2014 Oklahoma Corporation Income Tax Forms and …€¢ Includes Form 512, Form 512-TI and Form...

20

• Includes Form 512, Form 512-TI and Form 512-TI-SUP 2014 Oklahoma Corporation Income Tax Forms and Instructions This packet contains: • Instructions for completing the Form 512 • 512 corporation income tax form • Form 512-TI Computation of Oklahoma Consolidated Taxable Income • Form 512-TI-SUP Supplemental schedule for Form 512-TI Filing date: • Your Oklahoma return is generally due the 15th day of the third month following the close of the taxable year. For assistance or forms: • See page 13 for methods of contacting the Oklahoma Tax Commission. • 2-D Fill-in Forms with Online Calculations • Download Forms 24/7 • View FAQs or Email the OTC a Question • Latest Tax News www.tax.ok.gov One Site with Many Oklahoma Filing Options www.tax.ok.gov

Transcript of 2014 Oklahoma Corporation Income Tax Forms and …€¢ Includes Form 512, Form 512-TI and Form...

• Includes Form 512,Form 512-TI andForm 512-TI-SUP

2014 Oklahoma Corporation

Income Tax Forms and Instructions

This packet contains: • Instructionsforcompletingthe

Form512 • 512corporationincometaxform • Form512-TIComputationof

OklahomaConsolidatedTaxableIncome

• Form512-TI-SUPSupplementalscheduleforForm512-TI

Filing date: •YourOklahomareturnisgenerally

duethe15thdayofthethirdmonthfollowingthecloseofthetaxableyear.

For assistance or forms: •Seepage13formethodsof

contactingtheOklahomaTaxCommission.

•2-D Fill-in Forms with

Online Calculations•

Download Forms 24/7•

View FAQs or Email the OTC a Question

•Latest Tax News

www.tax.ok.govOne Site with Many

Oklahoma Filing Options

www.tax.ok.gov

What’s New in the 2014 Oklahoma Packet?

AnycorporationdoingbusinesswithinorderivingincomefromsourceswithinOklahomaisrequiredtofileanOkla-homaCorporationIncomeTaxReturn,whetherornotataxisdue.NOTE:SmallBusinessCorporations(SubchapterS)mustuseForm512-S.

Time and Place for Filing...Thereturnmustbefiledonorbeforethe15thdayofthethirdmonthfollowingthecloseofthetaxableyear.Inthecaseofcompleteliquidationorthedissolutionofacor-poration,thereturnshallbemadeonorbeforethe15thdayofthefourthmonthfollowingthemonthinwhichthecorporationiscompletelyliquidated.WhenthelastdateforfilinganydocumentorperforminganyactrequiredbytheOklahomaTaxCommission(OTC)fallsonadaywhentheofficesarenotopenforbusiness,thefilingofthedocu-mentorperformanceoftheactshallbeconsideredtimelyifitisperformedbytheendofthenextbusinessday.AvalidextensionoftimeinwhichtofileyourfederalreturnautomaticallyextendstheduedateofyourOklahomare-turnifnoOklahomaliabilityisowed.AcopyofthefederalextensionmustbeenclosedwithyourOklahomareturn.Ifyourfederalreturnisnotextended,oranOklahomali-abilityisowed,anextensionoftimetofileyourOklahomareturnmaybegrantedonForm504.TheForm504mustbefiledonorbeforetheduedateofthereturn.Toavoiddelinquentpenaltyforlatepayment,90%ofthetaxliabilitymustbepaidwiththeextension.Toavoiddelinquentinter-estforlatepayment,100%ofthetaxliabilitymustbepaidwiththeextension.Paperreturnswithouta2-DbarcodeshouldbemailedtotheOklahomaTaxCommission,POBox26800,OklahomaCity,OK73126-0800.Paperreturnswitha2-DbarcodeshouldbemailedtotheOklahomaTaxCommission,POBox269045,OklahomaCity,OK73126-9045.Formoreinformationonthe2-Dbarcode,seepage11.

General Filing Information

GeneralFilingInformation.................................. 2-4EstimatedIncomeTaxInformation........................ 3AmendedReturns.................................................. 3LinebyLineInstructions................................... 4-11GeneralInstructionsforDeterminingOklahomaTaxableIncome................................. 4-5ScheduleAInstructions...................................... 6-7ScheduleBInstructions...................................... 7-8PageOneofForm512Instructions.................. 8-11DirectDepositInformation................................... 12WhenYouAreFinished....................................... 12HowtoContacttheOTC..................................... 13OkTAPInformation.............................................. 13

Table of Contents

2

•WhencomputingOklahoma’sadditionaldepletion,onlymajoroilcompaniesarelimitedto50%ofthenetincomeperwell.SeetheinstructionsonForm512,page2.•IncomefromdischargeofindebtednesswhichwasaddedbacktocomputeyourOklahomataxableincomeintaxyear2010maybepartiallydeductible.SeetheinstructionsforScheduleA,lines12-26onpage7orScheduleB,line3onpage7forinformation.

Who Must File... Fiscal Year and Short Period Returns...Forallfiscalyearandshortperiodreturns,thebeginningandendingdatesofthetaxyearmustbeshownonthetopportionofthereturnwhereindicated.Omissionofthisinformationmaycauseasignificantdelayintheprocess-ingofthereturnandnointerestwillaccrueonanyrefundpending.

Common Errors

Belowarethemostcommonerrors.Toaidinprocessingyourreturn,pleasedoublecheckyourreturncarefully.

•Refundsmustbemadebydirectdeposit.Failuretosupplydirectdepositinformationwilldelaytheprocessingoftherefund.

•CheckyourFEINonallformsandschedules.

•Fiscalyeardatesareacommonproblem.Ifyoufilebasedonafiscalyear,pleaselistdatesontopofformwhereindicated.

•Encloseacompletecopyofyourfederalreturn,andallrequiredschedules.Failuretodosocanslowdowntheprocessingofyourreturn.

•TheCoalCreditandtheCreditforElectricityGeneratedbyZero-EmissionFacilitiesmayberefundable.Seetheinstructionsforline8onpage9andForms577and578.

Common AbbreviationsFound in this Packet

IRC - InternalRevenueCodeOS - OklahomaStatutesOTC - OklahomaTaxCommissionSec. - Section(s)

Don’t forget to sign and make a copy of your return before mailing!

General Filing Information

3

Consolidated Returns...Ifafederalconsolidatedreturnisfiled,anOklahomaconsolidatedreturnmayberequiredorpermittedundercertaincircumstances.

Anelectiontofileaseparateorconsolidatedreturnismadewiththetimelyfilingofthereturn.IfanaffiliatedgroupofcorporationselectstofileaconsolidatedOkla-homaincometaxreturn,suchelectionshallbebinding.TheaffiliatedgroupofcorporationsshallberequiredtofileaconsolidatedOklahomaincometaxreturnforallfuturetaxyearsunlesstheOTCreleasestheaffiliatedgroupofcorporationsfromsuchelection.

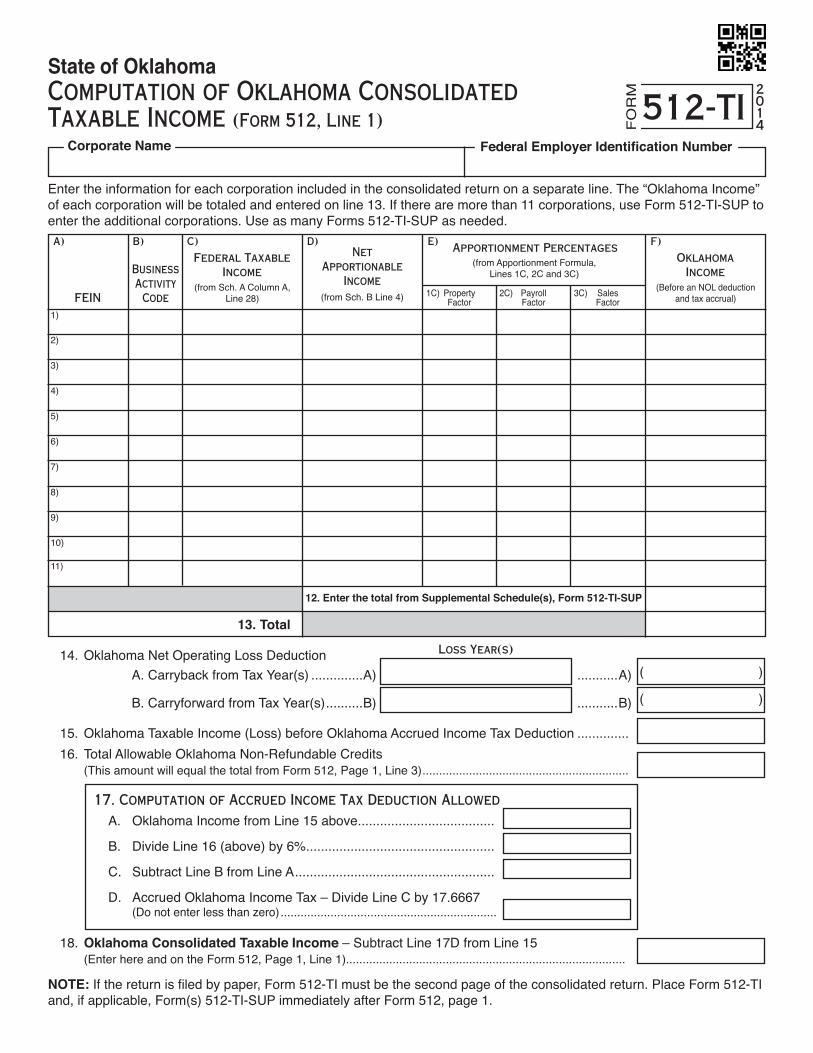

InfilingaConsolidatedIncomeTaxReturnforOklahoma,theOklahomataxableincomeforeachcorporationiscomputedseparatelyonitsownfactorsandthencombinedforonetotalincomeuponwhichthetaxiscomputed.Complete Form 512-TI “Computation of Oklahoma Consolidated Taxable Income” to determine the combined taxable income to report on page 1, line 1 of Form 512. Submit a separate Schedule A and Schedule B, if applicable, for each company within the consolidation.Iffilingbypaper,theForm512-TImustbethesecondpage.

Encloseacopyofthefederalconsolidatedreturnwithanincomestatement,balancesheet,M-1,M-2,M-3andsupportingschedulesforeachmemberoftheconsolidatedgroup.68OklahomaStatutes(OS)Sec.2367.

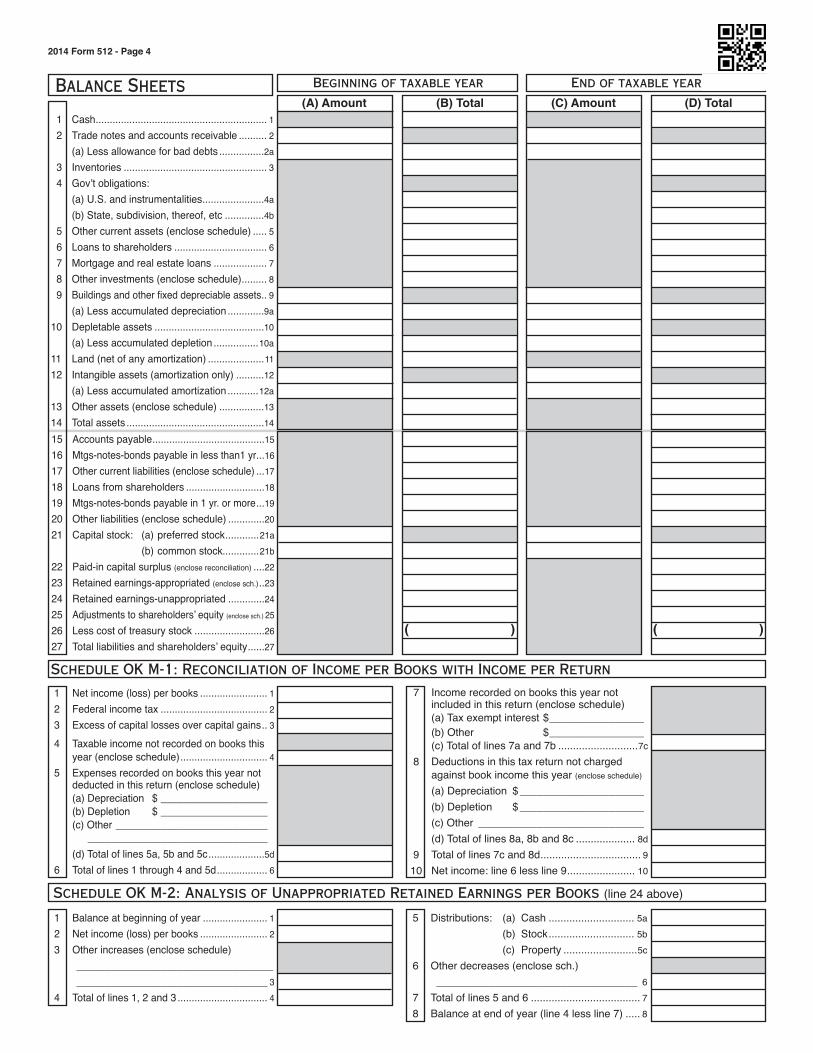

Special Instructions Regarding Form 512, Page 4...CompletePage4orattachacopyoftheFederalForm1120SchedulesL,M-1andM-2.CorporationsthatarenotrequiredtocompleteFederalForm1120SchedulesL,M-1andM-2arestillrequiredtocompletetheOklahomaForm512,Page4-BalanceSheets,ReconciliationofIncomeperBookswithIncomeperReturn(OKM-1)andAnalysisofUnappropriatedRetainedEarningsperBooks(OKM-2).

CorporationsthatarenotrequiredtocompleteFederalForm1120ScheduleM-1duetotherequirementtocompleteScheduleM-3musteithercompletetheOklahomaScheduleM-1orencloseacopyoftheFederalScheduleM-3.

Declaration of Estimated Tax...Corporationsmustmakeestimatedtaxpaymentswhenthetaxliabilityforthecurrentyearcanreasonablybeexpectedtobe$500ormore.Theestimatedtaxpaymentsshallbethelesserof70%ofyourcurrentyear’staxliabilityor100%ofthetaxliabilityshownonyourreturnfortheprecedingtaxableyearof12months.

Declaration of Estimated Tax (continued)Theestimatedtaxpaymentsshallbepaidinfourequal*installmentsof: • one-quarteronorbeforethe15thdayof

thefourthmonthofthetaxableyear; •one-quarteronorbeforethe15thdayof

thesixthmonthofthetaxableyear; •one-quarteronorbeforethe15thdayof

theninthmonthofthetaxableyear; •one-quarteronorbeforethe15thdayof

thefirstmonthofthesucceeding taxableyear.

Amendeddeclarationsmaybefiledonanyofthepaymentdates.FormOW-8-ESC,forfilingestimatedpayments,canbeobtainedfromourwebsiteatwww.tax.ok.gov.

*Forpurposesofdeterminingtheamountoftaxdueonanyoftherespectivedates,taxpayersmaycomputethetaxbyplacingtaxableincomeonanannualizedbasisasprescribedinRule710:50-13-9.

EstimatedpaymentscanbemadeelectronicallythroughtheOTCwebsite.Visitthe“OnlineServices”pageonthewebatwww.tax.ok.govforfurtherinformation.

Thereisnoprovisioninthepresentlawfortentativereturns.

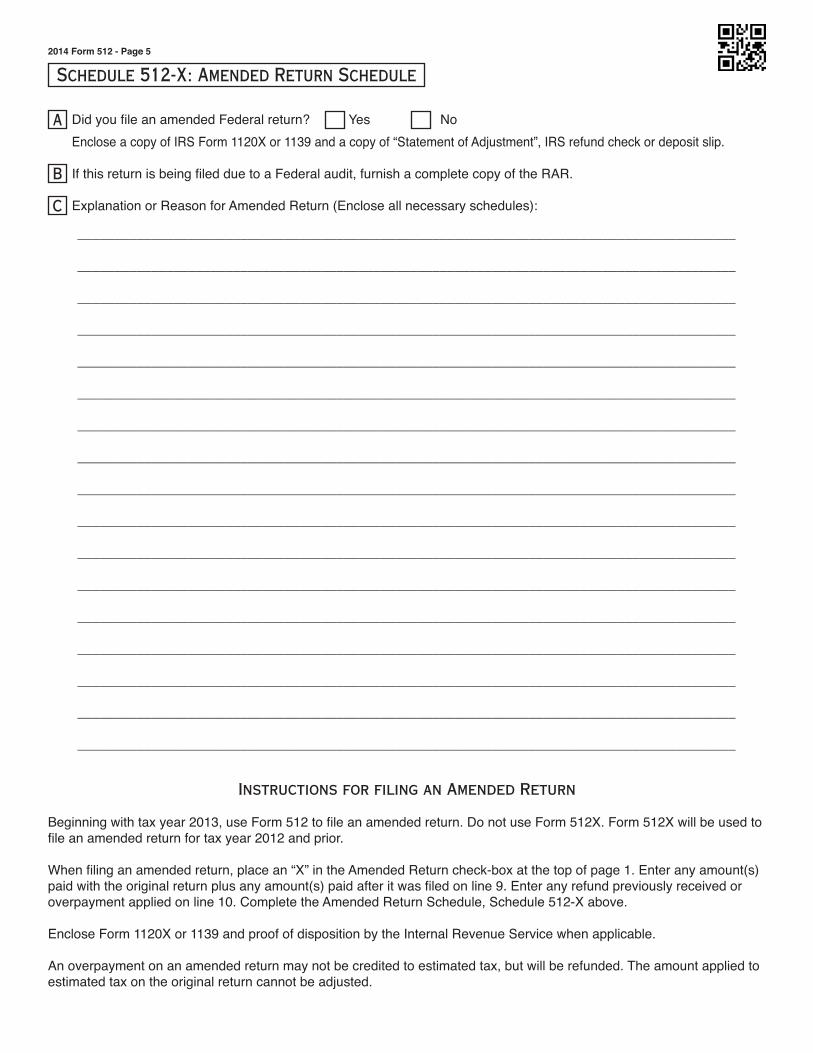

Amended Returns...Beginningwithtaxyear2013,theForm512willbeusedtofileanamendedreturn.SeeForm512,page5forcompleteinstructions.TheForm512Xwillonlybeusedfortaxyear2012andprior.

Adjustments by Internal Revenue Service...Taxpayerswhofile“consents”extendingthetimeformakingfederaladjustmentsautomaticallyextendthetimeformakingstateadjustments.ThetaxpayerisalsorequiredtofileanamendedreturnreportingallInternalRevenueServiceadjustments.AcopyofthefinalizedRARmustbeenclosedwitheachreturn.

Banks and Credit Unions...Stateandnationalbanksandstatecreditunionsaresubjecttoan“InLieu”tax.See68OSSec.2370.WhenreportingincomeonScheduleA,line(s)5and/or6b,pleasefurnishadetailedscheduleoftheinterestincomebysourceandamount.Expensedeductionsclaimedinarrivingattaxableincomeshallbereducedbyanamountequalto50%ofexcludedinterestincomeonobligationsoftheUnitedStatesgovernmentoragen-ciesthereofandobligationsoftheStateofOklahomaorpoliticalsubdivisionsthereof.

General Filing Information

4

Real Estate Investment Trusts…Arealestateinvestmenttrustthatdoesnotbecomereg-ularlytradedonanestablishedsecuritiesmarketwithinoneyearofthedateonwhichitfirstbecomesareales-tateinvestmenttrustshallbedeemednottohavebeenregularlytradedonanestablishedsecuritiesmarket,retroactivetothedateitfirstbecamearealestateinvest-menttrust.Anamendedreturnshallbefiledreflectingsuchretroactivedesignationforanytaxyearorpartyearoccurringduringitsinitialyearofstatusasarealestateinvestmenttrust.Forpurposesofthisparagraph,arealestateinvestmenttrustbecomesarealestateinvest-menttrustonthefirstdayithasmettherequirementsofSection856oftheInternalRevenueCode(IRC)andhaselectedtobetreatedasarealestateinvestmenttrustpursuanttoIRCSection856(c)(1).68OSSec.2358.

Oklahoma Net Operating Loss Deduction...

Notice:TheamountofanynetoperatinglossdeductionclaimedonScheduleA,line29aorScheduleB,line6d,mustalsobeenteredonthefrontofForm512inthespaceprovidedatthetopoftheform.Thereisalsoaspaceprovidedtoenterthelossyear(s).

Theamountofanyfederalnetoperatinglossdeductionshallbeadjustedasfollows:

Oklahoma Net Operating Loss Deduction (continued)

TheamountofanynetoperatinglossdeductionallowedforthetaxableyearshallbeanamountequaltotheaggregateoftheOklahomanetoperatinglosscarryoversandcarrybackstosuchyear.OklahomanetoperatinglossesshallbeseparatelydeterminedbyreferencetoIRCSection172asmodifiedbytheOklahomaIncomeTaxActandshallbeallowedwithoutregardtotheexistenceofafederalnetoperatingloss.Fortaxyears1996-2000,netoperatinglossesmaynotbecarriedbackbutmaybecarriedforwardforaperiodoftimenottoexceed15years.For tax years 2001 – 2007 and tax years 2009 and subsequent, the years to which such losses may be carried shall be determined solely by reference to IRC Section 172. For tax year 2008, years to which such losses may be carried back shall be limited to two years. 68OSSec.2358(A)(3).

Adetailedschedulemustbefurnishedforanynetoper-atinglosscarriedforwardtothecurrenttaxyear.

Anelectionmaybemadetoforegothecarrybackperiod.Awrittenstatementoftheelectionmustbepartoftheorigi-naltimelyfiledOklahomaloss-yearreturn.Ifthecorpora-tiontimelyfileditsreturnfortheloss-yearwithoutmakingtheelection,itmaymaketheelectiononanamendedreturnfiledwithin6monthsoftheduedateofthelossyearreturn(excludingextensions).Attachtheelectiontotheamendedreturn.Oncemade,theelectionisirrevocable.

Line by Line Instructions

General Instructions for Determining Oklahoma Taxable Income

Income Computation...Beginningwithfederaltaxableincome,properadjust-mentsaretobemadetoarriveatOklahomataxableincome.Someoftheadjustmentsmaybetoaddinterestincomefromobligationsofstateandpoliticalsub-divi-sionsthereof,andtodeductinterestfromU.S.obliga-tions.Oilandminingproductionorroyaltiesandgainorlossfromdispositionofsuchpropertyshallbeallocatedaccordingtotheirsitus.Generalandadministrativeexpenses,suchasinterestexpense,etc.,willordinarilybeallocatedonthebasisofOklahomadirectexpensetototaldirectexpense.

Safety Pays OSHA Consultation Service Exemption:(ScheduleA,Line26,columnBorScheduleB,Line3)AnemployerthatiseligibleforandutilizestheSafetyPaysOSHAConsultationServiceprovidedbytheOklahomaDepartmentofLaborshallreceivea$1,000exemptionforthetaxyeartheserviceisutilized.EmployersmustbeabletosubstantiatetheirparticipationintheOklahomaDepartmentofLabor’sSafetyPaysConsultationServiceuponrequest.

Qualified Refinery Property:(ScheduleA,Line10,columnBorScheduleB,Line2)IftheelectionwasmadetoexpensethecostofqualifiedOklahomarefinerypropertyplacedinservicebeforeJan-uary1,2012onapreviousyear’sOklahomareturn,thedepreciationdeductionclaimedonthefederalreturnforsuchpropertymustbeaddedbacktoarriveatOklahomataxableincome.Thisadditionmustbemaderegardlessofwhethertheexpensewasclaimedonthecorporatereturnorallocatedtoitsowners.68OSSec.2357.204

Looking for a form that will do the math for you?

Check out Oklahoma Form 512 2-D on our website at www.tax.ok.gov.

Line by Line Instructions

5

Cost of complying with Sulfur Regulations: (68OSSec.2357.205)AqualifiedrefinerymaymakeanirrevocableelectiontoallocatealloraportionofthecostofcomplyingwithsulfurregulationsissuedbytheEnvironmentalProtectionAgencyasadeductionallowabletoitsowners.Theallocationforeachpersonisequaltotheratableshareofthetotalamountallocated,determinedonthebasisoftheownershipinterestoftheperson.Thetaxableincomeoftherefineryshallnotbereducedbythereasonofanyamountallowedunderthissection.

If you are the Refinery -Tomaketheelection,attachaschedulestatingyourcorporatenameandFederalEmployerIdentificationNumber,alistofthecostsofcomplyingwithsulfurregulationssomeorallofwhicharebeingallocatedtoyourowners,andtheportionofsuchcostsallocatedtoeachowner,includingtheowner’snameandfederalidentificationnumber.Youshallalsoprovideeachownerwithwrittennoticeoftheamountoftheallocation.ThenoticemustincludeyourcorporatenameandFederalEmployerIdentificationNumberandtheowner’snameandfederalidentificationnumber.

If you are the Owner -(ScheduleA,Line26,columnBorScheduleB,Line6)Deducttheportionofthecostofcomplyingwithsulfurregulationswhichhavebeenallocatedtoyou.Attachthewrittennoticeoftheallocationreceivedfromtherefinery.

Oklahoma Capital Gain Deduction:(ScheduleA,Line26,columnBorScheduleB,Line6)Corporationscandeductqualifyinggainsreceivingcapitaltreatmentwhichareincludedinfederaltaxableincome.“Qualifyinggainsreceivingcapitaltreatment”meanstheamountofthenetcapitalgains,asdefinedunderIRCSection1222(11).Thequalifyinggainmust:

1) BeearnedonrealortangiblepersonalpropertylocatedwithinOklahomathatyouhaveowned,eitherdirectlyorindirectly,foratleastfiveuninterruptedyearspriortothedateofthesale;

2) BeearnedonthesaleofstockorownershipinterestinanOklahomaheadquarteredcompany,limitedliabilitycompany,orpartnershipwheresuchstockorownershipinteresthasbeenowned,eitherdirectlyorindirectly,byyouforatleastthreeuninterruptedyearspriortothedateofthesale;or

Oklahoma Capital Gain Deduction - (continued) 3) Beearnedonthesaleofrealproperty,tangible

personalpropertyorintangiblepersonalpropertylocatedwithinOklahomaaspartofthesaleofallorsubstantiallyalloftheassetsonanOklahomacompany,limitedliabilitycompany,orpartnershipwheresuchpropertyhasbeendirectlyorindirectlyownedbysuchentityorownedbytheownersofsuchentity,andusedinorderivedfromsuchentityforaperiodofatleastthreeuninterruptedyearspriortothedateofthesale.

EncloseForm561-CandacopyofyourFederalScheduleDandForm8949.

Agricultural Commodity Processing Facility Exclusion:(ScheduleA,Line26,columnBorScheduleB,Line6)Ownersofagriculturalcommodityprocessingfacilitiesmayexclude15%oftheirinvestmentcostsinaneworexpandedagriculturalcommodityprocessingfacil-itylocatedwithinOklahoma.Agriculturalcommodityprocessingfacilitymeansbuilding,structures,fixturesandimprovementsusedoroperatedprimarilyfortheprocessingorproductionofagriculturalcommoditiestomarketableproducts.Theinvestmentisdeemedmadewhenthepropertyisplacedinservice.

Undernocircumstancesshallthisexclusionloweryourtaxableincomebelowzero.Intheeventtheexclusiondoesexceedtaxableincome,anyunusedportionmaybecarriedoverforaperiodnottoexceedsixyears.Aschedulemustbeenclosedshowingthetypeofinvestment(s),thecostoftheinvestment,andthedateplacedinservice.

Captive Real Estate Investment Trusts: (Sched-uleA,Line10,columnBorScheduleB,Line2)Acaptiverealestateinvestmenttrust,whichissubjecttoFederalincometax,isrequiredtoadd-backthedivi-dends-paiddeductionotherwiseallowedbyfederallawincomputingnetincome.68OSSec.2358.

General Instructions for Determining Oklahoma Taxable Income, continued

OkTAP: More than your Filing Solution

www.tax.ok.gov/OkTAP

Access to file, pay, update, interact…all on your time, anytime!

See page 13 for more information.

Line by Line Instructions

6

Tax Tips:√ Checkyourcalculationscarefully.√ Don’t forget to sign your tax returns.√ Alwayscopyyourreturnforyourrecords.

Page Two - Schedule A

Schedule A, Column A is to be completed by all corporations. All corporations start with Schedule A.

Schedule A, Column B is to be used by all corporations domesticated in Oklahoma deriving all of their income within Oklahoma or by corporations whose business within and without Oklahoma is oil and gas production, min-ing, farming, or rental. This should be completed using the direct accounting method.

Income (loss) shall be allocated in accordance with the situs of such property. Overhead expense shall be allo-cated on the basis of direct expense in Oklahoma to the total direct expense everywhere.

Line 5 - Interest on U.S. Government ObligationsIfyoureportinterestonbonds,notes,andotherobliga-tionsoftheU.S.onyourfederalreturn,itmaybeexclud-edfromyourOklahomaincomeifadetailedscheduleisfurnished,accompaniedwith1099sshowingtheamountofinterestincomeandthenameoftheobligationfromwhichtheinterestisearned.Iftheincomeisfromamu-tualfundwhichinvestsinU.S.Governmentobligations,enclosedocumentationfromthemutualfundtosubstan-tiatethepercentageofincomederivedfromobligationsexemptfromOklahomatax. Interest from entities such as FNMA & GNMA does not qualify.

Line 6a - Other InterestAccountsreceivableinterestincomeandinterestincomefrominvestmentsheldtogenerateworkingcapitalshallbeallocatedtoOklahomaonthebasisofdirectexpense.

Allotherintangibleincome(loss)shallbeallocatedinaccordancewiththesitusofthecorporation.

Line 6b - State and Municipal InterestCorporationsdomiciledinOklahomathatreceiveincomeonbondsissuedbyanystateorpoliticalsubdivisionthereof,exemptfromfederaltaxationbutnotexemptfromtaxationbythelawsoftheStateofOklahoma,shalladdthetotalofsuchincometoarriveatOklahomaincome.

1) Incomefromallbonds,notesorotherobligationsissuedbytheStateofOklahoma,theOklahomaCapitalImprovementAuthority,theOklahomaMunicipalPowerAuthority,theOklahomaStudentLoanAuthority,andtheOklahomaTransportationAuthority(formerlyTurnpikeAuthority)isexemptfromOklahomaincometax.Theprofitfromthesaleofsuchbond,noteorotherobligationsshallbefreefromtaxation.

Line 6b - State and Municipal Interest (continued) 2) IncomefromlocalOklahomagovernmental

obligationsissuedafterJuly1,2001,otherthanthoseprovidedforin1,isexemptfromOklahomaincometax.Theexceptionsarethoseobligationsissuedforthepurposeofprovidingfinancingforprojectsfornonprofitcorporations.Localgovernmentalobligationsshallincludebondsornotesissuedby,oronbehalfof,orforthebenefitofOklahomaeducationalinstitutions,cities,towns,orcountiesorbypublictrustsofwhichanyoftheforegoingisabeneficiary.

3) IncomefromOklahomaStateandMunicipalBondsissuedpriortoJuly2,2001,otherthanthoseprovidedforin1,isexemptfromOklahomaincometaxonlyifsoprovidedbythestatuteauthorizingtheirissuance.

4) Incomeonbondsissuedbyanotherstateorpoliticalsubdivisionthereof(non-Oklahoma),exemptfromfederaltaxation,istaxableforOklahomaincometax.

Encloseascheduleofallmunicipalinterestreceivedbysourceandamount.Iftheincomeisfromamutualfundwhichinvestsinstateandlocalgovernmentobligations,enclosedocumentationfromthemutualfundtosubstantiatethepercentageofincomederivedfromobligationsexemptfromOklahomatax.

Note:Iftheinterestisexempt,thecapitalgain/lossfromthesaleofthebondmayalsobeexempt.Thegain/lossfromsaleofastateormunicipalbond,otherthanthoseprovidedforin1,isexemptonlyifsoprovidedbythestatuteauthorizingitsissuance.

Line 7 and 8 - Rents and RoyaltiesIncomefromrealortangiblepersonalproperty,leaseroyaltyorbonusshallbeallocatedinaccordancewiththesitusoftheproperty.

Line 9 - Gains or LossesGainsorlossesfromthesaleofleasesandgainsorlossesfromthesaleofrealandtangiblepersonalprop-erty,shallbeallocatedinaccordancewiththesitusoftheproperty.

Page Two - Schedule A

7

Line by Line Instructions

Line 10 - Other Income(ColumnB)RentsandinterestexpensespaidtoacaptiverealestateinvestmenttrustanddeductedonyourfederalreturnmustbeaddedbacktocomputeOklahomataxableincome.Suchadd-backisnotrequiredifthecaptiverealestateinvestmenttrustissubjecttotheadd-backforthedividends-paiddeduction.See“CaptiveRealEstateInvestmentTrusts”onpage15.

Page Two - Schedule A, continued

Line 12 through 26 - ExpensesExpensesrelativetotheincomeaboveshallbeallocateddirectlytothatincome.IncomefromdischargeofindebtednessdeferredunderIRCSection108(i)(1)whichwasaddedbacktocomputeOklahomataxableincomeintaxyear2010maybepartiallydeducted.Deduct,inColumnB,line26,anamountequaltotheportionofsuchdeferredincomeincludedinfederaltaxableincomefortaxyear2014.

Page Three - Schedule B

Line 3 - Deductions IncomefromU.S.obligations(seepage6,ScheduleAinstructions)andnetincomeseparatelyallocated(oilandgasproduction,mining,farming,orrentals)willbeenteredhere.Gainsorlossesfromsaleofintangiblepersonalpropertywhichisdirectlyallocatedshouldalsobeenteredhere.

IncomefromdischargeofindebtednessdeferredunderIRCSection108(i)(1),whichwasaddedbacktocom-puteOklahomataxableincomeintaxyear2010,maybepartiallydeducted.Deductanamountequaltothepor-tionofsuchdeferredincomeincludedinfederaltaxableincomefortaxyear2014.

Line 6 - Oklahoma Additions and DeductionsIncomeseparatelyallocatedtoOklahomashouldbeenteredhere.(Examples:interestincomefromstateob-ligationsorpoliticalsubdivisions,oilandgasproduction,mining,farmingorrentals,etc.).

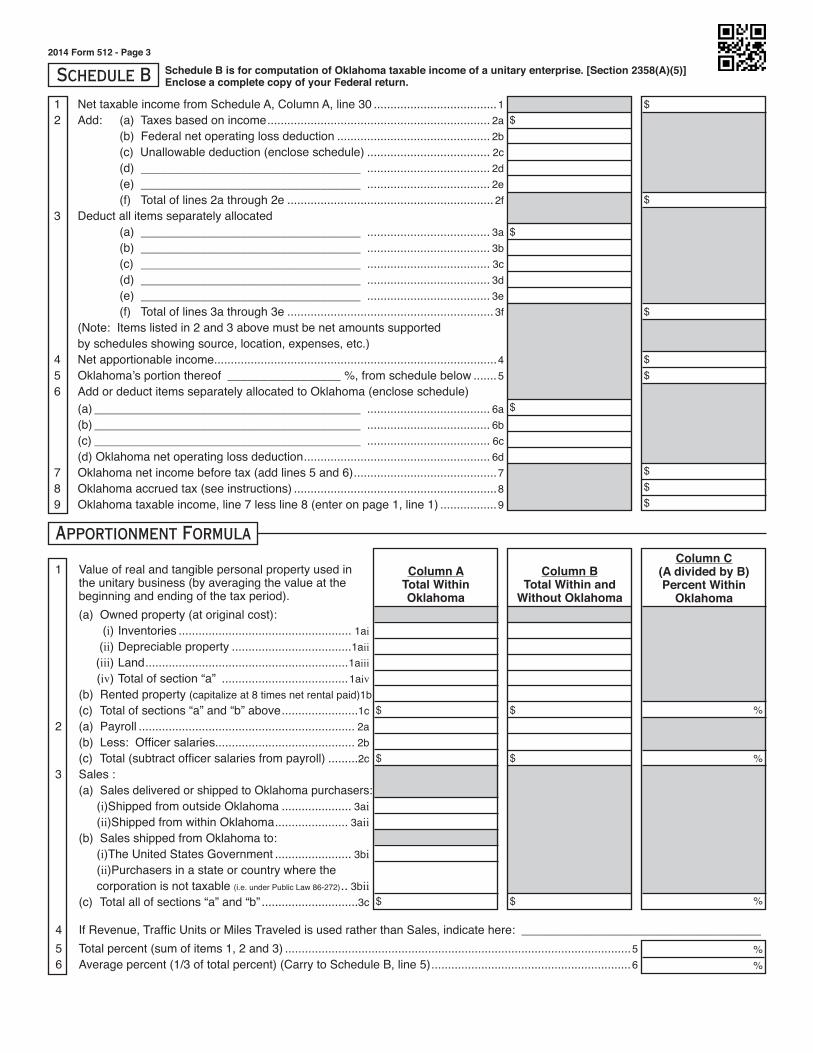

ScheduleBistobeusedbycorporationsconductingabusinessofaunitarynature.Aunitarybusinessisonewhoseincomeisderivedfromtheconductinmorethanonestateofasinglebusinessenterprise,allthefactorsofwhichareessentialtotherealizationofanultimategainderivedfromtheenterpriseasawhole,andnotfromitscomponentpartswhicharetoocloselycon-nectedandnecessarytoeachothertojustifydivisionorseparateallocation.

GenerallytheresultingamountisapportionedtoOkla-homabasedonthe3-factorformula.Thebasisoftheap-portionmentisthearithmeticalaverageofthreefactorsconsistingofproperty,payrollandsales.Iflessthan3factorsarepresent,theresultingamountisapportionedtoOklahomaona2-factororsinglefactorformulacon-sistingofthearithmeticalaverageofthefactorspresent.Afactorisconsideredpresentifthereisadenominator.

NOTE:FACTORSARENOTCOMPUTEDFROMTHECONSOLIDATEDTOTALS.EachfactorisaratioofthetotalwithinOklahomatothetotaleverywhere.Forin-comeapportionedtoOklahoma,thereistobeaddedallincomeseparatelyallocatedtoOklahomawiththeresultbeingOklahomataxableincome.68OSSec.2358.

Line 1 - Federal Taxable IncomeEnterNetTaxableIncomefromScheduleA,ColumnA,line30.

Line 2 - AdditionsDeductionsrelatingtoincomewhichisseparatelyallocat-edshallnotbeallowedandwillbeenteredhere.

RentsandinterestexpensespaidtoacaptiverealestateinvestmenttrustanddeductedonyourfederalreturnmustbeaddedbacktocomputeOklahomataxableincome.Suchadd-backisnotrequiredifthecaptiverealestateinvestmenttrustissubjecttotheadd-backforthedividends-paiddeduction.See“CaptiveRealEstateInvestmentTrusts”onpage5.

Log on to our website at www.tax.ok.gov. Click on the “Online Services” link to pay online.

Youcanpaythebalanceduebycreditcard.Paymentscanbemadeforanytaxyear.Estimatedincometaxpaymentsarealsoaccepted.

Aconveniencefeewillbeaddedtocreditanddebitcardtransactions.Formoreinformationregardingthisservice,pleasevisitourwebsiteatwww.tax.ok.govorcallourTaxpayerAssistanceOfficeat(405)521-3160.

Make Your Paymentsby Credit Card...

8 (continuedonpage9)

Line by Line Instructions

Page Three - Schedule B, continued

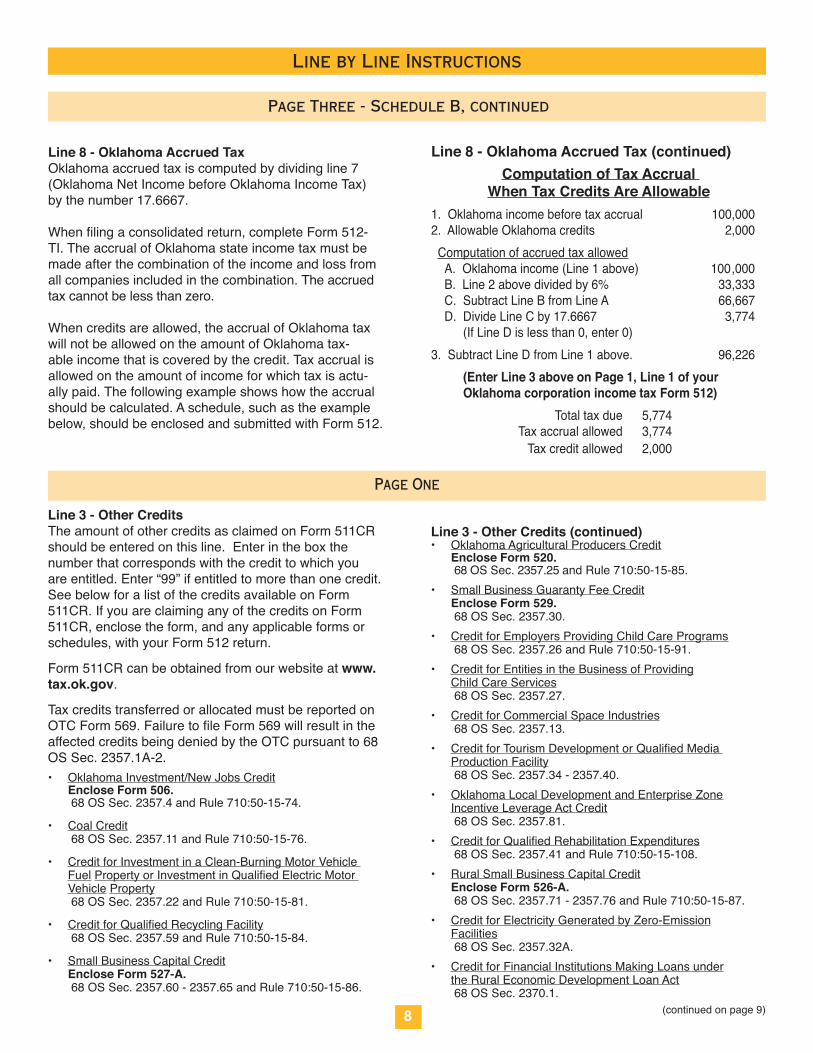

Line 8 - Oklahoma Accrued TaxOklahomaaccruedtaxiscomputedbydividingline7(OklahomaNetIncomebeforeOklahomaIncomeTax)bythenumber17.6667.

Whenfilingaconsolidatedreturn,completeForm512-TI.TheaccrualofOklahomastateincometaxmustbemadeafterthecombinationoftheincomeandlossfromallcompaniesincludedinthecombination.Theaccruedtaxcannotbelessthanzero.

Whencreditsareallowed,theaccrualofOklahomataxwillnotbeallowedontheamountofOklahomatax-ableincomethatiscoveredbythecredit.Taxaccrualisallowedontheamountofincomeforwhichtaxisactu-allypaid.Thefollowingexampleshowshowtheaccrualshouldbecalculated.Aschedule,suchastheexamplebelow,shouldbeenclosedandsubmittedwithForm512.

Line 8 - Oklahoma Accrued Tax (continued)Computation of Tax Accrual

When Tax Credits Are Allowable1.Oklahomaincomebeforetaxaccrual 100,0002.AllowableOklahomacredits 2,000 Computationofaccruedtaxallowed A.Oklahomaincome(Line1above) 100,000 B.Line2abovedividedby6% 33,333 C.SubtractLineBfromLineA 66,667 D.DivideLineCby17.6667 3,774 (IfLineDislessthan0,enter0)3.SubtractLineDfromLine1above. 96,226 (Enter Line 3 above on Page 1, Line 1 of your Oklahoma corporation income tax Form 512) Totaltaxdue 5,774 Taxaccrualallowed 3,774 Taxcreditallowed 2,000

Page One

Line 3 - Other CreditsTheamountofothercreditsasclaimedonForm511CRshouldbeenteredonthisline.Enterintheboxthenumberthatcorrespondswiththecredittowhichyouareentitled.Enter“99”ifentitledtomorethanonecredit.SeebelowforalistofthecreditsavailableonForm511CR.IfyouareclaiminganyofthecreditsonForm511CR,enclosetheform,andanyapplicableformsorschedules,withyourForm512return.

Form511CRcanbeobtainedfromourwebsiteatwww.tax.ok.gov.

TaxcreditstransferredorallocatedmustbereportedonOTCForm569.FailuretofileForm569willresultintheaffectedcreditsbeingdeniedbytheOTCpursuantto68OSSec.2357.1A-2.• OklahomaInvestment/NewJobsCredit Enclose Form 506. 68OSSec.2357.4andRule710:50-15-74.

• CoalCredit 68OSSec.2357.11andRule710:50-15-76.

• CreditforInvestmentinaClean-BurningMotorVehicleFuel PropertyorInvestmentinQualifiedElectricMotorVehicle Property

68OSSec.2357.22andRule710:50-15-81.

• CreditforQualifiedRecyclingFacility 68OSSec.2357.59andRule710:50-15-84.

• SmallBusinessCapitalCredit Enclose Form 527-A. 68OSSec.2357.60-2357.65andRule710:50-15-86.

Line 3 - Other Credits (continued)• OklahomaAgriculturalProducersCredit Enclose Form 520. 68OSSec.2357.25andRule710:50-15-85.• SmallBusinessGuarantyFeeCredit Enclose Form 529. 68OSSec.2357.30.• CreditforEmployersProvidingChildCarePrograms 68OSSec.2357.26andRule710:50-15-91.• CreditforEntitiesintheBusinessofProviding

ChildCareServices 68OSSec.2357.27.• CreditforCommercialSpaceIndustries 68OSSec.2357.13.• CreditforTourismDevelopmentorQualifiedMedia

ProductionFacility 68OSSec.2357.34-2357.40.• OklahomaLocalDevelopmentandEnterpriseZone

IncentiveLeverageActCredit 68OSSec.2357.81.• CreditforQualifiedRehabilitationExpenditures

68OSSec.2357.41andRule710:50-15-108.• RuralSmallBusinessCapitalCredit Enclose Form 526-A. 68OSSec.2357.71-2357.76andRule710:50-15-87.• CreditforElectricityGeneratedbyZero-Emission

Facilities 68OSSec.2357.32A.• CreditforFinancialInstitutionsMakingLoansunder

theRuralEconomicDevelopmentLoanAct 68OSSec.2370.1.

9

Electronic ChecksNow Accepted

Through WebsitePaperchecksarenotyouronlyoptionwhenpayingyourbalancedue.Youmaypayelectronicallyfromyourcheck-ingaccountthroughourwebsite.Logontowww.tax.ok.govandvisitthe“Online Servic-es”linktoviewallyourpaymentoptions.Othertaxtypesarealsoacceptedthroughthispaymentsystem,includingestimatedtaxpayments.

Line by Line Instructions

(continuedonpage10)

Page One, continued

Line 3 - Other Credits (continued)• CreditforManufacturersofSmallWindTurbines 68OSSec.2357.32BandRule710:50-15-92.

• CreditforQualifiedEthanolFacilities 68OSSec.2357.66andRule710:50-15-106.

• PoultryLitterCredit 68OSSec.2357.100andRule710:50-15-95.

• CreditforQualifiedBiodieselFacilities 68OSSec.2357.67andRule710:50-15-98.

• FilmorMusicProjectCredit Enclose Form 562. 68OSSec.2357.101andRule710:50-15-101.

• CreditforBreedersofSpeciallyTrainedCanines 68OSSec.2357.203andRule710:50-15-97.

• CreditforWagesPaidtoanInjuredEmployee 68OSSec.2357.47andRule710:50-15-107.

• CreditforModificationExpensesPaidforanInjuredEmployee 68OSSec.2357.47andRule710:50-15-107.

• DryFireHydrantCredit 68OSSec.2357.102andRule710:50-15-99.

• CreditfortheConstructionofEnergyEfficientHomes 68OSSec.2357.46andRule710:50-15-104.

• CreditforRailroadModernization 68OSSec.2357.104andRule710:50-15-103.

• ResearchandDevelopmentNewJobsCredit Enclose Form 563. 68OSSec.54006andRule710:50-15-105.

• CreditforStaffordLoanOriginationFee (availableforbanksandcreditunions) 68OSSec.2370.3.

• CreditforBiomedicalResearchContribution 68OSSec.2357.45andRule710:50-15-113.

• CreditforEmployersintheAerospaceSector Enclose Form 565. 68OSSec.2357.301,2357.302and2357.303andRule

710:50-15-109.

• WireTransferFeeCredit 68OSSec.2357.401andRule710:50-15-111.

• CreditforManufacturersofElectricVehicles 68OSSec.2357.402andRule710:50-15-112.

• CreditforCancerResearchContribution 68OSSec.2357.45andRule710:50-15-113.

• OklahomaCapitalInvestmentBoardTaxCredit 74OSSec.5085.7.

• CreditforContributionstoaScholarship-Granting Organization 68OSSec.2357.206andRule710:50-15-114.

• CreditforContributionstoanEducationalImprovement GrantOrganization 68OSSec.2357.206andRule710:50-15-115.

Line 7 - Oklahoma Withholding1. EntertheOklahomaincometaxwithheldfromyour

royaltypayments.

2. Oklahomaincometaxiswithheldfromdistributionsmadebypass-throughentitiestononresidentmem-bers,unlesssuchnonresidentmemberhasfiledawithholdingexemptionaffidavit(FormOW-15).Ifyouareanonresidentmemberofapass-throughentitywhohasnotfiledanaffidavit,OklahomaincometaxshouldhavebeenwithheldondistributionsofOkla-homataxableincome.EntertheOklahomaincometaxwithheldonyourdistribution.

EnclosetheForm500-A,Form1099-MISC,Form500-B,FormK-1orotherdocumentationtosubstantiateOkla-homawithholding.Line 8 - Refundable CreditsPlacean“X”inthebox(es)online8toreportanycreditfromForm577orForm578.

IfclaimingtheRefundable Coal Credit,encloseForm577.Creditsearned,butnotused,baseduponactivityoccurringonorafterJanuary1,2014willberefundedat85%ofthefaceamountofthecredits.Apass-throughentitythatdoesnotfileaclaimforadirectrefundwillallocatethecredittooneormoreofitsshareholders,partnersormembers.

IfclaimingtheRefundable Credit for Electricity Gen-erated by Zero-Emission Facilities,encloseForm578.Creditsgenerated,butnotused,onorafterJanuary1,2014willberefundedtothetaxpayerat85%ofthefaceamountofthecredits.Apass-throughentitythatdoesnotfileaclaimforadirectrefundwillallocatethecredittooneormoreofitsshareholders,partnersormembers.Line 14 - DonationsYouhavetheopportunitytomakeafinancialgiftfromyourrefundtoavarietyofOklahomaorganizations.Entertheamountofyourdonationandplacethelinenumberoftheorganizationintheboxonline14ofForm512.Ifyougivetomorethanoneorganization,puta“99”intheboxandattachascheduleshowinghowyouwouldlikeyourdonationsplit.

10

Line by Line Instructions

Page One, continued

Line 14 - Donations (continued) Support of Domestic Violence and Sexual Assault ServicesYoumaydonatefromyourtaxrefundforthebenefitofdomesticviolenceandsexualassaultservicesinOkla-homathathavebeencertifiedbytheAttorneyGeneral.Yourdonationwillbeusedtoprovidegrantstodomesticviolenceandsexualassaultserviceprovidersforthepurposeofprovidingdomesticviolenceandsexualas-saultservicesinOklahoma.Theterm“services”includesbutisnotlimitedtoprograms,sheltersoracombinationthereof.Ifyouarenotreceivingarefund,youmaystilldonate.Mailyourcontributionto:AttorneyGeneral,Do-mesticViolenceandSexualAssaultServicesFund,313NE21stStreet,OklahomaCity,OK73105.

Support of Volunteer Fire DepartmentsYoumaydonatefromyourtaxrefundforthebenefitofvolunteerfiredepartmentsinOklahoma.Yourdonationwillbeusedtoprovidegrantstovolunteerfiredepart-mentsinthisstateforthepurposeofpurchasingbunkergear,wildlandgearandotherprotectiveclothing.Ifyouarenotreceivingarefund,youmaystilldonate.Mailyourcontributionto:OklahomaStateFireMarshal,Attn:VolunteerFireDepartmentFund,2401NW23rdStreet,Suite4,OklahomaCity,OK73107.

Oklahoma Lupus Revolving FundYoumaydonatefromyourrefundforthebenefitoftheOklahomaLupusRevolvingFund.MoniesfromthefundwillbeusedbytheStateDepartmentofHealthtopro-videgrantstotheOklahomaMedicalResearchFoun-dationforthepurposeoffundingresearchintotreatingandcuringlupusinthisstate.Ifyouarenotreceivingarefund,youmaystilldonate.Mailyourcontributionto:StateDepartmentofHealth,LupusRevolvingFund,P.O.Box268823,OklahomaCity,OK73152-8823.

Oklahoma Sports Eye Safety ProgramYoumaydonatefromyourrefundforthebenefitoftheOklahomaSportsEyeSafetyProgram.YourdonationwillbeusedbytheStateDepartmentofHealthtoestab-lishasportseyesafetygrantprogramforthepurchaseanddistributionofsportseyesafetyprogramsandmaterialstoOklahomaclassroomsandsportseyesafetyprotectiveweartochildrenage18andunder.Monieswillalsobeusedtoexploreopportunitiestoutilizenonprofitorganizationstoprovidesuchsafetyinformationorequipment.Ifyouarenotreceivingarefund,youmaystilldonate.Mailyourcontributionto:StateDepartmentofHealth,SportsEyeSafetyFund,P.O.Box268823,OklahomaCity,OK73152-8823.

Line 14 - Donations (continued) Support of Programs for Volunteers to Act as

Court Appointed Special Advocates for Abused or Neglected Children

YoumaydonatefromyourtaxrefundtosupportprogramsforvolunteerstoactasCourtAppointedSpecialAdvo-catesforabusedorneglectedchildren.DonationswillbeplacedintheIncomeTaxCheckoffRevolvingFundforCourtAppointedSpecialAdvocates.MonieswillbeexpendedbytheOfficeoftheAttorneyGeneralforthepurposeofprovidinggrantstotheOklahomaCASAAs-sociation.Ifyouarenotreceivingarefund,youmaystilldonate.Mailyourcontributionto:OklahomaCASAAsso-ciation,Inc.,P.O.Box54946,OklahomaCity,OK73154.

Support of the Oklahoma National GuardYouhavetheopportunitytodonatefromyourtaxrefundforthebenefitofprovidingfinancialrelieftoqualifiedmembersoftheOklahomaNationalGuardandtheirfamilies.DonationswillbeplacedintheIncomeTaxCheckOffRevolvingFundfortheSupportoftheOkla-homaNationalGuardReliefProgram.Monies,toassistOklahomaNationalGuardmembersandtheirfamilieswithapprovedhardshipexpenses,willbeexpendedbytheMilitaryDepartment.Ifyouarenotreceivingarefund,youmaystilldonate.Mailyourcontributionto:OperationHomefrontTaskForce,3501MilitaryCircle,OklahomaCity,OK73111-4398.

Support of Programs for Regional Food Banks in OklahomaYoumaydonatefromyourtaxrefundforthebenefitoftheRegionalFoodBankofOklahomaandtheCom-munityFoodBankofEasternOklahoma(OklahomaFoodBanks).TheOklahomaFoodBanksarethelargesthunger-relieforganizationsinthestate-distributingfoodtocharitableandfaith-basedfeedingprogramsthrough-outall77countiesinOklahoma.Yourdonationwillbeusedtohelpprovidefoodtothemorethan500,000Oklahomansatriskofhungeronadailybasis.Ifyouarenotreceivingarefund,youmaystilldonatebymailingyourcontributionto:OklahomaDepartmentofHumanServices,RevenueProcessingUnit,Re:ProgramsforOKFoodBanks,POBox248893,OklahomaCityOK73142.

Support Oklahoma Honor FlightsYouhavetheopportunitytodonateanyamountofyourtaxrefundtosupportOklahomaHonorFlights.OklahomaHonorFlightsisa501(c)(3)not-for-profitorganizationthattransportsOklahomaWorldWarIIveteranstoWash-ington,D.C.tovisitthememorialdedicatedtohonortheirserviceandsacrifice.Ifyouarenotreceivingarefund,youmaystilldonate.Mailyourcontributionto:OklahomaHonorFlights,POBox10492,MidwestCityOK73140.

1

3

4

7

8

5

62

(continuedonpage11)

11

Line by Line Instructions

Page One, continued

Line 14 - Donations (continued) Public School Classroom Support FundDonationstothePublicSchoolClassroomSupportRe-volvingFundwillbeusedbytheStateBoardofEduca-tiontoprovideoneormoregrantsannuallytopublicschoolclassroomteachers.Grantswillbeusedbytheclassroomteacherforsupplies,materials,orequipmentfortheclassorclassestaughtbytheteacher.Grantap-plicationswillbeconsideredonastatewidecompetitivebasis.Youmayalsomailadonationto:OklahomaStateBoardofEducation,PublicSchoolClassroomSupportFund,OfficeoftheComptroller,2500NorthLincolnBou-levard,Room415,OklahomaCity,OK73105-4599.

Line 16 - RefundCompletethedirectdepositsectiononthetaxreturntohavetherefunddepositedintoyouraccountatabankorotherfinancialinstitution.Seepage12“DirectDepositInformation”fordetail.

Line 18 Public School Classroom Support FundAdonationtothisfundmaybemadeonataxduereturn.Forinformationregardingthisfund,seeLine14,#10.

Line 19 - Underpayment of Estimated Tax InterestAllcorporationsarerequiredtomakeestimatedtaxpaymentsifthetaxliabilityis$500ormore.Toavoidthe20%UnderpaymentofEstimatedTaxInterest,timelyfiledestimatedtaxpaymentsarerequiredtobeequaltothesmallerof70%ofthecurrentyeartaxliabilityor 100%ofyourprioryeartax.Thetaxliabilityisthetaxduelessallcreditsexceptamountspaidonestimatedtaxandextensionpayments.

Placean“X”intheboxiftheunderpaymentofestimatedtaxwascomputedusingtheannualizedincomeinstall-mentmethod.

Note: NoUnderpaymentofEstimatedTaxInterestshallbeimposedifthetaxliabilityshownonthereturnislessthan$1,000.EncloseFormOW-8-P.

Ifanamended returnisfiledbeforetheduedateforfilingtheoriginalreturn,includinganyextension,thetaxshownontheamendedreturnisusedtodeterminetheamountofunderpayment.Iftheamendedreturnisfiledaftertheduedate,includingextension,thetaxshownontheamendedreturnwillnotbeusedtocomputetheamountofunderpayment.

Line 20 - Delinquent Penalty and InterestInterestattherateof11/4%permonthshallbepaidonthetaxduefromtheoriginalduedateuntilpaid.90%ofthetaxliabilitymustbepaidbytheoriginalduedateofthereturntoavoidadelinquentpenaltychargeof5%forlatepayment.

Line 14 - Donations (continued) Historic Greenwood District Music Festival FundWithpartofyourtaxrefundyoucansupportmusicfestivalsintheHistoricGreenwoodDistrictofTulsa.YourdonationwillbeusedbytheOklahomaHistoricalSocietytoassistwithmusiceducation,publicconcerts,andacelebrationofTulsa’sandOklahoma’smusicalheritage.Youmayalsomailyourcontributionsto:GreenwoodDis-trictMusicFestivalFund,OklahomaHistoricalSociety,800NazihZuhdiDr.,OklahomaCity,OK73105.

Does Your Form Have One of These?

2-D Barcode Information

Ifyourecognizethisbarcodefromyourtaxreturn,yourreturnwaspreparedusingcomputersoftwareutilizingtwodimensionalbarcoding.Thismeansyourtaxinformationwillbeprocessedfasterandmoreac-curatelyandyouwillseeyourrefundfaster!

Belowareanswerstocommonquestionsaboutbarcoding.

What Are the Benefits of 2-D Barcoding? Thistechnologyconvertstheinformationonataxreturnintoascannablebarcode.Inseconds,theOklahomaTaxCommissioncanreadthebarcode,processitimmediatelyintooursystem,andeliminatetheneedforanymanualdataentry.ThisenablestheOklahomaTaxCommissiontoprocessmorereturns,fasterandwithnoerrors.Ultimately,thismeansfasterrefundsforthetaxpayersofOklahoma.

What about Print Quality? Generally,evenwhendamaged,a2-Dbarcodecanbereadwith100%accuracy,aslongastheprintqualityissetatahighlevel(notdraft).

Where Do I Mail 2-D forms? Themailingaddressfor2-Dincometaxformsis:

OklahomaTaxCommissionPostOfficeBox269045

OklahomaCity,OK73126-9045

This special mailing address is for 2-D forms only.

9 10

12

Direct Deposit Information

ABC Corporation123MainStreetAnyplace,OK00000

1234

ANYPLACE BANKAnyplace,OK00000

For

PAYTOTHE ORDEROF $

15-0000/0000

DOLLARS

:120120012 : 2020268620 1234

RoutingNumber

AccountNumberSAMPLE

SAMPLE Note:Theroutingandaccountnumbersmayappearindifferentplacesonyourcheck.

Placean‘X’intheappropriateboxastowhethertherefundwillbegoingintoacheckingorsavings account.Pleasekeepinmindyouwillnotreceivenotificationofthedeposit. Fillouttheroutingnumber.Theroutingnumbermustbeninedigits.Usingthesamplecheckshown

below,theroutingnumberis120120012.Ifthefirsttwodigitsarenot01through12or21through32,thedirectdepositwillfailtoprocess.Aletterrequestingcorrectbankinginformationwillbemailedtotheaddressshownonyourtaxreturn.

Enteryouraccountnumber.Theaccountnumbercanbeupto17characters(bothnumbersand letters).Includehyphensbutomitspacesandspecialsymbols.Enterthenumberfromlefttoright andleaveanyunusedboxesblank.Onthesamplecheckshownbelow,theaccountnumberis 2020268620.

12

3

WARNING!Duetoelectronicbankingrules,theOTCwillNOTallowdirectdepositstoorthroughforeignfinancialinstitu-tions.Ifyouuseaforeignfinancialinstitution,orhaveaforeignaddressonyourincometaxreturn,youwillbeissuedapa-percheck.IfyouhaveanaddresswithanAPO,FPOorDPOyouarenotconsideredtohaveaforeignaddress;yourrefundwillbedirectdeposited.

Please Note: TheOTCisnotresponsibleifafinancialinstitutionrefusedadirectdeposit.Ifadirectdepositisre-fused,acheckwillbeissuedtotheaddressshownonthetaxreturn.

Completethedirectdepositsectiononthetaxreturntohavetherefunddirectlydepositedintoyouraccountatabankorfinancialinstitution.Refunds,withlimitedexceptions,mustbemadebydirectdeposit.

•Intheeventthatyouowetaxes,pleaseencloseacheckormoneyorderpayableto“OklahomaTaxCommission”.ThetaxpayerFEINandthetaxyearshouldbeonyourcheckormoneyorderforyourpaymenttobeproperlycredited.•Paymentsmayalsobemadeelectronicallyonline.Logontowww.tax.ok.govandvisitthe“Online Services” section.•Whencomplete,makecopiesofallthedocu-mentsforyourrecords.

When You Are Finished...•Donotencloseanycorrespondenceotherthanthosedocumentsandschedulesrequiredforyourreturn.

• Forproperaccountapplication,pleasedonotencloseanyestimatedpaymentsand/orvoucherswiththisreturn.Mailtaxyear2015estimatedpay-mentsseparately.

•Returnmustbesigned.

•Ifyourreturnhasa2-Dbarcode,mailtheoriginalreturnalongwithanypaymentdueto: Oklahoma Tax Commission Income Tax PO Box 269045 Oklahoma City, OK 73126-9045

•Ifyourreturndoesnothavea2-Dbarcode,mailtheoriginalreturnalongwithanypaymentdueto: Oklahoma Tax Commission Income Tax PO Box 26800 Oklahoma City, OK 73126-0800Whatisa2-Dbarcode?Seepage11.Whatisa2-Dbarcode?Seepage11.

13

How to Contact the Oklahoma Tax CommissionWhether you need a tax form,

have a question or need further information, there are many ways to reach us.

The Oklahoma Tax Commission is not required to give actual notice to taxpayers of changes in any state tax law.

Federal Employer Identification Number (FEIN): The request for your FEIN is authorized by Section 405, Title 42, of the United States Code. You MUST provide this information. It will be used to establish your identity for tax purposes only.

Give Us a Call!

TheOklahomaTaxCommissioncanbereached

at(405) 521-3160.Thein-statetollfreenumber

is(800) 522-8165.Press“0”tospeaktoa

representative.

Office Locations!

Oklahoma City2501NorthLincolnBoulevard

(405) 521-3160

Tulsa440SouthHouston,5thFloor

(918) 581-2399

Visit Us on the Web!You’llfindawealth

ofinformationonourweb-site,includingdownloadable

taxforms,answerstocommonquestions,andonlinefilingoptionsforbothincome

andbusinesstaxes! www.tax.ok.gov

Use OkTAP to File and Pay your Taxes

For more information visit www.tax.ok.gov/OkTAP

With OkTAP you can: • File and pay taxes for your sales, withholding, franchise and mixed

beverage accounts along with many more tax types• View OTC returns, letters and notices• Engage in secure messaging with OTC representatives• Order coin-operated device decals• Register new businesses with the OTC• Register a third-party preparer to manage your account

1 Oklahoma taxable income (as shown on Schedule A or B or, if consolidated, from Form 512-TI) .................1 2 Tax: 6% of line 1 ........................................................................................................................2 3 Less: Other Credits Form (total from Form 511CR) (see instructions) ..................... ....3 4 Balance of tax due (line 2 minus line 3, but not less than zero) ................................................4 5 2014 Oklahoma estimated tax payments (i.e. Form(s) OW-8-ESC) ...... 5 6 Amount paid with extension request .................................................. 6 7 Oklahoma withholding (enclose Form 1099, 500-A or other withholding statement) ...... 7 8 Refundable Credits from Form ................a) 577 .......b) 578 .... 8 9 Amountpaidwithoriginalreturnandamountpaidafteritwasfiled (amended return only) ........................................................................ 9 10 Any refunds or overpayment applied (amended return only) ........... 1011 Total of lines 5 through 10 ....................................................................................................... 1112 Overpayment (line 11 minus line 4) .........................................................................................12 13 Amount of line 12 to be credited to 2015 estimated tax (original return only) ... 13

$ .00

If the Oklahoma Tax Commission may discuss this return with your tax preparer, place an ‘X’ here:Under penalties of perjury, I declare I have examined this return, including any accompanying schedules and statements, and to the best of my knowledge and belief, it is true, correct and complete. If prepared by person other than the taxpayer, this declaration is based on all information of which preparer has any knowledge.

Corporate Seal

SignatureofOfficer Date

Title

Phone Number

SignatureofPreparer Date

Preparer’sAddress

Phone Number

00000000

0000

0000

000000

0000

00000000

0000

00

00

The

Okl

ahom

a Ta

x C

omm

issi

on is

not

requ

ired

to g

ive

actu

al n

otic

e to

taxp

ayer

s of

cha

nges

in a

ny s

tate

tax

law

.

Notice:

Line 13 instructions provide you the opportunity to make a financial gift from your refund to a variety of Oklahoma organizations. Place the line number of the organization from the line 14 instructions in the box below and enter the amount you are donating. If giving to more than one organization, put a “99” in the box and attach a schedule showing how you would like your donation split.

Corporation Income Tax ReturnState of Oklahoma

B. Business Code Number

A. Federal EmployerIdentificationNumber If you have applied for an extension

fromtheIRS,placean‘X’hereandenclose a copy.

Ifthisisafinalreturn,placean‘X’here:

Type of Return FiledExtension

Oklahoma or Federal or

(page 3 of instructions)

Separate Consolidated

17 TaxDue(line4minusline11) ............................................................................TaxDue 1718 Donation:PublicSchoolClassroomSupportFund ........ $2 $5 $ _________ .. 1819 Underpayment of estimated tax interest ......................................................... Annualized 19 20 For delinquent payment add penalty of 5% .............. $ ________________________ plus interest of 1.25% per month ........................................ $ ________________________ ........ 2021 Total tax, donation, penalty and interest (add lines 17 - 20) ........................BalanceDue 21

Preparer’sPTIN

Name of Corporation:

Street Address:

City, State or Province, Country and ZIP or Foreign Postal Code:

14 Donationsfromyourrefund .... $2 $5 $ _______ . 14 15 Total (add lines 13 and 14) ......................................................................................................................15 16 Amount of line 12 to be refunded to you (line 12 minus line 15) ......................................Refund 16

Form 5122014

AMENDED RETURN!

For the year January 1 - December 31, 2014, or other taxable yearbeginning:

2014ending:

, ,

If this is an Amended Returnplace an‘X’ here

See Schedule 512-X on page 5.

Is this refund going to or through an account that is located outside of the United States? Yes No

Routing Number:

checking account savings account

Account Number:

Deposit my refund in my: Direct Deposit Note:All refunds must be by direct deposit. See Direct Deposit Information on page 12 of the 512 Packet for details.

Enter the amount of Oklahoma net operating loss as shown on Sch. A, line 29(a) or Sch. B, line 6(d) .....................Loss year(s): .......

( )

Make check payable to the Oklahoma Tax Commission

Enclose a copy of Federal return - Remit to Oklahoma Tax Commission - Post Office Box 26800 - Oklahoma City, OK 73126-0800

Has the Internal Revenue Service redetermined your tax liability for prior years? Yes No What years? ____________________Didyoufileamendedreturnsfortheyearsstatedabove? Yes No N/AHas the statute of limitations been extended by consent for any prior years? Yes No What years? ____________________Business name _________________________________________________ DatebusinessbeganinOklahoma ________________Principal location(s) in Oklahoma _________________________________________________________________________________Givename,addressandrelationshipofallaffiliatedcorporations-encloseFederalForm851________________________________________________________________________________________________________________________________________________________________________________________________________________________

1 Gross receipts or gross sales __________________ (less: returns and allowances) .............. 1 2 Less: Cost of goods sold ....................................................................................... 23 Grossprofit(line1minusline2) ............................................................................. 34 Dividends ................................................................................................................ 4 5 Interest on obligations of the United States and U.S. Instrumentalities.................. 5 6 (a) Other interest ..................................................................................................6a (b) Municipal interest ............................................................................................6b 7 Gross rents ............................................................................................................. 7 8 Gross royalties........................................................................................................ 8 9 (a) Net capital gains..............................................................................................9a (b) Ordinary gain or [loss] .....................................................................................9b10 Other income (enclose schedule) ..........................................................................1011 Total income (add lines 3 through 10) ..................................................................11

Gross Income (lines 1 through 11)

Schedule A, Column B is for corporations whose income is all within Oklahoma and/or for corporations whose income is partly within and partly without Oklahoma (not unitary). Enclose a complete copy of your Federal return.

Deductions (lines 12 through 27)

Totals (lines 28 through 30)

Column AAs reported on Federal Return

Column BTotal applicable

to Oklahoma

Important:Allapplicablelinesandschedulesmustbefilledin.

Note: Indicate method used to allocate expenses to Oklahoma and enclose schedule of computations.

Oklahoma Depletion in Lieu of Federal Depletion - Oklahoma depletion on oil and gas may be computed at 22% of gross income derivedfromeachOklahomapropertyduringthetaxableyear.Majoroilcompanies,asdefinedin52OklahomaStatutesSection288.2,whencomputingOklahomadepletionshall be limited to 50% of the net income (computed without the allowance for depletion) from each property. Depletion schedule by property must be enclosed with return. Note: General and administrative expense (computed on basis of Oklahoma direct expense to total direct expense) must be deducted before applying the 50% test.

2014 Form 512 - Page 2

Schedule A

Address City State Zip

Location of Principal Accounting RecordsAdditional Information

28 Taxable income before net operating loss deductions and special deductions .....28 29 Less: (a) Net operating loss deduction (schedule) ............................................29a (b) Special deductions ..............................................................................29b30 Taxable income (line 28 minus lines 29a & b). Enter Column B on page 1, line 1 .....30

12 Compensationofofficers .......................................................................................12 13 Salaries and wages ...............................................................................................1314 Repairs ..................................................................................................................1415 Bad debts ..............................................................................................................1516 Rents .....................................................................................................................1617 Taxes .....................................................................................................................1718 Interest...................................................................................................................1819 Charitable Contributions ........................................................................................1920 Depreciation ..........................................................................................................2021 Depletion(seeinstructionsbelow).........................................................................2122 Advertising .............................................................................................................2223 Pension,profit-sharingplans,etc. .........................................................................2324 Employeebenefitprograms...................................................................................2425 Domesticproductionactivitiesdeduction ..............................................................2526 Other deductions (enclose schedule) ....................................................................2627 Total Deductions (add lines 12 through 26) .........................................................27

1 Value of real and tangible personal property used in the unitary business (by averaging the value at the beginning and ending of the tax period). (a) Owned property (at original cost): (i) Inventories .................................................... 1ai (ii)Depreciableproperty ....................................1aii (iii) Land .............................................................1aiii (iv) Total of section “a” ......................................1aiv (b) Rented property (capitalize at 8 times net rental paid) 1b (c) Total of sections “a” and “b” above .......................1c 2 (a) Payroll ................................................................. 2a (b)Less:Officersalaries.......................................... 2b (c)Total(subtractofficersalariesfrompayroll) .........2c 3 Sales : (a) Sales delivered or shipped to Oklahoma purchasers: (i) Shipped from outside Oklahoma ..................... 3ai (ii) Shipped from within Oklahoma ...................... 3aii (b) Sales shipped from Oklahoma to: (i) The United States Government ....................... 3bi (ii) Purchasers in a state or country where the corporation is not taxable (i.e. under Public Law 86-272) .. 3bii (c) Total all of sections “a” and “b” .............................3c

4 IfRevenue,TrafficUnitsorMilesTraveledisusedratherthanSales,indicatehere: ____________________________________ 5 Total percent (sum of items 1, 2 and 3) ........................................................................................................56 Averagepercent(1/3oftotalpercent)(CarrytoScheduleB,line5) ............................................................6

2014 Form 512 - Page 3

Schedule B is for computation of Oklahoma taxable income of a unitary enterprise. [Section 2358(A)(5)] Enclose a complete copy of your Federal return.

Apportionment Formula

1 Net taxable income from Schedule A, Column A, line 30 .....................................1 2 Add: (a) Taxes based on income ................................................................... 2a (b) Federal net operating loss deduction .............................................. 2b (c) Unallowable deduction (enclose schedule) ..................................... 2c (d) _________________________________ ..................................... 2d (e) _________________________________ ..................................... 2e (f) Total of lines 2a through 2e .............................................................. 2f3 Deductallitemsseparatelyallocated (a) _________________________________ ..................................... 3a (b) _________________________________ ..................................... 3b (c) _________________________________ ..................................... 3c (d) _________________________________ ..................................... 3d (e) _________________________________ ..................................... 3e (f) Total of lines 3a through 3e .............................................................. 3f (Note: Items listed in 2 and 3 above must be net amounts supported by schedules showing source, location, expenses, etc.) 4 Net apportionable income.....................................................................................45 Oklahoma’sportionthereof _________________ %, from schedule below .......5 6 Add or deduct items separately allocated to Oklahoma (enclose schedule) (a) ________________________________________ ..................................... 6a (b) ________________________________________ ..................................... 6b (c) ________________________________________ ..................................... 6c (d) Oklahoma net operating loss deduction ........................................................ 6d 7 Oklahoma net income before tax (add lines 5 and 6) ...........................................7 8 Oklahoma accrued tax (see instructions) .............................................................8 9 Oklahoma taxable income, line 7 less line 8 (enter on page 1, line 1) .................9

$$

$

$

$

$

$

$

$$$

Column ATotal WithinOklahoma

Column BTotal Within and

Without Oklahoma

Column C(A divided by B)Percent Within

Oklahoma

Schedule B

$ $ %

%

%

%%

$ $

$ $

1 Cash ............................................................. 1 2 Trade notes and accounts receivable .......... 2 (a) Less allowance for bad debts ................2a 3 Inventories ................................................... 34 Gov’tobligations: (a) U.S. and instrumentalities ......................4a (b) State, subdivision, thereof, etc ..............4b 5 Other current assets (enclose schedule) ..... 5 6 Loans to shareholders ................................. 6 7 Mortgage and real estate loans ................... 7 8 Other investments (enclose schedule) ......... 8 9 Buildingsandotherfixeddepreciableassets .. 9 (a) Less accumulated depreciation .............9a10 Depletableassets .......................................10 (a) Less accumulated depletion ................10a11 Land (net of any amortization) ....................1112 Intangible assets (amortization only) ..........12 (a) Less accumulated amortization ...........12a13 Other assets (enclose schedule) ................1314 Total assets .................................................14

(A) Amount (B) Total (C) Amount (D) TotalBeginning of taxable year

( ) ( )

Schedule OK M-1: Reconciliation of Income per Books with Income per Return

1 Net income (loss) per books ........................ 1 2 Federal income tax ...................................... 2 3 Excess of capital losses over capital gains .. 3

4 Taxable income not recorded on books this year (enclose schedule) ............................... 4 5 Expenses recorded on books this year not deducted in this return (enclose schedule) (a)Depreciation $ ___________________ (b)Depletion $ ___________________ (c) Other ___________________________ ________________________________ (d) Total of lines 5a, 5b and 5c ....................5d 6 Total of lines 1 through 4 and 5d .................. 6

7 Income recorded on books this year not included in this return (enclose schedule) (a) Tax exempt interest $ ________________ (b) Other $ ________________ (c) Total of lines 7a and 7b ...........................7c 8 Deductionsinthistaxreturnnotcharged against book income this year (enclose schedule)

(a)Depreciation $ _____________________ (b)Depletion $ _____________________ (c) Other ____________________________ (d) Total of lines 8a, 8b and 8c .................... 8d 9 Total of lines 7c and 8d .................................. 910 Net income: line 6 less line 9 ....................... 10

1 Balance at beginning of year ....................... 1 2 Net income (loss) per books ........................ 2 3 Other increases (enclose schedule) ___________________________________ __________________________________ 3 4 Total of lines 1, 2 and 3 ................................ 4

5 Distributions: (a) Cash ............................. 5a (b) Stock ............................. 5b (c) Property .........................5c 6 Other decreases (enclose sch.) __________________________________ 6 7 Total of lines 5 and 6 ..................................... 7 8 Balance at end of year (line 4 less line 7) ..... 8

Balance Sheets

Schedule OK M-2: Analysis of Unappropriated Retained Earnings per Books (line 24 above)

2014 Form 512 - Page 4

15 Accounts payable ........................................1516 Mtgs-notes-bonds payable in less than1 yr...1617 Other current liabilities (enclose schedule) ...17 18 Loans from shareholders ............................1819 Mtgs-notes-bonds payable in 1 yr. or more ...1920 Other liabilities (enclose schedule) .............2021 Capital stock: (a) preferred stock ............21a (b) common stock.............21b22 Paid-in capital surplus (enclose reconciliation) ....22 23 Retained earnings-appropriated (enclose sch.) ..2324 Retained earnings-unappropriated .............2425 Adjustmentstoshareholders’equity(enclose sch.) 2526 Less cost of treasury stock .........................2627 Totalliabilitiesandshareholders’equity ......27

End of taxable year

2014 Form 512 - Page 5

Schedule 512-X: Amended Return Schedule

DidyoufileanamendedFederalreturn? Yes No EncloseacopyofIRSForm1120Xor1139andacopyof“StatementofAdjustment”,IRSrefundcheckordepositslip.

IfthisreturnisbeingfiledduetoaFederalaudit,furnishacompletecopyoftheRAR.

Explanation or Reason for Amended Return (Enclose all necessary schedules):

_________________________________________________________________________________________

_________________________________________________________________________________________

_________________________________________________________________________________________

_________________________________________________________________________________________ _________________________________________________________________________________________

_________________________________________________________________________________________

_________________________________________________________________________________________

_________________________________________________________________________________________

_________________________________________________________________________________________

_________________________________________________________________________________________

_________________________________________________________________________________________

_________________________________________________________________________________________

_________________________________________________________________________________________

_________________________________________________________________________________________

_________________________________________________________________________________________

_________________________________________________________________________________________

_________________________________________________________________________________________

A

B

C

Instructions for filing an Amended Return Beginningwithtaxyear2013,useForm512tofileanamendedreturn.DonotuseForm512X.Form512Xwillbeusedtofileanamendedreturnfortaxyear2012andprior. Whenfilinganamendedreturn,placean“X”intheAmendedReturncheck-boxatthetopofpage1.Enteranyamount(s)paidwiththeoriginalreturnplusanyamount(s)paidafteritwasfiledonline9.Enteranyrefundpreviouslyreceivedoroverpaymentappliedonline10.CompletetheAmendedReturnSchedule,Schedule512-Xabove. EncloseForm1120Xor1139andproofofdispositionbytheInternalRevenueServicewhenapplicable. An overpayment on an amended return may not be credited to estimated tax, but will be refunded. The amount applied to estimated tax on the original return cannot be adjusted.

State of OklahomaComputation of Oklahoma Consolidated Taxable Income (Form 512, Line 1)

14. Oklahoma Net Operating Loss Deduction A. Carryback from Tax Year(s) ..............A) ...........A)

B. Carryforward from Tax Year(s) ..........B) ...........B)

15. Oklahoma Taxable Income (Loss) before Oklahoma Accrued Income Tax Deduction ..............16. Total Allowable Oklahoma Non-Refundable Credits (This amount will equal the total from Form 512, Page 1, Line 3) ..............................................................

A. Oklahoma Income from Line 15 above .....................................

B. Divide Line 16 (above) by 6% ...................................................

C. Subtract Line B from Line A ......................................................

D. Accrued Oklahoma Income Tax – Divide Line C by 17.6667 (Do not enter less than zero) .................................................................

18. Oklahoma Consolidated Taxable Income – Subtract Line 17D from Line 15 (Enter here and on the Form 512, Page 1, Line 1)....................................................................................

Corporate Name

Enter the information for each corporation included in the consolidated return on a separate line. The “Oklahoma Income” of each corporation will be totaled and entered on line 13. If there are more than 11 corporations, use Form 512-TI-SUP to enter the additional corporations. Use as many Forms 512-TI-SUP as needed.

NOTE: If the return is filed by paper, Form 512-TI must be the second page of the consolidated return. Place Form 512-TI and, if applicable, Form(s) 512-TI-SUP immediately after Form 512, page 1.

Loss Year(s)

Federal Employer Identification Number

17. Computation of Accrued Income Tax Deduction Allowed

12. Enter the total from Supplemental Schedule(s), Form 512-TI-SUP

13. Total

( )

( )

FEIN

BusinessActivity

Code

Net Apportionable

Income

Apportionment Percentages

FO

RM

512-TI2014

(from Sch. B Line 4)

(from Apportionment Formula,Lines 1C, 2C and 3C)

PropertyFactor

1C) 2C) 3C)PayrollFactor

SalesFactor

A) B) C) D) E) F)

Federal TaxableIncome

OklahomaIncome

(from Sch. A Column A, Line 28)

(Before an NOL deductionand tax accrual)

1)

2)

3)

4)

5)

6)

7)

8)

9)

10)

11)

State of OklahomaSupplemental Schedule forForm 512-TI

Corporate Name FEIN

Total. Enter here and on Form 512-TI, line 12

FEIN

BusinessActivity

Code

Federal TaxableIncome

Net Apportionable

Income

Apportionment PercentagesOklahoma

Income

FO

RM

512-TI-SUP2014

(from Sch. A Column A, Line 28)

(Before an NOL deductionand tax accrual)(from Sch. B Line 4)

(from Apportionment Formula,Lines 1C, 2C and 3C)

PropertyFactor

1C) 2C) 3C)PayrollFactor

SalesFactor

Page______ of ______

NOTE: If the return is filed by paper, place Form(s) 512-TI-SUP immediately after Form 512-TI. Make note of the number of Forms 512-TI-SUP that are included in the consolidated return (e.g. If there are five Forms 512-TI-SUP, the second Form 512-TI-SUP would have 2 of 5 shown in the Page section below.)

A) B) C) D) E) F)

1)

2)

3)

4)

5)

6)

7)

8)

9)

10)

11)

12)

13)

14)

15)

16)

17)

18)

19)

20)

21)

22)

23)

24)

25)