cfotalks.com · 2019-05-29 · Nomura | Asia Economic Monthly 10 May 2019 Forecast table Research...

77

Nomura | Asia Economic Monthly 10 May 2019 Research analysts Asia Economics Rob Subbaraman - NSL [email protected] +65 6433 6548 Ting Lu - NIHK [email protected] +852 2252 1306 Sonal Varma - NSL [email protected] +65 6433 6527 Euben Paracuelles - NSL [email protected] +65 6433 6956 What do you think? Results from our last survey Where is Asia headed over the next three months? 46.2% 28.2% 25.6% UP: Economic recovery and market rally DOWN: Weak economies and markets correct FLAT: Weak economies amid buoyand assets Forecast table 2 Asia letter 3 Trade tensions threaten Asia’s dawn 3 Asia views 5 US/China: Trade tensions escalate 5 China monthly: Beijing can’t afford to stop easing yet, as double… 13 China: The Politburo turns more cautious, but it cannot afford to… 15 China: The NDRC plans a new round of consumption stimulus 17 China’s delicate policy balancing act 21 India Election Watch #8: In opinion polls we somewhat trust 24 India: Global headwinds, Indian sails 28 Korea: April data for exports and inflation suggest weak… 36 Malaysia: BNM kickstarts monetary easing in ASEAN 38 Philippines: One-notch upgrade by S&P to BBB+ 39 Indonesia: A clear win for Jokowi 41 Thailand: Gauging the drought impact 44 What if oil prices keep rising? 48 Chart alerts 51 Asia stockpiles look larger than in 2015-16 51 Nomura’s leading index of Asian exports 51 China: Excavator operating hours improved in March 52 India: Glass half empty on GST collections 52 India’s two-speed manufacturing cycle 53 India: Core matter 53 Philippines: Slowing money supply growth… 54 Philippines: The president's popularity rebounds further ahead of… 54 Thailand: Condominium price index growth fell sharply in Q1 55 Thailand: Evidence of further slowdown in tourism 55 Calendar 56 The month ahead 56 Outlooks 2019-20 57 Australia: Underwhelming; RBA to cut 57 China: A full recovery yet to come 58 India: All eyes on the election verdict 59 Indonesia: A clear Jokowi win 60 Japan: Signs of stabilization 61 Malaysia: BNM kick-starts monetary easing 62 Philippines: Temporary fiscal tightening 63 Singapore: A dovish turn 64 South Korea: A negative shadow on exports 65 Thailand: Political risks weigh on growth 66 Asia in charts 67 Recent articles 74 Asia Economic Monthly ECONOMICS Trade tensions threaten Asia’s dawn The outcome of US-China trade negotiations will determine Asia’s path ahead. Global Markets Research 10 May 2019 See Appendix A-1 for analyst certification, important disclosures and the status of non-US analysts. Visit Nomura Connects for our global thought leadership. Please participate in our anonymous real-time survey. Click an option below to see a current tally of results. If the US hikes tariffs, how will China respond? • Tariff hikes • Allow RMB depreciation • Sell US Treasurys • Boycott US products Production Complete: 2019-05-09 22:54 UTC

Transcript of cfotalks.com · 2019-05-29 · Nomura | Asia Economic Monthly 10 May 2019 Forecast table Research...

Nomura | Asia Economic Monthly 10 May 2019

Research analysts

Asia Economics

Rob Subbaraman - NSL [email protected] +65 6433 6548

Ting Lu - NIHK [email protected] +852 2252 1306

Sonal Varma - NSL [email protected] +65 6433 6527

Euben Paracuelles - NSL [email protected] +65 6433 6956

What do you think?

Results from our last survey

Where is Asia headed over the next

three months?

46.2%

28.2%

25.6%

UP: Economic recovery and market rally

DOWN: Weak economies and markets correct

FLAT: Weak economies amid buoyand assets

Forecast table 2 Asia letter 3

Trade tensions threaten Asia’s dawn 3

Asia views 5 US/China: Trade tensions escalate 5 China monthly: Beijing can’t afford to stop easing yet, as double… 13 China: The Politburo turns more cautious, but it cannot afford to… 15 China: The NDRC plans a new round of consumption stimulus 17 China’s delicate policy balancing act 21 India Election Watch #8: In opinion polls we somewhat trust 24 India: Global headwinds, Indian sails 28 Korea: April data for exports and inflation suggest weak… 36 Malaysia: BNM kickstarts monetary easing in ASEAN 38 Philippines: One-notch upgrade by S&P to BBB+ 39 Indonesia: A clear win for Jokowi 41 Thailand: Gauging the drought impact 44 What if oil prices keep rising? 48

Chart alerts 51 Asia stockpiles look larger than in 2015-16 51 Nomura’s leading index of Asian exports 51 China: Excavator operating hours improved in March 52 India: Glass half empty on GST collections 52 India’s two-speed manufacturing cycle 53 India: Core matter 53 Philippines: Slowing money supply growth… 54 Philippines: The president's popularity rebounds further ahead of… 54 Thailand: Condominium price index growth fell sharply in Q1 55 Thailand: Evidence of further slowdown in tourism 55

Calendar 56 The month ahead 56

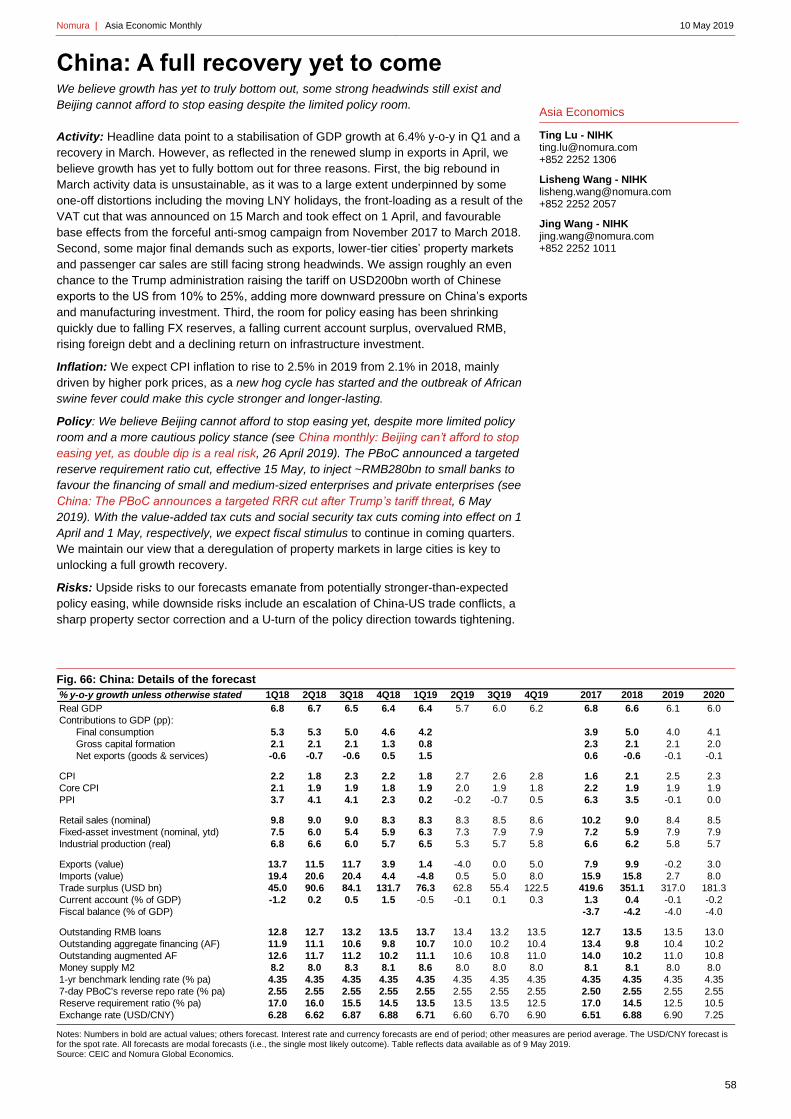

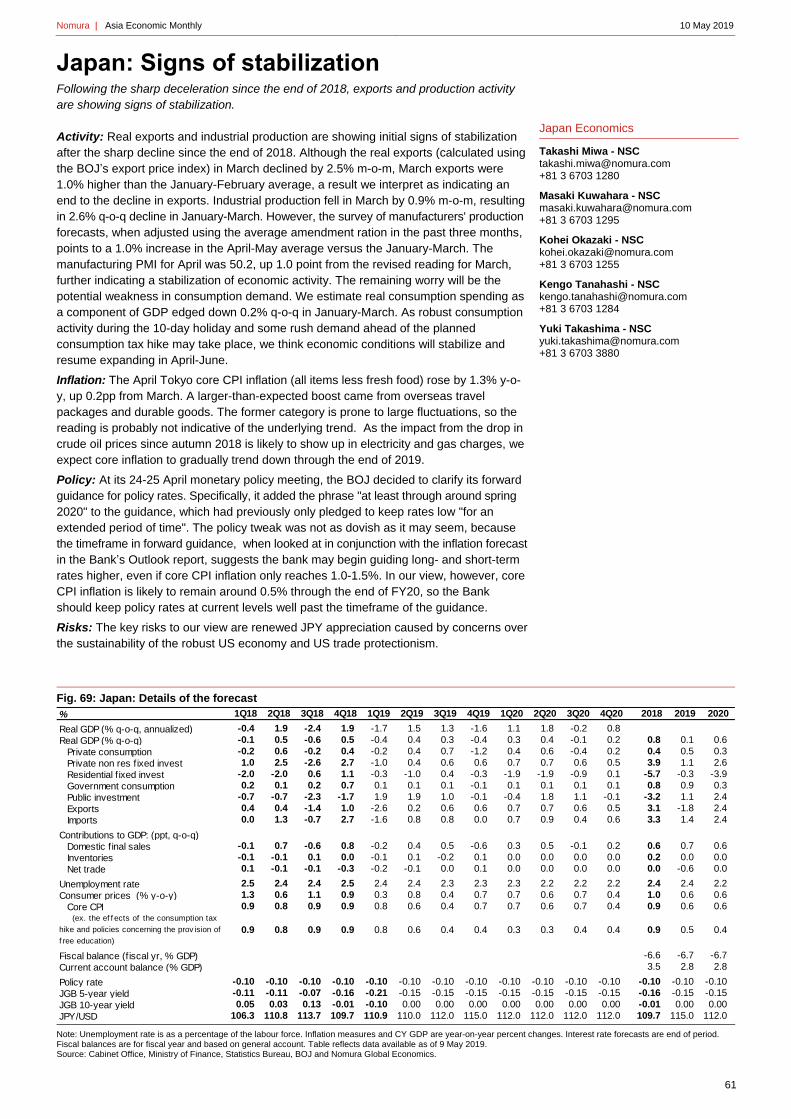

Outlooks 2019-20 57 Australia: Underwhelming; RBA to cut 57 China: A full recovery yet to come 58 India: All eyes on the election verdict 59 Indonesia: A clear Jokowi win 60 Japan: Signs of stabilization 61 Malaysia: BNM kick-starts monetary easing 62 Philippines: Temporary fiscal tightening 63 Singapore: A dovish turn 64 South Korea: A negative shadow on exports 65 Thailand: Political risks weigh on growth 66

Asia in charts 67 Recent articles 74

Asia Economic Monthly

ECONOMICS

Trade tensions threaten Asia’s dawn

The outcome of US-China trade negotiations will determine Asia’s path ahead.

Global Markets Research

10 May 2019

See Appendix A-1 for analyst certification, important disclosures and the status of non-US analysts.

Visit Nomura Connects for our global

thought leadership.

Please participate in our anonymous

real-time survey. Click an option below

to see a current tally of results.

If the US hikes tariffs, how will China

respond?

• Tariff hikes

• Allow RMB depreciation

• Sell US Treasurys

• Boycott US products

Production Complete: 2019-05-09 22:54 UTC

Nomura | Asia Economic Monthly 10 May 2019

2

Forecast table

Fig. 1: Forecast table

2018 2019 2020 2018 2019 2020

Japan 0.8 0.1 0.6 1.0 0.6 0.6

Australia 2.8 2.1 ↓ 2.0 2.6 1.9 1.6 ↑ 1.7 2.0

China 6.6 6.0 ↑ 6.1 6.0 2.1 2.5 2.3

Hong Kong 3.0 2.7 3.0 2.4 2.4 2.5

India 7.4 6.6 7.1 3.9 3.1 4.1

Indonesia 5.2 5.4 5.7 3.2 2.9 3.3

Malaysia 4.7 4.0 4.2 1.0 0.5 1.3

Philippines 6.2 6.8 6.6 5.2 3.0 ↓ 2.9 3.1

Singapore 3.2 2.5 2.2 0.4 0.3 0.5

South Korea 2.7 2.4 ↓ 1.8 2.1 1.5 0.8 1.4

Taiwan 2.6 2.5 2.5 1.3 1.1 1.2

Thailand 4.1 3.4 3.0 1.1 0.7 1.0

Asia ex-Japan, Aus. 6.2 5.6 ↑ 5.7 5.8 2.5 2.4 2.6 ↑ 2.7

Asia 5.5 5.0 5.2 2.4 2.2 2.4

2018 2019 2020 2018 2019 2020

Japan 3.5 2.8 2.8 -6.6 -6.7 -6.7

Australia -2.2 -2.1 -2.4 -0.4 0.1 0.4

China 0.4 -0.1 -0.2 -4.2 -4.0 -4.0

Hong Kong 4.3 3.2 3.4 2.0 1.3 1.6

India -2.4 -1.9 -2.2 -3.4 -3.4 -3.2

Indonesia -3.0 -2.7 -2.6 -1.8 -2.1 -2.5

Malaysia 2.3 2.0 2.0 -3.7 -3.7 -3.4

Philippines -2.4 -2.9 -3.1 -3.2 -3.3 -3.2

Singapore 17.7 15.8 14.6 0.4 -0.7 -1.0

South Korea 4.7 4.5 ↑ 4.9 4.0 ↑ 4.3 1.7 0.6 0.0

Taiwan 11.5 11.4 10.7 -1.9 -1.9 -1.9

Thailand 6.9 5.9 6.0 -2.4 -2.6 -3.0

Asia ex-Japan, Aus. 0.4 0.2 0.0 -3.3 -3.3 -3.3

Asia 0.7 0.4 0.2 -3.6 -3.6 -3.6

2018 2019 2020 2018 2019 2020

Japan -0.10 -0.10 -0.10 109.7 115.0 112.0

Australia 1.50 1.00 1.00 0.70 0.71 0.70

China 2.55 2.55 2.55 6.88 6.90 7.25

Hong Kong 7.83 7.83 7.80

India 6.50 5.75 5.75 69.8 67.5 67.0

Indonesia 6.00 6.00 ↓ 5.50 5.00 14481 13600 12700

Malaysia 3.25 3.00 3.00 4.14 4.08 4.00

Philippines 4.75 4.25 4.25 52.6 52.5 51.5

Singapore 1.89 1.90 1.90 1.36 1.33 1.30

South Korea 1.75 1.50 1.25 1111 1100 1060

Taiwan 30.5 30.3 29.2

Thailand 1.75 1.75 1.75 32.4 31.3 30.2

Official Policy Rate Currency per US Dollar

Note: All figures relate to the modal forecast, ie, the "most likely" outcome. The policy rate for Singapore refers to the 3-month SIBOR, for China the

7-day reverse repo rate. Fiscal balances are for the central government and do not include off-budget. They are calculated for fiscal years for India

(Apr-Mar), Singapore (Apr-Mar) and Thailand (Oct-Sep). Bolded values are actual. Forecasts for Hong Kong and Taiwan's real gdp, consumer

prices, current account, and fiscal balance are from the IMF World Economic Outlook, and fiscal balance for them refers to the general government

balance. Source: IMF, CEIC, Bloomberg, Nomura.

Real GDP Consumer Prices

Current Account (% of GDP) Fiscal Balance (% of GDP)

Nomura | Asia Economic Monthly 10 May 2019

3

Asia Economics

Sonal Varma - NSL [email protected] +65 6433 6527

Rob Subbaraman - NSL [email protected] +65 6433 6548

Michael Loo - NSL [email protected] +65 6433 6296

Asia letter

Trade tensions threaten Asia’s dawn If trade tensions fade quickly, then our base case of Asia’s ‘dawn’ is within reach; else,

expect a prolonged slowdown and frontloaded policy easing across the region.

The recent escalation of US-China trade tensions come at a time when Asian economies

are weakening and business confidence is fragile. Weak global capex, the slump in the

tech cycle and sluggish China demand have already sapped growth. In our base case,

Q2 will mark the trough and a ‘dawn’ will emerge in H2 2019 and into 2020, as Asian

economies recover with support from China stimulus, easier financial conditions and an

upturn in the tech cycle. A trade shock at this vulnerable moment could derail this scenario.

Why Asia is more vulnerable

An escalation of US-China trade tensions is more damaging for Asia’s export-oriented

economies than for China itself, because many of the smaller Asian economies are big

suppliers of high value-added parts and components to China, which are then

assembled and re-exported, with the US being the largest final destination. We find that

six of the top ten largest contributors of value-added to China’s exports are Asian (see

The impact of US trade protectionism, centring on China, 23 March 2017).

Trade tensions can hurt Asia through direct and indirect channels. Directly, they disrupt

the supply chain and weaken exports. Indirectly, the high policy uncertainty hurts

business confidence and results in companies delaying investment and cutting jobs.

Tighter financial conditions can accentuate the weakness in investment demand.

Two points are worth highlighting: (1) China’s growth is more vulnerable than US growth;

and (2) the indirect effects can dominate the direct effects. For instance, in a scenario of

mutual 25% tariffs on all US and Chinese exports, a 25% tariff on all US imported cars,

and including second-round effects on investment, the IMF’s model estimates a loss of

0.8% in world GDP, 1.6% in China’s GDP and 0.9% for the US, relative to baseline.

Four possible scenarios

The outcome of US-China trade negotiations, therefore, is critical in determining where

Asia is headed. As outlined in US/China: Trade tensions escalate, we present four

possible scenarios (Figure 1).

Fig. 2: US-China trade negotiation scenarios and their likely impact on Asia ex-Japan’s economic outlook

Note: Black = Positive/higher impact; Grey = Neutral; Red = Negative/lower. Source: Nomura Global Economics estimates.

Scenario 1: Deal reached – 10% probability

In this best-case scenario, even though Asian growth would remain weak in Q2, reduced

policy uncertainty, China stimulus and a major easing in financial conditions should set

the stage for both exports and the investment cycle to gradually recover in H2 2019 and

into 2020. Given benign inflation, we still expect policy easing. We currently expect rate

cuts in India (25bp in Q3), Indonesia (50bp in Q4 and 50bp in 2020), Philippines (50bp in

H2) and South Korea (25bp in Q4 and 25bp in 2020).

Scenario 2: Negotiations continue without new tariffs – 40% probability

This scenario is closer to our current base case for Asia’s economic outlook. Prevailing

policy uncertainty could delay investment until a deal is finalised in the next few

weeks/months. However, with no implementation of additional tariffs and easier financial

conditions after a deal, we would expect Asia’s growth to pick up around mid-Q3 and into

Direct

Trade

channel

Policy

uncertainty

Financial

conditions

Confidence

channel

Monetary/

fiscal policy

(vs. baseline)

Commodity

prices

Successful deal

10% No No

Positive for exports and investment. Growth to bottom in Q2;

recovery in H2 and 2020. Policy easing as per our baseline.

Asia to attract large capital inflows.

Continued

negotiation; no

retaliation

40% No No

Uncertainty to continue for a few weeks/months, but no

retaliation a positive. Growth bottoming out process to last

longer with a recovery from mid-Q3 onwards. Policy easing as

per our baseline

Delayed negotiation;

retaliation45% Yes No

Tit-for-tat retaliation to delay exports/investment recovery.

Slowdown to extend to Q3 and recovery likely only from Q4

2019 onwards. Frontloaded rate cuts likely

Deal breakdown 5% Yes Yes

Risk of consumption slowdown, on top of investment/export

slowdown. No recovery in 2019. Rate cuts to be larger in

quantum and also frontloaded. Fiscal easing, where possible.

Recovery in 2020.

Indirect Positive offsets

CommentProbability

Trade negotiation

scenarios

(Best to worse)

Will tariffs on

USD200bn be

increased

from 10% to

Will new tariffs

on USD325bn of

imports be

proposed?

Nomura | Asia Economic Monthly 10 May 2019

4

2020, setting the stage for the region to attract large capital inflows as the growth

differentials widen in its favour.

Scenario 3: New tariffs go into effect but negotiations continue – 45% probability

Initial tit-for-tat retaliation will amplify the indirect effects and extend the ongoing slump in

exports and investment into Q3. Policy uncertainty is already at a record high and bodes

poorly for investment (Figure 2). However, weaker-than-expected growth should result in

front-loaded rate cuts across Asia (versus our current baseline) which, along with

sustained easing from China, lower commodity prices and an eventual conclusion of a

trade deal will likely support an economic recovery from Q4 2019 onwards.

Scenario 4: Negotiations completely break down – 5% probability

In the worst case scenario of a deal breakdown and ongoing tit-for-tat retaliation, Asia’s

current growth slowdown would likely deepen through end-2019. Beyond the hit to

investment and exports, a bigger risk is the slowdown spills over into consumption

demand, due to lower consumer confidence and job cuts. China will step up its easing

measures and policymakers across Asia will respond with bigger stimulus in an attempt to

offset the major tightening in financial conditions. Rate cuts are likely to be both frontloaded

and larger in size than our base case. The significant easing in fiscal and monetary policies

should support a recovery in Asian export growth, but only in 2020 (Figure 3).

Winners versus losers

Nobody wins in a trade war, but trade tensions can result in more differentiation.

• Most exposed: Countries with a higher value-added component in China’s exports are

more vulnerable: Taiwan (6.3% of its GDP), Malaysia (4.1%), Korea and Hong Kong

(3.2%) and Singapore (3.1%) stand out.

• Import substitution relative winners: If companies decide to substitute production

away from China, then Malaysia would stands out as the biggest beneficiary from

import substitution, followed by Japan, Pakistan, Thailand and the Philippines (see A

US-Sino trade war is not all lose-lose: We assess the potential beneficiaries in Asia, 20

November 2018).

• Production relocation relative winners: If MNCs decide to relocate production and

FDI away from China, then we estimate that the biggest medium-term beneficiaries

would be Vietnam, followed by Malaysia, Singapore and India.

Fig. 3: Policy uncertainty and investment growth

Note: AEJ ex-China GFCF refers to the real gross fixed capital formation of Hong Kong, India, Indonesia, Malaysia, Philippines, Singapore, Korea, Taiwan and Thailand, weighted by each country’s 2018 nominal GDP. The global policy uncertainty index is published by Economic Policy Uncertainty, and is a GDP-weighted average of 20 nations’ national uncertainty indices calculating the relative frequency of news articles containing terms pertaining to economy, policy and uncertainty. See www.policyuncertainty.com. Source: Economic Policy Uncertainty, CEIC and Nomura Global Economics.

Fig. 4: China’s credit impulse versus Asian export growth

Note: China’s credit impulse is calculated by taking the 12-month change in the ratio of the 12-month change in outstanding augmented aggregate financing to the 4-quarter rolling sum of nominal GDP, after augmenting official aggregate financing outstanding by including the outstanding value of local government bonds, asset backed securities and loan writeoff. Asia ex-Japan’s exports are the aggregate exports of China, India, Indonesia, Malaysia, Philippines, Korea, Taiwan, Thailand; domestic exports of Hong Kong, and non-oil domestic exports of Singapore. Source: CEIC and Nomura Global Economics.

20

70

120

170

220

270-15

-9

-3

3

9

15

Mar-99 Mar-03 Mar-07 Mar-11 Mar-15 Mar-19

Index, 3mma% y-o-y AEJ ex-China GFCF, lhs

Global policy uncertainty (axis reversed), rhs

Higher uncertainty

-15

-10

-5

0

5

10

15

20

25

-30

-20

-10

0

10

20

30

40

50

Apr-05 Oct-08 Apr-12 Oct-15 Apr-19

% y-o-y, 3mmaPercentage points

Asia ex-Japan's exports (lagged 6 months), rhs

China's credit impulse, lhs

Nomura | Asia Economic Monthly 10 May 2019

North America Economics

Lewis Alexander - NSI [email protected] +1 212 667 9665

Aichi Amemiya - NSI [email protected] +1 212 667 9347

Robert Dent - NSI [email protected] +1 212 667 9514

Kenny Lee - NSI [email protected] +1 212 436 8146

Asia Economics

Ting Lu - NIHK [email protected] +852 2252 1306

Lisheng Wang - NIHK [email protected] +852 2252 2057

Jing Wang - NIHK [email protected] +852 2252 1011

Global FX Strategy

Craig Chan - NSL [email protected] +65 6433 6106

Wee Choon Teo - NSL [email protected] +65 6433 6107

Dushyant Padmanabhan - NSL [email protected] +65 6433 6526

Asia views

US/China: Trade tensions escalate

Assessing scenarios, economic impacts and FX strategy.

President Trump’s sudden shift in tone highlights trade risk in 2019

Over the weekend, in an abrupt departure from recent rhetoric, President Trump

threatened to raise the current tariff rate on roughly $200bn of imports from China from

10% to 25% on Friday and to apply a 25% tariff to another $325bn of imports “shortly”.

Late on Monday, USTR Lighthizer and Treasury Secretary Mnuchin confirmed that the

US is planning to impose additional tariffs on China later this week.

Chinese Vice Premier Liu He will travel to Washington on Thursday for another round of

talks that are scheduled to run through Friday.

This sudden shift highlights the continued threat that US protectionism poses to the

global economy despite the recent lull in aggressive action from the Trump

administration (see Implications from the Trump-Xi Meeting: We’ve only just begun, 2

December 2018). Trump’s pivot over the weekend likely reflects a number of factors,

including a pickup in Q1 real GDP growth, an improvement in financial markets and

strong bipartisan support in Congress. A similar dynamic may be at work for President

Xi. China’s economy is showing nascent signs of recovery, which may have encouraged

the Chinese government to take a tougher stance in its negotiations with the US.

US-China negotiations, while making progress, have slowed in recent weeks and press

reports suggest that some US negotiators view recent proposals from China as backing

away from previous commitments. Trump’s aggressive stance makes it costly, in

domestic political terms, for President Xi to offer quick concessions. The fact that

Lighthizer and Mnuchin have set a tight deadline may make it difficult to avoid another

round of US tariff increases, even if the US and China can find a way to keep talking and

ultimately reach an agreement. On the other hand, both sides are no doubt cognizant of

the high stakes of not bringing negotiations back on track. President Trump’s threatened

tariff hike, worth USD30bn (0.15xUSD200bn) would be the largest so far, and at a time

when business sentiment is fragile. Finally, the sudden turn in events over the weekend

also underscores the domestic political pressure facing both Trump and Xi.

Scenario analysis

Figure 5 lays out four possible scenarios for how US-China trade negotiations could play

out from here. We believe that there is an essentially equal likelihood that either the

Trump administration raises the tariffs on $200bn by 15pp at 12:01am EDT on Friday or

they back down after managing to quickly get back on track during the negotiations on

Thursday, consistent with the considerable uncertainty around a fluid situation.

Scenario 1: Deal reached – 10%

It is possible that the US and China will be able to reach agreement on the key elements

of a comprehensive trade deal this week. Given all of the previous negotiations this

certainly seemed possible before Trump’s tweets on Sunday. That said, this outcome

would require either the US or China to back down in a significant and very public way.

That does not seem likely in such a short period of time.

Scenario 2: Negotiations continue without new tariffs – 40%

If the negotiations make significant progress this week, it is possible that President

Trump will postpone the imposition of any new tariffs as final negotiations continue, with

the aim of both presidents signing a deal late this month or next. This is only likely if the

two sides can get very close to a deal. Again, given the preparation to date, this seems

possible, and a little extra time could reduce the negative domestic political

consequences of the concessions on both sides that will be necessary to reach an

agreement. So this seems significantly more likely that a quick agreement.

Scenario 3: New tariffs go into effect but negotiations continue – 45%

At this point, we think that both the Trump administration and the Chinese government

will have a hard timing backing down from the negotiating positions they have laid out in

the last few days. Given the solid bipartisan support Trump has received for his “tough”

Nomura | Asia Economic Monthly 10 May 2019

6

stance in these negotiations, it will be hard for Trump to back down without major

concessions from China. But Xi will not want to be seen as giving in to foreign pressure.

Consequently, we think it is likely that the Trump administration will raise tariffs by 15pp

on $200bn of US imports from China on Friday. In this case, we expect China to

implement a proportionate response essentially immediately. There is a possibility that

the Trump administration partially follows through on its threat, raising tariffs on the

USD200bn but not by the full 15pp.

That said, we believe that both sides will want to continue negotiations. The two sides

may step back for a short time but, as the negative impacts on financial markets and the

economies become more clear, we think they will have a strong incentive to keep talking

and ultimately reach an agreement. We think this is the most likely outcome.

Scenario 4: Negotiations completely break down – 5%

If the Trump administration imposes new tariffs, and China responds, it is possible that

there could be a more substantial breach. The Trump administration could start the

process of expanding US tariffs to cover essentially all US imports from China, as Trump

threatened in his tweets last Sunday. China could decide that it is not worth negotiating

with the Trump administration. This would be the most disruptive outcome to which we

assign the lowest probability.

Fig. 5: Alternative scenarios for US-China trade negotiations

Source: Nomura

Implications for the US outlook

Trump’s threat is likely an effort to gain leverage, but a quick response from China

resulting in a deal this week seems unlikely. At this point, we do not expect China to offer

material concessions before the Friday deadline for raising tariffs. It seems likely that

Trump will have to choose between imposing the tariffs he proposed or backing down.

Incoming data have strengthened in the US. US real GDP grew 3.2% q-o-q saar in Q1

and the labor market has remained solid (see Q1 GDP Growth Surprises to the Upside,

26 April 2019 and April Employment Recap, 3 May 2019). In addition, financial

conditions have eased substantially since early January. Trump’s inclination to pursue an

aggressive trade agenda has always depended on the strength of the domestic economy

and financial markets. Trump has tended to announce new tariffs during periods of

strong US growth (Figure 6).

Despite the upside surprise in Q1, US economic growth has slowed since mid-2018 and

increased business uncertainty around US trade policy, via weaker business investment,

likely contributed to some of the deceleration. Several analyses suggests that, if the

US-China trade negotiation outcome Most positive for Growth Most Negative for Growth

Scenario: 1 2 3 4

Successful deal Negotiations continue Negotiations continue Breakdown

Will a deal be announced this week? Deal No deal No deal No deal

Do negotiations continue? Concluded Yes Temporary delay Prolonged delay

Will tariffs on USD200bn be increased from

10% to 25%?No No Yes Yes

Will new tariffs on USD325bn of imports be

proposed?No No No Yes

China retaliation? No NoModerate, proportional to 15pp

US tariff hike

Strong, proportional to 15pp US

hike and 25% on $325bn

Will there be any indications of partial

suspension of exisiting tariffs?Yes No No No

Comments

It will be difficult for China to

make the concessions

necessary to reach a deal this

week.

If they make progress this week

and and are close to a deal

Trump may delay tariff

increases while negotiations

continue.

Without substantial progress

we expect tariffs on $200bn to

go up from 10% to 25%. We

expect China to respond to the

increase in tariffs but we think

both sides will want talks to

continue. The US could soften

its action by raising tariffs less

than 15pp.

If there is little prospect of

progress both side may accept

a suspension of talks. In this

case Trump could widen the

tariff increase beyond the

$200bn which would result in

stronger retaliation from China.

Probability 10% 40% 45% 5%

Nomura | Asia Economic Monthly 10 May 2019

7

current negotiations with China, or any of other the major trade developments highlighted

above, break down, the direct impact on the economy would likely be noticeable but not

overwhelming (see Incorporating Additional Trade Uncertainty into our Outlook, 19

August 2018 and Figure 11, “Estimated economic implications,” US Trade Policy

Monitor, 18 August 2018). Such developments would, however, heighten uncertainty

substantially, would would likely drag on business confidence and investment. Moreover,

financial conditions are likely to tighten in response. The deterioration in equity markets

since Trump’s tweet over the weekend highlights that vulnerability.

Trump’s actions also highlight the risk around a number of other trade policy challenges

including: (1) USMCA ratification and (2) ongoing negotiations with the EU and Japan.

For the latter, Trump faces a 18 May deadline for determining whether to impose auto

tariffs under national security grounds with the highest risk likely facing the EU. Trade

talks with Japan have generally shown progress and we believe a narrow agreement

could be reached over the next few months.

Developments between the US and China show how a sudden decision to impose

broad-based auto tariffs or to withdraw from NAFTA remain distinct possibilities.

We remain cautious on other aspect of the US trade outlook. We expect:

• The administration will remain in NAFTA in an effort to ensure that Congress ratifies the

USMCA, a key legislative priority ahead of the 2020 presidential election (see Setting

the Table for the USMCA in 2019, 9 April 2019).

• President Trump will grant the EU and Japan exemptions from any auto tariffs as talks

continue. With steady US-Japan progress we think the risk is higher for the EU.

However, concern around the economic impact and congressional anger will keep auto

tariffs at bay, for now.

Higher tariffs on imports from China will likely exert modest upward pressure on

consumer prices. Raising the tariff rate from 10% to 25% on USD200bn of imports would

add roughly 12bp on US consumer prices on a 12-month basis and 16bp on core prices

(see Update on the CPI Tariff Impact, 8 February 2019). We think higher tariffs are likely

to have an only modest direct effect on US real GDP growth, likely less than 0.1pp from

2019 y-o-y. However, as has been the case with other tariff-related uncertainty, the more

important effect will likely come from decreased business confidence impacting business

investment and tighter financial conditions.

Fig. 6: US-China trade tensions: Key dates in the context of Nomura’s GDP tracking and equity markets

Note: GDP tracking estimates from Nomura’s daily real GDP growth tracking model based on incoming data. All values for GDP shown on the left hand axis (lhs). Source: BEA, Bloomberg, Nomura

A more confident Beijing might be less accommodative on trade talks

In our view, China’s growth recovery in March and booming stock markets since late

2018 make Beijing less dovish on policy easing (see China: The Politburo turns more

cautious, but it cannot afford to stop easing yet, 22 April 2019) and less accommodative

in the China-US trade negotiations.

17000

18000

19000

20000

21000

22000

23000

24000

25000

26000

27000

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

Aug-16 Nov-16 Feb-17 May-17 Aug-17 Nov-17 Feb-18 May-18 Aug-18 Nov-18 Feb-19 May-19

Q4 2016 Q1 2017 Q2 2017 Q3 2017 Q4 2017 Q1 2018Q2 2018 Q3 2018 Q4 2018 Q1 2019 Q2 2019 DJIA (rhs)

% q-o-q, ar Index

2016election

US initiates Section301 China investigation

Section 301report released

Trump-Xi

summit

5 MayTweet

Tariff rounds (1), (2) and (3)March tariff

delay

Nomura | Asia Economic Monthly 10 May 2019

8

On the growth recovery, real GDP growth stabilized at 6.4% y-o-y in Q1, higher than

expected. The official manufacturing PMI jumped to 50.5 in March from 49.2 in February.

Industrial production growth shocked markets by surging to 8.5% y-o-y in March from

5.3% in January-February, while export growth, albeit volatile, is showing signs of

bottoming out (from -4.6% y-o-y in January-February to 5.2% in March-April). Regarding

the property sector, growth of new home sales by floor space improved to 1.8% y-o-y in

March from -3.6% in January-February (Q4 2018: -2.0%) and property investment

growth improved further to 12.0% in March from 11.6% in January-February (Q4 2018:

8.4%). Stock market sentiment turned much more bullish before May this year, with the

Shanghai Composite Index and offshore H-share index having rebounded by 23.4% and

14.0%, respectively, in the first four months this year. These big improvements in both

the economy and stock markets stand in sharp contrast to the situations last year.

The impact of additional US tariffs on China’s growth

The 10-25% additional tariff on the USD250bn worth of China’s exports to the US has

already significantly impaired China’s US-bound exports and may have already shaved

China’s year-on-year GDP growth by ~0.2 percentage points (pp) from Q2 2018 to the

period of Q3 2018 - Q1 2019. If the Trump administration raises the additional tariff on the

USD200bn worth of Chinese exports from 10% to 25% and imposes an additional 25%

tariff on the remaining USD325bn of exports, this could shave 0.6pp y-o-y from China’s

nominal GDP growth in the four quarters following the tariff hikes, based on our estimates

(only short-term direct impact is counted; see more details below). This calculation does

not include the indirect impacts from swooning financial markets and sagging business

confidence, and we may see a more severe longer-term impact if exporters, including

multinationals, shift their factories to other countries to avert the tariff hikes.

The existing tariffs significantly weighed on China’s US-bound exports…

Growth of China’s export to the US slowed sharply from 12.9% y-o-y in Q3 2018 to 6.3%

in Q4 and -9.0% in Q1 2019. As export growth was distorted by the front-loading ahead

of tariff hikes and payback afterwards, we compare the average export growth between

Q3 2018 and Q1 2019 to that of Q2 2018 to estimate the impact of the additional tariff

imposed on Chinese exports to the US. In this regard, growth of China’s exports to the

US slumped by 7.7pp from 12.2% in Q2 2018 to 4.5% y-o-y in Q3 2018-Q1 2019.

… and lowered China’s GDP growth by 0.2pp in the past three quarters

As the share of domestic value-added in total exports is ~70% and the US-bound

exports account for 3.5% of China’s nominal GDP based on 2017 data (we use 2017

data for estimates as the 2018 data may have been affected by tariff hikes), the sharp

slowdown in the US-bound exports may have shaved ~0.2pp y-o-y (=70%*3.5%*7.7pp)

off of nominal GDP growth from Q2 2018 to Q3 2018-Q1 2019. This is close to our

earlier estimate of 0.28pp on impact of tariff hikes (see China-US trade conflict: Tit-for-tat

2.0, 20 September 2018).

We estimate the impact of tariff hikes using a bottom-up approach

Our estimates rely on sectoral value-added shares of gross exports and consider the

weighted-average impact of four situations: 1) Chinese exporters are forced to cut all

exports to the US; 2) Chinese exporters wholly absorb the additional tariff costs; 3)

additional tariff costs are borne evenly between exporters and importers; and 4) US

importers fully bear the additional tariff costs. To gauge the overall impact of tariffs for

each tariff list, we assign a probability distribution to the above-mentioned four situations

(i.e., the likelihoods of the four situations are 20%, 30%, 30%, and 20%, respectively,

with situations 2 and 3 being more likely to occur) . We then estimate the weighted

average impact based on these assumptions.

Threatened additional tariffs may lower China’s GDP growth by 0.6pp

We estimate the short-term direct impact of the threatened additional tariffs on China’s

year-on-year GDP growth as follows:

• If the existing 10% tariff on the USD200bn worth of Chinese exports to the US are

raised to 25%, this could shave 0.2pp annually from China’s year-on-year GDP growth;

• If additional tariffs of 25% are imposed on the remaining USD325bn of Chinese exports

to the US, this could additionally shave 0.4pp annually from China’s year-on-year GDP

growth;

• If the above two tariff hikes are enacted at the same time, the overall negative impact

on China’s year-on-year GDP growth may reach 0.6pp (=0.2pp+0.4pp) annually.

Nomura | Asia Economic Monthly 10 May 2019

9

The longer-term impact could be more severe

It is important to note that our above-mentioned estimates for China only focus on the

short-term direct impact of tariffs and are silent on the longer-term impact, which we

believe could be much more severe. Specifically, there could be bigger indirect impacts

through rising uncertainty, especially when considering mounting domestic challenges

(more credit defaults, a problematic property sector and overloaded debt). Moreover,

rising trade tensions may seep into investment, as exporters, including multinationals,

could shift their factories to other countries to avoid the tariff. Consequently, in the

medium-to-long term, if China-US trade tensions sustain, China’s growth would likely be

hit beyond the scale indicated by these estimates.

How will China respond if the US increases tariffs?

If the US announces tariffs hikes on USD200bn of China’s exports to the US, China will

almost surely retaliate with tit-for-tat tariff hikes. In addition to tariff hikes, we believe

there is an increasing likelihood that some non-tariff measures will be used. Below, we

list some measures that could be employed, as well as those that seem very unlikely to

be taken. In our view, a number of recent signs indicate that Beijing has started to rethink

its strategy and stance in positioning itself in the global economy. In our opinion, rationality

and practicality will dominate Beijing’s policymaking circle, and Beijing is very unlikely to

turn to populist approaches to boycott US products and harass US business in China.

A list of possible retaliatory measures

• There is high likelihood of tit-for-tat tariff hikes. In the worst case, China could impose

an additional 25% tariff on most of its imports from the US (except those for mere

intermediate goods). Between July and December 2018, China has imposed three

rounds of retaliatory tariff hikes, ranging from 5% to 25%, on the USD110bn worth of

imports from the US. Based on 2017 data, the targeted imports from the US with

additional tariff account for 71.4% (=USD110bn/ USD154bn) of total imports from the

US. Among the USD110bn worth of imports, USD50bn imports are subject to tariff

hikes of 25%, while the remaining USD60bn are exposed to tariff hikes of either 5% or

10%, according to different tariff lists. However, the 5-25% tariff hikes on imported auto

and auto parts from the US were suspended on 1 January 2019, following the Trump-Xi

summit last December.

• Non-tariff barriers such as setting import quotas, raising barriers of entry into the

Chinese market for US companies and products, and/or complicating customs

processing for US imports. The Chinese government can even directly order importers,

especially those owned by the state, to slash or stop importing goods and services from

the US.

• Last year, Beijing allowed RMB to depreciate against the USD right after the US

initiated the trade war. In the past six months, despite a strong USD, RMB first

appreciated against USD and then was pegged at around 6.7. Based on our estimates,

RMB appreciated by around 3.7% against its trading partners between November 2018

and April 2019. If the US hikes tariffs on its USD200bn of imports from China, China

would likely allow RMB to depreciate against the USD towards 7.0, in our view.

• Limits/restrictions on Chinese nationals travelling or receiving education in the US:

despite its merchandise trade surplus with the US, China has a consistent deficit on

service trade. Chinese nationals’ overseas spending has been welcomed by many

countries, and has helped to boost growth of recipient economies. A ban on traveling

and receiving higher education in the US would be negative for the US economy,

though the impact may not be as significant as the ban on tourism to South Korea.

• Subsidies to those Chinese enterprises affected by additional US tariff hikes: industrial

subsidies have been a frequently and widely cited example of unfair trade treatment

when countries apply for trade sanctions or other protectionist measures. So we view

the likelihood of this measure as rather slim.

Measures unlikely to be employed

• Heavy selling of US treasuries. We think this is very unlikely, as falling prices of US

treasury securities would also be a loss for China, as it is the largest foreign holder of

US treasury bonds. In addition, we believe it would be very difficult for China to re-

invest its US dollar holdings in a sensible way after selling US Treasuries. That said,

another less aggressive option for China might be to cease purchasing additional US

Treasuries.

• Instigating a boycott of US products by Chinese nationals. This also seems very

unlikely, since US products are sold all over China, including chips in almost all

Nomura | Asia Economic Monthly 10 May 2019

10

computers. Based on our observations, Chinese nationals overall do not seem to be

unduly prejudiced against the US, as evidenced by the soaring number of Chinese

students studying in the US. According to the Institute of International Education, for

the past eight years, China has been the largest source of foreign students in the US,

and, in mid-2017, Chinese students comprised 32.5% of the total 1.08mn foreign

students in the US.

• Harassing US business based in the China. We believe this is unlikely, as it is in

China’s interest to woo US businesses to support domestic growth and improve the

economic structure. China may even take advantage of its significant domestic market

and the US trade tariff by attracting US firms to produce in China to bypass the tariff.

Beijing may keep and even sustain its easing measures

How would China ease the pain if the trade war with the US escalates? Despite our

much more cautious stance on policy stimulus, we believe Beijing cannot afford to stop

easing yet. Also, if the trade war escalates, Beijing could very likely step up its easing

measures. On this point, we note that right after Trump’s tariff threats on 5 May, the

People’s Bank of China (PBoC) announced a targeted reserve requirement ratio cut,

effective 15 May, to inject ~RMB280bn to small banks to favor the financing of small and

medium-sized enterprises and private enterprises (see China: The PBoC announces a

targeted RRR cut after Trump’s tariff threat, 6 May 2019).

We expect the PBoC to continue adding liquidity to the banking system, with a

combination of high-profile RRR cuts (we expect a total of 100bp RRR cuts through the

rest of this year) and low-profile lending facilities such as medium-term lending facility

(MLF), targeted MLF (TMLF), pledged supplementary lending (PSL), re-lending and re-

discounting. If China’s stock markets drift lower due to a worsening trade conflict, the

PBoC would likely use high-profile RRR cuts again to add liquidity. We maintain our call

for 100bp in total RRR cuts over the remainder of this year.

On the fiscal side, with the value-added tax cuts and social security tax cuts coming into

effect on 1 April and 1 May, respectively, we expect fiscal stimulus to continue in coming

quarters. However, if China’s export growth is hit significantly by the escalation of the

trade conflict, China may have to rely more on infrastructure to stabilize growth. As such,

Beijing may have to give local governments more flexibility on funding via off-budget

channels, including local government special bond issuance, local government financing

vehicles and public-private partnership programmers (see China: Infrastructure not a

quick fix; Beijing could be bolder on fiscal deficit, 18 January 2019).

On consumption stimulus, Beijing could speed up the introduction of its stimulus plan for

the auto sector if there is a further escalation of trade war (see China: The NDRC plans a

new round of consumption stimulus, 17 April 2019).

On the property sector, the Chinese government now is in a wait-and-see mode after

allowing some easing measures in the past couple of months (see China’s property

sector: A recovery is in the making thanks to policy easing, 3 April 2019). We believe

that, if the trade war worsens, Beijing will step up its easing measures in the property

sector. Since late 2018 Beijing has shifted its stance on the property sectors in large

cities, from a broad-based tightening to “one policy for one city” and “city-specific polices

based on local situations”, which essentially granted local governments more discretion

in formulating their own property policies. Against this backdrop, we have seen a couple

of cities start to ease their local property-related policies in recent months and, thanks to

recent policy easing, we have seen a recovery in the property sector, especially in large

cities (see China’s property sector: A recovery is in the making thanks to policy easing, 3

April 2019).

Nomura | Asia Economic Monthly 10 May 2019

11

RMB: Strategy views around the upcoming US-China talks

The near-term risks around US-China trade negotiations are substantial in that they

could lead to significant moves in USD/RMB (possibly to/test 7.0 or fall below 6.70) and

impact on other global markets. As we highlight in US/China trade: Trump adds

uncertainty to trade talks, 6 May 2019, given growing uncertainties and the risk of sharp

RMB depreciation, we decided to buy a short-dated 2W 6.83 USD/CNH calls (expiry 20

May 2019; 31.2bp) as a partial hedge to our overall long CNH position. We further add to

this position through buying a 1W 6.835/6.73 risk reversal (notional: USD10m; expiry: 15

May 2019).

We believe the next risk before US-China trade talks begin (9-10 May) is the USTR

through the Federal Register formalizing the tariff increase to 25% (from 10%) on

USD200bn of imports from China (12:01am EDT; 10 May). This could emerge soon to

further pressure China, which would add further to the uncertainty in the market, even

though the tariff increase could still be rescinded before the proposed start time/date

despite this formalization.

A close call on tariffs; we assign a 50% aggregate likelihood…

Overall, even though the probabilities suggested by our four scenarios indicate the US

raising tariffs on USD200bn of China imports to 25% this Friday is an extremely close

call (total 50% probability), the scenario to which the global research team assigns the

highest probability (45%) is scenario 3 (Figure 5). In this scenario, the US raises tariffs to

25% on USD200bn of imports from China on Friday, China retaliates, and negotiations

are temporarily delayed.

… but scenario 3 – where additional tariffs are imposed – is the single most likely

scenario…

We expect that, if the tariff hike is recorded in the Federal Register to become effective

(could be anytime), then the market will increasingly shift its view towards this negative

scenario 3 (45%) amid a lack of public statements indicating a further delay or a

rescinding by Thursday earlier afternoon (EDT). This could lead spot USD/CNH higher

by around 50bp initially and, once the tariffs become effecting, we would expect

USD/CNH to rise above 6.90 soon thereafter (100bp above current levels). However,

given we would expect China to eventually retaliate and China/global markets to face

notable selling pressure, we believe USD/CNH rising back to and potentially testing

7.0 would become the consensus view. Indeed, even if the PBoC were to intervene to

prevent a further sharp sell-off, the depreciation forces would likely be significant and the

PBoC would likely end up allowing for some sporadic depreciation in part to avoid a

sharp draining of FX reserves. Authorities could also allow for greater RMB flexibility (as

seen in the 5.6% CFETS depreciation from mid-June 2018-end July 2018) to offset the

negative impact from the additional tariffs.

We would see a setback in foreign portfolio inflows (likely net outflows worse than those

experienced at the end of 2018), local corporates hoarding foreign currency (especially

exporters), and increased risk of a pickup in local diversification into foreign assets (E&O

outflows, tourism spending, FDI outflows etc.), all of which would imply a further

clamping down on channels of local capital flight (see Asia Insights - The major drivers of

RMB, 15 April 2019).

… with scenario 2 of no additional tariffs and continued negotiations being the

next highest probability…

Scenario 2 (40%) is one where the US and China are able to pick up discussions from

the previous agreements, leading to no additional tariffs, but there is a delay in the timing

of a deal. Although the risk of Trump ordering a tariff hike remains, it becomes less likely

as talks get back on track (US Treasury Secretary Mnuchin comments; CNBC and NYT;

6 May). This scenario of no imminent tariffs and an extension to the timing of a trade

deal (assuming continuous progress/trade delegation meetings) would likely provide

some relief to RMB/broad risk markets, but we do not believe there would be any sharp

CNH appreciation momentum, even if USD/CNH is likely to fall back to around 6.75.

… and the best outcome and worst outcomes are tail events

We believe the best case for risk markets/RMB (scenario 1; 10%) is if the US-China

trade delegation are able to strike a trade deal this week that leads to US President

Trump stepping away from his threat to hike tariffs. We assigned a 10% probability to

this, but such an outcome would lead to relatively sharp near-term appreciation with

USD/CNH likely to fall back towards and test 6.70-levels. The details of the deal

Nomura | Asia Economic Monthly 10 May 2019

12

would be the next focus, with a roll back in some of the tariffs, FX agreements and

liberalization likely to add to the rationale for likely more favourable overall flow conditions.

That said, we also assigned a 5% probability to scenario 4, which is the most negative

outcome with tariffs rising to 25% on the USD200bn of China imports, a risk of tariffs

imposed on the remaining USD325bn of imports from China (highlighted by Trump),

retaliation from China and a prolonged delay in trade talks. This scenario would likely

result in a more sustained break of USD/CNH through 7.0, even if there are periods of

sporadic FX USD selling intervention and other actions to stabilize RMB.

Trade details:

Buy 1W 6.835/6.73 USD/CNH RR (notional: USD10mn; i.e., buy 1W 6.835 USD/CNH

call, sell 6.73 USD/CNH put; expiry: 15 May 2019; premium: 8.7bp or USD8.7k; spot ref:

6.7884).

Please see FX Portfolio Update - FX Portfolio Performance (2 May 2019) for a full list of

our recommendations.

This report was originally published on 8 May 2019.

Nomura | Asia Economic Monthly 10 May 2019

13

Asia Economics

Ting Lu - NIHK [email protected] +852 2252 1306

Lisheng Wang - NIHK [email protected] +852 2252 2057

Jing Wang - NIHK [email protected] +852 2252 1011

China monthly: Beijing can’t afford to stop easing yet, as double dip is a real risk

Even room for credit easing seems much smaller.

In the past month there seems to have been a big shift in markets’ perceptions on

China’s growth momentum and Beijing’s policy stance. China’s economy staged a major

comeback in March with the official manufacturing PMI jumping to 50.5 in March from

49.2 in February and industrial production growth spiking to 8.5% y-o-y in March from

just 5.3% in the first two months. Having been encouraged by the rebound, Beijing

surprised markets by swiftly fine-tuning its monetary easing stance through re-

mentioning “deleveraging” and “keeping money supply under control”. For most

investors, the euphoria of surging stock prices, falling bond yields, a recovering economy

and accommodative policies seems to be too short. In our view, investors are

questioning whether the growth recovery is sustainable, whether Beijing is en route to

scaling back its policy easing, and if China’s economy will dip again if Beijing’s ending of

easing measures turns out to be premature.

In our view, the surprisingly big rebound in March activity data is unsustainable, growth

has yet to truly bottom, and the actual slowdown since mid-2018 could be significantly

worse than what official statistics have indicated. The dash of stimulus played a key role

in pushing up the data in March, which is the first month following the Lunar New Year

(LNY) holiday, but the rapid improvement in March data were also a result of some

temporary special distortions: 1) the moving LNY holidays; 2) the front-loading as a result

of the value-added tax (VAT) cut that was announced on 15 March to take effect on 1

April and 3) the anti-smog campaign from November 2017 and March 2018. For April,

some data such as PMI could continue to rise, but we expect some important data such

as industrial production growth and export growth to drop again.

Re-examining our views: What we got right and wrong

Before March this year, our views could be summarized as: 1) China’s growth slowdown

could be worse in H1 2019 due to synchronised demand shocks; 2) Beijing has less

scope for policy easing; 3) the growth slowdown could last longer; 4) credit easing is

necessary, but alone is not sufficient to drive a growth recovery and 5) deregulation of

the property sector is needed to deliver a full recovery of the economy (see China:

Economic growth needs more than money and credit to recover, 26 February 2019). In

hindsight, we were correct on being bearish on growth in 2018 and the first two months

in 2019, but too pessimistic on March activity data as we underestimated the dash of

stimulus. The property easing, which played a key role in bolstering growth in Q1 and

March, was implemented earlier than we had projected, but we were correct in

emphasising that the room of policy easing is more limited in this cycle than before. We

also correctly flagged that policymakers may have learned from the stock market crash

in 2015, thus they are keen in adjusting policy measures to avert another bubble and

crash in stock markets.

Beijing’s constraints: Limited room for monetary/credit easing

In our opinion, the key to understanding Beijing’s recent change in policy stance is to

acknowledge its constraints (see China: Deja vu? This time the easing cycle might be a

bit different, 15 August 2018). Compared with previous easing cycles, there seems to be

much less room for easing and stimulus this time around because of surging debt, a

much smaller current account surplus and falling FX reserves, while the decision-making

process is longer owing to the lack of consensus on direction and strategy. Another key

factor that may have been easily dismissed is that Beijing’s last significant stimulus

campaign was introduced only four years ago after the stock market crash in 2015.

Having spent significant monetary and fiscal easing capacity just a few years ago,

authorities may find that they have more limited room to launch another stimulus/easing

campaign in this cycle.

Some strong headwinds still exist

Other than those short-term distortions, we believe activity data could face some

downward pressure in coming months from the following headwinds:

Nomura | Asia Economic Monthly 10 May 2019

14

• A very high debt repayment pressure in 2019 due to the credit easing in 2015-16. Due

to a limited room of monetary easing, a rebound in financing costs could weigh on

growth recovery very soon.

• Exports could be still under strong downward pressure as the global economy is

slowing, the RMB could be increasingly overvalued with a new round of monetary

easing, and there may still be some payback after the front-loading of exports in

previous quarters.

• The stimulus-driven boom of small city property markets is coming to an end (see

China’s property sector: Winter is coming, 15 November 2018).

• The replacement cycle of durable goods such as construction machinery is over, while

the sharp slowdown of auto sales could also extend into coming months.

Beijing can’t afford to stop easing yet

Despite our much more cautious stance on policy stimulus, we believe Beijing can’t

afford to stop easing yet. The Chinese Communist Party’s Politburo, the country’s de

facto top decision-making body, convened on 19 April and issued a briefing after its

meeting. The slight change in the Politburo’s tone on monetary easing confirms our long-

held view that the room for monetary easing is much more limited in this easing cycle,

and Beijing may need to rely more on other policy measures to bolster growth. However,

we believe the growth recovery is as yet not solid despite the rebound in March data,

and there could be a double dip in the next few months. We believe the pace of

monetary easing will slow, but it still seems too early to withdraw monetary easing

measures despite the limited monetary policy scope.

More specifically, we expect the People’s Bank of China (PBoC) to continue to add

liquidity to the banking system, though it might replace those high-profile tools such as

reserve requirement ratio (RRR) cuts with low-profile tools such as medium-term lending

facility (MLF), targeted MLF (TMLF), pledged supplementary lending (PSL), re-lending or

other facilities (see China: The PBoC injects cheaper base money via targeted MLF, 24

April 2019). It’s still quite likely that Beijing could stimulate demand on other fronts,

especially on the severely hit auto sector (see China: The NDRC plans a new round of

consumption stimulus, 17 April 2019).

This is an excerpt from China monthly: Beijing can't afford to stop easing yet, as double

dip is a real risk, originally published on 26 April 2019.

Nomura | Asia Economic Monthly 10 May 2019

15

Asia Economics

Ting Lu - NIHK [email protected] +852 2252 1306

Lisheng Wang - NIHK [email protected] +852 2252 2057

Jing Wang - NIHK [email protected] +852 2252 1011

China: The Politburo turns more cautious, but it cannot afford to stop easing yet

The Chinese Communist Party’s Politburo, the de facto top decision-making body in

China, convened on 19 April and issued a briefing after its meeting. In line with the

briefing of the PBoC’s Q1 Monetary Policy Committee meeting (see China: The PBoC

sounded a cautious tone at its quarterly MPC meeting, 16 April 2019), the Politburo has

turned more bullish on the economy and less dovish on monetary easing. It has called

for more focus on improving efficiency of fiscal stimulus and pushing forward structural

reforms. Markets could interpret this Politburo briefing as the end of Beijing’s monetary

easing and may turn significantly bearish on asset prices. We beg to differ.

The slight change in the Politburo’s tone on monetary easing confirms our long-held view

that the room for monetary easing is much more limited in this easing cycle, and Beijing

has to rely on other policy measures to bolster growth (see China: Economic growth

needs more than money and credit to recover, 26 February 2019). The slight change in

tone is understandable due to the rapid build-up of debt and a potential irrational

exuberance in stock markets and big cities’ property markets. However, we believe the

growth recovery is not solid yet despite the rebound in March data, and there could be a

double dip in the next few months. We believe the pace of monetary easing will slow, but it

is still too early to withdraw monetary easing measures despite the limited monetary

policy scope. More specifically, we expect liquidity injections through a targeted RRR cut

or other facilities, as we believe Beijing cannot afford to let financing costs rise at the

pace of the past two weeks (see China: A targeted RRR cut is in the making, 18 April

2019).

Highlights of the Politburo’s briefing

• The briefing said that the economy is off to a good start and is better than expectations.

While acknowledging the growth headwinds, the Politburo claimed those are more

structural than cyclical, and required more structural reforms and market liberalisation.

• Compared with its previous briefing, the Politburo removed the call for “stabilising

employment, financial markets, foreign trade, investment, foreign capital and market

expectations”, suggesting so far it is satisfied with the stability in growth and financial

markets.

• On policy, compared with the last briefing, the Politburo further qualified its prudent

monetary policy “with an appropriate degree of intensity” (in line with the PBoC’s Q1

MPC meeting’s briefing). It reiterated a proactive fiscal policy but highlighted the need

for higher efficiency.

• The Politburo brought back the requirement of “structural deleveraging” after dropping it

in its October 2018 briefing.

• After finding no mention since the October 2018 meeting, property markets were re-

emphasised by the Politburo this time. In the briefing, the Politburo added back the line

“homes should be for living in, not for speculation”.

Beijing is right to be cautious, but too premature a withdrawal is not good

We have long argued that Beijing’s monetary easing room is quite limited this time

around due to the too rapid build-up of debt, a rise in foreign debt, a fall in FX reserves,

an expected current account deficit this year, a sharp decline in return on investment and

the need to stabilise RMB (see China: Deja vu? This time the easing cycle might be a bit

different, 15 August 2018). However, too premature a stop after an all-out campaign to

push up credit growth could do unnecessary harm to both growth and financial markets.

In our view, Beijing cannot afford to slam on the brakes regarding monetary easing, and

the Politburo merely strikes a cautious tone, partially because: (1) it has taken lessons

from 2015 when its credit easing instigated stock market mania and a crash, as well as a

surge in property prices; (2) it is really concerned about too rapid debt growth and

realises all the constraints that it faces.

The recovery is not solid, and a double dip is likely

Despite the Politburo’s more sanguine growth outlook, we see China’s economy still in a

tug-of-war between headwinds and policy easing. While it is true that some parts of the

economy are recovering and we have seen evidence of green shoots, we also need to

keep in mind that the global economy is slowing, property markets in lower-tier cities

Nomura | Asia Economic Monthly 10 May 2019

16

could continue to fall, exports may weaken further and sales of some durable goods –

such as cars, construction machinery and even mobile phones – are under heavy

pressure. In our view, it is still too early to say whether growth has fully recovered and

policymakers can remove policy easing measures.

The jump in industrial production (IP) growth in March was partly due to a low base

related to the anti-smog campaign (see China: The anti-smog campaign likely less in

force this winter, 19 September 2018) and more export-oriented production boosted by

value-added tax (VAT) cuts, as exporters likely sped up custom clearing in March to

avoid a reduction in VAT rebates in April (see China: Export growth surged while import

growth slumped in March, 12 April 2019). As the effects of these factors are likely to be

one-offs and reverse in coming months, headline year-on-year IP growth should

moderate in April and May.

Despite these policy-related distortions which boosted March activity growth, we are still

seeing a raft of bad readings such as: (1) growth of auto sales in volume terms slowed to

-11.7% y-o-y in March from -9.7% in January-February (Q1 2019: -10.4%; Q4 2018: -

16.9%; full-year 2018: -5.8%); (2) import growth in USD terms dropped to a worse-than-

expected -7.6% y-o-y in March from -3.2% in January-February (Q1 2019: -4.8%; Q4

2018: 4.4%; full-year 2018: 15.8%), reflecting still-weak domestic demand; (3) land sales

(by volume) continued to contract in March, with growth remaining sluggish at -31.5%

y-o-y in March, despite an uptick from -34.1% in January-February (Q1 2019: -33.1%;

Q4 2018: 11.4%; full-year 2018: 14.2%); and (4) the monthly average operating ratio of

blast furnaces moderated to 63.8% in March from 65.3% in January-February (Q1 2019:

64.8%; Q4 2018: 67.0%; full-year 2018: 67.2%).

We believe the economy has yet to fully recover, the credit easing cycle is shorter and

smaller than before and the incoming growth recovery should also be shorter and

smaller. We also believe the PBoC will continue to ease, but the intensity and the pace

of policy easing measures will be quite data dependent, and the PBoC will struggle with

worsening data quality when assessing and predicting economic conditions. The PBoC

has to balance policy easing with the need to control financial risks, given the rapid rise

of debt and very volatile stock markets, but we believe it is too early for it to withdraw

policy easing measures. We expect credit growth, defined as year-on-year outstanding

augmented aggregate financing (AAF) growth, to slightly tick up further and stay in an

11.0-11.5% range this year.

The Politburo on the property sector

Compared with the July 2018 meeting, where it had vowed to prevent too rapid a rise in

property prices, the Politburo this time did not mention property prices. Instead, it called

for more forceful implementation of the “one policy for one city (一城一策)” and “city-

specific polices based on local situations (因城施策)” pilot programs. Also, it highlighted

the municipal governments’ responsibilities in managing the local markets to prevent

speculation. As “one policy for one city” grants local governments more discretion to

formulate their own property policies, we view this as an easing signal (see China’s

property sector: A recovery is in the making thanks to policy easing, 3 April 2019).

More policy support for SMEs and private enterprises, more market reforms

The Politburo recognised the need for more policy support to private enterprises and

small- and medium-size enterprises (SMEs), in line with the tones of recent policy

meetings (see China: President pledges to better support the private sector, 2 November

2018). Moreover, it emphasised some key points related to reforms and market

liberalisation, including 1) a stabilisation of growth should be more reliant on high-quality

growth of the manufacturing sector; 2) a truly registration-based IPO system should be

implemented at the science and technology innovation board; 3) the liberalisation of

domestic markets and the lowering of entry barriers to foreign investments should

continue, to deepen reforms; and 4) more efforts should be made for poverty alleviation

and production safety.

This report was originally published on 22 April 2019.

Nomura | Asia Economic Monthly 10 May 2019

17

Asia Economics

Ting Lu - NIHK [email protected] +852 2252 1306

Lisheng Wang - NIHK [email protected] +852 2252 2057

Jing Wang - NIHK [email protected] +852 2252 1011

China: The NDRC plans a new round of consumption stimulus

Targeting auto, home appliance and electronics.

On 11 April, the National Development and Reform Commission (NDRC), China’s top

planning agency, distributed a draft to seek feedback on its proposed stimulus measures

for auto, home appliance and consumer electronic products. These proposed measures,

if implemented, will officially kick off a new round of consumption stimulus. Unlike some

informal talks over the past few months (see China: Policies targeting auto and home

appliance sales may have limited impact, 15 January 2019), the proposed stimulus by

the NDRC is material, as it would cut the purchase tax by half for rural residents and

double the quota for new vehicle licences in some major cities. The NDRC’s draft itself

suggests Beijing is still quite concerned about the growth slowdown, despite GDP growth

seemingly stabilising in Q1 and the jump in activity data in March (see China: Growth

stabilised in Q1, March activity data displayed a recovery, 17 April 2019).

Assessing the potential impact of this consumption stimulus

The proposed stimulus might be smaller in scale than the previous two consumption

stimuli (one started in January 2009 amid the global financial crisis, and the other started

in October 2015 after the stock markets crash amid a severe growth slowdown). We

expect sales of auto and home appliances to benefit from the stimulus in 2019 and 2020,

and a rebound in auto and home appliance sales growth should help to deliver a real and

more sustainable growth recovery. Acknowledging the previous stimulus for auto

purchases was implemented as recently as 2015-17, we believe the impact of the

incoming stimulus on auto sales could be smaller, as those that bought cars in 2015-17

may not need to buy new ones. However, a frontloading of some consumption demand

of durable goods in 2019-20 will inevitably result in a payback in 2021.

The NDRC’s proposed measures for boosting auto purchases

In the NDRC’s draft plan, we see a few policy measures worthy of additional attention:

• Local governments are prohibited to roll out new restrictions on auto purchases.

Existing restrictions are required to be relaxed in a gradual manner. Specifically for

those cities imposing quotas on vehicle licenses, these quotas should be raised by

50% and 100%, respectively, in 2019 and 2020, from the level in 2018.

• For rural citizens, the vehicle purchase tax is cut by half until end-2020 for the

purchases on small-engine cars (1.6L or below) and the replacement of motorized

rickshaw for small trucks (3.5 tons or below).

• No purchase bans should be imposed for households without car ownership.

• For cities imposing restrictions for vehicle licenses, these restrictions should be lifted for

non-congestion areas.

• No restrictions should be imposed for the use and purchase of new energy cars.

• To support the use of new energy cars, state-owned enterprises and state entities are

required to install a minimum number of charging stations, which accounts for 10% of

the number of parking lots.

• Local governments are encouraged to lower the toll fees by half for new energy cars.

• Removal of entry bans on used non-local autos.

The NDRC’s proposed measures for supporting sales of home appliances

There are many details in the NDRC draft, but we found the following most relevant: A

maximum of 13% discount off the prices will be subsidised for the purchases of new eco-

friendly and intelligent home appliances, which are backed by the China Compulsory

Certification (CCC) and above the grade II energy efficiency. The subsidy for each unit of

home appliance is capped at RMB800.

A short history of auto-related stimulus in the past decade

The sector is already one of the country’s pillar industries. Auto production involves a

variety of inputs from other sectors, including steel, metals, fuels, plastics, rubber, glass

and electronics. In 2017, the gross industrial output of the auto sector was RMB3.6trn.

Netting out the value of imported auto parts at RMB250bn, the auto sector contributed

~4.0% (=RMB3.3trn/RMB82.7trn) to nominal GDP.

Nomura | Asia Economic Monthly 10 May 2019

18

As the auto sector is becoming increasingly important, it has been a recipient of Beijing’s

largesse when forced to boost growth. During the 2008 Global Financial Crisis (GFC),

passenger car sales in volume terms plunged to 0.5% y-o-y in Q3 2008 from 10.6% in

Q2. In January 2009, the State Council lowered the purchase tax on small-engine cars

(1.6L or below) from 10% to 5% for 2009 and to 7.5% for 2010. Auto sales growth

instantly spiked to 54.7% y-o-y in 2009, from 7.7% in 2008, before moderating to 32.0%

in 2010 and to 6.2% in 2011.

In 2015, this stimulus was essentially repeated after stock markets crashed in late June

amid a severe growth slowdown. With auto sales growth plunging to 2.4% y-o-y in Q3

from 17.8% in Q1 2015, the State Council in September that year adopted the same tax

cut scheme as in 2009: the purchase tax on small-engine cars was reduced to 5% from

10% for the period October 2015-December 2016, and to 7.5% in 2017, before being

raised back to 10% in 2018. Auto sales growth surged to 16.3% y-o-y in Q4 2015 and to

18.5% for 2016.

The ongoing slowdown of auto sales

According to the China Passenger Car Association (CPCA), growth of passenger car

sales in volume terms slowed to -11.7% y-o-y in March from -9.7% in January-February

(Figure 7), taking Q1 growth to -10.4% y-o-y from -16.9% in Q4 2018 and -9.2% in Q3

2018. To smooth out some distortions, the average growth of auto sales in Q1 2019 and

Q4 2018 was -14.1% y-o-y, much lower than -9.2% in Q3 and 3.3% in Q2 2018

(2018: -5.8%). Based on the weekly sales data from 1-12 April reported by the CPCA,

our estimate of the April auto sales growth (by volume) is tracked at -33.8% y-o-y, much

weaker than the -11.7% reading in March.

The ongoing slowdown was due mainly to the stimulus in 2015-17. A decade ago, when

the car ownership penetration ratio was so much lower, this stimulus had a much larger

and longer-lasting impact. With an ever-increasing penetration ratio, as is typical of

consumer durables, high sales in the past are negative for sales in the immediate future.

The 2016-17 tax cut front-loaded sales, with the payback seen, and expected, in 2018-

19. According to the CPCA, growth of passenger car sales in volume terms tumbled

to -19.2% y-o-y in December 2018, taking annual growth to -5.8% in 2018 from 2.0% in

2017 and 18.6% in 2016, the first annual auto sales contraction in two decades. Other

factors may also have contributed to the slump. The collapse of auto financing through

P2P lending (see China monthly: The dramatic rise and fall of online peer-to-peer

lending, 30 August 2018) could also have had an impact on car sales.

How big is the impact of the proposed stimulus?

Given the limited information, it’s hard to quantify the impact of the incoming stimulus on

auto purchases. Compared with the two previous stimuli, the incoming stimulus is

weaker on the following fronts:

• The incoming purchase tax cut is limited to rural citizens. Note 57.6% of China’s

1.395bn population are rural citizens based on the Hukou system. Also, according to

the National Bureau of Statistics (NBS), the average disposable income of rural

residents in 2018 was just RMB14617, way below the RMB39251 disposable income of

urban residents.

• The 50% purchase tax cut is effective in coming quarters until end-2020, which is likely

longer than the 15 months in the 2015-2017 stimulus and 12 months in the 2009-10

stimulus. The longer the stimulus period, the smaller the impact for the current year.

• The previous stimulus was just as recent as in 2015-2017. The durable goods

characteristics of cars suggest the impact of another purchase tax cut could be much

smaller.

• China’s car penetration ratio is now 175 per 1000, from 118 back in 2015 when the

purchase tax was last cut. The higher penetration ratio also suggests that a new round

stimulus would have smaller impact.

However, other proposed measures could deliver bigger impact than the previous two