2016-01-19_iot_platforms

of 25

-

Upload

rajeshtripathi2004 -

Category

Documents

-

view

215 -

download

0

Transcript of 2016-01-19_iot_platforms

-

7/25/2019 2016-01-19_iot_platforms

1/25

IoT Platforms: Chasing Valuein a Maturing MarketAUTHORS: DANNY DICKS AND SIMON SHERRINGTON, CONTRIBUTING

ANALYSTS, HEAVY READING

Independent market research and

competitive analysis of next-generation

business and technology solutions for

service providers and vendors

-

7/25/2019 2016-01-19_iot_platforms

2/25

HEAVY READING | JANUARY 2016 | IOT PLATFORMS: CHASING VALUE IN A MATURING MARKET 2

TABLE OF CONTENTS

1. EXECUTIVE SUMMARY .................................................................................. 3

1.1 Key Findings ............................................................................................. 3

1.2 Companies Covered ................................................................................... 4

2. TELECOM SERVICE PROVIDERS UP THEIR IOT GAME ................................... 5

3. EVOLVING VALUE CHAINS & THE ROLE OF PLATFORMS ............................... 7

3.1 Where the Value Is in IoT ........................................................................... 7

3.2 Defining an IoT Platform ............................................................................ 8

3.3 Standards ................................................................................................ 9

4. THE GROWING SIGNIFICANCE OF INDUSTRIAL IOT .................................. 10

5. VENDOR POSITIONING .............................................................................. 11

6. VENDOR ANALYSIS .................................................................................... 13

6.1 Aeris Communications.............................................................................. 13

6.2 Amdocs ................................................................................................. 14

6.3 Cisco ..................................................................................................... 15

6.4 Cumulocity ............................................................................................. 15

6.5 Ericsson ................................................................................................. 16

6.6 Jasper ................................................................................................... 18

6.7 Oracle ................................................................................................... 18

6.8 PTC ....................................................................................................... 20

6.9 Telit ...................................................................................................... 21

6.10 Xively (LogMeIn) ..................................................................................... 23

7. CONCLUSIONS ............................................................................................ 24

TERMS OF USAGE ................................................................................................. 25

Use of this PDF file is governed by the terms and conditions stated in the license agreement included in this file.Any violation of the terms of this agreement, including unauthorized distribution of this file to third parties, is con-

sidered a breach of copyright. Heavy Reading will pursue such breaches to the full extent of the law. Such acts arepunishable in court by fines of up to $100,000 for each infringement.

For questions about subscriptions and account access, please [email protected].

For questions and comments about report content, please contact Heavy Reading [email protected].

mailto:[email protected]:[email protected]:[email protected]:[email protected]:[email protected]:[email protected]:[email protected]:[email protected] -

7/25/2019 2016-01-19_iot_platforms

3/25

HEAVY READING | JANUARY 2016 | IOT PLATFORMS: CHASING VALUE IN A MATURING MARKET 3

1. EXECUTIVE SUMMARY

Since our short-form report on Internet of Things (IoT) platforms in May 2014,IoT Plat-forms: A Heavy Reading Competitive Analysis,the market has changed in many respects.However, there is still a feeling among platform vendors interviewed for this report that the

market for their products and services is at an early stage in its development, that morechange is likely, and that understanding of how the market works is still incomplete.

Positive changes reported by vendors are that the build-it-yourself approach to IoT is start-ing to give way to increased use of commercial off-the-shelf (COTS) platforms. And moretelecom operators particularly wireless operators are considering how they can take ad-vantage of the coming wave of connected devices beyond simply providing 2G or 3G SIMsor connectivity services to enterprises, solution providers or other third parties. Respondingto competition from new network providers, telecom operators are pushing the idea of cellu-lar connectivity direct to devices through the development of new standards and as anintrinsic part of future 5G networks. The issues of security, standardization and interopera-bility are also being talked about more than they were in the past.

In our interviews, however, this momentum is tempered with realism regarding the monetaryvalue of managing connectivity and devices, the sector-specific nature of much data manage-ment and analysis and, perhaps, also disappointment about the growth rate of mass-marketresidential IoT applications (where the horizontal platform approach may be better suited).

What seems to be happening is a functional enhancement and marketing repositioning ofplatforms higher up the technology stack to support the creation of applications built to runin multiple environments, as well as to provide interfaces to sector-specific data manage-ment and analytics engines and tools. Simultaneously, there is a recognition of who isspending money on IoT, and that is driving platform providers to change their offers andstrengthen their commercial and informal partnerships in order to address the real marketthat's out there today: industrial, largely machine-to-machine (M2M)-style IoT.

One vendor summed up these changes neatly: "The market's not floundering, but pivotingas people understand how it all fits together and what the needs are for commercial organi-zations. In the beginning, many platforms were built with small-scale innovators in mind.Many companies, including platform providers, are still working out where they fit, andwe've changed our platform in response to our customers' requirements." He added that hethought the market was now growing exponentially.

This report examines the market for horizontal, multi-sector platforms to enable IoT appli-cations. It considers the role of, and opportunities for, telecom operators in this market;considers where value resides in the process of developing, supporting and delivering an IoTapplication; and considers how much of this value can be captured through use of a hori-zontal platform. It looks at the role of standards and the importance of interoperability andinterfaces, and it assesses the offerings of 10 leading vendors of IoT platforms.

1.1 Key Findings

The key findings of this report are as follows:

Telecom operators are looking at IoT with renewed interestas they face challengesfrom other communications networks, such as SIGFOX, for their core IoT offers: connectivity

http://www.heavyreading.com/insider/details.asp?sku_id=3207&skuitem_itemid=1565&promo_code=&aff_code=&next_url=%2Finsider%2Flist%2Easp%3Fpage_type%3Dall_reportshttp://www.heavyreading.com/insider/details.asp?sku_id=3207&skuitem_itemid=1565&promo_code=&aff_code=&next_url=%2Finsider%2Flist%2Easp%3Fpage_type%3Dall_reportshttp://www.heavyreading.com/insider/details.asp?sku_id=3207&skuitem_itemid=1565&promo_code=&aff_code=&next_url=%2Finsider%2Flist%2Easp%3Fpage_type%3Dall_reportshttp://www.heavyreading.com/insider/details.asp?sku_id=3207&skuitem_itemid=1565&promo_code=&aff_code=&next_url=%2Finsider%2Flist%2Easp%3Fpage_type%3Dall_reportshttp://www.heavyreading.com/insider/details.asp?sku_id=3207&skuitem_itemid=1565&promo_code=&aff_code=&next_url=%2Finsider%2Flist%2Easp%3Fpage_type%3Dall_reportshttp://www.heavyreading.com/insider/details.asp?sku_id=3207&skuitem_itemid=1565&promo_code=&aff_code=&next_url=%2Finsider%2Flist%2Easp%3Fpage_type%3Dall_reports -

7/25/2019 2016-01-19_iot_platforms

4/25

HEAVY READING | JANUARY 2016 | IOT PLATFORMS: CHASING VALUE IN A MATURING MARKET 4

and management of connected devices. They are cooperating to offer extended networkreach to IoT app developers and working toward new technologies and standards that bettersuit IoT requirements.

Value in providing connectivity for devices is falling fast, and platform vendors are

quickly repositioning their products and services to enable more of what an IoT applicationneeds beyond a cloud-based database of devices and connections with some interfacesnorthbound and southbound. Some vendors are extending their scope through acquisition;others through internal development.

Some standards are emerging as significant in particular those relating to the waydevices exchange data with systems and most vendors believe an open approach with ap-plication programming interfaces (APIs) is the way to go, rather than closed, end-to-endtechnology stacks.

Industrial, largely M2M, IoT markets are increasingly seen as significantby plat-form vendors especially the largest IT players, which are partnering or acquiringtechnology companies to help them address this market.

1.2 Companies Covered

Companies covered in this report include:

Aeris Communications Inc.

Amdocs Inc. (Nasdaq: DOX)

Cisco Systems Inc. (Nasdaq: CSCO)

Cumulocity GmbH

Ericsson AB (Nasdaq: ERIC)

Jasper Technologies Inc.

Oracle Corp. (NYSE: ORCL)

PTC Inc. (Nasdaq: PTC)

Telit Communications PLC

Xively, a division of LogMeIn Inc. (Nasdaq: LOGM)

-

7/25/2019 2016-01-19_iot_platforms

5/25

HEAVY READING | JANUARY 2016 | IOT PLATFORMS: CHASING VALUE IN A MATURING MARKET 5

2. TELECOM SERVICE PROVIDERS UP THEIR IOT GAME

According to operators and observers, 2016 will likely see significant momentum build be-hind IoT, including operators' involvement in platforms and applications. For some time,forward-thinking operators in North America, Asia/Pacific and Europe have been building

their presence in IoT. While this process has not been completely smooth, we believe thatmany mainstream operators are now in a position to benefit from the revenue opportunitiespresented by increasing connectivity of things.

Many IoT platform vendors sell to, and through, operators some exclusively so and theyare bullish about prospects. Jari Salminen of Cumulocity says there is definitely a platformopportunity for operators because "they are good at running platforms and they alreadyhave the connectivity piece."

Among hundreds of IoT-related news announcements during 2015, some recent eventsstand out as particularly significant, showing how operators' IoT efforts back up vendors'optimism:

In December 2015, AT&T reported it had signed 300 IoT deals during 2015 in theU.S. and abroad, and that about 25 million connected devices (M2M devices and con-nected tablets) were on the AT&T network with particularly fast growth in thenumber of connected cars during the year.

In September 2015, Swisscom joined the original six major international operators(Deutsche Telekom, Orange, TeliaSonera, Telecom Italia Mobile, Bell Canada andSoftBank) that created the Global M2M Association (GMA) in February 2015. Thesecarriers are cooperating to create a global network for seamless M2M connectivity (amulti-domestic service) using Ericsson's device connection platform (DCP).

Vodafone has been championing the NB-IoT communications standard: In December2015, the operator announced it had sent the first "pre-standard" message using this

standard for low-power, wide-area (LPWA) communications, in conjunction withHuawei and u-blox, to connect a water meter to its network in Spain.

In a December 2015 report entitledUnblocking the Value of IoT Through Big Data,theGSMA mobile operator industry group made the case for operators' expertise in device,network, data, application, security and identity management, as well as data analy-sis, reporting, billing and charging, as a pivotal part of an IoT "big data ecosystem."Vendors such as Amdocs and Aeris have also pointed out the importance of opera-tors' expertise in security and a platform approach to service enablement (capable ofdealing with high-volume, low-ARPU services) as strengths on which to build.

Vendors suggest operators may still take up either a connectivity-only position (in which casethey will need a connectivity-and possibly device-management platform) or a full service ena-

blement position (in which case they need a "service enablement platform" and, perhaps, anecosystem of partners to offer broader functionality). They also need to decide how horizontaltheir platform offer can be; many are likely to focus on some specific vertical markets andbuild platform offers tailored for those applications. Ericsson's Anders Hillbur references oneexample of a broad carrier offer: "Operators need to ask themselves the question of how theyare going to exploit the IoT opportunity. Some already have a well-defined and flexible offer for instance, Telia with its M2M in a Box concept, which can be bought either as a full stack oras specific solutions with SDKs [software development kits] to enable customization," he said.

http://www.gsma.com/connectedliving/wp-content/uploads/2015/12/cl_iot_bigdata_11_15-004.pdfhttp://www.gsma.com/connectedliving/wp-content/uploads/2015/12/cl_iot_bigdata_11_15-004.pdfhttp://www.gsma.com/connectedliving/wp-content/uploads/2015/12/cl_iot_bigdata_11_15-004.pdfhttp://www.gsma.com/connectedliving/wp-content/uploads/2015/12/cl_iot_bigdata_11_15-004.pdf -

7/25/2019 2016-01-19_iot_platforms

6/25

HEAVY READING | JANUARY 2016 | IOT PLATFORMS: CHASING VALUE IN A MATURING MARKET 6

Making a case for sector specialization, Macario Namie of Jasper a vendor that has longworked very closely with operators says operators make IoT work best when they partnerwith or acquires a specialist in a specific market: "We have seen this, for instance, in vehicletelematics and logistics where operators have a big presence," says Namie. Examples includeAT&T's CargoView service, Verizon Telematics (acquired from Hughes) and Telefnica's logis-

tics service built in connection with Masternaut. Indeed, the ecosystem approach can be seenacross the IoT landscape platform and other vendors, operators and system/solution build-ers are all putting in place partnerships to better enable them to address specific markets.

Our discussions with vendors suggests that more operators, along with other companieswanting to develop IoT applications and services, are increasingly adopting the view thateven if they have specific opportunities in mind, they need not build the required platformtechnology themselves. Further, they believe that if they are to succeed in the IoT market,they need to look for help in several areas even with connectivity (the Global M2M Associ-ation initiative mentioned above is an example). Ericsson's Hillbur pointed out that whilesome operators (such as Orange, Vodafone, Verizon and AT&T) are building their own globalIoT networks, many use third-party platforms and networks such as Ericsson's to build theirIoT offers: "Their own national networks aren't enough to support app developers who have

global ambition (which is most of them). Operators' own networks have been optimized forspecific purposes: some are business-focused; some are optimized for fast data in cities,some for ubiquitous geographic coverage, and so on," he said.

More widely, operators are looking for help to develop broader IoT offers. An Oracle spokes-person told us: "Operators can specialize in device management and connectivity only; theycan sell their own cloud services and an app development platform like ours to IoT appdevelopers and service providers; or they can work with partners like Oracle and directlydelivery IoT services to enterprises and consumers."

It is important to realize that there are IoT platforms relating to application-specific datacollection, aggregation, analysis and reporting that are strongly sector-specific. This report

does not aim to cover vendors of those platforms. Further, there are generic data analysisplatforms and tools whose usefulness extends far beyond IoT applications. Again, this reportdoes not cover vendors of these platforms. Finally, the application development environ-ments, offered as a platform to app builders (and either generic or sector-specific) are alsonot covered here. IoT-focused platform vendors tell us that the industry is increasingly rec-ognizing that applications will be built using customers' own choice of app developmentenvironment whether that is a widely used enterprise software environment, such as SAPor Oracle, or a sector-specific environment.

Section 3looks at how IoT platforms and other components of value in IoT fit together.

-

7/25/2019 2016-01-19_iot_platforms

7/25

HEAVY READING | JANUARY 2016 | IOT PLATFORMS: CHASING VALUE IN A MATURING MARKET 7

3. EVOLVING VALUE CHAINS & THE ROLE OF PLATFORMS

When we interviewed vendors for this report we asked them whether there was a settledview of the IoT value chain: Their responses were varied. There was a consensus that valueexisted in a long chain stretching from devices and communications modules at one end,

and from end-user applications (for consumers and businesses) at the other end. They alsoagreed that, in between, there was value in device and connectivity management, data col-lection, analysis and reporting. But many pointed out that vertical markets exist: In effect,there is no single "IoT value chain"; further, the specific data requirementsof each IoTapplication are what makes these value chains complex.

This difficulty translates into a somewhat complex market that is only now becoming moremature. Jasper's Namie feels it necessary to define where his company one of the longer-established in IoT platforms currently positions itself. He says that these are still the earlydays of IoT and it's too soon to call it an industry: "The situation is very messy, and manycompanies offer all sorts of things, but we are clear: We focus on service lifecycle manage-ment. The service lifecycle varies per sector, but our platform can support these different

lifecycles because it is configurable and customizable."

Increasingly, platform vendors are trying to identify the right role for their technology in dif-ferent markets, a response to fluidity in the way IoT applications are built and offered, aswell as some changes in the value of different parts of this process.

3.1 Where the Value Is in IoT

Analysis of the distribution of value across the chain outlined above is difficult, though ana-lysts, including McKinsey Global Institute, have attempted to do this in a verycomprehensive report into IoT value,The Internet of Things: Mapping the Value Beyond theHype.But as Jari Saminen of Cumulocity pointed out: "Where the value is created variesfrom vertical to vertical." And Oracle acknowledged that pricing models for its white-label

IoT platform services also vary somewhat by application, with recurring charges on a per-user or volume basis whichever makes most sense for the specific service.

Some vendors quote benchmarks: Russ Fadel, from industrial IoT specialist vendor PTC,says "45 percent of the value in the IoT value chain is in the app enablement and the appitself; 25 percent is in the comms network." Oracle told us that only around 10% of spendon IoT services will go on connectivity. Fadel agrees that value in connecting devices to theInternet is not what it was at the start of 2015: "There is intense price pressure in the de-vice cloud market we've seen prices drop from 40 cents per connected device per monthto 2 cents over the last year or so," he says. This has profound implications for vendorswhose platforms have been built to provide just that functionality: They must be capable ofscaling and delivering connectivity management very cheaply.

Some vendors are confident they can deliver. For instance, Janet Jaiswal, VP of marketingat Aeris, told us: "Our platforms were purpose-built to support very large scale and end-to-end IoT/M2M applications; the price of connectivity management is falling, but we are prof-itable even at low connectivity ARPU."

The primary reason prices are falling in connectivity management is that the growth in thenumber of connected things, while rapid, has not been sufficiently explosive to stop anoversupply of cloud-based services that enable devices to be connected. Vendors told us

http://www.slideshare.net/yannlegigan/unlocking-the-potentialoftheinternetofthingsfullreport-50479611http://www.slideshare.net/yannlegigan/unlocking-the-potentialoftheinternetofthingsfullreport-50479611http://www.slideshare.net/yannlegigan/unlocking-the-potentialoftheinternetofthingsfullreport-50479611http://www.slideshare.net/yannlegigan/unlocking-the-potentialoftheinternetofthingsfullreport-50479611http://www.slideshare.net/yannlegigan/unlocking-the-potentialoftheinternetofthingsfullreport-50479611http://www.slideshare.net/yannlegigan/unlocking-the-potentialoftheinternetofthingsfullreport-50479611 -

7/25/2019 2016-01-19_iot_platforms

8/25

HEAVY READING | JANUARY 2016 | IOT PLATFORMS: CHASING VALUE IN A MATURING MARKET 8

that there are hundreds of device cloud providers worldwide, and basic economics saysprices will fall.

Simultaneously, the build-it-yourself approach in many areas of IoT is giving way: "We areat that point in the market where the IoT space is moving toward commercial off-the-shelf

solutions it's becoming mature. The reason for this is that COTS application developmentplatforms can now take away a lot of the technical problems of setting up IoT applications,"says Fadel of PTC. One issue that typically emerges at this stage of market developmentwhere horizontal platform approaches are being adopted is that of interoperability andstandardization. We'll look at this in more detail in Section 3.3, but first we need to beclear about what platforms we are dealing with.

3.2 Defining an IoT Platform

Figure 1shows our view of the IoT technology stack, identifying some specific types ofplatform. As we pointed out earlier, there are some products and services that fulfil platformrequirements (ability to interface to multiple devices or processes or applications) that arenonetheless developed with a specific, often vertical-market-oriented set of users and appli-

cations in mind (particularly in the data management Layer 4).

Figure 1: Technology layers in IoT

Source: Heavy Reading

There are also some generic data analysis platforms (at Layer 4) and application develop-ment environments (at Layer 6) that have broader applicability than just IoT. Vendorscovered in this report typically provide products and services at Layers 3 and 5. Layer 5 inFigure 1is highlighted because this is where many vendors are focusing their efforts per-ceiving there to be more value at this layer while recognizing the importance in the stack

-

7/25/2019 2016-01-19_iot_platforms

9/25

HEAVY READING | JANUARY 2016 | IOT PLATFORMS: CHASING VALUE IN A MATURING MARKET 9

of data analytics as deployed applications scale up and users' focus switches to operationalaspects of the application.

But not all connection management platforms and approaches are the same. For instance, amajor question concerns whether it should be integrated with a specific network (typically a

public wireless network) or be more open to include other communications technologies.There are certainly serious competitors to public networks notably the license-free, spec-trum-based SIGFOX cellular network that aims to cover 60 countries and has launched in 12(as of the end of 2015).

Whether or not the platform resides in the cloud or in specific data centers is another differ-entiator. Jasper, for instance, is in the latter camp; Oracle points out that a cloud gatewayenables processing logic to be created closer to the device, which can reduce latency; Telit'sFred Yentz says that the very many cloud-based connection management platforms some-times deliver low levels of functionality. "[They have] some APIs for data collection andsome APIs so that you can use the data you collect; [they are] just a dual-ported databasein the cloud," he says.

As we noted earlier, the fact that IoT applications vary so much from sector to sector andfrom user to user means that platforms to enable services (at Level 5 in Figure 1) can, atbest, provide some reusable components and appropriate interfaces, which is what manyvendors now aim to do. But where existing applications are becoming IoT applications, thereare legacy systems to be integrated, and appropriate interfaces are not always availablewithout extensive customization. As Anders Hilbert of Ericsson notes: "The less legacy thereis to integrate, the more horizontal platforms will work."

3.3 Standards

There is a large number of places in the process of building an IoT application where in-teroperability and standards might apply, but not all of them are appropriate for a

standards-based approach. Some believe that openness, APIs (Jasper, for instance, says itoffers over 100, northbound and southbound), SDKs and interoperability demonstration ismore important than standardization, while acknowledging the significance of some stand-ards: "There are few M2M or IoT standards yet the open approach supports the quickerdevelopment of a bigger ecosystem, but the lightweight OMA standard is important becauseit enables devices to be plug-and-play. We have participated in interoperability tests during2015," says Salminen of Cumulocity. He adds that a closed-stack, end-to-end approach isadvocated by some vendors.

Fadel of PTC notes that it's easier to have standards for device connectivity (such as MQTTand CoAP) than for application data, where he says a RESTful interface and support for au-tomated discovery are needed: "We see the value of over-the-air lightweight devicemanagement standards so we will support these as they become established," he adds

while recounting that "standards are like toothbrushes: Everyone knows you need them, butno one wants to use somebody else's."

-

7/25/2019 2016-01-19_iot_platforms

10/25

HEAVY READING | JANUARY 2016 | IOT PLATFORMS: CHASING VALUE IN A MATURING MARKET 10

4. THE GROWING SIGNIFICANCE OF INDUSTRIAL IOT

Automotive IoT applications have been significant for operators and major vendors for sometime (for instance, Volvo's connected car services have been supported by the Ericsson IoTplatform service, and both U.S. giant operators Verizon and AT&T have established telemat-

ics services). Device cloud platform service vendors have focused on enabling novelconsumer and business IoT applications and services by lowering the barriers to getting de-vices connected to the Internet. But a third sector of the market and one that we believewill be increasingly significant is industrial automation.

Factories, utilities and other large, complex industrial segments have always been highlyautomated. In general, these industries have developed sector-specific technologies to con-nect equipment to control systems; the availability of low-cost (and wireless) sensors andcommunications modules developed and manufactured in high volumes as the potential ofthe IoT becomes clearer means that legacy Supervisory Control and Data Acquisition(SCADA) systems can be significantly enhanced, their range extended and their scope in-creased. The Industrie 4.0 concept developed in Germany and involving Deutsche Telekom

and Siemens has gained traction around the world as a description of the potential of indus-trial IoT; in the U.S., an industrial Internet project involving AT&T, Cisco, General Electricand Intel that has been running since 2013 has similar aims.

Here, though, the dynamic world of the Internet meets the somewhat slower world capex-heavy manufacturing, with its typically long-term investment cycles and in many sectors,risk-averse mindset. But vendors are enthusiastic about prospects for their platforms, withindustrial sectors maturing quickly and healthcare and medical markets a little further be-hind. Telit pointed to the effort being put into device connectivity standardization inmanufacturing, citing the MQTT connectivity protocol: "It's ANSI-approved and created spe-cifically for M2M connectivity. There will be some dissenters to the standards-basedapproach, but it will prevail," said the company's Yentz.

There has been significant merger and acquisition (M&A) and ecosystem-building activity inthe industrial IoT field as industrial automation giants look to ensure that IoT start-ups don'teat their lunch and large Internet players recognize the importance of this large market sec-tor. Examples include Telit's acquisition of ILS Technology, industrial control specialist PTC'sacquisition of IoT platform vendors Axeda and ThingWorx (as well as data analytics com-pany Coldlight), Cisco's investment in "intelligent plant" specialist Covacsis, andpartnerships with Itron and RivaSoft, and the establishing of partnerships between multipleIoT platform vendors and industrial data analytics platform GE Predix.

What the platform players are trying to achieve (if they don't have it already) is domaincompetence so that they can understand the intricacies of the data acquisition, analysis andreporting that we identified earlier as the stubbornly sector-specific aspect of IoT, and ena-ble user-specific applications for industrial businesses. Jasper's Namie points out that this iswhere business customers often need help: "The biggest challenge for enterprises is choos-ing the service they want (to deliver) and HOW to deliver itvertical market expertise isvital." His view is that the technology isn't actually that difficult, and that while system inte-grators can develop solutions, it remains a niche area for some of them.

-

7/25/2019 2016-01-19_iot_platforms

11/25

HEAVY READING | JANUARY 2016 | IOT PLATFORMS: CHASING VALUE IN A MATURING MARKET 11

5. VENDOR POSITIONING

The vendors profiled in this report represent a subsection of the very many providers ofplatforms supporting IoT applications. We have focused on those vendors that have gainedsignificant traction in the market through number or size of deals done, or whose approach

is distinctive, or who are major providers to the telecom sector. As well as specialist ven-dors, or the IT product and solution companies that have a significant communicationsfocus, others also develop platforms for IoT examples include big IT solution providers,such as HP, PwC and IBM, that have been building their own capabilities in this space.

As we noted earlier, the scope of platforms is changing, and vendors' offers are somewhatfluid right now as they chase IoT platform value by moving up the technology stack as bestthey can. Some we spoke to were not optimistic that all vendors would survive unless theybroaden the scope of what they offer. Aeris's Amit Khetawat told us: "The breadth of our port-folio is a real strength; as the IoT platform market matures, it's going to get much harder forone-trick ponies." Telit's Yentz said he believed some platform companies were little morethan provisioning platforms for device clouds, though he agreed that new-entrant devicecloud companies could teach established players about innovation in dashboard capabilities.

Jasper's Namie expects consolidation especially acquisition of vertical-market specialistsolution providers by big companies and Xively's Ryan Lester agrees; he sees the func-tionality and scope of platforms growing. "Large players [will add] new IoT-specific featuresinto their offerings and early platforms, providing differentiated value to solve key IoT chal-lenges. We see connected product management as a key space where consolidation willhappen as more companies try to run a connected business [as products are launched]the need to scale becomes more apparent and we will see companies consolidate on plat-forms that are both scalable and simple to use," he says.

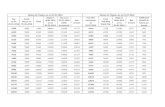

Figure 2gives our assessment of vendor positioning; Section 6goes into more detail ofvendors' approaches and offers.

Figure 2: Heavy Reading Assessment of Selected IoT Platform Vendor Positioning

Vendor Products/Services Positioning

AerisAerCloud enablement platform; Aer-Port connectivity managementplatform; AerVoyance analytics

M2M application enablement and device con-nection through platforms and co-developedservices and solutions; platforms sold forwhite-label service building

Amdocs

Amdocs M2M Connected Device Plat-form; Amdocs Connected HomeSolution; Amdocs Insight Big Data An-alytics Platform

Focus on broadest possible support for com-munications service providers building IoTservices (though also supporting IoT applica-tion developers)

Cisco

Cisco IoT System, including Fog DataServices (embedded in IOx platform);IoT Field Network Director manage-ment software; Fog Director applicationmanagement platform; Cisco IoT CloudConnect hosted platform

Support for mobile service providers, but anincreasing focus on industrial IoT and directsale to enterprises; broad reach across tech-nology stack layers

CumulocityCloud-based Cumulocity platform(event processing, data analytics,provisioning)

Service-provider and solution-builder focuseddevice and data management platform for ser-vice enablement

-

7/25/2019 2016-01-19_iot_platforms

12/25

HEAVY READING | JANUARY 2016 | IOT PLATFORMS: CHASING VALUE IN A MATURING MARKET 12

Vendor Products/Services Positioning

EricssonDevice Connection Platform; ServiceEnablement Platform; global connec-

tivity services

Connectivity management, service enablement,global IoT platform services with expertise inautomotive and some other verticals; support

for operators, large enterprises and third-partyapplication developers

Jasper

Control Center lifecycle management(devices, connections); integratedwith sector-specific third-party datamanagement/analytics platforms

Flexible platform service (SaaS) offered to op-erators only for white-labeling; partnershipapproach with other platform players; increas-ingly extending beyond connectionmanagement to encompass device manage-ment and app development support

Oracle

Oracle Application Enablement Plat-form (encompassing Oracle IoT CloudService); Oracle Communications plat-forms for network and policymanagement; Fusion Middleware com-

ponents, analytics solutions andmultiple industry IT solutions

Enterprise and operator support; recent em-phasis on device connection, security andlifecycle management; and out-of-the-box inte-gration with existing enterprise applications,

including those used in manufacturing

PTCThingWorx IoT Platform (includingThingWorx Machine Learning analyticstool); Axeda Machine Cloud

Service enablement and lifecycle management;device and connectivity management; focus onmanufacturing industry but has IoT platformcustomers in other sectors; sells direct to en-terprises, as well as through operators; workswith third-party app developers

TelitIoT Portal solution (PaaS); deviceWISEapplication enablement platform;modules and connectivity services

M2M focus; broad technology spread frommodules to application enablement; two ver-sions of deviceWISE platform sold/licensed (tooperators and to industrial enterprises) and of-fered as a PaaS end-to-end solution

Xively(LogMeIn)

Xively Platform for connectivity anddevice management

Connected device management (including secu-rity/identity management) and serviceenablement, for light industrial/B2B2C applica-tions (home or commercial end use); sellsdirectly and to application developers ratherthan large enterprises or mobile operators

Source: Heavy Reading

-

7/25/2019 2016-01-19_iot_platforms

13/25

HEAVY READING | JANUARY 2016 | IOT PLATFORMS: CHASING VALUE IN A MATURING MARKET 13

6. VENDOR ANALYSIS

6.1 Aeris Communications

Aeris, founded in 1992, provides a broad range of services that span much of the IoT value

chain; the company has a particular focus on M2M applications rather than consumer appli-cations. It claims it is in the top 10 global providers of device connectivity globally based onnumber of devices connected. Where it sells platforms, these are used to build white-labelIoT/M2M services.

The company has grown fast in terms of numbers of connected devices 100 percent yearon year in the last four years which it claims outperforms the industry by three to fourtimes. Aeris is particularly strong in the vehicle telematics sector where it has built a strongpresence through acquisition and partnerships; its customers include Hyundai, Honda andChrysler. In October 2015, Aeris announced a partnership with Isotrak to offer fleettelematics services. The company sees the automotive sector as its big growth opportunity.Other verticals where Aeris is strong include healthcare, point-of-sale, fleet, utility and in-dustrial and utility monitoring and control.

Aeris says its key differentiators are its focus on machine connectivity, its ability to deliveran end-to-end solution encompassing both an extensive technology stack and a range ofnetwork connectivity options, the carrier-agnostic nature of its connectivity and a strongcommitment to very high levels of customer service.

The key platforms underpinning Aeris services are:

AerCloud a generic application enablement platform that the company says ena-bles rapid prototyping, development and launch of IoT/M2M applications. AerCloud isintegrated with an app toolkit (called AppExpress) that uses widgets to speed upWeb-based app development. Development work is currently focusing on user inter-

face simplification and the integration with other applications, such as customerrelationship management (CRM).

AerPort a connectivity management platform built for large scale, that providestraffic and alert management and reporting, as well as connection management;Aeris also offers AerConnect, a cellular connectivity service.

AerVoyance IoT analytics software with an intuitive visual interface to help man-age IoT/M2M deployments and address challenges of gaining insight into devices,connectivity and billing information.

Complementing these three core platforms is the AerB/OSS billing and rating engine. Ser-vices built on Aeris's core technology include:

Neo a self-serve connectivity service that provides SIMs and connectivity via an on-line marketplace, reducing the time and cost of dealing directly with cellular operators.

JumpStart IoT a service jointly offered with Tech Mahindra and other servicepartners, aimed at cellular operators that want to develop and offer IoT services toenterprises.

These two services broaden the company's revenue streams to include carrier sell-through;Aeris says it has around 20 deals for JumpStart, including with Aircell, and adds that it sees

-

7/25/2019 2016-01-19_iot_platforms

14/25

HEAVY READING | JANUARY 2016 | IOT PLATFORMS: CHASING VALUE IN A MATURING MARKET 14

the carrier market starting to heat up, particularly in Asia/Pacific and Europe. Neo alsoopens up revenues from IoT/M2M solution builders. The company also has a commercial re-lationship with Cisco that resells Aeris solutions, and partner relationships with distributorsand mobile network operators (MNOs) for its solutions.

Aeris says that it will not develop its own end-to-end IoT applications in its existing marketsas it does not want to compete with its customers, but remains open to the idea of develop-ing new applications in niche areas.

6.2 Amdocs

One of the biggest software and service providers to telecom operators globally, Amdocshas offered solutions for M2M/IoT solutions since before 2013. Notably, AT&T uses Amdocssolutions to underpin its OnStar vehicle telematics offer, and an unnamed global mobile op-erator uses Amdocs for M2M partner management. Amdocs sees opportunities to support itsexisting operator customers as they develop M2M and IoT services whether those are con-nectivity based or more substantial service enablement offers. As well as developing specificIoT/M2M solutions and platforms, Amdocs has been positioning its other core solutions (for

instance, customer experience management, charging/billing and big data analytics) as ena-bling technologies for IoT.

Amdocs has identified different types of customer from both telco and application developersides of the market. These are: mature communications service providers that have a rapidlymaturing IoT offer already; emerging communications service providers that need help to de-velop their IoT offers; emerging IoT service providers that are product manufacturersdeveloping services based on connectivity to their products; and IoT consumer electronicsoriginal equipment manufacturers (OEMs), for whom Amdocs can act as a route to activate,register and bill consumers directly for both communications and IoT products and services.

In addition to the company's core customer experience and billing/charging solutions, rele-

vant Amdocs products and solutions targeting one or other of these customer groups, andinvolving both its own and third-party partner products, include:

Amdocs MINT: a platform that manages wholesale and retail connectivity and bill-ing. The platform is offered as a standalone, multi-tenant IoT platform that enables aservice provider to rapidly onboard IoT OEMs and generate revenue beyond connec-tivity. Capabilities include an OEM portal, defining new service offerings, billing andcustomer care. MINT leverages Amdocs CES portfolio.

Amdocs M2M Connected Device Platform:the company's core platform thatmanages device connectivity. It is offered as a stand-alone platform, an add-on toother core Amdocs BSS solutions and as a cloud-based service. Amdocs says thisflexibility is important because different IoT applications have different commercial,

regulatory, security and international reach contexts, so a flexible delivery model forconnectivity management is needed.

Amdocs Connected Home Solution:includes the Amdocs Device Connection Plat-form and home security systems and services from a third party; Amdocs is workingto develop this to include services built for other connected devices within the home.

Amdocs Insight Big Data Analytics Platform:a platform that can be used toanalyze and refine IoT applications and services in the same ways as for other tele-com services.

-

7/25/2019 2016-01-19_iot_platforms

15/25

HEAVY READING | JANUARY 2016 | IOT PLATFORMS: CHASING VALUE IN A MATURING MARKET 15

Amdocs is also participating in an initiative on open data and interoperability calledMatrix.org that aims to establish a set of secure vaults for IoT data (as well as for otherreal-time applications, including WebRTC signaling and persistent chat rooms).

6.3 Cisco

Unlike most vendors in this report, Cisco's offer in IoT goes much wider than just connectiv-ity or service enablement platforms, but also encompasses hardware (chipsets, modules,devices and network) and a broad set of relevant enterprise and service-provider solutions.

Cisco's key IoT offer for network operators and their enterprise and small to medium enter-prise (SME) customers is the Cisco IoT System, launched in June 2015. Cisco says it hasbuilt its IoT System on six pillars: network connectivity (routing, switching and wirelessproducts); "fog" computing (Cisco's term for the distributed computing infrastructure thatIoT will use); security (IP surveillance and built-in security of Cisco's products); data analyt-ics (based on Cisco Connected Analytics portfolio and third-party systems); managementand automation (security, control and support for multiple siloed functions); and an applica-tion enablement platform (offering a set of APIs on which others can build applications).

Cisco is betting on the importance of computing at the edge in IoT applications. In the con-text of this report, the most relevant new-product components of the Cisco IoT System arethose in the final three pillars, specifically:

Fog Data Services data flow monitoring and policy service embedded in the CiscoIOx platform

IoT Field Network Director management software to allow operators to monitorand customize network infrastructure, as Cisco puts it, "for an industrial scale."

Fog Director a central management platform for multiple edge applications withfunctionality spanning the lifecycle of an app and a way for administrators to havevisibility of large-scale IoT deployments.

The Cisco IoT System is aimed at industrial IoT uses and, recognizing the importance of do-main-specific understanding in the data layer for IoT, Cisco has been very active in putting inplace partners in an ecosystem to help it target industrial markets. Companies that haveported software to run on the System include GE (its widely deployed Predix analytics applica-tion), Itron (Riva data aggregation and analytics platform for utility companies) and OSIsoft(PI real-time data and event aggregation and analytics platform). Cisco has also invested inCovacsis, a specialist in "intelligent plant" data platforms for manufacturing industries.

Complementing the new IoT System, Cisco's IoT Cloud Connect hosted platform is a hostedmanaged IoT platform aimed at mobile service providers. It provides management and au-tomation of IoT services. The platform is built on Cisco's M2M service delivery platformcoupled with Cisco's virtualized packet core solution (based on widely deployed StarOS soft-ware) and relevant applications from Cisco ecosystem partners. Cisco says its IoT CloudConnect platform helps operators reduce the cost and increase the speed of deploying IoTservices to business customers.

6.4 Cumulocity

Cumulocity began life in 2010 as an innovation project within Nokia Siemens Networks(now Nokia); it was spun out into a separate company in 2012. Managing director, sales

-

7/25/2019 2016-01-19_iot_platforms

16/25

HEAVY READING | JANUARY 2016 | IOT PLATFORMS: CHASING VALUE IN A MATURING MARKET 16

and strategic partnerships, Jari Salminen says this telecom equipment provider heritage hasinfluenced the way its IoT platform has developed with service providers in mind in terms ofrobustness, scalability and feature set. The company's focus for its first two years was ondirectly addressing the enterprise segment; today its customers are increasingly telecomoperators and system integrators/solution builders. Reference customers and partners in-

clude Deutsche Telekom and Etisalat on the operator side (Salminen says the company is indiscussion with over 30 operators globally), and Wipro, Tech Mahindra and Tieto on the sys-tem integrator (SI)/solution builder side.

Cumulocity is working with numerous device and module vendors to integrate and, in somecases, pre-certify their products for use with the Cumulocity platform. Example vendors in-clude NetComm Wireless, Option and Gemalto. Cumulocity offers free trial accounts anddevelopment tools for app developers and other partners. Through its customers and applica-tion development partners, the Cumulocity platform underpins IoT applications in industrialIoT, transport/fleet management, vending machines, healthcare, the utility sector and others.

Cumulocity focuses on device and data management (getting data from assets in the field,analyzing it in real time and publishing it through APIs) rather than connectivity manage-

ment (it has partnerships with others, such as Jasper, for handling connectivity). It alsodelivers device management functions, such as mass provisioning and over-the-air updates,and some real-time analytics capabilities. Script-based event processing, a graphical userinterface and a library of dashboard widgets for the platform to help users start to connectdevices and build applications as quickly as possible.

While Cumulocity performs real-time analytics to trigger events and actions based on thedata, it does not provide application-specific integrated data analytics environments: "Ourcustomers will use the data managed by our platform in their own analytics software," saysSalminen. He adds that "as the final 10-20 percent of the application development is alwaysunique, flexibility and openness are critical from an IoT platform, and that includes choice ofapp development environment and tools you are familiar with already. We provide fully doc-umented and public REST APIs and SDKs to support this, and free code examples to many

device environments like Java, Linux, Posix and Lua, among others."

Cumulocity's revenue model is based on a per-device, per-month fee, which is typical for aplatform provider. The platform can be white labeled, and is delivered from the cloud formaximum flexibility. Salminen says, "Anything you can do on the platform can be doneelsewhere via an API."

6.5 Ericsson

Ericsson acquired some IoT platform technology from Telenor in 2011 and has significantlydeveloped its platform product and service offers since then. It already had several M2M-ori-ented IoT customers in significant vertical markets, including Volvo (for a range of connectedcar applications) and the Maersk shipping line (for a sophisticated set of logistics and shipmonitoring applications). The company sees automotive and transport as among its most im-portant markets in the future: Ericsson's Connected Vehicle Cloud offers a way for appdevelopers to reach a large market, and it allows car makers, retailers and others to developnew services. Other core markets for the company in IoT are utilities and energy, and Erics-son identifies healthcare and smart cities and communities as the big areas for the future.

Ericsson offers two IoT platforms: the Device Connection Platform (DCP) and the M2M vari-ant of its Service Enablement Platform (SEP). It also offers a full IoT stack as a service and

-

7/25/2019 2016-01-19_iot_platforms

17/25

HEAVY READING | JANUARY 2016 | IOT PLATFORMS: CHASING VALUE IN A MATURING MARKET 17

it demonstrated a solution alongside other members of the Global M2M Association at MobileWorld Congress in February 2015. Ericsson has also been working to develop the new mo-bile technologies that will enable use of IoT applications in the future, such as low-powerradio modules and the next generation of mobile technologies for 5G that will enable low la-tency and orders-of-magnitude increases in the number of connections.

Ericson's DCP aggregates devices (sensors and modules) and the messages to and fromthose devices at a gateway that connects to a network. The company sells the DCP to wire-less and wireline telecom network operators, and into some specific verticals as a primesolution provider, including the automotive sector. Ericsson says that one enterprise per dayis being added to DCP.

Figure 3: Ericsson's Positioning in the IoT Market & Technology Stack

Source: Ericsson (used with permission)

Anders Hillbur of Ericsson's cloud and IP business unit says that the network and connectiv-ity management are, de facto, a common architecture and platform for all applications:"This part of the IoT value chain requires a platform approach so new applications can bedeveloped by multiple users," he adds.

Hillbur says that it is important to be able to deploy a global platform that can deal with thesituation that operators' core networks are all slightly different. "For a global IoT applicationdeveloper or service provider, it is better not to have to integrate the application separatelywith multiple operators' networks, but to use a global system and platform. That's what Er-icsson offers." Of course, operator customers of Ericsson can offer this to customers on aglobal basis, too.

Ericsson says service enablement can also be made horizontal, though the company recog-nizes that the more legacy technology there is to be integrated, the harder it is to adopt aplatform approach. Its SEP is composed of several products that, together with productsfrom ecosystem partners, enable service creation and exposure, ecosystem management,personalized and dynamic user experience management, analytics and data management,customer and revenue management, and device management.

-

7/25/2019 2016-01-19_iot_platforms

18/25

HEAVY READING | JANUARY 2016 | IOT PLATFORMS: CHASING VALUE IN A MATURING MARKET 18

6.6 Jasper

Jasper is one of the longest-established vendors of platforms for IoT, and its Control Centersupports IoT applications around the world. The company's platform supports services of-fered and used by some of the biggest names globally, including operators AT&T andTelefnica and enterprises such as ABB, Heineken and Minolta, among very many others.

Jasper was founded in 2004 with the aim of supporting what it believed was an inevitabletransition that product companies would make as products became connected and func-tioned as the platform for services. Jasper believes that the way the IoT platform marketwill develop is analogous to the way enterprise software developed: first a do-it-yourself ap-proach, then an off-the-shelf software approach and then managed services.

Jasper's core platform in called Control Center. It delivers rules-engine-based lifecycle man-agement (encompassing device and connection management) for enterprise IoT services ofmultiple types. The solution is customizable and configurable to suit applications in differentsectors there are over 100 APIs northbound and southbound from the platform.

The company's VP of Strategy, Macario Namie, says there is no "generic IoT solution," rather,everything needs wrapping into a specific vertically oriented solution. Control Center deliversthe service lifecycle part of the solution, which is capable of being made generic. In commonwith most IoT platform vendors, Jasper develops its solution in partnership with its users.

There are functions/features that are too specific for Jasper to put them on to its platform it has declined to do so in the past in some cases. Namie points out that data managementand analytics is too sector specific to be included in a broadly applicable IoT platform. Rather,vertical-oriented data management platforms can incorporate service lifecycle management,and Namie cites GE's Predix as an example of a data management and analytics platformthat is integrated with Jasper's platform. Jasper also works with system integrators (it has apartnership with Accenture and works with many others including Deloitte).

Control Center is delivered exclusively through mobile operators worldwide. Namie says thatwhile mobile operators have variable record in building solutions, the Jasper platform hasserved mobile operators very well, and the arrangement has worked well for Jasper, too:"Mobile operators have great reach and sales/marketing capabilities. For Jasper, they are avery good route to market," says Namie. Jasper uses a software-as-a-service (SaaS) model,taking a percentage of revenues MOs charge for whatever IoT service is enabled by the Jas-per platform. Recent customers include major operators in Asia/Pacific, including Reliance inIndia and an operator in Thailand.

Control Center differs from some other platforms in being hosted from Jasper's own datacenters (15 of them around the world) rather than on public cloud infrastructure. Namiesays that "many application areas have legal or corporate requirements as to where data

can go e.g., for government or military or big enterprises and public cloud based servicesare forbidden." He adds that the company is looking into public cloud delivery, but has noplans to change the service delivery architecture right now.

6.7 Oracle

Oracle has a very extensive range of solutions that support the commercialization and oper-ation of the IoT. The company's depth of involvement with telecom operators and other

-

7/25/2019 2016-01-19_iot_platforms

19/25

HEAVY READING | JANUARY 2016 | IOT PLATFORMS: CHASING VALUE IN A MATURING MARKET 19

service providers, and with the enterprises that are the users of many IoT applications andservices, means it is well positioned to understand how IoT will develop and what is needed.

Two business units contribute the most significant relevant products and solutions: OracleCommunications and Oracle Fusion Middleware. Between them, these units deliver plat-

forms for business operation, network and policy management, and application enablement.In addition, the Oracle Internet of Things Cloud Service enables asset- and service-intensiveprocesses within business applications to interact with devices and equipment in the physi-cal world. Oracle partners to deliver industry solutions and enterprise applications.

Figure 4: Oracle's IoT Solutions Overview

Source: Oracle (used with permission)

Oracle Communications products making up the business operations platform include a hostof business support systems developed from those that support communications services inmany operators around the world. Among the most significant solutions is Oracle Communi-cations Billing and Revenue Management (BRM), which is used within other IoT platforms,as well as Oracle's own. Other components of the Oracle business operations platform in-clude customer, partner and channel management, order management and activation, andservice exposure and delivery. Among the IoT customers for Oracle's business operationsplatform are service providers Verizon Telematics, OnStar (General Motors' vehicle telemat-ics and connected car business), Lyse (smart home and utility services), Minacs (IToutsourcing) and Cisco (uses BRM to underpin charging for its enterprise services).

The company's network and policy management platform includes solutions from its Tekelecacquisition, including Policy and Charging Rules Function (PCRF). The platform delivers sub-scriber data management and Diameter routing, as well as policy management. Thisfunctionality is embedded in Jasper's IoT platform and also used by OnStar and Verizon.

Oracle's application enablement platform includes the Oracle IoT Cloud Service (launched inOctober 2015). The company says this service allows organizations to bridge the gap be-tween operational technology (OT) and IT systems, move from manual monitoring and

-

7/25/2019 2016-01-19_iot_platforms

20/25

HEAVY READING | JANUARY 2016 | IOT PLATFORMS: CHASING VALUE IN A MATURING MARKET 20

reactive controls to more active command and control of the assets/equipment and providepredictive maintenance, better asset tracking, utilization and improved customer services.Core features include:

Connect:connecting to devices/sensors directly or indirectly via gateways, device

virtualization, high-speed bi-directional messaging, end-to-end security (with devicelifecycle management and secure communication).

Analyze:analysis of device streams, both in real time, using stream processingcomponents and big data analysis for event generation, pattern recognition, predic-tive analytics and business intelligence.

Integrate/Act:integration with a variety of applications and platform-as-a-service(PaaS) services. The service provides out-of-the-box integration with manufacturingapps (E-Business Suite and JD Edwards), transportation apps and PaaS services,such as Integration Cloud Service, Mobile Cloud Service and BI Cloud Service.

Oracle has also developed partnerships to create white-label managed IoT services that canbe rapidly branded and offered by communications service providers. Oracle Communica-

tions provides the business and operations management platforms, and Tata ConsultancyServices has developed a range of eight ready-made IoT applications in the areas of con-nected cars, connected buildings, security and mobile health. Oracle also partners with, andsells to, other solution builders and service providers (including Minacs, Lyse and VerizonTelematics) and will also sell platforms directly to enterprises, bringing in service providersas partners, if required.

6.8 PTC

PTC provides industrial enterprise software, largely to the manufacturing sector. Its portfoliospans CAD, mathematical computing, technical publishing and application, product and ser-vice lifecycle management. The company has become a major IoT player over the last twoyears, having spent over $700 million in acquisitions and through organic development.

PTC's CEO, Jim Heppelmann has also contributed to industry debate on the impact of theIoT on business. Its IoT tech stack, largely built through acquisitions, complements the restof its portfolio, as its customers connect more of their products to the Internet. PTC de-scribes this as a move to "smart, connected products." Its IoT solutions have beensuccessful in the following sectors: manufacturing, agriculture, smart cities, utilities, build-ing management and telematics.

In 2013, PTC acquired ThingWorx, a well-established rapid application development platformfor IoT. It includes the ThingWorx Composer (an application modeling environment), CodelessMashup Builder (a drag-and-drop graphical user interface [GUI] for build applications fromcomponents), data storage and SQEAL structured query engine, collaboration platform, an or-chestrator for business process management and a data integration framework (or hub). In2014, the company acquired Axeda, which added device connectivity management (devicecloud), new customers and a way to address new markets for PTC's solutions.

PTC acquired Coldlight in May 2015, boosting the company's capabilities in the data layer ofthe IoT technology stack. The Coldlight Neuron predictive analytics solution has been re-branded as ThingWorx Machine Learning. It offers machine-learning-based analysis ofhistorical data for multiple purposes in the manufacturing context, such as predicting utiliza-tion levels, improving factory operations, preventing defects, increasing yields andimproving sales targeting.

-

7/25/2019 2016-01-19_iot_platforms

21/25

HEAVY READING | JANUARY 2016 | IOT PLATFORMS: CHASING VALUE IN A MATURING MARKET 21

More recently, PTC has acquired the augmented reality specialist Vuforia, and has announcedit is intending to buy Kepware, a software development company that provides communica-tions connectivity to industrial automation environments. These acquisitions, coupled with itslong history lifecycle management for industry, make PTC one of the most interesting compa-nies in the industrial IoT space.

PTC's IoT business is run under the ThingWorx brand, and consists of the capabilities fromthese acquisitions. ThingWorx supports multiple connectivity options (including multiple de-vice clouds), and can be deployed on-premises, in the cloud or embedded into other solutions.

PTC points out that it is a large player in the IoT platform market: It has 6,000 employees intotal and has an R&D budget of $100 million. "There are hundreds of companies just provid-ing device cloud," says Russ Fadel, president and GM of PTC's ThingWorx division, ""but ourcompetitors are those that can offer end-to-end solutions, including application platforms. Wecompete with some very large enterprise software players, manufacturing technology special-ists and some networking players that are either building their own IoT platform capability oracquiring it. We compete on the basis of our ability to execute at scale." Fadel adds thatThingWorx has been growing very fast, adding 500 new customers per year.

PTC sells its platforms both directly to enterprise customers and through partners. Referencesinclude enterprises such as Caterpillar and GE (its "Brilliant Factory" concept uses ThingWorx),IoT app and solution builders such as OnFarm, telcos such as AT&T and Docomo (with five tosix deals more lined up, Fadel says), and cloud infrastructure specialists such as Wind River.It also works with system integrators such as Accenture, Wipro, HCL and Infosys. More than400 colleges and universities worldwide also use ThingWorx in the classroom. PTC says themission of its academic program is to teach young men and women the language of the IoT.

6.9 Telit

Telit is a U.K.-headquartered multinational manufacturer of cellular, short-range radio,

global navigation satellite system (GNSS) and automotive IoT modules, and IoT connectivityand platform services. It acquired U.S.-based IoT platform player ILS Technology (estab-lished by former IBM staff) in 2013, and rebranded the business as Telit IoT Platforms inSeptember 2015, retaining the deviceWISE product name as the core of Telit's IoT servicesbusiness. Telit is unusual among IoT platform vendors in having a portfolio that stretchesdeep into the device end of the value chain while also supporting application enablementand connectivity and data management.

Telit's core IoT platform and service offers are:

IoT Portal a PaaS solution offering managed connectivity using multiple networksand device clouds/connected device platforms, connectivity management (includingalarm setting and management dashboards), over-the-air device management func-

tionality, data management, security management and application enablement(through dashboards and integration with ERP and other enterprise software andmultiple clouds). IoT Portal is built on the deviceWISE Application EnablementPlatform(AEP) that connects devices to apps.

deviceWISE for MNOs the deviceWISE platform licensed to operators, IT out-sourcing companies and system integrators. Telit provides customization, integrationservices, technical maintenance and support. The customer can brand its own IoTservices based on the platform.

-

7/25/2019 2016-01-19_iot_platforms

22/25

HEAVY READING | JANUARY 2016 | IOT PLATFORMS: CHASING VALUE IN A MATURING MARKET 22

deviceWISE for Factory an industrial automation platform to connect productionmachinery and processes with enterprise applications. Architecture is scalable andthe platform is configurable, using a library of built-in standardized device driversand enterprise connectors. It is pre-configured for cloud connectivity. Manufacturingsectors where deviceWISE for Factory is suitable include automotive, pharmaceuti-

cals, machinery, oil and gas, power generation and water utilities.

Telit's ability to tightly integrate modules, connectivity and device management, as well asprovide an app enablement platform that leverages this integration, delivers tangible benefitsto IoT and M2M users, according to the company's CTO Fred Yentz: "We use industry-stand-ard TR50 MQTT APIs, and an agent installed on all our partner devices that interfaces with ourAsset Gateway to make it much easier to connect devices to the IoT. Our Proxy Gateway cando the same for legacy devices and avoids adding latency that can otherwise happen." Headds that Telit's ability to filter data by application means that its infrastructure isn't over-whelmed by consumer app data, increasing the robustness of Telit's industry-focused service.

Figure 5: Telit IoT Portal Functionality

Source: Telit Communications (used with permission)

The company also stresses the number of APIs it has developed to widely deployed enterprisesoftware and cloud platforms; it provides automatic interfacing to SAP Hana, for instance, and

its IoT platform serves as an on-ramp for Google Cloud Platform (GCP) and GE Predix.

Telit sells to enterprises in very many vertical markets, including transportation, agriculture,retail, healthcare, security/surveillance, food/drink, manufacturing, energy/buildings andautomotive. Reference customers include Cisco, SAP, Mitsubishi and Tennant (a large U.S.-based industrial equipment manufacturer), as well as some mobile operators for instance,it has worked with Proximus in Belgium to enable Smart City applications based on the LoRanetworking standard.

-

7/25/2019 2016-01-19_iot_platforms

23/25

HEAVY READING | JANUARY 2016 | IOT PLATFORMS: CHASING VALUE IN A MATURING MARKET 23

The company sells either full, end-to-end IoT enablement solutions, including modules andmultiple platform functionality, or solutions on an a la cartebasis. Revenue models aremixed and flexible: modules are charged for as a capex item, then a monthly volume-basedfee for connection is added. The enterprise gateway is a traditional software license ap-proach, and data storage is charged for in the same way as other cloud services. Public or

private clouds can be used depending on customer requirements.

6.10 Xively (LogMeIn)

Xively is a connected product management platform developed by LogMeIn, a provider ofremote connectivity, collaboration and customer engagement services delivered from thecloud. It enables products to be connected via a message broker to the Internet (providingRESTful APIs and SDKs for app developers) and allows devices, users and apps to be man-aged in an efficient way, organizing the data in device models and an object directory. Xivelywas created and continues to evolve in response to customer needs for organizing a con-nected business, integrating with existing business systems and app development support.

Xively is seeing traction in light-industrial or B2B2C applications that support connected prod-

ucts in the home (rather than in factories), in medical devices/healthcare and solar energy.Products connected via Xively include printers, home electronics equipment, environmentalmonitoring sensors and education, scientific and medical research equipment. "Our successhas been based on doing two things very well: connectivity at scale for concurrent messagesand providing structure to connected products and users. That's what is helping build con-nected products businesses," says Ryan Lester, director of product marketing for Xively.

Xively works with partners throughout the IoT value chain, from chip and module vendorssuch as ARM, Qualcomm and Freescale, through cloud stack specialists such as Heroku anddata management companies such as Splunk, to solution builders and enterprise applica-tions, including Salesforce, Mphasis and Global Logic. Lester says that wireless operatorshave a legitimate place in the IoT value chain and Xively is in discussion with operators allthe time; it has worked much more with service integrators/solution builders.

Xively is built on the MQTT message bus standard as a way to improve the performance ofdata transport from connected products to the platform. The company points out that appli-cations may need to scale from a few thousand up to a few million concurrent messageswhile maintaining sub 100ms message time.

A significant development during 2015 involves ID and access management. "Xively simpli-fies authentication and solves several IoT security issues," says Lester. It can create anobject model for every entity that accesses devices and applications it has templates foreach of these entities and the model contains the permission information, so messagesbetween the entities can be checked against the model to ensure the necessary permissionsare in place. In October 2015, LogMeIn added Identity Manager to Xively. The companysays this provides an easy-to-implement option for onboarding and managing new IoT endusers; it is applicable to Web and mobile applications.

Xively is moving along the value chain (and up the technology stack) from connectivitymanagement to application enablement, where it will escape from the commoditization ofconnectivity but start to meet different, well-established competitors. Indeed, Lesteracknowledges that modeling a connected business is very important for Xively, adding thatthe company is "offering a real out-of-the-box service much more than the frameworksand concepts that some other enablement platform providers offer."

-

7/25/2019 2016-01-19_iot_platforms

24/25

HEAVY READING | JANUARY 2016 | IOT PLATFORMS: CHASING VALUE IN A MATURING MARKET 24

7. CONCLUSIONS

While still in its early stages, vendors are certain that the market for IoT platforms is matur-ing; enterprises and smaller businesses that are developing IoT applications and servicesare recognizing that some of the technology challenges do not have to be solved afresh for

each application, but can be overcome by using appropriate horizontal platforms.

Platforms for device connection have reached the stage where supply is outstripping de-mand and prices are falling. This is causing those vendors whose platforms are efficient tobegin to add functionality around their initial connectivity offer and to reposition them-selves. They have found that some aspects of IoT, such as service lifecycle management,can be delivered on a platform, though other aspects remain very difficult to deliver effec-tively on a new cross-sector, horizontal platform. In particular, application developmentenvironments will continue to be those already used by developers, and much data analyticstechnology remains the preserve of sector specialists: deep vertical market expertise isneeded before an IoT application can be developed or even properly supported.

Even at a basic level, some vendors Aeris and Xively made the case strongly to us be-lieve there has been a lack of expertise of IoT application developers and also in theplatform market (particularly around the areas of security and scalability), which is leadingto significant hurdles that delay product development and end up costing more than antici-pated. Xively's Ryan Lester says: "The key to early success in the IoT will be reducing theinitial development costs and timeline by making easy for companies to connect productsand then mapping those products back to existing business systems."

Platform vendors recognize the role that telecom operators play in IoT: they can readilyprovide national and in some cases international connectivity, and it is relatively straightfor-ward to extend this offer to device and connectivity management (even if this requirespartnerships with other operators). Their experience with IT platforms stands them in goodstead as providers of other support to IoT app developers and business users. In particular,

as IoT reaches across more and more areas of commercial activity, the way that telecomcompanies resolved interoperability and standards issues may serve as a model for IoT.

Platform providers are also identifying the significance of industrial IoT as a sector with po-tential for direct sales, and many players in the space are beginning to form partnershipsand put together ecosystems in order to attack this market better. We expect this to be astrong feature of the IoT platform space throughout 2016 and 2017.

-

7/25/2019 2016-01-19_iot_platforms

25/25

TERMS OF USAGE

LICENSE AGREEMENTThis report and the information therein are the property of or licensed to Heavy Reading, and permis-sion to use the same is granted to purchasers under the terms of this License Agreement

("Agreement"), which may be amended from time to time without notice. The purchaser acknowledgesthat it is bound by the terms and conditions of this Agreement and any amendments thereto.

OWNERSHIP RIGHTSAll Reports are owned by Heavy Reading and protected by United States Copyright and internationalcopyright/intellectual property laws under applicable treaties and/or conventions. The purchaseragrees not to export this report into a country that does not have copyright/intellectual property lawsthat will protect Heavy Reading's rights therein.

GRANT OF LICENSE RIGHTSHeavy Reading hereby grants the purchaser a non-exclusive, non-refundable, non-transferable licenseto use the report for research purposes only pursuant to the terms and conditions of this Agreement.Heavy Reading retains exclusive and sole ownership of all reports disseminated under this Agreement.The purchaser agrees not to permit any unauthorized use, reproduction, distribution, publication or

electronic transmission of this report or the information/forecasts therein without the express writtenpermission of Heavy Reading.

DISCLAIMER OF WARRANTY AND LIABILITYHeavy Reading has used its best efforts in collecting and preparing this report. Heavy Reading, its em-ployees, affiliates, agents and licensors do not warrant the accuracy, completeness, currentness,noninfringement, merchantability or fitness for a particular purpose of any material covered by thisAgreement. Heavy Reading, its employees, affiliates, agents or licensors shall not be liable to the pur-chaser or any third party for losses or injury caused in whole or part by Heavy Reading's negligence orby contingencies beyond Heavy Reading's control in compiling, preparing or disseminating this report,or for any decision made or action taken by the purchaser or any third party in reliance on such infor-mation, or for any consequential, special, indirect or similar damages (including lost profits), even ifHeavy Reading was advised of the possibility of the same. The purchaser agrees that the liability ofHeavy Reading, its employees, affiliates, agents and licensors, if any, arising out of any kind of legal

claim (whether in contract, tort or otherwise) in connection with its goods/services under this Agree-ment shall not exceed the amount the purchaser paid to Heavy Reading for use of this report.