2017 Investor Day - Centene Corporation · PDF fileCENTENE - JUNE 2017 INVESTOR DAY 20...

129

2017 Investor Day June 16, 2017 SSID: Centene Corp Password: welcome2017

Transcript of 2017 Investor Day - Centene Corporation · PDF fileCENTENE - JUNE 2017 INVESTOR DAY 20...

2017 Investor DayJune 16, 2017

SSID: Centene Corp Password: welcome2017

2CENTENE - JUNE 2017 INVESTOR DAY

IntroductionEdmund E. Kroll, SVP, Finance and Investor Relations

3CENTENE - JUNE 2017 INVESTOR DAY

Forward-Looking StatementsThe company and its representatives may from time to time make written and oral forward-looking statements within the meaning of the Private Securities Litigation Reform Act(“PSLRA”) of 1995, including statements in this and other presentations, press releases, filings with the Securities and Exchange Commission (“SEC”), reports to stockholders and inmeetings with investors and analysts. In particular, the information provided in this presentation may contain certain forward-looking statements with respect to the financialcondition, results of operations and business of Centene and certain plans and objectives of Centene with respect thereto, including but not limited to the expected benefits of theacquisition of Health Net, Inc. These forward-looking statements can be identified by the fact that they do not relate only to historical or current facts. Without limiting the foregoing,forward-looking statements often use words such as “anticipate”, "seek", “target”, “expect”, “estimate”, “intend”, “plan”, “goal”, “believe”, “hope”, “aim”, “continue”, “will”, “may”,"can", “would”, “could” or “should” or other words of similar meaning or the negative thereof. We intend such forward-looking statements to be covered by the safe-harbor provisionsfor forward-looking statements contained in PSLRA. A number of factors, variables or events could cause actual plans and results to differ materially from those expressed or implied inforward-looking statements. Such factors include, but are not limited to, Centene’s ability to accurately predict and effectively manage health benefits and other operating expensesand reserves; competition; membership and revenue declines or unexpected trends; changes in healthcare practices, new technologies, and advances in medicine; increased health carecosts; changes in economic, political or market conditions; changes in federal or state laws or regulations, including changes with respect to government health care programs as wellas changes with respect to the Patient Protection and Affordable Care Act and the Health Care and Education Affordability Reconciliation Act and any regulations enacted thereunderthat may result from changing political conditions; rate cuts or other payment reductions or delays by governmental payors and other risks and uncertainties affecting Centene’sgovernment businesses; Centene’s ability to adequately price products on federally facilitated and state based Health Insurance Marketplaces; tax matters; disasters or majorepidemics; the outcome of legal and regulatory proceedings; changes in expected contract start dates; provider, state, federal and other contract changes and timing of regulatoryapproval of contracts; the expiration, suspension or termination of Centene’s contracts with federal or state governments (including but not limited to Medicaid, Medicare, andTRICARE); challenges to Centene's contract awards; cyber-attacks or other privacy or data security incidents; the possibility that the expected synergies and value creation fromacquired businesses, including, without limitation, the Health Net acquisition, will not be realized, or will not be realized within the expected time period, including, but not limited to, asa result of conditions, terms, obligations or restrictions imposed by regulators in connection with their approval of, or consent to, the acquisition; the exertion of management’s timeand Centene’s resources, and other expenses incurred and business changes required in connection with complying with the undertakings in connection with certain regulatoryapprovals; disruption from the acquisition making it more difficult to maintain business and operational relationships; the risk that unexpected costs will be incurred in connection with,among other things, the acquisition and/or the integration; changes in expected closing dates, estimated purchase price and accretion for acquisitions; the risk that acquired businesseswill not be integrated successfully; Centene's ability to maintain or achieve improvement in the Centers for Medicare and Medicaid Services (CMS) Star ratings and other quality scoresthat impact revenue; availability of debt and equity financing, on terms that are favorable to Centene; inflation; foreign currency fluctuations; and risks and uncertainties discussed inthe reports that Centene has filed with the SEC. These forward-looking statements reflect Centene’s current views with respect to future events and are based on numerous assumptionsand assessments made by Centene in light of its experience and perception of historical trends, current conditions, business strategies, operating environments, future developmentsand other factors it believes appropriate. By their nature, forward-looking statements involve known and unknown risks and uncertainties and are subject to change because they relateto events and depend on circumstances that will occur in the future. The factors described in the context of such forward-looking statements in this presentation could cause Centene’splans with respect to the Health Net acquisition, actual results, performance or achievements, industry results and developments to differ materially from those expressed in or impliedby such forward-looking statements. Although it is currently believed that the expectations reflected in such forward-looking statements are reasonable, no assurance can be given thatsuch expectations will prove to have been correct and persons reading this presentation are therefore cautioned not to place undue reliance on these forward-looking statements whichspeak only as of the date of this presentation. Centene does not assume any obligation to update the information contained in this presentation (whether as a result of newinformation, future events or otherwise), except as required by applicable law. This list of important factors is not intended to be exhaustive. We discuss certain of these matters morefully, as well as certain other risk factors that may affect Centene's business operations, financial condition and results of operations, in Centene's filings with the SEC, including theannual reports on Form 10-K, quarterly reports on Form 10-Q and current reports on Form 8-K.

4CENTENE - JUNE 2017 INVESTOR DAY

Earnings Guidance PolicyOur Company’s policy is, “that the Company undertakes no obligation to update its earningsguidance, other than as part of its quarterly or yearly earnings disclosure, and that silence onguidance by the Company or Company officials should not be interpreted that guidance has or hasnot changed. In any event, no updated guidance would ever be given that is not previously orsimultaneously disclosed in an SEC filing or other broad non-exclusionary means.”

“Further, it is Company policy to generally not hold discussions with investors commencing twoweeks prior to earnings release.”

5CENTENE - JUNE 2017 INVESTOR DAY

Strategic OverviewMichael F. Neidorff, Chairman, President & CEO

6CENTENE - JUNE 2017 INVESTOR DAY

EPS

HBR

$ 69% increaseTotal Revenues

51% increaseAdjusted Diluted

110 bps improvementHealth Benefits Ratio

Q1 2017 Financials(year-over-year)

EPS

$ 42% increaseTotal Revenues

40% increaseAdjusted Diluted

2017 5-Year CAGR(based on the mid-point of 2017 guidance )

7CENTENE - JUNE 2017 INVESTOR DAY

30,900 employees

WHO WE ARE

St. Louisbased company founded in Milwaukee in 1984

WHAT WE DO

28 stateswith government sponsored healthcare programs

12.1 million members

~300 product / market solutions

Serving ~900,000 individuals

$46-46.8B

2 international markets

2017 revenue guidance

EnvolveFederalServices

Commercial(Marketplace)

MedicareComplexCareMedicaid

*Including 3 implementation markets

8CENTENE - JUNE 2017 INVESTOR DAY

Continued Operational Success

2017 - #662016 - #1242015 - #1862014 - #2512013 - #3032012 - #4532011 - #493

9CENTENE - JUNE 2017 INVESTOR DAY

HealthcareReform

Haley BarbourFounding Partner - BGR Group;Former Governor of Mississippi

Richard GephardtCentene Board Member; CEO – Gephardt Group; Former Majority Leader of the U.S. House of Representatives

David SchiappaPartner at the Duberstein Group

Joe AntosWilson H. Taylor Scholar in Health Care and Retirement Policy - American Enterprise Institute

Jonathan DinesmanSVP, Government Relations - Centene

Expert Panel

10CENTENE - JUNE 2017 INVESTOR DAY

Focused on Vulnerable and Low Income Populations

118M

318M US Population

Medicare and Medicaid Population

Population Demographics

60% below 400% FPL

76% below 400% FPL

* Source: U.S. Census Bureau | Current Population Survey (CPS) | Last Revised: March, 2016

11CENTENE - JUNE 2017 INVESTOR DAY

Need for High Quality, Affordable Healthcare Remains Constant

The healthcare industry will continue to strive to:

Improve access

Promote appropriate utilization

Increase quality outcomes

LeverageExpertise

Execute onGrowth

Strategies

Focus onFundamentals

Centene will continue to:

12CENTENE - JUNE 2017 INVESTOR DAY

Value Based Provider Partnerships

Analytics Infrastructure

Integrated Solutions

Business Operations

Multi-product Portfolio Business Model

CA Market Update

Partnering with State Governments

Product Leadership

Product Updates and Growth Pipeline

International

13CENTENE - JUNE 2017 INVESTOR DAY

Value Based Provider Partnerships

Analytics Infrastructure

Integrated Solutions

Business Operations

Multi-product Portfolio Business Model

CA Market Update

Partnering with State Governments

Product Leadership

Product Updates and Growth Pipeline

International

Leveraging our business model:

15 subsidiaries exceeding $1B in revenue

14CENTENE - JUNE 2017 INVESTOR DAY

Value Based Provider Partnerships

Analytics Infrastructure

Integrated Solutions

Business Operations

Partnering with State Governments

CA Market Update

Product Leadership

Product Updates and Growth Pipeline

International

15CENTENE - JUNE 2017 INVESTOR DAY

Value Based Provider Partnerships

Analytics Infrastructure

Integrated Solutions

Business Operations

CA Market Update

Product Leadership

Product Updates and Growth Pipeline

InternationalIntegration of HNT is on track

or ahead of schedule

16CENTENE - JUNE 2017 INVESTOR DAY

Analytics Infrastructure

Integrated Solutions

Business Operations

Value Based Provider Partnerships

Product Leadership

Product Updates and Growth Pipeline

International

Furthering our value based partnerships with providers

JV owned health plan with North Carolina Medical Society and the

North Carolina Community Health Center Association

17CENTENE - JUNE 2017 INVESTOR DAY

Analytics Infrastructure

Business Operations

Integrated Solutions

Product Leadership

Product Updates and Growth Pipeline

International

18CENTENE - JUNE 2017 INVESTOR DAY

Business Operations

Analytics Infrastructure

Product Leadership

Product Updates and Growth Pipeline

InternationalData

AnalysisData

IntegrationData

CaptureFaster:

HealthInterventionsPerformance

ImprovedQuality

ReducedCosts

Results in:

19CENTENE - JUNE 2017 INVESTOR DAY

Business Operations

Product Leadership

Product Updates and Growth Pipeline

International

MarketplaceFederalServicesMLTSS

MedicaidManaged

Care

National Leading Products

20CENTENE - JUNE 2017 INVESTOR DAY

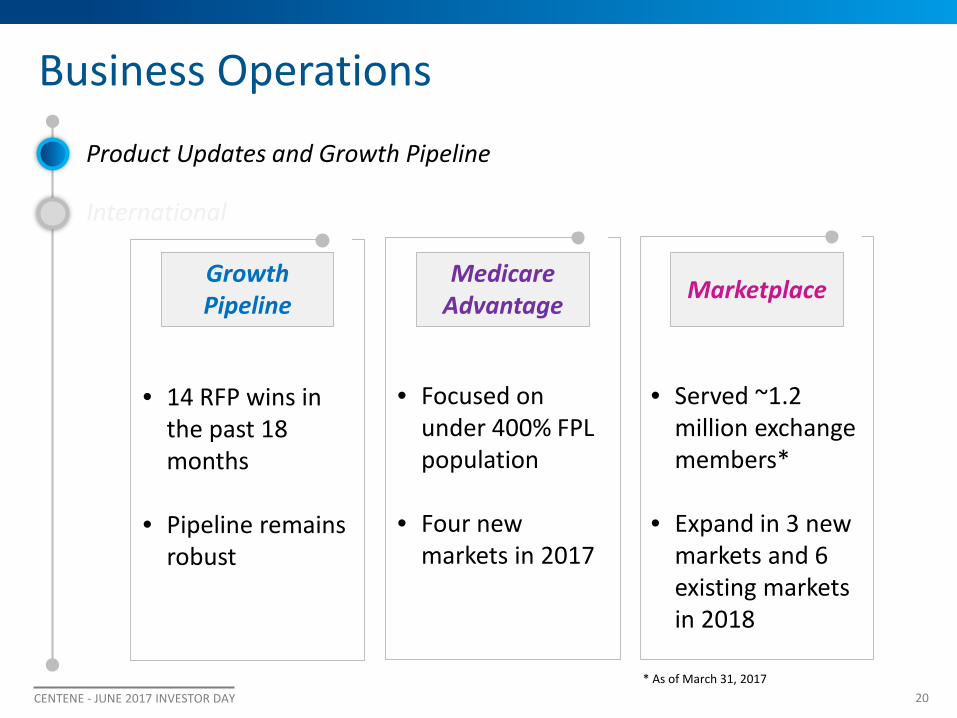

Business Operations

Product Updates and Growth Pipeline

International

GrowthPipeline

• 14 RFP wins in the past 18 months

• Pipeline remains robust

MedicareAdvantage

• Focused on under 400% FPL population

• Four new markets in 2017

Marketplace

• Served ~1.2 million exchange members*

• Expand in 3 new markets and 6 existing markets in 2018

* As of March 31, 2017

21CENTENE - JUNE 2017 INVESTOR DAY

Business Operations

International

World Economic Forum

22CENTENE - JUNE 2017 INVESTOR DAY

Poised for Continued Growth

2012

$46.4 billion

Today

2017 mid-point revenue guidance$8 billionRevenue:

2814States:Including 3 implementation markets

$13.6 billion$1.4 billionMarket Cap.:

30,9006,800Employees:

12 million2 millionMembers:

as of June 15, 2017

as of March 31, 2017

as of March 31, 2017

as of June 30, 2012

23CENTENE - JUNE 2017 INVESTOR DAY

Finance UpdateJeffrey Schwaneke – EVP, CFO & Treasurer

24CENTENE - JUNE 2017 INVESTOR DAY

1 Represents a non-GAAP measure. See Appendix A for reconciliation of non-GAAP measures.

(CONTINUING OPERATIONS)

Diluted EPS of $3.41

Total Revenues of $40.6 billionFortune 500 #66 + 78%

+ 18%

Revenues

Added 6.3 million members between years + 124%Membership

Diluted EPS

Adjusted Diluted EPS of $4.43 + 41%Adjusted Diluted EPS1

Health Benefits Ratio of 86.5%HBR 240 bps improvement

2016 Performance

25CENTENE - JUNE 2017 INVESTOR DAY

Diluted EPS of $0.79

Total Revenues of $11.7 billion + 69%

+ $0.91

Revenues

Added 605K members between years + 5%Membership

Diluted EPS

Adjusted Diluted EPS of $1.12 + 51%Adjusted Diluted EPS1

Health Benefits Ratio of 87.6%HBR 110 bps improvement

Q1 2017 Performance

1 Represents a non-GAAP measure. See Appendix A for reconciliation of non-GAAP measures.

26CENTENE - JUNE 2017 INVESTOR DAY

$ 42%Total Revenues1

EPS 40%Adj. Diluted EPS2

CNC 42%Stock Price3

Delivering ShareholderValue

5 Year Compound Annual Growth Rates2012-2017(F), excluding stock price

1 Based upon 2017 guidance midpoint.2 Represents a non-GAAP measure using the guidance midpoint. See Appendix A for reconciliation of non-GAAP measures. The 5 year GAAP diluted EPS CAGR is 37% using the guidance midpoint. 3 5 year stock price CAGR as of June 13, 2017.

27CENTENE - JUNE 2017 INVESTOR DAY

Source: SEC filings and Yahoo!Finance 2017 analyst estimates. Peer group includes Aetna, Anthem, Cigna, Humana, Molina, United and WellCare.

7% 8% 8%11%

13%

18%

27%

42%

CNC

Total Revenues CAGR vs. Peers5 YEAR CAGR, 2012-2017(F)

28CENTENE - JUNE 2017 INVESTOR DAY

$1.47

$2.31 $3.14

$4.43

2013 2014 2015 2016 2017 (F)

CNC 5 Year CAGR +40%2

Guidance Range

$4.50 – $4.90

Adjusted Diluted Earnings Per Share1(FROM CONTINUING OPERATIONS)

1 Represents a non-GAAP measure. See Appendix A for reconciliation of non-GAAP measures.2 Based on 2017 guidance range mid-point.

29CENTENE - JUNE 2017 INVESTOR DAY

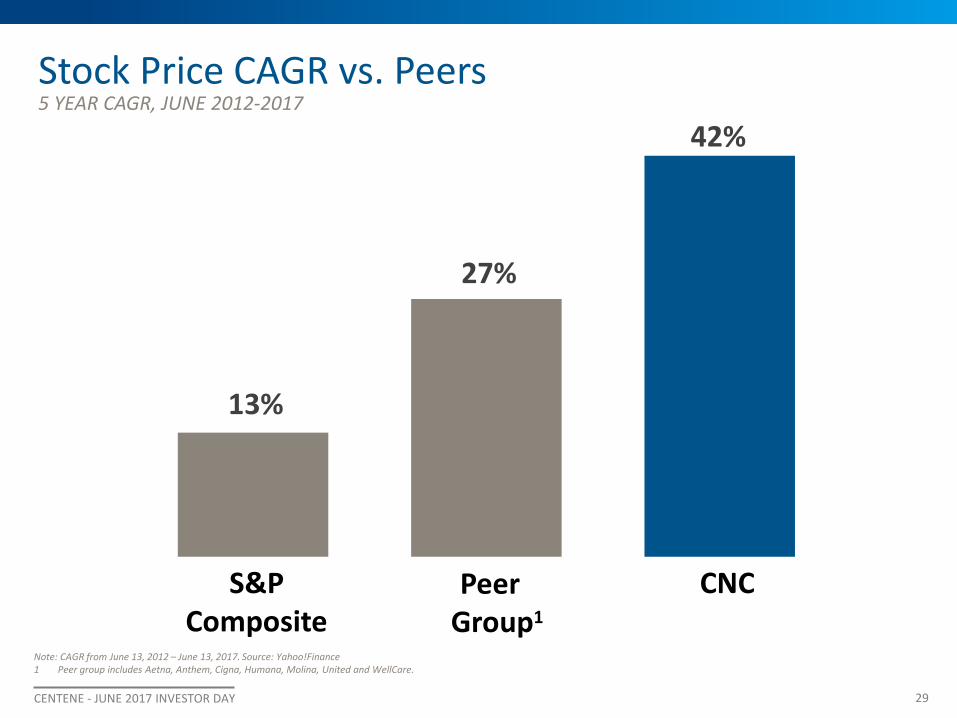

Note: CAGR from June 13, 2012 – June 13, 2017. Source: Yahoo!Finance1 Peer group includes Aetna, Anthem, Cigna, Humana, Molina, United and WellCare.

13%

27%

42%

Stock Price CAGR vs. Peers

S&P Composite

PeerGroup1

CNC

5 YEAR CAGR, JUNE 2012-2017

30CENTENE - JUNE 2017 INVESTOR DAY

2.6 2.94.1

5.1

11.4

$8.1 $10.9

$16.6

$22.8

$40.6

2012 2013 2014 2015 2016 2017(F)

Membership

Total Revenues

Guidance Mid-point

$46.4

Total Revenues/Membership Growth($ IN BILLIONS, MEMBERSHIP IN MILLIONS)

31CENTENE - JUNE 2017 INVESTOR DAY

-

500

1,000

1,500

2,000

2014 2015 2016 Q1 2017

Large/Small Group &Individual Off-Exchange

Health InsuranceMarketplace

Commercial Membership

Key Drivers:• Health Net acquisition• Growth in Health Insurance

Marketplace• Reached over 1 million

exchange members in Q1 2017

Commercial Expansion Driving Growth(MEMBERSHIP IN THOUSANDS)

●

●

●

States with large/small group & individual off-exchange membership●

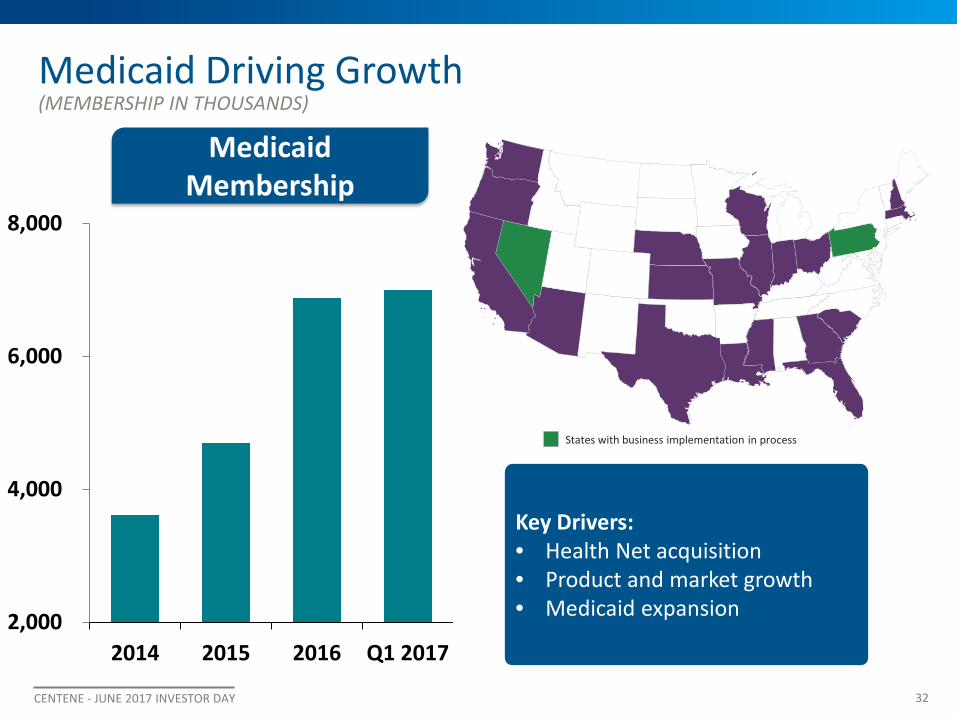

32CENTENE - JUNE 2017 INVESTOR DAY

2,000

4,000

6,000

8,000

2014 2015 2016 Q1 2017

Medicaid Membership

Key Drivers:• Health Net acquisition• Product and market growth• Medicaid expansion

Medicaid Driving Growth(MEMBERSHIP IN THOUSANDS)

States with business implementation in process

33CENTENE - JUNE 2017 INVESTOR DAY

2015: $22.8 Billion 2016: $40.6 Billion 2017(F): $46.4 Billion1

88.9%

86.5%8.3%

9.2%

2015 2016 2017(F)

HBR

Adj. SG&A2

1

Commercial and Medicare growth driving changes in

HBR & SG&A

Diversifying Revenues

Medicaid Medicare/Duals CommercialSpecialty/Government

2 Adjusted SG&A expense excludes certain items. See Appendix A for reconciliation of non-GAAP measures. 2017(F) excludes Health Net acquisition related expenses of $5 - $8 million and the Penn Treaty assessment expense of $47 million.

84%

2% 4%

10%

72%

13%9%

6%68%

17%

9%6%

1 Midpoint of guidance range.

34CENTENE - JUNE 2017 INVESTOR DAY

TANF, CHIP & Foster Care

64%

Commercial 17%

Other7%

Medicare/Duals3%ABD 8%

LTC 1%

TANF, CHIP, Foster CareAvg. PMPM $200–$600

CommercialAvg. PMPM $375

DualsAvg. PMPM $2,250

Long-Term CareAvg. PMPM $3,600

At-Risk Membership Characteristics

Other/Service

Lower HBR

ABDAvg. PMPM $900

Higher HBR

MedicareAvg. PMPM $1,000

35CENTENE - JUNE 2017 INVESTOR DAY

As of Q1 2017

Membership Revenue

Medicaid:

TANF, CHIP & Foster Care 61% 39%

ABD & LTC 9% 29%

Behavioral Health 5% 2%

Commercial 20% 19%

Medicare & Duals 3% 10%

Correctional 2% 1%

100% 100%

At-Risk Membership and Premium Revenue

36CENTENE - JUNE 2017 INVESTOR DAY

December 31, 2015

December 31, 2016

March 31,2017

Cash and investments $3,978 $9,118 $10,340

Total assets 7,339 20,197 21,362

Debt:

Senior notes, at par 925 4,600 4,600

Revolving credit agreement 225 100 100

Mortgage notes 67 64 63

Other debt & cap. leases 4 (109) (116)

Total debt 1,221 4,655 4,647

Total stockholders’ equity 2,168 5,909 6,084

Debt to capital ratio, excl. non recoursedebt

34.7% 43.7% 43.0%

Balance Sheet($ IN MILLIONS)

Reduced leverage by 130 basis points subsequent to the acquisition of Health Net

37CENTENE - JUNE 2017 INVESTOR DAY

Q12016

Q22016

Q32016

Q42016

Q12017

42.0%

42.5%

43.0%

43.5%

44.0%

44.5%

45.0%Strategically manage our

balance sheet

Debt to capital ratio expected to be in low 40%’s by Q4 2017Note: excludes non-recourse mortgage note

Leverage

Continue to reduce our debt-to-capital ratio

Aligning financial statement exposure through interest

rate swaps

38CENTENE - JUNE 2017 INVESTOR DAY

Balance March 31, 2017

March 31, 2017Effective

Interest Rate1

$1,400 million 5.625% Senior Notes, due February 2021 $1,400 5.47%

$1,000 million 4.75% Senior Notes, due May 2022 $1,008 3.98%

$1,000 million 6.125% Senior Notes, due February 2024 $1,000 5.48%

$1,200 million 4.75% Senior Notes, due January 2025 $1,200 4.10%

Revolving credit agreement $100 4.50%

Total Debt/ Weighted average rate $4,708 4.78%

1 Including impact of any interest rate swaps.

Senior Notes and Revolver

Centene’s S&P rating upgraded to ‘BB+’ from ‘BB’ in May 2017

($ IN MILLIONS)

39CENTENE - JUNE 2017 INVESTOR DAY

$6.0B$4.3B

Investment PortfolioQ1 2017

$2.7B$2.0B

Total DebtQ1 2017

Swapped Floating Rate Debt at 1 or 3

month LIBOR

Floating rate debt expense offset by

short-term investment income

Cash & Investments highly correlated to

LIBOR rate

Impact of Short-Term Interest Rates

40CENTENE - JUNE 2017 INVESTOR DAY

Estimated Impact of Change in 3-Month LIBORAs of March 31, 2017.

($7 )($14)

($20)($27)

$11

$22

$32

$43

Interest Expense Interest Income

+$4

+$8

+$12

+$16

Annual Net Favorable Pre-tax Impact

Impact of Short-Term Interest Rates

+75 bps+50 bps+25 bps +100 bps

($ IN MILLIONS)

41CENTENE - JUNE 2017 INVESTOR DAY

32.7% 36.7% 34.9% 36.7%

0.3%0.4%

2.1%3.3%9.9%

11.5% 14.8%

2014 2015 2016 2017(F)

Nondeductible Compensation

ACA Health Insurer Fee

All Other Income Tax

42.9%

51.8%48.6%

39-41%

2017 nondeductible compensation represents approx. $38M or $0.211 per diluted share of income tax expense.

Effective Tax Rate

1 Based on 2017 guidance range mid-point.

42CENTENE - JUNE 2017 INVESTOR DAY

Timeline – uncertain based on current

environment

Immediate tax deduction for capital

expenditures

Corporate tax rate from 35% to

15%-20%

Potential implications of proposed tax reform

Eliminate net interest expense

deduction

Proposed Income Tax Reform

43CENTENE - JUNE 2017 INVESTOR DAY

Effective TaxRate

CorporateTax Rate

Net InterestAddback

CompensationDeductions

Annualized RateOutlook with

Proposed Reforms

Tax ReformHealthcare

Reform

39-41%

Potential Implications of Tax & Healthcare Reform

18-25%

(15-20%)+2% (3%)

In addition, we would benefit from a one-time deferred rate change of ~15% in the year tax reform is enacted (>$100 million after tax).

44CENTENE - JUNE 2017 INVESTOR DAY

$792

$1,534 $129

$270

2015 2016 2017 (F)

HIF Impact$1,804

$921Guidance

Range $1,800 to

$2,000

Adjusted EBITDA1

1 Represents a non-GAAP measure. See Appendix A for reconciliation of non-GAAP measures.2 Based on 2017 guidance range mid-point.

YOY Increase 45% 96% 5%2

Adj. EBITDA as % of Revenue 4.0% 4.4% 4.1%2

($ IN MILLIONS)

45CENTENE - JUNE 2017 INVESTOR DAY

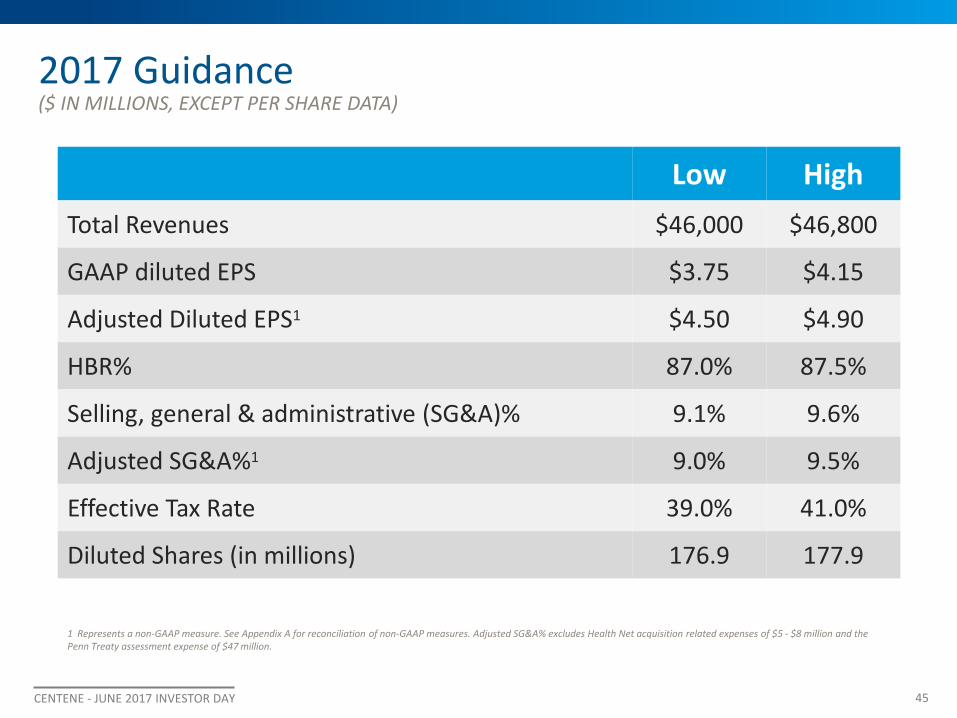

Low HighTotal Revenues $46,000 $46,800

GAAP diluted EPS $3.75 $4.15

Adjusted Diluted EPS1 $4.50 $4.90

HBR% 87.0% 87.5%

Selling, general & administrative (SG&A)% 9.1% 9.6%

Adjusted SG&A%1 9.0% 9.5%

Effective Tax Rate 39.0% 41.0%

Diluted Shares (in millions) 176.9 177.9

1 Represents a non-GAAP measure. See Appendix A for reconciliation of non-GAAP measures. Adjusted SG&A% excludes Health Net acquisition related expenses of $5 - $8 million and the Penn Treaty assessment expense of $47 million.

2017 Guidance($ IN MILLIONS, EXCEPT PER SHARE DATA)

46CENTENE - JUNE 2017 INVESTOR DAY

Update: Markets Christopher Bowers, EVP - Markets

47CENTENE - JUNE 2017 INVESTOR DAY

State Health Plan Membership Growth

0.0

1.0

2.0

3.0

4.0

5.0

6.0

3.7M

0.5M<15k0.1M

4.4M

(in m

illio

ns)

Total Membership(as of 1/1/16)

*excludes Correctional, Behavioral Health, Federal Services, ASO and Envolve membership

Medicaid Complex Care Commercial Medicare

48CENTENE - JUNE 2017 INVESTOR DAY

State Health Plan Membership Growth

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

Medicaid Complex Care Commercial Medicare

5.7M,~50%

0.8M,~60%

0.3M,~2,600%

1.9M,~1,800%

Total Membership(as of 3/31/17)

8.7M, ~100%

(in m

illio

ns)

*excludes Correctional, Behavioral Health, Federal Services, ASO and Envolve membership

49CENTENE - JUNE 2017 INVESTOR DAY

Increasing Scale and Diversification

HEALTH PLANS BY PREMIUM SIZE

12

1

10

12

Under $1 billion Over $1 billion

2017(P)

2012

50CENTENE - JUNE 2017 INVESTOR DAY

Key Membership Drivers in 2017

12/31/16 2017(P)

Marketplace

New States (NE, NV)

ExistingMarket

Expansions

OrganicGrowth

2017 Growth Areas

~9%

*excludes Correctional, Behavioral Health, Federal Services, ASO and Envolve membership

51CENTENE - JUNE 2017 INVESTOR DAY

2017 Market Updates

State Start Date Product Mix

EstimatedMarket Size

Numberof Plans Membership

NE 1/1/17 All populations(acute only –LTSS & I/DD)

228,000 3 plans 79k*

MO 5/1/17 Medicaid 737,500 3 plans 280k**

NV 7/1/17 TANF, CHIP, Medicaid Expansion 425,000 4 plans ~35k**

*as of March 31, 2017**Estimates

52CENTENE - JUNE 2017 INVESTOR DAY 52

ManagingMarket Level

Trends

53CENTENE - JUNE 2017 INVESTOR DAY

Centene Playbook to Offset Trends

Trends

HBRInitiatives

PaymentIntegrity

Public PolicyEngagement

QualityManagement

RiskAdjustment

Actuarial Coordination

54CENTENE - JUNE 2017 INVESTOR DAY

Centene Medicaid Rate Experience

2014 2015 2016

Est. Cost Trend 1.5%-2.5%

Net Rate Increase 0-1%

Health Benefits Ratio Consistent HBR performance

Playbook strategies maintain HBR levels despite increasing trends

55CENTENE - JUNE 2017 INVESTOR DAY

Plan Example - Large Traditional Medicaid Product

Strategies to Offset to Medical Trend

• ED utilization reduction of ~5% (onsite ED Diversion)

• Improved Rx utilization by 12% to mitigate inflationary pressures

• Incremental payment integrity strategies

56CENTENE - JUNE 2017 INVESTOR DAY

Continue to Generate Strong Growth Through:

• Expansion and retention of existing business

• Acquisition of new business

• Broader product penetration

Managing and offsetting rate pressures and cost trends through our

comprehensive playbook of Health Plan tools and strategies

57CENTENE - JUNE 2017 INVESTOR DAY

Business Unit UpdateSteven Sell, CEO & Plan President - CA Market

58CENTENE - JUNE 2017 INVESTOR DAY

California: Progress Update

Improved financial performance

Improved operational performance

Well positioned for the future

15 Months after the Merger Close

59CENTENE - JUNE 2017 INVESTOR DAY

A Large Market….• 39M Californians• Over 27M in risk-based care models*

In All Segments….• Medicaid, Medicare, Duals• Employer Group, Individual• Military, Correctional• Specialty

With Strong Stakeholder Alignment.• Physicians, Medical Groups, Hospitals• CDI, DMHC, DHCS, CMS, CovCA• Brokers, GA’s and Consultants

California: Market Overview

* Does not include self-insured population (approx. 6M) or Medicare FFS population (approx. 3.5M)

60CENTENE - JUNE 2017 INVESTOR DAY

Improved Financial Performance

• No Premium Deficiency Reserves taken for 2017

• On track to meet all merger-related synergy targets

• Successfully managing Medicaid Expansion rates

• Expertise in managing heavily capitated population

• Applying rigor to management of Fee For Service costs

Leveraging Best of Both Model

Financial Performance

61CENTENE - JUNE 2017 INVESTOR DAY

Operational Performance

• Processing improvements

• Medical cost reduction initiatives

• Expanded fraud, waste & abuse capability

• Enhanced case management

• Insourcing care management to Centene systems & processes

• Concurrent review

Medical Management

Claims Management

62CENTENE - JUNE 2017 INVESTOR DAY

Operational Performance cont’d

• Improved Covered CA Net Promoter Score

• Positive member satisfaction trend

• Network is stable

• Maintaining low medical cost trend

• Improved management of FFS providers

• Risk Adjustment improvements

Provider Engagement

Quality & Customer Experience

63CENTENE - JUNE 2017 INVESTOR DAY

California Market Culture

Local Accountability and Control

Employee Engagement and Development

Performance Orientation

64CENTENE - JUNE 2017 INVESTOR DAY

• Medicaid

• Duals/MMP

• Correctional Health

Well Positioned for the Future

Medicaid Plan with ~2M lives and 19%

market share

Market share statewide with

~3M lives

#1 11%

Power of MCO Portfolio

A Market Leader

12% Market Share in Sacramento

29% Market Share in the Central Valley

18% Market Share in Los Angeles County

*as of March 31, 2017

65CENTENE - JUNE 2017 INVESTOR DAY

Update: Products Jesse Hunter, EVP - Products

66CENTENE - JUNE 2017 INVESTOR DAY

Product Focus

National Product Leadership

Multi-Product Strategy

Marketplace Update

Medicare Update

67CENTENE - JUNE 2017 INVESTOR DAY

Product Focus

National Product Leadership

Multi-Product Strategy

Marketplace Update

Medicare Update

68CENTENE - JUNE 2017 INVESTOR DAY

Product Objective

EnvolveHealth

FederalServices

Commercial(Marketplace)

Medicare

ComplexCare

Medicaid

Market leading products focused on

government sponsored healthcare

programs

69CENTENE - JUNE 2017 INVESTOR DAY

Demonstrating Product Leadership

1st or 2nd in Membership

NationalMarket leadingposition across

Products

1987

2007

2008

2013

2014

2017

1984

70CENTENE - JUNE 2017 INVESTOR DAY 70

AHIPProduct Thought Leadership

MHPA

MACPAC

MLTSS

AMSUS

ECHBC

National MLTSS Health Plan Association

Medicaid and CHIP Payment and Access Commission

Association of Military Surgeons of the United States

America’s Health Insurance Plans

Medicaid Health Plans of America

Envolve Center for Health Behavior Change

71CENTENE - JUNE 2017 INVESTOR DAY

Product Focus

National Product Leadership

Multi-Product Strategy

Marketplace Update

Medicare Update

72CENTENE - JUNE 2017 INVESTOR DAY

Multi-Product Strategy

Medicaid

Medicare & Duals

MSO

Correctional Marketplace

73CENTENE - JUNE 2017 INVESTOR DAY

Product Focus

National Product Leadership

Multi-Product Strategy

Marketplace Update

Medicare Update

74CENTENE - JUNE 2017 INVESTOR DAY

Membership Demographics

93%

7%

2015* 2016 2017

93%

* 2015 does not include Health Net

7% 9%

91%

78%

22%

2015* 2016 2017

85%

12% 8%

90%

3% 2%

Subsidized

Unsubsidized

Premium Subsidies

Silver

Bronze

Gold & Platinum

Metal Tier

75CENTENE - JUNE 2017 INVESTOR DAY 75

Peak Membership

2014 76,000

2015 167,000

2016 683,000

2017 1,200,000

2017 Marketplace Footprint

Centene State

Centene HIM Membership

#1 National Carrieron Marketplace

76CENTENE - JUNE 2017 INVESTOR DAY

Carrier Exit Case Study – Broward County, FL

Carrier’s market exit resulted in a large number of auto-assignments, including 18,000 members assigned to Ambetter

Premium Subsidy

CostSharing

Reduction

Total Enrollees

Members Auto Assigned to Ambetter 83.6% 70.0% 18,114

Auto Assignments that Effectuated with Ambetter 95.1% 84.9% 6,564

All New Ambetter Members 92.9% 79.8% 55,202

77CENTENE - JUNE 2017 INVESTOR DAY

Path to 2018

5/1 - 6/21Initial State Filings

5/1 - 8/16DOI Reviews, Negotiations and Revisions

May Dec.Nov.Oct.Sept.Aug.Jul.Jun.

8/1 - 8/16Rate Finalization by DOIs and Handoff to CMS

8/20Court Date for CSRs

9/16 - 9/27FFM QHP certification signing

10/12Feds FFM QHP certification signing

11/1 – 12/15Open Enrollment

2 0 1 7

78CENTENE - JUNE 2017 INVESTOR DAY

• 2018 “business as usual” approach based on ACA• Plan design and pricing reflect market variability and need for flexibility

• Pursue strategic expansion and membership growth• Strive to maintain our price advantage• Deliver targeted profit margin

Centene State

Centene HIM Membership

New HIM Markets in 2018

HIM Expansion Markets

2018 Marketplace Positioning

79CENTENE - JUNE 2017 INVESTOR DAY

Product Focus

National Product Leadership

Multi-Product Strategy

Marketplace Update

Medicare Update

80CENTENE - JUNE 2017 INVESTOR DAY

2017 Medicare Profile Products

MA /MAPD

D-SNP

I-SNP

80

• Membership: 328,000 (March 31, 2017)

• $3B Medicare Platform (2016)

• Multi-product

• Multi-state

• 4 Star Parent Organization Rating

Centene State

Centene Medicare Market

MMP

C-SNP

Med. Supp.

EGWP

81CENTENE - JUNE 2017 INVESTOR DAY

Medicare Strategy

Geography Beneficiary Plan Design

Focus onCNC Markets

Focus onindividuals

under 400% FPL

Creating lowor no cost

premium plans

82CENTENE - JUNE 2017 INVESTOR DAY

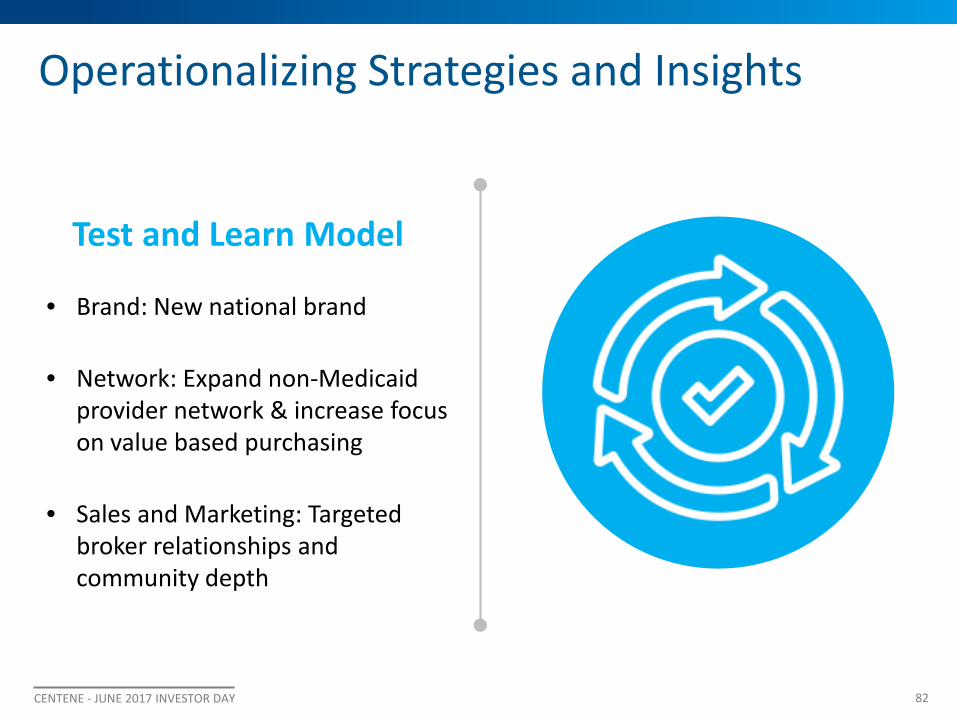

Operationalizing Strategies and Insights

Test and Learn Model

• Brand: New national brand

• Network: Expand non-Medicaid provider network & increase focus on value based purchasing

• Sales and Marketing: Targeted broker relationships and community depth

83CENTENE - JUNE 2017 INVESTOR DAY

2018 OutlookFocused Growth Strategy

• Submitted 11 new market LOIs originally and plan to enter six new markets

• Launch two D-SNP focused markets

• Additional growth investment in new 2017 markets

• Launch targeted 2018 markets that align with network, plan design, and sales opportunity

Medicare to represent 20%+ of total Centene growth

Longer-term Expectations:

84CENTENE - JUNE 2017 INVESTOR DAY

Industry Leading Multi-Product Portfolio

Ability to leverage multi-product portfolio

Demonstrated commitment to national product leadership

Focused on diversified growth across government healthcare landscape

85CENTENE - JUNE 2017 INVESTOR DAY

Value in ExperienceC. David Minifie, Chief Experience Officer & EVP

86CENTENE - JUNE 2017 INVESTOR DAY

Transforming the Health of the Community, One Person at a Time

OUR PURPOSE | why we do what we do

OUR BRAND PILLARS | How we go about doing it

Focus on the Individual

WholeHealth

Active LocalInvolvement

87CENTENE - JUNE 2017 INVESTOR DAY

Focus on the IndividualWhat are the challenges our consumers face on the road to better health?

KNOWN & UNKNOWN

PRESENT & FUTURE

DIRECT & INDIRECT

88CENTENE - JUNE 2017 INVESTOR DAY

MEMBERS AND THEIR FAMILIES, PROVIDERS & CAREGIVERSan expansive consumer ecosystem, includes

89CENTENE - JUNE 2017 INVESTOR DAY

Changing Landscape

HISTORICAL BUSINESS CONSUMER REALITY

• Auto-assignment• State Government• Product• Transaction

• Consumer Choice• Individual Consumer• People• Engagement

Satisfaction drives results

More Likely to Renew

More Likely to Recommend

More Likely to Forgive

More Likely to Try a New Offering

92%

88%

67%

57%

90CENTENE - JUNE 2017 INVESTOR DAY

91CENTENE - JUNE 2017 INVESTOR DAY

Learning More About Our Consumers

Sophisticated Segmentation Research Detailed Mapping & Targeting

TO WHERE THEY AREFROM WHO THEY ARE

92CENTENE - JUNE 2017 INVESTOR DAY

Local Still Matters

93CENTENE - JUNE 2017 INVESTOR DAY

*Figures represent Ambetter membership only (does not include Covered CA members)

94CENTENE - JUNE 2017 INVESTOR DAY

Adults 65+Includes those who are

about to “age-in,” as well as switchers.

95CENTENE - JUNE 2017 INVESTOR DAY

• Brand matters; hard to break in with well-entrenched competitors

• Overall Medicare-eligible carrier switching is small in any one year (about 6%)

• Major switch triggers are: bad customer experience, PCP falling out of plan, Rx price changes

• Age-ins shop for: brand, price/cost, doctor, formulary• Providers can be very influential, as can brokers/agents

The Consumer: Highlights

96CENTENE - JUNE 2017 INVESTOR DAY

Emotional Journey to Get to a Medicare Plan Decision

“Do I qualify for Medicare?”“What does MA cover?”

“Do I need other coverage?”

“What are my options?”“What plan is best for me?”

“How do I enroll?”

Most feel confusion, uncertainty & anxiety

Our goal: guided, confident & relieved

97CENTENE - JUNE 2017 INVESTOR DAY

98CENTENE - JUNE 2017 INVESTOR DAY

• The name Allwell is simple, clear and easy to understand.

• Individuals feel that the name conveys the concepts of “good health and being taken care of.”

• Tested well against competitor brands already in market.

CONSISTENTLY PERFORMED WELL IN RESEARCH AMONG MEDICARE ELIGIBLES

Medicare consumers prefer a brand with a local extension, with 61% of consumers preferring a local brand name.

99CENTENE - JUNE 2017 INVESTOR DAY

Local, flexible and scalable brand architecture

Trusted, local partner for all Texans and their community

Covers full range of government-sponsored Medicaid & Children’s Health Insurance Plans (CHIP)

STATE-BASED MARKET BRAND

PRODUCT BRAND FOR MARKETPLACE

PRODUCT BRAND FOR MEDICARE

EXTENSIONS FOR CONSUMER CATAGORIES

100CENTENE - JUNE 2017 INVESTOR DAY

Transforming the Health of the Community, One Person at a Time

OUR PURPOSE | why we do what we do

OUR BRAND PILLARS | How we go about doing it

Focus on the Individual

WholeHealth

Active LocalInvolvement

101CENTENE - JUNE 2017 INVESTOR DAY

Question and Answer

Break

SSID: Centene Corp Password: welcome2017

2017 Investor Day

103CENTENE - JUNE 2017 INVESTOR DAY

Growth and DiversificationCynthia Brinkley, EVP - Global Corporate Development

104CENTENE - JUNE 2017 INVESTOR DAY 104

$677BAddressable Markets Pipeline $798B

$100B

$9B

$105B

$175B

Correctional Healthcare

Health Insurance Marketplace

Federal Services

Medicaid

Medicare

International*Data based on Congressional Budget Office projections and Company estimates for FY 2019

$1.86 trillion*

105CENTENE - JUNE 2017 INVESTOR DAY 105

Correctional Healthcare

Health Insurance Marketplace

Federal Services

Medicaid

Medicare

International

$249 billion

TargetedPipeline

106CENTENE - JUNE 2017 INVESTOR DAY

2018 Revenue Visibility

2017P 2018P

• HIM and Medicare Market Expansions

• Full Year of MO & NV• PA Go-live• IL, MS, MA

Reprocurements• New Envolve Contracts • HIF Return

• CA In-Home Support Services (IHSS) carve-out

GROWTH DRIVERS

$50B+

$46.4B

2018P

$51B+

*2017 mid-point of guidance range

107CENTENE - JUNE 2017 INVESTOR DAY

Growth Verticals

Existing Markets

New Markets

Specialty Products

Medicare Advantage

M&A

108CENTENE - JUNE 2017 INVESTOR DAY

Growth Verticals

Existing Markets

New Markets

Specialty Products

Medicare Advantage

M&A

109CENTENE - JUNE 2017 INVESTOR DAY

2017 Success

North Central Region Integrated Physical and Behavioral Health

• Awarded May 22nd ; Go-Live January 1, 2018

110CENTENE - JUNE 2017 INVESTOR DAY

Existing Market - Pending Announcements

MississippiCAN Reprocurement

RFP submitted Apr. 7th

MassHealth Reprocurement

RFP submitted Apr. 13th

ICP & Family Health Plan Reprocurement

RFP submitted May 15th

111CENTENE - JUNE 2017 INVESTOR DAY

Existing Market - Reprocurements

CHIP Rural Service Area ReprocurementRFP due July 2017

Go-Live September 2018

STAR+PLUS ReprocurementRFP anticipated August 2017

Go-Live February 2019

STAR and CHIP ReprocurementRFP anticipated in 2018Go-Live January 2020

Statewide Medicaid Managed Care and Long Term Care Reprocurement

RFP anticipated last week of JuneGo-Live January 2019

Acute Care ReprocurementRFP expected early November 2017

Go-Live October 2018

KanCare ReprocurementRFP anticipated late 2017

Go-Live January 2019

112CENTENE - JUNE 2017 INVESTOR DAY

Existing Markets HIM Membership Growth (Peak)

112

Centene State

Centene HIM Market (2018)

New HIM Market (2018)

HIM Expansion Market (2018)

Centene Medicare Market (2017)

2015

167,000

2016

683,000

2017

1,200,000

328,000Medicare &

Duals Members

(Q1 2017)

113CENTENE - JUNE 2017 INVESTOR DAY

Growth Verticals

Existing Markets

New Markets

Specialty Products

Medicare Advantage

M&A

114CENTENE - JUNE 2017 INVESTOR DAY

New Markets

Heritage Health

Went live 1/1/17

Managed Care Program

7/1/17 go-live

Community HealthChoicesPhased in from

1/1/18 to 1/1/19

HealthChoices1/1/18 go-live

115CENTENE - JUNE 2017 INVESTOR DAY

Growth Verticals

Existing Markets

New Markets

Specialty Products

Medicare Advantage

M&A

116CENTENE - JUNE 2017 INVESTOR DAY

Specialty Products

Addressing market needs and driving external

revenue growth via an integrated platform that leverages the strength of

Centene’s specialty solutions

REPRESENTATIVE CLIENTS

Population health technology, risk stratification, care coordination and project management support

Presenter

Presentation Notes

Aon Hewitt Care management, behavioral health, pharmacy benefit and health & wellness services Texas Association of Community Health Centers Nurse Advice Line services for 1.2 million Texans offered through a group purchasing arrangement with TACHC. Maryland Physicians Care Comprehensive backroom supports and services for health plan serving 185,000 Medicaid members.

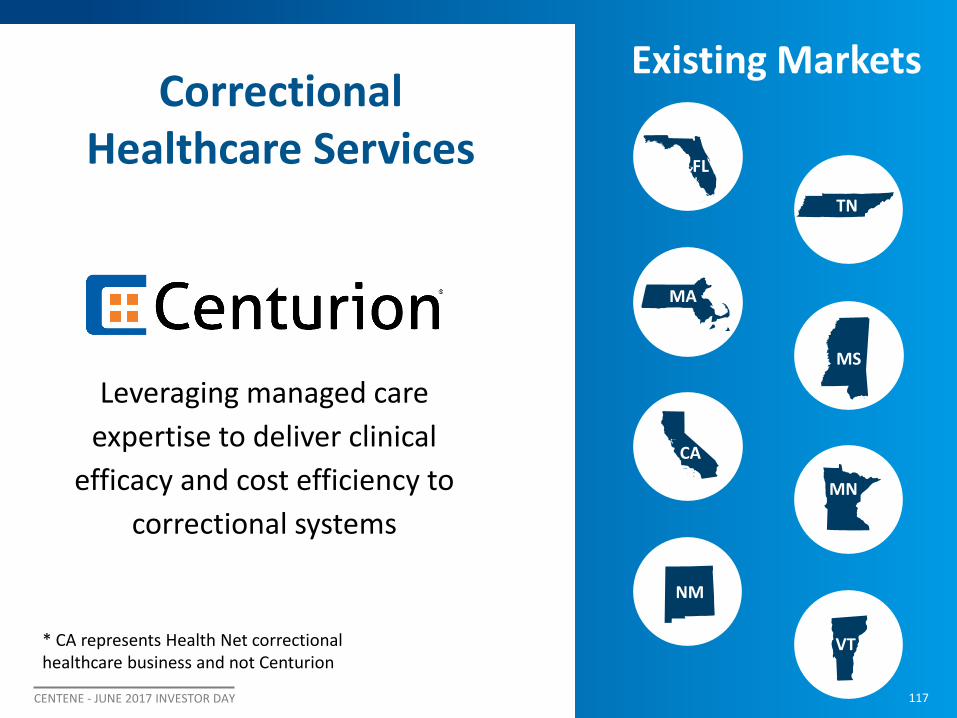

117CENTENE - JUNE 2017 INVESTOR DAY

Correctional Healthcare Services

Existing Markets

117

Leveraging managed care expertise to deliver clinical

efficacy and cost efficiency to correctional systems

* CA represents Health Net correctional healthcare business and not Centurion

NM

MS

MN

MA

VT

TN

CA

FL

118CENTENE - JUNE 2017 INVESTOR DAY

Growth Verticals

Existing Markets

New Markets

Specialty Products

Medicare Advantage

M&A

119CENTENE - JUNE 2017 INVESTOR DAY

Medicare Advantage

GROWTH STRATEGY

• Targeting low-income enrollees <400% FPL

• Building upon the strength of Centene’s local approach

• Leveraging parent organization’s 4-Star rating

• Entering new markets

• Expansion in current markets

120CENTENE - JUNE 2017 INVESTOR DAY

Growth Verticals

Existing Markets

New Markets

Specialty Products

Medicare Advantage

M&A

121CENTENE - JUNE 2017 INVESTOR DAY

M&A Strategic Objectives

CAPABILITYM&A targets that add capabilities for existing service offerings

SCALEAdd scale to existing operations and increase our geographic footprint

VALUECREATION

Generating appropriate returns on our investments for our shareholders

CONSISTENT CRITERIA & FINANCIAL DISCIPLINE

122CENTENE - JUNE 2017 INVESTOR DAY

In Summary…

Scale Momentum RobustPipeline

WE ARE A GROWTH COMPANY

123CENTENE - JUNE 2017 INVESTOR DAY

Healthcare Policy UpdatePanel Discussion

124CENTENE - JUNE 2017 INVESTOR DAY

Healthcare Policy Update

Haley Barbour, Founding Partner - BGR Group;Former Governor of Mississippi

Richard GephardtCentene Board Member; CEO – Gephardt Group; Former Majority Leader of the U.S. House of Representatives

David SchiappaPartner at the Duberstein Group

Joe AntosWilson H. Taylor Scholar in Health Care and Retirement Policy –American Enterprise Institute

Jonathan DinesmanSVP, Government Relations - Centene

125CENTENE - JUNE 2017 INVESTOR DAY

Question and Answer

126CENTENE - JUNE 2017 INVESTOR DAY

Finance Update: Appendix A

127CENTENE - JUNE 2017 INVESTOR DAY

Reconciliation of GAAP Earnings from Continuing Operations to Adjusted Diluted EPS:2012 2013 2014 2015 2016 Q1 2016 Q1 2017

GAAP Earnings from continuing operations 89$ 161$ 268$ 356$ 559$ (15)$ 139$ Amortization of acquired intangible assets 5 6 16 24 147 9 40 Health Net acquisition related expenses - - - 27 234 189 5 California minimum medical loss ratio change - - - - (195) - - Charitable contribution - - - - 50 - - Debt extinguishment - - - - 11 - - Penn Treaty assessment expense - - - - - - 47 Income tax effects of adjustments (2) (2) (6) (20) (79) (87) (34)

Adjusted Earnings from Continuing Operations 92$ 165$ 278$ 387$ 727$ 96$ 197$ Diluted shares outstanding (in thousands) 107,429 112,494 120,360 123,066 163,975 129,531 175,836

GAAP diluted EPS from Continuing Operations 0.83$ 1.43$ 2.23$ 2.89$ 3.41$ (0.12)$ 0.79$ Adjusted Diluted EPS 1 0.86$ 1.47$ 2.31$ 3.14$ 4.43$ 0.74$ 1.12$

Reconciliation of GAAP diluted EPS to Adjusted Diluted EPS:

GAAP diluted EPSAmortization of acquired intangible assets 2

Health Net acquisition related expenses 3

Penn Treaty assessment expense 4

Adjusted Diluted EPS 1

$0.54 - $0.58 $0.02 - $0.03

$0.17 $4.50 - $4.90

$3.75 - $4.15

Annual Guidance December 31, 2017

Included in this presentation is Adjusted Diluted EPS. Management believes that this non-GAAP financial measure provides information that is useful to investors in understanding period-over-period operating results and enhances the ability of investors to analyze Centene’s business trends and performance. This non-GAAP financial measure should not be considered in isolation, or as a substitute for the corresponding GAAP financial measure and may not be comparable to similar measures used by other companies. A reconciliation of this non-GAAP financial measure with the most directly comparable financial measure calculated in accordance with GAAP follows:

1 Adjusted Diluted EPS is defined as GAAP diluted net earnings from continuing operations before amortization of acquired intangible assets, Health Net acquisition related expenses, and the tax impact of such adjustments, calculated on a per share basis. In 2016, Adjusted Diluted EPS excludes debt extinguishment costs and the impact associated with the retroactive change in the minimum MLR calculation and associated charitable contribution. In Q1 2017, Adjusted Diluted EPS excludes the Penn Treaty assessment expense. We believe these adjustments are not indicative of future performance.

2 The amortization of acquired intangible assets per diluted share presented are net of the income tax benefit estimated to be $0.31 to $0.35 for the year ended December 31, 2017.

3 The Health Net acquisition related expenses per diluted share presented are net of the income tax benefit estimated to be $0.01 to $0.02 for the year ended December 31, 2017.

4 The Penn Treaty assessment expense per diluted share is net of the estimated income tax benefit of $0.09 for the year ended December 31, 2017.

Reconciliation of Non-GAAP Measures($ IN MILLIONS, EXCEPT PER SHARE DATA)

128CENTENE - JUNE 2017 INVESTOR DAY

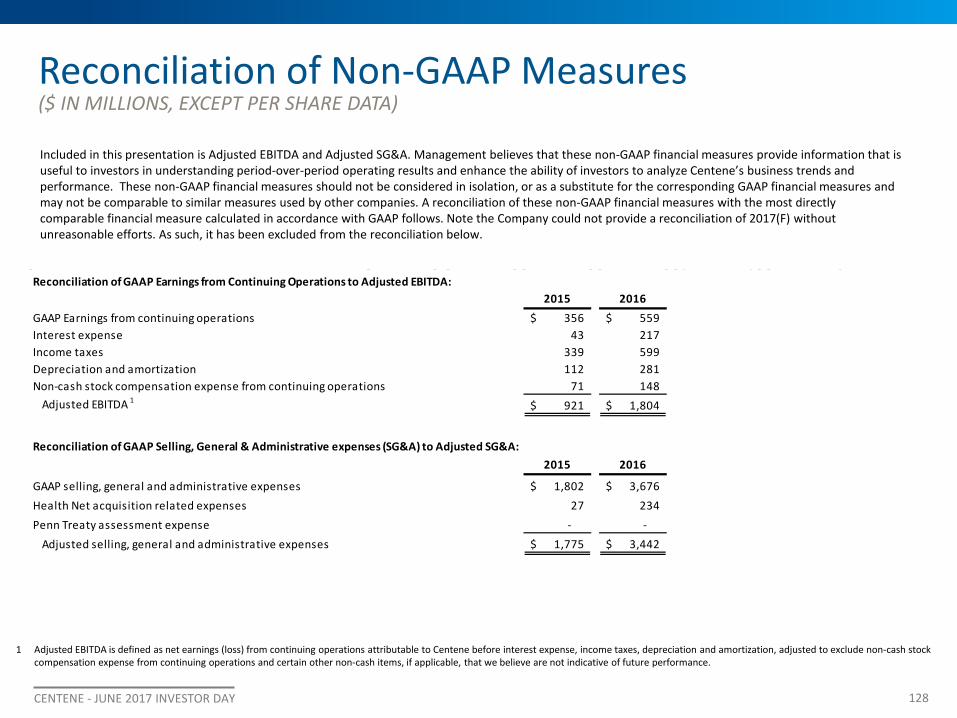

Reconciliation of GAAP Earnings from Continuing Operations to Adjusted EBITDA:2015 2016

GAAP Earnings from continuing operations 356$ 559$ Interest expense 43 217 Income taxes 339 599 Depreciation and amortization 112 281 Non-cash stock compensation expense from continuing operations 71 148 Adjusted EBITDA 1 921$ 1,804$

Reconciliation of GAAP Selling, General & Administrative expenses (SG&A) to Adjusted SG&A:2015 2016

GAAP selling, general and administrative expenses 1,802$ 3,676$ Health Net acquisition related expenses 27 234 Penn Treaty assessment expense - - Adjusted selling, general and administrative expenses 1,775$ 3,442$

Included in this presentation is Adjusted EBITDA and Adjusted SG&A. Management believes that these non-GAAP financial measures provide information that is useful to investors in understanding period-over-period operating results and enhance the ability of investors to analyze Centene’s business trends and performance. These non-GAAP financial measures should not be considered in isolation, or as a substitute for the corresponding GAAP financial measures and may not be comparable to similar measures used by other companies. A reconciliation of these non-GAAP financial measures with the most directly comparable financial measure calculated in accordance with GAAP follows. Note the Company could not provide a reconciliation of 2017(F) without unreasonable efforts. As such, it has been excluded from the reconciliation below.

1 Adjusted EBITDA is defined as net earnings (loss) from continuing operations attributable to Centene before interest expense, income taxes, depreciation and amortization, adjusted to exclude non-cash stock compensation expense from continuing operations and certain other non-cash items, if applicable, that we believe are not indicative of future performance.

Reconciliation of Non-GAAP Measures($ IN MILLIONS, EXCEPT PER SHARE DATA)

Thank You!

SSID: Centene Corp Password: welcome2017

2017 Investor Day