20141003 cielo october

46

Presentation October, 2014 Corporate

-

Upload

cielositeri -

Category

Documents

-

view

12.266 -

download

1

description

Transcript of 20141003 cielo october

Presentation October, 2014

Corporate

The THE COMPANY MAKES FORWARD LOOKINGSTATEMENTS THAT ARE SUBJECT TO RISKS AND UNCERTAINTIES

DISCLAIMER

These statements are based on the beliefs and assumptions of our management as well as on information currently available to us. Forward-looking statements

include information regarding our current intent, beliefs or expectations, in addition to those of the members of the Board of Directors and Executive Officers of the

Company.

Forward-looking statements also include information regarding our possible or assumed future operating results, as well as statements preceded or followed by, or

that include, the words ''believes”, ''may”, ''will”, ''continues”, ''expects”, ''anticipates”, ''intends”, ''plans”, ''estimates”, or similar expressions.

Forward-looking statements are not guarantees of performance. They involve risks, uncertainties and assumptions, for they relate to future events, thus depending on

circumstances that may or may not occur. Our future results and the creation of value to shareholder s may differ significantly from those expressed in or suggested by these

forward-looking statements. Many factors determining these results and values are beyond Cielo’s ability to control or predict.

#1 MERCHANT ACQUIRER

AND PAYMENT

PROCESSOR IN BRAZIL

AND LATIN AMERICA

OF GDP CAPTURED

THROUGH CIELO´S

NETWORK

MARKET CAP – AMONG

10 LARGEST IN

BM&FBOVESPA

BRL 65 BILLION

9.3%

EXCHANGE RATE: 1USD = BRL2.2

CIELO | LEADING MERCHANT ACQUIRER

3

Copyright © Cielo | Todos os direitos reservados

MULTI-BRAND

MULTICHANNEL

MULTI SERVICE

THE MOST COMPLETE ELECTRONIC

PAYMENTS SOLUTION IN THE

MARKET SO THAT OUR CUSTOMERS

CAN SELL EVEN MORE

CIELO | THE MOST COMPLETE SOLUTION

5

CIELO | A DIFFERENTIATED STORY

Market driven

by powerful

Secular Trends

Leader in a

growing and

unique market

Strongest

market

distribution

Resilient

Growth and

Profitability

Differentiation

and Innovation

Experienced

Management

Team

6

CIELO|MARKET DRIVEN BY POWERFUL SECULAR TRENDS

Source: IBGE,ABECS 6

* Excluding Private Labels

1.787 1.980

2.249 2.499

2.745 3.017

789 799

2008 2009 2010 2011 2012 2013 1Q14 2Q14

PCE - Private Consumption Expenditure (R$ billion)

329 394

487

601

710

837

219 229

2008 2009 2010 2011 2012 2013 1Q14 2Q14

Card Expenditure (R$ billion)*

18,4% 19,9%

21,7% 24,1%

25,9% 27,7% 27,8% 28,7%

2008 2009 2010 2011 2012 2013 1Q14 2Q14

Cards Expenditure over PCE (%)

CIELO | LEADER IN A GROWING AND UNIQUE

MARKET

Unique Credit Product

• Credit in Installments product – monthly payments with no interest to cardholder

Fully Integrated Business Model

• Present in the whole value chain: affiliation, capturing, processing and settlement

Prepayment of Receivables

• Consequence of D+30 days cycle in a credit transaction

Industry Structure

• Strong concentration as a consequence of the few large banks in Brazil

7

CIELO | STRONGEST MARKET DISTRIBUTION

Brazil has a total area of 8,514,876 km

NUMBER OF BRANCHES

Others Total

NORTH 322 276 96 39 176 39 0 0 2 0 0 57 1,007

NORTHEAST 1,186 842 294 196 640 56 3 7 9 0 0 193 3,426

MIDWEST 488 344 293 109 309 103 1 6 7 111 1 106 1,878

SOUTHEAST 2,410 2,413 2,525 1,912 1,588 425 7 103 73 3 2 683 12,144

SOUTH 1,083 777 634 370 644 229 513 10 16 0 2 255 4,533

TOTAL 5,489 4,652 3,842 2,626 3,357 852 524 126 107 114 5 1,293 22,918

Banking distribution is the main barrier to new players

45% of the affiliations occur through Cielo

SOURCE: BRAZILIAN CENTRAL BANK , AUGUST 2014 8

CIELO | EXPERIENCED MANAGEMENT TEAM

Management Team

• Rômulo de Mello Dias CEO

• Clovis Poggetti Jr CFO and IRO

• Eduardo Chedid Simões EVP – Commercial Retail

• Adriano Navarini EVP – Corporate

• Dilson Tadeu Ribeiro EVP – Products and Strategic Planning

• Plínio Cardoso da Costa Patrão COO

• Roberto Menezes Dumani EVP – Organizational Development

A very experienced management team has helped build the payments industry in Brazil

• Net Profit

• Financial Volume Growth

• Customer Satisfaction

Metrics for Management’s Variable Compensation

9 * EVP: Executive Vice President

10

CIELO PROMO

Cielo’s offering is the most comprehensive available including some unique products

CIELO FIDELIDADE

CIELO LINKCI

CIELO CREDIÁRIO

• Loyalty program developed exclusively to merchants

• Largest B2B in Latin America

• Accrual of points based on merchant’s volume with Cielo

• Most flexible and the

easiest to use

promotional

marketing tool in the

market

• Can be offered to

merchants, brands

and issuers

• Allows the merchant to offer check-in solution to its customers and the possibility to develop free advertising

• Allows the cardholder to recommend its favorite locals and redeem rewards

• Additional payment method that allows cardholders to pay in up to 48 installments, accessing a pre-approved credit line from their checking accounts through their bank cards

CIELO| NEW PRODUCTS

CIELO| NEW TECHNOLOGIES

11

Cielo invests in new technologies for capturing devices we make available to our merchants

• Wireless POS terminals (GPRS)

Corresponds to 59% of Cielo’s installed basis (as of 2Q14)

Strong demand from our merchants

• NFC (Near Field Communication)

Up to now, more than 1 million terminals installed with

such technology

• Mobile Chip & Pin

Perfect for professionals and merchants that require

convenience and mobility

Data protected to ensure the integrity of transactions

Sales Receipt may be sent by email to the cardholder

CIELO| STRATEGIC PLANNING

Acquisition of M4U

Acquisition of Braspag

May

2011 January 2010

March 2012

September

2012

Partnership with CyberSource

Acquisition of MeS

August 2010

November

2012

Partnership with Facebook

and Planet Payment

Cielo has been active to be well positioned in eCommerce and mobile payment

12

Launching of Cielo Mobile Chip & Pin

October

2013

April

2014

MoU to participate in Stelo

June

2014

MoU to create a JV between Cielo and Linx

Launching the new e-commerce platform

12,9%

9,7%

13,1% 14,4% 14,0%

10,9%

13,5% 14,4%

12,1%

15,9% 15,9%

13,2%

15,9%

17,4%

9,0%

11,9% 12,5%

8,1% 9,6%

10,2%

6,8%

2,6%

5,7% 6,9%

6,3%

3,7%

6,2% 7,1%

5,1%

8,7% 8,9%

5,7%

8,8%

11,4%

2,2%

4,8% 5,5%

0,5%

3,5% 3,7%

0,1%

2,1%

4,1%

6,1%

8,1%

10,1%

12,1%

14,1%

16,1%

18,1%

20,1%

Source: CIELO

CIELO´S AMPLIFIED RETAIL INDEX (ICVA) NOMINAL REVENUE OF SALES GROWTH (YOY)

DIFFERENTIAL

Territorial coverage of 99% of the

country

Scope sized companies: from small retailers to

large retailers

Based on actual information

and not in sample surveys

Dynamic model, based on the actual mix

of each sector in the economy

Over 20 economic sectors, including services (eg: airlines, restaurants and e-commerce)

Improved disclosure

13

163.941 202.084 244.960 279.617

98.742 118.315

138.368

169.131

Quarterly Evolution (R$ million)

67.246 73.120 75.979

39.039 46.454 49.359

2Q13 2Q14 1Q14

119,574 125,338

106,284

Annual Evolution (R$ million)

2012 2013

448,748

320,399

Credit

Debit

17.9%

4.8%

CAGR: 19.5%

14 The financial volume does not include Merchant E-Solutions transactions, i.e., it comprises the financial volume of the domestic market only.

CIELO| TRANSACTION FINANCIAL VOLUME

2011 2010

383,329

262,683

CIELO| NUMBER OF TRANSACTIONS

Quarterly Evolution (R$ million) 556 592 625

602 727 734

2Q13 1Q14 2Q14

1,318 1,359 1,158

Annual Evolution (R$ million)

2012 2013

4,902

3,317

Credit

Debit

4.8%

15 The number of transactions does not include Merchant E-Solutions transactions, i.e., it comprises the number of transactions of the domestic market only.

17.3%

2010 2011

1,601 1,837 2,062 2,283

1,716 1,964

2,240 2,618

3,801 4,302

CAGR: 13.9%

* Points of Sales Merchants are those that have made at least a single transaction in the last 30 days . The year is measured based on the closing

CIELO| OPERATIONAL INDICATORS

POS Terminals

Points of Sales Merchants (30 days)*

16

2010

1.743 1.867 1.899

1.324 1.435 1.473

2Q13 1Q14 2Q14

Quarterly Evolution (Thousand)

11.3%

9.0%

1.7%

2.6%

1.277

1.484

1.727 1.831

1.069 1.156 1.282

1.426

Annual Evolution (Thousand)

2010 2011 2013

CAGR: 10.1%

CAGR 12.8%

2012

2012 2013

1.619,8

1.817,7 1.840,7

2Q13 1Q14 2Q14

Annual Evolution (R$ million)

CIELO| NET OPERATING REVENUE

NET OPERATING REVENUE

Quarterly Evolution (R$ million)

CAGR: 19.0%

13.6%

17

2011 2010

3.992,5 4.208,7

5.385,3

6.734,2

1.3%

CIELO| COSTS + EXPENSES

2012* 2013

610,4 659,7 703,8

235,5 259,2

285,2

2Q13 1Q14 2Q14

Annual Evolution (R$ million)

Costs + Expenses per transaction

2Q13 1Q14 2Q14

Total (R$ cents)

0.73 0.70 0.73

Costs+ Expenses

per transaction

2010 2011 2012 2013

Total (R$ cents)

0.49 0.54 0.60 0.72

Quarterly Evolution (R$ million)

918.9 989.0

845.8

3,550.2

2,603.3

Costs

Expenses

CAGR: 29.8%

16.9%

7.6%

18

*2012 figures were impacted by Merchant E-Solutions in costs and expenses only in 4Q12

2010 2011

1.180,8 1.425,2 1.807,6

2.549,7 441,0 613,4

795,7

1.000,6

2,038.7

1,621.9

2012 2013

CIELO| PREPAYMENT OF RECEIVABLES

268,1

410,2 439,1

143,1 191,0 218,1

2Q13 1Q14 2Q14

Quarterly Evolution (R$ million)

Gross Revenue of Prepayment of Receivables Net Revenue of Prepayment of Receivables*

52.4%

63.8%

7.0%

14.2%

848.0

1,201.7

524.0 592.8 Annual Evolution (R$ million)

13.1%

41.7%

*Net of Cost od Funding Managerial 19

10.340,1 15.407,5

26.409,3

44.286,2

6,3% 7,6%

10,8%

15,9%

-

5.00 0,0

10.0 00,0

15.0 00,0

20.0 00,0

25.0 00,0

30.0 00,0

35.0 00,0

40.0 00,0

45.0 00,0

50.0 00,0

0,0 %

5,0 %

10, 0%

15, 0%

20, 0%

25, 0%

2012 2013

10.580

13.618 13.566

16,1%

18,7% 17,9%

2Q13 1Q14 2Q14

Annual Evolution (R$ million)

Average Term

2Q13 1Q14 2Q14

# Business Days

41.5 39.5 39.3

# Calendar Days

59.6 58.4 56.9

CIELO| PREPAYMENT OF RECEIVABLES INDICATORS

% Prepayment over Total Credit Volume

Financial Volume of Prepayment

Average Term

2010 2011 2012 2013

# Businesss

Dayss 47.2 39.8 39.9 41.5

# Calendar Days

68.5 57.9 58.7 60.3

Quarterly Evolution (R$ million)

28.2%

-0.4%

CAGR: 62.4%

20

2011 2010

2012* 2013

Annual Evolution (R$ million)

CIELO| EBITDA

Quarterly Evolution (R$ million)

EBITDA MARGIN %

EBITDA

9.3%

CAGR: 11.7%

2Q13 1Q14 2Q14

-4.6%

21

*2012 figures were only impacted by Merchant E-Solutions in 4Q12

2.564,0 2.388,5

3.097,9

3.575,2

64,2% 56,8% 57,5%

53,1%

-

500 ,0

1.00 0,0

1.50 0,0

2.00 0,0

2.50 0,0

3.00 0,0

3.50 0,0

4.00 0,0

0,0 %

10, 0%

20, 0%

30, 0%

40, 0%

50, 0%

60, 0%

70, 0%

80, 0%

90, 0%

100 ,0%

2011 2010

873.9 1,001.4 955.5

54,0% 55,1% 51,9%

2012* 2013

633,1

802,7 796,8

39,1% 44,2%

43,3%

2Q13 1Q14 2Q14

Annual Evolution (R$ million)

CIELO| NET INCOME

Quarterly Evolution (R$ million)

NET MARGIN %

NET INCOME

* 2012 figures were only impacted by Merchant E-Solutions in 4Q12

25.9%

-0.7%

CAGR: 13.5%

22

2011 2010

1.830,9 1.816,9

2.320,6

2.673,6

45,9% 43,2% 43,1%

39,7%

-

500 ,0

1.00 0,0

1.50 0,0

2.00 0,0

2.50 0,0

35, 0%

37, 0%

39, 0%

41, 0%

43, 0%

45, 0%

47, 0%

49, 0%

51, 0%

53, 0%

55, 0%

OUTLOOK | SOME KEY CONSIDERATIONS

23

• Brazilian Central Bank named the official regulator

• Initial guidelines released in November 2013

Regulatory Environment

• New business model adopted by second largest player

• New players gaining market share

Competitive Landscape

• Economic activity remains a question mark

• Moderated increase in inflation benefits the business in the short term

Macroeconomic Scenery

CIELO | INVESTMENT HIGHLIGHTS

Leader in a growing market

Strong balance sheet, high cash generation and low capex requirements

Minimum dividend pay out of 50% of net profit* distributed twice a year

Focus on innovation and continuous growth

* After constitution of legal reserve of 20% of the Company´s capital stock

24

CIELO | ADR

Cielo has a sponsored Level I ADR

Ticker: CIOXY

ADR Ratio (ADR:ORD): 1:1

Depositary bank: Deutsche Bank Trust Company Americas

Depositary bank contacts:

ADR broker helpline:

Tel: +1 212 250 9100 (New York)

Tel: +44 207 547 6500 (London)

Email: [email protected]

ADR website: www.adr.db.com

Depositary bank’s local custodian: Banco Bradesco

* Since December 2013 no IOF charged

25

APPENDIX

1995

4 Visa acquirers

2009 2010

June 2009

Single Visa Acquirer

R$ 8.4 billion IPO

+

Multi-brand acquirer

CIELO | TIMELINE

27

28.6%

28.6%

42.3%

0.4%

Banco Bradesco Banco do Brasil

Free-float Treasury

1,572,230,938 common shares

CIELO | CAPITAL OWNERSHIP

28

BRAZIL | ECONOMIC SCHEME

Gross MDR

Net MDR Interchange Fee

The brand defines

the interchange

fee. The acquirer negotiates

the gross MDR with the

merchant.

MERCHANTS

29

BRAZIL | MERCHANT DISCOUNT RATES

Source: Central Bank 30

2,90

2,91

2,93

2,95

2,92

2,97 2,98

2,99

2,96

2,98 2,99 2,98

2,95

2,96

2,94

2,84

2,80 2,80 2,79 2,79

2,76 2,77 2,78 2,78

2,75 2,77

2,75 2,75

MARKET CREDIT GROSS MDR EVOLUTION (%)

Credit

BRAZIL | MERCHANT DISCOUNT RATES

Source: Central Bank 31

1,58 1,57

1,58

1,59

1,59 1,58 1,58

1,60 1,60

1,57 1,57

1,61 1,61

1,59

1,57

1,56

1,57

1,55

1,57

1,59 1,59

1,56

1,58

1,59 1,59 1,59 1,59

1,58

MARKET DEBIT GROSS MDR (%)

Debit

45 -99 -207 12 102 1 22 34 17

-101 35 152 -47 -135 -34 -75 -43 -47

54 61 42 29 29 27 47 5 21

1 3 13 6 5 6 6 4 10

200

16.6%

2 (1.1%)

9 (4.4%)

82 (41.0%)

107 (53.4%)

3Q12

173

16.4%

2 (1.0%)

6 (4.0%)

68 (39.5%)

96 (55.5%)

2Q12

165

17.1%

2 (1.0%)

4 (3.4%)

64 (39.2%)

93 (56.5%)

2Q141

227

16.3%

3 (1.5%)

13

(6.0%)

84

(37.2%)

125

(55.3%)

1Q141

217

18.9%

3

(1.4%)

12

(5.7%)

82

(37.7%)

120 (55.2%)

4Q131

240

20.2%

3 (1.4%)

14 (5.7%)

92 (38.1%)

132 (54.8%)

3Q131

207

19.7%

3 (1.3%)

11 (5.2%)

4Q12 1

113 (54.6%)

2Q131

195

18.3%

2 (1.2%)

10 (5.0%)

76 (39.2%)

81 (38.9%)

1Q131

182

17.0%

2 (1.2%)

9 (4,7%)

74 (40.6%)

98 (53.6%) 106

(54.6%)

Vero

Santander

Rede

Cielo

1) Itaú reported Redecard e Hipercard results blended.

Source: Public information, released by the companies (Cielo, Rede/Itaú, Santander e Banrisul); Cielo Analysis

∆ share qoq

17.9%

10.4%

39.6%

40.5%

yoy [%]

BRAZIL | MARKET SHARE – TOP 4 ACQUIRER Captured volume [R$ Bi], market share [%], market share variation [bps]

32

BRAZIL | TRANSACTION FLOW

MERCHANTS CARD HOLDERS

ISSUER

CARD

HOLDERS MERCHANTS

ISSUER

Credit Transaction Cycle

(in # of average days)

33

One of the specific characteristics of the Brazilian market is the long period for credit

transaction settlement

Debit Transaction Cycle

(in # of average days)

It takes 30 days on average in a credit transaction until the merchant is paid

On debit, the settlement occurs one day after - the international standard

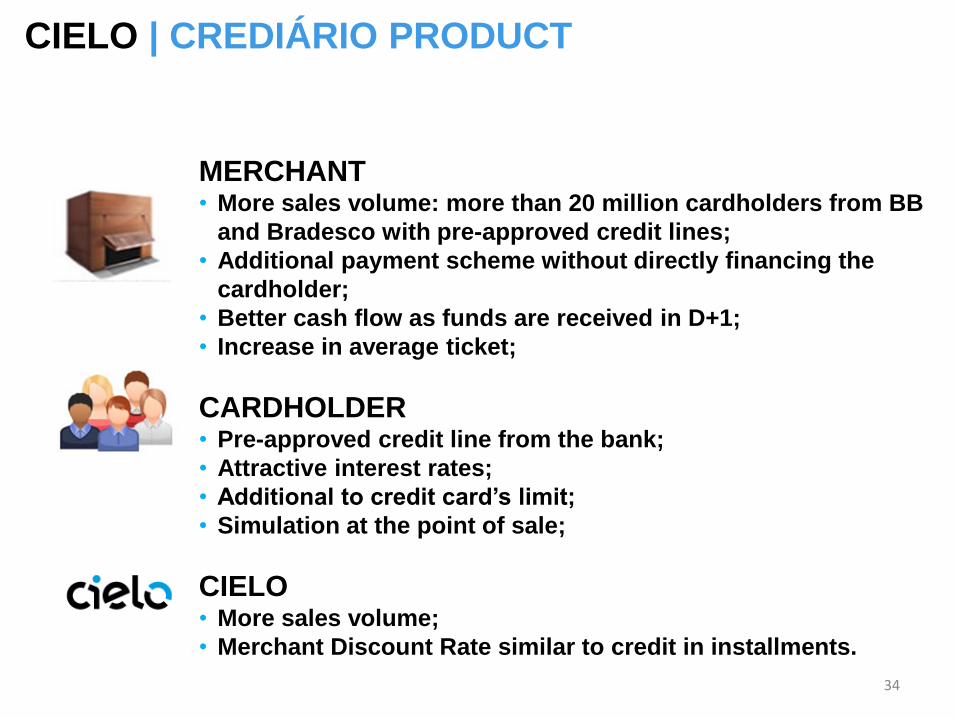

MERCHANT • More sales volume: more than 20 million cardholders from BB

and Bradesco with pre-approved credit lines;

• Additional payment scheme without directly financing the

cardholder;

• Better cash flow as funds are received in D+1;

• Increase in average ticket;

CARDHOLDER • Pre-approved credit line from the bank;

• Attractive interest rates;

• Additional to credit card’s limit;

• Simulation at the point of sale;

CIELO • More sales volume;

• Merchant Discount Rate similar to credit in installments.

CIELO | CREDIÁRIO PRODUCT

34

CIELO | MERCHANT e-SOLUTIONS ACQUISITION

MeS Highlights

• Proprietary, internet-based, next-

generation technology platform with

best-in-class scalability, analytical

capabilities, delivery speeds and cost of

services

• Leading e-Commerce payment

services provider with full range of

merchant acquiring, e-Commerce &

fraud management solutions

• In-house development of products and

services provides superior transaction

economics across the value chain

• Portable platform with upside for

expansion

• Good organic revenue growth, margins

and free cash flow

• Seasoned management team

Rationale

• Enhancement of Technology Platform

– Opportunity to leverage MeS’ technology

to the Brazilian market and Rest of World

– MeS platform designed to achieve

maximum scalability, efficiency and

reliability at a low cost

• E-Commerce Improvement

– E- Commerce is fastest growth merchant

category in payments

– MeS has expertise and proprietary

technology tailored to serving e-

commerce merchants

• Strong MeS Financial Performance

– Organic growth and attractive margins

Cielo acquired 100% of MeS for $670 million

35

CIELO | FACEBOOK PARTNERSHIP

• Partnership is the first step in the development of B2B2C

services with social engagement at the digital world. Innovative in

Brazil and worldwide, this service allows the connection of

shopping experience with the act of payment.

• This innovation allows the merchant to offer the check-in solution

to its customers and also the possibility to develop free

advertising to his own business. In addition, Cielo created two

new features to Facebook, focusing in the cardholders: the

possibility of recommending your favorite locals and also redeem

rewards. All that integrating the physical with the on-line world,

with Facebook, at the act of payment, through Cielo’s equipment.

36

CIELO | PLANET PAYMENT PARTNERSHIP

• An unprecedented initiative in Brazil, the partnership with Planet

Payment, a leader in processing international and multi-currency

payments, will allow Cielo to offer its clients “Pay in Your

Currency” and “Shop in Your Currency” solutions.

• These solutions offer high added-value to Cielo’s clients and

their consumers, especially foreign tourists who will visit Brazil

for the 2014 World Cup and 2016 Olympics. With the new tool,

foreign consumers can easily pay in their local currencies at the

point of sale via Cielo machines

37

CIELO | ORIZON AQUISITION

• Orizon was founded in 2006

• Cielo’s Ownership interest of 40.95%

• Interconnection between healthcare and dental operators and

services providers

38

CIELO | M4U AQUISITION

• M4U was founded in 2000

• Deal announced August 2010

• Total amount of R$ 50.1 million

• Innovation in the development of technological mobility platforms

• Largest mobile top up and mobile payment platforms in the Brazil

• Developed several applications under the most diverse cell phone

standards for a wide range of clients in the financial and telecom

markets

• Founders will continue to head the business 39

CIELO | eCommerce POSITION

Card

Slip

Acquirers

Wallets/ Subacquirers

Gateways

Banks

Debit

Source: Company, Broker reports, Cybersource 40

CIELO | BRASPAG AQUISITION

• Braspag was founded in 2005

• Deal announced May 2011

• Total amount of R$ 40 million

• Leader as a gateway for e-commerce in Brazil, with

approximately 65% market share

• Platform integrates online stores, financial institutions and

acquirers, and is responsible for capturing, routing and

managing payment transactions with cards, collection slips and

online debit

41

CIELO | STELO INICIATIVE

• MoU signed in April 16 with Cia. Brasileira de Soluções e Serviços

(“CBSS”) – controlled by Banco Bradesco S.A. and by Banco do

Brasil S.A. – to hold a stake in Stelo S.A.’s capital stock, a whole

subsidiary of CBSS operating as a facilitator for online payment and

digital wallet, for both the physical world and for eCommerce.

• Consolidation in eCommerce, adding Stelo facilitator to its available

portfolio to merchants and, via Stelo, Cielo will now participate in the

digital wallets business.

• The completion of the transaction is subject to execution of definitive

documents and approval of applicable regulatory authorities. 42

CIELO | DEBT EVOLUTION

43

2009 2010 2011 2012 2013

151

2.114

2.488

0,1 x

0,7 x

0.7 x

0

500

1.000

1.500

2.000

2.500

3.000

0,00

0,10

0,20

0,30

0,40

0,50

0,60

0,70

0,80

2009 2010 2011 2012 2013

Total Debt Evolution (R$ million)

Total Debt Total Debt/ EBITDA

(514) (251) (142)

1.710

2.065

(0,2) x

(0,1) x (0,1) x

0,5 x

0,5 x

-1.000

-500

0

500

1.000

1.500

2.000

2.500

-0,3

-0,2

-0,1

0,0

0,1

0,2

0,3

0,4

0,5

0,6

0,7

Net Debt Evolution (R$million)

Net Debt/Cash Net Debt/EBITDA

CIELO | DEBT AMORTIZATION SCHEDULE

44

R$423

R$3.575

2013Cash EBITDA

R$273 R$145

R$39

R$2.031

2014 2015 2016 2022

Interest and Principal

CIELO | CIEL3 OUTPERFORMING IBOV

45

Stock performance (IPO date* = 100)

*06/29/2009