20140610 Currence CPSP meeting - Ward Hagenaar

33

Ward Hagenaar Amsterdam Business Consultant & Partner Connective Payments 10 June 2014 The changing face of payments CPSP meeting iDEAL

-

Upload

ward-hagenaar -

Category

Documents

-

view

112 -

download

4

Transcript of 20140610 Currence CPSP meeting - Ward Hagenaar

Ward Hagenaar

Amsterdam

Business Consultant & Partner

Connective Payments

10 June 2014

The changing face of paymentsCPSP meeting iDEAL

|

Agenda

A changing market place

The evolution of the checkout proces

Impact on Payment Service Providers

10 June 2014The changing face of payments - Currence CPSP meeting 2

|

Agenda

A changing market place

The evolution of the checkout proces

Impact on Payment Service Providers

10 June 2014The changing face of payments - Currence CPSP meeting 3

|4

Omni channel retail: Technology is dramatically changing

the shopping process and experience

|

Major changes for retailers!

Customer behaviour is changing fast

The smartphone drives channel convergence

Consumers expect ease of use and personalisation

Card schemes finally focus on the consumer

eCommerce giantsconnect consumers on a major scale

Spending limit based on customer profile

10 June 2014The changing face of payments - Currence CPSP

meeting5

|

The changing role of identity

Customer experiencedefines design

Checkin is the new checkout

Amazon is ahead! Authentication is key

Everybody wants a piece of the identity-cake

Open ID schemes are the future

10 June 2014The changing face of payments - Currence CPSP

meeting6

|

Payments integrate in the buying process

Omnichannel retailing starts to happen

Apps enable convenient ordering, search,

loyalty and payment

“There is an app for that!”

iBeacon, Bluethooth Low Energy, GPS and

NFC

10 June 2014The changing face of payments - Currence CPSP meeting 7

|

Integration with delivery services

Commercial consolidation, DHL covers the full chain.

Local ordering and delivery

Google Wallet integratesshipping options (Express)

Cross channel delivery services

Amazon Fresh & Prime, ShopRunner, eBay Now

PostNL puts the consumerin the lead

10 June 2014The changing face of payments - Currence CPSP meeting 8

|

Companies move to Omni-channel to offer a

seamless shopping experience

9

Experience

Single touch point Channels act alone,

customer experience

differences

Channels strengthen each

other

Experience is aligned across

all channels

PropositionAligned Different assortment,

prices services

New services: C&C, in-

store home delivery, etc

Unified brand, high service,

extensive assortment

Focus - Learn Grow Make profitable

Organization

One organization Separate eCommerce

department

eCommerce department

becomes part organization

Integrated channel

management for

communication & commerce

Technology

One platform Systems are silo’s Logistics, assortment &

CRM (the basics) are

integrated

Shared platform all channels

from web, to mobile to cash

register

Single Channel Multi-Channel Cross-Channel Omni-Channel

The Past The Reality The AmbitionThe Work in Progress

10 June 2014The changing face of payments - Currence CPSP

meeting

|

The impact on banks

Individual banks lack the scale to compete internationally

on the issuing / consumer side. Rely on the brands for

products and services or create domestic winners.

Have not been succesfull in extending their acquiring

portfolio. But all are working on that.

Regulation SEPA, Basel3, PSD2, XS2A

Bitcoin, Ripple

Telco’s

10 June 2014The changing face of payments - Currence CPSP meeting 10

|

Financials:

• Big challenge to stay

visible and relevant for

the consumer

• International competition

• Mobile payments

• KYC

Retailer:• In search for new customers and

conversion increase

•Via mobile to omni-channel

•Customer experience is leading

•New technology available

Technology:

• Convergence of channels

• Many contenders to offer the

best checkouts

• ID is key

• Ordering, loyalty, delivery and

payment integrate

Consumer:

• Always online via any device

• Solutions needed for mobile

• Expects security and convenience

Seamless

payments

needed to

facilitate the

buying proces

Summary marketdrivers

|

Position

PSP’s need to be part of the omnichannel future or can stay pure player?

10 June 2014The changing face of payments - Currence CPSP meeting 12

|

Agenda

A changing market place

The revolution of the checkout proces

Impact on Payment Service Providers

10 June 2014The changing face of payments - Currence CPSP meeting 13

|

The best checkout experiences are exclusive for

top retailers

Otto Group – Yapital

PSP, Wallet, open invoice, P2P, etc!

BOL & wehkamp.nl

Major differentiator are the customer data

and profiles. Payment after delivery or

installments are USP’s.

Faster checkouts by retailers

Major retailers offer optimised checkout

experiences based on customer data and

established accounts.

10 June 2014The changing face of payments - Currence CPSP meeting 14

|

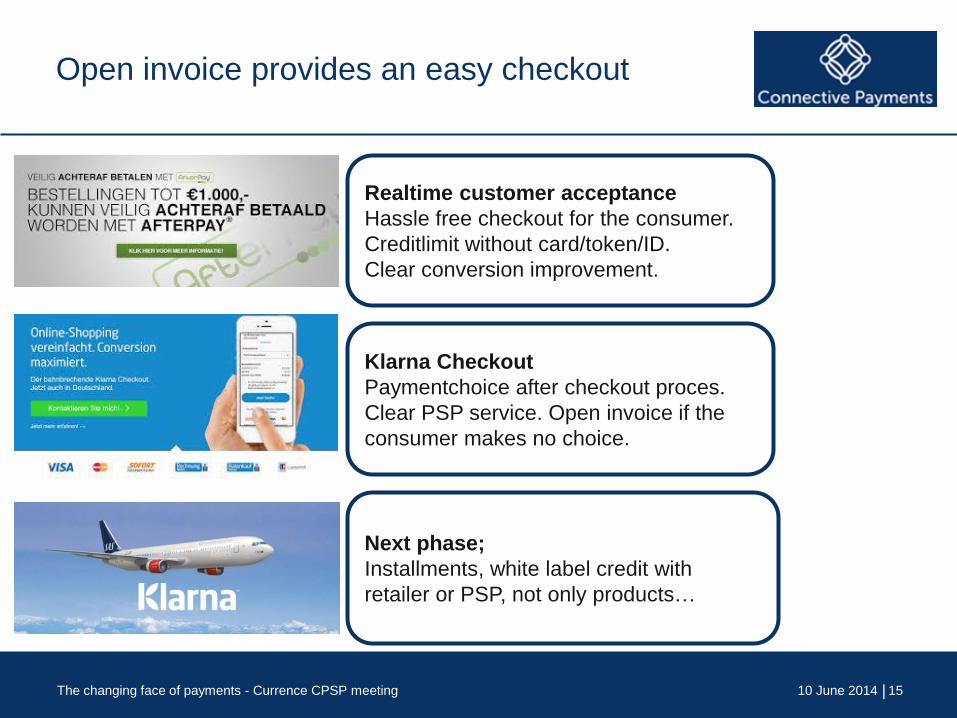

Open invoice provides an easy checkout

Realtime customer acceptance

Hassle free checkout for the consumer.

Creditlimit without card/token/ID.

Clear conversion improvement.

Klarna Checkout

Paymentchoice after checkout proces.

Clear PSP service. Open invoice if the

consumer makes no choice.

Next phase;

Installments, white label credit with

retailer or PSP, not only products…

10 June 2014The changing face of payments - Currence CPSP meeting 15

|

Part Payment sum - Increasing sales

Customer can choose number of months to

pay and see the partial amount

|

Evolution of the online checkoutproces

• Renovation of the classic checkout flow

• Central customer centric account;

- 1 ID

- up to date personal data

- adressbook

- payment preferences

- payment data

- loyalty & offers

• Less friction;

- overlay GUI

- strong reduction of steps

10 June 2014The changing face of payments - Currence CPSP meeting 17

|

Evolution of the checkoutproces for any shop

|

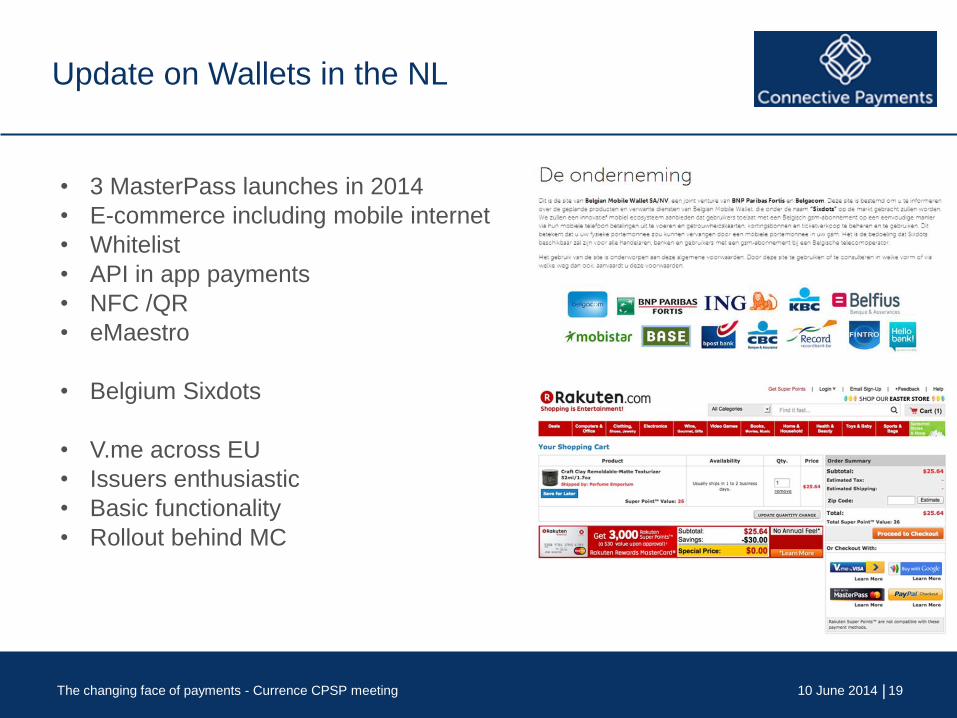

Update on Wallets in the NL

• 3 MasterPass launches in 2014

• E-commerce including mobile internet

• Whitelist

• API in app payments

• NFC /QR

• eMaestro

• Belgium Sixdots

• V.me across EU

• Issuers enthusiastic

• Basic functionality

• Rollout behind MC

10 June 2014The changing face of payments - Currence CPSP meeting 19

|

• Major importance for the card schemes

• Partnering banks but also Telefonica

and Samsung

• Investing in technology partners

• Leverage new processing platform

• $2 bln acquisition Cybersource

• $110 mln acquisition of Fundamo

specialist in mobile banking

• $190 mln acquisition of PlaySpan

• Investment in Monitise, Beyond

Analysis (data analytics) and Square

Visa V.me

|

Rabo MyOrder & Rabo Wallet Sidekick

21

Prepaid Wallet (MiniTix) withorder functionalty

Top up via PayPal/iDEAL

Remote LBS payments in physical stores from the app alsowith NFC/QR

Coupons, cashback, tickets, trx history, offers parking, barcode scannen, check in with GPS/NFC cash register interfacing

Closed system, 12.000 acceptance points

MyOrder

Rabo consumers

Current account connected via Maestro

No pincode under25 Euro

NFC in physicalstores only

International acceptance on allMaestro PayPass terminals

Rabo Wallet

10 June 2014The changing face of payments - Currence CPSP meeting

|

PayPal

• PayPal focus on mobile online and in store

• BLE and face recognition

• Integration with cash registers, magento

• API for mobile payments and apps

• Widget “integration” like Amazon login & pay

• Order function

• Check is the new checkout

https://www.youtube.com/watch?feature=player_embedded&v=Rww0ZcannKg

|

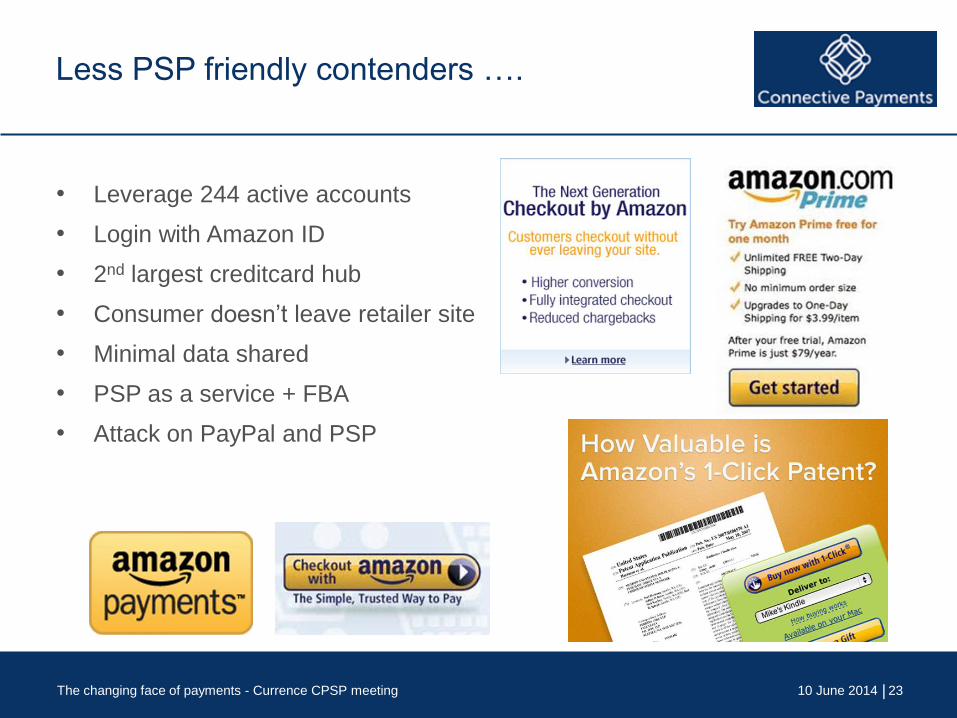

Less PSP friendly contenders ….

• Leverage 244 active accounts

• Login with Amazon ID

• 2nd largest creditcard hub

• Consumer doesn’t leave retailer site

• Minimal data shared

• PSP as a service + FBA

• Attack on PayPal and PSP

10 June 2014The changing face of payments - Currence CPSP meeting 23

|

Position

Are those contenders competitors to the PSP role?

10 June 2014The changing face of payments - Currence CPSP meeting 24

|

Agenda

A changing market place

Changing payments

Wallets

Impact on Payment Service Providers

10 June 2014The changing face of payments - Currence CPSP meeting 25

|

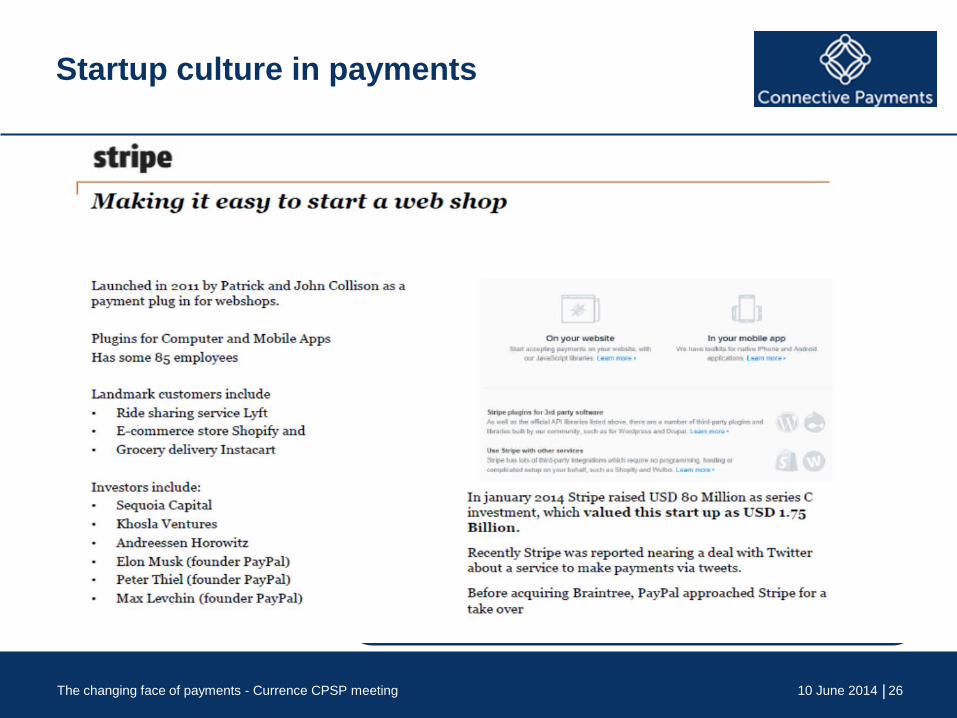

Startup culture in payments

Huge amount of capital invested in payment startups.

High valuations.

Many new use cases, data analytics, loyalty, gift cards,

point of sale interaction, lending, ordering, fast

transactions and security/authentication.

0% interchangefee?

10 June 2014The changing face of payments - Currence CPSP meeting 26

|

VS ecosystem

2710 June 2014The changing face of payments - Currence CPSP meeting

|

Value chain integration

Acquisition Braintree, DataCash,

CyberSource

Introduction

ShuttleAcquirer

Acquisition Biedmeer

Acquisition Ogone

New checkout solutions digital

Wallets including mobile

Mobile increasingly important in

purchasing proces

IPG connected to core FD platform

Global Collect Elevate data services

Introduction Omnikassa

Payment app SeQR

|

Impact for acquirers

10 June 2014The changing face of payments - Currence CPSP meeting 29

Retailer new expectations

• Omnichannel support

• Customer experience and support for technology

• Face fierce competition

Chain and platformintegration in acquiring

• Forwards; CCV buys BiedMeer next …

• Backwards; PayPal buys Braintree, MasterCard - DataCash,

• Horizontal; WorldPay & NETS by BAIN

• Bankacquirers prepare omnichannel propositions

• Loyalty, analytics, vouchers/deals & payment

Portfolio

• Pricepressure on single channel solutions

• Increasing importance VAS

• Integration capabilities and support for enabling technologies

|

Impact for PSP’s

Competition heats up

- Amazon, PayPal, Klarnaoffer PSP services

- (Bank) acquirers enter the market again as profits

decrease

- Lean PSP’s excel in modern integration

Value chain

- PSP’s become acquirer

- Some active in mPOS(EMV experience)

- Integration andacquisition with POS

terminal providers andcard brands

Omnichannel

- Retailer and consumerneeds change

- Payments integrate in orderingprocess

- Apps en Wallets integration

- New technology in retail, remote mobile payments

10 June 2014The changing face of payments - Currence CPSP meeting 30

|

SWOT PSP services

Strenghts

1. Customer focus

2. Ability to adapt and develop IT solutions

3. Capable full service providers

Threats

1.Klarna, Amazon, PayPal offer PSP

replacing services for SME

2.Position is hard to defend as no end

consumer ties (vs Klarna, Amazon, PayPal)

3.Price competition is growing as added

value is restricted

Weaknesses

1. Single channel focus

2. Focus on operations and daily business

3. Limited scale per player, interchangeable

services

Opportunities

1.Specialize or broaden up to be the (P)SP

for transaction authorisation, from loyalty, to

checkin

2.Develop true omnichannel payment

services – value is in the data not payment

3.Embrace all new (checkout) solutions and

offer new API’s to retailers and developpers

31

|

Position

Can you share other opportunities for the PSP?

10 June 2014The changing face of payments - Currence CPSP meeting 32

|

Position

Thank you for your attention. [email protected]

10 June 2014The changing face of payments - Currence CPSP meeting 33