201406 Pap

of 44

-

Upload

tbpthinktank -

Category

Documents

-

view

229 -

download

0

Transcript of 201406 Pap

-

8/13/2019 201406 Pap

1/44

Finance and Economics Discussion SeriesDivisions of Research & Statistics and Monetary Affairs

Federal Reserve Board, Washington, D.C.

Bank Lending Channels during the Great Recession

Samuel Haltenhof, Seung Jung Lee, and Viktors Stebunovs

2014-06

NOTE: Staff working papers in the Finance and Economics Discussion Series (FEDS) are preliminarymaterials circulated to stimulate discussion and critical comment. The analysis and conclusions set forthare those of the authors and do not indicate concurrence by other members of the research staff or theBoard of Governors. References in publications to the Finance and Economics Discussion Series (other thanacknowledgement) should be cleared with the author(s) to protect the tentative character of these papers.

-

8/13/2019 201406 Pap

2/44

Bank Lending Channels during the Great Recession

Samuel Haltenhof

University of Michigan

Seung Jung LeeViktors Stebunovs

Board of Governors of the Federal Reserve System

October 29, 2013

Abstract

We study the existence and economic signicance of bank lending channels that affectemployment in U.S. manufacturing industries. In particular, we address the questionof how a dramatic worsening of rm and consumer access to bank credit, such as theone observed over the Great Recession, translates into job losses in these industries. Toidentify these channels, we rely on differences in the degree of external nance depen-dence and of asset tangibility across manufacturing industries and in the sensitivity of these industries output to changes in the supply of consumer credit. We show thathousehold access to bank loans matters more for employment than rm access to localbank loans. Our results suggest that, over the recent nancial crisis, tightening ac-cess to commercial and industrial loans and consumer installment loans explains jointlyabout a quarter of the drop in employment in the manufacturing sector. In addition, a

decrease in the availability of home equity loans explains an extra one-tenth of the drop.

JEL Classification : G21, G28, G30, J20, L25Keywords : bank credit channels, bank lending standards, home equity extraction,credit crunch, employment, job losses, Great Recession.

The views expressed in this paper are solely the responsibility of the authors and should not be in-terpreted as reecting the views of the Board of Governors of the Federal Reserve System or the FederalReserve System. All errors and omissions are our own responsibility alone.

University of Michigan, Department of Economics; emal: [email protected] Board of Governors of the Federal Reserve System, 20th Street and Constitution Avenue, NW, Wash-

ington, DC 20551; email: [email protected] and [email protected] , respectively.

1

-

8/13/2019 201406 Pap

3/44

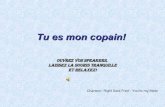

Figure 1: Four credit supply channels

Firm depends on external sources of funds

Firm produces durable goods

Bank

C&I loans

Tangible coll.

BankFundsFirm

Smallbusi-ness

owner

Home equity

HELOCs

Bank

Money

Firm House-hold

Home equity

Cons. loans

Durable goodsHELOCs

1 Introduction

We study the existence and economic signicance of several bank lending channels.In particular, we address the question of how a dramatic worsening of rm and consumeraccess to bank credit, such as the one observed during the Great Recession, translates into job losses in U.S. manufacturing industries. The focus of the paper is on the economicsignicance of bank lending channels, rather than credit channels more broadly, and thekey for identifying the economic effects of bank lending channels is that bank loans are not

perfectly substitutable with other types of external nance.To x the ideas further, Figure 1 shows four separate channels through which bank

credit might affect employment and industry dynamics in the manufacturing sector: (1)through the supply of commercial and industrial (C&I) loans directly to rms, (2) throughthe accessibility of home equity lines of credit (HELOCs) to small business owners to propup their businesses, (3) through the supply of consumer installment loans to households,and (4) through the accessibility of HELOCs to households for consumption purposes. Inthis paper, we examine these four channels using data for U.S. manufacturing industriesand large commercial banks over the 1991-2011 period.

There are three main reasons behind our choice of studying specically the linkagesbetween access to bank credit and U.S. manufacturing employment. First, by studying thereal effects of changes in the supply of bank credit, we account for the possible substitu-tion of funding sources at the rm and household levels. One might imagine that rmsand households will substitute away from more limited bank credit to more easily availablealternatives, perhaps mitigating the effect of a decline in supply of bank credit on manu-

1

-

8/13/2019 201406 Pap

4/44

facturing employment. Second, over the past few decades, manufacturing industries havehad relatively stable establishment structures and banks seem to have continued to supplya signicant share of their C&I loans to the manufacturing sector. In contrast, other in-dustries, such as retail trade, have experienced a shift over time toward multi-unit rms,often with access to national capital markets. Hence, this shift likely has weakened thesenon-manufacturing industries reliance on local bank credit. Third, manufacturing indus-tries outputin particular, durable goods outputis sensitive to changes in the supply of consumer credit. Indeed, most purchases of household durable goods, such as cars or largeappliances, tend to be nanced. This economic feature allows us to judge the importanceof consumer access to bank credit on employment in manufacturing.

Our explained variablestotal employment, number of establishments, and average es-tablishment sizeare from the Quarterly Census of Employment and Wages (QCEW). Toour knowledge, this is a novel application of the QCEW data. One of the advantages of this

data set is that it does not contain a structural break in the classication of industries dueto the transition from the Standard Industrial Classication (SIC) to the North AmericanIndustry Classication System (NAICS) in the late 1990s. Hence, the data set covers afew recessions, including the Great Recession, on a consistent basis. We focus on employ-ment in manufacturing rather than output because employment at the industry-state levelcan be more precisely measured. While the U.S. Census makes industry-state level outputdata available, the data are noisy by the Census own admission, and the data compilationapproaches alternate between census and non-census years.

Our explanatory variables come from a few sources. We associate changes in rm and

household access to bank credit with changes in commercial banks C&I lending standardsand in their willingness to originate consumer installment loans based on bank-specicresponses to questions in the Senior Loan Officer Opinion Survey on Bank Lending Practices(SLOOS). Indeed, the data on the net fraction of banks indicating a tightening of C&Ilending standards is highly negatively correlated with the growth in employment in themanufacturing sector, as shown in Figure 2. We also associate changes in household accessto home equity loans with growth in home equity. We use the state- and national-level houseprice indices compiled by CoreLogic, state- and national-level mortgage debt per borrowertaken from TransUnions Trend Data, and the national level household balance sheet datafrom the Federal Reserves statistical release Z.1 to construct proxies for growth in homeequity.

To better isolate the different bank lending channels, we minimize the risk that ourresults will be driven by either reverse causality or by omitted variables.

Our identication assumption takes advantage of the differences in national bank pres-ence across U.S. states and is somewhat similar to that is regularly used in the literature.

2

-

8/13/2019 201406 Pap

5/44

Figure 2: Changes in C&I lending standards and growth in employment in the U.S. man-ufacturing sector

-80

-60

-40

-20

0

20

40

60

80

1992 1994 1996 1998 2000 2002 2004 2006 2008 2010-15

-10

-5

0

5

10

15

Percent Percent

Changes in standards (left axis)Growth in employment (right axis)

E a s

i n g

T i g h t e n

i n g

*Net percentage of respondent banks reporting tightening of standards on C&I loans, weighted by total loans.Source: Federal Reserve Board, Senior Loan Officer Opinions Survey on Bank Lending Practices.

Note: Shaded areas are NBER-dened recessions.

We posit that changes in major banks C&I lending standards, apportioned to a particularstate, and households growth in home equity are exogenous to developments in a givenmanufacturing industry in a given state and at a given point in time. That is, in accor-dance with the questions in the SLOOS, we postulate that national banks tighten (or ease)C&I lending standards for small rms broadly across the country rather than targeting aparticular state or a particular industry in a given state. Variation in geographical presence

of banks and in their timing of tightening (or easing) generates variation of our C&I lendingstandards measure across states. Similarly, we postulate that changes in commercial bankswillingness to originate consumer installment loans is exogenous to developments in a givenmanufacturing industry in a given state and at a given point in time.

We control for omitted variable bias (1) by comparing manufacturing industries thatdo or do not depend on external sources of nance and do or do not have a high degreeof pledgeable tangible assets and (2) by comparing industries that produce durable vs.non-durable goods.

The rst comparison is an improvement on the setup that has been widely used in the

literature to tease out a differential impact of credit supply changes on industries dependenton external nance, for example, as in Cetorelli and Strahan (2006). Its novelty is thatwe take into account not only the need to borrow to nance physical capital investment(captured by the Rajan and Zingales (1998) measure of external nance dependence) butalso the ability to access C&I loans by manufacturing rms (captured by the tangibleasset measure as in Braun (2002) and Claessens and Laeven (2003)). We interact these

3

-

8/13/2019 201406 Pap

6/44

industry-specic indicators with measures of changes in state-level commercial banks C&Iloan lending standards to isolate the local bank lending channel to rms.

The second comparison is quite intuitive, too. 1 Consumption of durable goods is morelikely to be nanced rather than paid for outright, and hence changes in consumer accessto credit, though affecting both consumption of durable and non-durable goods, are morelikely to affect the consumption of the former. We recognize that the location of productionand the location of consumption of durable goods are usually not the same. After all, if households in one state have difficulties obtaining consumer installment or home equityloans, then the production of durable goods in other states should be affected. Hence,we interact national-level measures of household access to bank loans to identify the banklending channel to households.

Our results show that measures of changes in lending standards on C&I loans andchanges in willingness to originate consumer installment loans by major commercial banks,

and the availability of home equity lines of credit affect notably the manufacturing em-ployment over the sample period. 2 We show that household access to loans matters morefor employment than rm access to local loans and that access to bank credit affects em-ployment mostly through changes in the size of rms rather than through changes in theirnumbers.

The latter nding is consistent with a couple of literature strands. First, for largerrms, consistent with the exporter hysteresis international trade literature, it may bethat, following a tightening of access to credit, the sunk cost aspect of the rm entrydecision in the presence of xed per-period costs results in these rms continuing to serve

the market despite unfavorable economic or nancial conditions, but perhaps at a smallerscale requiring fewer employees. Second, at the other extreme, for smaller rms, consistentwith the literature on lending relationships, as in Berger and Udell (1994) and Petersen andRajan (1994), smaller (nascent) rms may depend less on bank loans than larger (older)ones, and, hence, their entry decisions might depend less on bank credit availability. Indeed,in our data, while the smallest establishments employ relatively a small fraction of employeesin aggregate, they are numerous and introduce some noise into the aggregate series for thenumber of establishments.

Our results highlight the adverse effects that tightening access to credit, especially forhouseholds, over the Great Recession and the subsequent slow recovery had on employmentin manufacturing industries. Structural break tests support the idea that a signicant por-

1 This breakdown of industries into industries producing durable vs. non-durable goods has been used inthe growth and nancial development literature.

2 Although we do not consider a short-term credit supply channel, which includes trade credit or short-term bank loans, we believe that disruptions in the supply of loans of these types over the Great Recessionalso possibly had a signicant impact on employment in manufacturing industries.

4

-

8/13/2019 201406 Pap

7/44

tion of such employment losses were the manifestation of an unusually large tightening of credit availability to the economy rather than a structural change in the bank lending chan-nels. Indeed, our model-based back-of-the-envelope calculations suggest that, between 2007and 2010, the tightening of lending standards and a decrease in willingness to orginate loanscaused a 4.4 percent decline in employment in the manufacturing sector. The explanatorypower of the effects of these bank lending channel based on our approach is notable, asthe actual drop in employment was 17 percent. Our exercise suggests that, over the recentnancial crisis, tightening access to C&I loans and and a decrease in willingness to originateconsumer installment loans explain jointly about a quarter of the drop in employment inthe manufacturing sector. Our further back-of-the envelope calculations suggest that, overthe same period, the decline in home equity loan accessibility explains an extra tenth of themanufacturing employment decline.

Our estimate of the impact of changes in C&I lending standards, changes in willing-

ness to originate consumer loans, and the growth in the availability of home equity on themanufacturing industries have implications for the recovery in the labor market going for-ward. To some extent, the tightening of lending standards and the decrease in willingnessto originate loans reect commercial banks efforts to deleverage. The greater anticipatedregulatory burden faced by commercial banks may have temporarily held back employ-ment growth in manufacturing, thus contributing to weak overall labor market conditions.Moreover, the sluggish housing market improvement may have been a further drag on man-ufacturing employment, for example, because of limited access to HELOCs. Although inthe longer term, the displaced manufacturing workers might be absorbed by other sectors

in the economy.When dealing with the unusually low levels of employment in manufacturing in an

environment like the Great Recession, the policy prescription that follows from our back-of-the-envelope exercise is that policymakers should pay attention to restoring the functioningof the bank credit supply channel to households relatively more than that to rms. Ourresults should not be taken though as advocating an implementation of Keynesian policiesin a recession. Note the focus of the paper is on employment losses in the manufacturingindustries attributable to cutbacks in credit supply. As long as the supply of credit isconstrained by bank-related factors, ceteris paribus , policymakers might be urged to step into restore credit ow, which implies a different policy response than simply trying to boostaggregate demand.

The outline of the paper is as follows. After a short literature review, the followingsection provides a description of our data sources and the ways we transformed the rawdata. The fourth section goes over our empirical strategy and econometric specication.The fth section presents the estimation results. We then detail the economic signicance

5

-

8/13/2019 201406 Pap

8/44

of the bank lending channels by estimating employment losses in manufacturing industriesattributable to tightening access to C&I loans or decreased willingness to originate consumerinstallment loans over the Great Recession. We end with some concluding remarks.

2 Literature

As mentioned earlier, our identication assumption takes advantage of the differencesin bank presence across U.S. states and is somewhat similar to that in Peek and Rosengren(2000), Garmaise and Moskowitz (2006), and Lee and Stebunovs (2012). For example,Peek and Rosengren (2000) use the Japanese banking crisis to test whether a loan supplyshock to branches and agencies of Japanese banks affected construction activity in the U.S.commercial real estate market. Similarly, Garmaise and Moskowitz (2006) study the effectsof changes in large bank mergers on changes in crime at the MSA level, arguing that such

merger activity instruments for changes in bank competition at the local level. Lee andStebunovs (2012) use a similar setup to study the effects of bank balance sheet pressuremanifested through state-level bank capital ratios on the employment and net rm dynamicsin different manufacturing industries within a given state.

Our paper also contributes to the nascent literature that tackle various bank lendingchannels and their real effects over the Great Recession. In this literature strand, usingemployee-specic data, Duygan-Bump, Levkov, and Montroiol-Garriga (2010) nd thatworkers in small rms are more likely to become unemployed during the 2007-2009 nancialcrisis if they work in industries with high external nancing needs. From a more interna-

tional perspective, Bijlsma, Dubovik, and Straathof (2010) nd evidence that the creditcrunch in 2008 and 2009 resulted in lower industrial growth in industries that are moredependent on external nance in the OECD countries. Bentolila, Jansen, Jimenez, andRuano (2013) provide evidence from Spain on how employment at rms funded by weakbanks fell considerably more than employment at rms funded by healthier banks. Finally,Fort, Haltiwanger, Jarmin, and Miranda (2013) suggest that the collapse in house pricesaccounts for a signicant part of the large decline in young/small businesses during theGreat Recession. However, because of their VAR approach, their nancing channel ad-mittedly reects both the associated credit demand and supply factors, whereas we attemptto identify the economic impact of disruptions in bank credit supply only.

3 Description of the data

In this section, we justify our focus on manufacturing industries and review our datasources and the ways we transformed the raw data. Our explained variables come from the

6

-

8/13/2019 201406 Pap

9/44

QCEW. We derive our explanatory variables from the SLOOS, TransUnions Trend Data,CoreLogics data, Federal Reserves statistical release Z.1, and other sources.

3.1 Focus on manufacturing industries at the state level

Our analysis focuses on manufacturing industries. These industries are often studied in thenance and banking literaturefor example, Cetorelli and Strahan (2006) and Kerr andNanda (2009). In contrast to some other industries that have experienced a shift over timetoward multi-unit rms, the manufacturing industries have had relatively stable structuresand many smaller manufacturing rms continue to rely on local bank loans. 3

3.2 The Quarterly Census of Employment and Wages

The QCEW program publishes quarterly employment and wages data reported by

employers accounting for 98 percent of U.S. jobs, available at the county, MSA, state,and national levels by industry. 4 The programs primary outlet is the tabulation of theemployment and wages of establishments that report to the Unemployment Insurance (UI)programs of the United States. Employment covered by these UI programs represents about99.7 percent of all wage and salary civilian employment in the country. Ultimately, theQCEW data have broad economic signicance for the evaluation of labor market trends andmajor industry developments, for time-series analyses, and for interindustry comparisons.

The QCEW data are collected on an establishment basis. An establishment is an eco-nomic unit, such as a farm, mine, factory, or store that produces goods or provides services.It is typically at a single physical location and engaged in one, or predominantly one, typeof economic activity for which a single industrial classication may be applied. Accord-ing the Bureau of Labor Statistics (BLS), most employers have only one establishment;thus, the establishment is the predominant reporting unit or statistical entity for reportingemployment data.

Admittedly, if someone is interested in the number of rms rather than the number of establishments in a given industry, then there might be some measurement error in our de-pendent variable induced by the fact that large rms often operate multiple establishments.Nevertheless, the number of establishments from the QCEW is highly correlated with theeconomic quantity, such as rms or net rm entry, that we are trying to observe, for atleast two reasons. First, the analysis of the U.S. Census Bureaus Longitudinal Business

3 For example, the retail trade sector has undergone a pronounced shift away from single-unit rms tonational chains with access to national capital markets. In fact, Jarmin, Klimek, and Miranda (2009) reportthat the share of U.S. retail activity accounted for by single-establishment rms fell from 60 percent in 1967to just 39 percent in 1997.

4 We draw on the Bureau of Labor Statistics materials to write parts of this section.

7

-

8/13/2019 201406 Pap

10/44

Database suggests that most U.S. rms have only one establishment. 5 For example, Davis,Haltiwanger, Jarmin, and Miranda (2006) report that on average, each publicly traded rmoperates about 90 establishments, while each privately held rm only 1.16 establishments.Note that in 1990, there were over 4.2 million privately held rms and less than 6 thousandpublicly traded rms. In 2000, there were about 4.7 milion privately hed rms and lessthan 7.4 thousand publicly traded rms. 6 Second, earlier researchby, for example Blackand Strahan (2002)has shown that the rate of the creation of new businesses is correlatedwith the share of new establishments in a local economy.

In accordance with BLS policy, data reported under a promise of condentiality are notpublished in an identiable way and are used only for specied statistical purposes. The BLSwithholds the publication of UI-covered employment and wage data for any industry levelwhen necessary to protect the identity of cooperating employers. Totals at the industry levelfor the states and the nation include the undisclosed data suppressed within the detailedtables.

Although the QCEW data provide a wealth of disaggregate information, we limit our-selves to studying total employment, the number of establishments, and the average estab-lishment size measured in employees over the 1991-2011 period at the state level. 7

3.3 External nance dependence for rms and households

We consider several channels through which bank credit affects manufacturing employ-ment: the supply of C&I loans directly to rms, the supply of home equity loans to smallbusiness owners to prop up their businesses, the supply of consumer installment loans tohouseholds, and the supply of home equity loans to households for consumption purposes.

To examine the bank lending channels to rms or small business owners, we follow theliterature in constructing a measure of dependence on external sources of nance. One mea-sure for external nance dependence based on Rajan and Zingales (1998) is calculated asthe fraction of total capital expenditure not nanced by internal cash ows from operationsand reects rms requirements for outside capital. 8 This measure is viewed as a techno-

5 The Longitudinal Business Database (LBD) covers all business establishments in the U.S. private non-farm economy that le payroll taxes with the IRS. As such, it covers all establishments in the U.S. nonfarmbusiness sector with at least one paid employee. In some industries, the share of multi-establishment rmsis higher than in others. For example, the retail trade sector has undergone a pronounced shift away from

single-unit rms to national chains.6 Similarly, Haltiwanger, Jarmin, and Miranda (2009) say that the LBD covers about 6 million rms and 7million establishments in a typical year that have at least one paid employee, which implies that, on average,each rm operates 1.17 establishments.

7 More precisely, average establishment size calculated as the average number of employees per establish-ment.

8 We calculate the Rajan-Zingales measures for each manufacturing industry at the three digit NAICSlevel for manufacturing industries using COMPUSTAT. This measure is dened as capital expenditures(CAPX) minus cash ows from operations divided by capital expenditures. Cash ows are calculated by

8

-

8/13/2019 201406 Pap

11/44

logically determined characteristic of a sector that is innate to the manufacturing processand exogenous from the perspective of an individual rm. Following Cetorelli and Strahan(2006), we calculate a Rajan-Zingales measure for each NAICS three-digit manufacturingindustry by summing both capital expenditures and cash ows over the sample period foreach U.S.-based rm that has been in existence in the COMPUSTAT database for morethan ten years and by taking the median value of rms in each manufacturing industry. Wethen categorize industries that lie above the median value of the Rajan-Zingales measuresas industries dependent on external nance ( EF = 1) and those that lie below as industriesnot dependent on external nance ( EF = 0).

Although rms dependence on bank loans may be somewhat limited in the U.S., thisdependence is larger for some rms (such as relatively small privately held rms) than forothers (such as large publicly traded rms). Moreover, as shown in Colla, Ippolito, andLi (2013), even larger rms may specialize in a certain debt type and may not be able to

substitute away from scarce bank loans quickly and, hence, may be forced to downsize orshut down. In other words, if small and large rms alike were able to substitute away fromscarce bank loans completely, we would not be able to identify the banking lending channelsusing our regression models.

Moreover, using a more specic measure capturing dependence on bank loans subjectsus to endogeneity concerns as low dependence may simply indicate nancing constraints.Likewise, Cetorelli and Strahan (2006) argue that the EF measures computed for onlymature rms provide a powerful instrument for small rms demand for bank credit, buta direct measure of bank credit dependence, for example, based on bank-loans-to-assets

ratios of small businesses from the 1998 Survey of Small Business Finance (SSBF) doesnot. 9

To sharpen our identication approach, we consider rms ability to pledge collateralin securing bank loans. As suggested by the Survey of Terms of Bank Lending (FRB: E.2Release), C&I loans tend to be secured by collateral, such as equipment and machinery. Toreect this particular feature of C&I loans, we consider asset tangibility by industry. Wereason that rms in manufacturing industries with a high share of tangible assets relativeto total book-value assets should have easier access to external nance. Following theguidelines in Braun (2002) and Claessens and Laeven (2003), we compute the tangibilityratios at the three-digit NAICS level using the data for large U.S.-based rms over thesample period. Again, we are not interested in the exact value of the asset tangibilitymetric for each industry as such; we sort industries into the industries with a low tangible

summing up the following items in Compustat: IBC, DPC, TXDC, ESUBC, SPPIV, and FOPO.9 Still, we re-estimate the benchmark model with control and treatment groups based on the 1998 SSBF

data on bank loans, with the estimation results shown in the second column in Table 10 in the Appendix.Not surprisingly, the results are somewhat different and are explained in our robustness checks.

9

-

8/13/2019 201406 Pap

12/44

asset share (indicating a low ability to pledge collateral for C&I loans, T A = 0) and a hightangible asset share (indicating a high ability to pledge collateral for C&I loans, T A = 1)based on the whether an asset tangibility ratio for a given industry is below or above themedian. 10

Finally, we can dene one of our treatment groups: these are the industries that aredependent on external sources of funding in the Rajan and Zingales (1998) sense and haveahigh ability to pledge collateral to secure access to C&I loans in the sense of Braun (2002)and Claessens and Laeven (2003). The rst indicator tells us the need to borrow in a givenindustry, and the second indicator, the ability to do so. In addition, we also consider theEF = 1 and T A = 1 treatment groups separately to stay consistent with the literature.

To examine the bank lending channel to households-consumers, we recognize that thedegree of consumer reliance on bank credit for consumption of non-durable goods is differentfrom that for consumption of durable goods. Consumption of durable goods is more likely to

be nanced with consumer installment or home equity loans (rather than paid for outrightor nanced directly in capital markets) than consumption of non-durable goods. Hence, toa large extent, the producers of durable goods are at the mercy of lenders to consumers. Wefollow the U.S. Census Bureaus breakdown of manufacturing industries into either durablegoods (DG = 1) or non-durable goods producers ( DG = 0).

Table 1 shows the breakdown of three-digit NAICS manufacturing industries into in-dustries dependent on external nance ( EF = 1), industries with high tangible asset shares(T A = 1), and industries producing durable goods ( DG = 1). Some industries do not haveany of these characteristics, yet others have one, two, or all three of these characteristics,

which helps with our identication.Having dened the control and treatment groups, we look into the growth in total

employment, the number of establishments, and the average establishment size in each of the groups. Figures 3 to 5 plot these measures for the entire economy. The gures suggestthat employment and average establishment size in the treatment group are more procyclicalthan that in the control group. However, for the number of establishments, the businesscycle pattern for the treatment group relative to the control group is less clear. 11

10 We calculate the asset tangibility measures based on all rms as used in the literature. Although theRajan-Zingales measure is sensitive to whether we use only mature rms or all rms, the tangibility measureis not, implying that nancially constrained rms may be more constrained in the total size of the balance

sheet, and not necessarily in the composition of their assets.11 We discuss later in the paper why this might be the case.

10

-

8/13/2019 201406 Pap

13/44

Table 1: Characteristics of manufacturing industries

NAICS Description EF T A DG Empl. Share Output Share(Percent) (Percent)

311 Food Manufacturing 1.2 2.8312 Beverage and Tobacco Product Manufacturing 0.0 0.0313 Textile Mills 0.2 0.2314 Textile Product Mills 0.0 0.0315 Apparel Manufacturing 0.2 0.1316 Leather and Allied Product Manufacturing 0.0 0.0321 Wood Product Manufacturing 0.4 0.4322 Paper Manufacturing 0.3 0.7323 Printing and Related Support Activities 0.4 0.4324 Petroleum and Coal Products Manufacturing 0.1 2.3325 Chemical Manufacturing 0.6 2.6326 Plastics and Rubber Products Manufacturing 0.5 0.8327 Nonmetallic Mineral Product Manufacturing 0.4 0.5331 Primary Metal Manufacturing 0.3 1.0332 Fabricated Metal Product Manufactur ing 1.1 1.3333 Machinery Manufacturing 0.8 1.3

334 Computer and Electronic Product Manufacturing 0.9 1.6335 Electrical Equipment, Appliance, and Component 0.3 0.5336 Transportation Equipment Manufacturing 1.2 2.9337 Furniture and Related Product Manufacturing 0.4 0.3339 Miscellaneous Manufacturing 0.5 0.6

31-33 Total Manufacturing 9.7 20.3

Note: Employment and output shares are relative to the entire economy as of 2007.

3.4 Denitions of loan types and the Senior Loan Officer Opinion Survey

3.4.1 Denitions of loan types

To identify different bank lending channels, we focus on three types of loans: C&Iloans, consumer installment loans, and HELOCs.

C&I loans include loans for commercial and industrial purposes to sole proprietorships,partnerships, corporations, and other business enterprises, whether secured or unsecured,single payment, or installment. C&I loans exclude the following: loans secured by realestate; loans to nancial institutions; loans to nance agricultural production and otherloans to farmers; loans to individuals for household, family, and other personal expenditures;and other miscellaneous loan categories. Typically, the interest rate for C&I loans is set asa spread over the prime rate or Libor and adjusts with movement in the benchmark rateover the loan term.

Consumer installment loans are loans to individualsfor household, family, and otherpersonal expendituresthat are not secured by real estate, such as auto loans. Typically,the interest rate for new consumer installment loans is set as a spread over the prime rateor Libor and remains xed over the full loan term.

In recent years, the popularity of HELOCsrevolving, open-ended lines of credit se-cured by residential propertieshas overshadowed the use of non-collateralized consumer

11

-

8/13/2019 201406 Pap

14/44

-

8/13/2019 201406 Pap

15/44

Figure 4: Growth in the number of establishments in manufacturing industries in the U.S.

1992 1994 1996 1998 2000 2002 2004 2006 2008 2010-10

-8

-6

-4

-2

0

2

4

6

8

10Percent

EFxTA=0, DG=0EFxTA=1DG=1

Source: QCEW

Note: EF T A = 0 are manufacturing industries that either do not dependent on external sources of funding or do not have the ability

to pledge collateral to secure access to C&I loans. DG = 0 are manufacturing industries that produce nondurable goods. EF T A 10

are manufacturing industries that depend on external sources of funding and have the ability to pledge collateral to secure access to

C&I loans. DG = 1 are manufacturing industries that produce durable goods. Shaded areas are NBER-dened recessions.

the largest banks in each Federal Reserve district and is roughly nationally representative.The surveyed banks are all considered large in the sense that no bank has assets of lessthan $3 billion in the survey. The top 5 banks (by total assets) had deposit-taking branchesin more than 20 states in the beginning of our sample period and have had branches in all29 states in our sample since 2004. On average, only 7 banks have bank branches in onlyone state in our survey per year.

Banks are asked to report whether they have changed their credit standards over thepast three months on six categories of core loans including C&I loans. Data measuringchanges in credit standards on C&I loans are available beginning with the May 1990 survey.Questions regarding changes in standards on credit card loans and other consumer loanswere added to the survey in February 1996 and May 1996, respectively. However, a seriesindicating changes in banks willingness to originate consumer loans is available over theentire sample period.

The SLOOS surveys follow a somewhat irregular schedule. The SLOOS asks banks toreport changes in their lending practices over the previous three months, and the survey is

13

-

8/13/2019 201406 Pap

16/44

Figure 5: Growth in the average size of establishments in manufacturing industries in theU.S.

1992 1994 1996 1998 2000 2002 2004 2006 2008 2010-15

-10

-5

0

5

10

15Percent

EFxTA=0, DG=0EFxTA=1DG=1

Source: QCEW

Note: EF T A = 0 are manufacturing industries that either do not dependent on external sources of funding or do not have the ability

to pledge collateral to secure access to C&I loans. DG = 0 are manufacturing industries that produce nondurable goods. EF T A 10

are manufacturing industries that depend on external sources of funding and have the ability to pledge collateral to secure access to

C&I loans. DG = 1 are manufacturing industries that produce durable goods. Shaded areas are NBER-dened recessions.

conducted so that it coincides with regular meetings of the Federal Open Market Committee.Hence, the January SLOOS refers to the period from October to December of the prior year.

To make individual bank responses operational, we transform them into an aggregatemeasure in two steps.

First, we map individual bank responses into indicator variables. The question aboutchanges in C&I lending standards reads, Over the past three months, how have your bankscredit standards for approving applications for C&I loans or credit linesother than thoseto be used to nance mergers and acquisitionsto large and middle-market rms and tosmall rms changed?Banks respond to that question using a categorical scale from 1 to 5:1 = eased considerably, 2 = eased somewhat, 3 = remained about unchanged, 4 = tightenedsomewhat, and 5 = tightened considerably. We use the answers based on banks responseswith respect to small rms because the QCEW data is predominantly composed of smallbusinesses and we attempt to capture the local bank lending channel to rms. 13 Although

13 However, changes in C&I lending standards for large and middle-market rms is highly correlated tothose for small rms.

14

-

8/13/2019 201406 Pap

17/44

-

8/13/2019 201406 Pap

18/44

measure is in fact representative for a given state.Questions regarding changes in standards on credit card loans and other consumer loans

were added to the SLOOS only in 1996. However, we associate these changes with thechanges in banks willingness to originate consumer installment loans, which are availableover the entire sample period. The question about changes in consumer installment loansreads, Please indicate your banks willingness to make consumer installment loans now asopposed to three months ago. By analogy with the C&I index, we construct a nationalcomposite index of changes in willingness to make consumer installment loans, W t , weightedby total consumer loans (excluding residential real-estate loans). We consider W t as a proxyfor changes in the tightness of lending standards for consumer loans.

Figure 6 shows our measure of the changes in the net fraction of banks reporting atightening of C&I lending standards for three states: New York, Texas, and California. Itshows a drastic tightening of C&I lending standards around the past three recessions as

well as a notable loosening of the standards in the mid-2000s. Across the 29 states in oursample, the variation is particularly high around the recessions, which provides us withadequate cross-sectional variation for our identication.

Figure 7 plots our national measure of the net share of banks reporting an increasedwillingess to originate consumer installment loans. Notice that credit cycles vary by loancategory in terms of timing and magnitude, which can be quite different from the macroe-conomic business cycle. According to the Federal Reserve H.8 statistical release, C&I loansoutstanding at commercial banks stopped contracting in the fourth quarter of 2004, whereasconsumer loans were minimally affected by the 2001 recession. In terms of the credit mar-

kets, if the consumer loan market was relatively more impaired than the C&I loan marketin the 2007 recession, it was the opposite for the 2001 recession; hence, it took the C&I loanmarket longer to recover after the 2001 recession.

3.5 State and national variables

We use the real GDP series from the Bureau of Economic Analysis and the state; thenational level house price indices compiled by CoreLogic; and mortgages, HELOCs, homeequity loans secured by junior liens, and net worth from the Federal Reserves statisticalrelease Z.1. We also use state-level mortgage debt per borrower from TransUnions Trend

Data. 17 There is notable heterogeneity across states in the timing and magnitudes of houseprices changes. Some areas experienced strong decreases in home values over the recentcrisis, while other areas avoided the housing boom and experienced no signicant house

Massachusetts, Michigan, Minnesota, Missouri, Nevada, New York, North Carolina, Ohio, Oregon, Pennsyl-vania, Rhode Island, South Carolina, South Dakota, Tennessee, Texas, Virginia, and Washington.

17 Trend Data is an aggregated consumer credit database that offers quarterly snapshots of randomlysampled consumers.

16

-

8/13/2019 201406 Pap

19/44

Figure 6: Net fraction of banks reporting a tightening of C&I Lending Standards for smallrms

1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011-80

-60

-40

-20

0

20

40

60

80Percent

New YorkTexasCalifornia

Source: Federal Reserve Board, Senior Loan Officer Opinions Survey on Bank Lending Practices.

E a s

i n g

T i g h t e n

i n g

Note: Shaded areas are NBER-dened recessions.

price depreciation.We use a measure of growth in unemcumbered home equity as a proxy for changes in

lending standards for HELOCs. Indeed, though we only have data going back to 2007, thecorrelation between the home equity growth we estimate on a national level and an aggregatemeasure of tightening of credit standards for HELOCs constructed based on the SLOOS is-0.90 on an annual basis and -0.77 on a quarterly basis, implying that unemcumbered homeequity growth is a good indicator for changes in credit standards as well.

We construct our measure of growth in home equity at the state or national level asfollows. We start with the premise of Avery, Brevoort, and Samolyk (2011) that the differ-ence between house prices and outstanding mortgage debt should approximate home equity.Since we cast our regression models in growth rates, we construct a proxy for the growthrate of the equity ratio (the inverse of the loan-to-value ratio):

HE s,t = HP s,t MD s,t ,

where HE s,t is the growth rate of home equity in state s at time t , HP s,t is the growthrate of the house price (value) index in state s at time t, and MD s,t is the growth rate of

17

-

8/13/2019 201406 Pap

20/44

Figure 7: Net fraction of banks reporting an increase in their willingness to originate con-sumer installment loans

1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011-80

-60

-40

-20

0

20

40

60

80Percent

U.S.

Source: Federal Reserve Board, Senior Loan Officer Opinions Survey on Bank Lending Practices.

L e s s

W i l l i n g

M o r e

W i l l i n g

Note: Shaded areas are NBER-dened recessions.

mortgage debt in state s at time t .18 This admittedly might be a noisy proxy for growth in

the equity ratio, but we believe it is the best available state-level measure. At the nationallevel, there is an alternative reported in the Z.1 statistical release, which we denote as HE t .19

To make sure that growth in home equity is indeed an indicator of home equity loansavailability, rather than a proxy for household wealth-driven demand, we include into ourregression models growth in aggregate household net worth ( NW t ), constructed using theFederal Reserve statistical release Z.1.

18 Dene the equity ratio as HE s,t = H P s,t /MD s,t and, after taking logs and differentiating, obtain theexpression in the text.

19 Comparing the national measure of the home equity growth rate computed from TransUnion withthe national official level reported in the Z.1 Federal Reserve statistical release, we nd a correlation of 0.74. Therefore, we are comfortable using the state-level measure as an adequate proxy for growth in homeequity. CoreLogic produces another variable of interestthe share of negative home equity measures at thestate level; however, the reporting began only in 2009.

18

-

8/13/2019 201406 Pap

21/44

4 Variation, identication, and the empirical model

We choose our unit of observation to be a NAICS three-digit manufacturing industryin a given state and a given year. To ensure even more robust identication, we could haveworked with county- or MSA-level data, but, at such a low level of aggregation, there wouldhave been too many missing observations due to condentiality and non-disclosure issues.In contrast, the QCEW industry data at the state level are available over a long period andinclude the undisclosed data suppressed within the detailed disaggregated tables. Hence,working with state-level data appears to strike a balance between exogeneity concerns anddata availability. Although the QCEW is a quarterly frequency data set, we choose to workwith annual averages for a few reasons. We are interested neither in immediate responsesof employment to changes in access in credit, which later might be reversed, nor in theseasonality of manufacturing employment. 20

We examine how credit supply conditions for both rms and households affect manu-facturing industry dynamics. To isolate these effects and control for omitted variable bias,we exploit the variation in rm external nance dependence and asset tangibility across themanufacturing industries and the variation in consumer loan dependence across non-durableand durable goods manufacturing industries. Specically, we examine whether changes inC&I lending standards, the ability for home equity extraction by small business owners,banks willingness to originate consumer installment loans, and the ability for home equityextraction by households for consumption purposes matter for employment in manufactur-ing industries.

Given a high degree of persistence in the number of manufacturing establishments andtheir average size and other variables over the sample period, as well as the nature of ourmeasure of changes in C&I lending standards and the willingness to originate consumerinstallment loans, we work with an empirical model cast in growth rates; this model isstationary and allows us to control for aggregate trends in levels and growth rates (becauseof included xed effects). Growth rates of the explained variables are not persistent, withautoregressive coefficients below 0.20; so, to avoid potential endogeneity, we omit laggeddependent variables from our regression models.

Our identication assumption is that changes in major banks lending standards, appor-tioned to a particular state, and growth in home equity are exogenous to developments in agiven manufacturing industry in a given state and at a given point in time. In accordancewith the questions in the SLOOS survey, we postulate that banks tighten C&I lending stan-dards broadly across the country rather than targeting a particular state and/or a particularindustry. Variation in the geographical presence of banks and in the timing of tightening

20 In a quarterly model, a set of lagged explanatory variables would weaken identication because of collinearity.

19

-

8/13/2019 201406 Pap

22/44

generates variation in the changes our measure of changes in C&I lending standards acrossstates. 21

Besides omitted variables, we control for aggregate credit, state, and national economicconditions. Aggregate credit conditions are proxied by the change in the realized real interestrate. As a proxy for national economic conditions, we include the growth rate of U.S. realGDP. To address the potential endogeneity of industry location choices and industry-state-specic trends, we include industry-state xed effects in the benchmark model. To checkthe robustness of our results, we estimate additional models with various error clusteringassumptions.

Putting all the pieces together, we estimate the following specication:

Y i,s,t = T EF i T A i T s,t + H EF i HE s,t

factors for supply of credit to rms+ W DG i W t + H DG i HE t factors for supply of credit to households

+ N DG i NW t + S SC s,t + N NC t + i,s + i,s,t ,

where

Y i,s,t is the growth rate of employment (or the growth rate of the number of establish-ments or the growth rate of the average establishment size) in industry i and state sat time t;

T is the coefficient of the interaction term between the indicator for external nancedependence of industry i, EF i , asset tangibility, T Ai , and the net percentage of bankstightening standards for C&I loans in state s at time t, T s,t ;

H is the coefficient of the interaction term between the indicator for the externalnance dependence of industry i , EF i , and the growth rate of house equity in state sat time t, HE s,t ;

W is the coefficient of the interaction term between the indicator for durable goodsindustry i, DG i , and the net percentage of banks reporting increased willingness tomake consumer installment loans, W t ;

H is the coefficient of the interaction term between the indicator for durable goodsindustry i, DG i , and the growth rate of aggregate home equity at time t, HE t ;

21 Moreover, the SLOOS data suggest that C&I lending standards tightening for large and small rms ishighly correlated, and so many banks change their standards on C&I loans in general rather than targetinga subset of borrowers.

20

-

8/13/2019 201406 Pap

23/44

N is the coefficient of the interaction term between the indicator for durable goodsindustry i, DG i , and the growth rate of aggregate household net worth at time t, NW t ;22

S and N are the coefficients of the state and national economic conditions variables,captured by SC s,t and N C s,t , respectively, which include T s,t , W t , HE t , NW t , U.S.real GDP growth, and the rst difference of the Libor-based realized real interest rate;

i,s is the coefficient for the industry-state xed effect, which should take into accountany trends in the level of employment in the manufacturing sector by industry andstate; 23

and nally i,s,t is the error term robust to heteroskedasticity.

We compute errors clustered separately in several ways: clustering by industry state ,clustering by year , and double clustering by industry state and year . The multiple clus-tered errors are calculated using the Cameron, Gelbach, and Miller (2011) code.

4.1 Sample selection and representativeness

Our restricted sample for 29 states appears to be representative of the population of manufacturing industries in the entire country. We checked the data breakdown by employ-ment, number of establishments, and average establishment size for two years, 2007 and2010. The population measures are shown in Table 2. In percentage terms, the breakdownof employment and number of establishments in our sample is very similar to that in thepopulation, and the average establishment size in the sample is nearly identical to that inthe population. 24

5 Results

5.1 Four bank lending channels

First, we see if each credit channel exists separately from the others in Table 3. Weexploit the variation in rm external nance dependence across all manufacturing industries

(to identify the effects of the supply of credit to rms) and the sensitivity of the manufac-turing industries output to changes in consumer credit (to identify the effect of the supply

22 Unfortunately, we do not have an acceptable estimate for state-level net worth. However, because wedo not nd statistically signicant effects from the home equity channel from the business side, we believethat this is less critical to have in our regressions.

23 The industry-state xed effects should also control for self-selected locations across the states.24 We also check whether balancing the panel introduces any selection biases by estimating the regression

model on an unbalanced panel. The results are largely unaffected.

21

-

8/13/2019 201406 Pap

24/44

Table 2: Breakdown of employment in manufacturing industrie

Employment in manufacturing in 2007EF T A = 0 EF T A = 1 Row tota l

DG = 0 3,514,947 1,537,086 5,052,033DG = 1 7,311,679 1,469,312 8,780,991

Column total 10,826,626 3,006,398 13,833,024

Employment in manufacturing in 2010EF T A = 0 EF T A = 1 Row tota l

DG = 0 3,193,000 1,254,642 4,447,642DG = 1 5,971,005 1,068,850 7,039,855

Column total 9,164,005 2,323,492 11,487,497

Percentage change in employment in manufacturing (2007-10)EF T A = 0 EF T A = 1 Row tota l

DG = 0 -9.2 -18.4 -12.0DG = 1 -18.3 -27.3 -19.8

Column total -15.4 -22.7 -17.0

Note: EF T A = 0 are manufacturing industries that either do not dependent on external sources of funding or do not have the ability

to pledge collateral to secure access to C&I loans. DG = 0 are manufacturing industries that produce nondurable goods. EF T A 10

are manufacturing industries that depend on external sources of funding and have the ability to pledge collateral to secure access to

C&I loans. DG = 1 are manufacturing industries that produce durable goods. Shaded areas are NBER-dened recessions.

of credit to households). Specically, we nd that employment in industries dependent onexternal nance and with high asset tangibility is affected by the net share of commercialbanks reporting changes in C&I loan lending standards, in the rst column. In the secondcolumn, we also nd that the availability for home equity extraction by households-businessowners also matters for those industries dependent on external nance. In addition, em-ployment in durable goods manufacturing industries falls with a decline in the net shareof banks reporting a decreased willingness to originate consumer installment loans, in thethird column. Finally, in the fourth column, the availability of home equity for extractionhas a positive effect on employment in durable goods industries as well, even controllingfor the growth in household net worth. All coefficients are statistically signicant at the 1percent level.

Next, we present our empirical results with all of the four bank credit channels com-bined in Tables 4 to 6. We are also interested in examining whether credit supply conditionsaffect employment in manufacturing on the extensive or intensive margin. Hence, we es-timate two additional sets of models: one for the number of establishments and anotherfor the average establishment size. Given that the growth rate of employment is just asum of the growth rates of the number of establishments and the average establishmentsize, the regression coefficients in the employment regression are nearly exact sums of thecorresponding coefficients in Tables 5 and 6.

Table 4 shows regression results for the models for total employment in manufacturingindustries. While all the three models in the table have common industry-state xed effects,

22

-

8/13/2019 201406 Pap

25/44

Table 3: Separate lending channel regression results for employment

(1) (2) (3) (4)EF T A T s 0.040

( 5.232)EF HE s 0.068

(2 .115)

DG W 0.059(7 .739)

DG HE 0.098(3 .122)

DG NW 0.071(3 .479)

T s 0.028 0.042 0.043 0.042( 4.304) ( 7.506) ( 7.622) ( 7.557)

HE s 0.010 0.024 0.010 0.010(0 .546) ( 0.924) (0 .580) (0 .570)

W 0.040 0.041 0.012 0.041(7 .402) (7 .423) (1 .929) (7 .435)

HE 0.004 0.004 0.004 0.043(0 .229) (0 .239) (0 .242) ( 1.590)

NW 0.023 0.023 0.023 0.057( 2.206) ( 2.190) ( 2.208) ( 3.369)

Real GDP 0 .938 0.939 0.937 0.939(13 .385) (13 .439) (13 .432) (13 .466)

Real interest rate 0.091 0.092 0.092 0.092( 2.311) ( 2.325) ( 2.318) ( 2.320)

Num. of observations 9500 9500 9500 9500Num. of clusters 500 500 500 500R-sq. overall 0 .14 0.14 0.15 0.14Fixed effects I S I S I S I S Error clustering I S I S I S I S

Note: EF denotes a dummy for industries dependent on external nance, T A a dummy for industries with relatively high asset

tangibility, and DG a dummy for industries producing durable goods. T s is the net fraction of banks reporting a tightening of C&I

lending standards for small rms at the state level. HE s is growth in home equity at the state level. W is the net fraction of banks

reporting an increase in willingness to originate consumer installment loans at the national level. HE is growth in home equity at

the national level. NW is the growth of net worth at the national level. Standard errors are clustered by I S ( industry state ).

Coefficients are reported with * if signicant at the 10% level, ** at the 5% level, and *** at the 1% level. t-statistics are reported

below the coefficients.

each model has a different specication of error clustering: in the rst column, errors areclustered by industry-state; in the second, by year; and, in the third, double-clustered byindustry-state and year.

With respect to the credit supply to rms, the results show that a percentage pointincrease in the net share of banks reporting a tightening of C&I lending standards reduces

23

-

8/13/2019 201406 Pap

26/44

the growth rate in employment in manufacturing industries with a high share of tangibleassets and which are dependent on external nance by 0.04 percentage point. Note thatthis regression coefficient is statistically signicant at conventional levels in the regressionwith double-clustered errors. The economic signicance of this and other coefficients will beexplored later in a separate section. The regression coefficient capturing the impact of theability for home equity extraction to nance rms dependent on external nance is positive,but no longer robustly statistically signicant. As for the credit supply to households,the results show that a percentage point increase in the net share of banks reporting anincreased willingness to originate consumer installment loans increases the growth rate of employment in the manufacturing industries producing durable goods by 0.07 percentagepoint. In addition, a 1 percentage point increase in the growth in home equitya measureof potential home equity extraction by householdsboosts the growth rate in employmentin the manufacturing industries producing durable goods by 0.15 percentage point.

Table 5 shows regression results for the models for the number of establishments. Forcredit supply to rms, the results show that our measure for tightening credit standardsdoes not appear to have a statistically signicant effect for two out of the three modelspecications. As for credit supply to households, the results also show that an increase inthe net share of banks reporting an increased willingness to originate consumer installmentloans increases the growth rate of the number of establishments in industries producingdurable goods in a statistically signicant manner for only one out of the three specications.The ability for home equity extraction appears to have no statistically signicant effect oneither the growth rate of establishments in industries dependent on external nance or that

in industries which produce durable goods all three specications.The lack of statistically robust evidence that the supply of bank credit to rms has

little effect on the number of establishments appears to be consistent with a few literaturestrands. First, for the the larger and more mature rms, consistent with the exporterhysterisis international trade literature, it may be that, following a tightening of access tocredit, the sunk cost aspect of the rm entry decision in the presence of xed per-period costsresults in these rm continuing to serve the market despite unfavorable economic or nancialconditions, but perhaps at a smaller scale requiring fewer employees, as noted in Alessandriaand Choi (2007) and other works. Second, at the other extreme, for smaller rms, consistentwith the literature on lending relationships as in Berger and Udell (1994) and Petersen andRajan (1994), nascent rms may depend less on bank loans than older rms. In addition,setting up a rm may not be that costly. For example, according to Djankov, Porta, Lopez-De-Silanes, and Shleifer (2002), entrepreneurs average cost of starting a rm (including thetime to start up a rm) was 1.7 percent of per-capita income in the United States in 1999,or $520. Likewise, layoffs by rms that are induced by stricter lending standards may spur

24

-

8/13/2019 201406 Pap

27/44

-

8/13/2019 201406 Pap

28/44

Table 5: Number of establishments regression results

(1) (2) (3)

EF T A T s 0.010

0.010 0.010( 1.716) ( 0.900) ( 0.757)

EF HE s 0.021 0.021 0.019( 1.001) ( 0.507) ( 0.437)

DG W 0.012 0.012 0.012(2 .364) (1 .587) (1 .310)

DG HE 0.027 0 .027 0.027(0 .895) (0 .640) (0 .516)

DG NW 0.002 0 .002 0.002(0 .129) (0 .084) (0 .069)

T s 0.007 0 .007 0.007(1 .328) (0 .503) (0 .432)

HE s 0.030 0.030 0.028(2 .145) (0 .985) (0 .800)

W 0.021 0.021 0.021(4 .131) (1 .584) (1 .387)

HE 0.069 0.069 0.068( 2.751) ( 1.335) ( 1.128)

NW 0.005 0 .005 0.005(0 .358) (0 .092) (0 .081)

Real GDP 0 .202 0.202 0.203(4 .433) (0 .912) (0 .819)

Real interest rate 0 .045 0 .045 0.044(1 .500) (0 .284) (0 .251)

Num. of observations 9500 9500 9500Num. of clusters 500 19 500 19R-sq. overall 0 .02 0.02 0.02Fixed effects I S I S I S Error clustering I S Y I S Y

Note: EF denotes a dummy for industries dependent on external nance, T A a dummy for industries with relatively high asset

tangibility, and DG a dummy for industries producing durable goods. T s is the net fraction of banks reporting a tightening of C&I

lending standards for small rms at the state level. HE s is growth in home equity at the state level. W is the net fraction of banks

reporting an increase in willingness to originate consumer installment loans at the national level. HE is growth in home equity at

the national level. NW is the growth of net worth at the national level. Standard errors are clustered by I S ( industry state )

in column (1), by Y (year ) in column (2), and double-clustered by I S Y ( industry state and year ) in column (3). Coefficients

are reported with * if signicant at the 10% level, ** at the 5% level, and *** at the 1% level. t-statistics are reported below the

coefficients.

Indeed, in our data, while the smallest establishments employ relatively a small fractionof employees in aggregate, they are numerous and introduce some noise into the aggregatenumber of establishment series.

26

-

8/13/2019 201406 Pap

29/44

Although conducting our analysis separately for small and larger rms would be idealto analyze this further, our data do not have this categorization at the industry-state levelthat we require to ensure the exogeneity setup. However, we can infer from a separatedata set, the Census Bureaus County Business Patterns (CBP) data, that, indeed, for theentire country, changes in the number of establishments in the smallest establishment sizeclasses introduce noise to the aggregate number of establishments. 25 However, because theyaccount in aggregate for a small fraction of the employment, changes in employment at theseestablishments have little impact in the aggregate. Breaking down these establishmentsby industry types reveals, at times, perverse behavior of metrics for the treatment groupindustries relative to the control groups, introducing further noise into the estimation.

Table 6 shows regression results for the models for the average establishment size. Forcredit supply to rms, the results show that a percentage point increase in the net fraction of banks reporting a tightening of credit standards reduces the growth rate of the average size

of the establishments with a high share of tangible assets and dependent on external nanceby 0.03 percentage point. The results also show that an improvement in access to HELOCsfor rms does not have a statistically robust impact on the average establishment size fortwo of the three specications. As for credit supply to households, the results show thata percentage point increase in the net share of banks reporting an increased willingness tooriginate consumer installment loans increases the growth rate of the average establishmentsize in industries producing durable goods by 0.06 percentage point. In addition, a 1percentage point increase in home equitya measure of potential home equity extractionby householdsboosts the growth rate of the average size by 0.14 percentage point.

5.2 Breakdown of the EF T A channel for employment

In this section, we check whether dependence on external nance or pledgable assetavailability matters equally for employment in manufacturing industries. To accomplishthis, we estimate separately the impact of access to external funding on EF = 1 andT A = 1 industries. As Table 7 shows, it is the former that is statistically signicant.

However, we still believe it is correct to study the intersection of EF = 1 and T A = 1industries for at least two reasons. First, the C&I loan denition and other survey resultssuggest the importance of pledgable assets for rms access to bank credit. Indeed, it

might be the case that the literature denes pledgable assets too narrowly. For example,accounts receivable may serve as collateral for C&I loans as well. Second, the consideration

25 The reason we do not use the CBP data for our analysis is that the CBP time coverage is too shortand the industry-state-size-class coverage is not comprehensive for our purposes. The CBP data have somebreaks in industry classication, making it impossible to merge the data into a long sample. In addition, forsome industries in some states, coverage is quite limited due to condentiality concerns. Finally, the CBPdata are compiled as of the rst quarter for each year, rather than on a year-average basis.

27

-

8/13/2019 201406 Pap

30/44

Table 6: Average size of establishments regression results

(1) (2) (3)

EF T A T s 0.034

0.034

0.034

( 4.934) ( 1.980) ( 1.789)

EF HE s 0.063 0.063 0.064(2 .033) (1 .710) (1 .392)

DG W 0.055 0.055 0.055(7 .867) (2 .482) (2 .260)

DG HE 0.141 0.141 0.141(3 .475) (2 .445) (2 .024)

DG NW 0.041 0.041 0.041(1 .829) (0 .680) (0 .618)

T s 0.035 0.035 0.035( 5.235) ( 2.331) ( 2.103)

HE s 0.042 0.042 0.043( 1.655) ( 1.669) ( 1.250)

W 0.012 0.012 0.012( 1.748) ( 0.630) ( 0.550)

HE 0.013 0.013 0.013( 0.389) ( 0.222) ( 0.183)

NW 0.051 0.051 0.051( 2.766) ( 1.406) ( 1.249)

Real GDP 0 .758 0.758 0.759(11 .246) (3 .230) (2 .908)

Real interest rate 0.157 0.157 0.158( 3.663) ( 1.301) ( 1.180)

Num. of observations 9500 9500 9500Num. of clusters 500 19 500 19R-sq. overall 0 .10 0.10 0.10Fixed effects I S I S I S Error clustering I S Y I S Y

Note: EF denotes a dummy for industries dependent on external nance, T A a dummy for industries with relatively high asset

tangibility, and DG a dummy for industries producing durable goods. T s is the net fraction of banks reporting a tightening of C&I

lending standards for small rms at the state level. HE s is growth in home equity at the state level. W is the net fraction of banks

reporting an increase in willingness to originate consumer installment loans at the national level. HE is growth in home equity at

the national level. NW is the growth of net worth at the national level. Standard errors are clustered by I S ( industry state )

in column (1), by Y (year ) in column (2), and double-clustered by I S Y ( industry state and year ) in column (3). Coefficients

are reported with * if signicant at the 10% level, ** at the 5% level, and *** at the 1% level. t-statistics are reported below the

coefficients.

of EF = 1 and T A = 1 industries jointly, as a comparison of Tables 4 and 7 reveals,strengthens the impact of the effects of tightening of C&I lending standards on employmentin manufacturing industries. More specically, the coefficient on the triple-interacted term

28

-

8/13/2019 201406 Pap

31/44

Table 7: Separation of EF and T A channels for employment

(1) (2) (3)

EF T s 0.025

0.025

0.025

( 3.200) ( 2.975) ( 2.257)

T A T s 0.004 0.004 0.004( 0.507) ( 0.271) ( 0.230)

EF HE s 0.045 0 .045 0.046(1 .423) (2 .081) (1 .273)

DG W 0.064 0.064 0.064(7 .970) (2 .548) (2 .317)

DG HE 0.155 0.155 0.155(4 .867) (2 .636) (2 .289)

DG NW 0.044 0.044 0.044(2 .209) (0 .885) (0 .792)

T s 0.028 0.028 0.028( 3.520) ( 1.321) ( 1.165)

HE s 0.011 0.011 0.014( 0.448) ( 0.328) ( 0.304)

W 0.010 0 .010 0.010(1 .490) (0 .401) (0 .355)

HE 0.071 0.071 0.071( 2.561) ( 0.922) ( 0.788)

NW 0.045 0.045 0.045( 2.621) ( 0.702) ( 0.609)

Real GDP 0 .936 0.936 0.938

(13 .430) (3 .289) (2 .915)

Real interest rate 0.092 0.092 0.092( 2.310) ( 0.456) ( 0.402)

Num. of observations 9500 9500 9500Num. of clusters 500 19 500 19R-sq. overall 0 .15 0.15 0.15Fixed effects I S I S I S Error clustering I S Y I S Y

Note: EF denotes a dummy for industries dependent on external nance, T A a dummy for industries with relatively high asset

tangibility, and DG a dummy for industries producing durable goods. T s is the net fraction of banks reporting a tightening of C&I

lending standards for small rms at the state level. HE s is growth in home equity at the state level. W is the net fraction of banks

reporting an increase in willingness to originate consumer installment loans at the national level. HE is growth in home equity at

the national level. NW is the growth of net worth at the national level. Standard errors are clustered by I S ( industry state )

in column (1), by Y (year ) in column (2), and double-clustered by I S Y ( industry state and year ) in column (3). Coefficients

are reported with * if signicant at the 10% level, ** at the 5% level, and *** at the 1% level. t-statistics are reported below the

coefficients.

we use in our baseline specication is almost as twice as large as the coefficient on thechanges in C&I credit standards interacted with EF only.

29

-

8/13/2019 201406 Pap

32/44

5.3 Structural breaks in the bank lending channels for employment

In this section, we check whether our results are driven by the developments over theGreat Recession and the subsequent recovery. To do so, we estimate a regression model

that allows a change in the coefficients on the measures of access to rm-oriented nance(the change in C&I lending standards and the state-level home equity growth measure)and to consumption-oriented nance (the change in the willingness to originate consumerinstallment loans and the country-level home equity growth measure). The estimationresults shown in Table 8 on the various interactions with the Crisis indicator, denoting theperiod from 2007 to 2011, suggest no statistically robust evidence of structural breaks inthese channels. That said, there is some indication that the change in home equity extractionability for rm funding may have become more important and changes in willingness tooriginate consumer installment loans and home equity extraction ability for durable goodsconsumption may have become less important over the crisis.

6 Economic signicance and the real macro effects of bank

lending channels

6.1 The real effects of bank lending channels during the Great Recession

With the estimates of the marginal effects in hand, we now perform back-of-the-envelope calculations of the effects of bank lending channels on employment during theGreat Recession based on the estimated differential effects. In our calculations, we assume

that the effect of tightening of C&I lending standards or a decline in the willingness to origi-nate consumer loans does not affect the manufacturing industries in the control groupthatis, the non-durables industries with a low degree of external nance dependence and assettangibility. 26

The economic signicance of our results can be quantied by looking at the combinedmarginal effect of a tightening in C&I lending standards and a decrease in the willingnessto originate consumer installment loans over the Great Recession and the subsequent slowrecovery. The marginal effect of a 1 percentage point increase (decrease) in the net fractionof banks reporting a tightening in C&I lending standards or a decrease in the willingness

to originate consumer installment loans are directly inferred from Table 4. We base thesecalculatesion from the changes in the net share of banks reporting a change in C&I lendingstandards and a willingness to originate consumer installment loans, which are inferred fromFigures 6 and 7. These gures suggest that about 33 percent of banks tightened C&I lending

26 This approach provides a conservative estimate of the impact of credit-supply disruptions on employmentin the manufacturing industries.

30

-

8/13/2019 201406 Pap

33/44

Table 8: Structural breaks in bank lending channels for employment

(1) (2) (3)

EF T A T s 0 . 039 0 . 039 0 . 039

( 4.614) ( 3

.046) ( 2

.616)

EF HE s 0 . 005 0 . 005 0 . 003( 0 . 149) ( 0 . 094) ( 0 . 040)

EF T A T s Crisis 0 . 004 0 . 004 0 . 004( 0 . 344) ( 0 . 178) ( 0 . 149)

EF HE s Crisis 0. 098 0 . 098 0 . 097(2 . 013) (1 . 185) (0 . 956)

DG W 0. 112 0 . 112 0 . 112

(9 . 682) (2 . 307) (2 . 093)

DG HE 0. 207 0 . 207 # 0 . 206 #

(5 . 719) (1 . 725) (1 . 533)

DG NW 0. 057 0 . 057 0 . 057(2 . 548) (0 . 708) (0 . 640)

DG W Crisis 0 . 069 0 . 069 0 . 069( 4 . 982) ( 1 . 120) ( 1 . 008)

DG HE Crisis 0 . 115 0 . 115 0 . 114( 3 . 057) ( 0 . 719) ( 0 . 652)

DG NW Crisis 0 . 025 0 . 025 0 . 025( 1 . 021) ( 0 . 210) ( 0 . 189)

T s 0 . 028 0 . 028 0 . 028( 3 . 989) ( 1 . 808) ( 1 . 552)

HE s 0. 001 0 . 001 0 . 001(0 . 052) (0 . 039) ( 0 . 024)

W 0. 008 0 . 008 0 . 008(1 . 165) (0 . 334) (0 . 300)

HE 0 . 083 0 . 083 0 . 082( 2 . 904) ( 1 . 038) ( 0 . 868)

NW 0 . 048 0 . 048 0 . 048( 2 . 813) ( 0 . 789) ( 0 . 685)

Real GDP 0 . 928 0 . 928 0 . 930

(11 . 678) (3 . 404) (3 . 017)

Real interest rate 0 . 127 0 . 127 0 . 128( 2 . 576) ( 0 . 651) ( 0 . 574)

Num. of observations 9500 9500 9500Num. of clusters 500 19 500 x 19R-sq. overall 0 . 16 0 . 16 0 . 16Fixed effects I S I S I SError clustering I S Y I S Y

Note: EF denotes a dummy for industries dependent on external nance, T A a dummy for industries with relatively high asset

tangibility, and DG a dummy for industries producing durable goods. T s is the net fraction of banks reporting a tightening of C&I

lending standards for small rms at the state level. HE s is growth in home equity at the state level. W is the net fraction of banks

reporting an increase in willingness to originate consumer installment loans at the national level. HE is growth in home equity at

the national level. NW is the growth of net worth at the national level. Crisis is a dummy variable indicating the period from the

beginning of the most recent recession to the subsequent recovery from 2007 to 2011. Standard errors are clustered by I S ( industry

state ) in column (1), by Y (year ) in column (2), and double-clustered by I S Y ( industry state and year ) in column (3).

Coefficients are reported with * if signicant at the 10% level, ** at the 5% level, *** at the 1% level, and # at the under 12% level.

t-statistics are reported below the coefficients.

31

-

8/13/2019 201406 Pap

34/44

Table 9: Back-of-the envelope macro effects in growth rates

Predicted percentage changes in employment in manufacturing (2007-10)EF T A = 0 EF T A = 1 Row total

DG = 0 0.0 -4.2 -1.3DG = 1 -5.4 -9.6 -6.1

Column total -3.7 -6.9 -4.4

Predicted changes in employment in manufacturing (2007-10)EF T A = 0 EF T A = 1 Row total

DG = 0 0 -64,773 -64,773DG = 1 -395,708 -141,436 -537,144

Column total -395,708 -206,209 -601,917

Goodness of t (predicted percentage change/actual percentage change)EF T A = 0 EF T A = 1 Row total

DG = 0 0.0 22.9 10.7DG = 1 29.5 35.3 30.9

Column total 23.8 30.2 25.7

standards on net per year, and that about 27 percent of banks decreased their willingness tooriginate consumer installment loans on net per year from 2007 to 2010. Bassett, Chosak,Driscoll, and Zakrajsek (forthcoming) and Lown and Morgan (2006) also use similar logic intheir VAR framework in describing changes in credit standards and how they affect lendingand output. 27

For the entire U.S. manufacturing sector (rather than the sample used in estimation),the pre- and post-crisis breakdown in employment are shown in Table 2. Over the GreatRecession total employment in the manufacturing sector declined, with the treatment groups

experiencing notably larger declines than the control group ( EF

T A = 0 or DG = 0). Andamong the treatment groups, the manufacturing industries depending on external nance,with high asset tangibility, and producing durable goods were affected the most.