2018 Employee Enefit Guide - My Benefithelp...

28

2018 EMPLOYEE BENEFIT GUIDE VERSO BENEFITS GROUP 2018 Annual Enrollment November 3-17, 2017 www.MyVersoBenefits.com

Transcript of 2018 Employee Enefit Guide - My Benefithelp...

1

MyVersoBenefits.com

2018 EMPLOYEE BENEFIT GUIDE

VERSO BENEFITS GROUP

2018 Annual Enrollment November 3-17, 2017

www.MyVersoBenefits.com

2

MyVersoBenefits.com

3

MyVersoBenefits.com

WELCOME

Make Every Moment Count

Annual Enrollment is your once a year opportunity to review your benefits and make new

choices for the coming year. Verso is committed to offering affordable, competitive, quality

benefit options for you and your dependents.

It is no secret that health care costs continue to climb. As the health care landscape continues

to evolve, we must evolve with it. This means all of us need to take personal responsibility for

managing our benefit dollars wisely to help keep costs in check for our families. Taking an

active role in understanding, utilizing and purchasing health care services not only helps us get

the most value for our health care dollars, but also helps Verso manage overall benefit costs

more effectively and helps keep insurance premiums as low as possible.

Your benefit choices are important decisions that affect how you receive benefits and how

much you pay for them. Please take time to fully understand Verso’s benefit plans available in

2018. The elections you make during Annual Enrollment will be effective January 1, 2018, and

will remain in place for the entire year. You can only change your benefits during the year if

you have a qualified change in status, such as a marriage, birth, divorce, etc.

What’s in This Guide?

4 Benefit Changes for 2018

5 Enrollment for Plan Year 2018

6 Core Benefits

15 Other Benefits

16 Voluntary Benefits

18 Eligibility and How to Enroll

20 Important Rights and Information

28 Contacts

This guide is intended to provide a summary of benefits offered to employees. In determining actual benefit coverage and

eligibility, the official text of the legal plan document (including any insurance contracts and other coverage documents) are the

governing source. For more information about the coverage described in this guide, refer to the Summary Plan Descriptions and

other booklets.

4

MyVersoBenefits.com

BENEFIT CHANGES FOR 2018

TELEMEDICINE BENEFIT

Telemedicine allows you to

visit with a doctor remotely.

No need to schedule an

appointment, travel to your

doctor’s office or wait for your

appointment. You can do it all

through a mobile application

or a phone call. Physicians

can treat common issues and

prescribe medications – all

done remotely and generally

at a lower cost than a

traditional office visit.

HSA CORE PLAN

The new HSA Core Plan has

lower premiums, the

opportunity to earn wellness

credits and a higher

deductible than the HSA

Choice Plan. This HSA Core

Plan gives you more flexibility

and accountability to decide

how to receive health care

services and how to spend

your health care dollars.

HSA PLAN RENAMED

TO HSA CHOICE PLAN

The HSA Plan will be renamed

the HSA Choice Plan. The new

name reflects our expanded

HSA medical plan offerings.

HRA PLAN ELIMINATION

Effective January 1, 2018, the

HRA Plan will no longer be

offered as a medical plan.

SURCHARGES

Verso will implement

surcharges for tobacco users

and working spouses who

have access to other health

care coverage.

STD PLANS

HARMONIZED

All non-represented

employees will move to a

common Short-Term

Disability (STD) plan

design.

TAXABILITY OF

VOLUNTARY AFLAC

BENEFITS

The deductions for all

voluntary Aflac benefits

will be from post-tax

rather than pre-tax dollars

in 2018.

TOBACCO / NON

TOBACCO RATES FOR

LIFE INSURANCE

Voluntary life insurance

rates now reflect

separate rates for

tobacco users and non-

tobacco users.

HEALTH CARE FSA

NOT OFFERED

Because Verso will only

offer HSA compatible

health care plans in 2018,

the Health Care Flexible

Spending Account (FSA)

will no longer be

available.

HSA DOLLARS

Verso will continue to

contribute to your Health

Savings Account (HSA). Part

of the reward will be in the

form of a matching

contribution and you will be

able to earn the other portion

through activities designed to

help you focus on your health.

HSA CHOICE PREMIUM

AND DEDUCTIBLE

CHANGES

Payroll deductions and

deductibles for the HSA

Choice Plan will increase.

5

MyVersoBenefits.com

ENROLLMENT FOR 2018

2018 Annual Enrollment is

November 3 -17, 2017

Your Coverage Dates

January 1, 2018 through December 31, 2018

Annual Enrollment

Annual Enrollment is your opportunity to

choose the plans you and your family will have

in 2018. Changes made become effective on

January 1, 2018 and remain in effect through

December 31, 2018.

What You Need to Do During

Annual Enrollment

Review the benefits available and choose the

plans that best meet the needs of you and

your family.

Go to www.MyVersoBenefits.com to enroll.

Review and update your personal information

(address, phone, email, etc.).

Review your covered dependents to verify

that they meet Verso’s benefit eligibility

requirements. Make sure you account for

events such as divorce, guardianship changes,

etc. that occurred in 2017.

Review and update your beneficiaries.

www.MyVersoBenefits.com

During Annual Enrollment

YOU MUST ENROLL

IN BENEFITS.

If you do not enroll,

you will not have

benefits coverage in

2018.

First Deduction of 2018

Remember to review your first paycheck in 2018 to ensure that the deductions reflect your 2018 enrollment elections.

ID Cards

You will have one ID card for medical and

pharmacy, a different ID card for dental, and an ID

card for Vision. If you change plans during Annual

Enrollment, you should receive a new card in

December 2017 to use beginning January 1, 2018.

6

MyVersoBenefits.com

MEDICAL PLAN

Health care is one of the most important and valuable benefits Verso

offers. You can choose between two medical plans designed to help you

and your family maintain good health. Both plans cover in-network

preventive care at 100% and both are administered by BlueCross

BlueShield of Tennessee (BCBST).

Both plans are HSA compatible high deductible health plans (sometimes

referred to as HDHPs). Refer to page 7 for more information about

Health Savings Accounts.

VERSO

Medical Plans HSA Choice Plan HSA Core Plan

Annual Deductible $2,200 Single

$4,400 Family

$3,500 Single

$7,000 Family

Out-of-Pocket Maximum $4,400 / $8,800 $6,650/ $13,300

Maximum OOP per Individual

with family coverage

Embedded $6,650

per individual

Embedded $6,650

per individual

Co-insurance after

Deductible

80% of Maximum

Allowable Charge

80% of Maximum

Allowable Charge

HSA Employer Match &

Reward

Up to

$750 / $1,500

Up to

$750 / $1,500

Office Visit 80% after deductible 80% after deductible

Specialist 80% after deductible 80% after deductible

Outpatient 80% after deductible 80% after deductible

Diagnostic Testing 80% after deductible 80% after deductible

Emergency Room Services 80% after deductible 80% after deductible

Preventive Health 100% 100%

Prescription Benefits +

Generic, Preferred Brand, Non-

Preferred Brand & Specialty Drugs

80% after deductible

Monthly Premium Rates*

HSA Choice HSA Core

Employee Only $ 130.99 $ 82.26

Employee + Spouse $ 268.53 $ 168.04

Employee + Child(ren) $ 235.78 $ 148.07

Employee + Family $ 392.97 $ 246.78

Annual Deductible

The deductible is the amount of covered medical

expenses you pay each year before the plan begins

paying co-insurance. If you cover dependents on

your medical plan, the entire amount of the family

deductible must be met first. It can be met by

one family member or a combination of

family members.

Co-Insurance

The percentage of covered medical costs paid

by your health care plan after you have met

your deductible.

Out-of-Pocket (OOP) Maximum

The out-of-pocket maximum limits your annual

exposure such as co-insurance and deductible

amounts. Both plans have an embedded OOP

maximum, meaning they contain two parts, an

individual out-of-pocket maximum and a family out-

of-pocket maximum. This allows for your coverage

to pay 100% of your medical bills once you exceed

your individual out-of-pocket prior to the family out

-of-pocket being met.

Surcharges

Working Spouse Surcharge

If you have a spouse who works and has other

coverage available through work and you enroll that

spouse in the Verso plan, you will be required to

pay an additional $100/month working spouse

surcharge.

Tobacco User Surcharge

To discourage use of tobacco products and cover

additional health care costs associated with such

use, Verso is implementing a tobacco surcharge of

$100/month. Health care costs for tobacco users

are significantly higher and they are growing at a

faster rate versus the national average. If you are a

tobacco user, you can avoid the surcharge by

completing the tobacco cessation program at no

charge to you. Information on this program can be

found by visiting the BCBST website at BCBST.com.

* Does not include surcharges

+ Generic and formulary brand medications determined to be value based (cholesterol,

diabetes and hypertension) will result in no cost when obtained from an in-network provider.

7

MyVersoBenefits.com

HEALTH SAVINGS ACCOUNT (HSA)

A Health Savings Account (HSA) is a tax-advantaged savings account

you can use to pay for qualified medical expenses, including eligible

dental and vision costs. An HSA puts you in control of your health

care spending, letting you decide how much to save and allowing you

to pay for qualified medical expenses with tax-advantaged dollars.

If you choose to open an HSA, you will receive a debit card that you

can use to access the money in your HSA. You can use your debit card

to pay for qualified medical expenses directly or you can pay qualified

expenses out of your own pocket and reimburse yourself from the

HSA at a later date. That later date can be whenever you choose and

can be withdrawn tax-free as long as you can prove you had eligible

medical expenses to support the withdrawal.

Taking a Long Term View of an HSA

You can also think of your HSA as a long-term investment. Since the

funds roll over from year to year you have the ability to contribute up

to the limit, even if you won’t use that much in a given year.

Every year you get the opportunity to contribute more and your

account will continue to grow tax-free, including interest and/or

investment earnings, for future use. There is no limit to how much

your account can accumulate.

Advantages of an HSA Triple tax savings:

Contributions made through payroll deductions

are made with pre-tax dollars, meaning they are

not subject to federal income tax. Employer

contributions from Verso are also excluded from

gross income.

Interest earned on your HSA balance is not

subject to federal income tax.

Withdrawals for qualified medical expenses

are not subject to federal income tax.

There’s no “use it or lose it” rule.

An HSA has no “use it or lose it” feature like the

Health Care Flexible Spending Account, so your

account balance rolls over each year. It’s your choice

to save for future health expenses or pay for current

health care costs.

The money is yours to keep—forever. The HSA is

completely portable. Any unused funds in your

account are yours to keep, even if you leave Verso

or retire.

2018 HSA contribution limit (employer + employee): Self-only: $3,450, Family: $6,900 * If age 55 or over by 12/31/2018, an additional $1,000 contribution is allowed in 2018 (catch-up contribution).

By performing these activities you could earn up

to $375 if you have single coverage or $750 if

you have family coverage.

Take a Personal Health

Assessment

Get an annual check-up

with your doctor

Participate in the Virgin

Pulse Program

Do These Simple Activities

Verso HSA Contributions In 2018 Verso will contribute to your Health Savings Account in two different ways up to a total contribution of $750 for those with coverage for just themselves and up to $1500 for those with coverage for their family.

There are two ways you can earn these HSA contributions from Verso Corporation.

Verso Match The first is an employer match. If you elect to contribute to your HSA account, Verso will match $1 for $1 up to the following amounts:

Single Coverage - $375; Family Coverage - $750.

Activity Rewards The second is a rewards-based contribution earned when you do one or all of the activities listed to the right under “Do These Simple Activi-ties.”

8

MyVersoBenefits.com

Special Tax Rules for HSA Withdrawals

You can withdraw funds from your HSA account at any

time; however, those withdrawals are taxable and subject

to a penalty if the money is used for anything other than

qualified medical expenses before you reach age 65. If you

use the money for other expenses when you’re older than

65 there is no penalty, but the money will be taxed upon

withdrawal.

Note: You cannot participate in the HSA if you are covered

by health insurance or other health plan coverage that is

not a qualified high deductible health plan or if you are

enrolled in Medicare. Once your Medicare coverage

begins, you can no longer contribute to an HSA. However,

you can still use your existing account balance to pay your

health expenses tax-free, including Medicare premiums

and other plan costs.

HEALTH SAVINGS ACCOUNT (HSA)

TELEMEDICINE

Important:

The IRS prevents you from having a Health Care FSA

and a Health Savings Account in the same year. If you

participated in the Health Care FSA in 2017 you must

exhaust all your funds by December 31, 2017. If you

do not you will not be able to make any HSA

contribution (or receive any Verso HSA contribution)

until the 2017 Health Care FSA grace period expires on

March 15, 2018 (that is, you may not make any HSA

contributions until April 1, 2018).

Refer to IRS Publications 969 and 502 for help in

determining HSA eligible expenses. The IRS limits how

much you can contribute to an HSA each year but it

does not limit how much your account can accumulate.

No Appointments Needed

No need to schedule an appointment, travel to your doctor’s office or wait for your appointment. You can do it all through the mobile application, which is available online for both iPhone or Android devices. You have access to doctors all day, every day via video consultation, secure messaging or telephone.

Welcome to Health Care Made Simple MDLive is a market leader in telemedicine which allows you to visit with board-certified doctors and pediatricians remotely, 24/7/365, to treat common issues and prescribe medications, all at a lower cost than a traditional office visit.

Common Adult and Pediatric Conditions Treated

Cold and flu Constipation Ear aches Diarrhea Nausea and vomiting Pinkeye Respiratory issues Skin conditions Sore throat Urinary tract infections Allergies Fever Sinus infections * Children under the age of 36 months with a fever will be referred to their primary care pediatrician.

9

MyVersoBenefits.com

PRESCRIPTION DRUGS

Because of the cost savings associated with generic medications, our plan requires the use of a generic drug unless your physician specifies on the prescription that you must take the brand-name product.

If your prescribing physician does not specify the need to take the brand-name drug, the plan will only cover the cost of the generic equivalent. The cost difference will be considered an ineligible expense and will not apply toward your deductible or out-of-pocket maximum, and will not be reimbursable under the co-insurance portion of the plan.

Specialty Drugs

Specialty drugs are typically designed and used to treat complex and chronic conditions such as multiple sclerosis or rheumatoid arthritis. These drugs can be difficult to administer and often need to be administered by a physician and require special handling.

Specialty drugs are the most expensive class of medication. The average monthly cost of a specialty drug is $3,000, which is 10 times the cost for non-specialty medications.

To help control these costs, the plan puts limits on specialty drugs. First, specialty drugs are dispensed in a maximum 30 day supply. Second, specialty drugs will only be covered if they are obtained through select specialty pharmacies. This applies even if your physician orders and administers the specialty drug.

To find a list of specialty pharmacies, visit your HelpSite at MyVersoBenefits.com or login to BlueAccess website at bcbst.com

Prescription Drugs Covered in the HSA Choice and

HSA Core Plans

What you pay for your prescriptions will depend on what

type of prescriptions you need and the class of drug you

choose to take.

The plan classifies drugs by four levels: generic, formulary

brand, non-formulary brand and specialty. Each level of drug

is a different cost. Generic medications are the lowest cost

options. Formulary brand, non-formulary brand and

specialty are higher priced medications. Your doctor may be

able to prescribe a similar drug from another level with a

lower cost.

In both the HSA Choice and the HSA Core plans you pay the

full discounted price of the drug until the deductible is met.

After the deductible is met, you pay the 20% co-insurance

until you reach your out-of-pocket maximum. You can use

your HSA account to cover these expenses.

To locate an in-network pharmacy, use the resources

available on MyVersoBenefits.com or go to the BlueAccess

website at bcbst.com.

Mail Order and 90-Day Supply

If you take certain medications on a regular basis you can

save time and money using mail order or the 90-day

program. With the mail order program you can get up to a

90-day supply with the convenience of home delivery.

With the 90-day Rx program you can get a 90-day supply of

your medication through many popular retail pharmacies.

Find the pharmacies that participate in the 90-day program

by visiting MyVersoBenefits.com or go to the BlueAccess

website at bcbst.com.

Should I Use a Brand-Name or Generic Drug?

Many brand-name drugs have a generic equivalent.

Generic drugs are equivalent to brand-name drugs in dosage,

strength, route of administration, quality, performance and

10

MyVersoBenefits.com

DENTAL PLAN

Cigna Dental PPO Plan (DPPO)

The Cigna DPPO plan offers you the

choice of using network or non-

network dentists. You’ll save the most

money when you use a Cigna DPPO

network dentist.

How to Find a Cigna DPPO

Network Dentist

Go to Cigna.com, click on “Find a

Doctor” at the top of the screen.

Then, choose a Directory by

clicking on the “If Your Insurance

Plan is Offered through Work

or School” option.

SELECT A PLAN by clicking on the

drop down icon and selecting

“Cigna Dental PPO or EPO” under

the Dental Plans section.

VERSO

Dental Plans

Base

Plan

Buy-Up

Plan

Preventive & Diagnostic Services

Oral exams, X-Ray, Cleanings, Brush

biopsy, Topical fluoride, Space

maintainers, Sealants

100% covered

No Deductible

100% covered

No Deductible

Basic Services

Restorative services using amalgam,

synthetic porcelain, and plastic filling

material, Periodontics, Endodontic,

Oral surgery, Nitrous Oxide

80% covered

No Deductible

80% covered

No Deductible

Major Services

Prosthetics: Bridges and Dentures,

Crowns, Jackets, Labial Veneers,

Implants, Inlays and Onlays

50% covered

No Deductible

50% covered

No Deductible

Orthodontia Services

Adults & Dependent Child(ren)

Not

Covered

50% covered

No Deductible

Plan Deductibles and Maximums

(waived for preventive services)

$50 Single /

$100 Family

$50 Single /

$100 Family

Calendar Year Maximum

(per covered member) $1,500 $1,500

Orthodontic Lifetime Maximum

(per eligible member)

Not Applicable $1,500

Monthly Premium Rates

Base

Plan

Buy-Up

Plan

Employee Only $12.54 $13.14

Employee + Spouse $25.09 $26.27

Employee + Child(ren) $30.11 $37.92

Employee + Family $46.42 $58.18

There’s no better way to protect your smile than with regular

dental care. Verso offers dental coverage to help with the cost

of many dental services, including orthodontia.

The comparison below gives a side-by-side view of covered

services and plan features for in-network coverage.

11

MyVersoBenefits.com

VISION PLAN

Besides helping you see better, regular vision checkups can

detect serious conditions such as glaucoma, cataracts, diabetes

and even tumors.

Vision Care

With the Humana VisionCare Plan (VCP)

you have access to more than 35,000

optometrists, ophthalmologists,

and national retail providers, such

as LensCrafters®, Pearle Vision®,

Sears® Optical, Target® Optical and

JC Penney® Optical.

Finding A Provider

Go to HumanaVisionCare.com

anytime and select the Humana

VCP provider locator.

You may also call a

Humana Customer Care

representative at

1-866-537-0229.

Services

See a

participating

Provider

See a

non-participating

Provider

Exam with Dilation

(as necessary) 100% after $15 copay $50 allowance

Lenses

• Single

• Bifocal

• Trifocal

100% after $15 copay

100% after $15 copay

100% after $15 copay

$50 allowance

$75 allowance

$100 allowance

Frames $50 wholesale

allowance

$70 retail

allowance

Contact Lenses

• Elective (conventional

and disposable)

• Medically necessary

(limit one pair)

$130 allowance

100%

$105 allowance

$210 allowance

Frequency (based on date of service)

• Examination

• Lenses or contact

lenses

• Frame

Once every 12 months

Once every 12 months

Once every 12 months

Once every 12 months

Once every 12 months

Once every 12 months

Monthly Premium Rates

Employee Only $ 9.66

Employee + Spouse $15.19

Employee + Child(ren) $15.51

Employee + Family $25.00

12

MyVersoBenefits.com

DISABILITY COVERAGE

Long-Term Disability

Long-term disability insurance helps

provide financial security if you are

unable to work for an extended

period of time due to a covered

injury or illness. If approved, long-

term disability benefits begin after you have been disabled

and out of work for 180 days.

Once you’re approved and for as long as you meet the plan’s

definition of a covered disability, the long-term disability

plan will pay a monthly benefit of 60% of your base income

(up to a maximum of $10,000 monthly) until you are able to

return to work or you reach the Social Security Normal

Retirement Age (SSNRA), whichever occurs first.

Disability benefits provide income when you cannot work

due to an illness or injury. All full-time employees are

automatically covered by short-term and long-term disability

plans. You do not need to enroll and Verso pays the full cost

of your coverage.

Short-Term Disability

Short-term disability coverage

provides income protection when

you are unable to work due to a

non-work-related illness or injury.

Once approved, you are eligible to

receive 100% of your base pay for a period of up to eight

weeks under this benefit. If you need to remain off work

longer, you are eligible to receive 67% of your base pay for

up to an additional 18 weeks, provided that you remain

disabled and your illness is certified by your doctor and

approved by the administrator.

Your short-term disability covers a maximum benefit

eligibility period of up to 26 weeks of income protection.

To Qualify for Short-Term

Disability Benefits

You must be unable to work

and be receiving treatment for

or recovering from a qualifying

medical condition, as certified by

your doctor.

You May Qualify for Long-Term

Disability Benefits

If you are unable to return to work at

the end of the short-term disability

coverage period, you may be eligible

for long-term disability benefits if

you are unable to work because of a

covered disability.

13

MyVersoBenefits.com

COMPANY PAID LIFE INSURANCE AND AD&D

Financial and Survivor Benefits

To protect those who rely on your income for their support,

Verso pays the full cost of basic life and accidental death &

dismemberment (AD&D) insurance. Coverage is equal to 1

times your base salary.

This coverage is provided even if you are not enrolled in

other benefits.

SUPPLEMENTAL LIFE INSURANCE AND AD&D

You have the opportunity to purchase additional term life and AD&D coverage for yourself and your eligible

dependents. This coverage is paid for by the employee with after-tax dollars.

How Much Coverage Can You Buy?

You can elect supplemental life and AD&D

insurance in amounts equal to 1 to 7 times your

base pay. However, your total life insurance

amount cannot exceed $1,500,000 (company

provided basic life and voluntary life combined).

Spouse: You can purchase voluntary life and AD&D

insurance for your spouse in increments of

$10,000 up to $100,000.

Child/Children: Voluntary life and AD&D insurance

in the amounts of $10,000 or $25,000 is available

for your children (up to age 26).

Tobacco User Rates

If you are a tobacco user (including e-cigarettes)

you will be asked to self-identify during the

enrollment process. As a tobacco user, your rates

will be higher to reflect the insurer’s additional risk

of providing life insurance coverage.

Increasing Your Supplemental Life

Insurance

If you want to increase your life insurance

coverage, you will be required to provide evidence

of good health to Cigna. Your evidence of good

health must be satisfactory to Cigna before an

increase in coverage will take effect.

Reductions in Insurance

Coverage amounts for employee and spouse life

insurance (both basic and supplemental) are

reduced by 11% a year starting at age 65.

Spouse coverage is not available after age 70.

Child life insurance amounts are limited as follows:

Birth to 14 days: $500

15 days to 6 months: $2,000

14

MyVersoBenefits.com

DEPENDENT CARE FLEXIBLE SPENDING ACCOUNT

A Dependent Care Flexible Spending Account (FSA) pro-

vides a tax advantaged way to pay for eligible dependent

care (including elder care) expenses.

Dependent Care FSA

The Dependent Care FSA enables you to set aside

pre-tax dollars to pay for qualified dependent care

expenses. Funds can be used to pay for eligible day care,

preschool, elder care or other dependent care.

The IRS requires that the dependent care is necessary

for you and your spouse to work, look for work or

attend school full time, along with other requirements.

Remember…

You must file claims for eligible expenses

you incur while you are participating in 2018 or

during the 2018 grace period (January 1, 2019-

March 15, 2019) or the unused amount in your

Dependent Care FSA will be forfeited.

For more information, visit HealthEquity online

at http://learn.healthequity.com/verso/fsa/

or by calling 1-866-375-1323.

Refer to IRS Publication 503 and/or visit HealthEquity online at Healthequity.com for information on eligible

dependent care expenses.

2018

Dependent Care Flexible Spending Account

Eligible Expenses

Out-of-pocket expenses for dependent care for a child

up to 13 years old or eldercare to enable you (and your

spouse, if applicable) to work (or to attend school or class).

Contribution Maximum $5,000 per year

($2,500 if married and filing separate tax return)

Access to Contributions You can be reimbursed for expenses only up to

the amount currently in your account.

15

MyVersoBenefits.com

EMPLOYEE ASSISTANCE PROGRAM

Verso’s Employee Assistance Program (EAP) is provided to all Verso employees at no charge regardless of whether the employee is enrolled in a Verso medical plan. The EAP, provided by Freckman & Associates, is a confidential service for you and your family and covers a wide-range of issues (emotional, social, financial, family, substance abuse, job performance, stress, etc.)

Benefits Include:

Face-to-face counseling sessions. Four visits per issue at no cost. If additional visits are needed, they may be coordinated under your medical plan, though you do not need to use your EAP before accessing counseling benefits under the Verso medical plans.

Legal consultation. Receive a 30-minute free consultation and up to a 25% discount on select fees.

Debt counseling. Receive 30-minute free telephonic consultation with a credit counselor.

Parenting. Guidance on child development, sibling rivalry, separation anxiety and much more.

Senior care. Learn about challenges and solutions associated with caring for an aging loved one.

Child care. Whether you need care all day or just after school, find a place that is right for your family.

Pet care. From grooming to boarding to veterinary services, find what you need to care for your pet.

To speak with an EAP counselor 24/7 call toll free 1-800-331-3226 or go online at www.freckmanandassociates.com, select Work Life Services, then enter your password: Verso

You can find an array of helpful resources in your community and receive advice on topics such as:

Family issues

Work problems

Anger management

Retirement

And much more.

RETIREMENT

While you are considering your health and welfare choices

for 2018, it is a good time to consider how much you are

saving in the 401(k) Plan. Verso matches the first 3% you

save at a rate of 100% and matches the second 3% you save

at a rate of 50%.

If you are enrolled, you should review your savings level,

your investments and beneficiary designations, and decide

if any changes are needed.

Please visit www.trsretire.com or call

Transamerica at 1-800-422-6103, Option 4 for

more information. There you can find tools and

calculators to help you determine how much

you should be saving to meet your retirement

goals.

16

MyVersoBenefits.com

VOLUNTARY BENEFITS

With Critical Illness insurance, benefits are paid directly to you to help cover:

Deductibles, co-pays and co-insurance of your health insurance

Home health care needs and household modifications

Travel expenses to and from treatment centers

Lost income

Rehabilitation

Child care expenses and more...

With Accident Insurance, benefits are paid

directly to you to help with the costs

associated with out-of-pocket expenses and

bills such as:

Emergency room visits

Surgery and anesthesia

Bandages, stitches and casts

Ambulance rides

Wheelchairs, crutches and other medical appliances

This information is provided for convenience. These coverages are not a part of the Verso Corporation Health and Welfare Benefit Plan.

Verso makes convenient premium payments (on a post-tax basis)

available to you if you elect the following Aflac coverage(s).

If you have any questions about these products, contact Aflac

at 1-800-992-3522.

Critical Illness Insurance

Aflac Critical Illness insurance is designed to help offset the

financial effects of a catastrophic illness. With this coverage, you

receive a lump sum benefit in the event that you are diagnosed

with and/or receive treatment for a covered critical illness.

Critical Illness: How Does It Work? No medical questions. Plans are guaranteed issue

during Annual Enrollment.

You can elect benefit amounts of $5,000, $10,000 or $20,000.

Pays a lump-sum benefit at the diagnosis of a

covered illness.

Coverage is available for you, your spouse and

dependent children.

Coverage is portable - you can take it with you if

you change jobs or retire.

Accident Insurance Accidents happen when you least expect them and can include

motor vehicle accidents, sports injuries, slips, falls or just every

day mishaps. An accident policy from Aflac may pay cash to help

you offset the expenses associated with accidents or injuries.

Accident Insurance: How Does It Work?

No medical questions. Plans are guaranteed issue during

Annual Enrollment.

Pays a lump-sum tax-free benefit based on type of

injury sustained and treatment needed.

Covered injuries include broken bones, cuts, burns,

eye injuries, ruptured discs, etc.

Coverage is available for you, your spouse and

dependent children.

Coverage is portable - you can take it with you if you

change jobs or retire.

17

MyVersoBenefits.com

VOLUNTARY BENEFITS

MetLife® Auto & Home Insurance

MetLife’s voluntary Auto & Home group insurance

program is available to all Verso employees. As part of

the program, you have access to special group

discounts on auto and home insurance*, as well as a

variety of other insurance policies.

Get a Price Quote

To get a price quote for Auto and Home insurance,

call 800-GET-MET8 (1-800-438-6388).

*Specific coverage offerings and discounts depend on state insurance rules.

MetLife representatives can describe details about coverage available in

your area.

Convenient Home Billing

This benefit will not be payroll

deducted. You will be billed at home

at the discounted rates.

18

MyVersoBenefits.com

ELIGIBILITY and COVERAGE

Employee Eligibility

If you are reasonably expected to average 20 or

more hours of service per week you will be deemed

eligible for medical and dental benefits.

All other benefit eligibility is based upon working 36+ hours per week.

The EAP is available to all employees.

When Coverage Begins

For Salaried, Non-Represented Hourly Employees:

There is no waiting period.

When Coverage Ends

Dependent Care Flexible Spending Account, Life

Insurance and Disability Coverages:

Coverage ends on the last day of employment.

Other Benefits: Coverage ends on the last day of the

month in which you terminate employment or

become ineligible for benefits.

Qualified Change in Status Events

You can change your benefit elections outside of Annual

Enrollment only if you have a Qualified Event or Family

Status Change, which include:

Change in marital status

Gain/loss of other coverage

Employment change that affects your benefits

You or a dependent becomes eligible for Medicare or Medicaid

If you experience one of these events and want to

change your benefits coverage, you must do so within

31 days of the event (60 days in the case of Medicaid or

CHIP related events) (or in the event of a birth, adoption

or placement for adoption).

To change your benefits you must complete the

status change request available through the Enroll

button on MyVersoBenefits.com.

Dependents

Dependents added after Annual Enrollment cannot

be enrolled for coverage during the 2018 plan year

unless you experience a Qualified Event or Family

Status Change.

Required Verification Documents

To add dependents to your benefit plans for the

first time during this annual enrollment you must

provide the following documentation no later than

November 30, 2017:

Spouse: Marriage License

Natural Children: Birth Certificate

Step Children: Birth Certificate and Marriage

License showing both parents’ names

Dependent Child(ren), Legal Guardian,

Adopted or Foster: Birth Certificate, Final

Court Order of legal guardianship with judge’s

signature and/or final adoption decree with

judge’s signature

Beneficiary Information

Please make sure you keep your life insurance

beneficiaries updated if you have a life change.

Changes can be made online by visiting

MyVersoBenefits.com

Gain/loss of

dependent

Disability or death

19

MyVersoBenefits.com

HOW TO ENROLL

Step 1: Log in to:

MyVersoBenefits.com and click “ENROLL”

First Time Login

Username: Up to the first six characters of your last name,

first character of your first name, and the last four digits of

your Social Security number (SSN)

Password: Your full (nine-digit) SSN without dashes

If you have already registered, you can login in by entering

the username and password that you previously created

during registration.

Step 2: Welcome Page

Navigate to the Welcome page. The displayed telephone

number connects you to a Verso benefits counselor who

can assist you with benefit questions and technical

support.

Progress to the next step by selecting the “Get Started”

button at the bottom of the page.

Step 3: Personal Information

Complete your personal information by adding your name,

address, telephone number and email address as

indicated. Don’t forget to read and answer the last two

“additional questions” regarding tobacco use and work

status before progressing to the next page.

Step 4: Emergency Contact Information

Add an emergency contact by completing the name,

telephone number, relationship and email address in the

appropriate sections, and click “Save”.

Step 5: Dependent and Beneficiary

Information

Select the appropriate blue button to add both dependent

and beneficiary information to your account.

1-800-422-6103

8 a.m. – 5 p.m. CST (during Annual En-rollment)

After making your selections, be sure

to thoroughly review your dependent

elections and then click “Submit” to

enroll in benefits.

20

MyVersoBenefits.com

You may not need to take action on these notices.

We are required by law to provide the enclosed notices about your benefits.

Included on page 27, you’ll find the Medicare Part D notice that explains prescription options for Medicare-eligible individuals. The

information can help you decide whether to enroll in coverage. Open enrollment for Medicare Part D coverage runs October 15

through December 7. If you and your family members are not eligible for Medicare, you may disregard the notice.

Availability of Summary of Benefits and Coverage (SBC)

Provides information about receiving a standard summary of your health coverage so you can compare your options.

As an employee, the health benefits available to you represent a significant component of your compensation package. They also

provide important protection for you and your family in the case of illness or injury.

You have available to you a series of health coverage options. Choosing a health coverage option is an important decision. To help

you make an informed choice, your plan makes available a Summary of Benefits and Coverage (SBC), which summarizes important

information about any health coverage option in a standard format, to help you compare across options.

You can view the applicable SBCs on our website at MyVersoBenefits.com. A paper copy is also available, free of charge, by calling

the Verso Benefits Group at 1-937-528-3608.

Health Insurance Portability and Accountability Act of 1996 (HIPAA)

The Health Insurance Portability and Accountability Act of 1996 (HIPAA) provides for protection of personal health information and

stipulates who may have access to the information. Protected health information includes identifiable information about you and your

covered dependents, and your patient records.

Protected health information can only be used or disclosed in certain instances as permitted by HIPAA or with the consent or authori-

zation of the individual. The Plan administrator may grant access to protected health information only as necessary to fulfill its obliga-

tions to the Plan. In no way may protected health information be disclosed for employment purposes. In addition, you have the right to

request a copy of your health information, and may make changes to correct errors. You may also request an accounting of all disclo-

sures of your protected health information.

Notice of Privacy Practices is available on MyVersoBenefits.com under the Legal Notices tab, a paper copy is also available free of

charge by calling the Verso Benefits Group at 937-528-3608.

Women’s Health and Cancer Rights Act of 1998

If you ever need a benefit-covered mastectomy, your Verso health benefits comply with the Women’s Health and Cancer Rights Act of

1998, which provides for:

• All stages of reconstruction of the breast(s) that underwent a covered mastectomy.

• Surgery and reconstruction of the other breast to produce a symmetrical appearance.

• Prostheses and treatment of physical complications related to all stages of a covered mastectomy, including

lymphedema.

All applicable benefit provisions will apply, including existing deductibles, copayments and coinsurance.

IMPORTANT RIGHTS AND INFORMATION

20

21

MyVersoBenefits.com

Premium Assistance Under Medicaid and the

Children’s Health Insurance Program (CHIP)

If you or your children are eligible for Medicaid or CHIP and you’re eligible for health coverage from your employer, your state may

have a premium assistance program that can help pay for coverage, using funds from their Medicaid or CHIP programs. If you or your

children aren’t eligible for Medicaid or CHIP, you won’t be eligible for these premium assistance programs but you may be able to buy

individual insurance coverage through the Health Insurance Marketplace. For more information, visit www.healthcare.gov.

If you or your dependents are already enrolled in Medicaid or CHIP and you live in a State listed below, contact your State Medicaid or

CHIP office to find out if premium assistance is available.

If you or your dependents are NOT currently enrolled in Medicaid or CHIP, and you think you or any of your dependents might be eligi-

ble for either of these programs, contact your State Medicaid or CHIP office or dial 1-877-KIDS NOW or www.insurekidsnow.gov to find

out how to apply. If you qualify, ask your state if it has a program that might help you pay the premiums for an employer-sponsored

plan.

If you or your dependents are eligible for premium assistance under Medicaid or CHIP, as well as eligible under your employer plan,

your employer must allow you to enroll in your employer plan if you aren’t already enrolled. This is called a “special enrollment” oppor-

tunity, and you must request coverage within 60 days of being determined eligible for premium assistance. If you have questions

about enrolling in your employer plan, contact the Department of Labor at www.askebsa.dol.gov or call 1-866-444-EBSA (3272).

_________________________________________________________________________________________________________

If you live in one of the following states, you may be eligible for assistance paying your employer health plan premiums.

The following list of states is current as of August 10, 2017. Contact your State for more information on eligibility –

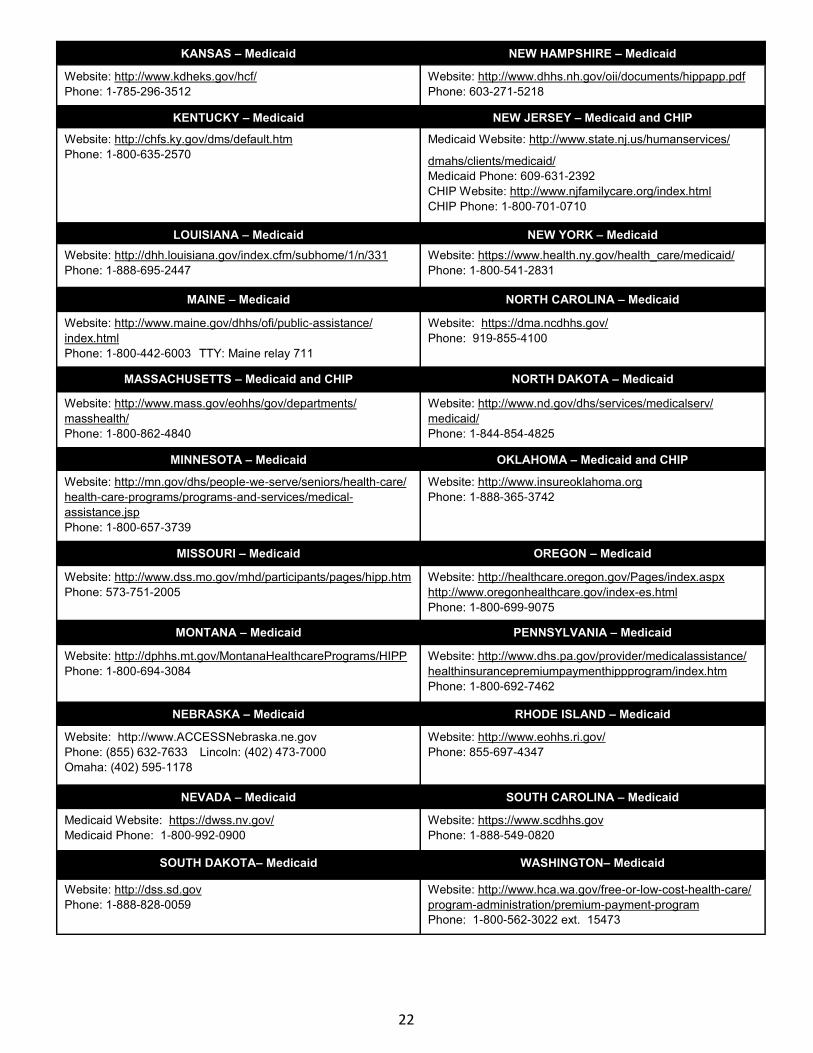

ALABAMA – Medicaid FLORIDA – Medicaid

Website: http://myalhipp.com/

Phone: 1-855-692-5447 Website: http://flmedicaidtplrecovery.com/hipp/

Phone: 1-877-357-3268

ALASKA – Medicaid GEORGIA – Medicaid

The AK Health Insurance Premium Payment Program Website: http://myakhipp.com/

Phone: 1-866-251-4861 Email: [email protected]

Medicaid Eligibility: http://dhss.alaska.gov/dpa/Pages/medicaid/

default.aspx

Website: http://dch.georgia.gov/medicaid

- Click on Health Insurance Premium Payment (HIPP) Phone: 404-656-4507

ARKANSAS – Medicaid INDIANA – Medicaid

Website: http://myarhipp.com/

Phone: 1-855-MyARHIPP (855-692-7447) Healthy Indiana Plan for low-income adults 19-64 Website: http://www.in.gov/fssa/hip/

Phone: 1-877-438-4479 All other Medicaid Website: http://www.indianamedicaid.com

Phone 1-800-403-0864

COLORADO – Health First Colorado (Colorado’s Medicaid

Program) & Child Health Plan Plus (CHP+) IOWA – Medicaid

Health First Colorado Website:

https://www.healthfirstcolorado.com/

Health First Colorado Member Contact Center: 1-800-221-3943/ State Relay 711 CHP+: Colorado.gov/HCPF/Child-Health-Plan-Plus CHP+ Customer Service: 1-800-359-1991/ State Relay 711

Website: http://dhs.iowa.gov/ime/members/medicaid-a-to-z/

hipp

Phone: 1-888-346-9562

21

22

MyVersoBenefits.com

KANSAS – Medicaid NEW HAMPSHIRE – Medicaid

Website: http://www.kdheks.gov/hcf/

Phone: 1-785-296-3512 Website: http://www.dhhs.nh.gov/oii/documents/hippapp.pdf

Phone: 603-271-5218

KENTUCKY – Medicaid NEW JERSEY – Medicaid and CHIP

Website: http://chfs.ky.gov/dms/default.htm

Phone: 1-800-635-2570 Medicaid Website: http://www.state.nj.us/humanservices/

dmahs/clients/medicaid/

Medicaid Phone: 609-631-2392 CHIP Website: http://www.njfamilycare.org/index.html

CHIP Phone: 1-800-701-0710

LOUISIANA – Medicaid NEW YORK – Medicaid

Website: http://dhh.louisiana.gov/index.cfm/subhome/1/n/331

Phone: 1-888-695-2447 Website: https://www.health.ny.gov/health_care/medicaid/

Phone: 1-800-541-2831

MAINE – Medicaid NORTH CAROLINA – Medicaid

Website: http://www.maine.gov/dhhs/ofi/public-assistance/

index.html

Phone: 1-800-442-6003 TTY: Maine relay 711

Website: https://dma.ncdhhs.gov/

Phone: 919-855-4100

MASSACHUSETTS – Medicaid and CHIP NORTH DAKOTA – Medicaid

Website: http://www.mass.gov/eohhs/gov/departments/

masshealth/

Phone: 1-800-862-4840

Website: http://www.nd.gov/dhs/services/medicalserv/

medicaid/

Phone: 1-844-854-4825

MINNESOTA – Medicaid OKLAHOMA – Medicaid and CHIP

Website: http://mn.gov/dhs/people-we-serve/seniors/health-care/

health-care-programs/programs-and-services/medical-

assistance.jsp

Phone: 1-800-657-3739

Website: http://www.insureoklahoma.org

Phone: 1-888-365-3742

MISSOURI – Medicaid OREGON – Medicaid

Website: http://www.dss.mo.gov/mhd/participants/pages/hipp.htm

Phone: 573-751-2005 Website: http://healthcare.oregon.gov/Pages/index.aspx

http://www.oregonhealthcare.gov/index-es.html

Phone: 1-800-699-9075

MONTANA – Medicaid PENNSYLVANIA – Medicaid

Website: http://dphhs.mt.gov/MontanaHealthcarePrograms/HIPP

Phone: 1-800-694-3084 Website: http://www.dhs.pa.gov/provider/medicalassistance/

healthinsurancepremiumpaymenthippprogram/index.htm

Phone: 1-800-692-7462

NEBRASKA – Medicaid RHODE ISLAND – Medicaid

Website: http://www.ACCESSNebraska.ne.gov Phone: (855) 632-7633 Lincoln: (402) 473-7000 Omaha: (402) 595-1178

Website: http://www.eohhs.ri.gov/

Phone: 855-697-4347

NEVADA – Medicaid SOUTH CAROLINA – Medicaid

Medicaid Website: https://dwss.nv.gov/

Medicaid Phone: 1-800-992-0900 Website: https://www.scdhhs.gov

Phone: 1-888-549-0820

SOUTH DAKOTA– Medicaid WASHINGTON– Medicaid

Website: http://dss.sd.gov

Phone: 1-888-828-0059 Website: http://www.hca.wa.gov/free-or-low-cost-health-care/

program-administration/premium-payment-program

Phone: 1-800-562-3022 ext. 15473

22

23

MyVersoBenefits.com

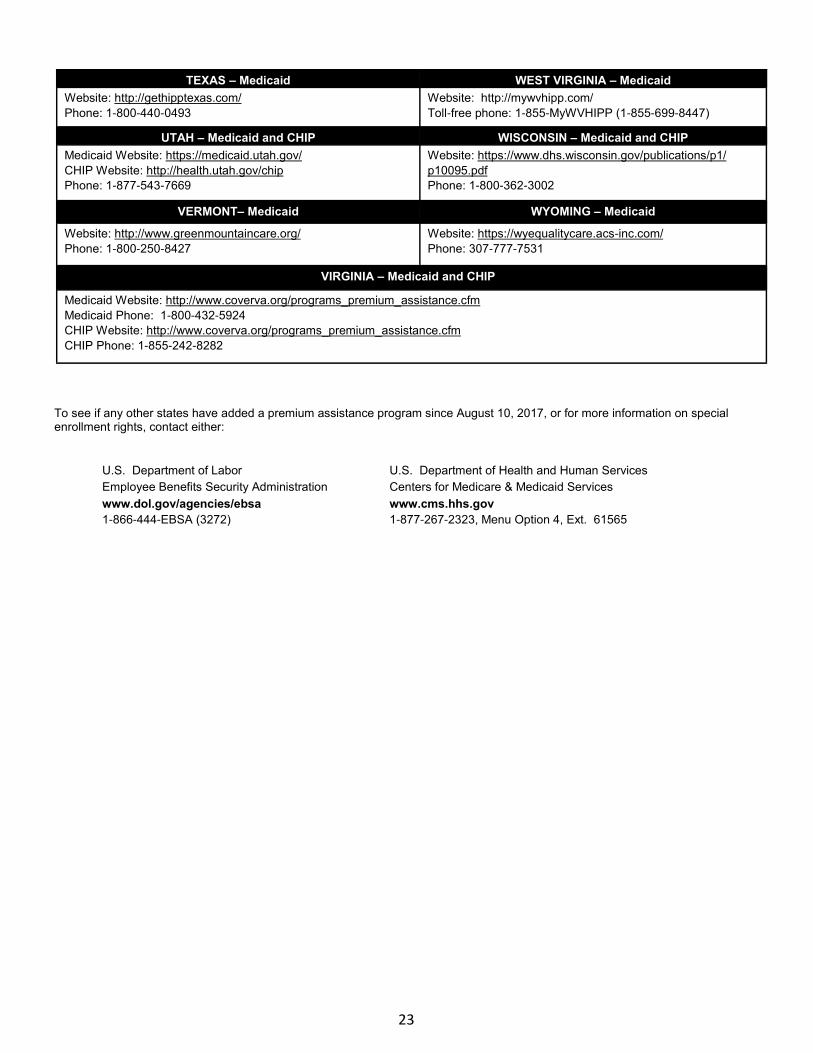

TEXAS – Medicaid WEST VIRGINIA – Medicaid

Website: http://gethipptexas.com/

Phone: 1-800-440-0493 Website: http://mywvhipp.com/ Toll-free phone: 1-855-MyWVHIPP (1-855-699-8447)

UTAH – Medicaid and CHIP WISCONSIN – Medicaid and CHIP

Medicaid Website: https://medicaid.utah.gov/

CHIP Website: http://health.utah.gov/chip

Phone: 1-877-543-7669

Website: https://www.dhs.wisconsin.gov/publications/p1/

p10095.pdf

Phone: 1-800-362-3002

VERMONT– Medicaid WYOMING – Medicaid

Website: http://www.greenmountaincare.org/

Phone: 1-800-250-8427 Website: https://wyequalitycare.acs-inc.com/

Phone: 307-777-7531

VIRGINIA – Medicaid and CHIP

Medicaid Website: http://www.coverva.org/programs_premium_assistance.cfm

Medicaid Phone: 1-800-432-5924 CHIP Website: http://www.coverva.org/programs_premium_assistance.cfm

CHIP Phone: 1-855-242-8282

To see if any other states have added a premium assistance program since August 10, 2017, or for more information on special enrollment rights, contact either:

U.S. Department of Labor U.S. Department of Health and Human Services

Employee Benefits Security Administration Centers for Medicare & Medicaid Services

www.dol.gov/agencies/ebsa www.cms.hhs.gov

1-866-444-EBSA (3272) 1-877-267-2323, Menu Option 4, Ext. 61565

23

24

MyVersoBenefits.com

Continuation of Coverage (COBRA) Introduction You are receiving this notice because you may have recently become covered under a group health plan (the Plan). This notice contains important information about your right to COBRA continuation coverage, which is a temporary extension of coverage under the Plan. This notice generally explains COBRA continuation coverage, when it may become available to you and your family, and what you need to do to protect the right to receive it. The right to COBRA continuation coverage was created by a federal law, the Consolidated Omnibus Budget Reconciliation Act of 1985 (COBRA). COBRA continuation coverage can become available to you when you would otherwise lose your group health coverage. It can also become available to other members of your family who are covered under the Plan when they would otherwise lose their group health coverage. For additional information about your rights and obligations under the Plan and under federal law, you should review the Plan’s Summary Plan Description or contact the Plan Administrator.

What is COBRA Continuation Coverage? COBRA continuation coverage is a continuation of Plan coverage when coverage would otherwise end because of a life event known as a “qualifying event.” Specific qualifying events are listed later in this notice. After a qualifying event, COBRA continuation coverage must be offered to each person who is a “qualified beneficiary.” You, your spouse, and your dependent children could become qualified beneficiaries if coverage under the Plan is lost because of the qualifying event. Under the Plan, qualified beneficiaries who elect COBRA continuation coverage must pay for COBRA continuation coverage. If you are an employee, you will become a qualified beneficiary if you lose your coverage under the Plan because either one of the following qualifying events happens:

• Your hours of employment are reduced, or

• Your employment ends for any reason other than your gross misconduct.

If you are the spouse of an employee, you will become a qualified beneficiary if you lose your coverage under the Plan because any of the following qualifying events happens:

• Your spouse dies;

• Your spouse’s hours of employment are reduced;

• Your spouse’s employment ends for any reason other than his or her gross misconduct;

• Your spouse becomes entitled to Medicare benefits (under Part A, Part B, or both); or

• You become divorced or legally separated from your spouse.

Your dependent children will become qualified beneficiaries if they lose coverage under the Plan because any of the following qualifying events happens:

• The parent-employee dies;

• The parent-employee’s hours of employment are reduced;

• The parent-employee’s employment ends for any reason other than his or her gross misconduct;

• The parent-employee becomes entitled to Medicare benefits (Part A, Part B, or both);

• The parents become divorced or legally separated; or

• The child stops being eligible for coverage under the plan as a “dependent child.”

When is COBRA Coverage Available? The Plan will offer COBRA continuation coverage to qualified beneficiaries only after the Plan Administrator has been notified that a qualifying event has occurred. When the qualifying event is the end of employment or reduction of hours of employment, death of the employee, or the employee becoming entitled to Medicare benefits (under Part A, Part B, or both), the employer must notify the Plan Administrator of the qualifying event. You Must Give Notice of Some Qualifying Events For the other qualifying events (divorce or legal separation of the employee and spouse or a dependent child’s losing eligibility for coverage as a dependent child), you must notify the Plan Administrator within 60 days after the qualifying event occurs by visiting MyVersoBenefits.com, select “Enroll in Your Benefits” button on the home page, and then log in to the system to select changes and provide certified documentation. You may also provide certified documentation to your local HR Department.

24

25

MyVersoBenefits.com

How is COBRA Coverage Provided? Once the Plan Administrator receives notice that a qualifying event has occurred, COBRA continuation coverage will be offered to each of the qualified beneficiaries. Each qualified beneficiary will have an independent right to elect COBRA continuation coverage. Covered employees may elect COBRA continuation coverage on behalf of their spouses, and parents may elect COBRA continuation coverage on behalf of their children. COBRA continuation coverage is a temporary continuation of coverage. When the qualifying event is the death of the employee, the employee's becoming entitled to Medicare benefits (under Part A, Part B, or both), your divorce or legal separation, or a dependent child's losing eligibility as a dependent child, COBRA continuation coverage lasts for up to a total of 36 months. When the qualifying event is the end of employment or reduction of the employee's hours of employment, and the employee became entitled to Medicare benefits less than 18 months before the qualifying event, COBRA continuation coverage for qualified beneficiaries other than the employee lasts until 36 months after the date of Medicare entitlement. For example, if a covered employee becomes entitled to Medicare 8 months before the date on which his employment terminates, COBRA continuation coverage for his spouse and children can last up to 36 months after the date of Medicare entitlement, which is equal to 28 months after the date of the qualifying event (36 months minus 8 months). Otherwise, when the qualifying event is the end of employment or reduction of the employee’s hours of employment, COBRA continua-tion coverage generally lasts for only up to a total of 18 months. There are two ways in which this 18-month period of COBRA continuation coverage can be extended. Disability extension of 18-month period of continuation coverage If you or anyone in your family covered under the Plan is determined by the Social Security Administration to be disabled and you notify the Plan Administrator in a timely fashion, you and your entire family may be entitled to receive up to an additional 11 months of COBRA continuation coverage, for a total maximum of 29 months. The disability would have to have started at some time before the 60th day of COBRA continuation coverage and must last at least until the end of the 18-month period of continuation coverage.

Second qualifying event extension of 18-month period of continuation coverage If your family experiences another qualifying event while receiving 18 months of COBRA continuation coverage, the spouse and dependent children in your family can get up to 18 additional months of COBRA continuation coverage, for a maximum of 36 months, if notice of the second qualifying event is properly given to the Plan. This extension may be available to the spouse and any dependent children receiving continuation coverage if the employee or former employee dies, becomes entitled to Medicare benefits (under Part A, Part B, or both), or gets divorced or legally separated, or if the dependent chi ld stops being eligible under the Plan as a dependent child, but only if the event would have caused the spouse or dependent child to lose coverage under the Plan had the first qualifying event not occurred. If You Have Questions about COBRA Questions concerning your Plan or your COBRA continuation coverage rights should be addressed to the contact or contacts identified below. For more information about your rights under ERISA, including COBRA, the Health Insurance Portability and Accountability Act (HIPAA), and other laws affecting group health plans, contact the nearest Regional or District Office of the U.S. Department of Labor’s Employee Benefits Security Administration (EBSA) in your area or visit the EBSA website at www.dol.gov/ebsa

Keep Your Plan Informed of Address Changes

In order to protect your family’s rights, you should keep the Plan Administrator informed of any changes in the addresses

of family members. You should also keep a copy, for your records, of any notices you send to the Plan Administrator.

Verso Corporation

Attn: Verso Benefits Group

8540 Gardner Creek Drive

Miamisburg, OH 45342

25

26

MyVersoBenefits.com

As a result of some key parts of the health care law that took effect in 2014, there are now new ways to buy health insurance:

the Health Insurance Marketplace.

What is the Health Insurance Marketplace?

The Marketplace is designed to help you find health insurance that meets your needs and fits your budget. The Marketplace at www.healthcare.gov offers "one-stop shopping" to find and compare private health insurance options. You may also be eligible for a new kind of tax credit that lowers your monthly premium right away.

Can I Save Money on my Health Insurance Premiums

in the Marketplace?

You may qualify to save money and lower your monthly premium, but only if your employer does not offer coverage, or offers coverage that doesn't meet certain standards. The savings on your premium that you're eligible for depends on your household income.

Does Employer Health Coverage Affect Eligibility for Premium Savings though the Marketplace?

Yes. If you have an offer of health coverage from your employer that meets certain standards, you will not be eligible for a tax credit through the Marketplace and may wish to enroll in your employer's health plan. However, you may be eligible for a tax credit that lowers your monthly premium, or a reduction in certain cost-sharing if your employer does not offer coverage to you at all or does not offer coverage that meets certain standards. If the cost of a plan from your employer that would cover you (and not any other members of your family) is more than 9.69% of your household income for the year, or if the coverage your employer provides does not meet the "minimum value" standard set by the Affordable Care Act, you may be eligible for a tax credit.1

Note: If you purchase a health plan through the Marketplace instead of accepting health coverage offered by your employer, then you may lose the employer contribution (if any) to the employer-offered coverage. Also, this employer contribution -as well as your employee contribution to employer-offered coverage- is often excluded from income for Federal and State income tax purposes. Your payments for coverage through the Marketplace are made on an after-tax basis. 1https://www.healthcare.gov/fees-exemptions/fee-for-not-being-covered/

Your Responsibility Under Health Care Reform

Individual Mandate. The law now requires that most individuals maintain health insurance coverage or otherwise pay a

penalty. If you don’t have medical coverage in 2018, you’ll pay the higher of these two amounts1:

• 2.5% of your yearly household income.

(Only the amount of income above the tax filing threshold, about $10,000 for an individual, is used to calculate the penalty.)

The maximum penalty is the national average premium for a bronze plan.

• $695 per person for the year ( $347.50 per child under 18 ).

The maximum penalty per family using this method is $2,085.

Please Note: The above was the 2016 maximum.

In 2018, the maximum may be adjusted to increase on par with the national rate of inflation.

1https://www.healthcare.gov/fees-exemptions/fee-for-not-being-covered/

NOTICE OF HEALTH INSURANCE MARKETPLACE

26

27

MyVersoBenefits.com

Medicare Part D Prescription Drug Coverage - Notice of Creditable Prescription Drug Coverage

Explains the prescription options available to those eligible for Medicare and can help you decide whether or not to enroll in coverage.

At the end is information about where you can get help to make decisions about your prescription drug coverage.

Note: If you enroll in one of the Medicare-approved plans which offer prescription drug coverage, you may need to provide a copy of this notice to show you are not required to pay a higher premium amount.

Medicare prescription drug coverage became available in 2006 to everyone with Medicare through Medicare prescription drug plans and

Medicare Advantage Plans that offer prescription drug coverage. All Medicare prescription drug plans provide at least a standard level of

coverage set by Medicare. Some plans may offer more coverage for a higher monthly premium.

Verso Corporation has determined that the prescription drug coverage offered by the Verso medical plans is, on average for all plan

participants, expected to pay out as much as the standard Medicare prescription drug coverage will pay and is considered Creditable

Coverage.

Because your existing coverage is on average at least as good as standard Medicare prescription coverage, you can keep the Verso

coverage and not pay extra if you later decide to enroll in Medicare prescription coverage. Individuals can enroll in a Medicare

prescription drug plan when they first become eligible for Medicare and each year from October 15 through December 7. Beneficiaries leaving

employer/union coverage may be eligible for a Special Enrollment Period to sign up for a Medicare prescription drug plan. You should compare

your current coverage, including which drugs are covered, with the coverage and cost of the plans offering Medicare prescription drug coverage

in your area.

If you decide to enroll in a Medicare prescription drug plan and elect to drop your Verso combined medical and prescription drug

coverage, be aware that you and your dependents will not be able to get the Verso coverage back. Please contact us for more

information about what happens to your coverage if you enroll in a Medicare prescription drug plan. You should also know that if you

drop or lose your coverage with Verso and don’t enroll in Medicare prescription drug coverage after your current coverage ends, you may pay

more (a penalty) to enroll in Medicare prescription drug coverage later. If you go 63 days or longer without prescription drug coverage that’s at

least as good as Medicare’s prescription drug coverage, your monthly premium will go up at least one percent per month for every month that

you did not have that coverage. For example, if you go 19 months without coverage, your premium will always be at least 19 percent higher

than what many other people pay. You’ll have to pay this higher premium as long as you have Medicare prescription drug coverage. In addition,

you may have to wait until the following October to enroll.

For more information about this notice or your prescription drug coverage, contact Verso Benefit Group at 937-528-3608. You may receive

this notice at other times in the future, such as before the next period you can enroll in Medicare prescription drug coverage, and if your Verso

coverage changes. You also may request a copy.

For more information about your options under Medicare, the “Medicare & You” handbook contains more detailed information about Medicare

plans that offer prescription drug coverage. If you’re eligible for Medicare coverage, you’ll receive a copy of the handbook in the mail every year

from Medicare. You may also be contacted directly by Medicare prescription drug plans. For more information about Medicare prescription drug

plans:

Visit www.medicare.gov.

Call your State Health Insurance Assistance Program (see your copy of the Medicare & You handbook for the telephone number).

Call 1-800-MEDICARE (1-800-633-4227).

TTY users, call 1-877-486-2048.

For people with limited income and resources, extra help paying for a Medicare prescription drug plan is available. Information about extra help

is available from the Social Security Administration online at www.socialsecurity.gov or by calling

1-800-772-1213 (TTY 1-800-325-0778).

27

28 MyVersoBenefits.com

The information included in this guide is intended to summarize the benefits offered in language that is clear and easy to

understand. Every effort has been made to ensure that this information is accurate. It is not intended to replace the legal

plan document or insurance contract, which contains the complete provisions of the program. In case of any discrepancy

between this handout and the legal plan document or insurance contract, the legal plan document or (contract) will

govern in all cases. A participant or beneficiary may review the legal plan documents upon request. Verso Corporation

reserves the right to suspend, revoke or modify the benefit programs offered to employees at any time.

Medical Plans

BlueCross BlueShield of TN

1-877-420-3266

www.BCBSTN.com

Mon-Fri, 7 am - 5 pm CST

Dental Plan

Cigna

1-800-244-6224

www.Cigna.com

24 hours a day, 7 days a week

Vision Plan

Humana

1-866-537-0229

www.HumanaVisionCare.com

Mon-Sat, 6:30 am. - 10 pm CST

Sun, 10am - 7pm CST

Dependent Care FSA

Health Equity

1-866-375-1323

www.HealthEquity.com

24 hours a day, 7 days a week

Employee Benefit Advocacy

BenefitHelp™

1-800-422-6103 (option 8)

Mon-Thurs, 8.am. - 5 p.m. CST

Fri, 8 a.m. - 4 p.m. CST

www.MyVersoBenefits.com

HSA

Benefit Wallet

1-877-472-4200

www.mybenefitwallet.com

Mon-Fri, 7.am. - 10 p.m. CST

Sat-Sun 8 am. - 5 p.m. CST

Life Insurance & Disability

Cigna

1-800-362-4462

www.Cigna.com

24 hours a day, 7 days a week

Employee Assistance Program

Freckman & Associates

1-800-331-3226

www.FreckmanandAssociates.com

Mon-Fri, 8 am - 5 pm CST

General Benefit Questions

Verso One Number

1-800-422-6103 (option 5, option 3)

Mon-Thurs, 8.am. - 5 p.m. CST

Fri, 8 a.m. - 4 p.m. CST

Mon-Fri, 8 am - 5 pm CST

Voluntary Critical Illness &

Accident

AFLAC

1-800-992-3522

www.AFLAC.com

24 hours a day, 7 days a week

Group Auto & Home Insurance

MetLife®

1-877-619-5604www.MetLife.com/versocorporation

24 hours a day, 7 days a week

401(k)

TransAmerica

1-800-422-6103, option 4

www.TRSretire.com

BENEFIT CONTACTS

© BenefitHelp

![[XLS]engineeringstudentsdata.comengineeringstudentsdata.com/downloads/2018/2018 AP... · Web view2018 2018 2018 2018 2018 2018 2018 2018 2018 2018 2018 2018 2018 2018 2018 2018 2018](https://static.fdocuments.in/doc/165x107/5ad1e56f7f8b9a482c8bcbab/xlseng-apweb-view2018-2018-2018-2018-2018-2018-2018-2018-2018-2018-2018-2018.jpg)