Secure Payments: How Card Issuers and Merchants Can Stay Ahead of Fraudsters

Upload

dennis-van-allemeerschCategory

view

120download

0

1 1

TITEL Future of check-out

Merchants & Payments 2015

London, September 15th

2 2

3 3

Online

Travel

Agency

2002

~110

Hotel Booker ?

4 4

REACH

5 5

Trend: Rise alternative payment methods

… however: hassle from merchant perspective

6 6

Thesis: Reach = Ease of use for merchant

… however: European payment methods don’t

have enough footprint <> rise of global giants

7 7

Challenge: I welcome them as merchant

… because: prepared to pay bit more for ease of

use & big reach

=

8 8

EASE

9 9

Trend: Further European payments integration

… however: focus on ‘traditional’ payments, online

still too country specific (= hassle)

XS2A

10 10

Thesis: Online payments market only mature at a

national level

… because: too fragmented, making it difficult for

cross-border trade & merchants in particular

11 11

Challenge: Seamless integration and at a min.

interoperability (ideally full harmonization)

… accelerating the API-economy for banks, with

further regulation as potential pressure instrument

12 12

CONVERSION

13 13

Trend: Alternative identification & authentification

… safe, but simple and ideally integrated

identification & authentification

14 14

Trend: … and no trend would be complete

w/o Mobile of course

… once at the booking page, bring clients as fast

as possible to payment w/o need to think

=> 1 (2) - click payment, also on mobile!

15 15

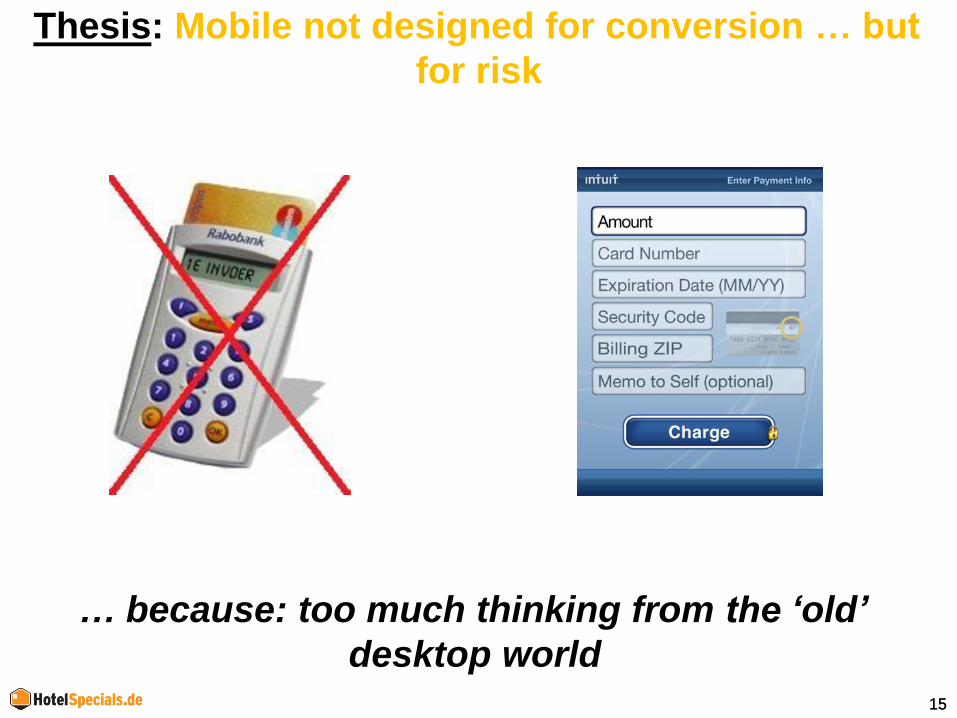

Thesis: Mobile not designed for conversion … but

for risk

… because: too much thinking from the ‘old’

desktop world

16 16

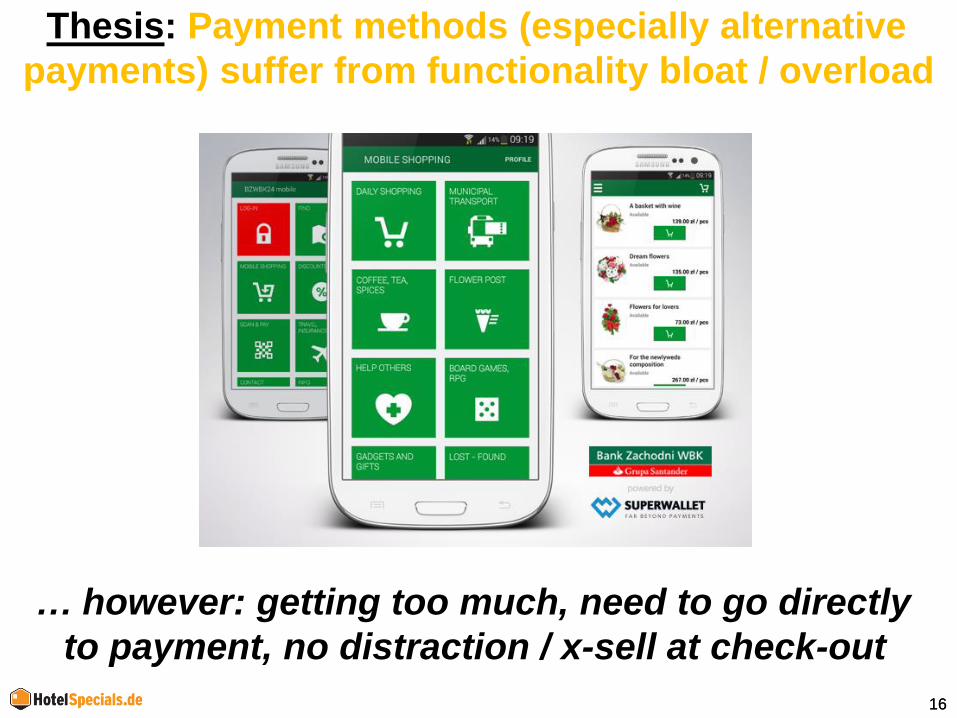

Thesis: Payment methods (especially alternative

payments) suffer from functionality bloat / overload

… however: getting too much, need to go directly

to payment, no distraction / x-sell at check-out

17 17

Challenge: Innovation needs to serve simplification

instead of diversification !

… less is more!

Stick to your core trade ?!

18 18

Challenge: Mobile innovation also needs to facilitate

x-border ease of use

… ideally with 1 European protocol for mobile

payments

19 19

COST

20 20

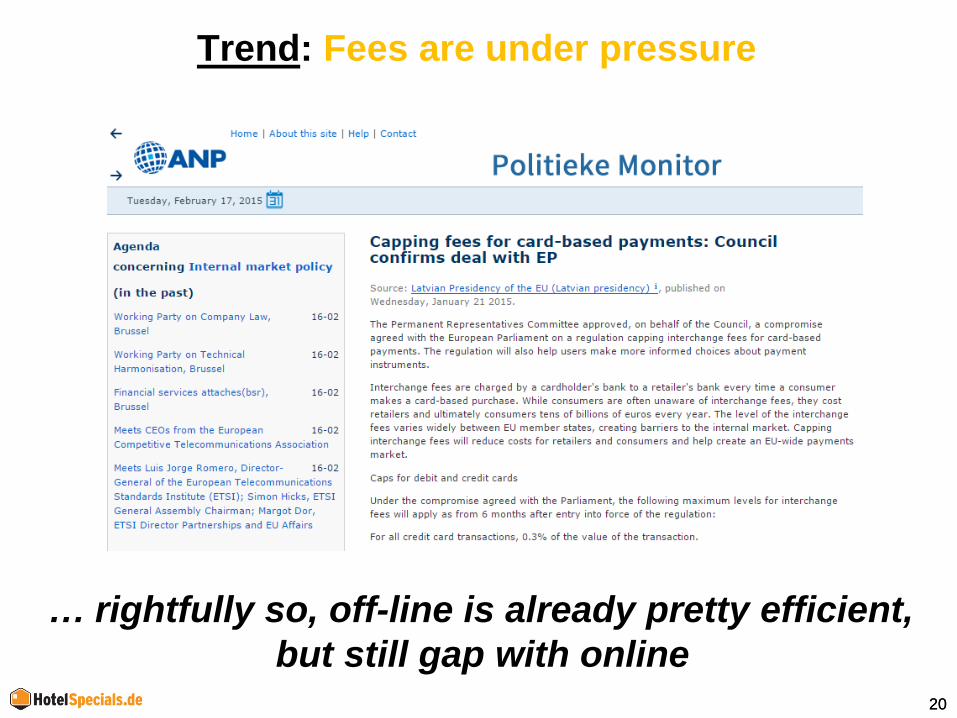

Trend: Fees are under pressure

… rightfully so, off-line is already pretty efficient,

but still gap with online

21 21

Thesis: Not only direct, but also indirect costs need

to go down

… because: payment disruptions cost money and

settlement days still date from the batch days

22 22

Challenge: Reduce payment disruptions

… invest again in online payments (tackle legacy)

+ manage perception

23 23

Challenge: eliminate T+2/3 settlement days

… because transactions are more & more real-time,

with also here pressure of further regulation