20150514 mobile money in latam gsma rio

32

Mobile Money in latin america Jesper Rhode Head of Marketing Ericsson Latin America and Caribbean

-

Upload

jesper-rhode-andersen -

Category

Documents

-

view

84 -

download

1

Transcript of 20150514 mobile money in latam gsma rio

Mobile Money in latin america

Jesper RhodeHead of MarketingEricsson Latin America and Caribbean

User trends

Market Insights

Asbanc Project

Future trends

M-Commerce Latam | Ericsson Internal | 2014-11-03 | Page 3

Ericsson ConsumerLabThe Voice of the Consumer

M-Commerce Latam | Ericsson Internal | 2014-11-03 | Page 4

Key Take-aways

Convenience a key driver for m-commerce for both strugglers and achievers.

1

Safety and control is essential for Latin Americans.

2

Consumers lack overall trust in institutions and network performance.

3

› There are three conclusive consumer take-aways from this m-commerce study in Latin America:

M-Commerce Latam | Ericsson Internal | 2014-11-03 | Page 5

Method and purpose of study

Method

• 4080 online interviews

• 30 expert interviews

• 50 in-depth interviews

• Diaries and “shop alongs”

• In home interviews

M-Commerce Latam | Ericsson Internal | 2014-11-03 | Page 6

Regions of study

The markets in focus for the study were chosen to achieve a mixture of geographical location, sociocultural factors and level of maturity of the telecom and financial sectors and consumer markets

BRAZIL ARGENTINA COLOMBIA CHILE MEXICO

M-Commerce Latam | Ericsson Internal | 2014-11-03 | Page 7

Barriers for not using mobile payments

M-Commerce Latam | Ericsson Internal | 2014-11-03 | Page 8

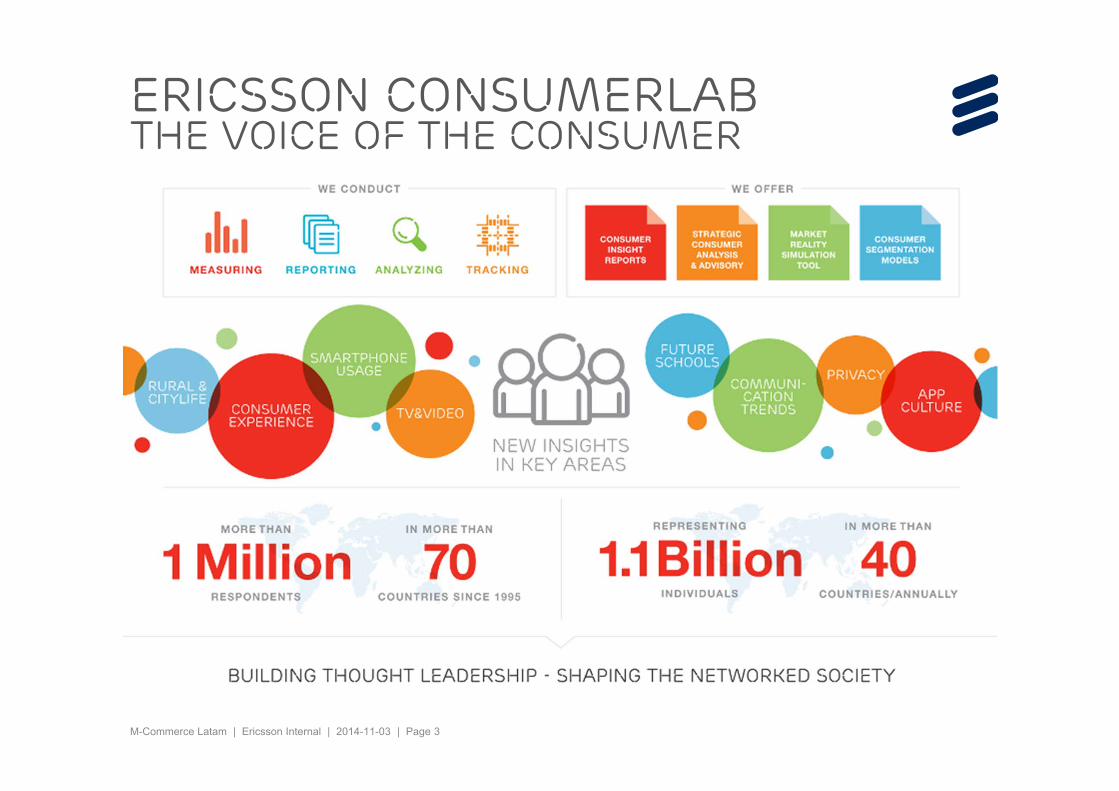

Payment for goods

M-Commerce Latam | Ericsson Internal | 2014-11-03 | Page 9

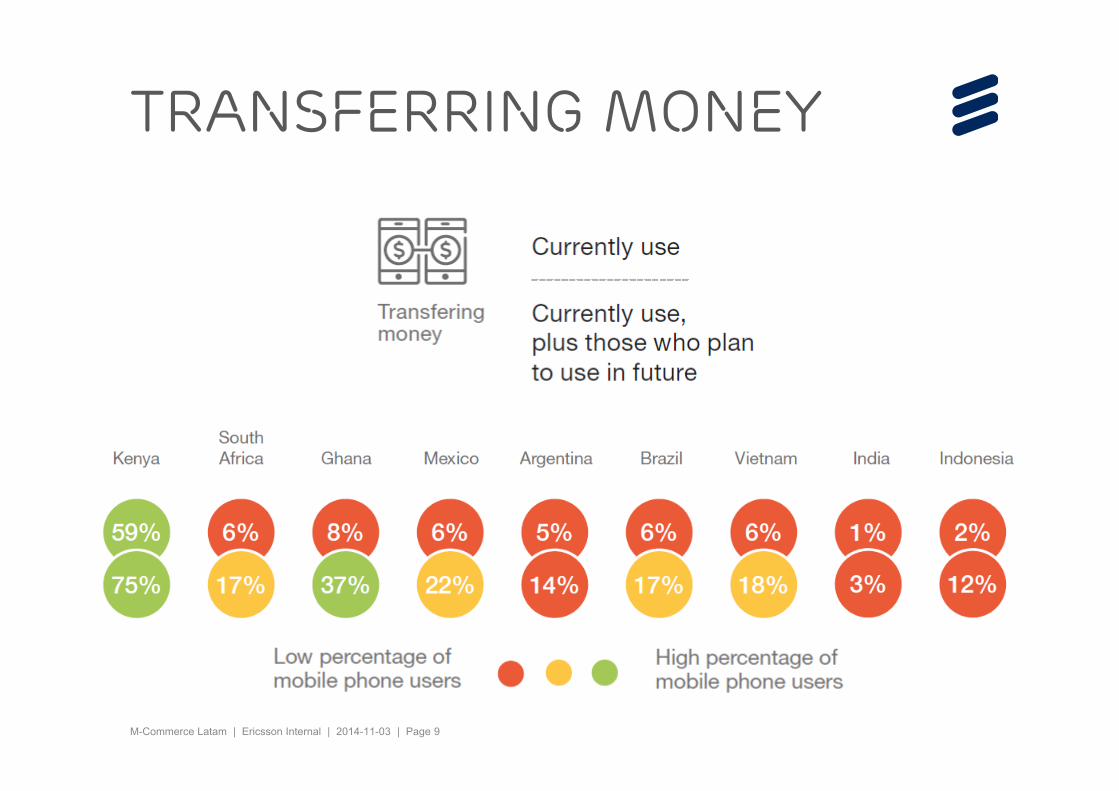

Transferring money

M-Commerce Latam | Ericsson Internal | 2014-11-03 | Page 10

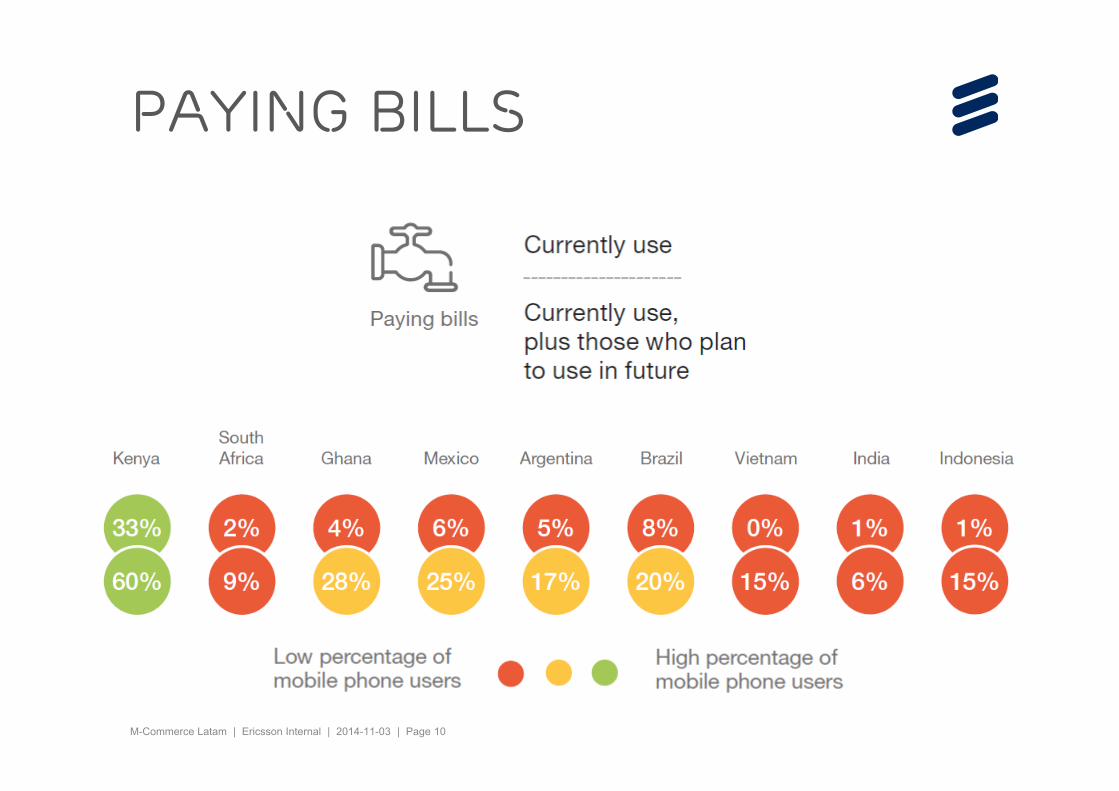

Paying bills

General market insights

M-Commerce Latam | Ericsson Internal | 2014-11-03 | Page 12

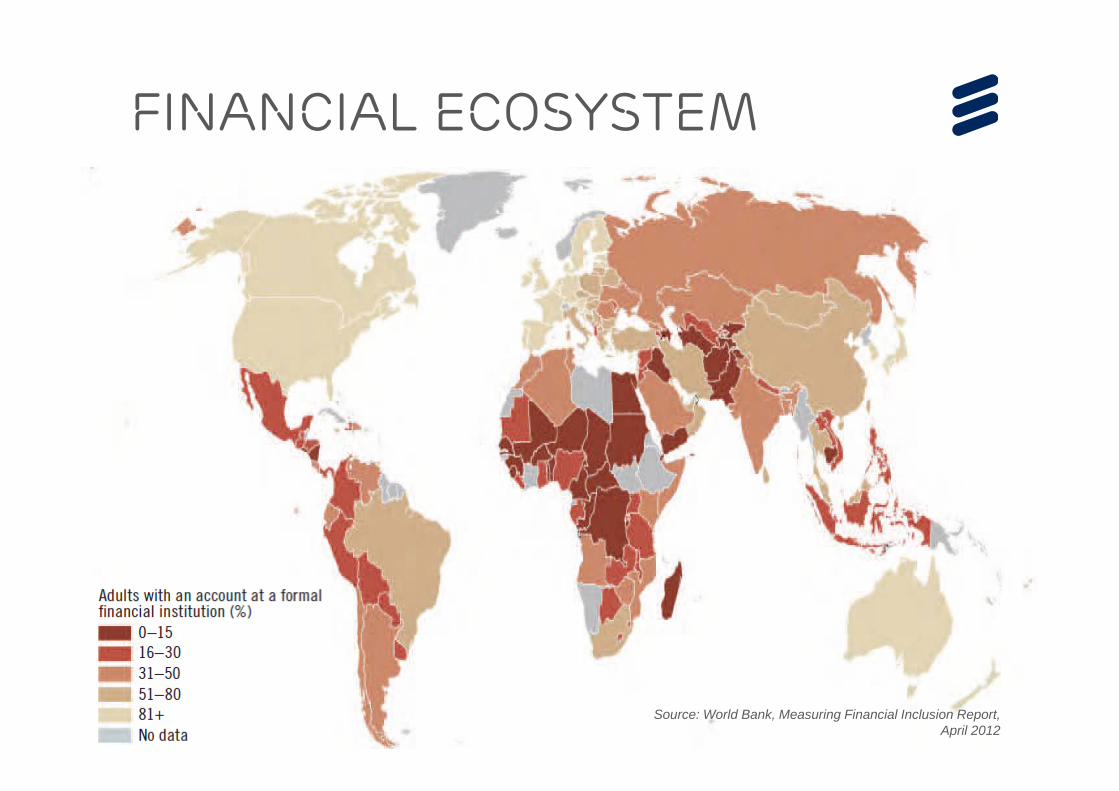

Financial Ecosystem

Source: World Bank, Measuring Financial Inclusion Report, April 2012

M-Commerce Latam | Ericsson Internal | 2014-11-03 | Page 13

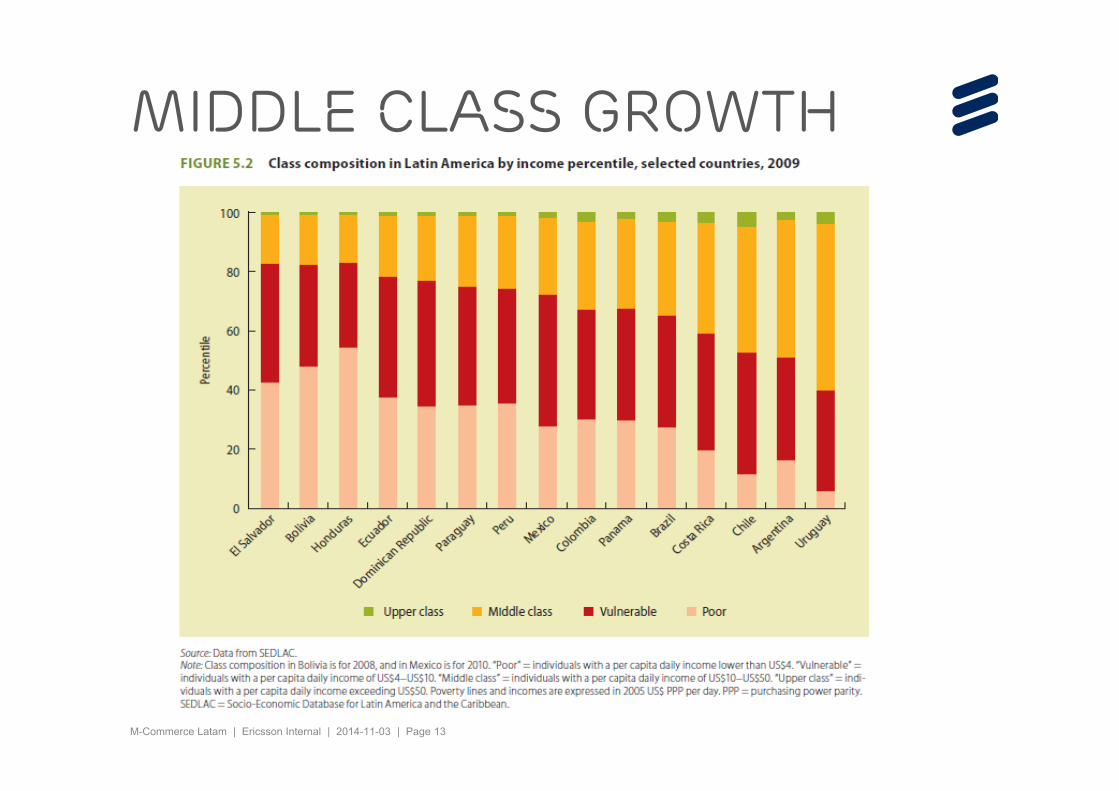

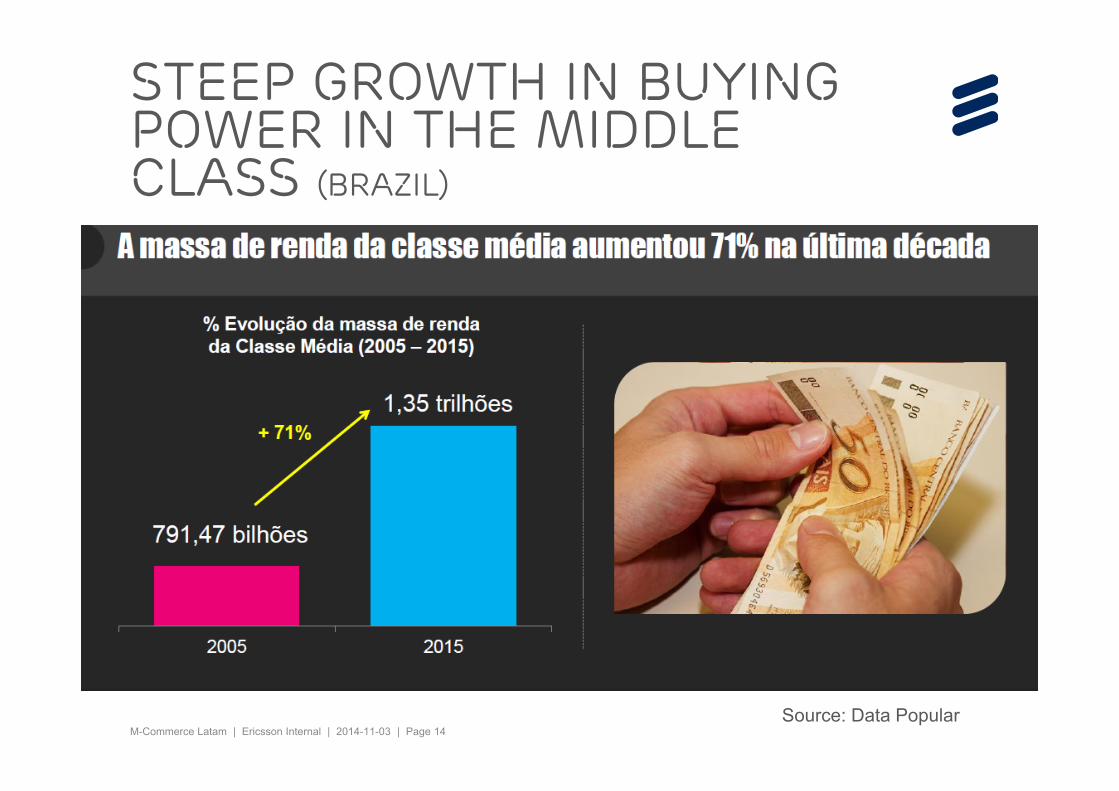

Middle class growth

M-Commerce Latam | Ericsson Internal | 2014-11-03 | Page 14

Steep growth in buying power in the middle class (brazil)

Source: Data Popular

M-Commerce Latam | Ericsson Internal | 2014-11-03 | Page 15

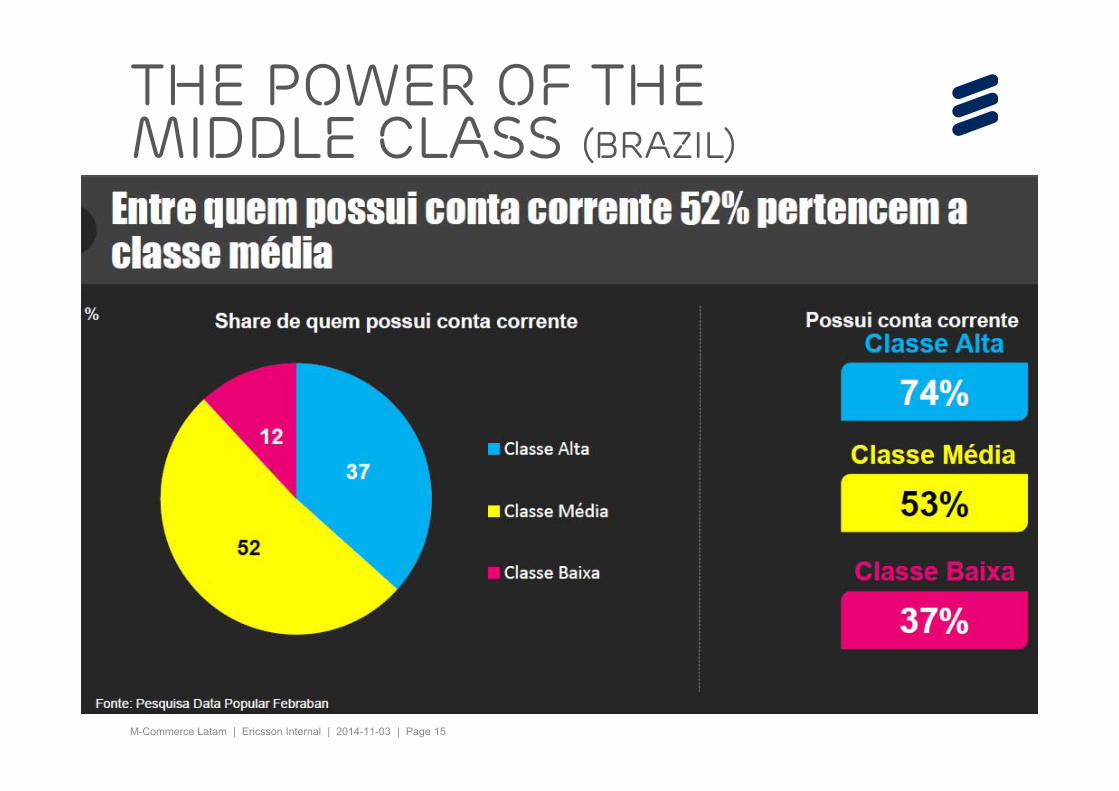

The power of the middle class (Brazil)

M-Commerce Latam | Ericsson Internal | 2014-11-03 | Page 16

Credit cards in the middle class (BRAZIl)

Source: Data Popular

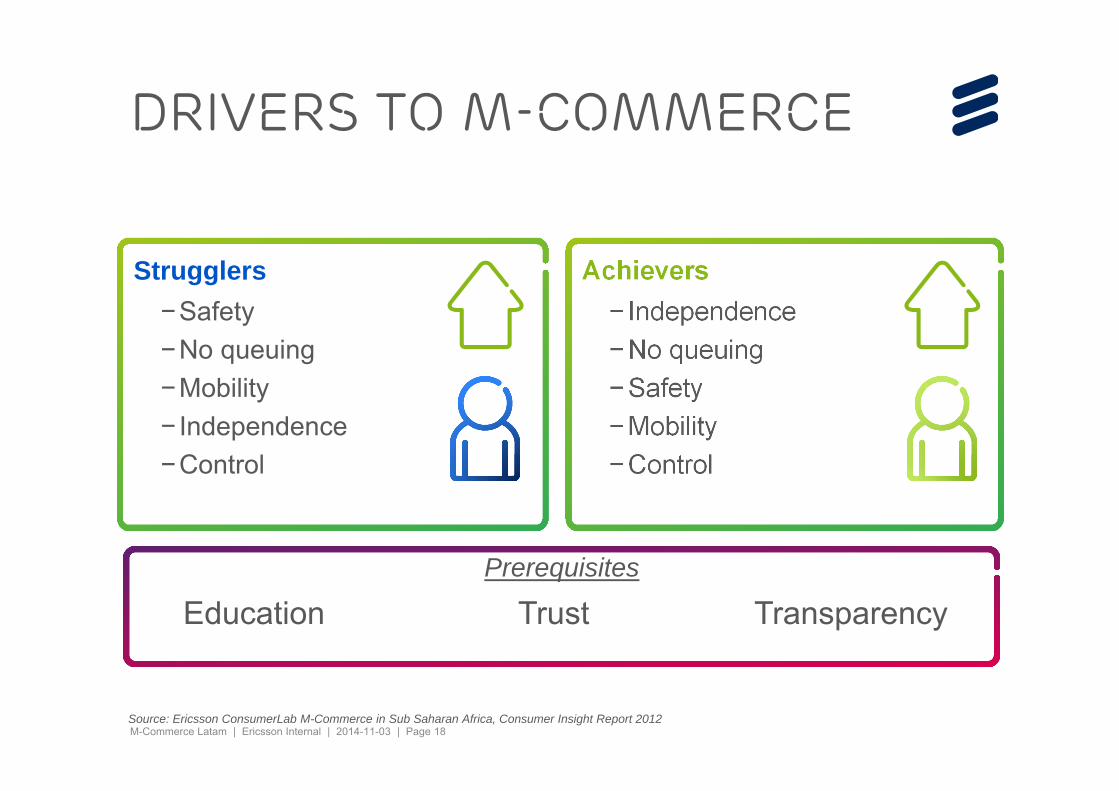

M-commerce: drivers & barriers

M-Commerce Latam | Ericsson Internal | 2014-11-03 | Page 18

Drivers to m-commerce

Achievers− Independence−No queuing−Safety−Mobility−Control

Prerequisites

Source: Ericsson ConsumerLab M-Commerce in Sub Saharan Africa, Consumer Insight Report 2012

Education Trust Transparency

Strugglers−Safety−No queuing−Mobility− Independence−Control

M-Commerce Latam | Ericsson Internal | 2014-11-03 | Page 19

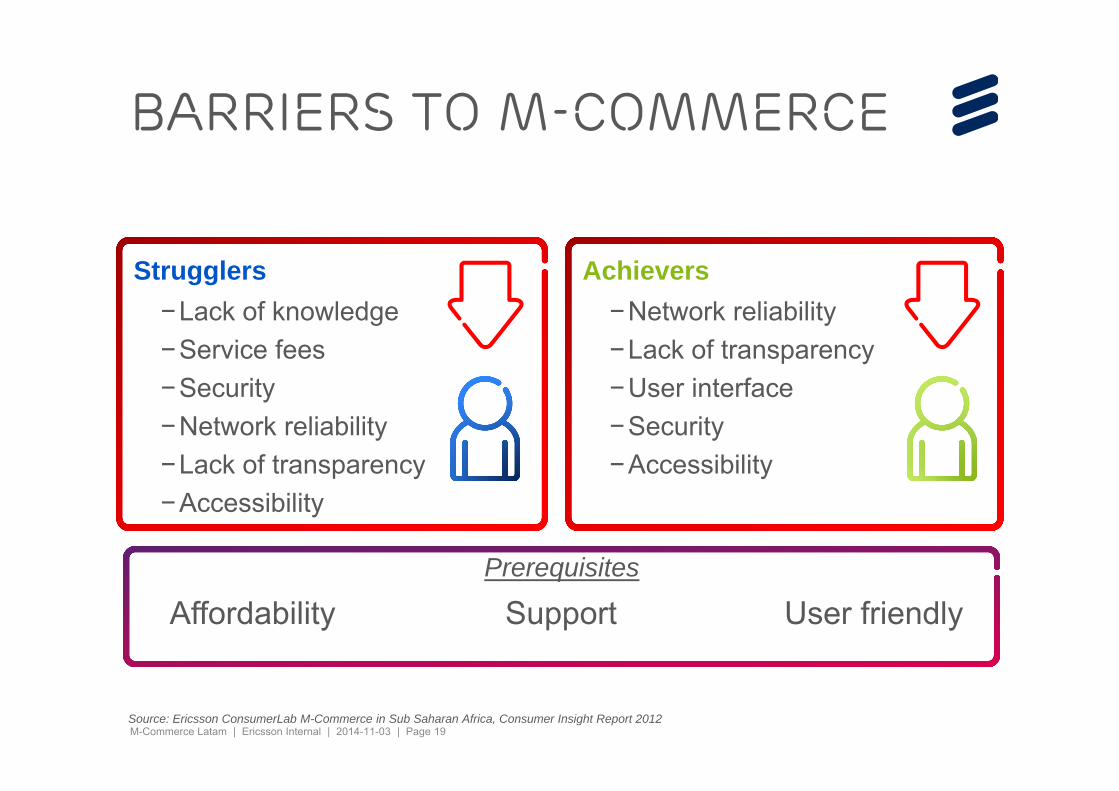

Barriers to m-commerce

Achievers−Network reliability−Lack of transparency−User interface−Security−Accessibility

Prerequisites

Source: Ericsson ConsumerLab M-Commerce in Sub Saharan Africa, Consumer Insight Report 2012

Strugglers−Lack of knowledge−Service fees−Security−Network reliability−Lack of transparency−Accessibility

Affordability Support User friendly

Relationship:Banks & operators

M-Commerce Latam | Ericsson Internal | 2014-11-03 | Page 21

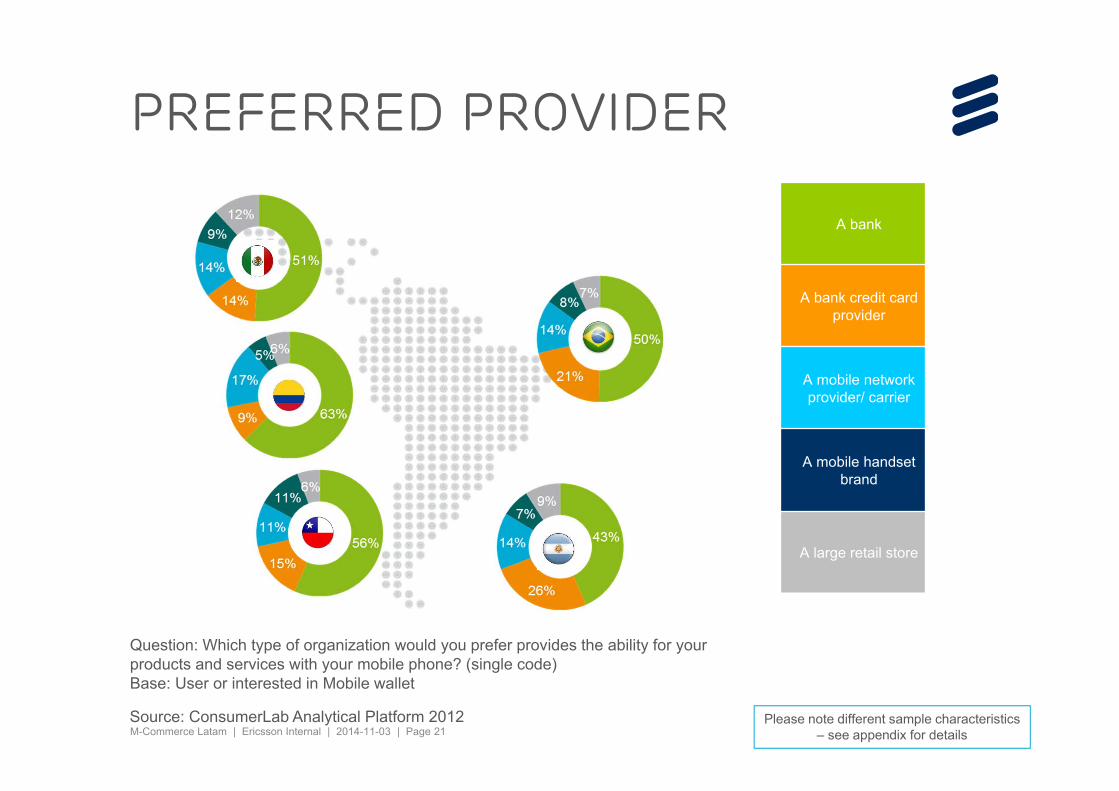

Preferred provider

Question: Which type of organization would you prefer provides the ability for your products and services with your mobile phone? (single code)Base: User or interested in Mobile wallet

Please note different sample characteristics– see appendix for details

Source: ConsumerLab Analytical Platform 2012

A bank

A bank credit card provider

A mobile network provider/ carrier

A mobile handset brand

A large retail store

M-Commerce Latam | Ericsson Internal | 2014-11-03 | Page 22

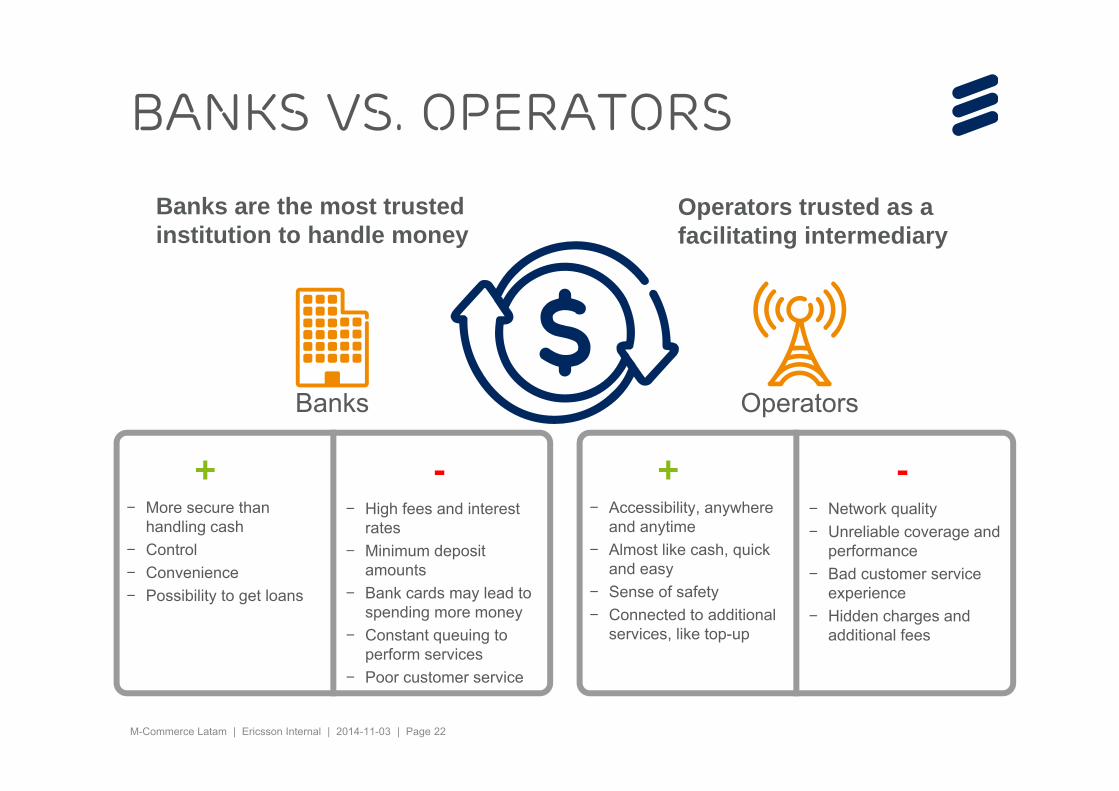

Banks vs. Operators

OperatorsBanks

Banks are the most trusted institution to handle money

Operators trusted as a facilitating intermediary

– More secure than handling cash

– Control– Convenience– Possibility to get loans

– High fees and interest rates

– Minimum deposit amounts

– Bank cards may lead to spending more money

– Constant queuing to perform services

– Poor customer service

+ -– Accessibility, anywhere

and anytime– Almost like cash, quick

and easy– Sense of safety – Connected to additional

services, like top-up

– Network quality– Unreliable coverage and

performance– Bad customer service

experience– Hidden charges and

additional fees

+ -

M-commerceWITH ASBANC PERU

M-Commerce Latam | Ericsson Internal | 2014-11-03 | Page 24

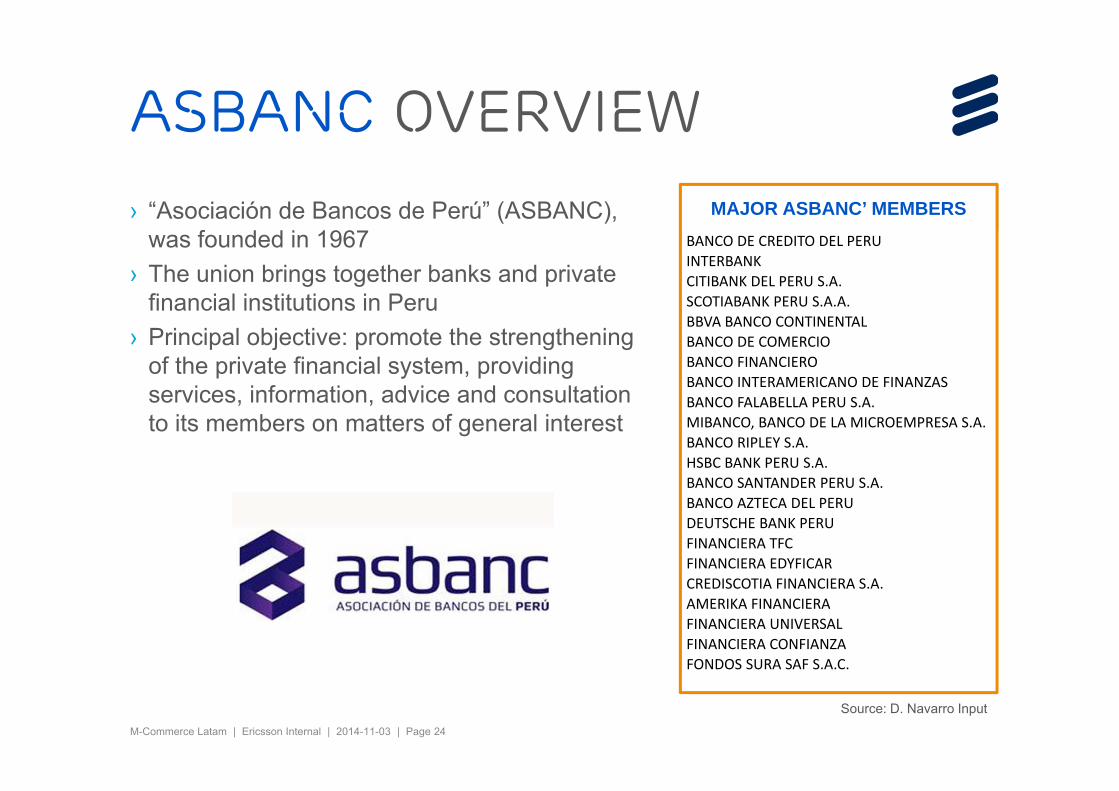

› “Asociación de Bancos de Perú” (ASBANC), was founded in 1967

› The union brings together banks and private financial institutions in Peru

› Principal objective: promote the strengthening of the private financial system, providing services, information, advice and consultation to its members on matters of general interest

ASBANC OVERVIEWMAJOR ASBANC’ MEMBERS

BANCO DE CREDITO DEL PERUINTERBANKCITIBANK DEL PERU S.A.SCOTIABANK PERU S.A.A.BBVA BANCO CONTINENTALBANCO DE COMERCIOBANCO FINANCIEROBANCO INTERAMERICANO DE FINANZASBANCO FALABELLA PERU S.A.MIBANCO, BANCO DE LA MICROEMPRESA S.A.BANCO RIPLEY S.A.HSBC BANK PERU S.A.BANCO SANTANDER PERU S.A.BANCO AZTECA DEL PERUDEUTSCHE BANK PERUFINANCIERA TFCFINANCIERA EDYFICARCREDISCOTIA FINANCIERA S.A.AMERIKA FINANCIERAFINANCIERA UNIVERSALFINANCIERA CONFIANZAFONDOS SURA SAF S.A.C.

Source: D. Navarro Input

M-Commerce Latam | Ericsson Internal | 2014-11-03 | Page 25

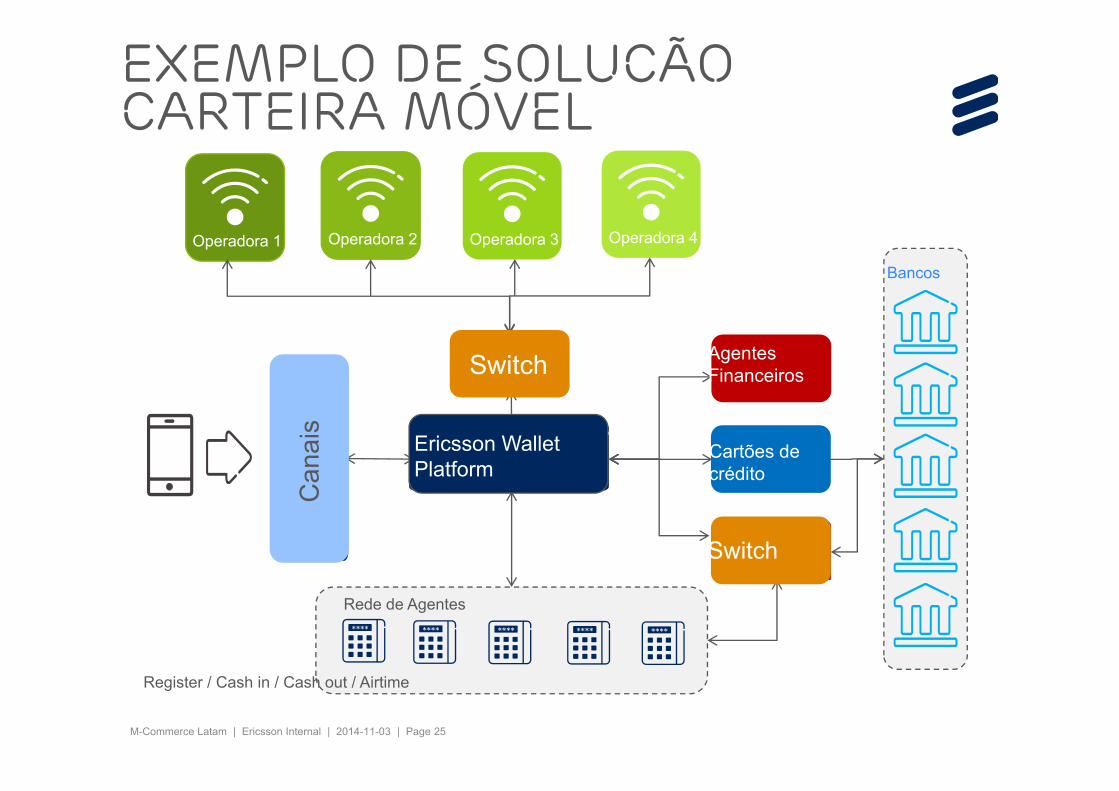

ExEMPLO de Solucão Carteira móvel

Switch

Cha

nnel

s ASBANC Wallet Platform

Switch

Bancos

Rede de Agentes

Operadora 1 Operadora 3 Operadora 4Operadora 2

Agentes Financeiros

Cartões de crédito

Switch

Switch

Ericsson Wallet Platform

Can

ais

Register / Cash in / Cash out / Airtime

M-Commerce Latam | Ericsson Internal | 2014-11-03 | Page 26

HOW TO CREATE SUSTAINABLE M-COMMERCE ECOSYSTEM?

Stage 1Basic connectivityCritical mass of mobile coverage and penetration among rural poor

Stage 2Digital remote paymentsPoor people adopt and use digital for person-to-person transfers and government payments

Stage 3Full range of digital financial servicesPoor people adopt and use digital for savings, credit and insurance services

Stage 4Digital in-store purchasesPoor people conduct a majority of transactions (including small in-store purchases) digitally.

Inclusive digital Economy

M-Commerce Latam | Ericsson Internal | 2014-11-03 | Page 27

supporting financial inclusion in peru

Mobile coverage

Connecting local partners

Financial Training

People Development

Socio-Economic growth

Enable baseline and socio-economic impact measurements

Educate the population about their rights and duties, regarding to financial and insurance system and also the private pension funds

Promote better access and use to financial services to the population, so it will lead an increase in the well

Connect local partners (NGOs) that will train communities for m-Commerce and others

Partners receive free training in financial literacy and have the opportunity to transmit this knowledge and experience to the community

The ecosystem

Alignment is needed from all parties involved in the

mobile banking ecosystem for these services to reach

more people

The Future ofpayments

M-Commerce Latam | Ericsson Internal | 2014-11-03 | Page 29

Integrated payment

M-Commerce Latam | Ericsson Internal | 2014-11-03 | Page 30

Integrated relationship

M-Commerce Latam | Ericsson Internal | 2014-11-03 | Page 31

Disruption I the horizon