2015 Haldor Topsoe Catalytic Forum · PDF file2015 Haldor Topsoe Catalytic Forum ... CUMENE...

58

2015 Haldor Topsoe Catalytic Forum Refining and Petrochemicals: Challenges and Solutions August 2015 1 Rafael Larraz

Transcript of 2015 Haldor Topsoe Catalytic Forum · PDF file2015 Haldor Topsoe Catalytic Forum ... CUMENE...

2015 Haldor Topsoe Catalytic Forum

Refining and Petrochemicals: Challenges and Solutions

August 2015

1

Rafael Larraz

2Haldor Topsoe Catalytic Forum, 2015

1. CEPSA Overview

2. Refining and Petrochemical Market Outlook

3. Refinery Petrochemical Integration

4. Refinery Petrochemical Integration. Future trends

5. Conclusions

DISCLAIMER: The information included in this presentation has been collected from public sources and does notrepresent neither CEPSA strategy nor CEPSA position on these topics.

1. CEPSA Overview

3Haldor Topsoe Catalytic Forum, 2015

THE COMPANY

Cepsa is an integrated company which operates in all the stages of the oil and gas value chain

Cepsa Today

Cepsa | Global Energy | 2015

• More than 80 years in the oil business

• More than 10,800 professionals

• Strong commitment with R&D activities

IPIC - OUR SHAREHOLDER

Since August 2011, Cepsa's sole shareholder is International Petroleum InvestmentCompany (IPIC), an investment group established in 1984 by the Government ofAbu Dhabi, which has had a stake in the Company for the past 26 years.

For Cepsa, integration in IPIC represents a great opportunity for growth andinternational expansion, a major business challenge.

Cepsa Today

Cepsa | Global Energy | 2015

OUR ACTIVITIES

EXPLORATION AND PRODUCTION

REFINING DISTRIBUTION AND MARKETING

PETROCHEMICALS GAS AND ELECTRICITY

Cepsa Today

Cepsa | Global Energy | 2015

CEPSA Research Centre

Haldor Topsoe Catalytic Forum, 2015 7

• Founded in 1975

• New facilities inaugurated 2008

• Located in Alcalá de Henares (Spain)

• 9000 m2 laboratories

• More than 30 pilot plants. CEPSA Technology

• Budget 2015 10 M€

• R&D activities for CEPSA Group• Upstream• Downstream• Petrochemicals• Innovation

Haldor Topsoe Catalytic Forum, 2015

Refinery Petrochemical Integration: 12,7%

CEPSA Oil Refining

TENERIFE4.5 million t/yr.

1930Nelson Index:5.3

LA RÁBIDA10 million t/yr.

1967Nelson Index: 9.7

GIBRALTAR-SAN ROQUE12 million t/yr.1969Nelson Index:12.3

ASESA50% (asphalt refinery)0.73 million tonnes per year

CEPSA

Other Companies

8

BENZENE

LAB

PHENOL

PTA/PIAXYLENES

CEPSA Petrochemistry

TOLUENE

PROPYLENE

PET

CUMENE

ACETONE

Haldor Topsoe Catalytic Forum, 2015 9CICLOHEXANE

Petrochemistry

LAB plantBécancour, QuebecCanada120,000 t/yr. LAB

LAB plantSalvador de BahíaBrazil220,000 t/yr. LAB80,000 t/yr. LABSA

Phenol PlantPalos de la Frontera800,000 t/yr. Cumene600,000 t/yr. Phenol370,000 t/yr. Acetone24,000 t/yr. AMS15,000 t/yr. Methyl amines7,000 t/yr. Derivatives

PTA plantGuadarranque650,000 t/yr. PTA220,000 t/yr. PIA175,000 t/yr. PET

LAB plantPuente Mayorga

220,000 t/yr. LAB80,000 t/yr. LABSA

400,000 t/yr. Paraffins

Phenol and acetone plantShanghai (China)

360,000 t/yr. Cumene250,000 t/yr. Phenol

150,000 t/yr. Acetone$200 million investment

Haldor Topsoe Catalytic Forum, 2015 10

CEPSA Phenol & Acetone Plant, Shanghai China –CEPSA’s chemical plant in Shanghai was inaugurated inApril and has been one of the biggest projects inCEPSA´s international growth and expansion strategy.

WRA Petrochemical Plant of the year , May 2015

2. Refining and Petrochemical Market Outlook

11Haldor Topsoe Catalytic Forum, 2015

Haldor Topsoe Catalytic Forum, 2015 12

World GDP Outlook

GDP GROWTH BY REGION

(Annual percent change)

2005 2010 2011 2012 2013 2014

North America 3,33 2,61 1,73 2,28 2,20 2,41

Latin America 4,35 5,97 4,14 2,57 2,64 0,93

Europe 2,41 2,29 2,04 (0,17) 0,30 1,35

CIS 6,59 4,89 4,70 3,44 2,00 0,72

Africa 5,47 5,02 0,92 5,17 3,93 3,46

Middle East 5,67 5,50 5,50 2,28 2,47 3,06

Asia Pacific 5,26 7,37 4,64 4,65 4,60 4,24

Total World 3,81 4,33 3,03 2,41 2,47 2,56

Source: WB, 2015

World GDP mainly to growth in Africa, Middle East and Asia.

Petrochemical linked to GDP growth, specially in the emergent areas.

Source: Nexant, 2014

3,85

3,9

3,95

4

4,05

4,1

4,15

4,2

4,25

0

10

20

30

40

50

60

70

80

90

1995 2000 2005 2010 2015 2020 2025 2030 2035

kg P

etCh

em/$

m G

DP

Kg P

etCh

em p

er c

apita

Petrochemicals and GDP

Consumption per capita Consumption per GDP

Haldor Topsoe Catalytic Forum, 2015 13

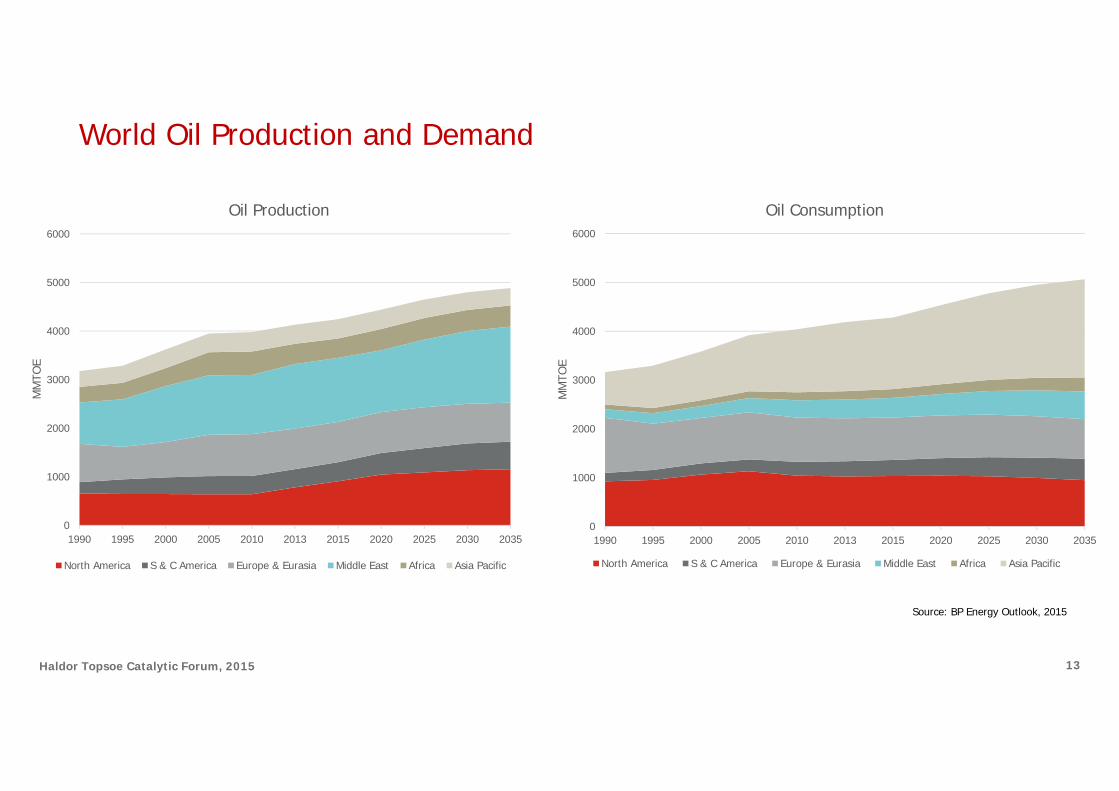

World Oil Production and Demand

0

1000

2000

3000

4000

5000

6000

1990 1995 2000 2005 2010 2013 2015 2020 2025 2030 2035

MM

TOE

Oil Production

North America S & C America Europe & Eurasia Middle East Africa Asia Pacific

Source: BP Energy Outlook, 2015

0

1000

2000

3000

4000

5000

6000

1990 1995 2000 2005 2010 2013 2015 2020 2025 2030 2035

MM

TOE

Oil Consumption

North America S & C America Europe & Eurasia Middle East Africa Asia Pacific

Haldor Topsoe Catalytic Forum, 2015 14

World Natural Gas Production and Demand

Source: BP Energy Outlook, 2015

0

1000

2000

3000

4000

5000

6000

1990 1995 2000 2005 2010 2013 2015 2020 2025 2030 2035

MM

TOE

Natural Gas Consumption

North America S & C America Europe & Eurasia Middle East Africa Asia Pacific

0

1000

2000

3000

4000

5000

6000

1990 1995 2000 2005 2010 2013 2015 2020 2025 2030 2035

MM

TOE

Natural Gas Production

North America S & C America Europe & Eurasia Middle East Africa Asia Pacific

Haldor Topsoe Catalytic Forum, 2015 15

World Oil Demand by sector

CAGR

-3,7%

1,2%

1,5%

0,5%

Refineries should improve its complexity in order to address the demand in petrochemicals and fuels

47,5

54,9

3,5 1,02,9

2013 Diesel Gasoline Others 2025

World Oil Demand Growth Drivers

Transport, MBb/d

10,7

12,5

0,50,5

0,8

2013 Ethane LPG Naphtha 2025

Petrochemical Feedstock, MBb/d

5,3

47,510,7

23,5

3,4

54,912,5

24,9Power generation

Transport

Petrochemicals

Others (*)

201389 MBb/d

202598 MBb/d

(*) Other Industry, Buildings, Agriculture, …

Sources: EIA AEO 2013; WTO , World Trade Report 2013

Haldor Topsoe Catalytic Forum, 2015 16

Crude Oil Cost Curve

25

4048

53 54 55 5762

88

0

10

20

30

40

50

60

70

80

90

100

0 20 40 60 80 100 120

US$

/Bbl

MBoe/d

Source: Oil&Gas Journal Financial, 2015

OnShore Middle East

OffShore Shelf

Extra Heavy Oil

Deepwater

Onshore Russia

OnShore Row

UltraDeepwater

NAM Shale

Oil Sands

Brent Price- May 2014

Brent Price- August 2015

EIA World Oil Demand92 million Bbl/d

Haldor Topsoe Catalytic Forum, 2015 17

Shale Gas and Oil

Directional drilling and hydraulic fracturing maketight oil and gas possible.

Recovery factor for the tight oil and gas formation is extremly low, around 10%.

Fields production periods are low in comparisonwith conventional oil and gas reservoirs.

Those facts make tight formation productionmuch more expensive than Middle East fields.

Haldor Topsoe Catalytic Forum, 201518

Shale Gas and Oil

0

100

200

300

400

500

600

700

800

900

1000

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

MM

T

Shale Gas US

0

100

200

300

400

500

600

700

800

900

1000

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

MM

T

Shale Oil US

% Vol.Marcellus

ShaleBarnettShale

Methane 82,1 91,8

Ethane 14 4,4

Propane 3,5 0,4

Carbon Dioxide 0,1 2,3

Nitrogen 0,3 1,1

Crude Country API º

Eagle Ford USA 44,7

Bakken USA 40,8

Source: BP Statistical Review 2015

Haldor Topsoe Catalytic Forum, 2015 19

Coal Production And China

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

MM

T

Coal Production

China World

China produces 3874 MT of Coal outof a World production of 8165 MT.

China has huge coal reserves, much of which is used for power generation.

Coal reserves in western China are lowquality and remote from consumptioncentres.

Source: BP Statistical Review 2015

Haldor Topsoe Catalytic Forum, 2015 20

Oil&Gas(106 MT)

Upstream(105 MT)

Intermediate(104MT)

DownstreamConversionIndustries

E&P

Oil Refinery

Gas Separation

Olefins:

Ethylene

Propylene

Aromatics:

Benzene

Toluene

Xylene´s

Olefins:

EDC/VCM

EO/EG

Oxoalcohols

Acrylonitrile

Aromatics:

EthylBenzene

Styrene

Ciclohexane

Caprolactam

Cumene/Fenol

LAB

PTA/PIA

Plastic Resins:

PE, PP, PVC, PS, EPS, PET

PC, POM, PBT, Nylon 6,6, PMMA

Synthetic Fibers:

Polyester

Nylon 6

Polypropylene

Acrylic

Synthetic Rubber Elastomers:

BR, SBR, EPDM

PTA/PIA/PET

Synthetic Coating Adhesives:

PVA, Silicone

Petrochemical Value Chain

PriceVolume

Haldor Topsoe Catalytic Forum, 201521

Petrochemical Derivatives

Haldor Topsoe Catalytic Forum, 2015 22

Petrochemical Business Cycle

Over investment in thesector

Manufacturers start losingpricing power

Supplies slowly startexceeding demand

Era of competitivedevaluation

Beginning of consolidationand closures

Manufacturers startregaining pricing power

Demand starts exceedingsupply

Demand excedes supply

Beginning of investmentin the sector

Era of high margin and expansion

Start of theCycle

ExcessCapacityEnd Of cycle

Product LTGREthylene 1-1,5 x GDP

Propylene 2 x GDP

Benzene 1 x GDP

P-Xylene 1,5 x GDP

HDPE 1,5 x GDP

LDPE 2 x GDP

PP 1-1,5 x GDP

Deutsche Bank, 2013

Haldor Topsoe Catalytic Forum, 2015 23

Petrochemical Production Process

Steam Cracking

Produce olefins and some aromatics.Processing feedstocks include ethane, LPG and naphta.Aromatics yields are low when natural gas is used as feedstock.

Fluidized Catalytic Cracking

Produces Propylene as a by productAfter some years of low margins, propylene production might turn it into a key process for refinery petrochemical integration.

Catalytic Reforming

Produces Aromatics as a by product.New catalyst generations focused on xylenes

Refiner has to consider petrochemicals as a high priced alternative option, but for a smallmarket.

Haldor Topsoe Catalytic Forum, 2015 24

Petrochemical Feedstocks

Most Petrochemicals are made from ethane, propaneor naphta, that come from oil refineries and gas processing.

Regions with surplus, low priced ethane are atractivefor steam cracking

Olefins (ethylene, propylene, butadiene) and aromatics(benzene, toluene and xylenes) make up 90% of thepetrochemical production, and are building blocks foralmost all other petrochemicals and polymers

These petrochemicals are commodities and its marketis cost driven and very price sensitive.

Naphtha Reforming

29%

GasOil5%

Methanol1%

Ethane12%

LPG9%

Naphtha Steam Cracking

44%

Petrochemical Feedstock Consumption

Source: Nexant, 2015

Haldor Topsoe Catalytic Forum, 2015 25

Petrochemical Feedstocks Prices

* Source: 1984-1990 German Federal Statistical Office 1991-2014 German Federal Office of Economics and Export Control (BAFA).

† Source: ICIS Heren Energy Ltd.‡ Source: Energy Intelligence Group, Natural Gas Week.BP Statistical Review, 2015

0

2

4

6

8

10

12

14

16

18

20

US$

/MM

Btu

LNG Japan LNG German import NBP Henry Hub † Canada Brent‡ *

Haldor Topsoe Catalytic Forum, 2015 26

Petrochemical Products Prices

Credit Suisse. Benchmark Prices, 2015

0

200

400

600

800

1000

1200

1400

1600

2009 2010 2011 2012 2013 2014 2015 2016

US$

/Ton

Naphtha Ethylene Propylene Brent

0

200

400

600

800

1000

1200

1400

1600

2,00 2,50 3,00 3,50 4,00 4,50

US$

/Ton

Henry Hub, US$/MMBtu

Ethylene Propylene

400

600

800

1000

1200

1400

1600

50 60 70 80 90 100 110 120

US$

/Ton

Brent, US$/Bbl

Ethylene Propylene

Haldor Topsoe Catalytic Forum, 2015 27

Petrochemical Products Prices

Credit Suisse. Benchmark Prices, 2015

0

200

400

600

800

1000

1200

1400

2009 2010 2011 2012 2013 2014 2015 2016

US$

/Ton

Naphtha Benzene Toluene Xylene Brent

0

200

400

600

800

1000

1200

1400

2,00 2,50 3,00 3,50 4,00 4,50

US$

/Ton

Henry Hub, US$/MMBtu

Benzene Toluene Xylene

400

600

800

1000

1200

1400

50 60 70 80 90 100 110 120

US$/Ton

Brent, US$/Bbl

Benzene Toluene Xylene

Haldor Topsoe Catalytic Forum, 201528

Basic Petrochemical Market and Trends

World Petrochemical market value estimationis 1300 US$ billion.

Basic Petrochemical Market size is around423 MMT and 530 US$ billion value.

World Oil Consumption in 2014 4211 MMT

Aromatics (BTX) represents 119 MMT and 130 US$ billion value. Paraxylene market represents 38 MMT

Deloitte, 2014IHS, 2015ICIS, 2015OGJ, 2015

Additional Ethylene capacity expansions (2015-17) represents 15 MT mainly is USA and ME.

On purpose propylene capacity will increase from 17 MMT to 42 MMT by 2020.

Additional world BTX demand (2015-2020) is around 17 MMT, of which 85% of new BTX supply is dominated by Asia (63%) and ME (22%).

Ethylene; 139

Propylene; 90Butadiene; 11

Benzene; 46

Toluene; 29

Xylene; 44

Methanol; 64,9

Base Petrochemicals Demand, MMT

Haldor Topsoe Catalytic Forum, 201529

Petrochemical Trends by Geographic Region

North America, Shale gas boost petrochemicals, mainlyethylene. Propylene and aromatics a possible issue. Today ethaneaccounts for 55% of the olefin slate and propane 20%. Shale gasis bringing cheap feed stocks and more ethane cracking.

Western Europe, Petrochemicals threatened by lack of cheapfeedstocks. Refinery naphtha is the main cracker feed. Naphthaand condensates provided about 75% of the feed to the Europeanethylene crackers. 12.5% came from ethane, propane and butaneand the balance from gasoil and other sources.

Middle East, Feedstock availability, expansion projects in refiningand petrochemicals. Ethane is the primary cracker feedstock.Some countries has promoted, through incentive pricing, LPGcracking. ME has been leading the petrochemical expansion due tothe rich hydrocarbon availability in the region

Asia, China is the main player. Coal an alternative feedstock.Refinery naphtha is the main cracker feed. This area is driving theglobal petrochemicals demand.

3. Refinery Petrochemical Integration

30Haldor Topsoe Catalytic Forum, 2015

Haldor Topsoe Catalytic Forum, 201531

Oil Refining Business

* Año 2002

0

10

20

30

40

50

60

70

80

90

100

MarketDemand 2015

SAHARAN BLEND ARABIAN LIGHT SAFANIYAH BOSCAN

GAS 3,3

GASOLINE30.2

DISTILLATES

56,4

FUELS10,3

DENSITY

º API

SULFUR % P

0,806 0,855 0,893 0,995

44 34 27 10,7

0,2 1,7 2,8 5,27

% W

eigh

t

Haldor Topsoe Catalytic Forum, 2015 32

Oil Refining Trends

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

% W

orld

Cap

acity

North America S & C America Europe & Eurasia Middle East Africa Asia Pacific

World Refining Capacity 96 MBbl/d World Oil refined Products Demand

Source: BP Satistical Review 2015

0

10.000

20.000

30.000

40.000

50.000

60.000

70.000

80.000

90.000

2005 2010 2015 2020 2025 2030 2035 2040

kBbl

/d

Gasoline Naphtha Jet Fuel Diesel/Gasoil Fuel Oil

Haldor Topsoe Catalytic Forum, 2015 33

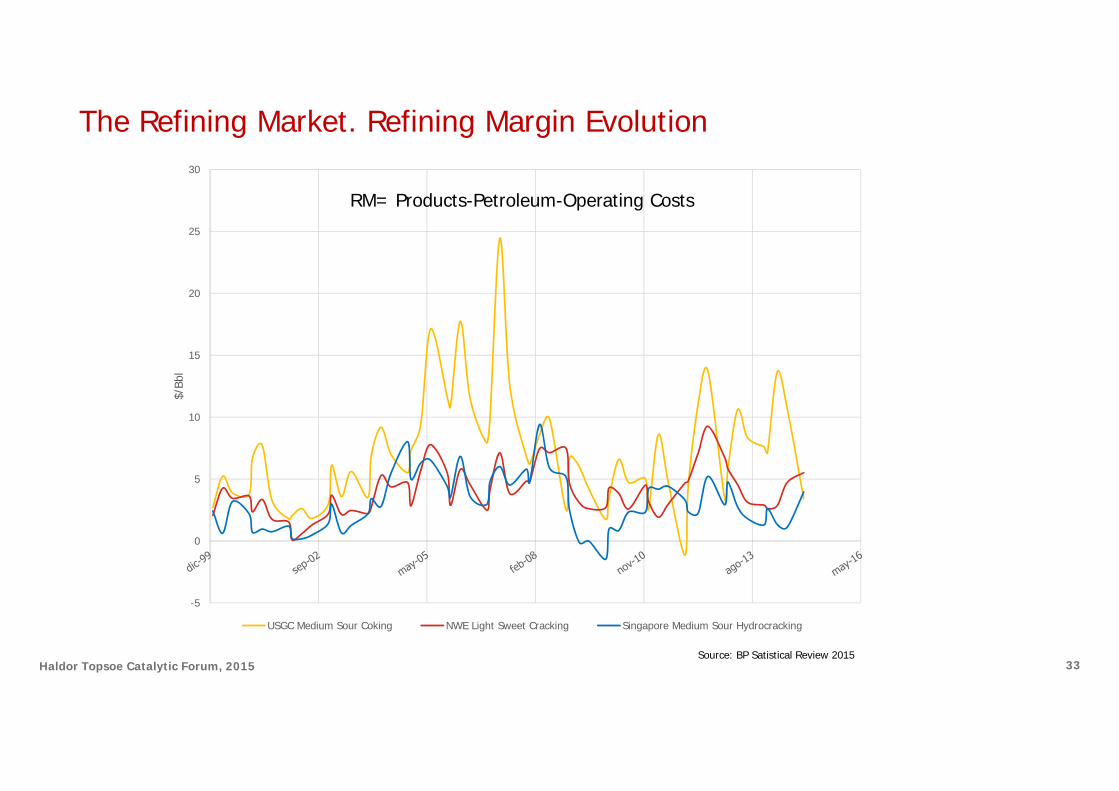

The Refining Market. Refining Margin Evolution

-5

0

5

10

15

20

25

30$/

Bbl

USGC Medium Sour Coking NWE Light Sweet Cracking Singapore Medium Sour Hydrocracking

Source: BP Satistical Review 2015

RM= Products-Petroleum-Operating Costs

Haldor Topsoe Catalytic Forum, 2015 34

Oil Refining Cost Curve

0

2

4

6

8

10

12

14

16

0 20 40 60 80 100

US$

/Bbl

MBbl/d

2008 Marginal Refinery Configuration Curve

0

2

4

6

8

10

12

14

0 20 40 60 80 100US$/Bbl

MBbl/d

2013 Marginal Refinery Configuration Curve

VB

Source: BCG, 2014

Source: BCG, 2014

HSK

0

2

4

6

8

10

12

14

0 50 100 150 200 250 300

US$

/Bbl

KBbl/d

Distillation. Topping.

Residue Conversion Units. VB,Coker, RFCC, RHCK Refinery

VGO Conversion Units. FCC/HCX Refinery

Catalytic Reformer. Hydroskimming

Haldor Topsoe Catalytic Forum, 2015 35

Reported Refineries in trouble are those with:

- Capacity < 200 kBPSD and Nelson Complexity < 8

- Difficult acces to crude supply, i.e. inland refineries

Oil Refining in Europe. Refinery closures

35

Only complex refineries will capture the market opportunities and remain competitive.

2000 2012

Net margins of individual EU28 refineries against EU28 average

European refining sector to close around1,5 – 2,5 MBbl/d capacity equivalent to aproximately ten refineries.

Source: EU Commision

02468

10121416

0 100 200 300 400

Nel

son

Inde

x

kBbl/dAsia America Europe Australia

Credit Suisse. Benchmark Prices, 2015

Haldor Topsoe Catalytic Forum, 2015 36

Oil Refining in Europe. Homogeneous Specifications to come.

Gasoline

Diesel(*)

3010

43545

1010

18017

875175

19540

50020

1510

87040

1010

40025

3350400

32545

113050

Expected Sulphur Content by Region (ppm)

2013

2025Further Investments in qualityimprovements will be needed.

MARPOL’s Sulphur Emission Limits (%wt)

2010 2015 2020 2025 2030

GLOBAL

ECAs

3,5%

0,5%0,1%

Pending on feasibilityreview in 20184,5%.

.

..

-Refiners to produce low sulphur bunker fuel

-Ships sulphur emmisions to be abated by on boardSOx scrubbers

-Natural Gas engines (*) On-road Diesel

Sources: OPEC World Oil Outlook 2013; DNV, Shipping 2020

Export Oriented Refineries will have to deal with complex logistics derived from the differentspecifications to handle

Haldor Topsoe Catalytic Forum, 2015 37

Oil Refining in Europe. Oil Refining Fitness Check

Economic impact on refinery sector of directives analysed in Fitness Check

Has EU legislation contributed to increased refining energy costs?

EU ETS increases costs of purchased electricity

Increased energy consumption due to FQD

Switch to low-sulphur crude oil for refinery energy due to pollution legislation (IED/LCPD/IPPCD)

Demand impacts (RED, ETD, IED) reduce utilization rate, which can negatively affect refineries' energy efficiency

Source: EU Commision

Haldor Topsoe Catalytic Forum, 201538

Refinery Petrochemical Integration Drivers

0

200

400

600

800

1000

1200

1400

1600

1800

Brent Naphta Ethylene HDPE LDPE LLDPE PP

US$

/Ton

No transportation costs. Specially for olefins

Resilient Value Chain Market demand and prices flexibility

Regional clusters

Feedstock and product flexibility

Feedstock Availability

By Products streams

Hydrogen balance management

Maximise the potential value of hydrocarbon streams, upgrading from fuel value to higher value transport fuels or petrochemical feedstock.

Capital, OPEX and Resource Optimization

Shared Infrastructure, Storage & Utilities

Lower Logistic & Energy cost

Minimize overhead and waste

Trained workforce and contractors

Credit Suisse. Benchmark Prices, 2015

Haldor Topsoe Catalytic Forum, 2015

Refinery Petrochemical Integration Scheme

Natural Gas

Crude Oil Refinery

AromaticsRecovery

Steam Cracker

(O, P, M)-Xylene

Toluene

Benzene

CondensateSplitter

FCCComplex

Reformate

Condensates

Ethylene

Propylene

Butadiene

Py Gas

VGO / ResiduePropylene

HCN

Hydrogen

Gasoline Blend

ETBE

Gasoline Blend

Diesel Blend

Naphtha

Ethane

NGL

Methane

39

Haldor Topsoe Catalytic Forum, 2015 40

Refinery Petrochemical Integration. Steam Cracker

Steam Cracking yields strongly rely on the kind of feedstock

NaphthaIs the most common feedstock for crackersProduces a broad range of productsFor each ton of ethylene produced, 3,3 tons of naphta are needed

%Weight Ethane Propane Butane Naphtha GasOil

Hydrogen&Methane 13 28 24 26 18

Ethylene 80 45 37 30 25

Propylene 2 15 18 13 14

Butadiene 1 2 2 5 5

Mixed Butenes 2 1 6 8 6

C5+ 2 9 13 8 7

Benzene 5 5

Toluene 4 3

Fuel Oil 2 18

EthanePresent a very high selectivity to ethyleneNegligible aromatics and propylene productionFor each ton of ethylene produced, 1,2 tons of ethane are needed

Source: Chemistry of Petrochemical Processes. Matar, Hatch, 2005

0

200

400

600

800

1000

1200

1400

1600

1800

0 20 40 60 80 100 120 140 160

US$/Ton

MMT/y BCG, 2015

Ethane, ME

Ethane, US

Naphtha RPI, Asia

Naphtha/LPG, Europe

Haldor Topsoe Catalytic Forum, 2015 41

High propylene world demand.

Propylene Gap, more than 10 MMT/y.

Steam Cracker. The increase in US ethane cracking has led to a drop in propylene production.

On purpose production: Propane DehydrogenationOlefin MetathesisMethanol to Propylene

Petrochemical FCC

Refinery Petrochemical Integration. Propylene Gap

Source: Booz&Allen, 2012

0

200

400

600

800

1000

1200

1400

1600

0 20 40 60 80 100 120

US$

/Ton

MMT/y

Steam Cracking and FCC

Met

athe

sis

PDH

Propylene Cost curve

Haldor Topsoe Catalytic Forum, 2015 42

On purpose Propylene. Propane Dehydrogenation

0

200

400

600

800

1000

1200

1400

1600

2009 2010 2011 2012 2013 2014 2015 2016

US$

/Ton

Propane Propylene Spread

Credit Suisse. Benchmark Prices, 2015

PropaneTerminal PDH Petrochemical

Use

H2

PropylenePropane Feed

Propane dehydrogenation produces propylene with rather high selectivity.

The economics of dehydrogenation of propane to propylene depends on thedifferential among propane and propylene.

Most of today’s activity in dehydrogenation is centered in the US, Middle East and China

Haldor Topsoe Catalytic Forum, 2015 43

China is using its low value coal reserves to feed Coal to Liquids and Methanol to Olefin (MTO) technologiesto produce ethylene and propylene.

In China metanol consumption for olefins productionramps up to more than 8 MMT/y. China is thebiggest metanol producer in the world with a share of 50%.

At low oil prices economics of MTO are weak.

No economic direct routes for converting methane to propylene.

Methane from Natural Gas must first be converted to methanol (or DME), and then it can be converted to ethylene and propylene.

High capital intensity for such Methane (or Methanol) to Olefins (MTO) processes

0123456789

2006 2008 2010 2012 2014 2016M

MT

Methanol to Olefins consumption in China

On purpose Propylene. Propylene in China

Nexant, 2014

Coal

Gasification Synthesis Gas

Methanol

Power

F-T Liquids

Steam, H2

Chemicals

Natural Gas

Haldor Topsoe Catalytic Forum, 2015 44

Ethylene

Gua

rdBe

d

Met

athe

sis

Reac

tor

C2=

Tow

er

Power

F-T Liquids

Steam, H2

Chemicals

C4=

C3=

Tow

er

Lights

Propylene

C4+Purge

On purpose Propylene. Olefin Metathesis

Source: J. Mol, 2004

Metathesis is the reaction of ethylene with 2-butene to form propylene, the reaction is equilibrium limited.

Feasibility depending on ethylene vs. propylene prices (typical historical value for the P/E price ratio has ranged from 0,7 – 0,8)

Propylene Gap make this unit competitive under some specific scenarios

Grass roots steam crackers, which incorporate metathesis as a method to increase propylene production must over-produceethylene feed to unit, increasing the overall capital expenditure.

Haldor Topsoe Catalytic Forum, 201545

OligomerizationUnit

AlkylationUnit

PropyleneSplitter

Refinery

IsobutanePropyleneRefinery grade 60%

NaphthaVGO/ Resid

C4=ETBE

BioEthanol

Gasoline Blending

PropylenePolymer Grade 99,5%Chemical Grade 94,5%

C4=

FCC EtherificationUnit

Alkylates

Propane

SHT Unit

C4=, C5= Diesel Blending

Naphtha

HDT/S Unit

LCO

HCO

Diesel blending

Haldor Topsoe Catalytic Forum, 2015

46

Refinery Petrochemical Integration. The Petrochemical FCC

Shift FCC operation to olefin production:

ZSM5 addition convert C7-C10 molecules to olefinic LPG.

Send Light Naphtha to a dedicated FCC riser orto the steam cracker. Depending on the energyvs. yield balance.

High severity FCC, propylene from 4% to 25% yield. Naphtha Aromatics content to increase.

Significant changes to the gas and lighter product recovery sections are necessary

Residue FCC

LCO

Vacuum Residue

Heavy Naphtha

FuelGas

HCO

VGO

MainFractionator

Propylene

Butylene

Light Naphtha

Air

Catalyst Addition

Flue Gas

HDS

Gas Plant

FCC Loop

VacuumColumn

Haldor Topsoe Catalytic Forum, 2015

CatalyticReforming

Steam CrackerPy Gas

Adsorption

AromaticsExtracton

BenzeneTow

er

Raffinate

TolueneDisproportionation/

Transalkylation

O-Xylene

Benzene

A10+

Paraxylene

TolueneTow

er

XyleneTow

er

O-XyleneTow

er

A9Tow

er

Isomerization

Refinery Petrochemical Integration. Aromatics Complex

Toluene

47

HT Naphta

Naphtha/Ethane/ LPG

Production / Demand / Isomer23% 18% o-Xylene53% 2% m-Xylene24% 80% p-Xylene

Naphtha Petrochemical Use 41%Naphta Gasoline Use 59%

World Naphtha demand 817 MMT

29

368

% Aromatics Source

Reforming Coke Oven Lt. Oil Py GasolineICIS, 2015

Haldor Topsoe Catalytic Forum, 2015

48

ProductElectricity

(GJ/ t product)Feedstock*(GJ/t product)

Fuel(GJ/t product)

Steam(GJ/ t product)

Benzene (SC) 0,3 0 13,1 -1,4

Benzene (AE) 0,1 45 2

Ethylene 0,3 45 13,1 -1,4

Propylene (SC) 0,3 45 13,1 -1,4

Propylene (FCC) 0,1 45 2 0,1

Toluene (AE) 0,1 22,5 2

Xylene 0,1 45 2

P-Xylene 0,2 0 6,3 0,8

Source: IEA OECD, 2009

0

1

2

3

4

5

6

7

0 5 10 15

GJ/

t Fe

edst

ock

Nelson Index

High Efficiency Low Efficiency

Refinery Petrochemical Integration Energy

Ocic, 2005 Typical Steam Cracking energy consumption varies from12 GJ/t to 18 GJ/t

*Feedstock consumption is accounted for by means of the calorific value of the basic chemicalsfollowing the first conversion of fossil fuels to chemicals

Haldor Topsoe Catalytic Forum, 2015 49

The “Antifragile“ Refinery

Capacity:A minimum size to reach economy of scales

Complexity:Ability to deliver high value light products

Flexibility on feedstocks:Ability to process different slates of crudes thanks to an efficient trading unit and an adapted logistics system

High distillate yield:Adapted to the European market with a strong demand for diesel

Energy efficiency:Integration of the different units with efficient energy use

Petrochemical Integration:Combined optimization of the feedstock streams, sharing units and transfers of products between refining and petrochemicals.

Source: BP Satistical Review 2015, Credit Suisse, 2015

0

0,1

0,2

0,3

0,4

0,5

0,6

0,7

(-2-4) (0-2) <0 0-2 2-4 4-6 6-8 8-10 10-12 12-14 14-16 16-18

P(RM

)

US$/Bbl

Refining Margin Distribution

Hydroskimming FCC Hydrocracker Petrochemical

0

10

20

30

40

50

0 5 10 15 20 25

IInv

estm

ent

Cost

, k$/

Bbl

Gross Margin, $/Bbl

Oil Refining Profitability

Jacobs, 2009

Hydroskimming

FCC Conversion

Deep Conversion

Petrochemical Integration

4. Refinery Petrochemical Integration. Future trends

50Haldor Topsoe Catalytic Forum, 2015

Haldor Topsoe Catalytic Forum, 2015

Refinery Petrochemical Integration. FCC and Aromatics Complex

SteamCrackerPy gas

CatalyticReforming

Adsorption

AromaticsExtracton

BenzeneTow

er

Raffinate

TolueneDisproportionation/

Transalkylation

O-Xylene

VGO/Resid

A10+

ParaxyleneTolueneTow

er

Xylene

Tower

O-X

yleneTow

er

A9

Tower

Isomerization

Toluene

HDT

HDTFCC

Hydrocracker

AromaticsExtracton

Benzene

VGO/Resid HDT (*)

(*) Optional

Naphtha/LPG

Raffinate

Aromatics

Source: Jechura, 2011

Naphtha

Aromatization

LCO

Maximum aromatics recovery. Significant technology challenges.

51

Paraffinic Naphta

Haldor Topsoe Catalytic Forum, 2015 52

Refinery Petrochemical Integration. Oxidative Methane Coupling

Haldor Topsoe Catalytic Forum, 2015 53

Refinery Petrochemical Integration. Crude Cracking

ExxonMobil, 2010

Haldor Topsoe Catalytic Forum, 2015 54

Vege

tabl

e O

il

IsoB

uten

esEtherification Bio-ETBE

Technology Development StatusResearch Industrial Commercial

On hold due to current lack of commercial viabilityIsomerizationDeoxy-

genationBio-kerosene

TransEsterification

(ExternalSupply)

FAME (7%Max).

Die

sel

Deoxy-genation

HVO

Bio

Eth

anol

Met

hano

lGasoline

Diesel

Diesel

Refinery Petrochemicals Integration.Biofuels and Biochemicals

Biofuels accounts for 1,4 MBboe/d % the 1,5% of the world demand. 10% by 2020

Haldor Topsoe Catalytic Forum, 2015 55

Dehydration BioEthylene

Technology Development StatusResearch Industrial Commercial

FCC

Deoxy-genation

Bio-Naphtha

Hydrocracking

BioEthanol

BioPropanol

BioButanol

BioPropylene

BioButylene

Vegetable Oil

Sugars

Deoxy-genation

Lignocellulosics FurfuralFurfural

Derivatives

Bio-Chemicals

Glycerine Bio-Hydrogen

Refinery Petrochemicals Integration.Biofuels and Biochemicals

5. Conclusions

56Haldor Topsoe Catalytic Forum, 2015

57

CONCLUSIONS

• Petrochemicals is a cyclical market of high value products. Petrochemicals market size is 10% of the whole oil market.

• Petrochemicals strongly rely on feedstocks cost and availability. Shale gas boom and present oil glut, strongly affect the marketdynamics.

• USA, ME and Asia are the most favored locations forpetrochemicals production due to feedstock costs and productdemand.

• Petrochemicals integration improves refinery´s economics despitethe required investments are significant.The FCC seems to be themost promising unit for petrochemical integration.

• Petrochemical strongly contribute to improve refinery economicperformace on a disparate set of economic environments

Haldor Topsoe Catalytic Forum, 2015

Thank you for your attention

To provide the energy that every reality

needs

SafetySustainabilityLeadershipContinuous

ImprovementSolidarity

To be a global energy

company of choice

VISIONMISSION VALUES