2016 Annual Report (pdf) - Rockhopper...

88

Building a well-funded, full-cycle, exploration-led E&P company Report and Accounts for the year ended 31 December 2016

Transcript of 2016 Annual Report (pdf) - Rockhopper...

RO

CK

HO

PP

ER

EX

PLO

RATIO

N P

LC R

eport and Accounts for the year ended 31 D

ecember 2016

Telephone +44 (0)207 486 1677info@rockhopperexploration.co.ukwww.rockhopperexploration.co.uk

@RockhopperExplo

Company Reg. No. 05250250

Rockhopper Exploration plc

Head office:4th Floor5 Welbeck StreetLondon W1G 9YQ

Rome office: Via Cornelia, 49800166 RomaItalia

Egypt office: Level 16A Road 22Maadi Sarayat,CairoEgypt

Building a well-funded, full-cycle, exploration-led E&P company

Report and Accounts for the year ended 31 December 2016

Des

igne

d an

d pr

oduc

ed b

y Ja

ckso

nBon

e Li

mite

d.P

rint

ed in

Eng

land

by

Syne

rgy

Gro

up.

Shareholder information

Key contacts

Registered address and head office:4th Floor5 Welbeck StreetLondon W1G 9YQ

Mediterranean office: Via Cornelia, 49800166 RomaItalia

Egypt office:Level 16A Road 22Maadi SarayatCairoEgypt

NOMAD and brokerCanaccord Genuity Limited88 Wood Street London EC2V 7QR

SolicitorsAshurst LLPBroadwalk House5 Appold StreetLondonEC2A 2DA

Principal BankersRoyal Bank of Scotland plc36 St Andrew SquareEdinburghEH2 2YB

AuditorKPMG LLP15 Canada SquareLondonE14 5GL

RegistrarComputershare Investor Services plcVintners Place68 Upper Thames StreetLondonEC4V 3BJ

Glossary

AGM Annual General Meetingbbl barrelbcf billion cubic feetBeach Egypt Beach Petroleum (Egypt) Pty Limited (now Rockhopper Egypt Pty Ltd)Board the Board of Directors of Rockhopper Exploration plcboe barrel(s) of oil equivalentboepd barrel(s) of oil equivalent per dayBOP blow out preventerbopd barrel(s) of oil per dayCapex capital expenditureCompany Rockhopper Exploration PLCE&P exploration and productionEIS Environmental Impact StatementESA Exploration Study AgreementExCo Executive CommitteeFarm-in to acquire an interest in a licence from another partyFarm-out to assign an interest in a licence to another partyFDP field development planFEED front end engineering and designFID Final Investment DecisionFIG Falkland Islands GovernmentFOGL Falkland Oil & Gas LimitedFPSO floating production, storage and offtake vesselG&A General & Administration expensesGroup The Company and its sunsidiariesGSA Gas Sales AgreementHoA Heads of AgreementHSE health, safety and environmentIAS International Accounting StandardIFRS International Financial Reporting StandardJV Joint Venturekboepd thousand barrels of oil equivalent per daykbopd thousand barrels of oil per dayKPI key performance indicatorLoI Letter of IntentLTI Lost Time IncidentLTIP Long Term Incentive PlanMOG Mediterranean Oil & Gas plcmmbbls million barrelsmmboe million barrels of oil equivalentmmbtu million British thermal unitsmmscfd million standard cubic feet per daymscf thousand standard cubic feetmt metric tonneNAV net asset valuePremier Premier Oil plcPSA Production Sharing AgreementPSC Production Sharing Contractscm standard cubic metreSIP Share Incentive Planspud to commence drilling a wellSTOIIP stock-tank oil initially in placeTSR total shareholder return2C best estimate of contingent resources2P proven plus probable$/US$ United States dollarWI working interest

Concerns and procedures

General [email protected]

Audit committee [email protected]

Websitewww.rockhopperexploration.co.uk

Shareholder concerns:Should shareholders have concerns which have not been adequately addressed by the chairman or chief executive, please contact the chairman of the audit committee at:[email protected]

Whistle-blowing procedures:Should employees, consultants, contractors or other interested parties have concerns which have not been adequately addressed by the chairman or chief executive, please contact the chairman of the audit committee at:[email protected]

85Report & Accounts for the year ended 31 December 2016

Rockhopper Exploration plc

Rockhopper Exploration plc (AIM: RKH) is an oil and gas exploration and production company with key interests in the North Falkland Basin and the Greater Mediterranean region.

Rockhopper Exploration plc Strategic Report

1Report & Accounts for the year ended 31 December 2016

STRATEGIC REPORT2 2016 highlights Rockhopper – the story so far4 Rockhopper at a glance6 Vision and business model8 ChairmanandChief ExecutiveOfficer’sReview10 Key Performance Indicators (KPIs)11 Marketoverview12 Chief OperatingOfficer’sReview18 Chief FinancialOfficer’sReview21 Internal controls and risk management22 Principal risks and uncertainties 26 Health, Safety, Environmental and Social Management

GOVERNANCE28 Chairman’sGovernanceReport30 Board of Directors32 CorporateGovernanceStatement35 Remuneration Report46 Statutory information48 Independentauditor’sreporttothe

members of Rockhopper Exploration plc

ACCOUNTSGroup company financial statements49 Groupincomestatement49 Groupstatementof comprehensiveincome50 Groupbalancesheet51 Groupstatementof changesinequity52 Groupcashflowstatement53 Notestothegroupfinancialstatements

Parent company financial statements76 Company balance sheet77 Companystatementof changesinequity78 Companycashflowstatement79 Notestothecompanyfinancialstatements

84 Key licence interests as at 1 April 201785 Shareholder information

2 Report & Accounts for the year ended 31 December 2016

Rockhopper Exploration plcStrategic Report

2016 highlights

2

> Building a material, full-cycle, exploration-led portfolio: > Consolidated leading North Falkland Basin acreage position through the all-share

mergerwithFalklandOil&GasLimited(“FOGL”) > Acquirednon-operatedproductionandexplorationassetsinEgyptfromBeachEnergy > AmbitiontofurthergrowtheGreaterMediterraneanassetbase> Maintaining operational resilience based on compelling portfolio economics: > Material increase in economic production*to1,350barrelsofoilequivalentperday(“boepd”) > CashoperatingcostsinGreaterMediterraneanreducedtoUS$14perboe > SeaLionprojecteconomicsenhancedwithfurthercostreductionsachieved – SeaLionlifeoffieldcostsestimatedatUS$35perbarrelandproject

“break-even”atUS$45perbarrel

*Economicproductionincludesproductionfromtheeffectivedate(being1January2016)oftheacquisitionofassetsinEgypt.

Rockhopper – the story so far

Q1 2017 2016

Ombrina Mare arbitration commencesRockhopper commences international arbitration proceedings,seekingverysignificantmonetarydamages,asaresultoftheRepublicofItaly’sbreaches of the Energy Charter Treaty in relation to theOmbrinaMareproject.

Sea Lion enters FEEDSeaLionprojectentersFEEDwithsetofworld-classcontractors.

RockhoppercompletesmergerwithFalklandOil&GasfollowingshareholderapprovalfrombothRockhopperandFOGLshareholders.

Rockhopperacquiresnon-operatedproductionandexplorationassetsinEgypt.

Farm-OutInJuly,Rockhopperannouncedithadentered intoafarm-outagreementwithPremierOilplc(“Premier”),wherebyPremieracquireda60%operatedinterestinRockhopper’sNorthFalklandBasin licences for undiscounted consideration of c.$1bn(comprisingcash,developmentcarryandexplorationcarry).

InrecognitionofRockhopper’sunrivalledunderstandingoftheNorthFalklandBasin,itwasagreedthatRockhopperwouldretainthesub-surfaceleadinrelationtofutureexplorationactivities.

20122013

Consolidates interests in NFB acreage Rockhopper consolidates its interests in the Falklands through the farm-in to acreage held by Desire Petroleum.Asaresult,RockhopperincreasesitsinterestsinlicencesPL004a,PL004bandPL004cto24%.

3Report & Accounts for the year ended 31 December 2016

Rockhopper Exploration plc Strategic Report

3

>Continuedtoprogressthedevelopmentof thelargescaleSeaLionproject: > FEEDcontractsfortheSeaLionPhase1developmentawardedtoaset

ofworld-classcontractors > Independentresourceauditconfirmed517mmbbl(2C)and900mmbbl(3C)oilresources

(gross),andnear-field,low-riskexplorationupsideof207mmbbl(gross,midcase,unrisked) > UpdateddraftFieldDevelopmentPlananddraftEnvironmentalImpact

StatementsubmittedtoFalklandIslandsGovernment>Protectingfinancialstrengthtoenablegrowth: > Debt-free and fully funded for current commitments > StrongbalancesheetmaintainedwithcashandtermdepositsofUS$81million

(at 31 December 2016) > GeneralandAdministrativecostsexpectedtobelargelycoveredbyexistingproduction

goingforward > Initiatedinternationalarbitrationtoseeksignificantmonetarydamages

in relation to Ombrina Mare

2015

NFB exploration campaign commences In March, the Eirik Raude rig arrives in the North FalklandBasintocommenceamulti-welldrillingcampaign.ExplorationsuccessesatZebedeeandIsobelDeepwithmultipleoildiscoveriesmade.

In November, Rockhopper announced the terms ofitsall-sharemergerwithFalklandOil&Gas.ThroughthemergerwithFOGL,Rockhopperconsolidates its leading acreage and resource position intheNorthFalklandBasin.

Sea Lion DiscoveryInFebruary,theOceanGuardiandrillingrigarrivedinFalklandswaterstocarryoutamulti-wellprogrammeonbehalfofmultipleoperators.Inthespring,Rockhopper(asoperator)drilleditsfirstexplorationwellontheSeaLionprospectwhichresultedinanoildiscovery.ThewellwassuccessfullyflowtestedinSeptember.

2010

Sea Lion AppraisalFollowingthesuccessfulflowtestinlate2010afurthereightexplorationandappraisalwellsweredrilled by Rockhopper across the complex, six of thosebeingdiscoveries.

In addition, Rockhopper participated inafurtherfivenon-operatedwells.

2011

2014

Acquisition of MOG In May, Rockhopper announced a recommended cashandshareoffertoacquireAIMlistedMediterraneanOil&Gasplc.ThetransactioncompletedinAugust.ThroughtheacquisitionRockhopperacquiredaportfolioofproduction,development, appraisal and exploration interests in Italy,MaltaandFrance.

4 Report & Accounts for the year ended 31 December 2016

Rockhopper Exploration plcStrategic Report

Rockhopper at a glance

*Operator’sestimate

† SeaLionPhase2straddleslicencesPL032inwhich Rockhopperholdsa40%interestandPL004in whichRockhopperholdsa64%interest.

North Falkland Basin

SeaLionPhase1(PL032)> 40%workinginterest> 220 mmbbls gross*

88 mmbbls net to Rockhopper*

> Targeting FID in mid 2018, subjecttosecuringfunding

SeaLionPhase2(PL032/PL004)> 40-64%workinginterest†> 300 mmbbls gross*

120-192 mmbbls net to Rockhopper*

Phase3–Isobel-Elaine(PL004)> 64%workinginterest> Isobel-Elaine complex

significantlyde-risked during recent NFB exploration campaign

Head OfficeLondon, UK

Regional OfficesRome, Italy Cairo, Egypt

Jayne East

Chatham

Beverley East

Elaine South

Elaine North

Doreen

Lydia

EmilyIsobel

Isobel Deep

Irene

_

M

M MM

M]

L

_

L

_

_

W

LZebedee:14/15b-5

Chatham: 14/10-10

14/15-2

14/15-3

14/10-8

14/10-1 14/10-614/10-214/10-514/10-4

14/10-7

14/10-3

14/15-1, 1Z

14/15-4, 4Z

14/10-9, 9Z

0 10

Kilometers

PL03a

PL01 PL032 PL033

PL04b

PL04c

PL04a

Isobel

120m

100m

80m

60m

40m

20m

0m

Phase 1

Phase 2

Phase 3

Isobel-ElaineComplex

Sea LionComplex

Falkland Islands

5Report & Accounts for the year ended 31 December 2016

Rockhopper Exploration plc Strategic Report

ITALY

0 300

Kilometers

TUNISIA

LIBYA

EGYPT

TURKEYGREECE

Exploration

Production

Discovery

Block 9

Guendalina

Monte Grosso

Block 9

Ombrina Mare

Guendalina

Monte Grosso

Civita

GuendalinaAbu SennanGuendalinaEl Qa’a Plain

0 100 200

Kilometers

M e d i t e r r a n e a n S e a

R e dS e a

ABUSENNAN

EL QA’APLAIN

Cairo Suez

E G Y P T

GuendalinaEl Qa’a Plain

GPT

GPT SW

GPY

Abu El GharadigWestern Desert 33

Abu El Gharadig NE

BW1

Abo Senan

Sheiba 181Badr El Din 11

Abu SennanAbu SennanAbu Sennan

Badr El Din 01

Abu Sennan

Badr El Din 04

WesternDesert 33/15

Al Jahraa-1 GPZZ-1

GPZZ

ASA-1X

El Salmiya-1

Al Ahmadi-1X

ASH-1X

!(

!(

!(

!(

!(

!

Oil wellAbu Sennan LicenceProduction leaseSeismic areaOil �eldGas �eld

Al Jahraa SE-1X

!

0 5 10

Kilometers

GPY

AsaAl Jahraa Al Ahamadi

Ash

El SalmiyaAl Jahraa SE

ItalyGuendalina> 20%workinginterest> Northern Adriatic production

Ombrina Mare> 100%workinginterest> International arbitration

commenced

Civita> 100%workinginterest> Onshore gas production

MonteGrosso> 23%workinginterest> Exploration stage

EgyptAbu Sennan> 22%workinginterest> Western Desert production

CroatiaBlock 9 > 40%workinginterest> Blockawardedin2015–

subjecttosignatureof PSA

Greater Mediterranean

6 Report & Accounts for the year ended 31 December 2016

Rockhopper Exploration plcStrategic Report

Vision

Tobuildawell-funded,full-cycle,exploration-ledE&Pcompany

> Building a balanced portfolio in core areas>FocusonNorthFalklandBasinandGreater

Mediterranean > Across the full asset life cycle>Productionbasetoenablegrowththrough

exploration> Maintaining balance sheet strength

> Prudent balance sheet management> Partial monetisation of assets to fund development> Disciplined approach to cost management

> Value accretive exploration>Leveragingtechnicalskillset> Focus on proven hydrocarbon basins> Managed exposure to high-impact opportunities

4 Acquisition and integration of exploration and production assets in Egypt

4 Material increase in economic production* to 1,350 boepd

4 Year-end cash and term deposits $81 million; no debt

4 Reduced recurring G&A by 30% over last two years

4 Independent resources audit confirmed 517 mmbbl (2C) in Sea Lion Complex with 207 mmbbl of near-field exploration upside

*Economicproductionincludesproductionfromtheeffectivedate (being1January2016)oftheacquisitionofassetsinEgypt.

Delivering on strategy

StrategyStrategic aim Delivery in 2016

Economic production(boepd)

272

2014

322

2015

1,350

2016

Revenue(US$m)

1.9

2014

4.0

2015

7.4

2016

Net assets(US$m)

255

2014

262

2015

427

2016

Gross Sea LionComplex resources(mmbbl)

386

March2012

2C

560

3C

517

2C

900

3C

April2016

7Report & Accounts for the year ended 31 December 2016

Rockhopper Exploration plc Strategic Report

Business model

> Proven basins> High impact> Managed exposure

> Right-sized to fund exploration

> Self-funded through operating cash flows or partial monetisation

Exploration >

<Developmen

t<Production

Creatingvalue

8 Report & Accounts for the year ended 31 December 2016

Rockhopper Exploration plcStrategic Report

Chairman and Chief Executive Officer’s Review

Left: David McManusChairmanRight: Samuel MoodyChief Executive Officer

Rockhopper’s strategy is to build a well-funded, full-cycle, exploration-led E&P company.

In 2016, Rockhopper delivered on a number of operational,corporateandstrategicobjectives:completinga highly successful exploration campaign in the Falklands, progressingtheCompany’sflag-shipSeaLiondevelopmentintoFEED,whilstatthesametimeaddingmaterialincrementalproductionintheGreaterMediterranean.

Ourbalancesheetremainsstrongwithnodebt,whichensureswearewellplacedtotakeadvantageoftheopportunitiescreatedbythechallengingcommoditypriceenvironment.

In the Falkland Islands, we have grown our resource position substantially through exploration and acquisitionInJanuary2016,wecompletedthemergerwithFalklandOil&GasLimited.TheBoardbelievesthecombinationofRockhopperandFOGLwillcreatesignificantvaluefor shareholders, not only by positioning Rockhopper as the largest acreage holder in the North Falkland Basin, butourenhancedinterestsprovideuswithastrongerstrategic position in the future commercialisation of our world-classSeaLionproject.

InFebruary2016,weconcludedourhighlysuccessfulNorth Falkland Basin exploration drilling campaign, whichsawmaterialoildiscoveriesateachofZebedee,IsobelDeepandIsobelElaine.

Followingtheconclusionoftheexplorationcampaign,ERCEquipoiseLimited(“ERCE”)wereappointedtoconduct an independent audit of resources in the North FalklandBasin.FurtherdetailsareoutlinedintheChief

OperatingOfficer’sReviewbuttheBoardwasparticularlypleasedtoseetheauditconfirmoilinplaceontheSeaLionComplexisestimatedatmorethan1.6billionbarrelsgrosswithestimatedgrossrecoverablecontingentoilresourcesof517mmbbls(2C)and900mmbbls(3C).

The impressive results of this campaign and the subsequentindependentresourceauditendorseRockhopper’sviewthattheNorthFalklandBasinhasthepotential to deliver multiple future phases of development and,ultimately,abillionbarrelsofrecoverableoil.

Continued cost optimisation materially reduces project break-even cost at Sea LionInJanuary2016,theSeaLionPhase1projectenteredFEEDwithasetofworld-classcontractors.ThePhase1development aims to commercialise the resources in the northoftheSeaLionComplexinlicencePL032.

Thelatestestimatesofcapextofirstoilare US$1.5billionwhich,combinedwithothercostandefficiencyimprovements,hasresultedinalife-of-fieldcost(capex,opexandlease)ofapproximatelyUS$35perbarrel.Theproject“break-even”oilpriceisapproximatelyUS$45perbarrel(withbreak-eveneconomicspremisedonachievinganungearedprojectIRRof10%).

A draft Environmental Impact Statement and revised draftFieldDevelopmentPlanweresubmittedtotheFalklandIslandsGovernment(“FIG”)inlate2016.

Rockhopper is an engaged and active participant in the SeaLionjointventureprovidingsupportandchallengetoPremierOilplc(“Premier”)acrosstherangeofsubsurface,engineering,commercialandfinancingaspectsoftheproject.

9Report & Accounts for the year ended 31 December 2016

Rockhopper Exploration plc Strategic Report

Having operated in the Falklands for over 12 years wehaveunparalleledinsightsandbringthesetobear aswemovetheprojecttowardssanction.

InSeptember2016,theBoardnotedwithinterestthejointstatementbetweentheBritishGovernmentandtheGovernmentofArgentinainrelationtoclosercooperationonareasofmutualinterest.ThisannouncementisbelievedtobethefirstpositivestatementmadebybothcountriesonSouth Atlantic issues since 1999 and sets out a commitment toworktowardsremovingrestrictivemeasuresaffectingtheoilandgasandotherindustriesintheFalklandIslands.

Building a second core area in the Greater MediterraneanInourGreaterMediterraneanportfolio,wehavebenefittedfromamaterialincreaseinproductionfollowingthecompletionofthesuccessfulGuendalinaside-trackandthe Rockhopper operated Civita development in H2 2015.Productionfurtherincreasedin2016followingtheacquisitionofaportfolioofinterestsinEgypt.Economicproduction*in2016averaged1,350boepd.

FollowingthedecisioninFebruary2016bytheMinistryofEconomicDevelopmentnottoawardtheCompanyaProductionConcessioncoveringtheOmbrinaMarefield,in March 2017 the Company commenced international arbitrationproceedingsagainsttheRepublicofItaly.Basedon legal and other expert opinions, Rockhopper has been advised that it has strong prospects of recovering very significantmonetarydamagesasaresultoftheRepublicofItaly’sbreachesoftheEnergyCharterTreaty.Damageswouldbesoughtonthebasisoflostprofits,withthearbitrationprocessexpectedtotake2-3years.

Portfolio management and corporate cost reduction initiativesOver the last 24 months a corporate cost reduction programhasbeenimplementedacrosstheGroup–asaresult, headcount in Italy has reduced to eight (a reduction ofovertwo-thirdssincetheacquisitionofMediterraneanOil&GasplcinAugust2014).InitiativestostreamlinetheGroup’sUKoperationshavebeenachievedbycombiningourLondonandSalisburystaffinasingleofficeinLondon.Asaresult,theGroup’snetrecurringgeneralandadministrative(“G&A”)costin2016 hasreducedtoUS$7.4million(comparedwith US$9.4millionin2015andUS$10.8millionin2014†) – furtherG&Asavingsareanticipatedin2017.

Board changesFollowingtheCompany’sAGMinMay,DrPierreJungelsretiredasNon-executiveChairmanhaving servedasChairmanoftheCompanyforover10years.David McManus, an existing Non-executive Director, wasappointedNon-ExecutiveChairmanfollowingPierre’sretirement.WepaytributetoPierre’sachievementsoverthattimeandofferoursincere thanksfortheleadershipprovided.

In addition, Robert (Bob) Peters, Senior Independent Director,retiredfromtheBoardeffective31December2016.WethankBobforhissignificantcontributionandinputtoBoarddeliberationsoverhissixyearswiththeCompany.KeithLough,Non-executiveDirectorandChairmanoftheAuditandRiskCommittee,wasappointedSeniorIndependentDirectorfollowingBobPeters’retirement.

OutlookAsthetechnicalengineeringphaseoftheSeaLionFEEDapproachesconclusion,focuswillshiftin2017tothecommercial,fiscalandfinancingelementsoftheproject.EngagementwithFIGonarangeofoperational,fiscaland regulatory matters is expected to continue through H12017.

WiththespotpriceforBrentcrudefluctuatingaround$55perbarrelinearly2017,andthecostefficienciesrealised through the FEED process, the Board is convincedtheeconomicsoftheSeaLionprojectaresufficientlyrobusttobesanctionedinthecurrentenvironment,assumingtherequiredcapitalinvestmentcanbesecured.

Withthatinmind,Premier,Rockhopper’spartnerintheSeaLionproject,hasconfirmedthat,giventheirfinancingposition,anyfinalinvestmentdecisionon SeaLionwillbesubjecttothesuccessfulconclusion ofafarm-downoralternativefinancingprocess.

GiventheimportanceoftheSeaLionprojecttoRockhopperandourshareholders,wearededicatedto investigating every possible means to progress the development,includingassistingPremierintheirfinancingefforts,activelyengagingwithanumberofoilindustryparticipantswithregardtopotentialfarm-intransactionsandanumberofinitiativestofurtherreducethepre-firstoilcapitalrequiredtosanctiontheproject.WebelievethecompletionofthePremier’srefinancingwillsignificantlyenhance the discussions around the funding and resulting sanctionoftheSeaLiondevelopment.

AsaresultoftheacquisitionofBeachEgypt,combinedwithcorporatecostsavingsachievedthroughtheyear,operatingcashflowsareexpectedtobroadlycovertheGroup’soverheadsduring2017.TheBoardbelievesthatthisproductionandcashflow,whencombinedwithourexistingbalance sheet, helps secure the long-term sustainability of theCompanywhilstpreservingflexibilitytofurthergrowourGreaterMediterraneanbusinessin2017.

David McManus Samuel MoodyNon-ExecutiveChairman ChiefExecutiveOfficer

10 April 2017

* Economic production includes production fromtheeffectivedate(being1January2016)oftheacquisitionofBeachEgypt.

† Based on audited results for the nine month period to 31 December 2014, pro-rated for a fullyear.

10 Report & Accounts for the year ended 31 December 2016

Rockhopper Exploration plcStrategic Report

BringinganadditionalpayingpartnerintotheSeaLionDevelopmentprojectand/orworkingcloselywiththeoperatortodeliverafinancingsolutiontoenablethejointventuretoadvanceprojectsanction.

Additionof amaterialnewventurethataddssubstantialproductionandmeetstheCompany’scorporateinvestmentcriteria.

Preservationof theCompany’scashposition.

Definition

Key Performance Indicators (KPIs)

Bringing an additional paying partner intotheSeaLiondevelopmentproject.

Completionof aCompetentPerson’sReportthatmeetsspecificobjectivessetbytheBoard.

Achievementof specificmilestonesfortheFinalInvestmentDecisionfortheSeaLiondevelopment.

Discussionsheldwitharangeof potentialcapital providers to establish appetite to investintheSeaLionproject.

Independent resource audit prepared by ERCEquipoiseannouncedinMay2016.AuditconfirmedSeaLionComplex2Cresources of 517 mmbbl and 3C resources of 900mmbbl.

ProjectenteredFEEDwithasetof worldclasscontractors.

Draft Field Development Plan prepared andsubmittedtotheFIG.

Significantcostsavingsachievedandprojectbreak-evenoilpricereducedto$45perbarrel.

Definition Performance Attainment

TheBoardmonitorstheCompany’sprogressagainst its Key Performance Indicators to assess performance anddeliveryagainstpre-definedstrategicobjectives.

KPIs have been set based on short-term targets designed toensuretheCompanyachievesitslong-termstrategy.

The Company measures a number of operational and financialmetricstoascertainperformance.In2016,Rockhopper continued to deliver on a number of its keymetrics.

Not achieved

Fully achieved

Partially achieved

Achievementof productionrelatedtargets.

Partially achieved

Economic production of 1,350 boepd achieved during 2016, a material increase over2015levels.

2016

2017

KPI #1

KPI #1

KPI #2

KPI #3

KPI #2

KPI #3

KPI #4

11Report & Accounts for the year ended 31 December 2016

Rockhopper Exploration plc Strategic Report

Market overview

Economic and political>Significantpoliticalandeconomicuncertainty

through 2016 as a result of: –UKdecisiontoleavetheEuropeanUnion –USPresidentialelection – Eurozone instability>SterlingweaknessandinterestratecutfollowingBrexit>InEurope,continuedeasingofmonetarypolicywithafocusonquantitativeeasing

>Incontrast,theUScontinuestoexperienceGDPrecovery and declining unemployment leading to increasedconfidenceandinterestraterises.

Equity market>StrongUKequitymarketperformanceacrossFTSE

100 and 250>HighvolatilityfollowingBrexitdecisioninJunewithrecoverydriveninlargepartbySterlingweakness andlarge-capexposuretoUSearnings

>WhilsttheFTSE350Oil&Gassectoroutperformedthewidermarket,investorappetiteforsmallandmid–capE&Premainsmuted.

Oil price>SignificantrecoveryinBrentoilpricesthroughtheyear>January2016sawlowsofbelow$30perbarreldriven

by oversupply concerns and demand uncertainty>OPECandnonOPECsupplycutsinH2,thefirstinmanyyears,sawBrentre-rateabove$50perbarrel

>Thebalanceofdemandandsupplygoingforwardremainsuncertainwithmanycontributingfactors– ontheonehanddemandgrowthin2017looksstrong(driven by China and the Far East) on the other, sustainableUSshaleproductiongrowthcouldcap prices in the medium term

>Consensusforecastsfor2017/18generallysitinthe $50-60perbarrelrange.

Industry dynamics >Earlysignsofstabilityinoilpricesnotyetsufficienttoturnaroundfocusoncostreductionsandprojectdeferrals

>Costreductionsachievedthrough“across-the-sector”price cuts – leading to service sector consolidation and in somecasesfinancialrestructuringorinsolvency

> Next phase of cost reductions likely to be driven byefficienciesofdesignandengineering,industrystandardisation and co-operation around shared infrastructure

>Industrywillcontinuetofocusoncapitalallocationwithcapitalemployedonlyonthoseprojectswhichdeliverthemostcompetitiveriskadjustedreturns.

Mergers and acquisitions>OutsideofNorthAmericamergersandacquisition

activity remained relatively subdued>AssetrecyclingremainsmajorthemewithOilMajorsseekingtoreleasecapitalfromlegacy/mature/lowgrowth/lowreturnprojects

> Industry farm-out market limited to select geographic “hot-spots”

>SuperMajorsincreasingfocusongas–BP/Senegal;Shell/BG;ExxonMobil/Mozambique.

Liquids demand

Source: BP 2007 Energy Outlook

2010 2015 2020 2025 2030 2035

Power

Buildings

Industry

Ships, trains & planes

Trucks (inc SUVs)

Transport

Cars (inc. two-wheelers& other light duty vehicles

Non-combusted

20052000

20

0

40

60

80

100

120

Mb/dTechnology-driven supplies

Source: ExxonMobil Outlook for Energy 2040

MBDOE

0

5

10

15

20NGLs

‘10 ‘25 ‘40

Tight oil

‘10 ‘25 ‘40

Deepwater

‘10 ‘25 ‘40

Oil sands

‘10 ‘25 ‘40

Supply base, Falkland Islands

12 Report & Accounts for the year ended 31 December 2016

Rockhopper Exploration plcStrategic Report

Sea Lion FEED targets significant cost reductions 2016wasayearof intenseactivityfollowingthecommencement of Front End Engineering and Design (“FEED”)fortheSeaLionPhase1development.FEEDcontractswereawardedtoanalignedpartnershipof world-classcontractorscomprisingSBMOffshoreforthe FPSO, Subsea 7 for the subsea installation, National OilwellVarcofortheflexibleflowlinesandOneSubseaforthesubseaproductionsystem.Theinnovativecontractor partnership having been designed to create collaborativeengagementwithaviewtooptimisingthe facilities design and installation methodology and toreduceprojectcosts.Intandemengagementwithdrilling and logistics service providers is progressing, againwitharangeof innovativecommercialandcontractualarrangementsbeingdiscussed.

Thejointventureteamof PremierandRockhopperhaveworkedcollaborativelytosupportandchallengethedesignspecificationsthroughouttheFEEDprocess,leadingtosignificantsavingsacrosstheproject.

Additionally, support from Rockhopper has enabled arightsizingof theoperatorsprojectteamandasignificantreductionintheprojectmanagementcosts for2017.

Costestimatesforfieldsupportservices,including supply boats, helicopters and shuttle tankers have seen amaterialreduction.Asaresult,fieldoperatingcostsforSeaLionPhase1arenowestimatedat$15perbarrel,downfromover$20perbarrel,whilethetotalprojectbreakevencosthasreducedtojustbelow$45perbarrelfrom$55perbarrel.

Giventhemagnitudeof resourcesalreadydiscoveredin the North Falkland Basin, a phased approach todevelopmentisbeingpursued.Phase1willcommercialise approximately 220 mmbbls in the north of PL032(inwhichRockhopperhasa40%workinginterest).ThePhase2developmentwillcommercialisea further 300 mmbbls from the remaining resources in PL032andtheadjacentresourcesinPL004(inwhichRockhopperhasa64%workinginterest).Subjecttofurtherappraisaldrilling,Phase3willdeveloptheresources in the Isobel-Elaine Complex to the south of PL004.

AnapplicationwasmadetoFIGtoextendthelicencefortheSeaLionDiscoveryArea.FIGhasconfirmedthat an extension to April 2020 has been granted by the SecretaryofState.Additionally,extensionsarebeinggranted to all licences held in the North Falkland Basin byFIG.

Fiona MacAulayChief Operating Officer

Chief Operating Officer’s Review

13Report & Accounts for the year ended 31 December 2016

Rockhopper Exploration plc Strategic Report

Success of recent North Falkland Basin exploration campaign confirmed by independent resource auditInFebruary2016,weconcludedtheIsobelElainewell,thelastinourmulti-wellexplorationcampaignintheNorth Falkland Basin and continued our success in theroleof sub-surfaceleadforexploration,inwhichRockhopperhavehadunparalledsuccessinthebasin.

Followingthesuccessof theexplorationcampaign,ERCEwereappointedtoconductanindependentauditof the contingent and prospective resources in licences PL032andPL004whichwascompletedinApril2016.Asummaryof theresourceupdateisoutlinedbelow.

Sea Lion complexERCE audit > Discovered STOIIP 1,667MMstb, 834MMstb net

to RKH (Mid Case)> Discovered 2C resources 517MMstb oil, 258MMstb

net to RKH> Discovered 3C resources 900MMstb oil, 452MMstb

net to RKH> Total discovered 2C resources including gas

747MMboe, 392MMboe net to RKH> Total discovered 3C resources including gas 1,462MMboe,798MMboenettoRKH.

Upside>ERCEauditednearfieldlowriskexplorationupside

of 207MMstb, 105MMstb net to RKH (Mid Case, unrisked)

> Management estimates additional resource upside in WestFlankof 60MMstbif oil-bearing.

Isobel-Elaine complexERCE auditUtilisingtheoperationallycompromiseddatasuiteERCEauditedsignificantdiscoveredandprospectiveSTOIIP and resources in the Isobel-Elaine Complex of:> Discovered STOIIP 277MMstb oil, 177MMstb

net to RKH (Mid Case)> Discovered STOIIP 832MMstb oil, 532MMstb

net to RKH (High Case)> Discovered 2C resources for Isobel Deep (F3H Fan)

20MMstb oil, 13MMstb net to RKH> Prospective STOIIP 282MMstb oil, 180MMstb

net to RKH (Mid Case)

Management estimatesWithoutthebenefitof completedformationpressuredata, management has applied conservative recovery factorsof 25%and35%respectivelyfor2Cand3Cresources against audited STOIIP for each of the Emily, IsobelandIsobelDeep(J)fans:> Management 2C resources 49MMstb oil, 31MMstb

net to RKH> Management 3C resources 198MMstb oil, 127MMstbnettoRKH.

Management plus ERCE audited resources > 2C resources 69MMstb oil, 43MMstb net to RKH> 3C resources 270MMstb oil, 173MMstb net to RKH> Prospective (Mid Case) resources 70MMstb,

45MMstb net to RKH> Prospective (High Case) resources 350MMstb, 224MMstbnettoRKH.

Sea Lion development schematic

14 Report & Accounts for the year ended 31 December 2016

Rockhopper Exploration plcStrategic Report

_M

M MMM]

L

_

L

_

_

W

L

SL30

Sea Lion

Casper

CasperSouth East

CasperSouth West

BeverelyWest

BeverelyEast

Hector

Zebedee

Ninky South

Orca / Ann

Elaine SouthDoreen

Elaine North

Lydia

Isobel

Isobel Deep

Irene

Emily

Liz

Susan

Helen

ISOBEL 2

CHATHAM

ISOBEL DEEP

ZEBEDEE

CHATHAM

ISOBEL DEEPISOBEL 2

ZEBEDEE

Jayne East

Chatham

PL03b

PL01 PL032 PL033

PL04b

PL04c

PL04a

PL03a

PL05

10 Kms

Leading acreage position post acquisition of FOGL Rockhopper FOGL Combined Group Operator

PL032 40% n/a 40% Premier

PL003a 3% 92.5% 95.5% Rockhopper

PL003b 3% 57.5% 60.5% Rockhopper

PL004a 24% 40% 64% Premier

PL004b 24% 40% 64% Premier

PL004c 24% 40% 64% Premier

PL005 n/a 100% 100% Rockhopper

Source: xxxx

0 5 10 15 20

120

160

0

20

40

60

80

100

140Phase 2Phase 1

Aver

age

annu

al d

aily

oil

rate

(mbo

pd)

Years from first production

Projected production profile

North Falkland Basin snapshot

15Report & Accounts for the year ended 31 December 2016

Rockhopper Exploration plc Strategic Report

Duringthesecondhalfof2016,boththeAlJahraaSE-1XexplorationwellandtheASH-1XST2developmentwellswerebroughtontoproductionwithadditionalzonesinthewellstobebroughtintoproductionatalaterdate.

Anewdevelopmentleaseofc.30squarekmwasawardedaroundtheAlJahraaSE-1XwellwithEGPCattributing gross reserves of over 9 mmbbl to the development area, a material increase to the net 4.5mmbblof2P/2CacquiredinAugust2016.

The2017workprogrammeandbudgetforthe Abu Sennan Concession sees the drilling of both anexplorationandadevelopmentwellclosetothe AlJahraaandAlJahraaSEfieldsduringthefirst halfof2017.ThesewellsareaimedatimprovingthejointventurestechnicalunderstandingofAlJahraa SEaswellasmaintainingproductionlevels byoffsettingnaturaldeclinefromexistingwells withintheConcession.

TheRockhoppersub-surfaceteamhavebeenworkingcloselywiththeoperatorsincecompletion oftheacquisitiontobothprioritisethelargeprospectinventory and to better understand the reservoir managementofthefieldsalreadyonproduction.

Theexplorationwell,AlJahraa-SE2,whichisduetospudshortly,willtargettheAR-CreservoirinthefaultblockimmediatelytothesouthoftheAlJahraaSEfieldandwhichhasthepotentialtoincreasetheAlJahraaSEfieldareatotheupthrownsideofthatfault.

Oncompletionoftheexplorationwell,therigwillmovedirectlytoAlJahraa-9,whichisadevelopmentwell.ThisdevelopmentwelltargetstheAR-Creservoirat a location deeper than the current deepest oil penetrationatAlJahraa-4(nooilwatercontacthasyetbeenencounteredinthefield)therebyaimingtoproveadditionalreserves.ThewellalsoseekstodemonstratetheconnectionbetweentheAlJahraaandAlJahraaSEfieldsthroughtheoilleg.Inaddition,theoperatorhasproposedtwowork-overoperationsduringQ22017.

The outcome of operations in H1 2017 on the Abu SennanConcessionwilldeterminetheactivitiesduringthesecondhalf of theyear.

Inaddition,theCompanyexpectstoreceivefinalratificationfora5-yearextensiontotheAbuSennanexplorationlicenceinH12017.Onceapproved,theCompanywillundertaketoparticipateinatleasttwoexplorationwellsoverthenext3yearsatacommitment(nettoRockhopper’s22%workinginterest)of approximatelyUS$1.3million.

RockhopperwasdelightedthattheauditconfirmedtheCompany’snet2Coilcontingentresourcebaseinthe North Falkland Basin, as a result of the exploration campaignandtheacquisitionofFOGL,hadincreasedto over 270 million barrels, or over 300 million barrels including management estimates for the Emily, Isobel andIsobelDeepJfans.

IntheIsobel-ElaineComplex,wheredatacollectionwascompromisedforoperationalreasons,ERCEhasevaluated the discovered STOIIP for each of the fans and attributed contingent resources to the Isobel Deep (F3H) fanfromwhichsignificantoilwasrecoveredtosurface.For the other oil-bearing fans (Emily, Isobel and Isobel DeepJ),ERCEbelievesthatrecoveryfactorscomparableto those applied to discoveries could be achieved if an appraisalprogrammedemonstratesthepotentialtoflowoilataratecomparabletowellsintheseoffsetdiscoveries.Forthesefans,managementhasassigneda25%recoveryfactorforthe2Cand35%forthe3Cresources.

In addition to the discovered resources, management believestherearealargenumberofnearfieldprospectsintheattractiveandrelativelylowriskIsobel/ElaineappraisalareaforwhichestimatesofSTOIIPandoilprospectiveresourceshavebeenmade.

South and East Falkland BasinThroughtheacquisitionofFOGL,Rockhopperacquireda52%interestinNobleoperatedacreagetotheSouthandEastoftheFalklandIslands.FollowingtheresultsoftheHumpbackwell,NobleEnergyandEdisonhavegivennoticetowithdrawfromthisacreage(althoughretainaninterestinPL001intheNorthFalklandBasin).Asaresult,Rockhopperexpects to become operator of the South and East FalklandBasinacreagewitha100%workinginterestwhentheprocessofassignmentiscomplete.SelectivetechnicalworkbytheRockhoppersub-surfaceteamwillcontinuetoestablishtheremainingprospectivityontheacreageandadecisiononwhethertoextendthecurrentphaseofthelicenceswillthenbemade.

Step-change in production in Greater Mediterranean following acquisition in EgyptRockhopper is focused on building a second core area intheGreaterMediterraneanregionfollowingitsacquisitionofMediterraneanOil&Gasplcin2014.

InAugust2016,RockhoppercompletedtheacquisitionofBeachPetroleum(Egypt)PtyLimited(“BeachEgypt”),asaresultacquiringa22%interestinthe AbuSennanconcessionanda25%interestinthe ElQa’aPlainconcession.

Abu Sennan, Egypt (Rockhopper 22%)OperatedbyKuwaitEnergy,theAbuSennanConcessionislocatedintheAbuGharadigbasinin theWesternDesert.TheConcessionwassignedin June2007withfirstcommercialproductionachievedduring2012.

16 Report & Accounts for the year ended 31 December 2016

Rockhopper Exploration plcStrategic Report

Civita

Adriatic Sea

Campobasso

ITALY

0 50

Kilometres

ItalyCivita

> 100%workinginterest

> Onshore gas production

> 2016 production 130 boepd

Guendalina

Adriatic Sea

Rimini

ITALY

CROATIA

0 50

Kilometres

Italy Guendalinia

> 20%workinginterest

> Northern Adriatic> 2016 production

410 boepd

Cairo

Abu Sennan

Mediterranean Sea

EGYPT0 200

Kilometres

Monte Grosso

Adriatic Sea

Taranto

Tyrrhenian Sea

ITALY

0 100

Kilometres

Bari

Egypt Abu Sennan

> 22%workinginterest

> Western Desert> 2016 economic

production 810 boepd

Italy MonteGrosso

> 23%workinginterest

> ~250 mmbbl oil prospect

> 23%chance of success

Ombrina Mare

Adriatic Sea

Pescara

ITALY

0 50

Kilometres

Block 9

Adriatic Sea

ITALY

CROATIA

0 100

Kilometres

Italy Ombrina Mare

> 100%workinginterest

> International arbitration commenced

CroatiaBlock 9

> 40%workinginterest

> Blockawardedin2015–subjecttosignature of PSA

Greater Mediterranean snapshot

17Report & Accounts for the year ended 31 December 2016

Rockhopper Exploration plc Strategic Report

Guendalina, Italy (Rockhopper 20%)OperatedbyEni,theGuendalinagasfield,locatedin the Northern Adriatic, has been in production since October2011.

Guendalinahascontinuedtoproducetoforecast during 2016 and production over the year averaged 68,000 scm per day net to Rockhopper ( approximately 410boeperday).Plantavailabilityovertheyearhasbeencloseto100%andproductionfromthesidetrackwell in 2015 continues to make a material contribution to fieldproduction.

TheRockhopperteamhaveworkedcloselywiththeoperatortolookatmoreefficientandcosteffectivemethodologiesofproducedwaterdisposalwhichshouldhaveasignificantreductiononfieldopexgoingforward.

Civita, Italy (Rockhopper 100%)OperatedbyRockhopper,theCivitagasfieldlocatedonshore Abruzzo, came into production in November 2015.

During2016,productionfromthefieldaveragedapproximately 21,000 scm per day (approximately 130boeperday).GascompressionwassuccessfullycommissionedatthesiteinDecember2016.

Ombrina Mare, Italy (Rockhopper 100%)FollowingthedecisioninFebruary2016bytheMinistryof EconomicDevelopmentnottoawardtheCompanya Production Concession covering the Ombrina Mare field,adecisionwasmadetoplugandabandon(“P&A”)theexistingOM-2wellandremovethetri-podstructurewhichhadbeenconstructedin2008andatthattimeintended to form part of the future production facilities onthefield.TheP&AoperationwassuccessfullycompletedwithoutincidentinearlyAugust2016usingtheAttwoodBeaconrig,takingadvantageof depressedrigrates.Thedecommissioningandremovalof the tri-pod structure is anticipated to take place during H22017andafixedpricecontractforthisworkhasbeenawarded.

Monte Grosso, Italy (Rockhopper 23%)OperatedbyEni,theSerraSanBernadopermitwhichcontainstheMonteGrossooilprospectislocatedintheSouthernApenninethrust-foldbeltontrendwithValD’AgriandTempaRossa,inthelargestonshoreoilproductionanddevelopmentareainWesternEurope.MonteGrossoremainsoneof thelargestundrilledprospectsonshoreWesternEurope.

Rockhopper transferred the operatorship of the Serra SanBernadopermittoEniduring2016.Itishopedthatthetransferof operatorshipwillacceleratetheregulatoryandpermittingprocesstoenabledrilling.

El Qa’a Plain, Egypt (Rockhopper 25%)OperatedbyDanaPetroleum,theElQa’aPlainconcessionislocatedontheeasternshoreof theGulf of Suezandcontainsanumberof oilleadsidentifiedonexisting2Dseismicdata.TheconcessionwassignedinJanuary2014.Approximately470sqkmof 3Dseismicplus35kmof 2Dseismicwasacquiredinearly2016andiscurrentlybeingprocessed.Thedrillingof anexplorationcommitmentwellisplannedinlate2017/early2018.

Area 3, Malta (Rockhopper 40%)InlinewithRockhopper’shighlyselectiveapproachtonewexplorationventuresandfollowingcompletionof seismicandgeologicalevaluationwork,theCompanyhas given notice to the operator and the Maltese regulator that it does not intend to participate in any extension of the current term of the Area 3 Exploration StudyAgreementwhichexpiredinDecember2016.

Block 9, Croatia (Rockhopper 40%)InJanuary2015,Rockhopperwasawardeda40%interestinoffshoreBlock9inCroatiainpartnershipwithEni(60%interestandoperator).Theawardwasmadesubjecttotheexecutionof aProductionSharingAgreement(“PSA”)withtheCroatianHydrocarbonAuthority(“CHA”).GiventhegeneralelectionsinCroatia in November 2015 and September 2016, significantdelayshavebeenexperiencedinthesigningof aPSAwiththeCHA.Rockhopperisindiscussionswith theCHAtounderstandthestatusof theBlockawardandoptionsgoingforward.

Fiona MacAulay Chief OperatingOfficer

10 April 2017

Rockhopper operated Civita production site

18 Report & Accounts for the year ended 31 December 2016

Rockhopper Exploration plcStrategic Report

OverviewDuring 2016, Rockhopper continued to allocate capital primarilytoitsworld-classassetsintheNorthFalklandBasinwhilstatthesametimeactivelypursuingvalue-accretiveacquisitionstomeetourstrategicobjectives.Rockhopperretainsitsrobustfinancialpositiondespitethelowoilandgaspriceenvironmentexperiencedthroughmuchof 2016.

IntheNorthFalklandBasin,wehavegrownourassetbasethroughthemergerwithFalklandOil&GasLimited(“FOGL”)andthroughexplorationdrillingontheIsobel-Elainecomplex.

Asin2015,wehaveseenastepchangeinproductionandrevenuescomparedwiththepreviousyear,primarilyasaresultoftheacquisitionofaportfolioofassetsinEgypt.

Ourbalancesheetremainsstrongwithyear-endcashandtermdepositsof US$81million.

Results summary 9 months $m (unless otherwise specified) FY2016 FY2015 2014

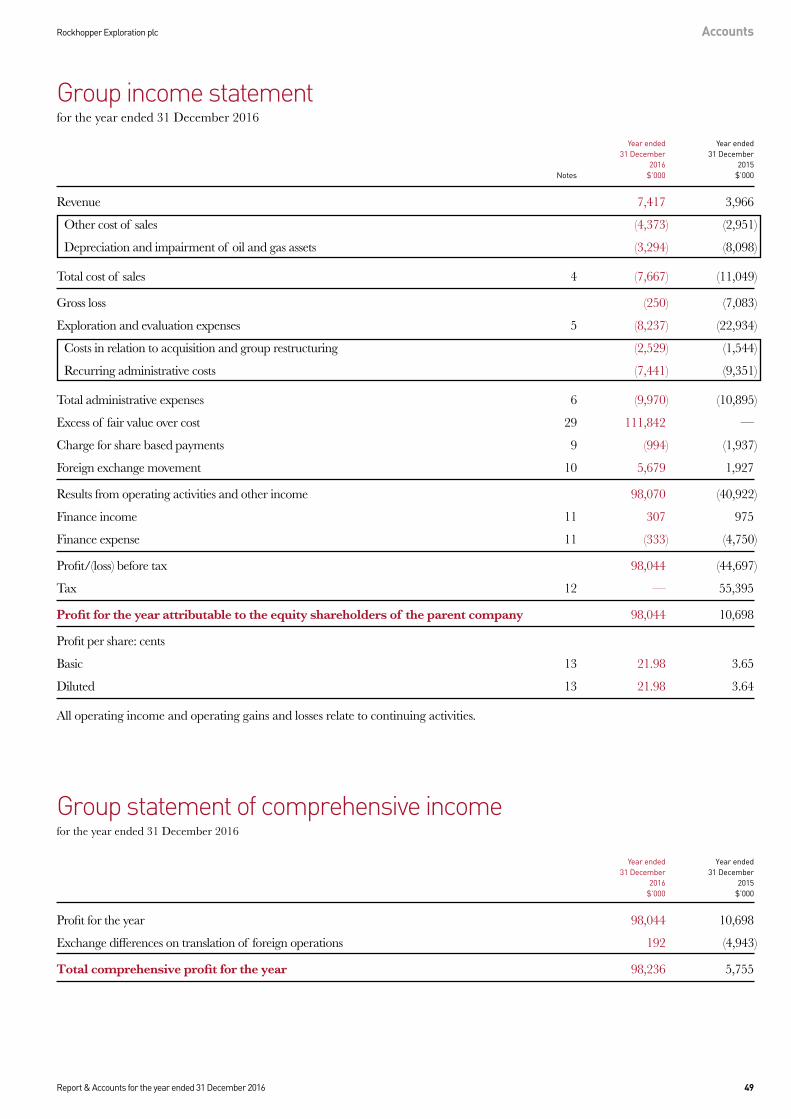

Economic production* (boepd) 1,350 322 272Revenue 7 4 2Profitaftertax 98 11 (8)Cashflowfromoperatingactivities (21) (7) (11)Cash 81 110 200Net assets 427 262 255

Results for the periodFor the year ended 31 December 2016, the Company reportedrevenuesofUS$7.4millionandaprofitaftertaxofUS$98million.Theprofitaftertaxintheyeararoseprimarily due to the excess of fair value over consideration

associatedwiththeacquisitionofFOGL.Excludingthe impact of the excess fair value over consideration associatedwiththeFOGLacquisitionwouldhaveresultedinalossaftertaxintheyearofUS$14million.

RevenueTheGroup’srevenuesofUS$7.4million(2015: $4.0million)duringtheyearrelateentirelytothesaleofoilandnaturalgasintheGreaterMediterranean(EgyptandItaly).Theincreaseinrevenuesfromthecomparableyearreflects:(i)theacquisitionofproductionassetsinEgypt,whichcompletedinAugust2016;and(ii)theincreaseinrealisedoilandgasprices.

Working interest economic production* averaged 1,350 boepd in 2016, a more than trebling of production fromtheprioryear(2015:322boepd).

Duringtheyear,theGroup’sgasproductioninItalywassoldundershort-termcontractwithanaveragerealisedpriceof€0.15perstandardcubicmetre(scm),equivalenttoUS$4.85perthousandstandardcubicfeet(“mscf”).GasissoldatapricelinkedtotheItalian“PSV”(VirtualExchangePoint)gasmarkerprice.

InEgypt,alloftheGroup’soilandgasproductionissoldtotheEgyptianGeneralPetroleumCompany(“EGPC”).TheaveragerealisedpriceforoilwasUS$46.2perbarrel,a small discount to the average Brent price over the same period.GasissoldatafixedpriceofUS$2.65permmbtu.

Operating costsCash operating costs, excluding depreciation and impairmentcharges,amountedtoUS$4.4million(2015:US$3.0million).Theincreaseinunderlyingcash operating costs is principally due to the addition ofEgyptianproduction.CashoperatingcostsonaperbarrelofoilequivalentbasisreducedfromUS$25.5perboein2015toUS$14.4perboein2016.

TheGroup’sgeneralandadministrative(“G&A”)cost,excludingnon-recurringexpensesrelatedtoacquisitionsand group restructuring, reduced further in 2016 to US$7.4million(2015:US$9.4million)–furtherG&Asavingsareanticipatedin2017.

Impairment of oil and gas assetsRockhopper has tested the carrying value of our assets forimpairment.Carryingvaluesarecomparedtothevalueinuseoftheassetsbasedondiscountedcashflowmodels.FuturecashflowswereestimatedusinganoilpriceassumptionequaltotheBrentforwardcurveduringtheperiod2017to2019,withalong-termpriceofUS$75/bbl(in“real”terms)thereafter.Apost-taxnominaldiscountrateof12.5%wasusedfortheGroup’sFalklandIslandassets.

Chief Financial Officer’s Review

Stewart MacDonaldChief Financial Officer

19Report & Accounts for the year ended 31 December 2016

Rockhopper Exploration plc Strategic Report

19

WithnocashflowgenerationexpectedfromSeaLionuntil2020attheearliest,theimpactoftheBrentforwardcurve during the period 2017 to 2019 on the fair value calculationislimited.Assuch,noimpairmentarisesontheSeaLionproject.Arangeofsensitivitieshavebeenconsideredaspartoftheimpairmenttestingprocess.Evenintheeventofa$20perbarrelreductioninitslong-termoilprice,noimpairmentonSeaLionarises.Equally,noimpairmentwouldariseeveniftheCompanyassumedprojectsanctionwasdelayedby10years.

Cash movements and capital expenditureAt 31 December 2016, the Company had cash resourcesof US$81.0million(31December2015:US$110.4million)andnodebt.

Cash and term deposit movements during the period: US$m

Opening cash balance (31 December 2015) 110Revenue 7Cost of sales (4)Falkland Islands (net of insurance proceeds) 7GreaterMediterranean (4)Recurring administration (7)Acquisitionofsubsidiaries(FOGLandBeachEgypt) (14)Other (14)Closing cash balance (31 December 2016) 81

TherewasanetinflowfortheFalklandIslandsin2016ofUS$7milliondueto(i)insuranceproceedsexceedingoutflowsthatprimarilyrelateto the2015/16drillingcampaign,aswellas(ii)spendrelating to the pre-development activities on Sea Lion.Foravarietyofreasons,thecostsofdrillingtheZebedee,IsobelDeepandIsobel-Elainewellswerehigherthanoriginallyanticipated.Certaincostsincurred during the North Falkland Basin exploration campaignwerethesubjectofaninsuranceclaimwhichsettledinlate2016.Intotal,US$49millionofinsuranceproceedswerereceived,nettoRockhopper.

SpendonassetsintheGreaterMediterraneanlargelyrelatestoresidualcostsassociatedwiththeGuendalinaside-track and Civita development in H2 2015 and the plugging and abandonment of the Ombrina Mare-2 wellfollowingthedecisionearlierintheyearbytheMinistryofEconomicDevelopmentnottoawardthe Company a Production Concession covering theOmbrinaMarefield.Inadditiontherehasbeenexpenditure on the Abu Sennan production concession andElQa’aexplorationconcessioninEgypt.

Othercashoutflowsincludeforeignexchangelosses,movementsinworkingcapitalbalances,grouprestructuringcostsaswellasnonrecurringliabililitesacquiredaspartof theFOGLacquisition.

Lessthan15%oftheGroup’scashresourcesasatmidJune2016wereheldinSterlingandthereforetheimpactoftheweaknessinSterling:USdollarexchangeratesontheGroup’scashposition,followingtheUKreferendumdecisiontoleavetheEuropeanUnion,waslimited.

Mergers, acquisitions and disposalsThemergerwithFalklandOil&GasLimitedcompletedinJanuary2016.Throughthemergerof FOGL,RockhopperconsolidateditsleadingNorthFalklandBasinacreageposition.

Underthetermsofthemerger,shareholdersofFOGLreceived0.2993newRockhoppersharesforeachFOGLshareheld.

The transaction has been accounted for by the purchase methodofaccountingwithaneffectivedateof 18January2016beingthedateonwhichtheGroupgainedcontrolofFOGL.InformationinrespectoftheassetsandliabilitiesacquiredandthefairvalueallocationtotheFOGLassetsinaccordancewiththeprovisionsof“IFRS3–BusinessCombinations”hasbeendeterminedonafirmbasisasfollows:

Recognised values on acquisition

US$m

Intangibleexplorationandappraisalassets 170.0Property,plantandequipment 0.1Inventories 0.2Tradeandotherreceivables 21.0Tradeandotherpayables (19.2)Netidentifiableassetsandliabilities 172.0

ThefairvalueofthenetassetsacquiredwasUS$172.0millionresulting in an excess of fair value over consideration of US$111.8million,recordedasacreditintheincomestatement.

Thefairvalueofequityinstrumentshasbeendeterminedby reference to the closing share price on the trading day immediatelypriortothecompletionoftheacquisition.

In determining the fair value of the assets, the Directors acknowledgetheinherentsubjectivityandwiderangeofpossiblevaluesgiventheuniquenatureoftheFOGLassetsacquired,a lack of truely comparable transactions and the highly volatilecommoditypriceenvironmentatthetimeofacquisition.

The excess of fair value over consideration has arisen primarilyduetothefactthatthefinancialpositionofFOGLhaddeterioratedduetocostoverrunsattheHumpbackexplorationwellaswellasmergerterms beingagreedpriortotheIsobel-Elainewellresults, whichsubstantiallyde-riskedtheIsobel-Elainecomplex.

In April 2016, Rockhopper announced revised terms fortheacquisitionofBeachEgyptforcashconsiderationofUS$11.9million.TheacquisitionofBeachEgyptcompletedinAugust2016.

In September 2016, Rockhopper completed the sale of a package of non-core assets in Italy including interests in theMonteardoneandFornovodiTarofieldstoalocalcompanyfornominalconsideration.Asaresultofthistransaction,US$1.1millionofprovisionsrelatedtofutureabandonment and decommissioning have been removed fromthebalancesheet.

* Economic production includes production fromtheeffectivedate(being1January2016) oftheacquisitionofBeachEgypt.

20 Report & Accounts for the year ended 31 December 2016

Rockhopper Exploration plcStrategic Report

TaxationOnthe8April2015theGroupagreedbindingdocumentation(“TaxSettlementDeed”)withtheFalklandIslandsGovernmentinrelationtothetaxarisingfromtheGroup’sfarmouttoPremierOilplc.

TheTaxSettlementDeedconfirmsthequantumanddeferment of the outstanding tax liability and is made underExtraStatutoryConcession16.

As a result of the Tax Settlement Deed the outstanding taxliabilitywasconfirmedat£64.4millionandispayableontheearlierof:(i)thefirstroyaltypaymentdateonSeaLion;(ii)thedateofwhichRockhopperdisposesofallorasubstantialpartoftheCompany’sremaininglicenceinterestsintheNorthFalklandBasin;or(iii)achangeofcontrolofRockhopperExplorationplc.

DuetothemovementintheSterling:USdollarexchangerate,theoutstandingtaxliabilityinUSdollartermshasreducedtoUS$79million(31December2015: US$95million).

Theoutstandingtaxliabilityisclassifiedasnon-currentanddiscountedtoayearendvalueofUS$39million.

As the Company received the full Exploration Carry fromPremierduringthe2015/16NorthFalklandBasinexploration campaign, the Company is entitled under thetermsoftheTaxSettlementDeedtorequesttheoutstandingtaxliabilityisreducedby£4.7million.SucharequesthasbeenmadetoFIGalthoughnoadjustmentin the outstanding tax liability has yet been recorded as thisissubjecttoagreementwiththeFalklandIslands’CommissionerofTaxation.

Full details of the provisions and undertakings of the Tax SettlementDeedweredisclosedintheCompany’s2014AnnualReportbuttheseinclude“creditorprotection”provisions including undertakings not to declare dividends ormakedistributionswhilethetaxliabilityremainsoutstanding(inwholeorinpart).

Liquidity, counterparty risk and going concernThe Company monitors its cash position, cash forecasts andliquidityonaregularbasisandtakesaconservativeapproachtocashmanagementwithsurpluscashheldontermdepositswithanumberofmajorfinancialinstitutions.

FollowingtheCompany’sacquisitionofproductionandexploration assets in Egypt, the Company is exposed to potentialpaymentdelayfromEGPC,whichisanissuecommon to many upstream companies operating in the country.Asat31December2016,Rockhopper’sEGPCreceivable balance (net of amounts due to Beach Energy) was$4.2million.TheCompanymaintainsanactivedialoguewithEGPCandhasseenamaterialincreaseinmonthlypaymentsfollowingtheyear-end.PaymentsfromEGPCarereceivedinUSdollarsdirectlytobankaccountsheldintheUK.

The Directors have assessed that the cash balance held providestheCompanywithadequateheadroomoverforecastexpenditureforthefollowing12months–asaresult, the Directors have adopted the going concern basis ofaccountinginpreparingtheannualfinancialstatements.

Principal risks and uncertaintiesAdetailedreviewofthepotentialrisksanduncertaintieswhichcouldimpacttheCompanyareoutlinedelsewhereinthisStrategicReport.TheCompanyidentifieditsprincipal risks at the end of 2016 as being:

>sustainedlowoilprice; >jointventurepartneralignmentandfundingissues;bothofwhichcouldultimatelycreateadelaytotheSeaLionFinalInvestmentDecision.

OutlookOurbalancesheetremainsstrongwithyear-end2016cashof$81million.Adjustingtheyear-endcashpositionforRockhopper’scontributiontoanticipatedNorthFalkland Basin exploration campaign close out costs and thepreviouslyannouncedsettlementwithOceanRig,maintainsRockhopper’sadjustedyear-end2016cashbalanceinlinewiththeCompany’spreviousguidance of$60-65million.

FollowingthecompletionoftheacquisitionofBeachEgypt,revenuesfromourGreaterMediterraneanassetsareestimatedtobeinexcessofUS$10millionin2017(basedon current commodity prices, foreign exchange rates and productionprojections).

2017 development, exploration and abandonment spend isexpectedtobeapproximatelyUS$13million,ofwhichUS$8millionrelatestopre-developmentactivitiesonSeaLion,US$3milliontoexplorationanddevelopmentactivitiesinEgyptandUS$2milliontoabandonmentcosts.Theabandonmentspendprincipallyrelatestothedecommissioning and removal of the Ombrina Mare tripod–thecostofwhichRockhopperwillseektorecoverthrough the recently commenced international arbitration processthecostsofwhichwillbefundedonanon-recoursebasisfromaspecialistarbitrationfunder.

Rockhopperhasbeenanactiveacquirerduring2016asweseek to take advantage of the current market environment togrowourbusiness.WehavesignificantlyincreasedproductionandcashflowintheGreaterMediterraneanregion during 2016 and see further scope to materially growthatbusinessintheyearahead.

Stewart MacDonaldChiefFinancialOfficer

10 April 2017

* Economic production includes production from theeffectivedate(being1January2016)of theacquisitionof BeachEgypt.

21Report & Accounts for the year ended 31 December 2016

Rockhopper Exploration plc Strategic Report

Thedirectorsareresponsibleforthegroup’ssystemof internalcontrolandforreviewingitseffectiveness.Thegroup’ssystemof internalcontrolisdesignedtomanagerather than eliminate the risk of failure to achieve thegroup’sbusinessobjectivesandthereforeprovidesreasonable, rather than absolute, assurance against materialmisstatementorloss.

The group operates a series of controls to meet its needs.Thegroupreceivesreportsfromtheexternalauditor concerning the system of internal control and anymaterialcontrolweaknesses.Theboardconsidersthat there is no necessity at the present time to establish an independent internal audit function given the currentsizeandcomplexityof thebusiness.However,aninitialinternalauditreviewwasconductedduring2016usinganindependentthirdpartyauditfirm.ThatreviewfocusedontheGroup’sfinancialcontrolsandencompassedthekeyfinancialtransactioncyclesincluding:

>capitalprojects >monthlyfinancialreporting > bank and treasury >revenuetoreceivables.

The process of monitoring and updating internal controls and procedures continues throughout the year andariskmanagementprocessisinplace.Existingprocessesandpracticesarereviewedtoensurethat risksareeffectivelymanagedaroundasoundinternalcontrolstructure.

A fundamental element of the internal control structure involvestheidentificationanddocumentationof significantrisks,thelikelihoodof thoserisksoccurring,their potential impact and the plans for managing and mitigatingeachof thoserisks.Theseassessmentsarereviewedbytheboard.Theplansarediscussed,updatedandreviewedateachboardmeeting,andanymattersarisingfrominternalreviewsorexternalauditare alsoconsidered.

Internal controls and risk management

Rockhopper Board

Executive Committee Process

> Risks and mitigation validated withtheExecutiveCommittee andpresentedtoAudit&Risk Committeeforreview

Audit&RiskCommitteeReview and confirmation

>Reviewandconfirmation by the Board

Senior ManagementIdentification and mitigation

> Identify key risks and develop mitigation actions

Ongoing review and control There is ongoing review of the risks and controls in place to mitigate these risks by the Audit & Risk Committee.

> The Board is responsible for establishing and maintaining the system of internal controls whichhasbeeninplacethroughout2016.

Internal Controls

22 Report & Accounts for the year ended 31 December 2016

Rockhopper Exploration plcStrategic Report

Principal risks and uncertainties

Strategic risks Description Impact Mitigants Recent changes and ongoing initiatives

DelayinSeaLionFinalInvestmentDecisionduetolowoilpriceoutlook,increasedprojectcostsorpartner funding issues

> Increased costs>Delayinfuturecashflow> Reduced value creation>Lossof investorconfidence

>Activeengagementwiththeoperatorandregulatorstoestablishconstructiveandtrustedworkingrelationships

>Activeparticipationintechnicalmeetingstochallenge,influenceand/orsupportpartnerstoestablishacohesiveJVviewanddecisionmaking

>Activesupporttooperatorinitsobjectiveof introducinganotherpartner/securingalternativefundingfortheJV

>ProjectenteredFEEDwithsetof worldclasscontractorsinJanuary2016

>CommercialarrangementsbetweentheCompanyandtheoperatorwererevisedinJanuary2016toensuregreateralignment

> Draft Field Development Plan and draft Environmental Impact StatementsubmittedtoFalklandIslandGovernmentinlate2016

>Companytosupportoperatorduringitsfarm-out/alternativefunding process

Concentration risk through focus on the North Falkland Basin

> Over-reliance on a single operating region> Changesinoperating,sovereign,politicalorfiscalmatters couldhaveamaterialimpactontheCompany’soperations

> Diversify portfolio through asset additions outside of the North Falkland Basin

> Continuedpursuitof low-cost,low-commitment,value-accretiveacquisitionsintheGreaterMediterraneanregion

> Acquisitionof MediterraneanOil&GasplcinAugust2014addedproduction,developmentandexplorationassetsinGreaterMediterranean region

> Acquisitionof BeachEgyptPtyLimitedinAugust2016addedproduction and exploration assets in Egypt

Poorexecutionof M&Aactivity

>Reducedliquidityandbalancesheetstrength> Value loss

>ExperiencedBoardoverseesandapprovesallM&Adecisions> Established processes in place to ensure that an appropriate level of technical,commercial,financial,taxandlegalduediligenceisperformed on every opportunity assessed

>MergerwithFalklandOil&GasLimited(“FOGL”)completedinJanuary2016

>Continuedpursuitof selectiveandvalueaccretiveM&Aopportunities

The sovereignty of the Falkland Islands is disputed

> Open aggression is not expected>Certainserviceprovidersandfinancialinstitutionsmay

choose not to provide services for fear of the impact an association may have on their business in Argentina

>TheBritishGovernmenthasissuedstrongrebuttalstotheArgentineclaims

>TheCompanyisinregularcontactwiththeForeign&CommonwealthOffice

> Recent change of government in Argentina is expected to mitigate impact

>InSeptember2016,theBritishGovernmentandtheGovernmentof Argentinaagreedajointstatementonareasof cooperation,includingworkingtowardsremovingrestrictivemeasuresaffectingtheoil&gasindustryintheFalklandIslands

Operational risks Description Impact Mitigants Recent changes and ongoing initiatives

RelianceonJVoperatorsforassetperformance

> Cost and schedule overruns> Poor performance of assets> HSE performance

>ActivelyengagewithallJVpartnerstoestablishtrustedworkingrelationships

> Active participation in technical meetings to challenge, apply influenceand/orsupportpartnerstoestablishacohesiveJVviewand decision making

>FollowingawardofFEEDontheSeaLionproject,aManagementBoardcomprisingkeyprojectmanagersfromeachoftheJVpartners and contractors has been established to oversee the FEED process.Rockhopper’sGeneralManagerfortheFalklandIslandsattends such meetings

The North Falkland Basin is remote and at the end of a long supply chain

> Cost and schedule overruns> Ability to secure certain contractors

>Activeco-operationwithoperatorsintheSouthFalklandBasintoachieve operational and cost synergies through rig and infrastructure sharing

>Supplychainwellunderstoodgivenhistoryof operationsinthebasin

>ActiveengagementwithFIGandMinistryofDefencetocooperateand share infrastructure

>AdditionalcommercialflightroutetotheFalklandIslandsunderadvanced consideration

The assumptions used to estimate hydrocarbon resources may prove incorrect or inaccurate

>Explorationandappraisaleffortsmaytargetultimatelyuncommercial volumes of hydrocarbons

>TheCompanyemploysqualifiedandexperiencedtechnicalpersonnel> External consultants are regularly commissioned to support technical

evaluations or provide independent assessments>Aprudentrangeof possibleoutcomesareconsideredwithinthe

planning and budgeting process – current development scenario planningforSeaLionconservativelyassumesthepresenceof agascap

> Analysis of commerciality thresholds is inherent in exploration planningandlicenceacquisitionanalysis

> In May 2016 the Company announced completion of an

independent audit of the contingent and prospective resources in licencesPL032andPL004intheNorthFalklandsBasin

23Report & Accounts for the year ended 31 December 2016

Rockhopper Exploration plc Strategic Report

Strategic risks Description Impact Mitigants Recent changes and ongoing initiatives

DelayinSeaLionFinalInvestmentDecisionduetolowoilpriceoutlook,increasedprojectcostsorpartner funding issues

> Increased costs>Delayinfuturecashflow> Reduced value creation>Lossof investorconfidence

>Activeengagementwiththeoperatorandregulatorstoestablishconstructiveandtrustedworkingrelationships

>Activeparticipationintechnicalmeetingstochallenge,influenceand/orsupportpartnerstoestablishacohesiveJVviewanddecisionmaking

>Activesupporttooperatorinitsobjectiveof introducinganotherpartner/securingalternativefundingfortheJV

>ProjectenteredFEEDwithsetof worldclasscontractorsinJanuary2016

>CommercialarrangementsbetweentheCompanyandtheoperatorwererevisedinJanuary2016toensuregreateralignment

> Draft Field Development Plan and draft Environmental Impact StatementsubmittedtoFalklandIslandGovernmentinlate2016

>Companytosupportoperatorduringitsfarm-out/alternativefunding process

Concentration risk through focus on the North Falkland Basin

> Over-reliance on a single operating region> Changesinoperating,sovereign,politicalorfiscalmatters couldhaveamaterialimpactontheCompany’soperations

> Diversify portfolio through asset additions outside of the North Falkland Basin

> Continuedpursuitof low-cost,low-commitment,value-accretiveacquisitionsintheGreaterMediterraneanregion

> Acquisitionof MediterraneanOil&GasplcinAugust2014addedproduction,developmentandexplorationassetsinGreaterMediterranean region

> Acquisitionof BeachEgyptPtyLimitedinAugust2016addedproduction and exploration assets in Egypt

Poorexecutionof M&Aactivity

>Reducedliquidityandbalancesheetstrength> Value loss

>ExperiencedBoardoverseesandapprovesallM&Adecisions> Established processes in place to ensure that an appropriate level of technical,commercial,financial,taxandlegalduediligenceisperformed on every opportunity assessed

>MergerwithFalklandOil&GasLimited(“FOGL”)completedinJanuary2016

>Continuedpursuitof selectiveandvalueaccretiveM&Aopportunities

The sovereignty of the Falkland Islands is disputed

> Open aggression is not expected>Certainserviceprovidersandfinancialinstitutionsmay

choose not to provide services for fear of the impact an association may have on their business in Argentina

>TheBritishGovernmenthasissuedstrongrebuttalstotheArgentineclaims

>TheCompanyisinregularcontactwiththeForeign&CommonwealthOffice

> Recent change of government in Argentina is expected to mitigate impact

>InSeptember2016,theBritishGovernmentandtheGovernmentof Argentinaagreedajointstatementonareasof cooperation,includingworkingtowardsremovingrestrictivemeasuresaffectingtheoil&gasindustryintheFalklandIslands

Operational risks Description Impact Mitigants Recent changes and ongoing initiatives

RelianceonJVoperatorsforassetperformance

> Cost and schedule overruns> Poor performance of assets> HSE performance

>ActivelyengagewithallJVpartnerstoestablishtrustedworkingrelationships

> Active participation in technical meetings to challenge, apply influenceand/orsupportpartnerstoestablishacohesiveJVviewand decision making

>FollowingawardofFEEDontheSeaLionproject,aManagementBoardcomprisingkeyprojectmanagersfromeachoftheJVpartners and contractors has been established to oversee the FEED process.Rockhopper’sGeneralManagerfortheFalklandIslandsattends such meetings

The North Falkland Basin is remote and at the end of a long supply chain

> Cost and schedule overruns> Ability to secure certain contractors

>Activeco-operationwithoperatorsintheSouthFalklandBasintoachieve operational and cost synergies through rig and infrastructure sharing

>Supplychainwellunderstoodgivenhistoryof operationsinthebasin

>ActiveengagementwithFIGandMinistryofDefencetocooperateand share infrastructure

>AdditionalcommercialflightroutetotheFalklandIslandsunderadvanced consideration

The assumptions used to estimate hydrocarbon resources may prove incorrect or inaccurate

>Explorationandappraisaleffortsmaytargetultimatelyuncommercial volumes of hydrocarbons

>TheCompanyemploysqualifiedandexperiencedtechnicalpersonnel> External consultants are regularly commissioned to support technical

evaluations or provide independent assessments>Aprudentrangeof possibleoutcomesareconsideredwithinthe

planning and budgeting process – current development scenario planningforSeaLionconservativelyassumesthepresenceof agascap

> Analysis of commerciality thresholds is inherent in exploration planningandlicenceacquisitionanalysis

> In May 2016 the Company announced completion of an

independent audit of the contingent and prospective resources in licencesPL032andPL004intheNorthFalklandsBasin

24 Report & Accounts for the year ended 31 December 2016

Rockhopper Exploration plcStrategic Report

Financial risks Description Impact Mitigants Recent changes and ongoing initiatives

Insufficientliquidityandfundingcapacity >Uncertainfinancialoutcome>Inabilitytomeetfinancialobligations

> Short-term and long-term cash forecasts are reported to the Board on a regular basis

> The Company has no debt>Throughthe2012farm-outandsubsequentrevisions,Rockhoppersecureda$337millionDevelopmentCarryfortheinitialphaseof developmentof SeaLion,a$337millionDevelopmentCarryforthesubsequentphaseof developmentof SeaLionanda$750millionStandbyLoanfacilityfromPremierOil

>Agreementreachedtodefertaxliabilityassociatedwith 2012 farm-out

>UndertherevisedcommercialarrangementswithPremier,Rockhopperaccessedthefull$48mExplorationCarryduring the2015/16campaign

>ActiveengagementwithcommercialbankmarkettosecurefundingfortheuncarriedportionofSeaLiondevelopmentcostsonmoreattractive(costandflexibility)termscomparedwiththeStandbyLoanavailablefromPremier

>AgreementreachedwithFIGastoquantumandtimingoftaxpayment–taxdeferreduntilthefirstroyaltypaymentdateon SeaLion

Uncertaintyof fiscalregimeandregulatoryrequirements;SeaLionremainstheonlycommercial oil discovery declared in the Falkland Islands

> Schedule risk>Lossof value>Uncertainfinancialoutcome

>Regularengagementwithregulators>Legalagreementsinplacetoprotectinterests> Seek appropriate legal and tax advice

>Participation,inconjunctionwithotheroperatorsintheFalklandIslands,inrecentFIGTaxconsultationexercise

>ContinuedparticipationinconsultationwithFIGinrelationtooptimal approach to oil export

FailurebyJVpartnerstofundtheirfinancialobligations

> Increased costs>Potentialfailuretomeetfinancialandoperational

obligations> In extreme, potential loss of licence interests

> Partner selection is a critical component of any investment decision>JointOperatingAgreementsandothercommercialarrangementsprovidelegalprotectionsintheeventjointventurepartnersfailtomeet their obligations

>Activeengagementwithjointventurepartnerstoensurealignment>Ongoingmonitoringandregularreviewof theCompany’sfinancialexposuretojointventurepartnercreditrisk

Uncertaintyandvolatilityof commodityprices >Impactonexpectedfuturerevenuesandcashflow> Impact on capital and operating costs> Impact on future debt capacity

>Contingencybuiltintoplanningandbudgetingprocesstoallowfordownsidemovementsincommodityprices(andexpectedimpactoncosts)

> The Company may consider it appropriate in the future to hedge a proportion of its production, particularly if the Company is reliant on such production to service debt

>Oilpriceweaknesscontinuedthrough2016> As a result, industry and service costs have reduced and, through the SeaLionFEEDprocess,itisanticipatedthatfurthercostsreductionscan be achieved

Recoverability of receivables and exposure to foreign exchange

>Uncertaintyontimingof receiptandcurrency of payments

> Monitor macro-economic environment and lobby through establishedrelationshipsif required

> Active treasury management to minimise funds held in foreign currenciesandmatchwithcreditorbalances

>ActiveengagementwithEGPCandjointventurepartnerstomanagepaymentsandtheCompany’sforeigncurrencyliquidity

>Recentmacro-economicchangesinEgypthaveallowedaccesstoadditionalIMFfundingwhichshouldimprovegovernmentliquidity

>EGPCpaymentsreceivedinUSdollars,directtobankaccountsheldintheUK

Health, safety and environment risks Description Impact Mitigants Recent changes and ongoing initiatives

Health, safety and environment incidents >Seriousinjuryordeath> Environmental impacts>Lossof reputation> Regulatory penalties

>Regularreviewof HSEpoliciesandprocedurestoensurefullcompliancewithindustry“bestpractice”aswellasallappropriateinternational and local rules and regulations

>Changesasaresultof recentlyintroducedEUlegislationandoperationaldirectiveswereimplementedacrosstheCompany’soperating procedures

>TheCompanyfullyfulfilledtheenhancedriskassessmentauthorisationprocessaheadof therecentOmbrinaMarewellabandonment

Organisational risks Description Impact Mitigants Recent changes and ongoing initiatives

Staffrecruitment,developmentandretention > Disruption to business>Lossof keyknowledgeandexperience

>Traininganddevelopmentopportunitiesareconsideredforallstaff>Executivedirectorsandseniorstaffhavenoticeperiodof betweensixand12monthstoensuresufficienttimetohandoverresponsibilitiesin the event of a departure

> Succession planning considered regularly at Board level > The Remuneration Committee regularly evaluates compensation

and incentivisation schemes to ensure they remain competitive

> A short-term succession plan is in place for executive directors and keystaffmembers

> Consideration is being given to implement an all employee share scheme

25Report & Accounts for the year ended 31 December 2016

Rockhopper Exploration plc Strategic Report

Financial risks Description Impact Mitigants Recent changes and ongoing initiatives

Insufficientliquidityandfundingcapacity >Uncertainfinancialoutcome>Inabilitytomeetfinancialobligations

> Short-term and long-term cash forecasts are reported to the Board on a regular basis

> The Company has no debt>Throughthe2012farm-outandsubsequentrevisions,Rockhoppersecureda$337millionDevelopmentCarryfortheinitialphaseof developmentof SeaLion,a$337millionDevelopmentCarryforthesubsequentphaseof developmentof SeaLionanda$750millionStandbyLoanfacilityfromPremierOil

>Agreementreachedtodefertaxliabilityassociatedwith 2012 farm-out

>UndertherevisedcommercialarrangementswithPremier,Rockhopperaccessedthefull$48mExplorationCarryduring the2015/16campaign

>ActiveengagementwithcommercialbankmarkettosecurefundingfortheuncarriedportionofSeaLiondevelopmentcostsonmoreattractive(costandflexibility)termscomparedwiththeStandbyLoanavailablefromPremier

>AgreementreachedwithFIGastoquantumandtimingoftaxpayment–taxdeferreduntilthefirstroyaltypaymentdateon SeaLion

Uncertaintyof fiscalregimeandregulatoryrequirements;SeaLionremainstheonlycommercial oil discovery declared in the Falkland Islands

> Schedule risk>Lossof value>Uncertainfinancialoutcome

>Regularengagementwithregulators>Legalagreementsinplacetoprotectinterests> Seek appropriate legal and tax advice

>Participation,inconjunctionwithotheroperatorsintheFalklandIslands,inrecentFIGTaxconsultationexercise

>ContinuedparticipationinconsultationwithFIGinrelationtooptimal approach to oil export

FailurebyJVpartnerstofundtheirfinancialobligations

> Increased costs>Potentialfailuretomeetfinancialandoperational

obligations> In extreme, potential loss of licence interests

> Partner selection is a critical component of any investment decision>JointOperatingAgreementsandothercommercialarrangementsprovidelegalprotectionsintheeventjointventurepartnersfailtomeet their obligations

>Activeengagementwithjointventurepartnerstoensurealignment>Ongoingmonitoringandregularreviewof theCompany’sfinancialexposuretojointventurepartnercreditrisk

Uncertaintyandvolatilityof commodityprices >Impactonexpectedfuturerevenuesandcashflow> Impact on capital and operating costs> Impact on future debt capacity

>Contingencybuiltintoplanningandbudgetingprocesstoallowfordownsidemovementsincommodityprices(andexpectedimpactoncosts)

> The Company may consider it appropriate in the future to hedge a proportion of its production, particularly if the Company is reliant on such production to service debt

>Oilpriceweaknesscontinuedthrough2016> As a result, industry and service costs have reduced and, through the SeaLionFEEDprocess,itisanticipatedthatfurthercostsreductionscan be achieved

Recoverability of receivables and exposure to foreign exchange

>Uncertaintyontimingof receiptandcurrency of payments

> Monitor macro-economic environment and lobby through establishedrelationshipsif required

> Active treasury management to minimise funds held in foreign currenciesandmatchwithcreditorbalances

>ActiveengagementwithEGPCandjointventurepartnerstomanagepaymentsandtheCompany’sforeigncurrencyliquidity

>Recentmacro-economicchangesinEgypthaveallowedaccesstoadditionalIMFfundingwhichshouldimprovegovernmentliquidity

>EGPCpaymentsreceivedinUSdollars,directtobankaccountsheldintheUK

Health, safety and environment risks Description Impact Mitigants Recent changes and ongoing initiatives

Health, safety and environment incidents >Seriousinjuryordeath> Environmental impacts>Lossof reputation> Regulatory penalties

>Regularreviewof HSEpoliciesandprocedurestoensurefullcompliancewithindustry“bestpractice”aswellasallappropriateinternational and local rules and regulations

>Changesasaresultof recentlyintroducedEUlegislationandoperationaldirectiveswereimplementedacrosstheCompany’soperating procedures

>TheCompanyfullyfulfilledtheenhancedriskassessmentauthorisationprocessaheadof therecentOmbrinaMarewellabandonment

Organisational risks Description Impact Mitigants Recent changes and ongoing initiatives