2014 Long Term Care - Risk - Retirement - Health | Aon term care provider, a jury awarded $91 .5...

54

Risk. Reinsurance. Human Resources. 2014 Long Term Care General Liability and Professional Liability Actuarial Analysis, November 2014 Aon Risk Solutions

Transcript of 2014 Long Term Care - Risk - Retirement - Health | Aon term care provider, a jury awarded $91 .5...

Risk. Reinsurance. Human Resources.

2014 Long Term CareGeneral Liability and Professional Liability Actuarial Analysis, November 2014

Aon Risk Solutions

Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

Purpose . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

Scope . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

Executive Summary . . . . . . . . . . . . . . . . . . . . . . . 2

Key Findings . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2

Liability and the Long Term Care Profession . . . . . . . 2

Advisory Estimates . . . . . . . . . . . . . . . . . . . . . . . 3

State Findings . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

Indemnity and Expense Statistics . . . . . . . . . . . . 5

Claim Lag Statistics . . . . . . . . . . . . . . . . . . . . . . . 7

Reporting Lag . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

Closing Lag . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

Countrywide Estimates . . . . . . . . . . . . . . . . . . . 8

California . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

Florida . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

Georgia . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

Illinois . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

Indiana . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

Kentucky . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

Maryland . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

Table of Contents

Massachusetts . . . . . . . . . . . . . . . . . . . . . . . . . . 24

Michigan . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26

Minnesota . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28

North Carolina . . . . . . . . . . . . . . . . . . . . . . . . . 30

Ohio . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32

Pennsylvania . . . . . . . . . . . . . . . . . . . . . . . . . . . 34

Tennessee . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36

Texas . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38

West Virginia . . . . . . . . . . . . . . . . . . . . . . . . . . . 40

Wisconsin . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42

All Other States . . . . . . . . . . . . . . . . . . . . . . . . . 44

Database . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 46

Actuarial Analysis . . . . . . . . . . . . . . . . . . . . . . . 47

Conditions and Limitations . . . . . . . . . . . . . . . 47

Definitions . . . . . . . . . . . . . . . . . . . . . . . . . . . . 48

About Aon . . . . . . . . . . . . . . . . . . . . . . . . . . . . 52

Aon Risk Solutions 2014 Long Term Care General Liability and Professional Liability Actuarial Analysis 1

Purpose

The Actuarial and Analytics Practice of Aon Global Risk Consulting (Aon)

conducted an actuarial analysis of general liability and professional liability (GL/

PL) claim costs for the long term care profession in the United States .

Scope

The specific objectives of this study are to:

• Identify the overall trends in the cost of GL/PL claims for long term care

• Identify state specific trends in the cost of GL/PL claims for long term care

• Identify trends in frequency and severity overall and on a state by state basis

• Present closed claim statistics related to report lag, closing lag and

expense versus indemnity

An overview of the findings can be found in the Executive Summary section of this report .

Please contact us if you have any questions regarding this report .

Respectfully submitted,

Christian Coleianne, FCAS, MAAA Associate Director and Actuary +1 .410 .309 .0741 christian .coleianne@aon .com

Konstantin Sakherzon Senior Actuarial Analyst +1 .215 .255 .1806 konstantin .sakherzon@aon .com

Donald Riggins, FCAS, MAAA, CPCU Associate Director and Actuary+1 .410 .309 .4539 donald .riggins@aon .com

Molly Rozran Actuarial Analyst+1 .410 .381 .2439 molly .rozran@aon .com

Introduction

Aon Risk Solutions 2014 Long Term Care General Liability and Professional Liability Actuarial Analysis 2

Executive Summary

Key Findings Based on the actuarial analysis of GL/PL claims data

from long term care providers on a national level:

• Long term care loss rates are increasing by

5 .0% annually .

• The overall forecasted 2015 accident year long term

care GL/PL loss rate limited to $1 million per occurrence

is $2,030 per bed .

• Long term care frequency is increasing by

3 .0% annually .

• The forecasted 2015 accident year long term care GL/PL

frequency is 0 .93 claims per 100 occupied beds .

• Long term care claim severity is increasing by 2 .0%

annually on an overall basis .

• The forecasted 2015 accident year long term care

GL/PL severity is $218,000 per claim limited to $1

million per occurrence .

Liability and the Long Term Care Profession The cost of liability continues to increase for

the Long Term Care profession . At the national

level, the overall loss rate is expected to grow by

5% annually, with claim frequency driving the

increase at an expected 3% growth rate .

For the states profiled in this report, the projected

2015 loss rates vary tremendously, with Kentucky

at $9,220 per occupied bed and Texas at $320 per

occupied bed . For a provider with 100 occupied

beds, this implies an annual liability cost of

$922,000 in Kentucky and $32,000 in Texas .

Kentucky’s high cost of liability at $9,220 may be

related to its lack of restrictions on tort actions . The

state constitution prohibits limits on non-economic

damages and there are no statutes concerning

qualification of expert witnesses, certificates of

merit, pre-trial alternative dispute resolution or

limits on attorney’s fees . Kentucky has the highest

average claim severity among the profiled states .

West Virginia has the second highest loss rate in

this report at $6,950 per occupied bed . While West

Virginia has a limit on non-economic damages of

$250,000 per claimant (West Virginia Code §55-7B),

it has not been clear whether this limit applied to

long term care providers . In a 2011 trial involving a

long term care provider, a jury awarded $91 .5 million

of which $80 million were non-economic damages .

The state legislature extended the protections of

the cap to long term care providers in 2013, and

this appears to be reducing claims frequency .

In contrast, with a loss rate of just $320 per occupied

bed, Texas amended its state constitution to protect

the tort reforms enacted in 2003 . Texas has a $250,000

limit on non-economic damages per claimant (Civil

Practice & Remedies §74 .301) and rules concerning

expert witnesses (Civil Practice & Remedies §74 .401-

403) . Attorney’s fees are not limited and there

are requirements to provide special wording in

arbitration agreements (Civil Practice & Remedies

§74 .451) in order for the agreements to be valid .

Aon Risk Solutions 2014 Long Term Care General Liability and Professional Liability Actuarial Analysis 3

Advisory Estimates

Claim FrequencyOverall claim frequency is the number of claims per 100 occupied beds . Indemnity

claim frequency is the number of claims that resolve with a payment to the claimant

per 100 occupied beds .

Claim SeverityClaim severity is the average size of claims, with claims limited to $1 million

per occurrence .

Loss RateThe loss rate is the annual amount per occupied bed required to defend, settle or

litigate claims in a given year .

The projected 2015 loss rate is $2,030 and is projected to grow by 5 .0% annually .

Projected 2015 Estimate Annual Trend

Overall Claim Frequency* 0 .93 3 .0%

Indemnity Claim Frequency* 0 .73 3 .0%

Severity $218,000 2 .0%

Loss Rate** $2,030 5 .0%

LTC Estimates and Annual Trends for Losses Limited to $1 Million per Occurrence

* Number of claims per 100 occupied beds

** Liability cost per occupied bed

Aon Risk Solutions 2014 Long Term Care General Liability and Professional Liability Actuarial Analysis 4

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

$8,000

$9,000

$10,000

All OtherWVWITXTNPAOHNCMNMIMDMAKYINILGAFLCA

Country-wide

$9,220$960$2,720$2,390$5,730$3,070$2,030 $430

4.2%2.7%4.6%5.0%4.0%2.5%4.4%100.0%

Loss Rate

% of Database

$2,030

$3,070

$5,730

$2,390$2,720

$960

$9,220

$430

$1,310$940

$440$1,110 $1,040

$1,910

$3,240

$320$1,000

$6,950

$1,610

$1,310 $940 $440 $1,110 $1,040 $1,910 $3,240 $320 $1,000 $6,950 $1,610

2.7%2.8%3.1% 11.3%5.4%5.9% 2.6%5.3%3.6% 27.8%2.4%

State FindingsThe following chart shows projected 2015 loss rate levels for the states that are profiled in this study .

The 2015 projected loss rates are determined by applying trend to our 2013 estimates by state . The

states were profiled based on the volume of data received, the stability of the results compared to

prior years, and the number of providers represented in the data .

Comparison of Projected 2015 Loss Rates Limited to $1 Million per Occurrence

Loss Rates are relative to 2015 occupied beds .

The % of Database is measured by occupied beds .

Aon Risk Solutions 2014 Long Term Care General Liability and Professional Liability Actuarial Analysis 5

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

341319

425

327

425 517

980 849 1,199 974 1,337 1,232

201320122011201020092008

Closed Year

Cla

im C

ount

Indemnity and Expense Statistics

Indemnity and Expense Only Claim Counts

Indemnity Claims Expense Only Claims

Closed claims are presented to show the relationship between indemnity and expense . The claims

were limited to those aged seven years or less from the occurrence date . This represents 97% of the

claims in each closing year .

The following chart shows the distribution of claims closed with expense only versus claims closed

with indemnity . The percent of claims closed with indemnity is about 74% over the experience

period and stable .

Aon Risk Solutions 2014 Long Term Care General Liability and Professional Liability Actuarial Analysis 6

$0

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

$35,000

Closed Year

201320122011201020092008

$33,000 $15,200 $15,800 $21,300 $17,400 $14,100

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

$58,900

$61,400 $64,700 $53,800

$57,400

$56,100

$159,000 $177,000

201320122011201020092008

Closed Year

Ave

rage

Cla

im S

ize

on C

laim

s C

lose

d w

ith

Inde

mni

ty

$181,000 $183,000 $216,000 $186,000

The following chart shows the average paid indemnity and expense for claims closed with

an indemnity payment . Indemnity costs are about 73% of total costs on claims closed with

indemnity . The average indemnity is growing over time, while the average expense is

relatively flat .

Claims Closed with Indemnity: Average Size—Unlimited

The following chart shows the average paid expense for claims closed without an

indemnity payment . The average expense on claims closed without indemnity is

generally at or below $20,000 .

Claims Closed without Indemnity: Average Expense—Unlimited

Average Paid Indemnity Average Paid Expense

Aon Risk Solutions 2014 Long Term Care General Liability and Professional Liability Actuarial Analysis 7

0%

20%

40%

60%

80%

100%

Number of Months from Report to Close

60-7248-6036-4824-3612-240-12

41.2% 69.4% 85.4% 93.2% 97.0% 98.6%

Claim Lag Statistics

Reporting Lag

The reporting lag is time between the occurrence date of an event and the time it is reported to the provider . 72% of incidents are reported within 12 months of the occurrence, and 92% are reported within 24 months .

Report Lag: Cumulative Percent of Claims Reported

Closing Lag

The closing lag is the number of months between the report date of the incident and the final settlement . 41% of claims close within 12 months of being reported and 69% of claims close within the first 24 months after being reported .

Close Lag: Cumulative Percent of Claims Closed

0%

20%

40%

60%

80%

100%

Number of Months from Incident to Report

60-7248-6036-4824-3612-240-12

71.8% 92.4% 98.2% 99.5% 99.8% 99.9%

Aon Risk Solutions 2014 Long Term Care General Liability and Professional Liability Actuarial Analysis 8

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

201420132012201120102009200820072006

0.53 0.52 0.57 0.68 0.70

Accident Year

0.54 0.65 0.69 0.71

0.18 0.180.17

0.19 0.20

0.16

0.190.19 0.20

0.71 0.700.74

0.87 0.90

0.70

0.840.88 0.91

Countrywide EstimatesThe participants in the study represent approximately 230,000 occupied beds countrywide. This is approximately 17% of the countrywide total beds.

Loss RateThe following chart shows the

loss rate per occupied bed .

Loss rates are increasing

since 2009 .

The current annual loss rate

trend is projected at 5 .0% .

Loss Rate per Occupied Bed Limited to $1M per Occurrence

Claim FrequencyThe following graph shows the

frequency per 100 occupied

beds . The stacked bar chart

provides frequency estimates

for claims with indemnity

(indemnity claims) and

claims without indemnity

(expense only claims) .

Claim frequency has increased

from 0 .71 per 100 occupied beds

to 0 .90 per 100 occupied beds .

Between 2009 and 2010,

frequency increased

significantly and has remained

at this higher level .

Claim Frequency per 100 Occupied Beds

$0

$500

$1,000

$1,500

$2,000

$2,500

Accident Year

201420132012201120102009200820072006

$1,200 $1,190 $1,210$1,370

$1,670

$1,940$1,780

$1,860 $1,850

Indemnity Claims Expense Only Claims

Aon Risk Solutions 2014 Long Term Care General Liability and Professional Liability Actuarial Analysis 9

0.0%

0.5%

1.%0

1.5%

2.0%

2.5%

3.0%

3.5%

2.26%2.12% 2.05%

2.26%

2.68%2.81%

2.89% 2.82%

20132012201120102009200820072006

$170.59$166.08$161.11$153.59$145.51 $173.56

$5.07$5.09$4.87$4.57$3.75$3.31$3.26$3.29

Average Medicaid per Diem Reimbursement

Per Diem Loss Rate per Bed

$175.84 $179.75

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$170,000 $169,000 $172,000$184,000

$199,000 $206,000 $207,000 $210,000

Accident Year

201420132012201120102009200820072006

$214,000

Liability Costs and Medicaid Reimbursement TrendsMedicaid is a significant

source of revenue for long

term care providers .

The following graph shows

the per diem loss rate per

bed as a percentage of the

Overall Medicaid per diem

reimbursement rate . The Overall

Medicaid reimbursement

rate shown here is a state rate

weighted by the exposure

distribution underlying

the per diem loss rate .

Concurrent with the recent

loss rate growth, liability costs

as a percent of the Medicaid

Reimbursement rate has

increased in recent years .

Loss Rate per OBE Limited to $2M per Occurrence

SeverityThe following graph shows

the average size per claim,

also called claim severity .

Claim severity has grown

over the experience period

from $170,000 in 2006 to a

projected $214,000 in 2014 .

Claim Severity Limited to $1M per Occurrence

Aon Risk Solutions 2014 Long Term Care General Liability and Professional Liability Actuarial Analysis 10

CaliforniaThe participants in this study represent approximately 10,000 occupied beds in the state. This is approximately 10% of the state total beds.

Loss Rate

Loss rates have increased to a level above $2,220 since 2010 .

Frequency

Claims frequency has grown slightly over the experience period .

Loss Rate per Occupied Bed Limited to $1M per Occurrence

Claim Frequency per 100 Occupied Beds

Indemnity Claims Expense Only Claims

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

201420132012201120102009200820072006

$1,630$1,810

$1,660

$1,900

$2,480

$2,220

$3,170

$2,790$2,930

Accident Year

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

201420132012201120102009200820072006

Accident Year

0.74

0.26 0.37 0.24

0.19

0.18 0.22 0.22 0.23

1.091.00

1.071.01

0.88

1.04 1.03

1.26

1.060.27

0.70 0.77 0.69 0.86 0.81 0.99 0.84 0.86

Aon Risk Solutions 2014 Long Term Care General Liability and Professional Liability Actuarial Analysis 11

Severity

Claim severity has been above $215,000 since 2009 .

Liability Costs and Medicaid Reimbursement Trends

The loss rate as a percentage of the Medicaid Reimbursement Rate has increased to 4 .28% .

Severity per Claim Limited to $1M per Occurrence

Loss Rate as a Percentage of Medicaid Reimbursement Limited to $1M per Occurrence

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

201420132012201120102009200820072006

$164,000 $168,000 $164,000

$216,000

$239,000

$215,000

$251,000$264,000 $269,000

Accident Year

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

20132012201120102009200820072006Accident Year

$178.11$175.24$168.05$163.40$156.56$150.69 $142.14 $178.61

$7.64$8.68$6.08$6.79$5.20$4.54$4.96$4.46

Avg Medicaid perDiem Reimbursement

Per Diem Loss Rateper Bed

3.14%3.29%

2.90%3.18%

4.04%

3.47%

4.87%

4.28%

Aon Risk Solutions 2014 Long Term Care General Liability and Professional Liability Actuarial Analysis 12

FloridaThe participants in this study represent approximately 5,900 occupied beds in the state. This is approximately 8% of the state total beds.

Loss Rate

Florida loss rates are increasing since 2007, with a projected 2014 loss rate at $5,450 per occupied bed .

Florida’s loss rate is the third highest among the profiled states and is noteworthy because of the elevated frequency of claims .

Frequency

Florida’s frequency is the highest of the profiled states at 2 .36 claims per 100 occupied beds .

Frequency has been increasing moderately over the experience period .

Loss Rate per Occupied Bed Limited to $1M per Occurrence

Claim Frequency per 100 Occupied Beds

Indemnity Claims Expense Only Claims

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

201420132012201120102009200820072006

$3,400

$2,840

$3,570

$4,210$4,570

$4,940$5,230 $5,180

$5,450

Accident Year

0.00

0.50

1.00

1.50

2.00

2.50

201420132012201120102009200820072006

Accident Year

1.39

0.29

0.19

0.23

0.280.16

0.29 0.300.31

2.36

1.68

1.39

1.85

2.09

1.90

2.22 2.24 2.29

0.29

1.20 1.62 1.81 1.74 1.93 1.95 1.99 2.05

Aon Risk Solutions 2014 Long Term Care General Liability and Professional Liability Actuarial Analysis 13

Severity

Florida’s claim severity has been over $220,000 since 2010 .

Liability Costs and Medicaid Reimbursement Trends

The liability costs as a percent of the Medicaid Reimbursement Rate is 6 .69%, and is the third highest among the profiled states .

Severity per Claim Limited to $1M per Occurrence

Loss Rate as a Percentage of Medicaid Reimbursement Limited to $1M per Occurrence

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

201420132012201120102009200820072006

$202,000 $204,000$193,000

$202,000

$241,000

$222,000$233,000 $226,000 $231,000

Accident Year

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

20132012201120102009200820072006Accident Year

$205.61$205.61$206.47$202.66$180.05$175.00 $160.43 $211.98

$14.18$14.32$13.52$12.51$11.53$9.77$7.78$9.31

Avg Medicaid perDiem Reimbursement

Per Diem Loss Rateper Bed

5.80%

4.45%

5.43%5.69%

6.06%6.58%

6.96%6.69%

Aon Risk Solutions 2014 Long Term Care General Liability and Professional Liability Actuarial Analysis 14

GeorgiaThe participants in this study represent approximately 9,100 occupied beds in the state. This is approximately 27% of the state total beds.

Loss Rate

Georgia’s loss rate has been increasing over time .

The sharp increase in 2010 may be related to the removal of the $350,000 cap on non-economic damages .

Frequency

Claim frequency in Georgia spiked in 2010 coincident with the Georgia Supreme Court’s ruling striking down the $350,000 cap on non-economic damages . While frequency has decreased since, it is still much higher than pre-ruling levels .

Loss Rate per Occupied Bed Limited to $1M per Occurrence

Claim Frequency per 100 Occupied Beds

Indemnity Claims Expense Only Claims

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

201420132012201120102009200820072006

$2,110

$790$980 $950

$2,730

$2,050

$2,250$2,160

$2,260

Accident Year

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

201420132012201120102009200820072006

Accident Year

1.00

0.34

0.080.11

0.24

0.31

0.22 0.23 0.23

1.01

1.34

0.50

0.61

0.75

1.23

0.94

1.070.98

0.25

0.42 0.50 0.51 0.92 0.72 0.82 0.75 0.78

Aon Risk Solutions 2014 Long Term Care General Liability and Professional Liability Actuarial Analysis 15

Severity

Claim severity in Georgia also increased in 2010, around the time of the Georgia Supreme Court ruling, and has remained elevated .

Liability Costs and Medicaid Reimbursement Trends

Georgia’s loss rates relative to the Medicaid Per Diem Reimbursement rate is substantially higher than levels pre-2010 .

Severity per Claim Limited to $1M per Occurrence

Loss Rate as a Percentage of Medicaid Reimbursement Limited to $1M per Occurrence

$0

$50,000

$100,000

$150,000

$200,000

$250,000

201420132012201120102009200820072006

$157,000 $157,000 $161,000

$126,000

$222,000 $218,000$211,000

$221,000 $225,000

Accident Year

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

20132012201120102009200820072006Accident Year

$146.38$141.59$141.78$135.22$133.48$127.43 $126.61 $156.10

$5.91$6.16$5.61$7.47$2.60$2.68$2.16$5.78

Avg Medicaid perDiem Reimbursement

Per Diem Loss Rateper Bed

4.57%

1.70%2.01% 1.92%

5.27%

3.96%4.21%

3.79%

Aon Risk Solutions 2014 Long Term Care General Liability and Professional Liability Actuarial Analysis 16

IllinoisThe participants in this study represent approximately 11,200 occupied beds in the state. This is approximately 15% of the state total beds.

Loss Rate

The loss rate in Illinois relatively stable since 2009 .

Frequency

Claim frequency in Illinois is the fourth highest among the states profiled in this report .

Loss Rate per Occupied Bed Limited to $1M per Occurrence

Claim Frequency per 100 Occupied Beds

Indemnity Claims Expense Only Claims

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

201420132012201120102009200820072006

$1,550

$2,560

$2,140

$2,440 $2,360

$2,560 $2,490 $2,460$2,590

Accident Year

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

201420132012201120102009200820072006

Accident Year

0.80

0.09

0.21

0.18

0.28 0.210.24 0.24 0.25

1.67

0.89

1.29

1.16

1.571.51

1.63 1.63 1.62

0.24

1.08 0.98 1.29 1.30 1.39 1.39 1.38 1.42

Aon Risk Solutions 2014 Long Term Care General Liability and Professional Liability Actuarial Analysis 17

Severity

Severity has been stable since 2009 around $155,000 .

Liability Costs and Medicaid Reimbursement Trends

Illinois’ loss rate relative to the Medicaid Per Diem Reimbursement rate is above 5% .

Severity per Claim Limited to $1M per Occurrence

Loss Rate as a Percentage of Medicaid Reimbursement Limited to $1M per Occurrence

$0

$50,000

$100,000

$150,000

$200,000

$250,000

201420132012201120102009200820072006

$173,000

$198,000$185,000

$155,000 $156,000 $157,000 $153,000 $152,000 $155,000

Accident Year

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

20132012201120102009200820072006Accident Year

$132.49$130.47$117.88$117.29$112.20$103.89 $96.94 $129.30

$6.74$6.82$7.01$6.46$6.68$5.86$7.01$4.24

Avg Medicaid perDiem Reimbursement

Per Diem Loss Rateper Bed

4.37%

6.75%

5.22%5.70% 5.48% 5.37% 5.15% 5.21%

Aon Risk Solutions 2014 Long Term Care General Liability and Professional Liability Actuarial Analysis 18

IndianaThe participants in this study represent approximately 10,700 occupied beds in the state. This is approximately 28% of the state total beds.

Loss Rate

Indiana’s loss rates have increased beginning in 2010 due to increasing severity .

Frequency

Generally, claim frequency has been stable since 2010 near the current level of 0 .70 claims per 100 occupied beds .

Loss Rate per Occupied Bed Limited to $1M per Occurrence

Claim Frequency per 100 Occupied Beds

Indemnity Claims Expense Only Claims

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

$1,000

201420132012201120102009200820072006

$420 $410 $410$450

$600

$720

$830$860

$910

Accident Year

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

201420132012201120102009200820072006

Accident Year

0.45

0.14

0.17

0.19

0.09

0.090.13

0.14 0.15

0.70

0.59

0.45

0.63

0.44

0.660.63

0.69 0.68

0.14

0.28 0.44 0.35 0.57 0.50 0.55 0.54 0.55

Aon Risk Solutions 2014 Long Term Care General Liability and Professional Liability Actuarial Analysis 19

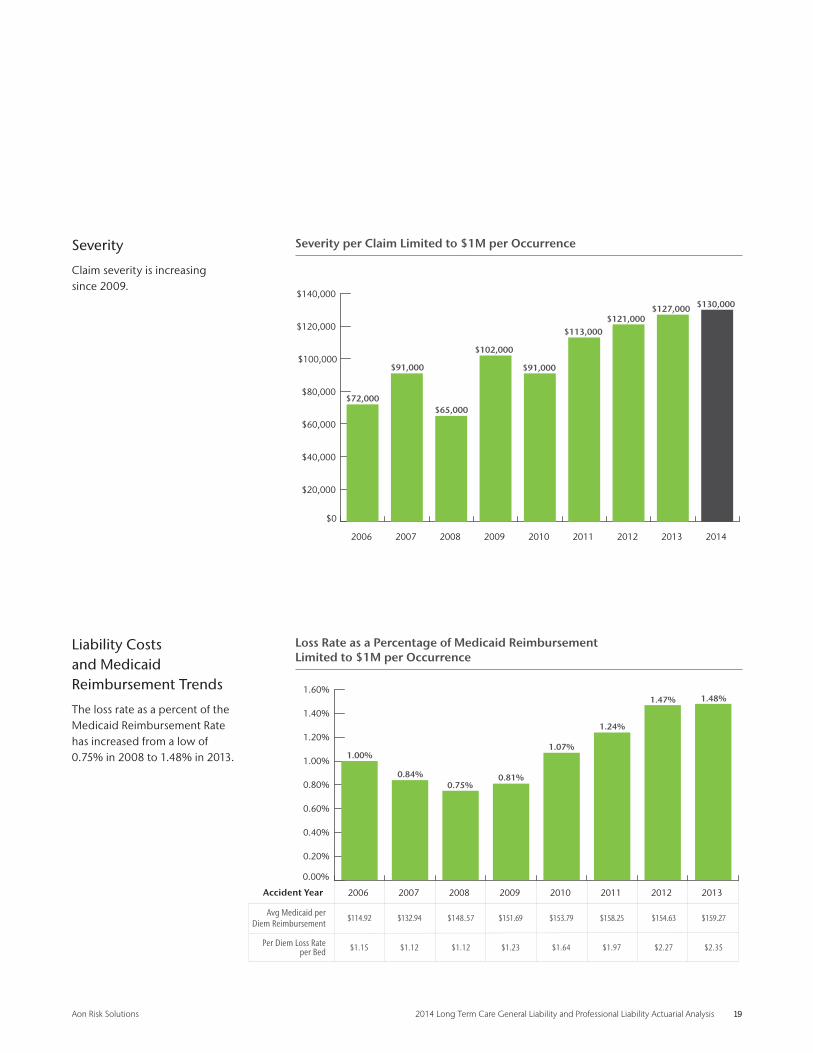

Severity

Claim severity is increasing since 2009 .

Liability Costs and Medicaid Reimbursement Trends

The loss rate as a percent of the Medicaid Reimbursement Rate has increased from a low of 0 .75% in 2008 to 1 .48% in 2013 .

Severity per Claim Limited to $1M per Occurrence

Loss Rate as a Percentage of Medicaid Reimbursement Limited to $1M per Occurrence

$0

$20,000

$40,000

$60,000

$80,000

$100,000

$120,000

$140,000

201420132012201120102009200820072006

$72,000

$91,000

$65,000

$102,000

$91,000

$113,000$121,000

$127,000 $130,000

Accident Year

0.00%

0.20%

0.40%

0.60%

0.80%

1.00%

1.20%

1.40%

1.60%

20132012201120102009200820072006Accident Year

$154.63$158.25$153.79$151.69$148.57$132.94 $114.92 $159.27

$2.35$2.27$1.97$1.64$1.23$1.12$1.12$1.15

Avg Medicaid perDiem Reimbursement

Per Diem Loss Rateper Bed

1.00%

0.84%0.75%

0.81%

1.07%

1.24%

1.47% 1.48%

Aon Risk Solutions 2014 Long Term Care General Liability and Professional Liability Actuarial Analysis 20

KentuckyThe participants in this study represent approximately 7,100 occupied beds in the state. This is approximately 31% of the state total beds.

Loss Rate

Kentucky has the highest loss rate of the profiled states in this study .

The loss rate has increased from $2,100 in 2007 to a projected $8,790 in 2014 .

Frequency

Claim frequency in Kentucky is the second highest among the profiled states .

Frequency has increased from a low 0f 0 .87 claims per occupied bed in 2006 to a projected high of 1 .94 claims per occupied bed in 2014 .

Loss Rate per Occupied Bed Limited to $1M per Occurrence

Claim Frequency per 100 Occupied Beds

Indemnity Claims Expense Only Claims

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

$8,000

$9,000

$10,000

201420132012201120102009200820072006

$2,670$2,100

$4,740$4,450

$6,350

$8,090 $8,020$8,360

$8,790

Accident Year

0.00

0.50

1.00

1.50

2.00

2.50

201420132012201120102009200820072006

Accident Year

0.73

0.14 0.28

0.250.24

0.41 0.39 0.39 0.40

1.94

0.870.99

1.361.24

1.88 1.87 1.91 1.89

0.40

0.71 1.11 1.00 1.47 1.48 1.51 1.50 1.54

Aon Risk Solutions 2014 Long Term Care General Liability and Professional Liability Actuarial Analysis 21

Severity

Claim severity in Kentucky is the highest of the states profiled in this study and has been above $330,000 per claim since 2008 .

Liability Costs and Medicaid Reimbursement Trends

The loss rate as a percentage of the per diem Medicaid Reimbursement rate is 14 .17% in 2013 .

This is the highest level among the profiled states .

Severity per Claim Limited to $1M per Occurrence

Loss Rate as a Percentage of Medicaid Reimbursement Limited to $1M per Occurrence

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

$350,000

$400,000

$450,000

$500,000

201420132012201120102009200820072006

$308,000

$212,000

$347,000 $358,000$338,000

$432,000$420,000

$443,000 $452,000

Accident Year

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

16.00%

20132012201120102009200820072006Accident Year

$156.86$151.41$147.14$142.72$137.49$132.72 $125.56 $161.57

$22.89$21.96$22.15$17.39$12.18$12.98$5.75$7.31

Avg Medicaid perDiem Reimbursement

Per Diem Loss Rateper Bed

5.82%

4.33%

9.44%8.53%

11.82%

14.63%14.00% 14.17%

Aon Risk Solutions 2014 Long Term Care General Liability and Professional Liability Actuarial Analysis 22

MarylandThe participants in this study represent approximately 7,700 occupied beds in the state. This is approximately 32% of the state total beds.

Loss Rate

The loss rates in Maryland have been stable since 2009 .

Frequency

Claim frequency in Maryland is stable around 0 .65 claims per 100 occupied beds .

Loss Rate per Occupied Bed Limited to $1M per Occurrence

Claim Frequency per 100 Occupied Beds

Indemnity Claims Expense Only Claims

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

201420132012201120102009200820072006

$1,360

$980 $940

$1,200$1,150 $1,180

$1,050

$1,190$1,250

Accident Year

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

201420132012201120102009200820072006

Accident Year

0.70

0.14

0.19

0.05

0.08 0.080.07 0.07 0.07

0.65

0.84

0.74

0.57

0.65 0.63 0.65

0.57

0.63

0.06

0.55 0.52 0.57 0.55 0.58 0.51 0.56 0.58

Aon Risk Solutions 2014 Long Term Care General Liability and Professional Liability Actuarial Analysis 23

Severity

Claim severity in Maryland has been stable at about $185,000 .

Liability Costs and Medicaid Reimbursement Trends

The loss rate as a percent of the Medicaid Reimbursement Rate is stable since 2007 .

Severity per Claim Limited to $1M per Occurrence

Loss Rate as a Percentage of Medicaid Reimbursement Limited to $1M per Occurrence

$0

$50,000

$100,000

$150,000

$200,000

$250,000

201420132012201120102009200820072006

$163,000

$132,000

$166,000

$185,000 $183,000 $182,000 $185,000 $187,000 $191,000

Accident Year

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

20132012201120102009200820072006Accident Year

$230.84$231.81$222.47$212.29$213.27$194.10 $186.41 $237.86

$3.26$2.87$3.23$3.15$3.29$2.57$2.68$3.72

Avg Medicaid perDiem Reimbursement

Per Diem Loss Rateper Bed

2.00%

1.38%1.21%

1.55%1.42% 1.39%

1.24%1.37%

Aon Risk Solutions 2014 Long Term Care General Liability and Professional Liability Actuarial Analysis 24

MassachusettsThe participants in this study represent approximately 10,200 occupied beds in the state. This is approximately 25% of the state total beds.

Loss Rate

The loss rate in Massachusetts has been just above $400 per occupied bed since 2009, with a surge to $550 in 2001 driven by claim severity .

Frequency

Claim frequency in Massachusetts has been stable over the experience and is currently at 0 .36 per 100 occupied beds, the lowest frequency among the profiled states .

Loss Rate per Occupied Bed Limited to $1M per Occurrence

Claim Frequency per 100 Occupied Beds

Indemnity Claims Expense Only Claims

$0

$100

$200

$300

$400

$500

$600

201420132012201120102009200820072006

$510$530

$490

$410

$450

$550

$410 $400$420

Accident Year

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

0.45

0.50

201420132012201120102009200820072006

Accident Year

0.25

0.11

0.15

0.08

0.04

0.08 0.070.06 0.07

0.360.36

0.46

0.37

0.30

0.38 0.38 0.380.35

0.07

0.31 0.29 0.26 0.30 0.31 0.31 0.29 0.29

Aon Risk Solutions 2014 Long Term Care General Liability and Professional Liability Actuarial Analysis 25

Severity

Claim severity in Massachusetts has been under $150,000 for the entire experience period .

The projected severity in 2014 is $115,000, the third lowest among the profiled states .

Liability Costs and Medicaid Reimbursement Trends

The loss rate as a percent of the Medicaid Reimbursement Rate has been declining over the experience period and, at 0 .56%, is the lowest of the profiled states .

Severity per Claim Limited to $1M per Occurrence

Loss Rate as a Percentage of Medicaid Reimbursement Limited to $1M per Occurrence

$0

$20,000

$40,000

$60,000

$80,000

$100,000

$120,000

$140,000

$160,000

201420132012201120102009200820072006

$141,000

$115,000

$133,000$138,000

$119,000

$147,000

$107,000$113,000 $115,000

Accident Year

0.00%

0.10%

0.20%

0.30%

0.40%

0.50%

0.60%

0.70%

0.80%

0.90%

20132012201120102009200820072006Accident Year

$199.35$197.40

$196.84$192.84$191.30$191.30 $177.16 $197.91

$1.10$1.12$1.51$1.23$1.12$1.34$1.45$1.40

Avg Medicaid perDiem Reimbursement

Per Diem Loss Rateper Bed

0.79%0.76%

0.70%

0.58%0.62%

0.76%

0.56% 0.56%

Aon Risk Solutions 2014 Long Term Care General Liability and Professional Liability Actuarial Analysis 26

MichiganThe participants in this study represent approximately 6,500 occupied beds in the state. This is approximately 17% of the state total beds.

Loss Rate

The loss rate in Michigan is growing since 2007 .

Frequency

Claim frequency is at or below 0 .70 claims per 100 occupied beds with the exception of 2006 .

Loss Rate per Occupied Bed Limited to $1M per Occurrence

Claim Frequency per 100 Occupied Beds

Indemnity Claims Expense Only Claims

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

201420132012201120102009200820072006

$1,290

$600$670

$760

$570

$830$790

$850$890

Accident Year

0.00

0.20

0.40

0.60

0.80

1.00

1.20

201420132012201120102009200820072006

Accident Year

0.87

0.21

0.220.09

0.120.19 0.17

0.16 0.17

0.68

1.08

0.60

0.51

0.68 0.68 0.700.63

0.66

0.16

0.38 0.42 0.56 0.49 0.53 0.47 0.50 0.51

Aon Risk Solutions 2014 Long Term Care General Liability and Professional Liability Actuarial Analysis 27

Severity

Severity has been under $135,000 for the entire experience period .

Liability Costs and Medicaid Reimbursement Trends

The loss rate as a percent of the Medicaid reimbursement rate is at 1 .04% .

Severity per Claim Limited to $1M per Occurrence

Loss Rate as a Percentage of Medicaid Reimbursement Limited to $1M per Occurrence

$0

$20,000

$40,000

$60,000

$80,000

$100,000

$120,000

$140,000

201420132012201120102009200820072006

$119,000

$100,000

$132,000

$111,000

$84,000

$119,000$126,000 $128,000 $131,000

Accident Year

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

20132012201120102009200820072006Accident Year

$215.39$211.44$207.40$195.18$187.31$180.92 $163.84 $223.76

$2.33$2.16$2.27$1.56$2.08$1.83$1.64$3.53

Avg Medicaid perDiem Reimbursement

Per Diem Loss Rateper Bed

2.15%

0.91%0.98%

1.07%

0.75%

1.07%1.00% 1.04%

Aon Risk Solutions 2014 Long Term Care General Liability and Professional Liability Actuarial Analysis 28

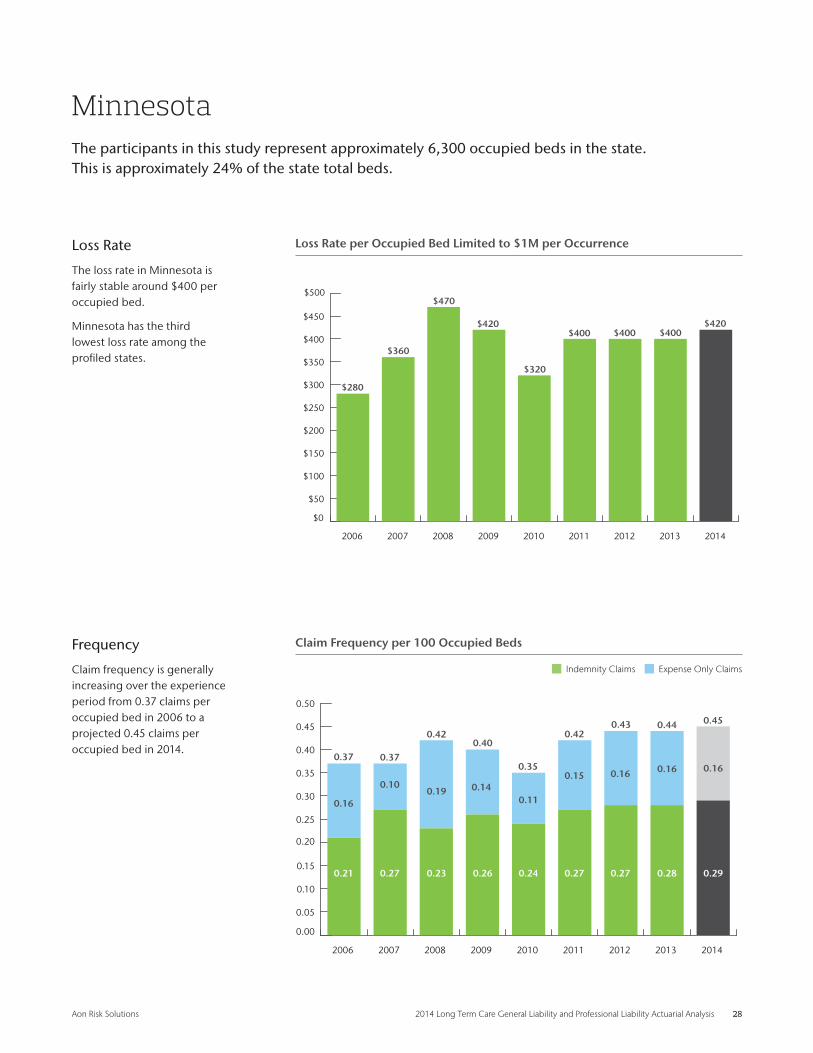

MinnesotaThe participants in this study represent approximately 6,300 occupied beds in the state. This is approximately 24% of the state total beds.

Loss Rate

The loss rate in Minnesota is fairly stable around $400 per occupied bed .

Minnesota has the third lowest loss rate among the profiled states .

Frequency

Claim frequency is generally increasing over the experience period from 0 .37 claims per occupied bed in 2006 to a projected 0 .45 claims per occupied bed in 2014 .

Loss Rate per Occupied Bed Limited to $1M per Occurrence

Claim Frequency per 100 Occupied Beds

Indemnity Claims Expense Only Claims

$0

$50

$100

$150

$200

$250

$300

$350

$400

$450

$500

201420132012201120102009200820072006

$280

$360

$470

$420

$320

$400 $400 $400

$890

Accident Year

$420

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

0.45

0.50

201420132012201120102009200820072006

Accident Year

0.21

0.16

0.100.19 0.14

0.11

0.150.16

0.17

0.16

0.45

0.37 0.37

0.420.40

0.35

0.420.43 0.44

0.16

0.27 0.23 0.26 0.24 0.27 0.27 0.28 0.29

Aon Risk Solutions 2014 Long Term Care General Liability and Professional Liability Actuarial Analysis 29

Severity

Severity has decreased from a high of $114,000 per occurrence in 2008 to a projected $92,000 per occurrence in 2014 .

This is the second lowest severity among the profiled states .

Liability Costs and Medicaid Reimbursement Trends

The loss rate as a percent of the Medicaid reimbursement rate is 0 .65% .

Severity per Claim Limited to $1M per Occurrence

Loss Rate as a Percentage of Medicaid Reimbursement Limited to $1M per Occurrence

$0

$20,000

$40,000

$60,000

$80,000

$100,000

$120,000

201420132012201120102009200820072006

$75,000

$99,000

$114,000

$106,000

$91,000$96,000

$92,000 $90,000 $92,000

Accident Year

0.00%

0.10%

0.20%

0.30%

0.40%

0.50%

0.60%

0.70%

0.80%

0.90%

20132012201120102009200820072006Accident Year

$168.97$165.82$164.34$164.34$154.24$147.68 $142.02 $169.63

$1.10$1.10$1.10$0.88$1.15$1.29$0.99$0.77

Avg Medicaid perDiem Reimbursement

Per Diem Loss Rateper Bed

0.54%

0.67%

0.84%

0.70%

0.54%

0.66% 0.65% 0.65%

Aon Risk Solutions 2014 Long Term Care General Liability and Professional Liability Actuarial Analysis 30

North CarolinaThe participants in this study represent approximately 13,800 occupied beds in the state. This is approximately 37% of the state total beds.

Loss Rate

The loss rate in North Carolina increased in 2010 and is now over $1,000 per bed . The increase is due to higher claim frequency . A $500,000 non-economic damages cap became effective October 1, 2011 .

Frequency

The frequency increase in 2010 may be related to claimants presenting before the implementation of tort reform effective October 1, 2011 . Claim frequency has not subsided since the legislation became effective .

Loss Rate per Occupied Bed Limited to $1M per Occurrence

Claim Frequency per 100 Occupied Beds

Indemnity Claims Expense Only Claims

$0

$200

$400

$600

$800

$1,000

$1,200

201420132012201120102009200820072006

$470

$1,140

$590$530

$980

$750

$1,010 $1,000

$890

Accident Year

$1,050

0.00

0.10

0.20

0.30

0.40

0.50

0.60

201420132012201120102009200820072006

Accident Year

0.23

0.08

0.07

0.09 0.05

0.07

0.09 0.09

0.17

0.09

0.50

0.31

0.48

0.440.41

0.55

0.49 0.50 0.49

0.09

0.41 0.35 0.36 0.48 0.40 0.41 0.40 0.41

Aon Risk Solutions 2014 Long Term Care General Liability and Professional Liability Actuarial Analysis 31

Severity

Claim severity has increased since 2008 and is now over $200,000

The claim severity spike in 2007 reflects several claims that exceed $1 million .

Liability Costs and Medicaid Reimbursement Trends

The loss rate as a percent of the Medicaid reimbursement rate is at 1 .55% .

Severity per Claim Limited to $1M per Occurrence

Loss Rate as a Percentage of Medicaid Reimbursement Limited to $1M per Occurrence

$0

$50,000

$100,000

$150,000

$200,000

$250,000

201420132012201120102009200820072006

$150,000

$236,000

$134,000 $130,000

$179,000

$155,000

$203,000 $205,000 $209,000

Accident Year

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

20132012201120102009200820072006Accident Year

$171.12$165.17$160.52$155.69$150.33$136.54 $134.18 $176.25

$2.74$2.77$2.05$2.68$1.45$1.62$3.12$1.29

Avg Medicaid perDiem Reimbursement

Per Diem Loss Rateper Bed

0.96%

2.29%

1.08%0.93%

1.67%

1.24%

1.62%1.55%

Aon Risk Solutions 2014 Long Term Care General Liability and Professional Liability Actuarial Analysis 32

OhioThe participants in this study represent approximately 12,200 occupied beds in the state. This is approximately 16% of the state total beds.

Loss Rate

Loss rates in Ohio have grown after reaching a low point of $370 per occupied bed in 2007 . The growth is related to increases in claim severity .

Frequency

Claim frequency in Ohio has been stable since 2009 between 0 .55 and 0 .60 claims per 100 occupied beds .

Loss Rate per Occupied Bed Limited to $1M per Occurrence

Claim Frequency per 100 Occupied Beds

Indemnity Claims Expense Only Claims

$0

$200

$400

$600

$800

$1,000

$1,200

201420132012201120102009200820072006

$470

$370

$710

$530

$780 $760

$890$940

$990

Accident Year

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

201420132012201120102009200820072006

Accident Year

0.37

0.42

0.21

0.20

0.230.19 0.20 0.21

0.22

0.60

0.79

0.55

0.65

0.56 0.57 0.56 0.58 0.58

0.21

0.34 0.45 0.33 0.38 0.36 0.37 0.37 0.38

Aon Risk Solutions 2014 Long Term Care General Liability and Professional Liability Actuarial Analysis 33

Severity

Claim severity has grown strongly over the experience period and is projected to be $164,000 in 2014 .

Liability Costs and Medicaid Reimbursement Trends

The loss rate as a percent of the Medicaid reimbursement rate is around 1 .50% .

Severity per Claim Limited to $1M per Occurrence

Loss Rate as a Percentage of Medicaid Reimbursement Limited to $1M per Occurrence

$0

$20,000

$40,000

$60,000

$80,000

$100,000

$120,000

$140,000

$160,000

$180,000

201420132012201120102009200820072006

$60,000$67,000

$110,000

$95,000

$137,000 $137,000

$153,000$161,000 $164,000

Accident Year

0.00%

0.20%

0.40%

0.60%

0.80%

1.00%

1.20%

1.40%

1.60%

20132012201120102009200820072006Accident Year

$168.43$172.33$177.77$172.16$166.07$163.96 $158.71 $174.64

$2.57$2.44$2.08$2.14$1.45$1.94$1.01$1.29

Avg Medicaid perDiem Reimbursement

Per Diem Loss Rateper Bed

0.81%

0.62%

1.17%

0.84%

1.20% 1.21%

1.45% 1.47%

Aon Risk Solutions 2014 Long Term Care General Liability and Professional Liability Actuarial Analysis 34

PennsylvaniaThe participants in this study represent approximately 26,300 occupied beds in the state. This is approximately 33% of the state total beds.

Loss Rate

The 2014 projected loss rate in Pennsylvania is $1,810 per occupied bed .

Frequency

The frequency of losses has increased from a low of 0 .56 in 2007 to a projected high of 1 .00 in 2014 .

Claim frequency appears to have reached a plateau in 2010 and is stable since .

Loss Rate per Occupied Bed Limited to $1M per Occurrence

Claim Frequency per 100 Occupied Beds

Indemnity Claims Expense Only Claims

$0

$500

$1,000

$1,500

$2,000

$2,500

201420132012201120102009200820072006

$1,080

$810$900

$1,250

$1,660

$2,000

$1,620$1,720

$1,810

Accident Year

0.00

0.20

0.40

0.60

0.80

1.00

1.20

201420132012201120102009200820072006

Accident Year

0.45

0.170.15

0.200.17

0.280.27 0.26 0.27

1.00

0.620.56

0.670.74

0.960.99

0.940.97

0.25

0.41 0.47 0.57 0.68 0.72 0.69 0.71 0.73

Aon Risk Solutions 2014 Long Term Care General Liability and Professional Liability Actuarial Analysis 35

Severity

Since 2009, claim severity has been around $170,000 to $180,000 with the exception of 2011 .

Liability Costs and Medicaid Reimbursement Trends

The liability cost as a percent of Medicaid per diem rate has grown over the experience period and is currently at 2 .25%

Severity per Claim Limited to $1M per Occurrence

Loss Rate as a Percentage of Medicaid Reimbursement Limited to $1M per Occurrence

$0

$50,000

$100,000

$150,000

$200,000

$250,000

201420132012201120102009200820072006

$173,000

$144,000$133,000

$168,000 $173,000

$203,000

$172,000 $177,000 $181,000

Accident Year

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

20132012201120102009200820072006Accident Year

$208.14$204.63$203.54$199.42$197.61$190.83 $179.17 $209.65

$4.71$4.44$5.48$4.54$3.42$2.46$2.22$2.96

Avg Medicaid perDiem Reimbursement

Per Diem Loss Rateper Bed

1.65%

1.16%1.24%

1.71%

2.23%

2.68%

2.13%2.25%

Aon Risk Solutions 2014 Long Term Care General Liability and Professional Liability Actuarial Analysis 36

TennesseeThe participants in this study represent approximately 8,800 occupied beds in the state. This is approximately 30% of the state total beds.

Loss Rate

The loss rate in Tennessee has grown from a low in 2008 of $1,310 per occupied bed to a projected $3,090 per occupied bed in 2014 .

The growth is primarily due to growth in frequency .

Tennessee enacted limits on non-economic damages effective October 1, 2011 .

Frequency

Claim frequency has increased since 2008 .

The continued growth in claim frequency after the implementation of tort limits in 2011 is surprising .

Loss Rate per Occupied Bed Limited to $1M per Occurrence

Claim Frequency per 100 Occupied Beds

Indemnity Claims Expense Only Claims

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

201420132012201120102009200820072006

$2,160

$1,890

$1,310$1,440

$1,690

$2,730$2,910 $2,950

$3,090

$890

Accident Year

$990

0.00

0.20

0.40

0.60

0.80

1.00

1.20

201420132012201120102009200820072006

Accident Year

0.72

0.180.16

0.16

0.16

0.22

0.23

0.27

0.17

0.28

1.11

0.900.85

0.61

0.72

0.83

0.93

1.041.08

0.26

0.69 0.45 0.56 0.61 0.70 0.78 0.81 0.83

Aon Risk Solutions 2014 Long Term Care General Liability and Professional Liability Actuarial Analysis 37

Severity

Claim severity has increased over the experience period and is the third highest severity of the profiled states .

Claim severity increased sharply in 2011 and is still elevated .

Liability Costs and Medicaid Reimbursement Trends

The loss rate as a percent of the Medicaid per diem reimbursement has increased from a low of 2 .54% in 2008 to 4 .95% in 2013 .

Severity per Claim Limited to $1M per Occurrence

Loss Rate as a Percentage of Medicaid Reimbursement Limited to $1M per Occurrence

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

$350,000

201420132012201120102009200820072006

$241,000$224,000

$214,000$201,000 $204,000

$292,000$279,000 $273,000 $278,000

Accident Year

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

20132012201120102009200820072006Accident Year

$158.60$153.09$148.77$144.30$141.56$136.12 $131.05 $163.36

$8.08$7.97$7.47$4.63$3.94$3.59$5.17$5.91

Avg Medicaid perDiem Reimbursement

Per Diem Loss Rateper Bed

4.51%

3.80%

2.54%2.73%

3.11%

4.88% 5.03% 4.95%

Aon Risk Solutions 2014 Long Term Care General Liability and Professional Liability Actuarial Analysis 38

TexasThe participants in this study represent approximately 12,300 occupied beds in the state. This is approximately 13% of the state total beds.

Loss Rate

The loss rate in Texas has been stable since 2009 .

Substantial decreases from 2006 through 2008 are the result of decreases in claim frequency .

Frequency

The claim frequency in Texas has decreased to under 0 .45 per 100 occupied beds .

Texas has the second lowest frequency rate among the profiled states .

Loss Rate per Occupied Bed Limited to $1M per Occurrence

Claim Frequency per 100 Occupied Beds

Indemnity Claims Expense Only Claims

$0

$100

$200

$300

$400

$500

$600

201420132012201120102009200820072006

$510

$450

$320$300

$260

$310$290 $290

$310

Accident Year

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

201420132012201120102009200820072006

Accident Year

0.42

0.26

0.30

0.170.26 0.29

0.18 0.17 0.18

0.44

0.680.66

0.44

0.54 0.54

0.44 0.44 0.43

0.18

0.36 0.27 0.28 0.25 0.26 0.26 0.26 0.26

Aon Risk Solutions 2014 Long Term Care General Liability and Professional Liability Actuarial Analysis 39

Severity

Claim severity in Texas has been under $75,000 for the entire experience period .

Texas has the lowest severity of the profiled states .

Liability Costs and Medicaid Reimbursement Trends

The loss rate as a percent of the Medicaid per diem reimbursement rate has decreased over the experience period to 0 .60%, the second lowest rate among the profiled states .

Severity per Claim Limited to $1M per Occurrence

Loss Rate as a Percentage of Medicaid Reimbursement Limited to $1M per Occurrence

$0

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

$70,000

$80,000

201420132012201120102009200820072006

$75,000

$68,000

$74,000

$55,000

$48,000

$70,000$67,000 $68,000 $69,000

Accident Year

0.00%

0.20%

0.40%

0.60%

0.80%

1.00%

1.20%

1.40%

20132012201120102009200820072006Accident Year

$128.33$126.87$128.09$123.20$111.89$106.48 $107.26 $131.61

$0.79$0.79$0.85$0.71$0.82$0.88$1.23$1.40

Avg Medicaid perDiem Reimbursement

Per Diem Loss Rateper Bed

1.16%

1.31%

0.79%

0.67%

0.55%

0.67%0.62% 0.60%

Aon Risk Solutions 2014 Long Term Care General Liability and Professional Liability Actuarial Analysis 40

0.0

0.5

1.0

1.5

2.0

2.5

201420132012201120102009200820072006

Accident Year

0.87 0.96 1.32 1.50 1.941.05 1.75 1.44 1.48

0.21 0.10

0.24

0.28

0.36

0.12

0.39

0.26

0.20

1.08 1.06

1.56

1.78

2.30

1.17

2.14

1.700.27

1.75

Accident Year

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

$8,000

$9,000

201420132012201120102009200820072006

$2,730 $2,530

$3,440

$5,590

$8,220

$6,620

$5,960

$7,910

$6,310

West VirginiaThe participants in this study represent approximately 5,400 occupied beds in the state. This is approximately 56% of the state total beds.

Loss Rate

The loss rate in West Virginia has grown from a low in 2007 of $2,530 to a projected $6,620 in 2014 .

West Virginia has the second highest loss rate among the profiled states .

Frequency

Frequency has increased from 1 .08 claims per 100 occupied beds in 2005 to a projected 1 .75 claims per 100 occupied beds in 2014 . West Virginia has the third highest frequency among the profiled states .

The bulge in claims for occurrence years 2010 and subsequent may be related to the large jury award in 2011 .

The state legislature explicitly applied statutory caps to long term care providers in 2013 and this may have reduced claims frequency from its peak in 2012 .

Loss Rate per Occupied Bed Limited to $1M per Occurrence

Claim Frequency per 100 Occupied Beds

Indemnity Claims Expense Only Claims

Aon Risk Solutions 2014 Long Term Care General Liability and Professional Liability Actuarial Analysis 41

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

20132012201120102009200820072006

4.44%3.97%

$193.31$187.50$180.64$174.36$168.11 $198.92

$17.28$21.66$16.32$22.51$15.30$9.42$6.93$7.47

Average Medicaid per Diem Reimbursement

Per Diem Loss Rate per Bed

$206.08 $212.26

5.21%

8.16%

11.64%

8.20%

10.51%

8.14%

Accident Year

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

$350,000

$400,000

$450,000

201420132012201120102009200820072006

$253,000$239,000

$294,000

$358,000$384,000

$335,000 $344,000$371,000 $378,000

Severity

Severity in West Virginia has been between $335,000 and $385,000 since 2009 .

This is more than twice the countrywide average severity over the same time period .

Liability Costs and Medicaid Reimbursement Trends

The loss rate as a percent of the Medicaid reimbursement rate has increased from a low of 3 .97% in 2007 to 8 .14% in 2013 .

Severity per Claim Limited to $1M per Occurrence

Loss Rate as a Percentage of Medicaid Reimbursement Limited to $1M per Occurrence

Aon Risk Solutions 2014 Long Term Care General Liability and Professional Liability Actuarial Analysis 42

WisconsinThe participants in this study represent approximately 6,200 occupied beds in the state. This is approximately 22% of the state total beds.

Loss Rate

Loss rates in Wisconsin have been volatile, ranging between $530 and a projected $950 in 2014 .

Frequency

Claim frequency in Wisconsin is projected to be 0 .56 claims per 100 occupied beds in 2013 . Claim frequency has been relatively stable over the experience period .

Loss Rate per Occupied Bed Limited to $1M per Occurrence

Claim Frequency per 100 Occupied Beds

Indemnity Claims Expense Only Claims

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

$1,000

201420132012201120102009200820072006

$530

$780

$850

$560

$750 $730

$880 $900$950

Accident Year

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

201420132012201120102009200820072006

Accident Year

0.41

0.160.19

0.13

0.14

0.140.13

0.140.15

0.560.57 0.56

0.63

0.45

0.52 0.510.54 0.55

0.14

0.37 0.50 0.31 0.38 0.38 0.40 0.41 0.41

Aon Risk Solutions 2014 Long Term Care General Liability and Professional Liability Actuarial Analysis 43

Severity

Claim severity is increasing in Wisconsin, with a projected average claim size of $169,000 in 2014 .

Liability Costs and Medicaid Reimbursement Trends

The loss rate as a percent of the Medicaid per diem Reimbursement rate varies over the experience period .

Severity per Claim Limited to $1M per Occurrence

Loss Rate as a Percentage of Medicaid Reimbursement Limited to $1M per Occurrence

$0

$20,000

$40,000

$60,000

$80,000

$100,000

$120,000

$140,000

$160,000

$180,000

201420132012201120102009200820072006

$93,000

$141,000$134,000

$126,000

$143,000 $143,000

$163,000 $166,000 $169,000

Accident Year

0.00%

0.20%

0.40%

0.60%

0.80%

1.00%

1.20%

1.40%

1.60%

1.80%

20132012201120102009200820072006Accident Year

$156.23$154.54$153.71$146.87$140.87$136.13 $133.21 $160.24

$2.46$2.41$2.00$2.05$1.53$2.33$2.14$1.45

Avg Medicaid perDiem Reimbursement

Per Diem Loss Rateper Bed

1.09%

1.57%1.65%

1.04%

1.33% 1.29%

1.54% 1.54%

Aon Risk Solutions 2014 Long Term Care General Liability and Professional Liability Actuarial Analysis 44

All Other StatesThe participants in this study represent approximately 64,200 occupied beds in the remaining states. This is approximately 12% of the remaining state total beds.

Loss Rate

The All Other States loss rate is slightly increasing over the experience period .

Frequency

The All Other States frequency has increased from a low of 0 .62 claims per 100 occupied beds in 2006 to a projected 0 .73 claims per 100 occupied beds in 2014 .

Loss Rate per Occupied Bed Limited to $1M per Occurrence

Claim Frequency per 100 Occupied Beds

Indemnity Claims Expense Only Claims

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$1,800

201420132012201120102009200820072006

$1,250

$1,440

$1,210$1,300

$1,350$1,460

$1,410$1,460

$1,530

Accident Year

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

201420132012201120102009200820072006

Accident Year

0.48

0.14

0.15

0.170.17 0.15

0.170.16

0.17

0.73

0.62

0.72

0.660.69 0.68

0.74 0.740.71

0.17

0.57 0.49 0.52 0.53 0.57 0.57 0.55 0.56

Aon Risk Solutions 2014 Long Term Care General Liability and Professional Liability Actuarial Analysis 45

Severity

All Other States claim severity is relatively flat over the experience period at just over $200,000 .

Liability Costs and Medicaid Reimbursement Trends

The All Other States liability cost as a percent of the Medicaid Reimbursement rate has increased from 2 .03% in 2008 to 2 .21% in 2013 .

Severity per Claim Limited to $1M per Occurrence

Loss Rate as a Percentage of Medicaid Reimbursement Limited to $1M per Occurrence

$0

$50,000

$100,000

$150,000

$200,000

$250,000

201420132012201120102009200820072006

$203,000 $200,000

$182,000$189,000

$199,000 $198,000$190,000

$204,000 $208,000

Accident Year

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

20132012201120102009200820072006Accident Year

$176.51$174.35$171.04$167.11$163.04$154.97 $146.41 $181.33

$4.00$3.86$4.00$3.70$3.31 $3.56$3.94$3.42

Avg Medicaid perDiem Reimbursement

Per Diem Loss Rateper Bed

2.34%

2.54%

2.03%2.13% 2.16%

2.29%2.19% 2.21%

Aon Risk Solutions 2014 Long Term Care General Liability and Professional Liability Actuarial Analysis 46

DatabaseIn an effort to present a comprehensive analysis from the perspective of all long term care systems,

Aon disseminated a request for data to for-profit and not-for-profit providers including independent

providers, regional multi-facility providers and national multi-facility providers .

The results presented in this study are based on the ensuing database of long term care GL/PL losses

and allocated loss adjustment expenses (ALAE) as reported to us by 34 long term care providers .

Data from the participants was aggregated, resulting in 13,700 non-zero claims and $2 .3 billion

in incurred losses . The facilities represented in the national study operate approximately 230,000

long term care beds, consisting primarily of skilled nursing facility beds but also including a number

of independent living, assisted living, home health care and rehabilitation beds . They represent

approximately 17% of the beds in the United States, and include six of the ten largest providers in

the country .

The results found in this study are representative of the participants . Providers that did not

participate may have different results, either higher or lower . This may be due to any number of

reasons, including levels of effectiveness in quality of care initiatives and the attractiveness of the

provider for tort actions . Based on standard actuarial techniques, the number of claims, number of

participants and bed representation ensure significant credibility of the results at the national level .

The proportion of statewide bed representation assures significant credibility of the results at the

state level . To increase credibility, a higher response rate among providers would be required .

All long term care results published in this report are based on losses (indemnity plus allocated

adjustment expense) limited to $1 million per occurrence unless otherwise noted . The $1 million

per occurrence limitation was selected to limit the impact of large claims on the results .

Statutory limitations were based on National Conference of State Legislatures research updated

August 2011, accessed September 26, 2014 from http://www .ncsl .org/issues-research/banking/

medical-liability-medical-malpractice-laws .aspx . Referenced statutory limitations were confirmed by

retrieving the individual state codes online .

The loss rates are presented relative to the Medicaid per diem reimbursement rate . The Medicaid

per diem reimbursement rate is based on data from “A Report on Shortfalls in Medicaid Funding for

Nursing Home Care” produced by Eljay LLC for the American Health Care Association and dated

January 2014 .The Overall Medicaid per diem reimbursement rate is based on the state exposure

distribution inherent in this study .

Aon Risk Solutions 2014 Long Term Care General Liability and Professional Liability Actuarial Analysis 47

Actuarial AnalysisThe statistics presented in this report are based on an actuarial analysis of the

aggregated long term care GL/PL claim database and related exposure data .

The analysis applies standard actuarial methods to the claim data to develop

ultimate losses and claim counts by accident year . These projections are used

to calculate the following statistics presented in this report:

• Loss Rate—ultimate loss projection per occupied bed equivalent

• Overall Frequency—annual number of non-zero claims per 100 occupied

bed equivalents

• Indemnity Frequency—annual number of claims with indemnity payments

per 100 occupied bed equivalents

• Severity—average ultimate size of each claim, where each claim is limited

to $1 million per occurrence

Conditions and LimitationsInherent UncertaintyActuarial calculations produce estimates of inherently uncertain future

contingent events . We believe that the estimates provided represent

reasonable provisions based on the appropriate application of actuarial

techniques to the available data . However, there is no guarantee that

actual future payments will not differ from estimates included herein .

Extraordinary Future EmergenceOur projections make no provision for the extraordinary future emergence of

losses or types of losses not sufficiently represented in the historical data or

which are not yet quantifiable .

Data RelianceIn conducting this analysis, we relied upon the provided data without audit

or independent verification; however, we reviewed it for reasonableness

and consistency . Any inaccuracies in quantitative data or qualitative

representations could have a significant effect on the results of our review

and analysis .

Use and DistributionUse of this report is limited for the specific purpose described in the

Introduction section . Other uses are prohibited without an executed

release with Aon .

Distribution is unrestricted . We request that Aon be notified of further

distribution of this report . This report should only be distributed in its

entirety, including all supporting exhibits .

Aon Risk Solutions 2014 Long Term Care General Liability and Professional Liability Actuarial Analysis 48

DefinitionsThe following definitions are provided to help the users of this report fully understand the analyses presented and the resulting conclusions.

ALAE ALAE is an abbreviation for allocated loss adjustment expense . ALAE refers to costs, in addition to indemnity payments and reserves, which are incurred in handling claims . Typically, these costs are comprised of legal fees paid by the insured entity in investigating and defending claims . In the context of this study ALAE represents defense costs . The majority of claim data used in this study contained a separate field to identify ALAE costs separately from indemnity costs . Whether separately identified or not, allocated loss adjustment expenses are included in the reported loss information, loss reserving methodologies and loss projections contained in this report . All references to losses throughout the report and exhibits include ALAE except where noted otherwise .

Accident Year An accident year is the year in which an incident giving rise to a claim occurred . All of the loss rate, frequency and severity analyses use grouped data by accident year, unless specifically noted otherwise .

Claim A claim is a demand by an individual or other entity to recover for a loss . It may involve a formal lawsuit but not necessarily, especially in the case of a general liability claim .

Exposure Actuaries select an exposure base such that the incidence of claims will tend to vary directly with the exposure of the entity at risk . The actuary must consider both the historical loss level and the corresponding exposures in evaluating historical claim liabilities and expected future costs . It is important to choose an exposure measure that is relevant to the unique situation of each risk group .

In this study the exposure base is occupied beds . Occupied beds are calculated by multiplying the number of licensed beds by the average annual occupancy rate . There is a strong correlation between the number of occupied beds and the total amount of losses incurred by a long term care facility . Not all beds are equal in terms of their risk exposure, however . An assisted living bed generates fewer dollars of GL/PL claim activity than a skilled care bed . All beds in this study have been adjusted to the equivalent of a skilled nursing care bed .

By dividing losses by exposures, comparative estimates of the long term care industry GL/PL loss rates are developed .

Frequency Frequency is the ratio of the number of claims divided by exposures . In this report, frequency is measured on an annual basis as the number of claims projected for the given time period divided by the number of occupied beds during that same period . In the summary exhibits, frequency is the annual number of claims per 100 occupied beds .

General Liability (GL) General liability exposure relates to those sums an entity becomes legally obligated to pay as damages because of a bodily injury (typically including personal and advertising injury) or property damage .

Indemnity Indemnity refers to the component of claim costs actually paid or reserved to be paid to the plaintiff . Indemnity costs include both the amount provided for the plaintiff, either as a jury award or a settlement, and the amount retained by the plaintiff’s attorney . However, in most claim files, including those used to do this study, the split between plaintiff award and plaintiff attorney is not provided . Indemnity may also include punitive damages, although this is not consistently treated among companies .

Indemnification Rate This is the ratio of claims that result in indemnity to all claims (claims with indemnity and claims with expense only) . This reflects the likelihood that a claimant will receive indemnification .

Limit of Liability A limit of liability is a maximum amount of coverage provided by an insurance transaction . Above the limit of liability, the insured is responsible for all losses . Limits of liability may be expressed on a per occurrence basis or an aggregate basis, similar to deductibles . The losses included in this study are limited to $1,000,000 per occurrence .

Loss Rate Loss rate is the cost per exposure of settling and defending claims . Loss rate is calculated as the ratio of total dollars of losses (indemnity and ALAE) to total exposures for a given period of time . In this report exposures are selected to be occupied beds and the time period is one year . Consequently, a loss rate represents the annual amount per occupied bed expected to be paid to defend, settle and/or litigate GL/PL claims arising from incidents occurring during the respective year .

Aon Risk Solutions 2014 Long Term Care General Liability and Professional Liability Actuarial Analysis 49

Loss Development Loss development refers to the change in the estimated value of losses attributable to a body of claims or to a time period until all the claims are closed .

Generally, the reported losses will increase over time for several reasons . First, it is impossible to estimate precisely the ultimate losses and legal expenses for claims when they are initially reported . The estimated unpaid loss for a claim, called a case reserve, is adjusted up or down as more information is obtained . In the aggregate, the upward adjustments tend to be greater than the downward ones . Second, it takes a period of time for some claims to be discovered, reported, and recorded . Claims that have been incurred but have not been reported are called “pure” IBNR claims . Third, closed claims are sometimes reopened . This may be due to legislation, which applies retroactively to claims that have closed . In this report, except where specifically noted, projected loss rates, frequencies and severities by state and by year are all inclusive of actuarially indicated expected loss development .

Loss development also refers to the increase in paid losses as claims are reported, paid to their ultimate values, and closed .

Loss Trend Loss trend is the change in claim frequency and/or severity from one time period to the next . Factors that affect the frequency and severity of claims are constantly changing over time . Examples of causes include inflation, societal attitudes toward legal action, and changes in laws . Actuaries use trend factors to adjust historical loss experience to comparable levels .

Professional Liability (PL) Professional liability exposure relates to those sums an entity becomes legally obligated to pay as damages and associated claims and defense expenses because of a negligent act, error or omission in the rendering or failure to render professional services .

Severity Severity refers to the total dollar amount of a claim including indemnity and ALAE . In this report, the average severity for a given year is measured by dividing the total dollars of losses for all claims incurred in the year by the total number of claims .

Aon Risk Solutions 2014 Long Term Care General Liability and Professional Liability Actuarial Analysis 50

About Aon’s Actuarial & Analytics PracticeAon’s Actuarial & Analytics Practice is the third largest North American property and

casualty consulting firm, providing actuarial services to clients for more than 20 years . Our

international capabilities are matched by our strong local presence that positions us to

deliver timely results and meaningful communication to every level of your organization .

Our practice is comprised of highly skilled and experienced professionals in the risk

quantification and analysis field . We have more than 100 consultants and 50+ Fellows and

Associates of the Casualty Actuarial Society . As part of Aon Global Risk Consulting, we

are dedicated to expanding our solutions to help our clients effectively and proactively

manage their risk in the current dynamic and challenging global economic market .

3 2014 Long Term Care General Liability and Professional Liability Actuarial Analysis

ContactsChristian Coleianne, FCAS, MAAA+1 .410 .309 .0741christian .coleianne@aon .com