2015 Finance in the South West Segment 1 - Background, debt and being investment ready

74

Finance in the South West 2015 May we live in interesting times… Sharon Austen Partner

-

Upload

francis-clark-llp -

Category

Business

-

view

164 -

download

2

Transcript of 2015 Finance in the South West Segment 1 - Background, debt and being investment ready

Finance in the

South West 2015

May we live in

interesting times…

Sharon Austen

Partner

www.francisclark.co.uk

Administration

Admin

Timetable

Slides – available on request or at http://www.slideshare.net/FrancisClarkLLP

Questions – Please keep questions until coffee/lunch

Presenters…

www.francisclark.co.uk

Presenters and other participants

…and many more

www.francisclark.co.uk

Structure of morning

• Background, Debt and Investment ready (8.30am to 9.50am)

• Key note speaker

• LEP and SME

• Debt and Investment ready (part 1)

• Equity, Grants and Investment ready (part 2) (10.10am to 11.25am)

• An SME perspective, business support and closing address (11.45am to 1pm)

• Q&A one to one / Networking (1pm to 2pm)

www.francisclark.co.uk

Follow us on twitter @francisclarkllp

Tweet about this event using

#FCFinanceSW

www.francisclark.co.uk

Key note speaker

Declan Curry

• Award winning business and

economics broadcaster

• Business presenter for the BBC for

more than a decade

• Broadcast in the United States and

Australia as well as throughout the

UK

www.francisclark.co.uk

Declan Curry

Finance in the South West

2015

Chris Garcia

“Driving growth in the Heart of the SW”

Reposition the Heart of the South West: our prosperity, profile and reputation, nationally and globally. Connecting people, places, businesses and ideas to transform our economy, securing investment in infrastructure and skills to create more jobs and enable more rewarding careers.

Our LEP is working to

What do we do

• Common priorities

• Partnerships

• Attract resources

• Make a difference to prosperity of businesses and employees

Strategy - Our LEP priorities in a nutshellCreating the Conditions for

Growth

Maximising Productivity and

Employment Opportunities

Building on our

Distinctiveness

Pla

ce

Infrastructure for growth:

Transport and accessibility

Digital infrastructure

Sustainable solutions for

flood management

Energy Infrastructure

The infrastructure and facilities

to create more and better

employment:

Enterprise infrastructure

Strategic employment sites

Unlocking housing growth

The infrastructure and facilities

needed to support higher value

growth:

Specialist marine sites

Innovation infrastructure

Our environmental assets

Bu

sin

ess

Creating a favourable business

environment

A simpler, more accessible,

business support system

Achieving more sustainable and

broadly based business growth:

Reaching new markets

Globalisation

Supporting higher value growth:

Innovation through Smart

Specialisation

Building innovation capacity

Peo

ple

Businesses and individuals can

reach their potential:

Skills infrastructure

Accessibility to

education/employment

Employer engagement and

ownership

Increasing employment,

progression and workforce

skills.

Moving people into

employment

Supporting people to

progress to better jobs

Improving workforce skills

Creating a world class workforce

to support higher value growth:

Enterprise and business skills

Technical and higher level

Skills for our

transformational

opportunities.

Achieving our aspirations

Strategy Resources Delivery

Management

Our Aspirations

for Jobs

Growth &

Prosperity

People

Place

Business

Monitoring and Evaluation of Performance

Marketing and Communications

Back office financial accounting, audit, and procurement

Partnership

LA teams

Successes

• GPF finance for stalled infrastructure

• Rural Growth Network initiatives

• Finance for business growth

• Hinkley Growth Deal 14-15

• Growth Deal 1

• Growth Deal 2

Going forwardOur opportunities and challenges

We know what we have to do but our work is dependent on:• Funding (we don’t have revenue; ESIF delays a real problem)• Joined up focus / support from govt to make things happen• Partnership – with intermediaries and business

Our focus is now on DELIVERY- Lots of

contracts going out door for April

How can the LEP help –

Its your LEP

What the LEP is not:

An agency of HMG like the RDA designed to act as a delivery

arm of central gov, nor are we simply a funder body.

What the LEP is:

A genuinely local platform for collaboration across public

and private sectors, to achieve mutual economic aims.

We support:

• Funding bids for national Government – e.g. Growth Deal

Directing European funds to where they’re needed most

• Influencing national Government strategy

• Strategic partnerships – e.g. with neighboring LEPs

We are always keen to hear your priorities

What can we do more of??

heartofswlep.co.uk

Debt – types and

sources an

overview (do not

forget the

Banks…)

Richard Wadman

Corporate Finance Director([email protected])

www.francisclark.co.uk

Banks: net lending v gross lending

Bank of England, Trends in Lending, January 2015

www.francisclark.co.uk

• Total borrowing facilities

£112.8bn

• £7.9bn of new SME

borrowing approved Q3 2014

• A 13% increase on same Q 2013

• and highest amount since 2011

• Borrowing “broadly based”

across geography and

industry sectors (demand

from ME strong)

But banks are not not lending

Source: BBA Bank support for SMEs – 3rd Quarter 2014

www.francisclark.co.uk

• ‘Net lending’ perhaps not the full story

• Cash deposits increasing as debt repaid

• High approval rates

• Lenders are ‘open for business’ (“truly open”)

• Significant variation in approach/process

But banks are not not lending

www.francisclark.co.uk

Rates and Terms

Source: Bank of England

3.00

3.50

4.00

4.50

5.00

5.50Ja

n 20

09

May

200

9

Sep

2009

Jan

2010

May

201

0

Sep

2010

Jan

2011

May

201

1

Sep

2011

Jan

2012

May

201

2

Sep

2012

Jan

2013

May

201

3

Sep

2013

Jan

2014

May

201

4

Sep

2014

(% m

argi

n ov

er b

ase)

SME Lending Rates (BofE)

All SMEs

Small

Medium

www.francisclark.co.uk

Funding For Lending

Banks borrow from Bank of England (using business loans

and mortgages as security)

• Reduces interests rate which Bank borrows at

• The more a Bank lends, the more they can borrow and the

lower the fees on borrowing

• Lower interest rates on Loans (1% discount/ cash back)

• Fees being waived

• Increased competition for ‘good customers’

www.francisclark.co.uk

Enterprise Finance Guarantee Scheme

• Designed for businesses that have been turned down by

lenders due to insufficient security

• Decision making on individual loans is fully delegated to

the participating lenders

• Government guarantees 75%. Borrower pays a 2% per

annum premium

• Lenders entitled to take security, personal guarantees but

prohibited from charge over principal private residence

• Export variant - ExEFG

www.francisclark.co.uk

Regional Growth Fund –

Assisted Asset Purchase

• Funding for purchases of new plant and machinery

• Grant for up to 20% of asset cost for small businesses,

10% for medium

• Criteria apply – job creation/protected, size and location

• Limitations of amount per job apply

• Taxable and state aid considerations

www.francisclark.co.uk

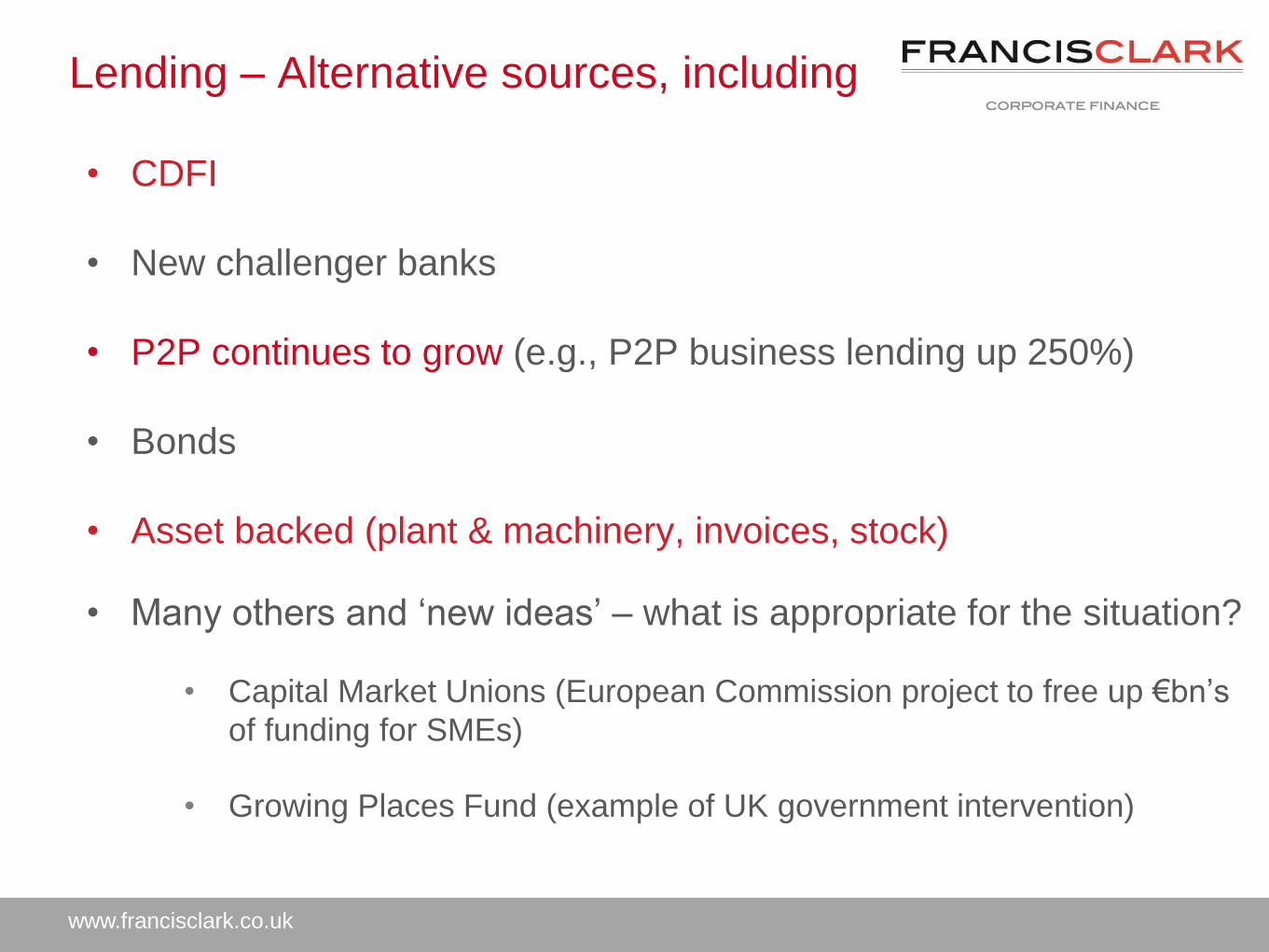

Lending – Alternative sources, including

• CDFI

• New challenger banks

• P2P continues to grow (e.g., P2P business lending up 250%)

• Bonds

• Asset backed (plant & machinery, invoices, stock)

• Many others and ‘new ideas’ – what is appropriate for the situation?

• Capital Market Unions (European Commission project to free up €bn’s

of funding for SMEs)

• Growing Places Fund (example of UK government intervention)

www.francisclark.co.uk

Summary

• Banks/debt lenders are keen – but make them keen for your

business by being properly prepared

• Consider the form and source of funding most appropriate for

your business situation

• Market test your terms and understand if you fit into any

lending ‘schemes’ to save costs

Chris Burt

Fund Manager

SWIG Finance

SWIG Finance

• Who we are

• What we do

• Why we do it

• Alternative funding is nothing new..

“

...a CDFI

“Community Development Finance

Institutions (CDFIs) lend money to businesses

(that) struggle to get finance from high street

banks. They are social enterprises that invest in

customers and communities”

SWIG = the South West’s CDFI

www.swigfinance.co.uk

01872 [email protected]

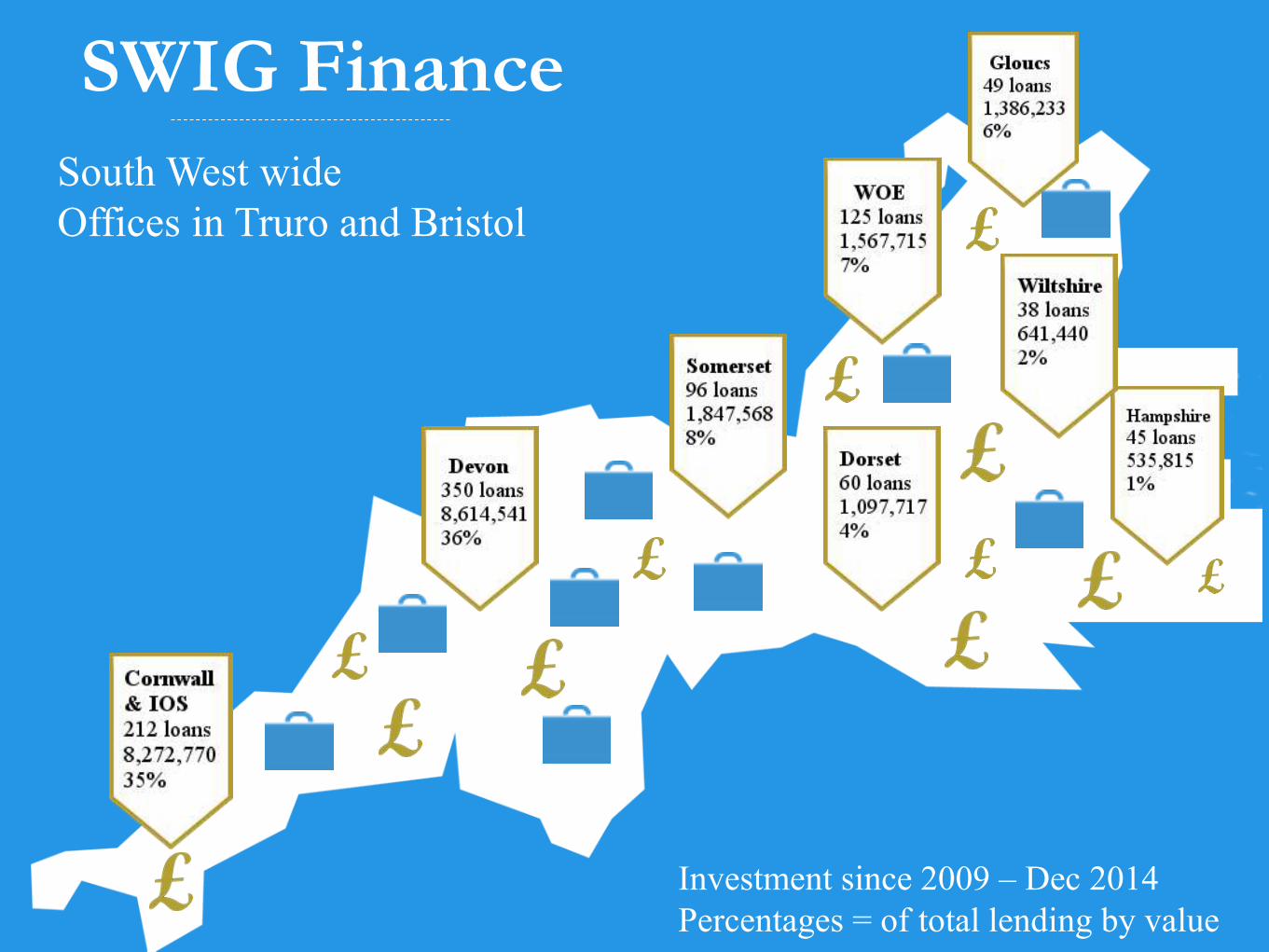

SWIG Finance

South West wide

Offices in Truro and Bristol

Investment since 2009 – Dec 2014

Percentages = of total lending by value

Who can we support?

• Start Up and existing SMEs

• Investing in growth or efficiency

• Jobs created or safeguarded

• Can’t access sufficient bank finance

Beran Instruments

• North Devon

• 4 loans for growth

between 1999 and

2006 from SWIG

• Grown from 21 staff

members to 130 with

a turnover £9 million

James Lovett

Business Development Manager

A Business Lending Revolution

An introduction to marketplace lending and how it

can help your business grow

What is peer-to-peer lending?

Traditional lending

Peer-to-peer lending

4

A simple model: Lenders can spread risk by lending

small amounts to hundreds of businesses

Business loan

Loan parts

Loan parts

Loan parts

Loan parts

Loan parts

Loan parts

Loan parts

Loan parts

Loan parts

5

The growth of alternative options is creating

healthy competition in the market

6.2

1.1

0

2

4

6

8

Total SME lending by provider

Bank lending Non-bank lending

Estimated 85% of SME lending is through the

five big banks

Source: Project Merlin, Bank of England; Funding Circle analysis; does not include loan secured on property

Bank lending includes lending from the five big banks: Barclays, HSBC, LBG, RBS and Santander

Lending pm, £bn

UK Business peer-to-peer lending (P2B) has

now surpassed £700 million

0

100

200

300

400

500

600

700

Q32010

Q42010

Q12011

Q22011

Q32011

Q42011

Q12012

Q22012

Q32012

Q42012

Q12013

Q22013

Q32013

Q42013

Q12014

Q22014

Q32014

Mill

ions

Other Business p2p lending Funding Circle lending

“71% of SMEs approach

only one provider

of finance”

British Business Bank, 2013

6

A global marketplace needs diversity

40

37k retail lenders

Central government

Local government

Passive institutions

Marketplace

for small

business

loans

Active institutions

Unsecured loans

Secured loans

Depth of lendersBreadth of products

Commercial property

Asset finance

Unsecured Loan

£5k - £200kSuitable for a wide range

of purposes

6 months to 5 year term

Rates from 6% (8.3% avgA+ over 36 months)

Fees between 3-4% of loan amount

No ERP’s

Secured Loan

£150k - £1m

All asset security agreement

Charge on specific properties or assets

Types of borrowing

41

Asset finance

£20k - £1m

Suitable for a wide range of hard assets

Hire purchase

Flexible on LTV–100% considered

Individual deals up to £250k, credit lines of up to £1m

Funding Circle loans can be used for almost

any purpose

Working capital

Buying equipment or assets

Deposits for property purchase

Taking on new staff

General cash-flow

Buying stock

General expansion

Replacing an overdraft

Paying down debt

Refurbishment

Growth – buying a new retail unit

Research and development

Marketing

IT upgrade

42

43

Minimum criteria includes

Limited companies, limited liability partnerships & non limited

Established: trading for 3+ years with at least 2 years of filed

accounts

Directors: A good credit history – no CCJs, CVA, CVL or liquidated

companies within past 6 years. UK resident.

Company: Min turnover £50,000, sufficient P&L strength to service

the additional borrowing. Upward growth trend and no consecutive

losses.

Beneficial ownership in UK

Loan supported by PG

44

How to apply

Apply online or use one of our registered introducers

Application reviewed by our credit team – decisions usually take 48 hrs

1

2

3

4

Your loan lists on our marketplace for up to 7 days for lenders to fund

You accept the loan and we transfer the funds to you

Typ

ica

lly 1

4 d

ays fro

m a

pp

lication to

dra

wd

ow

n

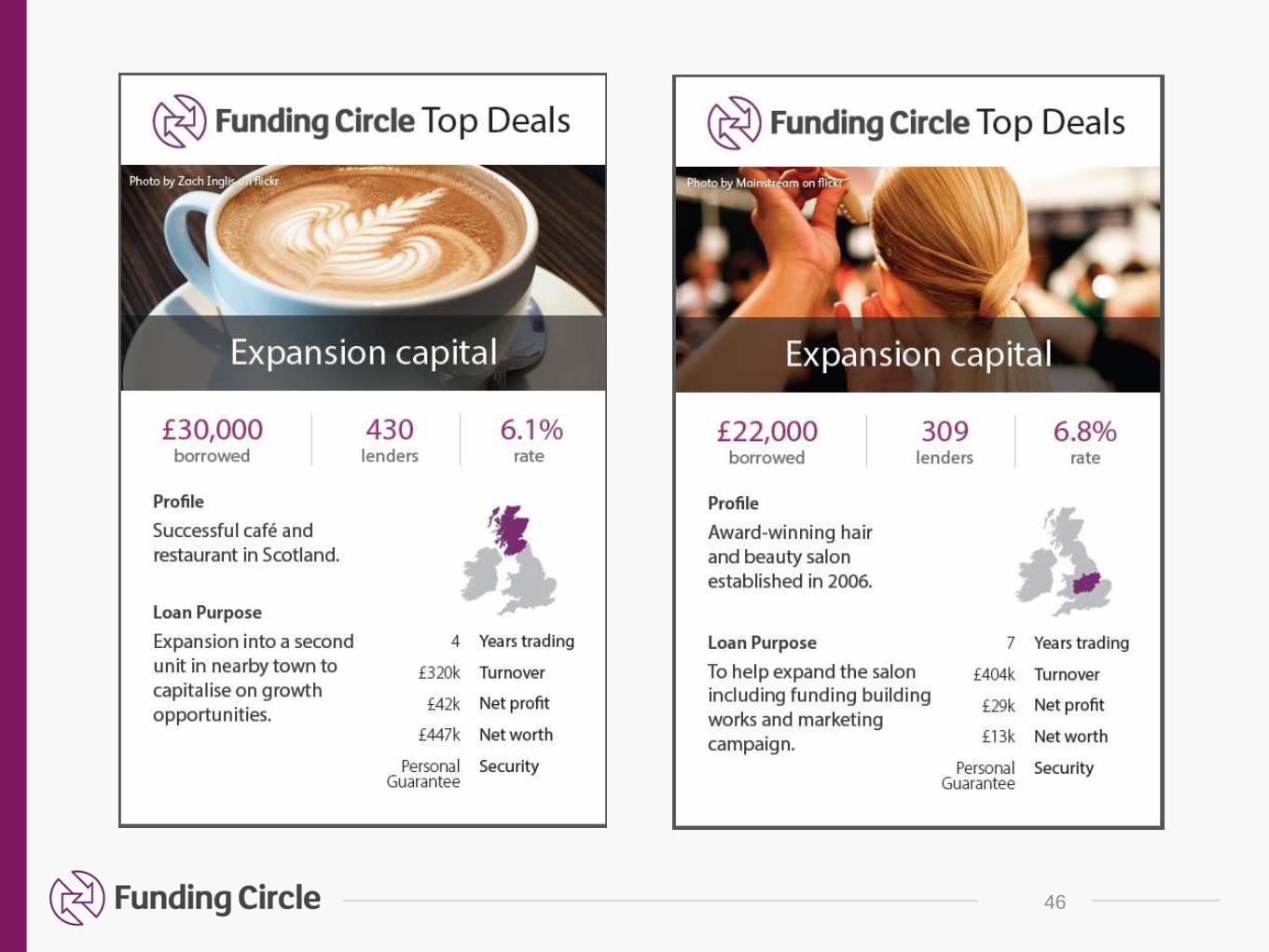

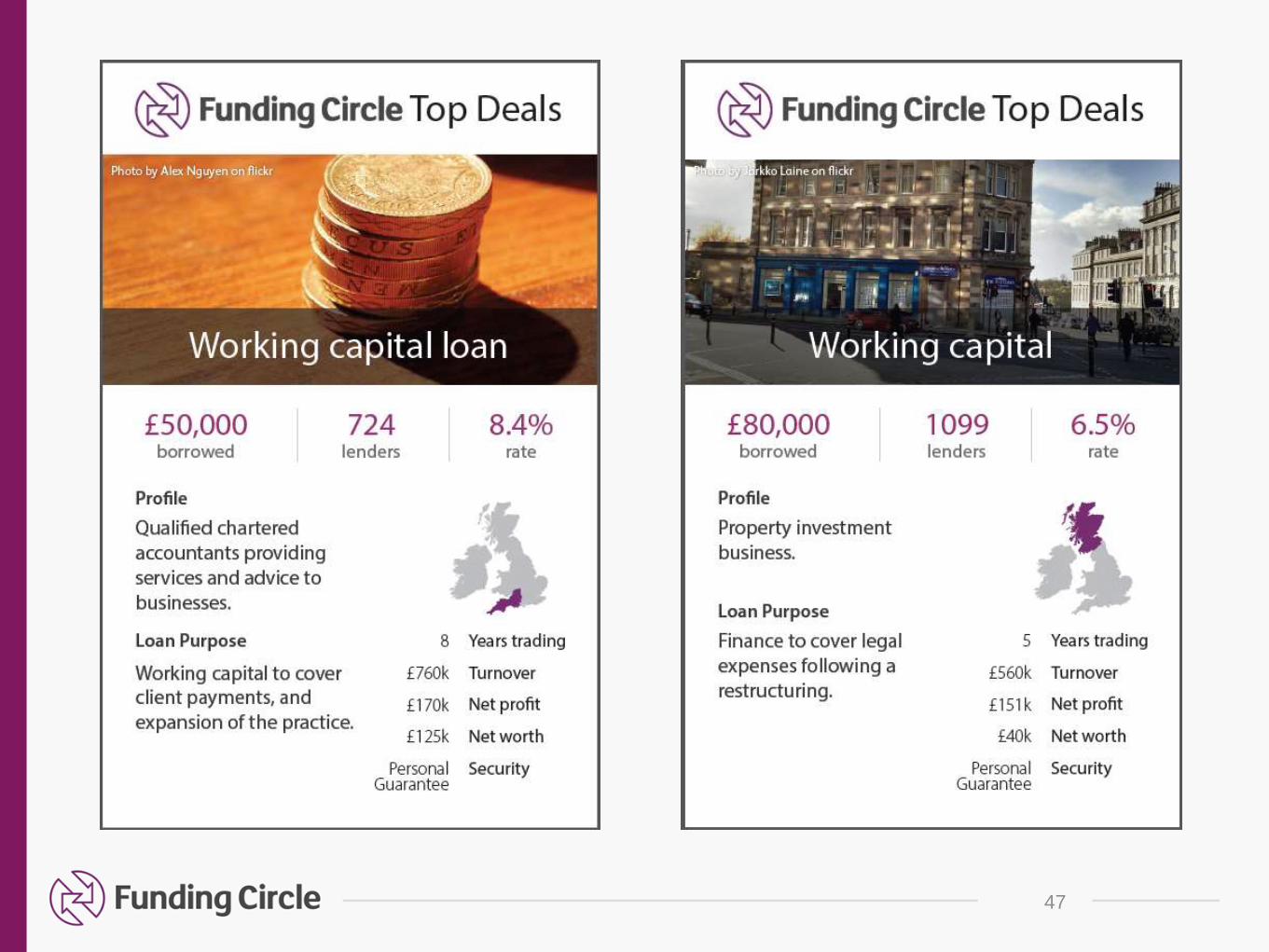

Borrower Case Studies

45

46

47

48

Paul Caunter, Ignition Credit

• Quick turnaround

• No lengthy application process or forms to complete.

• For deal sizes of up to £50k - 80% of decisions provided

within 4 hours & over £50k within 48 hours or less!

• Documentation completed for you & payment to your supplier arranged on your behalf.

Simple Process

Other Advantages

• Annual Investment Allowance of up to £500k available

until 31.12.2015 & other Tax advantages.

• Funding for Lending Scheme – 1% reduction in

published cost of funds (subscribed lenders only).

• Regional Growth Fund “RGF” of up to 20% deposit

contribution towards purchase of business critical assets

(conditions apply).

• “Asset re-finance” - raise working capital against assets

already owned.

• Asset Finance can assist in financing any moveable asset

from Cattle to Caterpillar’s.

• Finance agreements can be tailored to business needs, with

flexibility of terms & repayment schedule.

• Typical finance amounts range from £1k to £1m+

• Security generally taken on the asset alone, depending on

the asset & covenant of borrower.

• Quick & easy to put asset finance in place.

In Summary

Many thanks for your time!

Paul Caunter – 01872247208

www.ignitioncredit.co.uk

www.francisclark.co.uk

Matching requirements

Understand your

requirements

Understand funding

options and funders

requirements

Debt or Equity Risk?

www.francisclark.co.uk

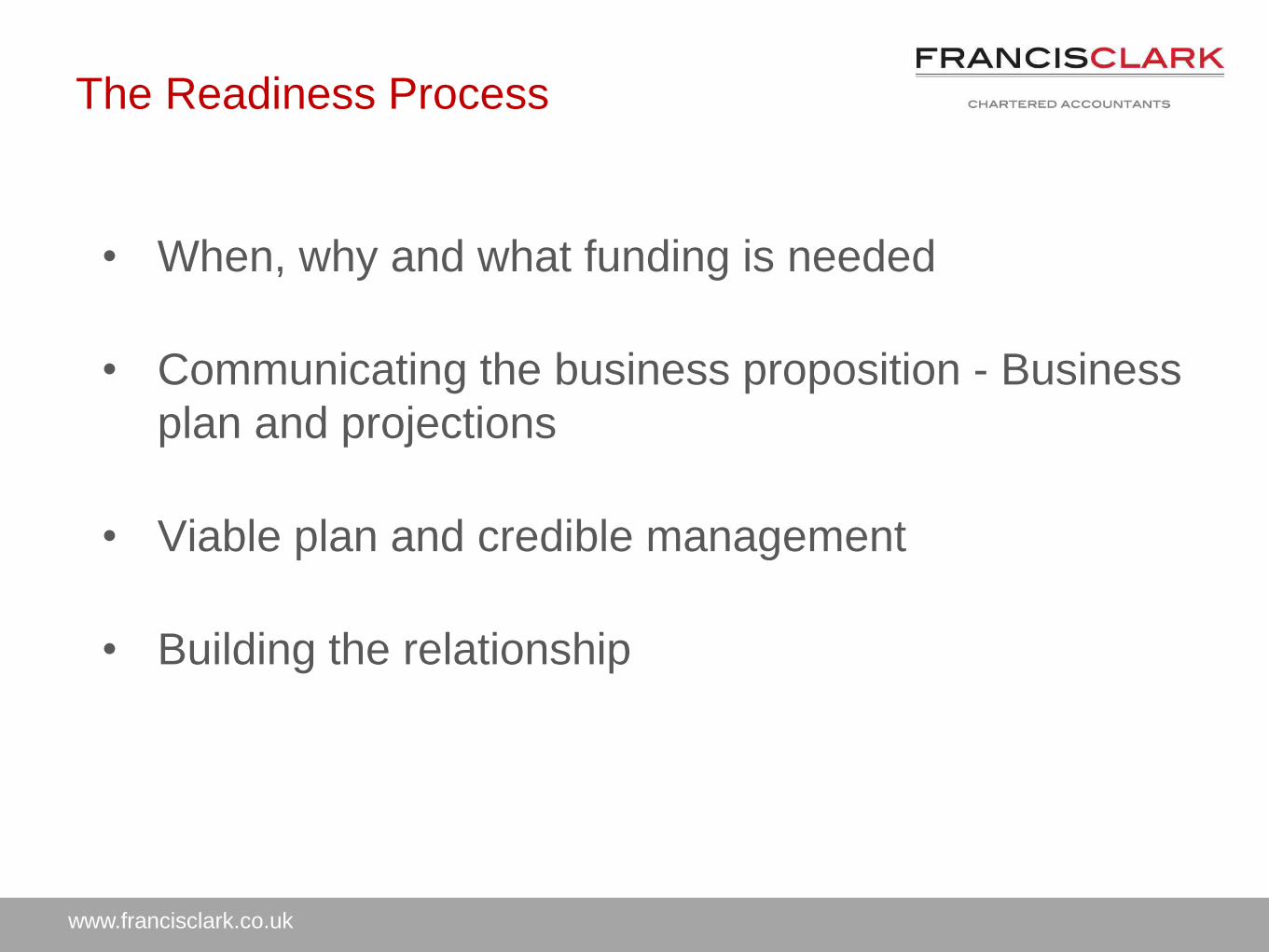

The Readiness Process

• When, why and what funding is needed

• Communicating the business proposition - Business

plan and projections

• Viable plan and credible management

• Building the relationship

www.francisclark.co.uk

Investment ready – housekeeping

• Compliance and Legal

Licences / contracts/ legal title?

IPR ownership in the company?

Statutory Accounts/management

accounts

VAT, PAYE/NI, Books and records in

order?

www.francisclark.co.uk

Requirements: Grants

• “Project” eligibility – sector, size, location…

• Timescale – prescriptive, process and panels, not

retrospective

• Match funding

• ‘Need for grant’ versus viable proposition

• Other factors - Environment, Equality, on going

requirements

www.francisclark.co.uk

Requirements: Debt

• Serviceability & Headroom

• Security / Personal Guarantees

• Conduits for government initiatives

• Covenants – achievable / appropriate?

www.francisclark.co.uk

Requirements: Equity

• Exit route and returns to the investor

• Investors expertise vs. loss of independence?

• Be prepared to discuss valuation

• Be aware of FSMA regulations

www.francisclark.co.uk

Investor Ready - Conclusions

• Appropriate funding / understand the funder

• Sufficient information for a risk assessment

• Know the ‘deal breakers’ – due diligence

• Build in sufficient time

Raising finance

– where do your

accounts fit in?

Stephanie Henshaw

Partner

www.francisclark.co.uk

Obtaining finance:Have you made the best of your balance sheet?

Current assets

- Stock X

- Debtors X

- Bank X

X

Creditors due within 1 year (X)

Net current liabilities (X)

Current assets

- Stock X

- Debtors X

- Bank X

X

Creditors due within 1

year

(X)

Net current assets X

Deferred income X

Deferred income

- Grants

- Customer

deposits

- Payments in

advance

www.francisclark.co.uk

Obtaining finance:Have you made the best of your balance sheet?

Current assets

- Stock X

- Debtors X

- Bank X

X

Creditors due within 1 year (X)

Net current liabilities (X)

Current assets

- Stock X

- Debtors X

- Bank X

X

Creditors due within 1 year (X)

Net current assets X

Creditors due after one year X

On demand

finance

• loans from

directors

• inter

company debt

Repayment <

12 months from

year end

Beware bullet repayments of loans falling due within 12 months

- consider early renewal/ replacement

www.francisclark.co.uk

Obtaining finance:How is your gearing?

• Fixed coupon preference shares,

fixed redemption shares

• Intercompany or director’s loan

where no intention/ expectation of

repayment

• Presented as debt (liabilities) on

balance sheet

• If redemption due within 12 months,

becomes current liability

• Presented as debt of balance sheet

• Consider capitalising into ordinary or

preference shares (no fixed coupon

or redemption obligation)

www.francisclark.co.uk

Obtaining finance:FRS 102: new rules, new challenges

Changes to net

assets

Additional provisions

Fair values for

financial instruments

Reporting

performance

Fair value

adjustments

Presentation changes

More complex

accounting

Must understand

detail of funding terms

www.francisclark.co.uk

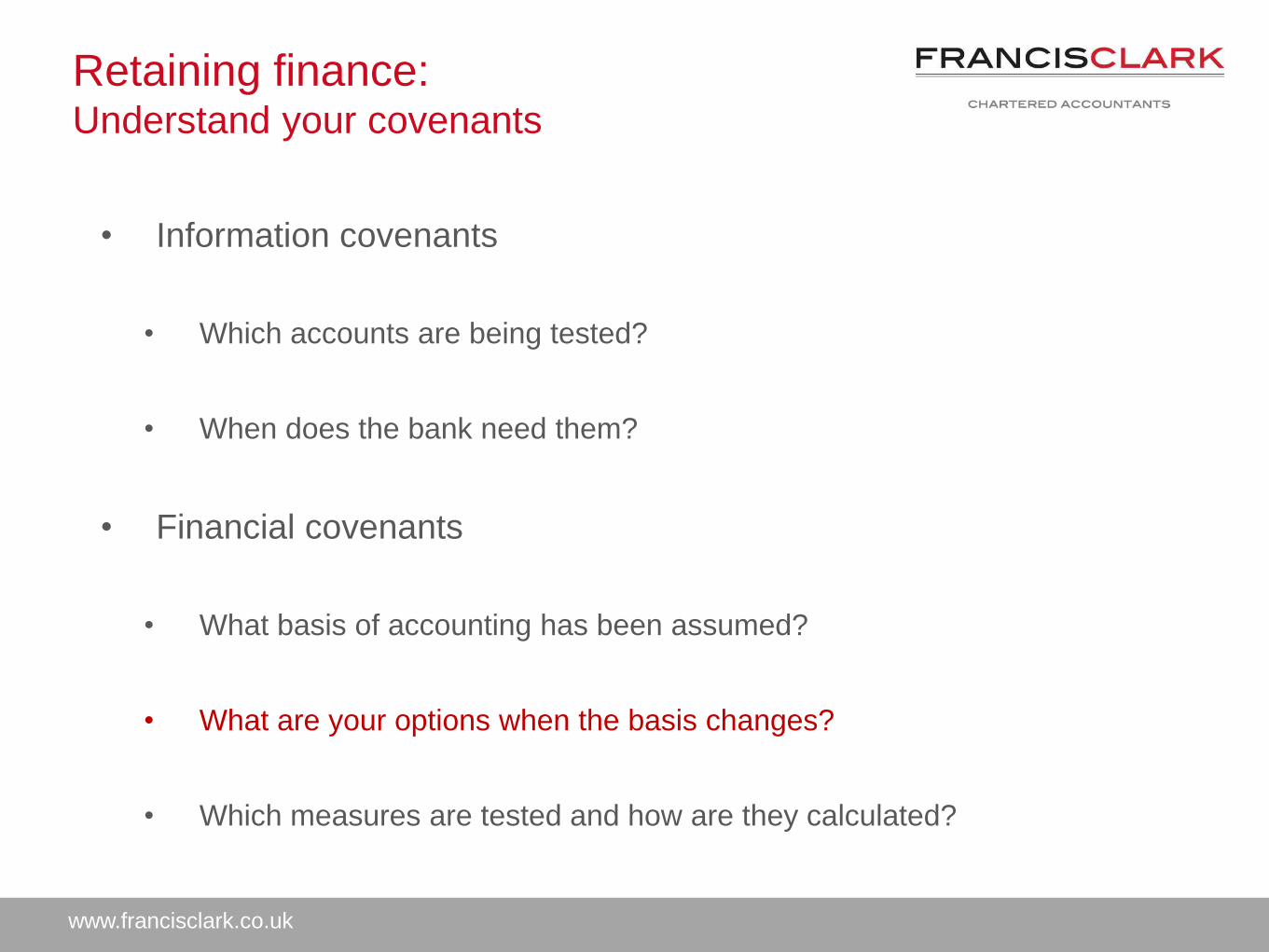

Retaining finance:Understand your covenants

• Information covenants

• Which accounts are being tested?

• When does the bank need them?

• Financial covenants

• What basis of accounting has been assumed?

• What are your options when the basis changes?

• Which measures are tested and how are they calculated?

www.francisclark.co.uk

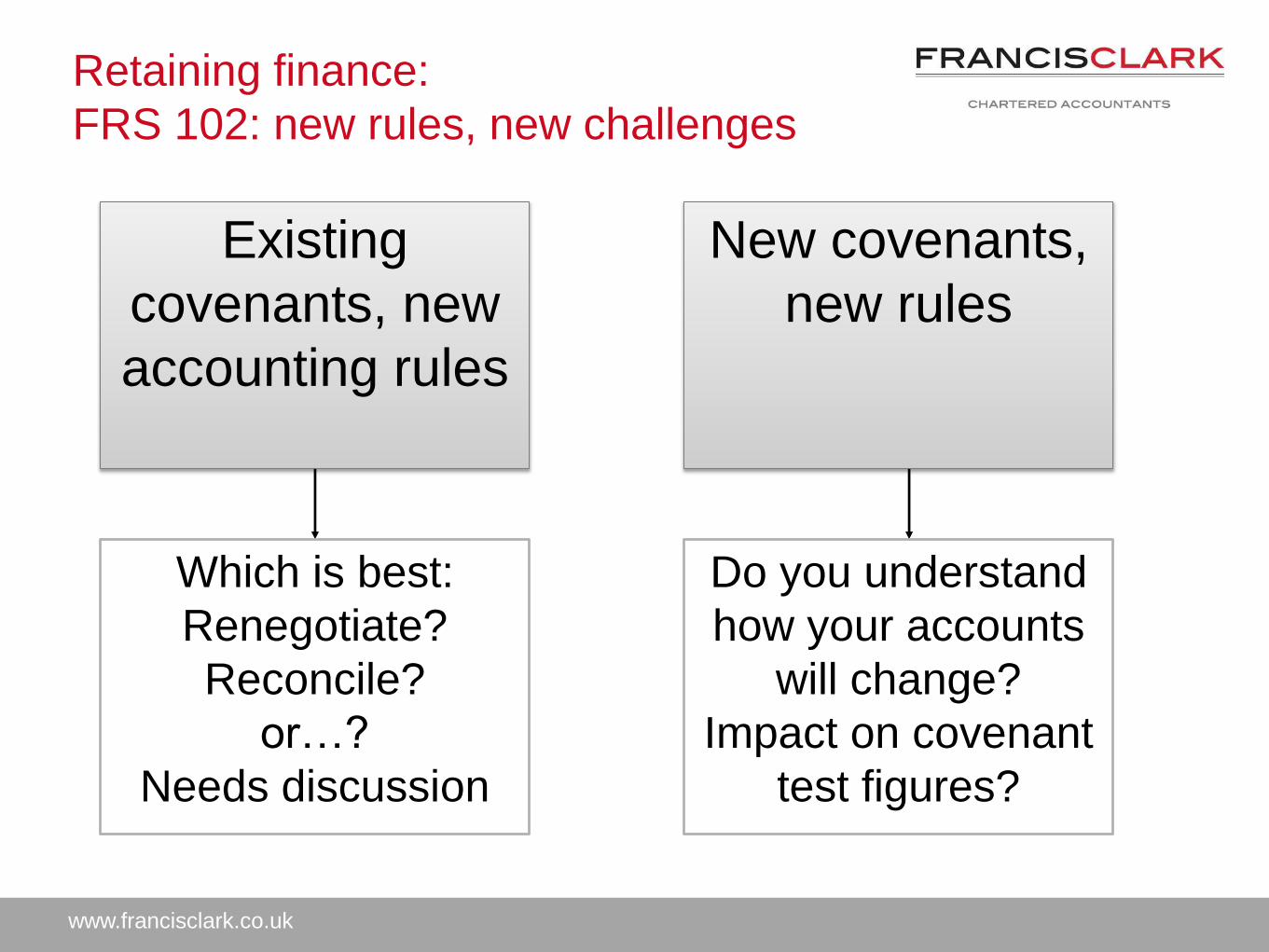

Retaining finance:

FRS 102: new rules, new challenges

Existing

covenants, new

accounting rules

New covenants,

new rules

Which is best:

Renegotiate?

Reconcile?

or…?

Needs discussion

Do you understand

how your accounts

will change?

Impact on covenant

test figures?

www.francisclark.co.uk

Break

Session 2 start time

10:10am

#FCFinanceSW