2019 CONTAINER SHIPPING OUTLOOK...Liner Carrier EBIT/Operating Profit 2010-2018 in Million USD...

43

TOC As i a – April 2019 © Sea-Intelligence Maritime Analysis 1 Alan Murphy CEO and Founder Sea-Intelligence April 9 th , 2019 TOC Asia 2019 CONTAINER SHIPPING OUTLOOK

Transcript of 2019 CONTAINER SHIPPING OUTLOOK...Liner Carrier EBIT/Operating Profit 2010-2018 in Million USD...

TOC As ia – April 2019© Sea-Intelligence Maritime Analysis

1

Alan MurphyCEO and Founder

Sea-Intelligence

April 9th, 2019TOC Asia

2019 CONTAINER SHIPPING OUTLOOK

TOC As ia – April 2019© Sea-Intelligence Maritime Analysis

Sea-Intelligence

2

Container Shipping Analysts

- Founded January 6th, 2011

- Fully independent, private company with no interests from brokers, banks or others.

- 10 Analysts, Developers & Consultants in Copenhagen, Bucharest and Singapore.

- 3-person Management Team with 60 years of experience in Container Shipping

Core values:

- Integrity

- Methodology

- Assumptions

- Data Quality

Major Milestones:

- 1,000+ Research & Analysis articles published since March 2011

- 5,000+ citations in Industry Press (Lloyd’s List, JoC, etc.)

- World’s most comprehensive database on Carrier Reliability

- Complete overview of all deep-sea networks and deployment

- Curriculum provider at the World Maritime University

- Curriculum provider at the Blue MBA at Copenhagen Business School

TOC As ia – April 2019© Sea-Intelligence Maritime Analysis

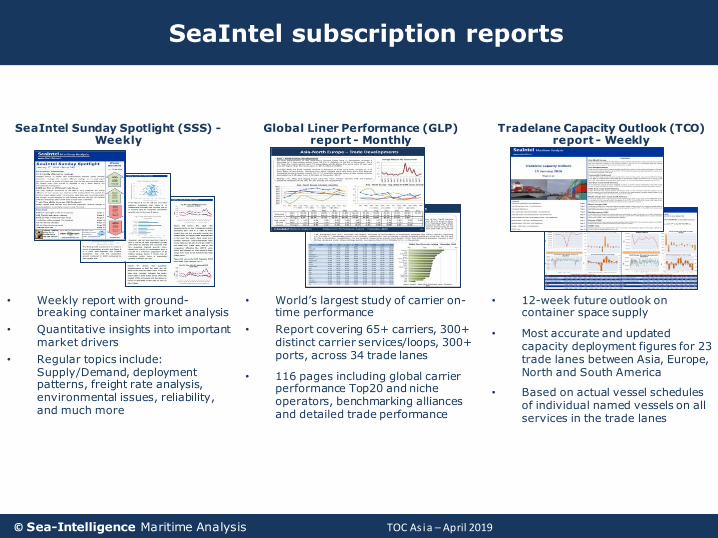

SeaIntel Sunday Spotlight (SSS) -Weekly

Global Liner Performance (GLP) report - Monthly

Tradelane Capacity Outlook (TCO) report - Weekly

• Weekly report with ground-breaking container market analysis

• Quantitative insights into important market drivers

• Regular topics include: Supply/Demand, deployment patterns, freight rate analysis, environmental issues, reliability, and much more

• World’s largest study of carrier on-time performance

• Report covering 65+ carriers, 300+ distinct carrier services/loops, 300+ ports, across 34 trade lanes

• 116 pages including global carrier performance Top20 and niche operators, benchmarking alliances and detailed trade performance

• 12-week future outlook on container space supply

• Most accurate and updated capacity deployment figures for 23 trade lanes between Asia, Europe, North and South America

• Based on actual vessel schedules of individual named vessels on all services in the trade lanes

SeaIntel subscription reports

3

TOC As ia – April 2019© Sea-Intelligence Maritime Analysis

Supply/Demand

4

TOC As ia – April 2019© Sea-Intelligence Maritime Analysis

Restrained ordering, but still 43 mega-vessels in orderbook

5

0%

1%

2%

3%

4%

5%

6%

7%

8%

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000Deliveries and Supply growth

Delivered Orderbook

0

2

4

6

8

10

12

14

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000VesselsTEU 16K+ Orderbook + Options

TOC As ia – April 2019© Sea-Intelligence Maritime Analysis

Weaker GDP/Goods ratio suggest 1-3% A-E demand growth

6

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

Asia-Europe Demand & EU economic growthAsia-Europe Demand Growth (TEU) EU Goods Imports (USD)

Average Demand growth: 12.5%Average Goods imp. growth: 5.2%Average GDP growth: 2.5%Demand/Goods imp. Ratio: 2.39Demand/Goods imp. Ratio: 5.19

Average Demand growth: 3.5%Average Goods imp. growth: 1.8%Average GDP growth: 0.9%Demand/Goods imp. Ratio: 1.91Demand/Goods imp. Ratio: 3.77

Average Demand growth: 2.4%Average Goods imp. growth: 3.3%Average GDP growth: 1.6%Demand/Goods imp. Ratio: 0.71Demand/Goods imp. Ratio: 1.45

Average Demand growth: 1.2%Average Goods imp. growth: 4.8%Average GDP growth: 2.3%Demand/Goods imp. Ratio: 0.25Demand/Goods imp. Ratio: 0.52

TOC As ia – April 2019© Sea-Intelligence Maritime Analysis

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

Transpacific Demand & US economic growthTranspacific Demand Growth (TEU) US GDP growth (constant prices)

GDP/Goods models suggest TP demand heading to 2-3%

7

Average Demand growth: 7.9%Average Goods imp. growth: 4.7%Average GDP growth: 2.4%Demand/Goods imp. Ratio: 1.68Demand/GDP imp. Ratio: 3.29

Average Demand growth: 3.9%Average Goods imp. growth: 3.3%Average GDP growth: 4.1%Demand/Goods imp. Ratio: 1.18Demand/Goods imp. Ratio: 0.89

TOC As ia – April 2019© Sea-Intelligence Maritime Analysis

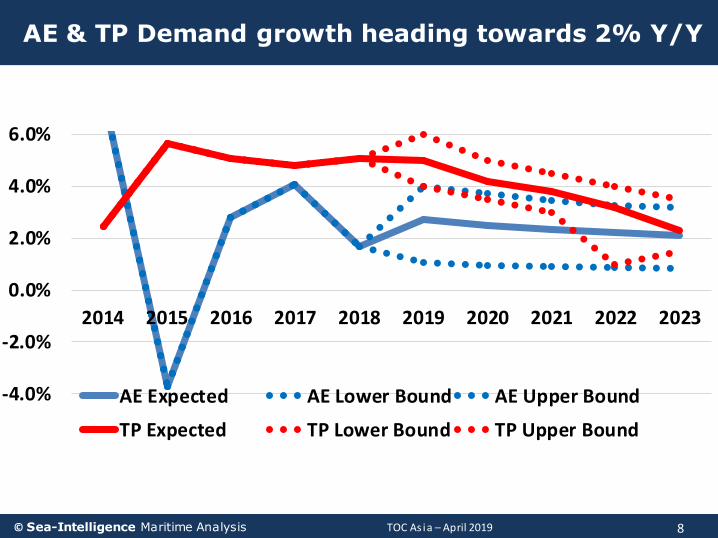

AE & TP Demand growth heading towards 2% Y/Y

8

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

AE Expected AE Lower Bound AE Upper Bound

TP Expected TP Lower Bound TP Upper Bound

TOC As ia – April 2019© Sea-Intelligence Maritime Analysis

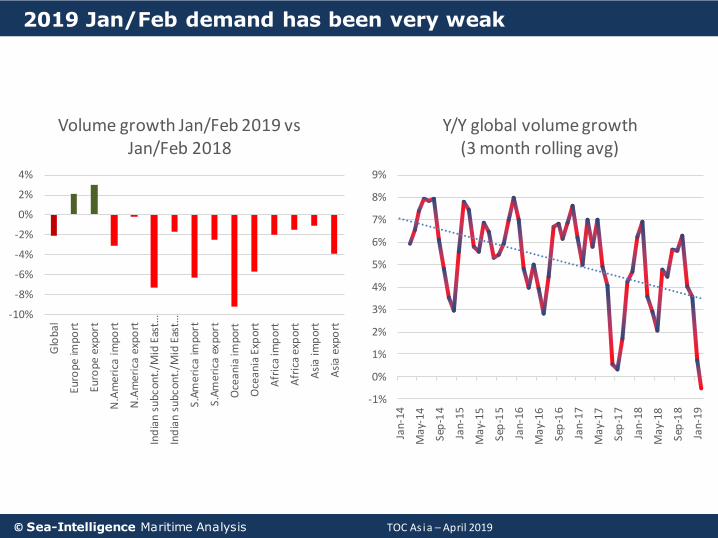

2019 Jan/Feb demand has been very weak

9

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

Glo

bal

Euro

pe im

port

Euro

pe e

xpor

t

N.A

mer

ica

imp

ort

N.A

me

rica

exp

ort

Ind

ian

subc

ont.

/Mid

Eas

t…

Ind

ian

subc

ont.

/Mid

Eas

t…

S.A

me

rica

imp

ort

S.Am

eric

a ex

port

Oce

ani

a im

port

Oce

an

ia E

xpo

rt

Afr

ica

imp

ort

Afr

ica

exp

ort

Asi

a im

por

t

Asi

a ex

port

Volume growth Jan/Feb 2019 vs Jan/Feb 2018

-1%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

Jan

-14

May

-14

Sep

-14

Jan

-15

May

-15

Sep

-15

Jan

-16

May

-16

Sep

-16

Jan

-17

May

-17

Sep

-17

Jan

-18

May

-18

Sep

-18

Jan

-19

Y/Y global volume growth (3 month rolling avg)

TOC As ia – April 2019© Sea-Intelligence Maritime Analysis

Impact on carrier returns

10

TOC As ia – April 2019© Sea-Intelligence Maritime Analysis

2018 carrier revenues have been strong

11

Liner Carrier Revenue 2010-2018 in Million USD Change Y/Y

2010 2011 2012 2013 2014 2015 2016 2017 2018 2018-9M* 2017 Y/Y

Maersk Line 26.038 25.108 27.117 26.196 27.351 23.729 20.715 22.023 28.366 21.556 28,8%

CMA CGM N/A 14.900 15.900 15.900 16.739 15.700 16.000 21.116 23.476 18.066 11,2%

COSCO** 7.015 6.497 7.700 7.896 8.183 8.047 9.586 13.336 N/A N/A N/A

Hapag Lloyd 8.222 7.964 9.044 8.997 8.309 10.029 8.138 11.966 13.192 9.966 10,2%

ONE N/A N/A N/A N/A N/A N/A N/A N/A N/A 8.055 N/A

Evergreen*** N/A N/A 4.837 4.622 4.545 4.148 3.839 5.069 5.534 4.263 9,2%

OOCL 6.033 6.012 6.459 6.232 6.522 5.953 5.298 5.425 5.963 4.585 9,9%

Yang Ming N/A N/A 4.508 3.947 4.246 3.954 3.559 4.412 4.638 3.567 5,1%

ZIM 3.717 3.784 3.960 3.682 3.409 2.991 2.539 2.978 3.248 2.497 9,1%

HMM 7.258 6.408 7.554 6.695 5.966 4.800 3.798 4.715 4.700 3.699 -0,3%

Wan Hai N/A N/A 2.159 1.982 2.110 1.980 1.769 2.046 2.184 1.669 6,8%

*Q2-Q4 as originally reported **COSCO SHIPPING Holdings Co., Ltd. ***Evergreen Marine Corp. (Taiwan) Ltd.

TOC As ia – April 2019© Sea-Intelligence Maritime Analysis

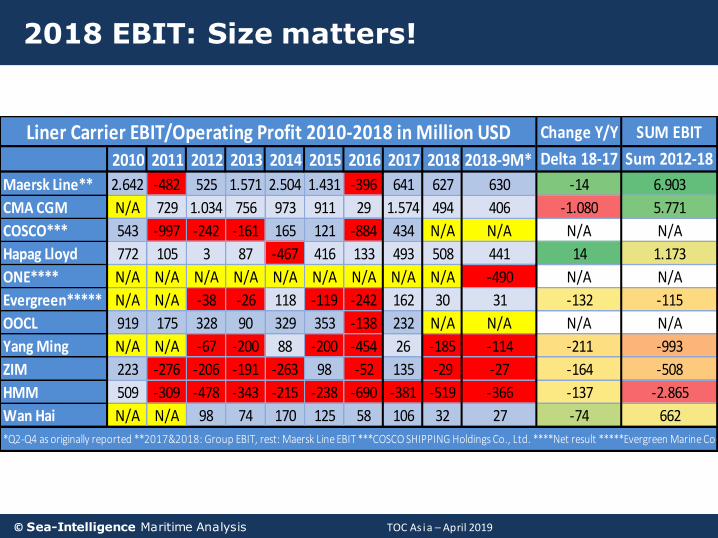

2018 EBIT: Size matters!

12

Change Y/Y SUM EBIT

2010 2011 2012 2013 2014 2015 2016 2017 2018 2018-9M* Delta 18-17 Sum 2012-18

Maersk Line** 2.642 -482 525 1.571 2.504 1.431 -396 641 627 630 -14 6.903

CMA CGM N/A 729 1.034 756 973 911 29 1.574 494 406 -1.080 5.771

COSCO*** 543 -997 -242 -161 165 121 -884 434 N/A N/A N/A N/A

Hapag Lloyd 772 105 3 87 -467 416 133 493 508 441 14 1.173

ONE**** N/A N/A N/A N/A N/A N/A N/A N/A N/A -490 N/A N/A

Evergreen***** N/A N/A -38 -26 118 -119 -242 162 30 31 -132 -115

OOCL 919 175 328 90 329 353 -138 232 N/A N/A N/A N/A

Yang Ming N/A N/A -67 -200 88 -200 -454 26 -185 -114 -211 -993

ZIM 223 -276 -206 -191 -263 98 -52 135 -29 -27 -164 -508

HMM 509 -309 -478 -343 -215 -238 -690 -381 -519 -366 -137 -2.865

Wan Hai N/A N/A 98 74 170 125 58 106 32 27 -74 662

Liner Carrier EBIT/Operating Profit 2010-2018 in Million USD

*Q2-Q4 as originally reported **2017&2018: Group EBIT, rest: Maersk Line EBIT ***COSCO SHIPPING Holdings Co., Ltd. ****Net result *****Evergreen Marine Corp. (Taiwan) Ltd.

TOC As ia – April 2019© Sea-Intelligence Maritime Analysis

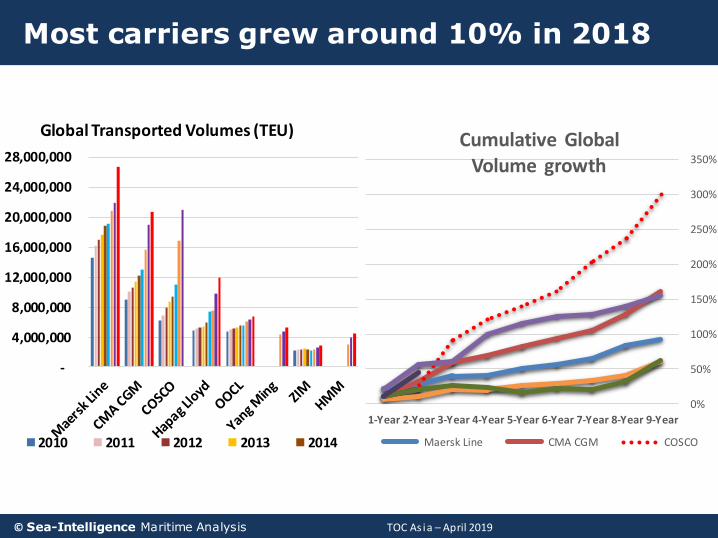

Most carriers grew around 10% in 2018

13

0%

50%

100%

150%

200%

250%

300%

350%

9-Year 8-Year 7-Year 6-Year 5-Year 4-Year 3-Year 2-Year 1-Year

Cumulative Global Volume growth

Maersk Line CMA CGM COSCO

-

4,000,000

8,000,000

12,000,000

16,000,000

20,000,000

24,000,000

28,000,000

Global Transported Volumes (TEU)

2010 2011 2012 2013 2014

TOC As ia – April 2019© Sea-Intelligence Maritime Analysis

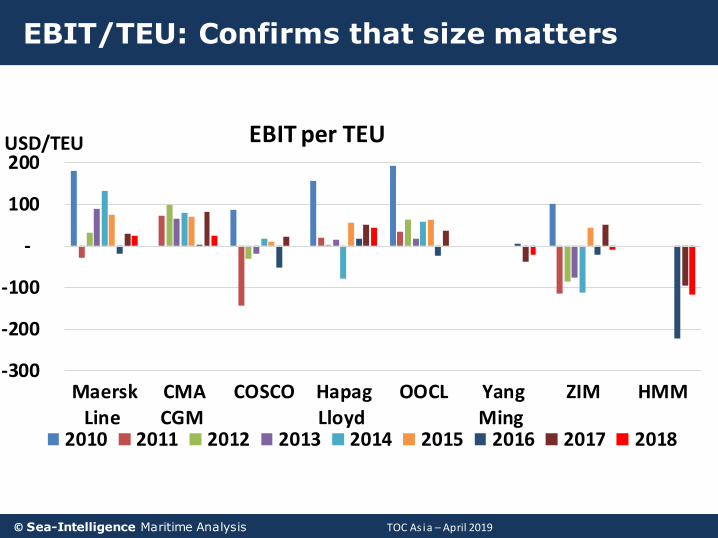

EBIT/TEU: Confirms that size matters

14

-300

-200

-100

-

100

200

MaerskLine

CMACGM

COSCO HapagLloyd

OOCL YangMing

ZIM HMM

USD/TEU EBIT per TEU

2010 2011 2012 2013 2014 2015 2016 2017 2018

TOC As ia – April 2019© Sea-Intelligence Maritime Analysis

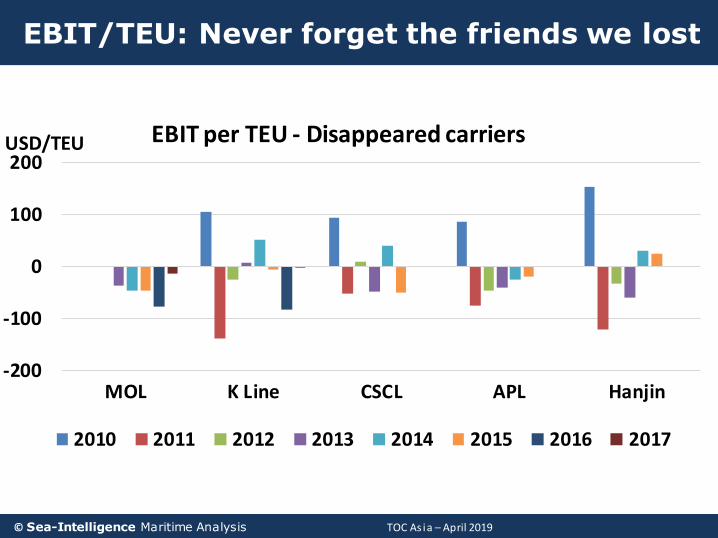

EBIT/TEU: Never forget the friends we lost

15

-200

-100

0

100

200

MOL K Line CSCL APL Hanjin

USD/TEU EBIT per TEU - Disappeared carriers

2010 2011 2012 2013 2014 2015 2016 2017

TOC As ia – April 2019© Sea-Intelligence Maritime Analysis

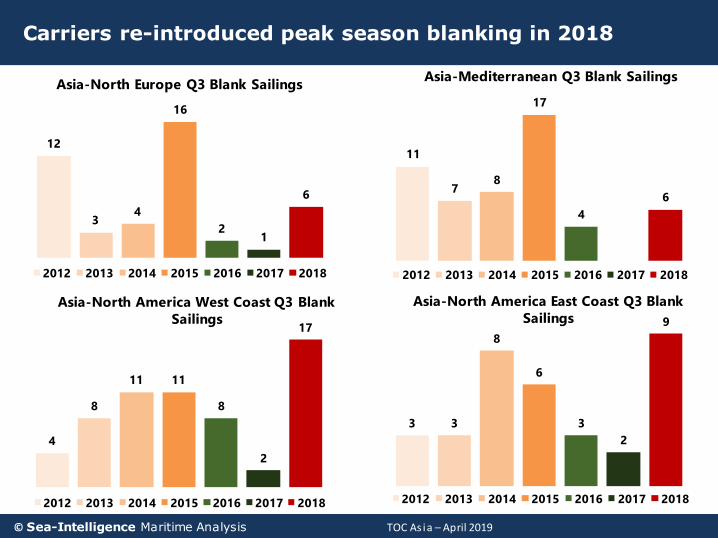

Carriers re-introduced peak season blanking in 2018

16

12

34

16

21

6

Asia-North Europe Q3 Blank Sailings

2012 2013 2014 2015 2016 2017 2018

11

78

17

4

6

Asia-Mediterranean Q3 Blank Sailings

2012 2013 2014 2015 2016 2017 2018

4

8

11 11

8

2

17

Asia-North America West Coast Q3 Blank

Sailings

2012 2013 2014 2015 2016 2017 2018

3 3

8

6

3

2

9

Asia-North America East Coast Q3 Blank

Sailings

2012 2013 2014 2015 2016 2017 2018

TOC As ia – April 2019© Sea-Intelligence Maritime Analysis

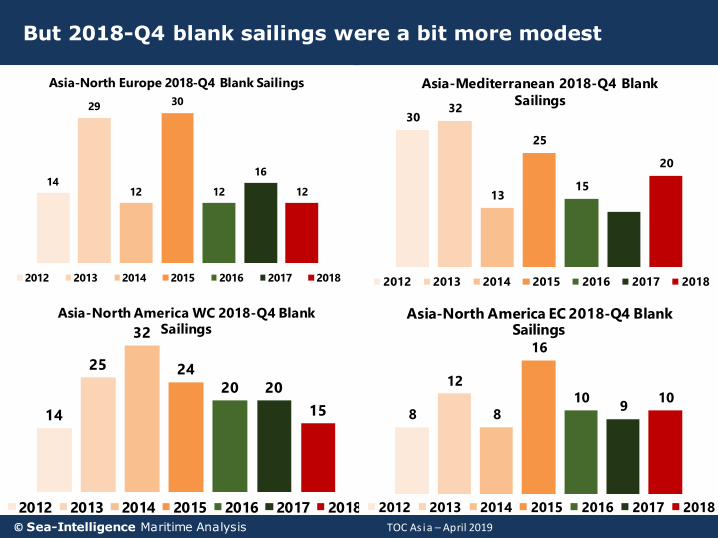

But 2018-Q4 blank sailings were a bit more modest

17

14

29

12

30

12

16

12

Asia-North Europe 2018-Q4 Blank Sailings

2012 2013 2014 2015 2016 2017 2018

3032

13

25

15

20

Asia-Mediterranean 2018-Q4 Blank

Sailings

2012 2013 2014 2015 2016 2017 2018

14

25

32

24

20 20

15

Asia-North America WC 2018-Q4 Blank Sailings

2012 2013 2014 2015 2016 2017 2018

8

12

8

16

109

10

Asia-North America EC 2018-Q4 Blank Sailings

2012 2013 2014 2015 2016 2017 2018

TOC As ia – April 2019© Sea-Intelligence Maritime Analysis

And 2019-Q1 blank sailings are in the higher end

18

26

17

22

26

29

13

21 20

Asia-North Europe 2018-Q4 Blank

Sailings

2012 2013 2014 2015 2016 2017 2018 2019

1820

1718

13

911

15

Asia-Mediterranean 2018-Q4 Blank Sailings

2012 2013 2014 2015 2016 2017 2018 2019

24

41 41

79

36

26

4552

Asia-North America West Coast 2019-Q1 Blank Sailings

2012 2013 2014 2015 2016 2017 2018 2019

8

23

13

9

23

9

22 21

Asia-North America East Coast 2019-Q1 Blank Sailings

2012 2013 2014 2015 2016 2017 2018 2019

TOC As ia – April 2019© Sea-Intelligence Maritime Analysis

Modeling TP contract rates on spot suggests a 20% increase

19

0

200

400

600

800

1000

1200

1400

Mar

-09

De

c-0

9Se

p-1

0Ju

n-1

1M

ar-1

2D

ec-

12

Sep

-13

Jun

-14

Mar

-15

De

c-1

5Se

p-1

6Ju

n-1

7M

ar-1

8D

ec-

18

CCFI versus model based on

spot rates (Asia-USWC)

CCFI-40%

-35%

-30%

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

Mar

-09

De

c-0

9Se

p-1

0Ju

n-1

1M

ar-1

2D

ec-

12

Sep

-13

Jun

-14

Mar

-15

De

c-1

5Se

p-1

6Ju

n-1

7M

ar-1

8D

ec-

18

Contract rate deviation from

spot model (Asia-USWC)

TOC As ia – April 2019© Sea-Intelligence Maritime Analysis

Impact on service levels

20

TOC As ia – April 2019© Sea-Intelligence Maritime Analysis

21

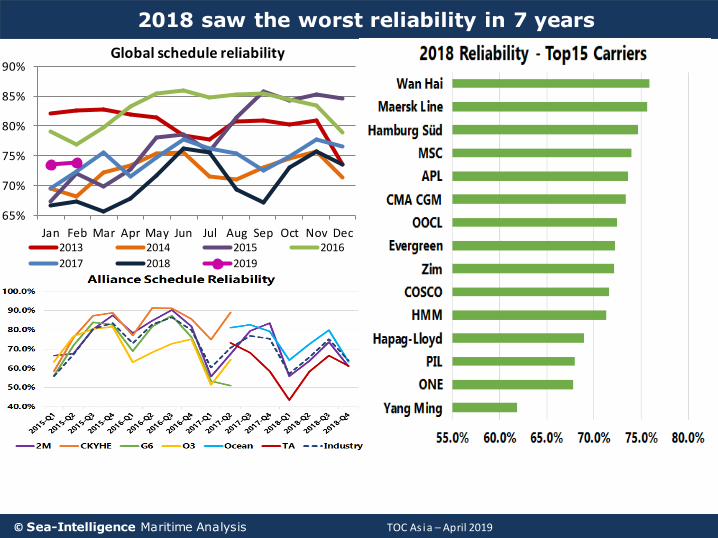

2018 saw the worst reliability in 7 years

65%

70%

75%

80%

85%

90%

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Global schedule reliability

2013 2014 2015 2016

2017 2018 2019

TOC As ia – April 2019© Sea-Intelligence Maritime Analysis

22

2018 reliability especially bad in Transpacific

30%35%40%45%50%55%60%65%70%75%80%85%

Asia-NAWC Alliance schedule reliability

2M Ocean TA

25%

35%

45%

55%

65%

75%

85%

Asia-NAEC Alliance schedule reliability

2M Ocean TA

10%20%30%40%50%60%70%80%90%

Asia - NAWC schedule reliability

2013 2014 2015 2016

30%35%40%45%50%55%60%65%70%75%80%85%90%

Asia - NAEC schedule reliability

2013 2014 2015 2016

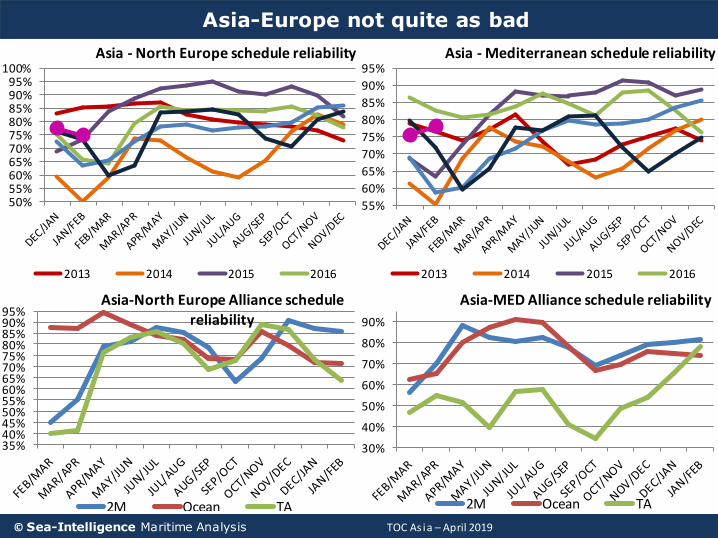

TOC As ia – April 2019© Sea-Intelligence Maritime Analysis

23

Asia-Europe not quite as bad

50%55%60%65%70%75%80%85%90%95%

100%Asia - North Europe schedule reliability

2013 2014 2015 2016

55%

60%

65%

70%

75%

80%

85%

90%

95%Asia - Mediterranean schedule reliability

2013 2014 2015 2016

35%40%45%50%55%60%65%70%75%80%85%90%95%

Asia-North Europe Alliance schedule reliability

2M Ocean TA

30%

40%

50%

60%

70%

80%

90%

Asia-MED Alliance schedule reliability

2M Ocean TA

TOC As ia – April 2019© Sea-Intelligence Maritime Analysis

Asia-NEUR service disruptions

24

TOC As ia – April 2019© Sea-Intelligence Maritime Analysis

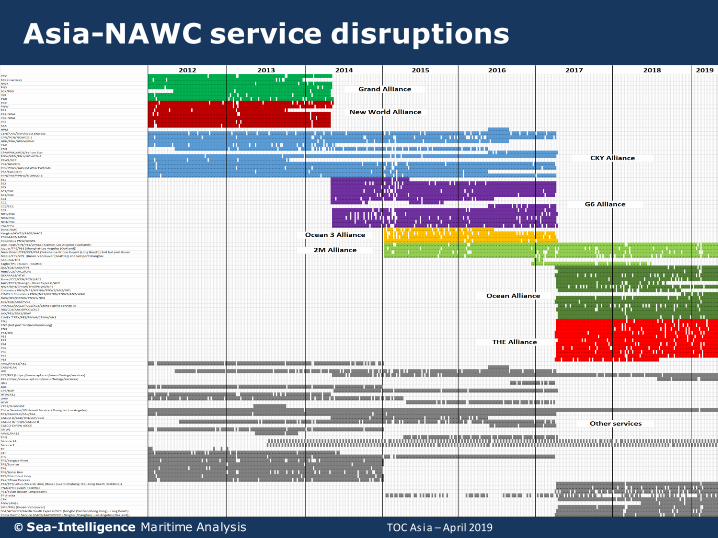

Asia-NAWC service disruptions

25

TOC As ia – April 2019© Sea-Intelligence Maritime Analysis

No. of direct ports has steadily declined

26

180

190

200

210

220

230

Asia-NEUR Distinct Port-Pairs

250

270

290

310

330

350

370

Asia-MED Distinct Port-Pairs

All Services Dedicated Asia-MED Services

TOC As ia – April 2019© Sea-Intelligence Maritime Analysis

Direct TP port-pairs see a sharp decline in 2018

27

140

150

160

170

180Asia-NAWC Distinct Port-Pairs

130

140

150

160

170Asia-NAEC Distinct Port-Pairs

TOC As ia – April 2019© Sea-Intelligence Maritime Analysis

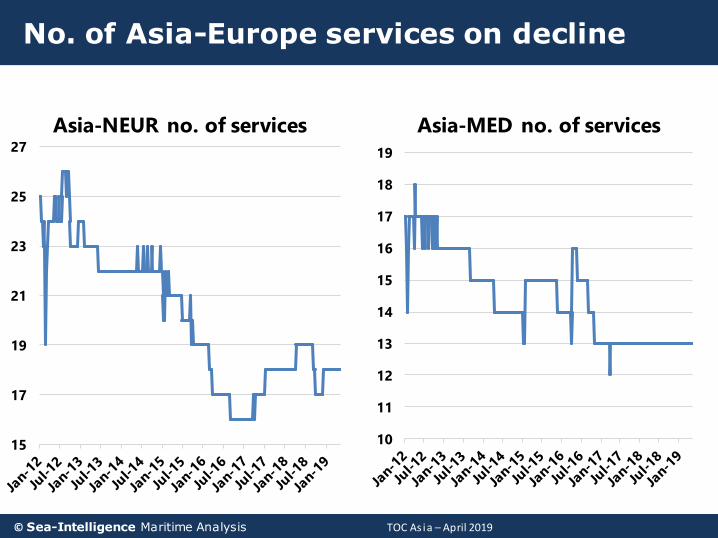

No. of Asia-Europe services on decline

28

15

17

19

21

23

25

27

Asia-NEUR no. of services

10

11

12

13

14

15

16

17

18

19

Asia-MED no. of services

TOC As ia – April 2019© Sea-Intelligence Maritime Analysis

No. of Transpac services seems to have stabilised

29

35

37

39

41

43

45

47

49

Jan

-12

Jul-

12

Jan

-13

Jul-

13

Jan

-14

Jul-

14

Jan

-15

Jul-

15

Jan

-16

Jul-

16

Jan

-17

Jul-

17

Jan

-18

Jul-

18

Jan

-19

Asia-NAWC no. of services

15

16

17

18

19

20

21

22

23

24

25

Jan

-12

Jul-

12

Jan

-13

Jul-

13

Jan

-14

Jul-

14

Jan

-15

Jul-

15

Jan

-16

Jul-

16

Jan

-17

Jul-

17

Jan

-18

Jul-

18

Jan

-19

Asia-NAEC no. of services

TOC As ia – April 2019© Sea-Intelligence Maritime Analysis

Concluding remarks

30

Things are gradually getting better for the shipping lines, but service levels are poor

• Supply/Demand balance slowly improving, with a pre-2009 balance possible by 2022-2023

• The market consolidation has mitigated the worst excesses of the past

• Service levels have been very poor in recent years

There are a number of major risks to this outlook

• If carriers fail to pass on the IMO 2020 bunker costs, they will be forced to lay up significant tonnage, with massive disruptions to service networks.

• Demand is slowing down to a long-term growth rate of 2-3% on the main East-West trades.

• The EU Commission may end the Block Exemption Regulation in 2020, making alliances and VSAs more difficult to set up, and more costly to run.

• Irrational vessel ordering (HMM?) could lead to a price war.

In the short term, expect carriers to fight for rate increase on TP

• Contract rates are 20% below comparable spot rates, and carriers showed in the 2018 peak season they are ready to cut capacity deep in order to get rates up.

• Service levels are likely to remain poor, at least to the turn of 2020.

TOC As ia – April 2019© Sea-Intelligence Maritime Analysis

Notes on the 2020 IMO Low-Sulphur requirement

31

TOC As ia – April 2019© Sea-Intelligence Maritime Analysis

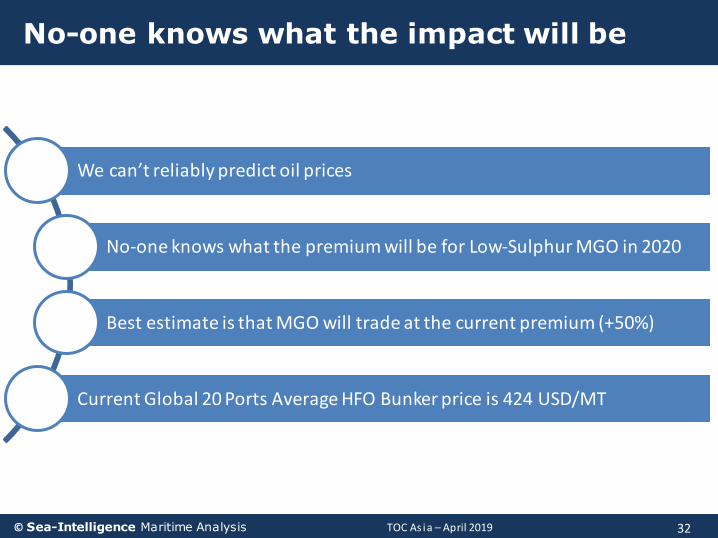

No-one knows what the impact will be

32

We can’t reliably predict oil prices

No-one knows what the premium will be for Low-Sulphur MGO in 2020

Best estimate is that MGO will trade at the current premium (+50%)

Current Global 20 Ports Average HFO Bunker price is 424 USD/MT

TOC As ia – April 2019© Sea-Intelligence Maritime Analysis

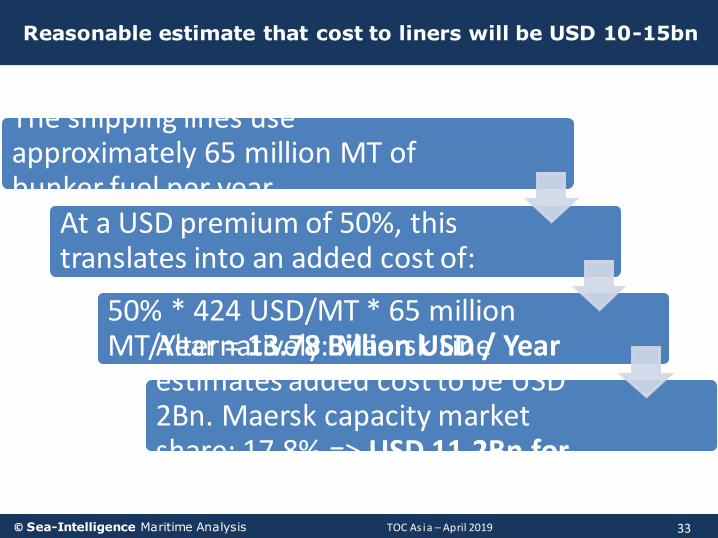

Reasonable estimate that cost to liners will be USD 10-15bn

33

The shipping lines use approximately 65 million MT of bunker fuel per year

At a USD premium of 50%, this translates into an added cost of:

50% * 424 USD/MT * 65 million MT/Year = 13.78 Billion USD / YearAlternatively: Maersk Line

estimates added cost to be USD 2Bn. Maersk capacity market share: 17.8% => USD 11.2Bn for Industry

TOC As ia – April 2019© Sea-Intelligence Maritime Analysis

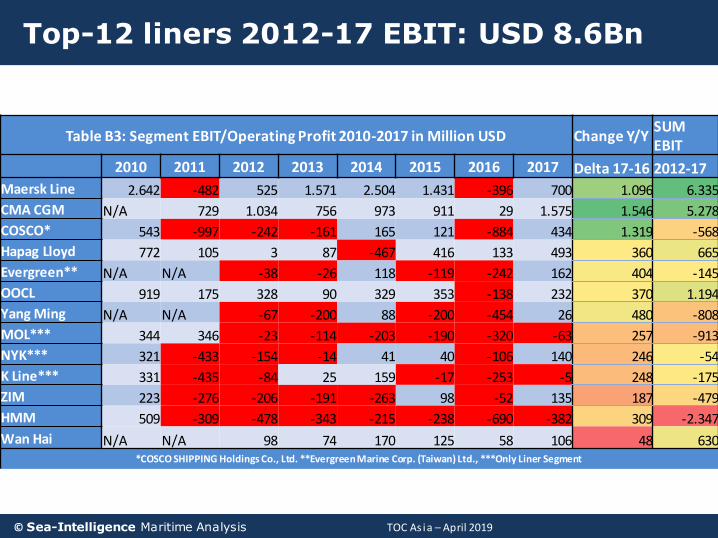

Top-12 liners 2012-17 EBIT: USD 8.6Bn

34

Table B3: Segment EBIT/Operating Profit 2010-2017 in Million USD Change Y/YSUM EBIT

2010 2011 2012 2013 2014 2015 2016 2017 Delta 17-16 2012-17

Maersk Line 2.642 -482 525 1.571 2.504 1.431 -396 700 1.096 6.335

CMA CGM N/A 729 1.034 756 973 911 29 1.575 1.546 5.278

COSCO* 543 -997 -242 -161 165 121 -884 434 1.319 -568

Hapag Lloyd 772 105 3 87 -467 416 133 493 360 665

Evergreen** N/A N/A -38 -26 118 -119 -242 162 404 -145

OOCL 919 175 328 90 329 353 -138 232 370 1.194

Yang Ming N/A N/A -67 -200 88 -200 -454 26 480 -808

MOL*** 344 346 -23 -114 -203 -190 -320 -63 257 -913

NYK*** 321 -433 -154 -14 41 40 -106 140 246 -54

K Line*** 331 -435 -84 25 159 -17 -253 -5 248 -175

ZIM 223 -276 -206 -191 -263 98 -52 135 187 -479

HMM 509 -309 -478 -343 -215 -238 -690 -382 309 -2.347

Wan Hai N/A N/A 98 74 170 125 58 106 48 630*COSCO SHIPPING Holdings Co., Ltd. **Evergreen Marine Corp. (Taiwan) Ltd., ***Only Liner Segment

TOC As ia – April 2019© Sea-Intelligence Maritime Analysis

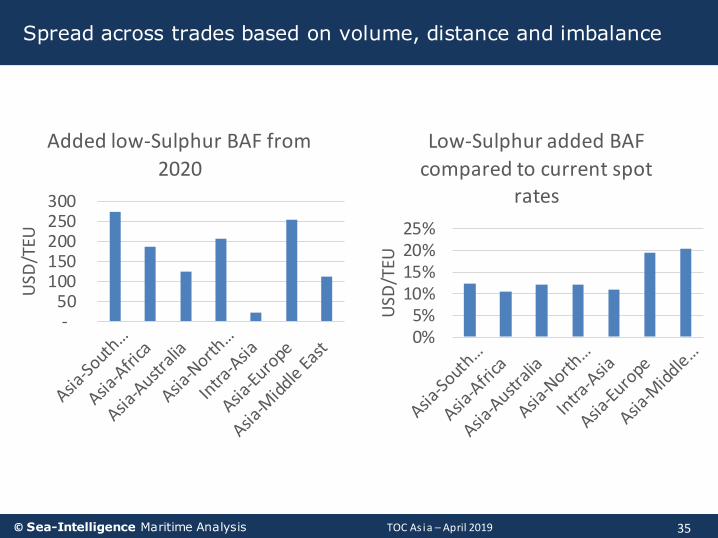

Spread across trades based on volume, distance and imbalance

35

- 50

100 150 200 250 300

USD

/TEU

Added low-Sulphur BAF from

2020

0%5%

10%15%20%25%

USD

/TEU

Low-Sulphur added BAF

compared to current spot rates

TOC As ia – April 2019© Sea-Intelligence Maritime Analysis

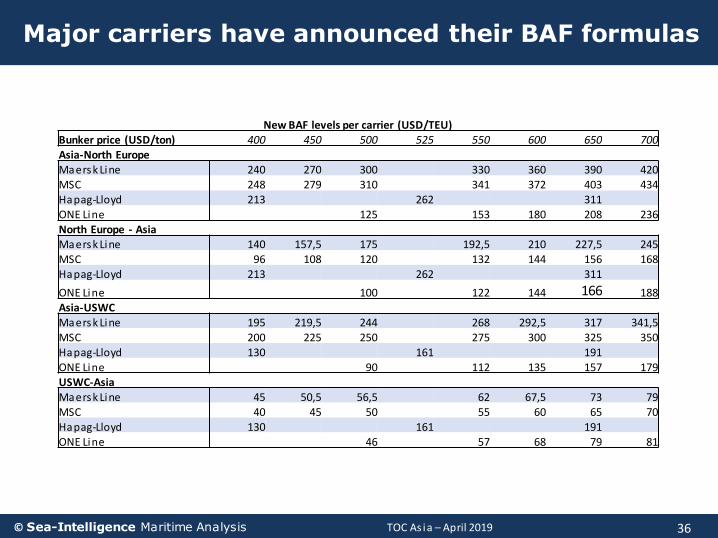

Major carriers have announced their BAF formulas

36

New BAF levels per carrier (USD/TEU)Bunker price (USD/ton) 400 450 500 525 550 600 650 700Asia-North EuropeMaersk Line 240 270 300 330 360 390 420MSC 248 279 310 341 372 403 434Hapag-Lloyd 213 262 311ONE Line 125 153 180 208 236North Europe - AsiaMaersk Line 140 157,5 175 192,5 210 227,5 245MSC 96 108 120 132 144 156 168Hapag-Lloyd 213 262 311

ONE Line 100 122 144 166 188Asia-USWCMaersk Line 195 219,5 244 268 292,5 317 341,5MSC 200 225 250 275 300 325 350Hapag-Lloyd 130 161 191ONE Line 90 112 135 157 179USWC-AsiaMaersk Line 45 50,5 56,5 62 67,5 73 79MSC 40 45 50 55 60 65 70Hapag-Lloyd 130 161 191ONE Line 46 57 68 79 81

TOC As ia – April 2019© Sea-Intelligence Maritime Analysis

Alliances and consolidation

37

TOC As ia – April 2019© Sea-Intelligence Maritime Analysis

9th

17th

CKYHE

14th

5th6th

2M Alliance

1st

2nd

THE Alliance

14th

8th6th

13th11th

16th

15th

G6 Alliance

4th

10th

11th

13th

15th

16th

12th

Ocean Three

3rd

7th

Ocean Alliance

3rd

9th

4th

5th

12th

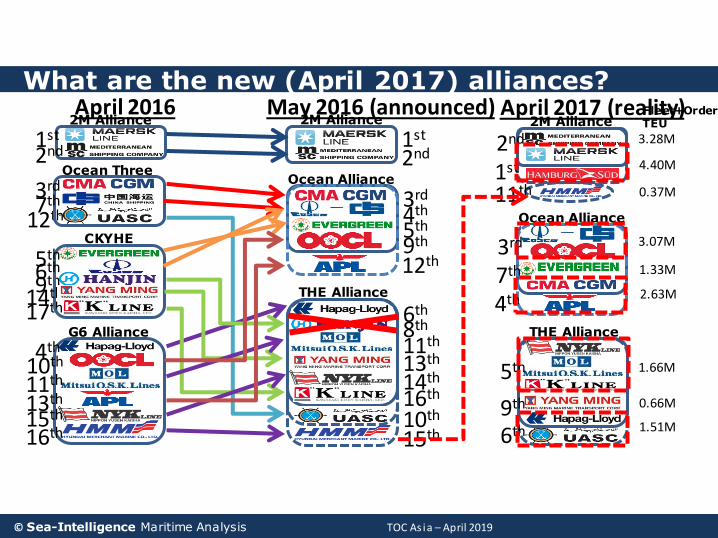

What are the new (April 2017) alliances?

38

2M Alliance

Ocean Alliance

THE Alliance

April 2017 (reality)

1st

2nd

7th

4th

11th

3rd

5th

9th

6th

4.40M

3.28M

1.33M

2.63M

0.37M

3.07M

1.66M

0.66M

1.51M

Fleet+OrderTEU

April 20162M Alliance

1st

2nd

May 2016 (announced)

10th

TOC As ia – April 2019© Sea-Intelligence Maritime Analysis

- 100,000 200,000 300,000 400,000 500,000 600,000

TEU

Ca

pa

city

(2

00

0)

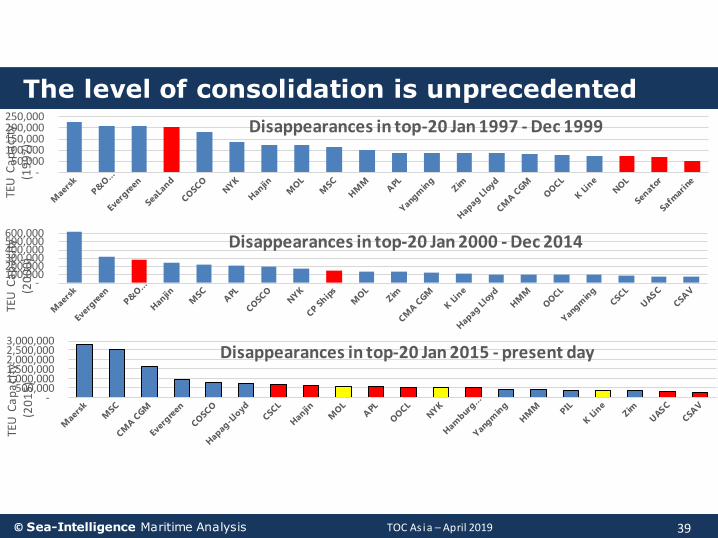

Disappearances in top-20 Jan 2000 - Dec 2014

The level of consolidation is unprecedented

39

- 50,000

100,000 150,000 200,000 250,000

TEU

Ca

pa

city

(1

99

7)

Disappearances in top-20 Jan 1997 - Dec 1999

- 500,000

1,000,000 1,500,000 2,000,000 2,500,000 3,000,000

TEU

Ca

pa

city

(2

01

5)

Disappearances in top-20 Jan 2015 - present day

TOC As ia – April 2019© Sea-Intelligence Maritime Analysis

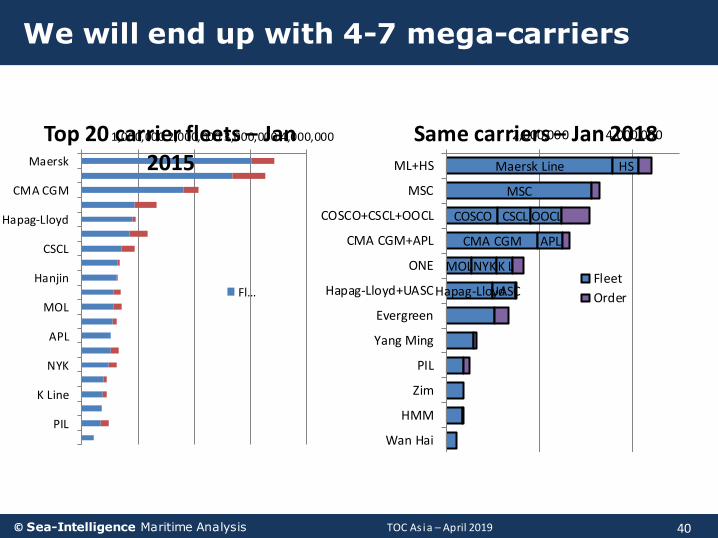

We will end up with 4-7 mega-carriers

40

1,000,000 2,000,000 3,000,000 4,000,000

Maersk

CMA CGM

Hapag-Lloyd

CSCL

Hanjin

MOL

APL

NYK

K Line

PIL

Top 20 carrier fleets – Jan 2015

Fl…

Maersk Line

MSC

COSCO

CMA CGM

MOL

Hapag-Lloyd

HS

CSCL

APL

NYK

UASC

OOCL

K L

2,000,000 4,000,000

ML+HS

MSC

COSCO+CSCL+OOCL

CMA CGM+APL

ONE

Hapag-Lloyd+UASC

Evergreen

Yang Ming

PIL

Zim

HMM

Wan Hai

Same carriers – Jan 2018

Fleet

Order

TOC As ia – April 2019© Sea-Intelligence Maritime Analysis

Front-loading of 2019-Q1 volumes due to US-China tariff hike

41

TOC As ia – April 2019© Sea-Intelligence Maritime Analysis

CTS data shows a loading surge in November

42

0.3

%

-5.1

%

20

.5%

5.2

%

5.0

%

0.6

%

-7.7

%

-4.9

%

1.9

%

6.9

%

3.5

%

-8.2

%

1.2

%

0.6

%

11

.7%

23

.0%

13

.1%

14

.2%

4.2

%

4.9

%

-0.8

%

1.0

%

7.6

%

3.8

%

3.5

%

3.0

%

6.6

%

4.0

%

9.6

%

19

.5%

4.5

%

6.0

%

OCT NOV DEC JAN

Oct-Jan Y/Y TP volume growth – NOTE: Time of loading

2012 2013 2014 2015 2016 2017 2012-17 Avg 2018

TOC As ia – April 2019© Sea-Intelligence Maritime Analysis

But limited imports surge, and only in NAWC

43

-6.4

%

-3.8

%

-9.0

% -2.2

%

-1.7

%

0.5

%7.3

% 13

.2%

2.7

%

10

.7%

9.4

%

10

.5%

2013 2014 2015 2016 2017 2018

North America East Coast

Q4 Laden Import Volumes

Q/Q

-7.4

%

-7.3

%

-10

.1% -2

.0%

-4.3

%

2.5

%

2.4

%

3.2

%

1.5

% 7.2

%

6.6

%

9.0

%

2013 2014 2015 2016 2017 2018

North America West Coast

Q4 Laden Import Volumes

Q/Q