©2015, College for Financial Planning, all rights reserved. Session 8 Transfer Tax Return Filing...

12

©2015, College for Financial Planning, all rights reserved. Session 8 Transfer Tax Return Filing Requirements CERTIFIED FINANCIAL PLANNER CERTIFICATION PROFESSIONAL EDUCATION PROGRAM Estate Planning

-

Upload

harold-hawkins -

Category

Documents

-

view

213 -

download

0

Transcript of ©2015, College for Financial Planning, all rights reserved. Session 8 Transfer Tax Return Filing...

©2015, College for Financial Planning, all rights reserved.

Session 8Transfer Tax Return Filing Requirements

CERTIFIED FINANCIAL PLANNER CERTIFICATION PROFESSIONAL EDUCATION PROGRAMEstate Planning

Session Details

Module 3

Chapter(s)

1

LOs 3-1 Describe the basic features of the federal estate tax.

Module 4

Chapter(s)

1

LOs 4-1 Describe the basic features of the federal gift tax.

Module 5

Chapter(s)

1

LOs 5-1 Identify the purpose and basic features of the federal generation-skipping transfer tax (GSTT).

8-2

Estate Tax Return Filing Requirements

• Use IRS Form 706.

• Return is due nine months after date of death; automatic six months extension available.

• The personal representative or, if none, the persons in possession of estate property are required to file.

• Property is valued as of the date of death or six months after the date of death (alternate valuation date).

• Return must be filed ifo gross estate exceeds exclusion amount for year of

death;oro gross estate plus adjusted taxable gifts exceed

exclusion amount for year of death;o file to transfer DSUE amount to surviving spouse

8-3

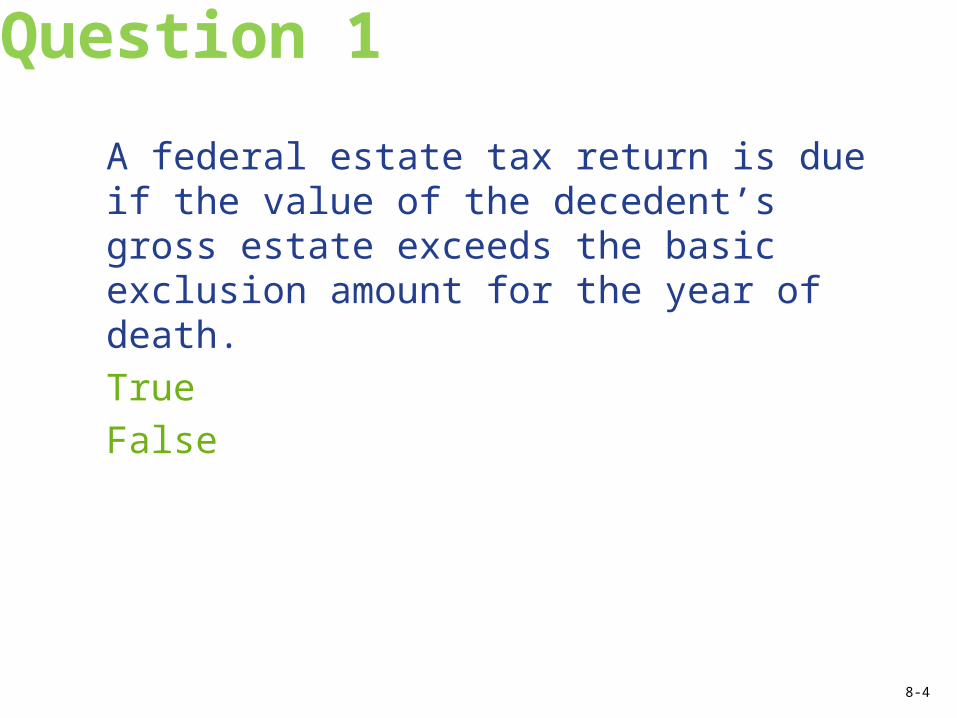

Question 1

A federal estate tax return is due if the value of the decedent’s gross estate exceeds the basic exclusion amount for the year of death.TrueFalse

8-4

Question 2

An estate tax return must be filed if the decedent’s estate has a tax base that exceeds the applicable ET exclusion amount in the year of death.TrueFalse

8-5

Gift Tax: Return Requirements

• Filed on IRS Form 709 on a calendar-year basis

• Return is due April 15 of following calendar year, or upon filing of the donor’s estate tax return if earlier

• Donor (or donor’s executor) is responsible for filing of return and payment of tax, if any

• Valuation date is the date of completion for each gift

• Return must be filed if donor has made:o present interest gifts > the maximum annual

exclusion (that do not also qualify automatically for the marital or charitable deduction)

o future interest gifts of any amounto split gifts with spouseo a gift for which the QTIP election is takeno a partial interest charitable gift is made

8-6

Question 3

Betty established and funded a QTIP trust for the benefit of her husband and their three children.

Which of the following statements are correct?

I. Betty must file a Form 706 tax return for her gifts to her husband and children.

II. Betty does not need to report that a generation-skipping transfer has occurred.

III. Betty must file a Form 709 tax return by nine months after the trust was funded.

IV. If Betty dies, and is required to file an ET return, and her ET return is due before the date for filing her GT return, the GT return must be filed with the ET return.a. I and III onlyb. II and IV onlyc. I, II, and III onlyd. II, III, and IV only

8-7

Question 4

Gary made the following gifts in the years shown:o 2010—gave $11,000 cash to his brothero 2011—established and funded a CRAT naming his wife as

sole income beneficiaryo 2014—gave $28,000 to his sister; Gary’s wife agreed to

split this giftWhich of the following statements are correct?

I. Gary does not need to file a gift tax return for the 2010 gift.

II. Gary does need to file a gift tax return for the 2014 gift.III. Gary does not need to file a gift tax return for the 2011

gift.IV. Gary’s wife must file a gift tax return for the 2014 gift, or

evidence her consent to split on Gary’s gift tax return.a. I and III onlyb. II and III onlyc. I, II, and IV onlyd. II, III, and IV only

8-8

GSTT: Return Requirements

Type of GST

IRSForm # Due Date

Liable Party

Valuation Date

Trigger to File

Inter vivos direct skip

709 Same as gift tax

Donor Completion of gift

Same as gift tax

Direct skip at death

706 Same as estate tax

PR of estate

DOD or 6 mos. later

Direct skip of any amount

Taxable termination (indirect skip)

706GS (T) 4/15 of year after termination

Trustee (or person in possession)

Date of taxable termination

Termination of nonskip interests in indirect skip

Taxable distribution (indirect skip)

706GS (D) 4/15 of yearafter distribution

Skip party receiving distribution

Date of taxable distribution

Distribution to a skip party in indirect skip

8-9

Question 5

For an indirect generation-skipping transfer, the return computing GSTT due will be filed by either a skip party or a trustee.TrueFalse

8-10

Question 6

Donald established an irrevocable inter vivos trust for the benefit of his only son and grandson. The son and grandson are to receive equal income at the discretion of an institutional trustee until one of them dies, when the remainder will go to the survivor.

Which one of the following statements is correct?

a. Donald will have to file a Form 706 by April15 of the year following the year of the transfer.

b. The trustee will have to file a Form 706GS(T) by April15 of the year following a distribution of income to the grandson.

c. The PR of the estate of Donald’s son will have to file a Form 706GS(D) by April15 of the year following his death if he dies first

d. Donald, or the PR of his estate, will have to file a Form 709 gift tax return by the earlier of 9 months after Donald’s death or April 15 of the calendar year following the year of the transfer.

8-11

©2015, College for Financial Planning, all rights reserved.

Session 8End of Slides

CERTIFIED FINANCIAL PLANNER CERTIFICATION PROFESSIONAL EDUCATION PROGRAMEstate Planning