202 0 Final Rating Report - FMDQ Group

23

Eat N' Go Limited 2020 Final Rating Report

Transcript of 202 0 Final Rating Report - FMDQ Group

Eat N' Go Limited

2020 Final Rating Report

The copyright of this document is reserved by Agusto & Co. Limited. No matter contained herein may be reproduced, duplicated or copied by any means whatsoever without the prior written consent of Agusto & Co. Limited. Action will be taken against companies or individuals who ignore this warning. The information contained in this document has been obtained from published financial statements and other sources which we consider to be reliable but do not guarantee as such. The opinions expressed in this document do not represent investment or other advice and should therefore not be construed as such. The circulation of this document is restricted to whom it has been addressed. Any unauthorized disclosure or use of the information contained herein is prohibited.

2019 Corporate Rating Report

2020 Corporate Rating Review Report

Eat N’ Go Limited

Rating Assigned:

Bbb- This refers to a company with satisfactory financial condition and adequate capacity to

meet obligations as and when they fall due.

Outlook: Stable

Issue Date: 17 February 2021

Expiry Date: 30 June 2021

Previous Rating: Bbb

Industry: Quick Service

Restaurant

Outline Page Rating Rationale 1

Company Profile 5

Financial Condition 9

Ownership, Mgt. & Staff 14

Outlook 17

Financial Summary 18

Rating Definition 20

Analysts:

Tolulope Obideyi [email protected]

Isaac Babatunde [email protected]

Agusto & Co. Limited

UBA House (5th Floor)

57, Marina

Lagos

Nigeria

www.agusto.com

RATING RATIONALE Agusto & Co. hereby reviews the rating assigned to Eat N’ Go Limited (“Eat N’ Go”,

“ENG” or “the Company”) to “Bbb-“. The assigned rating reflects the Company’s high

leverage profile, rising inflationary pressures on input raw materials and operating

costs, as well as the high finance cost leading to low profitability. Also, the rating

reflects the frail consumer purchasing power and shrinking income wallet, the weak

macroeconomic environment coupled with the adverse impact of COVID-19 pandemic

on the general economy and the Quick Service Restaurant Industry in particular.

However, the rating is supported by ENG’s satisfactory financial condition, evidenced

by good cash flow, adequate working capital and qualified and experienced

management team. This is in addition to ENG’s strong leadership position in the Quick

Service Restaurant (QSR) Industry in Nigeria, strong international brand franchise,

coupled with its innovative technology solutions to drive sales.

Eat N’ Go Limited, a wholly-owned subsidiary of Krone Holding Inc1, a leading player

in the QSR Industry in Nigeria, with operations in over 112 retail outlets across nine

states in the Country and processes over 4 million orders per annum. Eat N’ Go has the

sole and exclusive franchise rights with Domino’s Pizza International for its pizza food

chain (Domino’s Pizza) and Kahala Brands LLC, for its ice cream (Cold Stone Creamery)

and dairy products (Pinkberry) in Nigeria, with the right of first refusal for Cold Stone

Creamery and Pinkberry regarding expansion into the rest of West Africa.

In 2019, the Company’s revenue grew by 28% year-on-year to ₦16.9 billion, while cost

of sales stood at ₦6.9 billion, and translated to a cost of sales to revenue ratio of 41.2%

(FY 2018: 40.2%). During the 2019 financial year, operating expenses to revenue

improved marginally to 56.5% (FY 2018:58.1%), while operating profit margin also

etched higher at 2.4%, up from 1.7% in the prior year. However, interest expense to

revenue rose to 9.2% from 3.8% on the back of the ₦11.5 billion bond issuance in the

prior year and resulted in a pre-tax loss of ₦1.06 billion. Subsequent to 2019-year end,

the Company’s performance remained impacted especially in the Cold Stone Creamery

1 Krone Holding Inc is a limited liability company incorporated in the British Virgin Islands for the purpose of holding and operating

franchise rights.

2 2020 Corporate Rating Review Report

Eat N’ Go Limited

Eat N’ Go Limited

and Pinkberry segments owing to the COVID-19 induced lockdown. However, ENG’s

market position was largely sustained by the performance of the Domino’s Pizza

business segment2, which relied heavily on technology in taking and delivering

customer orders, following the imposition of social distancing rules by the Federal

Government. Consequently, the Company’s unaudited financial statements for the nine

months ended 30 September 2020 revealed a 3.2% dip in revenue compared to the

corresponding period in 2019. In addition, the Company renegotiated some of its

existing concessions, while ensuring reduction in wastages in a bid to sustain gross

and operating margins. However, interest expenses to revenue ratio rose markedly to

12% in Q3’ 2019, leading to a loss after tax. Similar to FYE 2019, ENG’s profitability

indicators such as pre-tax return on assets and pre-tax return on equity remained in

the negative territory.

In FY 2019, ENG’s operating cash flow (OCF) grew by 107% to ₦4.9 billion from the

prior year on the back of rise in other creditors and accruals, largely the recognition of

lease liabilities in line with IFRS 16. Eat N’ Go’s OCF was sufficient to cover returns to

providers of finance wholly comprising interest payments in the period. In addition,

ENG’s OCF as a percentage of returns to providers of finance of 312% and OCF to sales

ratio of 28.7% in FY 2019 were both better than our benchmarks, depicting a good cash

flow position.

As at 31 December 2019, the Company’s interest-bearing liabilities (IBL) rose by 4.2

times to ₦13 billion from the prior year, due to the receipt of ₦11.5 billion bond

proceeds from Eat & Go Finance SPV Plc (wholly owned subsidiary of ENG). Although

ENG’s interest coverage of 10 times is considered to be good, the interest expense to

revenue ratio of 9.2%, interest-bearing debt (net of cash) as a percentage of equity of

168% and net liabilities to total assets of 94%, are all significantly higher than our

benchmarks and reflect a high leverage profile.

The Company enjoys favourable terms of trade with its customers (sales are

predominantly on cash basis) and suppliers on account of its strong position in the

Quick Service Restaurant Industry in Nigeria. Thus, ENG’s spontaneous financing was

sufficient to cover working assets and translated to a short-term financing surplus of

₦4.8 billion. As at year end, ENG’s long-term funds were adequate to finance long term

assets, resulting in a long-term financing surplus of ₦2.3 billion. Overall, Eat N’ Go

recorded a working capital surplus of ₦7.1 billion as at 31 December 2019.

In view of the COVID-19 pandemic as well as the sustained social distancing rule,

coupled with the likelihood of further restrictions on the movement of human and

2 Domino’s pizza is the Company’s largest business segment, accounting for 57% of revenue

3 2020 Corporate Rating Review Report

Eat N’ Go Limited

Eat N’ Go Limited

material resources due to the rising second wave of the pandemic, management plans

to intensify the adoption of technology in taking customer orders, particularly in the

domino’s pizza segment which accounts for the bulk of the Company’s revenue3.

Management has also disclosed that additional 18 retail outlets, mainly in Lagos State,

will be completed and opened before end of FY 2020, which will bring ENG’s total

stores to 130. Most of these stores were already under construction until the COVID-

19 pandemic and lockdown which stalled construction activities and subsequent

commencement of the outlets. In addition, plans are on-going to ensure that other cost

optimising initiatives being implemented by the Company are sustained in the near

term.

Going forward, Agusto & Co. expects a rise in ENG’s revenue, supported by the

anticipated increase in the number of retail outlets in the near term. Notwithstanding

our expectation of an improvement in revenue, we believe that ENG’s high interest

expense will remain a drag on the Company’s performance in the short to medium

term.

We expect working capital to remain adequate due to the long-term funding obtained

through bond issuance in the period. However, we believe that leverage metrics will

remain high, propelled by ENG’s high finance cost associated with the bond issuance.

Nonetheless, Eat N’ Go’s continued favourable terms of trade with suppliers will ensure

that cash flow remains good in the near term. Furthermore, we believe that the

adoption of digital advertising and marketing strategies will increase the brand

awareness in the short to medium term and also reduce operating expenses as

traditional media platforms are being substituted with online media campaigns at

lower cost. Overall, we believe that Nigeria’s large and growing population coupled

with the change in eating patterns in urban centres where the Company’s outlets are

situated presents growth opportunities for the Company. In addition, the inclusion of

Nigerian variant in the domino’s pizza segment such as beef suya pizza, chicken suya

pizza, meat pie pizza,and bbq beef, including smaller sized pizzas at relatively low

prices will support the demand for ENG’s products in the near term.

Based on the aforementioned, Agusto & Co. hereby attaches a stable outlook to the

rating of Eat N’ Go Limited. Nonetheless, we remain concerned about the performance

of the Company as the COVID-19 pandemic lingers. Therefore, we have included

negative rating triggers which will adversely impact the Company’s rating if they are

breached in the near term.

3 In February 2021, ENG launched the online ordering platform in the Cold Stone Creamery and Pinkberry segments

4 2020 Corporate Rating Review Report

Eat N’ Go Limited

Eat N’ Go Limited

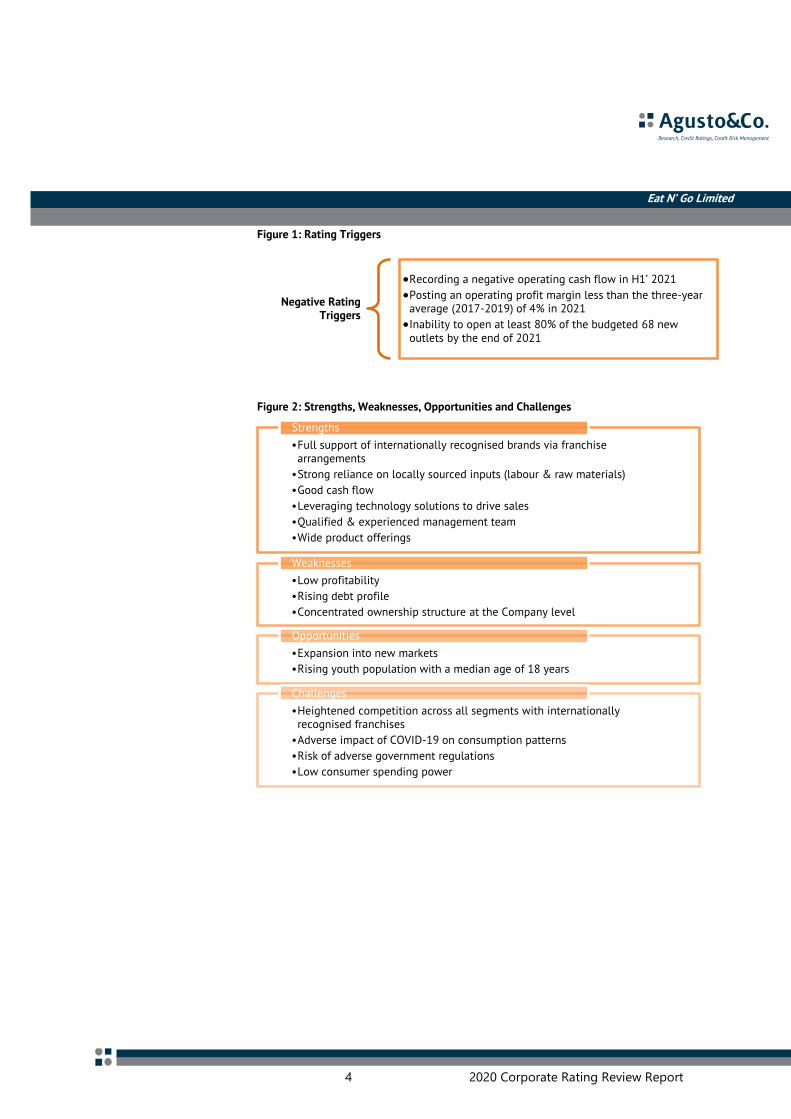

Figure 1: Rating Triggers

Figure 2: Strengths, Weaknesses, Opportunities and Challenges

•Full support of internationally recognised brands via franchise arrangements

•Strong reliance on locally sourced inputs (labour & raw materials)

•Good cash flow

•Leveraging technology solutions to drive sales

•Qualified & experienced management team

•Wide product offerings

Strengths

•Low profitability

•Rising debt profile

•Concentrated ownership structure at the Company level

Weaknesses

•Expansion into new markets

•Rising youth population with a median age of 18 years

Opportunities

•Heightened competition across all segments with internationally recognised franchises

•Adverse impact of COVID-19 on consumption patterns

•Risk of adverse government regulations

•Low consumer spending power

Challenges

Negative Rating Triggers

•Recording a negative operating cash flow in H1’ 2021

•Posting an operating profit margin less than the three-year average (2017-2019) of 4% in 2021

•Inability to open at least 80% of the budgeted 68 new outlets by the end of 2021

5 2020 Corporate Rating Review Report

Eat N’ Go Limited

Eat N’ Go Limited

PROFILE OF EAT N’ GO LIMITED Overview and Background

Eat N’ Go Limited (“ENG”, “the Company” or “Eat N’ Go”) was incorporated in Nigeria in 2011 as a limited liability

company and commenced operations in August 2012. The Company’s principal activity includes the provision

of affordable food and drink.

Eat N’ Go operates through exclusive long-term franchises with three international brands - Domino's Pizza,

Cold Stone Creamery and Pinkberry Frozen Yoghurt:

Domino’s Pizza (“Domino’s”)

This is the food restaurant chain and food delivery segment of Eat ‘N’ Go. Domino’s product offerings include

pizzas, chicken, bread and fries among others. Dominos operates through a chain of 52 stores across various

locations in Nigeria. Domino’s is a franchisee of Domino's Pizza, Inc, an American multinational pizza restaurant

chain founded in 1961. Domino's Pizza, Inc. is a dominant player in global pizza delivery, operating a chain of

17,200 stores in more than 90 countries, with an estimated daily sale of three million pizzas.

Cold Stone Creamy (“Cold Stone”)

This is the dairy products and drinks segment of Eat ‘N’ Go. Cold Stone’s menu includes ice creams, milk shakes,

ice cream cakes and cupcakes. The business segment has about 51 stores across nine states in Nigeria.

Coldstone is a franchisee of Cold Stone Creamery, an American ice cream parlor chain with headquarter in

Scottsdale, Arizona. The Brand whose main product is premium ice cream is owned and operated by Kahala

Brands. Other products offered by the brand includes ice cream-related products, such as ice cream cakes, pies,

cookie sandwiches, smoothies, shakes and iced or blended coffee drinks. The brand operates in over 1,000

locations in the United States and in nearly 30 international markets.

The Pinkberry Frozen Yoghurt

The business segment enjoys the support of the global Pinkberry brand and franchise. The flagship frozen

yoghurt segment was introduced by Eat N’ Go in 2018. Pinkberry’s product offerings include tart frozen

yoghurt, frozen yoghurt smoothies and Greek yoghurt smoothies with a variety of toppings. Pinkberry operates

through a chain of nine stores located in Lagos, Abuja and Port-Harcourt. The Pinkberry brand is a franchise of

frozen dessert restaurants headquartered in Scottsdale, Arizona. The brand operates through a chain of 260

stores in over 20 countries.

In the near term, Eat N’ Go plans to become the premier food operator in Africa by leveraging technology to

drive the sale of its diverse food offerings and beverage brands.

6 2020 Corporate Rating Review Report

Eat N’ Go Limited

Eat N’ Go Limited

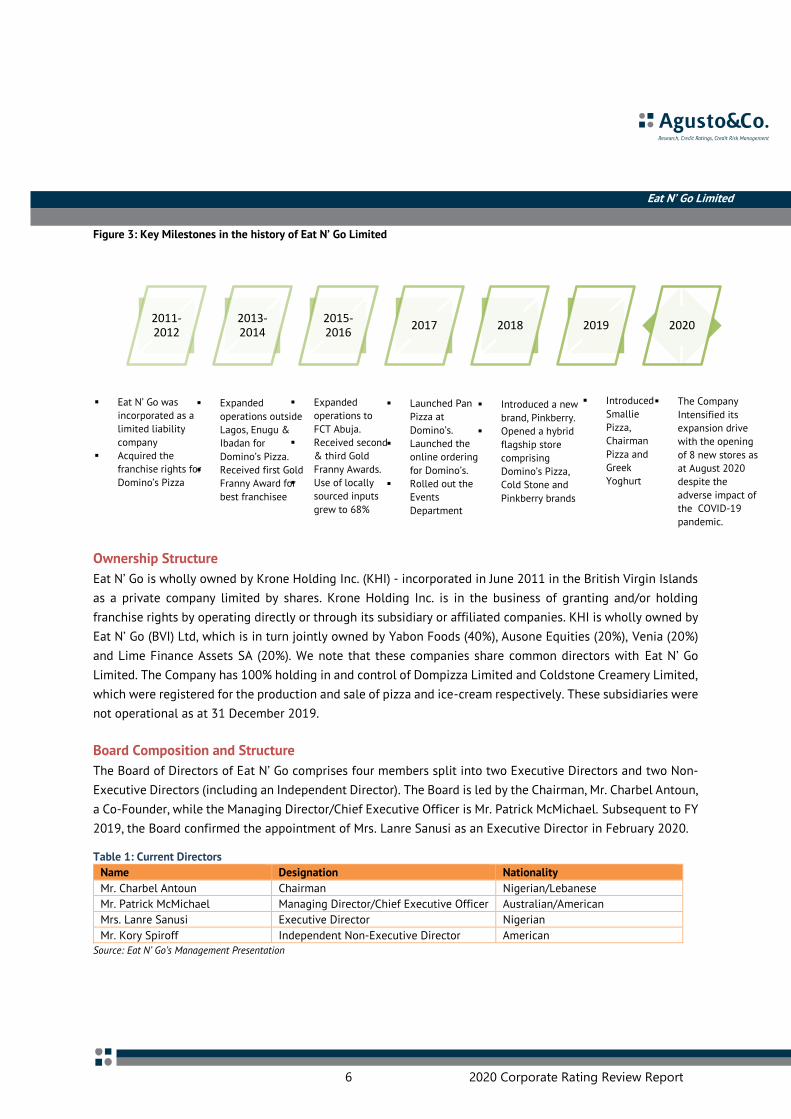

Figure 3: Key Milestones in the history of Eat N’ Go Limited

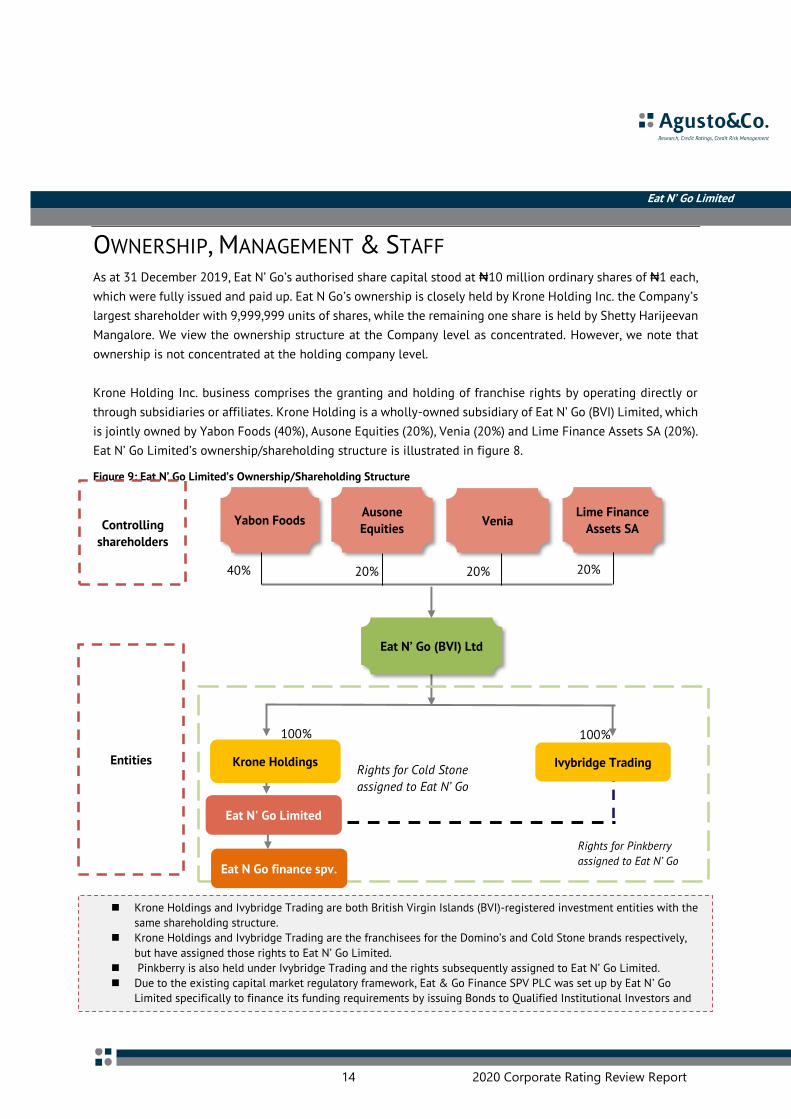

Ownership Structure

Eat N’ Go is wholly owned by Krone Holding Inc. (KHI) - incorporated in June 2011 in the British Virgin Islands

as a private company limited by shares. Krone Holding Inc. is in the business of granting and/or holding

franchise rights by operating directly or through its subsidiary or affiliated companies. KHI is wholly owned by

Eat N’ Go (BVI) Ltd, which is in turn jointly owned by Yabon Foods (40%), Ausone Equities (20%), Venia (20%)

and Lime Finance Assets SA (20%). We note that these companies share common directors with Eat N’ Go

Limited. The Company has 100% holding in and control of Dompizza Limited and Coldstone Creamery Limited,

which were registered for the production and sale of pizza and ice-cream respectively. These subsidiaries were

not operational as at 31 December 2019.

Board Composition and Structure

The Board of Directors of Eat N’ Go comprises four members split into two Executive Directors and two Non-

Executive Directors (including an Independent Director). The Board is led by the Chairman, Mr. Charbel Antoun,

a Co-Founder, while the Managing Director/Chief Executive Officer is Mr. Patrick McMichael. Subsequent to FY

2019, the Board confirmed the appointment of Mrs. Lanre Sanusi as an Executive Director in February 2020.

Table 1: Current Directors

Name Designation Nationality

Mr. Charbel Antoun Chairman Nigerian/Lebanese

Mr. Patrick McMichael Managing Director/Chief Executive Officer Australian/American

Mrs. Lanre Sanusi Executive Director Nigerian

Mr. Kory Spiroff Independent Non-Executive Director American Source: Eat N’ Go’s Management Presentation

▪ Eat N’ Go was

incorporated as a

limited liability

company

▪ Acquired the

franchise rights for

Domino’s Pizza

▪ Expanded

operations outside

Lagos, Enugu &

Ibadan for

Domino’s Pizza.

▪ Received first Gold

Franny Award for

best franchisee

▪ Expanded

operations to

FCT Abuja.

▪ Received second

& third Gold

Franny Awards.

▪ Use of locally

sourced inputs

grew to 68%

▪ Introduced a new

brand, Pinkberry.

▪ Opened a hybrid

flagship store

comprising

Domino’s Pizza,

Cold Stone and

Pinkberry brands

▪ Launched Pan

Pizza at

Domino’s.

▪ Launched the

online ordering

for Domino’s.

▪ Rolled out the

Events

Department

▪ Introduced

Smallie

Pizza,

Chairman

Pizza and

Greek

Yoghurt

▪ The Company

Intensified its

expansion drive

with the opening

of 8 new stores as

at August 2020

despite the

adverse impact of

the COVID-19

pandemic.

202020192018 20172015-2016

2013-2014

2011-2012

7 2020 Corporate Rating Review Report

Eat N’ Go Limited

Eat N’ Go Limited

Operating Structure

Since 2012, Eat N’ Go Limited has grown rapidly from two outlets to 112 outlets as at August 2020 across nine

states. Over the next four years, the Company plans to open circa 220 stores, with a presence in major cities

and towns in Nigeria.

The Company delivers centrally prepared food items (raw materials and packaging products) to various

restaurant outlets through a fleet of eight trucks. Eat N’ Go represents three major brands including Domino’s

Pizza, Cold Stone Creamery and Pinkberry. The Company’s product offerings include pizza, chicken wings,

chicken kickers, ice cream, cakes, smoothies, shakes and yoghurt.

The Company has sole and exclusive franchise rights with Domino’s Pizza International4 (“DPI”) for its pizza

food chain (Domino’s Pizza) and Kahala Brands LLC5, for its ice cream (Cold Stone Creamery) and dairy products

(Pinkberry) in Nigeria. In addition, ENG has the Right of First Refusal for Cold Stone Creamery and Pinkberry

regarding expansion into West Africa. As part of measures to ensure that all products are in strict compliance

with the procedures and global brands, the Company adopts the franchisors as its technical partners, who

provide guidance in the production process and technical fees are paid annually for such services.

The Company operates three Domino’s Pizza commissaries (central kitchens) in Lagos, Abuja and Port Harcourt.

Plans are on-going to open the fourth commissary in Magboro6 (Ogun State) in the near term. The Pizza

commissaries cumulatively process an average of 82 tons of flour, 447,000 dough balls, 7.7 tons of chicken, 10

tons of protein and 50 tons of cheese monthly. Eat N’ Go also operates three Cold Stone Creamery commissaries

- Lagos (established in 2012), Abuja (2015) and Port Harcourt (2019) altogether producing 90 tons of ice cream,

3 tons of mix-in, 9 tons of waffle flour and 3,600 cakes monthly, with plans to complete a fourth commissary

in Ibadan in the near term. As at the end of August 2020, Domino’s Pizza had 52 retail outlets, while Cold Stone

Creamery and Pinkberry Yogurt had 51 and 9 outlets respectively in Nigeria.

Eat N’ Go has a 10-year master franchise license for the Domino’s Pizza brand in Nigeria (which was obtained

in 20117), as well as a 10-year master franchise license for the Cold Stone brand in Nigeria (license is exclusive,

personal, non-transferable and was obtained in 2012, with sub-franchising right obtained in 2013). Kahala

Franchising LLC, which owns the Cold Stone Creamery brand is also the franchisor of the Pinkberry brand to

Eat N’ Go.

Krone Holdings and Ivybridge Trading are BVI registered investment entities, 100% owned by Eat N’ Go Ltd

BVI, an investment vehicle of the four founding shareholders, incorporated and domiciled in the British Virgin

Islands. Both entities are the franchisees for the Domino’s Pizza and Cold Stone brands respectively but have

assigned those rights to Eat N’ Go Limited. The franchise for Pinkberry is also held by Ivybridge Trading and

those rights have also been assigned to ENG.

4 DPI is the recognized world leader in pizza delivery and operates a network of company-owned and franchise-owned stores in international

markets, 5 Kahala Brands LLC is one of the largest holding companies for franchise fast food restaurants in North America. 6 This will replace the Lagos Dominos commissary, which is now over capacity 7 Management has disclosed that discussions are ongoing with regards to the extension of the franchise license for the Domino’s Pizza brand

before the end of Q1’2021

8 2020 Corporate Rating Review Report

Eat N’ Go Limited

Eat N’ Go Limited

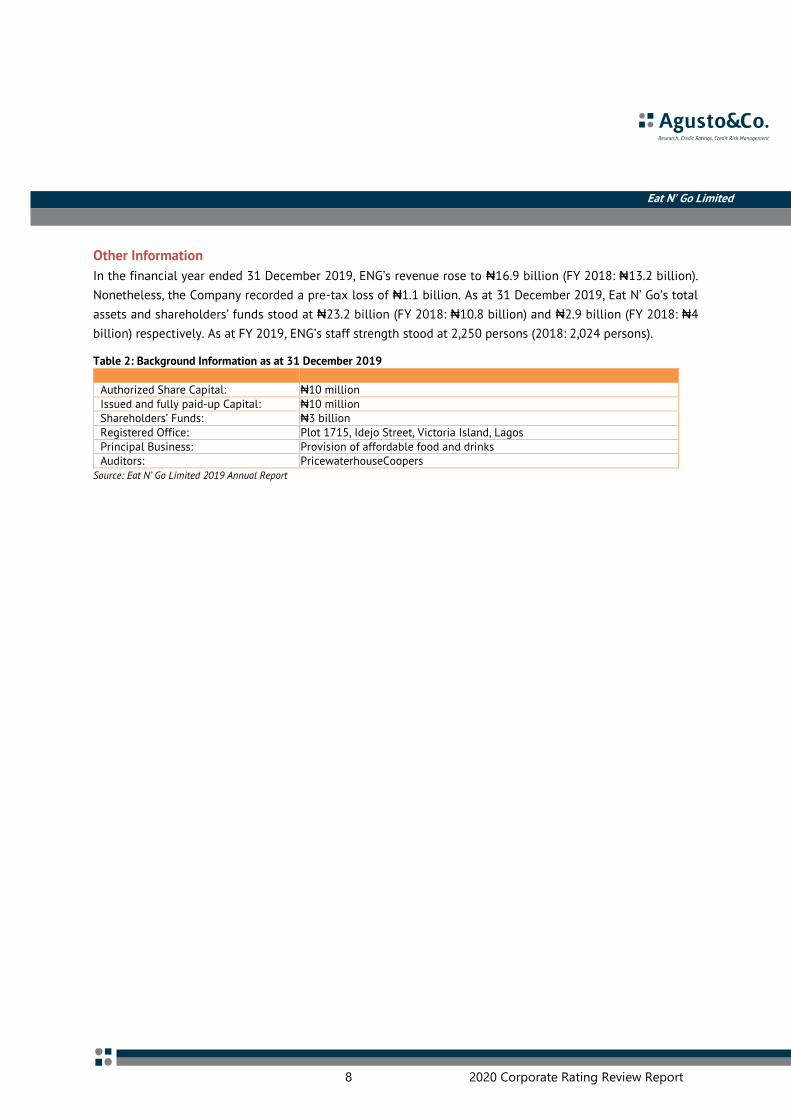

Other Information

In the financial year ended 31 December 2019, ENG’s revenue rose to ₦16.9 billion (FY 2018: ₦13.2 billion).

Nonetheless, the Company recorded a pre-tax loss of ₦1.1 billion. As at 31 December 2019, Eat N’ Go’s total

assets and shareholders’ funds stood at ₦23.2 billion (FY 2018: ₦10.8 billion) and ₦2.9 billion (FY 2018: ₦4

billion) respectively. As at FY 2019, ENG’s staff strength stood at 2,250 persons (2018: 2,024 persons). Table 2: Background Information as at 31 December 2019

Authorized Share Capital: ₦10 million Issued and fully paid-up Capital: ₦10 million Shareholders’ Funds: ₦3 billion Registered Office: Plot 1715, Idejo Street, Victoria Island, Lagos Principal Business: Provision of affordable food and drinks Auditors: PricewaterhouseCoopers

Source: Eat N’ Go Limited 2019 Annual Report

9 2020 Corporate Rating Review Report

Eat N’ Go Limited

Eat N’ Go Limited

FINANCIAL CONDITION ANALYSTS’ COMMENTS

In 2019, Eat N’ Go Finance SPV, wholly owned by Eat N’ Go Limited, issued a ₦11.5 billion bond, which was on-lent

through an intercompany arrangement to ENG to refinance existing debts and fund expansion plans. Due to the

interest bearing nature of the Bond, we have reclassified the intercompany borrowing as an interest bearing liability

for ENG for the period ended 31 December 2019.

PROFITABILITY Eat N’ Go is one of the leading players in the Nigerian quick service restaurant industry, operating 112 stores

across Nigeria. ENG’s primary activities include the sale of pizzas, chicken wings, chicken kickers, pizza bread,

ice cream, cakes, smoothies, shakes, drinks and yoghurt. During the financial year ended 31 December 2019,

Eat N’ Go’s revenue rose by 28% to ₦16.9 billion on account of the rise in sales volume, propelled by the

Company’s expansion drive, following the increase in the number of retail outlets by 20 to 104 in 2019. The

breakdown of Eat N’ Go’s revenue for FY 2019 revealed that Domino's Pizza, the food restaurant and food

delivery chain of the Company remained the main contributor, accounting for 57% of revenue. This is largely

due to the adoption of technology by the business segment which allows customers to place orders through

an online ordering system that also permits customers to track their respective orders. The Coldstone Creamery

and Pinkberry Yoghurt business segment accounted for 40% and 4% respectively of total revenue. This revenue

pattern is similar to the historical trend and we see this subsisting into the future given the brand affinity that

the Dominos Pizza attracts from the upward mobile and youthful population in the country.

Similarly, ENG’s cost of sales to revenue rose to 41.3% from 40.2% in the prior year, propelled by the rise in

the number of operating outlets, coupled with the adverse impact of inflationary pressure on prices of core

input materials such as mozzarella cheese (for Domino’s Pizza) and sweet cream (for Coldstone) which partially

offset the increased revenue. Subsequent to the 2019 financial year, the unaudited financial statements as at

September 2020 revealed a 3.2% decline in revenue compared to the corresponding period in 2019 owing to

the adverse impact of the COVID-19 pandemic. However, cost of sales to revenue ratio improved marginally to

40.9%, following the implementation of cost optimisation initiatives by the Company, which ENG intends to

consolidate going forward. Management disclosed further that the implementation of some revenue-

enhancing initiatives are on-going, largely with respect to diversification of the Company’s products offering

in the near term, which is expected to improve sales in the short to medium term.

During the year under review, operating expenses rose in absolute terms by 24.6%, largely due to an increase

in staff costs, resulting from an increase in the number of persons employed for the new outlets opened in the

period. The recognition of depreciation expense on the right of use assets on account of the adoption of IFRS

16 also contributed to the growth in operating expenses during the 2019 financial year. Nonetheless, operating

expenses to revenue improved marginally to 56.5% (FY 2018: 58.1%) and translated into an increase in the

Company’s operating profit margin to 2.4% from 1.7% in the prior year, though lower than our 6% benchmark

for companies in the QSR Industry. Subsequent to the year-end, ENG continued its cost optimisation strategy

targeted at enhancing operating efficiencies across its stores especially in the wake of the Covid-19 lockdown.

10 2020 Corporate Rating Review Report

Eat N’ Go Limited

Eat N’ Go Limited

Thus, the Company streamlined its staff strength and relied on the sustained adoption of technology in taking

customer orders. Other cost optimising initiatives implemented by ENG includes the adoption of digital

advertising and marketing strategies coupled with the reduction in wastages, which helped moderate

operating expenses.

In the year under review, the Company's other income amounted to ₦0.09 billion, significantly lower than the

₦0.68 billion recorded in the prior-year on account of the one-off write back of ₦0.68 billion relating to the

excess provision for tax related expenses recorded in FY 2018, and represented 0.6% of revenue (FY 2018:

5.1%).

In the same period, ENG’s finance cost rose markedly

by 211% to ₦1.6 billion precipitated by the

interest expense on the ₦11.5 billion bond

issued by Eat N’ Go Finance SPV Plc during the

review year. This translated to an interest

expense to revenue ratio of 9.2%, which is higher

than the three year average (2017-2019) of 5.2%

and also above our benchmark of 5%.

Consequently, ENG reported a pre-tax loss of

₦1.06 billion in FY 2019. Similarly, profitability

indicators dipped to the negative territory, with

a pre-tax return on average assets (ROA) of -

0.01% and pre-tax return on average equity

(ROE) of -30.45%. ENG’s three years (2017-2019)

ROE average of 3% is significantly lower than our

expectation.

In our view, Eat N’Go’s profitability is low and improvement is contingent on moderating the impact of finance

cost through revenue growth in the short to medium term.

2.4%

-30.5%

0.0%

1.7%

11.9%8.2%8.5%

27.6%

13.2%

-40.0%

-30.0%

-20.0%

-10.0%

0.0%

10.0%

20.0%

30.0%

40.0%

OPM ROE ROA2019 2018 2017

Figure 4: Profitability Ratios

11 2020 Corporate Rating Review Report

Eat N’ Go Limited

Eat N’ Go Limited

CASH FLOW Eat N’ Go’s terms of trade with its customers are largely on a cash basis across the various store operated by

the Company. Although the Company’s average trade creditor days dipped to 94 days from 161 days in the

prior year, the Company continued to enjoy favourable terms of trade with its suppliers on account of its strong

leadership position in the QSR Industry in Nigeria.

During the financial year ended 31 December 2019, ENG recorded an operating cash flow (OCF) of ₦4.9 billion

(FY 2018: ₦2.3 billion). The Company’s OCF was sufficient to cover returns to providers of finance (RTPOF) ,

amounting to ₦1.6 billion, mainly interest payment. We note that Eat N’ Go has demonstrated the capacity to

meet its recurring short-term obligations from its operating cash flow over the last three years.

In FY 2019, ENG’s OCF as a percentage of sales

inched up to 28.7%, while the three-year (2017

– 2019) average stood at 20.9%, both are in line

with our expectations. In addition, the

Company’s FY 2019 and three-year (2017 - 2019)

average OCF as a percentage of returns to

providers of financing of 312% and 381%

respectively are also better than our

expectations.

Overall, we consider the Company’s cash flow to

be good.

28.7%

17.8%16.2%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

2019 2018 2017

Figure 5: Operating cash flow to revenue ratio

12 2020 Corporate Rating Review Report

Eat N’ Go Limited

Eat N’ Go Limited

FINANCING STRUCTURE AND ADEQUACY OF WORKING CAPITAL As at 31 December 2019, Eat N’ Go Limited’s working assets stood at ₦2.3 billion, down from ₦2.6 billion in

the prior year. The Company’s working assets are dominated by inventory (principally raw materials) which

accounted for 83% in FY 2019, while other debtors & prepayments and trade debtors represented 16% and 1%

respectively of working assets. The Company’s policy of holding an optimum inventory level of three months

of imported materials and one month for local inputs is to ensure that there is always backup inventory to

meet customer demand in the unlikely event of a disruption in the supply chain of raw materials.

As at 31 December 2019, ENG’s spontaneous financing rose by 67% to ₦7.1 billion, owing to the rise in other

creditors and accruals which accounted for 70% of spontaneous financing. Other components of the Company’s

spontaneous financing include trade creditors (25%) and taxation payable (4%) and amounts due to related

parties (1%). As at the year end, spontaneous financing was sufficient to cover working assets, resulting in a

short term financing surplus of ₦4.8 billion. Agusto & Co. notes positively that ENG has traditionally recorded

short-term financing surpluses over the years due to its strategic operating cycle and business model, where

payments are generally received on a cash-and-carry basis, while suppliers and related parties and other

creditors offer trade credits days. We expect this trend to continue into the foreseeable future.

As at 31 December 2019, Eat N’ Go’s long-term assets stood at ₦12.7 billion, representing a 59% growth from

the prior year. The increase in long-term assets is primarily attributable to the 63% year-on-year rise in

properties, plants and equipment attributed to the increase in the number of retail outlets to 104 in 2019 (FY

2018: 84 outlets) on account of the on-going expansion. As at year end, ENG’s long-term assets comprised

mainly properties, plant and equipment (94%) and intangible assets (6%). As at 31 December 2019, the

Company’s long-term funds of ₦15 billion, which comprised equity (20%) and long term borrowings (80%)

were sufficient to finance the long term assets, resulting in a working capital of ₦2.3 billion. ENG’s available

working capital of ₦2.3 billion combined with its short-term financing surplus of ₦4.8 billion, resulted in an

overall working capital surplus of ₦7.1 billion, which we consider adequate.

In our view, Eat N’ Go’s overall working capital is adequate.

Figure 6: Short term financing surplus (₦’Billion)

Figure 7: Long term financing surplus/ need (₦’Billion)

4.8

1.7

0.8

0.0

1.0

2.0

3.0

4.0

5.0

6.0

2019 2018 2017

2.3

-3.2

-2.1

-4.0

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

2019 2018 2017

13 2020 Corporate Rating Review Report

Eat N’ Go Limited

Eat N’ Go Limited

LEVERAGE

As at 31 December 2019, ENG’s total liabilities stood at ₦20.2 billion, up by 198% from the prior year. The

main components were non-interest-bearing liabilities (35%) and interest-bearing liabilities (65%). The

Company’s non-interest-bearing liabilities (NIBL) were mainly made up of other creditors and accruals (70%),

trade creditors (25%), taxation payable (4%) and amounts due to related parties (1%). The interest-bearing

liabilities (IBL) component rose by 417% to ₦13.1 billion, following the receipt of the ₦11.5 billion Bond

proceed8, which accounts for 87% of IBL, while the outstanding balances on the Bank of Industry’s loan, loans

from related parties and bank overdraft9 accounted for the remaining 13%.

As at year end, Eat N’ Go’s total assets were funded by total liabilities (87%) and shareholders’ funds (13%),

depicting a low equity cushion. Furthermore, ENG’s liabilities as at FY 2019 were predominantly interest

bearing, thus interest-bearing debt (net of cash) as a percentage of equity rose markedly to 168% (FY 2018:

63%), significantly above our benchmark. In addition, the Company’s net liabilities to total assets, which inched

up to 94% from 75% in the prior year is above our benchmark and requires improvement. Nonetheless, we note

that ENG’s interest coverage of 10.4 times (FY 2018: 4.7 times) surpassed our benchmark of 3 times.

On account of the rise in IBL in FY 2019, ENG’s

interest expense to revenue ratio inched up to

9.2%, higher than the three-year average (2017-

2019) of 5.2% and our benchmark of 5%. Agusto

& Co. notes that the increase in the finance cost

will adversely impact the Company’s

performance in the near term, if there are no

substantial improvement in revenue to absorb

the incremental finance cost attributable to the

Bond issuance.

In our opinion, ENG’s leverage is high and requires improvement.

8 Some of ₦11.5 billion Bond proceeds from Eat & Go Finance SPV Plc was deployed in refinancing existing commercial loan obligations, 9 ENG’s bank overdraft has a limit of ₦700 million with a tenor of 1-year with three commercial banks at an average interest rate of 21%

per annum.

Figure 8: Interest expense to Revenue Ratio 9.2%

3.8%

2.7%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

2019 2018 2017

14 2020 Corporate Rating Review Report

Eat N’ Go Limited

Eat N’ Go Limited

OWNERSHIP, MANAGEMENT & STAFF As at 31 December 2019, Eat N’ Go’s authorised share capital stood at ₦10 million ordinary shares of ₦1 each,

which were fully issued and paid up. Eat N Go’s ownership is closely held by Krone Holding Inc. the Company’s

largest shareholder with 9,999,999 units of shares, while the remaining one share is held by Shetty Harijeevan

Mangalore. We view the ownership structure at the Company level as concentrated. However, we note that

ownership is not concentrated at the holding company level.

Krone Holding Inc. business comprises the granting and holding of franchise rights by operating directly or

through subsidiaries or affiliates. Krone Holding is a wholly-owned subsidiary of Eat N’ Go (BVI) Limited, which

is jointly owned by Yabon Foods (40%), Ausone Equities (20%), Venia (20%) and Lime Finance Assets SA (20%).

Eat N’ Go Limited’s ownership/shareholding structure is illustrated in figure 8.

Figure 9: Eat N’ Go Limited’s Ownership/Shareholding Structure

Source: Eat N’ Go Limited’s Management Presentation

100% 100%

Rights for Pinkberry

assigned to Eat N’ Go

40%

Controlling

shareholders

Venia Yabon Foods Ausone

Equities Lime Finance

Assets SA

20% 20%

Eat N’ Go (BVI) Ltd

Entities Krone Holdings Ivybridge Trading

◼ Krone Holdings and Ivybridge Trading are both British Virgin Islands (BVI)-registered investment entities with the

same shareholding structure.

◼ Krone Holdings and Ivybridge Trading are the franchisees for the Domino’s and Cold Stone brands respectively,

but have assigned those rights to Eat N’ Go Limited.

◼ Pinkberry is also held under Ivybridge Trading and the rights subsequently assigned to Eat N’ Go Limited.

◼ Due to the existing capital market regulatory framework, Eat & Go Finance SPV PLC was set up by Eat N’ Go

Limited specifically to finance its funding requirements by issuing Bonds to Qualified Institutional Investors and

High Net worth Individuals(“HNIs”)

Eat N' Go Limited

Rights for Cold Stone

assigned to Eat N’ Go

Eat N Go finance spv.

20%

15 2020 Corporate Rating Review Report

Eat N’ Go Limited

Eat N’ Go Limited

Eat N’ Go has a four-member Board of Directors led by the Chairman, Mr. Charbel Antoun, one of the Company’s

co-founders, two Executive Directors (including the Managing Director/Chief Executive Officer Mr. Patrick

McMichael and Mrs. Lanre Sanusi the Executive Director and Chief Financial Officer) and one Independent

Non-Executive Director.

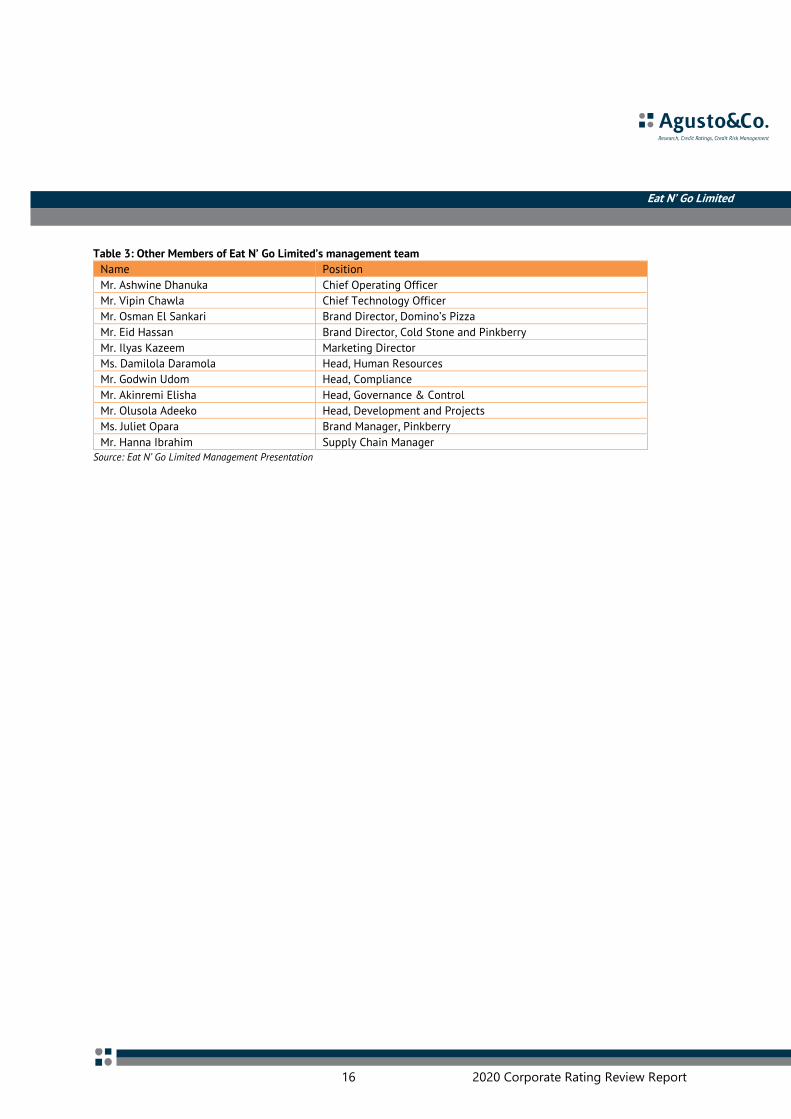

A team of twelve senior management staff with purview over various segments of the business supports the

Chief Executive Officer. During the 2019 financial year, Mr. Godwin Udom was recruited as the Head,

Compliance to provide expert leadership in internal and external compliance-related issues. We note that

members of the management team have relevant experience across various sectors of the economy including

hotel & quick-service restaurants, oil & gas, banking, real estate, marketing and administration. Thus, we

consider the Company’s management team to be qualified and experienced.

As at 31 December, 2019, ENG’s total staff strength rose by 11% to 2,250 employees, mainly due to the

Company’s expansion drive and the increase in the number of retail outlets. The Company’s average cost per

employee amounted to ₦1.4 million, which represented an 8% rise over the prior year. Nonetheless, ENG’s staff

productivity measured by net earnings per staff stood at ₦4.4 million and covered the average cost per

employee 3.3 times (FY 2018: 3.1 times), which we consider to be good.

Management Team

Mr. Patrick McMichael is the Managing Director/Chief Executive Officer of Eat N’ Go Limited. Mr. McMichael’s

experience spans almost three decades. Prior to joining ENG, Mr. McMichael had a long career at the Domino’s

Group, where he served in different capacities ranging from Store Manager to Chief Development and Franchise

Officer. He served as the Chief Executive Officer of Domino’s Pizza, Indonesia between January 2016 and

November 2017, where he oversaw an increase in the store count to 131 from 78 within a year, while improving

the company’s EBITDA to 11.4% from 5.8%. Mr. McMichael also served as the Chief Operating Officer of Retail

Zoo, the owners of multiple brands such as Boot Juice, Salsas Fresh Mex and CIBO Espresso.

He graduated from the Santa Barbara City College in California where he studied Hotel, Restaurant and Culinary

in 1991.

Mrs. Lanre Sanusi served as ENG’s Chief Financial Officer during the review year and was subsequently

appointed to the Board in February 2020. She has over 26 years work experience in the financial, healthcare,

QSR and agricultural sector. Prior to her appointment, she served as a Finance Director in various multinational

and private equity-backed companies including International Finance Corporation (IFC), SwissRe and Helios

Investment Partners UK. She also served as the Group CFO and Executive Director of Hygeia Nigeria Limited.

Mrs Sanusi holds a bachelor’s degree in Accounting from the University of Lagos and a Master of Business

Administration (MBA) from the Imperial College University, London. She is also a Fellow of the Institute of

Chartered Accountants of Nigeria.

16 2020 Corporate Rating Review Report

Eat N’ Go Limited

Eat N’ Go Limited

Table 3: Other Members of Eat N’ Go Limited’s management team

Name Position

Mr. Ashwine Dhanuka Chief Operating Officer

Mr. Vipin Chawla Chief Technology Officer

Mr. Osman El Sankari Brand Director, Domino’s Pizza

Mr. Eid Hassan Brand Director, Cold Stone and Pinkberry

Mr. Ilyas Kazeem Marketing Director

Ms. Damilola Daramola Head, Human Resources

Mr. Godwin Udom Head, Compliance

Mr. Akinremi Elisha Head, Governance & Control

Mr. Olusola Adeeko Head, Development and Projects

Ms. Juliet Opara Brand Manager, Pinkberry

Mr. Hanna Ibrahim Supply Chain Manager Source: Eat N’ Go Limited Management Presentation

17 2020 Corporate Rating Review Report

Eat N’ Go Limited

Eat N’ Go Limited

OUTLOOK Despite the adverse macro-economic environment, significant growth opportunities exist for players in the

Nigerian Quick Service Restaurant Industry, propelled by the rising urbanisation, changing consumers' taste

and preferences and income level. Eat N’ Go recorded a year-on-year increase in revenue owing to the

Company’s expansion drive. As part of measures to maintain ENG’s strong leadership in the Quick Service

Restaurant (QSR) Industry, the Company intensified its expansion drive subsequent to the 2019 financial year

with the opening of additional eight outlets as at August 2020 despite the adverse impact of the COVID-19

pandemic. ENG plans to set up eighteen more outlets before 31 December 2020, which will bring the total

outlets to 130 with presence in nine states. The Company is also implementing other revenue-enhancing

initiatives including; the expansion of its product offering, following the planned introduction of new products

in H1’2021, as well as the on-going construction of a new commissary in the outskirts of Lagos State, which

will increase ENG’s capacity to serve its teeming customers in Lagos and neighbouring states. We believe that

the implementation of these initiatives will fuel revenue growth in the medium term.

Notwithstanding the 28% revenue growth in 2019, ENG’s profitability indicators dipped to the negative

territory, owing to the ₦1.6 billion interest expense on the ₦11.5 billion bond issued by Eat N’ Go Finance SPV

Plc (wholly owned subsidiary of ENG) in the period. Agusto & Co believes that Eat N’ Go’s profitability will

remain pressured in the near term on account of finance cost associated with the bond obligation, except there

is a significant improvement in revenue to absorb the higher interest obligation. However, we believe that

lifestyle changes elicited by the advent of the COVID-19 pandemic will support the sustained technological

adoption, which in our opinion will further moderate the Company’s operating expenses in the short to medium

term.

Going forward, we expect profitability to remain low in the near term, on the back of high-interest expense,

coupled with higher inflationary pressures on operating costs. We believe that the Company’s cash flow will

remain good, owing to the favourable terms of trade with customers (predominantly on cash basis), as well as

suppliers. In our opinion, ENG’s leverage metrics will remain high due to low equity cushion as well as high

interest expense to revenue ratio, while we expect working capital to remain adequate on account of the

injection of long term funds into the business.

Based on the aforementioned, we have attached a stable outlook to the rating of Eat N’ Go Limited. However,

we note that the Company’s rating could be adversely impacted if the COVID-19 pandemic lingers and

economic activities remain tepid.

18 2020 Corporate Rating Review Report

Eat N’ Go Limited

Eat N’ Go Limited

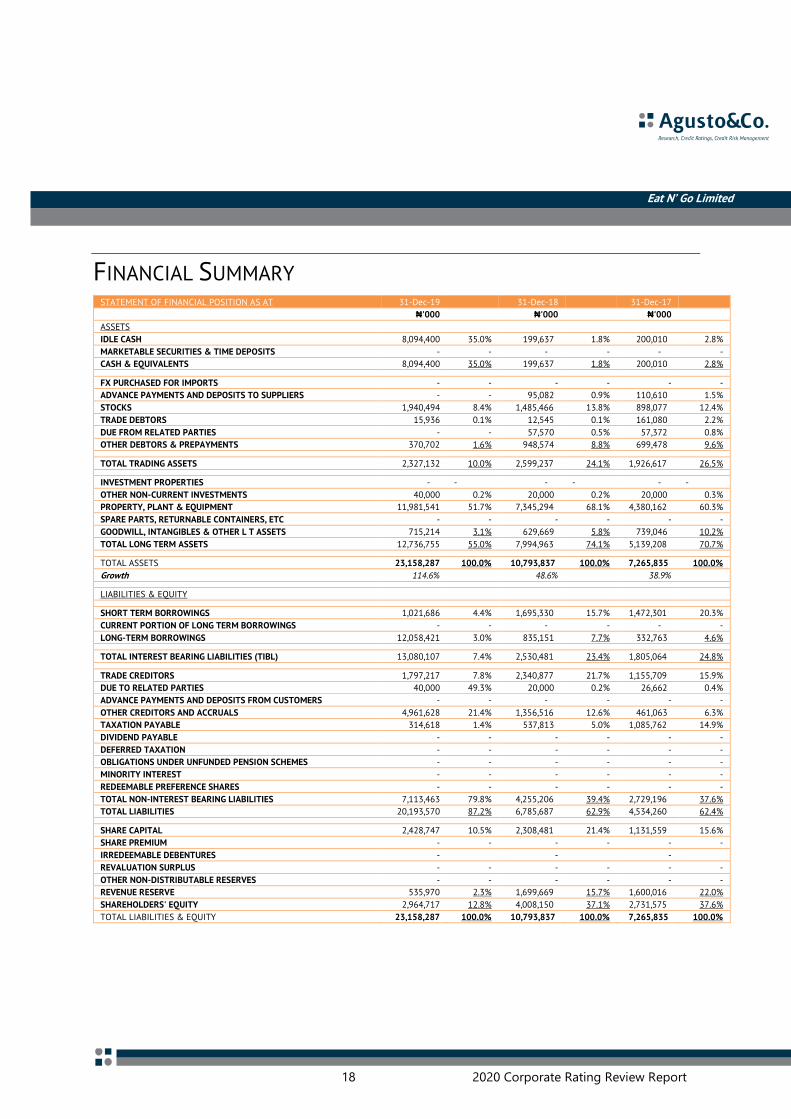

FINANCIAL SUMMARY STATEMENT OF FINANCIAL POSITION AS AT 31-Dec-19

31-Dec-18

31-Dec-17

₦'000

₦'000

₦'000

ASSETS

IDLE CASH 8,094,400 35.0% 199,637 1.8% 200,010 2.8%

MARKETABLE SECURITIES & TIME DEPOSITS - - - - - -

CASH & EQUIVALENTS 8,094,400 35.0% 199,637 1.8% 200,010 2.8%

FX PURCHASED FOR IMPORTS - - - - - -

ADVANCE PAYMENTS AND DEPOSITS TO SUPPLIERS - - 95,082 0.9% 110,610 1.5%

STOCKS 1,940,494 8.4% 1,485,466 13.8% 898,077 12.4%

TRADE DEBTORS 15,936 0.1% 12,545 0.1% 161,080 2.2%

DUE FROM RELATED PARTIES - - 57,570 0.5% 57,372 0.8%

OTHER DEBTORS & PREPAYMENTS 370,702 1.6% 948,574 8.8% 699,478 9.6%

TOTAL TRADING ASSETS 2,327,132 10.0% 2,599,237 24.1% 1,926,617 26.5%

INVESTMENT PROPERTIES - - - - - -

OTHER NON-CURRENT INVESTMENTS 40,000 0.2% 20,000 0.2% 20,000 0.3%

PROPERTY, PLANT & EQUIPMENT 11,981,541 51.7% 7,345,294 68.1% 4,380,162 60.3%

SPARE PARTS, RETURNABLE CONTAINERS, ETC - - - - - -

GOODWILL, INTANGIBLES & OTHER L T ASSETS 715,214 3.1% 629,669 5.8% 739,046 10.2%

TOTAL LONG TERM ASSETS 12,736,755 55.0% 7,994,963 74.1% 5,139,208 70.7%

TOTAL ASSETS 23,158,287 100.0% 10,793,837 100.0% 7,265,835 100.0%

Growth 114.6%

48.6%

38.9%

LIABILITIES & EQUITY

SHORT TERM BORROWINGS 1,021,686 4.4% 1,695,330 15.7% 1,472,301 20.3%

CURRENT PORTION OF LONG TERM BORROWINGS - - - - - -

LONG-TERM BORROWINGS 12,058,421 3.0% 835,151 7.7% 332,763 4.6%

TOTAL INTEREST BEARING LIABILITIES (TIBL) 13,080,107 7.4% 2,530,481 23.4% 1,805,064 24.8%

TRADE CREDITORS 1,797,217 7.8% 2,340,877 21.7% 1,155,709 15.9%

DUE TO RELATED PARTIES 40,000 49.3% 20,000 0.2% 26,662 0.4%

ADVANCE PAYMENTS AND DEPOSITS FROM CUSTOMERS - - - - - -

OTHER CREDITORS AND ACCRUALS 4,961,628 21.4% 1,356,516 12.6% 461,063 6.3%

TAXATION PAYABLE 314,618 1.4% 537,813 5.0% 1,085,762 14.9%

DIVIDEND PAYABLE - - - - - -

DEFERRED TAXATION - - - - - -

OBLIGATIONS UNDER UNFUNDED PENSION SCHEMES - - - - - -

MINORITY INTEREST - - - - - -

REDEEMABLE PREFERENCE SHARES - - - - - -

TOTAL NON-INTEREST BEARING LIABILITIES 7,113,463 79.8% 4,255,206 39.4% 2,729,196 37.6%

TOTAL LIABILITIES 20,193,570 87.2% 6,785,687 62.9% 4,534,260 62.4%

SHARE CAPITAL 2,428,747 10.5% 2,308,481 21.4% 1,131,559 15.6%

SHARE PREMIUM - - - - - -

IRREDEEMABLE DEBENTURES -

-

-

REVALUATION SURPLUS - - - - - -

OTHER NON-DISTRIBUTABLE RESERVES - - - - - -

REVENUE RESERVE 535,970 2.3% 1,699,669 15.7% 1,600,016 22.0%

SHAREHOLDERS' EQUITY 2,964,717 12.8% 4,008,150 37.1% 2,731,575 37.6%

TOTAL LIABILITIES & EQUITY 23,158,287 100.0% 10,793,837 100.0% 7,265,835 100.0%

19 2020 Corporate Rating Review Report

Eat N’ Go Limited

Eat N’ Go Limited

STATEMENT OF COMPREHENSIVE INCOME 31-Dec-19

31-Dec-18

31-Dec-17

₦'000

₦'000

₦'000

TURNOVER 16,934,410 100.0% 13,200,982 100.0% 10,722,295 100.0%

COST OF SALES (6,973,876) -41.2% (5,302,940) -40.2% (3,888,273) -36.3%

GROSS PROFIT 9,960,534 58.8% 7,898,042 59.8% 6,834,022 63.7%

OTHER OPERATING EXPENSES (9,559,626) -56.5% (7,672,062) -58.1% (5,922,213) -55.2%

OPERATING PROFIT 400,908 2.4% 225,980 1.7% 911,809 8.5%

OTHER INCOME/(EXPENSES) 95,636 0.6% 677,078 5.1% 2,786 0.0%

PROFIT BEFORE INTEREST & TAXATION 496,544 2.9% 903,058 6.8% 914,595 8.5%

INTEREST EXPENSE (1,558,254) -9.2% (500,677) -3.8% (286,838) -2.7%

PROFIT BEFORE TAXATION (1,061,710) -6.3% 402,381 3.0% 627,757 5.9%

TAX (EXPENSE) BENEFIT (92,693) -0.5% (302,728) -2.3% 289,633 2.7%

PROFIT AFTER TAXATION (1,154,403) -6.8% 99,653 0.8% 917,390 8.6%

NON-RECURRING ITEMS (NET OF TAX) -

-

-

MINORITY INTERESTS IN GROUP PAT -

-

-

PROFIT AFTER TAX & MINORITY INTERESTS (1,154,403) -6.8% 99,653 0.8% 917,390 8.6%

DIVIDEND -

-

-

PROFIT RETAINED FOR THE YEAR (1,154,403) -6.8% 99,653 0.8% 917,390 8.6%

SCRIP ISSUES -

-

-

OTHER APPROPRIATIONS/ ADJUSTMENTS (9,296)

-

-

PROFIT RETAINED B/FWD 1,699,669 - 1,600,016

682,626

PROFIT RETAINED C/FWD 535,970

1,699,669

1,600,016

ADDITIONAL INFORMATION 31-Dec-19

31-Dec-18

31-Dec-17

Staff costs (₦'000) 3,050,361

2,532,598

1,641,253

Average number of staff 2,250

2,024

1,443

Staff costs per employee (₦'000) 1,356

1,251

1,137

Staff costs/Turnover 18.0%

19.2%

15.3%

Capital expenditure (₦'000) 5,987,905

3,961,222

2,085,226

Depreciation expense - current year (₦'000) 1,332,397

891,704

598,531

(Profit)/Loss on sale of assets (₦'000) -

-

-

Number of 50 kobo shares in issue at year end ('000) 4,857,494

4,616,962

2,263,118

Market value per share of 50 kobo (year end) -

-

-

Market capitalisation (₦'000) -

-

-

Market/Book value multiple -

-

-

Non-operating assets at balance sheet date (₦'000) 40,000

20,000

20,000

Market value of tradeable assets (₦'000)

Revaluation date - Investment properties

Revaluation date - Other properties

Average age of depreciable assets (years) 2

2

2

Sales at constant prices - base year 1985 (₦'000) 51,925

40,478

36,640

Auditors PwC

PwC

PwC

Opinion CLEAN

CLEAN

CLEAN

20 2020 Corporate Rating Review Report

Eat N’ Go Limited

Eat N’ Go Limited

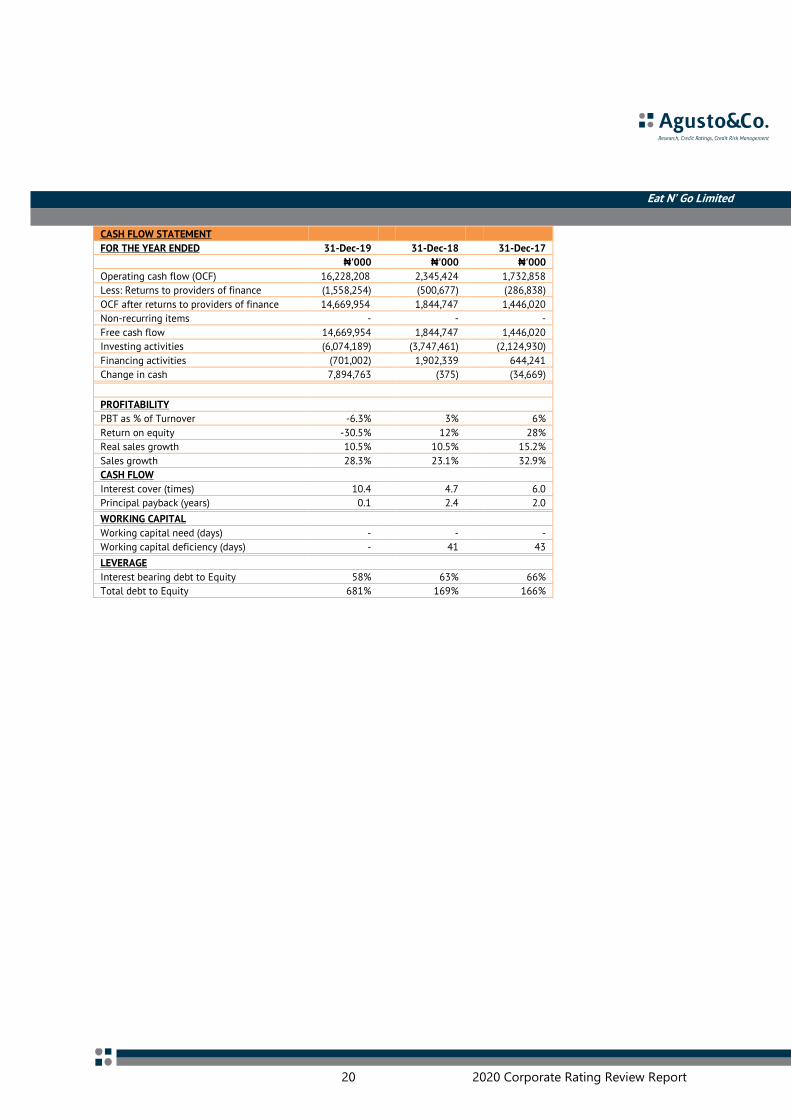

CASH FLOW STATEMENT

FOR THE YEAR ENDED 31-Dec-19

31-Dec-18

31-Dec-17 ₦'000

₦'000

₦'000

Operating cash flow (OCF) 16,228,208

2,345,424

1,732,858

Less: Returns to providers of finance (1,558,254)

(500,677)

(286,838)

OCF after returns to providers of finance 14,669,954

1,844,747

1,446,020

Non-recurring items -

-

-

Free cash flow 14,669,954

1,844,747

1,446,020

Investing activities (6,074,189)

(3,747,461)

(2,124,930)

Financing activities (701,002)

1,902,339

644,241

Change in cash 7,894,763

(375)

(34,669)

PROFITABILITY

PBT as % of Turnover -6.3%

3%

6%

Return on equity -30.5%

12%

28%

Real sales growth 10.5%

10.5%

15.2%

Sales growth 28.3%

23.1%

32.9%

CASH FLOW

Interest cover (times) 10.4

4.7

6.0

Principal payback (years) 0.1

2.4

2.0 WORKING CAPITAL

Working capital need (days) -

-

-

Working capital deficiency (days) -

41

43 LEVERAGE

Interest bearing debt to Equity 58%

63%

66%

Total debt to Equity 681%

169%

166%

21 2020 Corporate Rating Review Report

Eat N’ Go Limited

Eat N’ Go Limited

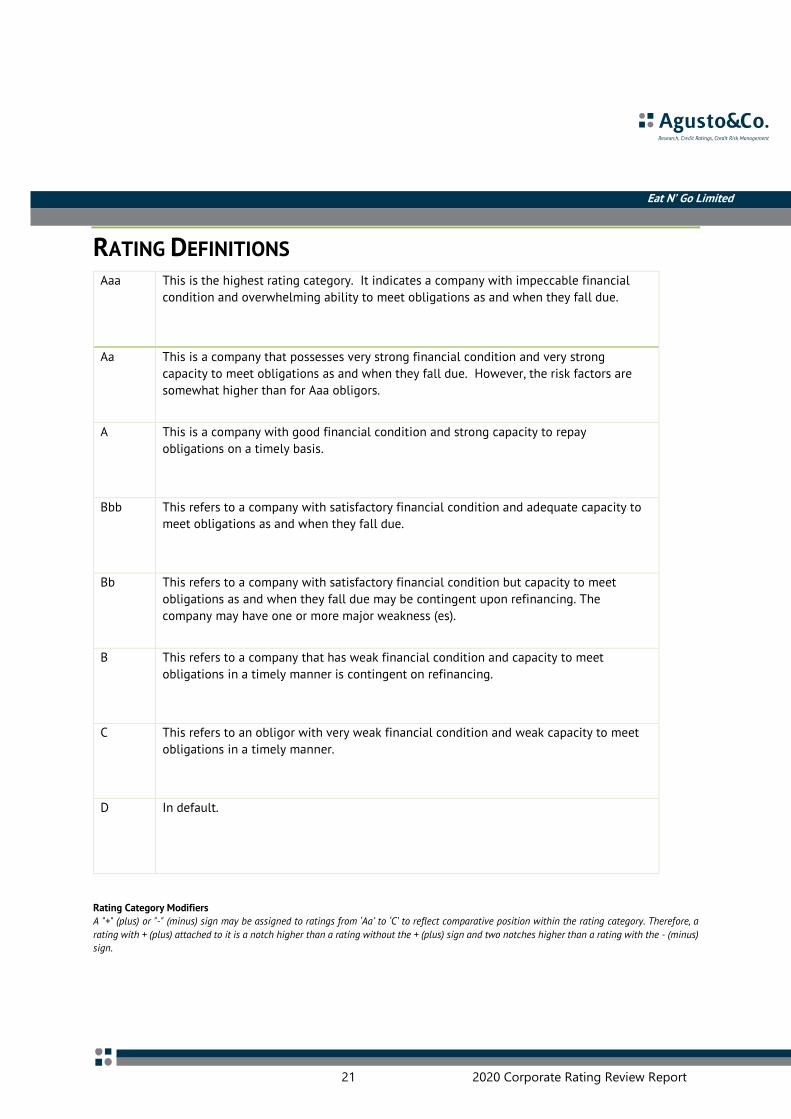

RATING DEFINITIONS Aaa This is the highest rating category. It indicates a company with impeccable financial

condition and overwhelming ability to meet obligations as and when they fall due.

Aa This is a company that possesses very strong financial condition and very strong

capacity to meet obligations as and when they fall due. However, the risk factors are

somewhat higher than for Aaa obligors.

A This is a company with good financial condition and strong capacity to repay

obligations on a timely basis.

Bbb This refers to a company with satisfactory financial condition and adequate capacity to

meet obligations as and when they fall due.

Bb This refers to a company with satisfactory financial condition but capacity to meet

obligations as and when they fall due may be contingent upon refinancing. The

company may have one or more major weakness (es).

B This refers to a company that has weak financial condition and capacity to meet

obligations in a timely manner is contingent on refinancing.

C This refers to an obligor with very weak financial condition and weak capacity to meet

obligations in a timely manner.

D In default.

Rating Category Modifiers

A "+" (plus) or "-" (minus) sign may be assigned to ratings from ‘Aa’ to ‘C’ to reflect comparative position within the rating category. Therefore, a

rating with + (plus) attached to it is a notch higher than a rating without the + (plus) sign and two notches higher than a rating with the - (minus)

sign.

www.agusto.com

© Agusto&Co.

UBA House (5th Floor)

57 Marina Lagos

Nigeria.

P.O Box 56136 Ikoyi

+234 (1) 2707222-4

+234 (1) 2713808

Fax: 234 (1) 2643576

Email: [email protected]