2016 Half Year Results - Nexans 2016_ ppt10.pdfNexans cables to connect Beatrice Offshore Windfarm...

35

2016 Half Year Results Photo Credits: David Beman, a Nexans employee July 28, 2016

-

Upload

nguyendang -

Category

Documents

-

view

215 -

download

0

Transcript of 2016 Half Year Results - Nexans 2016_ ppt10.pdfNexans cables to connect Beatrice Offshore Windfarm...

2016 Half Year Results

Photo Credits: David Beman, a Nexans employee

July 28, 2016

Safe Harbor ● Forward-looking statements in this presentation are subject to various risks and uncertainties that could affect the

Company's future performance. Actual results could therefore differ significantly from those currently expected or anticipated.

● Readers are also invited to log onto the Group's website where they can view and download the press release of the annual results and the 2015 financial statements, which include a description of the Group’s risk factors. Readers can also view and download the 2016 half-year financial statements, which include information on the investigations launched in 2009 on anti-competitive behavior in the submarine and underground high-voltage cable sector in various countries (see Note 15a, “Antitrust Investigation”).

● The main uncertainties related to the second half of 2016 primarily relate to : depressed demand in Oil & Gas related markets which could deteriorate further, potentially impacting several businesses in the Group,

and in particular the US based Amercable business which is also impacted by similar factors in the mining segment depressed demand in shipyards in China and Korea could impact order entry, and therefore revenues for subsequent periods impact of political instability and economic contraction in Brazil where demand levels may not stabilize and customer credit risks may

increase further. Brexit impacts which could include decreased growth in European economies generally, and in relation to the UK, notwithstanding the

absence of local cable production by the Group, (i) possible delays in financing of large infrastructure projects ongoing or planned in that country which could result in slow down of orders for the HV business, (ii) and possible exchange rate fluctuations which could penalize other exports to the UK.

economic developments in Greece and their impact on the Group's operations in that country; the economic and political environment in certain emerging markets where Nexans makes sales including in particular Lebanon, Libya

and Russia possible negative impact of recent or ongoing plant closures and reorganizations and streamlining of support functions increasing costs of pension obligations resulting from declining interest rates demand stagnation or decline which for certain factories could result in critical capacity underutilization.

INVESTOR RELATIONS: Michel GÉDÉON +33 1 73 23 85 31 [email protected] Julien CATEL +33 1 73 23 85 24 [email protected]

2 I 2016 Half Year results

● Net debt at 373 M€, reduced by 30% over the last 12 months ● Stronger balance sheet following 250 M€ bond issue ● Financial Flexibility reinforced

Limited Cash consumption

in line with expectations

● EBITDA up 22% at 203 M€ ● Operating margin at 135 M€, up to 5.9% of Sales at constant metal

price versus 4.0% in June 2015 ● 74 M€ contribution from Strategic Initiatives ● Group back to positive net result

Strategic Initiatives delivering

strong margin improvement

Key Take-aways

3 I

● Sales of 2,951 M€ ● 0.2% organic growth ● Subsea cables down -13% in line with expected projects phasing;

strong order intake in projects. Other activities up 2.3%

2016 Half Year results

Slight organic growth despite

unfavorable Project phasing

Half year 2016 highlights

Business review

Key Financials

Outlook

Appendix

Agenda

1

2

3

4

5

1 First half 2016 Highlights Arnaud POUPART-LAFARGE, CEO

37%

23%

28%

12%

Transmission, distribution & Operators Industry Distributors & Installers Others

Nexans, a global cable solution provider Well positioned on its four end-markets

6 I 2016 Half Year results

Sales by business segments

Energy and data infrastructures

Energy resources

Transport

Buildings

● Power transmission ● Power/data distribution ● Accessories

● Residential ● Commercial ● Data

● Mining ● O&G ● Renewables ● Power plants

● Aerospace ● Railways, city rail ● Automotive ● Shipbuilding

€3 bn Sales* in June 2016

1

End markets

HIGHLIGHTS

* Sales at actual metal prices

Nexans brings Energy to Life Energy transition and efficiency

7 I 2016 Half Year results

Reinforcing power grid and ensuring security of power supply

Two world records for Norway’s BKK grid connection: deepest and longest 420 kV XLPE submarine cable system

Reinforcing the grid in western Norway will allow to meet growing demand for electricity

1

HIGHLIGHTS

Nexans brings Energy to Life Energy transition and efficiency

8 I 2016 Half Year results

Connecting wind farms to the grid

Nexans cables to connect Beatrice Offshore Windfarm to the Scottish grid

Once fully operational, Beatrice may cover the energy needs of more than 450,000 British households

1

HIGHLIGHTS

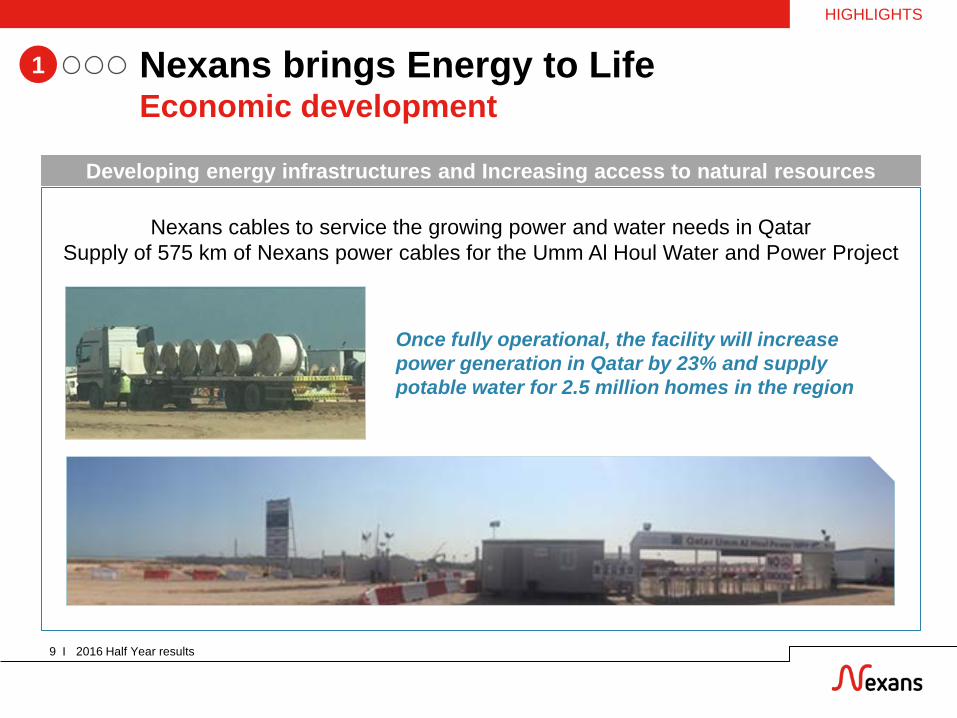

Nexans brings Energy to Life Economic development

9 I 2016 Half Year results

Developing energy infrastructures and Increasing access to natural resources

Nexans cables to service the growing power and water needs in Qatar Supply of 575 km of Nexans power cables for the Umm Al Houl Water and Power Project

1

HIGHLIGHTS

Once fully operational, the facility will increase power generation in Qatar by 23% and supply potable water for 2.5 million homes in the region

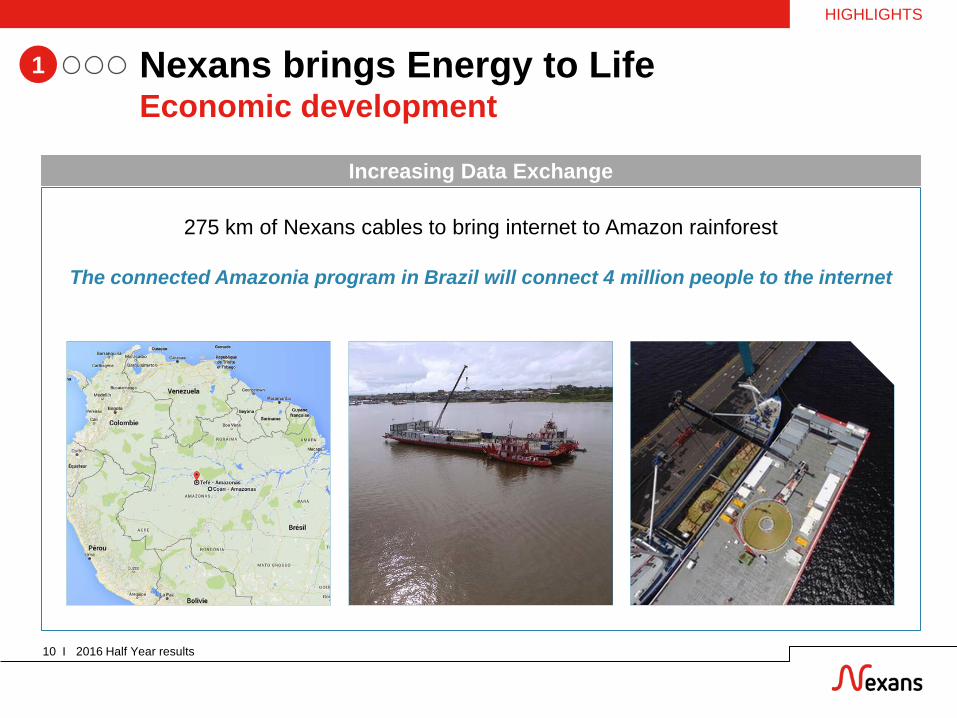

Nexans brings Energy to Life Economic development

10 I 2016 Half Year results

Increasing Data Exchange

275 km of Nexans cables to bring internet to Amazon rainforest

The connected Amazonia program in Brazil will connect 4 million people to the internet

1

HIGHLIGHTS

Nexans brings Energy to Life Economic development

11 I 2016 Half Year results

Supplying umbilicals for offshore Oil fields

Nexans umbilicals achieve global reach with new project in Australia

Nexans umbilical and accessories to develop the Greater Enfield project, offshore oil field located 60 km off the coast of Exmouth, Western Australia

1

HIGHLIGHTS

© Woodside

Nexans brings Energy to Life Innovation

12 I 2016 Half Year results

At the forefront of technology to meet customer needs

1

● Nexans drives the transition to higher voltage wind farm networks with its new range of 72.5 kV cable and power accessories

● Nexans continues to deploy EASYCALC™ cable sizing dematerialized tool

LANmark-OF ENSPACE ● Nexans new fibre system specifically designed for ultra high density

data centre applications

WINDLINK® ● Nexans new low voltage aluminum torsion-resistant loop cable solution for wind turbines

HIGHLIGHTS

2 Business Review Arnaud POUPART-LAFARGE, CEO

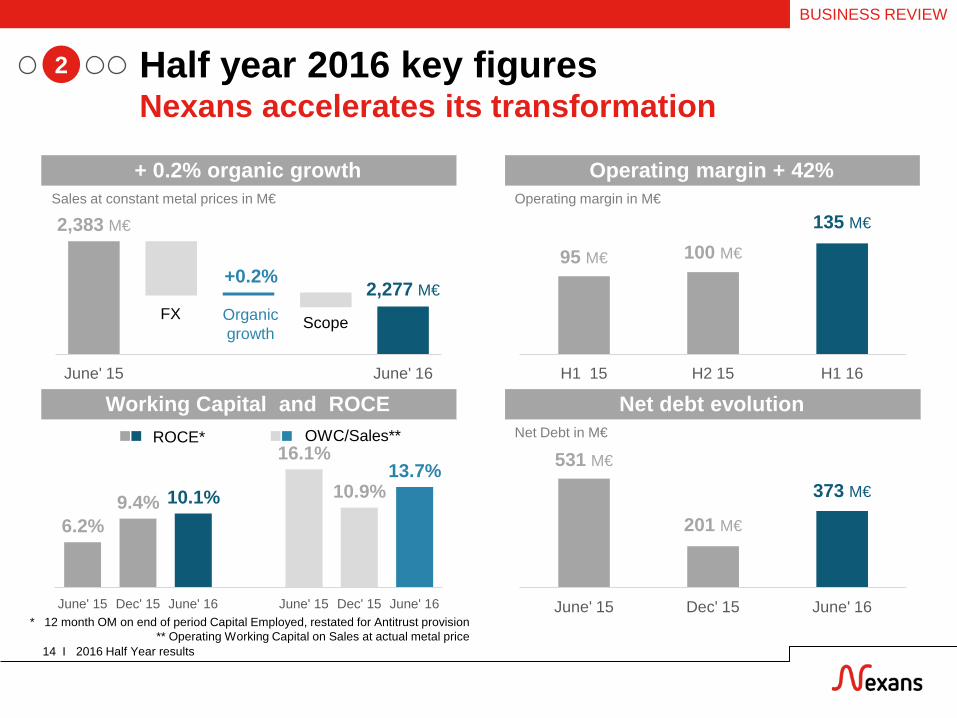

531 M€

201 M€

373 M€

June' 15 Dec' 15 June' 16

Sales at constant metal prices in M€

2,383 M€

2,277 M€

June' 15 June' 16

Net debt evolution

Half year 2016 key figures Nexans accelerates its transformation

2016 Half Year results 14 I

Working Capital and ROCE

+ 0.2% organic growth Operating margin + 42%

+0.2%

Organic growth

FX Scope

95 M€ 100 M€

135 M€

H1 15 H2 15 H1 16

Net Debt in M€

2

6.2% 9.4% 10.1%

16.1%

10.9% 13.7%

June' 15 Dec' 15 June' 16 June' 15 Dec' 15 June' 16 * 12 month OM on end of period Capital Employed, restated for Antitrust provision

** Operating Working Capital on Sales at actual metal price

Operating margin in M€

BUSINESS REVIEW

ROCE* OWC/Sales**

10%

18%

31%

13%

12%

9%

6%

Harnesses

High Voltage

Europe

NAM

APAC

MERA

SAM

Sales by geographies A contrasted business environment

2016 Half Year results 15 I

% of Standard Sales H1 2016 Organic Growth

3.8%

-6.1%

0.8%

2.3%

-10.7%

15.6%

12.5%

Harnesses

High Voltage

Europe

NAM

APAC

MERA

SAM

2

BUSINESS REVIEW

Distributors & Installers Margin improvement in all areas

2016 Half Year results 16 I

Business Update

Operating Margin : 52 M€

Margins

● Operating margin rate continues to progress as strategic initiatives and business mix contribute positively

BUILDING: Sales up 0.4% organically ● Positive momentum confirmed in MERA and SAM ● Signs of recovery in NAM and APAC ● Conditions remain difficult in Europe

LAN and CABLING SYSTEMS: +15.8% organic growth ● Strong momentum, in particular in the US and in China

577 559

580

H1' 15 H2' 15 H1' 16

-4.8% -0.5% +3.9%

Sales at constant metal: 580 M€

Sales

Organic growth

22 41 52

3.8%

7.4% 9.0%

H1' 15 H2' 15 H1' 16

Operating margin

OM Rate

37 27

14 14 9

-5.1 %

8.9% 9.5% 13.5% 4.8%

Europe NAM APAC MERA SAM

2

BUSINESS REVIEW

Organic growth % of Sales at constant metal

3%

-26% -14% 10%

-17% -28%

22% -8% 15%

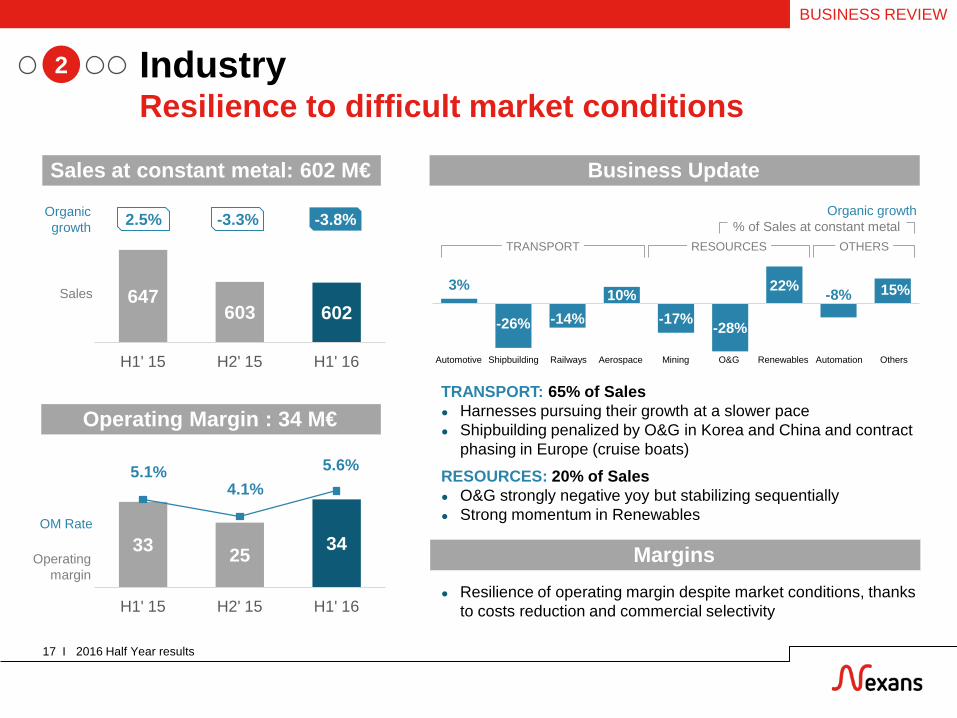

Industry Resilience to difficult market conditions

2016 Half Year results 17 I

Business Update

Operating Margin : 34 M€ TRANSPORT: 65% of Sales ● Harnesses pursuing their growth at a slower pace ● Shipbuilding penalized by O&G in Korea and China and contract

phasing in Europe (cruise boats)

RESOURCES: 20% of Sales ● O&G strongly negative yoy but stabilizing sequentially ● Strong momentum in Renewables

647 603 602

H1' 15 H2' 15 H1' 16

Sales at constant metal: 602 M€

Sales

33 25 34

5.1% 4.1%

5.6%

H1' 15 H2' 15 H1' 16

Operating margin

OM Rate

Organic growth % of Sales at constant metal

Margins ● Resilience of operating margin despite market conditions, thanks

to costs reduction and commercial selectivity

Automotive Shipbuilding Railways Aerospace Mining O&G Renewables Automation Others

TRANSPORT RESOURCES OTHERS

2

2.5% -3.3% -3.8% Organic growth

BUSINESS REVIEW

2000 2015

Transmission Distribution & Operators Positive momentum masked by Project phasing

2016 Half Year results 18 I

Market Drivers

Operating Margin : 63 M€

● Extension of the Transmission network to cope with Need for an interconnected European grid Development of Renewable Energy Sources

● Upgrade of Distribution networks Replacement of aging grid Development of Power consumption

1,012 923 945

H1' 15 H2' 15 H1' 16

+1% -3.5% -0.7%

Sales at constant metal: 945 M€

Sales

Organic growth

54 54 63

5.4% 5.8% 6.7%

H1' 15 H2' 15 H1' 16

Operating margin

OM Rate

POWER DEMAND WIND POWER

2

0

100

200

300

1990 2000 2010 2020 2030

Historical Projected

Power sector CO2 emissions

Electricity demand

433 GW

17

Source IEA/ WEO 2015 Cumulative global Wind Power Capacity Source GWEC

BUSINESS REVIEW

TD&O / Transmission Increasing order backlog

2016 Half Year results 19 I

Land High Voltage Order backlog

● Solid activity growth thanks to the order intake of 2015 ● As expected, Operating margin impacted negatively by

sub-optimal utilization of the US plant

Submarine Hybrid cables

Land

-6% -24% 17%

Organic Growth : -6.5%

Organic growth

Sub-sea

● Activity in Submarine High Voltage back to normal in Q2 2016 after low first quarter due to project phasing

● Hybrid Cables suffering from upstream O&G trough ● Operating margin negatively impacted by 1st quarter

maintenance and business mix year over year ● Order backlog keeps growing ; strong order intake in

umbilicals

2

June' 15 Dec' 15 June' 16 Submarine Hybrid Land

BUSINESS REVIEW

Years of activity

1.9x 2.1x 2.3x

Sales

Order Backlog

TD&O / Utilities and Operators Stronger Utility call-offs in first half

2016 Half Year results 20 I

UTILITIES: +4.2% organic growth ● Recovery in Europe ● Strong momentum confirmed in MERA .

SAM up 21% thanks to OHL projects in Brazil in particular

OPERATORS: down -2.4% organically ● Good level of activity in Europe after a slow start in Q1 ● Difficult market conditions in all other areas

Margins

● Operating margin rate doubled thanks to the recovery of volumes and the success of industrial and commercial efficiency programs

Operating Margin

H1' 15 H2' 15 H1' 16

-4.2% -2.9% +3.2%

Organic growth : +3.2%

Sales

Organic growth

H1' 15 H2' 15 H1' 16

Operating margin

OM Rate

58

13 12 12 6 1.6 %

22.8%

-12.7%

18.2%

-4.2%

Europe MERA APAC SAM NAM

Business Update

Organic growth % of Sales at constant metal

2

BUSINESS REVIEW

Strategic initiatives delivered as expected to overcome volume & price pressure effects

2016 Half Year results 21 I

2

95

135

(5)

74

(29)

June' 2015 June' 2016

FX & scope STRATEGIC INITIATIVES

PRICE COST SQUEEZE

Operating reserves & others*

Operating margin evolution in M€

BUSINESS REVIEW

(*) Note: Including +2 M€ impact from 2015 Impairments

Strategic Initiatives progressing as planned

2016 Half Year results 22 I

2

Fixed Cost Reduction

11 M€

● 2015 European plan starting to be implemented

● OPEX and other plan progressing as planned

Variable Cost

Reduction

25 M€

● Purchasing savings continue to deliver as planned

● Industrial saving plans back on track after 2015 difficulties related to negative volumes have been overcome

Market Leadership

38 M€

● LAN/Cabling Systems and Utilities

● Extended selective portfolio approach

BUSINESS REVIEW

Profitable Growth

Product Customer Optimization,

Service development

2013 European plan

2015 European plan

OPEX and other plans

Purchasing Saving

Industrial Efficiency

3 Key financials Nicolas BADRÉ, CFO

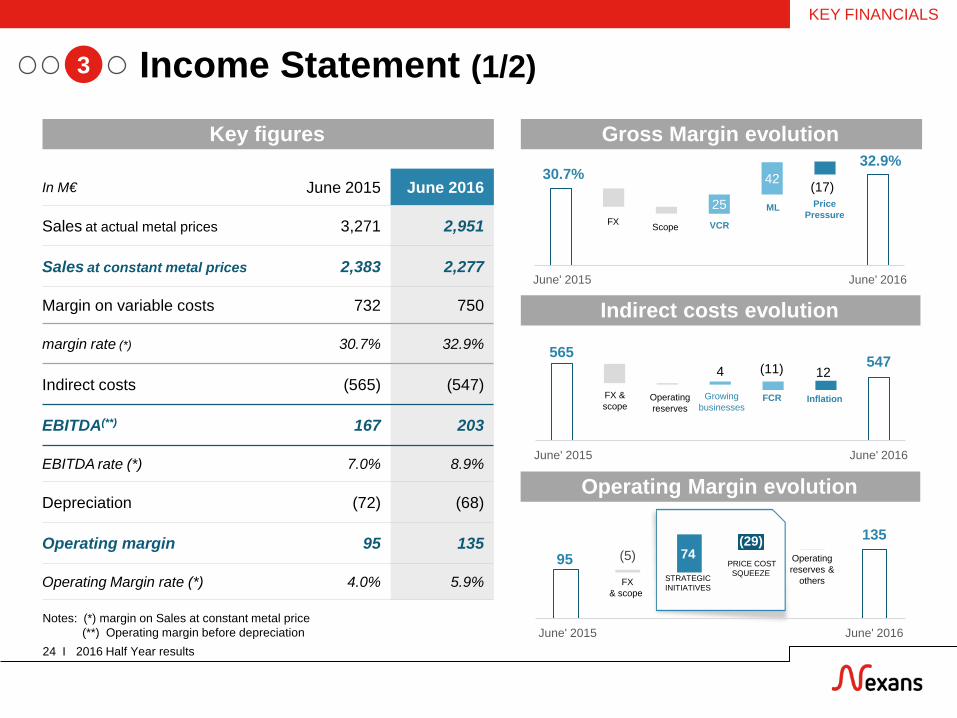

Income Statement (1/2)

2016 Half Year results 24 I

In M€ June 2015 June 2016

Sales at actual metal prices 3,271 2,951

Sales at constant metal prices 2,383 2,277

Margin on variable costs 732 750

margin rate (*) 30.7% 32.9%

Indirect costs (565) (547)

EBITDA(**) 167 203

EBITDA rate (*) 7.0% 8.9%

Depreciation (72) (68)

Operating margin 95 135

Operating Margin rate (*) 4.0% 5.9%

Indirect costs evolution

Operating Margin evolution

3

Key figures Gross Margin evolution

Notes: (*) margin on Sales at constant metal price (**) Operating margin before depreciation

95 135

(5) 74 (29)

June' 2015 June' 2016

FX & scope

STRATEGIC INITIATIVES

PRICE COST SQUEEZE

Operating reserves &

others

565 547 4 (11) 12

June' 2015 June' 2016

30.7% 32.9%

25

42 (17)

June' 2015 June' 2016

FX Scope

ML

VCR

Price Pressure

FX & scope

Operating reserves

FCR Growing businesses

Inflation

KEY FINANCIALS

Income Statement (2/2)

2016 Half Year results 25 I

From Operating Margin to Operating Income

In M€ June 2015 June 2016

Operating margin 95 135

Restructuring (98) (13)

Others (1) (32)

Operating income (4) 90

Financial charge (45) (44)

Income before tax (49) 46

Income tax (10) (17)

Net income from operations (59) 29

Net income Group share (58) 30

In M€ June’15 June’16

Cost of debt (38) (30)

Net foreign exchange gain loss 1 (6)

Interest on Pension (5) (5)

Others (3) (3)

Financial charge (45) (44)

In M€ June’15 June’16

Core exposure Impact (1) (25)

Restructuring (98) (13)

Net asset Impairment - -

Provision for Anti-trust investigation 1 (6)

Change in fair value of metal derivatives - (2)

Others (1) 1

Adjustments to operating margin (99) (45)

3

Key figures

Financial charge

KEY FINANCIALS

201

373

(123)

60 40

230 (16) (19)

Dec' 2015

June' 2016

531

373

(235) 161

93 (141)

(48) 12

June'15 June' 2016

Focus on cash management

2016 Half Year results 26 I

OWC 6 month evolution – cash impact

OCF

FX & Other

Non Operating

WC

3

Net Debt last 6 month evolution in M€

OWC on Sales - excluding Projects

KEY FINANCIALS

Net Debt last 12 month evolution in M€

OCF

Restructuring cash-out

FX & Other Non

Operating WC

CAPEX

Operating Working Capital

CAPEX

CAPEX

Operating Working Capital

20% 18% 15%

June'14 June'15 June'16

Operating Working

Capital

OWC/Sales

Restructuring cash-out

Evolution of Operating Working Capital excluding Project activities

Submarine HV Projects

Land HV

Down-payments

Cables activities

Balance Sheet strength

2016 Half Year results 27 I

3

Net debt and gearing ratios

Leverage ratios

Balance Sheet Interest Charge over EBITDA 28% 27% 24%

15%

Dec'13 Dec'14 Dec'15 June'16

21% 32%

16% 29%

Dec'13 Dec'14 Dec'15 June'16

Net Debt over Equity < 30%

1.1x 1.6x

0.6x

1.0x

Dec'13 Dec'14 Dec'15 June'16

Net Debt over LTM EBITDA = 1 year

Interest/ EBITDA

Interest charge

Net debt

Gearing

Net debt

Leverage

KEY FINANCIALS

In M€ Dec’ 2015

June 2016

Long term fixed assets

Of which goodwill 1,643

250 1,614

247

Deferred Tax 192 189

Non-current Assets 1,835 1,803

Working Capital 405 675

Total to finance 2,240 2,478

Net financial debt 201 373

Reserves Of which: - restructuring - pension & jubilee

690 128 453

700 105 481

Deferred tax liabilities 84 87

Derivative liability non current 38 17

Shareholders’ equity and minority interests 1,227 1,301

Total financing 2,240 2,478

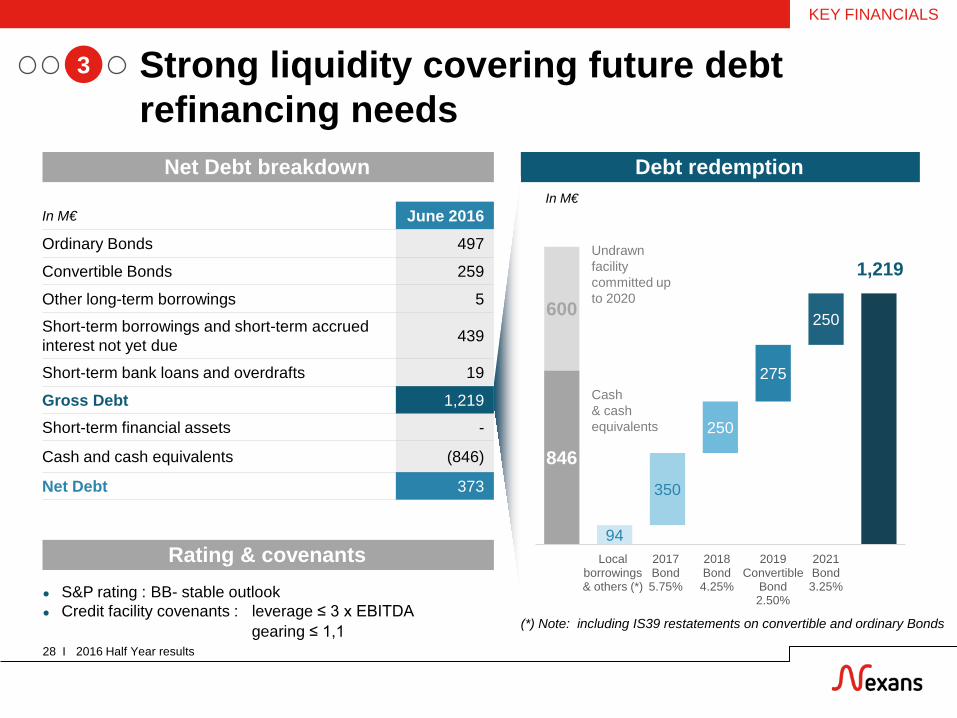

In M€ June 2016 Ordinary Bonds 497

Convertible Bonds 259

Other long-term borrowings 5

Short-term borrowings and short-term accrued interest not yet due 439

Short-term bank loans and overdrafts 19

Gross Debt 1,219

Short-term financial assets -

Cash and cash equivalents (846)

Net Debt 373

Net Debt breakdown Debt redemption

846

94

1,219

600

350

250

275

250

Local borrowings & others (*)

2017 Bond 5.75%

2018 Bond 4.25%

2019 Convertible

Bond 2.50%

2021 Bond 3.25%

Strong liquidity covering future debt refinancing needs

2016 Half Year results 28 I

● S&P rating : BB- stable outlook ● Credit facility covenants : leverage ≤ 3 x EBITDA

gearing ≤ 1,1

3

Rating & covenants

(*) Note: including IS39 restatements on convertible and ordinary Bonds

Cash & cash equivalents

Undrawn facility committed up to 2020

KEY FINANCIALS

In M€

4 Outlook Arnaud Poupart-Lafarge, CEO

Priorities ahead

● Keep momentum on strategic initiatives, in uncertain environment

● Capture profitable growth through continued Product Customer Optimization

● Maintain focus on cash control

● Explore available options for underperforming businesses

30 I 2016 Half Year results

4

OUTLOOK

Confidence in delivering in due time the full potential from strategic initiatives

Appendices

Sales and profitability by segment

2016 Half Year results 32 I

June 2015 June 2016

In M€ Sales OM OM % Sales OM OM %

Transmission, Distribution & Operators 1,012 54 5.4% 945 63 6.7%

Industry 647 33 5.1% 602 34 5.6%

Distributors & Installers 577 22 3.8% 580 52 9.0%

Other 147 (14) n/a 150 (14) n/a

TOTAL GROUP 2,383 95 4.0% 2,277 135 5.9%

APPENDICES

Impact of foreign exchange and consolidation scope

2016 Half Year results 33 I

Sales at constant metal prices, in M€ June 2015 FX Organic

growth Scope June 2016

Transmission, Distribution & Operators 1,012 (47) (7) (14) 945

Industry 647 (12) (24) (8) 602

Distributors & Installers 577 (23) 22 4 580

Other 147 (6) 15 (6) 150

TOTAL GROUP 2,383 (88) 6 (24) 2,277

APPENDICES

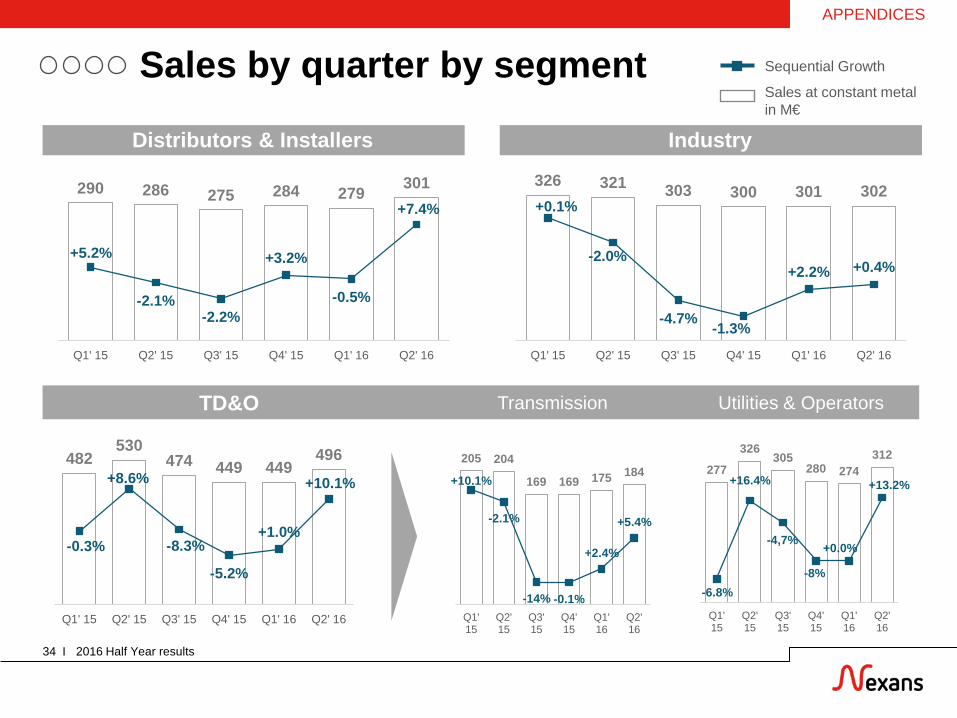

Distributors & Installers Industry

Sales by quarter by segment

TD&O Utilities & Operators Transmission

2016 Half Year results 34 I

Sales at constant metal in M€

Sequential Growth

290 286 275 284 279 301

+5.2%

-2.1% -2.2%

+3.2%

-0.5%

+7.4%

Q1' 15 Q2' 15 Q3' 15 Q4' 15 Q1' 16 Q2' 16

205 204

169 169 175 184 +10.1%

-2.1%

-14% -0.1%

+2.4%

+5.4%

Q1' 15

Q2' 15

Q3' 15

Q4' 15

Q1' 16

Q2' 16

326 321 303 300 301 302 +0.1%

-2.0%

-4.7% -1.3%

+2.2% +0.4%

Q1' 15 Q2' 15 Q3' 15 Q4' 15 Q1' 16 Q2' 16

482 530

474 449 449 496

-0.3%

+8.6%

-8.3%

-5.2%

+1.0%

+10.1%

Q1' 15 Q2' 15 Q3' 15 Q4' 15 Q1' 16 Q2' 16

277

326 305

280 274 312

-6.8%

+16.4%

-4,7%

-8%

+0.0%

+13.2%

Q1' 15

Q2' 15

Q3' 15

Q4' 15

Q1' 16

Q2' 16

APPENDICES

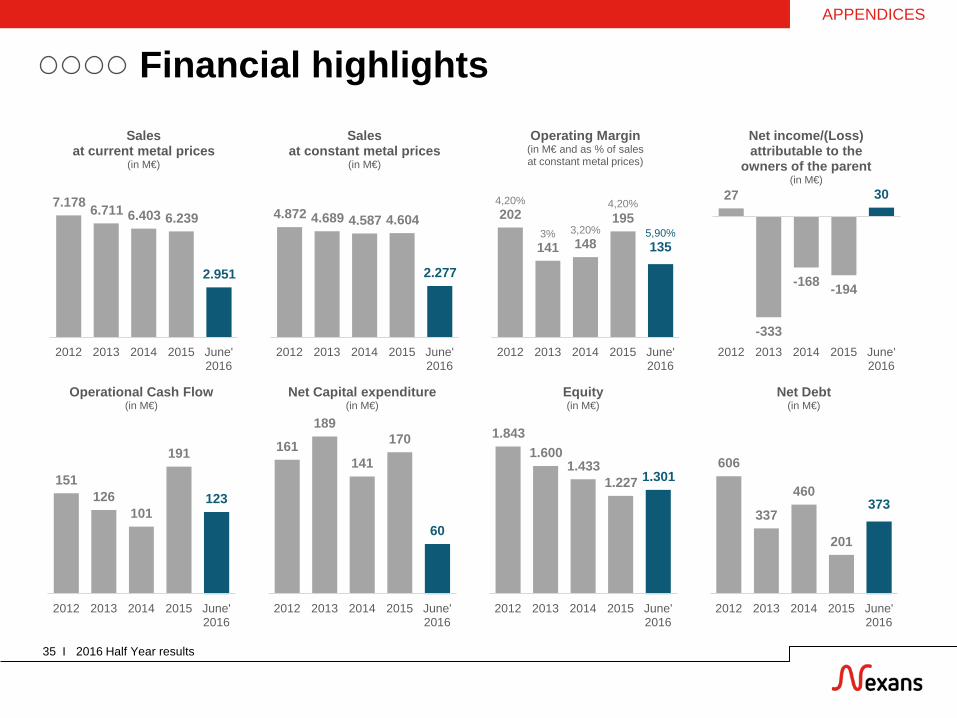

Financial highlights

2016 Half Year results 35 I

7.178 6.711 6.403 6.239

2.951

2012 2013 2014 2015 June' 2016

Sales at current metal prices

(in M€)

4.872 4.689 4.587 4.604

2.277

2012 2013 2014 2015 June' 2016

Sales at constant metal prices

(in M€)

4,20%202

3% 141

3,20% 148

4,20% 195

5,90%135

2012 2013 2014 2015 June' 2016

Operating Margin (in M€ and as % of sales at constant metal prices)

27

-333

-168 -194

30

2012 2013 2014 2015 June' 2016

Net income/(Loss) attributable to the

owners of the parent (in M€)

151 126

101

191

123

2012 2013 2014 2015 June' 2016

Operational Cash Flow (in M€)

161

189

141

170

60

2012 2013 2014 2015 June' 2016

Net Capital expenditure (in M€)

1.843 1.600

1.433 1.227 1.301

2012 2013 2014 2015 June' 2016

Equity (in M€)

606

337

460

201

373

2012 2013 2014 2015 June' 2016

Net Debt (in M€)

APPENDICES