2016 Economic and Housing Real Estate Forecast-California Realtors Association

76

2016 ECONOMIC AND HOUSING MARKET FORECAST April 22, 2016 CA Community College Real Estate Education Center Oscar Wei, Senior Economist of C.A.R.

-

Upload

realestateeducation -

Category

Real Estate

-

view

437 -

download

2

Transcript of 2016 Economic and Housing Real Estate Forecast-California Realtors Association

2016 ECONOMIC AND HOUSING MARKET

FORECASTApril 22, 2016

CA Community College Real Estate Education Center

Oscar Wei, Senior Economist of C.A.R.

OVERVIEW

• Economic Outlook

• California Housing Market Outlook

• Regional Housing Market Outlook

• 2016 Forecast

ECONOMIC OUTLOOK

MACRO ECONOMY SUMMARY

1.4%

GDP 2015-Q4

1.9%

Job Growth2016-02

5.0%

Unemployment2016-03

2.2%

Consumption2015-Q4

-4%

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

2005

2007

2009

2011

2013

2015

Q2-1

1

Q4-1

1

Q2-1

2

Q4-1

2

Q2-1

3

Q4-1

3

Q2-1

4

Q4-1

4

Q2-1

5

Q4-1

5

US GDP: AT RISK FROM WEAK GLOBAL GROWTH?

2015: 2.4%; 2015 Q4: 1.4%; 2016 (F): 2.7%

ANNUAL PERCENT CHANGE, CHAIN-TYPE (2005) $

ANNUALLY QUARTERLY

2009 Largest Annual Drop since 1938 (-3.4%)

SERIES: GDPSOURCE: US Dept. of Commerce, Bureau of Economic Analysis

PROGRESS CONTINUES, UNIMPRESSIVELY

10,000

11,000

12,000

13,000

14,000

15,000

16,000

17,000

18,000

19,000Q

1-0

0

Q1-0

1

Q1-0

2

Q1-0

3

Q1-0

4

Q1-0

5

Q1-0

6

Q1-0

7

Q1-0

8

Q1-0

9

Q1-1

0

Q1-1

1

Q1-1

2

Q1-1

3

Q1-1

4

Q1-1

5

$ B

illio

ns

Actual Trend

SERIES: U.S. Real Gross Domestic Product (GDP)

SOURCE: U.S. Bureau of Economic Analysis

24 Consecutive quarters of yty growth, but still below long-run trend

UNEMPLOYMENT RATES AT 8-YEAR LOWS

US 5.0% (Mar 2016), CA 5.4% (Mar 2016)

0%

2%

4%

6%

8%

10%

12%

14%

Jan

-05

Jul-

05

Jan

-06

Jul-

06

Jan

-07

Jul-

07

Jan

-08

Jul-

08

Jan

-09

Jul-

09

Jan

-10

Jul-

10

Jan

-11

Jul-

11

Jan

-12

Jul-

12

Jan

-13

Jul-

13

Jan

-14

Jul-

14

Jan

-15

Jul-

15

Jan

-16

CA US

SERIES: Unemployment Rate SOURCE: US Bureau of Labor Statistics, CA Employment Development Division

EMPLOYMENT GROWTH, CALIFORNIA VS. U.S.

2.6%

2.0%

-8

-6

-4

-2

0

2

4

6

Jan

-05

Jul-

05

Jan

-06

Jul-

06

Jan

-07

Jul-

07

Jan

-08

Jul-

08

Jan

-09

Jul-

09

Jan

-10

Jul-

10

Jan

-11

Jul-

11

Jan

-12

Jul-

12

Jan

-13

Jul-

13

Jan

-14

Jul-

14

Jan

-15

Jul-

15

Jan

-16

California USANNUAL PERCENT CHANGE

SERIES: Total Nonfarm EmploymentSOURCE: US Bureau of Labor Statistics, CA Employment Development Division

JOB TRENDS BY CALIFORNIA METRO AREA

1.0%

1.4%

2.0%

2.2%

2.3%

2.4%

2.6%

2.9%

3.1%

3.2%

3.3%

3.5%

3.7%

0.0% 0.5% 1.0% 1.5% 2.0% 2.5% 3.0% 3.5% 4.0%

Ventura

Bakersfield

Los Angeles

San Luis Obispo

Oakland

Sacramento

San Diego

Orange County

Fresno MSA

Modesto

Inland Empire

San Jose/Santa Clara

Stockton MSA

SERIES: Total Nonfarm Employment SOURCE: CA Employment Development Division

ANNUAL PERCENT CHANGE

March 2016: CA +2.6%, +420,800

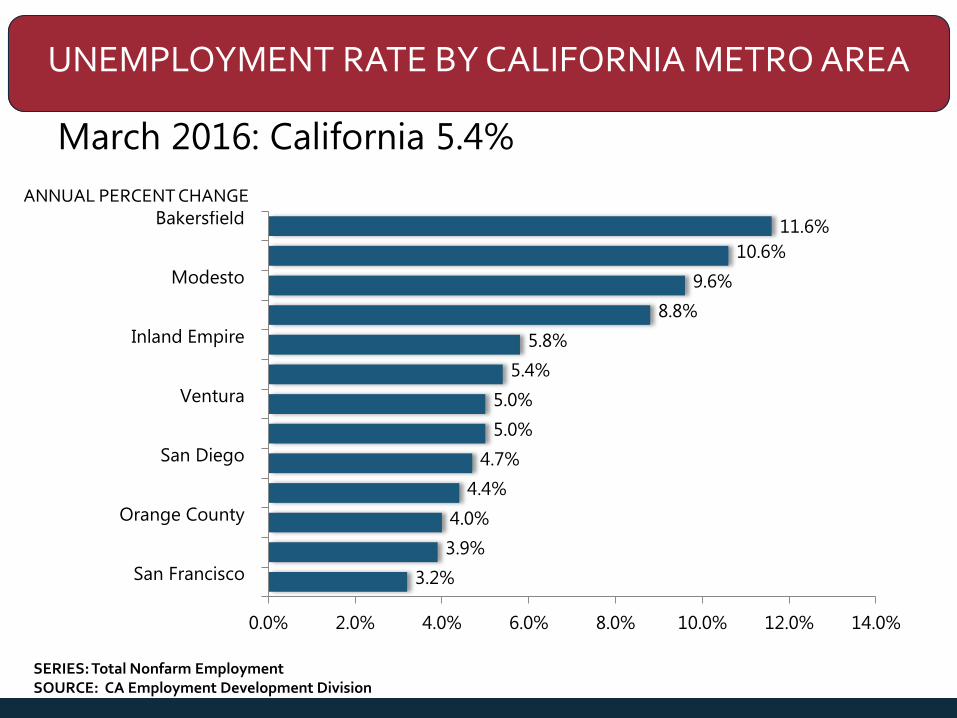

UNEMPLOYMENT RATE BY CALIFORNIA METRO AREA

3.2%

3.9%

4.0%

4.4%

4.7%

5.0%

5.0%

5.4%

5.8%

8.8%

9.6%

10.6%

11.6%

0.0% 2.0% 4.0% 6.0% 8.0% 10.0% 12.0% 14.0%

San Francisco

Orange County

San Diego

Ventura

Inland Empire

Modesto

Bakersfield

SERIES: Total Nonfarm Employment SOURCE: CA Employment Development Division

ANNUAL PERCENT CHANGE

March 2016: California 5.4%

OIL’S DRAG COMING TO CLOSE? MAYBE…

Dollars per Barrel

$0

$20

$40

$60

$80

$100

$120

$140

$160

Mar-

06

No

v-06

Jul-

07

Mar-

08

No

v-08

Jul-

09

Mar-

10

No

v-10

Jul-

11

Mar-

12

No

v-12

Jul-

13

Mar-

14

No

v-14

Jul-

15

Mar-

16

SERIES: Crude Oil Prices: West Texas IntermediateSOURCE: U.S. Energy Information Administration

3rd Week of March: $38.32; 5th consecutive week of growth

74% Drop

CONSUMER CONFIDENCE INDEX

March 2016: 96.2

0

20

40

60

80

100

120

Jan

-05

Jul-

05

Jan

-06

Jul-

06

Jan

-07

Jul-

07

Jan

-08

Jul-

08

Jan

-09

Jul-

09

Jan

-10

Jul-

10

Jan

-11

Jul-

11

Jan

-12

Jul-

12

Jan

-13

Jul-

13

Jan

-14

Jul-

14

Jan

-15

Jul-

15

Jan

-16

INDEX, 100=1985

SERIES: Consumer ConfidenceSOURCE: The Conference Board

MORTGAGE RATES LOWER NOW THAN 2015

January 2009 – March 2016

0%

1%

2%

3%

4%

5%

6%

2009/0

1

2009/0

7

2010/0

1

2010/0

7

2011/0

1

2011/0

7

2012/0

1

2012/0

7

2013/0

1

2013/0

7

2014/0

1

2014/0

7

2015/0

1

2015/0

7

2016/0

1

11.2

6.1

5

01.0

7.1

6

02.1

8.1

6

FRM

MONTHLY WEEKLY

SERIES: 30Yr FRM, 5Yr ARMSOURCE: Freddie Mac

WHERE ARE WE HEADED?

- Fed takes a more dovish tone, leave interest rates unchanged, will gradually increase rates in 2016 and 2017. Action will be “data determined”

- Risk of rates increasing too fast: bringing economic growth to a halt

- Risk of rates increasing too slow: zero leverage when next downturn hits

U.S. ECONOMIC OUTLOOK

2010 2011 2012 2013 2014 2015 2016f

US GDP 2.4% 1.8% 2.3% 2.2% 2.4% 2.4% 2.7%

Nonfarm Job Growth -0.7% 1.2% 1.7% 1.7% 1.9% 2.1% 1.8%

Unemployment 9.6% 8.9% 8.1% 7.4% 6.2% 5.3% 5.0%

CPI 1.6% 3.1% 2.1% 1.5% 1.6% 0.1% 2.1%

Real Disposable

Income, % Change 1.0% 2.5% 3.1% -1.4% 2.7% 3.5% 2.7%

30-Yr FRM 4.7% 4.5% 3.7% 4.0% 4.2% 3.9% 4.5%

SERIES: U.S. Economic OutlookSOURCE: CALIFORNIA ASSOCIATION OF REALTORS®

CALIFORNIA ECONOMIC OUTLOOK

2010 2011 2012 2013 2014 2015 2016f

Nonfarm Job Growth -1.1% 1.1% 2.4% 3.2% 3.1% 3.0% 2.3%

Unemployment Rate 12.3% 11.8% 10.4% 8.9% 7.5% 6.2% 5.5%

Population Growth 0.7% 0.7% 0.7% 0.9% 0.9% 0.9% 0.9%

Real Disposable

Income, % Change 0.9% 3.4% 4.7% 0.2% 3.0% 4.3% 4.5%

SERIES: CA Economic OutlookSOURCE: CALIFORNIA ASSOCIATION OF REALTORS®

CALIFORNIA HOUSING MARKET OUTLOOK

SALES OF EXISTING DETACHED HOMES

California, Mar. 2016 Sales: 415,220 Units, +6.9% YTD, +5.7% YTY

-

100,000

200,000

300,000

400,000

500,000

600,000

700,000

Jan

-05

Sep

-05

May-

06

Jan

-07

Sep

-07

May-

08

Jan

-09

Sep

-09

May-

10

Jan

-11

Sep

-11

May-

12

Jan

-13

Sep

-13

May-

14

Jan

-15

Sep

-15

*Sales are seasonally adjusted and annualized SERIES: Sales of Existing Single Family HomesSOURCE: CALIFORNIA ASSOCIATION OF REALTORS®

Mar16: 415,220

Mar-15: 392,660

HOUSEHOLD FORMATION REBOUNDING

SERIES: Household FormationSOURCE: U.S. Census Bureau, Housing Vacancy Survey

1.5

1.9

1.2

0.60.4

0.6 0.6 0.6

0.9

0.7

1.0

1.3

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Annual Household Growth Millions

MEDIAN PRICE OF EXISTING DETACHED HOMES

California, Mar. 2016: $483,280, +8.9% MTM, +4.0% YTY

$-

$100,000

$200,000

$300,000

$400,000

$500,000

$600,000

$700,000

Jan

-05

Sep

-05

May-

06

Jan

-07

Sep

-07

May-

08

Jan

-09

Sep

-09

May-

10

Jan

-11

Sep

-11

May-

12

Jan

-13

Sep

-13

May-

14

Jan

-15

Sep

-15

P: May-07$594,530

T: Feb-09$245,230

-59% frompeak

SERIES: Median Price of Existing Single Family HomesSOURCE: CALIFORNIA ASSOCIATION OF REALTORS®

Mar-16: $483,280

Mar-15: $464,640

INVENTORY CONTINUED TO DECLINE FROM LAST YEAR

Mar. 2015: 3.8 Months; Mar. 2016: 3.6 Months

Note: “Unsold Inventory Index” represents the number of months it would take to sell the remaining inventory for the month in question. The remaining inventory for the month is defined as the number of properties that were “Active”, “Pending”, and “Contingent” (when available) and divide the sum by the number of “Sold” properties for the month in question.

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

Jan

-05

Sep

-05

May-

06

Jan

-07

Sep

-07

May-

08

Jan

-09

Sep

-09

May-

10

Jan

-11

Sep

-11

May-

12

Jan

-13

Sep

-13

May-

14

Jan

-15

Sep

-15

SERIES: Unsold Inventory Index of Existing Single Family HomesSOURCE: CALIFORNIA ASSOCIATION OF REALTORS®

INVENTORY DROPPED SIGNIFICANTLY IN THE BAY AREA SINCE 2009 BUT REMAINED TIGHT

Note: “Unsold Inventory Index” represents the number of months it would take to sell the remaining inventory for the month in question. The remaining inventory for the month is defined as the number of properties that were “Active”, “Pending”, and “Contingent” (when available) and divide the sum by the number of “Sold” properties for the month in question.

2.6

3.33.3

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

Jan

-09

Jul-

09

Jan

-10

Jul-

10

Jan

-11

Jul-

11

Jan

-12

Jul-

12

Jan

-13

Jul-

13

Jan

-14

Jul-

14

Jan

-15

Jul-

15

Jan

-16

Bay Area So CA Central Valley

SERIES: Unsold Inventory Index of Existing Single Family HomesSOURCE: CALIFORNIA ASSOCIATION OF REALTORS®

INVENTORY IMPROVED IN THE BAY AREA, BUT DROPPED IN SO CA AND CENTRAL VALLEY

-8%

1%

7%

3%

-3%

-9%

-20%

-10%

0%

10%

San Francisco Bay Area Southern California Central Valley

Sales Active ListingsYear-to-Year % Chg

SOURCE: CALIFORNIA ASSOCIATION OF REALTORS®

Mar. 2016

WHERE IS THE INVENTORY?

– Affordability challenge for repeat buyers• Low rate on current mortgage • Low property taxes• Concerned with capital gains• Why list when there is nowhere to go I can

afford?• Could not qualify for a mortgage today

– New construction recovering but LOW– Demographics: Trade-up buyer pool is smaller– Measurement error? Off- MLS (aka “pocket’)

listings not being counted in listing stats

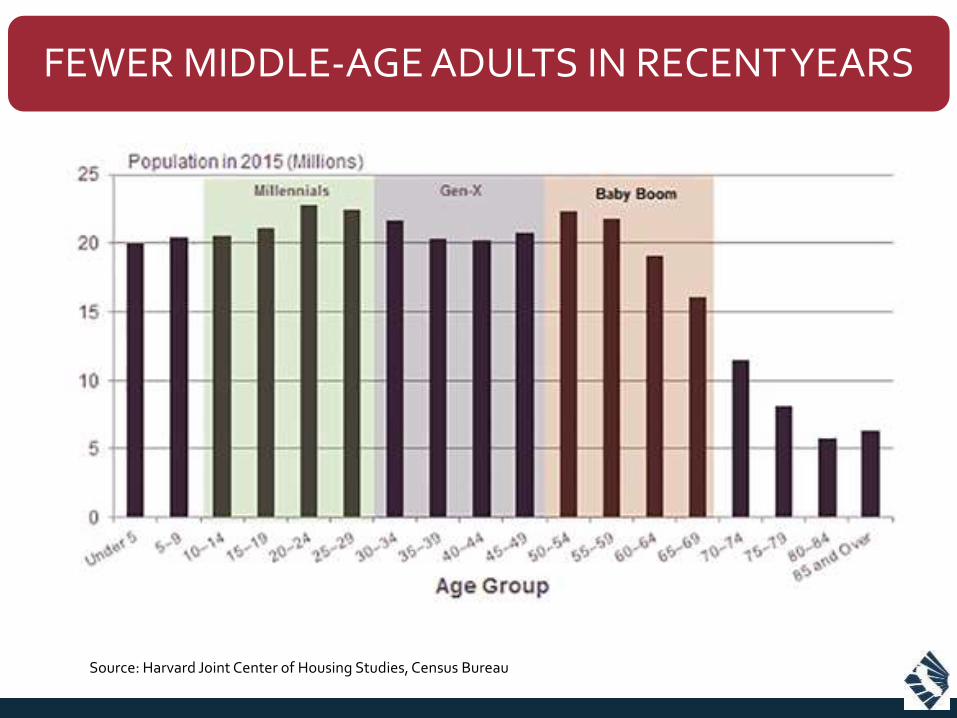

FEWER MIDDLE-AGE ADULTS IN RECENT YEARS

Source: Harvard Joint Center of Housing Studies, Census Bureau

DROP IN HOMEOWNERSHIP

Source: Harvard Joint Center of Housing Studies, Census Bureau

DECLINE IN # OF TRADE UP BUYERS DUE TO POPULATION LOSS & DROP IN HOMEOWNERSHIP RATE

Source: Harvard Joint Center of Housing Studies, Census Bureau

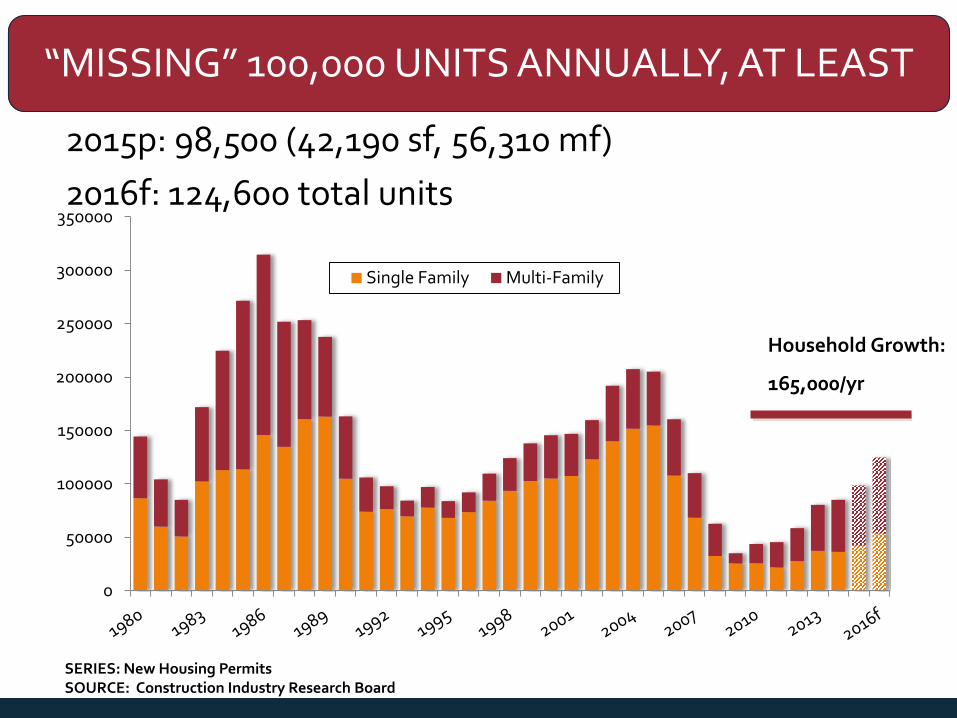

“MISSING” 100,000 UNITS ANNUALLY, AT LEAST

2015p: 98,500 (42,190 sf, 56,310 mf)

2016f: 124,600 total units

SERIES: New Housing PermitsSOURCE: Construction Industry Research Board

0

50000

100000

150000

200000

250000

300000

350000

Single Family Multi-Family

Household Growth:

165,000/yr

HOUSING AFFORDABILITY PEAKED Q1 2012PRICES V. LOW RATES AND INCOME GROWTH

California vs. U.S. – 1984-2015% OF HOUSEHOLDS THAT CAN BUY A MEDIAN-PRICED HOME

SERIES: Housing Affordability Index of Traditional BuyersSOURCE: CALIFORNIA ASSOCIATION OF REALTORS®

30%

58%

0%

10%

20%

30%

40%

50%

60%

70%

80% CA USAnnual Quarterly

6158

55 54 5349 48

46 45 4440 39 38 37

3027 26 26 26 25 25

23 22 21 21 21 2017

1411

0

10

20

30

40

50

60

70

HOUSING AFFORDABILITY IN CA: BY COUNTY

SERIES: Housing Affordability IndexSOURCE: CALIFORNIA ASSOCIATION OF REALTORS®

2015-Q4: % able to purchase median priced home

$27,010

$45,340

$69,990 $71,630

$87,520 $89,250

$98,400

$119,970

$96,642

$0

$20,000

$40,000

$60,000

$80,000

$100,000

$120,000

RetailSalespersons

Chefs andHead Cooks

ElementarySchool

Teachers

Firefighters Police andSherriff's

PatrolOfficers

ComputerProgrammers

RegisteredNurses

SoftwareDevelopers

(Applications)

Min. IncRequired toBuy a Med.

Home

HOW WAGES MEASURED AGAINST INCOME REQUIRED TO BUY A HOME

SOURCE: Bureau of Labor Statistics, C.A.R.

2014 Annual Mean Wage

California

SHARE OF FIRST-TIME BUYERS REMAINS BELOW LONG-RUN AVERAGE

29.5%

0%

10%

20%

30%

40%

50%

% First-Time Home Buyers Long Run Average

Long Run Average = 38%

SERIES: 2015 Housing Market SurveySOURCE: CALIFORNIA ASSOCIATION OF REALTORS®

THE SHARE OF INTERNATIONAL BUYERS DROPPED TO THE LOWEST LEVEL IN 8 YEARS

4%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

2008 2009 2010 2011 2012 2013 2014 2015

Q. Was the buyer an international buyer – a person who was a citizen of another country who wished to purchase residential real estate in the U.S.?

SERIES: 2015 Housing Market SurveySOURCE: CALIFORNIA ASSOCIATION OF REALTORS®

ESTIMATE OF SALES BY COUNTRY

SERIES: 2015 Profile of International Home Buying ActivitySOURCE: NATIONAL ASSOCIATION OF REALTORS®

ESTIMATE OF SALES TO INTERNATIONAL CLIENTS(IN BILLION DOLLARS)

SERIES: 2015 Profile of International Home Buying ActivitySOURCE: NATIONAL ASSOCIATION OF REALTORS®

4 STATES ACCOUNTED FOR ½ OF INTERNATIONAL SALES

SERIES: 2015 Profile of International Home Buying ActivitySOURCE: NATIONAL ASSOCIATION OF REALTORS®

COUNTRY OF INTERNATIONAL BUYER

• China (43%)

• Mexico (8%)

• South Korea (8%)

SERIES: 2015 Housing Market SurveySOURCE: CALIFORNIA ASSOCIATION OF REALTORS®

BAY AREA HOUSING MARKET

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

SALES OF EXISTING DETACHED HOMES

Bay Area, Mar. 2016: 3,665 Units, -3.4% YTD, -8.1% YTY

SERIES: Sales of Existing Detached HomesSOURCE: CALIFORNIA ASSOCIATION OF REALTORS®

0

10000

20000

30000

40000

50000

60000

70000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

SALES BOUNCED BACK AFTER DECLINING IN 2013 AND 2014

Bay Area, 2015: +3.5%, 2016 YTD: -3.4%

SERIES: Sales of Existing Detached HomesSOURCE: CALIFORNIA ASSOCIATION OF REALTORS®

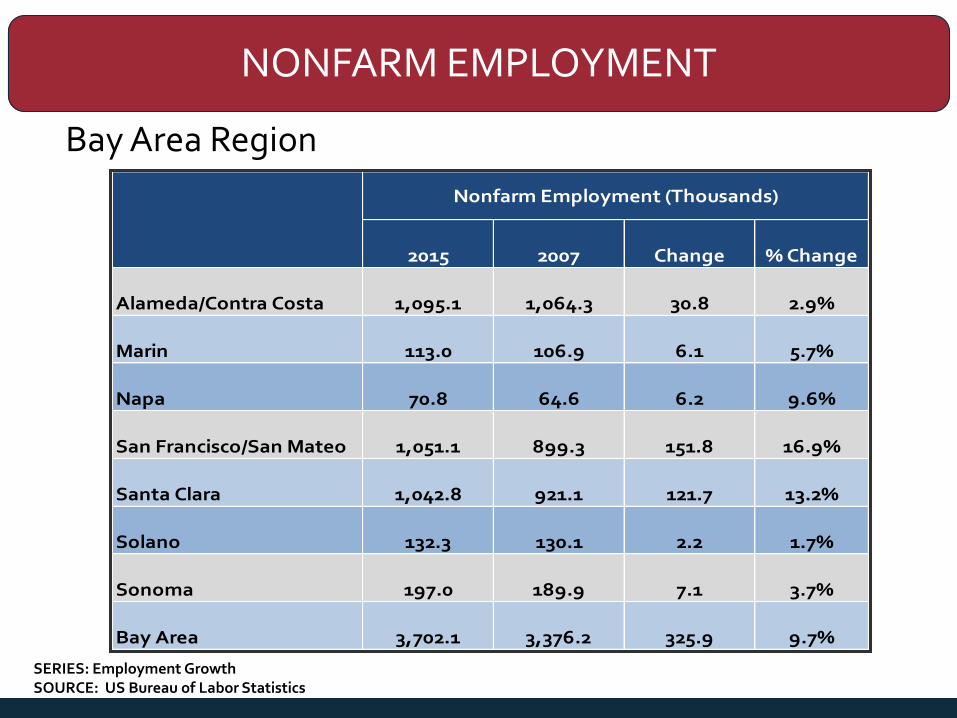

NONFARM EMPLOYMENT

Bay Area Region

SERIES: Employment GrowthSOURCE: US Bureau of Labor Statistics

2015 2007 Change % Change

Alameda/Contra Costa 1,095.1 1,064.3 30.8 2.9%

Marin 113.0 106.9 6.1 5.7%

Napa 70.8 64.6 6.2 9.6%

San Francisco/San Mateo 1,051.1 899.3 151.8 16.9%

Santa Clara 1,042.8 921.1 121.7 13.2%

Solano 132.3 130.1 2.2 1.7%

Sonoma 197.0 189.9 7.1 3.7%

Bay Area 3,702.1 3,376.2 325.9 9.7%

Nonfarm Employment (Thousands)

SALES OF EXISTING DETACHED HOMES

Bay Area Counties

Alameda 722 447 781 61.5% -7.6% -4.6%

Contra -Costa 798 541 866 47.5% -7.9% -6.6%

M arin 128 94 183 36.2% -30.1% -16.8%

Napa 94 55 105 70.9% -10.5% -5.8%

San Franc isc o 151 99 182 52.5% -17.0% -12.0%

San M a teo 302 199 349 51.8% -13.5% -2.3%

Santa Cla ra 741 488 846 51.8% -12.4% -2.3%

Solano 390 325 352 20.0% 10.8% 12.0%

Sonoma 339 243 323 39.5% 5.0% 8.5%

Y-t-DY-t-YCounty Mar-16 Feb-16 Mar-15 M-t-M

SERIES: Sales of Existing Detached HomesSOURCE: CALIFORNIA ASSOCIATION OF REALTORS®

March2016

February 2016

March2015

Median Time on the Market21.2 Days 25.5 Days 21.6 Days

Unsold Inventory Index2.6 Mos. 3.2 Mos. 2.1 Mos.

SUPPLY INDICATORS

Bay Area

Note: The Unsold Inventory Index represents the number of months it would take to deplete the remaining inventory at the end of a particular month with the sales rate of the month in consideration. Inventory includes listings with “Active”, “Pending”, and “Contingent” (when available) statuses.

SERIES: Median Time of Market, Unsold Inventory IndexSOURCE: CALIFORNIA ASSOCIATION OF REALTORS®

UNSOLD INVENTORY INDEX (MONTHS)

Bay Area

SERIES: Unsold Inventory IndexSOURCE: CALIFORNIA ASSOCIATION OF REALTORS®

County Mar-16 Feb-16 Mar-15

Alamed a 2.2 3.0 2.1

Contra-Costa 2.4 3.0 1.3

Marin 3.8 3.8 2.6

Napa 4.6 6.5 4.1

San Franc isco 2.7 3.3 1.6

San Mateo 2.2 2.7 1.6

Santa Clara 2.4 2.9 1.9

Solano 2.6 2.8 3.7

Sonoma 3.1 3.9 3.7

S. F. Bay Area 2.6 3.2 2.1

MASSIVE HOUSING SHORTAGE

MetroJob Creation2010-2015

New HomeConstruction2010-2015

Ratio

San Francisco-Oakland

234,000 30,000 7.8

Grand Rapids 46,000 6,000 7.8

San Jose 118,000 23,000 5.1

San Diego 101,000 21,000 4.9

Miami-Ft. Lauderdale

191,000 48,000 3.9

Salt Lake City 57,000 15,000 3.9

New York City 400,000 114,000 3.5

TIGHT SUPPLY CREATED MORE MARKET COMPETITION

4

3 3

0

1

1

2

2

3

3

4

4

5

San FranciscoBay Area

SouthernCalifornia

Other Counties inCalifornia

Number of Multiple Offers

SERIES: 2015 Housing Market SurveySOURCE: CALIFORNIA ASSOCIATION OF REALTORS®

36%

56%

63%

0% 20% 40% 60% 80%

Other Counties inCalifornia

Southern California

San Francisco BayArea

Percent with Multiple Offers

MEDIAN PRICE OF EXISTING DETACHED HOMES

Bay Area, March 2016: $761,160, Up 4.2% YTY

$-

$100,000

$200,000

$300,000

$400,000

$500,000

$600,000

$700,000

$800,000

$900,000

SERIES: Median Price of Existing Detached HomesSOURCE: CALIFORNIA ASSOCIATION OF REALTORS®

MEDIAN PRICE OF EXISTING DETACHED HOMES

Bay Area Counties

•

Alameda $762,570 $712,990 $713,060 7.0% 6.9%

Contra -Costa $572,620 $538,650 $491,780 6.3% 16.4%

M arin $1,148,150 $1,113,640 $1,085,230 3.1% 5.8%

Napa $666,670 $664,470 $562,500 0.3% 18.5%

San Franc isc o $1,360,580 $1,437,500 $1,275,000 -5.4% 6.7%

San M a teo $1,205,000 $1,200,000 $1,300,000 0.4% -7.3%

Santa Cla ra $1,065,000 $942,500 $932,100 13.0% 14.3%

Solano $376,420 $365,620 $345,100 3.0% 9.1%

Sonoma $596,090 $554,610 $519,500 7.5% 14.7%

Y-t-YCounty Mar-16 Feb-16 Mar-15 M-t-M

SERIES: Median Price of Existing Detached HomesSOURCE: CALIFORNIA ASSOCIATION OF REALTORS®

HOUSING DEMAND INCREASED IN MORE AFFORDABLE REGIONS

Annual % Change in Sales

SERIES: Sales of Existing SFHSOURCE: CALIFORNIA ASSOCIATION OF REALTORS®

County 2015 (yty% chg.)

Alam eda -0.7%

Contra-Costa 7.9%

Marin -3.8%

Napa 10.5%

San Franc isc o -8.2%

San Mateo -6.4%

Santa Clara 6.0%

Solano 18.6%

Sonom a 2.8%

S. F. Bay Area 3.5%

SAN FRANCISCO COUNTY

0

50

100

150

200

250

300

350

400

450

Jan

-05

Sep

-05

May-

06

Jan

-07

Sep

-07

May-

08

Jan

-09

Sep

-09

May-

10

Jan

-11

Sep

-11

May-

12

Jan

-13

Sep

-13

May-

14

Jan

-15

Sep

-15

SALES OF EXISTING DETACHED HOMES

San Francisco County, Mar. 2016: 151 Units, -12.0% YTD, -17.0% YTY

SERIES: Sales of Existing Single Family HomesSOURCE: CALIFORNIA ASSOCIATION OF REALTORS®

0

500

1000

1500

2000

2500

3000

3500

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

SALES DOWN TWO YEARS IN A ROW AFTER REACHING THE RECENT PEAK IN 2013

San Francisco, 2015: -8.2%, 2016 YTD: -7.8%

SERIES: Sales of Existing Detached HomesSOURCE: CALIFORNIA ASSOCIATION OF REALTORS®

EMPLOYMENT GROWTH:CALIFORNIA VS. SAN FRANCISCO/SAN MATEO

Feb 2016: 2.8%

Feb 2016: 4.0%

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

Jan

-08

Jul-

08

Jan

-09

Jul-

09

Jan

-10

Jul-

10

Jan

-11

Jul-

11

Jan

-12

Jul-

12

Jan

-13

Jul-

13

Jan

-14

Jul-

14

Jan

-15

Jul-

15

Jan

-16

California San Francisco/San MateoANNUAL PERCENT CHANGE

SERIES: Total Nonfarm EmploymentSOURCE: US Bureau of Labor Statistics, CA Employment Development Division

UNSOLD INVENTORY INDEX

San Francisco County, March 2016: 2.7 Months

Note: The Unsold Inventory Index represents the number of months it would take to deplete the remaining inventory at the end of a particular month with the sales rate of the month in consideration. Inventory includes listings with “Active”, “Pending”, and “Contingent” (when available) statuses.

0

2

4

6

8

10

12

Jan

-05

Sep

-05

May-

06

Jan

-07

Sep

-07

May-

08

Jan

-09

Sep

-09

May-

10

Jan

-11

Sep

-11

May-

12

Jan

-13

Sep

-13

May-

14

Jan

-15

Sep

-15

SERIES: Unsold Inventory Index of Existing Single Family HomesSOURCE: CALIFORNIA ASSOCIATION OF REALTORS®

NEW HOUSING PERMITS

San Francisco County, Feb. 2016: 635 Units, +101.8% YTD

0

200

400

600

800

1,000

1,200

Jan

-05

Sep

-05

May-

06

Jan

-07

Sep

-07

May-

08

Jan

-09

Sep

-09

May-

10

Jan

-11

Sep

-11

May-

12

Jan

-13

Sep

-13

May-

14

Jan

-15

Sep

-15

Single Family Multi-Family

SERIES: New Housing PermitsSOURCE: Construction Industry Research Board

0

1000

2000

3000

4000

5000

6000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Single Family Multi-Family

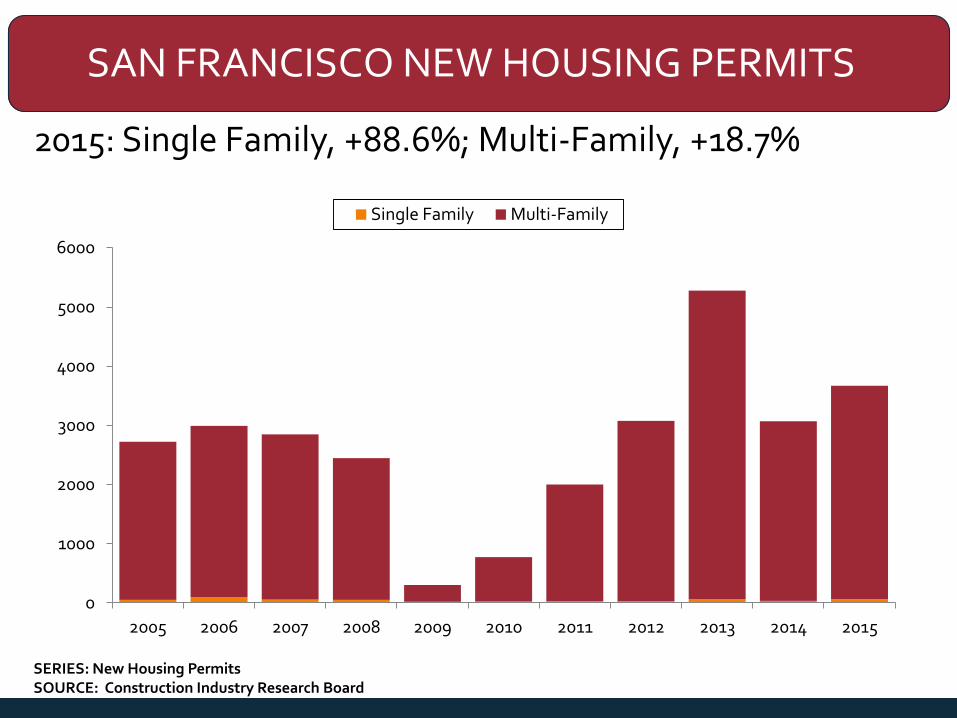

SAN FRANCISCO NEW HOUSING PERMITS

2015: Single Family, +88.6%; Multi-Family, +18.7%

SERIES: New Housing PermitsSOURCE: Construction Industry Research Board

MEDIAN PRICE OF EXISTING DETACHED HOMES

San Francisco County, Mar. 2016: $1,360,580, Up 6.7% YTY

$0

$200,000

$400,000

$600,000

$800,000

$1,000,000

$1,200,000

$1,400,000

$1,600,000

Jan

-05

Sep

-05

May-

06

Jan

-07

Sep

-07

May-

08

Jan

-09

Sep

-09

May-

10

Jan

-11

Sep

-11

May-

12

Jan

-13

Sep

-13

May-

14

Jan

-15

Sep

-15

SERIES: Median Price of Existing Single Family HomesSOURCE: CALIFORNIA ASSOCIATION OF REALTORS®

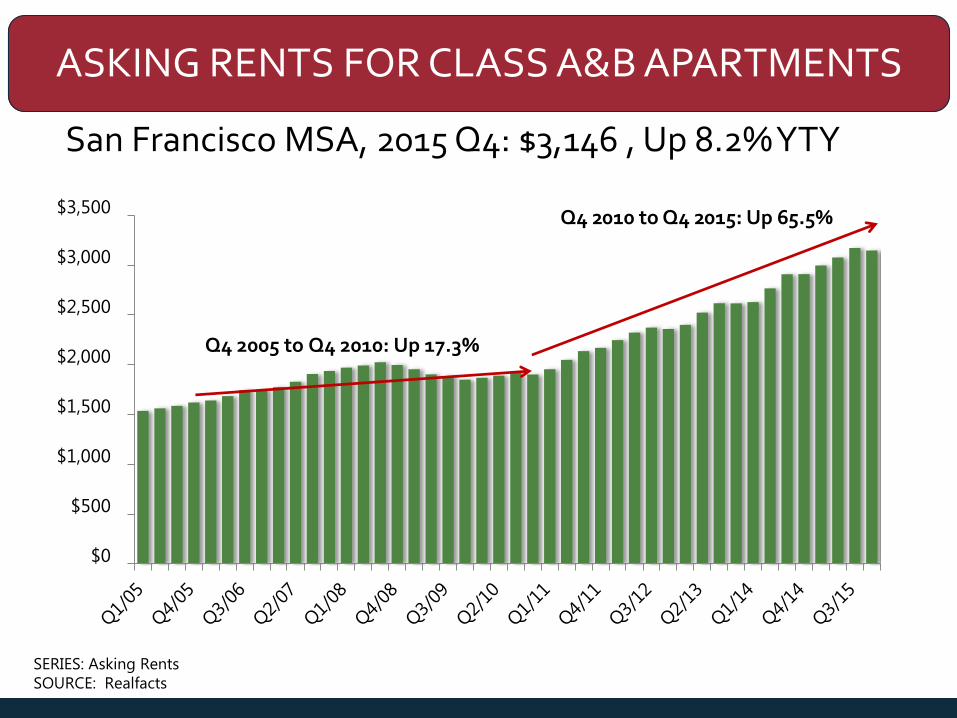

ASKING RENTS FOR CLASS A&B APARTMENTS

San Francisco MSA, 2015 Q4: $3,146 , Up 8.2% YTY

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

Q4 2005 to Q4 2010: Up 17.3%

SERIES: Asking RentsSOURCE: Realfacts

Q4 2010 to Q4 2015: Up 65.5%

0%

1%

2%

3%

4%

5%

6%

7%

Q1/05Q4/05Q3/06Q2/07Q1/08Q4/08Q3/09Q2/10Q1/11Q4/11Q3/12Q2/13Q1/14Q4/14Q3/15

VACANCY RATES FOR CLASS A&B APARTMENTS

San Francisco MSA, 2015 Q4: 5.6%

SERIES: Vacancy RatesSOURCE: Realfacts

HOUSING AFFORDABILITY INDEX

San Francisco County, 4th Quarter 2015: 11%% OF HOUSEHOLDS THAT CAN BUY

0%

5%

10%

15%

20%

25%

30%

35%

SERIES: Housing Affordability Index of Traditional BuyersSOURCE: CALIFORNIA ASSOCIATION OF REALTORS®

$30,340

$52,690 $49,230

$70,680$88,390

$97,570

$124,980 $118,690

$254,107

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

RetailSalespersons

Auto.Mechanics

Chefs andHead Cooks

ElementarySchool

Teachers

Firefighters ComputerProgrammers

RegisteredNurses

SoftwareDevelopers

(Applications)

Min. IncRequired toBuy a Med.

Home

HOW WAGES MEASURED AGAINST INCOME REQUIRED TO BUY A HOME

SOURCE: Bureau of Labor Statistics, C.A.R.

Annual Mean Wage

San Francisco

OAKLAND

SALES OF SINGLE FAMILY HOMES

Oakland, March 2016: 188 Units

-1.1% 2015 YTD, +4.5% 2016 YTD, +0.5% YTY

SOURCE: Clarus Market Metrics

MEDIAN PRICE OF SINGLE FAMILY HOMES

Oakland, March 2016: $600,000

Up 14.6% MTM, Up 10.1% YTY

SOURCE: Clarus Market Metrics

FOR SALE PROPERTIES

Oakland, March 2016: 561 Units

-9.4% 2015 YTD, -12.7% 2016 YTD, -9.7% YTY

SOURCE: Clarus Market Metrics

Note: “For Sale Properties” represents the overall supply that exist throughout the entire month, including any listings that appear as “Active” any point in time during the month.

CITY OF SANTA CLARA

SALES OF SINGLE FAMILY HOMES

City of Santa Clara, March 2016: 26 Units

-9.1% 2015 YTD, -19.7% 2016 YTD, -42.2% YTY

SOURCE: Clarus Market Metrics

MEDIAN PRICE OF SINGLE FAMILY HOMES

City of Santa Clara, March 2016: $1,200,000

Up 4.3% MTM, Up 29.0% YTY

SOURCE: Clarus Market Metrics

FOR SALE PROPERTIES

City of Santa Clara, March 2016: 88 Units

+0.6% 2015 YTD, -19.7% 2016 YTD, -3.3% YTY

SOURCE: Clarus Market Metrics

Note: “For Sale Properties” represents the overall supply that exist throughout the entire month, including any listings that appear as “Active” any point in time during the month.

2016 FORECAST

CALIFORNIA HOUSING MARKET OUTLOOK

2010 2011 2012 2013 2014 2015 2016f

SFH Resales (000s) 416.5 422.6 439.8 414.9 382.7 407.1 432.6

% Change -12.3% 1.4% 4.1% -5.9% -7.8% 6.4% 6.3%

Median Price ($000s) $305.0 $286.0 $319.3 $407.2 $446.9 $474.4 $489.4

% Change 10.9% -6.2% 11.6% 27.5% 9.8% 6.2% 3.2%

Housing Affordability

Index 48% 53% 51% 36% 30% 31% 28%

30-Yr FRM 4.7% 4.5% 3.7% 4.0% 4.2% 3.9% 4.5%

SERIES: CA Housing Market OutlookSOURCE: CALIFORNIA ASSOCIATION OF REALTORS®

SALES UP FOR 2015 AND CONTINUE TO IMPROVE IN 2016; PRICE WILL GROW STEADILY THIS YEAR AND NEXT

Units (Thousand)

407.1432.6

0

100

200

300

400

500

600

700

2005 2007 2009 2011 2013 2015

Th

ou

san

ds

Sales of Existing Detached Homes

$474 $489

$0

$100

$200

$300

$400

$500

$600

2005 2007 2009 2011 2013 2015p

Th

ou

san

ds

Median Price

Price (Thousand)

SERIES: CA Housing Market OutlookSOURCE: CALIFORNIA ASSOCIATION OF REALTORS®

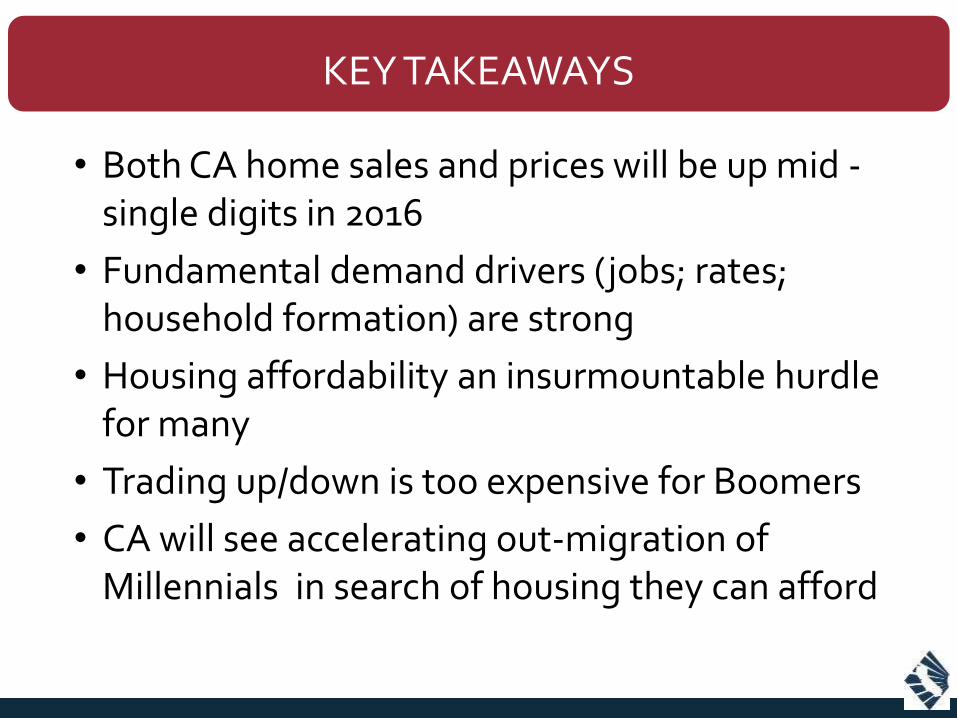

• Both CA home sales and prices will be up mid -single digits in 2016

• Fundamental demand drivers (jobs; rates; household formation) are strong

• Housing affordability an insurmountable hurdle for many

• Trading up/down is too expensive for Boomers

• CA will see accelerating out-migration of Millennials in search of housing they can afford

KEY TAKEAWAYS

STAY CONNECTED WITH RESEARCH

CARResearchGroup

CARResearchInfo

On.car.org/CARResearch

Housingmatters.car.org

“The Impact of Investors on California’s Housing Market”

Friday, April 29, 2016

1:00 PM – 1:30 PM

To register: WWW.CAR.ORG/MARKETDATA/VIDEOS

Join us for our next webinar…

THANK YOU!

www.car.org/marketdata

This presentation can be found on

www.car.org/marketdata

Speeches & Presentations