HCFSAs & HRAs – HSA Compatibility

Marsh & McLennan Agency LLC

• Run-Out Period – the time period a participant has after the end of the plan year to submit claims that were incurred during the plan year

• Grace Period – the time period a participant has after the end of the plan year to submit claims that were incurred during the plan year OR during the grace period

– COVID-19 relief allowed an extended grace period for plan years and/or grace periods than ended during 2020 until December 31, 2020

• Carryover Provision – provision permits participants to carry over the lesser of:

– The unspent HCFSA account balance as of the end of the plan year; or

– 20% of the overall HCFSA salary reduction limit (indexed by IRS Notice 2020-33 and is $550 from a 2020 plan year to a 2021 plan year)

13

HCFSA Design Considerations

COVID-19

Relief

Marsh & McLennan Agency LLC

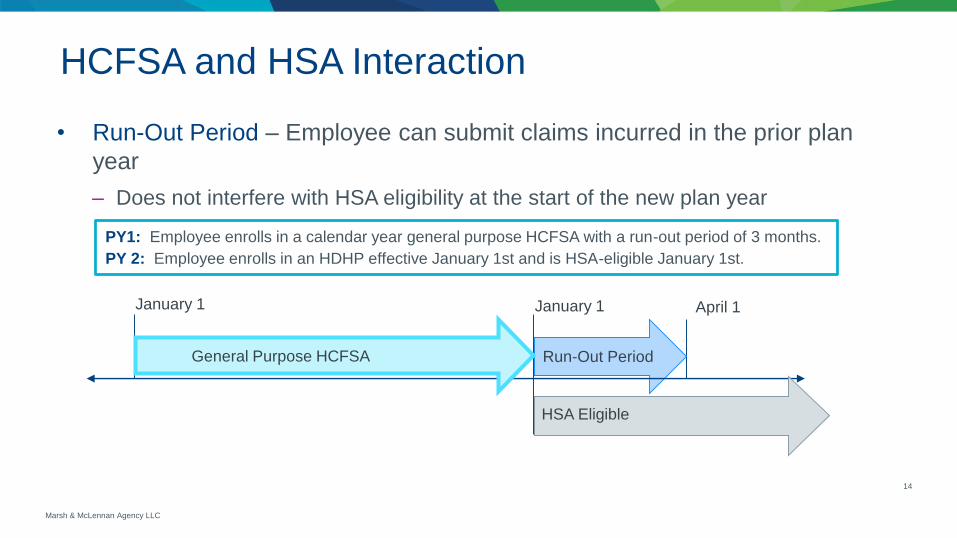

• Run-Out Period – Employee can submit claims incurred in the prior plan

year

– Does not interfere with HSA eligibility at the start of the new plan year

14

Run-Out Period

January 1 January 1 April 1

General Purpose HCFSA

HSA Eligible

PY1: Employee enrolls in a calendar year general purpose HCFSA with a run-out period of 3 months.

PY 2: Employee enrolls in an HDHP effective January 1st and is HSA-eligible January 1st.

HCFSA and HSA Interaction

Marsh & McLennan Agency LLC

• Grace Period – Employee has $0 HCFSA balance at the end of plan year

– Does not interfere with HSA eligibility

15

Grace Period

January 1 January 1 April 1

General Purpose HCFSA

HSA Eligible

PY1: Employee enrolls in a calendar year general purpose HCFSA with a grace period of 2 ½ months.

Employee’s HCFSA balance on December 31st is $0.

PY 2: Employee enrolls in an HDHP effective January 1st and is HSA-eligible on January 1st.

HCFSA and HSA Interaction

Marsh & McLennan Agency LLC

• Grace Period – Employee has HCFSA balance at the end of the plan year

– Interferes with HSA eligibility until the first of the month following the grace period

HSA Eligible

Grace Period

January 1 January 1 April 1

General Purpose HCFSA

16

PY1: Employee enrolls in a calendar year general purpose HCFSA with a grace period of 2 ½ months.

Employee has an HCFSA balance on December 31st.

PY 2: Employee enrolls in an HDHP effective January 1st and is HSA-eligible on April 1st.

HCFSA and HSA Interaction

Marsh & McLennan Agency LLC

• Carryover – Employee can carry over dollars to a general purpose HCFSA,

and HCFSA does not allow for carryover to a limited purpose HCFSA or

waiver of the carryover

– Interferes with HSA eligibility for the entire year

January 1 January 1

General Purpose HCFSA Carryover to GP HCFSA

No HSA Eligibility

17

PY1: Employee enrolls in a calendar year general purpose HCFSA with a carryover feature. HCFSA does not

allow carryover to limited purpose HCFSA or waiver of carryover.

PY 2: Employee enrolls in an HDHP effective January 1st and is HSA-ineligible for the entire year if the

employee has a carryover.

HCFSA and HSA Interaction

Marsh & McLennan Agency LLC

• Carryover – Employee can carry over dollars to a limited purpose HCFSA

– Does not interfere with HSA eligibility

January 1 January 1

General Purpose HCFSA Carryover to LP HCFSA

HSA Eligible

18

PY1: Employee enrolls in a calendar year general purpose HCFSA with a carryover feature to a

limited purpose HCFSA.

PY 2: Employee enrolls in an HDHP effective January 1st and is HSA-eligible for the entire year.

HCFSA and HSA Interaction

Marsh & McLennan Agency LLC

• Carryover – Employee can carry over dollars to a general purpose HCFSA,

but the HCFSA allows the employee to waive the carryover

– Does not interfere with HSA eligibility for the entire year if employee waives the carry over

January 1 January 1

General Purpose HCFSA

HSA Eligible

19

PY1: Employee enrolls in a calendar year general purpose HCFSA with a carryover provision. Employer gives

the employee the opportunity to waive the carryover.

PY 2: Employee waives the carryover, enrolls in an HDHP effective January 1st, and is HSA-eligible for the entire

year.

HCFSA and HSA Interaction

Marsh & McLennan Agency LLC

• Medicare – An individual who is actually enrolled in Medicare has

disqualifying other coverage for the first month Medicare coverage is

effective (mere eligibility is not a conflict)

• Medicaid – An individual enrolled in Medicaid has disqualifying other

coverage for the first month Medicaid coverage is effective

• TRICARE – An individual enrolled in TRICARE has disqualifying other

coverage for the first month TRICARE coverage is effective

20

Medicare, Medicaid, and TRICARE

Marsh & McLennan Agency LLC

If not limited to permitted care or after the HDHP deductible is met (unrealistic),

the issue is whether these provide “significant medical care”

• Clinics – Unless limited to first aid, dental/vision (unlikely), or preventive services,

these will generally cause an HSA conflict unless participants pay the fair market

value (FMV) for the services

• EAPs – These generally escape due to low visit limits

• Telemedicine – This is generally an issue unless participants

pay FMV (remember temporary COVID-19 relief applies)

– There is some “magic” to $45/visit (it’s the Medicare reimbursement rate)

21

Note: While some still claim the EAP exception applies to telemedicine, this is a myth. An employer

could increase its HSA seeding contribution as an offset.

Clinics, EAPs, and Telemedicine

COVID-19

Relief

Marsh & McLennan Agency LLC

• VA Medical Benefits – Generally disqualifying coverage for the month in

which VA medical benefits are received and the 2 months thereafter

– This conflict does not apply for care received in connection with a service-related disability

January 1

VA Conflict

HSA Eligible

March 1 June 1

HSA Eligible

22

Example: Employee is covered by an HSA-qualified HDHP. Employee receives VA medical benefits unrelated to

a service-related disability in March.

Veterans Affairs (VA) Benefits

Marsh & McLennan Agency LLC 23

What is a

Health Savings Account?

• A health savings account (HSA) is an individually owned account

that receives tax advantages

Earnings in the HSA are not

included in gross income

Tax-Free Growth

2

Employees put pre-tax dollars

into an HSA up to a statutory

cap, lowering the employees’

income subject to federal

taxes

Pre-Tax Contributions

1

24

Code Section 213(d) qualified

medical expenses, including

preventive care per 2019

Regulations

Tax-Free Distributions

3

Note: An individual could also contribute directly to the bank/trustee after-tax and take a tax deduction on his or her

federal personal income tax return using IRS Form 8889. This is an above-the-line deduction.

The HSA Triple-Tax Advantage

Marsh & McLennan Agency LLC 25

Contributions: Putting Money In

Distributions: Taking Money Out

26

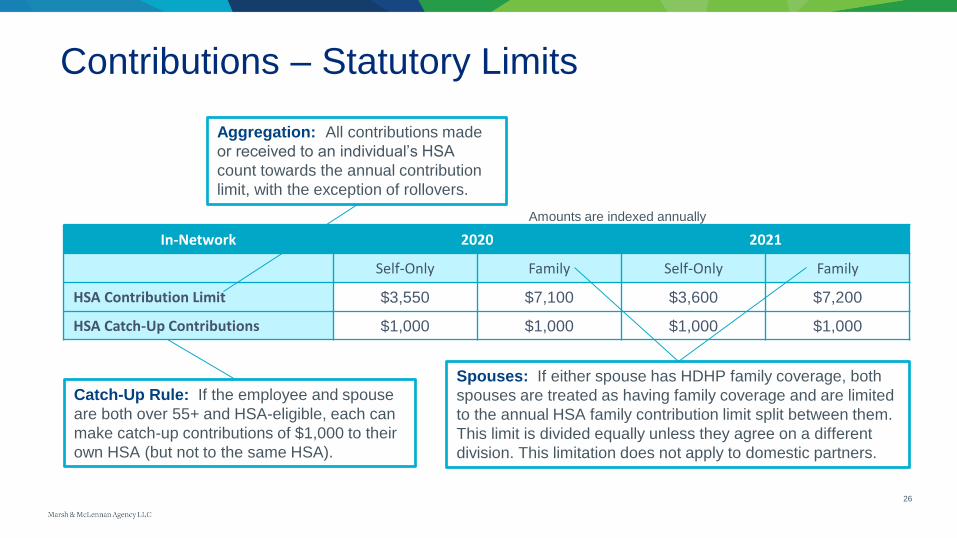

Amounts are indexed annually

Aggregation: All contributions made

or received to an individual’s HSA

count towards the annual contribution

limit, with the exception of rollovers.

Catch-Up Rule: If the employee and spouse

are both over 55+ and HSA-eligible, each can

make catch-up contributions of $1,000 to their

own HSA (but not to the same HSA).

Spouses: If either spouse has HDHP family coverage, both

spouses are treated as having family coverage and are limited

to the annual HSA family contribution limit split between them.

This limit is divided equally unless they agree on a different

division. This limitation does not apply to domestic partners.

In-Network 2020 2021

Self-Only Family Self-Only Family

HSA Contribution Limit $3,550 $7,100 $3,600 $7,200

HSA Catch-Up Contributions $1,000 $1,000 $1,000 $1,000

Contributions – Statutory Limits

Marsh & McLennan Agency LLC

MonthApplicable Annual Individual

or Family HSA Limit (2020)

January $7,100

February $7,100

March $7,100

April $3,550

May $3,550

June $3,550

July $3,550

August $3,550

September $3,550

October $3,550

November $3,550

December $3,550

Example: Employee is enrolled in family

coverage for all of January through March and

in employee-only coverage for all of April

through December. The blended annual HSA

contribution limit would be determined by:

27

Total for all 12 months =

$53,250Step1

Annual HSA Contribution Limit:

$53,250/12 = $4,437.50Step 2

Switching Tiers of HDHP Coverage

28

Question: Employee is enrolled in family coverage in a qualified HDHP. The spouse is enrolled in

Medicare. Is the employee allowed to contribute the family maximum?

Answer: Yes, the contribution limit is determined by the tier in which the employee is enrolled. It is

not relevant that any enrolled spouse or dependent be HSA eligible. It is not even relevant that the

individuals qualify as the employee’s tax dependent(s), although the employee cannot use an HSA

for tax free reimbursements for a non-tax dependent. If a spouse is HSA-ineligible, the spouse

cannot contribute to his/her own HSA.

In-Network 2020 2021

Self-Only Family Self-Only Family

HSA Contribution Limit $3,550 $7,100 $3,600 $7,200

HSA Catch-Up Contributions $1,000 $1,000 $1,000 $1,000

Amounts are indexed annually

Contributions – Medicare Entitlement (Enrollment)

29

Contribution limits

• Generally pro-rated monthly with eligibility determined as of the first day each month

• Employees can change their HSA contributions at least once a month without the need for a

qualifying life event (subject to what can be reasonably administered)

Last Month Rule

• If an individual is HSA eligible on December 1st, the individual can make or receive contributions

up to the full annual limit provided the individual remains HSA eligible through the end of the

following calendar year

• If HSA eligibility is lost during this period, the individual’s annual HSA contribution limit is

retroactively pro-rated monthly which usually leads to adverse tax consequences

Employee Contributions

30

“Must be present to win”

• Consider imposing a time limit on employees establishing an HSA to receive HSA

contributions

• Employer can stagger employer contributions and limit them to participants as of

that date (e.g. annually, quarterly)

Determine form of employer HSA seeding contributions

• Fixed based on tier?

• Matching?

Employer Contributions

31

Communicate HSA eligibility basics to employees

Tax Code nondiscrimination rules

• If employees can contribute pre-tax through cafeteria plan, employer contributions are also

deemed to be made through cafeteria plan and Tax Code Section 125 nondiscrimination rules

apply

• Otherwise, employer contributions are subject to HSA comparability rules which will require

uniform contributions by tier of coverage

• Problem if HSA contributions (employee and employer) disproportionately favor highly

compensated employees

• Matching contributions somewhat more likely to lead to disproportionate contributions without

relatively low cap on match

Other Considerations

Marsh & McLennan Agency LLC

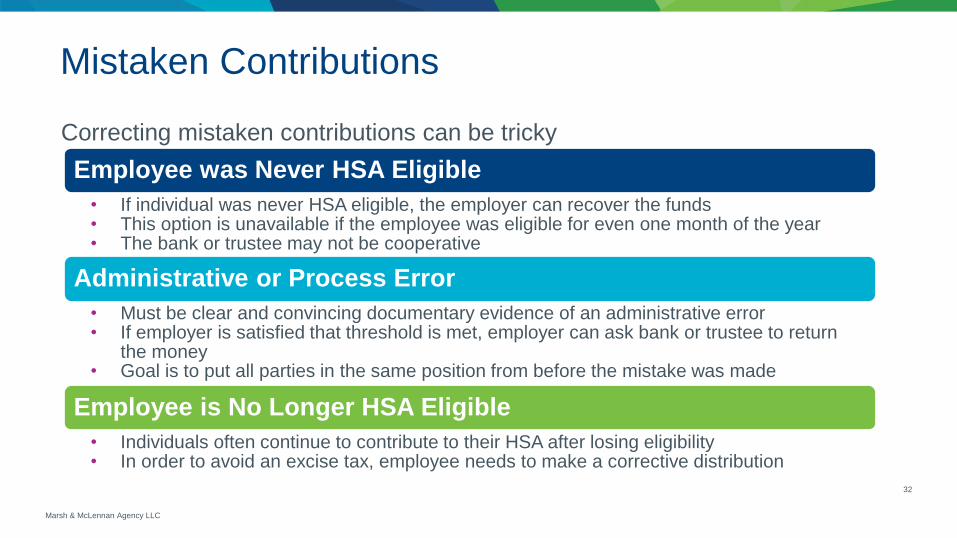

Correcting mistaken contributions can be tricky

32

Employee was Never HSA Eligible

• If individual was never HSA eligible, the employer can recover the funds• This option is unavailable if the employee was eligible for even one month of the year• The bank or trustee may not be cooperative

Administrative or Process Error

• Must be clear and convincing documentary evidence of an administrative error• If employer is satisfied that threshold is met, employer can ask bank or trustee to return

the money• Goal is to put all parties in the same position from before the mistake was made

Employee is No Longer HSA Eligible

• Individuals often continue to contribute to their HSA after losing eligibility• In order to avoid an excise tax, employee needs to make a corrective distribution

Mistaken Contributions

Marsh & McLennan Agency LLC

• Excess contributions are subject to a 6% excise tax

– This includes amounts made by employee and employer that were unable to be recouped

• In order to avoid the excise tax, the employee needs to take a corrective

distribution

– An individual can avoid a 6% excise tax if he or she receives a taxable distribution of any excess contributions (plus earnings) before his or her individual federal income tax deadline (plus extensions) for the year of the excess contribution

– The individual should notify the bank or trustee of the need for a corrective distribution

33

Excess Contributions

• Employee can receive distributions from the HSA even if not eligible to make or

receive additional contributions (i.e. not HSA eligible)

• Tax free distributions are limited to qualifying medical expenses for the account

holder, spouse, and tax dependents

– Excludes most domestic partners

– Excludes most adult children (this is different from ACA standard)

• Qualifying medical expenses include COBRA, deductible medical coverage for those

65+, coverage while receiving unemployment, and long-term care

• Distributions for non-qualifying medical expenses are included in the individual’s

taxable income and are subject to a 20% penalty (no penalty if account holder is

65+)

34

Distributions

Questions?

35

MarshMMA.com

This document is not intended to be taken as advice regarding any individual situation and should not be relied upon as such. Marsh & McLennan Agency LLC shall have no obligation to update this publication and shall have no liability to you

or any other party arising out of this publication or any matter contained herein. Any statements concerning actuarial, tax, accounting or legal matters are based solely on our experience as consultants and are not to be relied upon as

actuarial, accounting, tax or legal advice, for which you should consult your own professional advisors. Any modeling analytics or projections are subject to inherent uncertainty and the analysis could be materially affected if any underlying

assumptions, conditions, information or factors are inaccurate or incomplete or should change. Copyright © 2020 Marsh & McLennan Insurance Agency LLC. All rights reserved. CA Insurance Lic: 0H18131. MarshMMA.com