2016 CFP Board Ethics Course w Highlights€¦ · 2 STEP 6 – Obligations to CFP Board ..... 24...

67

2016 CFP BOARD ETHICS COURSE 2 HOURS COPYRIGHT © 2016 SUCCESS CONTINUING EDUCATION 2 Corporate Plaza Drive, Suite 100 Newport Beach, CA 92660 (949) 706-9425 (A member of the Success CE family of Companies)

Transcript of 2016 CFP Board Ethics Course w Highlights€¦ · 2 STEP 6 – Obligations to CFP Board ..... 24...

2016 CFP

BOARD ETHICS

COURSE 2 HOURS

COPYRIGHT © 2016 SUCCESS CONTINUING EDUCATION 2 Corporate Plaza Drive, Suite 100 Newport Beach, CA 92660 (949) 706-9425 (A member of the Success CE family of Companies)

2

© Copyright 2016 Success Continuing Education

All Rights Reserved. No part of this publication may be used or reproduced in any form or by any means, transmitted in any form or by any means, electronic or mechanical, for any purpose, without the express written permission of Success Continuing Education. This publication is designed to provide general information on the topic presented. It is sold with the understanding that the publisher is not engaged in rendering any legal or professional services. Although professionals prepared this content, it should not be used as a substitute for professional services. If legal or other professional advice is required, the services of a professional should be sought.

Throughout this text, references are made to the CFP Board’s copyrighted Standards of Professional Conduct. Success Continuing Education does not own or reserve any rights to this material.

CFP Board’s Code of Ethics and Professional Responsibility, Rules of Conduct, Financial Planning Practice Standards, Fitness Standards for Candidates and Registrants and Anonymous Case Histories are the property of CFP Board and may not be resold, republished or copied without the prior consent of CFP Board.

Copyright © 2016 Certified Financial Planner Board of Standards, Inc. All rights reserved. Reproduced with permission.

TABLE OF CONTENTS CHAPTER 1 .......................................................................................................... 1

CFP — THE STANDARDS OF EXCELLENCE ............................................................ 1LEARNING OBJECTIVES ..................................................................................... 1THE STUDY OF ETHICS ..................................................................................... 1

Why is the Study of Ethics So Important? ............................................................. 2CFP BOARD — STANDARDS OF PROFESSIONAL CONDUCT ................................. 2CFP® PROFESSIONAL FIDUCIARY RESPONSIBILITIES ........................................... 4

Establishing a Good Faith Relationship ................................................................ 5Maintaining Loyalty ............................................................................................... 6Skill and Care ........................................................................................................ 6Full Disclosure ....................................................................................................... 6Timeliness ............................................................................................................. 6Accountability of Funds ......................................................................................... 6Conflict of Interest ................................................................................................. 7Proper Business Solicitation ................................................................................. 7Competitive Fair Play ............................................................................................ 7

CASE IN POINT – BREACH OF FIDUCIARY RESPONSIBILITIES ................................ 8CHAPTER 1 REVIEW QUESTIONS ..................................................................... 11

CHAPTER 2 ........................................................................................................ 12CODE OF ETHICS AND PROFESSIONAL RESPONSIBILITY ........................................ 12

CODE OF ETHICS ............................................................................................ 12Principle 1 – Integrity ........................................................................................... 12Principle 2 – Objectivity ....................................................................................... 13Principle 3 – Competence ................................................................................... 14Principle 4 – Fairness .......................................................................................... 14Principle 5 – Confidentiality ................................................................................. 14Principle 6 – Professionalism .............................................................................. 15Principle 7 – Diligence ......................................................................................... 15

CHAPTER 2 REVIEW QUESTIONS ..................................................................... 17

CHAPTER 3 ........................................................................................................ 18RULES OF CONDUCT .......................................................................................... 18

CASE IN POINT – RULES OF CONDUCT VIOLATIONS ........................................... 19STEP 1 — Defining the Relationship with the Prospective Client or Client ........ 19STEP 2 – Information Disclosed to Prospective Clients and Clients .................. 21STEP 3 – Prospective Client and Client Information and Property ..................... 22STEP 4 – Obligations to Prospective Clients and Clients ................................... 23STEP 5 – Obligations to Employers .................................................................... 24

2

STEP 6 – Obligations to CFP Board ................................................................... 24CASE IN POINT DISCIPLINE IMPOSED ................................................................ 25CHAPTER 3 REVIEW QUESTIONS ..................................................................... 26

CHAPTER 4 ........................................................................................................ 27FINANCIAL PLANNING PRACTICE STANDARDS ...................................................... 27

THE SIX STEPS OF FINANCIAL PLANNING ENGAGEMENTS .................................. 29Establishing and Defining the Relationship With the Client ................................ 29Determining a Client’s Personal and Financial Goals, Needs and Priorities ....... 30Analyzing and Evaluating the Client’s Financial Status ...................................... 30Developing and Presenting Financial Planning Recommendations .................... 31Implementing the Financial Planning Recommendations ................................... 33Monitoring ........................................................................................................... 34

DETERMINING IF A FINANCIAL PLANNING ENGAGEMENT EXISTS .......................... 35Material Elements vs. Financial Planning ........................................................... 36

HYPOTHETICAL FINANCIAL PLANNING ENGAGEMENT ......................................... 38CHAPTER 4 REVIEW QUESTIONS ..................................................................... 41

CHAPTER 5 ........................................................................................................ 42DISCLOSURES .................................................................................................... 42

DISCLOSURE GUIDE ........................................................................................ 43THE ENGAGEMENT AGREEMENT ...................................................................... 45CASE IN POINT ............................................................................................... 47SAMPLE DISCLOSURE FORMS .......................................................................... 48

Other Professional Services (Form OPS) ........................................................... 50Financial Planning Disclosure Sample (Form FPD) ............................................ 52Financial Planning Disclosure and Agreement Sample (Form FPDA) ................ 54Sample Engagement Letter ................................................................................ 57

CHAPTER 5 REVIEW QUESTIONS ..................................................................... 60ANSWERS TO CHAPTER REVIEW QUESTIONS ....................................................... 61

3

How to Gain Maximum Knowledge from this Course!

In order to enhance the learning and knowledge process, this course incorporates several adult learning strategies designed to increase comprehension and retention of the material presented.

Since it may have been several years since you were involved in a formal learning process, we have included a brief description of the learning concepts employed by this course.

The format of this text includes the traditional headings and subheadings as well as highlighting to bring attention to critical concepts and facts.

1. Highlighting: As you study the text, pay particular attention to areas of text that are highlighted in Yellow and those areas that are highlighted in Gray. Understanding the concepts and facts contained within the yellow highlighted areas are critical to successful completion of the course final examination. Material within the gray highlighted areas will be reinforced later in the course through the use of Chapter Review Questions. (Note: Highlighting permissions vary by regulating authority.)

2. Case Studies: Some of the more variable concepts will be illustrated using case studies. These case studies are designed to reinforce the concept being discussed and it is recommended that you take the necessary time to digest the points made within the case studies.

3. For Insurance Licensees in Non-Monitored States, our exclusive web-based search feature allows quick retrieval of important data for maximizing the learning process. Simply execute Ctrl + F and enter keyword(s) or key phrase(s) to locate those items electronically within the course material.

Understanding all of the material in this text is necessary to achieve the overall learning strategies that have been incorporated to Success Continuing Education copyrighted courses to increase exposure to portions of the text that are fundamental to the learning process.

1

CHAPTER 1 CFP — THE STANDARDS OF EXCELLENCE

LEARNING OBJECTIVES

Effective January 2016, the CFP Board established the following required learning objectives for Ethics CE programs. Upon successful completion of this course, the student will be able to:

• Define and discuss a financial planning engagement, material elements of financial planning, and the financial planning process.

• Analyze specific fact patterns to determine if a financial planning relationship exists.

• Differentiate between the standards of care set forth in Rules 1.4 and 4.5 of the Rules of Conduct, and apply each standard of care to specific factual situations.

• Apply each Practice Standard set forth in the Financial Planning Practice Standards to a hypothetical financial planning engagement.

• Identify the information that must be disclosed to the client in writing by a CFP®

professional who is engaged in a financial planning relationship or providing material elements of financial planning.

• Define the required information that must be disclosed to clients and prospective clients, when that information must be disclosed, and apply each disclosure requirement to specific factual situations. (This includes but is not limited to the compensation and conflict-of-interest disclosure requirements set forth in Rule 2.2 of the Rules of Conduct and Practice Standards 100-1, 400-3, and 500-1.)

THE STUDY OF ETHICS

Simply put, ethical standards define what is considered acceptable and unacceptable behavior, but the overall scope is much more extensive.

Ethics is a moral philosophy—a system of moral principles—that involves systematizing, defending, and recommending concepts of right and wrong conduct.

2

A solid ethical foundation within the financial industry is of paramount importance — the value of which cannot be understated or underestimated. As a CFP® professional, you may be holding someone else’s future life quality in your hands. That’s a tremendous responsibility — one that cannot be taken lightly.

WHY IS THE STUDY OF ETHICS SO IMPORTANT?

Studying ethics can provide assistance in making the right decision when a person finds himself or herself in an ambiguous, confusing, or otherwise difficult situation. Situations of conflict often arise — some situations and their resulting behavior may be perfectly legal, but may not necessarily be ethical. CFP® professionals are required to advance their continuing knowledge of ethical standards through the ongoing study of ethics.

Ethical behavior is typically something a person doesn’t have to “think about.” More often than not, it comes naturally to “ethical people.” However, there are certain circumstances where an individual may “think” they are acting in an ethical manner yet find themselves on the cusp of questionable ethical behavior.

In this course, we will look at some specific case scenarios — some of the items in the scenarios may seem black and white, while others may appear to have a gray hue. These scenarios are presented through the use of CFP Board Anonymous Case Histories.

CFP BOARD — STANDARDS OF PROFESSIONAL CONDUCT

The Certified Financial Planner Board of Standards, Inc. (CFP Board), founded in 1985, is a non-profit organization, which acts in the public interest by fostering professional standards in personal financial planning through its setting and enforcement of the four E’s: (1) Education, (2) Examination, (3) Experience, and (4) Ethics — as well as other requirements for CFP® certification.

CFP Board’s mission statement:

“TobenefitthepublicbygrantingtheCFP®certificationandupholdingitastherecognizedstandardofexcellenceforcompetentandethicalpersonalfinancialplanning.”

When providing financial planning advice, CFP® professionals must comply with CFP Board Practice Standards. Those individuals who have achieved the high level of certification as a CFP® professional must adhere to the requirements of the CFP Board through continuing education to uphold the standard of excellence for competent and ethical personal financial planning.

3

Through CFP Board’s Code of Ethics and Professional Responsibility (“Code of Ethics”), CFP Board identifies the ethical principles CFP® professionals should meet in all of their professional activities. Through the Rules of Conduct, CFP Board establishes binding professional and ethical norms that protect the public and advance professionalism. CFP Board’s Financial Planning Practice Standards (“Practice Standards”) describe the best practices expected of CFP® professionals engaged in financial planning and refer to those sections of the Rules of Conduct that provide ethical guidance. Through its Disciplinary Rules and Procedures (“Disciplinary Rules”), CFP Board enforces the Code of Ethics, Rules of Conduct, and Practice Standards and establishes a process for applying the Standards of Professional Conduct to actual professional activities.

As a condition of CFP® certification, CFP® professionals agree to abide by the Standards of Professional Conduct and to be subject to CFP Board’s enforcement process. CFP Board has developed a set of principles and rules that apply to all CFP®

professionals and practice standards that apply when a CFP® professional provides financial planning advice.

The primary objectives of CFP Board are:

• To develop, promulgate, improve, and maintain a uniform code of ethics and uniform practice and product standards for Certified Financial Planners for the benefit and protection of the general public;

• To develop, promulgate, improve and maintain educational, testing and certification standards and procedures for financial planners;

• To grant to financial planners who have met the corporation’s educational, testing, experience and the standards and criteria the right to use the certification marks “Certified Financial Planner” and “CFP®”;

• To promote and maintain the highest professional standards of practice and conduct among financial planners;

• To establish, conduct and enforce investigatory and disciplinary procedures to regulate the professional conduct of Certified Financial Planner® Professionals for the protection of the general public;

• To promote public awareness and understanding of the professional preparation, role, competency and limitations of Certified Financial Planner® Professionals; and

• To lessen the burdens of government by cooperating with and assisting state and federal regulatory agencies to appropriately, effectively and uniformly regulate professional financial planners.

4

CFP Board works toward reaching its mission through five core objectives:

1. Competency — Establish and uphold rigorous competency standards for CFP®

certification.

2. Professional Standards & Enforcement — Protect the public’s interest through the establishment and enforcement of rigorous financial planning ethical and practice standards.

3. Public Advocacy — Influence policy to benefit the public and increase access for all to competent and ethical financial planning.

4. Communication & Outreach — Increase public and stakeholder awareness of and preference for CFP® certification as the standard for financial planning.

5. Sustainability — Strengthen CFP Board’s capacity to achieve its mission.

CFP® PROFESSIONAL FIDUCIARY RESPONSIBILITIES

Only the CFP® professional can display the certification trademarks which represent such a high level of competency, ethics and professionalism. CFP® professionals who provide financial planning services are held to a fiduciary standard of care—and are always required to act in the best interest of their clients and potential clients.

A “fiduciary” is a person in a position of special trust and confidence. The term fiduciary refers to a relationship in which one person has a responsibility of care for the assets or rights of another person.

CFP Board’s definition of fiduciary is: “Onewhoactsinutmostgoodfaith,inamannerheorshereasonablybelievestobeinthebestinterestoftheclient.”

When a business relationship is entered into, both parties have expectations of a mutually beneficial relationship. The fiduciary standard of care that CFP® professionals must uphold is of the highest degree.

The Standards require that all CFP® professionals who provide financial planning services and material elements of financial planning will be held to the duty of care of a fiduciary, as defined by CFP Board. While CFP Board’s fiduciary standard is reserved for financial planning services, the Standards nevertheless require a high duty of care for all CFP® professionals in any type of client relationship: “ACFP®professionalshallatalltimesplacetheinterestoftheclientaheadofhisorherown.” (Code of Ethics Rule 1.4)

The key to CFP Board’s definition of fiduciary is “…reasonablybelievestobeinthebestinterestoftheclient.” It would be impossible for any professional to review every possible

5

option that could benefit a prospective client or client, but CFP Board expects any financial planning services provided to be the best services and recommendations available, given the CFP® professional’s reasonable professional judgment and any limitations placed on the CFP® professional by any business or regulatory requirements.

If limitations exist, it is up to the CFP® professional to make complete disclosure of those limitations to the client, including any contractual or agency relationships that have a potential to affect the client and any terms under which proprietary products may be offered.

Practice Standards 400-2 explains that “therecommendationsdevelopedbythepractitionermaydifferfromthoseofotherpractitionersoradvisers,yeteachmayreasonablymeettheclient’sgoals,needsandpriorities.”

As you know, when providing financial planning or material elements of financial planning the CFP® professional’s duty of care rises to that of a fiduciary. When acting in a fiduciary capacity, the adviser owes his client or prospective client all of the following standards.

ESTABLISHING A GOOD FAITH RELATIONSHIP

If any one party in a relationship cannot be seen by the other as generally acting in a good faith manner, a mutually successful relationship cannot exist.

While each party in a relationship has their own needs and responsibilities, the unifying theme to the relationship is that of utmost good faith. Utmost good faith is a term that can be applicable in any financial transaction. The doctrine of utmost good faith is a minimum standard that requires both parties in a transaction to act honestly toward each other and not to mislead or withhold critical information from one another.

Operating with utmost good faith legally obliges all involved parties to reveal any information that might influence one party’s decision to enter into a contract with the other party. No matter what the subject of the relationship is in a mutually agreed upon business transaction, all parties involved should operate with utmost good faith.

One party alone cannot create a cohesive relationship. When all parties are oriented toward the same goal with each striving toward that goal, and all parties are mutually dependent on each other for the attainment of that goal, then there is a minimization of conflict and a maximization of cooperation among the parties.

6

MAINTAINING LOYALTY

CFP® professionals always act on behalf of the client or prospective client’s best interest. Demonstrating loyalty means exercising a genuine feeling of strong support and faithfulness to commitments or obligations.

SKILL AND CARE

CFP® professionals must demonstrate responsibility to handle the client or prospective client’s needs in a proficient and scrupulous manner, thus enabling the client’s goals to be reached. In order to accomplish this, the client or prospective client must be represented in a skillful manner. Should a subject arise in which the CFP® professional is unskilled, he/she must put his client’s needs above his/her own, even if that means referring the client elsewhere or to another source. Doing so insures the client or prospective client’s best representation.

FULL DISCLOSURE

Full disclosure is critical to the welfare of the client. Should any information remain undisclosed, the client cannot make a fully informed decision. Without having all the information at the client’s disposal, a fully informed decision cannot be made and, therefore, the client’s needs are not being serviced appropriately. Even if disclosure of an item could deter the client or prospective client from acting upon the recommendations made, it is best to avoid any potential conflicts of interest. It is the fiduciary’s responsibility to keep his/her ethics and motivations unquestionable and intact.

TIMELINESS

Obligations are typically based on time schedules. Any paperwork generated from a presentation or recommendation should be submitted on a timely basis to limit the client’s risk of not achieving their goals as expected.

ACCOUNTABILITY OF FUNDS

As in most cases and most business transactions, client funds should never be commingled with other funds, especially those of the individual serving in an advisory position.

7

CONFLICT OF INTEREST

A“conflictofinterest”existswhenacertificant’sfinancial,business,propertyand/orpersonalinterests,relationshipsorcircumstancesreasonablymayimpairhis/herabilitytoofferobjectiveadvice,recommendationsorservices.

CFP® professionals must act in all transactions to avoid any potential conflict of interest between himself, his client and the organization involved. The highest priority is the obligation to the client or potential client—acting at all times with the client’s best interest in mind is paramount.

A conflict of interest occurs when an individual or organization is involved in multiple interests, one of which could possibly corrupt the motivation. More generally, conflicts of interest can be defined as any situation in which an individual (or corporation) is in a position to exploit a professional or official capacity in some way for their own personal benefit.

CFP® professionals should never put themselves in a position in which they can benefit from both parties involved in a transaction. CFP® professionals represent the client or prospective client and act with the client’s best interest in mind.

For many professionals, it is virtually impossible to avoid having conflicts of interest from time to time. A conflict of interest can, however, become a legal matter; for instance, when an individual tries (and/or succeeds in) influencing the outcome of a decision for personal benefit. If any conflict of interest exists, it must be fully disclosed to the client or prospective client.

PROPER BUSINESS SOLICITATION

It is the financial planner’s professional obligation to solicit only that business which represents the risk element that involved parties are willing to take. To solicit higher risk business and omit or alter information in an effort to conceal any risk factor is unethical and not in keeping with the fiduciary responsibilities owed to the client.

COMPETITIVE FAIR PLAY

Defamation is malicious and should be avoided at all cost. Defamation of character can cause injury to one’s reputation, sometimes resulting in irreparable damage. Opinions, of course, need to be expressed but must be done so with thought and moral testimony.

8

Any intentional false communication, either written or spoken, that harms a person’s reputation can be construed as defamation of character. Not only is defamation unethical it can, in certain situations, also be construed as a criminal act.

CASE IN POINT – BREACH OF FIDUCIARY RESPONSIBILITIES

The following scenario is taken from CFP Board’s Anonymous Case Histories to demonstrate a breach of fiduciary responsibilities on the part of one CFP® professional.

Issue Presented:1

WhetheraCFP®certificant(“Respondent”)violatedCFPBoard’sStandardsofProfessionalConductwhenhe:(1)recommendedthataclientinvestherentireIRAportfolioinequitymutualfunds;(2)illustratedtheperformanceoftheequityfundstotheclientwithaninappropriatelyhighrateofreturn;and(3)didnotobtainfurtherinformationfromtheclientaftersheindicatedconflictinginvestmentgoals.

In this case, the CFP® professional (Respondent) met with the client to discuss retirement benefits options as the client’s employer had presented her with three options:

1. Lump sum distribution; 2. A Single Life Annuity with a monthly distribution; and/or 3. A Survivor Annuity.

Following the meeting, the client chose the lump sum distribution. She received a letter from the Respondent advising her to invest in equity mutual funds to diversify her retirement plan. Respondent presented the client with an illustration of the equity mutual funds in the sub-accounts of a variable annuity program that assumed a net rate of return of 9.85%.

Six months later, the client signed an IRA Rollover Agreement and also filled out a Fact Finder that indicated her investment objectives as income and long-term growth and her risk exposure as low and partially aggressive. Two months following, the client purchased Class B equity mutual funds (“Equities”) with nearly all of her IRA funds. The Equities were split between four funds recommended by the Respondent.

1 CFP Board ACH 22702

9

Six years later, the client filed a claim with NASD alleging that Respondent:

1. Recommended Equities that were unsuitable; 2. Misrepresented the risks associated with Equities; 3. Failed to supervise the account; and 4. Breached his fiduciary duty to the Client.

The Respondent filed an Answer to the claim stating that the client acted against his advice and attempted to time the market.

The Commission found that the Respondent failed to exercise reasonable and prudent professional judgment in providing professional services because he: (1) Recommended a portfolio of only Equities and put the client’s entire lump sum into Equities when the client wanted a dedicated income stream; and (2) used an inappropriate variable annuity illustration that reflected a net rate of return of 9.85%. Thus, Respondent violated Rule 4.4:

Rule 4.4 –“Acertificantshallexercisereasonableandprudentprofessionaljudgmentinprovidingprofessionalservicestoclients.”

The Commission also found that Respondent failed to provide services diligently and determined that Respondent was not thorough in obtaining information from the client to clarify her investment objectives after she gave Respondent a conflicting description of her risk exposure as low and partially aggressive, then wanted her entire account to be invested in Equities. Thus, Respondent violated Rule 701.

Rule 701 – “ACFPBoarddesigneeshallprovideservicesdiligently.”

The Commission found grounds for discipline because he violated Code of Ethics rules by providing false or misleading statements to CFP Board and making a false statement on the Declaration Section of his Initial Certification Application when he denied involvement in any civil action relating to his professional code.

The Commission considered the following mitigating factors when rendering their disciplinary action:

• Respondent is relatively new to the business;

• The ten (10) year bull market created an unreasonable expectation in investors; and

• Respondent was working with a difficult client.

10

A Private Censure to the CFP® professional was issued advising him to:

• Be properly trained in the services he chooses to provide to the public;

• Not accept clients he does not have the expertise to handle;

• Document all steps of the financial planning process;

• Help clients define their objectives thoroughly;

• Review all alternatives to be considered by the client;

• Not merely give the clients the answer they want to hear; and

• Use appropriate sales illustrations.

11

CHAPTER 1 REVIEW QUESTIONS

Which of the following answers each sentence the best? (Answers are in the back of the text.)

1. It is the financial planner’s professional obligation to solicit only that business which represents the risk element that ___________ is/are willing to take.

a) involved parties b) only the client c) only the professional entity d) only the CFP® professional

2. CFP Board acts in the public interest by fostering professional standards in personal financial planning through its setting and enforcement of the four E’s:

a) Excellence, Experiment, Ethics, and Examination. b) Education, Examination, Experience, and Ethics. c) Enosis, Enthusiasm, Enterprise, and Education. d) Ethics, Excellence, Enosis, and Education.

3. The Standards require that all CFP® professionals who provide financial planning services will be held to ___________, as defined by CFP Board.

a) the duty of care of a fiduciary b) enforcement process c) review d) the standard of Enosis

12

CHAPTER 2 CODE OF ETHICS AND PROFESSIONAL RESPONSIBILITY

CODE OF ETHICS

CFPBoardadoptedtheCodeofEthicstoestablishthehighestprinciplesandstandards.ThesePrinciplesaregeneralstatementsexpressingtheethicalandprofessionalidealsCFP®professionalsareexpectedtodisplayintheirprofessionalactivities.Assuch,thePrinciplesareaspirationalincharacterandprovideasourceofguidanceforCFP®professionals.ThePrinciplesformthebasisofCFPBoard’sRulesofConduct,PracticeStandardsandDisciplinaryRules,andthesedocumentstogetherreflectCFPBoard’srecognitionofCFP®professionals’responsibilitiestothepublic,theirrespectiveclients,colleaguesandemployers.

When it comes to ethics and professional responsibility, CFP® professionals are held to the highest of standards. They are obliged to uphold the principles of: (1) Integrity, (2) objectivity, (3) competence, (4) fairness, (5) confidentiality, (6) professionalism and (7) diligence. Within the Code of Ethics and Professional Responsibility, CFP Board defines these seven principles to serve as guidance for ethical behavior in professional activities.

PRINCIPLE 1 – INTEGRITY

Provide professional services with integrity. Integrity defined:

• Firmadherencetoacodeofespeciallymoralorartisticvalues:INCORRUPTIBILITY;• Anunimpairedcondition:SOUNDNESS;• Thequalityorstateofbeingcompleteorundivided:COMPLETENESS.

Example: “Heisamanofthehighestintegrity.Hehadtheintegritytorefusetocompromiseonmattersofprinciple.”

Integrity demands honesty and candor, which must not be subordinated to personal gain and advantage. Clients place certificants in positions of trust, and the ultimate source of that trust is the certificant’s personal integrity. Allowance can be made for

13

innocent error and legitimate differences of opinion, but integrity cannot co-exist with deceit or subordination of one’s principles.

Certificants should always be honest, and that honesty should be proactive, especially in situations that pit a certificant’s principles against personal gain. A certificant with integrity will keep their principles intact even if it means they receive less compensation from the engagement.

PRINCIPLE 2 – OBJECTIVITY

Provide professional services objectively. Objectivity defined:

• Thestateorqualityofbeingobjective;• Intentnessonobjectsexternaltothemind;• Externalreality.

Example: “Hetriestomaintainobjectivityinhisdecisions.”

Objectivity requires intellectual honesty and impartiality. Regardless of the particular service rendered or the capacity in which a certificant functions, certificants should protect the integrity of their work, maintain objectivity and avoid subordination of their judgment.

A certificant who subordinates their personal interest to the honest service of the client raises the reputation of their occupation while protecting them from litigation.

When a certificant and client do not see eye to eye, it is important for the certificant to put aside these biases and view the situation from the client’s point of view. Getting a different perspective on a disagreement enables the certificant to see both sides of the situation, and to notice where personal bias might be hindering their view. It also helps them to better communicate with the client and give the client a fuller understanding of the situation.

For instance, it is probably frustrating to a certificant if a client is not willing to accept any risk to meet their financial retirement goals, even though the client is young and has many years until retirement. Even though the certificant might believe that the client’s best interests are served by accepting some risk, they should realize that the decision ultimately belongs to the client.

In this situation, the certificant should educate the client about the nature of the risk, and try to understand his or her reasoning. Getting the client’s perspective may help to produce an agreement or compromise that addresses the client’s perspective and maintains the integrity of the certificant’s work.

14

PRINCIPLE 3 – COMPETENCE

Maintain the knowledge and skill necessary to provide professional services competently. Competence defined:

• Asufficiencyofmeans;theabilitytodosomethingwell;• Thequalityorstateofbeingcompetent.

Competence means attaining and maintaining an adequate level of knowledge and skill, and application of that knowledge and skill in providing services to clients. Competence also includes the wisdom to recognize the limitations of that knowledge and when consultation with other professionals is appropriate or referral to other professionals necessary. Certificants make a continuing commitment to learning and professional improvement.

PRINCIPLE 4 – FAIRNESS

Be fair and reasonable in all professional relationships. Disclose conflicts of interest. Fairness defined:

• Agreeingwithwhatisthoughttoberightoracceptable;treatingpeopleinawaythatdoesnotfavorsomeoverothers.

Fairness requires impartiality, intellectual honesty and disclosure of material conflicts of interest. It involves a subordination of one’s own feelings, prejudices and desires so as to achieve a proper balance of conflicting interests. Fairness is treating others in the same fashion that you would want to be treated.

PRINCIPLE 5 – CONFIDENTIALITY

Protect the confidentiality of all client information. Confidentiality defined:

• Entrustedwithconfidences;trustedwithsecretorprivateinformationanddemonstratingthatyouwillkeepthesubjectsecretorprivate.

The nature of financial planning requires certificants to gather sensitive information about their clients in order to make informed decisions. Clients place a great deal of trust in certificants by disclosing very personal details about their finances and their lives in general. Clients naturally expect that any intimate knowledge will be confidential, and it is the certificant’s duty to ensure the safety of this information, making it accessible only to those who are authorized to have access. A client’s information should be kept private regardless of whether or not sharing that information would cause harm to the client.

15

Confidentiality means ensuring that information is accessible only to those authorized to have access. A relationship of trust and confidence with the client can only be built upon the understanding that the client’s information will remain confidential.

When information about a client is required in a legal process, it must be given, and to do so is not in breach of the principle of confidentiality. In the case of a civil dispute between the certificant and the client, the confidentiality agreement is altered, since a certificant may need to use client information as evidence. This evidence could be vital to a certificant’s defense against any accusations made by the client.

PRINCIPLE 6 – PROFESSIONALISM

Act in a manner that demonstrates exemplary professional conduct. Professionalism defined:

• Theskill,goodjudgment,andpolitebehaviorthatisexpectedfromapersonwhoistrainedtodoajobwell;

• Theconduct,aims,orqualitiesthatcharacterizeormarkaprofessionoraprofessionalperson.

A high level of professionalism is expected when working with clients. The CFP®

professional acts in a manner that demonstrates exemplary professional conduct. Professionalism requires behaving with dignity and courtesy to clients, fellow professionals, and others in business-related activities. Certificants cooperate with fellow certificants to enhance and maintain the profession’s public image and to improve the quality of services.

In order to uphold the profession’s image and the quality of service delivered to clients, certificants must hold other certificants accountable for their actions. After all, the CFP designation is a mark of quality and ethical principles, and allowing unethical or illegal behavior to go unreported tarnishes the reputation of the profession as a whole rather than just the reputation of the guilty party(ies). If a certificant discovers that a fellow certificant is doing something that violates the Code of Ethics, they should report those actions to the CFP Board. If these actions are illegal as well as unethical, the certificant should notify the proper authorities.

PRINCIPLE 7 – DILIGENCE

Provide professional services diligently. Diligence defined:

• Theattentionandcarelegallyexpectedorrequiredofaperson;• Thecarethatareasonablepersonexercisestoavoidharmtootherpersonsortheir

property;

16

• Researchandanalysisofacompanyororganizationdoneinpreparationforabusinesstransaction.

Diligence is the provision of services in a reasonably prompt and thorough manner, including the proper planning for, and supervision of, the rendering of professional services. This includes keeping complete records of all transactions, funds, assets, property and agreements, and keeping those records organized.

When a certificant sets out to fulfill any aspect of their profession (i.e., completing paperwork, gathering and analyzing data, or rendering services to the client), they should act in a timely fashion. If the certificant does not meet deadlines or return paperwork in a timely manner, it signals to clients that the certificant does not value their business. This, in turn, negatively impacts the certificant along with the reputation of the profession itself.

17

CHAPTER 2 REVIEW QUESTIONS

Which of the following answers each sentence the best? (Answers are in the back of the text.)

1. If information about a client is required in a legal process, it:

a) is not a breach of the principle of confidentiality. b) is a breach of the principle of confidentiality. c) cannot be used against the certificant. d) can be used against the certificant.

2. If a certificant discovers that a fellow certificant is doing something that violates the Code of Ethics, they should:

a) withhold the information from the CFP Board. b) withhold the information from their employer, but make a report to the CFP

Board. c) inform the CFP Board. d) provide instruction to the fellow certificant of how to properly handle the situation.

3. If the certificant believes that the client’s best interests are served by accepting some risk and the client does not want to accept the risk, the certificant should:

a) educate the client as to why they should accept the risk. b) realize that the decision ultimately belongs to the client. c) minimize the risk to the client and make the investment anyway since the

certificant believes the investment is in the client’s best interest. d) find another investment vehicle in which the client is unaware of the risk.

18

CHAPTER 3 RULES OF CONDUCT

TheRulesofConductestablishthehighstandardsexpectedofCFP®professionalsanddescribethelevelofprofessionalismrequiredofCFP®professionals.TheRulesofConductarebindingonallCFP®professionals,regardlessoftheirtitle,position,typeofemploymentormethodofcompensationandtheygovernallthosewhohavetherighttousetheCFP®marks,whetherornotthosemarksareactuallyused.TheuniverseofactivitiesengagedinbyaCFP®professionalisdiverseandaCFP®professionalmayperformall,someornoneofthetypicalservicesprovidedbyfinancialplanningprofessionals.SomeRulesmaynotbeapplicabletoaCFP®professional’sspecificactivity.Asaresult,whenconsideringtheRulesofConduct,theCFP®professionalmustdeterminewhetheraspecificRuleisapplicabletothoseservices.ACFP®professionalwillbedeemedtobeincompliancewiththeseRulesifthatCFP®professionalcandemonstratethathisorheremployercompletedtherequiredaction.

Violations of the Rules of Conduct may subject a CFP® professional to disciplinary action by the CFP Board. The Disciplinary Rules describe the procedures followed by the CFP Board in enforcing the Rules of Conduct. Under the Disciplinary Rules, certificants are given notice of potential violations and an opportunity to be heard by a panel of other professionals.

Disciplinary action extends to the rights of certificants to use the designated CFP®

marks. Therefore, the Rules are not designed to be a basis for legal liability to any third party. The following is required of every CFP® professional:

• Defining the relationship with prospective clients and clients;

• Disclosure of information to prospective clients and clients;

• Treatment of prospective client information and property;

• Obligations to prospective clients and clients;

• Obligations to employers; and

• Obligations to CFP Board.

19

CASE IN POINT – RULES OF CONDUCT VIOLATIONS

In this study of the CFP Board Rules of Conduct, we will look at a specific anonymous case history and demonstrate how the case represents a violation of many of the Rules of Conduct. Following is a description of the case.

Issues Presented:2 WhetheraCFP®professional(“Respondent”)violatedCFPBoard’sStandardsofProfessionalConductwhenhe:

1) EngagedinanoutsidebusinessactivitywithoutprovidingnoticeandreceivingpriorwrittenapprovalfromhisFirm;and

2) Falselycertifiedtohisbroker-dealerthathewasnotengagedinoutsidebusinessactivity.

Following his employer’s (“Firm’s”) approval process, Respondent had occasionally engaged in approved outside business activities. However, on one specific occasion he had not followed the proper approval process. Instead:

“Respondentstatedthat,withthetransactionatissue,he“neededtogetpaidpromptly,ascomparedtowaitingthe4weekplus‘waitingperiod’tobepaidthroughthefirm’scompensationchannels.”Finally,Respondentstatedthathe“completedthisone,isolatedunauthorizedactivityduetofinancialhardship.”

Case in Point – Respondent solicited and sold a fixed indexed annuity to a customer outside the scope of his employment without informing the Firm of this business activity and receiving the required written approval. In addition, Respondent falsely certified to the Firm that he was not engaged in outside business activity. As a result of the undisclosed and unapproved outside business activity, the Respondent was suspended and fined.

At the end of each of the following Rules that were affected, the violations will be noted in CaseinPointViolationsinitalicsin this manner. To avoid confusion with CaseinPoint annotations, when Rules are quoted they will be presented in normal type following the Rule number.

STEP 1 — DEFINING THE RELATIONSHIP WITH THE PROSPECTIVE CLIENT OR CLIENT

Rule 1.1 – The certificant and the prospective client or client shall mutually agree upon the services to be provided by the certificant.

2 CFP Board ACH 28285

20

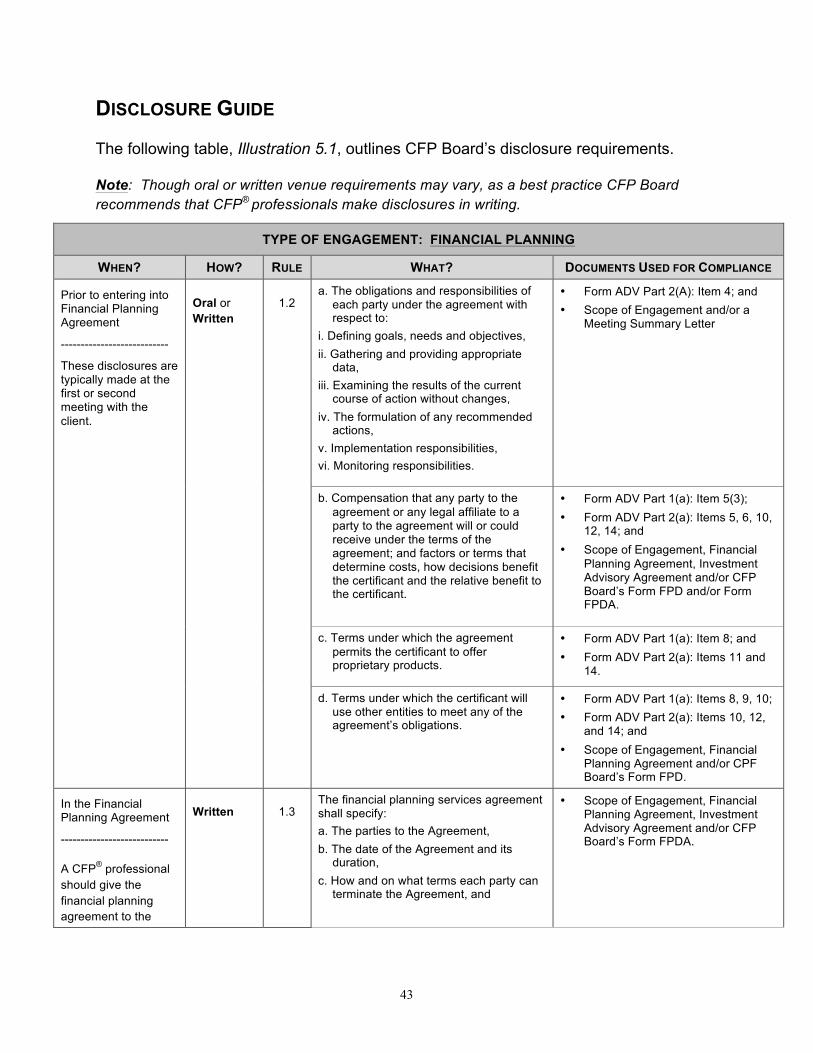

Rule 1.2 – If the certificant’s services include financial planning or material elements of financial planning, prior to entering into an agreement, the certificant shall provide written information or discuss with the prospective client or client the following:

a. The obligations and responsibilities of each party under the agreement with respect to:

i. Defining goals, needs and objectives, ii. Gathering and providing appropriate data, iii. Examining the result of the current course of action without changes, iv. The formulation of any recommended actions, v. Implementation responsibilities, and vi. Monitoring responsibilities.

b. Compensation that any party to the agreement or any legal affiliate to a party to the agreement will or could receive under the terms of the agreement; and factors or terms that determine costs, how decisions benefit the certificant and the relative benefit to the certificant.

c. Terms under which the agreement permits the certificant to offer proprietary products.

d. Terms under which the certificant will use other entities to meet any of the agreement’s obligations. If the certificant provides the above information in writing, the certificant shall encourage the prospective client or client to review the information and offer to answer any questions that the prospective client or client may have.

Rule 1.3 – If the services include financial planning or material elements of financial planning, the certificant or the certificant’s employer shall enter into a written Agreement governing the financial planning services (“Agreement”). The Agreement shall specify:

a. The parties to the Agreement,

b. The date of the Agreement and its duration,

c. How and on what terms each party can terminate the Agreement, and

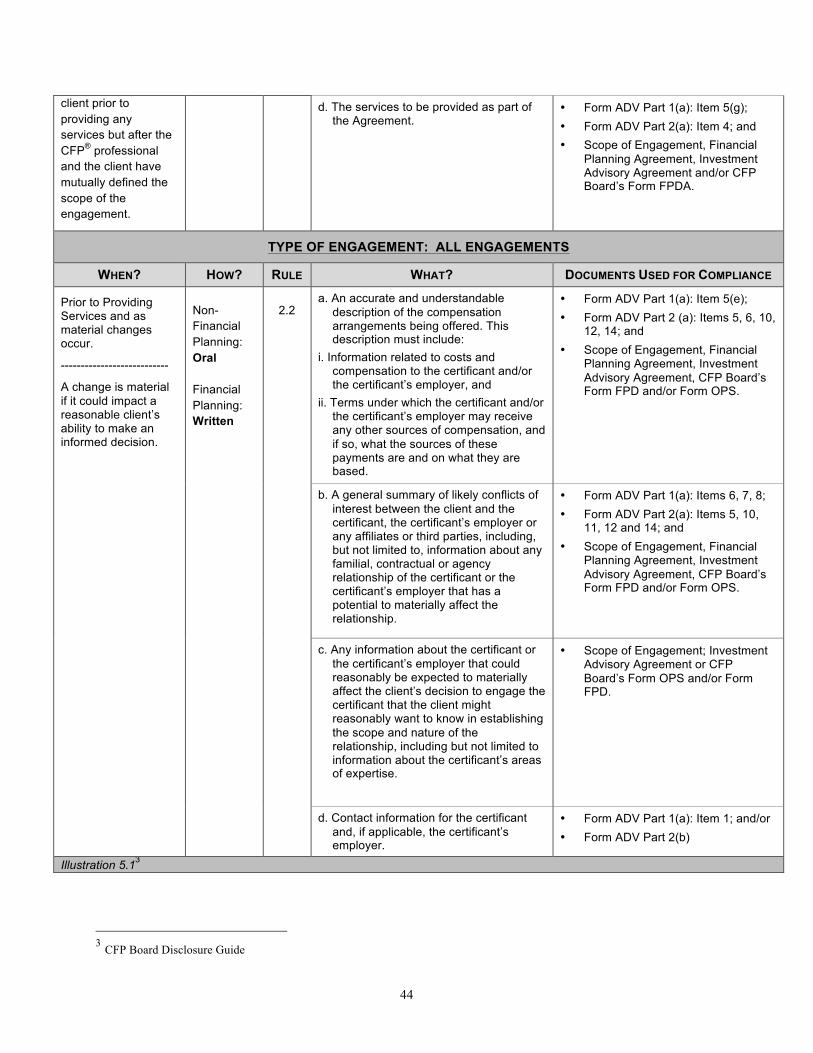

d. The services to be provided as part of the Agreement.

The Agreement may consist of multiple written documents. Written documentation that includes the items above and is used by a certificant or certificant’s employer in compliance with state or federal law, or the rules or regulations of any applicable

21

self-regulatory organization, such as the Securities and Exchange Commission’s Form ADV or other disclosure documents, shall satisfy the requirements of this Rule.

Rule 1.4 – A certificant shall at all times place the interest of the client ahead of his or her own. When the certificant provides financial planning or material elements of financial planning, the certificant owes to the client the duty of care of a fiduciary as defined by CFP Board.

STEP 2 – INFORMATION DISCLOSED TO PROSPECTIVE CLIENTS AND CLIENTS

Rule 2.1 – A certificant shall not communicate, directly or indirectly, to clients or prospective clients any false or misleading information directly or indirectly related to the certificant’s professional qualifications or services. A certificant shall not mislead any parties about the potential benefits of the certificant’s service. A certificant shall not fail to disclose or otherwise omit facts where that disclosure is necessary to avoid misleading clients.

Rule 2.2 – A certificant shall disclose to a prospective client or client the following information:

a. An accurate and understandable description of the compensation arrangements being offered. This description must include:

i. Information related to costs and compensation to the certificant and/or the certificant’s employer, and

ii. Terms under which the certificant and/ or the certificant’s employer may receive any other sources of compensation, and if so, what the sources of these payments are and on what they are based.

b. A general summary of likely conflicts of interest between the client and the certificant, the certificant’s employer or any affiliates or third parties, including, but not limited to, information about any familial, contractual or agency relationship of the certificant or the certificant’s employer that has a potential to materially affect the relationship.

c. Any information about the certificant or the certificant’s employer that could reasonably be expected to materially affect the client’s decision to engage the certificant that the client might reasonably want to know in establishing the scope and nature of the relationship, including but not limited to information about the certificant’s areas of expertise.

22

d. Contact information for the certificant and, if applicable, the certificant’s employer.

e. If the services include financial planning or material elements of financial planning, these disclosures must be in writing. The written disclosures may consist of multiple written documents. Written disclosures used by a certificant or certificant’s employer that includes the items listed above, and are used in compliance with state or federal laws, or the rules or requirements of any applicable self-regulatory organization, such as the Securities and Exchange Commission’s Form ADV or other disclosure documents, shall satisfy the requirements of this Rule.

The certificant shall timely disclose to the client any material changes to the above information.

CaseinPointViolationRule2.2(b)–TheCommissiondeterminedthatRespondentviolatedthisRulewhenhefailedtodisclosetoaclientthatafixedindexedannuitywasanoutsidebusinessactivitythatRespondenthadnotdisclosedtoandreceivedwrittenapprovalfromhisbroker-dealerbecauseRespondentneededtoreceivehiscommissionquickly.

TheCommissiondeterminedtherewasaconflictofinterestbecauseRespondentdidnotdisclosetotheclientthathewasbeingcompensateddifferentlyandwouldreceivehiscommissionquickeriftheclientpurchasedtherecommendedproductratherthanpurchasingaproductauthorizedbyRespondent’semployerandrunningthetransactionthroughFirm.Respondentshouldhavedisclosedthisdifferenceinthecompensationarrangementtotheclient.

STEP 3 – PROSPECTIVE CLIENT AND CLIENT INFORMATION AND PROPERTY

Rule 3.1 – A certificant shall treat information as confidential except as required in response to proper legal process; as necessitated by obligations to a certificant’s employer or partners; as required to defend against charges of wrongdoing; in connection with a civil dispute; or as needed to perform the services.

Rule 3.2 – A certificant shall take prudent steps to protect the security of information and property, including the security of stored information, whether physically or electronically, that is within the certificant’s control.

Rule 3.3 – A certificant shall obtain the information necessary to fulfill his or her obligations. If a certificant cannot obtain the necessary information, the certificant shall inform the prospective client or client of any and all material deficiencies.

23

Rule 3.4 – A certificant shall clearly identify the assets, if any, over which the certificant will take custody, exercise investment discretion, or exercise supervision.

Rule 3.5 – A certificant shall identify and keep complete records of all funds or other property of a client in the custody, or under the discretionary authority, of the certificant.

Rule 3.6 – A certificant shall not borrow money from a client. Exceptions to this Rule include:

a. The client is a member of the certificant’s immediate family, or

b. The client is an institution in the business of lending money and the borrowing is unrelated to the professional services performed by the certificant.

Rule 3.7 – A certificant shall not lend money to a client. Exceptions to this Rule include:

a. The client is a member of the certificant’s immediate family, or

b. The certificant is an employee of an institution in the business of lending money and the money lent is that of the institution, not the certificant.

Rule 3.8 – A certificant shall not commingle a client’s property with the property of the certificant or the certificant’s employer, unless the commingling is permitted by law or is explicitly authorized and defined in a written agreement between the parties.

Rule 3.9 – A certificant shall not commingle a client’s property with other clients’ property unless the commingling is permitted by law or the certificant has both explicit written authorization to do so from each client involved and sufficient recordkeeping to track each client’s assets accurately.

Rule 3.10 – A certificant shall return a client’s property to the client upon request as soon as practicable or consistent with a timeframe specified in an agreement with the client.

STEP 4 – OBLIGATIONS TO PROSPECTIVE CLIENTS AND CLIENTS

Rule 4.1 – A certificant shall treat prospective clients and clients fairly and provide professional services with integrity and objectivity.

Rule 4.2 – A certificant shall offer advice only in those areas in which he or she is competent to do so and shall maintain competence in all areas in which he or she is engaged to provide professional services.

Rule 4.3 – A certificant shall be in compliance with applicable regulatory requirements governing professional services provided to the client.

24

CaseinPointViolationRule4.3–TheCommissiondeterminedthatRespondentviolatedthisRulewhenhe:(1)engagedinanoutsidebusinessactivitywithoutprovidingnoticeandreceivingpriorwrittenapprovaland(2)falselycertifiedtoFirmthathewasnotengagedinoutsidebusinessactivity.AlthoughRespondentclaimedtohavedisclosedpossibleoutsideactivitiestohisemployerwhenhired,thatwasnotsufficientasRespondentwasrequiredtomakeannualdisclosuresandtoupdateFirmregardinganychangesinhisactivities.

Rule 4.4 – A certificant shall exercise reasonable and prudent professional judgment in providing professional services to clients.

Rule 4.5 – In addition to the requirements of Rule 1.4, a certificant shall make and/or implement only recommendations that are suitable for the client.

Rule 4.6 – A certificant shall provide reasonable and prudent professional supervision or direction to any subordinate or third party to whom the certificant assigns responsibility for any client services.

Rule 4.7 – A certificant shall advise his or her current clients of any certification suspension or revocation he or she receives from CFP Board.

STEP 5 – OBLIGATIONS TO EMPLOYERS

Rule 5.1 – A certificant who is an employee/agent shall perform professional services with dedication to the lawful objectives of the employer/principal and in accordance with CFP Board’s Code of Ethics.

CaseinPointViolationRule5.1–TheCommissiondeterminedthatRespondentviolatedRule5.1whenhe(1)engagedinanoutsidebusinessactivitywithoutprovidingnoticetoFirmandreceivingpriorwrittenapprovaland(2)falselycertifiedtoFirmthathewasnotengagedinoutsidebusinessactivity,inviolationofRules2.2(b),4.3,and6.5oftheRulesofConduct.

Rule 5.2 – A certificant who is an employee/agent shall advise his or her current employer/principal of any certification suspension or revocation he or she receives from CFP Board.

STEP 6 – OBLIGATIONS TO CFP BOARD

Rule 6.1 – A certificant shall abide by the terms of all agreements with CFP Board, including, but not limited to, using the CFP® marks properly and cooperating fully with CFP Board’s trademark and professional review operations and requirements.

Rule 6.2 – A certificant shall meet all CFP Board requirements, including continuing education requirements, to retain the right to use the CFP® marks.

25

Rule 6.3 – A certificant shall notify CFP Board of changes to contact information, including, but not limited to, e-mail address, telephone number(s) and physical address, within forty five (45) days.

(Rule 6.4 is superseded by Article 13.2 of the Disciplinary Rules.)

Rule 6.5 – A certificant shall not engage in conduct which reflects adversely on his or her integrity or fitness as a certificant, upon the CFP® marks, or upon the profession.

CaseinPointViolationRule6.5–TheCommissiondeterminedthatRespondentviolatedRule6.5whenhe:(1)engagedinanoutsidebusinessactivitywithoutprovidingnoticeandreceivingpriorwrittenapproval;and(2)falselycertifiedtohisbroker-dealerthathewasnotengagedinoutsidebusinessactivity.

CASE IN POINT DISCIPLINE IMPOSED

While considering the degree of sanction to impose, the Commission considered the following as mitigating factors:

1. Respondent’s conduct was an isolated incident involving only one client;

2. Respondent’s conduct did not result in client harm as the client’s money was returned and the transaction was reversed; and

3. According to Respondent, this investment was suitable and in the client’s best interests.

The Commission found grounds for discipline under CFP Board’s Disciplinary Rules and Procedures (“Disciplinary Rules”) for violations of the Rules of Conduct. The Commission found grounds for discipline under Article 3(d) of the Disciplinary Rules because the “Firm” suspended Respondent from association with any Firm member in any capacity for two months and fined Respondent $5,000. Pursuant to the Disciplinary Rules, the Commission issued a two-month suspension.

26

CHAPTER 3 REVIEW QUESTIONS

Which of the following answers each sentence the best? (Answers are in the back of the text.)

1) If a certificant is in violation of the Rules of Conduct, the certificant may be subject to CFP Board:

a) Financial Planning Standards. b) Codes of Conduct. c) Disciplinary Rules. d) Practice Standards.

2) According to Rule 1.3, if a certificant provides services that include material elements of financial planning:

a) a written Agreement is not necessary since the engagement did not elevate to financial planning.

b) a written Agreement is only necessary if the engagement elevates to financial planning.

c) the CFP Board must be consulted to determine if the engagement is deemed financial planning.

d) the certificant or the certificant’s employer must enter into a written Agreement governing the financial planning services.

27

CHAPTER 4 FINANCIAL PLANNING PRACTICE STANDARDS

The Practice Standards describe best practices of financial planning professionals providing professional services related to the six elements of the financial planning process. (The six elements are presented in detail below.) Each Standard is a statement relating to an element of the financial planning process, followed by an explanation of the Standard and its relationship to the Code of Ethics and Rules of Conduct.

CFPBoarddevelopedthePracticeStandardstoadvanceprofessionalisminfinancialplanningandenhancethevalueofthefinancialplanningprocess,fortheultimatebenefitofconsumersoffinancialplanningservices.

In general usage, a financial plan is created through a series of steps used to accomplish a financial goal or set of circumstances, such as debt elimination or preparation for retirement. CFP Board offers the following definitions for more extensive clarity.

A“financialplanningpractitioner”isapersonwhoprovidesfinancialplanningservicestoclients.A“financialplanningengagement”existswhenacertificantperformsanytypeofmutuallyagreeduponfinancialplanningserviceforaclient.

“Personalfinancialplanning”or“financialplanning”denotestheprocessofdeterminingwhetherandhowanindividualcanmeetlifegoalsthroughthepropermanagementoffinancialresources.Financialplanningintegratesthefinancialplanningprocesswiththefinancialplanningsubjectareas.Indeterminingwhetherthecertificantisprovidingfinancialplanningormaterialelementsoffinancialplanning,factorsthatmaybeconsideredinclude,butarenotlimitedto:

• Theclient’sunderstandingandintentinengagingthecertificant;• Thedegreetowhichmultiplefinancialplanningsubjectareasareinvolved;• Thecomprehensivenessofdatagathering;and• Thebreadthanddepthofrecommendations.

Financial planning does not have to occur within a specific format or timeframe. Avoiding a written financial plan does not mean an encounter will not be considered

28

financial planning. A financial planning determination may occur whether material elements are given to the client or prospective client simultaneously, consecutively, or even independent of each other.

“Personalfinancialplanningsubjectareas”or“financialplanningsubjectareas”denotesthebasicsubjectfieldscoveredinthefinancialplanningprocesswhichtypicallyinclude,butarenotlimitedto:

• Financialstatementpreparationandanalysis(includingcashflowanalysis/planningandbudgeting);

• Insuranceplanningandriskmanagement;• Employeebenefitsplanning;• Investmentplanning;• Incometaxplanning;• Retirementplanning;and• Estateplanning.

Financial planning is a thorough process and requires gathering detailed and comprehensive data about the client’s personal and financial situation. This data can be used to assess a client’s needs and goals within any of these financial planning subject areas.

The above list is not all-inclusive, and a financial planning engagement may involve subject areas not included above. A financial planning engagement can involve any or all of these areas, and there is no minimum number of subject areas required for an engagement to be considered financial planning. There are also no particular subject areas that must be included. However, for an engagement involving multiple subject areas, more comprehensive data is needed, and the breadth and depth of recommendations increases, rising to the level of financial planning. Here is a good rule of thumb for determining if an engagement constitutes financial planning:

An engagement integrating the financial planning process with two or more subject areas generally provides financial planning to the client.

“Personalfinancialplanningprocess”or“financialplanningprocess”denotestheprocess,whichtypicallyincludessomeorallofthefollowingsixsteps.Infinancialplanningengagements,aCFP®professionalmust:

1) Establishanddefinetherelationshipwiththeclient;2) Gatherclientdataandgoalsetting;3) Analyzegatheredinformationandevaluatetheclient’sfinancialstatus;

29

4) Developandpresentfinancialplanningrecommendations;5) Implementfinancialplanningrecommendations;and6) Monitortherecommendations.

Financial planning engagements are subject to extra rules set forth by the CFP Board. Of the 30 rules created by CFP Board, four apply specifically to financial planning: Rules 1.2, 1.3, 1.4, and 2.2(e).

THE SIX STEPS OF FINANCIAL PLANNING ENGAGEMENTS

Financial planning engagements follow the six-step process described above. By completing each step of this process in sequence, the CFP® professional ensures that they are providing the best possible service to the client while communicating all information to the client in an understandable manner. Communication is a priority throughout the process, since proper disclosure and communication ensures that both client and CFP® have the same expectations from the relationship. A healthy, communicative client-planner relationship invites frankness and understanding and minimizes the risk of dispute and litigation.

Below, we will look at each step of the six-step process, not only quoting the Standard, but also providing elaboration on how each step applies in financial planning engagements.

ESTABLISHING AND DEFINING THE RELATIONSHIP WITH THE CLIENT

100-1:Thefinancialplanningpractitionerandtheclientshallmutuallydefinethescopeoftheengagementbeforeanyfinancialplanningserviceisprovided.

At the outset of a financial planning engagement, the CFP® professional and the client should mutually define the scope of the engagement. This is the first step upon which all other steps of the process will be constructed.

According to the CFP Board, the objectives of this defining process are:

• To identify the service(s) to be provided;

• To disclose the CFP® professional’s material conflicts of interest;

• To disclose the CFP® professional’s compensation arrangement(s);

• To determine the responsibilities of the client and those of the CFP® professional;

30

• To establish the duration of the engagement; and

• To provide any additional information necessary to define or limit the scope.

DETERMINING A CLIENT’S PERSONAL AND FINANCIAL GOALS, NEEDS AND PRIORITIES

200-1:Thefinancialplanningpractitionerandtheclientshallmutuallydefinetheclient’spersonalandfinancialgoals,needsandprioritiesthatarerelevanttothescopeoftheengagementbeforeanyrecommendationismadeand/orimplemented.

The process of “mutually-defining” is essential in determining what activities may be necessary to proceed with the client engagement. Goals and objectives provide focus, purpose, vision and direction for the financial planning process.

With this information, the certificant cannot only help the client clarify their goals, but also help them to understand the ramifications of unrealistic goals. The goals resulting from this process should be defined in a way that progress towards their fulfillment can be measured with some certainty. Having measurable goals safeguard the client-planner relationship by allowing the client to see the results of the engagement in action. If the client’s goals are not easily measurable, the client might take the certificant’s inability to measure their progress as evidence of either a lazy certificant or an ineffective product or service. People tend to get suspicious when they don’t receive clear answers to questions regarding their finances, even when the questions are complex, and it is possible that a client might suspect that the certificant is not performing in an ethical manner.

Before making any specific recommendations of products or services to meet the client’s goals, the certificant must first gather as much measurable, quantitative information as possible. The scope of the engagement and the client’s goals and needs will help the certificant to determine what information is needed.

ANALYZING AND EVALUATING THE CLIENT’S FINANCIAL STATUS

300-1: Afinancialplanningpractitionershallanalyzetheinformationtogainanunderstandingoftheclient’sfinancialsituationandthenevaluatetowhatextenttheclient’sgoals,needsandprioritiescanbemetbytheclient’sresourcesandcurrentcourseofaction.

Once the certificant has the necessary data, they must thoroughly analyze it and apply it toward their financial goals and needs. By doing so the certificant should be able to determine the likelihood of success in the engagement—that is, whether the intended

31

services to the client can be supported by the client’s resources, and whether those services can meet the mutually agreed-upon objectives.

It will be necessary for the certificant to work under certain assumptions, in order to predict the results of the engagement. These assumptions must be reasonable and must be discussed with the client and agreed upon by both the client and the certificant. The client will often specify certain assumptions and as long as they are reasonable, the certificant should use these assumptions.

According to the CFP Board in their Practice Standards:

“Bothpersonalandeconomicassumptionsmustbeconsideredinthisstepoftheprocess.Theseassumptionsmayinclude,butarenotlimitedto,thefollowing:

• Personalassumptions,suchas:retirementage(s),lifeexpectancy(ies),incomeneeds,riskfactors,timehorizonandspecialneeds;and

• Economicassumptions,suchas:inflationrates,taxratesandinvestmentreturns.”

In analyzing this information, the certificant is able to discover the client’s financial strengths and weaknesses, and can determine how the advantages or disadvantages of a particular course of action may affect them. Other issues may come to light through this process, and may need to be identified and discussed with the client. As a result of analyzing the client data, it may be necessary to modify the client’s goals or the scope of the engagement.

DEVELOPING AND PRESENTING FINANCIAL PLANNING RECOMMENDATIONS

This step is considered the very heart of financial planning. It is at this point that recommendations are formulated.

400-1: Identifying and Evaluating Financial Planning Alternative(s) – Thefinancialplanningpractitionershallconsidersufficientandrelevantalternativestotheclient’scurrentcourseofactioninanefforttoreasonablymeettheclient’sgoals,needsandpriorities.

In this step, the certificant searches for “What is Possible?” The purpose here is to identify any viable alternatives to the client’s current course of action (the financial actions the client was taking before engaging the certificant). Any alternative should be evaluated for its effectiveness in meeting the client’s goals. At the end of this process, the certificant may have more than one alternative.

400-2: Developing the Financial Planning Recommendation(s) – Thefinancialplanningpractitionershalldeveloptherecommendation(s)basedontheselectedalternative(s)and

32

thecurrentcourseofactioninanefforttoreasonablymeettheclient’sgoals,needsandpriorities.

Once the certificant has identified the alternatives and evaluated them, they should form and develop recommendations. These recommendations are concrete, detailed plans, and may consist of a single action or a combination of actions to be taken together.

A certificant must place the interest of the client ahead of his/her own at all times (Rule 1.4). In addition to this requirement, the certificant must make and/or implement only those recommendations that are suitable for the client (Rule 4.5).

The CFP Board states in its Practice Standards:

“Therecommendation(s)shallbeconsistentwithandwillbedirectlyaffectedbythefollowing:

• Mutually-definedscopeoftheengagement;• Mutually-definedclientgoals,needsandpriorities;• Quantitativedataprovidedbytheclient;• Personalandeconomicassumptions;• Practitioner’sanalysisandevaluationofclient’scurrentsituation;and• Alternative(s)selectedbythepractitioner.

As you can see from the list of above, the recommendations are the cornerstone of financial planning since they are, in effect, the “plan.” Recommendations are synthesized from all of the previous steps of the process and are reliant on the adequate completion of all aspects of those steps.

400-3: Presenting the Financial Planning Recommendation(s) – Thefinancialplanningpractitionershallcommunicatetherecommendation(s)inamannerandtoanextentreasonablynecessarytoassisttheclientinmakinganinformeddecision.

Now that the certificant has all of their recommendations in order, it is time to show the client the results. Clients do not generally have the financial expertise or training of a financial planner, and the certificant should keep this in mind when presenting recommendations. The certificant should present their findings in such a way that the client can adequately comprehend the current state of their finances, the details of the recommendation, and the effect that the recommendation would have on the client’s needs and goals. Any questions or concerns posed by the client should be addressed to assist them in fully understanding the details of the presentation.

33

When presenting recommendations to the client, the certificant should enumerate the critical components and factors of the recommendation(s). The CFP Board states in its Practice Standards:

“Thefactorsmayincludebutarenotlimitedtomaterial:

• Personalandeconomicassumptions;• Interdependenceofrecommendations;• Advantagesordisadvantages;• Risks;and/or• Timesensitivity.”

The certificant should listen to the client’s views on the recommendations and ascertain whether or not the recommendation(s) comply with the client’s values, goals, and expectations. If the client is satisfied with the recommendations and is willing to implement them, the certificant may move on to the next step. If the client expresses dissatisfaction or unwillingness to act, the certificant should try to find a way to modify these recommendations to meet both the client’s needs while maintaining the CFP® professional’s integrity.

IMPLEMENTING THE FINANCIAL PLANNING RECOMMENDATIONS

500-1: Agreeing on Implementation Responsibilities – Thefinancialplanningpractitionerandtheclientshallmutuallyagreeontheimplementationresponsibilitiesconsistentwiththescopeoftheengagement.

At this point, each party, the client and the certificant, will know their respective roles in implementing the recommendations. Through mutually agreeing on these responsibilities, both parties understand their involvement in the engagement as well as their accountability to the other party. It is ultimately the client’s responsibility to accept or reject recommendations and also to divide the responsibilities between client and certificant. In this situation, it is the certificant’s duty to assist in this process and to ensure that the client understands the ramifications of retaining or delegating any responsibilities. The client and certificant will also agree upon any services that will be provided by the certificant. The original scope of the engagement may have to be modified in order to satisfy the client.

According to the CFP Board’s Practice Standards, responsibilities may include:

• Identifying activities necessary for implementation;

• Determining division of activities between the practitioner and the client;

• Referring to other professionals;

34

• Coordinating with other professionals;

• Sharing of information as authorized; and

• Selecting and securing products and/or services.

It is also at this point in the process when conflicts of interest, sources of compensation or material relationships with other professionals must be disclosed (if the information has not already been disclosed).

If the certificant refers the client to other professionals, consultants, or advisers, the certificant must explain to the client on what grounds the certificant thinks that the professional is qualified for the service to be provided. In these cases, it is also important for the certificant to divulge any material relationships with such professionals or advisers.

500-2: Selecting Products and Services for Implementation – Thefinancialplanningpractitionershallselectappropriateproductsandservicesthatareconsistentwiththeclient’sgoals,needsandpriorities.

After both parties have mutually established their implementation responsibilities, the certificant will choose the specific products that will be implemented. The certificant might have had specific products in mind when presenting his recommendations to the client, or may have had only a general product in mind. The certificant should investigate the different products available, judging them based on their ability to fulfill the client’s needs, goals, and priorities and their suitability to the client’s financial situation. The certificant should decide which products to use, choosing, as always, the products and services that are in the client’s best interest.

According to the CFP Board in their Practice Standards, when selecting these products:

“Thepractitionershallmakealldisclosuresrequiredbyapplicableregulations.”

Since each product has different regulations regarding disclosure requirements, it is the certificant’s responsibility to understand the disclosure requirements of any product they implement.

MONITORING

600-1: Defining Monitoring Responsibilities – Thefinancialplanningpractitionerandtheclientshallmutuallydefinemonitoringresponsibilities.

This process may reveal the need to reinitiate steps of the financial planning process, which may lead to modification of the current scope of the engagement. There could be

35

many reasons for plan modification. For instance, if a client has unreasonable expectations with regard to monitoring, it might be necessary to alter the scope of the engagement or even certain recommendations in order to adjust the engagement to meet the client’s expectations.

The certificant should explain to the client which monitoring responsibilities the certificant is capable of providing. The following should be addressed in this communication:

• The products and services to be monitored;

• Which details or aspects of those services should be monitored;

• The frequency with which they are to be monitored; and

• How this information will be communicated to the client.