2015 Second Quarter Results · 2020. 12. 10. · 2015 Second Quarter Results Maracay Homes...

34

2015 Second Quarter Results Maracay Homes – Pardee Homes – Quadrant Homes – Trendmaker Homes – TRI Pointe Homes – Winchester Homes

Transcript of 2015 Second Quarter Results · 2020. 12. 10. · 2015 Second Quarter Results Maracay Homes...

2015 Second Quarter ResultsMaracay Homes – Pardee Homes – Quadrant Homes – Trendmaker Homes – TRI Pointe Homes – Winchester Homes

Forward Looking Statement

Various statements contained in this presentation, including those that express a belief, expectation or intention, as well asthose that are not statements of historical fact, are forward-looking statements. These forward-looking statements may includeprojections and estimates concerning the timing and success of specific projects, our ability to achieve the anticipated benefitsof the Weyerhaeuser Real Estate Company (WRECO) transaction and our future production, operational and financial results,financial condition, prospects, and capital spending. Our forward-looking statements are generally accompanied by wordssuch as “estimate,” “project,” “predict,” “believe,” “expect,” “intend,” “anticipate,” “potential,” “plan,” “goal,” “will,” or other words that convey future events or outcomes. The forward-looking statements in this presentation speak only as of the date of this presentation, and we disclaim any obligation to update these statements unless required by law, and we caution you not to rely on them unduly. These forward-looking statements are inherently subject to significant business, economic, competitive,regulatory and other risks, contingencies and uncertainties, most of which are difficult to predict and many of which are beyondour control. The following factors, among others, may cause our actual results, performance or achievements to differmaterially from any future results, performance or achievements expressed or implied by these forward-looking statements: theeffect of general economic conditions, including employment rates, housing starts, interest rate levels, availability of financingfor home mortgages and strength of the U.S. dollar; market demand for our products, which is related to the strength of thevarious U.S. business segments and U.S. and international economic conditions; levels of competition; the successfulexecution of our internal performance plans, including restructuring and cost reduction initiatives; global economic conditions;raw material prices; energy prices; the effect of weather; the risk of loss from earthquakes, volcanoes, fires, floods, droughts,windstorms, hurricanes, pest infestations and other natural disasters; transportation costs; federal and state tax policies; theeffect of land use, environment and other governmental regulations; legal proceedings; risks relating to any unforeseenchanges to or effects on liabilities, future capital expenditures, revenues, expenses, earnings, synergies, indebtedness,financial condition, losses and future prospects; the risk that disruptions from the WRECO transaction will harm our business;our ability to achieve the benefits of the WRECO transaction in the estimated amount and the anticipated timeframe, if at all;our ability to integrate WRECO successfully and to achieve the anticipated synergies therefrom; changes in accountingprinciples; our relationship, and actual and potential conflicts of interest, with Starwood Capital Group or its affiliates; andadditional factors discussed under the sections captioned “Risk Factors” included in our annual and quarterly reports filed withthe Securities and Exchange Commission. The foregoing list is not exhaustive. New risk factors may emerge from time to timeand it is not possible for management to predict all such risk factors or to assess the impact of such risk factors on ourbusiness.

Management Team

Michael GrubbsChief Financial Officer

• 28 years of real estate and homebuilding experience

• Former SVP / CFO of William Lyon Homes

• Previously, real estate accountant at Kenneth Leventhal

Douglas BauerChief Executive Officer

• 28 years of real estate and homebuilding experience

• Former President and COO of William Lyon Homes

• Previously, managed WLH Northern California Division

Thomas Mitchell President & COO

• 28 years of real estate and homebuilding experience

• Former EVP and Southern California Regional President at William Lyon Homes

Working together for over 20 years, TRI Pointe senior management has significant experience running a large, geographically diverse, growth-oriented public homebuilder. Deep managerial talent at each operating division with key local relationships supports dynamic tailored growth strategies.

3

Market: Greater Puget Sound Area

LTM Orders: 399 LTM Deliveries: 355

LTM HB Revenue: $157,060 LTM ASP: $442

Lots Owned or Controlled: 1,416Markets: Washington DC,

Richmond

LTM Orders: 377

LTM Deliveries:394

LTM HB Revenue: $265,605

LTM ASP: $674

Lots Owned or Controlled: 2,732

Markets: Phoenix, Tucson

LTM Orders: 505 LTM Deliveries: 380

LTM HB Revenue: $146,465 LTM ASP: $385

Lots Owned or Controlled: 1,812

All lots owned or controlled as of June 30, 2015. The term “Adjusted” includes GAAP results plus legacy TRI Pointe operations for the period prior to July 7, 2014, the closing date of the WRECO transaction. See “Reconciliation of Non-GAAP Financial Measures” in the appendix of

the presentation.

Adjusted LTM Orders: 3,957 Adjusted LTM Deliveries: 3,432

Adjusted LTM HB Revenue: $1,898,226 Adjusted LTM ASP: $553

Lots Owned or Controlled: 28,921

Markets: Orange County, Los

Angeles, San Diego, San

Francisco Bay Area, Denver

LTM Orders: 1,068

LTM Deliveries: 719

LTM HB Revenue: $563,588

LTM ASP:$784

Lots Owned or Controlled: 3,655

Leading Brand Names Targeted to Specific Markets

Markets: Los Angeles/Ventura, Inland

Empire, San Diego, Las Vegas

LTM Orders: 1,104

LTM Deliveries: 1,061

LTM HB Revenue: $495,766

LTM ASP: $467

Lots Owned or Controlled: 17,195

Market: Houston

LTM Orders: 504 LTM Deliveries: 523

LTM HB Revenue: $269,742 LTM ASP: $516

Lots Owned or Controlled: 2,111

4

Second Quarter Highlights

2015 Second Quarter Highlights

SECOND QUARTER HIGHLIGHTS AND COMPARISONS TO SECOND QUARTER 2014New home orders increased 62% to 1,238New home deliveries up 27% to 798 with increased average sales price of 9% to $535kHome sale revenue up 38% to $427.2MHomebuilding gross margin of 20.0%Adjusted homebuilding gross margin of 22.0%(1)

SG&A expense improved to 12.6% compared to 13.6%Net income $54.9M; $0.34 per diluted share vs. $24.2M; $0.19 per diluted share

SECOND QUARTER HIGHLIGHTS AND COMPARISONS TO SECOND QUARTER 2014– “Adjusted”(1)(2)

New home orders increased 30% to 1,238New home deliveries up 9% to 798 with decreased average sales price of 1% to $535kHome sale revenue up 8% to $427.2M

(1) See “Reconciliation of Non-GAAP Financial Measures” in the appendix of the presentation.

(2) The term “Adjusted” includes GAAP results plus legacy TRI Pointe operations for the second quarter of 2014. 6

Arizona15%

California29%

Maryland5%

Nevada10%

Colorado5%

Texas20%

Virginia6%

Washington10%

Active Selling Communities and Absorption Rate

100

122

2.61

3.45

1.0

1.5

2.0

2.5

3.0

3.5

4.0

0

20

40

60

80

100

120

140

2014 2015

Communities Absorption Rate

22%

Active Communities and Absorption RateAs of and for the quarters ended June 30, 2014 and 2015

Communities by StateAs of June 30, 2015

7

Arizona15%

California45%

Maryland4%

Nevada8%

Colorado5%

Texas10%

Virginia4%

Washington9%

New Home Orders – Second Quarter Results

763

1,238

953

1,238

0

200

400

600

800

1,000

1,200

1,400

2014 2015

GAAP

Adjusted

Second Quarter - New Home OrdersFor the quarters ended June 30, 2014 and 2015 – GAAP and on an adjusted

basis(1)

(1) Includes legacy TRI Pointe operations for the second quarter of 2014. See “Reconciliation of Non-GAAP Financial Measures” in the appendix of this presentation.

Orders by StateFor the quarter ended June 30, 2015

8

Incre

ase 6

2%

YO

Y

Incre

ase 3

0%

YO

Y

Arizona11%

California36%

Maryland4%

Nevada11%

Colorado6%

Texas15%

Virginia6%

Washington11%

628

798

731

798

0

100

200

300

400

500

600

700

800

900

2014 2015

GAAP

Adjusted

New Home Deliveries – Second Quarter Results

Deliveries by StateFor the quarter ended June 30, 2015

(1) Includes legacy TRI Pointe operations for the second quarter of 2014. See “Reconciliation of Non-GAAP Financial Measures” in the appendix of this presentation.

Second Quarter – New Home DeliveriesFor the quarters ended June 30, 2014 and 2015- GAAP and on an adjusted

basis(1)

9

Incre

ase 2

7%

YO

Y

Incre

ase 9

% Y

OY

Arizona9%

California52%

Maryland5%

Nevada4%

Colorado6%

Texas11%

Virginia6%

Washington7%

Backlog – Units and Dollar Value (“GAAP”)

Backlog – Units and Dollar ValueAs of June 30, 2014 and 2015 (dollars in thousands)

Dollar Value by StateAs of June 30, 2015

1,191

1,998

0

500

1000

1500

2000

2500

Units

$670,225

$1,199,847

$-

$100,000

$200,000

$300,000

$400,000

$500,000

$600,000

$700,000

$800,000

$900,000

$1,000,000

$1,100,000

$1,200,000

$ Value

2014

2015

$563K $601K

Backlog ASP

10

Incre

ase 6

8%

YO

Y

Incre

ase 7

9%

YO

Y

Arizona9%

California52%

Maryland5%

Nevada4%

Colorado6%

Texas11%

Virginia6%

Washington7%

Backlog – Units and Dollar Value (“Adjusted”)(1)

Backlog – Units and Dollar Value (“Adjusted”)As of and for the quarters ended June 30, 2014 and 2015 (dollars in thousands)

Dollar Value by StateAs of June 30, 2015

1,473

1,998

0

500

1000

1500

2000

2500

Units

$901,951

$1,199,847

$-

$100,000

$200,000

$300,000

$400,000

$500,000

$600,000

$700,000

$800,000

$900,000

$1,000,000

$1,100,000

$1,200,000

$ Value

2014

2015

$612K $601K

Average Sales Price

(1) Includes legacy TRI Pointe operations for the second quarter of 2014. See “Reconciliation of Non-GAAP Financial Measures” in the appendix of this presentation. 11

Incre

ase 3

6%

YO

Y

Incre

ase 3

3%

YO

Y

Arizona8%

California44%

Maryland4%

Nevada8%

Colorado5%

Texas15%

Virginia8%

Washington8%

Home Sales Revenue – Second Quarter Results

$309,609

$427,328

$396,945

$427,238

$0

$100,000

$200,000

$300,000

$400,000

$500,000

GAAP

Adjusted

Second Quarter – Home Sales RevenueFor the quarter ended June 30, 2014 and 2015 (dollars in thousands)

Home Sales Revenue by StateFor the quarter ended June 30, 2015

$493K $543K $535K $535K

Average Sales Price

12

Incre

ase 3

8%

YO

Y

Incre

ase 8

% Y

OY

Orders, Deliveries and Absorption Rate year over year comparisons for the Second Quarter and YTD through June by Segment

(includes breakout by state for Pardee Homes and TRI Pointe Homes brands)

120

184

9391

2.4

3.4

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

0

20

40

60

80

100

120

140

160

180

200

2Q14 2Q15Orders Deliveries Absorption

Orders, Deliveries and Absorption Rate

For the second quarter ended June 30, 2014 and 2015

2Q14 2Q15

$377K $369K

Average Sales Price of Deliveries

53%

14

Orders, Deliveries and Absorption Rate

For the six months ended June 30, 2014 and 2015

225

345

192176

2.3

3.3

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

0

50

100

150

200

250

300

350

400

YTD14 YTD15Orders Deliveries Absorption

YTD14 YTD15

$366K $375K

Average Sales Price of Deliveries

53%

81

101

51

853.6

3.4

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

0

20

40

60

80

100

120

2Q14 2Q15Orders Deliveries Absorption

Orders, Deliveries and Absorption Rate

For the second quarter ended June 30, 2014 and 2015

25%

Nevada

15

2Q14 2Q15

$339K $394K

Average Sales Price of Deliveries

Orders, Deliveries and Absorption Rate

For the six months ended June 30, 2014 and 2015

135

201

98

1393.4

3.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

0

50

100

150

200

250

YTD14 YTD15Orders Deliveries Absorption

YTD14 YTD15

$358K $373K

Average Sales Price of Deliveries

49%

203

254

195

1575.3

6.3

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

6.0

6.5

7.0

0

50

100

150

200

250

300

2Q14 2Q15Orders Deliveries Absorption

Orders, Deliveries and Absorption Rate

For the six months ended June 30, 2014 and 2015

25%

California

16

2Q14 2Q15

$521K $489K

Average Sales Price of Deliveries

Orders, Deliveries and Absorption Rate

For the second quarter ended June 30, 2014 and 2015

394

462

283271

5.1

6.2

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

6.0

6.5

7.0

0

50

100

150

200

250

300

350

400

450

500

YTD14 YTD15Orders Deliveries Absorption

YTD14 YTD15

$534K $532K

Average Sales Price of Deliveries

17%

106

116

67

87

2.5

3.6

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

6.0

0

20

40

60

80

100

120

140

2Q14 2Q15Orders Deliveries Absorption

Orders, Deliveries and Absorption Rate

For the second quarter ended June 30, 2014 and 2015

9%

17

2Q14 2Q15

$376K $410K

Average Sales Price of Deliveries

Orders, Deliveries and Absorption Rate

For the six months ended June 30, 2014 and 2015

204

266

145

180

2.6

4.3

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

6.0

0

50

100

150

200

250

300

YTD14 YTD15Orders Deliveries Absorption

YTD14 YTD15

$388K $439K

Average Sales Price of Deliveries

30%

166

124

139

123

2.3

1.6

1.0

1.5

2.0

2.5

3.0

3.5

4.0

0

20

40

60

80

100

120

140

160

180

2Q14 2Q15Orders Deliveries Absorption

Orders, Deliveries and Absorption Rate

For the second quarter ended June 30, 2014 and 2015

(25%)

18

2Q14 2Q15

$487K $526K

Average Sales Price of Deliveries

309

256269

231

2.3

1.6

1.0

1.5

2.0

2.5

3.0

3.5

4.0

0

50

100

150

200

250

300

350

YTD14 2Q15Orders Deliveries Absorption

Orders, Deliveries and Absorption Rate

For the six months ended June 30, 2014 and 2015

YTD14 YTD15

$480K $523K

Average Sales Price of Deliveries

(17%)

24

60

10

444.4

3.2

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

6.0

0

10

20

30

40

50

60

70

2Q14 2Q15Orders Deliveries Absorption

Orders, Deliveries and Absorption Rate

For the second quarter ended June 30, 2014 and 2015 on an

adjusted basis(1)

150%

Colorado

19

2Q14 2Q15

$377K $472K

Average Sales Price of Deliveries

(1) Includes legacy TRI Pointe operations for the second quarter of 2014. See “Reconciliation of Non-GAAP Financial Measures” in the appendix of this presentation.

Orders, Deliveries and Absorption Rate

For the six months ended June 30, 2014 and 2015 on an adjusted

basis(1)

40

134

20

77

4.8

3.4

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

6.0

0

20

40

60

80

100

120

140

160

YTD14 YTD15Orders Deliveries Absorption

YTD14 YTD15

$379K $473K

Average Sales Price of Deliveries

235%

166

305

93

130

5.3

5.0

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

6.0

0

50

100

150

200

250

300

350

2Q14 2Q15Orders Deliveries Absorption

Orders, Deliveries and Absorption Rate

For the second quarter ended June 30, 2014 and 2015 on an

adjusted basis(1)

84%

California

20

2Q14 2Q15

$898K $844K

Average Sales Price of Deliveries

(1) Includes legacy TRI Pointe operations for the second quarter of 2014. See “Reconciliation of Non-GAAP Financial Measures” in the appendix of this presentation.

288

567

175

236

4.94.8

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

6.0

0

100

200

300

400

500

600

YTD14 YTD15Orders Deliveries Absorption

Orders, Deliveries and Absorption Rate

For the six months ended June 30, 2014 and 2015 on an adjusted

basis(1)

YTD14 YTD15

$872K $852K

Average Sales Price of Deliveries

97%

87

94

83

81

1.3

2.2

1.0

1.5

2.0

2.5

3.0

3.5

4.0

70

75

80

85

90

95

2Q14 2Q15Orders Deliveries Absorption

Orders, Deliveries and Absorption Rate

For the second quarter ended June 30, 2014 and 2015

8%

21

2Q14 2Q15

$756K $649K

Average Sales Price of Deliveries

163

201

149 156

1.2

2.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

0

50

100

150

200

250

YTD14 YTD15Orders Deliveries Absorption

Orders, Deliveries and Absorption Rate

For the six months ended June 30, 2014 and 2015

YTD14 YTD15

$735K $656K

Average Sales Price of Deliveries

23%

2015 Outlook

Re-iterate 2015 Outlook

Increase home deliveries by 25% over the 2014 deliveries of the combined company(1)

Average sales price of homes delivered of $550,000

Expand homebuilding gross margins for the year as compared to GAAP 2014 results; delivering full year homebuilding gross margin of approximately 21%

Improve the SG&A as a % of home sales revenue to a range of 10.5% to 11.0%

Earn $1.15 to $1.30 on a fully diluted per share basis

(1) Includes legacy TRI Pointe operations for the periods prior to July 7, 2014, the closing date of the WRECO transaction. 23

Third Quarter 2015 Update and Outlook

New home orders up 39% for the month of July over the combined company(1) results for the comparable month a year ago

Anticipate delivering approximately 50% of the 1,998 homes in backlog as of June 30, 2015

Open 8 new communities and close out of 14 communities, resulting in 116 active selling communities as of September 30, 2015

Anticipate expanding homebuilding gross margins on deliveries in 3Q15 as compared to 2Q15

(1) Includes legacy TRI Pointe operations for the period prior to July 7, 2014, the closing date of the WRECO transaction. 24

Significant Land Supply

TRI Pointe Solutions

Orders by Month

Debt

Significant Land Supply to Fuel Growth

Combined Lot Position

Market Owned Controlled Total Lots % Owned Inventory Dollars LTM Deliveries(2) Years of

Supply

California 17,834 533 18,367 97% $1,466,267 1,343 13.7

Colorado 456 202 658 69% $74,048 114 5.8

Washington, D.C. (1) 2,284 448 2,732 84% $283,413 394 6.9

Arizona 1,485 327 1,812 82% $189,036 380 4.8

Nevada 1,652 173 1,825 91% $156,468 321 5.7

Texas 837 1,274 2,111 40% $196,015 523 4.0

Washington 995 421 1,416 70% $170,506 355 4.0

Total 25,543 3,378 28,921 88% $2,535,753 3,430 8.4

As of June 30, 2015

64%

2%

10%

6%

6%

7%5%

California

Colorado

Washington, D.C. (1)

Arizona

Nevada

Texas

Washington

Total Lots

(1) Includes lots in the greater Washington D.C. area.

(2) Includes legacy TRI Pointe Homes operations for the period prior to July 7, 2014, the closing date of the WRECO transaction. See “Reconciliation of Non-GAAP Financial Measures” in the appendix of this presentation.

58%

3%

11%

7%

6%

8%

7%

Inventory Dollars

26

TRI Pointe Solutions

27

TRI Pointe Solutions – a wholly-owned subsidiary formed to provide

buyer services including mortgage and title insurance related services

100% owned by TRI Pointe Solutions

Title Agent for First American Title Insurance Company

Licensed in Texas, Maryland, and Virginia

Cash flow positive as of 2Q15

Mortgage company

Joint venture with imortgage

Licensed in Arizona, Washington, Colorado, Virginia, Maryland,

Texas, and Nevada

Anticipate California licensing in August

Venture expected to be cash flow positive in 3Q15

New Home Orders – July 2014 – July 2015

28

255

296

252 249 252

213

324

415

455

410

457

371355

0

50

100

150

200

250

300

350

400

450

500

Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul

New Home Orders (July 2014 through July 2015)

2.52 2.85 2.38 2.38 2.42 2.00 2.96 3.67 3.91 3.47 3.82 3.05 2.92

Absorption Rate = Orders per Month per Community

20152014

Selected Balance Sheet Metrics

29

$450 $450

$0

$100

$200

$300

$400

$500

4.375% Senior Notes 5.875% Senior Notes

• In May 2015, the Company

increased its unsecured revolving

credit facility from $425 million

to $550 million with an

additional $150 million

accordion feature in order to

provide additional liquidity for

working capital requirements to

fund growth.

$ in thousands 6/30/2015 12/31/2014

Cash and cash equivalents $ 121,907 $ 170,629

Real estate inventories $ 2,535,753 $ 2,280,183

Debt $ 1,300,049 $ 1,162,179

Stockholders' equity $ 1,528,772 $ 1,454,180

Net debt-to-capital(1) 43.5% 40.5%

Selected Balance Sheet Metrics

Debt Maturities (in millions)

(1) See “Reconciliation of Non-GAAP Measures” in the appendix of the presentation

Supplemental Data and Reconciliation

Reconciliation of Non-GAAP Financial Measures(unaudited)

In this presentation, we utilize certain financial measures that are non-GAAP financial measures as defined by the Securities and

Exchange Commission. We present these measures because we believe they and similar measures are useful to management and

investors in evaluating the Company’s operating performance and financing structure. We also believe these measures facilitate the

comparison of our operating performance and financing structure with other companies in our industry. Because these measures are not

calculated in accordance with Generally Accepted Accounting Principles (“GAAP”), they may not be comparable to other similarly titled

measures of other companies and should not be considered in isolation or as a substitute for, or superior to, financial measures prepared

in accordance with GAAP.

The following table reconciles homebuilding gross margin percentage, as reported and prepared in accordance with GAAP, to the non-

GAAP measure adjusted homebuilding gross margin percentage. We believe this information is meaningful as it isolates the impact that

leverage has on homebuilding gross margin and permits investors to make better comparisons with our competitors, who adjust gross

margins in a similar fashion.

31

Three Months Ended June 30,

2015 % 2014 %

(dollars in thousands)

Home sales $ 427,238 100.0 % $ 309,609 100.0 %

Cost of home sales 341,742 80.0 % 242,709 78.4 %

Homebuilding gross margin 85,496 20.0 % 66,900 21.6 %

Add: interest in cost of home sales 7,640 1.8 % 5,340 1.7 %

Add: impairments and lot option abandonments 882 0.2 % (22 ) 0.0 %

Adjusted homebuilding gross margin(1) $ 94,018 22.0 % $ 72,218 23.3 %

Homebuilding gross margin percentage 20.0 % 21.6 %

Adjusted homebuilding gross margin percentage(1) 22.0 % 23.3 %

Reconciliation of Non-GAAP Financial Measures (cont’d)(unaudited)

The merger with Weyerhaeuser Real Estate Company (“WRECO”) was accounted for as a "reverse acquisition" of TRI Pointe by WRECO

in accordance with ASC Topic 805, "Business Combinations." As a result, legacy TRI Pointe's financial results are not included in the

combined company’s GAAP results for any period prior to July 7, 2014, the closing date of the merger. This schedule provides certain

supplemental financial and operations information of the combined company that is “Adjusted" to include legacy TRI Pointe stand-alone

operations. No other adjustments have been made to the supplemental combined company information provided and this information is

summary only and may not necessarily be indicative of the results had the merger occurred at the beginning of the periods presented or

the financial condition to be expected for the remainder of the year or any future date or period.

The following schedule provides certain supplemental financial and operations information of the combined company that is “Adjusted" to

include legacy TRI Pointe stand-alone operations for the three month ending June 30, 2104 as though the WRECO merger was completed

on January 1, 2014.

32

Three Months Ended

June 30, 2015 June 30, 2014

Combined Legacy Combined Combined Legacy Combined

Reported Adjustments Adjusted Reported Adjustments Adjusted

Supplemental Operating Data: (dollars in thousands)

Home sales revenue $ 427,238 NA $ 427,238 $ 309,609 $ 87,336 $ 396,945

Net new home orders 1,238 NA 1,238 763 190 953

New homes delivered 798 NA 798 628 103 731

Average selling price of homes

delivered $ 535 NA $ 535 $ 493 $ 848 $ 543

Average selling communities 119.5 NA 119.5 97.5 12.3 109.8

Selling communities at end of period 122 NA 122 100 14 114

Cancellation rate 16 % NA 16 % 16 % 9 % 14 %

Backlog (estimated dollar value) $ 1,199,847 NA $ 1,199,847 $ 670,225 $ 231,726 $ 901,951

Backlog (homes) 1,998 NA 1,998 1,191 282 1,473

Average selling price in backlog $ 601 NA 601 $ 563 $ 822 $ 612

Reconciliation of Non-GAAP Financial Measures (cont’d)(unaudited)

The following schedule provides certain supplemental financial and operations information of the combined company that is “Adjusted" to

include legacy TRI Pointe stand-alone operations for the six month ending June 30, 2104 as though the WRECO merger was completed

on January 1, 2014.

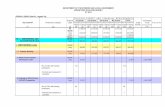

33

Six Months Ended

June 30, 2015 June 30, 2014

Combined Legacy Combined Combined Legacy Combined

Reported Adjustments Adjusted Reported Adjustments Adjusted

Supplemental Operating Data: (dollars in thousands)

Home sales revenue $ 801,503 NA $ 801,503 $ 551,511 $ 160,148 $ 711,659

Net new home orders 2,432 NA 2,432 1,430 328 1,758

New homes delivered 1,466 NA 1,466 1,136 195 1,136

Average selling price of homes

delivered $ 547 NA $ 547 $ 485 $ 821 $ 626

Average selling communities 116.1 NA 116.1 94.0 11.3 94.0

Selling communities at end of period 122 NA 122 100 14 100

Cancellation rate 14 % NA 14 % 15 % 9 % 14 %

Reconciliation of Non-GAAP Financial Measures (cont’d)(unaudited)

34

The following table reconciles the Company’s ratio of debt-to-capital to the ratio of net debt-to-capital. We believe that the ratio of net debt-to-

capital is a relevant financial measure for management and investors to understand the leverage employed in our operations and as an indicator of

the Company’s ability to obtain financing.

June 30, December 31,

2015 2014

(dollars in thousands)

Unsecured revolving credit facility $ 399,392 $ 260,000

Seller financed loans 12,390 14,677

Senior Notes 888,267 887,502

Total debt 1,300,049 1,162,179

Stockholders' equity 1,528,772 1,454,180

Total capital $ 2,828,821 $ 2,616,359

Ratio of debt-to-capital(1) 46.0 % 44.4 %

Total debt $ 1,300,049 $ 1,162,179

Less: Cash and cash equivalents (121,907 ) (170,629 )

Net debt 1,178,142 991,550

Stockholders' equity 1,528,772 1,454,180

Total capital $ 2,706,914 $ 2,445,730

Ratio of net debt-to-capital(2) 43.5 % 40.5 %

(1) The ratio of debt-to-capital is computed as the quotient obtained by dividing debt by the sum of debt plus equity. (2) The ratio of net debt-to-capital is computed as the quotient obtained by dividing net debt (which is debt less cash and cash

equivalents) by the sum of net debt plus equity. The most directly comparable GAAP financial measure is the ratio of debt-to-

capital.