CERTIFIED FINANCIAL PLANNER CERTIFICATION PROFESSIONAL EDUCATION PROGRAM Estate Planning

Upload

ross-powellCategory

view

217download

0

©2015, College for Financial Planning, all rights reserved.

Session 11Education Planning

CERTIFIED FINANCIAL PLANNER CERTIFICATION PROFESSIONAL EDUCATION PROGRAMFinancial Plan Development Course

Start Recording

This class is being recorded so you may review it at a future time.

11-2

Education Planning

• Need/Cost/Benefit• Funding Calculations• Funding Vehicles

11-3

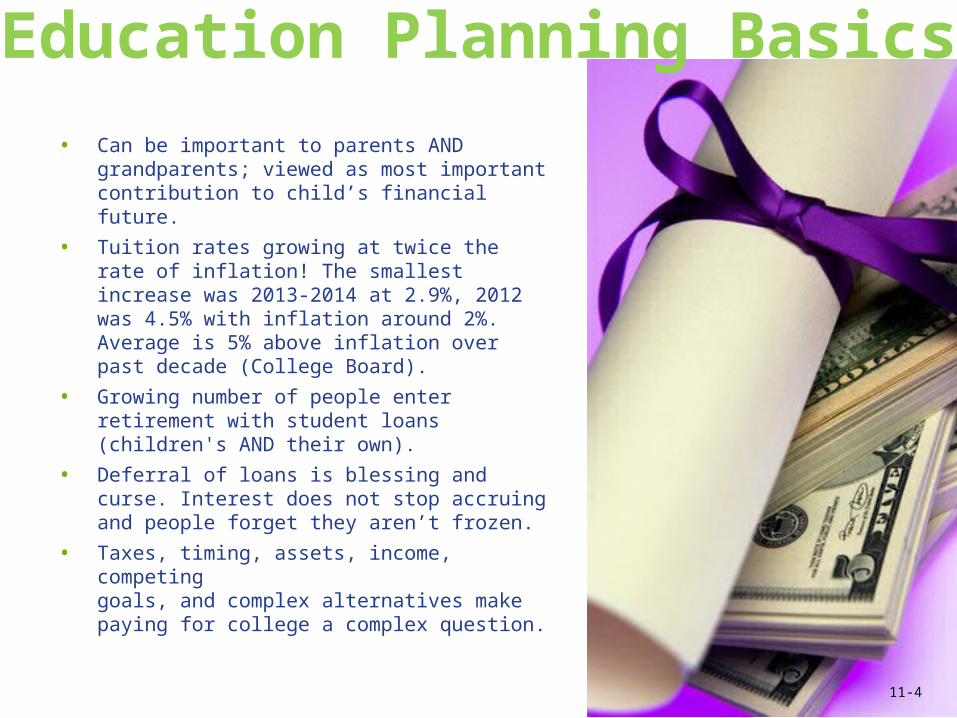

Education Planning Basics

• Can be important to parents AND grandparents; viewed as most important contribution to child’s financial future.

• Tuition rates growing at twice the rate of inflation! The smallest increase was 2013-2014 at 2.9%, 2012 was 4.5% with inflation around 2%. Average is 5% above inflation over past decade (College Board).

• Growing number of people enter retirement with student loans (children's AND their own).

• Deferral of loans is blessing and curse. Interest does not stop accruing and people forget they aren’t frozen.

• Taxes, timing, assets, income, competing goals, and complex alternatives make paying for college a complex question.

11-4

Common Obstacles“I put myself through school.”

• Tuition costs of public four-year school

• Minimum wage in 1979 = 254 hours per year

• Today = 923 hours to pay tuition (half-time with no living expenses)

• Makes it difficult to complete college in under 7 years, which is why many people start and fail to complete

“They/we can borrow the money.”

• Average student debt for undergraduate is $25,250; 5% higher than year before. This doesn’t reflect parental debt or debt other than student loans.

• Which college is attended makes a dramatic difference in amount of loans.

“We committed to pay for it.”

• Frequently there is no discussion with child on expectations, schools, costs, living at home, etc., which leads to parents over-committing.

“My child will get a scholarship or full ride.”

• What are the plans if they don’t?

11-5

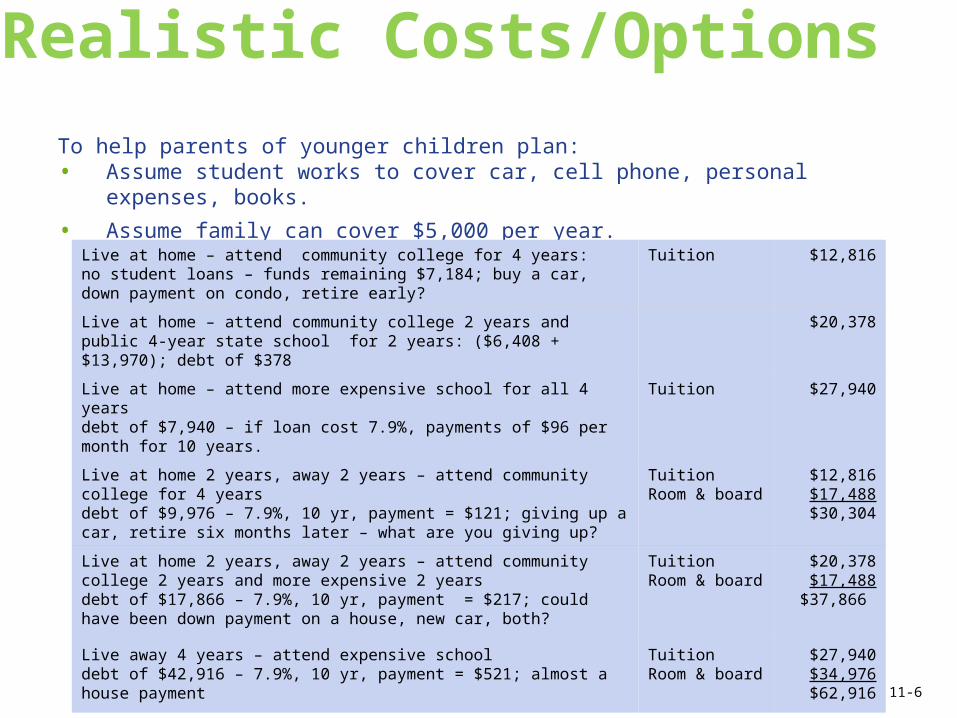

Realistic Costs/Options

To help parents of younger children plan:• Assume student works to cover car, cell phone, personal expenses, books.

• Assume family can cover $5,000 per year.

Live at home – attend community college for 4 years: no student loans – funds remaining $7,184; buy a car, down payment on condo, retire early?

Tuition $12,816

Live at home – attend community college 2 years and public 4-year state school for 2 years: ($6,408 + $13,970); debt of $378

$20,378

Live at home – attend more expensive school for all 4 years

debt of $7,940 – if loan cost 7.9%, payments of $96 per month for 10 years.

Tuition $27,940

Live at home 2 years, away 2 years – attend community college for 4 yearsdebt of $9,976 – 7.9%, 10 yr, payment = $121; giving up a car, retire six months later – what are you giving up?

TuitionRoom & board

$12,816$17,488$30,304

Live at home 2 years, away 2 years – attend community college 2 years and more expensive 2 yearsdebt of $17,866 – 7.9%, 10 yr, payment = $217; could have been down payment on a house, new car, both?

TuitionRoom & board

$20,378$17,488

$37,866

Live away 4 years – attend expensive schooldebt of $42,916 – 7.9%, 10 yr, payment = $521; almost a house payment

TuitionRoom & board

$27,940$34,976$62,916

11-6

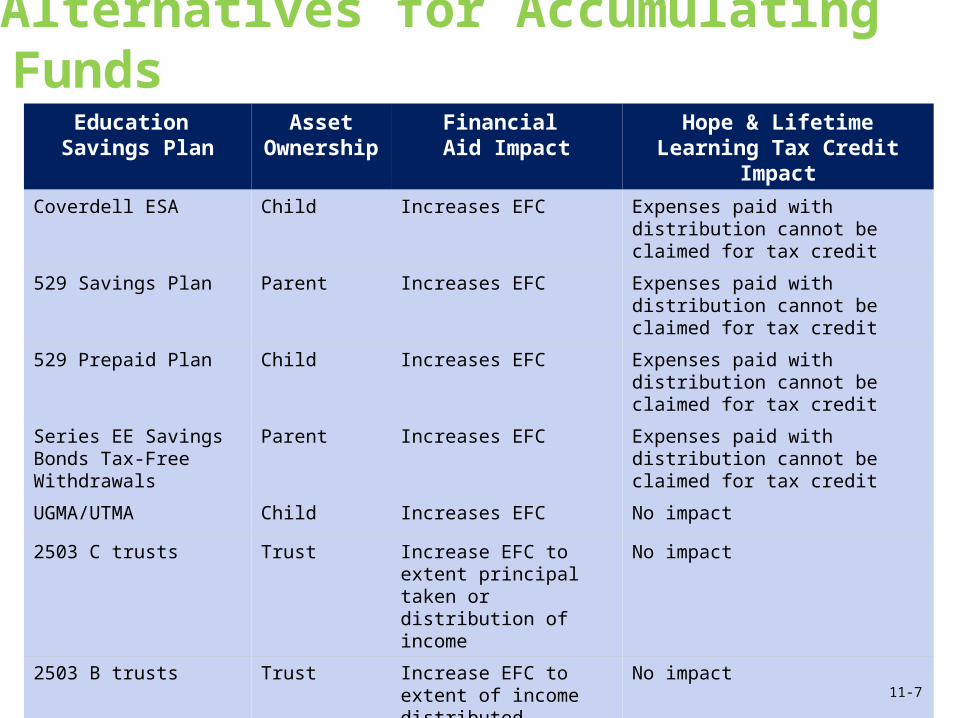

Alternatives for Accumulating Funds

Education Savings Plan

Asset Ownershi

p

Financial Aid Impact

Hope & Lifetime Learning Tax Credit

Impact

Coverdell ESA Child Increases EFC Expenses paid with distribution cannot be claimed for tax credit

529 Savings Plan Parent Increases EFC Expenses paid with distribution cannot be claimed for tax credit

529 Prepaid Plan Child Increases EFC Expenses paid with distribution cannot be claimed for tax credit

Series EE Savings Bonds Tax-Free Withdrawals

Parent Increases EFC Expenses paid with distribution cannot be claimed for tax credit

UGMA/UTMA Child Increases EFC No impact

2503 C trusts Trust Increase EFC to extent principal taken or distribution of income

No impact

2503 B trusts Trust Increase EFC to extent of income distributed

No impact

Retirement Plans Parent Does not increase EFC No impact

Variable Universal Life Insurance

Parent Does not increase EFC No impact11-7

Options

• Scholarships: average undergraduate was $2,523 in 2008

• Federal grantso Pell: undergraduates only, basis of financial need, part-time available,

maximum of $5,550.o FSEOGs: administered by individual schools, undergraduate, part-

time, need based.

• Federal Loanso Perkins Loans: administered by schools,

undergraduate and graduate, half-time, need based, 6% interest, interest doesn’t start until 9 months after graduating, 10-year repayment typical.

o Stafford Loans: direct subsidized and unsubsidized, subsidized has government pay interest while in school and for 6 months. Deferral allowed, at least half-time, no part-time students, maximum each year, fixed rates until graduation, direct at 4.66% undergraduate and 6.21% graduate in 2015. Subsidized Stafford: 3.86%/5.41%

11-8

PLUS Loans

• Parent Loan for Undergraduate Students

• Issued for difference between college defined cost of attendance (COA) and all other financial aid received

• Interest is now variable July 1 – June 30 fixed – now 7.21%

• Payment begins 60 days after loan is disbursed and can extend from 5–10 years

• Parents may be able to defer payment of principal while student is enrolled at least half-time but still required to make interest-only payments

11-9

Tuition & Fees: Adjustment or Credit?

9,842 00Autumn Dudella

$140,514

140,514

2,000

Better off with credit?

11-10

Education Deductions and Credits

Above the line deductions (adjustments to income)

• Student Loan Interest; maximum $2,500; phaseout

• Single: $65k-$80k; Married: $130k-$160k prorated

• Tuition and Fees (credits better unless phased out or used)

Credits

• American Opportunity Credit (100% of first $2,000 and 25% of next $2,000 for maximum of $2,500; subject to MAGI phaseout $80k-$90K single, $160-$180k married, until 2017)

• Lifetime Learning Credit ($2,000 per year, unlimited years with phaseout $55k-$65k single or $110k-$130k married)

11-11

Known About the Dudellas

Choice made:

“Providing for your child’s education is your number one concern. You are willing to sacrifice in order to provide four years of college at an in-state tuition rate for a public school. Autumn has just completed her first semester of college at Colorado State University. You have planned on using loans for the majority of the costs as you do not have the savings available to pay the expenses, although you are open to other suggestions.”

Existing loan: 7.9% for $15,386 deferred until after graduation.

11-12

Possible Recommendations

You have committed to helping Autumn attend four years of college at Colorado State at a cost of around $15,000 per year. She has completed her first year and your remaining liability is $45,000. You have a current loan for $15,500 and anticipate taking additional loans for the balance and repaying them as soon as possible. This last year the tax form was sent directly to Autumn rather than you.

Recommendation 1Make sure that you meet school procedures so that tax forms for deduction and credits are sent to you.

11-13

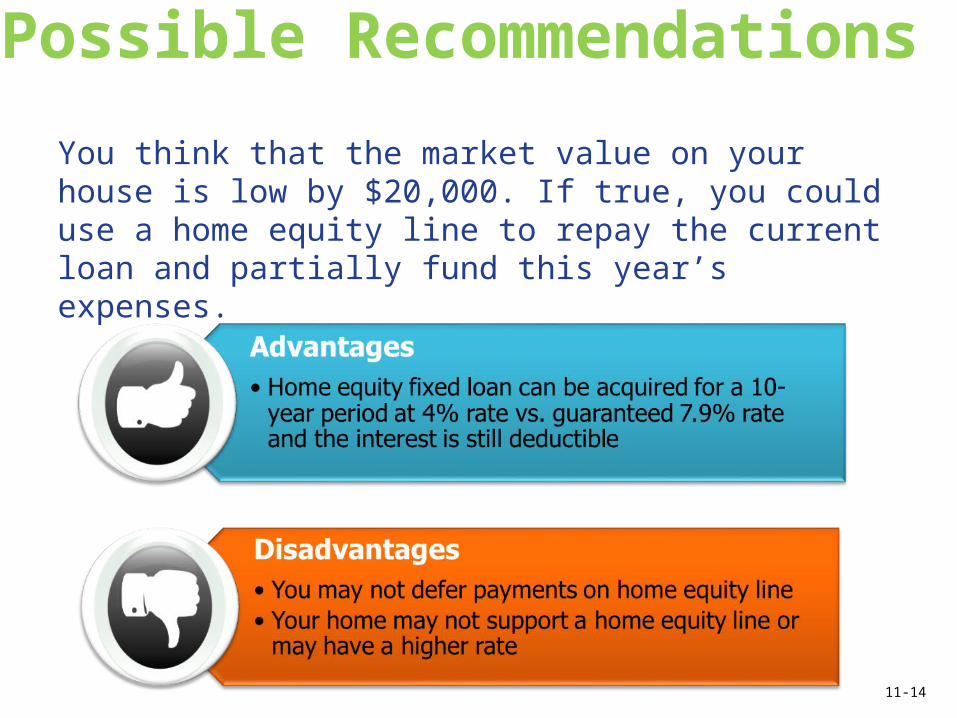

Possible Recommendations

You think that the market value on your house is low by $20,000. If true, you could use a home equity line to repay the current loan and partially fund this year’s expenses.

11-14

Possible Recommendations

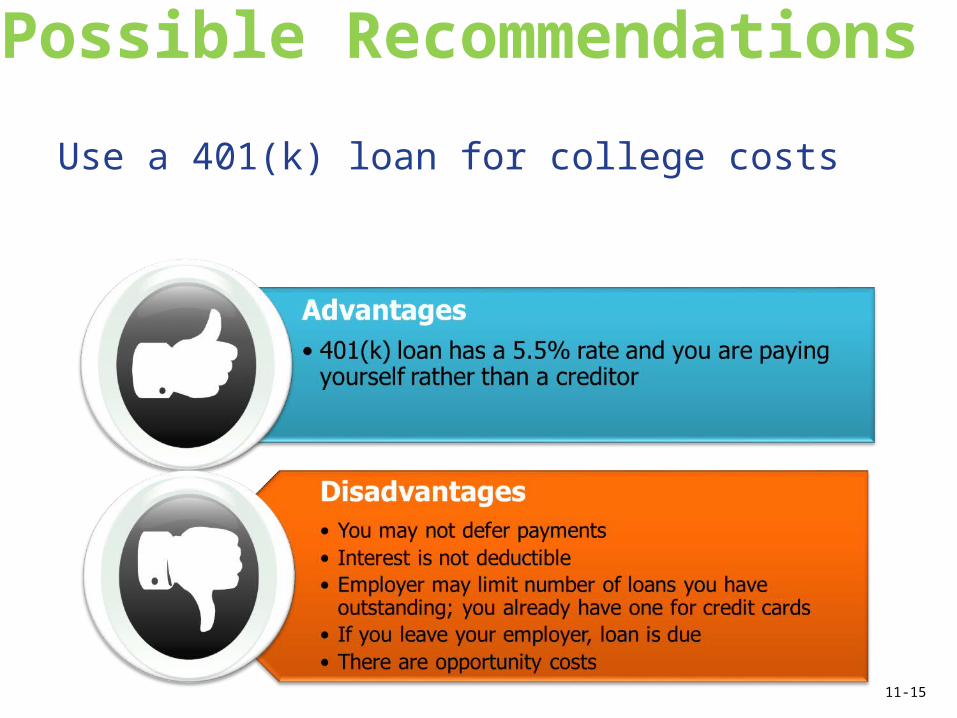

Use a 401(k) loan for college costs

11-15

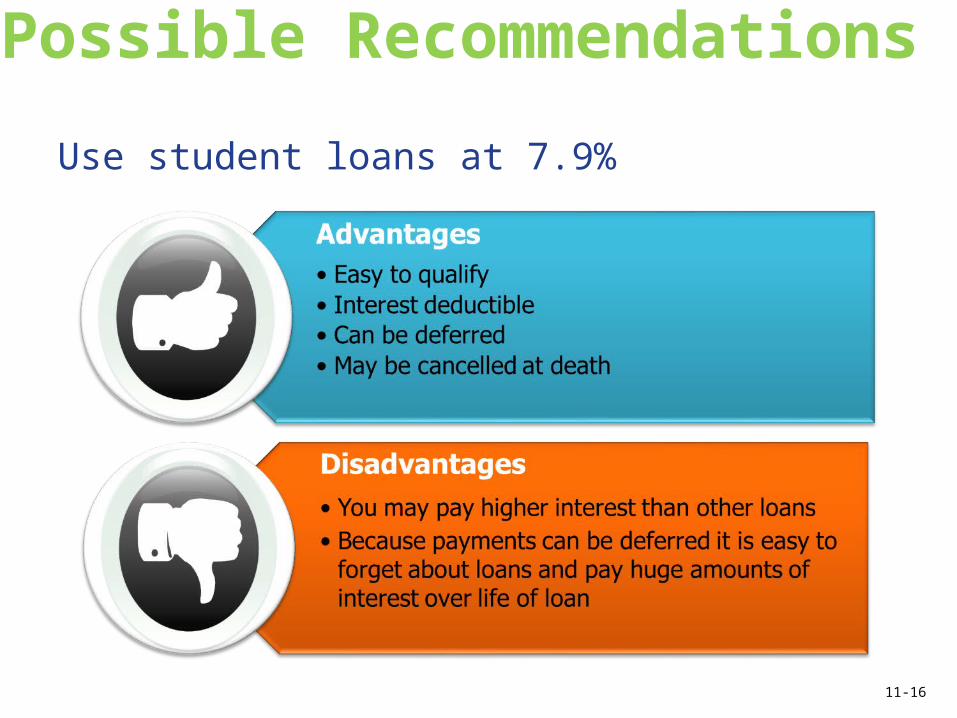

Possible Recommendations

Use student loans at 7.9%

11-16

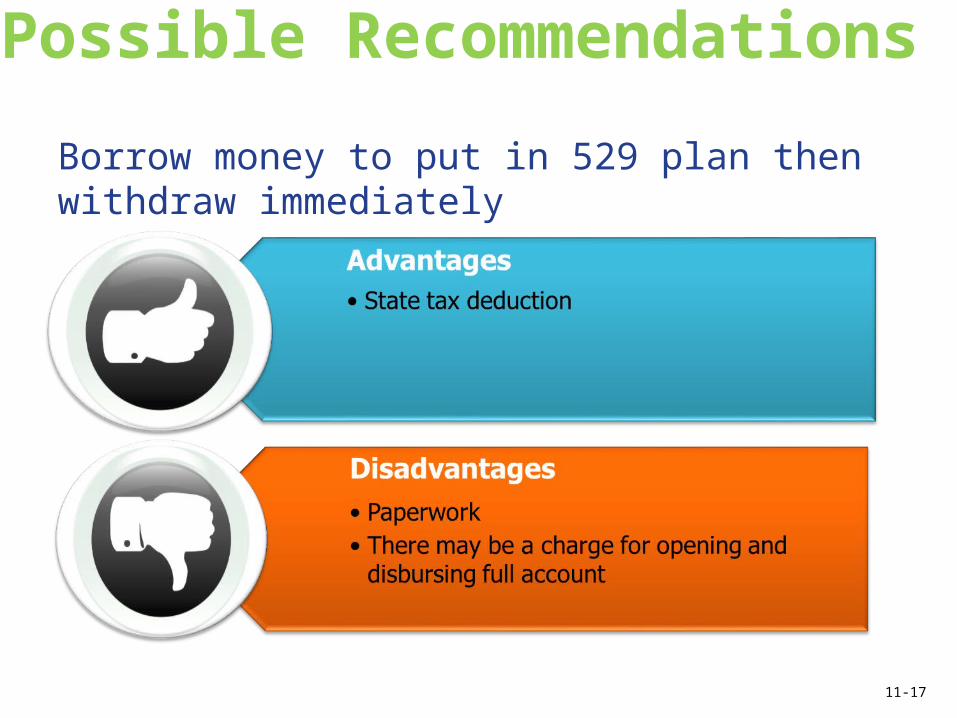

Possible Recommendations

Borrow money to put in 529 plan then withdraw immediately

11-17

Impact

• We can illustrate loans to pay for college. We have found no alternatives to suggest other than making sure the appropriate procedures are followed for tax purposes.

• We should reevaluate this next year or if increased home value turns out to be accurate. Home equity line may or may not be better alternative.

• Discounted stock purchase plan could help pay off loans or fund part of college more efficiently, but there are risks.

• May be able to contribute to 529 then immediately withdraw and get state tax deduction.

11-18

Dowler Education Goals

Planning for their son Matt’s education is one of Jim and Anne’s top goals. They are not currently using any specific strategies for accumulating funds; however, $22,000 of their municipal bonds were purchased with college in mind.

Jim’s parents just informed him that they set up a 529 plan for Matt’s college education and plan on depositing $100 per month into the account until Matt goes to college. This got Jim and Anne thinking that they should perhaps be gaining some tax efficiency and that there may be a more strategic way of accumulating college funds.

They wish to accumulate $20,000 to cover education costs for four years, adjusted for inflation at 4.5%. Part of that will come from the $100 per month from Jim’s parents and from the $22,000 they have already accumulated.

They would like to know what they need to save in order to have the money accumulated prior to Matt attending college because they believe there may be additional expenses during his college years that will need to be paid from current income.

11-19

More on Education Goal

Additionally, after discussing the relationship between normal inflation and college inflation, they realize that municipal bonds may not be the best answer. They would like to understand the benefits and drawbacks of both Coverdell and 529 plans. For purposes of this course, we are going to assume that the investments will achieve the same 5.5% after-tax return for both the grandparents’ and parents’ contributions.

#1. Calculate what they will need to save.

11-20

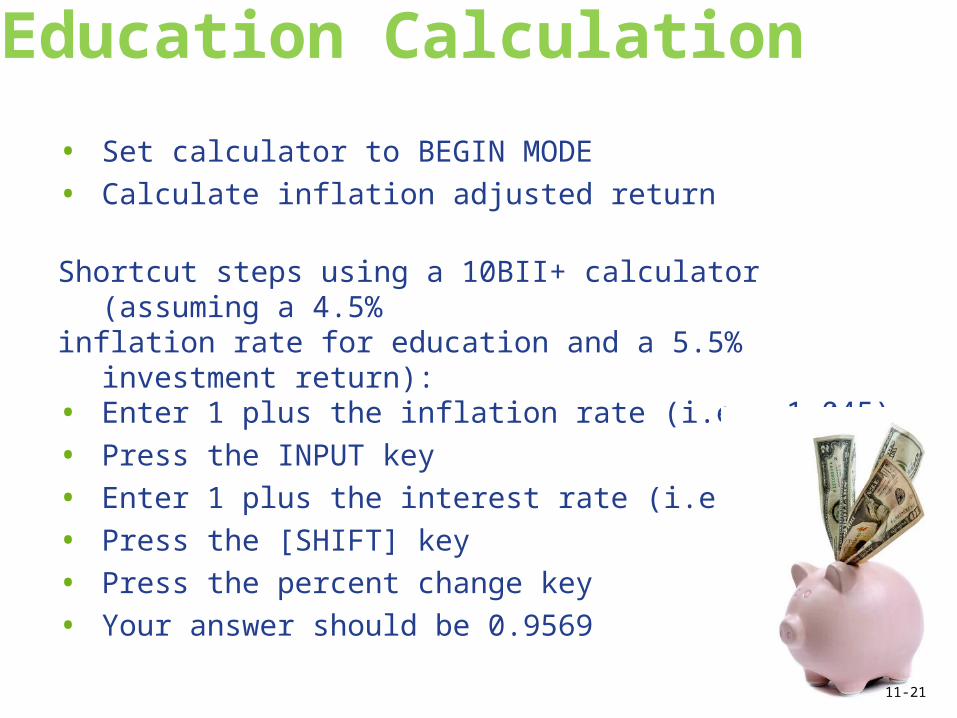

Education Calculation

• Set calculator to BEGIN MODE

• Calculate inflation adjusted return

Shortcut steps using a 10BII+ calculator (assuming a 4.5%

inflation rate for education and a 5.5% investment return):

• Enter 1 plus the inflation rate (i.e., 1.045)

• Press the INPUT key

• Enter 1 plus the interest rate (i.e., 1.055)

• Press the [SHIFT] key

• Press the percent change key

• Your answer should be 0.956911-21

Education Calculation

Follow these four steps:• Estimate amount needed at start of

education goal• Calculate lump sum of annuity due with

increasing costs over the four years• Project value of current investments and

subtract from amount needed to determine target

• Determine savings amount per year needed on level basis for this year

11-22

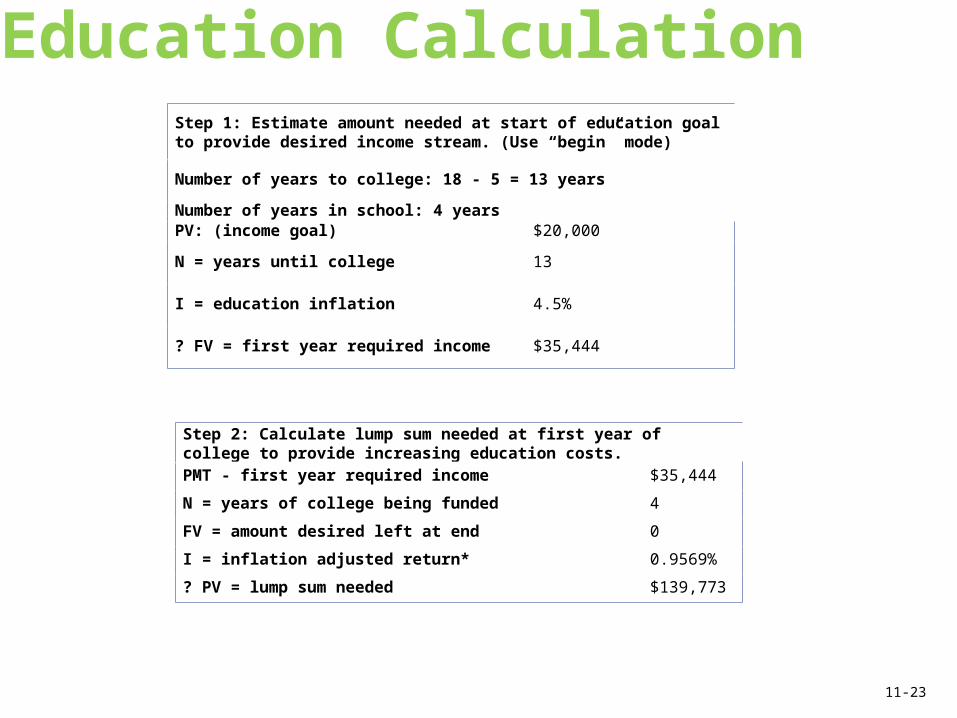

Education CalculationStep 1: Estimate amount needed at start of education goal to provide desired income stream. (Use “begin” mode)

Number of years to college: 18 - 5 = 13 years

Number of years in school: 4 yearsPV: (income goal) $20,000

N = years until college 13

I = education inflation 4.5%

? FV = first year required income $35,444

Step 2: Calculate lump sum needed at first year of college to provide increasing education costs. PMT - first year required income $35,444

N = years of college being funded 4

FV = amount desired left at end 0

I = inflation adjusted return* 0.9569%

? PV = lump sum needed $139,773

11-23

Education Calculation

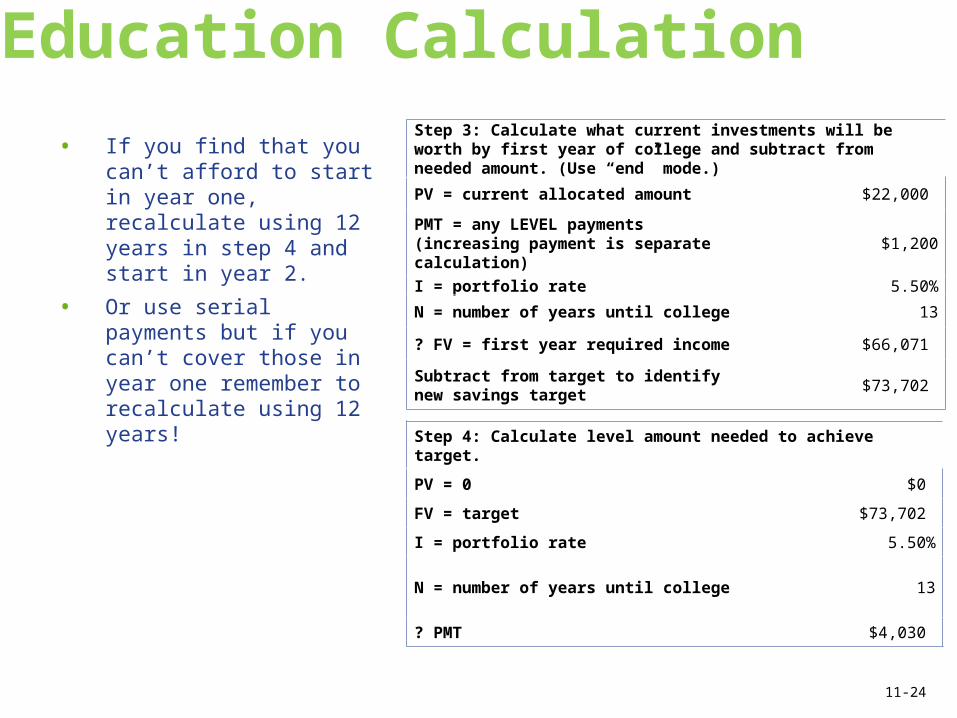

• If you find that you can’t afford to start in year one, recalculate using 12 years in step 4 and start in year 2.

• Or use serial payments but if you can’t cover those in year one remember to recalculate using 12 years!

Step 3: Calculate what current investments will be worth by first year of college and subtract from needed amount. (Use “end” mode.)

PV = current allocated amount $22,000

PMT = any LEVEL payments (increasing payment is separate calculation)

$1,200

I = portfolio rate 5.50%

N = number of years until college 13

? FV = first year required income $66,071

Subtract from target to identify new savings target

$73,702

Step 4: Calculate level amount needed to achieve target.

PV = 0 $0

FV = target $73,702

I = portfolio rate 5.50%

N = number of years until college 13

? PMT $4,030

11-24

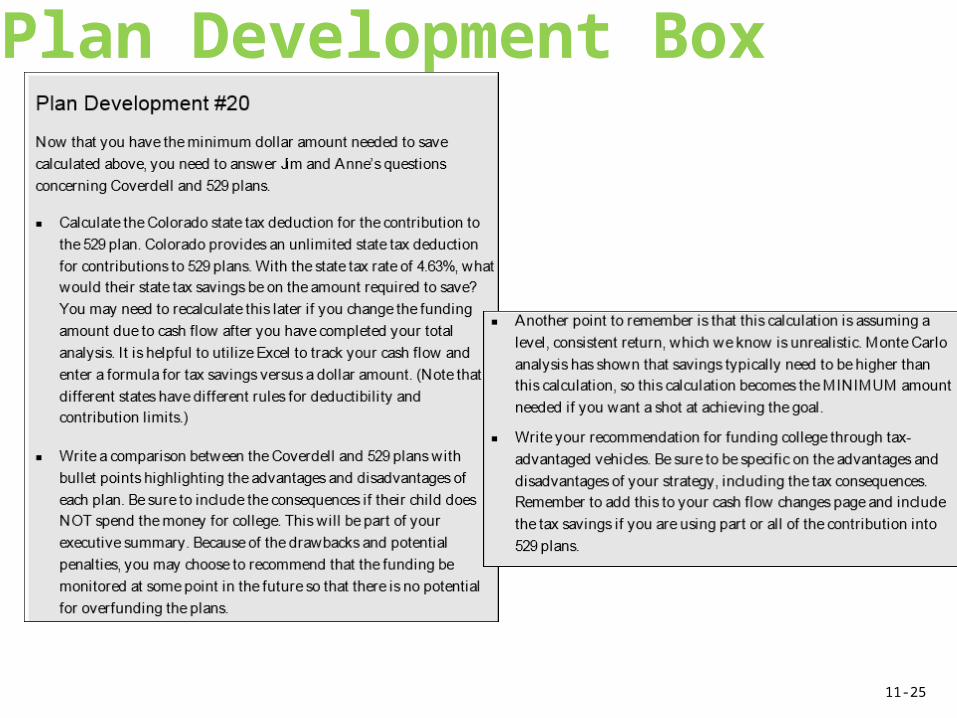

Plan Development Box

11-25

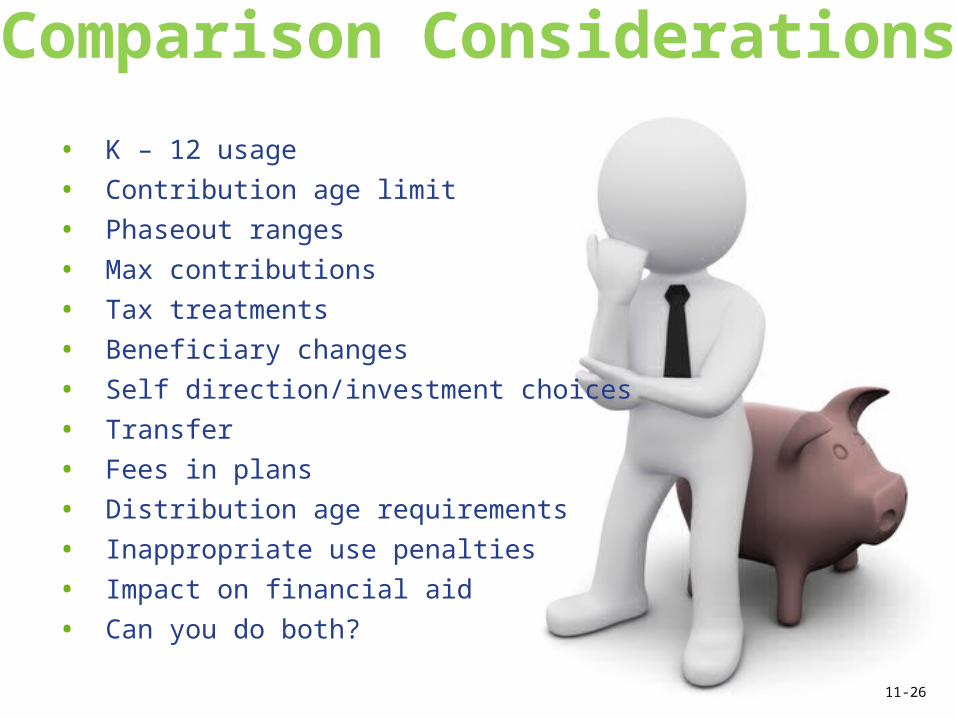

Comparison Considerations

• K – 12 usage

• Contribution age limit

• Phaseout ranges

• Max contributions

• Tax treatments

• Beneficiary changes

• Self direction/investment choices

• Transfer

• Fees in plans

• Distribution age requirements

• Inappropriate use penalties

• Impact on financial aid

• Can you do both?

11-26

Next Class

11-27

©2015, College for Financial Planning, all rights reserved.

Session 11End of Slides

CERTIFIED FINANCIAL PLANNER CERTIFICATION PROFESSIONAL EDUCATION PROGRAMFinancial Plan Development Course